Advanced forms of currency swaps

|

|

|

- Alexandrina O’Connor’

- 9 years ago

- Views:

Transcription

1 Advanced forms of currency swaps

2 Basis swaps Basis swaps involve swapping one floating index rate for another. Banks may need to use basis swaps to arrange a currency swap for the customers. Example A customer wants to arrange a swap in which he pays fixed dollars and receives fixed sterling. The bank might arrange 3 other separate swap transactions: an interest rate swap, fixed rate against floating rate, in dollars an interest rate swap, fixed sterling against floating sterling a currency basis swap, floating dollars against floating sterling

3

4 Hedging the Bank s risk Exposures arise from mismatched principal amounts, currencies and maturities. Hedging methods If the bank is paying (receiving) a fixed rate on a swap, it could buy (sell) government bonds as a hedge. If the bank is paying (receiving) a variable, it can hedge by lending (borrowing) in the money markets. When the bank finds a counterparty to transact a matching swap in the opposite direction, it will liquidate its hedge.

a variable, it can hedge by lending (borrowing) in the money markets.")

5 Multi-legged swaps In a multi-legged swap a bank avoids taking on any currency risk itself by arranging three or more swaps with different clients in order to match currencies and amounts. Example A company wishes to arrange a swap in which it receives floating rate interest on Australian dollars and pays fixed interest on sterling. a fixed sterling versus floating Australian dollar swap with the company a floating Australian dollar versus floating dollar swap with counterparty A a fixed sterling versus dollar swap with counterparty B

6

7 Amortizing swaps The principal amount is reduced progressively by a series of reexchanging during the life of the swap to match the amortization schedule of the underlying transaction. Example A company has an outstanding dollar loan that is being paid off gradually over 3 years. The company would like to swap this dollar liability into a sterling liability. An exchange of principal at initiation receives dollars in exchange for sterling. An annual re-exchange of part of the principal amount receives sufficient dollars each year to meet the repayment schedule on its loan. Regular exchanges of interest.

8 Semi-fixed swap with a FOREX trigger The buyer links its forex and interest rate exposures and produces an integrated hedge. Hedging the various underlying exposures separately often results in higher hedging costs, as the company is likely to be over hedged. Example The swap rate is 5%, the company would pay a lower rate, such as 4.5%, when the DM is above a trigger of DM 1.75 to the US dollar; a higher rate, such as 6.5%, when the DM is below the trigger. The three parameters in this structure makes the product more flexible than plain vanilla swaps.

9 THB/USD Gradual Annuity Swap Counterparties: Goldman Sachs Capital Markets, L.P. Counterparty Trade Date: To be determined Effective Date: To be determined Maturity Date: 5 years from the Effective Date USD Notional Amount: Amortizing as per USD Notional Schedule THB Notional Amount: Amorizing as per THB Notional Schedule Initial Principal Exchange: None Principal Exchanges: On each Principal Exchange Date as per the Notional Schedule: Counterparty pays THB Amorization Amount GSCM pays USD Amortization Amount Interest Period: Semi-annual Act/360 from the Effective Date

10 Period Payments: If MAX < Counterparty pays 4.90% If MAX > Counterparty pays 9.90% Otherwise Counterparty pays 4.90% (MAX 45.00)% on USD Notional Amount MAX: Maximum trade of THB/USD during the semi-annual Interest Period as determined by Calculation Agent Business Days: Example: New York, London and Bangkok If Maximum trade of THB/USD during a semiannual period is 52.00, then coupon for that period is * 7.00% = 8.40% Reference: 14.25% on THB Notional versus USD LIBOR Reference Principal Only: 6.25% on USD Notional Amount

11 Differential Swap (Quanto Swap) A special type of floating-against-floating currency swap that does not involve any exchange of principal, not even at maturity. The notional principal amount is in just one currency. Interest payments are exchanged by reference to a floating rate index in one currency and a floating rate index in a second currency. Both interest rates are applied to the same notional principal. Interest payments are made in the same currency as the notional principal amount.

12 A simple example of differential swap The semi-annual interest streams will be paid in dollars. six-month dollar LIBOR of 5.25% plus margin (reset every 6 months) six-month DM LIBOR of 6.75% (reset every 6 months) notional principal = $10 (million) swap counterparty US LIBOR + margin (say, 40 basis points) bank swap counterparty DM LIBOR bank

notional principal = $10 (million) swap counterparty US")

13 Applications of differential swaps Example In , an investor could earn over 500 basis points more from investing in DM than from in dollars. The differential swap allows (i) investors to enhance yields by securing higher foreign interest rates and (ii) borrowers to cut interest payments costs by taking advantage of lower foreign interest rates without incurring currency exposure.

borrowers to cut interest payments costs by taking advantage of lower foreign")

14 Example on the use of differential swap A client of the Bank has existing borrowings in sterling, paying floating rate interest linked to sterling LIBOR. The client would like to pay the lower interest rate available on the dollar, but does not want currency exposure to the dollar. dollars Sterling 3 months LIBOR 3% 9% 5 years fixed 8% 7% The client enters a diff swap with the Bank, paying $LIBOR paid in sterling (rate of 1.50) and receiving Sterling LIBOR.

15

16 Bank s viewpoint on the structure The bank need to take two offsetting swaps with two other parties. An interest rate swap, fixed rate of 8% against floating LIBOR, in dollars (notional principal of 150m dollars). An interest rate swap, fixed rate of 7% against floating LIBOR, in Sterling (notional principal of 100m Pounds). The bank is exposed to changes in the dollar / sterling exchange rate (need to take measures to hedge such positions).

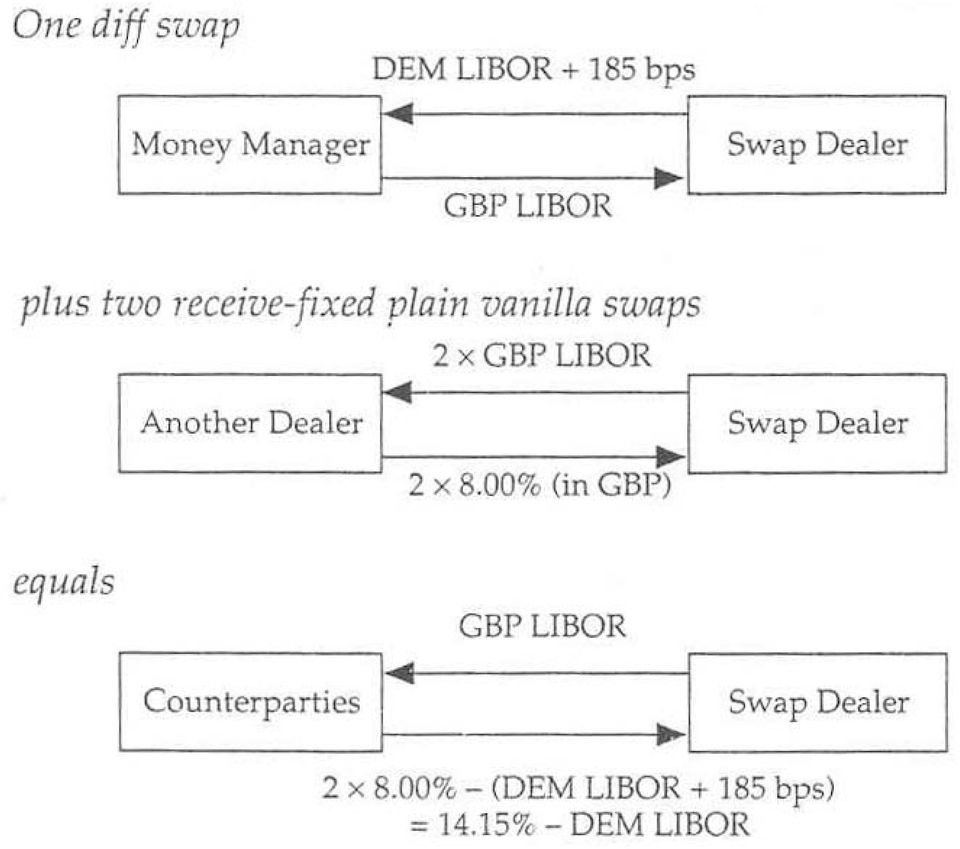

17 More example on diff swap The diff swap requires the swap dealer to pay DEM LIBOR plus 1.85 percent in exchange for Sterling LIBOR, with both rates translated into cash flows using the same GBP 10 million notional principal. The tenor of this agreement, which specified quarterly settlements, was two years.

18 Question Assuming that the swap dealer has left this position unhedged, what is the implicit view he is taking with respect to rate changes in the United Kingdom and Germany? Answer The dealer is implicitly assuming that the differential between the British and German short-term rates will widen more rapidly, and by a greater amount, than the current market view. Either the German rates fall as British rates rise, or Sterling LIBOR rises at an accelerated pace relative to DM LIBOR.

19

20 Given that the present pound and DM LIBOR differential (i.e., 110bps = 6.25% %) is less than the 185-basis-point swap spread differential, he will be required to make the first net settlement payment. Suppose that bid-ask fixed rates on twoyear, sterling-denominated, plain vanilla swaps (against threemonth sterling LIBOR) are currently being quoted in the interbank market at 8.00% and 8.05%, respectively. Question What combination of transactions would be needed to transform the diff swap into a contract by which the dealer receives a cash flow of the form (constant percent DM LIBOR) and pays sterling LIBOR? After the transactions, is it consistent with the implied view proposed earlier.

21 Answer The desired transformation could be made by combining a pay-dm LIBOR / receive-sterling LIBOR diff swap position with two receive-8.00% fixed/pay-sterling LIBOR swaps (or one for twice the GBP 10 million principal). Notice that the dealer s initial net cash flow on the combined transaction is now positive, with value equals 2.75% [obtained as (14.15% %) 6.25%]. Although the dealer still benefits from a German or British rate decline, an increase in either rate - regardless of the size of the differential between them will erode this advantage. Thus, the new position creates a markedly different exposure for the dealer than did the original diff swap.

22 Use of a currency swap to enhance yield Direct Synthetic US Treasury notes Investor 8.14% (US$) Yield pickup = 8.45% 8.14% = 0.31% German govt bonds 8.45% (DM) Investor 8.45% (DM) Swap house 8.14% (US$)

23 Instead of buying 10-year US Treasury notes yielding 8.14%, the investor purchased 10-year German government bonds yielding 8.45% (denominated and payable in deutshemarks), and simultaneously entered into a currency swap. Under the swap, the investor agreed to exchange its DM cashflows over the life of the swap for US dollars. Risks (besides the default risk of the German government) 1. Default risk of the swap counterparty; 2. Over the 10-year life, the investor might have desired to liquidate the investment early and sell the German bonds prior to the maturity of the swap (left with a swap for which it had no obvious use as a hedging instrument).

24 Combination of 4 swaps Combination of two plain vanilla commodity swaps, a plain vanilla currency swap, and a plain vanilla interest rate swap. Goal To enable an oil-producing nation to obtain a fixed long-term supply of rice in exchange for long-term quantity of oil. Without the swap The oil-producing nation was simply to sell oil on the spot market for US dollars, then convert those dollars into Japanese yen and purchase rice in Japan on the spot market.

25 Structure of the swaps 1. A commodity swap was entered into under which the oil producer locked in long-term fixed dollar price for selling future specified oil production. 2. The US dollars were indirectly converted into fixed yen using a combination of (a) fixed-for-floating US dollar denominated interest rate swap, then followed by (b) floating-rate dollar for fixed rate yen currency swap. 3. The fixed-rate yen were converted through a commodity swap into the yen needed to buy a fixed quantity of rice on the spot market. Counter-party risks of the four swaps!

CHAPTER 14 INTEREST RATE AND CURRENCY SWAPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 14 INTEREST RATE AND CURRENCY SWAPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Describe the difference between a swap broker and a swap dealer. Answer:

CHAPTER 14 INTEREST RATE AND CURRENCY SWAPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Describe the difference between a swap broker and a swap dealer. Answer:

FIXED-INCOME SECURITIES. Chapter 10. Swaps

FIXED-INCOME SECURITIES Chapter 10 Swaps Outline Terminology Convention Quotation Uses of Swaps Pricing of Swaps Non Plain Vanilla Swaps Terminology Definition Agreement between two parties They exchange

FIXED-INCOME SECURITIES Chapter 10 Swaps Outline Terminology Convention Quotation Uses of Swaps Pricing of Swaps Non Plain Vanilla Swaps Terminology Definition Agreement between two parties They exchange

Equity-index-linked swaps

Equity-index-linked swaps Equivalent to portfolios of forward contracts calling for the exchange of cash flows based on two different investment rates: a variable debt rate (e.g. 3-month LIBOR) and the

Equity-index-linked swaps Equivalent to portfolios of forward contracts calling for the exchange of cash flows based on two different investment rates: a variable debt rate (e.g. 3-month LIBOR) and the

Chapter 16: Financial Risk Management

Chapter 16: Financial Risk Management Introduction Overview of Financial Risk Management in Treasury Interest Rate Risk Foreign Exchange (FX) Risk Commodity Price Risk Managing Financial Risk The Benefits

Chapter 16: Financial Risk Management Introduction Overview of Financial Risk Management in Treasury Interest Rate Risk Foreign Exchange (FX) Risk Commodity Price Risk Managing Financial Risk The Benefits

What are Swaps? Spring 2014. Stephen Sapp

What are Swaps? Spring 2014 Stephen Sapp Basic Idea of Swaps I have signed up for the Wine of the Month Club and you have signed up for the Beer of the Month Club. As winter approaches, I would like to

What are Swaps? Spring 2014 Stephen Sapp Basic Idea of Swaps I have signed up for the Wine of the Month Club and you have signed up for the Beer of the Month Club. As winter approaches, I would like to

INTEREST RATE SWAP (IRS)

") INTEREST RATE SWAP (IRS) 1. Interest Rate Swap (IRS)... 4 1.1 Terminology... 4 1.2 Application... 11 1.3 EONIA Swap... 19 1.4 Pricing and Mark to Market Revaluation of IRS... 22 2. Cross Currency Swap...

INTEREST RATE SWAP (IRS) 1. Interest Rate Swap (IRS)... 4 1.1 Terminology... 4 1.2 Application... 11 1.3 EONIA Swap... 19 1.4 Pricing and Mark to Market Revaluation of IRS... 22 2. Cross Currency Swap...

VALUATION OF PLAIN VANILLA INTEREST RATES SWAPS

Graduate School of Business Administration University of Virginia VALUATION OF PLAIN VANILLA INTEREST RATES SWAPS Interest-rate swaps have grown tremendously over the last 10 years. With this development,

Graduate School of Business Administration University of Virginia VALUATION OF PLAIN VANILLA INTEREST RATES SWAPS Interest-rate swaps have grown tremendously over the last 10 years. With this development,

CHAPTER 6. Different Types of Swaps 1

CHAPTER 6 Different Types of Swaps 1 In the previous chapter, we introduced two simple kinds of generic swaps: interest rate and currency swaps. These are usually known as plain vanilla deals because the

CHAPTER 6 Different Types of Swaps 1 In the previous chapter, we introduced two simple kinds of generic swaps: interest rate and currency swaps. These are usually known as plain vanilla deals because the

INTEREST RATE SWAPS September 1999

INTEREST RATE SWAPS September 1999 INTEREST RATE SWAPS Definition: Transfer of interest rate streams without transferring underlying debt. 2 FIXED FOR FLOATING SWAP Some Definitions Notational Principal:

INTEREST RATE SWAPS September 1999 INTEREST RATE SWAPS Definition: Transfer of interest rate streams without transferring underlying debt. 2 FIXED FOR FLOATING SWAP Some Definitions Notational Principal:

Floating rate Payments 6m Libor. Fixed rate payments 1 300000 337500-37500 2 300000 337500-37500 3 300000 337500-37500 4 300000 325000-25000

Introduction: Interest rate swaps are used to hedge interest rate risks as well as to take on interest rate risks. If a treasurer is of the view that interest rates will be falling in the future, he may

Introduction: Interest rate swaps are used to hedge interest rate risks as well as to take on interest rate risks. If a treasurer is of the view that interest rates will be falling in the future, he may

Understanding Cross Currency Swaps. A Guide for Microfinance Practitioners

Understanding Cross Currency Swaps A Guide for Microfinance Practitioners Cross Currency Swaps Use: A Currency Swap is the best way to fully hedge a loan transaction as the terms can be structured to exactly

Understanding Cross Currency Swaps A Guide for Microfinance Practitioners Cross Currency Swaps Use: A Currency Swap is the best way to fully hedge a loan transaction as the terms can be structured to exactly

Financial-Institutions Management. Solutions 4. 8. The following are the foreign currency positions of an FI, expressed in the foreign currency.

Solutions 4 Chapter 14: oreign Exchange Risk 8. The following are the foreign currency positions of an I, expressed in the foreign currency. Currency Assets Liabilities X Bought X Sold Swiss franc (S)

Solutions 4 Chapter 14: oreign Exchange Risk 8. The following are the foreign currency positions of an I, expressed in the foreign currency. Currency Assets Liabilities X Bought X Sold Swiss franc (S)

Fixed Income Portfolio Management. Interest rate sensitivity, duration, and convexity

Fixed Income ortfolio Management Interest rate sensitivity, duration, and convexity assive bond portfolio management Active bond portfolio management Interest rate swaps 1 Interest rate sensitivity, duration,

Fixed Income ortfolio Management Interest rate sensitivity, duration, and convexity assive bond portfolio management Active bond portfolio management Interest rate swaps 1 Interest rate sensitivity, duration,

CHAPTER 11 CURRENCY AND INTEREST RATE FUTURES

Answers to end-of-chapter exercises ARBITRAGE IN THE CURRENCY FUTURES MARKET 1. Consider the following: Spot Rate: $ 0.65/DM German 1-yr interest rate: 9% US 1-yr interest rate: 5% CHAPTER 11 CURRENCY

Answers to end-of-chapter exercises ARBITRAGE IN THE CURRENCY FUTURES MARKET 1. Consider the following: Spot Rate: $ 0.65/DM German 1-yr interest rate: 9% US 1-yr interest rate: 5% CHAPTER 11 CURRENCY

Manual for SOA Exam FM/CAS Exam 2.

Manual for SOA Exam FM/CAS Exam 2. Chapter 7. Derivatives markets. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall

Manual for SOA Exam FM/CAS Exam 2. Chapter 7. Derivatives markets. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall

Currency and Interest Rate Swaps

MWF 3:15-4:30 Gates B01 Final Exam MS&E 247S Fri Aug 15 2008 12:15PM-3:15PM Gates B01 Or Saturday Aug 16 2008 12:15PM-3:15PM Gates B01 Remote SCPD participants will also take the exam on Friday, 8/15 Please

MWF 3:15-4:30 Gates B01 Final Exam MS&E 247S Fri Aug 15 2008 12:15PM-3:15PM Gates B01 Or Saturday Aug 16 2008 12:15PM-3:15PM Gates B01 Remote SCPD participants will also take the exam on Friday, 8/15 Please

International Bond and Money Markets. Quiz Questions. True-False Questions

Chapter 9 International Bond and Money Markets Quiz Questions True-False Questions 1. The abolition of the Interest Equalization Tax, Regulation M, the cold war, and the US and UK foreign exchange controls

Chapter 9 International Bond and Money Markets Quiz Questions True-False Questions 1. The abolition of the Interest Equalization Tax, Regulation M, the cold war, and the US and UK foreign exchange controls

2 Stock Price. Figure S1.1 Profit from long position in Problem 1.13

Problem 1.11. A cattle farmer expects to have 12, pounds of live cattle to sell in three months. The livecattle futures contract on the Chicago Mercantile Exchange is for the delivery of 4, pounds of cattle.

Problem 1.11. A cattle farmer expects to have 12, pounds of live cattle to sell in three months. The livecattle futures contract on the Chicago Mercantile Exchange is for the delivery of 4, pounds of cattle.

DERIVATIVES Presented by Sade Odunaiya Partner, Risk Management Alliance Consulting DERIVATIVES Introduction Forward Rate Agreements FRA Swaps Futures Options Summary INTRODUCTION Financial Market Participants

DERIVATIVES Presented by Sade Odunaiya Partner, Risk Management Alliance Consulting DERIVATIVES Introduction Forward Rate Agreements FRA Swaps Futures Options Summary INTRODUCTION Financial Market Participants

Financial Risk Management

176 Financial Risk Management For the year ended 31 December 2014 1. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES s major financial instruments include cash and bank balances, time deposits, principal-protected

176 Financial Risk Management For the year ended 31 December 2014 1. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES s major financial instruments include cash and bank balances, time deposits, principal-protected

Fixed-Income Securities. Assignment

FIN 472 Professor Robert B.H. Hauswald Fixed-Income Securities Kogod School of Business, AU Assignment Please be reminded that you are expected to use contemporary computer software to solve the following

FIN 472 Professor Robert B.H. Hauswald Fixed-Income Securities Kogod School of Business, AU Assignment Please be reminded that you are expected to use contemporary computer software to solve the following

General Forex Glossary

General Forex Glossary A ADR American Depository Receipt Arbitrage The simultaneous buying and selling of a security at two different prices in two different markets, with the aim of creating profits without

General Forex Glossary A ADR American Depository Receipt Arbitrage The simultaneous buying and selling of a security at two different prices in two different markets, with the aim of creating profits without

1. HOW DOES FOREIGN EXCHANGE TRADING WORK?

XV. Important additional information on forex transactions / risks associated with foreign exchange transactions (also in the context of forward exchange transactions) The following information is given

XV. Important additional information on forex transactions / risks associated with foreign exchange transactions (also in the context of forward exchange transactions) The following information is given

This act of setting a price today for a transaction in the future, hedging. hedge currency exposure, short long long hedge short hedge Hedgers

Section 7.3 and Section 4.5 Oct. 7, 2002 William Pugh 7.3 Example of a forward contract: In May, a crude oil producer gets together with a refiner to agree on a price for crude oil. This price is for crude

Section 7.3 and Section 4.5 Oct. 7, 2002 William Pugh 7.3 Example of a forward contract: In May, a crude oil producer gets together with a refiner to agree on a price for crude oil. This price is for crude

CHAPTER 7 FUTURES AND OPTIONS ON FOREIGN EXCHANGE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 7 FUTURES AND OPTIONS ON FOREIGN EXCHANGE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Explain the basic differences between the operation of a currency

CHAPTER 7 FUTURES AND OPTIONS ON FOREIGN EXCHANGE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Explain the basic differences between the operation of a currency

Practice set #4 and solutions

FIN-465 Derivatives (3 credits) Professor Michel Robe Practice set #4 and solutions To help students with the material, seven practice sets with solutions will be handed out. They will not be graded: the

FIN-465 Derivatives (3 credits) Professor Michel Robe Practice set #4 and solutions To help students with the material, seven practice sets with solutions will be handed out. They will not be graded: the

(1.1) (7.3) $250m 6.05% US$ Guaranteed notes 2014 (164.5) Bank and other loans. (0.9) (1.2) Interest accrual

(7.3) $250m 6.05% US$ Guaranteed notes 2014 (164.5) Bank and other loans. (0.9) (1.2) Interest accrual") 17 Financial assets Available for sale financial assets include 111.1m (2013: 83.0m) UK government bonds. This investment forms part of the deficit-funding plan agreed with the trustee of one of the principal

17 Financial assets Available for sale financial assets include 111.1m (2013: 83.0m) UK government bonds. This investment forms part of the deficit-funding plan agreed with the trustee of one of the principal

CHAPTER 9 SUGGESTED ANSWERS TO CHAPTER 9 QUESTIONS

INSTRUCTOR S MANUAL MULTINATIONAL FINANCIAL MANAGEMENT, 9 TH ED. CHAPTER 9 SUGGESTED ANSWERS TO CHAPTER 9 QUESTIONS 1. What is an interest rate swap? What is the difference between a basis swap and a coupon

INSTRUCTOR S MANUAL MULTINATIONAL FINANCIAL MANAGEMENT, 9 TH ED. CHAPTER 9 SUGGESTED ANSWERS TO CHAPTER 9 QUESTIONS 1. What is an interest rate swap? What is the difference between a basis swap and a coupon

Forwards and Futures

Prof. Alex Shapiro Lecture Notes 16 Forwards and Futures I. Readings and Suggested Practice Problems II. Forward Contracts III. Futures Contracts IV. Forward-Spot Parity V. Stock Index Forward-Spot Parity

Prof. Alex Shapiro Lecture Notes 16 Forwards and Futures I. Readings and Suggested Practice Problems II. Forward Contracts III. Futures Contracts IV. Forward-Spot Parity V. Stock Index Forward-Spot Parity

Interest Rate Swaps. Key Concepts and Buzzwords. Readings Tuckman, Chapter 18. Swaps Swap Spreads Credit Risk of Swaps Uses of Swaps

Interest Rate Swaps Key Concepts and Buzzwords Swaps Swap Spreads Credit Risk of Swaps Uses of Swaps Readings Tuckman, Chapter 18. Counterparty, Notional amount, Plain vanilla swap, Swap rate Interest

Interest Rate Swaps Key Concepts and Buzzwords Swaps Swap Spreads Credit Risk of Swaps Uses of Swaps Readings Tuckman, Chapter 18. Counterparty, Notional amount, Plain vanilla swap, Swap rate Interest

CHAPTER 7 SUGGESTED ANSWERS TO CHAPTER 7 QUESTIONS

INSTRUCTOR S MANUAL: MULTINATIONAL FINANCIAL MANAGEMENT, 9 TH ED. CHAPTER 7 SUGGESTED ANSWERS TO CHAPTER 7 QUESTIONS 1. Answer the following questions based on data in Exhibit 7.5. a. How many Swiss francs

INSTRUCTOR S MANUAL: MULTINATIONAL FINANCIAL MANAGEMENT, 9 TH ED. CHAPTER 7 SUGGESTED ANSWERS TO CHAPTER 7 QUESTIONS 1. Answer the following questions based on data in Exhibit 7.5. a. How many Swiss francs

How To Understand The Swap Market

CHAPTER 13 CURRENCY AND INTEREST RATE SWAPS Chapter Overview This chapter is about currency and interest rate swaps. It begins by describing the origins of the swap market and the role played by capital

CHAPTER 13 CURRENCY AND INTEREST RATE SWAPS Chapter Overview This chapter is about currency and interest rate swaps. It begins by describing the origins of the swap market and the role played by capital

Forwards, Futures and Money Market Hedging. Prof. Ian Giddy New York University. Hedging Transactions Exposure. Ongoing transactions exposure

Forwards, Futures and Money-Market Hedging/1 Forwards, Futures and Money Market Hedging Prof. Ian Giddy New York University Hedging Transactions Exposure Types of exposure One-shot exposure Hedging approaches:

Forwards, Futures and Money-Market Hedging/1 Forwards, Futures and Money Market Hedging Prof. Ian Giddy New York University Hedging Transactions Exposure Types of exposure One-shot exposure Hedging approaches:

CHAPTER 10. CURRENCY SWAPS

CHAPTER 10. CURRENCY SWAPS The advent of swaps, as much as anything else, helped transform the world s segmented capital markets into a single, truly integrated, international capital market. John F. Marshall

CHAPTER 10. CURRENCY SWAPS The advent of swaps, as much as anything else, helped transform the world s segmented capital markets into a single, truly integrated, international capital market. John F. Marshall

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT PROBLEM SETS 1. In formulating a hedge position, a stock s beta and a bond s duration are used similarly to determine the expected percentage gain or loss

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT PROBLEM SETS 1. In formulating a hedge position, a stock s beta and a bond s duration are used similarly to determine the expected percentage gain or loss

Trading in Treasury Bond Futures Contracts and Bonds in Australia

Trading in Treasury Bond Futures Contracts and Bonds in Australia Belinda Cheung* Treasury bond futures are a key financial product in Australia, with turnover in Treasury bond futures contracts significantly

Trading in Treasury Bond Futures Contracts and Bonds in Australia Belinda Cheung* Treasury bond futures are a key financial product in Australia, with turnover in Treasury bond futures contracts significantly

Introduction to swaps

Introduction to swaps Steven C. Mann M.J. Neeley School of Business Texas Christian University incorporating ideas from Teaching interest rate and currency swaps" by Keith C. Brown (Texas-Austin) and Donald

Introduction to swaps Steven C. Mann M.J. Neeley School of Business Texas Christian University incorporating ideas from Teaching interest rate and currency swaps" by Keith C. Brown (Texas-Austin) and Donald

Derivatives, Measurement and Hedge Accounting

Derivatives, Measurement and Hedge Accounting IAS 39 11 June 2008 Contents Derivatives and embedded derivatives Definition Sample of products Accounting treatment Measurement Active market VS Inactive

Derivatives, Measurement and Hedge Accounting IAS 39 11 June 2008 Contents Derivatives and embedded derivatives Definition Sample of products Accounting treatment Measurement Active market VS Inactive

January 1, Year 1 Equipment... 100,000 Note Payable... 100,000

Illustrations of Accounting for Derivatives Extension of Chapter 11 Web This reading illustrates the accounting for the interest rate swaps in Examples 13 and 14 in Chapter 11. Web problem DERIVATIVE 1

Illustrations of Accounting for Derivatives Extension of Chapter 11 Web This reading illustrates the accounting for the interest rate swaps in Examples 13 and 14 in Chapter 11. Web problem DERIVATIVE 1

Interest Rate and Currency Swaps

Interest Rate and Currency Swaps Eiteman et al., Chapter 14 Winter 2004 Bond Basics Consider the following: Zero-Coupon Zero-Coupon One-Year Implied Maturity Bond Yield Bond Price Forward Rate t r 0 (0,t)

Interest Rate and Currency Swaps Eiteman et al., Chapter 14 Winter 2004 Bond Basics Consider the following: Zero-Coupon Zero-Coupon One-Year Implied Maturity Bond Yield Bond Price Forward Rate t r 0 (0,t)

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. How would you define transaction exposure? How is it different from economic

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. How would you define transaction exposure? How is it different from economic

Assumptions: No transaction cost, same rate for borrowing/lending, no default/counterparty risk

Derivatives Why? Allow easier methods to short sell a stock without a broker lending it. Facilitates hedging easily Allows the ability to take long/short position on less available commodities (Rice, Cotton,

Derivatives Why? Allow easier methods to short sell a stock without a broker lending it. Facilitates hedging easily Allows the ability to take long/short position on less available commodities (Rice, Cotton,

Maturity The date where the issuer must return the principal or the face value to the investor.

PRODUCT INFORMATION SHEET - BONDS 1. WHAT ARE BONDS? A bond is a debt instrument issued by a borrowing entity (issuer) to investors (lenders) in return for lending their money to the issuer. The issuer

PRODUCT INFORMATION SHEET - BONDS 1. WHAT ARE BONDS? A bond is a debt instrument issued by a borrowing entity (issuer) to investors (lenders) in return for lending their money to the issuer. The issuer

Class Note on Valuing Swaps

Corporate Finance Professor Gordon Bodnar Class Note on Valuing Swaps A swap is a financial instrument that exchanges one set of cash flows for another set of cash flows of equal expected value. Swaps

Corporate Finance Professor Gordon Bodnar Class Note on Valuing Swaps A swap is a financial instrument that exchanges one set of cash flows for another set of cash flows of equal expected value. Swaps

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

The PricewaterhouseCoopers Credit Derivatives Primer

The PricewaterhouseCoopers Credit Derivatives Primer Financial Advisory Services John D. Finnerty Table of Contents What are Credit Derivatives?...................................3 A Definition............................................4

The PricewaterhouseCoopers Credit Derivatives Primer Financial Advisory Services John D. Finnerty Table of Contents What are Credit Derivatives?...................................3 A Definition............................................4

Introduction to Derivative Instruments Part 1 Link n Learn

Introduction to Derivative Instruments Part 1 Link n Learn June 2014 Webinar Participants Elaine Canty Manager Financial Advisory Deloitte & Touche Ireland [email protected] +353 1 417 2991 Christopher

Introduction to Derivative Instruments Part 1 Link n Learn June 2014 Webinar Participants Elaine Canty Manager Financial Advisory Deloitte & Touche Ireland [email protected] +353 1 417 2991 Christopher

SOCIETY OF ACTUARIES FINANCIAL MATHEMATICS. EXAM FM SAMPLE QUESTIONS Financial Economics

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS Financial Economics June 2014 changes Questions 1-30 are from the prior version of this document. They have been edited to conform

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS Financial Economics June 2014 changes Questions 1-30 are from the prior version of this document. They have been edited to conform

The Market for Foreign Exchange

The Market for Foreign Exchange Chapter Objective: 5 Chapter Five This chapter introduces the institutional framework within which exchange rates are determined. It lays the foundation for much of the

The Market for Foreign Exchange Chapter Objective: 5 Chapter Five This chapter introduces the institutional framework within which exchange rates are determined. It lays the foundation for much of the

Total Return Swaps: Credit Derivatives and Synthetic Funding Instruments

Learning Curve Total Return Swaps: Credit Derivatives and Synthetic Funding Instruments Moorad Choudhry YieldCurve.com 2004 Page 1 A total return swap (TRS), sometimes known as a total rate of return swap

Learning Curve Total Return Swaps: Credit Derivatives and Synthetic Funding Instruments Moorad Choudhry YieldCurve.com 2004 Page 1 A total return swap (TRS), sometimes known as a total rate of return swap

Learning Curve Interest Rate Futures Contracts Moorad Choudhry

Learning Curve Interest Rate Futures Contracts Moorad Choudhry YieldCurve.com 2004 Page 1 The market in short-term interest rate derivatives is a large and liquid one, and the instruments involved are

Learning Curve Interest Rate Futures Contracts Moorad Choudhry YieldCurve.com 2004 Page 1 The market in short-term interest rate derivatives is a large and liquid one, and the instruments involved are

OTC Derivatives: Benefits to U.S. Companies

OTC Derivatives: Benefits to U.S. Companies International Swaps and Derivatives Association May 2009 1 What are derivatives? Derivatives are financial instruments that: Transfer risk from one party to

OTC Derivatives: Benefits to U.S. Companies International Swaps and Derivatives Association May 2009 1 What are derivatives? Derivatives are financial instruments that: Transfer risk from one party to

SwapEx Contract Specifications. USD LIBOR Interest Rate Swaps: Fixedto-Floating

SwapEx Contract Specifications USD LIBOR Interest Rate Swaps: Fixedto-Floating There are two types of USD LIBOR Interest Rate Swaps; Fixed-to-Floating contracts available for trading on SwapEx: Fixed Rate

SwapEx Contract Specifications USD LIBOR Interest Rate Swaps: Fixedto-Floating There are two types of USD LIBOR Interest Rate Swaps; Fixed-to-Floating contracts available for trading on SwapEx: Fixed Rate

Assignment 10 (Chapter 11)

") Assignment 10 (Chapter 11) 1. Which of the following tends to cause the U.S. dollar to appreciate in value? a) An increase in U.S. prices above foreign prices b) Rapid economic growth in foreign countries

Assignment 10 (Chapter 11) 1. Which of the following tends to cause the U.S. dollar to appreciate in value? a) An increase in U.S. prices above foreign prices b) Rapid economic growth in foreign countries

Interest Rate Swap. Product Disclosure Statement

Interest Rate Swap Product Disclosure Statement A Product Disclosure Statement is an informative document. The purpose of a Product Disclosure Statement is to provide you with enough information to allow

Interest Rate Swap Product Disclosure Statement A Product Disclosure Statement is an informative document. The purpose of a Product Disclosure Statement is to provide you with enough information to allow

Learning Curve Forward Rate Agreements Anuk Teasdale

Learning Curve Forward Rate Agreements Anuk Teasdale YieldCurve.com 2004 Page 1 In this article we review the forward rate agreement. Money market derivatives are priced on the basis of the forward rate,

Learning Curve Forward Rate Agreements Anuk Teasdale YieldCurve.com 2004 Page 1 In this article we review the forward rate agreement. Money market derivatives are priced on the basis of the forward rate,

Renminbi (RMB) corporate and treasury services in London

corporate and treasury services in London") Renminbi (RMB) corporate and treasury services in London City of London RENMINBI SERIES London offers an extensive range of RMB corporate banking services including: o Corporate accounts; o Term deposits;

Renminbi (RMB) corporate and treasury services in London City of London RENMINBI SERIES London offers an extensive range of RMB corporate banking services including: o Corporate accounts; o Term deposits;

Eurodollar Futures, and Forwards

5 Eurodollar Futures, and Forwards In this chapter we will learn about Eurodollar Deposits Eurodollar Futures Contracts, Hedging strategies using ED Futures, Forward Rate Agreements, Pricing FRAs. Hedging

5 Eurodollar Futures, and Forwards In this chapter we will learn about Eurodollar Deposits Eurodollar Futures Contracts, Hedging strategies using ED Futures, Forward Rate Agreements, Pricing FRAs. Hedging

Understanding and Managing Interest Rate Risk

Understanding and Managing Interest Rate Risk Finance & Treasury April 2008 CPA Australia Ltd ( CPA Australia ) is the sixth largest professional accounting body in the world with more than 117,000 members

Understanding and Managing Interest Rate Risk Finance & Treasury April 2008 CPA Australia Ltd ( CPA Australia ) is the sixth largest professional accounting body in the world with more than 117,000 members

Swaps: complex structures

Swaps: complex structures Complex swap structures refer to non-standard swaps whose coupons, notional, accrual and calendar used for coupon determination and payments are tailored made to serve client

Swaps: complex structures Complex swap structures refer to non-standard swaps whose coupons, notional, accrual and calendar used for coupon determination and payments are tailored made to serve client

Fin 3312 Sample Exam 1 Questions

Fin 3312 Sample Exam 1 Questions Here are some representative type questions. This review is intended to give you an idea of the types of questions that may appear on the exam, and how the questions might

Fin 3312 Sample Exam 1 Questions Here are some representative type questions. This review is intended to give you an idea of the types of questions that may appear on the exam, and how the questions might

Forward exchange rates

Forward exchange rates The forex market consists of two distinct markets - the spot foreign exchange market (in which currencies are bought and sold for delivery within two working days) and the forward

Forward exchange rates The forex market consists of two distinct markets - the spot foreign exchange market (in which currencies are bought and sold for delivery within two working days) and the forward

ANALYSIS OF FIXED INCOME SECURITIES

ANALYSIS OF FIXED INCOME SECURITIES Valuation of Fixed Income Securities Page 1 VALUATION Valuation is the process of determining the fair value of a financial asset. The fair value of an asset is its

ANALYSIS OF FIXED INCOME SECURITIES Valuation of Fixed Income Securities Page 1 VALUATION Valuation is the process of determining the fair value of a financial asset. The fair value of an asset is its

An introduction to the foreign exchange market Moorad Choudhry September 2002

An introduction to the foreign exchange market Moorad Choudhry September 2002 The market in foreign exchange is an excellent example of a liquid, transparent and immediate global financial market. Rates

An introduction to the foreign exchange market Moorad Choudhry September 2002 The market in foreign exchange is an excellent example of a liquid, transparent and immediate global financial market. Rates

CHAPTER 8 SUGGESTED ANSWERS TO CHAPTER 8 QUESTIONS

INSTRUCTOR S MANUAL: MULTINATIONAL FINANCIAL MANAGEMENT, 9 TH ED. CHAPTER 8 SUGGESTED ANSWERS TO CHAPTER 8 QUESTIONS. On April, the spot price of the British pound was $.86 and the price of the June futures

INSTRUCTOR S MANUAL: MULTINATIONAL FINANCIAL MANAGEMENT, 9 TH ED. CHAPTER 8 SUGGESTED ANSWERS TO CHAPTER 8 QUESTIONS. On April, the spot price of the British pound was $.86 and the price of the June futures

How To Get A Long Euro Forward Position On Eurodollar From A Short Euro Position On A Short Currency

CHAPTER 3. FORWARD FOREIGN EXCHANGE In a forward foreign exchange (FX) contract, two parties contract today for the future exchange of currencies at a forward FX rate. No funds change hands when a typical

CHAPTER 3. FORWARD FOREIGN EXCHANGE In a forward foreign exchange (FX) contract, two parties contract today for the future exchange of currencies at a forward FX rate. No funds change hands when a typical

Condensed Interim Consolidated Financial Statements of. Canada Pension Plan Investment Board

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board September 30, 2015 Condensed Interim Consolidated Balance Sheet As at September 30, 2015 As at September 30,

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board September 30, 2015 Condensed Interim Consolidated Balance Sheet As at September 30, 2015 As at September 30,

Buy = Pay Fixed, Receive Float -or- Pay Float +/- Spread, Receive Float Sell = Receive Fixed, Pay Float -or- Receive Float +/- Spread, Pay Float

VIA Electronic Submission Office of the Secretariat Commodity Futures Trading Commission Three Lafayette Centre 1155 21 st Street, N.W. Washington, DC 20581 Re: Javelin SEF, LLC To Whom It May Concern,

VIA Electronic Submission Office of the Secretariat Commodity Futures Trading Commission Three Lafayette Centre 1155 21 st Street, N.W. Washington, DC 20581 Re: Javelin SEF, LLC To Whom It May Concern,

Advanced Derivatives:

Advanced Derivatives: (plain vanilla to Rainbows) advanced swaps Structured notes exotic options Finance 7523. Spring 1999 The Neeley School of Business at TCU Steven C. Mann, 1999. Equity Swaps Example:

Advanced Derivatives: (plain vanilla to Rainbows) advanced swaps Structured notes exotic options Finance 7523. Spring 1999 The Neeley School of Business at TCU Steven C. Mann, 1999. Equity Swaps Example:

Risk and Investment Conference 2013. Brighton, 17 19 June

Risk and Investment Conference 03 Brighton, 7 9 June 0 June 03 Acquiring fixed income assets on a forward basis Dick Rae, HSBC and Neil Snyman, Aviva Investors 8 June 0 Structure of Presentation Introduction

Risk and Investment Conference 03 Brighton, 7 9 June 0 June 03 Acquiring fixed income assets on a forward basis Dick Rae, HSBC and Neil Snyman, Aviva Investors 8 June 0 Structure of Presentation Introduction

DFA INVESTMENT DIMENSIONS GROUP INC.

PROSPECTUS February 28, 2015 Please carefully read the important information it contains before investing. DFA INVESTMENT DIMENSIONS GROUP INC. DFA ONE-YEAR FIXED INCOME PORTFOLIO Ticker: DFIHX DFA TWO-YEAR

PROSPECTUS February 28, 2015 Please carefully read the important information it contains before investing. DFA INVESTMENT DIMENSIONS GROUP INC. DFA ONE-YEAR FIXED INCOME PORTFOLIO Ticker: DFIHX DFA TWO-YEAR

Chapter 12. Page 1. Bonds: Analysis and Strategy. Learning Objectives. INVESTMENTS: Analysis and Management Second Canadian Edition

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 12 Bonds: Analysis and Strategy Learning Objectives Explain why investors buy bonds. Discuss major considerations

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 12 Bonds: Analysis and Strategy Learning Objectives Explain why investors buy bonds. Discuss major considerations

FIN 472 Fixed-Income Securities Forward Rates

FIN 472 Fixed-Income Securities Forward Rates Professor Robert B.H. Hauswald Kogod School of Business, AU Interest-Rate Forwards Review of yield curve analysis Forwards yet another use of yield curve forward

FIN 472 Fixed-Income Securities Forward Rates Professor Robert B.H. Hauswald Kogod School of Business, AU Interest-Rate Forwards Review of yield curve analysis Forwards yet another use of yield curve forward

CFA Level -2 Derivatives - I

CFA Level -2 Derivatives - I EduPristine www.edupristine.com Agenda Forwards Markets and Contracts Future Markets and Contracts Option Markets and Contracts 1 Forwards Markets and Contracts 2 Pricing and

CFA Level -2 Derivatives - I EduPristine www.edupristine.com Agenda Forwards Markets and Contracts Future Markets and Contracts Option Markets and Contracts 1 Forwards Markets and Contracts 2 Pricing and

Futures Price d,f $ 0.65 = (1.05) (1.04)

(1.04)") 24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

How To Understand The Swap Curve

INSTITUTE OF ECONOMIC STUDIES Faculty of social sciences of Charles University SWAPS Financial Market Instruments (Lecture s Notes No. ) Oldřich Dědek 2 A. INTEREST RATE SWAP 1. Basic concepts interest

INSTITUTE OF ECONOMIC STUDIES Faculty of social sciences of Charles University SWAPS Financial Market Instruments (Lecture s Notes No. ) Oldřich Dědek 2 A. INTEREST RATE SWAP 1. Basic concepts interest

Major Terms and Conditions of the IBRD Fixed Spread Loan (FSL) i

i") Major Terms and Conditions of the IBRD Fixed Spread Loan (FSL) i The interest rate on FSLs consists of (a) a variable base rate of six-month LIBOR 1 in respect of each interest period for each loan; and

Major Terms and Conditions of the IBRD Fixed Spread Loan (FSL) i The interest rate on FSLs consists of (a) a variable base rate of six-month LIBOR 1 in respect of each interest period for each loan; and

Lecture 12. Options Strategies

Lecture 12. Options Strategies Introduction to Options Strategies Options, Futures, Derivatives 10/15/07 back to start 1 Solutions Problem 6:23: Assume that a bank can borrow or lend money at the same

Lecture 12. Options Strategies Introduction to Options Strategies Options, Futures, Derivatives 10/15/07 back to start 1 Solutions Problem 6:23: Assume that a bank can borrow or lend money at the same

Test 4 Created: 3:05:28 PM CDT 1. The buyer of a call option has the choice to exercise, but the writer of the call option has: A.

Test 4 Created: 3:05:28 PM CDT 1. The buyer of a call option has the choice to exercise, but the writer of the call option has: A. The choice to offset with a put option B. The obligation to deliver the

Test 4 Created: 3:05:28 PM CDT 1. The buyer of a call option has the choice to exercise, but the writer of the call option has: A. The choice to offset with a put option B. The obligation to deliver the

LOCKING IN TREASURY RATES WITH TREASURY LOCKS

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

Chapter 16 OVER-THE-COUNTER INTEREST RATE DERIVATIVES

Page 238 The information in this chapter was last updated in 1993. Since the money market evolves very rapidly, recent developments may have superseded some of the content of this chapter. Chapter 16 OVER-THE-COUNTER

Page 238 The information in this chapter was last updated in 1993. Since the money market evolves very rapidly, recent developments may have superseded some of the content of this chapter. Chapter 16 OVER-THE-COUNTER

3. The Foreign Exchange Market

3. The Foreign Exchange Market The foreign exchange market provides the physical and institutional structure through which the money of one country is exchanged for that of another country, the rate of

3. The Foreign Exchange Market The foreign exchange market provides the physical and institutional structure through which the money of one country is exchanged for that of another country, the rate of

Fina4500 Spring 2015 Extra Practice Problems Instructions

Extra Practice Problems Instructions: The problems are similar to the ones on your previous problem sets. All interest rates and rates of inflation given in the problems are annualized (i.e., stated as

Extra Practice Problems Instructions: The problems are similar to the ones on your previous problem sets. All interest rates and rates of inflation given in the problems are annualized (i.e., stated as

Eris Interest Rate Swap Futures: Flex Contract Specifications

Eris Interest Rate Swap Futures: Flex Contract Specifications Trading Hours Contract Structure Contract Size Trading Conventions Swap Futures Leg Conventions Effective Date Cash Flow Alignment Date ( CFAD

Eris Interest Rate Swap Futures: Flex Contract Specifications Trading Hours Contract Structure Contract Size Trading Conventions Swap Futures Leg Conventions Effective Date Cash Flow Alignment Date ( CFAD

Unaudited financial report for the. sixt-month period ended 30 June 2015. Deutsche Bahn Finance B.V. Amsterdam

Unaudited financial report for the sixt-month period ended 30 June 2015 Deutsche Bahn Finance B.V. Table of contents Annual report of the directors 3 Balance sheet as at 30 June 2015 4 Profit and loss

Unaudited financial report for the sixt-month period ended 30 June 2015 Deutsche Bahn Finance B.V. Table of contents Annual report of the directors 3 Balance sheet as at 30 June 2015 4 Profit and loss

The determinants of the swap spread Moorad Choudhry * September 2006

The determinants of the swap spread Moorad Choudhry * September 6 YieldCurve.com 6 Page 1 Interest-rate swaps are an important ALM and risk management tool in banking markets. The rate payable on a swap

The determinants of the swap spread Moorad Choudhry * September 6 YieldCurve.com 6 Page 1 Interest-rate swaps are an important ALM and risk management tool in banking markets. The rate payable on a swap

Introduction to Fixed Income (IFI) Course Syllabus

Course Syllabus") Introduction to Fixed Income (IFI) Course Syllabus 1. Fixed income markets 1.1 Understand the function of fixed income markets 1.2 Know the main fixed income market products: Loans Bonds Money market instruments

Introduction to Fixed Income (IFI) Course Syllabus 1. Fixed income markets 1.1 Understand the function of fixed income markets 1.2 Know the main fixed income market products: Loans Bonds Money market instruments

How To Invest In Stocks And Bonds

Review for Exam 1 Instructions: Please read carefully The exam will have 21 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Review for Exam 1 Instructions: Please read carefully The exam will have 21 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Credit Derivatives. Southeastern Actuaries Conference. Fall Meeting. November 18, 2005. Credit Derivatives. What are they? How are they priced?

1 Credit Derivatives Southeastern Actuaries Conference Fall Meeting November 18, 2005 Credit Derivatives What are they? How are they priced? Applications in risk management Potential uses 2 2 Credit Derivatives

1 Credit Derivatives Southeastern Actuaries Conference Fall Meeting November 18, 2005 Credit Derivatives What are they? How are they priced? Applications in risk management Potential uses 2 2 Credit Derivatives

AUSTRALIAN BANKS GLOBAL BOND FUNDING 1

AUSTRALIAN BANKS GLOBAL BOND FUNDING 1 Introduction Over the past decade, Australian banks have sourced a sizeable share of their funding in offshore markets. This article examines various aspects of these

AUSTRALIAN BANKS GLOBAL BOND FUNDING 1 Introduction Over the past decade, Australian banks have sourced a sizeable share of their funding in offshore markets. This article examines various aspects of these

Foreign Exchange Market: Chapter 7. Chapter Objectives & Lecture Notes FINA 5500

Foreign Exchange Market: Chapter 7 Chapter Objectives & Lecture Notes FINA 5500 Chapter Objectives: FINA 5500 Chapter 7 / FX Markets 1. To be able to interpret direct and indirect quotes in the spot market

Foreign Exchange Market: Chapter 7 Chapter Objectives & Lecture Notes FINA 5500 Chapter Objectives: FINA 5500 Chapter 7 / FX Markets 1. To be able to interpret direct and indirect quotes in the spot market

A guide to managing foreign exchange risk

A guide to managing foreign exchange risk CPA Australia Ltd ( CPA Australia ) is one of the world s largest accounting bodies with more than 122,000 members of the financial, accounting and business profession

A guide to managing foreign exchange risk CPA Australia Ltd ( CPA Australia ) is one of the world s largest accounting bodies with more than 122,000 members of the financial, accounting and business profession

CHAPTER 12 INTERNATIONAL BOND MARKETS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 12 INTERNATIONAL BOND MARKETS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Describe the differences between foreign bonds and Eurobonds. Also discuss why

CHAPTER 12 INTERNATIONAL BOND MARKETS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Describe the differences between foreign bonds and Eurobonds. Also discuss why

General Risk Disclosure

General Risk Disclosure Colmex Pro Ltd (hereinafter called the Company ) is an Investment Firm regulated by the Cyprus Securities and Exchange Commission (license number 123/10). This notice is provided

General Risk Disclosure Colmex Pro Ltd (hereinafter called the Company ) is an Investment Firm regulated by the Cyprus Securities and Exchange Commission (license number 123/10). This notice is provided

Chapter 14 Foreign Exchange Markets and Exchange Rates

Chapter 14 Foreign Exchange Markets and Exchange Rates International transactions have one common element that distinguishes them from domestic transactions: one of the participants must deal in a foreign

Chapter 14 Foreign Exchange Markets and Exchange Rates International transactions have one common element that distinguishes them from domestic transactions: one of the participants must deal in a foreign

Form SR-4 Foreign Exchange and OTC Derivatives Notes to assist Completion

Form SR-4 Foreign Exchange and OTC Derivatives Notes to assist Completion Section 1 of this return is aimed at establishing the exposure to the risk of loss arising from adverse movements in foreign exchange

Form SR-4 Foreign Exchange and OTC Derivatives Notes to assist Completion Section 1 of this return is aimed at establishing the exposure to the risk of loss arising from adverse movements in foreign exchange

J. Gaspar: Adapted from Jeff Madura International Financial Management

Chapter3 International Financial Markets J. Gaspar: Adapted from Jeff Madura International Financial Management 3-1 International Financial Markets Can be segmented as follows: 1.The Foreign Exchange Market

Chapter3 International Financial Markets J. Gaspar: Adapted from Jeff Madura International Financial Management 3-1 International Financial Markets Can be segmented as follows: 1.The Foreign Exchange Market

Chapter 5. The Foreign Exchange Market. Foreign Exchange Markets: Learning Objectives. Foreign Exchange Markets. Foreign Exchange Markets

Chapter 5 The Foreign Exchange Market Foreign Exchange Markets: Learning Objectives Examine the functions performed by the foreign exchange (FOREX) market, its participants, size, geographic and currency

Chapter 5 The Foreign Exchange Market Foreign Exchange Markets: Learning Objectives Examine the functions performed by the foreign exchange (FOREX) market, its participants, size, geographic and currency

How Hedging Can Substantially Reduce Foreign Stock Currency Risk

Possible losses from changes in currency exchange rates are a risk of investing unhedged in foreign stocks. While a stock may perform well on the London Stock Exchange, if the British pound declines against

Possible losses from changes in currency exchange rates are a risk of investing unhedged in foreign stocks. While a stock may perform well on the London Stock Exchange, if the British pound declines against