Predictive Modeling Solutions for Small Business Insurance

|

|

|

- Roger Day

- 9 years ago

- Views:

Transcription

1 Predictive Modeling Solutions for Small Business Insurance Robert J. Walling, FCAS, MAAA October 6, 2008 CAS Predictive Modeling Seminar San Diego, CA

2 Presentation Outline Current BOP Market Dynamics Rating Plan Enhancements Underwriting Scorecards

3 Current BOP Market Dynamics

4 Current BOP Market Soft, Softer, Softest Impact of Agency & MGA Captives By-Peril Rating Enhanced Territory Definitions Expanded Eligibility Detailed Class Factors Expanded Amount of Insurance U/W Scorecards vs. Schedule Rating

5 BOP Predictive Modeling Here to Stay Five Leading BOP Insurers Using Predictive Modeling : Beat Industry Loss Ratio by Points Outperformed Industry 5 of 7 years, Up to 15 Points All Grew Faster Than Industry One Group by 5% per year! Superior Growth and Operating Results Sustained Competitive Advantage Cream Skimming, Adverse Selection

6 Rating Plan Enhancements

7 Class Refinement

8 Refined AOI Curves Personal Property Limit (000's) <$ Limit Of Insurance Relativity Group A Group B Group C

9 New Rating Factors Age of Building Credit Factors: Age Original Construction Significantly Renovated Franchise Factor: Property Liability Mall Credit Property Liability

10 Multi-Policy Discounts

11 Industry Specific Rating Factors

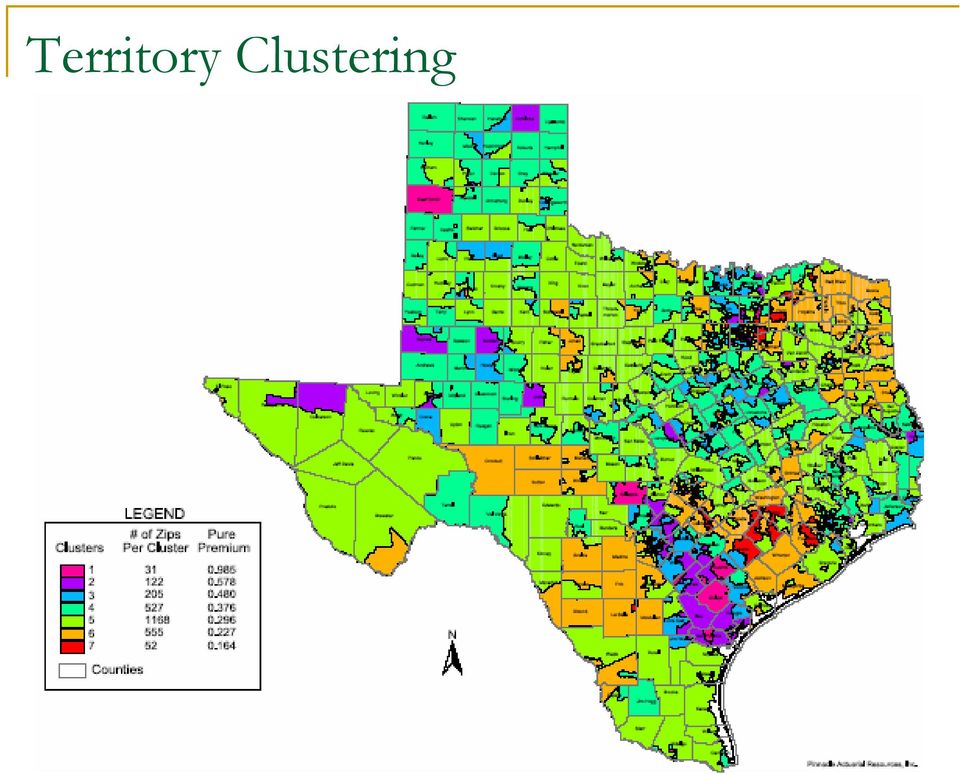

12 Territory Clustering

13 Underwriting Scorecards

14 Traditional Underwriting vs. Rating Historically Distinct (and often conflicting) Underwriting Determined Eligibility Rating Determined Manual Premium Underwriting then Applied IRPM/Schedule Rating

15 Historical Risk Selection & Pricing Flow Yes Underwriting Rating Overlaps IRPM/ Schedule No

16 Underwriting vs. Rating Today Lines are blurred Underwriting determines eligibility, often using modeled actuarial data Underwriting determines rating tier, often with actuarially determined tiers Actuarial determines tier relativities and rates

17 Current Risk Selection and Pricing Flow Tiering Rating Underwriting Yes Tiering Tiering Rating Rating No

18 Underwriting Score Definition A scaling of multiple predictive model factors into a single metric resulting in a single premium modification and/or an eligibility threshold.

19 Underwriting Scorecard Scaling Credit Score Credit Score Exposure Indicated On Balance Score Relativity Indicated Points A 359, M 153, NS 90, S 106, U 26,

20 Lots of Small Factors

21 Class-Specific Scoring

22 Additional Internal Information Percent Occupied Elevators Years in Business Years of Same Mgt. Age of Building Updated Systems Alarms Resp. for Parking Lot? Computer Back Ups Hours of Operation Building Height Deliveries? Swimming Pools Franchisee? Safety Program # of Employees/Leasing Type of Entity (Individual, Partnership, Corporation, LLC) Location of Building (Mall, Strip Mall, Attached to Habitational, Stand Alone) Not to mention Billing history, account experience

23 Additional External Information Credit Score Commercial Owner Lots of Operational Info Niche Specific (CLUE of Habitational Tenants) Adjacent Properties/Tenants Geographic Data Economic/Demographic Data Property Value Data Commercial CLUE

24 Potential ZIP Code Level Demographics Data Available Population Density Traffic Density Population Growth Unemployment Rates Building Vacancy Rates Industry Mix Prosperity Indices Sources Publicly available from census sources Useful for addressing location specific issues

25 Building of Underwriting Score Build predictive model with all rating variables and potential tiering variables (3 ways) Complete Tiering then rating Rating then tiering Develop selections for underwriting variables Calculate underwriting score for each risk Calculate final rating relativities

26 Interactions Matter Pure Premium Relativities by Program and Years in Business Pure Premium Relativity Contractors Habitational Office Restaurant Retail/Service Wholesale Years in Business

27 Underwriting Scorecards with Interactions Multivariate analysis allows the modeling of interactions and facilitates incorporation into scorecards Years of Score Points Current Control Contr. Habit. Off. Rest. Ret./Serv. Wholes

28 Underwriting Scorecard - Farmers

29 Underwriting Scorecard - Farmers

30 Underwriting Scorecard - Farmers

31 Travelers BOP Scorecard NOTICE THE LIFT!

32 Scorecard Advantages Regulatory Underwriting Guidelines Preserve Competitive Advantage To File or Not to File? Small & Class Specific Factors Response to Counter-Intuitive Results (e.g. ACV, named perils) Similarity to Credit Scoring (Intuitive) Ability for Underwriter/Agent Feedback

33 Intuitive Look & Feel Other intuitive scaling approaches are also quite common.

34 Benefits of Using GLM for BOP Scorecard Improves Predictive Accuracy of Net Pricing Increases Underwriting Effectiveness Increases Use of Who Characteristics Creates Adverse Selection for Competitors Reflects Interactions Fast, Cost-Effective Tool for U/W Decisions Demonstrated Success Personal and Commercial Lines Expand Your Markets Smarter Soft Market Reaction Provides Feedback to Underwriter, Agent & Insured

35 For More Information Monograph-PowerTools.pdf

36 Closing Thoughts It is a capital mistake to theorize before one has data. Insensibly one begins to twist facts to suit theories, instead of theories to suit facts. - Sir Arthur Conan Doyle You can use all the quantitative data you can get, but you still have to distrust it and use your own intelligence and judgment. - Alvin Toffler

Anti-Trust Notice. Agenda. Three-Level Pricing Architect. Personal Lines Pricing. Commercial Lines Pricing. Conclusions Q&A

Achieving Optimal Insurance Pricing through Class Plan Rating and Underwriting Driven Pricing 2011 CAS Spring Annual Meeting Palm Beach, Florida by Beth Sweeney, FCAS, MAAA American Family Insurance Group

Achieving Optimal Insurance Pricing through Class Plan Rating and Underwriting Driven Pricing 2011 CAS Spring Annual Meeting Palm Beach, Florida by Beth Sweeney, FCAS, MAAA American Family Insurance Group

Innovations and Value Creation in Predictive Modeling. David Cummings Vice President - Research

Innovations and Value Creation in Predictive Modeling David Cummings Vice President - Research ISO Innovative Analytics 1 Innovations and Value Creation in Predictive Modeling A look back at the past decade

Innovations and Value Creation in Predictive Modeling David Cummings Vice President - Research ISO Innovative Analytics 1 Innovations and Value Creation in Predictive Modeling A look back at the past decade

HOMEOWNERS BY-PERIL RATING PLAN

HOMEOWNERS BY-PERIL RATING PLAN Homeowners By-Peril Rating Plan Your Plan to Compete... Homeowners insurers are under intense pressure to rate policies more precisely. With more carriers utilizing refined

HOMEOWNERS BY-PERIL RATING PLAN Homeowners By-Peril Rating Plan Your Plan to Compete... Homeowners insurers are under intense pressure to rate policies more precisely. With more carriers utilizing refined

UBI-5: Usage-Based Insurance from a Regulatory Perspective

UBI-5: Usage-Based Insurance from a Regulatory Perspective Carl Sornson, FCAS Managing Actuary Property/Casualty NJ Dept of Banking & Insurance 2015 CAS RPM Seminar March 10, 2015 Antitrust Notice The

UBI-5: Usage-Based Insurance from a Regulatory Perspective Carl Sornson, FCAS Managing Actuary Property/Casualty NJ Dept of Banking & Insurance 2015 CAS RPM Seminar March 10, 2015 Antitrust Notice The

In comparison, much less modeling has been done in Homeowners

Predictive Modeling for Homeowners David Cummings VP & Chief Actuary ISO Innovative Analytics 1 Opportunities in Predictive Modeling Lessons from Personal Auto Major innovations in historically static

Predictive Modeling for Homeowners David Cummings VP & Chief Actuary ISO Innovative Analytics 1 Opportunities in Predictive Modeling Lessons from Personal Auto Major innovations in historically static

Large Scale Analysis of Persistency and Renewal Discounts for Property and Casualty Insurance

Large Scale Analysis of Persistency and Renewal Discounts for Property and Casualty Insurance Cheng-Sheng Peter Wu, FCAS, ASA, MAAA Hua Lin, FCAS, MAAA, Ph.D. Abstract In this paper, we study the issue

Large Scale Analysis of Persistency and Renewal Discounts for Property and Casualty Insurance Cheng-Sheng Peter Wu, FCAS, ASA, MAAA Hua Lin, FCAS, MAAA, Ph.D. Abstract In this paper, we study the issue

Personal Auto Predictive Modeling Update: What s Next? Roosevelt Mosley, FCAS, MAAA CAS Predictive Modeling Seminar October 6 7, 2008 San Diego, CA

Personal Auto Predictive Modeling Update: What s Next? Roosevelt Mosley, FCAS, MAAA CAS Predictive Modeling Seminar October 6 7, 2008 San Diego, CA You ve Heard Where predictive modeling for auto has been

Personal Auto Predictive Modeling Update: What s Next? Roosevelt Mosley, FCAS, MAAA CAS Predictive Modeling Seminar October 6 7, 2008 San Diego, CA You ve Heard Where predictive modeling for auto has been

Current Regulatory and Market Advancements in the China P&C Insurance Market

2015 CAS RPM Seminar, International Track Current Regulatory and Market Advancements in the China P&C Insurance Market Moderator: Cheng-sheng Peter Wu, FCAS, ASA, MAAA Panelists: Dr. Jun Yan Professor

2015 CAS RPM Seminar, International Track Current Regulatory and Market Advancements in the China P&C Insurance Market Moderator: Cheng-sheng Peter Wu, FCAS, ASA, MAAA Panelists: Dr. Jun Yan Professor

Intelligent Use of Competitive Analysis

Intelligent Use of Competitive Analysis 2011 Ratemaking and Product Management Seminar Kelleen Arquette March 21 22, 2011 2011 Towers Watson. All rights reserved. AGENDA Session agenda and objectives The

Intelligent Use of Competitive Analysis 2011 Ratemaking and Product Management Seminar Kelleen Arquette March 21 22, 2011 2011 Towers Watson. All rights reserved. AGENDA Session agenda and objectives The

Staying Ahead of the Analytical Competitive Curve: Integrating the Broad Range Applications of Predictive Modeling in a Competitive Market Environment

Staying Ahead of the Analytical Competitive Curve: Integrating the Broad Range Applications of Predictive Modeling in a Competitive Market Environment Jun Yan, Ph.D., Mo Masud, and Cheng-sheng Peter Wu,

Staying Ahead of the Analytical Competitive Curve: Integrating the Broad Range Applications of Predictive Modeling in a Competitive Market Environment Jun Yan, Ph.D., Mo Masud, and Cheng-sheng Peter Wu,

2008 CAS Ratemaking Seminar COM-2: Non-Standard Distribution Channels: Managing General Agents and Programs

2008 CAS Ratemaking Seminar COM-2: Non-Standard Distribution Channels: Managing General Agents and Programs Cameron J. Vogt, FCAS, CFA, MAAA Vice President, Munich Reinsurance America, Inc. March 17, 2008

2008 CAS Ratemaking Seminar COM-2: Non-Standard Distribution Channels: Managing General Agents and Programs Cameron J. Vogt, FCAS, CFA, MAAA Vice President, Munich Reinsurance America, Inc. March 17, 2008

Report to the 79 th Legislature. Use of Credit Information by Insurers in Texas

Report to the 79 th Legislature Use of Credit Information by Insurers in Texas Texas Department of Insurance December 30, 2004 TABLE OF CONTENTS Executive Summary Page 3 Discussion Introduction Page 6

Report to the 79 th Legislature Use of Credit Information by Insurers in Texas Texas Department of Insurance December 30, 2004 TABLE OF CONTENTS Executive Summary Page 3 Discussion Introduction Page 6

Product Management Case Study. What makes Effective Product Management Process?

What makes Effective Product Management Process? The Product: The steps involved in developing a product to eventually manage What is involved in the development of a product? Identify a Niche Consumer

What makes Effective Product Management Process? The Product: The steps involved in developing a product to eventually manage What is involved in the development of a product? Identify a Niche Consumer

Predictive Modeling and By-Peril Analysis for Homeowners Insurance

Predictive Modeling and By-Peril Analysis for Homeowners Insurance Contents Case for by-peril modeling By-peril model building Data Peril grouping Variables Interactions By-peril territories Model validation

Predictive Modeling and By-Peril Analysis for Homeowners Insurance Contents Case for by-peril modeling By-peril model building Data Peril grouping Variables Interactions By-peril territories Model validation

Predictive Modeling and Claims Analytics to Incorporate Leakage Analyses

Predictive and Analytics to Incorporate Leakage Analyses 2012 RPM March 21 2012 CAS antitrust notice The Casualty Actuarial Society (CAS) is committed to adhering strictly to the letter and spirit of the

Predictive and Analytics to Incorporate Leakage Analyses 2012 RPM March 21 2012 CAS antitrust notice The Casualty Actuarial Society (CAS) is committed to adhering strictly to the letter and spirit of the

Predictive Analytics: Achieving Greater Decision Accuracy, Better Risk Segmentation, and Greater Profitability

Predictive Analytics: Achieving Greater Decision Accuracy, Better Risk Segmentation, and Greater Profitability Lamont D. Boyd, CPCU, AIM Insurance Market Director FICO Scoring Solutions [email protected]

Predictive Analytics: Achieving Greater Decision Accuracy, Better Risk Segmentation, and Greater Profitability Lamont D. Boyd, CPCU, AIM Insurance Market Director FICO Scoring Solutions [email protected]

RPM Workshop 3: Basic Ratemaking

RPM Workshop 3: Basic Ratemaking Introduction to Ratemaking Relativities March 9, 2009 Mirage Hotel Las Vegas, NV Presented by: Chris Cooksey, FCAS, MAAA Nationwide Insurance Company Ain Milner, FCAS,

RPM Workshop 3: Basic Ratemaking Introduction to Ratemaking Relativities March 9, 2009 Mirage Hotel Las Vegas, NV Presented by: Chris Cooksey, FCAS, MAAA Nationwide Insurance Company Ain Milner, FCAS,

Credibility and Pooling Applications to Group Life and Group Disability Insurance

Credibility and Pooling Applications to Group Life and Group Disability Insurance Presented by Paul L. Correia Consulting Actuary [email protected] (207) 771-1204 May 20, 2014 What I plan to cover

Credibility and Pooling Applications to Group Life and Group Disability Insurance Presented by Paul L. Correia Consulting Actuary [email protected] (207) 771-1204 May 20, 2014 What I plan to cover

05/10/2015. Chapter 3 - Marketing Research. Marketing Project Plan

Chapter 3 - Marketing Research Copyright 2013 Pearson Canada Inc. Marketing Project Plan How do we begin the project? Identify product What do we need? We need to gather information We also need to do

Chapter 3 - Marketing Research Copyright 2013 Pearson Canada Inc. Marketing Project Plan How do we begin the project? Identify product What do we need? We need to gather information We also need to do

Understanding Captives and Alternative Risk Transfer

Understanding Captives and Alternative Risk Transfer Putting your insurance premiums to work for you Managing risk as you manage your bottom line What do Verizon, Coca-Cola, BP and most Fortune 500 sized

Understanding Captives and Alternative Risk Transfer Putting your insurance premiums to work for you Managing risk as you manage your bottom line What do Verizon, Coca-Cola, BP and most Fortune 500 sized

MapInfo Predictive Analytics Group

Welcome to the Science of Site Selection Online Seminar What s New at MapInfo: New Online Seminar: Predictive Analytics for Commercial Real Estate Developers, Leasing Agents, and Brokers Go to: http://mapinfoevents.webex.com

Welcome to the Science of Site Selection Online Seminar What s New at MapInfo: New Online Seminar: Predictive Analytics for Commercial Real Estate Developers, Leasing Agents, and Brokers Go to: http://mapinfoevents.webex.com

Direct Marketing of Insurance. Integration of Marketing, Pricing and Underwriting

Direct Marketing of Insurance Integration of Marketing, Pricing and Underwriting As insurers move to direct distribution and database marketing, new approaches to the business, integrating the marketing,

Direct Marketing of Insurance Integration of Marketing, Pricing and Underwriting As insurers move to direct distribution and database marketing, new approaches to the business, integrating the marketing,

Predictive Modeling in Workers Compensation 2008 CAS Ratemaking Seminar

Predictive Modeling in Workers Compensation 2008 CAS Ratemaking Seminar Prepared by Louise Francis, FCAS, MAAA Francis Analytics and Actuarial Data Mining, Inc. www.data-mines.com [email protected]

Predictive Modeling in Workers Compensation 2008 CAS Ratemaking Seminar Prepared by Louise Francis, FCAS, MAAA Francis Analytics and Actuarial Data Mining, Inc. www.data-mines.com [email protected]

Revising the ISO Commercial Auto Classification Plan. Anand Khare, FCAS, MAAA, CPCU

Revising the ISO Commercial Auto Classification Plan Anand Khare, FCAS, MAAA, CPCU 1 THE EXISTING PLAN 2 Context ISO Personal Lines Commercial Lines Property Homeowners, Dwelling Commercial Property, BOP,

Revising the ISO Commercial Auto Classification Plan Anand Khare, FCAS, MAAA, CPCU 1 THE EXISTING PLAN 2 Context ISO Personal Lines Commercial Lines Property Homeowners, Dwelling Commercial Property, BOP,

Workers Compensation Ratemaking An Overview

Workers Compensation Ratemaking An Overview Insurance Company Perspective Andrew Doll, QBE Regional Insurance Company CAS 2010 Ratemaking and Product Management Seminar Chicago, Illinois - March 16, 2010

Workers Compensation Ratemaking An Overview Insurance Company Perspective Andrew Doll, QBE Regional Insurance Company CAS 2010 Ratemaking and Product Management Seminar Chicago, Illinois - March 16, 2010

INSURANCE AGENTS APPLICATION FORM

INSURANCE AGENTS APPLICATION FORM Last Name First Name Title Mailing Address Town/City State Zip Phone E-mail Address Do you have a current professional liability policy in place? If, what is the Retro-active

INSURANCE AGENTS APPLICATION FORM Last Name First Name Title Mailing Address Town/City State Zip Phone E-mail Address Do you have a current professional liability policy in place? If, what is the Retro-active

Measuring per-mile risk for pay-as-youdrive automobile insurance. Eric Minikel CAS Ratemaking & Product Management Seminar March 20, 2012

Measuring per-mile risk for pay-as-youdrive automobile insurance Eric Minikel CAS Ratemaking & Product Management Seminar March 20, 2012 Professor Joseph Ferreira, Jr. and Eric Minikel Measuring per-mile

Measuring per-mile risk for pay-as-youdrive automobile insurance Eric Minikel CAS Ratemaking & Product Management Seminar March 20, 2012 Professor Joseph Ferreira, Jr. and Eric Minikel Measuring per-mile

Preparing for ORSA - Some practical issues Speaker:

2013 Seminar for the Appointed Actuary Colloque pour l actuaire désigné 2013 Session 13: Preparing for ORSA - Some practical issues Speaker: André Racine, Principal Eckler Ltd. Context of ORSA Agenda Place

2013 Seminar for the Appointed Actuary Colloque pour l actuaire désigné 2013 Session 13: Preparing for ORSA - Some practical issues Speaker: André Racine, Principal Eckler Ltd. Context of ORSA Agenda Place

Summary. January 2013»» white paper

white paper A New Perspective on Small Business Growth with Scoring Understanding Scoring s Complementary Role and Value in Supporting Small Business Financing Decisions January 2013»» Summary In the ongoing

white paper A New Perspective on Small Business Growth with Scoring Understanding Scoring s Complementary Role and Value in Supporting Small Business Financing Decisions January 2013»» Summary In the ongoing

Large Account Pricing

Workshop 5: Large Account Pricing Large Account Pricing Presenter: Joshua Taub, FCAS CAS Ratemaking and Product Management Seminar March 30, 2014 Washington, D.C. 1 / 34 CAS Antitrust Notice The Casualty

Workshop 5: Large Account Pricing Large Account Pricing Presenter: Joshua Taub, FCAS CAS Ratemaking and Product Management Seminar March 30, 2014 Washington, D.C. 1 / 34 CAS Antitrust Notice The Casualty

Utilizing Experian next generation decision management software to bring customer management to the next level of client experience and value creation

Utilizing Experian next generation decision management software to bring customer management to the next level of client experience and value creation Susan Duffy Scotiabank Robert Stone Experian Christopher

Utilizing Experian next generation decision management software to bring customer management to the next level of client experience and value creation Susan Duffy Scotiabank Robert Stone Experian Christopher

NSP 3 Referenced Material

NSP 3 Referenced Material Home Mortgage Disclosure Act Information (Foreclosure -- Response.org): 2009 Geographic Identifier CT #49 CT #51 CT #52 CT #53 CT #12 CT #5* CT #16* Omaha Median Value of First

NSP 3 Referenced Material Home Mortgage Disclosure Act Information (Foreclosure -- Response.org): 2009 Geographic Identifier CT #49 CT #51 CT #52 CT #53 CT #12 CT #5* CT #16* Omaha Median Value of First

PPC Marketing with Google AdWords

PPC Marketing with Google AdWords 1. Overview 1.1 What is PPC Marketing? PPC stands for Pay Per Click, which is one of the most popular paid search engine marketing programs. Google is the leader in search

PPC Marketing with Google AdWords 1. Overview 1.1 What is PPC Marketing? PPC stands for Pay Per Click, which is one of the most popular paid search engine marketing programs. Google is the leader in search

Predictive Modeling Techniques in Insurance

Predictive Modeling Techniques in Insurance Tuesday May 5, 2015 JF. Breton Application Engineer 2014 The MathWorks, Inc. 1 Opening Presenter: JF. Breton: 13 years of experience in predictive analytics

Predictive Modeling Techniques in Insurance Tuesday May 5, 2015 JF. Breton Application Engineer 2014 The MathWorks, Inc. 1 Opening Presenter: JF. Breton: 13 years of experience in predictive analytics

BEFORE THE INSURANCE COMMISSIONER OF THE STATE OF CALIFORNIA

CALIFORNIA DEPARTMENT OF INSURANCE LEGAL DIVISION Rate Enforcement Bureau Nikki S. McKennedy, Bar No. Fremont Street st Floor San Francisco CA Telephone: -- Facsimile: -0-0 Email: [email protected]

CALIFORNIA DEPARTMENT OF INSURANCE LEGAL DIVISION Rate Enforcement Bureau Nikki S. McKennedy, Bar No. Fremont Street st Floor San Francisco CA Telephone: -- Facsimile: -0-0 Email: [email protected]

Application for Claims-Made Professional Liability Insurance Coverage

Application for Claims-Made Professional Liability Insurance Coverage Your acceptance is subject to Underwriter s approval. All questions must be answered. Please attach additional sheets for comments

Application for Claims-Made Professional Liability Insurance Coverage Your acceptance is subject to Underwriter s approval. All questions must be answered. Please attach additional sheets for comments

GALLAGHER FOOD & AGRIBUSINESS. Risk Management Solutions

GALLAGHER FOOD & AGRIBUSINESS Risk Management Solutions We have the food and agribusiness expertise you need; from field to fork. The Food and Agribusiness industries are vital to the viability and sustenance

GALLAGHER FOOD & AGRIBUSINESS Risk Management Solutions We have the food and agribusiness expertise you need; from field to fork. The Food and Agribusiness industries are vital to the viability and sustenance

Delta Lloyds Insurance Company Homeowner Underwriting Guidelines For Mobile Homes

Delta Lloyds Insurance Company Homeowner Underwriting Guidelines For Mobile Homes As of November 15, 2012 Available Homeowner Program for Mobile Homes Delta Lloyds Insurance Company of Houston Texas provides

Delta Lloyds Insurance Company Homeowner Underwriting Guidelines For Mobile Homes As of November 15, 2012 Available Homeowner Program for Mobile Homes Delta Lloyds Insurance Company of Houston Texas provides

JAMAICA. Agricultural Insurance: Scope and Limitations for Weather Risk Management. Diego Arias Economist. 18 June 2009

JAMAICA Agricultural Insurance: Scope and Limitations for Weather Risk Management Diego Arias Economist 18 June 2009 Financed partly by the AAACP EU Support to the Caribbean Agenda The global market Products

JAMAICA Agricultural Insurance: Scope and Limitations for Weather Risk Management Diego Arias Economist 18 June 2009 Financed partly by the AAACP EU Support to the Caribbean Agenda The global market Products

Session1: Commercial Pricing & Rate Adequacy

08/08/2014 INSTITUTE OF ACTUARIES OF INDIA 5th Capacity Building Seminar in GI Session1: Commercial Pricing & Rate Adequacy Table of Contents 1. What is Commercial Insurance? 2. SME and Large Enterprises

08/08/2014 INSTITUTE OF ACTUARIES OF INDIA 5th Capacity Building Seminar in GI Session1: Commercial Pricing & Rate Adequacy Table of Contents 1. What is Commercial Insurance? 2. SME and Large Enterprises

The New NCCI Hazard Groups

The New NCCI Hazard Groups Greg Engl, PhD, FCAS, MAAA National Council on Compensation Insurance CAS Reinsurance Seminar June, 2006 Workers Compensation Session Agenda History of previous work Impact of

The New NCCI Hazard Groups Greg Engl, PhD, FCAS, MAAA National Council on Compensation Insurance CAS Reinsurance Seminar June, 2006 Workers Compensation Session Agenda History of previous work Impact of

The Role Actuaries Play in Mergers & Acquisitions

The Role Actuaries Play in Mergers & Acquisitions Gail Ross, FCAS, MAAA Principal & Consulting Actuary Milliman, Inc. [email protected] +1 609 452 6403 Due Diligence Issues Balance Sheet Operational

The Role Actuaries Play in Mergers & Acquisitions Gail Ross, FCAS, MAAA Principal & Consulting Actuary Milliman, Inc. [email protected] +1 609 452 6403 Due Diligence Issues Balance Sheet Operational

Private Passenger Automobile Insurance Coverages

Private Passenger Automobile Insurance Coverages An Actuarial Study of the Frequency and Cost of Claims for the State of Michigan by EPIC Consulting, LLC Principal Authors: Michael J. Miller, FCAS, MAAA

Private Passenger Automobile Insurance Coverages An Actuarial Study of the Frequency and Cost of Claims for the State of Michigan by EPIC Consulting, LLC Principal Authors: Michael J. Miller, FCAS, MAAA

The Relationship of Credit-Based Insurance Scores to Private Passenger Automobile Insurance Loss Propensity

The Relationship of Credit-Based Insurance Scores to Private Passenger Automobile Insurance Loss Propensity An Actuarial Study by EPIC Actuaries, LLC Principal Authors: Michael J. Miller, FCAS, MAAA Richard

The Relationship of Credit-Based Insurance Scores to Private Passenger Automobile Insurance Loss Propensity An Actuarial Study by EPIC Actuaries, LLC Principal Authors: Michael J. Miller, FCAS, MAAA Richard

Session 25 L, Introduction to General Insurance Ratemaking & Reserving: An Integrated Look. Moderator: W. Scott Lennox, FSA, FCAS, FCIA

Session 25 L, Introduction to General Insurance Ratemaking & Reserving: An Integrated Look Moderator: W. Scott Lennox, FSA, FCAS, FCIA Presenter: Houston Cheng, FCAS, FCIA Society of Actuaries 2013 Annual

Session 25 L, Introduction to General Insurance Ratemaking & Reserving: An Integrated Look Moderator: W. Scott Lennox, FSA, FCAS, FCIA Presenter: Houston Cheng, FCAS, FCIA Society of Actuaries 2013 Annual

Reserving for loyalty rewards programs Part I

Reserving for loyalty rewards programs Part I Rachel C. Dolsky, FCAS, MAAA Casualty loss reserving seminar Disclaimer The views expressed by the presenter are not necessarily those of EY or its member

Reserving for loyalty rewards programs Part I Rachel C. Dolsky, FCAS, MAAA Casualty loss reserving seminar Disclaimer The views expressed by the presenter are not necessarily those of EY or its member

Umbrella & Excess Liability - Understanding & Quantifying Price Movement

Umbrella & Excess Liability - Understanding & Quantifying Price Movement Survey of Common Umbrella Price Monitoring Methods Jason Kundrot CARe Seminar on Reinsurance, 1 Survey of Common Umbrella Price

Umbrella & Excess Liability - Understanding & Quantifying Price Movement Survey of Common Umbrella Price Monitoring Methods Jason Kundrot CARe Seminar on Reinsurance, 1 Survey of Common Umbrella Price

BIG DATA and Opportunities in the Life Insurance Industry

BIG DATA and Opportunities in the Life Insurance Industry Marc Sofer BSc FFA FIAA Head of Strategic Initiatives North Asia & India RGA Reinsurance Company BIG DATA I keep saying the sexy job in the next

BIG DATA and Opportunities in the Life Insurance Industry Marc Sofer BSc FFA FIAA Head of Strategic Initiatives North Asia & India RGA Reinsurance Company BIG DATA I keep saying the sexy job in the next

Objectives. 2- What types of loss potential are insurable and why? 3- How insurers protect against catastrophic loss through reinsurance?

INSURANCE 1 Objectives 1- What insurance is and how it works? 2- What types of loss potential are insurable and why? 3- How insurers protect against catastrophic loss through reinsurance? 4- What is meant

INSURANCE 1 Objectives 1- What insurance is and how it works? 2- What types of loss potential are insurable and why? 3- How insurers protect against catastrophic loss through reinsurance? 4- What is meant

3/21/2014. Designing a Commercial UBI Program. Disclaimer

Designing a Commercial UBI Program CAS Ratemaking and Product Management Seminar, March 31, 2014 Erin Bellott, FCAS, MAAA Disclaimer The views expressed in this presentation are solely those of the author

Designing a Commercial UBI Program CAS Ratemaking and Product Management Seminar, March 31, 2014 Erin Bellott, FCAS, MAAA Disclaimer The views expressed in this presentation are solely those of the author

HUD Real Estate Owned (REO) Loan Program Guide

Loan Program Guide") Table of Contents HUD Real Estate Owned (REO) Loan Program Guide Wholesale Lending January 9, 2014 Program Guide... 2 Pacific Union Financial Credit Philosophy... 2 Ability to Repay and Qualified Mortgages...

Table of Contents HUD Real Estate Owned (REO) Loan Program Guide Wholesale Lending January 9, 2014 Program Guide... 2 Pacific Union Financial Credit Philosophy... 2 Ability to Repay and Qualified Mortgages...

LISC Small Business Loan Fund

LISC Small Business Loan Fund P R E S E N T E D BY: K EN ROSENTHAL CDC S M A L L B U S I N E S S F I NA N C E Kevin Boes LISC N e w M a r ke t s S u p p o r t C o m p a ny LISC Small Business Loan Fund

LISC Small Business Loan Fund P R E S E N T E D BY: K EN ROSENTHAL CDC S M A L L B U S I N E S S F I NA N C E Kevin Boes LISC N e w M a r ke t s S u p p o r t C o m p a ny LISC Small Business Loan Fund

FASB / IASB Insurance Contracts Project Update Webinar

FASB / IASB Insurance Contracts Project Update Webinar November 1, 2012 International Accounting Standards Task Force Insurance Contracts Project Update 1 Presenters Noel Harewood, MAAA, FSA; Member, International

FASB / IASB Insurance Contracts Project Update Webinar November 1, 2012 International Accounting Standards Task Force Insurance Contracts Project Update 1 Presenters Noel Harewood, MAAA, FSA; Member, International

Regulatory Process for Reviewing Hurricane Models and use in Florida Rate Filings

Regulatory Process for Reviewing Hurricane Models and use in Florida Rate Filings Robert Lee, FCAS Florida Office of Insurance Regulation CAS IN FOCUS TAMING CATS OCTOBER 2012 1 Antitrust Notice The Casualty

Regulatory Process for Reviewing Hurricane Models and use in Florida Rate Filings Robert Lee, FCAS Florida Office of Insurance Regulation CAS IN FOCUS TAMING CATS OCTOBER 2012 1 Antitrust Notice The Casualty

Predictive modelling around the world 28.11.13

Predictive modelling around the world 28.11.13 Agenda Why this presentation is really interesting Introduction to predictive modelling Case studies Conclusions Why this presentation is really interesting

Predictive modelling around the world 28.11.13 Agenda Why this presentation is really interesting Introduction to predictive modelling Case studies Conclusions Why this presentation is really interesting

Modifying Insurance Rating Territories Via Clustering

Modifying Insurance Rating Territories Via Clustering Quncai Zou, New Jersey Manufacturers Insurance Company, West Trenton, NJ Ryan Diehl, New Jersey Manufacturers Insurance Company, West Trenton, NJ ABSTRACT

Modifying Insurance Rating Territories Via Clustering Quncai Zou, New Jersey Manufacturers Insurance Company, West Trenton, NJ Ryan Diehl, New Jersey Manufacturers Insurance Company, West Trenton, NJ ABSTRACT

Taking A Proactive Approach To Loyalty & Retention

THE STATE OF Customer Analytics Taking A Proactive Approach To Loyalty & Retention By Kerry Doyle An Exclusive Research Report UBM TechWeb research conducted an online study of 339 marketing professionals

THE STATE OF Customer Analytics Taking A Proactive Approach To Loyalty & Retention By Kerry Doyle An Exclusive Research Report UBM TechWeb research conducted an online study of 339 marketing professionals

Analysis of Internet Purchasing Behavior. October 3, 2011. Roosevelt Mosley, FCAS, MAAA Principal Pinnacle Actuarial Resources

Analysis of Internet Purchasing Behavior October 3, 2011 CAS In Focus Seminar Kevin Levitt Senior Vice President comscore, Inc. Roosevelt Mosley, FCAS, MAAA Principal Pinnacle Actuarial Resources Nick

Analysis of Internet Purchasing Behavior October 3, 2011 CAS In Focus Seminar Kevin Levitt Senior Vice President comscore, Inc. Roosevelt Mosley, FCAS, MAAA Principal Pinnacle Actuarial Resources Nick

Commercial Lines Program Summary: TOWER HILL PRIME

Commercial Lines Program Summary: TOWER HILL PRIME COMPANY BACKGROUND Founded in 1972, Tower Hill Insurance Group has become one of Florida's most trusted names in homeowners insurance and select commercial

Commercial Lines Program Summary: TOWER HILL PRIME COMPANY BACKGROUND Founded in 1972, Tower Hill Insurance Group has become one of Florida's most trusted names in homeowners insurance and select commercial

GABRIELE BRIDGES 8/9/2013-8/9/2014 1001006314 DP3 STANDARD. Date of Birth ***-**-**** Social Security Number SINGLE. Cell Phone

APPLICATION DETAIL Insured Effective-Expiration Date Policy Number Form Program GABRIELE BRIDGES 892013-892014 1001006314 DP3 STANDARD AGENCY INFORMATION Agency Number Agency Name Address City, State Zip

APPLICATION DETAIL Insured Effective-Expiration Date Policy Number Form Program GABRIELE BRIDGES 892013-892014 1001006314 DP3 STANDARD AGENCY INFORMATION Agency Number Agency Name Address City, State Zip

State of the Workers Compensation Market

State of the Workers Compensation Market Natasha Moore, FCAS, MAAA Practice Leader and Senior Actuary August 25, 2015 WCEC Orlando, Florida Copyright 2015 National Council on Compensation Insurance, Inc.

State of the Workers Compensation Market Natasha Moore, FCAS, MAAA Practice Leader and Senior Actuary August 25, 2015 WCEC Orlando, Florida Copyright 2015 National Council on Compensation Insurance, Inc.

How to Analyze Group Insurance Product Pricing and Underwriting. Stan Talbi SVP, U.S. Insurance Operations April 7, 2004

How to Analyze Group Insurance Product Pricing and Underwriting Stan Talbi SVP, U.S. Insurance Operations April 7, 2004 Group Group Insurance Product Offerings Rule #1: Know your Company s product offering

How to Analyze Group Insurance Product Pricing and Underwriting Stan Talbi SVP, U.S. Insurance Operations April 7, 2004 Group Group Insurance Product Offerings Rule #1: Know your Company s product offering

Processing FHA TOTAL and VA Mortgages

This reference contains information to help you process Federal Housing Administration (FHA) mortgages and Department of Veteran Affairs (VA) mortgages using Loan Prospector. Information on FHA TOTAL Mortgage

This reference contains information to help you process Federal Housing Administration (FHA) mortgages and Department of Veteran Affairs (VA) mortgages using Loan Prospector. Information on FHA TOTAL Mortgage

Leveraging ITV and Replacement Cost Tools in Structural Claims

Leveraging ITV and Replacement Cost Tools in Structural Claims Xactware User Conference 2011 Lynn Mora David Luse Agenda The value of insurance to value (ITV) in a claims environment Best practices for

Leveraging ITV and Replacement Cost Tools in Structural Claims Xactware User Conference 2011 Lynn Mora David Luse Agenda The value of insurance to value (ITV) in a claims environment Best practices for

2012 Minnesota Homeowners Report

2012 Minnesota Homeowners Report Minnesota Department of Commerce 2012 Homeowners Insurance Report Page 1 2012 Minnesota Homeowners Report The Minnesota Homeowners Report is completed annually by the Minnesota

2012 Minnesota Homeowners Report Minnesota Department of Commerce 2012 Homeowners Insurance Report Page 1 2012 Minnesota Homeowners Report The Minnesota Homeowners Report is completed annually by the Minnesota