Australian RMBS Index Report Q3 2014: Housing Loan Arrears Hit Eight-Year Low

|

|

|

- Alaina Perry

- 10 years ago

- Views:

Transcription

1 Australian RMBS Index Report Q3 2014: Housing Loan Arrears Hit Eight-Year Low Primary Credit Analyst: Erin Kitson, Melbourne (61) ; Secondary Contacts: Kate J Thomson, Melbourne (61) ; [email protected] Narelle Coneybeare, Sydney (61) ; [email protected] Table Of Contents Major Banks Still Dominate New Issuance Prime Arrears Levels Fall To Their Lowest Level In Nine Years Counterparty Ratings Exposure Cumulative Net Losses Stable And Prepayments Up Outlook Related Criteria And Research NOVEMBER 27,

2 Australian RMBS Index Report Q3 2014: Housing Loan Arrears Hit Eight-Year Low Table 1 Performance Indicators Total delinquencies (including repossessions) Q Q Q Q Q Australian prime (%) Australian subprime and nonconforming (%) plus day delinquencies (including repossessions) Australian prime (%) Australian subprime and nonconforming (%) Prepayment rate Australian prime (%) Australian subprime and nonconforming (%) House price growth (weighted average of eight capital cities)* House Price Index (%) Economic data Unemployment rate (%) *Percentage change from corresponding quarter of previous year. Source: Australian Bureau of Statistics. Table 2 Scenarios For Australian RMBS Collateral: f 2015f 2016f Comment/outlook Real GDP growth (%) Softer growth as economy rebalances away from mining investment Collateral credit quality Neutral Unemployment rate (%) Unemployment expected to ease Neutral to somewhat positive House Price Index (HPI)* 9.2 N.A. N.A. Strong house price growth not abating Neutral to somewhat positive Official cash rate (%) Normalization of interest rates forecast over the medium term Consumer Price Index (CPI) (%) Neutral to somewhat negative CPI forecast to decline Neutral Source: Real GDP growth, unemployment rate, official cash rate, and CPI forecasts derived by Standard & Poor's. HPI (weighted average of eight capital cities) provided by the Australian Bureau of Statistics. *Percentage change from corresponding quarter of previous year. N.A.--Not available. Major Banks Still Dominate New Issuance New issuance levels for residential mortgage-backed securities' (RMBS) have continued to keep pace with the levels observed in Six new publicly rated prime RMBS transactions totaling approximately A$8.9 billion were issued during the third quarter (Q3). Issuance in Q3 was up about 9% year on year. Various originator types undertook new NOVEMBER 27,

* House Price Index (%) 9.2 10.3 11.0 10.5 8.3 Economic data Unemployment rate (%) 6.1 5.9 6.2 5.7 5.")

3 issuance during the quarter. (Watch the related CreditMatters TV segment, "With Interest-Only Lending On The Up, What's The Outlook For Australian RMBS In 2015?" dated Nov. 28, 2014.) The major banks have continued to dominate the new issuance ranks, with Commonwealth Bank of Australia ranked No.1 and Westpac Banking Corp. at No.2 in that category on the Top 10 Sponsor List. The residential lending market in Australia has become increasingly cutthroat, making it difficult for smaller residential mortgage lenders to compete against the major banks (see "Business Pressures Rising For Australian Mutual Financial Institutions," published Oct. 26, 2014). Macquarie Securitisation Ltd. was ranked No.3 on the Top 10 Sponsor List as of Sept. 30, 2014, making it a notable standout in the new issuance ranks. Macquarie's rise through the new issuance ranks reflects the bank's growth and the rapid expansion of its residential mortgage portfolio. We expect 2014 issuance levels to remain roughly on track with the levels observed in Prime Arrears Levels Fall To Their Lowest Level In Nine Years Prime arrears continued their downward trajectory in Q3, reaching a low of 0.98%. This is the lowest level recorded since November 2005 (see chart 8). The days' bucket recorded the most pronounced decrease during the quarter, with arrears levels falling 0.10%. The ongoing low interest-rate environment has influenced the decline in arrears during recent months. The Reserve Bank of Australia (RBA) said in its most recent Statement of Monetary Policy that the decline in average lending rates during recent months is partly due to the ongoing replacement of more expensive fixed and discount variable-rate loans from previous years as well as a reduction in interest rates on offer for some borrowers. Lower interest rates have enabled many borrowers to stay on top of their mortgage repayments. The Standard & Poor's Performance Index (SPIN) for subprime and nonconforming mortgages increased to 5.23% during Q3 from 4.58% in Q2 (chart 8). The subprime SPIN is subject to greater volatility, given the smaller number of transactions that comprise the index. However, the increase in arrears might reflect increasing cash flow pressure for this borrower type, many of whom are self-employed. Self-employed borrowers are more likely to experience mortgage stress as a result of a subdued economy. Also, the participation rate for employment is currently around its lowest level since the mid-2000s and the unemployment rate is at its highest level in more than a decade. Has the recent rise in interest-only lending in the residential mortgage market been reflected in the RMBS market? Interest-only lending has become more prominent in Australia in recent years. Interest-only lending as a share of new lending for authorized deposit-taking institutions (ADIs) is around 40% (chart 1). NOVEMBER 27,

. Macquarie Securitisation Ltd. was ranked No.3 on the Top 10 Sponsor List as of Sept.")

4 Chart 1 The level of interest-only loans underlying RMBS transactions has varied over time, based on our observations. However, the proportion of interest-only loans tends to change in line with interest-rate movements (chart 2). A period of low interest rates is generally followed by an uptick in interest-only lending (chart 2). NOVEMBER 27,

.")

.")

5 Chart 2 Do interest-only loans comprise a material share of RMBS? More than half of the outstanding balance of interest-only loans underlying RMBS is for investment purpose (chart 3). Investment loans make up approximately 26% of RMBS loans. NOVEMBER 27,

6 Chart 3 The recent growth in interest-only lending has been partly driven by an increase in financing needs for investment properties, particularly in Sydney and Melbourne. Investors have a stronger incentive to take out interest-only loans than owner occupiers because interest expenses are tax deductible for investment loans. Furthermore, investors tend to maximize the potential tax benefit by taking out loans with longer interest-only periods (table 3). Table 3 Repayment Profile Breakdown Across Borrower Type Owner-occupied (%) Investment PI amort Less than three years years years Greater than 10 years Source: Standard & Poor's. Note: Data as of August About three-quarters of interest-only loans securitized are from the portfolios of financial institutions. However, nonbank originators and other banks have a disproportionate share of interest-only lending relative to their total share of RMBS outstandings (chart 4). NOVEMBER 27,

Investment PI amort. 97.96 85.93 Less than three years 0.07 0.00 3-5 years 0.42 2.70 5-10 years 1.35 9.")

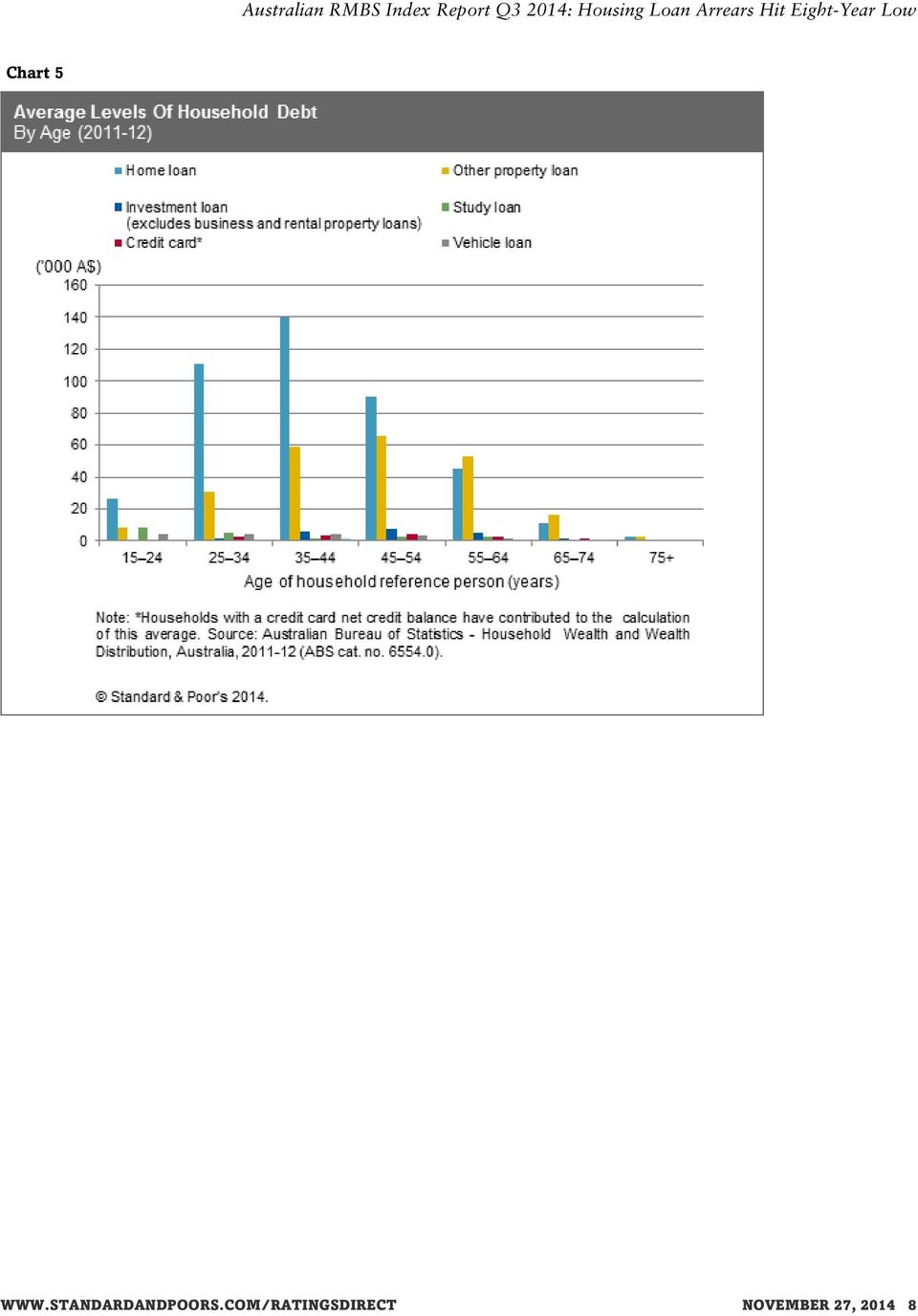

7 Chart 4 Are interest-only loans inherently riskier from a credit perspective? Interest-only loans carry a higher risk of repayment shock, particularly when the loan reverts to a principal and interest repayment profile, and of the loan going into a negative equity position should the loan balance exceed the property value if house prices were to decline. Investors are more likely to take out an interest-only loan, given the tax incentives available to them. These types of borrowers are usually in an age cohort with stronger earning capacity and a higher net worth (chart 5 and chart 6). NOVEMBER 27,

8 Chart 5 NOVEMBER 27,

9 Chart 6 Interest-only loans tend to be underwritten at lower loan-to-value (LTV) ratios, and the debt-serviceability assessments carried out by many lenders are based on a borrower's ability to service both the principal and interest because most interest-only periods are for a limited period, limiting the risk of repayment shock. Most lenders also qualify borrowers at an interest-rate payment level that is higher than the prevailing interest rate. Across the RMBS portfolios, we have not observed a material difference in the arrears performance of investment loans compared with owner-occupied loans (chart 7). NOVEMBER 27,

. WWW.")

10 Chart 7 The Australian Prudential Regulation Authority (APRA)'s latest Prudential Practice Guide (APG 223 Residential Mortgage Lending) is likely to further entrench the sound lending practices that have been a key characteristic of the Australian banking system, in our view. According to the guide, APRA expects interest-only loans would not be approved if the borrower cannot qualify for a loan on a principal and interest basis, and that a debt-serviceability assessment would include a buffer over a loan's interest rate. Many lenders already adopt this approach in their underwriting practices. We believe the key risk of interest-only loans is that they are more susceptible to a downturn in property prices. Borrowers with interest-only loans can have less incentive than owner-occupiers to prepay the loan, particularly if the loan is for investment purposes. This means there is less equity built up and therefore less of a buffer to withstand a downturn in property prices. Counterparty Ratings Exposure In terms of rating transition, counterparty risk is a key rating risk for Australian RMBS. The lowering of the financial strength ratings of lenders' mortgage insurance (LMI) providers would affect the ratings on subordinated notes in NOVEMBER 27,

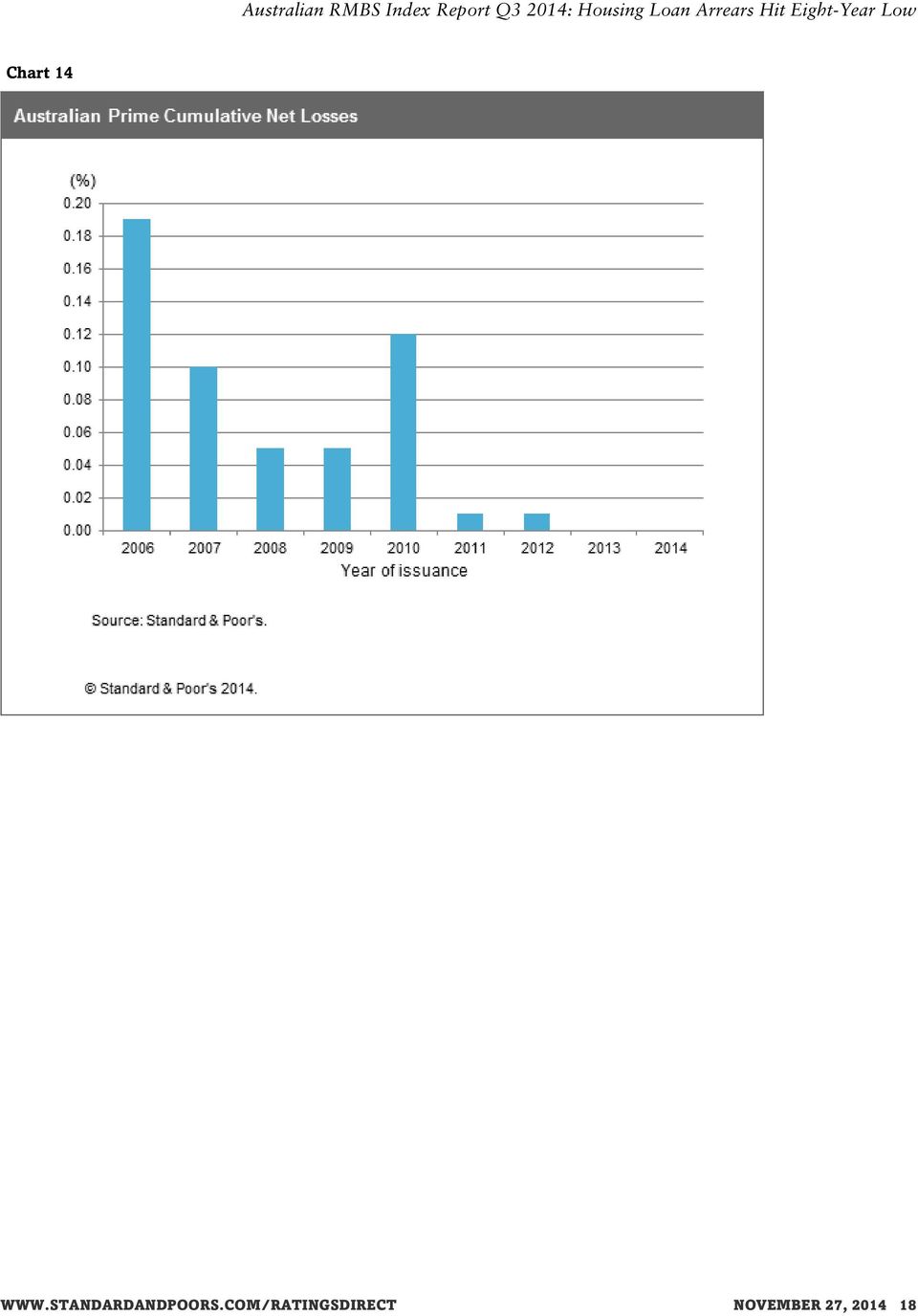

11 prime RMBS, as would any change in criteria for recognizing LMI as a form of credit enhancement (see "Request For Comment: Methodology For Assessing Mortgage Insurance And Similar Guarantees And Supports In Structured And Public Sector Finance and Covered Bonds" published Aug. 18, 2014). We placed 150 tranches of RMBS transactions in Australia and New Zealand on CreditWatch with negative implications on Nov. 11, 2014, after we lowered our ratings on Genworth Financial Mortgage Insurance Pty Ltd. and its parent, Genworth Financial Inc. (see "Research Update: Genworth Financial Inc. And Genworth Life Insurance Ratings Lowered; Outlook Negative," published on Nov. 7, 2014). About 64% of loans are insured by LMI providers across the RMBS portfolios. Approximately half of insured loans are insured by Genworth Financial Mortgage Insurance Pty Ltd. Cumulative Net Losses Stable And Prepayments Up Cumulative net losses are relatively low for a majority of vintages across the prime and nonconforming sector. In the prime space, the 2006 vintage has the highest level of losses, at 0.19%, followed by the 2010 vintage, for which a majority of losses are largely attributable to one transaction (chart 14). Cumulative net losses for the nonconforming sector are relatively low, with a majority of vintages reporting as of Sept. 30, 2014, a cumulative net loss below 1.6%, except the 2008 vintage, which is limited to two transactions (chart 15). Prepayment rates across the prime and nonconforming sectors increased during Q3 (chart 16). The increase probably reflects a rise in refinance activity, given the lower interest-rate environment. The rise in the nonconforming space in particular reflects the greater ability of many of these borrowers to refinance their loans at a better rate, given their performance history and the current market environment. Outlook A fall in property prices and an rising interest-rate environment present a risk for certain borrowers. However, we believe such borrowers are a minority across the RMBS space. A majority of loans underlying RMBS transactions are well placed to weather such a scenario, given their relatively high levels of seasoning and modest LTV ratio positions. We expect the solid collateral performance of RMBS transactions to continue, with changes in arrears levels primarily being driven by changes in the interest rate. NOVEMBER 27,

12 Chart 8 NOVEMBER 27,

13 Chart 9 NOVEMBER 27,

14 Chart 10 NOVEMBER 27,

15 Chart 11 NOVEMBER 27,

16 Chart 12 NOVEMBER 27,

17 Chart 13 NOVEMBER 27,

18 Chart 14 NOVEMBER 27,

19 Chart 15 NOVEMBER 27,

20 Chart 16 Related Criteria And Research Related Criteria Criteria: Outlook Assumptions For The Australian Residential Mortgage Market, Feb. 10, 2014 Criteria: Counterparty Risk Framework Methodology And Assumptions, June 25, 2013 Criteria: Australian RMBS Rating Methodology And Assumptions, Sept. 1, 2011 Use Of CreditWatch and Outlooks, Sept. 14, 2009 Criteria: Australia And New Zealand RMBS: Analyzing Credit Quality, Feb. 21, 2007 Related Research Asia-Pacific Economies Limp Toward Higher-Quality Growth, Nov. 26, 2014 Australia's Regional Banks And Mutual Financial Institutions Losing The Pricing War Against The Major Banks In the Home Loan Market, Nov. 17, 2014 Genworth Financial Inc. And Genworth Life Insurance Ratings Lowered; Outlook Negative, Nov. 6, 2014 Business Pressures Rising For Australian Mutual Financial Institutions, Oct. 26, 2014 Industry And Economic Ratings Outlook: Australian RMBS Fundamentals Reflect A Stable Economic Environment, Sept. 30, 2014 Comparing The U.K., Dutch, Australian, And Japanese RMBS And Mortgage Markets, Sept. 18, NOVEMBER 27,

21 Request For Comment: Methodology For Assessing Mortgage Insurance And Similar Guarantees And Supports In Structured And Public Sector Finance And Covered Bonds, Aug. 18, 2014 Australia And New Zealand Structured Finance Scenario And Sensitivity Analysis: Understanding The Effects Of Macroeconomic Factors On Credit Quality, Aug. 1, 2014 An Overview Of Australia's Housing Market And Residential Mortgage-Backed Securities, Jan. 15, 2014 Scenario Analysis: 2013 Update To Lenders' Mortgage Insurance Sensitivity Analysis On Australian Prime RMBS, Nov. 25, 2013 Under Standard & Poor's policies, only a Rating Committee can determine a Credit Rating Action (including a Credit Rating change, affirmation or withdrawal, Rating Outlook change, or CreditWatch action). This commentary and its subject matter have not been the subject of Rating Committee action and should not be interpreted as a change to, or affirmation of, a Credit Rating or Rating Outlook. Standard & Poor's (Australia) Pty. Ltd. holds Australian financial services licence number under the Corporations Act Standard & Poor's credit ratings and related research are not intended for and must not be distributed to any person in Australia other than a wholesale client (as defined in Chapter 7 of the Corporations Act). NOVEMBER 27,

22 Copyright 2015 Standard & Poor's Financial Services LLC, a part of McGraw Hill Financial. All rights reserved. No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages. Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such acknowledgement at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any damage alleged to have been suffered on account thereof. S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process. S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, (free of charge), and and (subscription) and (subscription) and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at NOVEMBER 27,

Four Ratings Raised From GreatAmerica Leasing Receivables Funding L.L.C.; 10 Ratings Affirmed

Four s Raised From GreatAmerica Leasing Receivables Funding L.L.C.; 10 s Affirmed Primary Credit Analyst: Srabani C Chandra-Lal, New York (1) 212-438-5036; [email protected] Secondary

Four s Raised From GreatAmerica Leasing Receivables Funding L.L.C.; 10 s Affirmed Primary Credit Analyst: Srabani C Chandra-Lal, New York (1) 212-438-5036; [email protected] Secondary

RBS Citizens Financial Group Ratings Affirmed; Outlook Remains Negative; Stand-Alone Credit Profile Lowered To 'a-'

Research Update: RBS Citizens Financial Group Ratings Affirmed; Outlook Remains Negative; Stand-Alone Credit Profile Lowered To 'a-' Primary Credit Analyst: Barbara Duberstein, New York (1) 212-438-5656;

Research Update: RBS Citizens Financial Group Ratings Affirmed; Outlook Remains Negative; Stand-Alone Credit Profile Lowered To 'a-' Primary Credit Analyst: Barbara Duberstein, New York (1) 212-438-5656;

Lake Oswego, Oregon; Water/Sewer

Summary: Lake Oswego, Oregon; Water/Sewer Primary Credit Analyst: Aaron Lee, San Francisco (1) 415-371-5066; [email protected] Secondary Contact: Tim Tung, San Francisco (415) 371-5041; [email protected]

Summary: Lake Oswego, Oregon; Water/Sewer Primary Credit Analyst: Aaron Lee, San Francisco (1) 415-371-5066; [email protected] Secondary Contact: Tim Tung, San Francisco (415) 371-5041; [email protected]

Residential Real Estate Company Deutsche Wohnen 'BBB+' Ratings Placed On CreditWatch Negative On Conwert Takeover Offer

Research Update: Residential Real Estate Company Deutsche Wohnen 'BBB+' Ratings Placed On CreditWatch Negative On Conwert Takeover Offer Primary Credit Analyst: Marie-Aude Vialle, London (44) 20-7176-3655;

Research Update: Residential Real Estate Company Deutsche Wohnen 'BBB+' Ratings Placed On CreditWatch Negative On Conwert Takeover Offer Primary Credit Analyst: Marie-Aude Vialle, London (44) 20-7176-3655;

Turkey-Based Appliance Manufacturer Vestel Outlook Revised To Positive; 'B-' Rating Affirmed

Research Update: Turkey-Based Appliance Manufacturer Vestel Outlook Revised To Positive; 'B-' Rating Affirmed Primary Credit Analyst: Alexander Griaznov, Moscow (7) 495-783-4109; [email protected]

Research Update: Turkey-Based Appliance Manufacturer Vestel Outlook Revised To Positive; 'B-' Rating Affirmed Primary Credit Analyst: Alexander Griaznov, Moscow (7) 495-783-4109; [email protected]

Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed And Removed From CreditWatch; Outlook Stable

Research Update: Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed And Removed From CreditWatch; Outlook Stable Primary Credit Analyst: Oluwatosin S Adesiyan, London (44) 20-7176-3279;

Research Update: Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed And Removed From CreditWatch; Outlook Stable Primary Credit Analyst: Oluwatosin S Adesiyan, London (44) 20-7176-3279;

Research Update: Danish Mortgage Bank DLR Kredit A/S Assigned 'BBB+/A-2' Ratings. Table Of Contents

May 31, 2012 Research Update: Danish Mortgage Bank DLR Kredit A/S Assigned 'BBB+/A-2' Ratings Primary Credit Analyst: Per Tornqvist, Stockholm (46) 8-440-5904;[email protected] Secondary

May 31, 2012 Research Update: Danish Mortgage Bank DLR Kredit A/S Assigned 'BBB+/A-2' Ratings Primary Credit Analyst: Per Tornqvist, Stockholm (46) 8-440-5904;[email protected] Secondary

Market Data Analysis - Pacific Life

Research Update: 'A+', Pacific LifeCorp 'BBB+' Ratings Affirmed; Outlook Stable; New Senior Notes Rated 'BBB+' Primary Credit Analyst: Carmi Margalit, CFA, New York (1) 212-438-1000; [email protected]

Research Update: 'A+', Pacific LifeCorp 'BBB+' Ratings Affirmed; Outlook Stable; New Senior Notes Rated 'BBB+' Primary Credit Analyst: Carmi Margalit, CFA, New York (1) 212-438-1000; [email protected]

R.V.I. Guaranty Co. Ltd. And Subsidiaries 'BBB' Ratings Affirmed After Insurance Criteria Change; The Outlook Is Stable

Research Update: R.V.I. Guaranty Co. Ltd. And Subsidiaries 'BBB' Ratings Affirmed After Insurance Criteria Change; The Outlook Is Stable Primary Credit Analyst: David S Veno, New York (1) 212-438-2108;

Research Update: R.V.I. Guaranty Co. Ltd. And Subsidiaries 'BBB' Ratings Affirmed After Insurance Criteria Change; The Outlook Is Stable Primary Credit Analyst: David S Veno, New York (1) 212-438-2108;

Gemini Securitization Corp., LLC (As Of May 2014)

") ABCP Portfolio Data: Gemini Securitization Corp., LLC (As Of May 2014) Primary Credit Analyst: Thomas G Dunn, New York (1) 212-438-1623; [email protected] Surveillance Credit Analyst: Marc

ABCP Portfolio Data: Gemini Securitization Corp., LLC (As Of May 2014) Primary Credit Analyst: Thomas G Dunn, New York (1) 212-438-1623; [email protected] Surveillance Credit Analyst: Marc

Spanish Multi-Cedulas Rating Actions As Of Aug. 2, 2012

Spanish Multi-Cedulas Rating Actions As Of Aug. 2, 2012 Covered Bonds Frankfurt: Karlo S Fuchs, Analytical Manager, Frankfurt (49) 69-33-999-156; [email protected] Covered Bonds London:

Spanish Multi-Cedulas Rating Actions As Of Aug. 2, 2012 Covered Bonds Frankfurt: Karlo S Fuchs, Analytical Manager, Frankfurt (49) 69-33-999-156; [email protected] Covered Bonds London:

Interest-Only Loans Could Destabilize Denmark's Mortgage Market

STRUCTURED FINANCE RESEARCH Interest-Only Loans Could Destabilize Denmark's Mortgage Market Primary Credit Analyst: Casper R Andersen, London (44) 20-7176-6757; [email protected] Table

STRUCTURED FINANCE RESEARCH Interest-Only Loans Could Destabilize Denmark's Mortgage Market Primary Credit Analyst: Casper R Andersen, London (44) 20-7176-6757; [email protected] Table

AEG Power Solutions Downgraded To 'CCC-' On Heightened Risk Of Missing An Interest Payment; Outlook Negative

Research Update: AEG Power Solutions Downgraded To 'CCC-' On Heightened Risk Of Missing An Interest Payment; Outlook Negative Primary Credit Analyst: Abigail Klimovich, CFA, London (44) 20-7176-3554; [email protected]

Research Update: AEG Power Solutions Downgraded To 'CCC-' On Heightened Risk Of Missing An Interest Payment; Outlook Negative Primary Credit Analyst: Abigail Klimovich, CFA, London (44) 20-7176-3554; [email protected]

Electricity Transmission System Operator TenneT's Hybrid Equity Content Revised To Intermediate; 'A-' Ratings Affirmed

Research Update: Electricity Transmission System Operator TenneT's Hybrid Equity Content Revised To Intermediate; 'A-' Ratings Affirmed Primary Credit Analyst: Beatrice de Taisne, CFA, London (44) 20-7176-3938;

Research Update: Electricity Transmission System Operator TenneT's Hybrid Equity Content Revised To Intermediate; 'A-' Ratings Affirmed Primary Credit Analyst: Beatrice de Taisne, CFA, London (44) 20-7176-3938;

Interactive Brokers LLC

Summary: Interactive Brokers LLC Primary Credit Analyst: Clayton D Montgomery, New York (1) 212-438-5079; [email protected] Secondary Contact: Robert B Hoban, New York (1) 212-438-7385;

Summary: Interactive Brokers LLC Primary Credit Analyst: Clayton D Montgomery, New York (1) 212-438-5079; [email protected] Secondary Contact: Robert B Hoban, New York (1) 212-438-7385;

Kuwait Projects Co. (Holding) Affirmed At 'BBB-/A-3'; Outlook Stable

Affirmed At 'BBB-/A-3'; Outlook Stable") Research Update: Kuwait Projects Co. (Holding) Affirmed At 'BBB-/A-3'; Outlook Stable Primary Credit Analyst: Per Karlsson, Stockholm (46) 8-440-5927; [email protected] Secondary Contact:

Research Update: Kuwait Projects Co. (Holding) Affirmed At 'BBB-/A-3'; Outlook Stable Primary Credit Analyst: Per Karlsson, Stockholm (46) 8-440-5927; [email protected] Secondary Contact:

Sirius International Group Outlook Revised To Stable On Plans To Retain Its Strategy Post Acquisition; Ratings Affirmed

Research Update: Sirius International Group Outlook Revised To Stable On Plans To Retain Its Strategy Post Acquisition; Ratings Affirmed Primary Credit Analyst: Anvar Gabidullin, CFA, London (44) 20-7176-7047;

Research Update: Sirius International Group Outlook Revised To Stable On Plans To Retain Its Strategy Post Acquisition; Ratings Affirmed Primary Credit Analyst: Anvar Gabidullin, CFA, London (44) 20-7176-7047;

Guardian Life Insurance, Core Operating Subsidiaries 'AA+' Ratings Affirmed On Criteria Review, Outlook Negative

Research Update: Guardian Life Insurance, Core Operating Subsidiaries 'AA+' Ratings Affirmed On Criteria Review, Outlook Negative Primary Credit Analyst: Neal I Freedman, New York (1) 212-438-1274; [email protected]

Research Update: Guardian Life Insurance, Core Operating Subsidiaries 'AA+' Ratings Affirmed On Criteria Review, Outlook Negative Primary Credit Analyst: Neal I Freedman, New York (1) 212-438-1274; [email protected]

FWD Life Insurance Co. (Bermuda) Ltd. Assigned 'A-' And 'cnaa' Ratings; Outlook Stable

Ltd. Assigned 'A-' And 'cnaa' Ratings; Outlook Stable") Research Update: FWD Life Insurance Co. (Bermuda) Ltd. Assigned 'A-' And 'cnaa' Ratings; Outlook Stable Primary Credit Analyst: Anna Kong, FSA, FRM, Hong Kong (852) 2533-3571; [email protected]

Research Update: FWD Life Insurance Co. (Bermuda) Ltd. Assigned 'A-' And 'cnaa' Ratings; Outlook Stable Primary Credit Analyst: Anna Kong, FSA, FRM, Hong Kong (852) 2533-3571; [email protected]

Six Russian Real Estate Companies On CreditWatch Amid Higher Interest Rates, Weakening Demand, Sharp Ruble Depreciation

Research Update: Six Russian Real Estate Companies On CreditWatch Amid Higher Interest Rates, Weakening Demand, Sharp Ruble Depreciation Primary Credit Analyst: Anton Geyze, Moscow (7) 495-783-4134; [email protected]

Research Update: Six Russian Real Estate Companies On CreditWatch Amid Higher Interest Rates, Weakening Demand, Sharp Ruble Depreciation Primary Credit Analyst: Anton Geyze, Moscow (7) 495-783-4134; [email protected]

S&P Takes Rating Actions On Section 15 Bonds Issued By Various Danish Mortgage Banks

S&P Takes Rating Actions On Section 15 Bonds Issued By Various Danish Mortgage Banks Primary Credit Analyst: Casper R Andersen, London (44) 20-7176-6757; [email protected] Secondary

S&P Takes Rating Actions On Section 15 Bonds Issued By Various Danish Mortgage Banks Primary Credit Analyst: Casper R Andersen, London (44) 20-7176-6757; [email protected] Secondary

Bertelsmann SE & Co. KGaA's Hybrid Equity Content Revised To "Intermediate"; 'BBB+/A-2' Ratings Affirmed

Research Update: Bertelsmann SE & Co. KGaA's Hybrid Equity Content Revised To "Intermediate"; 'BBB+/A-2' Ratings Affirmed Primary Credit Analyst: Florence Devevey, Madrid (34) 91-788-7236; [email protected]

Research Update: Bertelsmann SE & Co. KGaA's Hybrid Equity Content Revised To "Intermediate"; 'BBB+/A-2' Ratings Affirmed Primary Credit Analyst: Florence Devevey, Madrid (34) 91-788-7236; [email protected]

Central Texas Regional Mobility Authority; Toll Roads Bridges

Summary: Central Texas Regional Mobility Authority; Toll Roads Bridges Primary Credit Analyst: Todd R Spence, Dallas (1) 214-871-1424; [email protected] Secondary Contact: Peter V Murphy,

Summary: Central Texas Regional Mobility Authority; Toll Roads Bridges Primary Credit Analyst: Todd R Spence, Dallas (1) 214-871-1424; [email protected] Secondary Contact: Peter V Murphy,

Dogus Holding 'BB/B' Ratings Affirmed On Sustained Investments And Expected Completion Of Garanti Sale; Outlook Negative

Research Update: Dogus Holding 'BB/B' Ratings Affirmed On Sustained Investments And Expected Completion Of Garanti Sale; Outlook Negative Primary Credit Analyst: Renato Panichi, Milan (39) 02-72111-215;

Research Update: Dogus Holding 'BB/B' Ratings Affirmed On Sustained Investments And Expected Completion Of Garanti Sale; Outlook Negative Primary Credit Analyst: Renato Panichi, Milan (39) 02-72111-215;

Ten Japanese Insurers Downgraded; Outlooks On Two Other Insurers Revised Down To Stable Following Downgrade Of Japan

Ten Japanese Insurers Downgraded; Outlooks On Two Other Insurers Revised Down To Stable Following Primary Credit Analyst: Reina Tanaka, Tokyo (81) 3-4550-8587; [email protected] Secondary

Ten Japanese Insurers Downgraded; Outlooks On Two Other Insurers Revised Down To Stable Following Primary Credit Analyst: Reina Tanaka, Tokyo (81) 3-4550-8587; [email protected] Secondary

Mounting Student Debt Is Reshaping The U.S. Student Loan Market

STRUCTURED FINANCE RESEARCH Mounting Student Debt Is Reshaping The U.S. Student Loan Market Primary Credit Analyst: Erkan Erturk, PhD, New York (1) 212-438-2450; [email protected] Business

STRUCTURED FINANCE RESEARCH Mounting Student Debt Is Reshaping The U.S. Student Loan Market Primary Credit Analyst: Erkan Erturk, PhD, New York (1) 212-438-2450; [email protected] Business

Danish Bank DLR Kredit Affirmed At 'BBB+/A-2'; Junior Subordinated Debt Downgraded To 'BB'; Outlook Remains Stable

Research Update: Danish Bank DLR Kredit Affirmed At 'BBB+/A-2'; Junior Subordinated Debt Downgraded To 'BB'; Outlook Remains Stable Primary Credit Analyst: Sean Cotten, Stockholm (46) 8-440-5928; [email protected]

Research Update: Danish Bank DLR Kredit Affirmed At 'BBB+/A-2'; Junior Subordinated Debt Downgraded To 'BB'; Outlook Remains Stable Primary Credit Analyst: Sean Cotten, Stockholm (46) 8-440-5928; [email protected]

Pohjola Non-Life Insurance Downgraded To 'A+' After Government Support Review Of Pohjola Bank; Outlook Remains Negative

Research Update: Pohjola Non-Life Insurance Downgraded To 'A+' After Government Support Review Of Pohjola Bank; Outlook Remains Negative Primary Credit Analyst: Anna Glennmar, Stockholm (46) 8-440-5922;

Research Update: Pohjola Non-Life Insurance Downgraded To 'A+' After Government Support Review Of Pohjola Bank; Outlook Remains Negative Primary Credit Analyst: Anna Glennmar, Stockholm (46) 8-440-5922;

Research Update: Banco Monex S.A. Rated Global Scale 'BB+/B', National Scale 'mxa+/mxa-1' Rating Affirmed. Table Of Contents

May 17, 2012 Research Update: Banco Monex S.A. Rated Global Scale 'BB+/B', National Scale 'mxa+/mxa-1' Rating Affirmed Primary Credit Analyst: Arturo Sanchez, Mexico City (52) 55-5081-4468;[email protected]

May 17, 2012 Research Update: Banco Monex S.A. Rated Global Scale 'BB+/B', National Scale 'mxa+/mxa-1' Rating Affirmed Primary Credit Analyst: Arturo Sanchez, Mexico City (52) 55-5081-4468;[email protected]

AEG Power Solutions Downgraded To 'CCC+' On Weak Earnings And Delays In Customer Payments; Outlook Negative

Research Update: AEG Power Solutions Downgraded To 'CCC+' On Weak Earnings And Delays In Customer Payments; Outlook Negative Primary Credit Analyst: Abigail Klimovich, CFA, London (44) 20-7176-3554; [email protected]

Research Update: AEG Power Solutions Downgraded To 'CCC+' On Weak Earnings And Delays In Customer Payments; Outlook Negative Primary Credit Analyst: Abigail Klimovich, CFA, London (44) 20-7176-3554; [email protected]

Volkswagen Bank Ratings Lowered To 'A-/A-2'; Outlook Negative

Research Update: Volkswagen Bank Ratings Lowered To 'A-/A-2'; Outlook Negative Primary Credit Analyst: Salla von Steinaecker, Frankfurt (49) 69-33-999-164; [email protected] Secondary

Research Update: Volkswagen Bank Ratings Lowered To 'A-/A-2'; Outlook Negative Primary Credit Analyst: Salla von Steinaecker, Frankfurt (49) 69-33-999-164; [email protected] Secondary

New York Life Insurance Co. 'AA+/A-1+' Rating Affirmed On Criteria Review; Outlook Stable

Research Update: New York Life Insurance Co. 'AA+/A-1+' Rating Affirmed On Criteria Review; Outlook Stable Primary Credit Analyst: Michael E Gross, San Francisco (1) 415-371-5003; [email protected]

Research Update: New York Life Insurance Co. 'AA+/A-1+' Rating Affirmed On Criteria Review; Outlook Stable Primary Credit Analyst: Michael E Gross, San Francisco (1) 415-371-5003; [email protected]

Swedbank Outlook Revised To Stable From Negative On Improved Business Position; Ratings Affirmed At 'A+/A-1'

Research Update: Swedbank Outlook Revised To Stable From Negative On Improved Business Position; Ratings Primary Credit Analyst: Alexander Ekbom, Stockholm (46) 8-440-5911; [email protected]

Research Update: Swedbank Outlook Revised To Stable From Negative On Improved Business Position; Ratings Primary Credit Analyst: Alexander Ekbom, Stockholm (46) 8-440-5911; [email protected]

Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed; Outlook Negative

Research Update: Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed; Outlook Negative Primary Credit Analyst: Oliver Herbert, London (44) 20-7176-7054; [email protected]

Research Update: Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed; Outlook Negative Primary Credit Analyst: Oliver Herbert, London (44) 20-7176-7054; [email protected]

Spain-Based IT Service Provider Amadeus IT Holding Rating Raised To 'BBB/A-2' On Strong Financials, Outlook Stable

Research Update: Spain-Based IT Service Provider Amadeus IT Holding Rating Raised To 'BBB/A-2' On Strong Financials, Outlook Stable Primary Credit Analyst: Stefan Kirschner, Frankfurt (49) 69-33-999-281;

Research Update: Spain-Based IT Service Provider Amadeus IT Holding Rating Raised To 'BBB/A-2' On Strong Financials, Outlook Stable Primary Credit Analyst: Stefan Kirschner, Frankfurt (49) 69-33-999-281;

Healthcare Support (North Staffs) Finance Outlook Revised To Stable On Operating Risk; 'BBB-' Issue Ratings Affirmed

Finance Outlook Revised To Stable On Operating Risk; 'BBB-' Issue Ratings Affirmed") Research Update: Healthcare Support (North Staffs) Finance Outlook Revised To Stable On Operating Risk; 'BBB-' Issue Ratings Affirmed Primary Credit Analyst: Manuel Dusina, London (44) 20-7176-5530; [email protected]

Research Update: Healthcare Support (North Staffs) Finance Outlook Revised To Stable On Operating Risk; 'BBB-' Issue Ratings Affirmed Primary Credit Analyst: Manuel Dusina, London (44) 20-7176-5530; [email protected]

Constellium Holdco B.V. Recovery Rating Profile

Recovery Report: Constellium Holdco B.V. Recovery Rating Profile Recovery Analyst: Franck Rizzoli, London (44) 20-7176-3934; [email protected] Primary Credit Analyst: Tatjana Lescova,

Recovery Report: Constellium Holdco B.V. Recovery Rating Profile Recovery Analyst: Franck Rizzoli, London (44) 20-7176-3934; [email protected] Primary Credit Analyst: Tatjana Lescova,

Research Update: Ratings Lowered On Netherlands-Based SNS REAAL N.V. Group And Core Subs On Slower Recovery Prospects; Outlook Stable

March 1, 2012 Research Update: Ratings Lowered On Netherlands-Based SNS REAAL N.V. Group And Core Subs On Slower Recovery Prospects; Outlook Stable Primary Credit Analysts: Alexandre Birry, London 44 (0)

March 1, 2012 Research Update: Ratings Lowered On Netherlands-Based SNS REAAL N.V. Group And Core Subs On Slower Recovery Prospects; Outlook Stable Primary Credit Analysts: Alexandre Birry, London 44 (0)

International Finance Corp. 'AAA/A-1+' Rating Affirmed; Outlook Remains Stable

Research Update: International Finance Corp. 'AAA/A-1+' Rating Affirmed; Outlook Remains Stable Primary Credit Analyst: Elie Heriard Dubreuil, London (44) 207-176-7302; [email protected]

Research Update: International Finance Corp. 'AAA/A-1+' Rating Affirmed; Outlook Remains Stable Primary Credit Analyst: Elie Heriard Dubreuil, London (44) 207-176-7302; [email protected]

Centennial Water and Sanitation District, Colorado; Water/Sewer

Summary: Centennial Water and Sanitation District, Colorado; Water/Sewer Primary Credit Analyst: Scott D Garrigan, Chicago (1) 312-233-7014; [email protected] Secondary Contact: Tim Tung,

Summary: Centennial Water and Sanitation District, Colorado; Water/Sewer Primary Credit Analyst: Scott D Garrigan, Chicago (1) 312-233-7014; [email protected] Secondary Contact: Tim Tung,

A Financial Analysis of Energies and Gas Pipelines

Research Update: Interconexion Electrica S.A. E.S.P. (ISA) 'BBB' Credit Rating Affirmed, Outlook Remains Stable Primary Credit Analyst: Maria del Sol S Gonzalez, CFA, New York (1) 212-438-4443; [email protected]

Research Update: Interconexion Electrica S.A. E.S.P. (ISA) 'BBB' Credit Rating Affirmed, Outlook Remains Stable Primary Credit Analyst: Maria del Sol S Gonzalez, CFA, New York (1) 212-438-4443; [email protected]

Covea Group Core And Guaranteed Companies Outlooks Revised To Positive; 'A' Ratings Affirmed

Research Update: Covea Group Core And Guaranteed Companies Outlooks Revised To Positive; 'A' Ratings Affirmed Primary Credit Analyst: David D Anthony, London (44) 20-7176-7010; [email protected]

Research Update: Covea Group Core And Guaranteed Companies Outlooks Revised To Positive; 'A' Ratings Affirmed Primary Credit Analyst: David D Anthony, London (44) 20-7176-7010; [email protected]

SNS REAAL Insurance Operations Ratings Raised To 'A-'; Outlook Negative

Research Update: SNS REAAL Insurance Operations Ratings Raised To 'A-'; Outlook Negative Primary Credit Analyst: Mark D Nicholson, London (44) 20-7176-7991; [email protected] Secondary

Research Update: SNS REAAL Insurance Operations Ratings Raised To 'A-'; Outlook Negative Primary Credit Analyst: Mark D Nicholson, London (44) 20-7176-7991; [email protected] Secondary

Stand-Alone Credit Profiles: One Component Of A Rating

General Criteria: Stand-Alone Credit Profiles: One Component Of A Rating Criteria Officer, EMEA Corporates: Emmanuel Dubois-Pelerin, Paris (33) 1-4420-6673; [email protected]

General Criteria: Stand-Alone Credit Profiles: One Component Of A Rating Criteria Officer, EMEA Corporates: Emmanuel Dubois-Pelerin, Paris (33) 1-4420-6673; [email protected]

Rating Research Services

Rating Research Services Media Release: Ratings On Taiwan Mobile Co. Ltd. Affirmed On Sustainable Market Position; Outlook Stable Primary Credit Analyst: Anne Kuo, CFA; (886) 2 8722-5829; [email protected]

Rating Research Services Media Release: Ratings On Taiwan Mobile Co. Ltd. Affirmed On Sustainable Market Position; Outlook Stable Primary Credit Analyst: Anne Kuo, CFA; (886) 2 8722-5829; [email protected]

Lear Corp.'s Recovery Rating Profile

Recovery Report: Lear Corp.'s Recovery Rating Profile Primary Credit Analyst: Lawrence Orlowski, CFA, New York (1) 212-438-1000; [email protected] Recovery Analyst: Greg Maddock, New

Recovery Report: Lear Corp.'s Recovery Rating Profile Primary Credit Analyst: Lawrence Orlowski, CFA, New York (1) 212-438-1000; [email protected] Recovery Analyst: Greg Maddock, New

Vienna Insurance Group AG Wiener Versicherung Gruppe

Summary: Vienna Insurance Group AG Wiener Versicherung Gruppe Primary Credit Analyst: Johannes Bender, Frankfurt (49) 69-33-999-196; [email protected] Secondary Contact: Ralf Bender,

Summary: Vienna Insurance Group AG Wiener Versicherung Gruppe Primary Credit Analyst: Johannes Bender, Frankfurt (49) 69-33-999-196; [email protected] Secondary Contact: Ralf Bender,

Companhia Energetica de Minas Gerais Upgraded To 'BB+' From 'BB' On Stronger Business Risk Profile, Outlook Stable

Research Update: Companhia Energetica de Minas Gerais Upgraded To 'BB+' From 'BB' On Stronger Business Risk Profile, Outlook Stable Primary Credit Analyst: Alejandro Gomez Abente, Sao Paulo (55) 11-3039-9741;

Research Update: Companhia Energetica de Minas Gerais Upgraded To 'BB+' From 'BB' On Stronger Business Risk Profile, Outlook Stable Primary Credit Analyst: Alejandro Gomez Abente, Sao Paulo (55) 11-3039-9741;

Evaluating Insurers Enterprise Risk Management Practice

Evaluating Insurers Enterprise Risk Management Practice Li Cheng, CFA, FRM, FSA Director Financial Services Ratings October 3, 2013 Permission to reprint or distribute any content from this presentation

Evaluating Insurers Enterprise Risk Management Practice Li Cheng, CFA, FRM, FSA Director Financial Services Ratings October 3, 2013 Permission to reprint or distribute any content from this presentation

Tri-Township Consolidated School Building Corp., Indiana Tri-Township Consolidate School Corp.; School State Program

Summary: Tri-Township Consolidated School Building Corp., Indiana Tri-Township Consolidate School Corp.; School State Program Primary Credit Analyst: Ryan Schultz, Chicago (1) 312-233-7066; [email protected]

Summary: Tri-Township Consolidated School Building Corp., Indiana Tri-Township Consolidate School Corp.; School State Program Primary Credit Analyst: Ryan Schultz, Chicago (1) 312-233-7066; [email protected]

German Utility RWE Downgraded To 'BBB-/A-3'; Outlook Negative

Research Update: German Utility RWE Downgraded To 'BBB-/A-3'; Outlook Negative Primary Credit Analyst: Vittoria Ferraris, Milan (39) 02-72111-207; [email protected] Secondary Contact: Tobias

Research Update: German Utility RWE Downgraded To 'BBB-/A-3'; Outlook Negative Primary Credit Analyst: Vittoria Ferraris, Milan (39) 02-72111-207; [email protected] Secondary Contact: Tobias

Workshop B: Credit Spread Trends In The Energy Sector

Workshop B: Credit Spread Trends In The Energy Sector James West Director, FIOTC Product Management 26 November, 2014 Permission to reprint or distribute any content from this presentation requires the

Workshop B: Credit Spread Trends In The Energy Sector James West Director, FIOTC Product Management 26 November, 2014 Permission to reprint or distribute any content from this presentation requires the

Duke Energy International Geracao Paranapanema 'BBB-' Global And 'braaa' National Scale Ratings Affirmed

Research Update: Duke Energy International Geracao Paranapanema 'BBB-' Global And 'braaa' National Scale Ratings Affirmed Primary Credit Analyst: Sergio Fuentes, Buenos Aires (54) 114-891-2131; [email protected]

Research Update: Duke Energy International Geracao Paranapanema 'BBB-' Global And 'braaa' National Scale Ratings Affirmed Primary Credit Analyst: Sergio Fuentes, Buenos Aires (54) 114-891-2131; [email protected]

Methodology: Business Risk/Financial Risk Matrix Expanded

Criteria Corporates General: Methodology: Business Risk/Financial Risk Matrix Expanded Criteria Officer: Mark Puccia, Managing Director, New York (1) 212-438-7233; [email protected] Table

Criteria Corporates General: Methodology: Business Risk/Financial Risk Matrix Expanded Criteria Officer: Mark Puccia, Managing Director, New York (1) 212-438-7233; [email protected] Table

Highlands Ranch Metropolitan District, Colorado; General Obligation

Summary: Highlands Ranch Metropolitan District, Colorado; General Obligation Primary Credit Analyst: Bryan A Moore, San Francisco (1) 415-371-5077; [email protected] Secondary Contact: Lisa

Summary: Highlands Ranch Metropolitan District, Colorado; General Obligation Primary Credit Analyst: Bryan A Moore, San Francisco (1) 415-371-5077; [email protected] Secondary Contact: Lisa

China Life Insurance Co. Ltd.

Primary Credit Analyst: Connie Wong, Singapore (65) 6239-6353; [email protected] Secondary Contact: Philip P Chung, CFA, Singapore (65) 6239-6343; [email protected] Table

Primary Credit Analyst: Connie Wong, Singapore (65) 6239-6353; [email protected] Secondary Contact: Philip P Chung, CFA, Singapore (65) 6239-6343; [email protected] Table

Sul America Upgraded To 'BBB-' And Sul America Companhia Nacional de Seguros To 'BBB+' Under New Criteria Review

Research Update: Sul America Upgraded To 'BBB-' And Sul America Companhia Nacional de Seguros To 'BBB+' Under New Criteria Review Primary Credit Analyst: Suzane M Iamamoto, Sao Paulo (55) 11-3039-9728;

Research Update: Sul America Upgraded To 'BBB-' And Sul America Companhia Nacional de Seguros To 'BBB+' Under New Criteria Review Primary Credit Analyst: Suzane M Iamamoto, Sao Paulo (55) 11-3039-9728;

South Padre Island, Texas; General Obligation

Summary: South Padre Island, Texas; General Obligation Primary Credit Analyst: Jim Tchou, New York (1) 212-438-3821; [email protected] Secondary Contact: Sarah L Smaardyk, Dallas (1) 214-871-1428;

Summary: South Padre Island, Texas; General Obligation Primary Credit Analyst: Jim Tchou, New York (1) 212-438-3821; [email protected] Secondary Contact: Sarah L Smaardyk, Dallas (1) 214-871-1428;

Italian Veneto Banca 'BB/B' Ratings Affirmed And Removed From CreditWatch Negative Following Review; Outlook Negative

Research Update: Italian Veneto Banca 'BB/B' Ratings Affirmed And Removed From CreditWatch Negative Following Review; Outlook Negative Table Of Contents Overview Rating Action Rationale Outlook Ratings

Research Update: Italian Veneto Banca 'BB/B' Ratings Affirmed And Removed From CreditWatch Negative Following Review; Outlook Negative Table Of Contents Overview Rating Action Rationale Outlook Ratings

Revised Criteria for Rating Nonbank Financial Institutions And Financial Services Companies

Revised Criteria for Rating Nonbank Financial Institutions And Financial Services Companies Financial Institutions Ratings Live Webcast: December 17, 2014 www.spratings.com/nbficriteria Permission to reprint

Revised Criteria for Rating Nonbank Financial Institutions And Financial Services Companies Financial Institutions Ratings Live Webcast: December 17, 2014 www.spratings.com/nbficriteria Permission to reprint

Codelco Rating Outlook Revised To Negative On Lower Copper Prices, 'AA-' Rating Affirmed

Research Update: Codelco Rating Outlook Revised To Negative On Lower Copper Prices, 'AA-' Rating Affirmed Primary Credit Analyst: Diego H Ocampo, Sao Paulo (55) 11-3039-9769; [email protected]

Research Update: Codelco Rating Outlook Revised To Negative On Lower Copper Prices, 'AA-' Rating Affirmed Primary Credit Analyst: Diego H Ocampo, Sao Paulo (55) 11-3039-9769; [email protected]

Largest South African Non-Life Insurer, Santam Ltd., Assigned 'A-' Long-Term And 'zaaa' National Scale Ratings

Research Update: Largest South African Non-Life Insurer, Santam Ltd., Assigned 'A-' Long-Term And 'zaaa' National Scale Ratings Primary Credit Analyst: Neil Gosrani, London (44) 20-7176-7112; [email protected]

Research Update: Largest South African Non-Life Insurer, Santam Ltd., Assigned 'A-' Long-Term And 'zaaa' National Scale Ratings Primary Credit Analyst: Neil Gosrani, London (44) 20-7176-7112; [email protected]

UBI Banca Ratings Lowered To 'BBB-/A-3' On Heightened Economic And Industry Risks In Italy; Outlook Negative

Research Update: UBI Banca Ratings Lowered To 'BBB-/A-3' On Heightened Economic And Industry Risks In Italy; Outlook Negative Analytical Group Contact: Financial Institutions Ratings Europe; [email protected]

Research Update: UBI Banca Ratings Lowered To 'BBB-/A-3' On Heightened Economic And Industry Risks In Italy; Outlook Negative Analytical Group Contact: Financial Institutions Ratings Europe; [email protected]