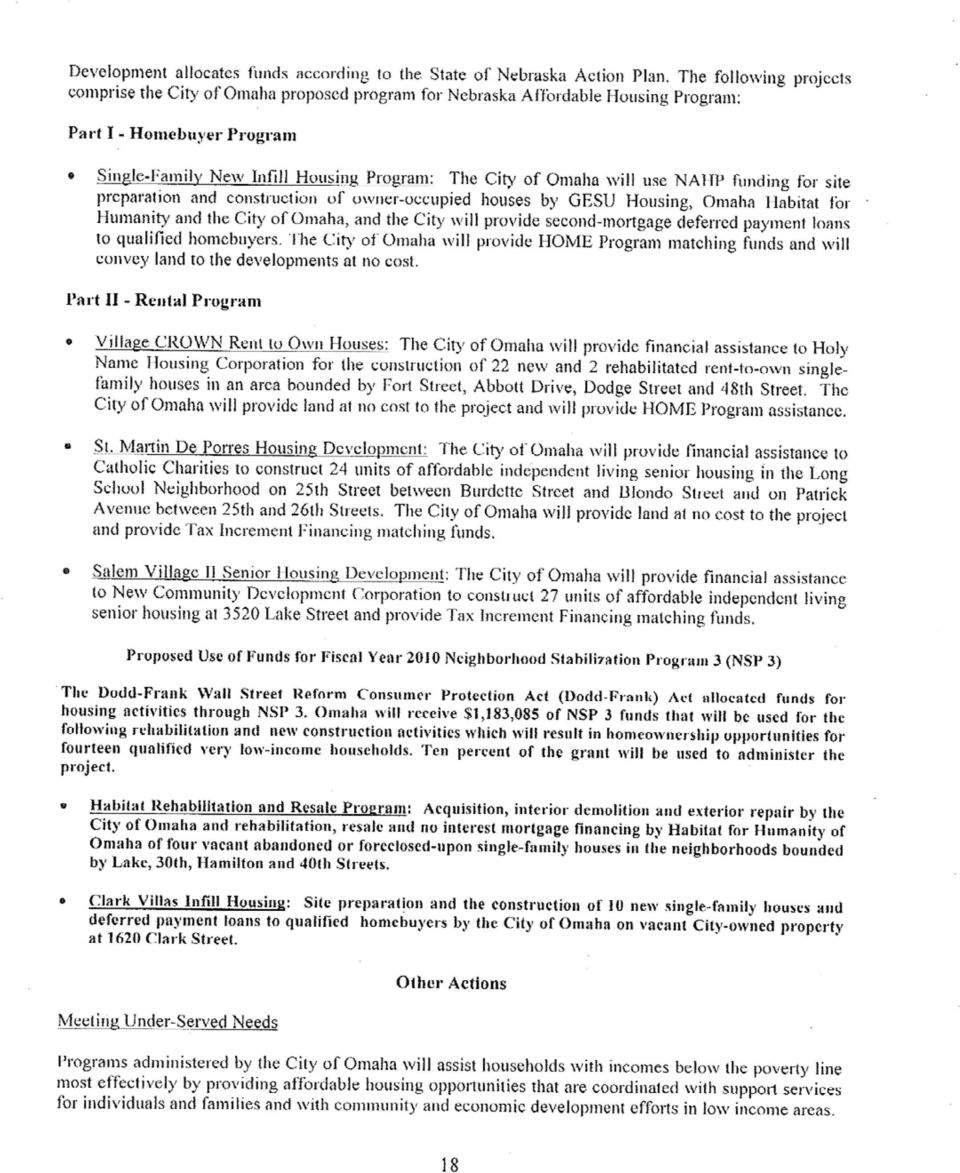

NSP 3 Referenced Material

|

|

|

- Flora Kennedy

- 9 years ago

- Views:

Transcription

1 NSP 3 Referenced Material Home Mortgage Disclosure Act Information (Foreclosure -- Response.org): 2009 Geographic Identifier CT #49 CT #51 CT #52 CT #53 CT #12 CT #5* CT #16* Omaha Median Value of First Lien Home Purchase Loans (1-4 Units), 2009 $92,500 $67,000 $8,500 $49,000 $79,500 $226,000 $109,000 $118,000 Number of First Lien Home Purchase Loans (1-4 Units), Number of First Lien Home Purchase Loans (1-4 Units), 2009, Per 1, Family Units Number of First Lien Investor Home Purchase Loans (1-4 Units), Number of First Lien Owner-Occupant Home Purchase Loans (1-4 Units), Percent of First Lien Home Purchase Loans (1-4 Units) that are Investors, Number of First Lien Investor Home Purchase Loans (1-4 Units), 2009, Per 1, Family Units Total Number of Housing Units, ,609 Total Number of 1-4 Family Housing Units, ,079 Number of High-Cost Home Purchase Loans (1-4 Units), ,259 Number of Home Purchase Loans (1-4 Units) with Interest Rate Info, ,666 Percent of Home Purchase Loans (1-4 Units) that are High-Cost, Number of High-Cost Home Purchase Loans, , Per 1, Family Units Number of High-Cost Home Purchase Loans, , Per 1,000 Total Housing Units Number of High-Cost Investor Home Purchase Loans (1-4 Units), Number of High-Cost Investor Home Purchase Loans, , Per 1, Family Units Number of High-Cost Refinance Loans (1-4 Units), ,524 Number of Refinance Loans (1-4 Units) with Interest Rate Info, ,130 Percent of Refinance Loans (1-4 Units) that are High-Cost, Number of High-Cost Refinance Loans, , Per 1, Family Units Number of High-Cost Refinance Loans, , Per 1,000 Total Housing Units

2 Home Mortgage Disclosure Act Information (Foreclosure -- Response.org): 2008 Geographic Identifier CT 4900 CT 5100 CT 5200 CT 5300 Ct 1200 CT5* CT16* Omaha Median Value of First Lien Home Purchase Loans (1-4 Units), 2008 $96,000 $75,000 $60,000 $57,000 $73,000 $203,000. $117,000 Number of First Lien Home Purchase Loans (1-4 Units), ,968 Number of First Lien Home Purchase Loans (1-4 Units), 2008, Per 1, Family Units Number of First Lien Investor Home Purchase Loans (1-4 Units), Number of First Lien Owner-Occupant Home Purchase Loans (1-4 Units), ,501 Percent of First Lien Home Purchase Loans (1-4 Units) that are Investors, Number of First Lien Investor Home Purchase Loans (1-4 Units), 2008, Per 1, Family Units Total Number of Housing Units, ,379 1, ,609 Total Number of 1-4 Family Housing Units, , ,079 Number of High-Cost Home Purchase Loans (1-4 Units), ,259 Number of Home Purchase Loans (1-4 Units) with Interest Rate Info, ,666 Percent of Home Purchase Loans (1-4 Units) that are High-Cost, Number of High-Cost Home Purchase Loans, , Per 1, Family Units Number of High-Cost Home Purchase Loans, , Per 1,000 Total Housing Units Number of High-Cost Investor Home Purchase Loans (1-4 Units), Number of High-Cost Investor Home Purchase Loans, , Per 1, Family Units Number of High-Cost Refinance Loans (1-4 Units), ,524 Number of Refinance Loans (1-4 Units) with Interest Rate Info, ,130 Percent of Refinance Loans (1-4 Units) that are High-Cost, Number of High-Cost Refinance Loans, , Per 1, Family Units Number of High-Cost Refinance Loans, , Per 1,000 Total Housing Units Market Strength and Foreclosure Risk Matrix and NSP 3 Need Score Data (Foreclosure.org): September 2010 CT #49 CT #51 CT #52 CT #53 CT #12 CT #5* CT #16* Risk Decile HMI Decile NSP 3 Need Score NSP 3 Minimum Score NSP 3 Eligibility? No Yes Yes Yes Yes No No The two indices were developed by the Local Initiatives Support Corporation (LISC). They make use of the most recent nationally available data that is pertinent to the issue. Index values are presented for all census tracts in U.S. metropolitan areas. Values for census tracts are calculated relative to the metropolitan area in which they are located. You can access all of the data for your metropolitan area, and a description of the source data and methodology, directly on this site. In each case, several separate measures were woven together statistically to form the index. (for further explanation go to the PDF document entitled Setting Priorities for Neighborhood Stabilization: A Guide to Using Foreclosure Response. Org Indexes at:

3 Housing and Economic Indicators: 2005 to 2009 American Community Estimates (and 2000 Census where noted) CT #49 CT #51 CT #52 CT #53 CT #12 CT #5* CT #16* Omaha Owner -occupied units ,591 Renter -occupied units 1, ,471 Owner-occupied in percent 32.0% 37.2% 29.8% 39.0% 41.0% 46.9% 0.0% 60.9% For sale only Sold, not occupied Owner-Occupied Homeowner Vacancy Rate 4.4% 0.0% 4.3% 1.8% 0.0% 21.8% 100.0% 2.4% O-occ. median hsng value, 2000 Census $71,000 $50,100 $33,400 $37,900 $51,800 $24,800 $100,001 $93,300 O-occ. median value, ACS Est. $106,900 $77,900 $71,400 $63,000 $73,200 $78,200 NA 131,500 % Change from 2000 to % 55.5% 113.8% 66.2% 41.3% 215.3% NA 40.9% Median HH. Income, 2000 Census $28,213 $24,651 $17,667 $21,290 $22,715 $20,924 $7,833 $40,006 Median HH. Income, ACS Est. $27,900 $32,063 $20,170 $19,139 $30,589 $36,397 $3,889 $47,184 % Change from 2000 to % 30.1% 14.2% -10.1% 34.7% 73.9% -50.4% 17.9% Unemployment Rate 4.9% 10.5% 32.3% 31.0% 15.8% 3.9% 0.5% 6.6% * Nearby census tract only, does not contain part of targeted area. Homeowner Vacancy Rate The homeowner vacancy rate is the proportion of the homeowner inventory that is vacant for sale. It is computed by dividing the number of vacant units for sale only by the sum of the owner-occupied units, vacant units that are for sale only, and vacant units that have been sold but not yet occupied, and then multiplying by 100. Demographics and Housing: 2000 Census Clark Villas Target Area Habitat Rehab. Resale Target Area Omaha # % # % # % Population and Ethnicity Total: 659 3, ,007 One Race % 3, % 382, % White % % 305, % African American % 2, % 51, % Native American 8 1.2% % 2, % Asian 6 0.9% % 6, %

4 Clark Villas Target Area Habitat Rehab. Resale Target Area Omaha # % # % # % Native Hawaiian and Other Pacific Islander 0 0.0% 0 0.0% % Some other race % % 15, % Two Races % % 7, % Hispanic % % 29, % Age Under % % 28, % 5 to % % 71, % 18 to % % 23, % 22 to % % 51, % 30 to % % 58, % 40 to % % 57, % 50 to % % 53, % 65 to Up % % 46, % Households Total 229 1, ,738 Family % % 94, % Housing Total Units Units 240 1, ,731 Vacant % % 8, % Tenure Owner-Occupied % % 93, % Renter-Occupied % % 63, % Clark Villas Target Area Habitat Rehab. Resale Target Area Area Total Acres Housing Density (2007 housing unit estimate)

5 MAP 1

6 Public Hearing Notice

7 Summary of Plan Amendment and start of Citizen Comment Period Notice

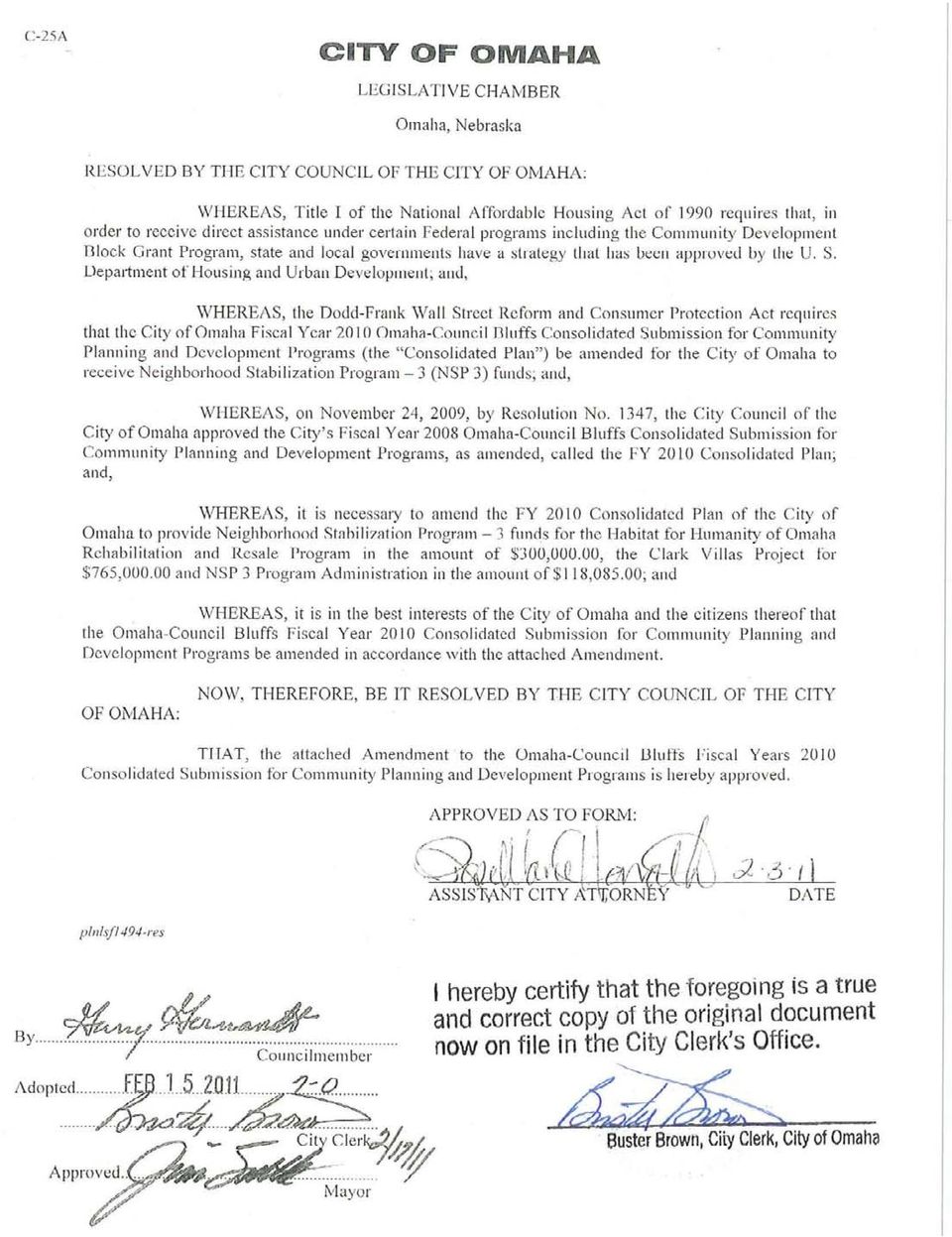

8 City of Omaha Approved Council Resolution

9

10

11

12

13

14

15

16

17

18

19

Moving Beyond the Gap

Moving Beyond the Gap Racial Disparities in September 2014 Central Corridor St. Paul Hopkins Blake Rd Corridor Eastside St. Paul South Minneapolis September 2014 Overview This report is part of a larger

Moving Beyond the Gap Racial Disparities in September 2014 Central Corridor St. Paul Hopkins Blake Rd Corridor Eastside St. Paul South Minneapolis September 2014 Overview This report is part of a larger

CONGRESSIONAL DISTRICT REPORT For the 113th Congress. California District 47. Representative Alan Lowenthal (D)

") CONGRESSIONAL DISTRICT REPORT For the 113th Congress District 47 Representative Alan Lowenthal (D) National Association of REALTORS 500 New Jersey Avenue, NW Washington, D.C. Congressional Districts 113th

CONGRESSIONAL DISTRICT REPORT For the 113th Congress District 47 Representative Alan Lowenthal (D) National Association of REALTORS 500 New Jersey Avenue, NW Washington, D.C. Congressional Districts 113th

U.S. Census Bureau News

U.S. Census Bureau News Robert R. Callis Melissa Kresin Social, Economic and Housing Statistics Division (301) 763-3199 U.S. Department of Commerce Washington, D.C. 20233 For Immediate Release Thursday,

U.S. Census Bureau News Robert R. Callis Melissa Kresin Social, Economic and Housing Statistics Division (301) 763-3199 U.S. Department of Commerce Washington, D.C. 20233 For Immediate Release Thursday,

Comparison Profile prepared by the New Mexico Economic Development Department State Data Center. Page 1 of 5

Comparing New Mexico to Colorado DEMOGRAPHICS Colorado New Mexico Population estimates, July 1, 2014 5,355,866 2,085,572 Population, percent change - April 1, 2010 to July 1, 2014 1.4% 1.4% Population

Comparing New Mexico to Colorado DEMOGRAPHICS Colorado New Mexico Population estimates, July 1, 2014 5,355,866 2,085,572 Population, percent change - April 1, 2010 to July 1, 2014 1.4% 1.4% Population

Selected Socio-Economic Data. Baker County, Florida

Selected Socio-Economic Data African American and White, Not Hispanic www.fairvote2020.org www.fairdata2000.com 5-Feb-12 C03002. HISPANIC OR LATINO ORIGIN BY RACE - Universe: TOTAL POPULATION Population

Selected Socio-Economic Data African American and White, Not Hispanic www.fairvote2020.org www.fairdata2000.com 5-Feb-12 C03002. HISPANIC OR LATINO ORIGIN BY RACE - Universe: TOTAL POPULATION Population

New Mexico. Comparison Profile prepared by the New Mexico Economic Development Department State Data Center. Page 1 of 5

DEMOGRAPHICS Population estimates, July 1, 2014 2,085,572 Population, percent change - April 1, 2010 to July 1, 2014 1.4% Population estimates, July 1, 2013 2,085,287 Population, percent change - April

DEMOGRAPHICS Population estimates, July 1, 2014 2,085,572 Population, percent change - April 1, 2010 to July 1, 2014 1.4% Population estimates, July 1, 2013 2,085,287 Population, percent change - April

PUBLIC DISCLOSURE. February 3, 2011 MORTGAGE LENDER COMMUNITY INVESTMENT PERFORMANCE EVALUATION IFREEDOM DIRECT CORPORATION ML3122

PUBLIC DISCLOSURE February 3, 2011 MORTGAGE LENDER COMMUNITY INVESTMENT PERFORMANCE EVALUATION IFREEDOM DIRECT CORPORATION ML3122 2363 SOUTH FOOTHILL DRIVE SALT LAKE CITY, UTAH 84109 DIVISION OF BANKS

PUBLIC DISCLOSURE February 3, 2011 MORTGAGE LENDER COMMUNITY INVESTMENT PERFORMANCE EVALUATION IFREEDOM DIRECT CORPORATION ML3122 2363 SOUTH FOOTHILL DRIVE SALT LAKE CITY, UTAH 84109 DIVISION OF BANKS

Who Could Afford to Buy a Home in 2009? Affordability of Buying a Home in the United States

Who Could Afford to Buy a Home in 200? Affordability of Buying a Home in the United States Current Housing Reports Ellen Wilson and Robert R. Callis Issued May 203 H2/3-02 IntroductIon This is the seventh

Who Could Afford to Buy a Home in 200? Affordability of Buying a Home in the United States Current Housing Reports Ellen Wilson and Robert R. Callis Issued May 203 H2/3-02 IntroductIon This is the seventh

HEALTH INSURANCE COVERAGE STATUS. 2009-2013 American Community Survey 5-Year Estimates

S2701 HEALTH INSURANCE COVERAGE STATUS 2009-2013 American Community Survey 5-Year Estimates Supporting documentation on code lists, subject definitions, data accuracy, and statistical testing can be found

S2701 HEALTH INSURANCE COVERAGE STATUS 2009-2013 American Community Survey 5-Year Estimates Supporting documentation on code lists, subject definitions, data accuracy, and statistical testing can be found

The goal is to transform data into information, and information into insight. Carly Fiorina

DEMOGRAPHICS & DATA The goal is to transform data into information, and information into insight. Carly Fiorina 11 MILWAUKEE CITYWIDE POLICY PLAN This chapter presents data and trends in the city s population

DEMOGRAPHICS & DATA The goal is to transform data into information, and information into insight. Carly Fiorina 11 MILWAUKEE CITYWIDE POLICY PLAN This chapter presents data and trends in the city s population

A Geographic Profile of. Chicago Lawn, Gage Park, West Elsdon and West Lawn. Neighborhoods Served by. The Southwest Organizing Project

A Geographic Profile of Chicago Lawn, Gage Park, West Elsdon and West Lawn Neighborhoods Served by The Southwest Organizing Project The Southwest Organizing Project (SWOP) is a broad based community organization

A Geographic Profile of Chicago Lawn, Gage Park, West Elsdon and West Lawn Neighborhoods Served by The Southwest Organizing Project The Southwest Organizing Project (SWOP) is a broad based community organization

ZIP PLUS 4 Centroid/Census to Block Group Geographic Conversion File AND EASI ZIP4 Updated Demographic Files

ZIP PLUS 4 Centroid/Census to Block Group Geographic Conversion File AND EASI ZIP4 Updated Demographic Files Introduction Easy Analytic Software, Inc. (EASI) is a New York-based independent developer and

ZIP PLUS 4 Centroid/Census to Block Group Geographic Conversion File AND EASI ZIP4 Updated Demographic Files Introduction Easy Analytic Software, Inc. (EASI) is a New York-based independent developer and

Making Home Affordable Program Request For Mortgage Assistance (RMA)

") Making Home Affordable Program Request For Mortgage Assistance (RMA) REQUEST FOR MORTGAGE ASSISTANCE (RMA) page 1 Loan I.D. Number Servicer Borrower s name BORROWER Co-borrower s name CO-BORROWER Social

Making Home Affordable Program Request For Mortgage Assistance (RMA) REQUEST FOR MORTGAGE ASSISTANCE (RMA) page 1 Loan I.D. Number Servicer Borrower s name BORROWER Co-borrower s name CO-BORROWER Social

PUBLIC DISCLOSURE FEBRUARY 12, 2015 MORTGAGE LENDER COMMUNITY INVESTMENT PERFORMANCE EVALUATION NE MOVES MORTGAGE, LLC MC2584

PUBLIC DISCLOSURE FEBRUARY 12, 2015 MORTGAGE LENDER COMMUNITY INVESTMENT PERFORMANCE EVALUATION NE MOVES MORTGAGE, LLC MC2584 52 SECOND AVENUE, 3RD FLOOR WALTHAM MA. 02451 DIVISION OF BANKS 1000 WASHINGTON

PUBLIC DISCLOSURE FEBRUARY 12, 2015 MORTGAGE LENDER COMMUNITY INVESTMENT PERFORMANCE EVALUATION NE MOVES MORTGAGE, LLC MC2584 52 SECOND AVENUE, 3RD FLOOR WALTHAM MA. 02451 DIVISION OF BANKS 1000 WASHINGTON

Logan City. Analysis of Impediments to Fair Housing

Logan City Analysis of Impediments to Fair Housing 2009-13 Consolidated Plan Page 36 of 92 EXECUTIVE SUMMARY Analysis of Impediments The Analysis of Impediments (AI) is a comprehensive review of a jurisdiction

Logan City Analysis of Impediments to Fair Housing 2009-13 Consolidated Plan Page 36 of 92 EXECUTIVE SUMMARY Analysis of Impediments The Analysis of Impediments (AI) is a comprehensive review of a jurisdiction

County Demographics, Economy & Housing Market

County Demographics, Economy & Housing Market County Demographics Palm Beach County is Florida's third most populous county with 7% of Florida's population. The county's total estimated population for

County Demographics, Economy & Housing Market County Demographics Palm Beach County is Florida's third most populous county with 7% of Florida's population. The county's total estimated population for

Total Males Females 34.4 36.7 (0.4) 12.7 17.5 (1.6) Didn't believe entitled or eligible 13.0 (0.3) Did not know how to apply for benefits 3.4 (0.

12.7 17.5 (1.6) Didn't believe entitled or eligible 13.0 (0.3) Did not know how to apply for benefits 3.4 (0.") 2001 National Survey of Veterans (NSV) - March, 2003 - Page 413 Table 7-10. Percent Distribution of Veterans by Reasons Veterans Don't Have VA Life Insurance and Gender Males Females Not Applicable 3,400,423

2001 National Survey of Veterans (NSV) - March, 2003 - Page 413 Table 7-10. Percent Distribution of Veterans by Reasons Veterans Don't Have VA Life Insurance and Gender Males Females Not Applicable 3,400,423

SELECTED SOCIAL CHARACTERISTICS IN THE UNITED STATES. 2012 American Community Survey 1-Year Estimates

DP02 SELECTED SOCIAL CHARACTERISTICS IN THE UNITED STATES 2012 American Community Survey 1-Year Estimates Supporting documentation on code lists, subject definitions, data accuracy, and statistical testing

DP02 SELECTED SOCIAL CHARACTERISTICS IN THE UNITED STATES 2012 American Community Survey 1-Year Estimates Supporting documentation on code lists, subject definitions, data accuracy, and statistical testing

How To Build A Home In A Neighborhood Of A Large Size

Action Plan Grantee: Grant: Worcester, MA B-08-MN-25-0004 Grant Amount: $ 2,390,858.00 Status: Reviewed and Approved Funding Sources No Funding Sources Found Narratives Areas of Greatest Need: The City

Action Plan Grantee: Grant: Worcester, MA B-08-MN-25-0004 Grant Amount: $ 2,390,858.00 Status: Reviewed and Approved Funding Sources No Funding Sources Found Narratives Areas of Greatest Need: The City

58% 61% 17% 24% 12% 20% PROFILE. ASSetS & opportunity ProfILe: NewArk. key HIgHLIgHtS ABOUT THE PROFILE ASSETS & OPPORTUNITY

ASSetS & opportunity ProfILe: NewArk ASSETS & OPPORTUNITY PROFILE key HIgHLIgHtS 58% of Newark residents live in asset poverty Cities have long been thought of as places of opportunity for low-income workers

ASSetS & opportunity ProfILe: NewArk ASSETS & OPPORTUNITY PROFILE key HIgHLIgHtS 58% of Newark residents live in asset poverty Cities have long been thought of as places of opportunity for low-income workers

PUBLIC DISCLOSURE. June 2, 2014 CRA FOR MORTGAGE LENDERS PERFORMANCE EVALUATION RADIUS FINANCIAL GROUP INC. ML1846

PUBLIC DISCLOSURE June 2, 2014 CRA FOR MORTGAGE LENDERS PERFORMANCE EVALUATION RADIUS FINANCIAL GROUP INC. ML1846 600 LONGWATER DRIVE SUITE 107 NORWELL, MA 02061 DIVISION OF BANKS 1000 WASHINGTON STREET

PUBLIC DISCLOSURE June 2, 2014 CRA FOR MORTGAGE LENDERS PERFORMANCE EVALUATION RADIUS FINANCIAL GROUP INC. ML1846 600 LONGWATER DRIVE SUITE 107 NORWELL, MA 02061 DIVISION OF BANKS 1000 WASHINGTON STREET

HOMEBUYER S ASSISTANCE PROGRAM (HAP) APPLICATION PROCESS

APPLICATION PROCESS") HOMEBUYER S ASSISTANCE PROGRAM (HAP) APPLICATION PROCESS 1. Prospective homebuyer (Participant) should contact the City of Modesto (Community and Economic Development Department) at (209) 577-5211 to determine

HOMEBUYER S ASSISTANCE PROGRAM (HAP) APPLICATION PROCESS 1. Prospective homebuyer (Participant) should contact the City of Modesto (Community and Economic Development Department) at (209) 577-5211 to determine

Milwaukee s Housing Crisis: Housing Affordability and Mortgage Lending Practices

Milwaukee s Housing Crisis: Housing Affordability and Mortgage Lending Practices by John Pawasarat and Lois M. Quinn, Employment and Training Institute, University of Wisconsin-Milwaukee, 2007 This report

Milwaukee s Housing Crisis: Housing Affordability and Mortgage Lending Practices by John Pawasarat and Lois M. Quinn, Employment and Training Institute, University of Wisconsin-Milwaukee, 2007 This report

Gloversville Community Development Agency. CDBG Housing Rehabilitation Program

Version 10/29/14 Gloversville Community Development Agency CDBG Housing Rehabilitation Program THE PROGRAM ELIGIBLE IMPROVEMENTS The Gloversville Community Development Agency is operating a housing rehabilitation

Version 10/29/14 Gloversville Community Development Agency CDBG Housing Rehabilitation Program THE PROGRAM ELIGIBLE IMPROVEMENTS The Gloversville Community Development Agency is operating a housing rehabilitation

Spotlight on the Housing Market in the Orlando-Kissimmee-Sanford, FL MSA

Spotlight on in Orlando-Kissimmee-Sanford, FL MSA The Orlando-Kissimmee-Sanford, FL Metropolitan Statistical Area (Orlando MSA) is located in central Florida and includes four counties: Lake, Orange, Osceola,

Spotlight on in Orlando-Kissimmee-Sanford, FL MSA The Orlando-Kissimmee-Sanford, FL Metropolitan Statistical Area (Orlando MSA) is located in central Florida and includes four counties: Lake, Orange, Osceola,

Cotuit Meadows Cotuit, MA 3-Bedroom, 2-Bath Single Family Homes $189,000

Cotuit Meadows Cotuit, MA 3-Bedroom, 2-Bath Single Family Homes $189,000 Cotuit Meadows is a 124-home development built on 50 acres of land located off Falmouth Road (Route 28) at the Barnstable-Mashpee

Cotuit Meadows Cotuit, MA 3-Bedroom, 2-Bath Single Family Homes $189,000 Cotuit Meadows is a 124-home development built on 50 acres of land located off Falmouth Road (Route 28) at the Barnstable-Mashpee

The Home Mortgage Disclosure Act History, Evolution, and Limitations Joseph M. Kolar Buckley Kolar LLP March 14, 2005 Washington, DC History of HMDA Enacted 30 years ago, HMDA s purposes and requirements

The Home Mortgage Disclosure Act History, Evolution, and Limitations Joseph M. Kolar Buckley Kolar LLP March 14, 2005 Washington, DC History of HMDA Enacted 30 years ago, HMDA s purposes and requirements

Metro Interfaith Housing Counseling. Tell Us About Yourself. General Information Primary

Metro Interfaith Housing Counseling 21 New St, Binghamton, NY 13903 Phone: 607.723.0582 Fax: 607.722.8912 Tell Us About Yourself Print clearly. Use additional sheets if necessary. Information provided

Metro Interfaith Housing Counseling 21 New St, Binghamton, NY 13903 Phone: 607.723.0582 Fax: 607.722.8912 Tell Us About Yourself Print clearly. Use additional sheets if necessary. Information provided

HARRIS COUNTY, TEXAS NEIGHBORHOOD STABILIZATION PROGRAM

HARRIS COUNTY, TEXAS NEIGHBORHOOD STABILIZATION PROGRAM SUBSTANTIAL AMENDMENT TO THE 2008-2012 CONSOLIDATED PLAN FY 2008 ANNUAL ACTION PLAN AMENDMENT APPLICATION Prepared by the Community Services Department

HARRIS COUNTY, TEXAS NEIGHBORHOOD STABILIZATION PROGRAM SUBSTANTIAL AMENDMENT TO THE 2008-2012 CONSOLIDATED PLAN FY 2008 ANNUAL ACTION PLAN AMENDMENT APPLICATION Prepared by the Community Services Department

Assistance for the Redevelopment of Abandoned and Foreclosed Properties City of Atlanta, Georgia

Community Development Block Grant Neighborhood Stabilization Program Title III, Section 2301 of the Housing and Economic Recovery Act of 2008 (HR 3221) Assistance for the Redevelopment of Abandoned and

Community Development Block Grant Neighborhood Stabilization Program Title III, Section 2301 of the Housing and Economic Recovery Act of 2008 (HR 3221) Assistance for the Redevelopment of Abandoned and

APPENDIX B LINCOLN HIGHWAY/ROUTE 31 CORRIDOR TAX INCREMENT FINANCING DISTRICT HOUSING IMPACT STUDY

APPENDIX B LINCOLN HIGHWAY/ROUTE 31 CORRIDOR TAX INCREMENT FINANCING DISTRICT HOUSING IMPACT STUDY Village of North Aurora, Illinois May, 2009 DRAFT Prepared by: Teska Associates, Inc. TABLE OF CONTENTS

APPENDIX B LINCOLN HIGHWAY/ROUTE 31 CORRIDOR TAX INCREMENT FINANCING DISTRICT HOUSING IMPACT STUDY Village of North Aurora, Illinois May, 2009 DRAFT Prepared by: Teska Associates, Inc. TABLE OF CONTENTS

ReNew Grant Guidelines

Brooklyn Center ReNew Buyer Incentive Program Greater Metropolitan Housing Corporation Program Summary The Economic Development Authority (EDA) of Brooklyn Center, Minnesota (EDA) has partnered with the

Brooklyn Center ReNew Buyer Incentive Program Greater Metropolitan Housing Corporation Program Summary The Economic Development Authority (EDA) of Brooklyn Center, Minnesota (EDA) has partnered with the

Neighborhoods & Housing

Chapter 6 Neighborhoods & Housing Introduction A major goal of this plan is to improve the livability of the City s neighborhoods. For existing neighborhoods, this may be achieved through conservation,

Chapter 6 Neighborhoods & Housing Introduction A major goal of this plan is to improve the livability of the City s neighborhoods. For existing neighborhoods, this may be achieved through conservation,

City of Madison 2010-2014 3-5 Year Strategic Plan

City of Madison 2010-2014 3-5 Year Strategic Plan This document includes Narrative Responses to specific questions that grantees of the Community Development Block Grant, HOME Investment Partnership, Housing

City of Madison 2010-2014 3-5 Year Strategic Plan This document includes Narrative Responses to specific questions that grantees of the Community Development Block Grant, HOME Investment Partnership, Housing

MORTGAGE PRE-APPROVAL

MORTGAGE PRE-APPROVAL THE FIRST STEP TO OWNING YOUR OWN HOME Welcome Before you start looking for a home, arm yourself with the knowledge of what you can afford to spend and borrow by obtaining a mortgage

MORTGAGE PRE-APPROVAL THE FIRST STEP TO OWNING YOUR OWN HOME Welcome Before you start looking for a home, arm yourself with the knowledge of what you can afford to spend and borrow by obtaining a mortgage

EASI Reseller Opportunities: Demographic Estimates and Forecasts; Life Stage Clusters; Major Merchandise Lines and Minor Store Groups

EASI Reseller Opportunities: Demographic Estimates and Forecasts; Life Stage Clusters; Major Merchandise Lines and Minor Store Groups Introduction Easy Analytic Software, Inc. (EASI) is a New York-based

EASI Reseller Opportunities: Demographic Estimates and Forecasts; Life Stage Clusters; Major Merchandise Lines and Minor Store Groups Introduction Easy Analytic Software, Inc. (EASI) is a New York-based

Demographic and Labor Market Profile of the city of Detroit - Michigan

Demographic and Labor Market Profile of the city of Detroit - Michigan Leonidas Murembya, PhD Regional Coordinator [email protected] www.michigan.gov/lmi 517-241-6574 State of Michigan Department

Demographic and Labor Market Profile of the city of Detroit - Michigan Leonidas Murembya, PhD Regional Coordinator [email protected] www.michigan.gov/lmi 517-241-6574 State of Michigan Department

Loss Mitigation Pre-Foreclosure Sale Request Instructions & Disclosures

Loss Mitigation Pre-Foreclosure Sale Request Instructions & Disclosures Member Name: Loan Number: If you have received a valid, reasonable, offer to purchase your home prior to a foreclosure and you would

Loss Mitigation Pre-Foreclosure Sale Request Instructions & Disclosures Member Name: Loan Number: If you have received a valid, reasonable, offer to purchase your home prior to a foreclosure and you would

PUBLIC DISCLOSURE. March 02, 2009 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION. First National Bank of Michigan Charter Number 24637

O SMALL BANK Comptroller of the Currency Administrator of National Banks Washington, DC 20219 PUBLIC DISCLOSURE March 02, 2009 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION First National Bank of Michigan

O SMALL BANK Comptroller of the Currency Administrator of National Banks Washington, DC 20219 PUBLIC DISCLOSURE March 02, 2009 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION First National Bank of Michigan

Uniform Residential Loan Application Washington Federal Savings

Uniform Residential Loan Application Washington Federal Savings This application is designed to be completed by the Applicant(s) with the Lender's assistance. Applicants should complete this form as "Borrower"

Uniform Residential Loan Application Washington Federal Savings This application is designed to be completed by the Applicant(s) with the Lender's assistance. Applicants should complete this form as "Borrower"

Small Business Administration Loan Application

BUSINESS INFORMATION Small Business Administration Loan Application Business Name Structure (Corporation, Partnership, Sole P., LLC) Address Type of Business City, State, Zip No. of Employees: Before After

BUSINESS INFORMATION Small Business Administration Loan Application Business Name Structure (Corporation, Partnership, Sole P., LLC) Address Type of Business City, State, Zip No. of Employees: Before After

2000 SF1 Census Data - Quick Reference Table

2000 SF1 Census Data - Quick Reference Table This reference table lists the most common census variables in SF1 for the 2000 Census. It was created to help users identify specific variables within the

2000 SF1 Census Data - Quick Reference Table This reference table lists the most common census variables in SF1 for the 2000 Census. It was created to help users identify specific variables within the

Near Eastside Neighborhood Indianapolis, IN

LISC Sustainable Communities Initiative Neighborhood Quality Monitoring Report Neighborhood Indianapolis, IN Baseline Report: May 2011 Original Version: September 2010 Revisions: April 2014 Neighborhood

LISC Sustainable Communities Initiative Neighborhood Quality Monitoring Report Neighborhood Indianapolis, IN Baseline Report: May 2011 Original Version: September 2010 Revisions: April 2014 Neighborhood

Residential Loan Application for Reverse Mortgages

Residential Loan Application for Reverse Mortgages This application is designed to be completed by the applicant(s) with the lender s assistance. Applicants should complete this form as Borrower or Co-Borrower,

Residential Loan Application for Reverse Mortgages This application is designed to be completed by the applicant(s) with the lender s assistance. Applicants should complete this form as Borrower or Co-Borrower,

Application for Free Home Repairs

Application for Free Home Repairs Name of Homeowner: Date of Birth: Gender Male Female Is this a female headed household? Is this a grandparent headed household? Street Address: City: County: Zip Marital

Application for Free Home Repairs Name of Homeowner: Date of Birth: Gender Male Female Is this a female headed household? Is this a grandparent headed household? Street Address: City: County: Zip Marital

City of Beaumont Owner-Occupied Housing Rehabilitation Program. Application Process

City of Beaumont Owner-Occupied Housing Rehabilitation Program Application Process Welcome The City of Beaumont s Owner-Occupied Housing Rehabilitation Program Assistance is available to homeowners who

City of Beaumont Owner-Occupied Housing Rehabilitation Program Application Process Welcome The City of Beaumont s Owner-Occupied Housing Rehabilitation Program Assistance is available to homeowners who

SOMERSET DISASTER RECOVERY APPLICATION FOR HOMEOWNER ASSISTANCE

SOMERSET DISASTER RECOVERY APPLICATION FOR HOMEOWNER ASSISTANCE Application # Applicant Name: Co-Applicant Name: Property Address: City: Zip Code: Home Phone: Work Phone: Cell Phone: Section 1 - Property

SOMERSET DISASTER RECOVERY APPLICATION FOR HOMEOWNER ASSISTANCE Application # Applicant Name: Co-Applicant Name: Property Address: City: Zip Code: Home Phone: Work Phone: Cell Phone: Section 1 - Property

DENVER URBAN RENEWAL AUTHORITY HOUSING PROGRAMS SINGLE FAMILY REHABILITATION PROGRAM

DENVER URBAN RENEWAL AUTHORITY HOUSING PROGRAMS SPONSORED BY THE CITY AND COUNTY OF DENVER S DEPARTMENT OF HOUSING & NEIGHBORHOOD DEVELOPMENT SERVICES PROGRAM SINGLE FAMILY REHABILITATION PROGRAM The Single

DENVER URBAN RENEWAL AUTHORITY HOUSING PROGRAMS SPONSORED BY THE CITY AND COUNTY OF DENVER S DEPARTMENT OF HOUSING & NEIGHBORHOOD DEVELOPMENT SERVICES PROGRAM SINGLE FAMILY REHABILITATION PROGRAM The Single

2014 HOUSING ELEMENT ADOPTED APRIL

2014 HOUSING ELEMENT APRIL 2015 ADOPTED APRIL 27, 2015 Cover photo courtesy of Flickr http://www.flickr.com/photos/bookrep/2776433902 Preface The Housing Element is a major part of San Francisco s General

2014 HOUSING ELEMENT APRIL 2015 ADOPTED APRIL 27, 2015 Cover photo courtesy of Flickr http://www.flickr.com/photos/bookrep/2776433902 Preface The Housing Element is a major part of San Francisco s General

CITY OF SHEBOYGAN COMMUNITY DEVELOPMENT BLOCK GRANT OWNER-INVESTOR REHABILITATION LOAN PROGRAM GUIDELINES AND APPLICATION

CITY OF SHEBOYGAN COMMUNITY DEVELOPMENT BLOCK GRANT OWNER-INVESTOR REHABILITATION LOAN PROGRAM 1 You must be the owner of the property to be rehabilitated. 2 The property must be located in the City of

CITY OF SHEBOYGAN COMMUNITY DEVELOPMENT BLOCK GRANT OWNER-INVESTOR REHABILITATION LOAN PROGRAM 1 You must be the owner of the property to be rehabilitated. 2 The property must be located in the City of

Homeowner Assistance Form

Homeowner Assistance Form Before you complete this form, contact us for assistance. Mortgage loan number: I/We want to: Keep the property Sell the property The property is my/our: Primary residence Second

Homeowner Assistance Form Before you complete this form, contact us for assistance. Mortgage loan number: I/We want to: Keep the property Sell the property The property is my/our: Primary residence Second

CITY OF MCKEESPORT, PENNSYLVANIA 500 Fifth Avenue, McKeesport, Pennsylvania 15132

CITY OF MCKEESPORT, PENNSYLVANIA 500 Fifth Avenue, McKeesport, Pennsylvania 15132 ANALYSIS OF IMPEDIMENTS TO FAIR HOUSING CHOICE UPDATED: FEBRUARY 2011 Regis T. McLaughlin, Honorable Mayor City Council:

CITY OF MCKEESPORT, PENNSYLVANIA 500 Fifth Avenue, McKeesport, Pennsylvania 15132 ANALYSIS OF IMPEDIMENTS TO FAIR HOUSING CHOICE UPDATED: FEBRUARY 2011 Regis T. McLaughlin, Honorable Mayor City Council:

NEIGHBORHOOD STABILIZATION PROGRAM (NSP) APPLICATION FOR NSP LOAN. Program Guidelines

APPLICATION FOR NSP LOAN. Program Guidelines") APPLICATION FOR NSP LOAN Income limits per household Program Guidelines Maximum Income 1 48,150 2 55,000 3 61,900 4 68,750 5 74,250 6 79,750 7 85,250 8 90,750 Homebuyer Requirements Home Education Minimum

APPLICATION FOR NSP LOAN Income limits per household Program Guidelines Maximum Income 1 48,150 2 55,000 3 61,900 4 68,750 5 74,250 6 79,750 7 85,250 8 90,750 Homebuyer Requirements Home Education Minimum

Barriers to Homeownership.

Who Could Afford to Buy a House in 995? 995 Issued August 999 Highlights In 995, about 56 (+/- 0.8) percent of American families (current owners as well as renters) could afford to purchase a modestly

Who Could Afford to Buy a House in 995? 995 Issued August 999 Highlights In 995, about 56 (+/- 0.8) percent of American families (current owners as well as renters) could afford to purchase a modestly

Neighborhood Housing Services of South Florida, Inc. B-09-CN-FL-0020

Action Plan Grantee: Grant: Grant Amount: Status: Neighborhood Housing Services of South Florida, Inc. B-09-CN-FL-0020 $ 89,375,000.00 Modified - Resubmit When Ready Funding Sources Funding Sources Found

Action Plan Grantee: Grant: Grant Amount: Status: Neighborhood Housing Services of South Florida, Inc. B-09-CN-FL-0020 $ 89,375,000.00 Modified - Resubmit When Ready Funding Sources Funding Sources Found

FIRST TIME HOMEBUYERS PROGRAM GUIDELINES (for Market Rate Units) Last Revised October 3, 2013

Last Revised October 3, 2013") FIRST TIME HOMEBUYERS PROGRAM GUIDELINES (for Market Rate Units) Last Revised October 3, 2013 I. Applicant Eligibility a. The total household income can be no greater than 120% of area median, adjusted

FIRST TIME HOMEBUYERS PROGRAM GUIDELINES (for Market Rate Units) Last Revised October 3, 2013 I. Applicant Eligibility a. The total household income can be no greater than 120% of area median, adjusted

Dear Applicant(s): Investors Bank Operations Center 101 Wood Avenue South Iselin, NJ 08830

: Investors Bank Operations Center 101 Wood Avenue South Iselin, NJ 08830") Dear Applicant(s): Thank you for applying for a Home Equity Loan with Investors Bank. In order to begin the application process, please complete the paperwork within this Application Packet: 1. ECOA Notice

Dear Applicant(s): Thank you for applying for a Home Equity Loan with Investors Bank. In order to begin the application process, please complete the paperwork within this Application Packet: 1. ECOA Notice

NFMC Client Level Data and Quarterly Reporting Requirements

NFMC Client Level Data and Quarterly Reporting Requirements The following data points will be collected for each draw request. If, upon implementation of the National Foreclosure Mitigation Counseling

NFMC Client Level Data and Quarterly Reporting Requirements The following data points will be collected for each draw request. If, upon implementation of the National Foreclosure Mitigation Counseling

BANK UNITED GROUND LEASE 2495 S. Orange Ave Orlando, FL

CONTACT: Erik Nelson 407-650-3667 [email protected] BANK UNITED GROUND LEASE 2495 S. Orange Ave Orlando, FL Investment Summary INVESTMENT OVERVIEW Investment Grade Tenant BankUnited (NYSE:BKU) 11+

CONTACT: Erik Nelson 407-650-3667 [email protected] BANK UNITED GROUND LEASE 2495 S. Orange Ave Orlando, FL Investment Summary INVESTMENT OVERVIEW Investment Grade Tenant BankUnited (NYSE:BKU) 11+

OFFICE SPACE FOR LEASE

OFFICE SPACE FOR LEASE www.kowitrealestate.com OFFICE SPACE FOR LEASE 1111 Superior Avenue Cleveland, Ohio Property Highlights Property Photos: Appriximately 1,500 to 180,000 SF of availalbe Class A office

OFFICE SPACE FOR LEASE www.kowitrealestate.com OFFICE SPACE FOR LEASE 1111 Superior Avenue Cleveland, Ohio Property Highlights Property Photos: Appriximately 1,500 to 180,000 SF of availalbe Class A office

Spotlight on the Housing Market in the Las Vegas-Henderson-Paradise, NV MSA

Spotlight on the in the Las Vegas-Henderson-Paradise, NV MSA The Las Vegas-Henderson-Paradise, NV Metropolitan Statistical Area (Las Vegas MSA) is located at the southern tip of Nevada and contains the

Spotlight on the in the Las Vegas-Henderson-Paradise, NV MSA The Las Vegas-Henderson-Paradise, NV Metropolitan Statistical Area (Las Vegas MSA) is located at the southern tip of Nevada and contains the

Villages at Paseo Del SOl

186 Single Family Attached Units Planned Over 23.000 Cars Per Day Margarita Rd De Portola Rd Paloma Del Sol Park 288 Apartments Planned Over 9,900 Cars Per Day Meadows Pkwy Campanula Way Proposed Medical

186 Single Family Attached Units Planned Over 23.000 Cars Per Day Margarita Rd De Portola Rd Paloma Del Sol Park 288 Apartments Planned Over 9,900 Cars Per Day Meadows Pkwy Campanula Way Proposed Medical

RICE COUNTY ENVIRONMENTAL SERVICES RICE COUNTY SUBSURFACE SEWAGE TREATMENT SYSTEM LOW INCOME FIXUP GRANT PROGRAM

(507) 332-6113 RICE COUNTY ENVIRONMENTAL SERVICES 320 Northwest Third Street Suite 9 Faribault, Minnesota 55021-6145 Toll free from Northfield (507) 645-9576 Toll free from Lonsdale (507) 744-5185 TDD

(507) 332-6113 RICE COUNTY ENVIRONMENTAL SERVICES 320 Northwest Third Street Suite 9 Faribault, Minnesota 55021-6145 Toll free from Northfield (507) 645-9576 Toll free from Lonsdale (507) 744-5185 TDD

Loan and Line of Credit. Home Equity

Loan and Line of Credit Home Equity Table of Contents Welcome... 2 Your Most Valuable Asset... 2 Compare Options... 2 Home Equity Loan... 3 Home Equity Line Of Credit... 3 Who Can Get An Equity Loan?...

Loan and Line of Credit Home Equity Table of Contents Welcome... 2 Your Most Valuable Asset... 2 Compare Options... 2 Home Equity Loan... 3 Home Equity Line Of Credit... 3 Who Can Get An Equity Loan?...

Demographic Profile of Wichita Unemployment Insurance Beneficiaries Q3 2015

Demographic Profile of Wichita Unemployment Insurance Beneficiaries Q3 2015 The Bureau of Labor Statistics defines an unemployed person as one 16 years and older having no employment and having made specific

Demographic Profile of Wichita Unemployment Insurance Beneficiaries Q3 2015 The Bureau of Labor Statistics defines an unemployed person as one 16 years and older having no employment and having made specific

THE MORTGAGE INTEREST DEDUCTION ACROSS ZIP CODES. Benjamin H. Harris and Lucie Parker Urban-Brookings Tax Policy Center December 4, 2014 ABSTRACT

THE MORTGAGE INTEREST DEDUCTION ACROSS ZIP CODES Benjamin H. Harris and Lucie Parker Urban-Brookings Tax Policy Center December 4, 2014 ABSTRACT This brief examines characteristics of the mortgage interest

THE MORTGAGE INTEREST DEDUCTION ACROSS ZIP CODES Benjamin H. Harris and Lucie Parker Urban-Brookings Tax Policy Center December 4, 2014 ABSTRACT This brief examines characteristics of the mortgage interest

PUBLIC DISCLOSURE. February 2, 2010 MORTGAGE LENDER COMMUNITY INVESTMENT PERFORMANCE EVALUATION EMBRACE HOME LOANS, INC. MC 0195

PUBLIC DISCLOSURE February 2, 2010 MORTGAGE LENDER COMMUNITY INVESTMENT PERFORMANCE EVALUATION EMBRACE HOME LOANS, INC. MC 0195 25 ENTERPRISE CENTER NEWPORT, RI 02842 DIVISION OF BANKS ONE SOUTH STATION

PUBLIC DISCLOSURE February 2, 2010 MORTGAGE LENDER COMMUNITY INVESTMENT PERFORMANCE EVALUATION EMBRACE HOME LOANS, INC. MC 0195 25 ENTERPRISE CENTER NEWPORT, RI 02842 DIVISION OF BANKS ONE SOUTH STATION

Residential Rehabilitation Loan Program Guidelines

Residential Rehabilitation Loan Program Guidelines City of Middletown Department of Planning, Conservation and Development Community Development Division February 1999 Table of Contents Purpose 1 General

Residential Rehabilitation Loan Program Guidelines City of Middletown Department of Planning, Conservation and Development Community Development Division February 1999 Table of Contents Purpose 1 General

Help for Homes Application

Help for Homes is the City of Thornton s minor home repair program. Qualified homeowners are eligible to have minor repairs or rehabilitation performed on their home free of charge. The goal of the Help

Help for Homes is the City of Thornton s minor home repair program. Qualified homeowners are eligible to have minor repairs or rehabilitation performed on their home free of charge. The goal of the Help

Thornton Home Repair Loan Program

OVERVIEW Homeowners who live in Thornton may be eligible for a 0% interest rate loan to pay for larger repairs needed on their home. This loan program, offered through the City of Thornton and Brothers

OVERVIEW Homeowners who live in Thornton may be eligible for a 0% interest rate loan to pay for larger repairs needed on their home. This loan program, offered through the City of Thornton and Brothers

BUSINESS LOAN APPLICATION

BUSINESS LOAN APPLICATION SECTION A: TYPE OF CREDIT APPLYING FOR Type of Loan Amount Requested Business Line of Credit Primary Purpose of this Loan(s): Equipment Term Loan - Length: Letter of Credit Commercial

BUSINESS LOAN APPLICATION SECTION A: TYPE OF CREDIT APPLYING FOR Type of Loan Amount Requested Business Line of Credit Primary Purpose of this Loan(s): Equipment Term Loan - Length: Letter of Credit Commercial

COMMERCIAL BUSINESS PURPOSE LOAN APPLICATION

COMMERCIAL BUSINESS PURPOSE LOAN APPLICATION IMPORTANT: Read these instructions before completing this application. Applicants should complete this form (including the referenced addenda) as or Co-, as

COMMERCIAL BUSINESS PURPOSE LOAN APPLICATION IMPORTANT: Read these instructions before completing this application. Applicants should complete this form (including the referenced addenda) as or Co-, as