The FUNdamentals of Full Cost Accounting

|

|

|

- Dulcie Tate

- 10 years ago

- Views:

Transcription

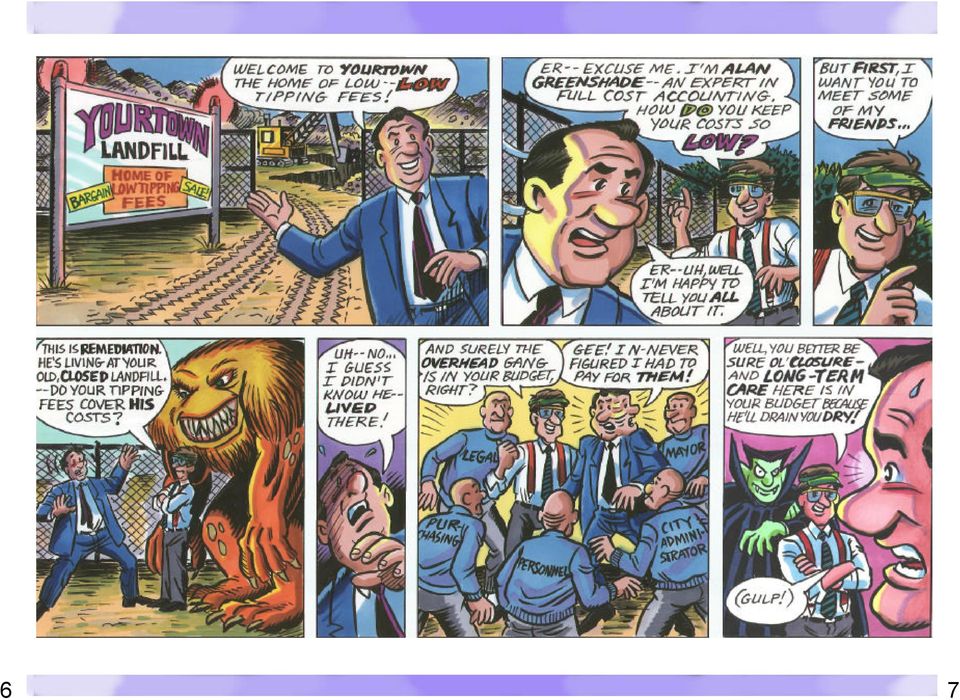

1 The FUNdamentals of Full Cost Accounting Featuring your friend and mine, that financial whiz of waste Alan Green shade! Test your skill on the Total Your Trash Quiz! and Don t miss the harrowing saga taking place at the Yourtown Landfill

2 The Fun Starts Here! Hi! We re from the Florida Department of Environmental Protection (DEP), and we re here to help you. Yes, really, please read on! We at DEP have resolved to do all we can to explain full cost accounting to local government solid waste managers. As a first step, this booklet will help explain the objectives and benefits of using full cost accounting for your solid waste collection, recycling, and disposal operations. Full cost accounting is a systematic approach for identifying, summing, and reporting the costs incurred to provide solid waste management services to a community. In addition to obvious and direct costs, full cost accounting aims to include hidden as well as overhead costs involved in solid waste management programs. Find out how your system scores when you Total Your Trash! Use the score sheets throughout the booklet to note the costs you consider to be part of the full cost of solid waste management in your community - and identify the ones you might have overlooked! Simply check off the costs you currently include and add them up for each quiz, giving yourself one point per item. Although we can t promise hours of unparalleled delight, we at least hope to convince you that full cost accounting will so greatly benefit you and your community that you will give it a try. What benefits, you ask? Well, there are many. Full cost accounting leads to more efficient management of costs and resources, and it gives you ammunition 1

3 for those political battles that seem to come with the territory of managing solid waste programs. Using full cost accounting data provided by local governments throughout the state, DEP will prepare and issue an annual comprehensive report. Using the report, you will see what other communities pay for solid waste management - and maybe pickup some tips on how to cut costs. While there is no guarantee that one local government will reduce its costs by adapting the strategies used in another community, the use of full cost accounting can provide useful information for solid waste managers and their communities to support sound management and planning. Local governments will not be ranked, and the report will not be a report card on how communities run their solid waste management systems. Like you, we realize that cost is one of many factors that determine the effectiveness of a solid waste management system, and that one system can t be considered better or worse than another simply because one community has higher costs than another. 2 The Total Your Trash Quiz in the pages of this booklet will help you evaluate your current knowledge of full cost accounting and assist you in identifying costs you might have overlooked in determining the full cost of solid waste management. We realize that not all the items listed will apply to every local government. Give the quiz a try anyway and relate the items listed to the solid waste management services you provide. Quiz 1 Up-Front Costs The initial investments and expenses necessary to manage solid waste. Check off the costs you include in calculating the up-front costs of solid waste management. Planning Land Acquisition Permitting Building Construction and Modification (4) Your Total Items Included for Up-Front Costs

4 What Is Full Cost Accounting? First of all, relax - full cost accounting is not rocket science. It s really just the application of basic cost accounting principles that can be highly beneficial to you as a solid waste manager. Full cost accounting provides you with a valuable tool for understanding and reporting your community s solid waste management costs. For a variety of reasons, most communities and their citizens do not know the real cost of managing solid waste, making it more difficult to reach good decisions about solid waste management options. Full cost accounting is not the same as cash flow or general fund accounting, which is the most common method of government accounting used today. In this system, outlays are recorded when cash is actually paid out for goods and services. However, for activities such as solid waste management, which often are funded through user fees based on cost, cash flow accounting gives a distorted picture of actual costs. As you are probably aware, not all solid waste management costs result from current outlays of funds - past and future capital outlays also contribute significantly to the overall cost of managing solid waste in your community. Cash flow accounting systems do not include up-front or back-end costs, such as those for land acquisition and long-term care. Those systems also do not take into account hidden costs, such as those for resources donated for recycling programs that do not result in cash outlays. All local governments can implement full cost accounting, regardless of how they structure their programs and keep their books. Full cost accounting uses generally accepted accounting principles to quantify all direct and indirect costs, as well as hidden costs. 3

5 Even when efforts are made to identify the costs of managing solid wastes, it is easy to overlook costs that are lumped into overhead or indirect accounts and should be recognized as direct costs. Some costs that often are not included in establishing a rate structure for solid waste fees are land acquisition costs, planning Operating Costs The everyday expenses of managing solid waste. Check off those operating costs you include in calculating the full cost of solid waste management. Personnel Wages, Salaries, and Benefits Building and Vehicle Maintenance Supplies Insurance Power and Fuel Rent and Leases Contract Services (including the cost of negotiating and administering contracts) Depreciation Debt Service Public Education and Outreach Quiz 2 Unexpected Costs (such as providing bottled water to citizens whose wells are found to be contaminated from landfill leachate) Indirect or Overhead Costs ((such as services provided by other departments or time on solid waste issues spent by the mayor, county administrator, and other elected officials) Hidden Costs (such as donated supplies or services) - (13) Your Total Items Included for Operating Costs 4

6 and permitting expenses, costs of closure and long-term care, the cost of support services provided by other local government departments, costs for negotiating and administering contracts, and an array of social and environmental costs that can be difficult to quantify. Full cost accounting also allows you to spread (depreciate of amortize) significant capital outlays over the active life of the facility. It is important to recoup those costs from tipping fees while the facility is open. Back-End Costs Quiz 3 The expenses of properly closing down solid waste management facilities at the end of their useful lives, as well as the costs of post-employment health and retirement benefits for current solid waste employees. Because cash outlays for backend costs are not made until after the useful life of the facility has ended, those costs are said to be accruing during the active life of the facility. Site closure Building and Equipment Decommissioning Long-Term Care - Retirement and Health Benefits for Employees (4) Your Total Items Included for Back-End Costs 5

7 6 7

8 Why Should You Implement Full Cost Accounting? A lthough it should not be your primary reason for implementing full cost accounting, the law in Florida requires that you determine and report full costs. In 1989, the Florida Legislature passed a law that requires local governments to report to the state and to the citizens in your community the full cost of solid waste management operations. Remediation Costs at Inactive Sites Quiz 4 The current cost of cleaning up contamination of soil, groundwater, and surface water caused by inactive facilities such as closed landfills. Investigation, Containment, and Cleanup of Known Releases - Closure and Long-Term Care at Inactive Sites (2) Your Total Items Included for Remediation Costs at Inactive Sites 8

9 A more compelling reason is self-defense. Garbage, as you are probably aware from personal experience, can be a highly political issue. Many state and local officials can attest to intense citizen interest in municipal solid waste management. Full cost accounting can help you make your case to the citizens and elected officials by providing you with sound, objective financial data to backup your decisions and recommendations. Determining what solid waste management really costs can help you. Accommodate the peaks and valleys in cash expenditures Explain costs to citizens more clearly Adopt a more businesslike approach to managing solid waste Develop a stronger position in negotiating with vendors Determine an appropriate mix of solid waste services Compare your costs with those of other communities Fine-tune your programs to increase cost-effectiveness Develop a sound system of user fees and charges to recover all the costs of managing solid waste Contingent Costs Future remediation and liability costs that may or may not be incurred. (Insurance premiums sometimes can be substituted for liability estimates.) Remediation Costs (undiscovered or future releases of contaminants to the environment) Liability Costs (property damage, personal injury, or damage to natural resources) Quiz 5 - (2) Your Total Items Included for Contingent Costs 9

10 Total Your Trash - Extra Credit Quizzes I t is difficult to quantify environmental and social costs. Currently, there is no widely accepted methodology for calculating those costs. However, if you are somehow factoring them in, check off the appropriate categories for extra credit. Extra Credit Quiz 1 Environmental Costs Environmental costs include the costs of the resources used, pollution created, and waste generated in providing solid waste management services. Upstream and downstream environmental effects commonly are termed externalities by economists. For example, the manufacture and transport of solid waste management equipment and vehicles can entail upstream environmental effects before such equipment is used, such as depletion of nonrenewable mineral resources, air and water pollution, and generation of waste. - Environmental Degradation Upstream Effects Downstream Effects (3) Your Total Items Included for Environmental Costs FOR ROCKET SCIENTISTS ONLY! Extra Credit Quiz 2 Social Costs Social costs include the adverse effects of solid waste management operations on people, their property, and their welfare that cannot be compensated through the legal system. For example, limitation of future land use, noise, odor, and traffic. Further, environmental justice issues can arise if such burdens fall disproportionately on certain social groups. - Effects on Property Values Image of the Community Aesthetic Effects Quality of Life (4) Your Total Items Included for Social Costs 10

11 Total Your Trash... The Final Score Quiz 1: Up-Front Costs Quiz 2: Operating Costs Quiz 3: Back-End Costs Quiz 4: Remediation Costs at Inactive Sites Quiz 5: Contingent Costs Extra Credit Quiz 1: Environmental Costs Extra Credit Quiz 2: Social Costs Total (possible high score, 32) Review the quizzes to find out how you can improve your score by including the missing cost elements in your full cost accounting system. Rank your score on the Greenshade Scale of Fiscal Responsibility! 11

Review the quizzes to find out how you can improve your score by including the missing cost")

12 Getting Started Congratulations! By reading this booklet and taking the full cost accounting quiz, you have already started. Take the next step by ordering a copy of Florida s user-friendly Full Cost Accounting Workbook for your accounting staff. Make sure your financial folks add any cost areas that you were unable to check off on the quiz. By taking the quiz, you may have discovered that you already are the Alan Greenshade of Garbage and currently track most of your costs. For you, implementing full cost accounting will be a snap and probably will require only minor adjustments to your current cost accounting system. On the other hand, you may have found that you really can t identify several of your solid waste management costs; some important factors are being left out of your calculations. The workbook will, however, show you how to calculate those costs and build them into an integrated full cost accounting system. Although using full cost accounting actually is pretty easy, some effort may be required to establish the procedures for collecting and quantifying the cost data you will need. However, the payback on this investment is a more cost-effective and efficient waste management system. By calculating the amount you actually spend each year to manage solid waste, you will be able to establish an appropriate fee structure to recover the full cost of managing solid waste during the active life of your facility. And, once you ve gone through the process of identifying data sources and developing a reporting procedure, preparing next year s full cost accounting report will be a breeze! 12

13 For Even More Fun... To obtain a copy of Florida s new Full Cost Accounting Workbook, please clip the order form below and mail to DEP. YES! Please send me a copy of Florida s new Full Cost Accounting Workbook Name: Title: Organization: Address: Phone No: ( ) Mail to: Florida Department of Environmental Protection Full Cost Accounting Program Solid Waste Section MS Blair Stone Rd. Tallahassee, FL Prepared in cooperation with: Florida Associations of Counties Florida League of Cities Recycle Florida Today SWANA Florida Sunshine Chapter

Amortization Cost. Depreciation. Overhead. Making Solid (Waste) Decisions With Full Cost Accounting 1EPA

Decisions With Full Cost Accounting 1EPA") United States Environmental Protection Agency EPA530-K-96-001 June 1996 1EPA Solid Waste and Emergency Response (5306W) Making Solid (Waste) Decisions With Full Cost Accounting Amortization Cost Depreciation

United States Environmental Protection Agency EPA530-K-96-001 June 1996 1EPA Solid Waste and Emergency Response (5306W) Making Solid (Waste) Decisions With Full Cost Accounting Amortization Cost Depreciation

Lane County, Oregon Statement of Net Assets June 30, 2010. Governmental Activities. Business-type

Statement of Net Assets June 30, 2010 Governmental Activities Business-type Activities Assets Current assets Cash and cash equivalents $ 152,238,503 $ 32,077,526 $ 184,316,029 Investments - 3,748,272 3,748,272

Statement of Net Assets June 30, 2010 Governmental Activities Business-type Activities Assets Current assets Cash and cash equivalents $ 152,238,503 $ 32,077,526 $ 184,316,029 Investments - 3,748,272 3,748,272

Financial Statement Guide. A Guide to Local Government Financial Statements

Financial Statement Guide A Guide to Local Government Financial Statements January, 2012 Ministry of Community, Sport and 1 Financial Statement Guide Table of Contents Introduction Legislative Requirements

Financial Statement Guide A Guide to Local Government Financial Statements January, 2012 Ministry of Community, Sport and 1 Financial Statement Guide Table of Contents Introduction Legislative Requirements

REPUBLIC SERVICES, INC. REPORTS THIRD QUARTER RESULTS

REPUBLIC CONTACTS Media Inquiries: Darcie Brossart (480) 718-6565 Investor Inquiries: Ed Lang (480) 627-7128 REPUBLIC SERVICES, INC. REPORTS THIRD QUARTER RESULTS Reports third quarter earnings of $0.42

REPUBLIC CONTACTS Media Inquiries: Darcie Brossart (480) 718-6565 Investor Inquiries: Ed Lang (480) 627-7128 REPUBLIC SERVICES, INC. REPORTS THIRD QUARTER RESULTS Reports third quarter earnings of $0.42

FULL COST ACCOUNTING PRACTICAL GUIDANCE ON CONVERTING TO FCA

FULL COST ACCOUNTING PRACTICAL GUIDANCE ON CONVERTING TO FCA Government Finance Officers Association under Cooperative Agreement with US EPA February 2000 INTRODUCTION Governmental entities all across

FULL COST ACCOUNTING PRACTICAL GUIDANCE ON CONVERTING TO FCA Government Finance Officers Association under Cooperative Agreement with US EPA February 2000 INTRODUCTION Governmental entities all across

CITY OF COLEMAN, TEXAS FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR'S REPORT SEPTEMBER 30, 2014

CITY OF COLEMAN, TEXAS FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR'S REPORT SEPTEMBER 30, 2014 Becky Roberts, CPA 104 Pine Street, Suite 610 Abilene, Texas 79601 325-665-5239 [email protected]

CITY OF COLEMAN, TEXAS FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR'S REPORT SEPTEMBER 30, 2014 Becky Roberts, CPA 104 Pine Street, Suite 610 Abilene, Texas 79601 325-665-5239 [email protected]

FLORIDA HAZARDOUS WASTE MANAGEMENT REGULATIONS THAT DIFFER FROM FEDERAL REQUIREMENTS

FLORIDA HAZARDOUS WASTE MANAGEMENT REGULATIONS THAT DIFFER FROM FEDERAL REQUIREMENTS Chapter 1: Introduction General Notes Lead Agency: Florida Department of Environmental Protection (DEP) Division of

FLORIDA HAZARDOUS WASTE MANAGEMENT REGULATIONS THAT DIFFER FROM FEDERAL REQUIREMENTS Chapter 1: Introduction General Notes Lead Agency: Florida Department of Environmental Protection (DEP) Division of

GASB Statement 49 Accounting and Financial Reporting for Pollution Remediation Obligations Implementation Issues in a Question and Answer Format

GASB Statement 49 addresses accounting and financial reporting standards for pollution (including contamination) remediation obligations, which are obligations to address the current or potential detrimental

GASB Statement 49 addresses accounting and financial reporting standards for pollution (including contamination) remediation obligations, which are obligations to address the current or potential detrimental

The Town of Fort Frances POLICY SECTION ACCOUNTING FOR TANGIBLE CAPITAL ASSETS. ADMINISTRATION AND FINANCE NEW: May 2009 1. PURPOSE: 2.

The Town of Fort Frances ACCOUNTING FOR TANGIBLE CAPITAL ASSETS SECTION ADMINISTRATION AND FINANCE NEW: May 2009 REVISED: POLICY Resolution Number: 05/09 Consent 156 Policy Number: 1.18 PAGE 1 of 11 Supercedes

The Town of Fort Frances ACCOUNTING FOR TANGIBLE CAPITAL ASSETS SECTION ADMINISTRATION AND FINANCE NEW: May 2009 REVISED: POLICY Resolution Number: 05/09 Consent 156 Policy Number: 1.18 PAGE 1 of 11 Supercedes

White Goods Accounting Worksheet

White Goods Accounting Worksheet The following worksheet was designed to help North Carolina counties accurately determine the annual reportable costs for managing white goods. Two tables are included

White Goods Accounting Worksheet The following worksheet was designed to help North Carolina counties accurately determine the annual reportable costs for managing white goods. Two tables are included

Landfill Disposal Capacity Value using Excel Model

A&WMA and OENIA 2015 Waste Management and GHG Reudction Conference Toronto, Ontario, October 7, 2015 Landfill Disposal Capacity Value using Excel Model Tian Gou, P.Eng. [email protected] AGENDA Full Cost

A&WMA and OENIA 2015 Waste Management and GHG Reudction Conference Toronto, Ontario, October 7, 2015 Landfill Disposal Capacity Value using Excel Model Tian Gou, P.Eng. [email protected] AGENDA Full Cost

Environmental Accounting Guidelines

Environmental Accounting Guidelines 2002 March 2002 Ministry of the Environment Contents Introduction... 1 1. What is Environmental Accounting?... 3 1.1 Definition...3 1.2 Functions and Roles of Environmental

Environmental Accounting Guidelines 2002 March 2002 Ministry of the Environment Contents Introduction... 1 1. What is Environmental Accounting?... 3 1.1 Definition...3 1.2 Functions and Roles of Environmental

STATE OF FLORIDA DEPARTMENT OF BUSINESS AND PROFESSIONAL REGULATION. BALANCE SHEET As of

STATE OF FLORIDA DEPARTMENT OF BUSINESS AND PROFESSIONAL REGULATION BALANCE SHEET As of ASSETS CURRENT ASSETS Cash and Cash Equivalents Cash - Restricted Accounts Receivable - Trade Accounts Receivable

STATE OF FLORIDA DEPARTMENT OF BUSINESS AND PROFESSIONAL REGULATION BALANCE SHEET As of ASSETS CURRENT ASSETS Cash and Cash Equivalents Cash - Restricted Accounts Receivable - Trade Accounts Receivable

IMPERIAL COUNTY FIXED ASSET ACCOUNTING STANDARD PRACTICE MANUAL

IMPERIAL COUNTY FIXED ASSET ACCOUNTING Adopted by Board of Supervisors December 23, 2008 Prepared by the Imperial County Auditor-Controller TABLE OF CONTENTS TITLE CHAPTER NO. PAGE NO. Fixed Asset Inventory

IMPERIAL COUNTY FIXED ASSET ACCOUNTING Adopted by Board of Supervisors December 23, 2008 Prepared by the Imperial County Auditor-Controller TABLE OF CONTENTS TITLE CHAPTER NO. PAGE NO. Fixed Asset Inventory

ENVIRONMENTAL MANAGEMENT ACCOUNTING IMPLEMENTATION GUIDELINE

ENVIRONMENTAL MANAGEMENT ACCOUNTING IMPLEMENTATION GUIDELINE ENVIRONMENTAL MANAGEMENT ACCOUNTING IMPLEMENTATION GUIDELINE 1. Introduction This guideline follows the Implementation Rules for Company Environmental

ENVIRONMENTAL MANAGEMENT ACCOUNTING IMPLEMENTATION GUIDELINE ENVIRONMENTAL MANAGEMENT ACCOUNTING IMPLEMENTATION GUIDELINE 1. Introduction This guideline follows the Implementation Rules for Company Environmental

DISTRICT OF NORTH VANCOUVER GUIDE TO FINANCIAL STATEMENTS

DISTRICT OF NORTH VANCOUVER GUIDE TO FINANCIAL STATEMENTS DISTRICT OF NORTH VANCOUVER Our goal at North Vancouver District is to make information sharing and reporting convenient, accessible and relevant

DISTRICT OF NORTH VANCOUVER GUIDE TO FINANCIAL STATEMENTS DISTRICT OF NORTH VANCOUVER Our goal at North Vancouver District is to make information sharing and reporting convenient, accessible and relevant

JUSTICE INSTITUTE OF BRITISH COLUMBIA

Financial Statements of JUSTICE INSTITUTE OF BRITISH COLUMBIA ABCD KPMG LLP Chartered Accountants Box 10426, 777 Dunsmuir Street Vancouver BC V7Y 1K3 Telephone (604) 691-3000 Telefax (604) 691-3031 Internet

Financial Statements of JUSTICE INSTITUTE OF BRITISH COLUMBIA ABCD KPMG LLP Chartered Accountants Box 10426, 777 Dunsmuir Street Vancouver BC V7Y 1K3 Telephone (604) 691-3000 Telefax (604) 691-3031 Internet

SHEET 1: CASH FLOW PROJECTED

Blended Value Business Plan Cash Flow Forecast User Guide OVERVIEW The Cash Flow Forecast is the listing of the sources and expenditures of cash plus the timing of when the cash is moving in and out of

Blended Value Business Plan Cash Flow Forecast User Guide OVERVIEW The Cash Flow Forecast is the listing of the sources and expenditures of cash plus the timing of when the cash is moving in and out of

United States Progress Report on Fossil Fuel Subsidies Part 1: Identification and Analysis of Fossil Fuel Provisions

A. Production Fossil Fuel Subsidies United States Progress Report on Fossil Fuel Subsidies Part 1: Identification and Analysis of Fossil Fuel Provisions There are a number of tax preferences, described

A. Production Fossil Fuel Subsidies United States Progress Report on Fossil Fuel Subsidies Part 1: Identification and Analysis of Fossil Fuel Provisions There are a number of tax preferences, described

Montgomery County Nursing Home

County Nursing Home A Component Unit of County, Arkansas Accountants Report and Financial Statements County Nursing Home A Component Unit of County, Arkansas Contents Independent Accountants Report on

County Nursing Home A Component Unit of County, Arkansas Accountants Report and Financial Statements County Nursing Home A Component Unit of County, Arkansas Contents Independent Accountants Report on

THE MICHIGAN BUSINESS TAX (MBT)

") Note: As of January 1, 2012, the MBT has been replaced by the Michigan Corporate Income Tax (CIT). Businesses with certificated credits may still elect to file under the MBT structure. See the Michigan

Note: As of January 1, 2012, the MBT has been replaced by the Michigan Corporate Income Tax (CIT). Businesses with certificated credits may still elect to file under the MBT structure. See the Michigan

AS 10 : Accounting for Fixed Assets

AS 10 : Accounting for Fixed Assets IPCC Paper 1: Accounting Chapter 1 Unit 2 Fixed Assets - AS 10 Related ASI is 2 CA. Yagnesh Desai 1 Applicability This standards was introduced in 1985 It is applicable

AS 10 : Accounting for Fixed Assets IPCC Paper 1: Accounting Chapter 1 Unit 2 Fixed Assets - AS 10 Related ASI is 2 CA. Yagnesh Desai 1 Applicability This standards was introduced in 1985 It is applicable

WHITE CLOUD AREA FIRE DEPARTMENT JOINT BUILDING AUTHORITY NEWAYGO COUNTY, MICHIGAN ANNUAL FINANCIAL REPORT YEAR ENDED DECEMBER 31, 2013

WHITE CLOUD AREA FIRE DEPARTMENT JOINT BUILDING AUTHORITY NEWAYGO COUNTY, MICHIGAN ANNUAL FINANCIAL REPORT YEAR ENDED DECEMBER 31, 2013 TABLE OF CONTENTS INDEPENDENT AUDITOR'S REPORT 1 MANAGEMENT S DISCUSSION

WHITE CLOUD AREA FIRE DEPARTMENT JOINT BUILDING AUTHORITY NEWAYGO COUNTY, MICHIGAN ANNUAL FINANCIAL REPORT YEAR ENDED DECEMBER 31, 2013 TABLE OF CONTENTS INDEPENDENT AUDITOR'S REPORT 1 MANAGEMENT S DISCUSSION

Table of Contents. Volume No. 1 Policies and Procedures TOPIC NO 30210 - Cardinal Section No. 30200 Asset Acquisition TOPIC Acquisition Valuation

Table of Contents Overview...2 Introduction...2 Cardinal Transition Entries...2 Policy...3 General...3 Procedures...5 Acquisition Value...5 Valuation Methods...8 Salvage Value...8 Avoid Overstating Asset

Table of Contents Overview...2 Introduction...2 Cardinal Transition Entries...2 Policy...3 General...3 Procedures...5 Acquisition Value...5 Valuation Methods...8 Salvage Value...8 Avoid Overstating Asset

Before beginning any construction or demolition activities at your construction site,

VII. Hazardous Substances (Superfund Liability) Requirements for Construction Activities Before beginning any construction or demolition activities at your construction site, you should evaluate the site

VII. Hazardous Substances (Superfund Liability) Requirements for Construction Activities Before beginning any construction or demolition activities at your construction site, you should evaluate the site

A Guide for Used Oil Transporter Training Programs. Following are excerpts from laws and rules pertaining to Used Oil Transporter Certification

A Guide for Used Oil Transporter Training Programs Introduction An used oil transporter that transports over public highways more than 500 gallons of used oil annually, not including oily waste, must become

A Guide for Used Oil Transporter Training Programs Introduction An used oil transporter that transports over public highways more than 500 gallons of used oil annually, not including oily waste, must become

Fundamentals Level Skills Module, Paper F6 (MYS)

") Answers Fundamentals Level Skills Module, Paper F6 (MYS) Taxation (Malaysia) Judlee Sdn Bhd June 20 Answers and Marking Scheme Marks (a) Income tax computation Year of assessment 200 Net profit before

Answers Fundamentals Level Skills Module, Paper F6 (MYS) Taxation (Malaysia) Judlee Sdn Bhd June 20 Answers and Marking Scheme Marks (a) Income tax computation Year of assessment 200 Net profit before

MIDDLESEX LONDON EMERGENCY MEDICAL SERVICES AUTHORITY

Financial Statements of MIDDLESEX LONDON EMERGENCY MEDICAL SERVICES AUTHORITY Year ended December 31, 2013 Statement of Financial Position December 31, 2013, with comparative information for 2012 Financial

Financial Statements of MIDDLESEX LONDON EMERGENCY MEDICAL SERVICES AUTHORITY Year ended December 31, 2013 Statement of Financial Position December 31, 2013, with comparative information for 2012 Financial

GOVERNMENT OF YUKON. Financial Statement Discussion and Analysis for the year ended March 31, 2007

1 2 Introduction The Public Accounts is a major accountability report of the Government of Yukon (the Government). The purpose of the financial statement discussion and analysis is to expand upon and explain

1 2 Introduction The Public Accounts is a major accountability report of the Government of Yukon (the Government). The purpose of the financial statement discussion and analysis is to expand upon and explain

Fairfax County Solid Waste Management Objectives

Chapter 4 Fairfax County Solid Waste Management Objectives Incorporating the Overall Objectives for Fairfax County s Solid Waste Management Program in the SWMP This chapter presents the overall objectives

Chapter 4 Fairfax County Solid Waste Management Objectives Incorporating the Overall Objectives for Fairfax County s Solid Waste Management Program in the SWMP This chapter presents the overall objectives

Questions from Water Celebration Day

Questions from Water Celebration Day Julie Archer, WV Surface Owners Rights Organization What barriers inhibit surface owners or counties from simply repurchasing several leases, or offering to purchase

Questions from Water Celebration Day Julie Archer, WV Surface Owners Rights Organization What barriers inhibit surface owners or counties from simply repurchasing several leases, or offering to purchase

FUND ACCOUNTING TRAINING

FUND ACCOUNTING TRAINING Module 6 Plant Funds The University of Texas System OBJECTIVES Define each of the three subgroups of Plant Funds Describe sources and uses of funds for each subgroup Explain interrelationship

FUND ACCOUNTING TRAINING Module 6 Plant Funds The University of Texas System OBJECTIVES Define each of the three subgroups of Plant Funds Describe sources and uses of funds for each subgroup Explain interrelationship

Fund 110 Refuse Disposal

Division of Solid Waste Disposal and a Resource Recovery Transfer Station Operations Administration a Mission To protect Fairfax County citizens against disease, pollution and other contamination associated

Division of Solid Waste Disposal and a Resource Recovery Transfer Station Operations Administration a Mission To protect Fairfax County citizens against disease, pollution and other contamination associated

CHARLESTON COUNTY COMBINING STATEMENTS - INTERNAL SERVICE FUNDS

CHARLESTON COUNTY COMBINING STATEMENTS - Internal Service Funds are used to account for the financing of goods or services provided by one department or agency to other departments of the government, on

CHARLESTON COUNTY COMBINING STATEMENTS - Internal Service Funds are used to account for the financing of goods or services provided by one department or agency to other departments of the government, on

Understanding Business Insurance

Version 4.0 Preparation Date: 2 November 2009 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to business insurance.

Version 4.0 Preparation Date: 2 November 2009 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to business insurance.

Sample Due Diligence Checklist

Sample Due Diligence Checklist 01.0. CORPORATE ORGANIZATION AND HISTORY 1.1. - Overview of corporate legal structure, banking relationships (other than transaction financing), organizational charts and

Sample Due Diligence Checklist 01.0. CORPORATE ORGANIZATION AND HISTORY 1.1. - Overview of corporate legal structure, banking relationships (other than transaction financing), organizational charts and

TOWN OF MANCHESTER, MARYLAND. FINANCIAL STATEMENTS June 30, 2015

FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT... 1 MANAGEMENT S DISCUSSION AND ANALYSIS... 3 FINANCIAL STATEMENTS... 13 Government wide Financial Statements Statement of Net Position...14

FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT... 1 MANAGEMENT S DISCUSSION AND ANALYSIS... 3 FINANCIAL STATEMENTS... 13 Government wide Financial Statements Statement of Net Position...14

FLORIDA HIGH SCHOOL FOR ACCELERATED LEARNING - WEST PALM BEACH CAMPUS, INC. d/b/a QUANTUM HIGH SCHOOL

LEARNING - WEST PALM BEACH CAMPUS, INC. Financial Statements with Independent Auditors Reports Thereon June 30, 2015 CONTENTS Page Management s Discussion and Analysis 1 6 Report of Independent Auditors

LEARNING - WEST PALM BEACH CAMPUS, INC. Financial Statements with Independent Auditors Reports Thereon June 30, 2015 CONTENTS Page Management s Discussion and Analysis 1 6 Report of Independent Auditors

Uniform Accounting Network Inventory Manual. Table of Contents. Warranty Maintenance Debt Management Depreciation Disposal

Inventory Manual Uniform Accounting Network Inventory Manual Table of Contents Introduction Parts of the Manual Part 1 Assets Chapter 1 Acquisition Warranty Maintenance Debt Management Depreciation Disposal

Inventory Manual Uniform Accounting Network Inventory Manual Table of Contents Introduction Parts of the Manual Part 1 Assets Chapter 1 Acquisition Warranty Maintenance Debt Management Depreciation Disposal

Description of Fund Types and Funds

Financial activities for local government fall into three broad categories, governmental, proprietary, and fiduciary fund categories. Governmental funds are used to account for activities primarily supported

Financial activities for local government fall into three broad categories, governmental, proprietary, and fiduciary fund categories. Governmental funds are used to account for activities primarily supported

A Quick Guide to Municipal Financial Statements MUNICIPAL AFFAIRS

A Quick Guide to Municipal Financial Statements MUNICIPAL AFFAIRS June 2010 Alberta Municipal Affairs (2010) A Quick Guide to Municipal Financial Statements Edmonton: Alberta Municipal Affairs For more

A Quick Guide to Municipal Financial Statements MUNICIPAL AFFAIRS June 2010 Alberta Municipal Affairs (2010) A Quick Guide to Municipal Financial Statements Edmonton: Alberta Municipal Affairs For more

9.1 Draft Revenue and financing policy

1. Policy purpose and overview The purpose of the Revenue and financing policy is to provide predictability and certainty about sources and levels of funding available to the council. It explains the rationale

1. Policy purpose and overview The purpose of the Revenue and financing policy is to provide predictability and certainty about sources and levels of funding available to the council. It explains the rationale

Expenditure Accounting: Governmental Funds. Chapter 6

Expenditure Accounting: Governmental Funds Chapter 6 Learning Objectives Define expenditures Understand & apply expenditure recognition guidance Understand multiple classifications of expenditures Account

Expenditure Accounting: Governmental Funds Chapter 6 Learning Objectives Define expenditures Understand & apply expenditure recognition guidance Understand multiple classifications of expenditures Account

UNIFORM SYSTEM OF ACCOUNTS FOR WATER AND WASTEWATER UTILITIES

23-1 CHAPTER 23 UNIFORM SYSTEM OF ACCOUNTS FOR WATER AND WASTEWATER UTILITIES CLASSIFICATION OF WATER AND WASTEWATER UTILITIES Water and Wastewater Utility Classes (based on annual revenues): Class A:

23-1 CHAPTER 23 UNIFORM SYSTEM OF ACCOUNTS FOR WATER AND WASTEWATER UTILITIES CLASSIFICATION OF WATER AND WASTEWATER UTILITIES Water and Wastewater Utility Classes (based on annual revenues): Class A:

FORT MYERS BEACH MOSQUITO CONTROL DISTRICT. September 30, 2014 BASIC FINANCIAL STATEMENTS, TOGETHER WITH REPORTS OF INDEPENDENT AUDITORS

FORT MYERS BEACH MOSQUITO CONTROL DISTRICT September 30, 2014 BASIC FINANCIAL STATEMENTS, TOGETHER WITH REPORTS OF INDEPENDENT AUDITORS TABLE OF CONTENTS Report of the Independent Auditors 1-2 Management's

FORT MYERS BEACH MOSQUITO CONTROL DISTRICT September 30, 2014 BASIC FINANCIAL STATEMENTS, TOGETHER WITH REPORTS OF INDEPENDENT AUDITORS TABLE OF CONTENTS Report of the Independent Auditors 1-2 Management's

Chart of Accounts for Banks

Chart of Accounts for Banks ASSETS Cash and Cash Equivalents 1 0 0 1 Cash in vault 1 0 0 2 Cash in ATM 1 0 0 3 Cash in transit 1 0 0 4 Damaged notes 1 0 0 5 Travellers cheques 1 0 0 6 Items for collection:

Chart of Accounts for Banks ASSETS Cash and Cash Equivalents 1 0 0 1 Cash in vault 1 0 0 2 Cash in ATM 1 0 0 3 Cash in transit 1 0 0 4 Damaged notes 1 0 0 5 Travellers cheques 1 0 0 6 Items for collection:

Federal Facility Cleanup. Reggie Cheatham, Director Federal Facilities Restoration and Reuse Office

Federal Facility Cleanup Reggie Cheatham, Director Federal Facilities Restoration and Reuse Office NAS Best Practices Workshop January 9, 2014 Overview of Presentation Facts about Federal Facility Cleanup

Federal Facility Cleanup Reggie Cheatham, Director Federal Facilities Restoration and Reuse Office NAS Best Practices Workshop January 9, 2014 Overview of Presentation Facts about Federal Facility Cleanup

Understanding Business Insurance

Level 7,34 Charles St Parramatta Parramatt NSW 2150 PO Box 103 Parramatta NSW 2124 Phone: 02 9687 1966 Fax: 02 9635 3564 Web: www.carnegie.com.au Guide Build Protect Manage Wealth Understanding Business

Level 7,34 Charles St Parramatta Parramatt NSW 2150 PO Box 103 Parramatta NSW 2124 Phone: 02 9687 1966 Fax: 02 9635 3564 Web: www.carnegie.com.au Guide Build Protect Manage Wealth Understanding Business

Lee County Mosquito Control District

BASIC FINANCIAL STATEMENTS Year Ended September 30, 2014 Table of Contents September 30, 2014 TAB: REPORT Independent Auditors Report 1 Management Discussion and Analysis 4 TAB: BASIC FINANCIAL STATEMENTS

BASIC FINANCIAL STATEMENTS Year Ended September 30, 2014 Table of Contents September 30, 2014 TAB: REPORT Independent Auditors Report 1 Management Discussion and Analysis 4 TAB: BASIC FINANCIAL STATEMENTS

INSTRUCTIONS FOR COMPLETING BUDGET REQUEST FORM

1. 2. INSTRUCTIONS FOR COMPLETING BUDGET REQUEST FORM In accordance with the requirements of WS 16-4-104 The Department of Audit has modified the Standard Form. Please follow the steps below: a. Download

1. 2. INSTRUCTIONS FOR COMPLETING BUDGET REQUEST FORM In accordance with the requirements of WS 16-4-104 The Department of Audit has modified the Standard Form. Please follow the steps below: a. Download

ČEZ, a. s. BALANCE SHEET in accordance with IFRS as of June 30, 2014 in CZK Millions

BALANCE SHEET Assets Property, plant and equipment: 30. 6. 2014 31. 12. 2013 Plant in service 319 440 319 081 Less accumulated provision for depreciation (188 197) (182 282) Net plant in service 131 243

BALANCE SHEET Assets Property, plant and equipment: 30. 6. 2014 31. 12. 2013 Plant in service 319 440 319 081 Less accumulated provision for depreciation (188 197) (182 282) Net plant in service 131 243

Bridges of America - The Turning Point Bridge, Inc. Orlando, Florida

Bridges of America - The Turning Point Bridge, Inc. Orlando, Florida Financial Statements and Supplementary Information Year Ended June 30, 2014 Table of Contents Page Independent Auditor s Report 1 Financial

Bridges of America - The Turning Point Bridge, Inc. Orlando, Florida Financial Statements and Supplementary Information Year Ended June 30, 2014 Table of Contents Page Independent Auditor s Report 1 Financial

AUDIT REPORT OF THE NEBRASKA COMMISSION ON MEXICAN-AMERICANS JULY 1, 1999 THROUGH JUNE 30, 2000

AUDIT REPORT OF THE NEBRASKA COMMISSION ON MEXICAN-AMERICANS JULY 1, 1999 THROUGH JUNE 30, 2000 TABLE OF CONTENTS Page Background Information Section Background 1 Mission Statement 1 Organizational Chart

AUDIT REPORT OF THE NEBRASKA COMMISSION ON MEXICAN-AMERICANS JULY 1, 1999 THROUGH JUNE 30, 2000 TABLE OF CONTENTS Page Background Information Section Background 1 Mission Statement 1 Organizational Chart

CAPITAL ASSET/LONG TERM DEBT ACCOUNTING ENTRY EXAMPLES

NOTE: All items in RED are offsets between the governmental fund and the SWGF 80 or SWGF 90. ADDITIONS: CAPITAL ASSET/LONG TERM DEBT ACCOUNTING ENTRY EXAMPLES CAPITAL ASSET EXAMPLES A vehicle was purchased

NOTE: All items in RED are offsets between the governmental fund and the SWGF 80 or SWGF 90. ADDITIONS: CAPITAL ASSET/LONG TERM DEBT ACCOUNTING ENTRY EXAMPLES CAPITAL ASSET EXAMPLES A vehicle was purchased

The Application of International Accounting Standards in the Financial Statements of Tearfund Partners

The Application of International Accounting Standards in the Financial Statements of Tearfund Partners Context: International Accounting Standards (IAS) have been developed primarily to bring consistency

The Application of International Accounting Standards in the Financial Statements of Tearfund Partners Context: International Accounting Standards (IAS) have been developed primarily to bring consistency

This is Superfund. A Community Guide to EPA s Superfund Program

This is Superfund A Community Guide to EPA s Superfund Program IF THERE IS A SUPERFUND SITE in your neighborhood, you are probably wondering, what will happen? and, what can I do? This brochure will give

This is Superfund A Community Guide to EPA s Superfund Program IF THERE IS A SUPERFUND SITE in your neighborhood, you are probably wondering, what will happen? and, what can I do? This brochure will give

10 TIPS. for better Fleet Management WHITE PAPER. Who should read this paper? CEOs CFOs COOs Fleet managers Finance executives

WHITE PAPER 10 TIPS for better Fleet Management by Valério Marques CEO, Frotcom International Who should read this paper? CEOs CFOs COOs Fleet managers Finance executives This paper shows that with a few

WHITE PAPER 10 TIPS for better Fleet Management by Valério Marques CEO, Frotcom International Who should read this paper? CEOs CFOs COOs Fleet managers Finance executives This paper shows that with a few

2113 - Municipal Road Fund To account for County grant money used for various street projects approved through the county s municipal road fund.

General Fund and Extensions of the General Fund 1001 - General Operating Fund The general fund accounts for all financial resources except those required to be accounted for in another fund. The general

General Fund and Extensions of the General Fund 1001 - General Operating Fund The general fund accounts for all financial resources except those required to be accounted for in another fund. The general

Arizona 1. Dependent Public School Systems (14) Arizona ranks 39th among the states in number of local governments, with 639 as of June 2002.

Arizona ranks 39th among the states in number of local governments, with 639 as of June 2002.") Arizona Arizona ranks 39th among the states in number of local governments, with 639 as of June 2002. COUNTY GOVERNMENTS (15) There are no areas in Arizona lacking county government. The county governing

Arizona Arizona ranks 39th among the states in number of local governments, with 639 as of June 2002. COUNTY GOVERNMENTS (15) There are no areas in Arizona lacking county government. The county governing

KANABEC COUNTY ORDINANCE NO. 30

KANABEC COUNTY ORDINANCE NO. 30 CLEANUP OF CLANDESTINE DRUG LAB SITES ORDINANCE Kanabec County ARTICLE I. GENERAL PROVISIONS SECTION 1.10 SECTION 1.20 SECTION 1.30 SECTION 1.40 SECTION 1.50 SECTION 1.60

KANABEC COUNTY ORDINANCE NO. 30 CLEANUP OF CLANDESTINE DRUG LAB SITES ORDINANCE Kanabec County ARTICLE I. GENERAL PROVISIONS SECTION 1.10 SECTION 1.20 SECTION 1.30 SECTION 1.40 SECTION 1.50 SECTION 1.60

Smart & Final Stores, Inc. Reports First Quarter 2016 Financial Results

Smart & Final Stores, Inc. Reports First Quarter 2016 Financial Results COMMERCE, Calif. (May 3, 2016) Smart & Final Stores, Inc. (the Company ) (NYSE:SFS), the value-oriented food and everyday staples

Smart & Final Stores, Inc. Reports First Quarter 2016 Financial Results COMMERCE, Calif. (May 3, 2016) Smart & Final Stores, Inc. (the Company ) (NYSE:SFS), the value-oriented food and everyday staples

Chapter 1 Buying Assets

1 Chapter 1 2 Chapter 1 Buying Assets Introduction (What we already know from Intro Acct Class) 3 Intro Acct Class When Buying Bundle of Assets E.g. Purch of Shopping Center Buying Land & Building Allocate

1 Chapter 1 2 Chapter 1 Buying Assets Introduction (What we already know from Intro Acct Class) 3 Intro Acct Class When Buying Bundle of Assets E.g. Purch of Shopping Center Buying Land & Building Allocate

Identifying Environmental Aspects

Identifying Environmental Aspects How an organization interfaces with the environment Environmental Aspect: Element of an organization s activities, products, or services that can interact with the environment.

Identifying Environmental Aspects How an organization interfaces with the environment Environmental Aspect: Element of an organization s activities, products, or services that can interact with the environment.

Town of Clinton Budget Recommendations

Town of Clinton Budget Recommendations Fiscal Year 2016 July 1, 2015 June 30, 2016 20-May-15 Fiscal Year 2015 Fiscal Year 2016 114 - Moderator Moderator Salary 100.00 100.00 Moderator Misc. Expense 50.00

Town of Clinton Budget Recommendations Fiscal Year 2016 July 1, 2015 June 30, 2016 20-May-15 Fiscal Year 2015 Fiscal Year 2016 114 - Moderator Moderator Salary 100.00 100.00 Moderator Misc. Expense 50.00

Actual Nonmajor Special Revenue Funds --------------------------------------------------------- 34

CONTENTS: FLORIDA DEPARTMENT OF EDUCATION SUPERINTENDENT S ANNUAL FINANCIAL REPORT (ESE 145) DISTRICT SCHOOL BOARD OF SUMTER COUNTY For the Fiscal Year Ended June 30, 2015 Return completed form to: Florida

CONTENTS: FLORIDA DEPARTMENT OF EDUCATION SUPERINTENDENT S ANNUAL FINANCIAL REPORT (ESE 145) DISTRICT SCHOOL BOARD OF SUMTER COUNTY For the Fiscal Year Ended June 30, 2015 Return completed form to: Florida

Intercompany Indebtedness. Chapter 8. Intercompany Indebtedness. Consolidation Overview. Consolidation Overview. Intercompany Indebtedness

Chapter 8 Intercompany Indebtedness Intercompany Indebtedness One advantage of having control over other companies is that management has the ability to transfer resources from one legal entity to another

Chapter 8 Intercompany Indebtedness Intercompany Indebtedness One advantage of having control over other companies is that management has the ability to transfer resources from one legal entity to another

City of Villa Rica. The Mill Amphitheater in Villa Rica, GA Photo Credit: Michael Valentine

City of Villa Rica The Mill Amphitheater in Villa Rica, GA Photo Credit: Michael Valentine CITY OF VILLA RICA, GEORGIA ANNUAL FINANCIAL REPORT For the Year Ended December 31, 2015 CITY OF VILLA RICA, GEORGIA

City of Villa Rica The Mill Amphitheater in Villa Rica, GA Photo Credit: Michael Valentine CITY OF VILLA RICA, GEORGIA ANNUAL FINANCIAL REPORT For the Year Ended December 31, 2015 CITY OF VILLA RICA, GEORGIA

GENERAL INSTRUCTIONS: ANNUAL FINANCIAL REPORT (CNPweb) National School Lunch, School Breakfast Programs 1/09

National School Lunch, School Breakfast Programs 1/09") GENERAL INSTRUCTIONS: ANNUAL FINANCIAL REPORT (CNPweb) National School Lunch, School Breakfast Programs 1/09 These are general guidelines for the online Annual Financial Report (AFR), explaining only the

GENERAL INSTRUCTIONS: ANNUAL FINANCIAL REPORT (CNPweb) National School Lunch, School Breakfast Programs 1/09 These are general guidelines for the online Annual Financial Report (AFR), explaining only the

Budget Process. Budget Calendar. The City s fiscal year is July 1 through June 30.

Budget Process The City s fiscal year is July 1 through June 30. To establish the budget, the Finance Department develops a plan for expenditure of projected available resources for the coming fiscal year.

Budget Process The City s fiscal year is July 1 through June 30. To establish the budget, the Finance Department develops a plan for expenditure of projected available resources for the coming fiscal year.

STORAGE NAME: h0781.elt.doc DATE: January 22, 2002 HOUSE OF REPRESENTATIVES COMMITTEE ON ELDER & LONG TERM CARE ANALYSIS BILL #: HB 781

HOUSE OF REPRESENTATIVES COMMITTEE ON ELDER & LONG TERM CARE ANALYSIS BILL #: HB 781 RELATING TO: SPONSOR(S): Continuing Care Retirement Communities Representative(s) Green & Others TIED BILL(S): ORIGINATING

HOUSE OF REPRESENTATIVES COMMITTEE ON ELDER & LONG TERM CARE ANALYSIS BILL #: HB 781 RELATING TO: SPONSOR(S): Continuing Care Retirement Communities Representative(s) Green & Others TIED BILL(S): ORIGINATING

The California State University GAAP Reporting Manual Effective June 2012 CHAPTER 6 STATEMENT OF CASH FLOWS

CHAPTER 6 STATEMENT OF CASH FLOWS OVERVIEW GASB Statement No. 34 requires the presentation of a statement of cash flows based on the provisions of GASB Statement No. 9. It further requires the use of the

CHAPTER 6 STATEMENT OF CASH FLOWS OVERVIEW GASB Statement No. 34 requires the presentation of a statement of cash flows based on the provisions of GASB Statement No. 9. It further requires the use of the

Municipal Accounting Manual

Municipal Accounting Manual March 2013 Updated: November 2015 1 Table of Contents Introduction......1 Municipal Financial Statements Overview...... 2 Municipal financial statement purpose...... 2 Municipal

Municipal Accounting Manual March 2013 Updated: November 2015 1 Table of Contents Introduction......1 Municipal Financial Statements Overview...... 2 Municipal financial statement purpose...... 2 Municipal

FLORIDA STATE COLLEGE AT JACKSONVILLE PATHWAYS ACADEMY A Charter School and Restricted Fund of Florida State College at Jacksonville

FLORIDA STATE COLLEGE AT JACKSONVILLE PATHWAYS ACADEMY A Charter School and Restricted Fund of Florida State College at Jacksonville NOTES TO FINANCIAL STATEMENTS Year Ended June 30, 2014 Note 1 - Nature

FLORIDA STATE COLLEGE AT JACKSONVILLE PATHWAYS ACADEMY A Charter School and Restricted Fund of Florida State College at Jacksonville NOTES TO FINANCIAL STATEMENTS Year Ended June 30, 2014 Note 1 - Nature

EXERCISES. The cash from operating activities detail is provided as follows for class discussion:

EXERCISES Ex. 14 1 There were net additions, such as depreciation and amortization of intangible assets of $389 million, to the net loss reported on the income statement to convert the net loss from the

EXERCISES Ex. 14 1 There were net additions, such as depreciation and amortization of intangible assets of $389 million, to the net loss reported on the income statement to convert the net loss from the

TABLE OF CONTENTS CHAPTER 9

TABLE OF CONTENTS CHAPTER 9 Purpose...1 Balance Sheet Accounts...1 Assets...1 Cash...1 Accounts Receivable...2 Accounts Receivable Allowances...4 Loans and Notes Receivable...4 Loans and Notes Allowances...5

TABLE OF CONTENTS CHAPTER 9 Purpose...1 Balance Sheet Accounts...1 Assets...1 Cash...1 Accounts Receivable...2 Accounts Receivable Allowances...4 Loans and Notes Receivable...4 Loans and Notes Allowances...5

A PRACTICAL GUIDE TO WRITING A BUSINESS PLAN

A PRACTICAL GUIDE TO WRITING A BUSINESS PLAN Louisiana Small Business Development Center At Southeastern Louisiana University 1514 Martens Drive Hammond, LA 70401 Phone: (985) 549-3831 Fax: (985) 549-2127

A PRACTICAL GUIDE TO WRITING A BUSINESS PLAN Louisiana Small Business Development Center At Southeastern Louisiana University 1514 Martens Drive Hammond, LA 70401 Phone: (985) 549-3831 Fax: (985) 549-2127

RELOCATION ASSISTANCE BUSINESSES, FARMS, AND NON-PROFIT ORGANIZATIONS

RELOCATION ASSISTANCE BUSINESSES, FARMS, AND NON-PROFIT ORGANIZATIONS STATE OF FLORIDA DEPARTMENT OF TRANSPORTATION HAYDON BURNS BUILDING 605 SUWANNEE STREET TALLAHASSEE, FLORIDA 32399-0450 October 1,

RELOCATION ASSISTANCE BUSINESSES, FARMS, AND NON-PROFIT ORGANIZATIONS STATE OF FLORIDA DEPARTMENT OF TRANSPORTATION HAYDON BURNS BUILDING 605 SUWANNEE STREET TALLAHASSEE, FLORIDA 32399-0450 October 1,