TEACHING LIFE SKILLS TO PARENTS PARTICIPANT GUIDE

|

|

|

- Bethany Sutton

- 10 years ago

- Views:

Transcription

1 TEACHING LIFE SKILLS TO PARENTS PARTICIPANT GUIDE 1632 Da Vinci Court, Davis, CA Phone: (530) Fax: (530) humanservices.ucdavis.edu/academy

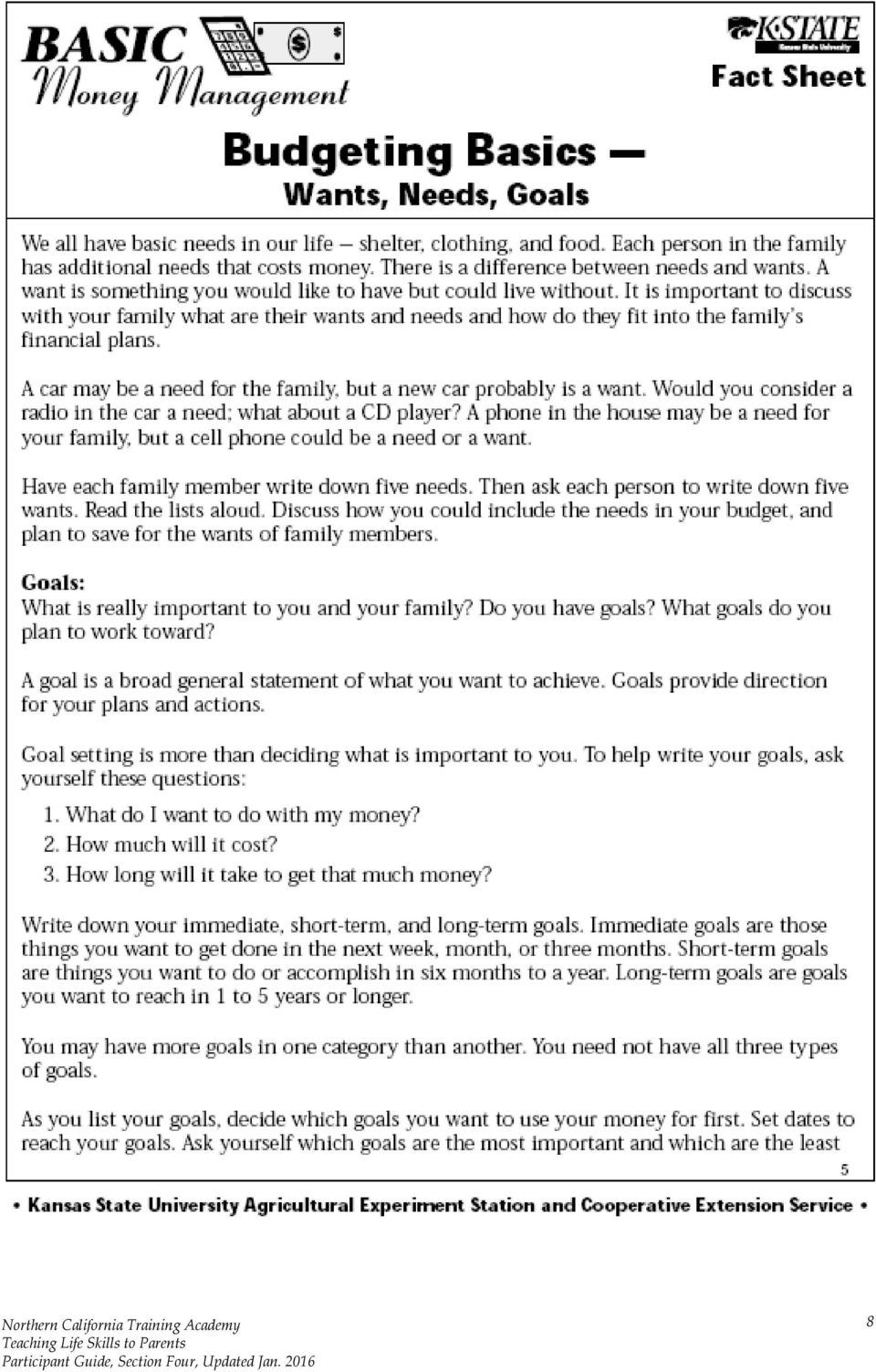

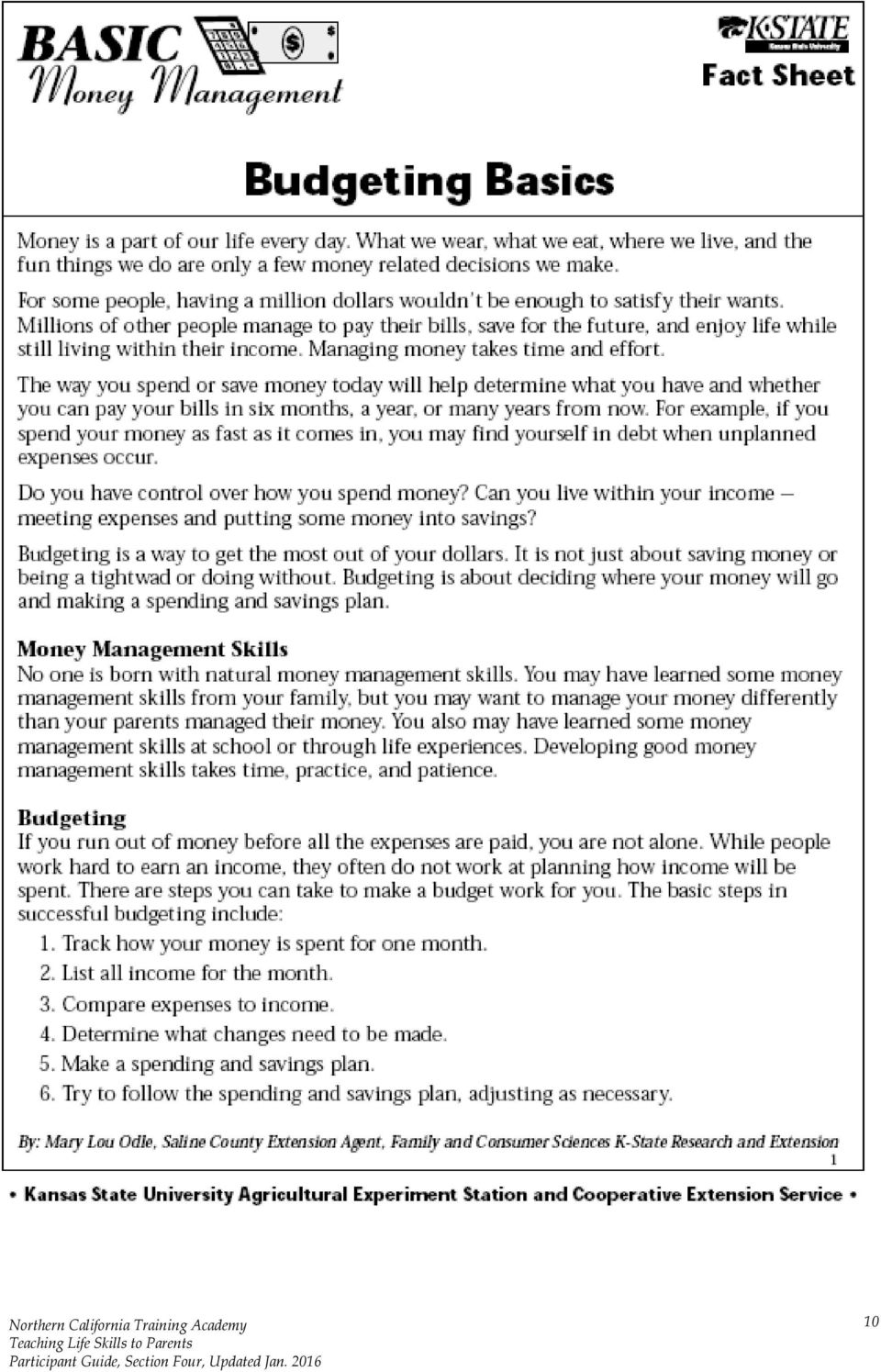

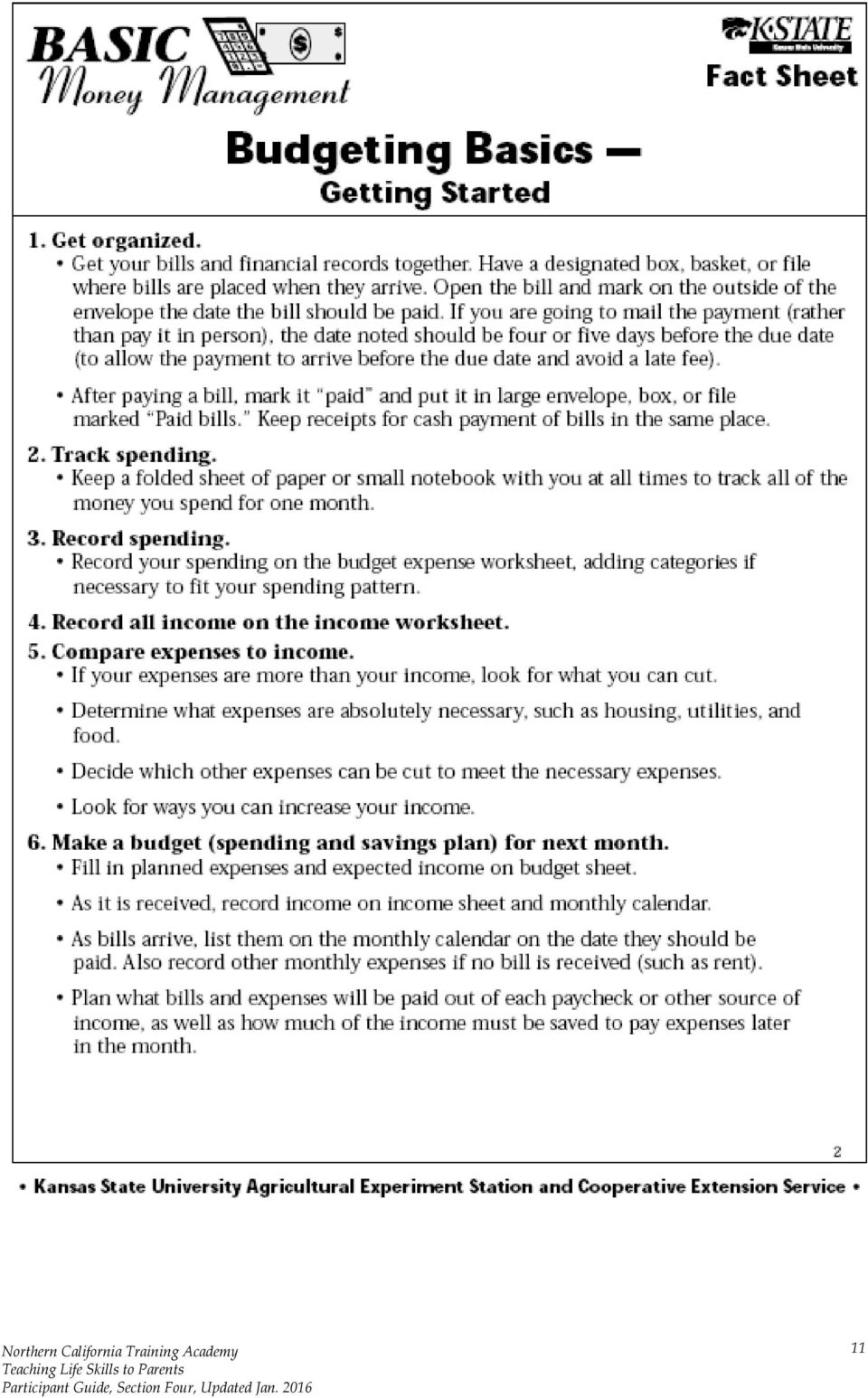

2 Section Four: Money Table of Contents Content Page Money Tool Kit 3 Curriculum Units for Money 4 Money Activities to Do With Clients 5 Exercise One: Your Values and Money 6 Take Charge of your Money 7 Budgeting Wants, Needs and Goals 8 Budgeting Basics: Money Management 10 Budgeting Basics: Getting Started 11 You and Your Money Quiz 13 What Do I/We Owe? Worksheet 14 Budgeting Worksheets 15 The Paycheck and Paystub 21 Read and Interpret Paystubs 23 Budgeting Basics: Saving for Tomorrow 26 Money Saving Suggestions 29 Banking Services 32 Northern California Training Academy 2

3 Money Tool Kit Teachable moments Client says to you that her money never lasts through the month. Client asks you for a loan. Client uses a check-cashing place to cash her checks. Client has been evicted. (Might be financial, might be something else. In any case, it s a good teachable moment.) Life skills questions Do you know who can help you with budgeting money? Do you have a budget? Do you have a bank account? Do you regularly put money into a savings account? Do you know where to find tax information on a pay stub? Does your money last through the month? What is the downside of buying something on credit? Do you plan for the expenses that you must pay each month? Do you keep a record when you pay bills? Are you impulsive when making significant purchases? Pitfalls Be mindful of whether or not there may be active substance abuse in the client s family. This just sucks the money out of any household and will foil any of your budgeting attempts with a client. Money is a charged subject. It may or may not be something your client feels comfortable discussing. People can get themselves into real financial trouble very quickly with credit cards, high interest payday loans and any kind of shady financial dealings. Client may be participating in the underground economy, either by working on a cash-only basis or by participating in illegal activities. This may make it hard to work with the client on money management. Life skills How to Develop a Budget. How to Decode a Pay Stub How to Save Money What Services Do Banks Offer How to Maintain a Bank Account How to Maintain Good Credit Northern California Training Academy 3

4 Curriculum Units for Money Setting priorities: Developing financial goals Learn the difference between Wants, Needs and Goals. Make a list of short and long-term financial goals Making a budget Get organized Track spending Make a list of income and expenses Where does the money go? Make a balanced spending and savings plan (a budget) The pay stub What is the difference between gross and net income? What are all the deductions on a pay stub for? Saving money What are various strategies for saving money? What are some specific ways to save money? Banking services What are the various services that banks offer? What are the different types of checks? Northern California Training Academy 4

5 Money Activities to do with Clients Setting priorities: Developing financial goals Help client make one short-term financial goal. Help client make one long-term financial goal. With client, look at any purchase $100 or more she has made in the last month and determine if it was a want or need. Making a budget Help client create a file for all her monthly expenses. Help client develop a system for keeping track of her monthly expenses. Using any of the budget worksheets, help client make a list of her income. Using any of the budget worksheets, help client put together a simple budget. The pay stub Look at the client's pay stub and make sure she understands all the deductions. Help the client calculate the weekly gross for various jobs. Saving money Help the client pick two ways to save to try for a month. With client, review the grocery shopping strategies she uses to save money. Banking services With client, shop around for the best deal on a checking account Go with the client to open a savings account. Northern California Training Academy 5

6 Exercise One: Your values and money Please write down two values you have regarding money: From whom did you learn these values? To whom do you talk about money? Who knows all about your finances (i.e. how much you make, how much you have in savings, etc. if you have any investments, etc.)? Northern California Training Academy 6

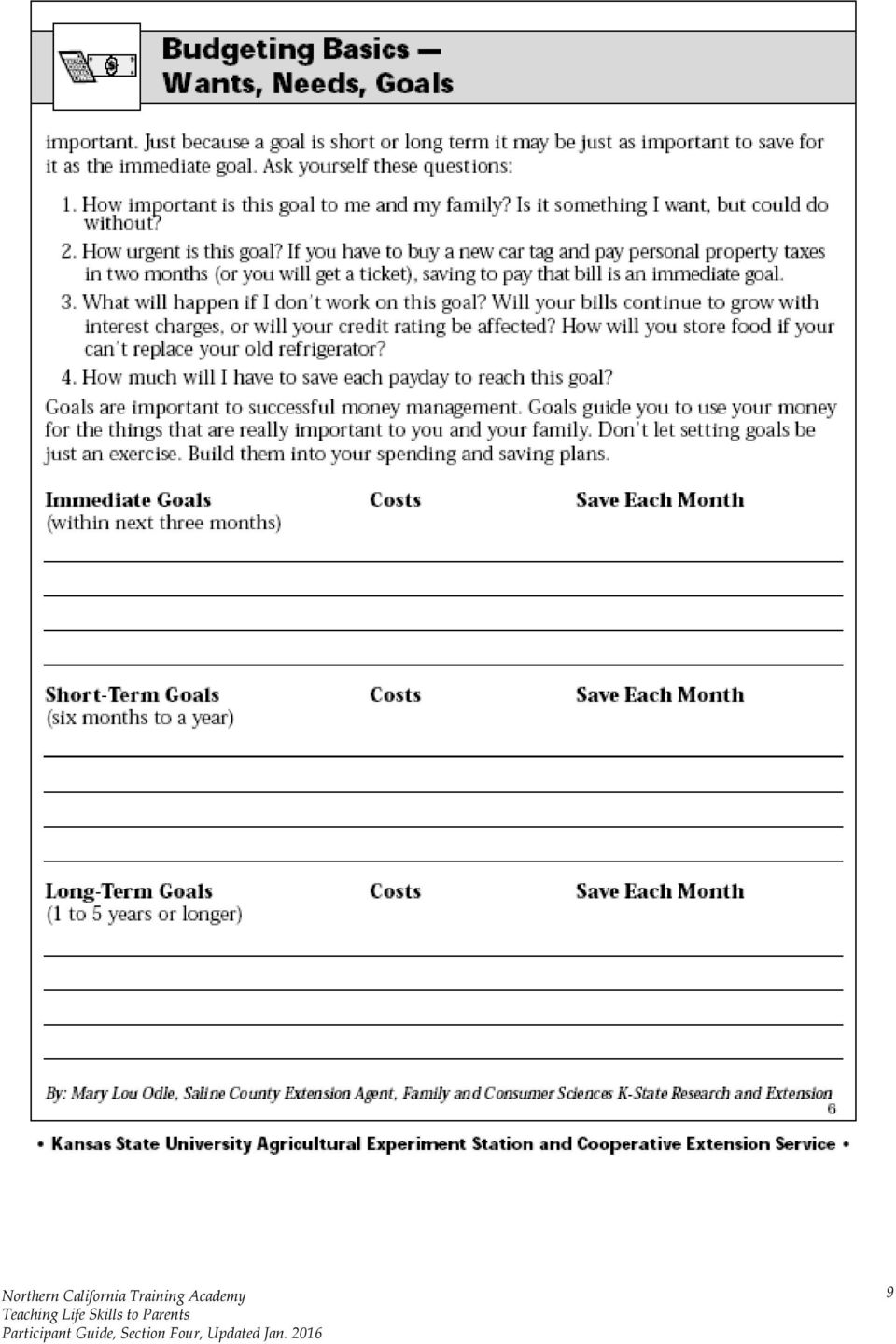

7 Adapted from material from the Federal Reserve System $$$$ Take Charge of Your Money $$$$ Set goals. Set short-term and long-term goals. Set due dates for reaching your goals. Be realistic. Be flexible. Go back and look at your goals to check your progress. Develop a budget. Find out where your money is going. Write down all of your income. Keep track of your expenses for a month. Look for places to save. Make a budget. Review it each month. Start saving, no matter how little. Put it in a savings account or someplace else where you won't be tempted to spend it. Shop for the best interest rates. Understand all fees and charges. As your income increases, increase your savings. Manage credit wisely. Always ask yourself if you really need to borrow money. Avoid spur-of-the-moment purchases. Set a monthly limit on credit card purchases. Pay more than the minimum. Protect your credit rating. Pay all bills on time. If you're having trouble paying bills, get advice from a reputable organization before you are delinquent. Find out your credit rating. Check your credit report every year. Alert the credit bureau if you see an error. Get the best deal on borrowing money. Know the loan's terms and conditions. What is the interest rate? What are the fees? How much will I have paid in interest? Can I pay it off early without a penalty? Shop around and compare. Question an offer that sounds too good to be true. Always read and understand the fine print. Seek help if you need it. Learn more about money. Look for organizations in your community that can help you learn more about setting financial goals, budgeting, savings, using credit wisely and getting the best deal. Northern California Training Academy 7

8 8

9 9

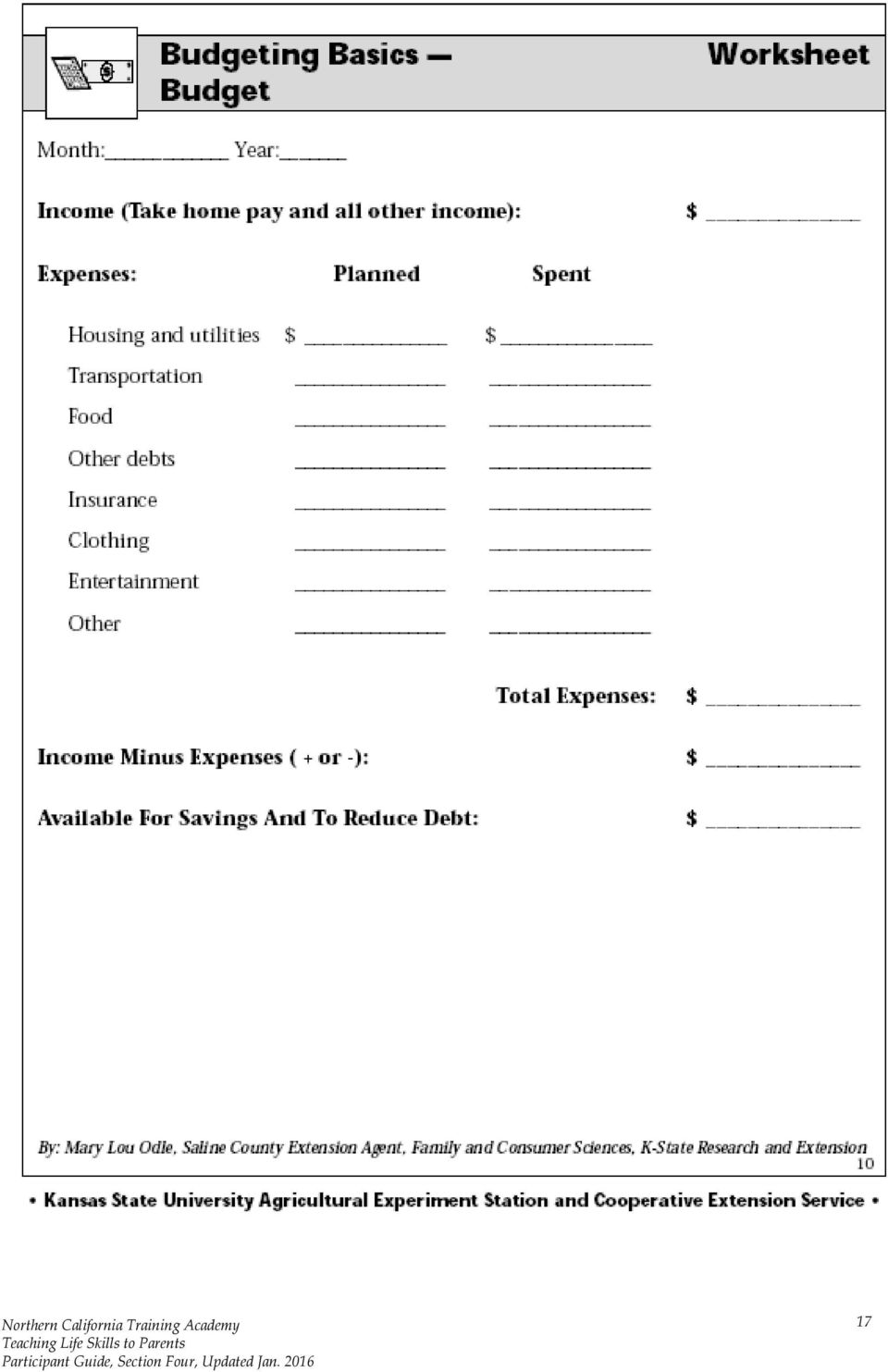

10 10

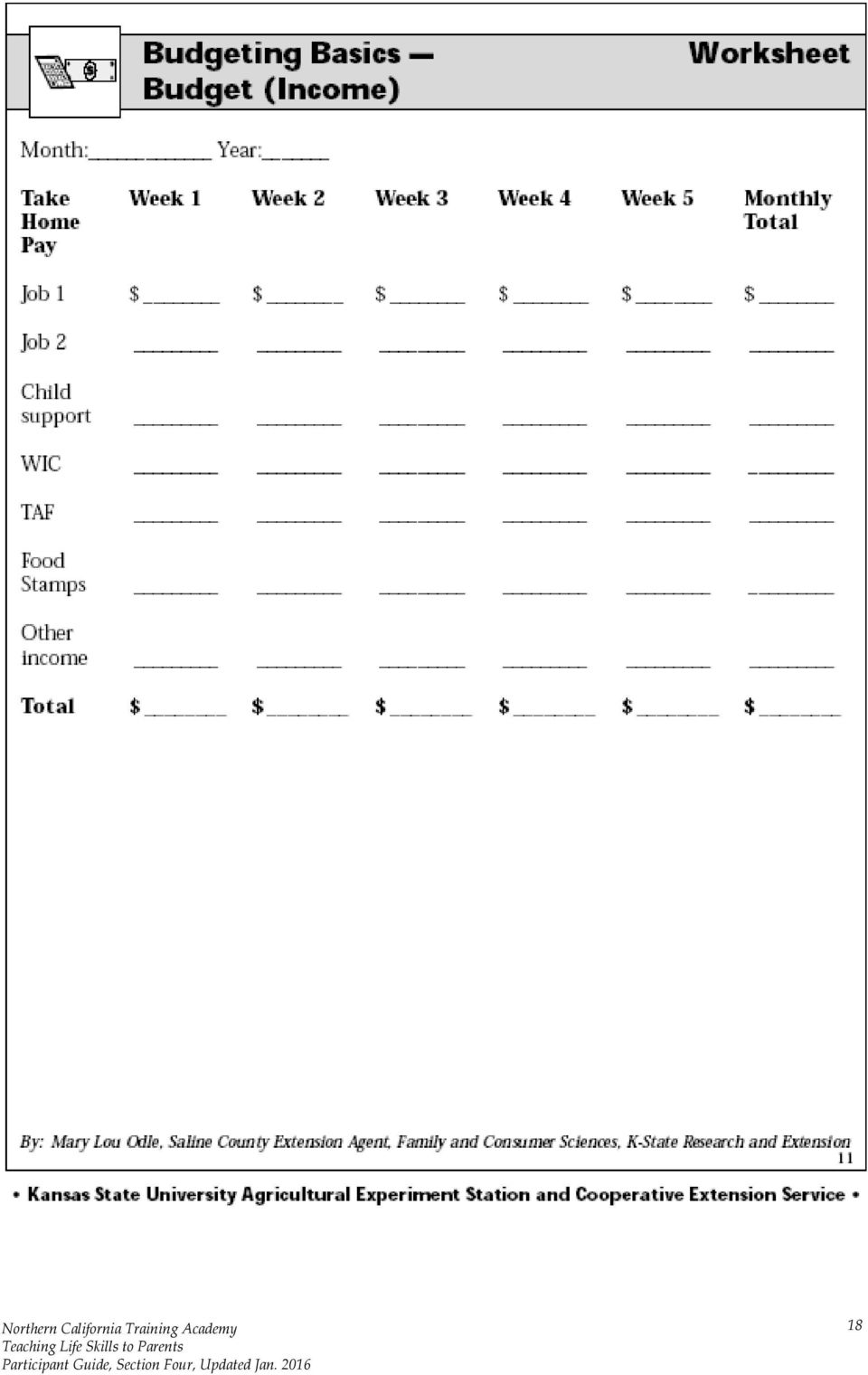

11 11

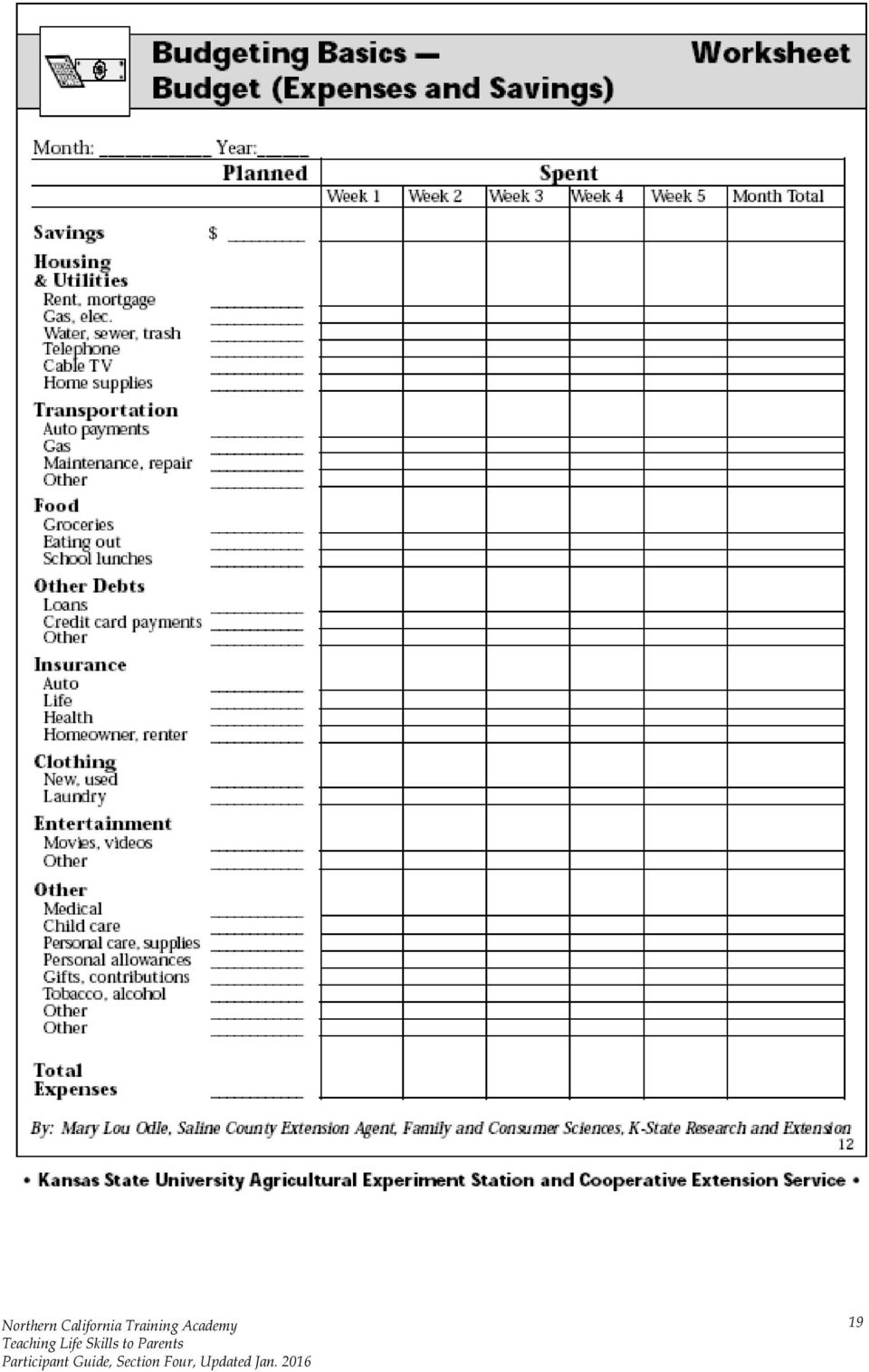

12 12

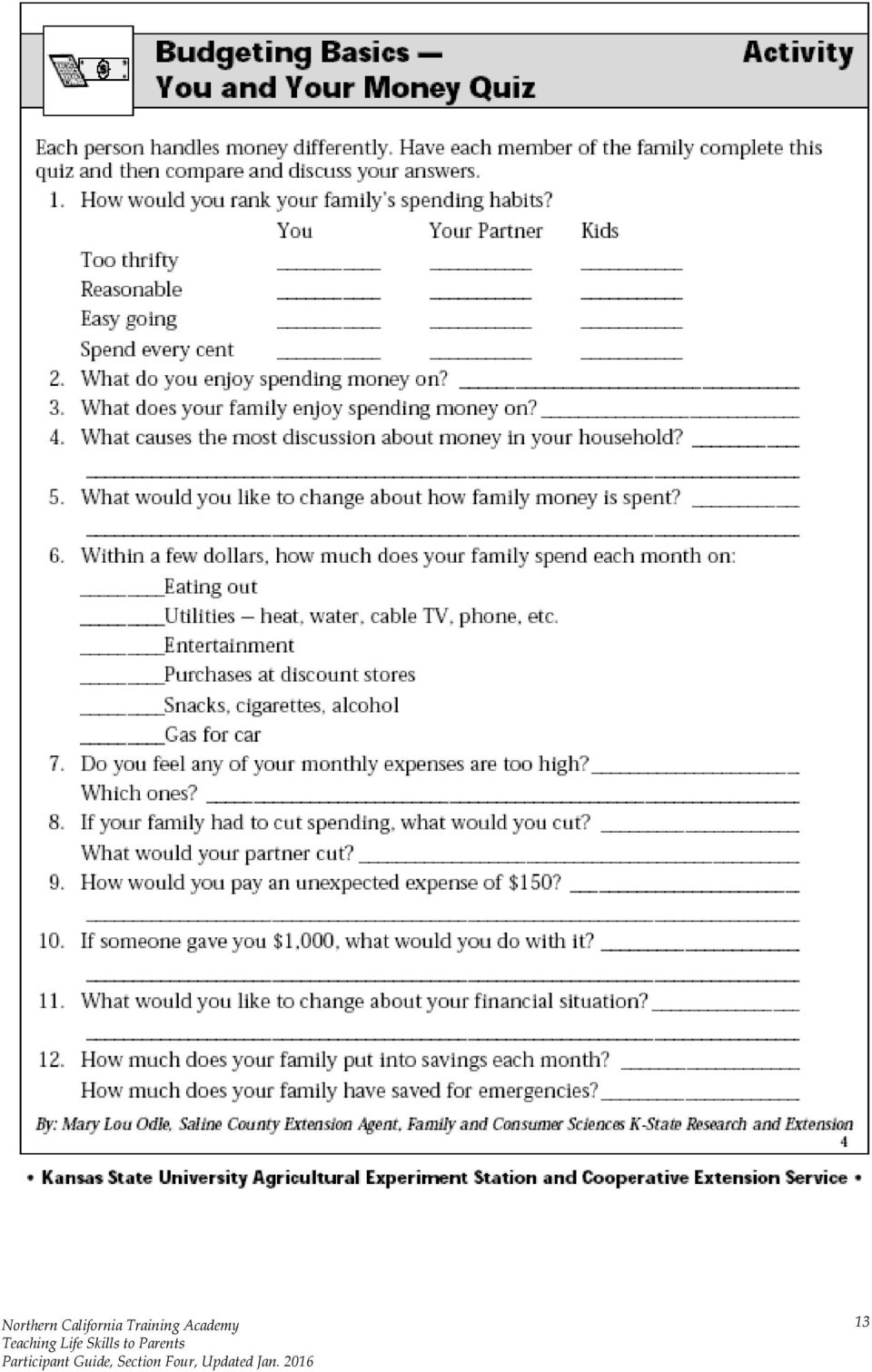

13 13

14 14

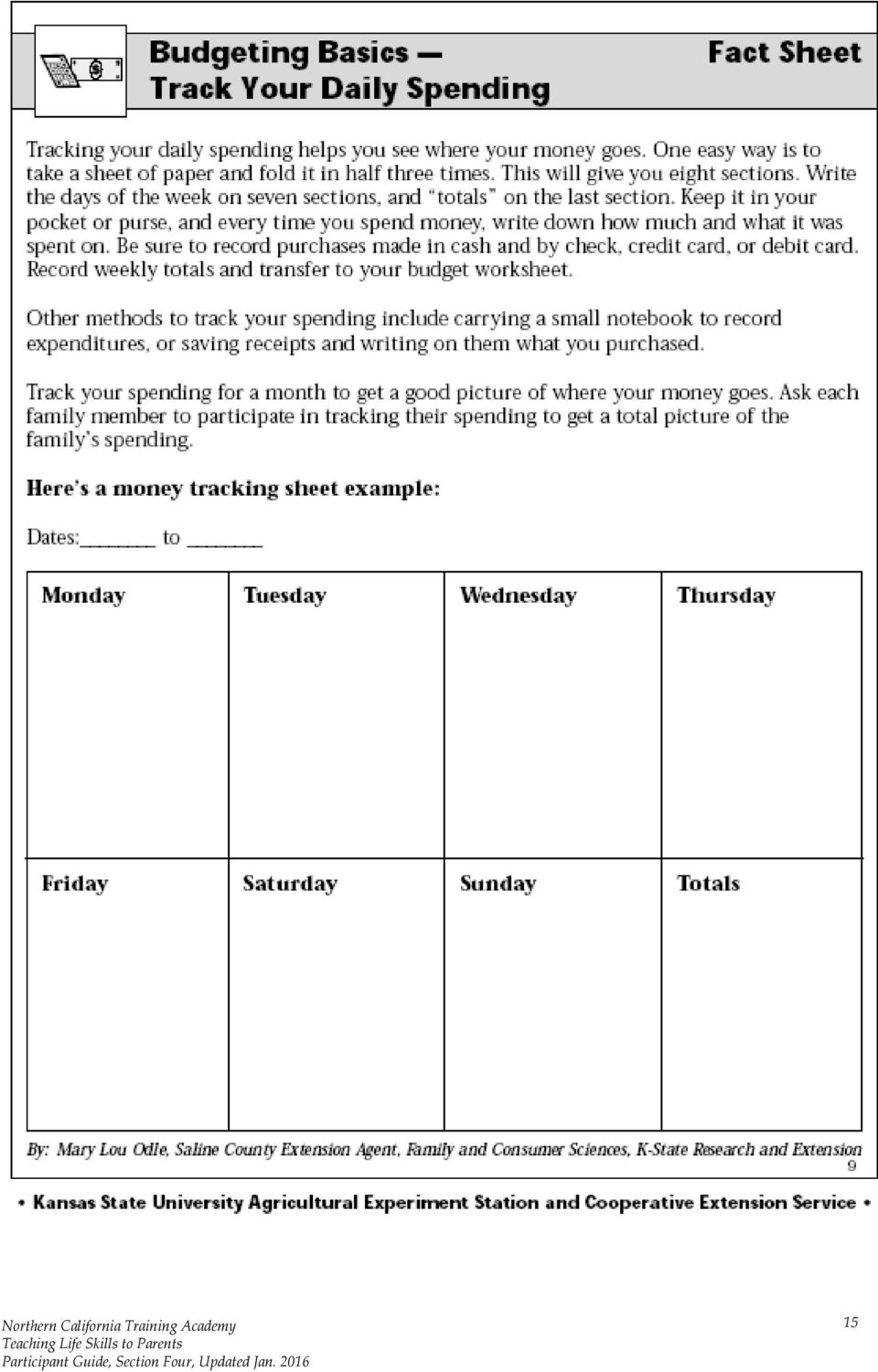

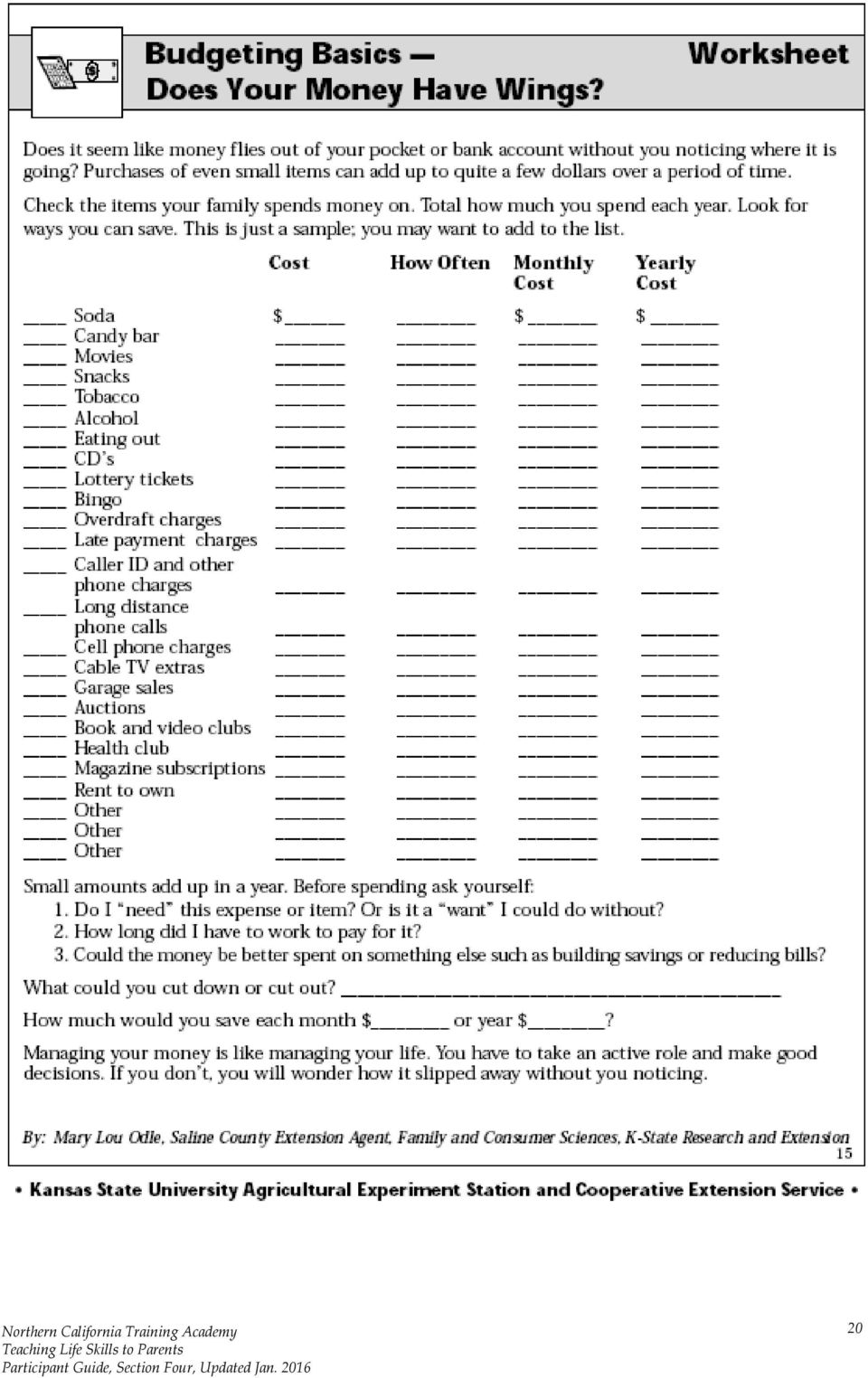

15 15

16 16

17 17

18 18

19 19

20 20

21 The Paycheck and Pay Stub Along with an actual check for your take-home pay, a paycheck generally has a pay stub attached that lists everything that happened to the money you just earned. A big adjustment when you get your first job is coming to understand the difference between gross pay and net pay. When you see what wage a job pays and calculate how much you are going to earn, based on the number of hours you anticipate working, the result is your gross pay. This is your total earnings before any deductions are taken out. What you are left with after all the deductions are taken out is your net pay--what you actually get in your paycheck. Here is an example: Employee: Jerry Brown Social Security Number: For week ending: April 12, 2014 McDonald's Corp Capitol Way Sacramento, Ca. 1. No. of regular hours worked: Gross pay $ Rate of pay: $8 an hour 4. FICA $ No. of overtime hours worked 8 5. Federal $31.00 Rate of pay: $12 an hour 6. State $ Disability $ Medical $ (K) $ Total Deductions $ Net Pay $ An Explanation: 1. Regular Hours Worked: A standard work week generally is between 35 ad 40 hours a week. This period of time (or anything less) is what a regular wage covers. In this case, the wages earned were $8 x 40 = $ Overtime Hours Worked: Any hours worked over 40 hours in a week is considered overtime for hourly workers. The usual pay for overtime is 1-1/2 times the regular hourly wage. In this case that is $12.00 an hour. The overtime wages earned were $12 x 8 = $96. Northern California Training Academy 21

22 3. Gross Pay: This is the total amount of money that Jerry Brown made this week, which is a total of the standard and overtime earnings: $320 + $96 = $ FICA: This stands for the Federal Insurance Contribution Act and is money that is deducted for a person's social security fund. This is a mandatory deduction. A worker will contribute to this fund during his/her whole working life. When someone retires or becomes disabled, this fund will be available to supplement any retirement, pension or other source of income. 5. Federal: Federal income tax. This is also a mandatory deduction and is calculated based on what you make and the number of deductions you claim. You decide on your deductions when you complete a W-4 form. 6. State: State income tax. This is a mandatory deduction, again based on what you earn and your deductions. 7. Disability: This is a deduction that goes towards a type of insurance that is available if you get hurt or sick and can't work for a short period of time. 8. Medical: Medical insurance. This deduction is an employee's contribution towards the medical insurance an employer supplies for employees (K): This is an employee's contribution to a tax-free retirement account established by an employer. A 401(K) is an account through a for-profit company. A 403(B) is a retirement account through a non-profit agency. 10. Total deductions: This is the total of all the deductions taken out of this paycheck. 11. Net pay: This is what Jerry Brown will take home from this pay period. This is not a complete list of deductions. There are other deductions that can be taken out of a paycheck such as city taxes and child care (if the employer has made a provision for it.) Northern California Training Academy 22

23 name: date: read and interpret pay stubs directions Answer the following questions using the pay stubs on the following pages: 1. What is the name of Jane Brown s employer? 2. How much did Jane earn before taxes? 3. What is Jane's hourly wage? 4. List Jane s deductions. 5. What pay period does Peter Smith s check cover? 6. How much federal income tax has been taken out of Peter s check so far during 1999? 7. How much did Peter contribute to a retirement plan from this paycheck? 8. How much is Peter s take-home pay? 9. Where does Mary Stone work? 10. How much is Mary s salary? 11. How much money was deducted from Mary s paycheck? 12. How much has Mary been paid in total during 1999? making money student activity 2-4a 23

24 read and interpret pay stubs HAMBURGER PALACE ENTERPRISES, INC. NAME PAYROLL ENDING CHECK NO. JANE BROWN 3/14/ EMPLOYEE NO. AMOUNT L4325 $87.50 EARNINGS TAXES WITHHELD OTHER DEDUCTIONS Description Hrs. Amount Tax Current YTD Description Amount Regular Fed Income Tax MEALS 7.00 CURRENT YTD Social Sec Medicare State Income Tax THE BANANA BREADBOX EMPLOYEE PETER SMITH SSN PAY PERIOD 8/06/09 TO 8/06/09 8/12/09 TO 8/12/09 PAY DATE 8/15/09 8/15/09 CHECK NO NET PAY $ EARNINGS TAXES WITHHELD OTHER DEDUCTIONS Description Hrs. Amount Tax Current YTD Description Amount Regular Fed Income Tax (K) Overtime Social Sec HEALTH Current Medicare YTD State Income Tax making money student activity 2-4b 24

25 read and interpret pay stubs (continued) EMPLOYEE Mary Stone EMPLOYEE # A5926 PAY PERIOD 7/01/09 TO 7/15/09 PAY DATE 7/01/09 7/14/09 TO 7/15/09 CHECK NO. 7/14/ NET PAY $ DANCE-O-RAMA EARNINGS TAXES WITHHELD OTHER DEDUCTIONS Description Hrs. Amount Tax Current YTD Description Amount Regular Fed Income Tax Salary Social Sec Current Medicare YTD State Income Tax making money student activity 2-4c 25

26 26

27 27

28 28

29 29

30 30

31 31

32 Banking Services Do I need a bank? A bank is a safer place to keep your money than a mattress. You can keep money in a checking account and write a check when you want to pay a bill. You can keep savings in a savings account and, not only will it be safe, but you will earn a little interest, too. You can deposit or cash checks. Without a bank account, it is often very hard to cash a check. Many times you have to use a check-cashing store which charges a fee (sometimes hefty) for the service. How do I choose a bank? Comparison-shop. Look for one that has the lowest fees, has the services you want and is convenient both in location and hours. Different types of accounts Savings Account: for people who want to keep their money in a safe place and earn a little interest. You can take your money out at any time. Almost no-risk savings. Checking Account: You keep your money in a checking account and can write checks from this money to pay a bill or to purchase something. Fees can very greatly. NOW Account: This is a checking account that pays interest. Some banks require that you keep a minimum balance. Money Market Deposit Account: Also an interest-paying checking account. They pay a higher interest rate than a NOW account but also require a higher balance and limit the number of checks you can write. Certificates of Deposit (CD): Savings accounts that require customers to keep a certain balance in a savings account for a certain fixed period of time. The Northern California Training Academy 32

33 interest rate is higher but you don t have access to your money for a period of time. Individual Retirement Accounts (IRAs): Savings deposits that require a customer to leave them in the account until a certain age (usually 60 or older.) There are significant tax benefits to this account but also significant penalties if the customer withdraws the money before the specified age. Different types of checks Certified Checks: Certified checks are usually used when called for by legal contract, such as real estate or automobile sale agreements. Certified checks are considered less risky than personal checks because the bank on which they are drawn has certified that the funds are available to the payee. Cashier s Checks: A less expensive alternative to a certified check is a cashier s check, sometimes called a bank money order or a treasurer s check. A person who buys a cashier s check does not need to have a checking account. He or she merely goes to the bank, requests a cashier s check for a certain amount, and pays the bank that amount plus a service charge. Personal and Postal Money Orders: For people who don t maintain a checking account or who prefer not to make payments with cash, money orders often serve the same function as personal checks. Personal money orders, sometimes called register checks, can be purchased at banks and some retail stores. Personal money orders are usually issued in smaller amounts and are cheaper than cashier s checks. Postal money orders, issued by the U.S. Postal Service, are similar to those issued by banks, but there are some differences. A postal money order will not be paid if it has more than one endorsement, so it must be cashed or deposited by the payee. Government Checks: Almost everyone has received a government check of one type or another: tax refunds, TANF, Social Security, and Supplemental Security Income. Sometimes people are surprised that a bank may be unwilling to cash a government check. A bank faces the risk that the person cashing the check may provide fraudulent identification, and it has no recourse to recover the funds. Loans Northern California Training Academy 33

34 Loans are often used to obtain goods or services that are expensive (i.e. beyond the person s regular budget) or to meet an emergency. Individuals can obtain a loan from commercial banks, savings and loans, credit unions, consumer finance or loan companies, or even life insurance companies (if you have a life insurance policy that has built up a cash value. ) Other sources of loans which can be very expensive include pawnshops, and those offering payday loans. Credit Basically the idea behind credit is that you buy now and pay later. A loan is a type of credit. One of the most common ways of using credit these days is the credit card. Having a credit card means that a bank has okayed you to borrow money up to certain limit. In turn, you agree to pay them interest on the money you have borrowed as you pay it back. There are advantages and disadvantages to using credit. These are: Advantages You get to use a purchase while you pay for it. You can buy things that are needed when you don t have enough money on hand to pay for them Credit can be helpful in financial emergencies. Credit is convenient. You do not have to carry a lot of money around with you. Disadvantages Purchases cost more when using credit. Don t forget to add in the price of the interest to the cost of the item. Credit ties up future income you need to pay the credit card off. Credit can encourage overspending. If poorly managed, credit can lead to financial problems!!!!!!!!!!!!!!! Using credit wisely helps build a good credit history. You may be able to take advantage of special bargains when you don t have enough money with you. Northern California Training Academy 34

Standard 1: The student will describe the importance of earning an income and explain how to manage personal income using a budget.

TEACHER GUIDE 1.2 EARNING AN INCOME PAGE 1 Standard 1: The student will describe the importance of earning an income and explain how to manage personal income using a budget. Income and Taxes Priority

TEACHER GUIDE 1.2 EARNING AN INCOME PAGE 1 Standard 1: The student will describe the importance of earning an income and explain how to manage personal income using a budget. Income and Taxes Priority

Standard 1: The student will describe the importance of earning an income and explain how to manage personal income using a budget.

STUDENT MODULE 1.2 EARNING AN INCOME PAGE 1 Standard 1: The student will describe the importance of earning an income and explain how to manage personal income using a budget. Income and Taxes Murphy cannot

STUDENT MODULE 1.2 EARNING AN INCOME PAGE 1 Standard 1: The student will describe the importance of earning an income and explain how to manage personal income using a budget. Income and Taxes Murphy cannot

It s Your Paycheck! Glossary of Terms

Annual percentage rate The percentage cost of credit on an annual basis and the total cost of credit to the consumer. APR combines the interest paid over the life of the loan and all fees that are paid

Annual percentage rate The percentage cost of credit on an annual basis and the total cost of credit to the consumer. APR combines the interest paid over the life of the loan and all fees that are paid

Financial Planning. Introduction. Learning Objectives

Financial Planning Introduction Financial Planning Learning Objectives Lesson 1 Budgeting: How to Live on Your Own and Not Move Home in a Week Prepare a budget and determine disposable income. Identify

Financial Planning Introduction Financial Planning Learning Objectives Lesson 1 Budgeting: How to Live on Your Own and Not Move Home in a Week Prepare a budget and determine disposable income. Identify

How to Use a Financial Institution

How to Use a Financial Institution Latino Community Credit Union & Latino Community Development Center HOW TO USE A FINANCIAL INSTITUTION LATINO COMMUNITY CREDIT UNION & LATINO COMMUNITY DEVELOPMENT CENTER

How to Use a Financial Institution Latino Community Credit Union & Latino Community Development Center HOW TO USE A FINANCIAL INSTITUTION LATINO COMMUNITY CREDIT UNION & LATINO COMMUNITY DEVELOPMENT CENTER

Banking Test - MoneyPower

Banking Test - MoneyPower Multiple Choice Identify the choice that best completes the statement or answers the question. 1. If a person makes a deposit of $10,000 or more into a bank account, the bank

Banking Test - MoneyPower Multiple Choice Identify the choice that best completes the statement or answers the question. 1. If a person makes a deposit of $10,000 or more into a bank account, the bank

- all the money you receive in a year - money from wages, tips, interest you earn, dividends, capital gains, etc.

4D Income Taxes there are 5 different categories Single You must be unmarried at the end of the year. Married filing jointly this is how most married people will file. Married filing separately occasionally,

4D Income Taxes there are 5 different categories Single You must be unmarried at the end of the year. Married filing jointly this is how most married people will file. Married filing separately occasionally,

Unit 4: Taxes. Read this unit including websites. You may want to take your own notes.

Taxes Read Chapter 4 in the text. Read Chapter 7 of The Financial Checkup. Read this unit including websites. You may want to take your own notes. Are taxes your favorite topic? They are not the favorite

Taxes Read Chapter 4 in the text. Read Chapter 7 of The Financial Checkup. Read this unit including websites. You may want to take your own notes. Are taxes your favorite topic? They are not the favorite

Online Advisor October 2015. Major Tax Deadlines For October 2015

Online Advisor October 2015 Major Tax Deadlines For October 2015 * October 1 - Generally the deadline for self-employeds and small businesses to establish a SIMPLE retirement plan for 2015. * October 15

Online Advisor October 2015 Major Tax Deadlines For October 2015 * October 1 - Generally the deadline for self-employeds and small businesses to establish a SIMPLE retirement plan for 2015. * October 15

Student Take Home Guide. Money Smart. Pay Yourself First

Student Take Home Guide Money Smart Table of Contents Table of Contents...1 Money Smart...2...3 Worksheet...4 Plan...5 Savings Tips...6 Compound Dividends Exercise...8 Compound Dividends...9 Savings $1

Student Take Home Guide Money Smart Table of Contents Table of Contents...1 Money Smart...2...3 Worksheet...4 Plan...5 Savings Tips...6 Compound Dividends Exercise...8 Compound Dividends...9 Savings $1

DOLLARS & SENSE Curriculum Map

DOLLARS & SENSE Curriculum Map Course ID: 8000/8001 Textbook: Economic Education for Consumers, 3E (Thomson/South-Western) ISBN: 0-538-44111-9 Credits:.50 Grade Level: 9 & 10 Course Description: Everyone

DOLLARS & SENSE Curriculum Map Course ID: 8000/8001 Textbook: Economic Education for Consumers, 3E (Thomson/South-Western) ISBN: 0-538-44111-9 Credits:.50 Grade Level: 9 & 10 Course Description: Everyone

YOUR MONEY, YOUR GOALS. A financial empowerment toolkit for community volunteers

YOUR MONEY, YOUR GOALS A financial empowerment toolkit for community volunteers Consumer Financial Protection Bureau April 2015 Table of contents INTRODUCTION PART 1: Volunteers and financial empowerment...

YOUR MONEY, YOUR GOALS A financial empowerment toolkit for community volunteers Consumer Financial Protection Bureau April 2015 Table of contents INTRODUCTION PART 1: Volunteers and financial empowerment...

Money Management Test - MoneyPower

Money Management Test - MoneyPower Multiple Choice Identify the choice that best completes the statement or answers the question. 1. A person s debt ratio shows the relationship between debt and net worth.

Money Management Test - MoneyPower Multiple Choice Identify the choice that best completes the statement or answers the question. 1. A person s debt ratio shows the relationship between debt and net worth.

If yes, complete the savings plan using the worksheet that follows. To complete this worksheet, you will need to know:

Savings plan This tool can help you make a plan to save money for: Your goals Expenses Unexpected expenses and emergencies There are two steps to making a savings plan. First, answer the set of questions

Savings plan This tool can help you make a plan to save money for: Your goals Expenses Unexpected expenses and emergencies There are two steps to making a savings plan. First, answer the set of questions

lesson six banking services overheads

lesson six banking services overheads beware of these high-cost financial services pawn shops charge very high interest for loans based on the value of tangible assets (such as jewelry or other valuable

lesson six banking services overheads beware of these high-cost financial services pawn shops charge very high interest for loans based on the value of tangible assets (such as jewelry or other valuable

Understanding Your Pay and Form W-2

Understanding Your Pay and Form W-2 Table of Contents 3 Welcome to Understanding Your Pay 3 How is My Pay Calculated? 3 Gross Wages 4 Pre-Tax Deductions 4 Income Taxes 5 Employment Taxes 5 Post-Tax Deductions

Understanding Your Pay and Form W-2 Table of Contents 3 Welcome to Understanding Your Pay 3 How is My Pay Calculated? 3 Gross Wages 4 Pre-Tax Deductions 4 Income Taxes 5 Employment Taxes 5 Post-Tax Deductions

1. I have something called a Chapter 13 plan. What is that exactly?

1. I have something called a Chapter 13 plan. What is that exactly? The Bankruptcy Code requires that every Chapter 13 bankruptcy have a plan. It is a summary sent to your creditors that, in effect, tells

1. I have something called a Chapter 13 plan. What is that exactly? The Bankruptcy Code requires that every Chapter 13 bankruptcy have a plan. It is a summary sent to your creditors that, in effect, tells

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account.

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Creating Your Financial Plan

Chapter 3 Creating Your Financial Plan Chapter 3 helps you create a spending and savings plan. In Chapter 2 you set your goal and estimated how much you need to save each month and for how long to achieve

Chapter 3 Creating Your Financial Plan Chapter 3 helps you create a spending and savings plan. In Chapter 2 you set your goal and estimated how much you need to save each month and for how long to achieve

MONEY MANAGEMENT WORKBOOK

MICHIGAN ENERGY ASSISTANCE PROGRAM MONEY MANAGEMENT WORKBOOK Life is a challenge. As the saying goes, just when you're about to make ends meet, someone moves the ends. While it can be a struggle to pay

MICHIGAN ENERGY ASSISTANCE PROGRAM MONEY MANAGEMENT WORKBOOK Life is a challenge. As the saying goes, just when you're about to make ends meet, someone moves the ends. While it can be a struggle to pay

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 BANKRUPTCY. Your Trustee is: Locke D. Barkley 601-355-6661. www.barkley13.com. Your Case Number is:

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 BANKRUPTCY This booklet contains some basic, general information about your Chapter 13 bankruptcy. Read this pamphlet completely to understand your obligations

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 BANKRUPTCY This booklet contains some basic, general information about your Chapter 13 bankruptcy. Read this pamphlet completely to understand your obligations

Effective Strategies for Personal Money Management

Effective Strategies for Personal Money Management The key to successful money management is developing and following a personal financial plan. Research has shown that people with a financial plan tend

Effective Strategies for Personal Money Management The key to successful money management is developing and following a personal financial plan. Research has shown that people with a financial plan tend

Teacher's Guide. Lesson Six. Banking Services 04/09

Teacher's Guide $ Lesson Six Banking Services 04/09 banking services websites Students will make wise choices about their banking services once they understand such fundamentals as: selecting and managing

Teacher's Guide $ Lesson Six Banking Services 04/09 banking services websites Students will make wise choices about their banking services once they understand such fundamentals as: selecting and managing

lesson thirteen in trouble overheads

lesson thirteen in trouble overheads why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies Materialism

lesson thirteen in trouble overheads why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies Materialism

BANKING 101. Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org

BANKING 101 Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org Congratulations on taking this important step to learn about issues dealing

BANKING 101 Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org Congratulations on taking this important step to learn about issues dealing

students can throw the bills away or make a pile of the discarded bills.)

") SM2-1: Budget Busters Purpose: Examine current personal money management habits by participating in this activity. Materials: Play money: enough so that each class member can have 10 bills. All bills can

SM2-1: Budget Busters Purpose: Examine current personal money management habits by participating in this activity. Materials: Play money: enough so that each class member can have 10 bills. All bills can

Grade 9-12 Subject Economics & Personal Finance Fourth Nine Weeks Instruction Dates: April 14 June 15

Classroom policies and procedures Curriculum Focus: Virginia Credit Union Smart Start Education Curriculum https://www.vacu.org/education_resources/articles_tips/financial_education_for_kids_teens/resources_for_teachers/smart_start_curriculu

Classroom policies and procedures Curriculum Focus: Virginia Credit Union Smart Start Education Curriculum https://www.vacu.org/education_resources/articles_tips/financial_education_for_kids_teens/resources_for_teachers/smart_start_curriculu

Saving And Investing

Student Activities $ Lesson Ten Saving And Investing 04/09 setting your financial goals Short-range goal (within 1 month) Goal: Estimated Cost $ Target Date $ Monthly Amount $ Medium-range goal (2 12 months)

Student Activities $ Lesson Ten Saving And Investing 04/09 setting your financial goals Short-range goal (within 1 month) Goal: Estimated Cost $ Target Date $ Monthly Amount $ Medium-range goal (2 12 months)

The FHLBI may, in its discretion, allow applicants to follow the income guidelines of other funding sources where differences exist.

Attachment D Income Guidelines For all FHLBI Affordable Housing Program (AHP) projects (including competitive AHP and the Homeownership Set-aside Programs) sponsors and members are required to use the

Attachment D Income Guidelines For all FHLBI Affordable Housing Program (AHP) projects (including competitive AHP and the Homeownership Set-aside Programs) sponsors and members are required to use the

Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities.

Accounting Fundamentals Lesson 8 8.0 Liabilities Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities. Current

Accounting Fundamentals Lesson 8 8.0 Liabilities Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities. Current

Prepared by the National Association of Insurance Commissioners. This guide does not endorse any company or policy.

Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association of state insurance regulatory officials. This association helps the

Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association of state insurance regulatory officials. This association helps the

Income Taxes module. After covering the topics in the module booklets or web pages and this workshop, learners will be able to:

Income Taxes module Trainer s Introduction Most people are aware that they must file an income tax return in Canada, if only to claim back any excess taxes that were withheld from their income. Filing

Income Taxes module Trainer s Introduction Most people are aware that they must file an income tax return in Canada, if only to claim back any excess taxes that were withheld from their income. Filing

INITIAL CLIENT QUESTIONNAIRE Financial. Name: SSN: DOB: Spouse: SSN: DOB: Address: City: State: Zip: Length of Residence:

FOR OFFICE USE ONLY Chapter 7 13 Individual Joint Attorney s Fee: Filing Fee: INITIAL CLIENT QUESTIONNAIRE Financial Date: Name: SSN: DOB: Spouse: SSN: DOB: Address: City: State: Zip: County: Length of

FOR OFFICE USE ONLY Chapter 7 13 Individual Joint Attorney s Fee: Filing Fee: INITIAL CLIENT QUESTIONNAIRE Financial Date: Name: SSN: DOB: Spouse: SSN: DOB: Address: City: State: Zip: County: Length of

How to Use Credit. Latino Community Credit Union & Latino Community Development Center

How to Use Credit Latino Community Credit Union & Latino Community Development Center How to Use Credit Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright

How to Use Credit Latino Community Credit Union & Latino Community Development Center How to Use Credit Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright

Payroll Deductions and Earnings Statements

Objectives In this lesson you will: learn and use terms related to payroll deductions learn to read earnings statements calculate net pay Employers must deduct certain amounts from their employees wages.

Objectives In this lesson you will: learn and use terms related to payroll deductions learn to read earnings statements calculate net pay Employers must deduct certain amounts from their employees wages.

IRS Form 668-W Part 1

IRS Form 668-W Part 1 REPLY THIS ISN'T A BILL FOR TAXES YOU OWE. THIS IS A NOTICE OF LEVY TO COLLECT MONEY OWED BY THE TAXPAYER NAMED ABOVE. The Internal Revenue Code provides that there is a lien for

IRS Form 668-W Part 1 REPLY THIS ISN'T A BILL FOR TAXES YOU OWE. THIS IS A NOTICE OF LEVY TO COLLECT MONEY OWED BY THE TAXPAYER NAMED ABOVE. The Internal Revenue Code provides that there is a lien for

Each payday, all employees receive one

Understanding Your Pay Information This brochure contains important information! Each payday, all employees receive one of the following: Pay statement for those who receive paper paychecks Access to epaystub

Understanding Your Pay Information This brochure contains important information! Each payday, all employees receive one of the following: Pay statement for those who receive paper paychecks Access to epaystub

Everything You Need to Know About Bankruptcy

Everything You Need to Know About Bankruptcy Raymond J. Sallum Bloomfield, Michigan http://bloomfieldlawgroup.com/chapter-7-bankruptcy B l o o m f i e l d L a w G r o u p R a y m o n d J. S a l l u m (

Everything You Need to Know About Bankruptcy Raymond J. Sallum Bloomfield, Michigan http://bloomfieldlawgroup.com/chapter-7-bankruptcy B l o o m f i e l d L a w G r o u p R a y m o n d J. S a l l u m (

Fixed Deferred Annuities

Buyer Buyer s Guide to: s Guide to: Fixed Deferred Annuities Prepared by the Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association

Buyer Buyer s Guide to: s Guide to: Fixed Deferred Annuities Prepared by the Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association

University of Northern Iowa

University of Northern Iowa Direct Deposit of Payroll Authorization Form Name (Please Print) (Last, First, MI) UNI ID# I hereby authorize the University of Northern Iowa to initiate direct deposit credit

University of Northern Iowa Direct Deposit of Payroll Authorization Form Name (Please Print) (Last, First, MI) UNI ID# I hereby authorize the University of Northern Iowa to initiate direct deposit credit

Unit 3 Banking: Opening an Account

Unit 3 Banking: Opening an Account Vocabulary a bank (banks) a bank teller (bank tellers) a window (windows) an ATM (ATMs) More Vocabulary: a line, (lines) waiting in line a deposit, (deposits) making

Unit 3 Banking: Opening an Account Vocabulary a bank (banks) a bank teller (bank tellers) a window (windows) an ATM (ATMs) More Vocabulary: a line, (lines) waiting in line a deposit, (deposits) making

NOLO. Nolo s Guide to Limited Liability Companies: Forming an LLC

NOLO Nolo s Guide to Limited Liability Companies: Forming an LLC Table of Contents LLC Basics...3 Limited Personal Liability for LLC Owners...3 Exceptions to LLC Owners Limited Liability...4 LLC Management...4

NOLO Nolo s Guide to Limited Liability Companies: Forming an LLC Table of Contents LLC Basics...3 Limited Personal Liability for LLC Owners...3 Exceptions to LLC Owners Limited Liability...4 LLC Management...4

Using Credit to Your Advantage

Hands on Banking Using Credit to Your Advantage Credit Reports, Credit Scores and Dealing with Debt The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the

Hands on Banking Using Credit to Your Advantage Credit Reports, Credit Scores and Dealing with Debt The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the

Personal Financial Literacy 2014

A Correlation of Table of Contents Standard 1: Income... 3 Standard 2: Money Management... 5 Standard 3: Spending & Credit... 7 Standard 4: Saving & Investing... 11 2 Course Description is a course designed

A Correlation of Table of Contents Standard 1: Income... 3 Standard 2: Money Management... 5 Standard 3: Spending & Credit... 7 Standard 4: Saving & Investing... 11 2 Course Description is a course designed

Preparing Family Net Worth and Income Statements

Family and Consumer Sciences FSFCS49 Preparing Family Net Worth and Income Statements Laura Connerly Instructor - Family Resource Management Arkansas Is Our Campus Visit our web site at: http://www.uaex.edu

Family and Consumer Sciences FSFCS49 Preparing Family Net Worth and Income Statements Laura Connerly Instructor - Family Resource Management Arkansas Is Our Campus Visit our web site at: http://www.uaex.edu

Chapter 15 PAYROLL 15-1

Chapter 15 PAYROLL Payroll responsibility varies from municipality to municipality. In smaller municipalities the Clerk- Treasurer is responsible for payroll preparation and maintenance of records. In

Chapter 15 PAYROLL Payroll responsibility varies from municipality to municipality. In smaller municipalities the Clerk- Treasurer is responsible for payroll preparation and maintenance of records. In

Unit 3 - Financial Services

Unit 3 - Financial Services Credit Unions vs. Banks Banks For profit companies owned by shareholders Offer services to everyone who wants to apply Owned by shareholders; customers do not vote Deposits

Unit 3 - Financial Services Credit Unions vs. Banks Banks For profit companies owned by shareholders Offer services to everyone who wants to apply Owned by shareholders; customers do not vote Deposits

Teacher's Guide. Lesson Nine. In Trouble 04/09

Teacher's Guide $ Lesson Nine In Trouble 04/09 in trouble websites It's hard to admit and deal with debt or financial trouble. It can be a painful time, but students need to learn practical, beneficial

Teacher's Guide $ Lesson Nine In Trouble 04/09 in trouble websites It's hard to admit and deal with debt or financial trouble. It can be a painful time, but students need to learn practical, beneficial

Life Insurance Buyer s Guide

Life Insurance Buyer s Guide This guide can help you when you shop for life insurance. It discusses how to: Find a Policy The Meets Your Needs and Fits Your Budget Decide How Much Insurance You Need Make

Life Insurance Buyer s Guide This guide can help you when you shop for life insurance. It discusses how to: Find a Policy The Meets Your Needs and Fits Your Budget Decide How Much Insurance You Need Make

MALIK ACADEMY AND AL BUSTAN PRESCHOOL FINANCIAL AID/REDUCED TUITION PROGRAM

MALIK ACADEMY AND AL BUSTAN PRESCHOOL FINANCIAL AID/REDUCED TUITION PROGRAM Dear Parent/Guardian: Sending children to private school can be expensive. In order to make our school affordable to as many

MALIK ACADEMY AND AL BUSTAN PRESCHOOL FINANCIAL AID/REDUCED TUITION PROGRAM Dear Parent/Guardian: Sending children to private school can be expensive. In order to make our school affordable to as many

Checking and Savings Accounts Pretest

Checking and Savings Accounts Pretest 1. It does not matter which kind of checking account you open. Just get the one with the lowest service charge. 2. Some checking accounts pay interest but the interest

Checking and Savings Accounts Pretest 1. It does not matter which kind of checking account you open. Just get the one with the lowest service charge. 2. Some checking accounts pay interest but the interest

Money Management THEME

THEME 3 Introduction Money Management Do you know people who handle money carelessly? Lots of seemingly smart people are clueless about where they stand financially. There is Beverly, a professional woman,

THEME 3 Introduction Money Management Do you know people who handle money carelessly? Lots of seemingly smart people are clueless about where they stand financially. There is Beverly, a professional woman,

Table of Contents. Money Smart for Adults Curriculum Page 2 of 21

Table of Contents Checking In... 3 Pre-Test... 4 What Is Credit?... 6 Collateral... 6 Types of Loans... 7 Activity 1: Which Loan Is Best?... 8 The Cost of Credit... 9 Activity 2: Borrowing Money Responsibly...

Table of Contents Checking In... 3 Pre-Test... 4 What Is Credit?... 6 Collateral... 6 Types of Loans... 7 Activity 1: Which Loan Is Best?... 8 The Cost of Credit... 9 Activity 2: Borrowing Money Responsibly...

6.15.1.7 Describe and use the steps involved in the banking reconciliation process

ND BUSINESS EDUCATION FRAMEWORKS Financial Literacy Course Code Course Name/Course Description Grade Levels Accreditation Time/Credit Options 14095 Financial Literacy is designed to help students understand

ND BUSINESS EDUCATION FRAMEWORKS Financial Literacy Course Code Course Name/Course Description Grade Levels Accreditation Time/Credit Options 14095 Financial Literacy is designed to help students understand

Arizona Form 2013 Individual Amended Income Tax Return 140X

Arizona Form 2013 Individual Amended Income Tax Return 140X Phone Numbers For information or help, call one of the numbers listed: Phoenix (602) 255-3381 From area codes 520 and 928, toll-free (800) 352-4090

Arizona Form 2013 Individual Amended Income Tax Return 140X Phone Numbers For information or help, call one of the numbers listed: Phoenix (602) 255-3381 From area codes 520 and 928, toll-free (800) 352-4090

C.A.L.M. 20 Unscheduled. Unit 5

C.A.L.M. 20 Unscheduled Unit 5 Independent Living Name: Unit 5 Independent Living Complete all parts of this unit on the assignment sheets provided. Assignment 1 Values and guiding principles for independent

C.A.L.M. 20 Unscheduled Unit 5 Independent Living Name: Unit 5 Independent Living Complete all parts of this unit on the assignment sheets provided. Assignment 1 Values and guiding principles for independent

Borrower Assistance Package

Borrower Assistance Package In order for us to properly evaluate your request for assistance with your mortgage loan or home equity loan, you must complete the enclosed forms and return it promptly to

Borrower Assistance Package In order for us to properly evaluate your request for assistance with your mortgage loan or home equity loan, you must complete the enclosed forms and return it promptly to

Texas Payroll Conference

Texas Payroll Conference Garnishments All Others Taunya Fritzsching, CPP Agenda Involuntary Deductions Garnishment Overview Federal Tax Levy State Tax Levy Student Loans Creditor Garnishments Bankruptcy

Texas Payroll Conference Garnishments All Others Taunya Fritzsching, CPP Agenda Involuntary Deductions Garnishment Overview Federal Tax Levy State Tax Levy Student Loans Creditor Garnishments Bankruptcy

Budgeting: Making the Most of Your Money

? Did You Know? Almost 60% of millionaires use a budget to manage their money. The Millionaire Next Door: The Surprising Secrets of America s Wealthy. In this unit, you will: Examine your spending habits

? Did You Know? Almost 60% of millionaires use a budget to manage their money. The Millionaire Next Door: The Surprising Secrets of America s Wealthy. In this unit, you will: Examine your spending habits

If you are 55 years or older and are retiring or separating from the County of San Diego, your

UTerminal Pay Plan Frequently Asked Questions If you are 55 years or older and are retiring or separating from the County of San Diego, your accrued sick and vacation leave will be paid out through the

UTerminal Pay Plan Frequently Asked Questions If you are 55 years or older and are retiring or separating from the County of San Diego, your accrued sick and vacation leave will be paid out through the

Meeting the West Virginia State Standards

Meeting the West Virginia State Standards Financial Avenue provides online courses and mini-modules to help students gain important knowledge about the basics of personal money management. The Financial

Meeting the West Virginia State Standards Financial Avenue provides online courses and mini-modules to help students gain important knowledge about the basics of personal money management. The Financial

Application form completely filled out and signed.

x INTERIOR REGIONAL HOUSING AUTHORITY Tribal Equity Advantage Mortgage (TEAM) Program 828 27 th Avenue i Fairbanks, Alaska 99701 Phone: (907) 452-8315 i Fax: (907) 452-8324 Applicant Name: Date of Application:

x INTERIOR REGIONAL HOUSING AUTHORITY Tribal Equity Advantage Mortgage (TEAM) Program 828 27 th Avenue i Fairbanks, Alaska 99701 Phone: (907) 452-8315 i Fax: (907) 452-8324 Applicant Name: Date of Application:

Student Activities. Lesson Six. Banking Services 07/10

Student Activities $ Lesson Six Banking Services 07/10 name: date: choosing a checking account name of bank: branch information Branch nearest your home: Branch nearest your work: Number of branches: number

Student Activities $ Lesson Six Banking Services 07/10 name: date: choosing a checking account name of bank: branch information Branch nearest your home: Branch nearest your work: Number of branches: number

GLOSSARY. Annual Percentage Rate (APR) The cost of credit on a yearly basis, expressed as a percentage rather than a dollar amount.

The cost of credit on a yearly basis, expressed as a percentage rather than a dollar amount.") These materials are intended for education purposes only. Any opinions expressed in these materials are not necessarily those of Citigroup and its affiliates. If legal, financial, tax, or other expert

These materials are intended for education purposes only. Any opinions expressed in these materials are not necessarily those of Citigroup and its affiliates. If legal, financial, tax, or other expert

How To Understand How To Get A Bank Account

Opening a Bank Account Section Objectives A basic component in establishing financial independence is Opening a Bank Account. Banking services are essential tools for managing personal finances and building

Opening a Bank Account Section Objectives A basic component in establishing financial independence is Opening a Bank Account. Banking services are essential tools for managing personal finances and building

Credit Cards: What You Need to Know

ALL ABOUT CREDIT A free publication provided by Consolidated Credit Counseling Services of Canada, Inc., a registered charitable credit counselling and debt management organization. Consolidated Credit

ALL ABOUT CREDIT A free publication provided by Consolidated Credit Counseling Services of Canada, Inc., a registered charitable credit counselling and debt management organization. Consolidated Credit

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS TABLE of CONTENTS A Letter to Employers.3 The Student Loan Program...4 Collection Authority...4 The Basic Steps Employers Follow for

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS TABLE of CONTENTS A Letter to Employers.3 The Student Loan Program...4 Collection Authority...4 The Basic Steps Employers Follow for

RICK A. YARNALL Chapter 13 Bankruptcy Trustee for the United States Bankruptcy Court District of Nevada

CHAPTER 13 THE THIRTEEN (13) MOST COMMON QUESTIONS and ANSWERS Prepared for: Your Case Number is: YOUR FIRST PAYMENT IS DUE ON Payments are due on the day of each month thereafter. Your Trustee is: RICK

CHAPTER 13 THE THIRTEEN (13) MOST COMMON QUESTIONS and ANSWERS Prepared for: Your Case Number is: YOUR FIRST PAYMENT IS DUE ON Payments are due on the day of each month thereafter. Your Trustee is: RICK

Part VI Retirement Accounts for Small Businesses and the Self-Employed

Part VI Retirement Accounts for Small Businesses and the Self-Employed While employees of most large companies have access to 401(k) plans or traditional pension plans, those employed by small firms often

Part VI Retirement Accounts for Small Businesses and the Self-Employed While employees of most large companies have access to 401(k) plans or traditional pension plans, those employed by small firms often

Credit Workshop. What I need to know about credit and lending products of financial institutions. Financial Education Supported by:

Credit Workshop What I need to know about credit and lending products of financial institutions. Financial Education Supported by: Concept Checklist What will I learn today? [ ] What is Credit? [ ] Advantages/

Credit Workshop What I need to know about credit and lending products of financial institutions. Financial Education Supported by: Concept Checklist What will I learn today? [ ] What is Credit? [ ] Advantages/

lesson six banking services supplemental materials 04/09

lesson six banking services supplemental materials 04/09 banking terms account Money deposited with a financial institution for investment and/or safekeeping purposes. assets Items of monetary value (e.g.,

lesson six banking services supplemental materials 04/09 banking terms account Money deposited with a financial institution for investment and/or safekeeping purposes. assets Items of monetary value (e.g.,

Supplemental Security Income Telephone Wage Report - Instructions

Telephone Wage Report - Instructions Beneficiaries, deemors and representative payees reporting a change in wages can report their monthly wages to SSA by telephone. These instructions explain what beneficiaries,

Telephone Wage Report - Instructions Beneficiaries, deemors and representative payees reporting a change in wages can report their monthly wages to SSA by telephone. These instructions explain what beneficiaries,

Do-it-Yourself Recovery of Unpaid Wages

Do-it-Yourself Recovery of Unpaid Wages How to Represent Yourself Before the California Labor Commissioner A Publication of: The Legal Aid Society-Employment Law Center 600 Harrison Street, Suite 120 San

Do-it-Yourself Recovery of Unpaid Wages How to Represent Yourself Before the California Labor Commissioner A Publication of: The Legal Aid Society-Employment Law Center 600 Harrison Street, Suite 120 San

keeping a running balance answer key

keeping a running balance answer key record deposits and keep a running balance in the checkbook register below. 1. On May 26, your balance is $527.96. 2. On May 27, you write check #107 to your landlord,

keeping a running balance answer key record deposits and keep a running balance in the checkbook register below. 1. On May 26, your balance is $527.96. 2. On May 27, you write check #107 to your landlord,

WORKFORCE INVESTMENT ACT

COMMONWEALTH OF VIRGINIA VIRGINIA COMMUNITY COLLEGE SYSTEM WORKFORCE INVESTMENT ACT VIRGINIA WORKFORCE LETTER (VWL) 13 05 TO: FROM: SUBJECT: LOCAL WORKFORCE INVESTMENT BOARDS WORKFORCE DEVELOPMENT SERVICES

COMMONWEALTH OF VIRGINIA VIRGINIA COMMUNITY COLLEGE SYSTEM WORKFORCE INVESTMENT ACT VIRGINIA WORKFORCE LETTER (VWL) 13 05 TO: FROM: SUBJECT: LOCAL WORKFORCE INVESTMENT BOARDS WORKFORCE DEVELOPMENT SERVICES

NORTH IOWA SINGLE-FAMILY NEW CONSTRUCTION APPLICATION FOR HOME BUYER ASSISTANCE

NORTH IOWA SINGLE-FAMILY NEW CONSTRUCTION APPLICATION FOR HOME BUYER ASSISTANCE Applicant Name: Social Security Number: Spouse /Co-Householder Name: Social Security Number: Address/City/Zip: Telephone

NORTH IOWA SINGLE-FAMILY NEW CONSTRUCTION APPLICATION FOR HOME BUYER ASSISTANCE Applicant Name: Social Security Number: Spouse /Co-Householder Name: Social Security Number: Address/City/Zip: Telephone

WHAT BANKRUPTCY CAN T DO

A decision to file for bankruptcy should only be made after determining that bankruptcy is the best way to deal with your financial problems. This brochure cannot explain every aspect of the bankruptcy

A decision to file for bankruptcy should only be made after determining that bankruptcy is the best way to deal with your financial problems. This brochure cannot explain every aspect of the bankruptcy

Personal Finance Standards (Assignment Code #22210)

") Personal Finance Standards (Assignment Code #22210) Rationale Statement: A citizen that lives within his or her income has more control over his or her life while expanding choices. Having the knowledge

Personal Finance Standards (Assignment Code #22210) Rationale Statement: A citizen that lives within his or her income has more control over his or her life while expanding choices. Having the knowledge

Credit Cards: Advantages & Disadvantages

Credit Cards: Advantages & Disadvantages Latino Community Credit Union & Latino Community Development Center CREDIT CARDS: BUILDING A better FUTURE ADVANTAGES AND DISADVANTAGES Latino Community Credit

Credit Cards: Advantages & Disadvantages Latino Community Credit Union & Latino Community Development Center CREDIT CARDS: BUILDING A better FUTURE ADVANTAGES AND DISADVANTAGES Latino Community Credit

SOCIAL SECURITY ADMINISTRATION OMB No. 0960-0037

Form Approved SOCIAL SECURITY ADMINISTRATION OMB. 0960-0037 Request For Waiver Of Overpayment Recovery Or Change In Repayment Rate We will use your answers on this form to decide if we can waive collection

Form Approved SOCIAL SECURITY ADMINISTRATION OMB. 0960-0037 Request For Waiver Of Overpayment Recovery Or Change In Repayment Rate We will use your answers on this form to decide if we can waive collection

Chapter 11: Payroll Taxes, Deposits, and Reports

Chapter 11: Payroll Taxes, Deposits, and Reports Chapter Opener: Thinking Critically Payroll accountants are responsible for keeping accurate records of all employees so paychecks can be processed properly

Chapter 11: Payroll Taxes, Deposits, and Reports Chapter Opener: Thinking Critically Payroll accountants are responsible for keeping accurate records of all employees so paychecks can be processed properly

SAVINGS BASICS101 TM %*'9 [[[ EPXEREJGY SVK i

SAVINGS BASICS101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

SAVINGS BASICS101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

K.4 Using Credit Wisely After Bankruptcy

Appx. K.4 K.4 Using Credit Wisely After Bankruptcy Beware of Credit Offers Aimed at Recent Bankruptcy Filers Disguised Reaffirmation Agreement Carefully read any credit card or other credit offer from

Appx. K.4 K.4 Using Credit Wisely After Bankruptcy Beware of Credit Offers Aimed at Recent Bankruptcy Filers Disguised Reaffirmation Agreement Carefully read any credit card or other credit offer from