International Master Economics and Finance

|

|

|

- Hilary Burns

- 7 years ago

- Views:

Transcription

1 International Master Economics and Finance Mario Bellia Pricing Derivatives using Bloomberg Professional Service 03/2013

2 IRS Summary FRA Plain vanilla swap Amortizing swap Cap, Floor, Digital Options and Dual Digital Options Example: a real contract OPTIONS Call Bull Spread Bear Spread Calendar Spread Straddle Strangle 2

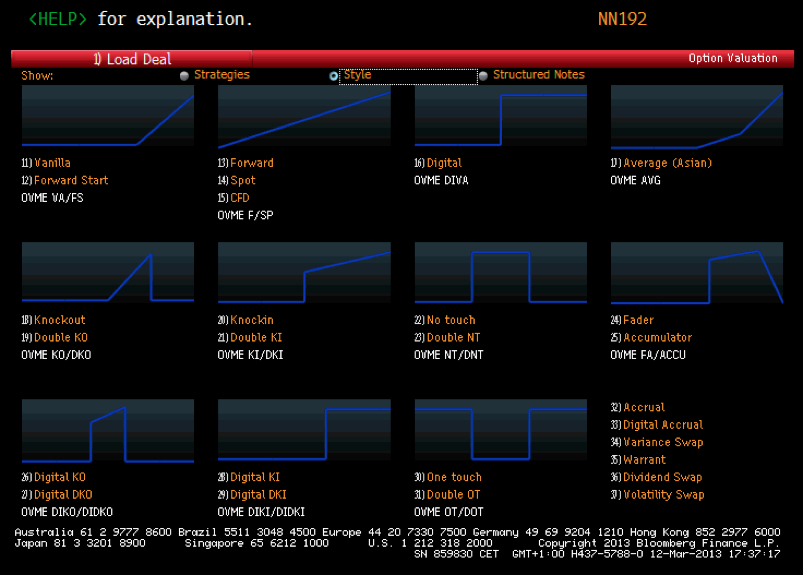

3 Functions in Bloomberg Two applications will be used in Bloomberg to evaluate derivatives: SWPM <GO> Swap Manager SWPM is the main interest rate derivatives pricing function in the Bloomberg professional System, allowing users to price a wide range of vanilla and exotic interest rate swaps, interest rate options, swaptions and interest rate and hybrid structured notes. OVME <GO> Options Valuation OVME is Bloomberg main pricing application for options on equity, indexes, funds, bonds, bond futures and short term interest rate futures. 3

4 Part I INTEREST RATE SWAP 4

5 Forward Rate Agreement A forward rate agreement (FRA) is an agreement that a certain rate will apply to a certain principal during a certain future time period FRAs are infinitely flexible over-the-counter instruments (OTCs), as they can be structured to mature on any date. In general, FRAs are traded on the future level of 3 or 6 month Libor (Euribor). An FRA is an Off Balance Sheet instrument. 5

6 How to price a FRA FRAs can be valued in SWPM as: a Spot start IMM date (International Money Market) third Wednesday of March, June, September and December Broken date (customized Start and end dates) Example: Suppose you enter in a FRA today, receiving a fixed rate for a 3- month period, starting in 3 months. Principal: Rate: 0.18% Today: March 14, 2013 Effective: June 18, 2013 Maturity: Sept 18,

7 How to price a FRA Lender receives difference of 0.18% and reset rate in 3 Months 7

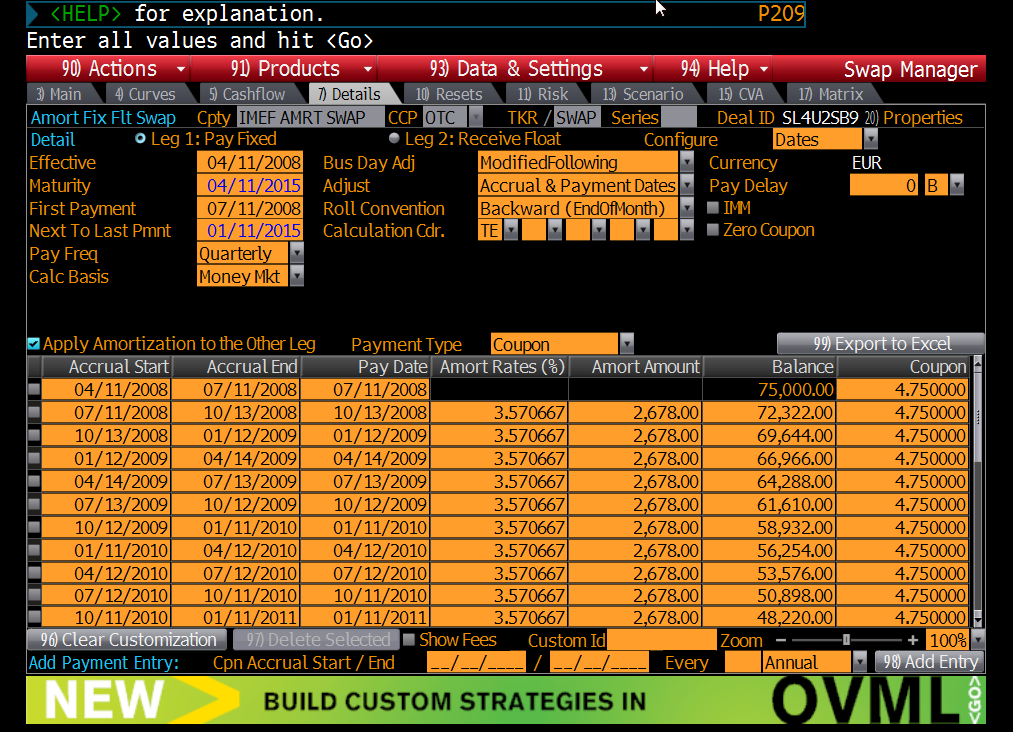

8 Plain vanilla Swaps A plain Vanilla interest rate swap is an agreement between two counterparties to exchange cash flows (Fixed vs. Float) in the same currency. The payments are made during the life of the swap in the frequency that was pre-established. In an interest rate swap the principal is not exchanged Used to convert a liability from fixed rate to floating rate floating rate to fixed rate With SWPM, one can configure many details of the deal, such as Dates, amortization scheme, start and end of a single payment 8

9 Valuation of Swaps The standard approach is to assume that forward rates will be realized This works for plain vanilla interest rate and plain vanilla currency swaps, but does not necessarily work for non-standard swaps 9

10 How to price a plain vanilla Swaps Run SWPM EUR <GO> In order to display SWPM in EURO currency. Enter the details of the IRS, in our example: Notional ,00 Receive Fixed % Pay Float rate EURIBOR 6M Contract starts March 18, 2013 Maturity is March 18, 2016 (3Y) Payments are quarterly (in advance) 10

11 How to price a plain vanilla Swaps 11

12 Example of the Book An agreement by Microsoft to receive 6-month LIBOR & pay a fixed rate of 5% per annum every 6 months for 3 years on a notional principal of $100 million Millions of Dollars LIBOR FLOATING FIXED Net Date Rate Cash Flow Cash Flow Cash Flow Mar. 5, % Sept. 5, % Mar. 5, % Sept. 5, % Mar. 5, % Sept. 5, % Mar. 5, %

13 Example of the Book 13

14 Example of the Book 14

15 Amortizing swap Can be either Fixed-versus-Float or Float-versus- Float. Both counterparties make interest payments that either are declining (amortizing) or accreting (increasing) over the life of the deal. Example: Notional ,00 Pay Fixed 4. 75% Receive Float EURIBOR 3M Contract starts April 11, 2008 Maturity is April 11,, 2015 (7Y) Payments frequency: quarterly 15

16 Amortizing swap Amortization scheme: Notional Start End Days 75'000,00 11/04/ /07/ '322,00 11/07/ /10/ '644,00 13/10/ /01/ '966,00 12/01/ /04/ '288,00 14/04/ /07/ '610,00 13/07/ /10/ '932,00 12/10/ /01/ '254,00 11/01/ /04/ '576,00 12/04/ /07/ '898,00 12/07/ /10/ '220,00 11/10/ /01/ '542,00 11/01/ /04/ '864,00 11/04/ /07/ '186,00 11/07/ /10/ '508,00 11/10/ /01/ '830,00 11/01/ /04/ '152,00 11/04/ /07/ '474,00 11/07/ /10/ '796,00 11/10/ /01/ '118,00 11/01/ /04/ '440,00 11/04/ /07/ '762,00 11/07/ /10/ '084,00 11/10/ /01/ '406,00 13/01/ /04/ '728,00 11/04/ /07/ '050,00 11/07/ /10/ '372,00 13/10/ /01/ '694,00 12/01/ /04/

17 Amortizing swap 17

18 Amortizing swap 18

19 Caps and Floors A cap is a portfolio of call options on a reference interest rate (i.e EURIBOR or LIBOR). It has the effect of guaranteeing that the interest rate in each of a number of future periods will not rise above a certain level Each call is called caplet, so a cap is a portfolio of caplets A floor is similarly a portfolio of put options. For this (and others) derivatives, one of the input is the volatility, that can be choose between flat volatility (manual input) and VCUB volatilities. (VCUB is available hitting VCUB <GO>) 19

20 Caps and Floors Example: Notional ,00 Receive Fixed % Pay Float rate EURIBOR 6M Contract starts March 18, 2013 Maturity is March 18, 2016 (3Y) Payments are quarterly (in advance) 20

21 Caps and Floors 21

22 Caps and Floors In order to change from Cap to Floor, select the appropriate deal from the dropdown menu: 22

23 Digital options An option whose payout is fixed after the underlying exceeds the predetermined threshold or strike price. It is also referred to as "binary" or "all-or-nothing option." A digital cap is a cap option that provides a payoff of specified coupon R% when strike K <= the floating rate. A digital floor is a floor option that provides a payoff of specified coupon R% when strike K >= the floating rate. Digitals provide the buyer with a fixed payout profile. This means that the buyer receives the same payout irrespective of how far above or below the Index reaches in relation to the strike. Digitals are cheaper to buy than standard options. 23

24 Digital cap Digital options 0.5% when strike 2% <= the floating rate. 24

25 Digital floor Digital options 0.5% when strike 2% >= the floating rate. 25

26 Dual Digital options The receiver of this exotic payoff will obtain either of 2 alternative payoffs decided upfront. The payoff to be received at each coupon date will depend from the level of the observation index immediately before the coupon payment date: a) If the index is above a pre-determined level (barrier), an A) payoff will be paid. b) If the index is below a pre-determined level, a B) payoff will be paid The two payoff can be either fixed rate, float rate, float rate minus (or plus) a spread. 26

27 Dual Digital options Example: Notional ,00 Barrier 0.5% Reference rate: EURIBOR 6M Contract starts March 18, 2013 Maturity March 18, 2016 (3Y) Payments are quarterly (in advance) Payoff a) If EUR6M >= Barrier EUR6M + 0.5% b) If EUR6M < Barrier Fixed rate 0.32% 27

28 Dual Digital options 28

29 In Arrears Swap Rate is observed at time t i and paid at time t i rather than time t i+1 It is necessary to make a convexity adjustment to each forward rate underlying the swap Suppose that F i is the forward rate between time t i and t i+1 and i is its volatility We should increase F i by F 2 i 2 i ( ti 1 1 F i i t i ) t i when valuing a in-arrears swap 29

30 Example of a contract Company Alpha decide to join a IRS with Bank Beta. (Notional is ,00 ) BANK PAYS: - From March 28, 2006 to March 28, 2007 EURIBOR 6M - From March 28, 2007 to March 28, 2009 EURIBOR 6M if EURIBOR 6M is less than 3.85% 4.35% if EURIBOR 6M is greater or equal to 3.85% ALPHA PAYS - From March 28, 2006 to March 28, 2007 EURIBOR 6M minus spread 0,1% with a max of 6,75%. - From March 28, 2007 to March 28, 2009 If EURIBOR 6M will be less than 3.85%, the rate will be 3,45%. If EURIBOR 6M will be greter or equal than 3.85%, rate will be EURIBOR 6M with a max of 6.75% 30

31 BANK PAYS: From March 28, 2006 to March 28, 2007 EURIBOR 6M Example of a contract ALPHA PAYS From March 28, 2006 to March 28, 2007 EURIBOR 6M minus spread 0,1% with max of 6,75%. From March 28, 2007 to March 28, 2009 EURIBOR 6M if EURIBOR 6M is less than 3.85% 4.35% if EURIBOR 6M is greater or equal to 3.85% From March 28, 2007 to March 28, 2009 If EURIBOR 6M less than 3.85%, the rate will be 3,45%. If EURIBOR 6M greter or equal than 3.85%, rate will be EURIBOR 6M with a max of 6.75% Bank Flows (Period 1) Alpha Flows (Period 1) EURIBOR 6M EURIBOR 6M - 0,10% with a max of 6.75% EUR 6M Floating Rate EUR 6M Floating Rate -0.10% Spread max (EU-6.85%;0) - Cap Bank Flows (Period 2) Alpha Flows (Period 2) EUR 6M if EUR6M < Barrier 3,85% 3.45% if EUR6M < Barrier 3,85% 4,25% if EUR6M >= Barrier 3,85% EUR 6M if EUR6M >= Barrier 3,85% with a max of 6.75% EUR 6M Floating Rate EUR 6M Floating Rate 0.40% se EU>=3.85% + Digital Cap MAX(3.85%-EU;0) Floor MAX(EU-3.85%;0) - Cap 0.40% se EU<3.85% - Digital Floor MAX(EU-6.75%;0) - Cap 31

32 Example of a contract - Payoff 32

33 Example of a contract - Valuation 33

34 Example of a contract - Valuation Expected Flows (discounted) Bank Period Floating rate 1 45'996,75 Digital Cap ,76 -cap ,97 tot 43'684,54 Alpha Period Float rate - spread 1 44'510,69 -cap 1 0,00 Floor 2 14'481,42 -Digital Floor 2-7'858,61 -Cap 2-137,31 tot 50'996,19 Valuation -7'311,65 34

35 Example of a contract:multi Leg Deal Expected Flows (discounted) Bank Period Digital Cap ,76 -cap ,97 tot -2'312,21 Alpha Period Floor 2 14'481,42 -Digital Floor 2-7'858,61 -Cap 2-137,32 Valuation -8'797,70 tot 6'485,49 35

36 Other swaps Floating-for-floating interest rate swaps, step up swaps, forward swaps, constant maturity swaps, compounding swaps,, accrual swaps, diff swaps, cross currency interest rate swaps, equity swaps, extendable swaps, puttable swaps, swaptions, commodity swaps, volatility swaps.. 36

37 Part II OPTIONS 37

38 Option Types A call is an option to buy A put is an option to sell A European option can be exercised only at the end of its life An American option can be exercised at any time Assets Underlying Exchange-Traded Options Stocks Foreign Currency Stock Indices Futures 38

39 Call and Put Options Profits Long Call Buy one European call option: price = $5 strike price = $100 Short Call Write one European call option: price = $5 strike price = $100 Long Put Buy one European put option: price = $7 strike price = $70 Short Put Write one European put option: price = $7 strike price = $70 39

40 OVME: basic settings Underlying: indicate the desired Equity ticker followed by the Equity key, Index ticker followed by Index key, or Fund, ETFs and Hedge Funds ticker followed by Equity key. Direction: indicate 'B' for Buy, 'S' for Sell. Style: specific kind of option Exercise: indicate 'AM' for American, 'EU' for European. Call/put and Strike Level: Indicate 'C' for Call, 'P' for Put Strike Moneyness: Indicate Strike in % Moneyness.o A indicates At the Moneyo ni indicates n% In the Moneyo no indicates n% Out of the Money Expiry Date: Expiry date can be any date in the future. Number of shares: The letter N (number of shares) with a number (you can abbreviate K for thousand, M for million. Model: for standard vanilla contract, can be BS Continuous, BS Discrete, Local Vol, Trinomial (see methods, next slide) Volatility: BVOL (Bloomberg Surface) or Historical 40

41 Methods used to price an option 41

Then, run OVME SL <GO> to a single leg deal.")

42 Single leg (or vanilla deal) First of all, select the underlying (Stocks, Stock Indices, Foreign Currency, Futures..) Then, run OVME SL <GO> to a single leg deal. Example Underlying: UNICREDIT Deal: EUROPEAN CALL OPTION Price Today: 3,806 Strike price: 4,4 Expire: May 14, 2013 (60 days) Position in shares:

43 Historical Line chart of underlying 43

44 Valuation of a European Call 44

45 Trading Strategies Involving Options: Types of Strategies Take a position in the option and the underlying Take a position in 2 or more options of the same type (spread) Take a position in a mixture of calls & puts (combination) 45

46 Spreads Options in Bloomberg Strategies involving spreads (i.e. same type of options) are available in: Products - Options Strategies - Call/Put Spread 46

47 Bull Spread Using Calls Buy a Call Option with a certain strike price and sell a call option with a higher strike, on the same underlying. View: price increase Example Underlying: UNICREDIT Deal: EUROPEAN CALL OPTIONS Price Today: 3,806 Strike price BUY: 3,807 Strike price SELL: 4,400 Expire: May 14, 2013 (60 days) Position in shares:

48 Bull Spread Using Calls 48

49 Bear Spread Using Puts Buy a put with a certain strike price and sell a put with a lower strike, on the same underlying. View: price decline Example Underlying: UNICREDIT Deal: EUROPEAN PUT OPTIONS Price Today: 3,806 Strike price BUY: 4,400 Strike price SELL: 3,807 Expire: May 14, 2013 (60 days) Position in shares:

50 Bear Spread Using Puts 50

51 Calendar Spread using calls Options have the same strike price, but different expiration dates. Strategy is sell a call and buy one with a longer maturity Example Underlying: UNICREDIT Deal: Calendar Spread Price Today: 3,806 Strike price : 4,000 Expire 1: May 14, 2013 (60 days) Expire 2: July 14, 2013 (120 days) Position in shares:

52 Calendar Spread using calls 52

53 Straddle Buy a call and a put with the same strike price and expiration date. Appropriate if a large move of the price is expected, but the direction is unknow. Example Underlying: UNICREDIT Deal: STRADDLE Price Today: 3,806 Strike price : 4,000 Expire 1: May 14, 2013 (60 days) Position in shares:

54 Straddle 54

55 Strangle Buy a call and a put with the same expiration date but different strike price. Appropriate if a large move of the price is expected, but the direction is unknow. The call strike is higher than the put strike. Example Underlying: UNICREDIT Deal: STRADDLE Price Today: 3,806 Strike price CALL : 4,400 Strike price PUT: 3,870 Expire 1: May 14, 2013 (60 days) Position in shares:

56 Strangle 56

57 Strategies 57

58 Styles 58

59 Structured notes 59

1.2 Structured notes

1.2 Structured notes Structured notes are financial products that appear to be fixed income instruments, but contain embedded options and do not necessarily reflect the risk of the issuing credit. Used

1.2 Structured notes Structured notes are financial products that appear to be fixed income instruments, but contain embedded options and do not necessarily reflect the risk of the issuing credit. Used

Introduction to Derivative Instruments Part 1

Link n Learn Introduction to Derivative Instruments Part 1 Leading Business Advisors Contacts Elaine Canty - Manager Financial Advisory Ireland Email: ecanty@deloitte.ie Tel: 00 353 417 2991 2991 Guillaume

Link n Learn Introduction to Derivative Instruments Part 1 Leading Business Advisors Contacts Elaine Canty - Manager Financial Advisory Ireland Email: ecanty@deloitte.ie Tel: 00 353 417 2991 2991 Guillaume

Swaps: complex structures

Swaps: complex structures Complex swap structures refer to non-standard swaps whose coupons, notional, accrual and calendar used for coupon determination and payments are tailored made to serve client

Swaps: complex structures Complex swap structures refer to non-standard swaps whose coupons, notional, accrual and calendar used for coupon determination and payments are tailored made to serve client

Advanced Derivatives:

Advanced Derivatives: (plain vanilla to Rainbows) advanced swaps Structured notes exotic options Finance 7523. Spring 1999 The Neeley School of Business at TCU Steven C. Mann, 1999. Equity Swaps Example:

Advanced Derivatives: (plain vanilla to Rainbows) advanced swaps Structured notes exotic options Finance 7523. Spring 1999 The Neeley School of Business at TCU Steven C. Mann, 1999. Equity Swaps Example:

Interest rate Derivatives

Interest rate Derivatives There is a wide variety of interest rate options available. The most widely offered are interest rate caps and floors. Increasingly we also see swaptions offered. This note will

Interest rate Derivatives There is a wide variety of interest rate options available. The most widely offered are interest rate caps and floors. Increasingly we also see swaptions offered. This note will

Introduction to Derivative Instruments Part 1 Link n Learn

Introduction to Derivative Instruments Part 1 Link n Learn June 2014 Webinar Participants Elaine Canty Manager Financial Advisory Deloitte & Touche Ireland ecanty@deloitte.ie +353 1 417 2991 Christopher

Introduction to Derivative Instruments Part 1 Link n Learn June 2014 Webinar Participants Elaine Canty Manager Financial Advisory Deloitte & Touche Ireland ecanty@deloitte.ie +353 1 417 2991 Christopher

Equity-index-linked swaps

Equity-index-linked swaps Equivalent to portfolios of forward contracts calling for the exchange of cash flows based on two different investment rates: a variable debt rate (e.g. 3-month LIBOR) and the

Equity-index-linked swaps Equivalent to portfolios of forward contracts calling for the exchange of cash flows based on two different investment rates: a variable debt rate (e.g. 3-month LIBOR) and the

1. BGC Derivative Markets, L.P. Contract Specifications... 2 1.1 Product Descriptions... 2 1.1.1 Mandatorily Cleared CEA 2(h)(1) Products as of 2nd

(1) Products as of 2nd") 1. BGC Derivative Markets, L.P. Contract Specifications............................................................... 2 1.1 Product Descriptions.....................................................................................

1. BGC Derivative Markets, L.P. Contract Specifications............................................................... 2 1.1 Product Descriptions.....................................................................................

Instructions and Guide for Pricing and Valuation of Interest Rate Swap Lab

Instructions and Guide for Pricing and Valuation of Interest Rate Swap Lab FINC413 Lab c 2014 Paul Laux and Huiming Zhang 1 Introduction 1.1 Overview In this lab, you will learn basic idea of meanings

Instructions and Guide for Pricing and Valuation of Interest Rate Swap Lab FINC413 Lab c 2014 Paul Laux and Huiming Zhang 1 Introduction 1.1 Overview In this lab, you will learn basic idea of meanings

Swaps. You can drag and drop the push pin on the top right corner to Excel to download data.

Swaps This session is designed to demonstrate how you can monitor current market rates, view and set defaults for swap curves and volatility, and value an interest rate swap and other swaps. Please go

Swaps This session is designed to demonstrate how you can monitor current market rates, view and set defaults for swap curves and volatility, and value an interest rate swap and other swaps. Please go

Derivatives Interest Rate Futures. Professor André Farber Solvay Brussels School of Economics and Management Université Libre de Bruxelles

Derivatives Interest Rate Futures Professor André Farber Solvay Brussels School of Economics and Management Université Libre de Bruxelles Interest Rate Derivatives Forward rate agreement (FRA): OTC contract

Derivatives Interest Rate Futures Professor André Farber Solvay Brussels School of Economics and Management Université Libre de Bruxelles Interest Rate Derivatives Forward rate agreement (FRA): OTC contract

Risk Management and Governance Hedging with Derivatives. Prof. Hugues Pirotte

Risk Management and Governance Hedging with Derivatives Prof. Hugues Pirotte Several slides based on Risk Management and Financial Institutions, e, Chapter 6, Copyright John C. Hull 009 Why Manage Risks?

Risk Management and Governance Hedging with Derivatives Prof. Hugues Pirotte Several slides based on Risk Management and Financial Institutions, e, Chapter 6, Copyright John C. Hull 009 Why Manage Risks?

FX, Derivatives and DCM workshop I. Introduction to Options

Introduction to Options What is a Currency Option Contract? A financial agreement giving the buyer the right (but not the obligation) to buy/sell a specified amount of currency at a specified rate on a

Introduction to Options What is a Currency Option Contract? A financial agreement giving the buyer the right (but not the obligation) to buy/sell a specified amount of currency at a specified rate on a

Options Markets: Introduction

Options Markets: Introduction Chapter 20 Option Contracts call option = contract that gives the holder the right to purchase an asset at a specified price, on or before a certain date put option = contract

Options Markets: Introduction Chapter 20 Option Contracts call option = contract that gives the holder the right to purchase an asset at a specified price, on or before a certain date put option = contract

The market for exotic options

The market for exotic options Development of exotic products increased flexibility for risk transfer and hedging highly structured expression of expectation of asset price movements facilitation of trading

The market for exotic options Development of exotic products increased flexibility for risk transfer and hedging highly structured expression of expectation of asset price movements facilitation of trading

Over-the-counter (OTC) options market conventions

options market conventions") Over-the-counter (OTC) options market conventions This article details the conventions used for Over the Counter options1. These conventions are important; as a very substantial amount of traded derivatives

Over-the-counter (OTC) options market conventions This article details the conventions used for Over the Counter options1. These conventions are important; as a very substantial amount of traded derivatives

Bank of America AAA 10.00% T-Bill +.30% Hypothetical Resources BBB 11.90% T-Bill +.80% Basis point difference 190 50

Swap Agreements INTEREST RATE SWAP AGREEMENTS An interest rate swap is an agreement to exchange interest rate payments on a notional principal amount over a specific period of time. Generally a swap exchanges

Swap Agreements INTEREST RATE SWAP AGREEMENTS An interest rate swap is an agreement to exchange interest rate payments on a notional principal amount over a specific period of time. Generally a swap exchanges

Lecture 12. Options Strategies

Lecture 12. Options Strategies Introduction to Options Strategies Options, Futures, Derivatives 10/15/07 back to start 1 Solutions Problem 6:23: Assume that a bank can borrow or lend money at the same

Lecture 12. Options Strategies Introduction to Options Strategies Options, Futures, Derivatives 10/15/07 back to start 1 Solutions Problem 6:23: Assume that a bank can borrow or lend money at the same

w w w.c a t l e y l a k e m a n.c o m 0 2 0 7 0 4 3 0 1 0 0

A ADR-Style: for a derivative on an underlying denominated in one currency, where the derivative is denominated in a different currency, payments are exchanged using a floating foreign-exchange rate. The

A ADR-Style: for a derivative on an underlying denominated in one currency, where the derivative is denominated in a different currency, payments are exchanged using a floating foreign-exchange rate. The

TREATMENT OF PREPAID DERIVATIVE CONTRACTS. Background

Traditional forward contracts TREATMENT OF PREPAID DERIVATIVE CONTRACTS Background A forward contract is an agreement to deliver a specified quantity of a defined item or class of property, such as corn,

Traditional forward contracts TREATMENT OF PREPAID DERIVATIVE CONTRACTS Background A forward contract is an agreement to deliver a specified quantity of a defined item or class of property, such as corn,

ASSET LIABILITY MANAGEMENT Significance and Basic Methods. Dr Philip Symes. Philip Symes, 2006

1 ASSET LIABILITY MANAGEMENT Significance and Basic Methods Dr Philip Symes Introduction 2 Asset liability management (ALM) is the management of financial assets by a company to make returns. ALM is necessary

1 ASSET LIABILITY MANAGEMENT Significance and Basic Methods Dr Philip Symes Introduction 2 Asset liability management (ALM) is the management of financial assets by a company to make returns. ALM is necessary

Accounting for Derivatives. Rajan Chari Senior Manager rchari@deloitte.com

Accounting for Derivatives Rajan Chari Senior Manager rchari@deloitte.com October 3, 2005 Derivative Instruments to be Discussed Futures Forwards Options Swaps Copyright 2004 Deloitte Development LLC.

Accounting for Derivatives Rajan Chari Senior Manager rchari@deloitte.com October 3, 2005 Derivative Instruments to be Discussed Futures Forwards Options Swaps Copyright 2004 Deloitte Development LLC.

Introduction to Fixed Income (IFI) Course Syllabus

Course Syllabus") Introduction to Fixed Income (IFI) Course Syllabus 1. Fixed income markets 1.1 Understand the function of fixed income markets 1.2 Know the main fixed income market products: Loans Bonds Money market instruments

Introduction to Fixed Income (IFI) Course Syllabus 1. Fixed income markets 1.1 Understand the function of fixed income markets 1.2 Know the main fixed income market products: Loans Bonds Money market instruments

Standard Financial Instruments in Tatra banka, a.s. and the Risks Connected Therewith

Standard Financial Instruments in Tatra banka, a.s. and the Risks Connected Therewith 1. Shares Description of Shares Share means a security which gives to the holder of the share (share-holder) the right

Standard Financial Instruments in Tatra banka, a.s. and the Risks Connected Therewith 1. Shares Description of Shares Share means a security which gives to the holder of the share (share-holder) the right

The new ACI Diploma. Unit 2 Fixed Income & Money Markets. Effective October 2014

The new ACI Diploma Unit 2 Fixed Income & Money Markets Effective October 2014 8 Rue du Mail, 75002 Paris - France T: +33 1 42975115 - F: +33 1 42975116 - www.aciforex.org The new ACI Diploma Objective

The new ACI Diploma Unit 2 Fixed Income & Money Markets Effective October 2014 8 Rue du Mail, 75002 Paris - France T: +33 1 42975115 - F: +33 1 42975116 - www.aciforex.org The new ACI Diploma Objective

BIS TRIENNIAL SURVEY OF FOREIGN EXCHANGE AND OVER-THE-COUNTER INTEREST RATE DERIVATIVES MARKETS IN APRIL 2013 UK DATA - RESULTS SUMMARY

BIS TRIENNIAL SURVEY OF FOREIGN EXCHANGE AND OVER-THE-COUNTER INTEREST RATE DERIVATIVES MARKETS IN APRIL 2013 UK DATA - RESULTS SUMMARY In April this year, central banks and monetary authorities in 53

BIS TRIENNIAL SURVEY OF FOREIGN EXCHANGE AND OVER-THE-COUNTER INTEREST RATE DERIVATIVES MARKETS IN APRIL 2013 UK DATA - RESULTS SUMMARY In April this year, central banks and monetary authorities in 53

Commodities. Product Categories

Commodities Material Economic Term Option Swaption Swap Basis Swap Index Swap Buyer Seller Premium Strike Price Premium Payment Date Resets Commodity Option Type (Call / Put) Commodity Option Style (European

Commodities Material Economic Term Option Swaption Swap Basis Swap Index Swap Buyer Seller Premium Strike Price Premium Payment Date Resets Commodity Option Type (Call / Put) Commodity Option Style (European

Exotic options [April 4]

![Exotic options [April 4]](/thumbs/27/9684816.jpg "Exotic options [April 4]") Exotic options [April 4] We ve looked at European and American Calls and Puts European options with general payoff functions From a theoretical point of view. This could be carried further, to more Exotic

Exotic options [April 4] We ve looked at European and American Calls and Puts European options with general payoff functions From a theoretical point of view. This could be carried further, to more Exotic

Interest Rate and Currency Swaps

Interest Rate and Currency Swaps Eiteman et al., Chapter 14 Winter 2004 Bond Basics Consider the following: Zero-Coupon Zero-Coupon One-Year Implied Maturity Bond Yield Bond Price Forward Rate t r 0 (0,t)

Interest Rate and Currency Swaps Eiteman et al., Chapter 14 Winter 2004 Bond Basics Consider the following: Zero-Coupon Zero-Coupon One-Year Implied Maturity Bond Yield Bond Price Forward Rate t r 0 (0,t)

How To Understand A Rates Transaction

International Swaps and Derivatives Association, Inc. Disclosure Annex for Interest Rate Transactions This Annex supplements and should be read in conjunction with the General Disclosure Statement. NOTHING

International Swaps and Derivatives Association, Inc. Disclosure Annex for Interest Rate Transactions This Annex supplements and should be read in conjunction with the General Disclosure Statement. NOTHING

Introduction to swaps

Introduction to swaps Steven C. Mann M.J. Neeley School of Business Texas Christian University incorporating ideas from Teaching interest rate and currency swaps" by Keith C. Brown (Texas-Austin) and Donald

Introduction to swaps Steven C. Mann M.J. Neeley School of Business Texas Christian University incorporating ideas from Teaching interest rate and currency swaps" by Keith C. Brown (Texas-Austin) and Donald

Underlying (S) The asset, which the option buyer has the right to buy or sell. Notation: S or S t = S(t)

The asset, which the option buyer has the right to buy or sell. Notation: S or S t = S(t)") INTRODUCTION TO OPTIONS Readings: Hull, Chapters 8, 9, and 10 Part I. Options Basics Options Lexicon Options Payoffs (Payoff diagrams) Calls and Puts as two halves of a forward contract: the Put-Call-Forward

INTRODUCTION TO OPTIONS Readings: Hull, Chapters 8, 9, and 10 Part I. Options Basics Options Lexicon Options Payoffs (Payoff diagrams) Calls and Puts as two halves of a forward contract: the Put-Call-Forward

FIXED-INCOME SECURITIES. Chapter 10. Swaps

FIXED-INCOME SECURITIES Chapter 10 Swaps Outline Terminology Convention Quotation Uses of Swaps Pricing of Swaps Non Plain Vanilla Swaps Terminology Definition Agreement between two parties They exchange

FIXED-INCOME SECURITIES Chapter 10 Swaps Outline Terminology Convention Quotation Uses of Swaps Pricing of Swaps Non Plain Vanilla Swaps Terminology Definition Agreement between two parties They exchange

Derivatives, Measurement and Hedge Accounting

Derivatives, Measurement and Hedge Accounting IAS 39 11 June 2008 Contents Derivatives and embedded derivatives Definition Sample of products Accounting treatment Measurement Active market VS Inactive

Derivatives, Measurement and Hedge Accounting IAS 39 11 June 2008 Contents Derivatives and embedded derivatives Definition Sample of products Accounting treatment Measurement Active market VS Inactive

Introduction to Options. Derivatives

Introduction to Options Econ 422: Investment, Capital & Finance University of Washington Summer 2010 August 18, 2010 Derivatives A derivative is a security whose payoff or value depends on (is derived

Introduction to Options Econ 422: Investment, Capital & Finance University of Washington Summer 2010 August 18, 2010 Derivatives A derivative is a security whose payoff or value depends on (is derived

Exchanges for Physicals (EFP)

") PROCEDURES FOR THE EXECUTION AND REPORTING OF EXCHANGE FOR PHYSICAL (EFP), EXCHANGE FOR RISK (EFR) AND SUBSTITUTION OF OTC DERIVATIVE INSTRUMENTS FOR FUTURES CONTRACTS TRANSACTIONS The purpose of the following

PROCEDURES FOR THE EXECUTION AND REPORTING OF EXCHANGE FOR PHYSICAL (EFP), EXCHANGE FOR RISK (EFR) AND SUBSTITUTION OF OTC DERIVATIVE INSTRUMENTS FOR FUTURES CONTRACTS TRANSACTIONS The purpose of the following

VANILLA OPTIONS MANUAL

VANILLA OPTIONS MANUAL BALANCE YOUR RISK WITH OPTIONS Blue Capital Markets Limited 2013. All rights reserved. Content Part A The what and why of options 1 Types of options: Profit and loss scenarios 2

VANILLA OPTIONS MANUAL BALANCE YOUR RISK WITH OPTIONS Blue Capital Markets Limited 2013. All rights reserved. Content Part A The what and why of options 1 Types of options: Profit and loss scenarios 2

Note 8: Derivative Instruments

Note 8: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices

Note 8: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices

Setting the scene. by Stephen McCabe, Commonwealth Bank of Australia

Establishing risk and reward within FX hedging strategies by Stephen McCabe, Commonwealth Bank of Australia Almost all Australian corporate entities have exposure to Foreign Exchange (FX) markets. Typically

Establishing risk and reward within FX hedging strategies by Stephen McCabe, Commonwealth Bank of Australia Almost all Australian corporate entities have exposure to Foreign Exchange (FX) markets. Typically

Over the Counter Options Oracle FLEXCUBE Universal Banking Europe Cluster Release 11.3.81.02.0 [October] [2013] Oracle Part Number E51523-01

![Over the Counter Options Oracle FLEXCUBE Universal Banking Europe Cluster Release 11.3.81.02.0 [October] [2013] Oracle Part Number E51523-01](/thumbs/26/8836565.jpg "Over the Counter Options Oracle FLEXCUBE Universal Banking Europe Cluster Release 11.3.81.02.0 [October] [2013] Oracle Part Number E51523-01") Over the Counter Options Oracle FLEXCUBE Universal Banking Europe Cluster Release 11.3.81.02.0 [October] [2013] Oracle Part Number E51523-01 0 Table of Contents Over the Counter Options 1. ABOUT THIS MANUAL...

Over the Counter Options Oracle FLEXCUBE Universal Banking Europe Cluster Release 11.3.81.02.0 [October] [2013] Oracle Part Number E51523-01 0 Table of Contents Over the Counter Options 1. ABOUT THIS MANUAL...

Advanced forms of currency swaps

Advanced forms of currency swaps Basis swaps Basis swaps involve swapping one floating index rate for another. Banks may need to use basis swaps to arrange a currency swap for the customers. Example A

Advanced forms of currency swaps Basis swaps Basis swaps involve swapping one floating index rate for another. Banks may need to use basis swaps to arrange a currency swap for the customers. Example A

Figure S9.1 Profit from long position in Problem 9.9

Problem 9.9 Suppose that a European call option to buy a share for $100.00 costs $5.00 and is held until maturity. Under what circumstances will the holder of the option make a profit? Under what circumstances

Problem 9.9 Suppose that a European call option to buy a share for $100.00 costs $5.00 and is held until maturity. Under what circumstances will the holder of the option make a profit? Under what circumstances

Trading Strategies Involving Options. Chapter 11

Trading Strategies Involving Options Chapter 11 1 Strategies to be Considered A risk-free bond and an option to create a principal-protected note A stock and an option Two or more options of the same type

Trading Strategies Involving Options Chapter 11 1 Strategies to be Considered A risk-free bond and an option to create a principal-protected note A stock and an option Two or more options of the same type

CHAPTER 6. Different Types of Swaps 1

CHAPTER 6 Different Types of Swaps 1 In the previous chapter, we introduced two simple kinds of generic swaps: interest rate and currency swaps. These are usually known as plain vanilla deals because the

CHAPTER 6 Different Types of Swaps 1 In the previous chapter, we introduced two simple kinds of generic swaps: interest rate and currency swaps. These are usually known as plain vanilla deals because the

The data model mining breakdown of financial derivatives

The data model mining breakdown of financial derivatives Buriánková, P. University of Finance and Administration, Prague, Czech Republic pet.buriankova@seznam.cz Abstract The work deals with the data model

The data model mining breakdown of financial derivatives Buriánková, P. University of Finance and Administration, Prague, Czech Republic pet.buriankova@seznam.cz Abstract The work deals with the data model

Foreign Currency Transactions and Hedging

Foreign Currency Transactions and Hedging History of Currency 1945-1973: US dollar was pegged to gold and other currencies were pegged to the dollar 1960 s: US had a balance of payments deficit o Other

Foreign Currency Transactions and Hedging History of Currency 1945-1973: US dollar was pegged to gold and other currencies were pegged to the dollar 1960 s: US had a balance of payments deficit o Other

CURRENT STANDARDS ON FIXED INCOME

CURRENT STANDARDS ON FIXED INCOME PRICING FIXED INCOME SECURITIES AGAINST AN INTEREST SWAP CURVE December 2012 CNO Association régie par la loi du 1 er juillet 1901 8 rue du Mail 75002 Paris http://www.cnofrance.org

CURRENT STANDARDS ON FIXED INCOME PRICING FIXED INCOME SECURITIES AGAINST AN INTEREST SWAP CURVE December 2012 CNO Association régie par la loi du 1 er juillet 1901 8 rue du Mail 75002 Paris http://www.cnofrance.org

Math 489/889. Stochastic Processes and. Advanced Mathematical Finance. Homework 1

Math 489/889 Stochastic Processes and Advanced Mathematical Finance Homework 1 Steve Dunbar Due Friday, September 3, 2010 Problem 1 part a Find and write the definition of a ``future'', also called a futures

Math 489/889 Stochastic Processes and Advanced Mathematical Finance Homework 1 Steve Dunbar Due Friday, September 3, 2010 Problem 1 part a Find and write the definition of a ``future'', also called a futures

Hedging Interest-Rate Risk: A Primer in Instruments. & Accounting. September 29, 2015. Presented by: Ruth Hardie

Hedging Interest-Rate Risk: A Primer in Instruments September 29, 2015 & Accounting Presented by: Ruth Hardie Hedge Trackers, LLC Integrated Derivative Management Interest Rate, Foreign Currency and Commodities

Hedging Interest-Rate Risk: A Primer in Instruments September 29, 2015 & Accounting Presented by: Ruth Hardie Hedge Trackers, LLC Integrated Derivative Management Interest Rate, Foreign Currency and Commodities

Option Values. Option Valuation. Call Option Value before Expiration. Determinants of Call Option Values

Option Values Option Valuation Intrinsic value profit that could be made if the option was immediately exercised Call: stock price exercise price : S T X i i k i X S Put: exercise price stock price : X

Option Values Option Valuation Intrinsic value profit that could be made if the option was immediately exercised Call: stock price exercise price : S T X i i k i X S Put: exercise price stock price : X

BLOOMBERG DERIVATIVE EXERCISES. 1. Select a stock of interest and identify the exchange-traded options traded on it.

BLOOMBERG DERIVATIVE EXERCISES OPTION CONCEPTS AND FUNDAMENTAL STRATEGIES 1. Select a stock of interest and identify the exchange-traded options traded on it. Example: Options on IBM Enter IBM [EQUITY]

BLOOMBERG DERIVATIVE EXERCISES OPTION CONCEPTS AND FUNDAMENTAL STRATEGIES 1. Select a stock of interest and identify the exchange-traded options traded on it. Example: Options on IBM Enter IBM [EQUITY]

Arbitrage spreads. Arbitrage spreads refer to standard option strategies like vanilla spreads to

Arbitrage spreads Arbitrage spreads refer to standard option strategies like vanilla spreads to lock up some arbitrage in case of mispricing of options. Although arbitrage used to exist in the early days

Arbitrage spreads Arbitrage spreads refer to standard option strategies like vanilla spreads to lock up some arbitrage in case of mispricing of options. Although arbitrage used to exist in the early days

Fundamentals of Finance

Euribor rates, forward rates and swap rates University of Oulu - Department of Finance Fall 2015 What next Euribor rates, forward rates and swap rates In the following we consider Euribor spot rate, Euribor

Euribor rates, forward rates and swap rates University of Oulu - Department of Finance Fall 2015 What next Euribor rates, forward rates and swap rates In the following we consider Euribor spot rate, Euribor

Note 10: Derivative Instruments

Note 10: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity

Note 10: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity

Caput Derivatives: October 30, 2003

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Learning Curve UNDERSTANDING DERIVATIVES

Learning Curve UNDERSTANDING DERIVATIVES Brian Eales London Metropolitan University YieldCurve.com 2004 Page 1 Understanding Derivatives Derivative instruments have been a feature of modern financial markets

Learning Curve UNDERSTANDING DERIVATIVES Brian Eales London Metropolitan University YieldCurve.com 2004 Page 1 Understanding Derivatives Derivative instruments have been a feature of modern financial markets

Interest Rate Risk Management for the Banking Book: Macro Hedging

Interest Rate Risk Management for the Banking Book: Macro Hedging Giuseppe Loforese Head of ALM - Intesa Sanpaolo Chair of ALM Hedge Accounting WG EBF Co-Chairman IRRBB WG - EBF AGENDA IRRBB: Macro Hedging

Interest Rate Risk Management for the Banking Book: Macro Hedging Giuseppe Loforese Head of ALM - Intesa Sanpaolo Chair of ALM Hedge Accounting WG EBF Co-Chairman IRRBB WG - EBF AGENDA IRRBB: Macro Hedging

Introduction. Part IV: Option Fundamentals. Derivatives & Risk Management. The Nature of Derivatives. Definitions. Options. Main themes Options

Derivatives & Risk Management Main themes Options option pricing (microstructure & investments) hedging & real options (corporate) This & next weeks lectures Introduction Part IV: Option Fundamentals»

Derivatives & Risk Management Main themes Options option pricing (microstructure & investments) hedging & real options (corporate) This & next weeks lectures Introduction Part IV: Option Fundamentals»

Chapter 5 Financial Forwards and Futures

Chapter 5 Financial Forwards and Futures Question 5.1. Four different ways to sell a share of stock that has a price S(0) at time 0. Question 5.2. Description Get Paid at Lose Ownership of Receive Payment

Chapter 5 Financial Forwards and Futures Question 5.1. Four different ways to sell a share of stock that has a price S(0) at time 0. Question 5.2. Description Get Paid at Lose Ownership of Receive Payment

Introduction to Equity Derivatives. February 2008 - The Derivatives Consulting Group Ltd www.dcgconsultants.com

Introduction to Equity Derivatives Course Agenda Part 1: Introduction to Equities The Basics Types of Stock Dividends Corporate Actions Underlyings Market Institutions Part 2: Introduction to Derivatives

Introduction to Equity Derivatives Course Agenda Part 1: Introduction to Equities The Basics Types of Stock Dividends Corporate Actions Underlyings Market Institutions Part 2: Introduction to Derivatives

Chapter 16: Financial Risk Management

Chapter 16: Financial Risk Management Introduction Overview of Financial Risk Management in Treasury Interest Rate Risk Foreign Exchange (FX) Risk Commodity Price Risk Managing Financial Risk The Benefits

Chapter 16: Financial Risk Management Introduction Overview of Financial Risk Management in Treasury Interest Rate Risk Foreign Exchange (FX) Risk Commodity Price Risk Managing Financial Risk The Benefits

The Quest to classify OTC Derivative Instruments for publication in the March edition of Trading Places

Document Ref: OTCD001-001 The Quest to classify OTC Derivative Instruments for publication in the March edition of Trading Places We have recently seen banks experiencing the financial equivalent of black

Document Ref: OTCD001-001 The Quest to classify OTC Derivative Instruments for publication in the March edition of Trading Places We have recently seen banks experiencing the financial equivalent of black

Options on 10-Year U.S. Treasury Note & Euro Bund Futures in Fixed Income Portfolio Analysis

White Paper Whitepaper Options on 10-Year U.S. Treasury Note & Euro Bund Futures in Fixed Income Portfolio Analysis Copyright 2015 FactSet Research Systems Inc. All rights reserved. Options on 10-Year

White Paper Whitepaper Options on 10-Year U.S. Treasury Note & Euro Bund Futures in Fixed Income Portfolio Analysis Copyright 2015 FactSet Research Systems Inc. All rights reserved. Options on 10-Year

Annex 2 Statistical definitions for the Foreign Exchange market

DNR 2009-333-AFS Annex 2 Statistical definitions for the Foreign Exchange market Sources: Sveriges Riksbank, Bank for International Settlements (BIS), European Commission and Nasdaq OMX. Selma FX (Foreign

DNR 2009-333-AFS Annex 2 Statistical definitions for the Foreign Exchange market Sources: Sveriges Riksbank, Bank for International Settlements (BIS), European Commission and Nasdaq OMX. Selma FX (Foreign

Application of Interest Rate Swaps in Indian Insurance Industry Amruth Krishnan Rohit Ajgaonkar Guide: G.LN.Sarma

Institute of Actuaries of India Application of Interest Rate Swaps in Indian Insurance Industry Amruth Krishnan Rohit Ajgaonkar Guide: G.LN.Sarma 21 st IFS Seminar Indian Actuarial Profession Serving the

Institute of Actuaries of India Application of Interest Rate Swaps in Indian Insurance Industry Amruth Krishnan Rohit Ajgaonkar Guide: G.LN.Sarma 21 st IFS Seminar Indian Actuarial Profession Serving the

General Forex Glossary

General Forex Glossary A ADR American Depository Receipt Arbitrage The simultaneous buying and selling of a security at two different prices in two different markets, with the aim of creating profits without

General Forex Glossary A ADR American Depository Receipt Arbitrage The simultaneous buying and selling of a security at two different prices in two different markets, with the aim of creating profits without

Module I Financial derivatives an introduction Forward market and products

Module I 1. Financial derivatives an introduction 1.1 Derivative markets 1.1.1 Past and present 1.1.2 Difference between exchange traded and OTC derivatives 1.2 Derivative instruments 1.2.1 Concept and

Module I 1. Financial derivatives an introduction 1.1 Derivative markets 1.1.1 Past and present 1.1.2 Difference between exchange traded and OTC derivatives 1.2 Derivative instruments 1.2.1 Concept and

JB Certificates and Warrants on Interest Rates in EUR, USD and CHF

JB Certificates and Warrants on Interest Rates in EUR, USD and CHF Efficient instruments to hedge bonds, mortgages and lombard loans against rising interest rates Zurich, 2013 Content Table Embedded risks

JB Certificates and Warrants on Interest Rates in EUR, USD and CHF Efficient instruments to hedge bonds, mortgages and lombard loans against rising interest rates Zurich, 2013 Content Table Embedded risks

MONETARY OPERATIONS DEPARTMENT Belgrade, 29 December 2011. Q & As ABOUT THE DECISION ON FINANCIAL DERIVATIVE TRANSACTIONS

MONETARY OPERATIONS DEPARTMENT Belgrade, 29 December 2011 Q & As ABOUT THE DECISION ON FINANCIAL DERIVATIVE TRANSACTIONS ( RS Official Gazette, No 85/2011) 1. Question: Does the open foreign currency balance

MONETARY OPERATIONS DEPARTMENT Belgrade, 29 December 2011 Q & As ABOUT THE DECISION ON FINANCIAL DERIVATIVE TRANSACTIONS ( RS Official Gazette, No 85/2011) 1. Question: Does the open foreign currency balance

Statistical definitions for the foreign exchange market (FX) reporting

reporting") Statistical definitions for the foreign exchange market (FX) reporting The foreign exchange market (FX) reporting covers the turnover of foreign exchange and turnover of short term interest rate derivatives

Statistical definitions for the foreign exchange market (FX) reporting The foreign exchange market (FX) reporting covers the turnover of foreign exchange and turnover of short term interest rate derivatives

Training Agenda. Structuring and Pricing Derivatives using Numerix CrossAsset XL, CrossAsset SDKs & CAIL (C++/Java/C#)

") Training Agenda Structuring and Pricing Derivatives using Numerix CrossAsset XL, CrossAsset SDKs & CAIL (C++/Java/C#) Numerix Training: CrossAsset XL and SDKs (C++/Java/C#): Orientation Implementation

Training Agenda Structuring and Pricing Derivatives using Numerix CrossAsset XL, CrossAsset SDKs & CAIL (C++/Java/C#) Numerix Training: CrossAsset XL and SDKs (C++/Java/C#): Orientation Implementation

INTEREST RATE SWAP (IRS)

") INTEREST RATE SWAP (IRS) 1. Interest Rate Swap (IRS)... 4 1.1 Terminology... 4 1.2 Application... 11 1.3 EONIA Swap... 19 1.4 Pricing and Mark to Market Revaluation of IRS... 22 2. Cross Currency Swap...

INTEREST RATE SWAP (IRS) 1. Interest Rate Swap (IRS)... 4 1.1 Terminology... 4 1.2 Application... 11 1.3 EONIA Swap... 19 1.4 Pricing and Mark to Market Revaluation of IRS... 22 2. Cross Currency Swap...

OVERVIEW OF THE USE OF CROSS CURRENCY SWAPS

OVERVIEW OF THE USE OF CROSS CURRENCY SWAPS PRACTICAL CONSIDERATIONS IVAN LARIN CAPITAL MARKETS DEPARTMENT FABDM Webinar for Debt Managers Washington, D.C. 20 th January, 2016 AGENDA 1. BASICS 2. Pre-TRADE

OVERVIEW OF THE USE OF CROSS CURRENCY SWAPS PRACTICAL CONSIDERATIONS IVAN LARIN CAPITAL MARKETS DEPARTMENT FABDM Webinar for Debt Managers Washington, D.C. 20 th January, 2016 AGENDA 1. BASICS 2. Pre-TRADE

MONEY MARKET FUTURES. FINANCE TRAINER International Money Market Futures / Page 1 of 22

MONEY MARKET FUTURES 1. Conventions and Contract Specifications... 3 2. Main Markets of Money Market Futures... 7 3. Exchange and Clearing House... 8 4. The Margin System... 9 5. Comparison: Money Market

MONEY MARKET FUTURES 1. Conventions and Contract Specifications... 3 2. Main Markets of Money Market Futures... 7 3. Exchange and Clearing House... 8 4. The Margin System... 9 5. Comparison: Money Market

Interest Rate Hedging. November 2007

November 2007 ASSET = LEASE Deal Example LIABILITY = DEBT Airbus A320 cost $40m 85% floating rate debt : $34m Aircraft placed on lease for 7 years at fixed rental of $350k per month, priced at 5% Libor

November 2007 ASSET = LEASE Deal Example LIABILITY = DEBT Airbus A320 cost $40m 85% floating rate debt : $34m Aircraft placed on lease for 7 years at fixed rental of $350k per month, priced at 5% Libor

INR Volatility - Hedging Options & Effective Strategies

INR Volatility - Hedging Options & Effective Strategies The purpose of the article is to draw attention on the recent volatility in Indian Rupee, various hedging options and effective hedging strategies.

INR Volatility - Hedging Options & Effective Strategies The purpose of the article is to draw attention on the recent volatility in Indian Rupee, various hedging options and effective hedging strategies.

EQUITY LINKED NOTES: An Introduction to Principal Guaranteed Structures Abukar M Ali October 2002

EQUITY LINKED NOTES: An Introduction to Principal Guaranteed Structures Abukar M Ali October 2002 Introduction In this article we provide a succinct description of a commonly used investment instrument

EQUITY LINKED NOTES: An Introduction to Principal Guaranteed Structures Abukar M Ali October 2002 Introduction In this article we provide a succinct description of a commonly used investment instrument

Butterflies, Condors, and Jelly Rolls: Derivatives Explained

Butterflies, Condors, and Jelly Rolls: Derivatives Explained American Translators Association 47 th Annual Conference, New Orleans November 1, 2006 Ralf Lemster 1 Derivatives Explained What are derivatives?

Butterflies, Condors, and Jelly Rolls: Derivatives Explained American Translators Association 47 th Annual Conference, New Orleans November 1, 2006 Ralf Lemster 1 Derivatives Explained What are derivatives?

2. Exercising the option - buying or selling asset by using option. 3. Strike (or exercise) price - price at which asset may be bought or sold

price - price at which asset may be bought or sold") Chapter 21 : Options-1 CHAPTER 21. OPTIONS Contents I. INTRODUCTION BASIC TERMS II. VALUATION OF OPTIONS A. Minimum Values of Options B. Maximum Values of Options C. Determinants of Call Value D. Black-Scholes

Chapter 21 : Options-1 CHAPTER 21. OPTIONS Contents I. INTRODUCTION BASIC TERMS II. VALUATION OF OPTIONS A. Minimum Values of Options B. Maximum Values of Options C. Determinants of Call Value D. Black-Scholes

Assumptions: No transaction cost, same rate for borrowing/lending, no default/counterparty risk

Derivatives Why? Allow easier methods to short sell a stock without a broker lending it. Facilitates hedging easily Allows the ability to take long/short position on less available commodities (Rice, Cotton,

Derivatives Why? Allow easier methods to short sell a stock without a broker lending it. Facilitates hedging easily Allows the ability to take long/short position on less available commodities (Rice, Cotton,

How To Calculate Interest Rate Derivative Options

The Pricing and Hedging of Interest-Rate Derivatives: Theory and Practice Ser-Huang Poon 1, Richard C. Stapleton 2 and Marti G. Subrahmanyam 3 April 28, 2005 1 Manchester Business School 2 Manchester Business

The Pricing and Hedging of Interest-Rate Derivatives: Theory and Practice Ser-Huang Poon 1, Richard C. Stapleton 2 and Marti G. Subrahmanyam 3 April 28, 2005 1 Manchester Business School 2 Manchester Business

IBUS 700. The Good, the Bad and the Ugly: FX Standard and Exotic Options

IBUS 700 FX Options Professor Robert Hauswald Kogod School of Business, AU The Good, the Bad and the Ugly: FX Standard and Exotic Options The derivative with an attitude: FX Options opinion: upward potential,

IBUS 700 FX Options Professor Robert Hauswald Kogod School of Business, AU The Good, the Bad and the Ugly: FX Standard and Exotic Options The derivative with an attitude: FX Options opinion: upward potential,

Options (1) Class 19 Financial Management, 15.414

Class 19 Financial Management, 15.414") Options (1) Class 19 Financial Management, 15.414 Today Options Risk management: Why, how, and what? Option payoffs Reading Brealey and Myers, Chapter 2, 21 Sally Jameson 2 Types of questions Your company,

Options (1) Class 19 Financial Management, 15.414 Today Options Risk management: Why, how, and what? Option payoffs Reading Brealey and Myers, Chapter 2, 21 Sally Jameson 2 Types of questions Your company,

ONIA Swap Index. The derivatives market reference rate for the Euro

ONIA Swap Index The derivatives market reference rate for the Euro Contents Introduction 2 What is an EONIA Swap? 3-4 EONIA Swap Index The new benchmark 5-8 EONIA 9-10 Basis Swaps 10 IRS vs. EONIA Swap

ONIA Swap Index The derivatives market reference rate for the Euro Contents Introduction 2 What is an EONIA Swap? 3-4 EONIA Swap Index The new benchmark 5-8 EONIA 9-10 Basis Swaps 10 IRS vs. EONIA Swap

TREASURY PRODUCTS AND SERVICES MANAGING FINANCIAL RISKS, ENHANCING RETURNS, ACHIEVEING INVESTMENT GOALS 2016

TREASURY PRODUCTS AND SERVICES MANAGING FINANCIAL RISKS, ENHANCING RETURNS, ACHIEVEING INVESTMENT GOALS 2016 CONTENT PIRAEUS BANK BULGARIA RELIABLE PARTNER IN THE PRESENT VOLATILE FINANCIAL WORLD FOREIGN

TREASURY PRODUCTS AND SERVICES MANAGING FINANCIAL RISKS, ENHANCING RETURNS, ACHIEVEING INVESTMENT GOALS 2016 CONTENT PIRAEUS BANK BULGARIA RELIABLE PARTNER IN THE PRESENT VOLATILE FINANCIAL WORLD FOREIGN

SwapEx Contract Specifications. USD LIBOR Interest Rate Swaps: Fixedto-Floating

SwapEx Contract Specifications USD LIBOR Interest Rate Swaps: Fixedto-Floating There are two types of USD LIBOR Interest Rate Swaps; Fixed-to-Floating contracts available for trading on SwapEx: Fixed Rate

SwapEx Contract Specifications USD LIBOR Interest Rate Swaps: Fixedto-Floating There are two types of USD LIBOR Interest Rate Swaps; Fixed-to-Floating contracts available for trading on SwapEx: Fixed Rate

LOCKING IN TREASURY RATES WITH TREASURY LOCKS

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

SECURITIES AND FUTURES (REPORTING OF DERIVATIVES CONTRACTS) REGULATIONS 2013

REGULATIONS 2013") Annex B SECURITIES AND FUTURES (REPORTING OF DERIVATIVES CONTRACTS) REGULATIONS 2013 DISCLAIMER: This version of the Regulations is in draft form and subject to change. It is also subject to review by

Annex B SECURITIES AND FUTURES (REPORTING OF DERIVATIVES CONTRACTS) REGULATIONS 2013 DISCLAIMER: This version of the Regulations is in draft form and subject to change. It is also subject to review by

SOCIETY OF ACTUARIES FINANCIAL MATHEMATICS. EXAM FM SAMPLE QUESTIONS Financial Economics

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS Financial Economics June 2014 changes Questions 1-30 are from the prior version of this document. They have been edited to conform

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS Financial Economics June 2014 changes Questions 1-30 are from the prior version of this document. They have been edited to conform

Market and Exercise Price Relationships. Option Terminology. Options Trading. CHAPTER 15 Options Markets 15.1 THE OPTION CONTRACT

CHAPTER 15 Options Markets 15.1 THE OPTION CONTRACT Option Terminology Buy - Long Sell - Short Call the right to buy Put the the right to sell Key Elements Exercise or Strike Price Premium or Price of

CHAPTER 15 Options Markets 15.1 THE OPTION CONTRACT Option Terminology Buy - Long Sell - Short Call the right to buy Put the the right to sell Key Elements Exercise or Strike Price Premium or Price of

WHS FX options guide. Getting started with FX options. Predict the trend in currency markets or hedge your positions with FX options.

Getting started with FX options WHS FX options guide Predict the trend in currency markets or hedge your positions with FX options. Refine your trading style and your market outlook. Learn how FX options

Getting started with FX options WHS FX options guide Predict the trend in currency markets or hedge your positions with FX options. Refine your trading style and your market outlook. Learn how FX options

Index, Interest Rate, and Currency Options

CHAPTER 3 Index, Interest Rate, and Currency Options INTRODUCTION In an effort to gauge the market s overall performance, industry participants developed indexes. Two of the most widely followed indexes

CHAPTER 3 Index, Interest Rate, and Currency Options INTRODUCTION In an effort to gauge the market s overall performance, industry participants developed indexes. Two of the most widely followed indexes

Fixed income traders should embrace options strategies, says III's Friesen

Fixed income traders should embrace options strategies, says III's Friesen By Garth Friesen August 5, 2013 Garth Friesen of III Associates outlines the role of options in fixed income relative value trading.

Fixed income traders should embrace options strategies, says III's Friesen By Garth Friesen August 5, 2013 Garth Friesen of III Associates outlines the role of options in fixed income relative value trading.

Introduction, Forwards and Futures

Introduction, Forwards and Futures Liuren Wu Zicklin School of Business, Baruch College Fall, 2007 (Hull chapters: 1,2,3,5) Liuren Wu Introduction, Forwards & Futures Option Pricing, Fall, 2007 1 / 35

Introduction, Forwards and Futures Liuren Wu Zicklin School of Business, Baruch College Fall, 2007 (Hull chapters: 1,2,3,5) Liuren Wu Introduction, Forwards & Futures Option Pricing, Fall, 2007 1 / 35

FX Key products Exotic Options Menu

FX Key products Exotic Options Menu Welcome to Exotic Options Over the last couple of years options have become an important tool for investors and hedgers in the foreign exchange market. With the growing

FX Key products Exotic Options Menu Welcome to Exotic Options Over the last couple of years options have become an important tool for investors and hedgers in the foreign exchange market. With the growing

Monthly Leveraged Mutual Funds UNDERSTANDING THE COMPOSITION, BENEFITS & RISKS

Monthly Leveraged Mutual Funds UNDERSTANDING THE COMPOSITION, BENEFITS & RISKS Direxion 2x Monthly Leveraged Mutual Funds provide 200% (or 200% of the inverse) exposure to their benchmarks and the ability

Monthly Leveraged Mutual Funds UNDERSTANDING THE COMPOSITION, BENEFITS & RISKS Direxion 2x Monthly Leveraged Mutual Funds provide 200% (or 200% of the inverse) exposure to their benchmarks and the ability

Learning Curve An introduction to the use of the Bloomberg system in swaps analysis Received: 1st July, 2002

Learning Curve An introduction to the use of the Bloomberg system in swaps analysis Received: 1st July, 2002 Aaron Nematnejad works in the fixed income analytics team at Bloomberg L.P. in London. He graduated

Learning Curve An introduction to the use of the Bloomberg system in swaps analysis Received: 1st July, 2002 Aaron Nematnejad works in the fixed income analytics team at Bloomberg L.P. in London. He graduated

How To Sell A Callable Bond

1.1 Callable bonds A callable bond is a fixed rate bond where the issuer has the right but not the obligation to repay the face value of the security at a pre-agreed value prior to the final original maturity

1.1 Callable bonds A callable bond is a fixed rate bond where the issuer has the right but not the obligation to repay the face value of the security at a pre-agreed value prior to the final original maturity

Risk Information for Expanded Investment Transactions and Forward Exchange Transactions

Risk Information for Expanded Investment Transactions and Forward Exchange Transactions May 2010 TABLE OF CONTENTS Preliminary Remarks...3 1. General Investment Risks...3 2. Forward Exchange Transactions...4

Risk Information for Expanded Investment Transactions and Forward Exchange Transactions May 2010 TABLE OF CONTENTS Preliminary Remarks...3 1. General Investment Risks...3 2. Forward Exchange Transactions...4

DERIVATIVES IN INDIAN STOCK MARKET

DERIVATIVES IN INDIAN STOCK MARKET Dr. Rashmi Rathi Assistant Professor Onkarmal Somani College of Commerce, Jodhpur ABSTRACT The past decade has witnessed multiple growths in the volume of international

DERIVATIVES IN INDIAN STOCK MARKET Dr. Rashmi Rathi Assistant Professor Onkarmal Somani College of Commerce, Jodhpur ABSTRACT The past decade has witnessed multiple growths in the volume of international