Alcohol Wholesaler Registration Scheme (AWRS) Briefing Pack

|

|

|

- Belinda Griffin

- 9 years ago

- Views:

Transcription

1 Alcohol Wholesaler Registration Scheme (AWRS) Briefing Pack

")

2

3 Contents Introduction of the Alcohol Wholesaler Registration Scheme 1 Decision making do you need to register? 5 Timeline 7 Questions and answers 8

4

5 Introduction of the Alcohol Wholesaler Registration Scheme (AWRS) HMRC is introducing a new scheme to help combat alcohol duty fraud. Criminals are targeting the UK, inserting duty unpaid goods into wholesale and retail supply chains. This scheme will help to reduce the estimated 1.3 billion in public money lost each year to this fraud, and lessen the damaging effects of competition from illicit trading on legitimate businesses. Who is affected? Anyone who sells, or arranges the sale, of alcohol to other businesses at or after the point at which excise duty becomes due 1 will need to apply to register for this scheme. The types of businesses likely to be affected include: manufacturers and other excise traders alcohol wholesalers and cash & carrys brokers auctioneers Even if you already hold an excise registration(s), you may also need to register for AWRS. Others who buy alcohol to sell to the consumer, such as retailers, hotels, pubs, restaurants, cafes and clubs ( trade buyers ) do not need to apply unless they also sell alcohol to other businesses, but from 1 April 2017 they must ensure they only buy alcohol from others approved by HMRC under this scheme. To find out if you need to register, please use the flowchart Decision making: Do you need to apply to register? on page 5 and, if you need to, the flowchart on page 6. 1 Alcohol is a dutiable product. This means that before it is released for UK consumption (unless there is a specific exemption or relief that has been granted for the goods in question) duty should be paid to HMRC. The duty point is often when the manufacturer sells the goods within the UK, when goods are imported and enter the UK market, or they are released from an excise registered premises approved by HMRC to hold and move duty unpaid goods. 1

6 When does the scheme take effect? From 1 October 2015, if you meet the criteria for registration: you will need to apply online to HMRC to register for AWRS, between 1 October 2015 and 31 December HMRC will begin to consider applications for AWRS from 1 January 2016 onwards, issuing decisions on your approval to trade in alcohol as soon as possible thereafter. Decisions will be based on whether a business is fit and proper to carry on trading (see below for a description of the criteria applied). Where a business fails the fit and proper test, HMRC will remove its right to wholesale alcohol. if you are a new business wishing to begin operating at any time after 31 December 2015, you must apply for registration at least 45 days before you intend to start and must wait until you receive an approval from HMRC before you start trading. From 1 April 2017, for all businesses selling alcohol: all businesses will need to make sure they buy from HMRC approved sources. This includes those selling to the consumer such as retailers, hotels, pubs, restaurants, cafes and clubs ( trade buyers ), as well as all other businesses in the supply chain who buy alcohol at or after the point at which excise duty becomes due to HMRC. HMRC will provide an online database of approved traders to help businesses carry out due diligence regarding the legitimacy of their suppliers. Preparing for AWRS what can you do to get ready? If you are selling, or arranging the sale, of alcohol to other businesses, and meet the registration criteria: There is much you can do now to get ready for applying for AWRS, and for most businesses you will already have much of this covered as part of your due diligence, including: making sure your business records are in order and accessible. reviewing your processes and supply chains to make sure you are sourcing only legitimate alcohol, and. introducing a corporate due diligence policy and procedures to prevent involvement in the illicit market. It is recommended you; o o o o consider and document the risks of fraud within your supply chain know your suppliers - satisfy yourself that deals look and feel genuine know the origin and supply chain for the goods you buy, and seek assurances from your supplier that duty has been paid do not readily accept deals which appear to be too good to be true 2

.")

7 If you are an alcohol trade buyer such as a retailer, hotel, pub, restaurant, cafe or club: If you buy alcohol from UK wholesalers to sell on to your own customers: you should review your processes and supply chains to make sure you are sourcing only legitimate alcohol check that your own wholesalers are aware of the scheme, so that they can prepare for the changes from 1 April 2017, once the new scheme is fully implemented, you will be able to check that the business you buy alcohol from has been approved by HMRC. Fit and proper criteria For a business to be approved to wholesale alcohol HMRC will assess its application against fit and proper criteria. This may involve a face-to-face visit. HMRC will need to make sure that: there is no evidence of illicit trading the applicant, or any person with an important role in the business has not previously been involved in any significant revenue non-compliance or fraud there are no connections between the business, or key persons involved in the business, with other known non-compliant or fraudulent businesses key people involved in the business have no criminal convictions which HMRC consider relevant - for example offences involving any dishonesty or links to organised criminal activity the application is accurate and complete and there has been no attempt to deceive there have not been persistent or negligent failures to comply with any HMRC recordkeeping requirements the applicant has not previously attempted to avoid registration nor traded unauthorised the business has provided sufficient evidence of its commercial viability and/or credibility there are no outstanding, unmanaged HMRC debts or a history of poor payment the business has satisfactory due diligence procedures to protect it from trading in illicit supply-chains. The criteria above are not exhaustive. HMRC may refuse approval to a wholesaler for reasons other than those listed if there are concerns that the applicant s activities pose a serious risk to public revenues. Any approval given may also be subject to conditions. Penalties New criminal and civil sanctions will be introduced for wholesalers who trade without HMRC approval, and for trade buyers who buy alcohol from non-registered wholesalers. 3

8 Further information You can find more information about the new scheme on the GOV.UK website, search for Alcohol Wholesaler Registration Scheme. Sign up for news alerts about alcohol duties at - this means you will get an when we publish more information about the scheme on GOV.UK. 4

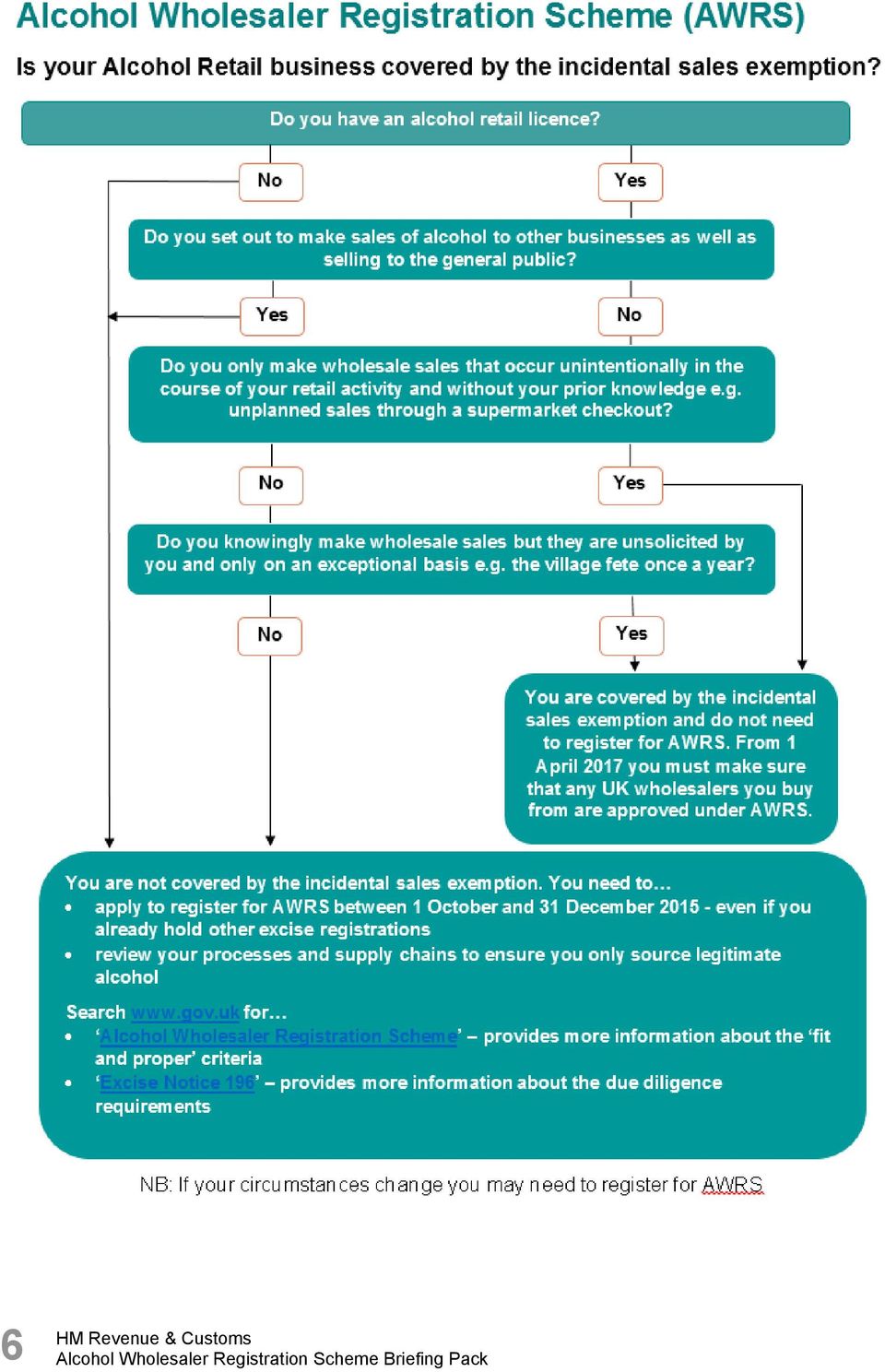

9 Decision making do you need to register? 5

10 6

11 Timeline 7

12 Questions and answers How and when do I register for the scheme if I am an existing wholesaler? Registration will be online via the Government Gateway. Existing wholesalers must apply for the scheme from 1 October 2015 to 31 December How and when do new businesses apply? Registration will be online via the Government Gateway. Any new businesses who wish to begin wholesaling alcohol at any time after 31 December 2015 must apply for registration at least 45 days before their intended start date and must wait until they receive HMRC s decision before they start trading. What information will I need when I apply to register? This will depend what kind of business you are. However, all applicants will need to provide the following as a minimum: legal entity name trading name VAT Registration Number (if registered) Self Assessment UTR number (if registered) registered business address and how long at that address contact telephone number address postal address number of employees your annual turnover types of customer products sold number of premises and their addresses business names and addresses of main suppliers confirm whether or not you import alcoholic goods confirm whether or not you are an Authorised Economic Operator (AEO) Corporate groups will also need to provide information about companies within the group which wholesale alcohol, this will include: their individual CT UTRs details of the group representative details of the group controlling body company registration number if incorporated in the UK Sole Proprietors will need to provide their: 8

13 title first name middle names surname National Insurance Number date of birth Self Assessment UTR and VAT Registration Number if they have one Partnerships will also need to provide the same details as for Sole Proprietors, for all of the partners. Limited Liability Partnerships will also need to provide: full names and details of partners as above company name trading name company registration number date of incorporation number Corporate bodies will need to provide: the number of directors title first name middle name surname date of birth National Insurance Number These are not exhaustive lists, and you may need to submit further information as part of the registration process following your initial application. What happens if existing wholesalers don t apply to register between 1 October and 31 December 2015? HMRC wants all existing alcohol wholesalers to apply for the scheme before 31 December If you don t apply during the period 1 October to 31 December 2015 you may face a penalty if you trade beyond 31 December Will I get an HMRC visit? We will visit wholesalers who apply to register for the scheme if we need further information or clarification of the details provided in the application. If we decide to visit you we will advise you as soon as possible to arrange a convenient date and time. How do I prepare for an HMRC visit? You will need to be prepared for us to look at your premises and everything you do there. We will ask you for details about (but not limited to) your suppliers, customers, business plans, 9

14 accounting and stock control systems, premises and financial viability. For further information on what to expect, search for Preparing for an Excise Visit Factsheet CC/FS16 at How long will I have to wait before I hear whether I ve been approved for registration? From 1 October 2015 to 1 April 2017, we will review all applications to ensure that only fit and proper wholesalers are registered. If you are a currently trading business and applied between October and December, you can continue to trade as normal until you have received HMRC s decision. Due to the volume of applications in this period, it is going to take HMRC some months to get through them all, so please be patient. You will be able to log into your Government Gateway account to see the progress of your application. What if I m not approved? If you fail the criteria you will not be permitted to trade in alcohol wholesale. You will have the right to review and appeal our decision. Refusal of an AWRS registration may also affect other approvals you hold with HMRC and we would contact you in due course to discuss. How do I make sure I only buy alcohol from HMRC registered wholesalers? From 1 April 2017, to help you ensure you only buy from a registered source, we ll provide an online database of approved registered traders for you to use. Using this will form part of the due diligence processes. What happens if I buy alcohol from wholesalers who are not registered with HMRC? HMRC wants to know about wholesalers trading without registration. If you discover you have inadvertently purchased from an unregistered wholesaler, you can report this to the Customs Hotline or use the Customs Hotline online form, search for Customs, Excise and VAT fraud reporting at In cases where traders are found to be knowingly buying from unregistered wholesalers, new criminal and civil sanctions will be introduced and applied from 1 April In addition, any alcohol found in the premises of unregistered businesses may be seized whether or not the duty has been paid. Businesses will have a similar right to review and appeal as they do for other HMRC regimes for any civil penalties raised. What makes a wholesaler a UK wholesaler? The requirement to register only applies to wholesalers with a UK establishment. A UK establishment exists if: the place where essential management decisions are made and the business s central administration is carried out is in the UK, and/or the business has a permanent physical presence with the human and technical resources to make or receive taxable supplies in the UK 10

15 We would normally consider a company which is incorporated in the UK to have an establishment here as long as it is able to receive business supplies at its registered office. What do you mean by sales at or after the point at which excise duty is due? Alcohol is a dutiable product, this means that somewhere in the supply chain for alcohol which is sold in the UK (unless there is a specific exemption or relief that has been granted for the goods in question) duty should be paid to HMRC. Only traders already approved by HMRC can trade in duty unpaid alcohol, so if you are not one these traders, you should only deal in alcohol which has had the duty paid to HMRC. HMRC already regulates people who trade in duty unpaid goods, so AWRS covers anyone who should pay duty over, or who deals with the goods after this point. This is usually at the point it is released to the UK market. What if all my sales are within a corporate group? If the only sales of alcohol you make are between members of the same corporate group, you do not need to register for AWRS. What if all my sales of alcohol are abroad? If all your trade in alcohol takes place abroad you do not need to register - sales where there has been, or is no liability to pay UK excise duty are outside the scope of AWRS. What if I have a retail licence but might also sell alcohol to other businesses? If you are a retailer selling alcohol you will need to work through the flowcharts within this pack to check whether you are required to register under AWRS. What do I need to do when I am approved and receive my AWRS number? On approval, you will be allocated a unique reference number (URN) and you must provide this to your customers. From 1 April 2017, you must include the URN on all sales invoices involving alcohol, and provide it on request to anyone purchasing alcohol from you. What do you mean by trade buyer of alcohol? Trade buyers are all traders who buy alcohol from a wholesaler for onward sale in their own trade, eg. pubs, clubs, restaurants, hotels anywhere that sells alcohol to the general public. From 1 April 2017, if buying from a UK wholesaler, trade buyers must only source alcohol from AWRS registered traders, and HMRC will provide an online look up to assist in this checking process. What about alcohol that has been exempted or has been granted a relief from payment of duty? You do not need to register if you only trade in alcohol that has been exempted or relieved from excise duty (e.g. denatured alcohol or alcohol sent to denaturers or authorised duty free 11

duty should be paid to HMRC.")

16 spirits users; supplies to diplomats etc.). Alcohol that has been exempted or relieved from UK excise duty is outside the scope of the scheme. Is alcohol received in duty suspense included in the scheme? No, duty suspended movements of alcohol and sales within the duty suspension regime are not included. I am not VAT registered. Do I need to register for AWRS? AWRS applies to alcohol wholesalers whether or not they are VAT registered. Check the flowcharts within this pack and the guidance above. What if I m not sure whether I need to register or not? Check the flowcharts within this pack and the guidance above. 12

Alcohol Wholesaler Registration Scheme (AWRS) Briefing Pack. If your business buys or sells alcohol this is for you.

Briefing Pack. If your business buys or sells alcohol this is for you.") Alcohol Wholesaler Registration Scheme (AWRS) Briefing Pack If your business buys or sells alcohol this is for you. Contents Introduction of the Alcohol Wholesaler Registration Scheme (AWRS) 5 Decision

Alcohol Wholesaler Registration Scheme (AWRS) Briefing Pack If your business buys or sells alcohol this is for you. Contents Introduction of the Alcohol Wholesaler Registration Scheme (AWRS) 5 Decision

VAT guide should I register for VAT?

VAT guide should I register for VAT? associates ltd Should I register for VAT? This guide will give you an understanding as to whether you should register, what the various schemes are for small businesses

VAT guide should I register for VAT? associates ltd Should I register for VAT? This guide will give you an understanding as to whether you should register, what the various schemes are for small businesses

ALCOHOL DUTY FRAUD TACKLING ILICIT COUNTERFEIT GOODS DAMAGING TRADE PERVASIVE AND PREVENTING EXCISE DUTY EVASION ILLEGITIMATE WHOLESALERS

PREVENTING PERVSIVE ND DMGING TRDE EXCISE EVSIN IICIT BEER, WINE ND SPIRITS IEGITIMTE WHESERS CUNTERFEIT GDS acs.org.uk H C Y T U D G N I D K C U T FR 2 H C Y T DU D U FR INTRDUCTIN lcohol duty fraud is

PREVENTING PERVSIVE ND DMGING TRDE EXCISE EVSIN IICIT BEER, WINE ND SPIRITS IEGITIMTE WHESERS CUNTERFEIT GDS acs.org.uk H C Y T U D G N I D K C U T FR 2 H C Y T DU D U FR INTRDUCTIN lcohol duty fraud is

A Guide to VAT. 02392 883337 [email protected] www.boox.co.uk

A Guide to VAT In this guide, we walk you through the different VAT schemes and explain how to comply with the relevant laws. 02392 883337 [email protected] www.boox.co.uk When you go self-employed, one

A Guide to VAT In this guide, we walk you through the different VAT schemes and explain how to comply with the relevant laws. 02392 883337 [email protected] www.boox.co.uk When you go self-employed, one

Use of Labour Providers. Advice on due diligence

Use of Labour Providers Advice on due diligence Who should read this? This guidance applies if you use labour supplied by a third party, supply or make arrangements to supply labour. HMRC has identified

Use of Labour Providers Advice on due diligence Who should read this? This guidance applies if you use labour supplied by a third party, supply or make arrangements to supply labour. HMRC has identified

1.3 What is the cash accounting scheme?

Foreword This notice cancels and replaces Notice 731 (August 2008). Details of any changes to the previous version can be found in paragraph 1.2 of this notice. The legal basis for the cash accounting

Foreword This notice cancels and replaces Notice 731 (August 2008). Details of any changes to the previous version can be found in paragraph 1.2 of this notice. The legal basis for the cash accounting

Disciplinary Procedure

Disciplinary Procedure 1. Purpose and Scope This procedure is designed to help and encourage employees to achieve and maintain acceptable standards of conduct and performance whilst ensuring the fair and

Disciplinary Procedure 1. Purpose and Scope This procedure is designed to help and encourage employees to achieve and maintain acceptable standards of conduct and performance whilst ensuring the fair and

Trading Application Form Page 1 of 6

Trading Application Form Page 1 of 6 Company Details Registered Company Name: Trading Name if different from above: Contact Name: Invoice Address: Registered Address: Company Registration Number: Date

Trading Application Form Page 1 of 6 Company Details Registered Company Name: Trading Name if different from above: Contact Name: Invoice Address: Registered Address: Company Registration Number: Date

A GUIDE TO STARTING UP A LIMITED COMPANY

A GUIDE TO STARTING UP A LIMITED COMPANY RIFTACCOUNTING.COM A GUIDE TO STARTING UP A LIMITED COMPANY This guide assumes that you have made a decision to become a Limited Company as opposed to operating

A GUIDE TO STARTING UP A LIMITED COMPANY RIFTACCOUNTING.COM A GUIDE TO STARTING UP A LIMITED COMPANY This guide assumes that you have made a decision to become a Limited Company as opposed to operating

A GUIDE TO STARTING UP AS A SOLE TRADER/SELF EMPLOYED

A GUIDE TO STARTING UP AS A SOLE TRADER/SELF EMPLOYED RIFTACCOUNTING.COM A GUIDE TO STARTING UP AS A SOLE TRADER/ SELF EMPLOYED This guide assumes that you have made a decision to become a Sole Trader

A GUIDE TO STARTING UP AS A SOLE TRADER/SELF EMPLOYED RIFTACCOUNTING.COM A GUIDE TO STARTING UP AS A SOLE TRADER/ SELF EMPLOYED This guide assumes that you have made a decision to become a Sole Trader

2016/17 TO... GUIDE TO... GUIDE TO WWW.NEWBYCASTLEMAN.CO.UK FOR ELECTRONIC USE ONLY

2015/16 2016/17 GUIDE TO 2016/17 TO... GUIDE TO... Value VALUE Added ADDED TAX Tax WWW.NEWBYCASTLEMAN.CO.UK FOR ELECTRONIC USE ONLY YOUR GUIDE TO Value Added Tax Value Added Tax (VAT) is a tax chargeable

2015/16 2016/17 GUIDE TO 2016/17 TO... GUIDE TO... Value VALUE Added ADDED TAX Tax WWW.NEWBYCASTLEMAN.CO.UK FOR ELECTRONIC USE ONLY YOUR GUIDE TO Value Added Tax Value Added Tax (VAT) is a tax chargeable

VAT CHANGE OF THE STANDARD RATE TO 20 PER CENT: A DETAILED GUIDE FOR VAT-REGISTERED BUSINESSES

VAT CHANGE OF THE STANDARD RATE TO 20 PER CENT: A DETAILED GUIDE FOR VAT-REGISTERED BUSINESSES Version 2: December 2010 Contents Page 1 INTRODUCTION... 4 2 SALES... 7 2.1 WHEN DO I HAVE TO START CHARGING

VAT CHANGE OF THE STANDARD RATE TO 20 PER CENT: A DETAILED GUIDE FOR VAT-REGISTERED BUSINESSES Version 2: December 2010 Contents Page 1 INTRODUCTION... 4 2 SALES... 7 2.1 WHEN DO I HAVE TO START CHARGING

This guide explains the basics of how VAT works. It tells you where you can find more information and advice. On this page:

Introduction to VAT Value Added Tax (VAT) is a tax that's charged on most goods and services that VAT-registered businesses provide in the UK. It's also charged on goods and some services that are imported

Introduction to VAT Value Added Tax (VAT) is a tax that's charged on most goods and services that VAT-registered businesses provide in the UK. It's also charged on goods and some services that are imported

The Consumer Protection from Unfair Trading Regulations 2008

Trading Standards Service Factsheet The Consumer Protection from Unfair Trading Regulations 2008 Background The Consumer Protection from Unfair Trading Regulations 2008 (CPR s), came into force on 26 th

Trading Standards Service Factsheet The Consumer Protection from Unfair Trading Regulations 2008 Background The Consumer Protection from Unfair Trading Regulations 2008 (CPR s), came into force on 26 th

TAX DIRECTIONS. What you need to know about GST

TAX DIRECTIONS Information to help your business Information to help your business What you need to know about GST IR 214 April 2014 IR 214 June 2007 This brochure gives you an overview of GST (goods and

TAX DIRECTIONS Information to help your business Information to help your business What you need to know about GST IR 214 April 2014 IR 214 June 2007 This brochure gives you an overview of GST (goods and

PLEASE READ BEFORE COMPLETING YOUR APPLICATION

Application to become a Licensed London Private Hire Operator Dear Applicant PLEASE READ BEFORE COMPLETIG OUR APPLICATIO Thank you for applying to become a Licensed London Private Hire Operator. Enclosed

Application to become a Licensed London Private Hire Operator Dear Applicant PLEASE READ BEFORE COMPLETIG OUR APPLICATIO Thank you for applying to become a Licensed London Private Hire Operator. Enclosed

Guidance on the fit and proper person criteria for pension scheme administrators

Guidance on the fit and proper person criteria for pension scheme administrators Legislation introduced from 1 September 2014 enables HM Revenue & Customs (HMRC) to refuse to register a new pension scheme

Guidance on the fit and proper person criteria for pension scheme administrators Legislation introduced from 1 September 2014 enables HM Revenue & Customs (HMRC) to refuse to register a new pension scheme

Sage 50 Accounts Construction Industry Scheme (CIS)

") Sage 50 Accounts Construction Industry Scheme (CIS) Copyright statement Sage (UK) Limited, 2012. All rights reserved We have written this guide to help you to use the software it relates to. We hope it

Sage 50 Accounts Construction Industry Scheme (CIS) Copyright statement Sage (UK) Limited, 2012. All rights reserved We have written this guide to help you to use the software it relates to. We hope it

CASH ISA SAVINGS CONDITIONS. For use from 2nd September 2016.

CASH ISA SAVINGS CONDITIONS. For use from 2nd September 2016. WELCOME TO HALIFAX This booklet explains how your Halifax savings account works, and includes its main conditions. This booklet contains: information

CASH ISA SAVINGS CONDITIONS. For use from 2nd September 2016. WELCOME TO HALIFAX This booklet explains how your Halifax savings account works, and includes its main conditions. This booklet contains: information

Most of the hard work of setting up and running a Limited Company is at the beginning of the process which Exceed will be able to assist you with.

Limited Companies Introduction Forming a Limited Company may appear to be very daunting to some people, and it is true that a lot of legislation is in place relating to company formation and operation.

Limited Companies Introduction Forming a Limited Company may appear to be very daunting to some people, and it is true that a lot of legislation is in place relating to company formation and operation.

Before beginning your journey there are a number of things you will need to consider, with the most important being finance.

Whether you have just started your own small businesses, or you are a budding entrepreneur with big aspirations, there has never been a better time to work for yourself. With the economy going from strength

Whether you have just started your own small businesses, or you are a budding entrepreneur with big aspirations, there has never been a better time to work for yourself. With the economy going from strength

HALIFAX CASH ISA. Conditions and information

HALIFAX CASH ISA. Conditions and information Welcome to Halifax 3 Section 1 How these conditions work 5 Section 2 Special Conditions 7 ISA Saver Variable 12 ISA Saver Online 13 ISA Saver Fixed 14 Junior

HALIFAX CASH ISA. Conditions and information Welcome to Halifax 3 Section 1 How these conditions work 5 Section 2 Special Conditions 7 ISA Saver Variable 12 ISA Saver Online 13 ISA Saver Fixed 14 Junior

APPLICATION FOR. License Fee Only. Non- NZTA

C4:08-15 NEW ZEALAND THOROUGHBRED RACING INC PO Box 38386, WMC Telephone: (04) 576 6240 Facsimile: (04) 568 8866 Web: www.nzracing.co.nz Email: [email protected] APPLICATION FOR Non- NZTA License

C4:08-15 NEW ZEALAND THOROUGHBRED RACING INC PO Box 38386, WMC Telephone: (04) 576 6240 Facsimile: (04) 568 8866 Web: www.nzracing.co.nz Email: [email protected] APPLICATION FOR Non- NZTA License

If you are VAT registered you must charge VAT on the products or services you sell.

An Introduction to VAT VAT (value added tax) is a tax levied on sales of goods and services. If you are VAT registered you must charge VAT on the products or services you sell. Upon submission of each

An Introduction to VAT VAT (value added tax) is a tax levied on sales of goods and services. If you are VAT registered you must charge VAT on the products or services you sell. Upon submission of each

11 VAT on Intra-Community Trade

11 VAT on Intra-Community Trade 11.1 Over the period 2007 to 2011, Value Added Tax (VAT) has accounted for just over 30% of total tax receipts in Ireland. Approximately 90% of Irish VAT receipts relate

11 VAT on Intra-Community Trade 11.1 Over the period 2007 to 2011, Value Added Tax (VAT) has accounted for just over 30% of total tax receipts in Ireland. Approximately 90% of Irish VAT receipts relate

If you would like to speak to someone in Welsh, please ring 0845 010 0300, between 8.00 am and 6.00 pm, Monday to Friday.

1 HM CUSTOMS AND EXCISE http://www.hmce.gov.uk Notice 701/21 Gold March 2002 This notice cancels and replaces Notice 701/21 (February 2000). Details of any changes to the previous version can be found

1 HM CUSTOMS AND EXCISE http://www.hmce.gov.uk Notice 701/21 Gold March 2002 This notice cancels and replaces Notice 701/21 (February 2000). Details of any changes to the previous version can be found

How to prepare for an audit: A guide for small businesses

Narrative video script Department of Revenue Department of Labor & Industries Employment Security Department Introduction If you re a small-business owner, the prospect of an audit can be intimidating.

Narrative video script Department of Revenue Department of Labor & Industries Employment Security Department Introduction If you re a small-business owner, the prospect of an audit can be intimidating.

Trading during difficult times for SMEs. November, 2009

November, 2009 Introduction In an effort to support small and medium sized enterprises (SMEs), which constitute the main fabric of the upstream oil and gas supply chain, the Supply Chain Forum of Oil

November, 2009 Introduction In an effort to support small and medium sized enterprises (SMEs), which constitute the main fabric of the upstream oil and gas supply chain, the Supply Chain Forum of Oil

ADVANTAGES AND DISADVANTAGES OF THE FORMS OF OWNERSHIP

ADVANTAGES AND DISADVANTAGES OF THE FORMS OF OWNERSHIP FORM OF OWNERSHIP Sole 1 Owner Partnership Minimum of 2 Partners, Maximum of 20 ADVANTAGES 1. Simple to form i.e. No registration. 2. Can have an

ADVANTAGES AND DISADVANTAGES OF THE FORMS OF OWNERSHIP FORM OF OWNERSHIP Sole 1 Owner Partnership Minimum of 2 Partners, Maximum of 20 ADVANTAGES 1. Simple to form i.e. No registration. 2. Can have an

An employer s guide to the administration of the civil penalty scheme

An employer s guide to the administration of the civil penalty scheme 28 July 2014 Produced by the Home Office Crown copyright 2014 Contents 1. Introduction... 3 Changes to the scheme in May 2014... 3

An employer s guide to the administration of the civil penalty scheme 28 July 2014 Produced by the Home Office Crown copyright 2014 Contents 1. Introduction... 3 Changes to the scheme in May 2014... 3

Value-Added Tax (VAT)

") June 2015 MY SMALL BUSINESS Value-Added Tax (VAT) What you need to know www.sars.gov.za 0800 00 7277 Value-Added Tax Value-Added Tax (VAT) is an indirect tax based on consumption of goods and services

June 2015 MY SMALL BUSINESS Value-Added Tax (VAT) What you need to know www.sars.gov.za 0800 00 7277 Value-Added Tax Value-Added Tax (VAT) is an indirect tax based on consumption of goods and services

Current Account, Current Account Plus, Student Current Account, Privilege Current Account, Privilege Premier Current Account. Terms and conditions

Current Account, Current Account Plus, Student Current Account, Privilege Current Account, Privilege Premier Current Account. Terms and conditions With effect from 5 July 2015 Terms and conditions of the

Current Account, Current Account Plus, Student Current Account, Privilege Current Account, Privilege Premier Current Account. Terms and conditions With effect from 5 July 2015 Terms and conditions of the

Starting In Business. Are you sure?

Starting In Business This guide is for whether you have already decided to start a new business, or you are simply considering your first move into self-employment. What do you need to think about before

Starting In Business This guide is for whether you have already decided to start a new business, or you are simply considering your first move into self-employment. What do you need to think about before

Code of Practice 9. HM Revenue & Customs investigations where we suspect tax fraud COP9 HMRC 06/14

Code of Practice 9 HM Revenue & Customs investigations where we suspect tax fraud COP9 HMRC 06/14 HM Revenue & Customs (HMRC) investigation of fraud statement The Commissioners of HMRC reserve complete

Code of Practice 9 HM Revenue & Customs investigations where we suspect tax fraud COP9 HMRC 06/14 HM Revenue & Customs (HMRC) investigation of fraud statement The Commissioners of HMRC reserve complete

Listing Agents and Corporate Advisers

Listing Agents and Corporate Advisers GUIDE TO BECOMING A LISTING AGENT OR CORPORATE ADVISER The Cayman Islands Stock Exchange P.O. Box 2408GT Grand Cayman Cayman Islands Telephone: +1 345 945 6060 Email:

Listing Agents and Corporate Advisers GUIDE TO BECOMING A LISTING AGENT OR CORPORATE ADVISER The Cayman Islands Stock Exchange P.O. Box 2408GT Grand Cayman Cayman Islands Telephone: +1 345 945 6060 Email:

Do you need a credit licence? An introduction to consumer credit licensing

Do you need a credit licence? An introduction to consumer credit licensing July 2008 Do you need a credit licence? To comply with the requirements of the Consumer Credit Act 1974, you must have a credit

Do you need a credit licence? An introduction to consumer credit licensing July 2008 Do you need a credit licence? To comply with the requirements of the Consumer Credit Act 1974, you must have a credit

smile current account Terms and Conditions

smile current account Terms and Conditions Terms and Conditions of the smile current account, overdraft and debit card (incorporating smilemore and smile student) With effect from 5 July 2015 Terms and

smile current account Terms and Conditions Terms and Conditions of the smile current account, overdraft and debit card (incorporating smilemore and smile student) With effect from 5 July 2015 Terms and

PERSONAL LICENCE TRAINING LIMITED. APLH Mock Exam AWARD FOR PERSONAL LICENCE HOLDERS LEVEL 2. Mock APLH Examination Paper 1

PERSONAL LICENCE TRAINING LIMITED APLH Mock Exam AWARD FOR PERSONAL LICENCE HOLDERS LEVEL 2 Mock APLH Examination Paper 1 This example mock examination paper will give a guide to type of questions contained

PERSONAL LICENCE TRAINING LIMITED APLH Mock Exam AWARD FOR PERSONAL LICENCE HOLDERS LEVEL 2 Mock APLH Examination Paper 1 This example mock examination paper will give a guide to type of questions contained

AWARD FOR PERSONAL LICENCE HOLDERS (LEVEL 2) Mock APLH Examination Paper

Mock APLH Examination Paper") AWARD FOR PERSONAL LICENCE HOLDERS (LEVEL 2) Mock APLH Examination Paper This example mock examination paper will give a guide to type of questions contained in the AWARD FOR PERSONAL LICENCE HOLDERS examination.

AWARD FOR PERSONAL LICENCE HOLDERS (LEVEL 2) Mock APLH Examination Paper This example mock examination paper will give a guide to type of questions contained in the AWARD FOR PERSONAL LICENCE HOLDERS examination.

How To Factoring

THE BASICS OF FACTORING A Guide to Understanding Accounts Receivable Financing The Basics of Factoring Table of Contents What is Factoring?.. 1 Benefits of Factoring 4 What Types of Businesses Utilize

THE BASICS OF FACTORING A Guide to Understanding Accounts Receivable Financing The Basics of Factoring Table of Contents What is Factoring?.. 1 Benefits of Factoring 4 What Types of Businesses Utilize

Sales and Use Taxes: Texas

Jay M. Chadha, Fulbright & Jaworski LLP A Q&A guide to sales and use tax law in Texas. This Q&A addresses key areas of sales and use tax law such as tax scope, multi-state transactions and collecting taxes

Jay M. Chadha, Fulbright & Jaworski LLP A Q&A guide to sales and use tax law in Texas. This Q&A addresses key areas of sales and use tax law such as tax scope, multi-state transactions and collecting taxes

Taxing remote gambling on a place of consumption basis: summary of consultation responses

Taxing remote gambling on a place of consumption basis: summary of consultation responses August 2013 Taxing remote gambling on a place of consumption basis: summary of consultation responses August 2013

Taxing remote gambling on a place of consumption basis: summary of consultation responses August 2013 Taxing remote gambling on a place of consumption basis: summary of consultation responses August 2013

Credit cards explained

Credit cards explained What is a credit card? As its name suggests, a credit card lets you buy things on credit meaning that you don t need to have the money upfront to pay for your purchases. If large,

Credit cards explained What is a credit card? As its name suggests, a credit card lets you buy things on credit meaning that you don t need to have the money upfront to pay for your purchases. If large,

MFFA Belastingadvies Tax Advice

MFFA Belastingadvies Tax Advice Specialized in Expats and International Companies Amsterdam Zwolle Assen The Netherlands VAT in Europe an introduction General comments European Union: 27 member states

MFFA Belastingadvies Tax Advice Specialized in Expats and International Companies Amsterdam Zwolle Assen The Netherlands VAT in Europe an introduction General comments European Union: 27 member states

Your guide to UK pension transfers

Your guide to UK pension transfers If you ve worked in the UK at some stage of your career you ve possibly built up a fund in a UK pension. Now that you re back living in Ireland you may wish to bring

Your guide to UK pension transfers If you ve worked in the UK at some stage of your career you ve possibly built up a fund in a UK pension. Now that you re back living in Ireland you may wish to bring

Code of Practice 9 (July 2011)

") Code of Practice 9 (July 2011) Introduction HM Revenue & Customs (HMRC) will investigate any situation where they suspect serious tax fraud. The investigation will be undertaken with or without your voluntary

Code of Practice 9 (July 2011) Introduction HM Revenue & Customs (HMRC) will investigate any situation where they suspect serious tax fraud. The investigation will be undertaken with or without your voluntary

1) Company Details. Trading/Contact Address. Registered Address (Limited Companies only) Firm Principal Contact Details

Company Details. Trading/Contact Address. Registered Address (Limited Companies only) Firm Principal Contact Details") AR FIRM APPLICATION FORM Please note for AR applications; only one principal at your firm is required to complete this. All principals and advisers, (including yourself) must also complete an individual

AR FIRM APPLICATION FORM Please note for AR applications; only one principal at your firm is required to complete this. All principals and advisers, (including yourself) must also complete an individual

Measuring tax gaps 2015 edition Tax gap estimates for 2013-14

edition Tax gap estimates for 2013-14 An Official Statistics release 22 October 2015 Contents 3 Introduction 4 At a glance 6 1. Summary 25 2. VAT 33 3. Alcohol 38 4. Tobacco 43 5. Oils 47 6. Income tax,

edition Tax gap estimates for 2013-14 An Official Statistics release 22 October 2015 Contents 3 Introduction 4 At a glance 6 1. Summary 25 2. VAT 33 3. Alcohol 38 4. Tobacco 43 5. Oils 47 6. Income tax,

Managing Cashflow Guide

Managing Cashflow Guide 1. Knowing your customer 2. Payment Terms 3. Invoicing 4. Chasing payment 5. Treating suppliers fairly 6. Credit Insurance 7. Financing options 8. When all else fails 9. When your

Managing Cashflow Guide 1. Knowing your customer 2. Payment Terms 3. Invoicing 4. Chasing payment 5. Treating suppliers fairly 6. Credit Insurance 7. Financing options 8. When all else fails 9. When your

MSC Group Chain of Custody (CoC) Guidance for Non-Reduced Risk Groups

Guidance for Non-Reduced Risk Groups") MSC Group Chain of Custody (CoC) Guidance for Non-Reduced Risk Groups 1. About this document This document is a non-normative guidance document intended to help companies understand CoC requirements. The

MSC Group Chain of Custody (CoC) Guidance for Non-Reduced Risk Groups 1. About this document This document is a non-normative guidance document intended to help companies understand CoC requirements. The

Notes to help you apply for VAT registration checklist where to send your application Glossary About Corporate body the business

Notes to help you apply for VAT registration These notes will help you answer questions on form VAT1 Application for registration. The notes are numbered to correspond with the questions on the form. If

Notes to help you apply for VAT registration These notes will help you answer questions on form VAT1 Application for registration. The notes are numbered to correspond with the questions on the form. If

Glasgow Kelvin College. Disciplinary Policy and Procedure

Appendix 1 Glasgow Kelvin College Disciplinary Policy and Procedure Document Control Information Status: Responsibility for Document and its implementation Responsibility for document review: Current version

Appendix 1 Glasgow Kelvin College Disciplinary Policy and Procedure Document Control Information Status: Responsibility for Document and its implementation Responsibility for document review: Current version

VAT guide for small businesses. VAT guide

VAT guide Contents VAT guide for small businesses What is VAT? Contents What is VAT? VAT, or Value Added Tax, is a tax that is charged on most goods and services that VAT registered businesses provide

VAT guide Contents VAT guide for small businesses What is VAT? Contents What is VAT? VAT, or Value Added Tax, is a tax that is charged on most goods and services that VAT registered businesses provide

There is help on form VAT1 itself but these notes provide extra help with some of the questions.

additional information to help you There is help on form VAT1 itself but these notes provide extra help with some of the questions. The notes have the same numbers as the questions they refer to. On the

additional information to help you There is help on form VAT1 itself but these notes provide extra help with some of the questions. The notes have the same numbers as the questions they refer to. On the

The Amendment of the Loan Agreement (for Business)/ Overdraft Facility Agreement (for Consumption)/ Money Mortgage Agreement*

/ Overdraft Facility Agreement (for Consumption)/ Money Mortgage Agreement*") The Amendment of the Loan Agreement (for Business)/ Overdraft Facility Agreement (for Consumption)/ Money Mortgage Agreement* No. Clause Reference Amendment Sanctions 1. Important notice Standard Chartered

The Amendment of the Loan Agreement (for Business)/ Overdraft Facility Agreement (for Consumption)/ Money Mortgage Agreement* No. Clause Reference Amendment Sanctions 1. Important notice Standard Chartered

A guide to self-employment

A guide to self-employment Why become self-employed? There is encouragement from the government for people to become self-employed and at first it seems attractive, especially if you have recently become

A guide to self-employment Why become self-employed? There is encouragement from the government for people to become self-employed and at first it seems attractive, especially if you have recently become

How to calculate your taxable profits

Helpsheet 222 Tax year 6 April 2013 to 5 April 2014 How to calculate your taxable profits A Contacts Please phone: the number printed on page TR 1 of your tax return the SA Helpline on 0300 200 3310 the

Helpsheet 222 Tax year 6 April 2013 to 5 April 2014 How to calculate your taxable profits A Contacts Please phone: the number printed on page TR 1 of your tax return the SA Helpline on 0300 200 3310 the

Welcome to your British Gas Business guide. Everything you need to know. Contract terms and conditions enclosed

Welcome to your British Gas Business guide Everything you need to know Contract terms and conditions enclosed Contents Welcome to your British Gas Business terms and conditions 1 Dedicated to you 1 Meanings

Welcome to your British Gas Business guide Everything you need to know Contract terms and conditions enclosed Contents Welcome to your British Gas Business terms and conditions 1 Dedicated to you 1 Meanings

We make life less taxing for you. HANS ACCOUNTING LTD. Company Brochure. www.hansaccounting.com

We make life less taxing for you. HANS ACCOUNTING LTD. Company Brochure www.hansaccounting.com Hans Accounting Ltd. Company Introduction Based in the Stanmore Middlesex, we serve a diverse client base

We make life less taxing for you. HANS ACCOUNTING LTD. Company Brochure www.hansaccounting.com Hans Accounting Ltd. Company Introduction Based in the Stanmore Middlesex, we serve a diverse client base

CGT is a tax on the profit you make from selling certain assets such as property, shares or other investments e.g. antiques and fine art.

Capital Gains Tax A brief history CGT was first introduced in 1965. Until then capital gains were not subject to tax. This had led many people to avoid Income Tax by converting (taxable) income into (tax

Capital Gains Tax A brief history CGT was first introduced in 1965. Until then capital gains were not subject to tax. This had led many people to avoid Income Tax by converting (taxable) income into (tax

Tax investigations helping you to help your clients. 18 October 2013

Tax investigations helping you to help your clients 18 October 2013 Agenda Introduction Eric Hindson, Partner, PKF Littlejohn International overview Ross Welland, Tax partner, PKF Littlejohn Investigations

Tax investigations helping you to help your clients 18 October 2013 Agenda Introduction Eric Hindson, Partner, PKF Littlejohn International overview Ross Welland, Tax partner, PKF Littlejohn Investigations

Santander Corporate & Commercial Intermediary registration and information renewal form

INTERMEDIARIES & BROKERS ONLY: NOT FOR PUBLIC DISTRIBUTION Santander Corporate & Commercial Intermediary registration and information renewal form Please fill in the form using BLOCK CAPITALS and black

INTERMEDIARIES & BROKERS ONLY: NOT FOR PUBLIC DISTRIBUTION Santander Corporate & Commercial Intermediary registration and information renewal form Please fill in the form using BLOCK CAPITALS and black

TABLE OF CONTENTS. 1.1 What is Value Added Tax?...2 2.1 How does VAT Work?...2 1.3 The Collection of VAT on a fully Taxed Supply...

TABLE OF CONTENTS PAGE INTRODUCTION........1 CHAPTER 1 VALUE ADDED TAX BASICS 1.1 What is Value Added Tax?...2 2.1 How does VAT Work?...2 1.3 The Collection of VAT on a fully Taxed Supply...5 CHAPTER 2

TABLE OF CONTENTS PAGE INTRODUCTION........1 CHAPTER 1 VALUE ADDED TAX BASICS 1.1 What is Value Added Tax?...2 2.1 How does VAT Work?...2 1.3 The Collection of VAT on a fully Taxed Supply...5 CHAPTER 2

Legal Update: Tax Administration Laws Amendment Act 39 of 2013

No.12 of 2014 June 2014 Legal Update: Tax Administration Laws Amendment Act 39 of 2013 The Tax Administration Laws Amendment Act ( the Act ) was promulgated on 16 January 2014. The Act amends the Transfer

No.12 of 2014 June 2014 Legal Update: Tax Administration Laws Amendment Act 39 of 2013 The Tax Administration Laws Amendment Act ( the Act ) was promulgated on 16 January 2014. The Act amends the Transfer

Owner managed businesses: Bringing your corporate and personal goals to life

Owner managed businesses: Bringing your corporate and personal goals to life Owner managed businesses PRECISE. PROVEN. PERFORMANCE. Bringing your corporate and personal goals to life Dynamic. Ambitious.

Owner managed businesses: Bringing your corporate and personal goals to life Owner managed businesses PRECISE. PROVEN. PERFORMANCE. Bringing your corporate and personal goals to life Dynamic. Ambitious.

Buying and selling an unincorporated business

Introduction This section covers the main tax issues that arise when buying or selling a business owned by a sole trader, a partnership or a company. The tax consequences differ, depending on whether the

Introduction This section covers the main tax issues that arise when buying or selling a business owned by a sole trader, a partnership or a company. The tax consequences differ, depending on whether the

Scammed out of his retirement. Don t be next.

Scammed out of his retirement. Don t be next. Visit www.pension-scams.com Geoff s story Tricked into being part of the scam Bold text highlights typical hallmarks of a scam. These are based on real life

Scammed out of his retirement. Don t be next. Visit www.pension-scams.com Geoff s story Tricked into being part of the scam Bold text highlights typical hallmarks of a scam. These are based on real life

APPLICANT INFORMATION. Billing Address(if different) Prior Address if less than 3 years: If home owner House Value Mortgage Outstanding

Prior Address if less than 3 years: If home owner House Value Mortgage Outstanding") Go Commercial Finance Limited, The Stables, Suite 5, Castle Land Street Barry CF63 4LL Office: 01446 506 508 Mobile: 07793 362 423 Email: [email protected] Web: www.gocommercialfinance.com

Go Commercial Finance Limited, The Stables, Suite 5, Castle Land Street Barry CF63 4LL Office: 01446 506 508 Mobile: 07793 362 423 Email: [email protected] Web: www.gocommercialfinance.com

Insurance, indemnity and medico-legal support

Insurance, indemnity and medico-legal support Statutory requirement for doctors to have insurance or indemnity We know doctors work hard to deliver good quality healthcare. But sometimes, things go wrong.

Insurance, indemnity and medico-legal support Statutory requirement for doctors to have insurance or indemnity We know doctors work hard to deliver good quality healthcare. But sometimes, things go wrong.

CONSULTATION PAPER NO 2. 2004

CONSULTATION PAPER NO 2. 2004 REGULATION OF GENERAL INSURANCE MEDIATION BUSINESS This consultation paper explains the need for the Island to regulate general insurance mediation business and examines the

CONSULTATION PAPER NO 2. 2004 REGULATION OF GENERAL INSURANCE MEDIATION BUSINESS This consultation paper explains the need for the Island to regulate general insurance mediation business and examines the

Set up and register a limited company (private or public)

") Page 1 of 8 Set up and register a limited company (private or public) Before your business can begin operating as a limited company, it has to be registered with the Registrar of Companies - Companies

Page 1 of 8 Set up and register a limited company (private or public) Before your business can begin operating as a limited company, it has to be registered with the Registrar of Companies - Companies

Gambia Revenue Authority (GRA) VAT GUIDE 2014

VAT GUIDE 2014") Gambia Revenue Authority (GRA) VAT GUIDE 2014 Page 1 of 67 TABLE OF CONTENTS CHAPTERS CONTENTS PAGE CHAPTER 1 INTRODUCTION TO VAT 1.1.0 Introduction 6 1.2.0 What is VAT 6 1.3.0 Why VAT 6 1.4.0 Advantages

Gambia Revenue Authority (GRA) VAT GUIDE 2014 Page 1 of 67 TABLE OF CONTENTS CHAPTERS CONTENTS PAGE CHAPTER 1 INTRODUCTION TO VAT 1.1.0 Introduction 6 1.2.0 What is VAT 6 1.3.0 Why VAT 6 1.4.0 Advantages

Potential saving ( 286,000 221,040) 64,960

64,960") Answers Professional Level Options Module, Paper P6 (UK) Advanced Taxation (United Kingdom) June 2012 Answers 1 Una (a) To The files From Tax senior Date 15 June 2012 Subject Una Gifts to son and granddaughter

Answers Professional Level Options Module, Paper P6 (UK) Advanced Taxation (United Kingdom) June 2012 Answers 1 Una (a) To The files From Tax senior Date 15 June 2012 Subject Una Gifts to son and granddaughter

Basic Account Basic Account

Basic Account Basic Account Looking after your money, everyday Contents Basic Account 3 Using your Basic Account 5 Getting more from your Visa debit card 6 How to pay money into your account 8 Paying your

Basic Account Basic Account Looking after your money, everyday Contents Basic Account 3 Using your Basic Account 5 Getting more from your Visa debit card 6 How to pay money into your account 8 Paying your

The certification process

TS004(COS)v01 The certification process for COSMOS standard Standard in force available on www.cosmos-standard.org or sent on request. 1 Contents I. When to apply... 3 II. The different steps in the certification

TS004(COS)v01 The certification process for COSMOS standard Standard in force available on www.cosmos-standard.org or sent on request. 1 Contents I. When to apply... 3 II. The different steps in the certification

A quick guide to competition and consumer protection laws that affect your business

A quick guide to competition and consumer protection laws that affect your business A quick guide to competition and consumer protection laws that affect your business 1 A quick guide to competition and

A quick guide to competition and consumer protection laws that affect your business A quick guide to competition and consumer protection laws that affect your business 1 A quick guide to competition and

Triodos Bank. Ethical Stocks and Shares ISA application form.

Triodos Bank. Ethical Stocks and Shares ISA application form. This is an application for a Triodos Ethical Stocks and Shares ISA for the tax year 2016/2017 and each subsequent year until further notice.

Triodos Bank. Ethical Stocks and Shares ISA application form. This is an application for a Triodos Ethical Stocks and Shares ISA for the tax year 2016/2017 and each subsequent year until further notice.

2016 FR-400M. Motor Fuel Tax Forms and Instructions

Government of the District of Columbia Office of the Chief Financial Officer Office of Tax and Revenue 2016 FR-400M Motor Fuel Tax Forms and Instructions Effective October 1, 2013, the District shall levy

Government of the District of Columbia Office of the Chief Financial Officer Office of Tax and Revenue 2016 FR-400M Motor Fuel Tax Forms and Instructions Effective October 1, 2013, the District shall levy

Full Permission. Checklist. Everything you need to prepare for your application

Full Permission Checklist Everything you need to prepare for your application Full Permission Checklist This checklist tells you exactly what you ll need to get Credit Ready, so you can start gathering

Full Permission Checklist Everything you need to prepare for your application Full Permission Checklist This checklist tells you exactly what you ll need to get Credit Ready, so you can start gathering

GE Capital Direct Savings accounts General Terms and Conditions

GE Capital Direct GE Capital Direct Savings accounts General Terms and Conditions If you applied for an account with us before 20 November 2014, these terms and conditions take effect on 20 January 2015.

GE Capital Direct GE Capital Direct Savings accounts General Terms and Conditions If you applied for an account with us before 20 November 2014, these terms and conditions take effect on 20 January 2015.

Self-Employment. Guidance Note GN4

Self-Employment Guidance Note GN4 Issued by the Income Tax Division 23 April 2012 PLEASE NOTE: This guidance has no binding force and does not affect your right of appeal on points concerning your liability

Self-Employment Guidance Note GN4 Issued by the Income Tax Division 23 April 2012 PLEASE NOTE: This guidance has no binding force and does not affect your right of appeal on points concerning your liability

VAT Refund Scheme for academies

VAT Refund Scheme for academies VAT Information Sheet 09/11 June 2011 1. Introduction 1.1 What is this Information Sheet about? This Information Sheet provides guidance for academies, free schools, 16

VAT Refund Scheme for academies VAT Information Sheet 09/11 June 2011 1. Introduction 1.1 What is this Information Sheet about? This Information Sheet provides guidance for academies, free schools, 16

Land Registry Help protect yourself from property fraud keep your contact details up-to-date. May 2016

Land Registry Help protect yourself from property fraud keep your contact details up-to-date May 2016 Could you be at risk of property fraud? If you own a property, it could be a target for fraudsters,

Land Registry Help protect yourself from property fraud keep your contact details up-to-date May 2016 Could you be at risk of property fraud? If you own a property, it could be a target for fraudsters,

The Essential Company Director In-depth guide

The Essential Company Director In-depth guide Icon or graphic 2 Running head The Essential Company Director All companies incorporated under the Companies Act 2006 (CA2006) must have a governing body most

The Essential Company Director In-depth guide Icon or graphic 2 Running head The Essential Company Director All companies incorporated under the Companies Act 2006 (CA2006) must have a governing body most

DISCIPLINARY PROCEDURE

DISCIPLINARY PROCEDURE 1. Purpose and Scope 1.1 The Company s procedure is designed to help and encourage all workers to achieve and maintain standards of conduct, attendance and job performance. The Company

DISCIPLINARY PROCEDURE 1. Purpose and Scope 1.1 The Company s procedure is designed to help and encourage all workers to achieve and maintain standards of conduct, attendance and job performance. The Company