State of Scottish Economy 2006

|

|

|

- Louisa Amie Shields

- 3 years ago

- Views:

Transcription

1 Post-election economic challenges: Scotland and the UK Professor Brian Ashcroft Fraser of Allander Institute Strathclyde Business School 1 July 2015

2 Outline 1. Capacity utilisation Any room to spare? Can things only get better? Scope for SG policy? 2. Capacity growth How are we doing? Is there an FFA growth challenge? What to do about productivity? The right strategy? Can we get inclusive growth?

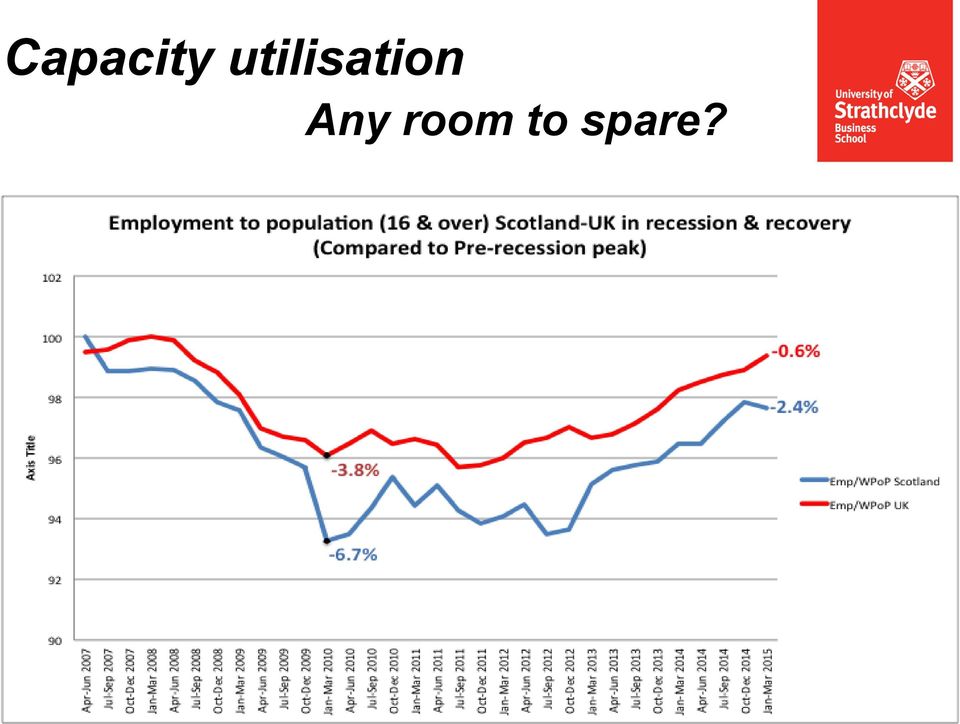

3 1. Capacity utilisation Any room to spare?

4 Capacity utilisation Any room to spare?

5 Capacity utilisation Any room to spare? Our conclusion on capacity utilisation is that despite the recovery the Scottish economy still has spare capacity available: the number of total weekly hours worked in Scotland is close to but still below the pre-recession peak. the ratio of employment to working population stood at - 2.4% below the pre-recession peak. On both indicators the position is better in the UK So the answer is, yes there is room to spare!

6 Capacity utilisation Can things only get better? The positives: domestic demand is still growing strongly boosted by investment; domestic inflation is close to zero, below nominal earnings/income growth and so boosting real income; external demand remains reasonably strong, with growth in the euro area beginning to strengthen while US growth having faltered earlier in the year looks set to pick up again.

7 Capacity utilisation Can things only get better? The negatives: Growth remains unbalanced with household spending the key driver fuelled largely by rising household debt, which we fear may soon become unsustainable. Investment is picking up especially in structures. Net trade strongly negative

8 Capacity utilisation Can things only get better? The negatives: the victory of the Conservatives with a small majority in the May UK General Election appears likely to lead to a continuation and perhaps a tightening of the previous Conservative / Liberal Democrat Coalition austerity plans. the growing threat of a Greek exit from the euro with the risk of contagion to other economies including Scotland.

9 Capacity utilisation Can things only get better? So our answer is: Mibbes aye, mibbes naw!

10 Capacity utilisation Scope for SG policy? Scope for Scottish Government to influence capacity utilisation is limited due to: Scottish economy highly open to the UK 70% of its exports Strong corporate / ownership links Labour market links via wage transmission and migration Limited fiscal policy powers, but increasing; yet scope to alter composition of spend to maximise multiplier effects. Part of UK monetary union, so no independent monetary policy. Slightly bigger public sector may act as stabiliser in face of private sector volatility: the flatter Scottish cycle

11 2. Capacity Growth

12 Capacity Growth How are we doing?

13 Capacity Growth How are we doing?

14 Capacity Growth How are we doing? So, our answer is: not too badly, thank you very much! Scottish trend GDP growth over last 50 years is nearidentical to UK growth at 2.3% p.a. Scottish trend GDP per head growth over last 50 years is 2.2% p.a. faster than UK s 2% p.a. (due to falling or slower population growth in Scotland) Interesting to see stronger Scottish growth in 1990s and 2000 s, latter in part due to weaker recession here. A little worrying that the recovery since 2010 is weaker in Scotland on both measures no room for complacency! Data health warning: data complied under ESA 1995: outturn likely to be different under the new ESA 2010

15 Capacity Growth Is there an FFA growth challenge? The answer is, yes! Here s why: Scottish trend GDP growth over last 50 years is 2.3% p.a. Latest GERS puts government spending (TME) at 44% of GDP and total revenues, incl. geog. share of North Sea oil, are 36% of GDP. To stabilise debt-to-gdp would require growth 6.5% p.a. on very favourable real interest rate assumptions of -1.5% and a real rate of zero pushes required growth up to 8% p.a. and so on as real rate rises. But assuming here that spending and tax shares of GDP remain constant.

16 Capacity Growth Is there an FFA growth challenge? Clearly, if spending ratio falls or remains same and tax ratio rises as growth increases, then lower growth is necessary to stabilise debt/gdp ratio. But still a big ask. Even faster growth would be necessary to lower debt ratio, stop the rise in the deficit, and faster growth still to lower absolute deficit. Also deficit needs to be funded at likely higher nominal interest rates than UK rates, raising necessary growth rate. Can t get away from the fact that FFA will require an increase in the tax burden and lower spending ratio. Argument that faster growth can secure a policy of FFA without higher tax and lower spending burdens is a red herring. (in my opinion!)

17 Capacity Growth What to do about productivity? Once capacity is utilised productivity growth is key to GDP growth. GDP per head is closer to prerecession peak in Scotland than UK. Although, recovery slower here, recession weaker and more jobs shed here. Hence, economywide productivity has held up slightly better in Scotland.

18 Capacity Growth What to do about productivity? Chart shows latest (June 24 th ) output per hour data from Scottish Govt. Labour productivity has risen absolutely in Scotland by 21% b/w 1998 & Despite this growth it fell behind the UK which grew faster. Scotland s relative productivity improved during and after the recession.

19 Capacity Growth What to do about productivity? So Scottish labour productivity while growing, has been weaker than in the UK. Moreover, there is research evidence (Richard Harris) that Total Factor Productivity productivity of all factors: labour, capital and land is also lower in Scotland than UK. Why should this be? Consensus (e.g. UK Treasury s 5 productivity drivers) is that we get stronger productivity growth via improvements in: Innovation/R&D Skills Competition Investment Enterprise

20 Capacity Growth What to do about productivity? The World Economic Forum / many academics rank innovation/r&d and business sophistication as key drivers of productivity. In Scotland: Very low business R&D (0.6% of GDP, 3.2% of UK BERD) and weak innovation a critical factor in the theory. But issues around definition and nature of innovation are crucial to policy. Weak entrepreneurship (GEM 2009: Scotland's rate of total early stage entrepreneurial activity, among lowest in 20 developed countries) Below average new firm formation: VAT registration data show a slight upward trend since the trough of the recession in 2009 and a trend rise in the Scottish share of UK VAT registrations since 2004, which peaked in 2010 at 6.60% but has fallen since to 6.45% in The historic problem with the business birthrate in Scotland is still evident since we are still adrift of a population share of 8.3%.

21 Capacity Growth The right strategy? The Scottish government s latest economic strategy seeks to improve competitiveness (ie productivity performance) and tackle inequality. Its four priorities are shown below :

22 Capacity Growth The right strategy? On the competitiveness front the Strategy is well grounded in theory and practice. Much of what the Strategy discusses is exciting and imaginative. Yet, in my view, it is weak in two areas: it lacks an organising theme or principle, specific to Scotland. it is not very specific on the how, or the implementation, tending to fall back on a plea for more powers. Much of the issues addressed in the Strategy could apply to any economy big or small. Scotland is a small to middling economy that is very open to trade, investment and migration, particularly with the rest of UK.

23 Capacity Growth The right strategy? In small, open economies the rules of economic development are not the same. For example, in large economies it is reasonable for policy to focus on domestic productivity to raise growth. But in an economy that is significantly open to trade and resource inflows and outflows, particularly inward investment, productivity change may often be the result of growth rather than its cause e.g. inward FDI raises GDP but since FDI activities are high productivity, average productivity also increases. In my view, it s the openness of the Scottish economy that should form the organising principle of Scotland s growth strategy.

24 Capacity Growth The right strategy? Internationalising the Scottish economy so that it links better to, and capitalises on, economic growth in global hubs should be the overarching priority of the Strategy. In addition, it also needs to be acknowledged that issues of scale and place probably matter more in small, open economies. Well known that economies of scale and agglomeration facilitate growth. Growth is concentrated in space and cities particularly are important in generating lower unit costs and higher productivity via facilitating people attraction and interaction, the creation of diversity and the generation of spillovers. The risk is that in smaller economies, by allowing growth to be spread, they may lose economies of scale and hence lose competitiveness unless policy intervenes.

25 Capacity Growth The right strategy? Classic example of this is the threat posed to Scotland by the UK government s Northern Powerhouse policy, which seeks to boost economic growth in the North of England through stimulating investment in the "Core Cities" of Liverpool, Manchester, Leeds, and Sheffield. So, the challenge for Scotland is to build an export base which is more vibrant and diversified than at present; a base that exploits Scotland s openness through attracting inward investment, skilled migrants, knowledge and skills via technology transfer; that builds on the growth advantages of cities; and, encourages R&D & innovation with the purpose of developing capabilities and hence the competitiveness of Scotland s business base.

26 Capacity Growth Can we get inclusive growth? The SG Economic Strategy puts great stress on securing growth that is inclusive. Evidence of the importance of an economy s social capital to sustained growth: its institutions, the degree of trust and the degree of inequality. The UK and Scotland have a high degree of income (and wealth) inequality (even after tax & benefits - see chart); Scotland would rank 20 th of 34 OECD countries with UK ranked 29 th in terms of degree of inequality.

27 Capacity Growth Can we get inclusive growth? But as the SG s recent Quarterly Income Inequality Briefing - March 2015 notes: Income inequality can be reduced through redistribution (via tax and benefit changes), but changes in market incomes (total income before any tax or benefits) have a greater impact on inequality. As John Hills makes clear in his brilliant recent book Good Times Bad Times the inequality of market pre-tax/benefit incomes in the UK and, with qualifications presumably Scotland, is extreme. In 2010 of 31 countries, only in Ireland and Chile was inequality pre-distribution worse than UK. However, when the difference between market incomes and disposable incomes is compared only 11 of the 31 countries were doing more than UK to redistribute income. The moral of this it seems to me is that, while we can and in my view should - do more through the tax and benefits system in Scotland and UK to effect more distribution, there is a bigger challenge. The big challenge for policy is how to tackle the extreme inequality in market incomes: the massive ratio of CEO pay to median company pay; the role of private versus public education; zero hours contracts; failure to pay minimum wage etc.

28 Conclusions I ve suggested that the post-election economic challenges facing Scotland and the UK can be divided into issues concerning capacity utilization and capacity growth. Our conclusion on capacity utilisation is that despite the recovery, the Scottish economy still has spare capacity. There are positives helping to sustain the recovery: domestic inflation remains close to zero and, combined with even modest earnings/income growth, is helping to boost real incomes; external demand remains reasonably strong, with growth in the Eurozone beginning to strengthen, and US growth, which faltered earlier in the year looks set to pick up again.

29 Conclusions But there are also threats to the recovery: a combination of unbalanced growth that relies unduly on household spending that depends mainly on rising and potentially unsustainable personal debt; the UK s overall weak trade performance; the UK Government continuing, or even tightening, planned austerity measures in the forthcoming Budget on 8 July; and the growing threat of a Greek exit from the euro with the risk of contagion to other economies including Scotland. The recovery should sustain but outturn remains highly uncertain. Scope for Scottish Government to influence capacity utilisation is limited largely because of the openness of the Scottish economy, part of UK monetary union, and limited fiscal powers.

30 Conclusions Scotland s (capacity) growth performance has been equal to the UK over the last 50 years averaging 2.3% p.a. GDP per head has grown faster here over that period 2.2% p.a. compared to 2% in UK. The recovery of Scottish GDP since 2010 is weaker than UK and suggests that there is no room for complacency. I ve suggested that the view that faster growth can secure a policy of FFA without higher tax and lower spending burdens is almost certainly misconceived. Productivity is a key driver of growth and is weaker in Scotland compared to UK where it is also weak.

31 Conclusions Scotland s Total Factor Productivity is probably also lower than UK. This may be due to low business R&D, low innovation, weak entrepreneurship, and especially a low new firm formation rate. The Scottish Government s economic strategy for the promotion of competitiveness and growth is well grounded in theory and practice. but it lacks a specific organising theme or principle specific to Scotland s needs and appears weak on implementation. In my view it is the openness of the Scottish economy that should form the organising principle of Scotland s growth strategy: to build an export base that links better to global growth hubs and that recognises the key role of cities in growth.

32 Conclusions The Scottish Government Economic Strategy puts great stress on securing growth that is inclusive. In view of the evidence that the distribution of market incomes is extremely unequal in the UK and probably Scotland, while we need do more through the tax and benefits system to effect a more equal income distribution, the big(ger) challenge for policy is how to tackle directly the extreme inequality in market incomes.

PERSONAL RETIREMENT SAVINGS ACCOUNT INVESTMENT REPORT

PENSIONS INVESTMENTS LIFE INSURANCE PERSONAL RETIREMENT SAVINGS ACCOUNT INVESTMENT REPORT FOR PERSONAL RETIREMENT SAVINGS ACCOUNT () PRODUCTS WITH AN ANNUAL FUND MANAGEMENT CHARGE OF 1% - JULY 201 Thank

PENSIONS INVESTMENTS LIFE INSURANCE PERSONAL RETIREMENT SAVINGS ACCOUNT INVESTMENT REPORT FOR PERSONAL RETIREMENT SAVINGS ACCOUNT () PRODUCTS WITH AN ANNUAL FUND MANAGEMENT CHARGE OF 1% - JULY 201 Thank

GOVERNMENT EXPENDITURE & REVENUE SCOTLAND 2013-14 MARCH 2015

GOVERNMENT EXPENDITURE & REVENUE SCOTLAND 2013-14 MARCH 2015 GOVERNMENT EXPENDITURE & REVENUE SCOTLAND 2013-14 MARCH 2015 The Scottish Government, Edinburgh 2015 Crown copyright 2015 This publication is

GOVERNMENT EXPENDITURE & REVENUE SCOTLAND 2013-14 MARCH 2015 GOVERNMENT EXPENDITURE & REVENUE SCOTLAND 2013-14 MARCH 2015 The Scottish Government, Edinburgh 2015 Crown copyright 2015 This publication is

UK Economic Forecast Q1 2015

UK Economic Forecast Q1 2015 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

UK Economic Forecast Q1 2015 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

Project LINK Meeting New York, 20-22 October 2010. Country Report: Australia

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Economic Review, April 2012

Economic Review, April 2012 Author Name(s): Malindi Myers, Office for National Statistics Abstract This note provides some wider economic analysis to support the Statistical Bulletin relating to the latest

Economic Review, April 2012 Author Name(s): Malindi Myers, Office for National Statistics Abstract This note provides some wider economic analysis to support the Statistical Bulletin relating to the latest

Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market

Communications P.O. Box, CH-8022 Zurich Telephone +41 44 631 31 11 Fax +41 44 631 39 10 Zurich, 13 September 2007 Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market The

Communications P.O. Box, CH-8022 Zurich Telephone +41 44 631 31 11 Fax +41 44 631 39 10 Zurich, 13 September 2007 Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market The

Joint Economic Forecast Spring 2013. German Economy Recovering Long-Term Approach Needed to Economic Policy

Joint Economic Forecast Spring 2013 German Economy Recovering Long-Term Approach Needed to Economic Policy Press version Embargo until: Thursday, 18 April 2013, 11.00 a.m. CEST Joint Economic Forecast

Joint Economic Forecast Spring 2013 German Economy Recovering Long-Term Approach Needed to Economic Policy Press version Embargo until: Thursday, 18 April 2013, 11.00 a.m. CEST Joint Economic Forecast

ENGINEERING LABOUR MARKET

ENGINEERING LABOUR MARKET in Canada Projections to 2025 JUNE 2015 ENGINEERING LABOUR MARKET in Canada Projections to 2025 Prepared by: MESSAGE FROM THE CHIEF EXECUTIVE OFFICER Dear colleagues: Engineers

ENGINEERING LABOUR MARKET in Canada Projections to 2025 JUNE 2015 ENGINEERING LABOUR MARKET in Canada Projections to 2025 Prepared by: MESSAGE FROM THE CHIEF EXECUTIVE OFFICER Dear colleagues: Engineers

UK Economic Forecast Q3 2014

UK Economic Forecast Q3 2014 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

UK Economic Forecast Q3 2014 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

An Evaluation of the Possible

An Evaluation of the Possible Macroeconomic Impact of the Income Tax Reduction in Malta Article published in the Quarterly Review 2015:2, pp. 41-47 BOX 4: AN EVALUATION OF THE POSSIBLE MACROECONOMIC IMPACT

An Evaluation of the Possible Macroeconomic Impact of the Income Tax Reduction in Malta Article published in the Quarterly Review 2015:2, pp. 41-47 BOX 4: AN EVALUATION OF THE POSSIBLE MACROECONOMIC IMPACT

UK Economic Outlook. July 2015. UK housing market outlook: the continuing rise of Generation Rent

July 2015 UK Economic Outlook UK housing market outlook: the continuing rise of Generation Rent Does trade hold the key to the UK services productivity puzzle? Visit our blog for periodic updates at: pwc.blogs.com/economics_in_business

July 2015 UK Economic Outlook UK housing market outlook: the continuing rise of Generation Rent Does trade hold the key to the UK services productivity puzzle? Visit our blog for periodic updates at: pwc.blogs.com/economics_in_business

The global economy Banco de Portugal Lisbon, 24 September 2013 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

Perspective. Economic and Market. Does a 2% 10-year U.S. Bond Yield Make Sense When...

James W. Paulsen, Ph.D. Perspective Bringing you national and global economic trends for more than 30 years Economic and Market January 27, 2015 Does a 2% 10-year U.S. Bond Yield Make Sense When... For

James W. Paulsen, Ph.D. Perspective Bringing you national and global economic trends for more than 30 years Economic and Market January 27, 2015 Does a 2% 10-year U.S. Bond Yield Make Sense When... For

Agents summary of business conditions

Agents summary of business conditions February Consumer demand had continued to grow at a moderate pace. Housing market activity had remained subdued relative to levels in H. Investment intentions for

Agents summary of business conditions February Consumer demand had continued to grow at a moderate pace. Housing market activity had remained subdued relative to levels in H. Investment intentions for

ANALYSIS OF SCOTLAND S PAST AND FUTURE FISCAL POSITION

CPPR Briefing Note ANALYSIS OF SCOTLAND S PAST AND FUTURE FISCAL POSITION Incorporating: GERS 2014 and the 2014 UK Budget Main authors: John McLaren & Jo Armstrong Editorial role: Ken Gibb March 2014 Executive

CPPR Briefing Note ANALYSIS OF SCOTLAND S PAST AND FUTURE FISCAL POSITION Incorporating: GERS 2014 and the 2014 UK Budget Main authors: John McLaren & Jo Armstrong Editorial role: Ken Gibb March 2014 Executive

General Certificate of Education Advanced Level Examination June 2013

General Certificate of Education Advanced Level Examination June 2013 Economics ECON4 Unit 4 The National and International Economy Tuesday 11 June 2013 9.00 am to 11.00 am For this paper you must have:

General Certificate of Education Advanced Level Examination June 2013 Economics ECON4 Unit 4 The National and International Economy Tuesday 11 June 2013 9.00 am to 11.00 am For this paper you must have:

INFLATION REPORT PRESS CONFERENCE. Thursday 4 th February 2016. Opening remarks by the Governor

INFLATION REPORT PRESS CONFERENCE Thursday 4 th February 2016 Opening remarks by the Governor Good afternoon. At its meeting yesterday, the Monetary Policy Committee (MPC) voted 9-0 to maintain Bank Rate

INFLATION REPORT PRESS CONFERENCE Thursday 4 th February 2016 Opening remarks by the Governor Good afternoon. At its meeting yesterday, the Monetary Policy Committee (MPC) voted 9-0 to maintain Bank Rate

Meeting with Analysts

CNB s New Forecast (Inflation Report II/2015) Meeting with Analysts Petr Král Prague, 11 May, 2015 1 Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

CNB s New Forecast (Inflation Report II/2015) Meeting with Analysts Petr Král Prague, 11 May, 2015 1 Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

Mario Draghi: Europe and the euro a family affair

Mario Draghi: Europe and the euro a family affair Keynote speech by Mr Mario Draghi, President of the European Central Bank, at the conference Europe and the euro a family affair, organised by the Bundesverband

Mario Draghi: Europe and the euro a family affair Keynote speech by Mr Mario Draghi, President of the European Central Bank, at the conference Europe and the euro a family affair, organised by the Bundesverband

Ageing, health spending and the long-term fiscal outlook: a UK perspective

Ageing, health spending and the long-term fiscal outlook: a UK perspective 31 January 2014 Robert Chote Chairman Long-term fiscal analysis at the OBR Annual Fiscal sustainability Report Public sector balance

Ageing, health spending and the long-term fiscal outlook: a UK perspective 31 January 2014 Robert Chote Chairman Long-term fiscal analysis at the OBR Annual Fiscal sustainability Report Public sector balance

December 2014 Labour market predictions for 2015 WORK WORKFORCE WORKPLACE

ember 2014 Labour market predictions for 2015 WORK WORKFORCE WORKPLACE LABOUR MARKET PREDICTIONS FOR 2015 Key points Economic growth of around 2.4% is expected in 2015, slightly lower than in 2014. Employment

ember 2014 Labour market predictions for 2015 WORK WORKFORCE WORKPLACE LABOUR MARKET PREDICTIONS FOR 2015 Key points Economic growth of around 2.4% is expected in 2015, slightly lower than in 2014. Employment

5 Comparison with the Previous Convergence Programme and Sensitivity Analysis

5 Comparison with the Previous Convergence Programme and Sensitivity Analysis 5.1 Comparison with the Previous Macroeconomic Scenario The differences between the macroeconomic scenarios of the current

5 Comparison with the Previous Convergence Programme and Sensitivity Analysis 5.1 Comparison with the Previous Macroeconomic Scenario The differences between the macroeconomic scenarios of the current

GCE Economics Candidate Exemplar Work ECON4: The National and International Economy

hij Teacher Resource Bank GCE Economics Candidate Exemplar Work ECON4: The National and International Economy The Assessment and Qualifications Alliance (AQA) is a company limited by guarantee registered

hij Teacher Resource Bank GCE Economics Candidate Exemplar Work ECON4: The National and International Economy The Assessment and Qualifications Alliance (AQA) is a company limited by guarantee registered

The Employment Crisis in Spain 1

The Employment Crisis in Spain 1 Juan F Jimeno (Research Division, Banco de España) May 2011 1 Paper prepared for presentation at the United Nations Expert Meeting The Challenge of Building Employment

The Employment Crisis in Spain 1 Juan F Jimeno (Research Division, Banco de España) May 2011 1 Paper prepared for presentation at the United Nations Expert Meeting The Challenge of Building Employment

Estonia and the European Debt Crisis Juhan Parts

Estonia and the European Debt Crisis Juhan Parts Estonia has had a quick recovery from the recent recession and its economy is in better shape than before the crisis. It is now much leaner and significantly

Estonia and the European Debt Crisis Juhan Parts Estonia has had a quick recovery from the recent recession and its economy is in better shape than before the crisis. It is now much leaner and significantly

2015 2018 Business Plan. Building Scotland s International Competitiveness

2015 2018 Business Plan Building Scotland s International Competitiveness CONTENTS 1 2 3 4 5 INTRODUCTION 1 A COMPETITIVE ECONOMY 2 DRIVERS OF GROWTH 3 TRACKING OUR PROGRESS 14 BUDGET 2015-18 18 Scottish

2015 2018 Business Plan Building Scotland s International Competitiveness CONTENTS 1 2 3 4 5 INTRODUCTION 1 A COMPETITIVE ECONOMY 2 DRIVERS OF GROWTH 3 TRACKING OUR PROGRESS 14 BUDGET 2015-18 18 Scottish

X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

Svein Gjedrem: Prospects for the Norwegian economy

Svein Gjedrem: Prospects for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 SR-Bank Stavanger, Stavanger, 26 March 2010. The text below

Svein Gjedrem: Prospects for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 SR-Bank Stavanger, Stavanger, 26 March 2010. The text below

Economic Snapshot for February 2013

Economic Snapshot for February 2013 Christian E. Weller on the State of the Economy Christian E. Weller, associate professor, Department of Public Policy and Public Affairs, University of Massachusetts

Economic Snapshot for February 2013 Christian E. Weller on the State of the Economy Christian E. Weller, associate professor, Department of Public Policy and Public Affairs, University of Massachusetts

The Economy - International Comparisons, 2011

The Economy - International Comparisons, 2011 Coverage: International Date: 14 May 2013 Geographical Area: Country Theme: People and Places Theme: Economy Theme: Labour Market Key Points The economy is

The Economy - International Comparisons, 2011 Coverage: International Date: 14 May 2013 Geographical Area: Country Theme: People and Places Theme: Economy Theme: Labour Market Key Points The economy is

State of the Economy

State 1 of State the Economy of the Economy June 2016 Office of Ril the - Junt Chief pr Economic f Adviser June 2016 State of the Economy Dr Gary Gillespie Chief Economist 3 June 2016 State of the Economy

State 1 of State the Economy of the Economy June 2016 Office of Ril the - Junt Chief pr Economic f Adviser June 2016 State of the Economy Dr Gary Gillespie Chief Economist 3 June 2016 State of the Economy

Be prepared Four in-depth scenarios for the eurozone and for Switzerland

www.pwc.ch/swissfranc Be prepared Four in-depth scenarios for the eurozone and for Introduction The Swiss economy is cooling down and we are currently experiencing unprecedented levels of uncertainty in

www.pwc.ch/swissfranc Be prepared Four in-depth scenarios for the eurozone and for Introduction The Swiss economy is cooling down and we are currently experiencing unprecedented levels of uncertainty in

The Year 2013 - An Inflation Risk

thelighthouse Issue 7 May 2013 welcome It seems like just the other day that New Year's resolutions were being planned, now we're almost halfway through the year! As financial planner and author, Suze

thelighthouse Issue 7 May 2013 welcome It seems like just the other day that New Year's resolutions were being planned, now we're almost halfway through the year! As financial planner and author, Suze

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA On the basis of the information available up to 22 May 2009, Eurosystem staff have prepared projections for macroeconomic developments in the

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA On the basis of the information available up to 22 May 2009, Eurosystem staff have prepared projections for macroeconomic developments in the

TREASURY MANAGEMENT UPDATE QUARTER 4 2014/15

Committee and Date Cabinet 10 June 2015 12.30 pm Item 9 Public TREASURY MANAGEMENT UPDATE QUARTER 4 2014/15 Responsible Officer James Walton e-mail: james.walton@shropshire.gov.uk Tel: (01743) 255011 1.

Committee and Date Cabinet 10 June 2015 12.30 pm Item 9 Public TREASURY MANAGEMENT UPDATE QUARTER 4 2014/15 Responsible Officer James Walton e-mail: james.walton@shropshire.gov.uk Tel: (01743) 255011 1.

CZECH ECONOMY CZECH ECONOMY. Ing. Jaroslav Vomastek Director of the Department of Economic Analysis

1 Overview of the Czech Economy GDP Employment Balance of Payments FDIs Balance of Budget Industry Foreign Trade 2 Main Characteristics of the Czech Economy High economic growth until mid 2008 catching

1 Overview of the Czech Economy GDP Employment Balance of Payments FDIs Balance of Budget Industry Foreign Trade 2 Main Characteristics of the Czech Economy High economic growth until mid 2008 catching

Labour market outlook, spring 2015 SUMMARY

Labour market outlook, spring 2015 SUMMARY Ura 2015:4 Labour market outlook Spring 2015 Summary The next few years will be characterised both by continued improvements in job growth and more people entering

Labour market outlook, spring 2015 SUMMARY Ura 2015:4 Labour market outlook Spring 2015 Summary The next few years will be characterised both by continued improvements in job growth and more people entering

Fiscal Sustainability of an Independent Scotland

Fiscal Sustainability of an Independent Scotland Michael Amior Rowena Crawford Gemma Tetlow Copy-edited by Judith Payne Institute for Fiscal Studies 7 Ridgmount Street London WC1E 7AE Published by The

Fiscal Sustainability of an Independent Scotland Michael Amior Rowena Crawford Gemma Tetlow Copy-edited by Judith Payne Institute for Fiscal Studies 7 Ridgmount Street London WC1E 7AE Published by The

AS Economics. Unemployment. tutor2u Supporting Teachers: Inspiring Students. Economics Revision Focus: 2004

Supporting Teachers: Inspiring Students Economics Revision Focus: 2004 AS Economics tutor2u (www.tutor2u.net) is the leading free online resource for Economics, Business Studies, ICT and Politics. Don

Supporting Teachers: Inspiring Students Economics Revision Focus: 2004 AS Economics tutor2u (www.tutor2u.net) is the leading free online resource for Economics, Business Studies, ICT and Politics. Don

THE RETURN OF CAPITAL EXPENDITURE OR CAPEX CYCLE IN MALAYSIA

PUBLIC BANK BERHAD ECONOMICS DIVISION MENARA PUBLIC BANK 146 JALAN AMPANG 50450 KUALA LUMPUR TEL : 03 2176 6000/666 FAX : 03 2163 9929 Public Bank Economic Review is published bi monthly by Economics Division,

PUBLIC BANK BERHAD ECONOMICS DIVISION MENARA PUBLIC BANK 146 JALAN AMPANG 50450 KUALA LUMPUR TEL : 03 2176 6000/666 FAX : 03 2163 9929 Public Bank Economic Review is published bi monthly by Economics Division,

Agents summary of business conditions

Agents summary of business conditions April Consumer demand had continued to grow moderately. Housing market transactions had picked up modestly since the start of the year, but were lower than a year

Agents summary of business conditions April Consumer demand had continued to grow moderately. Housing market transactions had picked up modestly since the start of the year, but were lower than a year

Meeting with Analysts

CNB s New Forecast (Inflation Report IV/) Meeting with Analysts Tibor Hlédik Prague, 7 November, Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

CNB s New Forecast (Inflation Report IV/) Meeting with Analysts Tibor Hlédik Prague, 7 November, Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

3.7% Historical trends in the UK. by Therese Lloyd. January 2015 FUNDING OVERVIEW

FUNDING OVERVIEW January 2015 Historical trends in the UK by Therese Lloyd SEE BRIEFING: NHS Finances The challenge all political parties need to face www.health.org.uk/ fundingbriefing In real terms,

FUNDING OVERVIEW January 2015 Historical trends in the UK by Therese Lloyd SEE BRIEFING: NHS Finances The challenge all political parties need to face www.health.org.uk/ fundingbriefing In real terms,

Measuring an independent Scotland s economic performance

CPPR Briefing Note (Embargoed til 00.01 Tuesday 23 rd April 2013) CPPR Briefing Paper Measuring an independent Scotland s economic performance Lead author: John McLaren Contributing authors: Jo Armstrong

CPPR Briefing Note (Embargoed til 00.01 Tuesday 23 rd April 2013) CPPR Briefing Paper Measuring an independent Scotland s economic performance Lead author: John McLaren Contributing authors: Jo Armstrong

The Norwegian economy

The Norwegian economy Slower speed ahead, but still growth Strong mechanisms support mainland economy Wriggle room to smooth business cycles Rune Bjerke CEO Just how bad is it? Slower speed ahead but still

The Norwegian economy Slower speed ahead, but still growth Strong mechanisms support mainland economy Wriggle room to smooth business cycles Rune Bjerke CEO Just how bad is it? Slower speed ahead but still

Adjusting to a Changing Economic World. Good afternoon, ladies and gentlemen. It s a pleasure to be with you here in Montréal today.

Remarks by David Dodge Governor of the Bank of Canada to the Board of Trade of Metropolitan Montreal Montréal, Quebec 11 February 2004 Adjusting to a Changing Economic World Good afternoon, ladies and

Remarks by David Dodge Governor of the Bank of Canada to the Board of Trade of Metropolitan Montreal Montréal, Quebec 11 February 2004 Adjusting to a Changing Economic World Good afternoon, ladies and

Debt, consolidation and growth

Debt, consolidation and growth Robert Chote Annual meeting of OECD PBO and IFI officials Paris, 23 February 2012 Outline Very interesting paper. Will focus on UK approach to these issues rather than detailed

Debt, consolidation and growth Robert Chote Annual meeting of OECD PBO and IFI officials Paris, 23 February 2012 Outline Very interesting paper. Will focus on UK approach to these issues rather than detailed

a) Aggregate Demand (AD) and Aggregate Supply (AS) analysis

Aggregate Demand (AD) and Aggregate Supply (AS) analysis") a) Aggregate Demand (AD) and Aggregate Supply (AS) analysis Determinants of AD: Aggregate demand is the total demand in the economy. It measures spending on goods and services by consumers, firms, the

a) Aggregate Demand (AD) and Aggregate Supply (AS) analysis Determinants of AD: Aggregate demand is the total demand in the economy. It measures spending on goods and services by consumers, firms, the

Economy, Capital Markets & Strategy

Sébastien Mc Mahon, CFA Economist Member, Asset Mix Committee Economy, Capital Markets & Strategy 2014 National Business Conference October 2014 1 October 23, 2014 Disclaimer Opinions expressed in this

Sébastien Mc Mahon, CFA Economist Member, Asset Mix Committee Economy, Capital Markets & Strategy 2014 National Business Conference October 2014 1 October 23, 2014 Disclaimer Opinions expressed in this

AUTUMN STATEMENT 2014

AUTUMN STATEMENT 2014 Cm 8961 December 2014 AUTUMN STATEMENT 2014 Presented to Parliament by the Chancellor of the Exchequer by Command of Her Majesty December 2014 Cm 8961 Crown copyright 2014 You may

AUTUMN STATEMENT 2014 Cm 8961 December 2014 AUTUMN STATEMENT 2014 Presented to Parliament by the Chancellor of the Exchequer by Command of Her Majesty December 2014 Cm 8961 Crown copyright 2014 You may

Credit Card Maxed Out? How UK debt statistics have been misrepresented

Credit Card Maxed Out? How UK debt statistics have been misrepresented Howard Reed If you have maxed out your credit card, if you put off dealing with the problem, the problem gets worse. (David Cameron,

Credit Card Maxed Out? How UK debt statistics have been misrepresented Howard Reed If you have maxed out your credit card, if you put off dealing with the problem, the problem gets worse. (David Cameron,

Eurozone. EY Eurozone Forecast September 2013

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Finland

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Finland

Government spending on public services in Scotland: current patterns and future issues

Government spending on public services in Scotland: current patterns and future issues IFS Briefing Note BN140 Ben Deaner David Phillips Government spending on public services in Scotland: current patterns

Government spending on public services in Scotland: current patterns and future issues IFS Briefing Note BN140 Ben Deaner David Phillips Government spending on public services in Scotland: current patterns

HOW BAD IS THE CURRENT RECESSION? LABOUR MARKET DOWNTURNS SINCE THE 1960s

HOW BAD IS THE CURRENT RECESSION? LABOUR MARKET DOWNTURNS SINCE THE 1960s Executive summary The New Zealand economy experienced a fall in real GDP over the five quarters to March 2009 and further falls

HOW BAD IS THE CURRENT RECESSION? LABOUR MARKET DOWNTURNS SINCE THE 1960s Executive summary The New Zealand economy experienced a fall in real GDP over the five quarters to March 2009 and further falls

Impact of the recession

Regional Trends 43 21/11 Impact of the recession By Cecilia Campos, Alistair Dent, Robert Fry and Alice Reid, Office for National Statistics Abstract This report looks at the impact that the most recent

Regional Trends 43 21/11 Impact of the recession By Cecilia Campos, Alistair Dent, Robert Fry and Alice Reid, Office for National Statistics Abstract This report looks at the impact that the most recent

An outlook on the Spanish economy Official Monetary and Financial Institutions Forum (OMFIF), London

, London") 09.02.2016 An outlook on the Spanish economy Official Monetary and Financial Institutions Forum (OMFIF), London Luis M. Linde Governor I would like to thank OMFIF and Mr. David Marsh for the invitation

09.02.2016 An outlook on the Spanish economy Official Monetary and Financial Institutions Forum (OMFIF), London Luis M. Linde Governor I would like to thank OMFIF and Mr. David Marsh for the invitation

Monetary Policy Report

Monetary Policy Report February 15 S V E R I G E S R I K S B A N K Correction 15--13 Two figures on page 3 were switched around in the previous version of the report. This meant that references to Figures

Monetary Policy Report February 15 S V E R I G E S R I K S B A N K Correction 15--13 Two figures on page 3 were switched around in the previous version of the report. This meant that references to Figures

The Saturday Economist

Special Feature - Who bought all the gits? According to the latest figures from the Debt Management Office (Q2 2011), the total market value of central government liabilities was 1.1 trillion of which

Special Feature - Who bought all the gits? According to the latest figures from the Debt Management Office (Q2 2011), the total market value of central government liabilities was 1.1 trillion of which

ANNEX 1 - MACROECONOMIC IMPLICATIONS FOR ITALY OF ACHIEVING COMPLIANCE WITH THE DEBT RULE UNDER TWO DIFFERENT SCENARIOS

ANNEX 1 - MACROECONOMIC IMPLICATIONS FOR ITALY OF ACHIEVING COMPLIANCE WITH THE DEBT RULE UNDER TWO DIFFERENT SCENARIOS The aim of this note is first to illustrate the impact of a fiscal adjustment aimed

ANNEX 1 - MACROECONOMIC IMPLICATIONS FOR ITALY OF ACHIEVING COMPLIANCE WITH THE DEBT RULE UNDER TWO DIFFERENT SCENARIOS The aim of this note is first to illustrate the impact of a fiscal adjustment aimed

Scotland s Balance Sheet. April 2013

Scotland s Balance Sheet April 2013 Contents Executive Summary... 1 Introduction and Overview... 2 Public Spending... 5 Scottish Tax Revenue... 12 Overall Fiscal Position and Public Sector Debt... 18 Conclusion...

Scotland s Balance Sheet April 2013 Contents Executive Summary... 1 Introduction and Overview... 2 Public Spending... 5 Scottish Tax Revenue... 12 Overall Fiscal Position and Public Sector Debt... 18 Conclusion...

UK Economic Outlook. The UK economic recovery: Better balanced than you might think Which industries will drive future jobs growth in the UK?

March 2016 UK Economic Outlook The UK economic recovery: Better balanced than you might think Which industries will drive future jobs growth in the UK? Visit our blog for periodic updates at: pwc.blogs.com/economics_in_business

March 2016 UK Economic Outlook The UK economic recovery: Better balanced than you might think Which industries will drive future jobs growth in the UK? Visit our blog for periodic updates at: pwc.blogs.com/economics_in_business

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation

August 2014 Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook for factors that typically impact

August 2014 Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook for factors that typically impact

IV. Investment dynamics in the euro area since the crisis (40)

") 199Q1 1997Q1 1999Q1 21Q1 23Q1 2Q1 27Q1 29Q1 211Q1 213Q1 IV. Investment dynamics in the euro area since the crisis (4) This section analyses the investment dynamics in the euro area since the global financial

199Q1 1997Q1 1999Q1 21Q1 23Q1 2Q1 27Q1 29Q1 211Q1 213Q1 IV. Investment dynamics in the euro area since the crisis (4) This section analyses the investment dynamics in the euro area since the global financial

Scottish Independence. Charting the implications of demographic change. Ben Franklin. I May 2014 I. www.ilc.org.uk

Scottish Independence Charting the implications of demographic change Ben Franklin I May 2014 I www.ilc.org.uk Summary By 2037 Scotland s working age population is expected to be 3.5% than it was in 2013

Scottish Independence Charting the implications of demographic change Ben Franklin I May 2014 I www.ilc.org.uk Summary By 2037 Scotland s working age population is expected to be 3.5% than it was in 2013

2. UK Government debt and borrowing

2. UK Government debt and borrowing How well do you understand the current UK debt position and the options open to Government to reduce the deficit? This leaflet gives you a general background to the

2. UK Government debt and borrowing How well do you understand the current UK debt position and the options open to Government to reduce the deficit? This leaflet gives you a general background to the

FLASH ECONOMICS. Are there good reasons not to accept 1% inflation in the euro zone? ECONOMIC RESEARCH

ECONOMICS ECONOMIC RESEARCH 7 November - No. 9 Are there good reasons not to accept % inflation in the euro zone? The ECB is going to adopt an even more expansionary monetary policy, with the risks that

ECONOMICS ECONOMIC RESEARCH 7 November - No. 9 Are there good reasons not to accept % inflation in the euro zone? The ECB is going to adopt an even more expansionary monetary policy, with the risks that

Tutor2u Economics Essay Plans Summer 2002

Macroeconomics Revision Essay Plan (2): Inflation and Unemployment and Economic Policy (a) Explain why it is considered important to control inflation (20 marks) (b) Discuss how a government s commitment

Macroeconomics Revision Essay Plan (2): Inflation and Unemployment and Economic Policy (a) Explain why it is considered important to control inflation (20 marks) (b) Discuss how a government s commitment

Gains from Trade? The Net Effect of the Trans-Pacific Partnership Agreement on U.S. Wages

September 2013 Gains from Trade? The Net Effect of the Trans-Pacific Partnership Agreement on U.S. Wages By David Rosnick* Center for Economic and Policy Research 1611 Connecticut Ave. NW Suite 400 Washington,

September 2013 Gains from Trade? The Net Effect of the Trans-Pacific Partnership Agreement on U.S. Wages By David Rosnick* Center for Economic and Policy Research 1611 Connecticut Ave. NW Suite 400 Washington,

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES. Hamid Raza PhD Student, Economics University of Limerick Ireland

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES Hamid Raza PhD Student, Economics University of Limerick Ireland Financialisation Financialisation as a broad concept refers to: a) an

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES Hamid Raza PhD Student, Economics University of Limerick Ireland Financialisation Financialisation as a broad concept refers to: a) an

Agents summary of business conditions

Agents summary of business conditions July Annual growth in the value of retail sales and consumer services had risen slightly over the first six months of the year, but remained modest. Activity in the

Agents summary of business conditions July Annual growth in the value of retail sales and consumer services had risen slightly over the first six months of the year, but remained modest. Activity in the

6. Economic Outlook. The International Economy. Graph 6.2 Terms of Trade Log scale, 2012/13 average = 100

6. Economic Outlook The International Economy Growth of Australia s major trading partners is expected to be around its long-run average in 015 and 016 (Graph 6.1). Forecasts for 015 have been revised

6. Economic Outlook The International Economy Growth of Australia s major trading partners is expected to be around its long-run average in 015 and 016 (Graph 6.1). Forecasts for 015 have been revised

Background. Key points

Background Employment forecasts over the three years to March 2018 1 are presented in this report. These employment forecasts will inform the Ministry s advice relating to immigration priorities, and priority

Background Employment forecasts over the three years to March 2018 1 are presented in this report. These employment forecasts will inform the Ministry s advice relating to immigration priorities, and priority

Price projection 2013

Price projection 2013 CONTENTS 1. PRICE PROJECTION 2013 3 2. ECONOMIC SITUATION 3 2.1. Finland 4 2.2. Sweden 5 2.3. Norway 5 2.4. Denmark 5 2.5. United Kingdom 5 2.6. The Netherlands 5 3. CURRENCY EXCHANGE

Price projection 2013 CONTENTS 1. PRICE PROJECTION 2013 3 2. ECONOMIC SITUATION 3 2.1. Finland 4 2.2. Sweden 5 2.3. Norway 5 2.4. Denmark 5 2.5. United Kingdom 5 2.6. The Netherlands 5 3. CURRENCY EXCHANGE

Economic Overview. East Asia managed to weather the global recession by relying on export-oriented

Economic Overview Economic growth remains strong in East Asia and retains healthy momentum thanks to strong commodity prices and increases in exports. leads the region in growth and its GDP is expected

Economic Overview Economic growth remains strong in East Asia and retains healthy momentum thanks to strong commodity prices and increases in exports. leads the region in growth and its GDP is expected

COMMISSION OPINION. of XXX. on the Draft Budgetary Plan of ITALY

EUROPEAN COMMISSION Brussels, XXX [ ](2013) XXX draft COMMISSION OPINION of XXX on the Draft Budgetary Plan of ITALY EN EN COMMISSION OPINION of XXX on the Draft Budgetary Plan of ITALY GENERAL CONSIDERATIONS

EUROPEAN COMMISSION Brussels, XXX [ ](2013) XXX draft COMMISSION OPINION of XXX on the Draft Budgetary Plan of ITALY EN EN COMMISSION OPINION of XXX on the Draft Budgetary Plan of ITALY GENERAL CONSIDERATIONS

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013 U.S. stock market performance in 2012 * +12.59% total return +6.35%

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013 U.S. stock market performance in 2012 * +12.59% total return +6.35%

General Certificate of Education Advanced Level Examination January 2010

General Certificate of Education Advanced Level Examination January 2010 Economics ECON4 Unit 4 The National and International Economy Tuesday 2 February 2010 1.30 pm to 3.30 pm For this paper you must

General Certificate of Education Advanced Level Examination January 2010 Economics ECON4 Unit 4 The National and International Economy Tuesday 2 February 2010 1.30 pm to 3.30 pm For this paper you must

FLEXIBLE EXCHANGE RATES

FLEXIBLE EXCHANGE RATES Along with globalization has come a high degree of interdependence. Central to this is a flexible exchange rate system, where exchange rates are determined each business day by

FLEXIBLE EXCHANGE RATES Along with globalization has come a high degree of interdependence. Central to this is a flexible exchange rate system, where exchange rates are determined each business day by

Scottish Socialist Party Submission to. the Local Tax Commission 2015

Scottish Socialist Party Submission to the Local Tax Commission 2015 1 INTRODUCTION The Scottish Socialist Party welcomes the Scottish Parliament s call for evidence on improved ways to fund Local Government

Scottish Socialist Party Submission to the Local Tax Commission 2015 1 INTRODUCTION The Scottish Socialist Party welcomes the Scottish Parliament s call for evidence on improved ways to fund Local Government

BANK OF UGANDA. Remarks by Prof. Emmanuel Tumusiime-Mutebile, Governor, Bank of Uganda, To members of the Uganda Manufacturers Association

BANK OF UGANDA Remarks by Prof. Emmanuel Tumusiime-Mutebile, Governor, Bank of Uganda, To members of the Uganda Manufacturers Association At Lugogo Show ground Thursday July 02, 2015 Page 1 of 5 The Depreciation

BANK OF UGANDA Remarks by Prof. Emmanuel Tumusiime-Mutebile, Governor, Bank of Uganda, To members of the Uganda Manufacturers Association At Lugogo Show ground Thursday July 02, 2015 Page 1 of 5 The Depreciation

Economic Outlook for Europe and Finland

Economic Outlook for Europe and Finland Finnish-British Chamber of Commerce 15 March 213 Seppo Honkapohja Member of the Board Bank of Finland 1 World economy: World industrial output improved, but international

Economic Outlook for Europe and Finland Finnish-British Chamber of Commerce 15 March 213 Seppo Honkapohja Member of the Board Bank of Finland 1 World economy: World industrial output improved, but international

LEVEL ECONOMICS. ECON2/Unit 2 The National Economy Mark scheme. June 2014. Version 1.0/Final

LEVEL ECONOMICS ECON2/Unit 2 The National Economy Mark scheme June 2014 Version 1.0/Final Mark schemes are prepared by the Lead Assessment Writer and considered, together with the relevant questions, by

LEVEL ECONOMICS ECON2/Unit 2 The National Economy Mark scheme June 2014 Version 1.0/Final Mark schemes are prepared by the Lead Assessment Writer and considered, together with the relevant questions, by

Economic and fiscal outlook

Economic and fiscal outlook March 2015 Cm 9024 Office for Budget Responsibility: Economic and fiscal outlook Presented to Parliament by the Economic Secretary to the Treasury by Command of Her Majesty

Economic and fiscal outlook March 2015 Cm 9024 Office for Budget Responsibility: Economic and fiscal outlook Presented to Parliament by the Economic Secretary to the Treasury by Command of Her Majesty

Explanation beyond exchange rates: trends in UK trade since 2007

Explanation beyond exchange rates: trends in UK trade since 2007 Author Name(s): Michael Hardie, Andrew Jowett, Tim Marshall & Philip Wales, Office for National Statistics Abstract The UK s trade performance

Explanation beyond exchange rates: trends in UK trade since 2007 Author Name(s): Michael Hardie, Andrew Jowett, Tim Marshall & Philip Wales, Office for National Statistics Abstract The UK s trade performance

NEWS FROM DANMARKS NATIONALBANK

1ST QUARTER 2015 N0 1 NEWS FROM DANMARKS NATIONALBANK PROSPECT OF HIGHER GROWTH IN DENMARK Danmarks Nationalbank adjusts its forecast of growth in the Danish economy this year and next year upwards. GDP

1ST QUARTER 2015 N0 1 NEWS FROM DANMARKS NATIONALBANK PROSPECT OF HIGHER GROWTH IN DENMARK Danmarks Nationalbank adjusts its forecast of growth in the Danish economy this year and next year upwards. GDP

Statistical Bulletin. The Effects of Taxes and Benefits on Household Income, 2011/12. Key points

Statistical Bulletin The Effects of Taxes and Benefits on Household Income, 2011/12 Coverage: UK Date: 10 July 2013 Geographical Area: UK and GB Theme: Economy Theme: People and Places Key points There

Statistical Bulletin The Effects of Taxes and Benefits on Household Income, 2011/12 Coverage: UK Date: 10 July 2013 Geographical Area: UK and GB Theme: Economy Theme: People and Places Key points There

Unemployment and Economic Recovery

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 11-17-2009 Unemployment and Economic Recovery Brian W. Cashell Congressional Research Service Follow this and

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 11-17-2009 Unemployment and Economic Recovery Brian W. Cashell Congressional Research Service Follow this and

Research. What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields?

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

ARC Assigns BBB Rating to Italy

ARC Assigns BBB Rating to Italy ISSUER RATINGS DATE Republic of Italy August 28, 2015 ISSUER RATINGS - FOREIGN CURRENCY Medium and Long Term BBB (BBB, Stable) ISSUER RATINGS - LOCAL CURRENCY Medium and

ARC Assigns BBB Rating to Italy ISSUER RATINGS DATE Republic of Italy August 28, 2015 ISSUER RATINGS - FOREIGN CURRENCY Medium and Long Term BBB (BBB, Stable) ISSUER RATINGS - LOCAL CURRENCY Medium and

Fiscal Consolidation, the Economy and Employment. Tony Makin Professor of Economics, Griffith Business School, Gold Coast campus

Fiscal Consolidation, the Economy and Employment Tony Makin Professor of Economics, Griffith Business School, Gold Coast campus 1 Key Themes Australia s Worsened Competitiveness Productivity and Labour

Fiscal Consolidation, the Economy and Employment Tony Makin Professor of Economics, Griffith Business School, Gold Coast campus 1 Key Themes Australia s Worsened Competitiveness Productivity and Labour

EFN REPORT. ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016 Spring 2015 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016 Spring 2015 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

2. The European insurance sector 1

2. The European insurance sector 1 As discussed in Chapter 1, the economic conditions in European countries are still fragile, despite some improvements in the first half of 2013. 2.1. Market growth The

2. The European insurance sector 1 As discussed in Chapter 1, the economic conditions in European countries are still fragile, despite some improvements in the first half of 2013. 2.1. Market growth The

Budget priorities: cut company tax, invest in infrastructure and balance budget within five years.

Ai Group Survey Business Priorities for the 2014-15 Federal Budget Budget priorities: cut company tax, invest in infrastructure and balance budget within five years. 4 May 2014 The top three priorities

Ai Group Survey Business Priorities for the 2014-15 Federal Budget Budget priorities: cut company tax, invest in infrastructure and balance budget within five years. 4 May 2014 The top three priorities

International Trade Monitor

British Small and Medium-Sized Enterprises Split Over Health of the UK Economy Overall SME importer and exporter confidence sees dip in Q1 Increase in SMEs hurt by sterling volatility Eurozone concerns

British Small and Medium-Sized Enterprises Split Over Health of the UK Economy Overall SME importer and exporter confidence sees dip in Q1 Increase in SMEs hurt by sterling volatility Eurozone concerns

Statement by. Janet L. Yellen. Chair. Board of Governors of the Federal Reserve System. before the. Committee on Financial Services

For release at 8:30 a.m. EST February 10, 2016 Statement by Janet L. Yellen Chair Board of Governors of the Federal Reserve System before the Committee on Financial Services U.S. House of Representatives

For release at 8:30 a.m. EST February 10, 2016 Statement by Janet L. Yellen Chair Board of Governors of the Federal Reserve System before the Committee on Financial Services U.S. House of Representatives

The Financial and Business Services growth sector is defined by the Standard Industrialisation Classification (SIC) 2007 codes:

2007 codes:") Growth Sector Briefing Financial and Business Services Office of the Chief Economic Adviser, Scottish Government May 2015 Growth Sector Definition Scotland s Financial and Business Services industry was

Growth Sector Briefing Financial and Business Services Office of the Chief Economic Adviser, Scottish Government May 2015 Growth Sector Definition Scotland s Financial and Business Services industry was

GCSE. Economics. Mark Scheme for June 2013. General Certificate of Secondary Education Unit A593: The UK Economy and Globalisation

GCSE Economics General Certificate of Secondary Education Unit A593: The UK Economy and Globalisation Mark Scheme for June 2013 Oxford Cambridge and RSA Examinations OCR (Oxford Cambridge and RSA) is a

GCSE Economics General Certificate of Secondary Education Unit A593: The UK Economy and Globalisation Mark Scheme for June 2013 Oxford Cambridge and RSA Examinations OCR (Oxford Cambridge and RSA) is a

The Credit Card Report May 4 The Credit Card Report May 4 Contents Visa makes no representations or warranties about the accuracy or suitability of the information or advice provided. You use the information

The Credit Card Report May 4 The Credit Card Report May 4 Contents Visa makes no representations or warranties about the accuracy or suitability of the information or advice provided. You use the information

The U.S. and Midwest Economy in 2016: Implications for Supply Chain Firms

The U.S. and Midwest Economy in 2016: Implications for Supply Chain Firms Rick Mattoon Senior Economist and Economic Advisor Federal Reserve Bank of Chicago Right Place Supply Chain Management Conference

The U.S. and Midwest Economy in 2016: Implications for Supply Chain Firms Rick Mattoon Senior Economist and Economic Advisor Federal Reserve Bank of Chicago Right Place Supply Chain Management Conference

Economic Outlook, November 2013 November 21, 2013. Jeffrey M. Lacker President Federal Reserve Bank of Richmond

Economic Outlook, November 2013 November 21, 2013 Jeffrey M. Lacker President Federal Reserve Bank of Richmond Asheboro SCORE Asheboro, North Carolina It's a pleasure to be with you today to discuss the

Economic Outlook, November 2013 November 21, 2013 Jeffrey M. Lacker President Federal Reserve Bank of Richmond Asheboro SCORE Asheboro, North Carolina It's a pleasure to be with you today to discuss the