SCB Announces its First Quarter, 2009 Financial Results Despite Adverse Headwinds, a Beacon of Strength & Resilience

|

|

|

- Morgan Davis

- 8 years ago

- Views:

Transcription

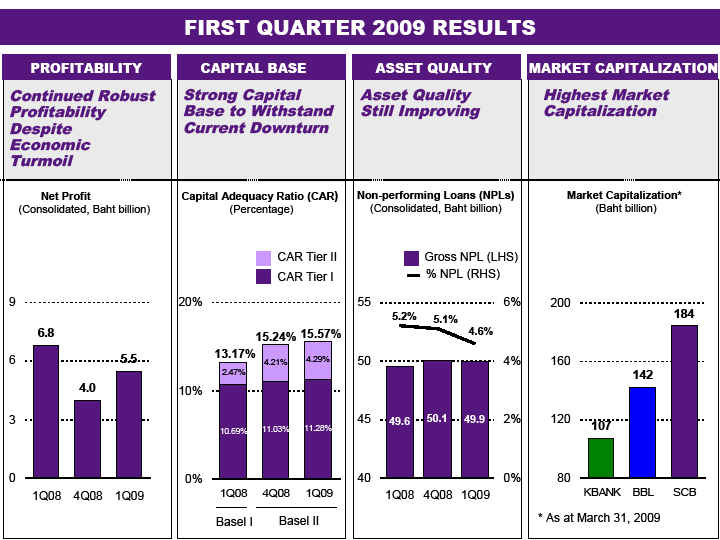

1 Press Release: 20 April, 2009 SCB Announces its First Quarter, 2009 Financial Results Despite Adverse Headwinds, a Beacon of Strength & Resilience Bangkok: The global economic turmoil shows no signs of abating and is taking its toll on the Thai economy. Despite these adverse headwinds, the Bank through its first quarter results was able to demonstrate the resilience of its business strategies and registered a net profit of Baht 5.5 billion, an increase of 39.3 % from 4Q08 but a fall of 18.3% compared to 1Q08. The main adverse impact to the Bank, as a result of the economic downturn, has been on its net interest margins, which dropped from 3.8% in 4Q08 to 3.6% in 1Q09 mainly from the sharp fall in the interbank rates. On the other hand, the Bank was able to successfully contain expense growth, which fell by 14.1% compared to 4Q08 and was flat when compared to 1Q08. Also, as a result of its adherence to prudent underwriting standards, the quality of the loan book has been maintained with the NPL level at 4.6% slightly better than the 5.1% recorded in 4Q08. Finally, the Bank s Capital Adequacy Ratio stands at a high of 15.6% and provides it with the strength to ride through the current economic downturn. Commenting on the first quarter financial results, Dr. Vichit Suraphongchai, Chairman of the Bank s Executive Committee, noted that these are hard times by any standard, and the banking sector as a whole will, inevitably, suffer from a weakened Thai economy. Yet, given its financial strength, this adversity provides SCB with an unprecedented opportunity to deepen relationships with selected customers and develop new capabilities as a springboard to the new post-crisis landscape. Our aim is not simply to weather the current economic storm relatively unscathed, but to emerge from it as clearly the strongest and best regarded financial services franchise in the country. It is the relentless drive to this value proposition which ultimately differentiates us from the other players in our industry. The Bank reported consolidated net profit of Baht 5.5 billion for the first quarter. This was up 39.3% from the 4Q08, although 18.3% behind the record profit registered in 1Q08. However, if one-time gains from investment income and loan provisions are excluded from the 1Q08 net profit, the comparable pre-tax operating profit for 1Q09 was lower by 10.6%. The profitability level of the current quarter has been impacted by the rapidly changing liquidity and interest rate environment. In particular, the Bank was disproportionately affected by the dramatic fall-off in yields in the money market as a larger volume of net interbank deposits were earning sharply lower interest. (The yield in the interbank markets dropped from 3.8% in 1Q08, to 3.2% in 4Q08, to an average yield of only 1.7% in 1Q09). The Bank plans to 1/17

2 address this situation through growing its loan book by lending to the blue-chip and similarly rated public sector enterprises over the coming months. The reported results have, however, benefited from the effective and on-going drive to manage Non Interest Expenses. At Baht 8.1 billion, these expenses have been kept at the same level as reported in 1Q08, and sharply improved from the seasonally high 4Q08 expenses of Baht 9.5 billion. This significant level of expense control has been achieved without forgoing the continued expansion of the retail franchise and other strategic and transformational initiatives that are underway. The Bank expects to maintain this strong expense control discipline. Despite the economic downturn the Bank has been able to maintain the quality of its loan book, and the level of NPLs actually fell from 5.1% (Baht 50.1 billion) at the end of 2008 to 4.6% (Baht 49.9 billion) at the end of 1Q09. In part, this reflects the robust collection and work-out capabilities that the Bank has developed and, in part, it reflects the stringent underwriting criteria that have been adopted by the Bank since early 2008 to forestall the build-up of new NPLs. Finally, the Bank has seen its rigorous capital conservation practices culminate in the high Capital Adequacy Ratio or CAR (using the BASEL II framework). The ratio has increased from the high of 15.2% at the end of last year to 15.6% at the end of 1Q09. This robust capital strength of the Bank not only positions it to ride the economic downturn but, in addition, to capitalize on market opportunities in this likely prolonged slump. Khun Kannikar Chalitaporn, the Bank President, noted that although there is no end in sight for the current global turmoil, the Bank s first quarter results attest to the soundness of the business strategies that we have adopted in response to these profound economic challenges. She added, we are likely to see further deterioration in the economic conditions and our focus on continuing to support selected customers and building market share gains in the blue-chip and public sector, while at the same time containing expenses, is likely to culminate in well above average profitability and strength, thus justifying a higher market premium for our franchise. Siam Commercial Bank PCL is a leading universal bank in Thailand. It was established by Royal Charter in 1906 as the first Thai Bank and, as at March 31, 2009, had the highest market capitalization among Thai Financial Institutions (Baht 184 billion). It has the largest branch (953), exchange booth (136), and ATM (6,249) network in the country, attesting to its dominant position in the retail financial services marketplace. It has a diverse range of Corporate, SME, Private, and Retail customers nationwide, and has an asset size of Baht 1,315 Billion). Further information is available on the Bank's web site at CONTACT Corporate Communications Division Tel: , corp.communications@scb.co.th 2/17

3 3/17

4 SCB Results at a Glance (Consolidated) Unit: Million Baht Q1, 2009 Q1, 2008 % Change yoy Q4, 2008% Change qoq I ncome 16,850 18, % 16, % NII 10,425 10, % 11, % Non NII 6,425 7, % 5, % Non interest expense 8,121 8, % 9, % Operating Profit 8,729 10, % 7, % Provision 1, % 1, % Tax 1,686 2, % 1, % Minority Interest % % Net Profit After Tax 5,547 6, % 3, % Loans 901, , % 916, % Growth (yoy) 43,858 Total Assets 1,314,567 1,196, % 1,241, % Deposit 984, , % 911, % Growth (yoy) 96,672 Loan to Deposit Ratio 91.6% 96.6% 100.6% Loan to Deposit Ratio (Bank only) 89.5% 89.5% 97.7% Loan to Deposit + B/E Ratio (Bank only) 86.4% 88.7% 94.5% Cost to Income Ratio 48.2% 43.9% 57.1% NIM on Earning Assets 3.57% 4.02% 3.82% NPL 49,926 49,573 50,067 NPL% 4.6% 5.2% 5.1% ROE 17.1% 23.7% 12.9% ROA 1.7% 2.3% 1.3% CAR* 15.57% 13.17% 15.24% *CARs for Q1, 2009 and Q4, 2008 are based on Basel II while CAR for Q1, 2008 is based on Basel I. 4/17

43,858 Total Assets 1,314,567 1,196,016 9.9% 1,241,640 5.9% Deposit 984,582 887,910 10.9% 911,482 8.0% Growth (yoy) 96,672 Loan to Deposit Ratio 91.6% 96.6% 100.")

5 Management Discussion and Analysis For the first quarter ended March 31, 2009 Siam Commercial Bank PCL announced unreviewed and unaudited operating results for the first quarter of 2009, with a consolidated net profit of Baht 5,547 million, an 18.3% yoy decrease of Baht 1,240 million from Baht 6,787 million recorded in 1Q08. The decline in net profit was mainly attributed to: (1) lower interest income, as the proportion of low-yield interbank lending (as a percentage of earning assets) increased significantly while rates fell; (2) lower dividend income from investments, particularly from the Vayupak Fund; and (3) lower gain on investments mainly as a result of one-time gain on the sale of an equity investment booked in 1Q08. Stripping out the above-mentioned one-time gain on the sale of an equity investment, operating profit (excluding allowance for doubtful accounts, income tax, and minority interest in subsidiaries) declined 10.6% yoy to Baht 8,729 million in 1Q09 from Baht 9,764 million in 1Q08. Alongside net profit and operating profit, earnings per share (EPS) for the quarter dropped from Baht 2.00 in 1Q08 to Baht 1.63 in 1Q09, while return on average equity (ROE) and return on average assets (ROA) decreased from 23.7% and 2.3% in 1Q08 to 17.1% and 1.7% in 1Q09, respectively. Compared to the previous quarter, net profit rose 39.3% qoq from Baht 3,983 million in 4Q08 to Baht 5,547 million in 1Q09, primarily attributable to (1) higher non-interest income, as losses arising from the disposal or mark down of domestic equity investments booked in 4Q08 did not recur; (2) lower personnel expenses, as the Bank paid out less bonuses than anticipated in the midst of a slowing economy, causing a partial reversal of bonus expenses accrued last year; and (3) lower overall noninterest expenses, as a result of seasonal factors and the Bank's continued effort to control costs. Operating profit increased 22.9% qoq from Baht 7,102 million in 4Q08 to Baht 8,729 million in 1Q09, mainly due to the same reasons above. Unit: Million Baht (Consolidated) 1Q09 4Q08 % qoq 1Q08 % yoy Net Interest and Dividend Income 10,425 11, % 10, % Non-Interest Income 6,425 5, % 7, % Non-Interest Expenses 8,121 9, % 8, % Operating Profit* 8,729 7, % 10, % Allowance for Doubtful Accounts 1,462 1, % % Income Tax 1,686 1, % 2, % Minority Interest in Subsidiaries NM % Net Profit 5,547 3, % 6, % EPS (Baht) % % ROE 17.1% 12.9% 23.7% ROA 1.7% 1.3% 2.3% NM = Not meaningful * Operating profit for 1Q08 was Baht 9,764 million if one-time gain on the sale of an equity investment is excluded 5/17

lower dividend income from investments, particularly from the Vayupak Fund; and (3) lower gain on investments mainly as a result of one-time gain on the sale of an equity investment booked")

6 1Q09 Income Statement (Consolidated basis) 1. Net interest and dividend income Net interest and dividend income declined 5.2% yoy and 5.3% qoq as interest income fell on the back of a sharp increase in the proportion of low-yield interbank lending as a percentage of earning assets, coupled with the reduction of interbank rates. A sharp influx of liquidity together with the Bank adopting a more cautious stance in lending amidst a slowing economy, led the Bank to place such excess liquidity in the low yielding interbank and money markets. Dividend income from investment also fell alongside the weakening market conditions, contributing to the contraction of net interest income. Unit: Million Baht (Consolidated) 1Q09 4Q08 % qoq 1Q08 % yoy Interest and Dividend Income 14,645 16, % 15, % - Loans 11,560 12, % 11, % - Interbank and money markets % 1, % - Hire purchase and financial lease income 1,161 1, % 1, % - Investments 1,334 1, % 1, % Interest Expenses 4,219 5, % 4, % - Deposits 3,247 4, % 3, % - Interbank and money markets % % - Short-term borrowings % % - Long-term borrowings % % Net Interest and Dividend Income 10,425 11, % 10, % Net Interest Margin 3.57% 3.82% 4.02% Yield on earning assets 5.03% 5.63% 5.65% Yield on loans 5.70% 6.28% 5.97% Yield on interbank 1.72% 3.22% 3.83% Yield on investment 3.76% 3.14% 4.99% Cost of funds* 1.58% 1.97% 1.72% Cost of deposit 1.39% 1.80% 1.53% Spread (yield on earning assets cost of funds) 3.45% 3.66% 3.93% Note Profitability ratios are calculated based on monthly average * Cost of funds = interest expenses / interest bearing liability Interest and dividend income in 1Q09 was Baht 14,645 million, a 5.3% yoy decrease of Baht 816 million from Baht 15,461 million in 1Q08. Details include: - Interest income from loans rose 2.6% yoy to Baht 11,560 million in 1Q09, mainly attributable to loan growth of 5.1% yoy which offset the lower yields from the reductions in the Bank s interest rates; 6/17

7 - Interest income from interbank and money markets fell significantly by 52.4% yoy to Baht 589 million in 1Q09, despite an expansion in interbank and money market lending as a result of excess liquidity in 1Q09; - Hire purchase and financial lease income declined 14.7% yoy to Baht 1,161 million in 1Q09, owing mainly to the impact to originations from the adoption of more stringent underwriting criteria in the midst of weakening economic conditions; - Interest and dividend income from investments decreased by 16.4% yoy to Baht 1,334 million in 1Q09, primarily as a result of lower dividend income from Vayupak Fund (Baht 160 million in 1Q09 vs Baht 428 million in 1Q08). Interest expenses fell 5.5% yoy to Baht 4,219 million in 1Q09. Interest expenses on interbank and money market declined 65.4% yoy in 1Q09 mainly due to fallen interbank interest rates, while interest expenses on deposits fell slightly by 1.5% yoy as a result of lower deposit rates, although the deposit base grew by 10.9% yoy. SCB Interest Rates Apr 23, 07 May 24, 07 Jul 20, 07 June 4, 08 Sep 30, 08 Dec 8, 08 Jan 21, 09 Feb 27, 09 Mar 24, 09 Lending Rate MLR 7.25% 7.00% 6.875% 7.25% 7.25% 6.75% 6.50% 6.25% 6.25% Savings Rate 0.75% 0.75% 0.75% 0.75% 0.75% 0.75% 0.75% 0.50% 0.50% Fixed Deposit Rate 3-month deposits % % % % % % % % 0.75% 6-month deposits % % % % % % 1.25% 1.00% 0.75% 12-month deposits % % 2.375% % % 1.75% 1.50% 1.25% 1.00% Apr 11, 07 May 23, 07 Jul 18, 07 Jul 16, 08 Aug 27, 08 Dec 3, 08 Jan 14, 09 Feb 25, 09 Mar 31, 09 Policy Rate 4.00% 3.50% 3.25% 3.50% 3.75% 2.75% 2.00% 1.50% 1.50% Compared with 4Q08, interest and dividend income declined 9.6% qoq from Baht 16,200 million in 4Q08 to Baht 14,645 million in 1Q09. Details are as follow: - Interest income from loans fell 10.9% qoq due to the reduction in lending rates (50 bps in December 2008 and 50 bps in the first quarter of 2009) and because of expected repayment from seasonal working capital loans; - Interest and dividend income from investments increased 22.7% qoq primarily as a result of dividend income from the Vayupak Fund booked in 1Q09; - Hire purchase and financial lease income rose slightly by 0.8% qoq as the Bank has intentionally reduced its risk appetite in this segment and more recent lending is better priced to reflect this change; - Interest income from interbank and money markets dropped 40.6% qoq alongside a sharp reduction in interbank interest rates. 7/17

8 Interest expenses fell 18.8% qoq from Baht 5,194 million in 4Q08 to Baht 4,219 million in 1Q09 as a result of the declining cost of deposits, which fell 21.1% qoq on the back of deposit rate cuts. Interest expenses on borrowings fell 6.3% qoq mainly owing to the reduction in interest rates. With interest income declining by a larger amount than interest expenses, net interest and dividend income dropped 5.2% yoy and 5.3% qoq to Baht 10,425 million in 1Q09. Net interest margin (NIM) fell to 3.57% in 1Q09 from 3.82% in 4Q08 and 4.02% in 1Q08, primarily as a result of increased proportion of low-yield interbank and money market lending as a percentage of earning assets, and the effect of the reduction in interest rates. The Bank s management is in the process of taking actions to mitigate the pressure on net interest income and margins. The Bank aims to channel some of the increased liquidity to loans to blue-chip corporates and the public sector, in order to become less reliant on the low-yielding interbank lending. 2. Non-interest income Non-interest income dropped 14.1% yoy to Baht 6,425 million in 1Q09, principally the result of a onetime gain on the sale of an equity investment booked in 1Q08. Additional details of non-interest income yoy are listed below: - Fee & service income dropped slightly by 0.9% yoy in 1Q09, mainly owing to a decline in brokerage fee as a result of dramatically lower volume in the stock market. Nonetheless, the fees from the card business and bancassurance have continued to grow; 8/17

fell to 3.57% in 1Q09 from 3.82% in 4Q08 and 4.")

9 - Gain on exchange rose 29.3% yoy in 1Q09 on the back of increased business transactions amid volatile foreign exchange markets; - Income from the equity interest in associated companies fell 53.4% yoy in 1Q09 in line with the performance of associated companies; - Gross underwriting income declined 16.9% yoy in 1Q09, in line with the lower business volume of the Bank's non-life insurance subsidiary; - Other income fell 46.6% yoy in 1Q09 as a result of lower gain from the sale of foreclosed properties; - Gain on investment fell significantly by 88.9% yoy, mainly a result of a one-time gain on the sale of an equity investment booked in 1Q08. Unit: Million Baht (Consolidated) 1Q09 4Q08 % qoq 1Q08 % yoy Fee and service income 4,387 4, % 4, % - Acceptances, aval, and guarantees % % - Others 4,133 3, % 4, % Gain on exchange 1,004 1, % % Income from equity interest in affiliated companies % % Underwritings income % % Other income % % Non-Interest Income excluding Gain on Investments 6,335 6, % 6, % Gain on investments NM % Total Non-Interest Income 6,425 5, % 7, % NM = Not meaningful Compared with the previous quarter, non-interest income rose 15.7% qoq from Baht 5,551 million in 4Q08 to Baht 6,425 million in 1Q09. Details include: - Fee and service income rose 8.9% qoq, driven mainly from fee income growth in the bancassurance and fund management business; 9/17

10 - Gain on exchange dropped slightly by 3.5% qoq in line with business transaction volume amid less volatile foreign exchange markets compared to the previous quarter; - Income from equity interests in associated companies dropped 37.0% qoq in line with the performance of associated companies; - Gross underwriting income dropped 4.5% qoq in line with the business volume of the Bank's non-life insurance subsidiary; - Other income fell 41.7% qoq as a result of lower gain from the sale of foreclosed properties; - The Bank booked a gain on investment of Baht 90 million in 1Q09, a sharp recovery from Baht 792 million losses recorded in 4Q08, primarily the result of disposal or mark down of domestic equity investments in the previous quarter. 3. Non-interest expenses Non-interest expenses remained relatively flat at Baht 8,121 million in 1Q09, compared to Baht 8,112 million recorded in 1Q08 reflecting the Bank s strong drive to contain expense growth in the current economic climate. Key items are explained as follows: - Personnel expenses remained relatively unchanged yoy at Baht 2,756 million; - Premises and equipment expenses rose slightly by 4.4% yoy mainly as a result of continued network expansion and systems enhancement initiatives; - Taxes and duties fell 16.5% yoy owing to the reduction in special business tax rates for income from interbank transactions, debt investments and derivatives from 3.3% to 0.01%; - Fee and service expenses increased 9.4% yoy; - Contribution to the FIDF rose 4.8% yoy alongside the expansion of the Bank's deposit base; - Underwriting expenses declined 31.6% yoy in line with business volume of the Bank's non-life insurance subsidiary; - Other expenses rose 4.0% yoy. Unit: Million Baht (Consolidated) 1Q09 4Q08 % qoq 1Q08 % yoy Personnel expenses 2,756 2, % 2, % Premises and equipment expenses 1,948 2, % 1, % Tax and duties % % Fee and service expenses % % Director remuneration % % Contribution to the FIDF % % Underwritings expenses % % Other expenses 916 1, % % Total Non-Interest Expenses 8,121 9, % 8, % Cost to Income Ratio 48.2% 57.1% 43.9% Cost to Income Ratio excluding SCB Samaggi Insurance 47.1% 54.3% 42.6% 10/17

11 Compared to the previous quarter, non-interest expenses fell 14.1% qoq due partly to the decline in personnel expenses as the actual bonus payment was lower than originally anticipated, leading to the partial reversal of bonus expenses accrued in A fall in non-interest expenses was also attributable to seasonal factors and the Bank s continued effort to control costs. Premises and equipment expenses declined 13.9% qoq while underwriting expenses dropped by Baht 38 million (-13.5% qoq). On the other hand, contribution to the FIDF rose slightly by 2.3% qoq as a result of the Bank's larger deposit base. Due mainly to the lower interest and dividend income and the significantly smaller gain on investment, the cost to income ratio rose from 43.9% in 1Q08 to 48.2% in 1Q09, although the figure was well within the Bank s full year target of 49%. Compared to the previous quarter, cost to income ratio dropped significantly from 57.1% in 4Q08 as operating expenses fell more steeply than total income. It should be noted that the consolidated cost to income ratio is distorted by the consolidation of the results of the Bank's non-life insurance subsidiary, SCB Samaggi Insurance. If the non-life insurance subsidiary is excluded, this ratio would further reduce to 47.1% in 1Q Loan loss provision On a bank only basis, the Bank set aside Baht 1,500 million for loan loss provision in 1Q09. The Bank increased the provisioning level from Baht 900 million per quarter for the first three quarters of 2008, to Baht 1,500 million per quarter in 4Q08 to reflect the potential increase in NPL given a rapidly slowing economy. The new provisioning policy was continued in 1Q09. On a consolidated basis, the provision was Baht 1,462 million in 1Q09. Total allowance for doubtful accounts as at the end of March 2009 stood at Baht 40,798 million, a reduction from Baht 41,711 million at the end of December 2008, reflecting the corresponding drop in NPLs from Baht 50,067 million to Baht 49,926 million. 11/17

. On the other hand, contribution to the FIDF rose slightly by 2.3% qoq as a result of the Bank's larger deposit base.")

12 Balance sheet as at March 31, 2009 (Consolidated basis) As at March 31, 2009, the Bank reported total assets of Baht 1,314,567 million, an increase of Baht 118,551 million (9.9%) yoy from Baht 1,196,016 million at the end of March 2008, and an increase of Baht 72,927 million (5.9%) qoq from Baht 1,241,640 million at the end of Details of the consolidated balance sheet are as follows: 1. Loans and Deposits As at March 31, 2009, total outstanding loans stood at Baht 901,885 million, an increase of Baht 43,858 million (5.1%) yoy from Baht 858,027 million at the end of March 2008, and a decrease of Baht 15,035 million (-1.6%) year to date from Baht 916,920 million at the end of Negative loan growth year to date was primarily attributable to expected loan repayments and lower originations following the Bank's adoption of more stringent underwriting criteria in the weakening market environment, as well as loans written-off of Baht 870 million during 1Q09. Good loans grew 5.0% yoy from Baht 817,348 million at the end of March 2008 to Baht 858,328 million at the end of March 2009, while loans under the Special Assets Group increased 7.1% from Baht 40,679 million to Baht 43,557 million. On a year-to-date basis good loans fell slightly by 1.9% from Baht 874,677 million at the end of 2008 to Baht 858,328 million at the end of March 2009, while loans under the Special Assets Group rose 3.1% from Baht 42,243 million at the end of 2008 to Baht 43,557 million. In 1Q09, loan under the Special Asset Group increased while non-performing loan (NPLs) declined year to date primarily because part of the NPLs under the Business Banking Group were transferred to the Special Assets Group in 1Q09. Additional details of loan breakdown by business units and loan types are as follows: - Corporate Banking loans increased 10.3% yoy while they were flat year to date; - Business Banking loans, or loans to SMEs, were flat yoy and fell by 5.6% year to date mainly as a result of loan repayment and the Bank's adoption of more stringent underwriting criteria for new lending; - Retail banking loans increased 3.7% yoy and decreased 1.1% year to date. Housing loans rose 7.6% yoy and increased 0.5% year to date, partly as the result of the Government's tax incentives for the purchase of new homes; Hire purchasing loans dropped 14.2% yoy and 2.8% year to date due to the Bank s adoption of more stringent underwriting criteria given the deteriorating market conditions in this segment; Other loans (largely personal and credit card loans) increased 16.7% yoy, but slid 4.8% year to date. 12/17

yoy from Baht 858,027 million at the end of March 2008, and a decrease of Baht 15,035 million (-1.6%) year to date from Baht 916,920 million at the end of 2008.")

13 Unit: Million Baht Loans Mar 31, 09 Dec 31, 08 % ytd Mar 31, 08 % yoy Good Bank 858, , % 817, % Corporate 310, , % 281, % SME 209, , % 209, % Retail 337, , % 325, % - Housing Loans 209, , % 195, % - Hire Purchase 68,478 70, % 79, % - Others Loans 59,352 62, % 50, % Special Assets Group 43,557 42, % 40, % Total Loans 901, , % 858, % As of March 31, 2009, deposits stood at Baht 984,582 million, up 10.9% yoy from Baht 887,910 million at the end of March 2008, and up 8.0% year to date from Baht 911,482 million at the end of The increase in deposit base was partly attributable to the Bank's special deposit campaign and the flight to safe havens in the midst of the global financial turmoil. Demand deposits, savings deposits and fixed deposits increased by 1.2%, 9.7% and 7.1% respectively year to date. The proportion of savings and demand deposits as a percentage of total deposit base rose slightly to 48.4% at the end of 1Q09 from 47.9% at the end of /17

14 Unit: Million Baht Deposits Mar 31, 09 Dec 31, 08 % ytd Mar 31, 08 % yoy Demand 37,888 37, % 41, % Savings 438, , % 399, % Fixed 508, , % 446, % - Less than 6 months 271, , % 255, % - 6 months and up to 1 year 56,954 50, % 70, % - Over 1 year 180, , % 120, % Total Deposits 984, , % 887, % Bill of Exchange (B/E) (Bank only) 35,489 31, % 8, % Gross Loans to Deposits Ratio (Consolidated) 91.6% 100.6% 96.6% Gross Loans to Deposits Ratio (Bank only) 89.5% 97.7% 89.5% Gross Loans to Deposits and B/E (Bank only) 86.4% 94.4% 88.7% As of March 31, 2009, loan to deposit ratio on a consolidated basis stood at 91.6%, a sharp decrease from 100.6% at the end of On a Bank-only basis, the ratio was 89.5% at the end of 1Q09, a decrease from 97.7% at the end of Loan to deposit and B/E ratio was at 86.4% in 1Q09, falling from 94.4% at the end of These changes underscore the sharp increase in liquidity in 1Q09. As at March 31,2009, interbank and money market items on the asset side stood at Baht 202,951 million, a 49.6% increase from Baht 135,666 million at the end of March 2008, and a 131.4% increase from Baht 87,707 million at the end of A significant rise in the interbank and money market items reflected a sharp influx of liquidity and the Bank adopting a more cautious stance in lending amidst a slowing economy, which led the Bank to place such excess liquidity in the low-yielding interbank and money markets. 2. Investments Investments rose 18.2% yoy to Baht 150,083 million at the end of 1Q09 mainly due to an increase in investment in bonds issued by the Bank of Thailand (BOT). Nonetheless, investments dropped when compared with 4Q08 as the Bank reduced its portfolio in the BOT bonds during 1Q09. 14/17

89.5% 97.7% 89.5% Gross Loans to Deposits and B/E (Bank only) 86.4% 94.4% 88.")

15 Unit: Million Baht Mar 31, 09 Dec 31, 08 % ytd Mar 31, 08 % yoy - Short-term investment-net 34,055 51, % 37, % - Long-term investment-net 111,711 99, % 85, % - Investment in associated companies-net 4,316 4, % 3, % Total Investments-net 150, , % 126, % 3. Borrowings Borrowings rose 61.5% yoy to Baht 84,897 million at the end of 1Q09 mainly from the increase in B/Es over the past four quarters and the issuance of subordinated debentures in May Borrowings also increased 3.0% year to date mainly due to the increase in B/Es during 1Q09. (The B/Es or Bill of Exchange are essentially akin to an uninsured deposit which has gained some popularity over the past few years.) 4. Shareholders equity As of March 31, 2009, shareholders equity stood at Baht 131,631 million, an 11.3% yoy increase of Baht 13,408 million, mainly from the net profit of 21,414 million in This was reduced by dividend payment of Baht 6,798 million (Baht 2 per share or dividend payout ratio of 39%) in accordance with Shareholder's Meeting Resolution in April Shareholders' equity increased 3.5% year to date or by Baht 4,427 million from the end of 2008, primarily attributable to the 1Q09 net profit of Baht 5,547 million more than offsetting the reduction of unrealized gain on investment of Baht 1,152 million. Book value per share as of March 31, 2009 was Baht (3,399 million ordinary and preferred shares at the end of March 2009), up from Baht at the end of Statutory Capital (Bank only) Total capital funds (Tier 1 and Tier 2) as of March 31, 2009 were solid at 15.57% of total risk-weighted assets, representing Tier-1-capital of 11.28% and Tier-2-capital of 4.29%. 15/17

4.")

at the end of March 2009. Net NPLs also fell from Baht 26,453 million (2.8%) at the end of 2008 to Baht 25,431 million (2.4%) at the end of March 2009.")

16 Non Performing Assets Gross NPLs on a consolidated basis continued to fall from Baht 50,067 million (5.1% of total loans) at the end of 2008 to Baht 49,926 million (4.6% of total loans) at the end of March Net NPLs also fell from Baht 26,453 million (2.8%) at the end of 2008 to Baht 25,431 million (2.4%) at the end of March The continued improvement in the group's asset quality in 1Q09 was mainly attributable to bad loan write-offs, the Bank's continued debt restructuring effort, as well as strengthened collection capability at the Bank s auto hire purchase subsidiary, SCBL. Allowance for doubtful accounts as of March 31, 2009 stood at Baht 40,798 million, a decrease of Baht 913 million from the end of 2008, mainly from bad debt write-offs. The coverage ratio (total allowance to non-performing loans) remained strong at 81.7% Gross NPLs on a bank basis were Baht 45,142 million (4.3%), an increase of Baht 546 million from the end of Net non-performing loans (net NPLs) were Baht 23,369 million or 2.3% of total loans, a decrease of Baht 366 million from Baht 23,735 million (2.6%) at the end of /17

17 (Bank only) Classified loans and Allowance for Doubtful Accounts Unit: Million Baht Mar 31, 09 Dec 31, 08 Mar 31, 08 Allowance Allowance Amount Allowance Amount for for for Amount Classified classified classified loans loans loans Normal 981,457 11, ,815 10, ,790 9,358 Special Mention 24,311 1,111 24,462 1,149 11, Substandard 5,589 2,619 6,984 2,974 8,741 3,315 Doubtful 6,635 1,856 6,709 1,951 6,555 2,785 Doubtful Loss 32,917 15,490 30,903 14,763 28,508 11,319 Total 1,050,910 32, ,873 30, ,120 27,690 General and Specific Allowance 7,830 8,430 11,092 Total Allowance 40,165 39,309 38,782 Non-performing Loans (net) (Substandard and lower) 23,368 23,735 22,709 % of Total Classified Loans (including loans to financial institutions) 2.3% 2.6% 2.6% As at March 2009, the Bank and its subsidiaries which are financial institutions have outstanding loans to the restructured debtors including accrued interest receivables of Baht 39,718 million in the consolidated financial statements and Baht 39,718 million for the Bank only (December 31, 2008: Baht 40,643 million and Baht 40,642 million, respectively.) The Bank's foreclosed properties in 1Q09 amounted to Baht 11,673 million, a decrease of Baht 314 million (-2.6% year to date) mainly achieved through the sale of these assets. 17/17

(Substandard and lower) 23,368 23,735 22,709 % of Total Classified Loans (including loans to financial institutions) 2.3% 2.6% 2.")

2 nd Quarter, 2012 Results ANALYST MEETING, 27 JULY, 2012

2 nd Quarter, 2012 Results ANALYST MEETING, 27 JULY, 2012 Agenda Page 1. Review of Result 2Q12 3-19 2. Future Positioning 21-25 3. 2012 Targets 27 IMPORTANT DISCLAIMER: Information contained in this document

2 nd Quarter, 2012 Results ANALYST MEETING, 27 JULY, 2012 Agenda Page 1. Review of Result 2Q12 3-19 2. Future Positioning 21-25 3. 2012 Targets 27 IMPORTANT DISCLAIMER: Information contained in this document

Review of 1 st Quarter, 2012

Review of 1 st Quarter, 2012 ANALYST MEETING, 26 APRIL, 2012 Deepak Sarup, CFO Agenda Page 1. Review of Result 1Q12 3-17 2. Future Positioning 19-23 3. 2012 Targets 25 IMPORTANT DISCLAIMER: Information

Review of 1 st Quarter, 2012 ANALYST MEETING, 26 APRIL, 2012 Deepak Sarup, CFO Agenda Page 1. Review of Result 1Q12 3-17 2. Future Positioning 19-23 3. 2012 Targets 25 IMPORTANT DISCLAIMER: Information

Performance of the Thai Banking System in the First Quarter of 2015

No. 26/2 Performance of the Thai Banking System in the First Quarter of 2 Mr. Jaturong Jantarangs, Senior Director, Financial Institutions Policy Group, reported the Thai banking system s performance in

No. 26/2 Performance of the Thai Banking System in the First Quarter of 2 Mr. Jaturong Jantarangs, Senior Director, Financial Institutions Policy Group, reported the Thai banking system s performance in

Bank of Ghana Monetary Policy Report. Financial Stability Report

BANK OF GHANA E S T. 1 9 5 7 Bank of Ghana Monetary Policy Report Financial Stability Report Volume 5: No.1/2013 February 2013 5.0 Introduction Conditions in global financial markets have improved significantly

BANK OF GHANA E S T. 1 9 5 7 Bank of Ghana Monetary Policy Report Financial Stability Report Volume 5: No.1/2013 February 2013 5.0 Introduction Conditions in global financial markets have improved significantly

How To Make Money From A Bank Loan

NEWS RELEASE FOR FURTHER INFORMATION: WEBSITE: www.bnccorp.com TIMOTHY J. FRANZ, CEO TELEPHONE: (612) 305-2213 DANIEL COLLINS, CFO TELEPHONE: (612) 305-2210 BNCCORP, INC. REPORTS THIRD QUARTER NET INCOME

NEWS RELEASE FOR FURTHER INFORMATION: WEBSITE: www.bnccorp.com TIMOTHY J. FRANZ, CEO TELEPHONE: (612) 305-2213 DANIEL COLLINS, CFO TELEPHONE: (612) 305-2210 BNCCORP, INC. REPORTS THIRD QUARTER NET INCOME

BALANCE SHEET AND INCOME STATEMENT

BANCOLOMBIA S.A. (NYSE: CIB; BVC: BCOLOMBIA, PFBCOLOM) REPORTS CONSOLIDATED NET INCOME OF COP 1,879 BILLION FOR 2014, AN INCREASE OF 24% COMPARED TO 2013. Operating income increased 23.8% during 2014 and

BANCOLOMBIA S.A. (NYSE: CIB; BVC: BCOLOMBIA, PFBCOLOM) REPORTS CONSOLIDATED NET INCOME OF COP 1,879 BILLION FOR 2014, AN INCREASE OF 24% COMPARED TO 2013. Operating income increased 23.8% during 2014 and

Business and Financial Highlights Nine Months Ended December 31, 2014. Shinsei Bank, Limited January 2015

Business and Financial Highlights Nine Months Ended December 31, 214 Shinsei Bank, Limited January 215 Table of Contents Q3 FY214 Results: Key Points ------------------------------------------ Q3 FY214

Business and Financial Highlights Nine Months Ended December 31, 214 Shinsei Bank, Limited January 215 Table of Contents Q3 FY214 Results: Key Points ------------------------------------------ Q3 FY214

Third Quarter 2014 Financial Results

Third Quarter 2014 Financial Results Core pre-provision income up by 8.0% in the third quarter 2014. Operating expenses further down by 3.7% q-o-q and 11.4% y-o-y on a comparable basis. Accelerated provisioning

Third Quarter 2014 Financial Results Core pre-provision income up by 8.0% in the third quarter 2014. Operating expenses further down by 3.7% q-o-q and 11.4% y-o-y on a comparable basis. Accelerated provisioning

Citizens Financial Group, Inc. Reports First Quarter Net Income of $223 Million Diluted EPS of $0.41 up 8% vs. 1Q15

Reports First Quarter Net Income of $223 Million Diluted EPS of $0.41 up 8% vs. 1Q15 Positive operating leverage of 3% on a year-over-year Adjusted basis* Good traction continues on strategic growth and

Reports First Quarter Net Income of $223 Million Diluted EPS of $0.41 up 8% vs. 1Q15 Positive operating leverage of 3% on a year-over-year Adjusted basis* Good traction continues on strategic growth and

Group Financial Review

Management Discussion and Analysis of Financial Statements. Fifth consecutive year of record performance for the Group. Simplified Income Statement RM Million +/- RM Million % Net interest income 2,065.9

Management Discussion and Analysis of Financial Statements. Fifth consecutive year of record performance for the Group. Simplified Income Statement RM Million +/- RM Million % Net interest income 2,065.9

Management s Discussion and Analysis for 2014

1 Business Overview Industry total premiums as of December were 504 billion baht 1, a 13.75% increase over the same period of the previous year. They can be divided into first year premiums of 171 billion

1 Business Overview Industry total premiums as of December were 504 billion baht 1, a 13.75% increase over the same period of the previous year. They can be divided into first year premiums of 171 billion

How To Understand The Turkish Economy

BRSA Bank Only Macro Outlook Q1 GDP growth at 3.2%, mostly backed by net exports. Budget deficit was TRY 6.7 billion in H1 12, one third of Latest GDP figure is supportive of the soft landing the government

BRSA Bank Only Macro Outlook Q1 GDP growth at 3.2%, mostly backed by net exports. Budget deficit was TRY 6.7 billion in H1 12, one third of Latest GDP figure is supportive of the soft landing the government

COMMERCIAL INTERNATIONAL BANK ( CIB ) REPORTS RECORD FULL-YEAR 2015 CONSOLIDATED REVENUE OF EGP 10.2 BILLION AND RECORD NET INCOME OF EGP 4

REPORTS RECORD FULL-YEAR 2015 CONSOLIDATED REVENUE OF EGP 10.2 BILLION AND RECORD NET INCOME OF EGP 4") News Release 10 February 2016 Commercial International Bank (Egypt) SAE Nile Tower, 21/23 Charles de Gaulle Street, Giza 11511, Egypt www.cibeg.com EGX Symbol: COMI COMMERCIAL INTERNATIONAL BANK ( CIB

News Release 10 February 2016 Commercial International Bank (Egypt) SAE Nile Tower, 21/23 Charles de Gaulle Street, Giza 11511, Egypt www.cibeg.com EGX Symbol: COMI COMMERCIAL INTERNATIONAL BANK ( CIB

Balance sheet structure absorbed adverse PSI+ effect

Full Year 2011 Results Participation in PSI+ 1 leads to additional impairment of Euro 3.2 billion Core Tier I at Euro 1.3 billion 2 post PSI+ related impairment Balance sheet structure absorbed adverse

Full Year 2011 Results Participation in PSI+ 1 leads to additional impairment of Euro 3.2 billion Core Tier I at Euro 1.3 billion 2 post PSI+ related impairment Balance sheet structure absorbed adverse

Second Quarter 2015 Trading Update. 28 September 2015

Second Quarter 2015 Trading Update 28 September 2015 Disclaimer This communication and the information contained herein has been approved by the Board of Directors of Eurobank Ergasias S.A. ( Eurobank

Second Quarter 2015 Trading Update 28 September 2015 Disclaimer This communication and the information contained herein has been approved by the Board of Directors of Eurobank Ergasias S.A. ( Eurobank

The Board of Directors of DBS Group Holdings Ltd ( DBSH ) reports the following:

reports the following:") DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number: 199901152M To: Shareholders The Board of Directors of DBS Group Holdings Ltd ( DBSH ) reports the following:

DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number: 199901152M To: Shareholders The Board of Directors of DBS Group Holdings Ltd ( DBSH ) reports the following:

News Release April 29, 2016. Performance Review: Quarter ended March 31, 2016

News Release April 29, Performance Review: Quarter ended March 31, 16% year-on-year growth in domestic advances; retail portfolio crossed ` 2,00,000 crore (US$ 30.2 billion) during the quarter ended March

News Release April 29, Performance Review: Quarter ended March 31, 16% year-on-year growth in domestic advances; retail portfolio crossed ` 2,00,000 crore (US$ 30.2 billion) during the quarter ended March

News Release January 28, 2016. Performance Review: Quarter ended December 31, 2015

News Release January 28, 2016 Performance Review: Quarter ended December 31, 20% year-on-year growth in total domestic advances; 24% year-on-year growth in retail advances 18% year-on-year growth in current

News Release January 28, 2016 Performance Review: Quarter ended December 31, 20% year-on-year growth in total domestic advances; 24% year-on-year growth in retail advances 18% year-on-year growth in current

Arrow Reports Solid First Quarter Operating Results and Strong Asset Quality Ratios

250 Glen Street Glens Falls, NY Contact: Timothy C. Badger Tel: (518)745-1000 Fax: (518)745-1976 TO: All Media DATE: Tuesday, April 19, 2011 Arrow Reports Solid First Quarter Operating Results and Strong

250 Glen Street Glens Falls, NY Contact: Timothy C. Badger Tel: (518)745-1000 Fax: (518)745-1976 TO: All Media DATE: Tuesday, April 19, 2011 Arrow Reports Solid First Quarter Operating Results and Strong

October 21, 2015 MEDIA & INVESTOR CONTACT Heather Worley, 214.932.6646 heather.worley@texascapitalbank.com

October 21, 2015 MEDIA & INVESTOR CONTACT Heather Worley, 214.932.6646 heather.worley@texascapitalbank.com TEXAS CAPITAL BANCSHARES, INC. ANNOUNCES OPERATING RESULTS FOR Q3 2015 DALLAS - October 21, 2015

October 21, 2015 MEDIA & INVESTOR CONTACT Heather Worley, 214.932.6646 heather.worley@texascapitalbank.com TEXAS CAPITAL BANCSHARES, INC. ANNOUNCES OPERATING RESULTS FOR Q3 2015 DALLAS - October 21, 2015

TCS Group Holding PLC Announces 1Q 2015 IFRS Results

TCS Group Holding PLC Announces 1Q 2015 IFRS Results Moscow, Russia 8 June 2015. TCS Group Holding PLC (TCS LI) (the Group ), Russia's leading provider of online retail financial services, including Tinkoff

TCS Group Holding PLC Announces 1Q 2015 IFRS Results Moscow, Russia 8 June 2015. TCS Group Holding PLC (TCS LI) (the Group ), Russia's leading provider of online retail financial services, including Tinkoff

Hong Leong Bank Announces Second Quarter FY2012 Results

For immediate release 27 February 2012 Hong Leong Bank Announces Second Quarter FY2012 Results Net profit after tax for 2Q FYE 30 June 2012 ( 2Q12 ) reached RM 381 million, a growth of 30% compared to

For immediate release 27 February 2012 Hong Leong Bank Announces Second Quarter FY2012 Results Net profit after tax for 2Q FYE 30 June 2012 ( 2Q12 ) reached RM 381 million, a growth of 30% compared to

Financial Results of Japan's Banks for Fiscal 2012

July 13 Financial Results of Japan's Banks for Fiscal 1 Financial System and Bank Examination Department Please contact the department below in advance to request permission when reproducing or copying

July 13 Financial Results of Japan's Banks for Fiscal 1 Financial System and Bank Examination Department Please contact the department below in advance to request permission when reproducing or copying

FOR IMMEDIATE RELEASE

FOR IMMEDIATE RELEASE FirstMerit Corporation Analysts: Thomas O Malley/Investor Relations Officer Phone: 330.384.7109 Media Contact: Robert Townsend/Media Relations Officer Phone: 330.384.7075 FirstMerit

FOR IMMEDIATE RELEASE FirstMerit Corporation Analysts: Thomas O Malley/Investor Relations Officer Phone: 330.384.7109 Media Contact: Robert Townsend/Media Relations Officer Phone: 330.384.7075 FirstMerit

Financial Overview INCOME STATEMENT ANALYSIS

In the first half of 2006, China s economy experienced steady and swift growth as evidenced by a 10.9% surge in GDP. In order to prevent the economy from getting overheated and to curb excess credit extension,

In the first half of 2006, China s economy experienced steady and swift growth as evidenced by a 10.9% surge in GDP. In order to prevent the economy from getting overheated and to curb excess credit extension,

Subject: Preliminary consolidated financial statements of the Capital Group of Bank Handlowy w Warszawie S.A. for the 2014

Warsaw, February 12, 2015 Subject: Preliminary consolidated financial statements of the Capital Group of Bank Handlowy w Warszawie S.A. for the 2014 Legal basis: Art. 5 section 1 item 25) of the Ordinance

Warsaw, February 12, 2015 Subject: Preliminary consolidated financial statements of the Capital Group of Bank Handlowy w Warszawie S.A. for the 2014 Legal basis: Art. 5 section 1 item 25) of the Ordinance

Finansbank Q2 15 Corporate Presentation

Finansbank Q2 15 Corporate Presentation 0 Agenda Turkish Banking Landscape & Finansbank Loan-based Balance Sheet Delivering High Quality Earnings Solid Financial Performance Appendix 1 Structurally attractive

Finansbank Q2 15 Corporate Presentation 0 Agenda Turkish Banking Landscape & Finansbank Loan-based Balance Sheet Delivering High Quality Earnings Solid Financial Performance Appendix 1 Structurally attractive

The first quarter was highlighted by:

Mercantile Bank Corporation Reports Strong First Quarter 2013 Results Diluted earnings per share increased 79 percent Continued asset quality improvement and outlook remains positive GRAND RAPIDS, Mich.,

Mercantile Bank Corporation Reports Strong First Quarter 2013 Results Diluted earnings per share increased 79 percent Continued asset quality improvement and outlook remains positive GRAND RAPIDS, Mich.,

Announcement of Financial Results 1999. for. Den Danske Bank Group

Announcement of Financial Results 1999 for Den Danske Bank Group 2 Den Danske Bank Group Highlights Core earnings and net profit for the year (DKr million) 1999 1998 1997 1996 1995 Net interest income,

Announcement of Financial Results 1999 for Den Danske Bank Group 2 Den Danske Bank Group Highlights Core earnings and net profit for the year (DKr million) 1999 1998 1997 1996 1995 Net interest income,

Mr. N. S. Kannan s opening remarks for analyst call on January 28, 2016

Mr. N. S. Kannan s opening remarks for analyst call on January 28, 2016 Good evening and welcome to the conference call on the financial results of ICICI Bank for the quarter ended December 31, 2015, that

Mr. N. S. Kannan s opening remarks for analyst call on January 28, 2016 Good evening and welcome to the conference call on the financial results of ICICI Bank for the quarter ended December 31, 2015, that

QBE INSURANCE GROUP Annual General Meeting 2009. All amounts in Australian dollars unless otherwise stated.

Annual General Meeting 2009 All amounts in Australian dollars unless otherwise stated. John Cloney Chairman 2 Results of proxy voting A total of 4,874 valid proxy forms were received. The respective votes

Annual General Meeting 2009 All amounts in Australian dollars unless otherwise stated. John Cloney Chairman 2 Results of proxy voting A total of 4,874 valid proxy forms were received. The respective votes

FACTORS AFFECTING THE LOAN SUPPLY OF BANKS

FACTORS AFFECTING THE LOAN SUPPLY OF BANKS Funding resources The liabilities of banks operating in Estonia mainly consist of non-financial sector deposits, which totalled almost 11 billion euros as at

FACTORS AFFECTING THE LOAN SUPPLY OF BANKS Funding resources The liabilities of banks operating in Estonia mainly consist of non-financial sector deposits, which totalled almost 11 billion euros as at

Ally Financial Inc. 3Q 2015 Earnings Review

Ally Financial Inc. 3Q 2015 Earnings Review October 29, 2015 Contact Ally Investor Relations at (866) 710-4623 or investor.relations@ally.com Forward-Looking Statements and Additional Information The following

Ally Financial Inc. 3Q 2015 Earnings Review October 29, 2015 Contact Ally Investor Relations at (866) 710-4623 or investor.relations@ally.com Forward-Looking Statements and Additional Information The following

2013 Annual Results. D. Francisco Gómez Martín CEO. Madrid, January 31 st, 2014

2013 Annual Results D. Francisco Gómez Martín CEO Madrid, January 31 st, 2014 Disclaimer This presentation has been prepared by Banco Popular Español solely for purposes of information. It may contain

2013 Annual Results D. Francisco Gómez Martín CEO Madrid, January 31 st, 2014 Disclaimer This presentation has been prepared by Banco Popular Español solely for purposes of information. It may contain

I will now give you an overview of our third quarter financial results using the document titled Consolidated Results of Operations.

I will now give you an overview of our third quarter financial results using the document titled Consolidated Results of Operations. Please turn to page two. 1 For the nine months to December, net revenue

I will now give you an overview of our third quarter financial results using the document titled Consolidated Results of Operations. Please turn to page two. 1 For the nine months to December, net revenue

Operating Performance 2011. - For Annual Results Briefing

Operating Performance 2011 - For Annual Results Briefing March 2012 Contents Operation and Management in 2011 Business Strategy for 2012 2 Part 1 Operation and Management in 2011 Note: Figures without

Operating Performance 2011 - For Annual Results Briefing March 2012 Contents Operation and Management in 2011 Business Strategy for 2012 2 Part 1 Operation and Management in 2011 Note: Figures without

ISBANK EARNINGS PRESENTATION 2016 Q1

ISBANK EARNINGS PRESENTATION 2016 Q1 2016 Q1 Recent Developments in the Economy Binler Global Outlook Main Indicators of Turkey US EA Moderate expansion in the US economy Solid labor market data Still

ISBANK EARNINGS PRESENTATION 2016 Q1 2016 Q1 Recent Developments in the Economy Binler Global Outlook Main Indicators of Turkey US EA Moderate expansion in the US economy Solid labor market data Still

BANCA SISTEMA GROWING ACROSS ALL BUSINESS LINES WITH A NET INCOME UP BY 21% YoY 1

PRESS RELEASE BANCA SISTEMA GROWING ACROSS ALL BUSINESS LINES WITH A NET INCOME UP BY 21% YoY 1 Business performance Factoring: turnover +20% yoy and growing customer base from 124 in 2014 to 294 in 2015

PRESS RELEASE BANCA SISTEMA GROWING ACROSS ALL BUSINESS LINES WITH A NET INCOME UP BY 21% YoY 1 Business performance Factoring: turnover +20% yoy and growing customer base from 124 in 2014 to 294 in 2015

Sberbank Group s IFRS Results for 6 Months 2013. August 2013

Sberbank Group s IFRS Results for 6 Months 2013 August 2013 Summary of 6 Months 2013 performance: Income Statement Net profit reached RUB 174.5 bn (or RUB 7.95 per ordinary share), a 0.5% decrease on RUB

Sberbank Group s IFRS Results for 6 Months 2013 August 2013 Summary of 6 Months 2013 performance: Income Statement Net profit reached RUB 174.5 bn (or RUB 7.95 per ordinary share), a 0.5% decrease on RUB

GOLDMAN SACHS REPORTS THIRD QUARTER LOSS PER COMMON SHARE OF $0.84

The Goldman Sachs Group, Inc. 200 West Street New York, New York 10282 GOLDMAN SACHS REPORTS THIRD QUARTER LOSS PER COMMON SHARE OF $0.84 NEW YORK, October 18, 2011 - The Goldman Sachs Group, Inc. (NYSE:

The Goldman Sachs Group, Inc. 200 West Street New York, New York 10282 GOLDMAN SACHS REPORTS THIRD QUARTER LOSS PER COMMON SHARE OF $0.84 NEW YORK, October 18, 2011 - The Goldman Sachs Group, Inc. (NYSE:

Report of 3Q 2015 consolidated results Information reported in Ps. billions (1) and under Full IFRS (1) We refer to billions as thousands of

and under Full IFRS (1) We refer to billions as thousands of") Report of 3Q 2015 consolidated results Information reported in Ps. billions (1) and under Full IFRS (1) We refer to billions as thousands of millions. isclaimer Grupo Aval Acciones y Valores S.A. ( Grupo

Report of 3Q 2015 consolidated results Information reported in Ps. billions (1) and under Full IFRS (1) We refer to billions as thousands of millions. isclaimer Grupo Aval Acciones y Valores S.A. ( Grupo

Northwest Bancshares, Inc. Announces Quarterly Earnings and Dividend Declaration

EARNINGS RELEASE FOR IMMEDIATE RELEASE Contact: William J. Wagner, President and Chief Executive Officer (814) 726-2140 William W. Harvey, Jr., Executive Vice President and Chief Financial Officer (814)

EARNINGS RELEASE FOR IMMEDIATE RELEASE Contact: William J. Wagner, President and Chief Executive Officer (814) 726-2140 William W. Harvey, Jr., Executive Vice President and Chief Financial Officer (814)

GOLDMAN SACHS REPORTS SECOND QUARTER EARNINGS PER COMMON SHARE OF $3.72. Highlights

The Goldman Sachs Group, Inc. 200 West Street New York, New York 10282 GOLDMAN SACHS REPORTS SECOND QUARTER EARNINGS PER COMMON SHARE OF $3.72 NEW YORK, July 19, 2016 - The Goldman Sachs Group, Inc. (NYSE:

The Goldman Sachs Group, Inc. 200 West Street New York, New York 10282 GOLDMAN SACHS REPORTS SECOND QUARTER EARNINGS PER COMMON SHARE OF $3.72 NEW YORK, July 19, 2016 - The Goldman Sachs Group, Inc. (NYSE:

Second Quarter Report June 30, 2005

Financial Highlights Second Quarter Report June 30, 2005 Three Months Ended For the Period Ended June 30 (Unaudited) In Thousands of Dollars (Except Per Share and Percentage Amounts) 2005 2004 2005 2004

Financial Highlights Second Quarter Report June 30, 2005 Three Months Ended For the Period Ended June 30 (Unaudited) In Thousands of Dollars (Except Per Share and Percentage Amounts) 2005 2004 2005 2004

QNB CORP. REPORTS SECOND QUARTER AND FIRST HALF EARNINGS

PO Box 9005 Quakertown PA 18951-9005 215.538.5600 1.800.491.9070 www.qnbbank.com FOR IMMEDIATE RELEASE QNB CORP. REPORTS SECOND QUARTER AND FIRST HALF EARNINGS QUAKERTOWN, PA (July 28, 2015) QNB Corp.

PO Box 9005 Quakertown PA 18951-9005 215.538.5600 1.800.491.9070 www.qnbbank.com FOR IMMEDIATE RELEASE QNB CORP. REPORTS SECOND QUARTER AND FIRST HALF EARNINGS QUAKERTOWN, PA (July 28, 2015) QNB Corp.

CorpBanca Announces First Quarter 2011 Financial Results and Conference Call on Tuesday, May 17, 2011

CorpBanca Announces First Quarter 2011 Financial Results and Conference Call on Tuesday, May 17, 2011 Santiago, Chile, CORPBANCA (NYSE: BCA), a Chilean financial institution offering a wide variety of

CorpBanca Announces First Quarter 2011 Financial Results and Conference Call on Tuesday, May 17, 2011 Santiago, Chile, CORPBANCA (NYSE: BCA), a Chilean financial institution offering a wide variety of

Q3 2014 IFRS Results. November 2014

Q3 4 IFRS Results November 4 Important Notice By attending the meeting where the presentation is made, or by reading the presentation slides, you agree to the following limitations and notifications and

Q3 4 IFRS Results November 4 Important Notice By attending the meeting where the presentation is made, or by reading the presentation slides, you agree to the following limitations and notifications and

Ally Financial Reports Full Year and Fourth Quarter 2015 Financial Results

Ally Financial Reports Full Year and Fourth Quarter 2015 Financial Results Full Year 2015 Financial Highlights Net income of $1.3 billion, up 12% compared to $1.2 billion Adjusted EPS of $2.00, up 19%

Ally Financial Reports Full Year and Fourth Quarter 2015 Financial Results Full Year 2015 Financial Highlights Net income of $1.3 billion, up 12% compared to $1.2 billion Adjusted EPS of $2.00, up 19%

GOLDMAN SACHS REPORTS FIRST QUARTER EARNINGS PER COMMON SHARE OF $4.02

The Goldman Sachs Group, Inc. 200 West Street New York, New York 10282 GOLDMAN SACHS REPORTS FIRST QUARTER EARNINGS PER COMMON SHARE OF $4.02 NEW YORK, April 17, 2014 - The Goldman Sachs Group, Inc. (NYSE:

The Goldman Sachs Group, Inc. 200 West Street New York, New York 10282 GOLDMAN SACHS REPORTS FIRST QUARTER EARNINGS PER COMMON SHARE OF $4.02 NEW YORK, April 17, 2014 - The Goldman Sachs Group, Inc. (NYSE:

Q4.14 Financial Results. March 23, 2015

Q4.14 Financial Results March 23, 2015 Table of Contents 1 Results overview 2 Liquidity 3 Profitability 4 Asset quality 5 Capital 6 Appendix Results overview 1 4Q14 results: key take-aways Liquidity Group

Q4.14 Financial Results March 23, 2015 Table of Contents 1 Results overview 2 Liquidity 3 Profitability 4 Asset quality 5 Capital 6 Appendix Results overview 1 4Q14 results: key take-aways Liquidity Group

How To Improve Bankia'S Financial Performance

Morgan Stanley European Financials Conference Bankia Overview March 2014 Mr. Leopoldo Alvear - CFO Bankia Contents 1. Strategy and restructuring plan 2. 2013 results 3. Asset quality and risk management

Morgan Stanley European Financials Conference Bankia Overview March 2014 Mr. Leopoldo Alvear - CFO Bankia Contents 1. Strategy and restructuring plan 2. 2013 results 3. Asset quality and risk management

Colleen Johnston Group Head Finance & CFO TD Bank Financial Group. Citi Financial Services Conference

Colleen Johnston Group Head Finance & CFO TD Bank Financial Group Citi Financial Services Conference January 28, 2009 Caution regarding forward-looking statements From time to time, the Bank makes written

Colleen Johnston Group Head Finance & CFO TD Bank Financial Group Citi Financial Services Conference January 28, 2009 Caution regarding forward-looking statements From time to time, the Bank makes written

2012 Interim Results 2012.08.23

2012 Interim Results 2012.08.23 1 Forward-Looking Statement Disclaimer This presentation and subsequent discussions may contain forwardlooking statements that involve risks and uncertainties. These statements

2012 Interim Results 2012.08.23 1 Forward-Looking Statement Disclaimer This presentation and subsequent discussions may contain forwardlooking statements that involve risks and uncertainties. These statements

SBERBANK GROUP S IFRS RESULTS. March 2015

SBERBANK GROUP S IFRS RESULTS 2014 March 2015 SUMMARY OF PERFORMANCE FOR 2014 STATEMENT OF PROFIT OR LOSS Net profit reached RUB 290.3bn (or RUB 13.45 per ordinary share), compared to RUB 362.0bn (or RUB

SBERBANK GROUP S IFRS RESULTS 2014 March 2015 SUMMARY OF PERFORMANCE FOR 2014 STATEMENT OF PROFIT OR LOSS Net profit reached RUB 290.3bn (or RUB 13.45 per ordinary share), compared to RUB 362.0bn (or RUB

BANCO SANTANDER CHILE ANNOUNCES RESULTS FOR THE FIRST QUARTER 2003

www.santandersantiago.cl BANCO SANTANDER CHILE ANNOUNCES RESULTS FOR THE FIRST QUARTER 2003 Net income for the first quarter of 2003 totaled Ch$40,497 million (Ch$0.21 per share and US$0.31/ADR) decreasing

www.santandersantiago.cl BANCO SANTANDER CHILE ANNOUNCES RESULTS FOR THE FIRST QUARTER 2003 Net income for the first quarter of 2003 totaled Ch$40,497 million (Ch$0.21 per share and US$0.31/ADR) decreasing

of Fiscal 2006 (Consolidated)

") Outline of Financial Results for the 3rd Quarter of Fiscal 2006 (Consolidated) Feb.3, 2006 For Immediate Release Company Name (URL http://www.fhi.co./jp/fina/index.html ) : Fuji Heavy Industries Ltd. (Code

Outline of Financial Results for the 3rd Quarter of Fiscal 2006 (Consolidated) Feb.3, 2006 For Immediate Release Company Name (URL http://www.fhi.co./jp/fina/index.html ) : Fuji Heavy Industries Ltd. (Code

GOLDMAN SACHS REPORTS EARNINGS PER COMMON SHARE OF $17.07 FOR 2014

The Goldman Sachs Group, Inc. 200 West Street New York, New York 10282 GOLDMAN SACHS REPORTS EARNINGS PER COMMON SHARE OF $17.07 FOR 2014 FOURTH QUARTER EARNINGS PER COMMON SHARE WERE $4.38 NEW YORK, January

The Goldman Sachs Group, Inc. 200 West Street New York, New York 10282 GOLDMAN SACHS REPORTS EARNINGS PER COMMON SHARE OF $17.07 FOR 2014 FOURTH QUARTER EARNINGS PER COMMON SHARE WERE $4.38 NEW YORK, January

4Q15. Management Discussion & Analysis and Complete Financial Statements

4Q15 Management Discussion & Analysis and Complete Financial Statements CONTENTS 03 Management Discussion & Analysis 05 Executive Summary 15 Income Statement and Balance Sheet Analysis 16 18 22 25 28 33

4Q15 Management Discussion & Analysis and Complete Financial Statements CONTENTS 03 Management Discussion & Analysis 05 Executive Summary 15 Income Statement and Balance Sheet Analysis 16 18 22 25 28 33

Territorial Bancorp Inc. Announces 2015 Results

PRESS RELEASE FOR IMMEDIATE RELEASE Contact: Walter Ida (808) 946-1400 Territorial Bancorp Inc. Announces 2015 Results Fully diluted earnings per share for the three months ended December 31, 2015 rose

PRESS RELEASE FOR IMMEDIATE RELEASE Contact: Walter Ida (808) 946-1400 Territorial Bancorp Inc. Announces 2015 Results Fully diluted earnings per share for the three months ended December 31, 2015 rose

COMMERCE BANCSHARES, INC. ANNOUNCES FOURTH QUARTER EARNINGS PER COMMON SHARE OF $.63

Exhibit 99.1 1000 Walnut Street / Suite 700 / Kansas City, Missouri 64106 / 816.234.2000 CBSH FOR IMMEDIATE RELEASE: Wednesday, January 20, 2016 COMMERCE BANCSHARES, INC. ANNOUNCES FOURTH QUARTER EARNINGS

Exhibit 99.1 1000 Walnut Street / Suite 700 / Kansas City, Missouri 64106 / 816.234.2000 CBSH FOR IMMEDIATE RELEASE: Wednesday, January 20, 2016 COMMERCE BANCSHARES, INC. ANNOUNCES FOURTH QUARTER EARNINGS

Managing diversified businesses against challenging conditions

Managing diversified businesses against challenging conditions April 21, 2003 DBS Group Holdings 1Q 2003 Financial Results Presentation to Media and Analysts This presentation is available at www.dbs.com/investor

Managing diversified businesses against challenging conditions April 21, 2003 DBS Group Holdings 1Q 2003 Financial Results Presentation to Media and Analysts This presentation is available at www.dbs.com/investor

K-IRQ: 2Q13 Page1. From CIRO. Dear KBank investors and analysts, 2Q13 Earnings Forecasts. No. of analysts

Page1 Second Quarter 2013 At a glance KBank Interest rates Deposits (%) Effective Date Savings Vol.2 No.4 0.75 22 Feb 12 Fixed-3m 1.60-2.00 14 Jan 13 Fixed-6m 1.95-2.25 14 Jan 13 Fixed-12m 2.30-2.45 14

Page1 Second Quarter 2013 At a glance KBank Interest rates Deposits (%) Effective Date Savings Vol.2 No.4 0.75 22 Feb 12 Fixed-3m 1.60-2.00 14 Jan 13 Fixed-6m 1.95-2.25 14 Jan 13 Fixed-12m 2.30-2.45 14

CUSTOMERS BANCORP REPORTS RECORD NET INCOME FOR FULL YEAR AND FOURTH QUARTER 2015

Customers Bancorp 1015 Penn Avenue Wyomissing, PA 19610 Contacts: Jay Sidhu, Chairman & CEO 610-935-8693 Richard Ehst, President & COO 610-917-3263 Investor Contact: Robert Wahlman, CFO 610-743-8074 CUSTOMERS

Customers Bancorp 1015 Penn Avenue Wyomissing, PA 19610 Contacts: Jay Sidhu, Chairman & CEO 610-935-8693 Richard Ehst, President & COO 610-917-3263 Investor Contact: Robert Wahlman, CFO 610-743-8074 CUSTOMERS

1. Rationale. 2. Statutory Power

1. Rationale Unofficial Translation With courtesy of the Association of International Banks This translation is for the convenience of those unfamiliar with the Thai language Please refer to the Thai text

1. Rationale Unofficial Translation With courtesy of the Association of International Banks This translation is for the convenience of those unfamiliar with the Thai language Please refer to the Thai text

E.SUN FHC Financial Review of 1Q 2015

E.SUN FHC Financial Review of 1Q 2015 May 2015 Disclaimer This Presentation is provided by E.SUN Financial Holding Co., Ltd. ( E.SUN FHC ). E.SUN makes no guarantee or warranties as to the accuracy or

E.SUN FHC Financial Review of 1Q 2015 May 2015 Disclaimer This Presentation is provided by E.SUN Financial Holding Co., Ltd. ( E.SUN FHC ). E.SUN makes no guarantee or warranties as to the accuracy or

BANCO SANTANDER CHILE ANNOUNCES RESULTS FOR THE FOURTH QUARTER 2002

Banco Santander Chile CONTACTS: Raimundo Monge Robert Moreno Desirée Soulodre Banco Santander Chile Banco Santander Chile Banco Santander Chile 562-320-8505 562-320-8284 562-647-6474 BANCO SANTANDER CHILE

Banco Santander Chile CONTACTS: Raimundo Monge Robert Moreno Desirée Soulodre Banco Santander Chile Banco Santander Chile Banco Santander Chile 562-320-8505 562-320-8284 562-647-6474 BANCO SANTANDER CHILE

Comprehensive Financial Analysis

First West Credit Union 2012 md&a Comprehensive Financial Analysis Comprehensive Financial Analysis Balance Sheet Management Total Assets Total assets increased $428 million or 7.8% in 2012 compared with

First West Credit Union 2012 md&a Comprehensive Financial Analysis Comprehensive Financial Analysis Balance Sheet Management Total Assets Total assets increased $428 million or 7.8% in 2012 compared with

FDIC Quarterly Banking Profile 2015 Q3

Commercial Banking Analysis FDIC Quarterly Banking Profile 2015 Q3 Filip Blazheski Positive Third Quarter but Profitability Remains Subdued as Risks Lurk grew and earnings were up in the third quarter

Commercial Banking Analysis FDIC Quarterly Banking Profile 2015 Q3 Filip Blazheski Positive Third Quarter but Profitability Remains Subdued as Risks Lurk grew and earnings were up in the third quarter

QUAINT OAK BANCORP, INC. ANNOUNCES SECOND QUARTER EARNINGS

FOR RELEASE: Tuesday, July 28, 2015 at 4:30 PM (Eastern) QUAINT OAK BANCORP, INC. ANNOUNCES SECOND QUARTER EARNINGS Southampton, PA Quaint Oak Bancorp, Inc. (the Company ) (OTCQX: QNTO), the holding company

FOR RELEASE: Tuesday, July 28, 2015 at 4:30 PM (Eastern) QUAINT OAK BANCORP, INC. ANNOUNCES SECOND QUARTER EARNINGS Southampton, PA Quaint Oak Bancorp, Inc. (the Company ) (OTCQX: QNTO), the holding company

Morgan Stanley Reports Full-Year and Fourth Quarter Results

Contact: Media Relations Investor Relations Jeanmarie McFadden Suzanne Charnas 212-762-6901 212-761-3043 Morgan Stanley Reports Full-Year and Fourth Quarter Results Full-Year Net Revenues of $23.4 Billion

Contact: Media Relations Investor Relations Jeanmarie McFadden Suzanne Charnas 212-762-6901 212-761-3043 Morgan Stanley Reports Full-Year and Fourth Quarter Results Full-Year Net Revenues of $23.4 Billion

Exane BNP Paribas Spain Investors Day

Exane BNP Paribas Spain Investors Day Francisco Sancha, CFO Madrid, January 13 th, 2015 Disclaimer This presentation has been prepared by Banco Popular Español solely for purposes of information. It may

Exane BNP Paribas Spain Investors Day Francisco Sancha, CFO Madrid, January 13 th, 2015 Disclaimer This presentation has been prepared by Banco Popular Español solely for purposes of information. It may

GOLDMAN SACHS REPORTS THIRD QUARTER EARNINGS PER COMMON SHARE OF $2.90

The Goldman Sachs Group, Inc. 200 West Street New York, New York 10282 GOLDMAN SACHS REPORTS THIRD QUARTER EARNINGS PER COMMON SHARE OF $2.90 NEW YORK, October 15, 2015 - The Goldman Sachs Group, Inc.

The Goldman Sachs Group, Inc. 200 West Street New York, New York 10282 GOLDMAN SACHS REPORTS THIRD QUARTER EARNINGS PER COMMON SHARE OF $2.90 NEW YORK, October 15, 2015 - The Goldman Sachs Group, Inc.

FOR IMMEDIATE RELEASE

Exhibit 99.1 FOR IMMEDIATE RELEASE FirstMerit Corporation Analysts: Thomas O Malley/Investor Relations Officer Phone: 330.384.7109 Media Contact: Robert Townsend/Media Relations Officer Phone: 330.384.7075

Exhibit 99.1 FOR IMMEDIATE RELEASE FirstMerit Corporation Analysts: Thomas O Malley/Investor Relations Officer Phone: 330.384.7109 Media Contact: Robert Townsend/Media Relations Officer Phone: 330.384.7075

First Quarter 2011 Update. Ta Chong Bank

First Quarter 2011 Update Ta Chong Bank Disclaimer The presentation contained within is not reviewed or reviewed by any accountant or any independent third party. While Ta Chong Bank endeavor to provide

First Quarter 2011 Update Ta Chong Bank Disclaimer The presentation contained within is not reviewed or reviewed by any accountant or any independent third party. While Ta Chong Bank endeavor to provide

Financial Results 3Q 2014. 5th November 2014

Financial Results 3Q 2014 5th November 2014 Disclaimer This document was prepared by LIBERBANK, S.A., ("LIBERBANK") and is presented exclusively for informational purposes. It is not a prospectus and does

Financial Results 3Q 2014 5th November 2014 Disclaimer This document was prepared by LIBERBANK, S.A., ("LIBERBANK") and is presented exclusively for informational purposes. It is not a prospectus and does

GOLDMAN SACHS REPORTS FIRST QUARTER EARNINGS PER COMMON SHARE OF $2.68

The Goldman Sachs Group, Inc. 200 West Street New York, New York 10282 GOLDMAN SACHS REPORTS FIRST QUARTER EARNINGS PER COMMON SHARE OF $2.68 NEW YORK, April 19, 2016 - The Goldman Sachs Group, Inc. (NYSE:

The Goldman Sachs Group, Inc. 200 West Street New York, New York 10282 GOLDMAN SACHS REPORTS FIRST QUARTER EARNINGS PER COMMON SHARE OF $2.68 NEW YORK, April 19, 2016 - The Goldman Sachs Group, Inc. (NYSE:

Second Quarter Report 2004

For the period ended April 30, 2004 Second Quarter Report 2004 I am pleased to present BMO Financial Group s Second Quarter 2004 Report to Shareholders. Tony Comper President and Chief Executive Officer

For the period ended April 30, 2004 Second Quarter Report 2004 I am pleased to present BMO Financial Group s Second Quarter 2004 Report to Shareholders. Tony Comper President and Chief Executive Officer

Standard Chartered Bank (Thai) PCL & its Financial Business Group Pillar 3 Disclosures 30 June 2015

PCL & its Financial Business Group Pillar 3 Disclosures 30 June 2015") Standard Chartered Bank (Thai) PCL & its Financial Business Group Registered Office: 90 North Sathorn Road, Silom Bangkok, 10500, Thailand Overview During 2013, the Bank of Thailand ( BOT ) published the

Standard Chartered Bank (Thai) PCL & its Financial Business Group Registered Office: 90 North Sathorn Road, Silom Bangkok, 10500, Thailand Overview During 2013, the Bank of Thailand ( BOT ) published the

implementing management vision looking forward five years

Results for the interim period of the year ending March 31, The Asahi Bank, Ltd. 1. Strong earnings base : Net operating profit exceeded forecast issued at the beginning of the period Sharp focus on domestic

Results for the interim period of the year ending March 31, The Asahi Bank, Ltd. 1. Strong earnings base : Net operating profit exceeded forecast issued at the beginning of the period Sharp focus on domestic

2015 Fourth Quarter Earnings. January 28, 2016

2015 Fourth Quarter Earnings January 28, 2016 Safe Harbor Statement Forward-Looking Statements Information in this presentation contains forward-looking statements. Any statements about our expectations,

2015 Fourth Quarter Earnings January 28, 2016 Safe Harbor Statement Forward-Looking Statements Information in this presentation contains forward-looking statements. Any statements about our expectations,

HSBC BANK CANADA FIRST QUARTER 2014 RESULTS

7 May 2014 HSBC BANK CANADA FIRST QUARTER 2014 RESULTS Profit before income tax expense for the quarter ended 2014 was C$233m, a decrease of 13.4% compared with the same period in and broadly unchanged

7 May 2014 HSBC BANK CANADA FIRST QUARTER 2014 RESULTS Profit before income tax expense for the quarter ended 2014 was C$233m, a decrease of 13.4% compared with the same period in and broadly unchanged

Overview Q1 2009 YTD 09 YTD 08 -35 37. Core income in DKK million. Cost and expenses in DKK million 399 343

Q1 29 Satisfactory growth in earnings before impairment - impairment of loans and advances and contributions to sectortargeted solutions slice pre-tax profits to DKK 49 million 29 April 29 Overview Q1

Q1 29 Satisfactory growth in earnings before impairment - impairment of loans and advances and contributions to sectortargeted solutions slice pre-tax profits to DKK 49 million 29 April 29 Overview Q1

H1 2014 IFRS Results. August 2014

H 4 IFRS Results August 4 Important Notice By attending the meeting where the presentation is made, or by reading the presentation slides, you agree to the following limitations and notifications and represent

H 4 IFRS Results August 4 Important Notice By attending the meeting where the presentation is made, or by reading the presentation slides, you agree to the following limitations and notifications and represent

Mighty oaks from little acorns

07.11.2005 Earnings announcement for 30.September.2005 consolidated financial results according to BRSA Mighty oaks from little acorns Total assets increased 36% (10% q-o-q) and reached TRY 10,974mn (USD

07.11.2005 Earnings announcement for 30.September.2005 consolidated financial results according to BRSA Mighty oaks from little acorns Total assets increased 36% (10% q-o-q) and reached TRY 10,974mn (USD

Taishin Financial Holding Company

Taishin Financial Holding Company 2003 Result Announcement & Analyst Meeting February 10, 2004 Agenda Section 1 2003 Performance Review (preliminary) Section 2 2004 Earnings Outlook Section 3 Business

Taishin Financial Holding Company 2003 Result Announcement & Analyst Meeting February 10, 2004 Agenda Section 1 2003 Performance Review (preliminary) Section 2 2004 Earnings Outlook Section 3 Business

STANDARD DOCUMENT COVER SHEET FOR SEC FILINGS. SEC Number 121 File Number

STANDARD DOCUMENT COVER SHEET FOR SEC FILINGS All documents should be submitted under a cover page which clearly identifies the company and the specific document form as follows: SEC Number 121 File Number

STANDARD DOCUMENT COVER SHEET FOR SEC FILINGS All documents should be submitted under a cover page which clearly identifies the company and the specific document form as follows: SEC Number 121 File Number

Emirates NBD (ENBD) Strong Buy. Target Price AED10.0. Global Research Investment Update Equity UAE Banking Sector 31 January, 2016

Strong Buy. Target Price AED10.0. Global Research Investment Update Equity UAE Banking Sector 31 January, 2016") Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Global Research Investment Update Equity UAE Banking Sector 31 January, 2016 Market Data Bloomberg Code: Emirates

Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Global Research Investment Update Equity UAE Banking Sector 31 January, 2016 Market Data Bloomberg Code: Emirates

AIB Group (UK) p.l.c. Highlights of 2015 Business and Financial Performance. For the year ended 31 December 2015. Company number: NI018800

p.l.c. Highlights of 2015 Business and Financial Performance. For the year ended 31 December 2015. Company number: NI018800") AIB Group (UK) p.l.c. Highlights of 2015 Business and Financial Performance For the year ended 31 December 2015 Company number: NI018800 Contents Page Financial and Business review 1. 2015 Performance

AIB Group (UK) p.l.c. Highlights of 2015 Business and Financial Performance For the year ended 31 December 2015 Company number: NI018800 Contents Page Financial and Business review 1. 2015 Performance

Important information

29 April 2014 1 Important information Banco Santander, S.A. ("Santander") cautions that this presentation contains forward-looking statements. These forward-looking statements are found in various places

29 April 2014 1 Important information Banco Santander, S.A. ("Santander") cautions that this presentation contains forward-looking statements. These forward-looking statements are found in various places

1Q15 Consolidated Earnings Results

1Q15 Consolidated Earnings Results Colombian Banking GAAP and IFRS June 2015 Disclaimer Grupo Aval Acciones y Valores S.A. ( Grupo Aval ) is an issuer of securities in Colombia and in the United States,

1Q15 Consolidated Earnings Results Colombian Banking GAAP and IFRS June 2015 Disclaimer Grupo Aval Acciones y Valores S.A. ( Grupo Aval ) is an issuer of securities in Colombia and in the United States,

José González de Castejón (787) 759-9094 Ana Calvo de Luis (212) 350-3903 Margie Alvarez (787) 250-3025

759-9094 Ana Calvo de Luis (212) 350-3903 Margie Alvarez (787) 250-3025") Santander BanCorp Press release For more information contact: Puerto Rico New York José González de Castejón (787) 759-9094 Ana Calvo de Luis (212) 350-3903 Margie Alvarez (787) 250-3025 SANTANDER BANCORP

Santander BanCorp Press release For more information contact: Puerto Rico New York José González de Castejón (787) 759-9094 Ana Calvo de Luis (212) 350-3903 Margie Alvarez (787) 250-3025 SANTANDER BANCORP

PULASKI FINANCIAL S SECOND FISCAL QUARTER EPS MORE THAN TRIPLES

PULASKI FINANCIAL S SECOND FISCAL QUARTER EPS MORE THAN TRIPLES Current Versus Prior Year Quarter Highlights Earnings growth - Diluted EPS $0.29 in 2013 versus $0.08 in 2012 - Annualized return on average

PULASKI FINANCIAL S SECOND FISCAL QUARTER EPS MORE THAN TRIPLES Current Versus Prior Year Quarter Highlights Earnings growth - Diluted EPS $0.29 in 2013 versus $0.08 in 2012 - Annualized return on average

2Q15 Consolidated Earnings Results

2Q15 Consolidated Earnings Results IFRS September 2015 Disclaimer Grupo Aval Acciones y Valores S.A. ( Grupo Aval ) is an issuer of securities in Colombia and in the United States, registered with Colombia

2Q15 Consolidated Earnings Results IFRS September 2015 Disclaimer Grupo Aval Acciones y Valores S.A. ( Grupo Aval ) is an issuer of securities in Colombia and in the United States, registered with Colombia

Territorial Bancorp Inc. Announces Second Quarter 2015 Results

PRESS RELEASE FOR IMMEDIATE RELEASE Contact: Walter Ida (808) 946-1400 Territorial Bancorp Inc. Announces Second Quarter 2015 Results Earnings per share for the three months ended June 30, 2015 rose to

PRESS RELEASE FOR IMMEDIATE RELEASE Contact: Walter Ida (808) 946-1400 Territorial Bancorp Inc. Announces Second Quarter 2015 Results Earnings per share for the three months ended June 30, 2015 rose to

April 25, 2016 (573) 778-1800

778-1800") FOR IMMEDIATE RELEASE Contact: Matt Funke, CFO April 25, 2016 (573) 778-1800 SOUTHERN MISSOURI BANCORP REPORTS PRELIMINARY THIRD QUARTER RESULTS, DECLARES QUARTERLY DIVIDEND OF $0.09 PER COMMON SHARE,

FOR IMMEDIATE RELEASE Contact: Matt Funke, CFO April 25, 2016 (573) 778-1800 SOUTHERN MISSOURI BANCORP REPORTS PRELIMINARY THIRD QUARTER RESULTS, DECLARES QUARTERLY DIVIDEND OF $0.09 PER COMMON SHARE,

THIRD QUARTER 2004 QUARTERLY REPORT FOR THE PERIOD ENDED JULY 31, 2004

THIRD QUARTER 2004 QUARTERLY REPORT FOR THE PERIOD ENDED JULY 31, 2004 Report to shareholders Laurentian Bank of Canada reports net income of $13.7 million for the third quarter of 2004 SUMMARY RESULTS

THIRD QUARTER 2004 QUARTERLY REPORT FOR THE PERIOD ENDED JULY 31, 2004 Report to shareholders Laurentian Bank of Canada reports net income of $13.7 million for the third quarter of 2004 SUMMARY RESULTS

Q3 INTERIM MANAGEMENT STATEMENT Presentation to analysts and investors. 28 October 2014

INTERIM MANAGEMENT STATEMENT Presentation to analysts and investors 28 October HIGHLIGHTS FOR THE FIRST NINE MONTHS OF Continued successful execution of our strategy and further improvement in financial

INTERIM MANAGEMENT STATEMENT Presentation to analysts and investors 28 October HIGHLIGHTS FOR THE FIRST NINE MONTHS OF Continued successful execution of our strategy and further improvement in financial

GOLDMAN SACHS REPORTS FIRST QUARTER EARNINGS PER COMMON SHARE OF $5.94 AND INCREASES THE QUARTERLY DIVIDEND TO $0.65 PER COMMON SHARE