Methodology For Calculating Damages in the Victim Compensation Fund

|

|

|

- Adela Gordon

- 10 years ago

- Views:

Transcription

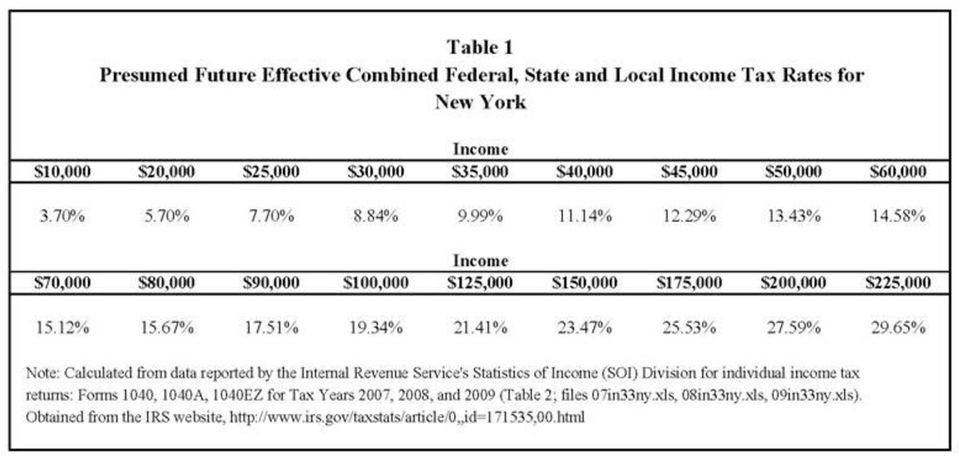

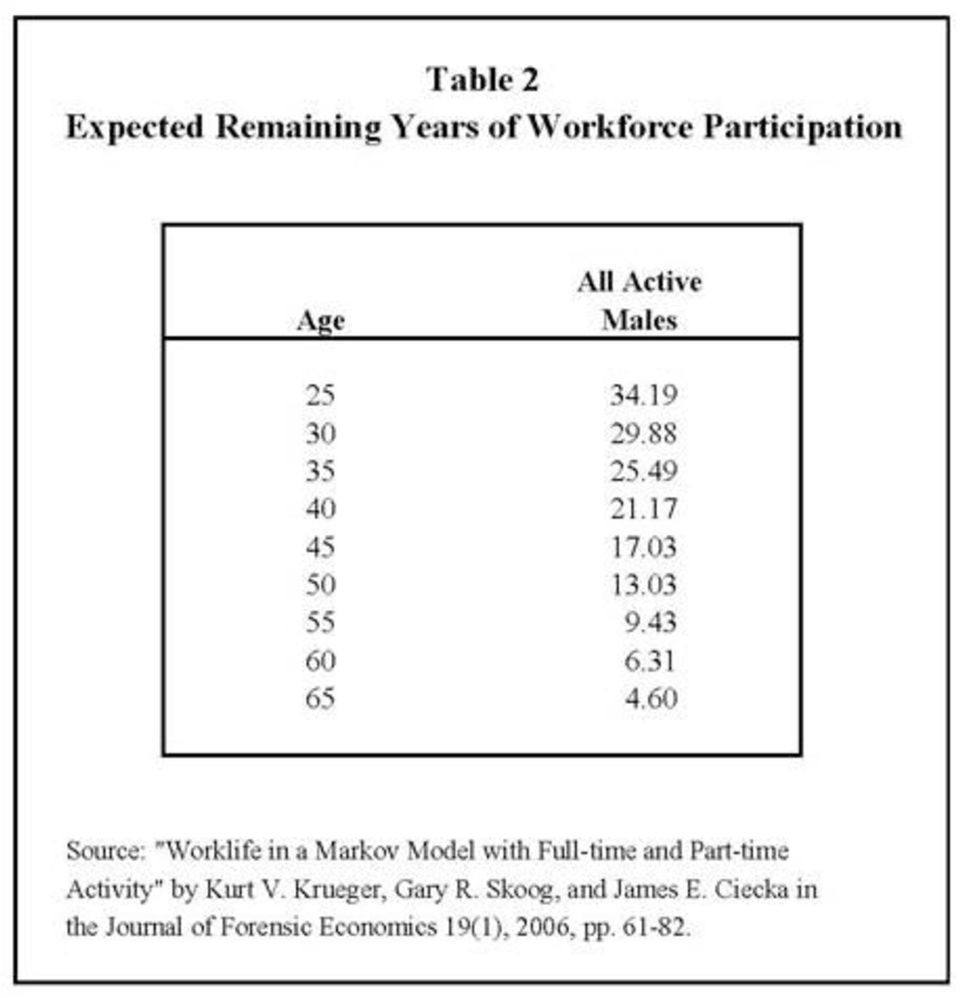

1 Methodology For Calculating Damages in the Victim Compensation Fund The calculation of presumed economic loss will generally follow the guidelines established in the original VCF. The Special Master will continue to review relevant developments that may affect the calculation of economic loss and will post any comments or updates. In general, the presumed economic loss both for claims on behalf of Deceased individuals and for claims of injured Claimants who are unable to work or whose earnings capacity has decreased as a result of the Claimant's disability due to the eligible conditions will be determined based on the individual's previous work history, compensation level and age. In general, the VCF will use the following procedures and assumptions for determining economic loss: 1. Establish the Decedent's or injured Claimant's age and compensable income at death or at the time the Decedent or injured Claimant was unable to work or had to reduce work as a result of eligible conditions. 1 Income will be determined based on the documents submitted with the claim. Generally, the Special Master will consider the three calendar years of employment history before the Decedent's death or decrease in the Decedent's or injured Claimant's earnings capacity as a result of the Decedent's or injured Claimant's disability due to the eligible condition(s). However, the Special Master may consider other factors or other years or combinations of years in evaluating the claim. 2. Determine after-tax compensable income by applying the average effective combined Federal, State and local income tax rate for the Decedent's or injured Claimant's income bracket currently applicable in the State of the Decedent's or injured Claimant's domicile for tax purposes. The Special Master will consider the Decedent's or injured Claimant's tax returns as well as effective income tax rates derived from published Internal Revenue Service (IRS) data on selected income and tax items for Individual Income Tax Returns by State. 2 Effective income tax rates derived from IRS data for New York are attached as Table Add the value of employer-provided benefits. These benefits will be set at actual levels if data are provided. If the claimant does not provide data, the pension is assumed at 4.6% of pension-eligible compensable income and medical benefits are assumed to be $5,242 per year in current year dollars and will be adjusted for applicable inflation. (To prepare the presumed award tables, the Special Master assumed that individuals would have benefits equal to 4.6% of compensable income and medical benefits of $5,242 per year.) 4. Determine a measure of the Decedent's or injured Claimant's expected remaining years of workforce participation using the tabulated work-life expectancies for the Decedent's or injured Claimant's age at the time of death or at the time the Decedent or injured Claimant was unable to work or had to reduce work as a result of eligible conditions contained in the publication, "Worklife in a Markov Model with Full-time and Part-time Activity" by Kurt V. Krueger, Gary R. Skoog, and James E.

2 Ciecka in the Journal of Forensic Economics, 19 (1) 2006, pp These are the most recent and generally accepted tables of work-life expectancy regarding the general population available. Work-life expectancies are based on actual experiences and behavior of the general population and measure the estimated remaining time in years an individual of a given age will be in the labor force (either employed or actively seeking work), allowing for age-specific mortality risks and rates of workforce transitions. The Special Master will use the expected work-life for Active Males, with a full-time beginning labor force state, to compute expected remaining years of workforce participation for both male and female Decedents and injured Claimants. The worklife expectancies are attached as Table 2. Because published estimated work-life expectancies by gender are lower for women than men, this specification increases the duration of estimated foregone earnings, and thus presumed economic losses, for female Decedents and injury Claimants and was implemented by the Special Master to accommodate for potential increases in labor force participation rates of women. 5. Project compensable income and benefits through the Decedent's or injured Claimant's expected work-life using growth rates that incorporate an annual inflationary or cost-of-living component, an annual real overall productivity or scale adjustment in excess of inflation, and an annual real life-cycle or age-specific increase derived using data on average full-time year around earnings by age bracket from the 2010 Current Population Survey (CPS), a monthly survey of households conducted by the Bureau of the Census for the Bureau of Labor Statistics. This survey is widely recognized as the primary source of data on employment status and workforce characteristics of the civilian non-institutional population ages 16 years and older. Because age-specific observed life-cycle increases for all males were higher than observed life-cycle increases for both men and women combined, the Special Master elected to incorporate the life-cycle increases for males into earnings growth for all Decedents or injured Claimants, both male and female. Independent of life-cycle increases, inflation and real overall productivity increases of 2% and 1%, respectively, were applied each year. These rates of increase are consistent with the long-term relationship between economy-wide wage growth and risk-free interest rates, which currently reflect lowered inflationary expectations. A schedule containing age-specific earnings growth rates reflecting the combined inflation, overall productivity and life-cycle increases is attached as Table 3. The Special Master has determined that individual age-specific growth rates, rather than growth independent on a particular age bracket at death, better reflects the expected pattern of earnings over one's career 3 and results in more equitable and consistent projections for Decedents or injured Claimants close to each other in age with otherwise similar family and employment characteristics.

3 6. To better reflect contingencies that the Decedents or injured Claimants would have faced, all future earnings amounts will be adjusted for a factor to account for the risk of unemployment because lifetime jobs are not representative of the modern economy. This adjustment is made because work-life expectancies are based on years of expected workforce participation, which, as defined by the Bureau of Labor Statistics, include periods an individual is either working or seeking work. Historical unemployment rates were examined and a reduction factor of 6% was applied to presumed earnings to account for this risk For claims for Deceased individuals, subtract from annual projected compensable income and benefits the Decedent's share of household expenditures or consumption as a percentage of income, using expenditure data by income level obtained from "Table 2. Income before taxes: Average annual expenditures and characteristics, Consumer Expenditure Survey, 2009," published by the Bureau of Labor Statistics (BLS). This subtraction is a standard adjustment in evaluating loss of earnings in wrongful death claims because some amount of the income the Decedent would have contributed to the household would have been consumed personally by the deceased and not available to other household members. A Decedent's expenditures were calculated as a share, based on household size, of certain expenditure categories. For married or single with dependents, these expenditure categories include Food, Apparel & Services, Transportation, Entertainment, Personal Care Products and Services, and Miscellaneous. For single without dependents, Housing, Education and Health are also included. 5 For lower income categories where total expenditures exceed income, expenditures were scaled to income, so as not to reduce income for expenses potentially met by other forms of support. This approach was intended to avoid a penalty to the claimant. Table 4 shows calculated consumption rates by income bracket and for various household sizes. In determining household size for claims for deceased individuals, the Special Master will assume that children will remain in the household through age 18. Consumption rates calculated using alternative techniques were considered but found to produce higher personal consumption rates and were not ultimately used to determine the Decedent's household consumption offset. Although the consumption rates determined from BLS data actually represent household expenditures as a percent of before-tax household income, the actual consumption reduction used to determine the Decedent's personal expenditures was calculated as a percent of lower after-tax income, which significantly reduces the resulting offset. 6 In addition, the Decedent's or injured Claimant's consumption is determined as a share of the Decedent's or injured Claimant's own earnings only, rather than the standard share of total household earnings. This further lessens the resulting subtraction, compared to personal consumption offsets typically applied in litigation, if there are other earners in the household.

4 8. Calculate the present value of projected compensable income and benefits using discount rates based on a weighted average of historical yields on mid- to longterm U.S. Treasury securities, adjusted for income taxes using a mid-range effective tax rate. 7 Because the period of presumed economic losses is either longer or shorter, depending on the Decedent's or injured Claimant's age, the present value calculations are performed using yields on a blend of securities with longer or shorter times to maturity. For computational efficiency, three blended after-tax discount rates were used, depending on the Decedent's or injured Claimant's age as of date of death or time the Decedent or injured Claimant was unable to work or had to reduce work as a result of eligible conditions, and assumed to apply for all years forward. These rates are shown on Table 5, attached. 8 The present value adjustments will be based on the period of presumed economic loss (which is in turn based on the age of the Decedent or injured Claimant). 9. The computation methodology adopts a number of assumptions implemented to facilitate analysis on a large scale. When viewed in total, these assumptions are designed to benefit the claimants and are more favorable than the standard assumptions typically applied in litigation. For example, the Special Master considered that over the course of their projected careers, younger Decedent's or injured Claimant's could expect to cross into higher income brackets, and be subject to corresponding higher income tax rates, on account of experience-based real lifetime earnings growth in excess of economy-wide national wage increases. To calculate presumed economic losses, however, whatever income tax rate corresponded to the Decedent's or injured Claimant's determined compensable income bracket as of date of death or time the Decedent or injured Claimant was unable to work or had to reduce work as a result of eligible conditions was assumed to apply for the remainder of the Decedent's or injured Claimant's career, without increase. Likewise, the calculations of presumed economic losses also assume that the personal consumption percent corresponding to the Decedent's or injured Claimant's determined compensable income bracket as of date of death or time the Decedent or injured Claimant was unable to work or had to reduce work as a result of eligible conditions applies for the remainder of the Decedent's or injured Claimant's career, without decrease. It was determined that the net effect of these and other facilitating assumptions was to increase the potential amount of presumed economic loss to the benefit of the claimant. Please click here for detailed Economic Loss Illustrations. 1 Income up to the IRS 98th percentile of wage earners is considered. 2 Average combined effective income tax rates by earnings bracket were calculated based on an analysis of IRS data for the most recent tax years available: 2007, 2008, and Real life-cycle increases are typically higher in the earlier stages of one's career, one reason being unrealized opportunities for advancement and promotion that individuals in later stages of their careers have already experienced. During the course of an individual's career, the rate of annual real life-cycle growth tends to gradually decline until a peak real earnings level is attained. Although CPS and other data used to study lifetime earnings profiles indicate that peak real earnings typically decline at some point, in calculating life-cycle earnings

5 growth in excess of inflation and overall productivity adjustments for Decedents and injured Claimants, the Special Master has assumed that peak earnings are maintained. 4 Application of individualized unemployment rates by age or occupation was infeasible and determined to be unnecessary. 5 Other standard expenditure categories sometimes included in litigation, namely Reading, Cash Contributions, Alcoholic Beverages, and Tobacco Products, were excluded. 6 These alternative techniques included an analysis of BLS data on household expenditures reported by household size, with expenditure categories allocated equally among household members or allocated according to the methodology suggested by authors Robert Patton & David Nelson in their 1991 Journal of Forensic Economics article, "Estimating Personal Consumption Costs in Wrongful Death Cases." 7 The tax rate used to determine after-tax interest rates is the computed combined Federal, State and Local income tax rate of 15.1% for New York for the $70,000 earnings bracket. Although it is recognized that a different after-tax interest rate could theoretically be calculated for each age, income, and state combination, such a computation was impracticable for the large-scale valuations to be undertaken here. It was determined that the benefit to the claimants of calculating the Decedent's personal consumption offset as a percent of after-tax individual earnings more than outweighed the potential effect of discounting future amounts by incomespecific after-tax discount rates. Moreover, computation of the after-tax discount rate using a relatively high combined New York income tax rate, compared to other states, results in a lower after-tax discount rate. The lower the after-tax discount rate, the higher the present value of presumed economic loss. 8 The blended discount rates, before tax adjustment, shown on Table 5 imply real interest rates in excess of inflation of 2.1%. 1.8%, and 1.2%, depending on the average time to maturity consistent with the average duration of presumed losses.

6

7

8

9

A Comparison of Period and Cohort Life Tables Accepted for Publication in Journal of Legal Economics, 2011, Vol. 17(2), pp. 99-112.

, pp. 99-112.") A Comparison of Period and Cohort Life Tables Accepted for Publication in Journal of Legal Economics, 2011, Vol. 17(2), pp. 99-112. David G. Tucek Value Economics, LLC 13024 Vinson Court St. Louis, MO

A Comparison of Period and Cohort Life Tables Accepted for Publication in Journal of Legal Economics, 2011, Vol. 17(2), pp. 99-112. David G. Tucek Value Economics, LLC 13024 Vinson Court St. Louis, MO

Table of Contents. Overview of Data Needed by the Economist. Determining the Value of Employer Paid Benefits

Table of Contents Chapter 1 Chapter 2 Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Chapter 10 Chapter 11 Chapter 12 Chapter 13 Chapter 14 Chapter 15 Chapter 16 Chapter 17 The Forensic

Table of Contents Chapter 1 Chapter 2 Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Chapter 10 Chapter 11 Chapter 12 Chapter 13 Chapter 14 Chapter 15 Chapter 16 Chapter 17 The Forensic

SAMPLE WRONGFUL DEATH ECONOMIC DAMAGES REPORT. Mary Jones

SAMPLE WRONGFUL DEATH ECONOMIC DAMAGES REPORT Of Mary Jones In the case: Elizabeth Jones, as Administratrix of the Estate of Mary Jones, Deceased v. Hospital Defendant Cause No. 2005-ABCD Prepared By:

SAMPLE WRONGFUL DEATH ECONOMIC DAMAGES REPORT Of Mary Jones In the case: Elizabeth Jones, as Administratrix of the Estate of Mary Jones, Deceased v. Hospital Defendant Cause No. 2005-ABCD Prepared By:

Presented by: Robert Vance, CPA, ABV, CFF, CVA, CFP Forensic & Valuation Services, PLC 901-507-9173 www.forensicval.com rvance@forensicval.

Presented by: Robert Vance, CPA, ABV, CFF, CVA, CFP Forensic & Valuation Services, PLC 901-507-9173 www.forensicval.com [email protected] DISCLAIMER All rights reserved. No part of this work covered

Presented by: Robert Vance, CPA, ABV, CFF, CVA, CFP Forensic & Valuation Services, PLC 901-507-9173 www.forensicval.com [email protected] DISCLAIMER All rights reserved. No part of this work covered

1960-61. United States

61-61 United States By, the U.S. population had surpassed 179 million, a gain of 19.0 percent from. The median age had decreased to 29.5 (28.7 for men and.3 for women), the first decline since 1900. The

61-61 United States By, the U.S. population had surpassed 179 million, a gain of 19.0 percent from. The median age had decreased to 29.5 (28.7 for men and.3 for women), the first decline since 1900. The

Income Replacement Adequacy in the Texas Workers Compensation System

Income Replacement Adequacy in the Texas Workers Compensation System Texas Department of Insurance Workers Compensation Research and Evaluation Group August 2010 1 Five Types of Income Benefits Under the

Income Replacement Adequacy in the Texas Workers Compensation System Texas Department of Insurance Workers Compensation Research and Evaluation Group August 2010 1 Five Types of Income Benefits Under the

Venue Matters: A Comparison of Hypothetical Damage Awards In Six States. Mitch Marino and Matthew Marlin. I. Introduction

Venue Matters: A Comparison of Hypothetical Damage Awards In Six States Mitch Marino and Matthew Marlin I. Introduction A tort is an injury caused either willingly or through someone s negligence and includes

Venue Matters: A Comparison of Hypothetical Damage Awards In Six States Mitch Marino and Matthew Marlin I. Introduction A tort is an injury caused either willingly or through someone s negligence and includes

Research Note: Assessing Household Service Losses with Joint Survival Probabilities

Research Note: Assessing Household Service Losses with Joint Survival Probabilities Victor A. Matheson and Robert A. Baade December 2006 COLLEGE OF THE HOLY CROSS, DEPARTMENT OF ECONOMICS FACULTY RESEARCH

Research Note: Assessing Household Service Losses with Joint Survival Probabilities Victor A. Matheson and Robert A. Baade December 2006 COLLEGE OF THE HOLY CROSS, DEPARTMENT OF ECONOMICS FACULTY RESEARCH

Old-Age and Survivors Insurance: Insured Workers and Their Representation in Claims

Old-Age and Survivors Insurance: Insured Workers and Their Representation in Claims By George E. Immerwahr and Harry Mehlman* ALMOST 4 million persons are estimated to have been insured under Federal old-age

Old-Age and Survivors Insurance: Insured Workers and Their Representation in Claims By George E. Immerwahr and Harry Mehlman* ALMOST 4 million persons are estimated to have been insured under Federal old-age

COLLEGE ENROLLMENT AND WORK ACTIVITY OF 2014 HIGH SCHOOL GRADUATES

For release 10:00 a.m. (EDT) Thursday, April 16, 2015 USDL-15-0608 Technical information: (202) 691-6378 [email protected] www.bls.gov/cps Media contact: (202) 691-5902 [email protected] COLLEGE ENROLLMENT

For release 10:00 a.m. (EDT) Thursday, April 16, 2015 USDL-15-0608 Technical information: (202) 691-6378 [email protected] www.bls.gov/cps Media contact: (202) 691-5902 [email protected] COLLEGE ENROLLMENT

Estimating Lost Secondary Childcare in Wrongful Death Cases Using Data From the American Time Use Survey (ATUS) Mark W. Erwin, M.A., J.D.

Mark W. Erwin, M.A., J.D.") Estimating Lost Secondary Childcare in Wrongful Death Cases Using Data From the American Time Use Survey (ATUS) Mark W. Erwin, M.A., J.D. INTRODUCTION When a parent dies, the childcare that they would

Estimating Lost Secondary Childcare in Wrongful Death Cases Using Data From the American Time Use Survey (ATUS) Mark W. Erwin, M.A., J.D. INTRODUCTION When a parent dies, the childcare that they would

Income Sustainability through Educational Attainment

Journal of Education and Training Studies Vol. 3, No. 1; January 2015 ISSN 2324-805X E-ISSN 2324-8068 Published by Redfame Publishing URL: http://jets.redfame.com Income Sustainability through Educational

Journal of Education and Training Studies Vol. 3, No. 1; January 2015 ISSN 2324-805X E-ISSN 2324-8068 Published by Redfame Publishing URL: http://jets.redfame.com Income Sustainability through Educational

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE CBO. The Distribution of Household Income and Federal Taxes, 2008 and 2009

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Percent 70 The Distribution of Household Income and Federal Taxes, 2008 and 2009 60 50 Before-Tax Income Federal Taxes Top 1 Percent 40 30 20 81st

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Percent 70 The Distribution of Household Income and Federal Taxes, 2008 and 2009 60 50 Before-Tax Income Federal Taxes Top 1 Percent 40 30 20 81st

The Big Payoff: Educational Attainment and Synthetic Estimates of Work-Life Earnings

The Big Payoff: Educational Attainment and Synthetic Estimates of Work-Life Earnings Special Studies Issued July 2002 P23-210 Does going to school pay off? Most people think so. Currently, almost 90 percent

The Big Payoff: Educational Attainment and Synthetic Estimates of Work-Life Earnings Special Studies Issued July 2002 P23-210 Does going to school pay off? Most people think so. Currently, almost 90 percent

RETIREMENT SECURITY. Better Information on Income Replacement Rates Needed to Help Workers Plan for Retirement

United States Government Accountability Office Report to Congressional Requesters March 2016 RETIREMENT SECURITY Better Information on Income Replacement Rates Needed to Help Workers Plan for Retirement

United States Government Accountability Office Report to Congressional Requesters March 2016 RETIREMENT SECURITY Better Information on Income Replacement Rates Needed to Help Workers Plan for Retirement

A New Way To Assess Damages For Loss Of Future Earnings

A New Way To Assess Damages For Loss Of Future Earnings Richard Lewis, Robert McNabb and Victoria Wass describe research which reveals claimants to have been under-compensated by tort This article summarises

A New Way To Assess Damages For Loss Of Future Earnings Richard Lewis, Robert McNabb and Victoria Wass describe research which reveals claimants to have been under-compensated by tort This article summarises

College graduates earn more money than workers with

The Financial Value of a Higher Education By Mark Kantrowitz Mark Kantrowitz is the founder and publisher of FinAid.org and author of FastWeb College Gold. Five years have passed since the U.S. Census

The Financial Value of a Higher Education By Mark Kantrowitz Mark Kantrowitz is the founder and publisher of FinAid.org and author of FastWeb College Gold. Five years have passed since the U.S. Census

Labor Force Analysis

Labor Force Analysis Greater Concordia Area and Cloud County, Kansas October 2012 Prepared by Center for Economic Development and Business Research W. Frank Barton School of Business Wichita State University

Labor Force Analysis Greater Concordia Area and Cloud County, Kansas October 2012 Prepared by Center for Economic Development and Business Research W. Frank Barton School of Business Wichita State University

Undergraduate Degree Completion by Age 25 to 29 for Those Who Enter College 1947 to 2002

Undergraduate Degree Completion by Age 25 to 29 for Those Who Enter College 1947 to 2002 About half of those who start higher education have completed a bachelor's degree by the ages of 25 to 29 years.

Undergraduate Degree Completion by Age 25 to 29 for Those Who Enter College 1947 to 2002 About half of those who start higher education have completed a bachelor's degree by the ages of 25 to 29 years.

CHAPTER 6 DEFINED BENEFIT AND DEFINED CONTRIBUTION PLANS: UNDERSTANDING THE DIFFERENCES

CHAPTER 6 DEFINED BENEFIT AND DEFINED CONTRIBUTION PLANS: UNDERSTANDING THE DIFFERENCES Introduction Both defined benefit and defined contribution pension plans offer various advantages to employers and

CHAPTER 6 DEFINED BENEFIT AND DEFINED CONTRIBUTION PLANS: UNDERSTANDING THE DIFFERENCES Introduction Both defined benefit and defined contribution pension plans offer various advantages to employers and

Indicator 3: Fatal Work-Related Injuries

Indicator 3: Fatal Work-Related Injuries Significance i Fatal work-related injuries are defined as injuries that occur at work and result in death. Each year, over 4,600 cases of work-related fatalities

Indicator 3: Fatal Work-Related Injuries Significance i Fatal work-related injuries are defined as injuries that occur at work and result in death. Each year, over 4,600 cases of work-related fatalities

Loss of Self-Employed Earning Capacity in Wrongful Death or Major Accident of the Self-Employed

Published in Journal of Legal Economics,Vol.12, No 1, Spring/Summer 2002, pp7-21. Copyright 2004 Loss of Self-Employed Earning Capacity in Wrongful Death or Major Accident of the Self-Employed By Lawrence

Published in Journal of Legal Economics,Vol.12, No 1, Spring/Summer 2002, pp7-21. Copyright 2004 Loss of Self-Employed Earning Capacity in Wrongful Death or Major Accident of the Self-Employed By Lawrence

Estimating economic loss - recent developments. Richard Cumpston

Estimating economic loss - recent developments Richard Cumpston This paper has been written for presentation at the Victorian State Conference of the Australian Plaintiff Lawyers Association, 23 to 25

Estimating economic loss - recent developments Richard Cumpston This paper has been written for presentation at the Victorian State Conference of the Australian Plaintiff Lawyers Association, 23 to 25

SOCIETY OF ACTUARIES THE AMERICAN ACADEMY OF ACTUARIES RETIREMENT PLAN PREFERENCES SURVEY REPORT OF FINDINGS. January 2004

SOCIETY OF ACTUARIES THE AMERICAN ACADEMY OF ACTUARIES RETIREMENT PLAN PREFERENCES SURVEY REPORT OF FINDINGS January 2004 Mathew Greenwald & Associates, Inc. TABLE OF CONTENTS INTRODUCTION... 1 SETTING

SOCIETY OF ACTUARIES THE AMERICAN ACADEMY OF ACTUARIES RETIREMENT PLAN PREFERENCES SURVEY REPORT OF FINDINGS January 2004 Mathew Greenwald & Associates, Inc. TABLE OF CONTENTS INTRODUCTION... 1 SETTING

Prepared by: Andrew Sum Ishwar Khatiwada With Sheila Palma. Center for Labor Market Studies Northeastern University

The Employment Experiences and College Labor Market Job Characteristics of Young Adult Associate Degree and Bachelor Degree Recipients in Massachusetts and the U.S. Prepared by: Andrew Sum Ishwar Khatiwada

The Employment Experiences and College Labor Market Job Characteristics of Young Adult Associate Degree and Bachelor Degree Recipients in Massachusetts and the U.S. Prepared by: Andrew Sum Ishwar Khatiwada

5. Defined Benefit and Defined Contribution Plans: Understanding the Differences

5. Defined Benefit and Defined Contribution Plans: Understanding the Differences Introduction Both defined benefit and defined contribution pension plans offer various advantages to employers and employees.

5. Defined Benefit and Defined Contribution Plans: Understanding the Differences Introduction Both defined benefit and defined contribution pension plans offer various advantages to employers and employees.

Health Insurance Coverage, Poverty, and Income of Veterans: 2000 to 2009

Health Insurance Coverage, Poverty, and Income of Veterans: 2 to 29 February 211 NCVAS National Center for Veterans Analysis and Statistics Data Source and Methods Data for this analysis come from years

Health Insurance Coverage, Poverty, and Income of Veterans: 2 to 29 February 211 NCVAS National Center for Veterans Analysis and Statistics Data Source and Methods Data for this analysis come from years

Assessment of Personal Injury Damages

Assessment of Personal Injury Damages Fifth Edition Christopher J. Bruce, Ph.D. Kelly A. Rathje, M.A. Laura J. Weir, M.A. f LexisNexis* Acknowledgments About the Authors Tables How to Use This Book v vii

Assessment of Personal Injury Damages Fifth Edition Christopher J. Bruce, Ph.D. Kelly A. Rathje, M.A. Laura J. Weir, M.A. f LexisNexis* Acknowledgments About the Authors Tables How to Use This Book v vii

Evaluating Economic Damages In Personal Injury. Christopher C. Pflaum, Ph.D. President Spectrum Economics, Inc.

Evaluating Economic Damages In Personal Injury by Christopher C. Pflaum, Ph.D. President Spectrum Economics, Inc. The dominant methodology for computing economic loss in personal injury cases is the "human

Evaluating Economic Damages In Personal Injury by Christopher C. Pflaum, Ph.D. President Spectrum Economics, Inc. The dominant methodology for computing economic loss in personal injury cases is the "human

2015 Veteran Economic Opportunity Report

215 Veteran Economic Opportunity Report Department of Veterans Affairs Executive Summary The Department of Veterans Affairs (VA) has a mission to help Veterans maximize their economic competitiveness,

215 Veteran Economic Opportunity Report Department of Veterans Affairs Executive Summary The Department of Veterans Affairs (VA) has a mission to help Veterans maximize their economic competitiveness,

ECONOMIC ANALYSIS OF CLAIM COSTS

ECONOMIC ANALYSIS OF CLAIM COSTS Prepared by Associated Economic Consultants Ltd. August 30, 2000 Table of Contents 1. INTRODUCTION...1 FIGURE 1...4 2. DEMOGRAPHIC AND ECONOMIC FACTORS...5 2.1 Population,

ECONOMIC ANALYSIS OF CLAIM COSTS Prepared by Associated Economic Consultants Ltd. August 30, 2000 Table of Contents 1. INTRODUCTION...1 FIGURE 1...4 2. DEMOGRAPHIC AND ECONOMIC FACTORS...5 2.1 Population,

ICI RESEARCH PERSPECTIVE

ICI RESEARCH PERSPECTIVE 1401 H STREET, NW, SUITE 1200 WASHINGTON, DC 20005 202-326-5800 WWW.ICI.ORG OCTOBER 2014 VOL. 20, NO. 6 WHAT S INSIDE 2 Introduction 2 Which Workers Want Retirement Benefits? 2

ICI RESEARCH PERSPECTIVE 1401 H STREET, NW, SUITE 1200 WASHINGTON, DC 20005 202-326-5800 WWW.ICI.ORG OCTOBER 2014 VOL. 20, NO. 6 WHAT S INSIDE 2 Introduction 2 Which Workers Want Retirement Benefits? 2

FAMILY LEAVE INSURANCE AND TEMPORARY DISABILITY INSURANCE PROGRAMS

FAMILY LEAVE INSURANCE AND TEMPORARY DISABILITY INSURANCE PROGRAMS The enactment P.L. 2008, chapter 17 on May 2, 2008 created the New Jersey Family Leave Insurance Program and required the Commissioner

FAMILY LEAVE INSURANCE AND TEMPORARY DISABILITY INSURANCE PROGRAMS The enactment P.L. 2008, chapter 17 on May 2, 2008 created the New Jersey Family Leave Insurance Program and required the Commissioner

Department of Veterans Affairs September 2010 Federal Employees and Veterans Benefits Liabilities Volume VI Chapter 7 0701 OVERVIEW...

VA Financial Policies and Procedures Federal Employees and Veterans Benefits Liabilities CHAPTER 7 0701 OVERVIEW...2 0702 POLICIES...3 0703 AUTHORITY AND REFERENCE...4 0704 ROLES AND RESPONSIBILITIES...5

VA Financial Policies and Procedures Federal Employees and Veterans Benefits Liabilities CHAPTER 7 0701 OVERVIEW...2 0702 POLICIES...3 0703 AUTHORITY AND REFERENCE...4 0704 ROLES AND RESPONSIBILITIES...5

Going Nowhere Workers Wages since the Mid-1970s

Going Nowhere Workers Wages since the Mid-1970s I n the late 1990s, many observers hoped that we had finally broken free of the slow income growth that had bogged down the American middle class for more

Going Nowhere Workers Wages since the Mid-1970s I n the late 1990s, many observers hoped that we had finally broken free of the slow income growth that had bogged down the American middle class for more

The Life-Cycle Motive and Money Demand: Further Evidence. Abstract

The Life-Cycle Motive and Money Demand: Further Evidence Jan Tin Commerce Department Abstract This study takes a closer look at the relationship between money demand and the life-cycle motive using panel

The Life-Cycle Motive and Money Demand: Further Evidence Jan Tin Commerce Department Abstract This study takes a closer look at the relationship between money demand and the life-cycle motive using panel

Fully Insured Pension Plan

Fully Insured Pension Plan Marketing Guide There are approximately 23 million small businesses in the U.S.* *Small Business Administration: Small Business Trends (sba.gov) The Market for Fully Insured

Fully Insured Pension Plan Marketing Guide There are approximately 23 million small businesses in the U.S.* *Small Business Administration: Small Business Trends (sba.gov) The Market for Fully Insured

College Enrollment by Age 1950 to 2000

College Enrollment by Age 1950 to 2000 Colleges compete with the labor market and other adult endeavors for the time and attention of young people in a hurry to grow up. Gradually, young adults drift away

College Enrollment by Age 1950 to 2000 Colleges compete with the labor market and other adult endeavors for the time and attention of young people in a hurry to grow up. Gradually, young adults drift away

7. Work Injury Insurance

7. Work Injury Insurance A. General Work injury insurance provides an insured person who is injured at work a right to receive a benefit or other defined assistance, in accordance with the nature of the

7. Work Injury Insurance A. General Work injury insurance provides an insured person who is injured at work a right to receive a benefit or other defined assistance, in accordance with the nature of the

Income Protection Benefits

Income Protection Benefits McAllen Independent School District Information About You Name: Social Security Number / Employee ID Number: Coverage Effective Date: Date of Birth: Date of Hire: Annual Salary:

Income Protection Benefits McAllen Independent School District Information About You Name: Social Security Number / Employee ID Number: Coverage Effective Date: Date of Birth: Date of Hire: Annual Salary:

Guide to Individual Disability Income. Insurance

About AHIP America s Health Insurance Plans is a national association representing nearly 1,300 members providing health benefits to more than 200 million Americans. AHIP and its predecessor organizations

About AHIP America s Health Insurance Plans is a national association representing nearly 1,300 members providing health benefits to more than 200 million Americans. AHIP and its predecessor organizations

West Virginia Department of Public Safety Death, Disability and Retirement Fund (Plan A)

") West Virginia Department of Public Safety Death, Disability and Retirement Fund (Plan A) Actuarial Valuation As of July 1, 2013 Prepared by: for the West Virginia Consolidated Public Retirement Board January

West Virginia Department of Public Safety Death, Disability and Retirement Fund (Plan A) Actuarial Valuation As of July 1, 2013 Prepared by: for the West Virginia Consolidated Public Retirement Board January

Seasonal Workers Under the Minnesota Unemployment Compensation Law

Seasonal Workers Under the Minnesota Unemployment Compensation Law EDWARD F. MEDLEY* THE PAYMENT of unemployment benefits to seasonal has raised practical and theoretical problems since unemployment compensation

Seasonal Workers Under the Minnesota Unemployment Compensation Law EDWARD F. MEDLEY* THE PAYMENT of unemployment benefits to seasonal has raised practical and theoretical problems since unemployment compensation

Report of the Actuary on the Annual Valuation of the Retirement System for Employees of the City of Cincinnati. Pension Report

Report of the Actuary on the Annual Valuation of the Retirement System for Employees of the City of Cincinnati Pension Report Prepared as of December 31, 2011 and Approved by the Board of Trustees on May

Report of the Actuary on the Annual Valuation of the Retirement System for Employees of the City of Cincinnati Pension Report Prepared as of December 31, 2011 and Approved by the Board of Trustees on May

Financial Review. 16 Selected Financial Data 18 Management s Discussion and Analysis of Financial Condition and Results of Operations

2011 Financial Review 16 Selected Financial Data 18 Management s Discussion and Analysis of Financial Condition and Results of Operations 82 Quantitative and Qualitative Disclosures About Market Risk 90

2011 Financial Review 16 Selected Financial Data 18 Management s Discussion and Analysis of Financial Condition and Results of Operations 82 Quantitative and Qualitative Disclosures About Market Risk 90

College Enrollment Hits All-Time High, Fueled by Community College Surge

Enrollment Hits All-Time High, Fueled by Community Surge FOR RELEASE: OCTOBER 29, 2009 Paul Taylor, Project Director Richard Fry, Senior Researcher Wendy Wang, Research Associate Daniel Dockterman, Research

Enrollment Hits All-Time High, Fueled by Community Surge FOR RELEASE: OCTOBER 29, 2009 Paul Taylor, Project Director Richard Fry, Senior Researcher Wendy Wang, Research Associate Daniel Dockterman, Research

Women s Participation in Education and the Workforce. Council of Economic Advisers

Women s Participation in Education and the Workforce Council of Economic Advisers Updated October 14, 214 Executive Summary Over the past forty years, women have made substantial gains in the workforce

Women s Participation in Education and the Workforce Council of Economic Advisers Updated October 14, 214 Executive Summary Over the past forty years, women have made substantial gains in the workforce

Calculating Changes in Worklife Expectancies and Lost Earnings in Personal Injury Cases

Calculating Changes in Worklife Expectancies and Lost Earnings in Personal Injury Cases Michael Nieswiadomy Eugene Silberberg Abstract This paper utilizes the Bureau of Labor Statistics (BLS) new worklife

Calculating Changes in Worklife Expectancies and Lost Earnings in Personal Injury Cases Michael Nieswiadomy Eugene Silberberg Abstract This paper utilizes the Bureau of Labor Statistics (BLS) new worklife

New Jersey Temporary Disability Benefits Law TDB

New Jersey Temporary Disability Benefits Law TDB Frequently Asked Questions General Questions - TDB What is TDB? TDB is the New Jersey Temporary Disability Benefits Law. This state-mandated Short Term

New Jersey Temporary Disability Benefits Law TDB Frequently Asked Questions General Questions - TDB What is TDB? TDB is the New Jersey Temporary Disability Benefits Law. This state-mandated Short Term

As the U.S. workforce comes to rely

Research Summary Expenditures of college-age students nonstudents Geoffrey D. Paulin As the U.S. workforce comes to rely increasingly on computer technology, including the Internet, higher levels of education

Research Summary Expenditures of college-age students nonstudents Geoffrey D. Paulin As the U.S. workforce comes to rely increasingly on computer technology, including the Internet, higher levels of education

GAO. UNEMPLOYMENT INSURANCE Receipt of Benefits Has Declined, with Continued Disparities for Low-Wage and Part-Time Workers

GAO For Release on Delivery Expected at 1:00 p.m. EDT Wednesday, September 19, 2007 United States Government Accountability Office Testimony Before the Subcommittee on Income Security and Family Support,

GAO For Release on Delivery Expected at 1:00 p.m. EDT Wednesday, September 19, 2007 United States Government Accountability Office Testimony Before the Subcommittee on Income Security and Family Support,

Discount Rates and Life Tables: A Review

Discount Rates and Life Tables: A Review Hugh Sarjeant is a consulting actuary and Paul Thomson is an actuarial analyst at Cumpston Sarjeant Pty Ltd Phone: 03 9642 2242 Email: [email protected]

Discount Rates and Life Tables: A Review Hugh Sarjeant is a consulting actuary and Paul Thomson is an actuarial analyst at Cumpston Sarjeant Pty Ltd Phone: 03 9642 2242 Email: [email protected]

How Social Security Benefits Are Computed: In Brief

How Social Security Benefits Are Computed: In Brief Noah P. Meyerson Analyst in Income Security February 4, 2015 Congressional Research Service 7-5700 www.crs.gov R43542 Summary With about $900 billion

How Social Security Benefits Are Computed: In Brief Noah P. Meyerson Analyst in Income Security February 4, 2015 Congressional Research Service 7-5700 www.crs.gov R43542 Summary With about $900 billion

An ageing workforce and workers compensation what are the implications, in particular with an increasing national retirement age?

An ageing workforce and workers compensation what are the implications, in particular with an increasing national retirement age? Prepared by Andrew McInerney Presented to the Institute of Actuaries of

An ageing workforce and workers compensation what are the implications, in particular with an increasing national retirement age? Prepared by Andrew McInerney Presented to the Institute of Actuaries of

Longevity insurance annuities are deferred annuities that. Longevity Insurance Annuities in 401(k) Plans and IRAs. article Retirement

Plans and IRAs. article Retirement") article Retirement Longevity Insurance Annuities in 401(k) Plans and IRAs What role should longevity insurance annuities play in 401(k) plans? This article addresses the question of whether participants,

article Retirement Longevity Insurance Annuities in 401(k) Plans and IRAs What role should longevity insurance annuities play in 401(k) plans? This article addresses the question of whether participants,

An update on the level and distribution of retirement savings

ASFA Research and Resource Centre An update on the level and distribution of retirement savings Ross Clare Director of Research March 2014 The Association of Superannuation Funds of Australia Limited (ASFA)

ASFA Research and Resource Centre An update on the level and distribution of retirement savings Ross Clare Director of Research March 2014 The Association of Superannuation Funds of Australia Limited (ASFA)

For Immediate Release

Household Income Trends May 2015 Issued July 2015 Gordon Green and John Coder Sentier Research, LLC For Immediate Release 1 Household Income Trends May 2015 Note This report on median household income

Household Income Trends May 2015 Issued July 2015 Gordon Green and John Coder Sentier Research, LLC For Immediate Release 1 Household Income Trends May 2015 Note This report on median household income

A cost-benefit analysis of accounting undergraduate education

A cost-benefit analysis of accounting undergraduate education ABSTRACT Robert Schadrie St. Norbert College Matthew Van Lanen St. Norbert College Amy Vandenberg St. Norbert College Jason Haen St. Norbert

A cost-benefit analysis of accounting undergraduate education ABSTRACT Robert Schadrie St. Norbert College Matthew Van Lanen St. Norbert College Amy Vandenberg St. Norbert College Jason Haen St. Norbert

The Role of a Forensic Economist in a Damage Assessment for Personal Injuries Draft date: 4/6/04. Thomas R. Ireland a

The Role of a Forensic Economist in a Damage Assessment for Personal Injuries Draft date: 4/6/04 I. Introduction Thomas R. Ireland a What is a forensic Economist? In any assessment of damages in a personal

The Role of a Forensic Economist in a Damage Assessment for Personal Injuries Draft date: 4/6/04 I. Introduction Thomas R. Ireland a What is a forensic Economist? In any assessment of damages in a personal

ICI RESEARCH PERSPECTIVE

ICI RESEARCH PERSPECTIVE 0 H STREET, NW, SUITE 00 WASHINGTON, DC 000 0-6-800 WWW.ICI.ORG OCTOBER 0 VOL. 0, NO. 7 WHAT S INSIDE Introduction Decline in the Share of Workers Covered by Private-Sector DB

ICI RESEARCH PERSPECTIVE 0 H STREET, NW, SUITE 00 WASHINGTON, DC 000 0-6-800 WWW.ICI.ORG OCTOBER 0 VOL. 0, NO. 7 WHAT S INSIDE Introduction Decline in the Share of Workers Covered by Private-Sector DB

Arizona Form 2013 Property Tax Refund (Credit) Claim 140PTC

Claim 140PTC") Arizona Form 2013 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

Arizona Form 2013 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

CENTER FOR LABOR MARKET STUDIES

The Complete Breakdown in the High Schoolto Work Transition of Young, Non College Enrolled High School Graduates in the U.S.; The Need for an Immediate National Policy Response Prepared by: Andrew Sum

The Complete Breakdown in the High Schoolto Work Transition of Young, Non College Enrolled High School Graduates in the U.S.; The Need for an Immediate National Policy Response Prepared by: Andrew Sum

Educational Attainment of Veterans: 2000 to 2009

Educational Attainment of Veterans: to 9 January 11 NCVAS National Center for Veterans Analysis and Statistics Data Source and Methods Data for this analysis come from years of the Current Population Survey

Educational Attainment of Veterans: to 9 January 11 NCVAS National Center for Veterans Analysis and Statistics Data Source and Methods Data for this analysis come from years of the Current Population Survey

GM Ignition Compensation Claims Resolution Facility FREQUENTLY ASKED QUESTIONS

GM Ignition Compensation Claims Resolution Facility FREQUENTLY ASKED QUESTIONS June 30, 2014 Table of Contents Section 1. General Information 4 1.1 What is the GM Ignition Compensation Claims Resolution

GM Ignition Compensation Claims Resolution Facility FREQUENTLY ASKED QUESTIONS June 30, 2014 Table of Contents Section 1. General Information 4 1.1 What is the GM Ignition Compensation Claims Resolution

THE IMPACT OF TORT REFORM ON THE DAMAGE ELEMENT OF PERSONAL INJURY AND MEDICAL NEGLIGENCE CASES

THE IMPACT OF TORT REFORM ON THE DAMAGE ELEMENT OF PERSONAL INJURY AND MEDICAL NEGLIGENCE CASES Michael J. Mohlman Smith Coonrod Mohlman, LLC 7001 W. 79th Street Overland Park, KS 66204 Telephone: (913)

THE IMPACT OF TORT REFORM ON THE DAMAGE ELEMENT OF PERSONAL INJURY AND MEDICAL NEGLIGENCE CASES Michael J. Mohlman Smith Coonrod Mohlman, LLC 7001 W. 79th Street Overland Park, KS 66204 Telephone: (913)

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES AUSTRALIA

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions AUSTRALIA Australia: pension system in 2008

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions AUSTRALIA Australia: pension system in 2008

Damage Estimation in Wrongful Termination Cases: Impact of the Great Recession

29 March 2012 Damage Estimation in Wrongful Termination Cases: Impact of the Great Recession By Dr. Laila Haider and Dr. Stephanie Plancich 1 Introduction The recent financial crisis was marked by the

29 March 2012 Damage Estimation in Wrongful Termination Cases: Impact of the Great Recession By Dr. Laila Haider and Dr. Stephanie Plancich 1 Introduction The recent financial crisis was marked by the

Volume URL: http://www.nber.org/books/feld87-2. Chapter Title: Individual Retirement Accounts and Saving

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Taxes and Capital Formation Volume Author/Editor: Martin Feldstein, ed. Volume Publisher:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Taxes and Capital Formation Volume Author/Editor: Martin Feldstein, ed. Volume Publisher:

Highlights of the. Boehringer Ingelheim. Retirement Savings Plan Retirement Plan. This brochure is intended for eligible employees of

Highlights of the Boehringer Ingelheim: Retirement Savings Plan Retirement Plan This brochure is intended for eligible employees of Boehringer Ingelheim hired after December 31, 2003. Table of Contents

Highlights of the Boehringer Ingelheim: Retirement Savings Plan Retirement Plan This brochure is intended for eligible employees of Boehringer Ingelheim hired after December 31, 2003. Table of Contents

Roth 401(k) Analyzer SM

Analyzer SM") Roth 401(k) Analyzer SM Supplemental Information Report Pre-tax or Roth 401(k)? Background Information Starting January 1, 2006, employers may add a new feature called a Roth 401(k) to their new or existing

Roth 401(k) Analyzer SM Supplemental Information Report Pre-tax or Roth 401(k)? Background Information Starting January 1, 2006, employers may add a new feature called a Roth 401(k) to their new or existing

COUNTY EMPLOYEES' ANNUITY AND BENEFIT FUND OF COOK COUNTY ACTUARIAL VALUATION AS OF DECEMBER 31,2011

COUNTY EMPLOYEES' ANNUITY AND BENEFIT FUND OF COOK COUNTY ACTUARIAL VALUATION AS OF DECEMBER 31,2011 GOLDSTEIN & ASSOCIATES Actuaries and Consultants 29 SOUTH LaSALLE STREET CHICAGO, ILLINOIS 60603 PHONE

COUNTY EMPLOYEES' ANNUITY AND BENEFIT FUND OF COOK COUNTY ACTUARIAL VALUATION AS OF DECEMBER 31,2011 GOLDSTEIN & ASSOCIATES Actuaries and Consultants 29 SOUTH LaSALLE STREET CHICAGO, ILLINOIS 60603 PHONE

Estimating the True Cost of Retirement

Estimating the True Cost of Retirement David Blanchett, CFA, CFP Head of Retirement Research Morningstar Investment Management 2013 Morningstar. All Rights Reserved. These materials are for information

Estimating the True Cost of Retirement David Blanchett, CFA, CFP Head of Retirement Research Morningstar Investment Management 2013 Morningstar. All Rights Reserved. These materials are for information

Generic Local School District, Ohio Notes to the Basic Financial Statements For the Fiscal Year Ended June 30, 2015

Note 2 - Summary of Significant Accounting Policies Pensions For purposes of measuring the net pension liability, information about the fiduciary net position of the pension plans and additions to/deductions

Note 2 - Summary of Significant Accounting Policies Pensions For purposes of measuring the net pension liability, information about the fiduciary net position of the pension plans and additions to/deductions

By: Garrick G. Zielinski, CFP, CDFA, CDS Divorce Financial Solutions, LLC Milwaukee, Wisconsin

ANATOMY OF A COLLABORATIVE PENSION VALUATION By: Garrick G. Zielinski, CFP, CDFA, CDS Divorce Financial Solutions, LLC Milwaukee, Wisconsin The terms and conditions of the plan, analysis and assumptions

ANATOMY OF A COLLABORATIVE PENSION VALUATION By: Garrick G. Zielinski, CFP, CDFA, CDS Divorce Financial Solutions, LLC Milwaukee, Wisconsin The terms and conditions of the plan, analysis and assumptions

NJ State Disability Benefits (TDB) An Employer Guide to how a private carrier can improve claims processing and lower costs.

An Employer Guide to how a private carrier can improve claims processing and lower costs.") NJ State Disability Benefits (TDB) An Employer Guide to how a private carrier can improve claims processing and lower costs. The Program At A Glance 2015 NJ Standard TDB Coverage Eligible Groups All NJ

NJ State Disability Benefits (TDB) An Employer Guide to how a private carrier can improve claims processing and lower costs. The Program At A Glance 2015 NJ Standard TDB Coverage Eligible Groups All NJ