EC3070 FINANCIAL DERIVATIVES. Exercise 1

|

|

|

- Brooke Ryan

- 10 years ago

- Views:

Transcription

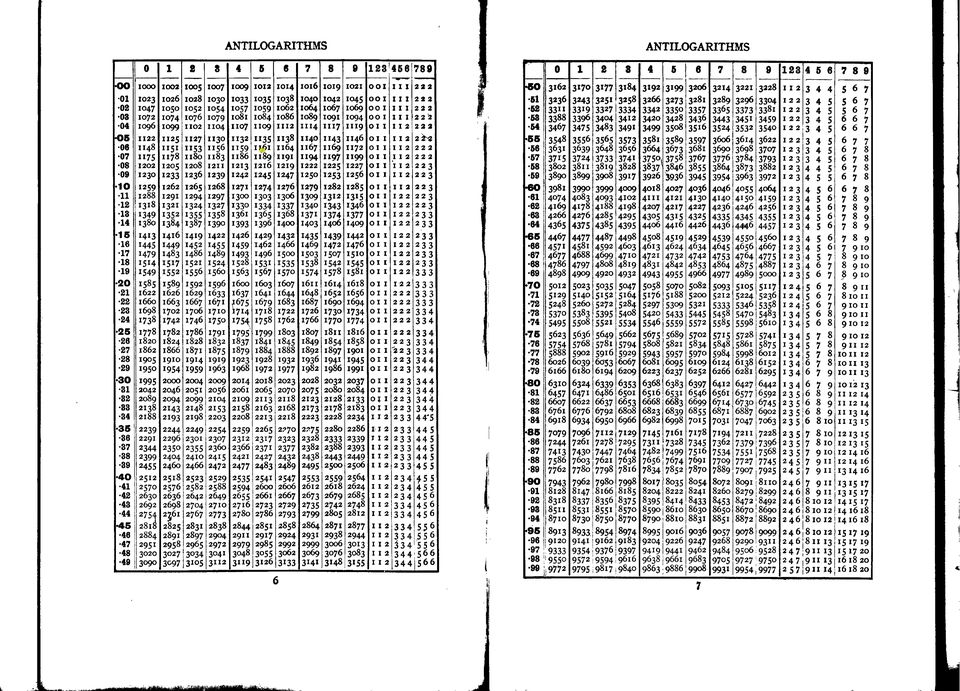

1 EC3070 FINANCIAL DERIVATIVES Exercise 1 1. A credit card company charges an annual interest rate of 15%, which is effective only if the interest on the outstanding debts is paid in monthly instalments. Otherwise, the interest charges are compounded with the borrowings. What would be the effective annual rate of interest if Q are borrowed at the beginning of the year and repaid with interest at the end of the year? Answer. Interest is charged each month on the outstanding loan at the rate of 15/12 = 1.25%. Therefore, after one year, the total amount that must be repaid is $Q( ) 12 =$Q1.161, which gives an effective annual rate of interest of 16%. Using log tables, I compute ( ) 12 as Antilog{12 log(1.0125)} = Antilog{ } = Antilog{0.0640} = , which gives 16% approximately. (In fact, for this calculation, four-figure base-10 logarithms are insufficiently accurate.) The alternative is to enter in your calculator to do the multiplication twelve times over. 1

2

3

4 EC3070 Exercise 1 2. How long will it take to double your investment if you receive an annual rate of interest of 5% and if the interest is compounded with the principal? Answer. The equation to be solved is (1 + r) n =2 where r =0.05 is the rate of interest. The solution, using log tables, is n = log 2 log(1 + r) = log 2 log(1.05) = =14.2, which is confirmed by my computer. My calculator tells me that =

= log 2 log(1.05) = 0.")

5 The Natural Number The natural number e. The number e = { } is defined by ( e = lim(n ) 1+ n) 1 n. The binomial expansion indicates that (a + b) n =a n + na n 1 n(n 1) b + a n 2 b 2 + 2! n(n 1)(n 2) a n 3 b ! Using this, we get ( 1+ n) 1 n ( ) ( ) 2 1 n(n 1) 1 =1+n + + n 2! n ( ) 3 n(n 1)(n 2) ! n Taking limits as n of each term of the expansion gives ( lim(n ) 1+ 1 ) n = 1 n 0! + 1 1! + 1 2! = e. 3!

3 n(n 1)(n 2) 1 +. 3! n Taking limits as n of each term of the expansion gives ( lim(n ) 1+ 1 ) n = 1 n 0!")

6 The Natural Number The expansion of e x. There is also ( e x = lim(p ) 1+ 1 ) px p ( = lim(n ) 1+ n) x n ; n = px. Using the binomial expansion in the same way as before, it can be shown that e x = x0 0! + x 1! + x2 2! + x3 3! +. Also e xt =1+xt + x2 t 2 2! + x3 t 3 3! +.

7 EC3070 FINANCIAL DERIVATIVES 3. With reference to the relevant Taylor-series expansions, demonstrate the following approximations ln(1 + x) x, e x 1+x, which are valid when x is small. Calculate the value of n in question 2 using the relevant approximation in the denominator. Answer. Observe that, in this case, we must work with natural logarithms as opposed to base-10 logarithms. The calculation is as follows: n = ln 2 ln(1 + r) ln 2 r =

8 Geometric Progression The Expansion of (1 x) 1 The simplest of all power series expansions is that of the geometric progression: 1 1 x =1+x + x2 + x 3 + x 4 +. There are various way of achieving this expansion, including by the use of Taylor s theorem. Another way is by the method of detached coefficients. We assume that (1 x) 1 = {α 0 + α 1 x + α 2 x 2 + }, and we rewrite this equation as 1= { 1 x} { α 0 + α 1 x + α 2 x 2 + }. Then, by performing the multiplication on the RHS, and by equating the coefficients of the same powers of x on the two sides of the equation, we find that 1=α 0, 0=α 1 α 0, 0=α 2 α 1,.. 0=α n α n 1, α 0 =1, α 1 = α 0 =1, α 2 = α 1 =1,.. α n = α n 1 =1.

9 Geometric Progression Another way of achieving the expansion is by long division: ) 1 x 1+x + x x x x x 2 x 2 x 2 x 3 The Sum of a Geometric Progression We can also proceed in the opposite direction. That is to say, we can evaluate S = {1+x + x 2 + } to show that S =(1 x) 1. The calculation is as follows: S =1+x + x 2 + xs = x + x 2 + S xs =1. Then S(1 x) = 1 immediately implies that S =1/(1 x).

10 Geometric Progression The Partial Sum of a Geometric Progression There is also a formula for the partial sum of the first n terms of the series, which is S n =1+x + + x n 1. Consider the following subtraction: S =1+x + + x n 1 + x n + x n+1 + x n S = x n + x n+1 + S x n S =1+x + + x n 1. This shows that S(1 x n )=S n, whence S n = 1 xn 1 x. Example. An annuity is a sequence of regular payments, made once a year, until the end of the nth year. Usually, such an annuity may be sold to another holder; and, almost invariably, its outstanding value can be redeemed from the institution which has contracted to make the payments. There is clearly a need to determine the present value of the annuity if it is to be sold or redeemed. The principle which is applied for this purpose is that of discounting.

11 Geometric Progression Imagine that a sum of A is invested for one year at an annual rate of interest of r 100%. At the end the year, the principal sum is returned together with the interest via a payment of (1 + r)a. A straightforward conclusion is that (1 + r)a to be paid one year hence has the value of A paid today. By the same token, A to be paid one year hence has a present value of V = A 1+r = Aδ, where δ = 1 1+r is the discount rate. It follows that A to be paid two years hence has a present value of Aδ 2. More generally, if the sum of A is to be paid n years hence, then it is worth Aδ n today. The present value of an annuity of ra to be paid for the next n years is therefore V n = Ar(δ + δ δ n )=Arδ ( 1+δ + + δ n 1) = Arδ 1 δn 1 δ = A(1 δn ), since δ 1 δ = r. If the principal sum is to be repaid at the end of the nth year, then the present value of the contract will be A(1 δ n )+Aδ n = A, which is precisely equal to the value of the sum that is to be invested.

12 EC3070 Exercise 1 4. Using the expression x = e y =10 z, find a formula that will enable you to convert between log e x and log 10 x, commonly denoted by log x and ln x, respectively the latter being described as a natural logarithm or a Naperian logarithm. Answer. Here, there are y = log e (x) and z = log 10 (x). By taking natural logarithms of the equation x = e y =10 z,weget Also, observe that y = log e (x) =z log e (10) = log 10 (x) log e (10) 10 = e log e (10) implies log 10 (10) = 1 = log e (10) log 10 (e). Therefore, log e (x) = log 10(x) log 10 (e) and log 10 (x) = log e(x) log e (10). 4

=z log e (10) = log 10 (x) log e (10) 10 = e log e")

13 ARTIST: Sam Cooke, TITLE: Wonderful World (Don t Know Much) Don t know much about history Don t know much biology Don t know much about a science book Don t know much about the French I took But I do know that I love you And I know that if you love me too What a wonderful world this would be Don t know much about geography Don t know much trigonometry Don t know much about algebra Don t know what a slide rule is for But I know that one and one is two And if this one could be with you What a wonderful world this would be Now, I don t claim to be an A student But I m trying to be For maybe by being an A student baby I can win your love for me

14 Basic Slide Rule Instructions Calculation on a slide rule To multiply two numbers on a typical slide rule, the user marks one of the factors on the upper C scale. (In this case, it is 16.6). The second factor is marked on the lower D scale (In this case, it is 42.2). Then, the upper scale is slid forwards until its starting value of unity is aligned with the point on the lower scale marking the second factor. The point which is reached on the lower scale by the mark on the upper scale corresponds to the product of the two factors (700). By these means, the user effectively adds the logs (lengths) of the two numbers and finds the antilog of the sum. A calculation on a slide rule showing that 42.2 x 16.6 = 700

.")

15 EC3070 FINANCIAL DERIVATIVES 5. Let S n =1+r + r r n 1, which is a partial sum of n terms of an geometric progression. Show that S n + r n =1+rS n and thence derive an expression of S n in terms of r. Answer. By rearranging the given expression, we get S n (1 r) =1 r n, whence S n = 1 rn 1 r. 5

16 EC3070 Exercise 1 6. Annual payments of M must be made over a period of n years to redeem a mortgage. The present value of this stream of payments is M(δ + δ δ n ). where δ =(1+r) 1 is the rate of discount and r is the rate of interest. The present value of the stream of payments must equate to the value L of the loan. If the loan was for 150,000 and the rate of interest was fixed at 5% for the entire period, what should be the size of the annual payment in order to redeem the loan in 20 year s time? Answer. The present value of the payments is Mδ(1 + δ + δ δ n 1 )=M δ(1 δn ) 1 δ = L, whence M = L 1 δ δ(1 δ n ) = (γ 1) Lγn γ n where γ = δ 1 =1+r. 1 with L = 150, 000, n = 20 and 1 + r =1.05, we find that M =12,

=M δ(1 δn ) 1 δ = L, whence M = L 1 δ δ(1 δ n ) = (γ 1) Lγn γ n where γ = δ 1 =1+r.")

9.2 Summation Notation

9. Summation Notation 66 9. Summation Notation In the previous section, we introduced sequences and now we shall present notation and theorems concerning the sum of terms of a sequence. We begin with a

9. Summation Notation 66 9. Summation Notation In the previous section, we introduced sequences and now we shall present notation and theorems concerning the sum of terms of a sequence. We begin with a

Solutions to Supplementary Questions for HP Chapter 5 and Sections 1 and 2 of the Supplementary Material. i = 0.75 1 for six months.

Solutions to Supplementary Questions for HP Chapter 5 and Sections 1 and 2 of the Supplementary Material 1. a) Let P be the recommended retail price of the toy. Then the retailer may purchase the toy at

Solutions to Supplementary Questions for HP Chapter 5 and Sections 1 and 2 of the Supplementary Material 1. a) Let P be the recommended retail price of the toy. Then the retailer may purchase the toy at

2.1 The Present Value of an Annuity

2.1 The Present Value of an Annuity One example of a fixed annuity is an agreement to pay someone a fixed amount x for N periods (commonly months or years), e.g. a fixed pension It is assumed that the

2.1 The Present Value of an Annuity One example of a fixed annuity is an agreement to pay someone a fixed amount x for N periods (commonly months or years), e.g. a fixed pension It is assumed that the

The Basics of Interest Theory

Contents Preface 3 The Basics of Interest Theory 9 1 The Meaning of Interest................................... 10 2 Accumulation and Amount Functions............................ 14 3 Effective Interest

Contents Preface 3 The Basics of Interest Theory 9 1 The Meaning of Interest................................... 10 2 Accumulation and Amount Functions............................ 14 3 Effective Interest

Chapter 2. CASH FLOW Objectives: To calculate the values of cash flows using the standard methods.. To evaluate alternatives and make reasonable

Chapter 2 CASH FLOW Objectives: To calculate the values of cash flows using the standard methods To evaluate alternatives and make reasonable suggestions To simulate mathematical and real content situations

Chapter 2 CASH FLOW Objectives: To calculate the values of cash flows using the standard methods To evaluate alternatives and make reasonable suggestions To simulate mathematical and real content situations

Discrete Mathematics: Homework 7 solution. Due: 2011.6.03

EE 2060 Discrete Mathematics spring 2011 Discrete Mathematics: Homework 7 solution Due: 2011.6.03 1. Let a n = 2 n + 5 3 n for n = 0, 1, 2,... (a) (2%) Find a 0, a 1, a 2, a 3 and a 4. (b) (2%) Show that

EE 2060 Discrete Mathematics spring 2011 Discrete Mathematics: Homework 7 solution Due: 2011.6.03 1. Let a n = 2 n + 5 3 n for n = 0, 1, 2,... (a) (2%) Find a 0, a 1, a 2, a 3 and a 4. (b) (2%) Show that

DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS

Chapter 5 DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS The basic PV and FV techniques can be extended to handle any number of cash flows. PV with multiple cash flows: Suppose you need $500 one

Chapter 5 DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS The basic PV and FV techniques can be extended to handle any number of cash flows. PV with multiple cash flows: Suppose you need $500 one

Introduction to Real Estate Investment Appraisal

Introduction to Real Estate Investment Appraisal Maths of Finance Present and Future Values Pat McAllister INVESTMENT APPRAISAL: INTEREST Interest is a reward or rent paid to a lender or investor who has

Introduction to Real Estate Investment Appraisal Maths of Finance Present and Future Values Pat McAllister INVESTMENT APPRAISAL: INTEREST Interest is a reward or rent paid to a lender or investor who has

CHAPTER 1. Compound Interest

CHAPTER 1 Compound Interest 1. Compound Interest The simplest example of interest is a loan agreement two children might make: I will lend you a dollar, but every day you keep it, you owe me one more penny.

CHAPTER 1 Compound Interest 1. Compound Interest The simplest example of interest is a loan agreement two children might make: I will lend you a dollar, but every day you keep it, you owe me one more penny.

Discounted Cash Flow Valuation

6 Formulas Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter Outline Future and Present Values of Multiple Cash Flows Valuing

6 Formulas Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter Outline Future and Present Values of Multiple Cash Flows Valuing

1 Interest rates, and risk-free investments

Interest rates, and risk-free investments Copyright c 2005 by Karl Sigman. Interest and compounded interest Suppose that you place x 0 ($) in an account that offers a fixed (never to change over time)

Interest rates, and risk-free investments Copyright c 2005 by Karl Sigman. Interest and compounded interest Suppose that you place x 0 ($) in an account that offers a fixed (never to change over time)

GEOMETRIC SEQUENCES AND SERIES

4.4 Geometric Sequences and Series (4 7) 757 of a novel and every day thereafter increase their daily reading by two pages. If his students follow this suggestion, then how many pages will they read during

4.4 Geometric Sequences and Series (4 7) 757 of a novel and every day thereafter increase their daily reading by two pages. If his students follow this suggestion, then how many pages will they read during

2.3. Finding polynomial functions. An Introduction:

2.3. Finding polynomial functions. An Introduction: As is usually the case when learning a new concept in mathematics, the new concept is the reverse of the previous one. Remember how you first learned

2.3. Finding polynomial functions. An Introduction: As is usually the case when learning a new concept in mathematics, the new concept is the reverse of the previous one. Remember how you first learned

International Financial Strategies Time Value of Money

International Financial Strategies 1 Future Value and Compounding Future value = cash value of the investment at some point in the future Investing for single period: FV. Future Value PV. Present Value

International Financial Strategies 1 Future Value and Compounding Future value = cash value of the investment at some point in the future Investing for single period: FV. Future Value PV. Present Value

Compound Interest. Invest 500 that earns 10% interest each year for 3 years, where each interest payment is reinvested at the same rate:

Compound Interest Invest 500 that earns 10% interest each year for 3 years, where each interest payment is reinvested at the same rate: Table 1 Development of Nominal Payments and the Terminal Value, S.

Compound Interest Invest 500 that earns 10% interest each year for 3 years, where each interest payment is reinvested at the same rate: Table 1 Development of Nominal Payments and the Terminal Value, S.

2. How would (a) a decrease in the interest rate or (b) an increase in the holding period of a deposit affect its future value? Why?

a decrease in the interest rate or (b) an increase in the holding period of a deposit affect its future value? Why?") CHAPTER 3 CONCEPT REVIEW QUESTIONS 1. Will a deposit made into an account paying compound interest (assuming compounding occurs once per year) yield a higher future value after one period than an equal-sized

CHAPTER 3 CONCEPT REVIEW QUESTIONS 1. Will a deposit made into an account paying compound interest (assuming compounding occurs once per year) yield a higher future value after one period than an equal-sized

4 Annuities and Loans

4 Annuities and Loans 4.1 Introduction In previous section, we discussed different methods for crediting interest, and we claimed that compound interest is the correct way to credit interest. This section

4 Annuities and Loans 4.1 Introduction In previous section, we discussed different methods for crediting interest, and we claimed that compound interest is the correct way to credit interest. This section

MATHEMATICS OF FINANCE AND INVESTMENT

MATHEMATICS OF FINANCE AND INVESTMENT G. I. FALIN Department of Probability Theory Faculty of Mechanics & Mathematics Moscow State Lomonosov University Moscow 119992 [email protected] 2 G.I.Falin. Mathematics

MATHEMATICS OF FINANCE AND INVESTMENT G. I. FALIN Department of Probability Theory Faculty of Mechanics & Mathematics Moscow State Lomonosov University Moscow 119992 [email protected] 2 G.I.Falin. Mathematics

Lecture Notes on the Mathematics of Finance

Lecture Notes on the Mathematics of Finance Jerry Alan Veeh February 20, 2006 Copyright 2006 Jerry Alan Veeh. All rights reserved. 0. Introduction The objective of these notes is to present the basic aspects

Lecture Notes on the Mathematics of Finance Jerry Alan Veeh February 20, 2006 Copyright 2006 Jerry Alan Veeh. All rights reserved. 0. Introduction The objective of these notes is to present the basic aspects

E INV 1 AM 11 Name: INTEREST. There are two types of Interest : and. The formula is. I is. P is. r is. t is

E INV 1 AM 11 Name: INTEREST There are two types of Interest : and. SIMPLE INTEREST The formula is I is P is r is t is NOTE: For 8% use r =, for 12% use r =, for 2.5% use r = NOTE: For 6 months use t =

E INV 1 AM 11 Name: INTEREST There are two types of Interest : and. SIMPLE INTEREST The formula is I is P is r is t is NOTE: For 8% use r =, for 12% use r =, for 2.5% use r = NOTE: For 6 months use t =

5. Time value of money

1 Simple interest 2 5. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 5. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

EAP/GWL Rev. 1/2011 Page 1 of 5. Factoring a polynomial is the process of writing it as the product of two or more polynomial factors.

EAP/GWL Rev. 1/2011 Page 1 of 5 Factoring a polynomial is the process of writing it as the product of two or more polynomial factors. Example: Set the factors of a polynomial equation (as opposed to an

EAP/GWL Rev. 1/2011 Page 1 of 5 Factoring a polynomial is the process of writing it as the product of two or more polynomial factors. Example: Set the factors of a polynomial equation (as opposed to an

COMPOUND INTEREST AND ANNUITY TABLES

COMPOUND INTEREST AND ANNUITY TABLES COMPOUND INTEREST AND ANNUITY TABLES 8 Percent VALUE OF AN NO. OF PRESENT PRESENT VALUE OF AN COM- AMORTIZ ANNUITY - ONE PER YEARS VALUE OF ANNUITY POUND ATION YEAR

COMPOUND INTEREST AND ANNUITY TABLES COMPOUND INTEREST AND ANNUITY TABLES 8 Percent VALUE OF AN NO. OF PRESENT PRESENT VALUE OF AN COM- AMORTIZ ANNUITY - ONE PER YEARS VALUE OF ANNUITY POUND ATION YEAR

Chapter 6. Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

Chapter 03 - Basic Annuities

3-1 Chapter 03 - Basic Annuities Section 7.0 - Sum of a Geometric Sequence The form for the sum of a geometric sequence is: Sum(n) a + ar + ar 2 + ar 3 + + ar n 1 Here a = (the first term) n = (the number

3-1 Chapter 03 - Basic Annuities Section 7.0 - Sum of a Geometric Sequence The form for the sum of a geometric sequence is: Sum(n) a + ar + ar 2 + ar 3 + + ar n 1 Here a = (the first term) n = (the number

Vilnius University. Faculty of Mathematics and Informatics. Gintautas Bareikis

Vilnius University Faculty of Mathematics and Informatics Gintautas Bareikis CONTENT Chapter 1. SIMPLE AND COMPOUND INTEREST 1.1 Simple interest......................................................................

Vilnius University Faculty of Mathematics and Informatics Gintautas Bareikis CONTENT Chapter 1. SIMPLE AND COMPOUND INTEREST 1.1 Simple interest......................................................................

1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%?

Chapter 2 - Sample Problems 1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%? 2. What will $247,000 grow to be in

Chapter 2 - Sample Problems 1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%? 2. What will $247,000 grow to be in

UNIT AUTHOR: Elizabeth Hume, Colonial Heights High School, Colonial Heights City Schools

Money & Finance I. UNIT OVERVIEW & PURPOSE: The purpose of this unit is for students to learn how savings accounts, annuities, loans, and credit cards work. All students need a basic understanding of how

Money & Finance I. UNIT OVERVIEW & PURPOSE: The purpose of this unit is for students to learn how savings accounts, annuities, loans, and credit cards work. All students need a basic understanding of how

The Black-Scholes Formula

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Black-Scholes Formula These notes examine the Black-Scholes formula for European options. The Black-Scholes formula are complex as they are based on the

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Black-Scholes Formula These notes examine the Black-Scholes formula for European options. The Black-Scholes formula are complex as they are based on the

Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26

![Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26](/thumbs/17/134163.jpg "Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26") Quick Quiz: Part 2 You know the payment amount for a loan and you want to know how much was borrowed. Do you compute a present value or a future value? You want to receive $5,000 per month in retirement.

Quick Quiz: Part 2 You know the payment amount for a loan and you want to know how much was borrowed. Do you compute a present value or a future value? You want to receive $5,000 per month in retirement.

Future Value. Basic TVM Concepts. Chapter 2 Time Value of Money. $500 cash flow. On a time line for 3 years: $100. FV 15%, 10 yr.

Chapter Time Value of Money Future Value Present Value Annuities Effective Annual Rate Uneven Cash Flows Growing Annuities Loan Amortization Summary and Conclusions Basic TVM Concepts Interest rate: abbreviated

Chapter Time Value of Money Future Value Present Value Annuities Effective Annual Rate Uneven Cash Flows Growing Annuities Loan Amortization Summary and Conclusions Basic TVM Concepts Interest rate: abbreviated

Geometric Series and Annuities

Geometric Series and Annuities Our goal here is to calculate annuities. For example, how much money do you need to have saved for retirement so that you can withdraw a fixed amount of money each year for

Geometric Series and Annuities Our goal here is to calculate annuities. For example, how much money do you need to have saved for retirement so that you can withdraw a fixed amount of money each year for

MATH1510 Financial Mathematics I. Jitse Niesen University of Leeds

MATH1510 Financial Mathematics I Jitse Niesen University of Leeds January May 2012 Description of the module This is the description of the module as it appears in the module catalogue. Objectives Introduction

MATH1510 Financial Mathematics I Jitse Niesen University of Leeds January May 2012 Description of the module This is the description of the module as it appears in the module catalogue. Objectives Introduction

Time Value of Money. Work book Section I True, False type questions. State whether the following statements are true (T) or False (F)

or False (F)") Time Value of Money Work book Section I True, False type questions State whether the following statements are true (T) or False (F) 1.1 Money has time value because you forgo something certain today for

Time Value of Money Work book Section I True, False type questions State whether the following statements are true (T) or False (F) 1.1 Money has time value because you forgo something certain today for

Finance CHAPTER OUTLINE. 5.1 Interest 5.2 Compound Interest 5.3 Annuities; Sinking Funds 5.4 Present Value of an Annuity; Amortization

CHAPTER 5 Finance OUTLINE Even though you re in college now, at some time, probably not too far in the future, you will be thinking of buying a house. And, unless you ve won the lottery, you will need

CHAPTER 5 Finance OUTLINE Even though you re in college now, at some time, probably not too far in the future, you will be thinking of buying a house. And, unless you ve won the lottery, you will need

1 Cash-flows, discounting, interest rate models

Assignment 1 BS4a Actuarial Science Oxford MT 2014 1 1 Cash-flows, discounting, interest rate models Please hand in your answers to questions 3, 4, 5 and 8 for marking. The rest are for further practice.

Assignment 1 BS4a Actuarial Science Oxford MT 2014 1 1 Cash-flows, discounting, interest rate models Please hand in your answers to questions 3, 4, 5 and 8 for marking. The rest are for further practice.

Level Annuities with Payments More Frequent than Each Interest Period

Level Annuities with Payments More Frequent than Each Interest Period 1 Examples 2 Annuity-immediate 3 Annuity-due Level Annuities with Payments More Frequent than Each Interest Period 1 Examples 2 Annuity-immediate

Level Annuities with Payments More Frequent than Each Interest Period 1 Examples 2 Annuity-immediate 3 Annuity-due Level Annuities with Payments More Frequent than Each Interest Period 1 Examples 2 Annuity-immediate

The time value of money: Part II

The time value of money: Part II A reading prepared by Pamela Peterson Drake O U T L I E 1. Introduction 2. Annuities 3. Determining the unknown interest rate 4. Determining the number of compounding periods

The time value of money: Part II A reading prepared by Pamela Peterson Drake O U T L I E 1. Introduction 2. Annuities 3. Determining the unknown interest rate 4. Determining the number of compounding periods

Bond Price Arithmetic

1 Bond Price Arithmetic The purpose of this chapter is: To review the basics of the time value of money. This involves reviewing discounting guaranteed future cash flows at annual, semiannual and continuously

1 Bond Price Arithmetic The purpose of this chapter is: To review the basics of the time value of money. This involves reviewing discounting guaranteed future cash flows at annual, semiannual and continuously

Financial Mathematics for Actuaries. Chapter 5 LoansandCostsofBorrowing

Financial Mathematics for Actuaries Chapter 5 LoansandCostsofBorrowing 1 Learning Objectives 1. Loan balance: prospective method and retrospective method 2. Amortization schedule 3. Sinking fund 4. Varying

Financial Mathematics for Actuaries Chapter 5 LoansandCostsofBorrowing 1 Learning Objectives 1. Loan balance: prospective method and retrospective method 2. Amortization schedule 3. Sinking fund 4. Varying

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY 1. The simple interest per year is: $5,000.08 = $400 So after 10 years you will have: $400 10 = $4,000 in interest. The total balance will be

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY 1. The simple interest per year is: $5,000.08 = $400 So after 10 years you will have: $400 10 = $4,000 in interest. The total balance will be

Lecture Notes on Actuarial Mathematics

Lecture Notes on Actuarial Mathematics Jerry Alan Veeh May 1, 2006 Copyright 2006 Jerry Alan Veeh. All rights reserved. 0. Introduction The objective of these notes is to present the basic aspects of the

Lecture Notes on Actuarial Mathematics Jerry Alan Veeh May 1, 2006 Copyright 2006 Jerry Alan Veeh. All rights reserved. 0. Introduction The objective of these notes is to present the basic aspects of the

Maths Workshop for Parents 2. Fractions and Algebra

Maths Workshop for Parents 2 Fractions and Algebra What is a fraction? A fraction is a part of a whole. There are two numbers to every fraction: 2 7 Numerator Denominator 2 7 This is a proper (or common)

Maths Workshop for Parents 2 Fractions and Algebra What is a fraction? A fraction is a part of a whole. There are two numbers to every fraction: 2 7 Numerator Denominator 2 7 This is a proper (or common)

Math 120 Basic finance percent problems from prior courses (amount = % X base)

") Math 120 Basic finance percent problems from prior courses (amount = % X base) 1) Given a sales tax rate of 8%, a) find the tax on an item priced at $250, b) find the total amount due (which includes both

Math 120 Basic finance percent problems from prior courses (amount = % X base) 1) Given a sales tax rate of 8%, a) find the tax on an item priced at $250, b) find the total amount due (which includes both

MAT116 Project 2 Chapters 8 & 9

MAT116 Project 2 Chapters 8 & 9 1 8-1: The Project In Project 1 we made a loan workout decision based only on data from three banks that had merged into one. We did not consider issues like: What was the

MAT116 Project 2 Chapters 8 & 9 1 8-1: The Project In Project 1 we made a loan workout decision based only on data from three banks that had merged into one. We did not consider issues like: What was the

Pre-Session Review. Part 2: Mathematics of Finance

Pre-Session Review Part 2: Mathematics of Finance For this section you will need a calculator with logarithmic and exponential function keys (such as log, ln, and x y ) D. Exponential and Logarithmic Functions

Pre-Session Review Part 2: Mathematics of Finance For this section you will need a calculator with logarithmic and exponential function keys (such as log, ln, and x y ) D. Exponential and Logarithmic Functions

FIN 3000. Chapter 6. Annuities. Liuren Wu

FIN 3000 Chapter 6 Annuities Liuren Wu Overview 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams Learning objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate

FIN 3000 Chapter 6 Annuities Liuren Wu Overview 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams Learning objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate

averages simple arithmetic average (arithmetic mean) 28 29 weighted average (weighted arithmetic mean) 32 33

28 29 weighted average (weighted arithmetic mean) 32 33") 537 A accumulated value 298 future value of a constant-growth annuity future value of a deferred annuity 409 future value of a general annuity due 371 future value of an ordinary general annuity 360 future

537 A accumulated value 298 future value of a constant-growth annuity future value of a deferred annuity 409 future value of a general annuity due 371 future value of an ordinary general annuity 360 future

TIME VALUE OF MONEY (TVM)

") TIME VALUE OF MONEY (TVM) INTEREST Rate of Return When we know the Present Value (amount today), Future Value (amount to which the investment will grow), and Number of Periods, we can calculate the rate

TIME VALUE OF MONEY (TVM) INTEREST Rate of Return When we know the Present Value (amount today), Future Value (amount to which the investment will grow), and Number of Periods, we can calculate the rate

Loans Practice. Math 107 Worksheet #23

Math 107 Worksheet #23 Loans Practice M P r ( 1 + r) n ( 1 + r) n =, M = the monthly payment; P = the original loan amount; r = the monthly interest rate; n = number of payments 1 For each of the following,

Math 107 Worksheet #23 Loans Practice M P r ( 1 + r) n ( 1 + r) n =, M = the monthly payment; P = the original loan amount; r = the monthly interest rate; n = number of payments 1 For each of the following,

Future Value of an Annuity Sinking Fund. MATH 1003 Calculus and Linear Algebra (Lecture 3)

") MATH 1003 Calculus and Linear Algebra (Lecture 3) Future Value of an Annuity Definition An annuity is a sequence of equal periodic payments. We call it an ordinary annuity if the payments are made at the

MATH 1003 Calculus and Linear Algebra (Lecture 3) Future Value of an Annuity Definition An annuity is a sequence of equal periodic payments. We call it an ordinary annuity if the payments are made at the

Math Common Core Sampler Test

High School Algebra Core Curriculum Math Test Math Common Core Sampler Test Our High School Algebra sampler covers the twenty most common questions that we see targeted for this level. For complete tests

High School Algebra Core Curriculum Math Test Math Common Core Sampler Test Our High School Algebra sampler covers the twenty most common questions that we see targeted for this level. For complete tests

Time Value of Money Concepts

BASIC ANNUITIES There are many accounting transactions that require the payment of a specific amount each period. A payment for a auto loan or a mortgage payment are examples of this type of transaction.

BASIC ANNUITIES There are many accounting transactions that require the payment of a specific amount each period. A payment for a auto loan or a mortgage payment are examples of this type of transaction.

2. Annuities. 1. Basic Annuities 1.1 Introduction. Annuity: A series of payments made at equal intervals of time.

2. Annuities 1. Basic Annuities 1.1 Introduction Annuity: A series of payments made at equal intervals of time. Examples: House rents, mortgage payments, installment payments on automobiles, and interest

2. Annuities 1. Basic Annuities 1.1 Introduction Annuity: A series of payments made at equal intervals of time. Examples: House rents, mortgage payments, installment payments on automobiles, and interest

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. The four pieces are the present value (PV), the periodic cash flow (C), the discount rate (r), and

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. The four pieces are the present value (PV), the periodic cash flow (C), the discount rate (r), and

Time Value of Money. 15.511 Corporate Accounting Summer 2004. Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology

Time Value of Money 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 LIABILITIES: Current Liabilities Obligations

Time Value of Money 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 LIABILITIES: Current Liabilities Obligations

GRE Prep: Precalculus

GRE Prep: Precalculus Franklin H.J. Kenter 1 Introduction These are the notes for the Precalculus section for the GRE Prep session held at UCSD in August 2011. These notes are in no way intended to teach

GRE Prep: Precalculus Franklin H.J. Kenter 1 Introduction These are the notes for the Precalculus section for the GRE Prep session held at UCSD in August 2011. These notes are in no way intended to teach

ICASL - Business School Programme

ICASL - Business School Programme Quantitative Techniques for Business (Module 3) Financial Mathematics TUTORIAL 2A This chapter deals with problems related to investing money or capital in a business

ICASL - Business School Programme Quantitative Techniques for Business (Module 3) Financial Mathematics TUTORIAL 2A This chapter deals with problems related to investing money or capital in a business

Six Functions of a Dollar. Made Easy! Business Statistics AJ Nelson 8/27/2011 1

Six Functions of a Dollar Made Easy! Business Statistics AJ Nelson 8/27/2011 1 Six Functions of a Dollar Here's a list. Simple Interest Future Value using Compound Interest Present Value Future Value of

Six Functions of a Dollar Made Easy! Business Statistics AJ Nelson 8/27/2011 1 Six Functions of a Dollar Here's a list. Simple Interest Future Value using Compound Interest Present Value Future Value of

Risk-Free Assets. Case 2. 2.1 Time Value of Money

2 Risk-Free Assets Case 2 Consider a do-it-yourself pension fund based on regular savings invested in a bank account attracting interest at 5% per annum. When you retire after 40 years, you want to receive

2 Risk-Free Assets Case 2 Consider a do-it-yourself pension fund based on regular savings invested in a bank account attracting interest at 5% per annum. When you retire after 40 years, you want to receive

CHAPTER 2. Time Value of Money 2-1

CHAPTER 2 Time Value of Money 2-1 Time Value of Money (TVM) Time Lines Future value & Present value Rates of return Annuities & Perpetuities Uneven cash Flow Streams Amortization 2-2 Time lines 0 1 2 3

CHAPTER 2 Time Value of Money 2-1 Time Value of Money (TVM) Time Lines Future value & Present value Rates of return Annuities & Perpetuities Uneven cash Flow Streams Amortization 2-2 Time lines 0 1 2 3

MATH-0910 Review Concepts (Haugen)

") Unit 1 Whole Numbers and Fractions MATH-0910 Review Concepts (Haugen) Exam 1 Sections 1.5, 1.6, 1.7, 1.8, 2.1, 2.2, 2.3, 2.4, and 2.5 Dividing Whole Numbers Equivalent ways of expressing division: a b,

Unit 1 Whole Numbers and Fractions MATH-0910 Review Concepts (Haugen) Exam 1 Sections 1.5, 1.6, 1.7, 1.8, 2.1, 2.2, 2.3, 2.4, and 2.5 Dividing Whole Numbers Equivalent ways of expressing division: a b,

PRESENT VALUE ANALYSIS. Time value of money equal dollar amounts have different values at different points in time.

PRESENT VALUE ANALYSIS Time value of money equal dollar amounts have different values at different points in time. Present value analysis tool to convert CFs at different points in time to comparable values

PRESENT VALUE ANALYSIS Time value of money equal dollar amounts have different values at different points in time. Present value analysis tool to convert CFs at different points in time to comparable values

Formulas and Approaches Used to Calculate True Pricing

Formulas and Approaches Used to Calculate True Pricing The purpose of the Annual Percentage Rate (APR) and Effective Interest Rate (EIR) The true price of a loan includes not only interest but other charges

Formulas and Approaches Used to Calculate True Pricing The purpose of the Annual Percentage Rate (APR) and Effective Interest Rate (EIR) The true price of a loan includes not only interest but other charges

This is Time Value of Money: Multiple Flows, chapter 7 from the book Finance for Managers (index.html) (v. 0.1).

(v. 0.1).") This is Time Value of Money: Multiple Flows, chapter 7 from the book Finance for Managers (index.html) (v. 0.1). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

This is Time Value of Money: Multiple Flows, chapter 7 from the book Finance for Managers (index.html) (v. 0.1). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

Annuities Certain. 1 Introduction. 2 Annuities-immediate. 3 Annuities-due

Annuities Certain 1 Introduction 2 Annuities-immediate 3 Annuities-due Annuities Certain 1 Introduction 2 Annuities-immediate 3 Annuities-due General terminology An annuity is a series of payments made

Annuities Certain 1 Introduction 2 Annuities-immediate 3 Annuities-due Annuities Certain 1 Introduction 2 Annuities-immediate 3 Annuities-due General terminology An annuity is a series of payments made

1.7. Partial Fractions. 1.7.1. Rational Functions and Partial Fractions. A rational function is a quotient of two polynomials: R(x) = P (x) Q(x).

= P (x) Q(x).") .7. PRTIL FRCTIONS 3.7. Partial Fractions.7.. Rational Functions and Partial Fractions. rational function is a quotient of two polynomials: R(x) = P (x) Q(x). Here we discuss how to integrate rational

.7. PRTIL FRCTIONS 3.7. Partial Fractions.7.. Rational Functions and Partial Fractions. rational function is a quotient of two polynomials: R(x) = P (x) Q(x). Here we discuss how to integrate rational

3. Time value of money. We will review some tools for discounting cash flows.

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

Study Questions for Actuarial Exam 2/FM By: Aaron Hardiek June 2010

P a g e 1 Study Questions for Actuarial Exam 2/FM By: Aaron Hardiek June 2010 P a g e 2 Background The purpose of my senior project is to prepare myself, as well as other students who may read my senior

P a g e 1 Study Questions for Actuarial Exam 2/FM By: Aaron Hardiek June 2010 P a g e 2 Background The purpose of my senior project is to prepare myself, as well as other students who may read my senior

AFM Ch.12 - Practice Test

AFM Ch.2 - Practice Test Multiple Choice Identify the choice that best completes the statement or answers the question.. Form a sequence that has two arithmetic means between 3 and 89. a. 3, 33, 43, 89

AFM Ch.2 - Practice Test Multiple Choice Identify the choice that best completes the statement or answers the question.. Form a sequence that has two arithmetic means between 3 and 89. a. 3, 33, 43, 89

Chapter 6 Contents. Principles Used in Chapter 6 Principle 1: Money Has a Time Value.

Chapter 6 The Time Value of Money: Annuities and Other Topics Chapter 6 Contents Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate present and future values

Chapter 6 The Time Value of Money: Annuities and Other Topics Chapter 6 Contents Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate present and future values

Statistical Models for Forecasting and Planning

Part 5 Statistical Models for Forecasting and Planning Chapter 16 Financial Calculations: Interest, Annuities and NPV chapter 16 Financial Calculations: Interest, Annuities and NPV Outcomes Financial information

Part 5 Statistical Models for Forecasting and Planning Chapter 16 Financial Calculations: Interest, Annuities and NPV chapter 16 Financial Calculations: Interest, Annuities and NPV Outcomes Financial information

Example. L.N. Stout () Problems on annuities 1 / 14

Problems on annuities 1 / 14") Example A credit card charges an annual rate of 14% compounded monthly. This month s bill is $6000. The minimum payment is $5. Suppose I keep paying $5 each month. How long will it take to pay off the

Example A credit card charges an annual rate of 14% compounded monthly. This month s bill is $6000. The minimum payment is $5. Suppose I keep paying $5 each month. How long will it take to pay off the

Integrals of Rational Functions

Integrals of Rational Functions Scott R. Fulton Overview A rational function has the form where p and q are polynomials. For example, r(x) = p(x) q(x) f(x) = x2 3 x 4 + 3, g(t) = t6 + 4t 2 3, 7t 5 + 3t

Integrals of Rational Functions Scott R. Fulton Overview A rational function has the form where p and q are polynomials. For example, r(x) = p(x) q(x) f(x) = x2 3 x 4 + 3, g(t) = t6 + 4t 2 3, 7t 5 + 3t

3 More on Accumulation and Discount Functions

3 More on Accumulation and Discount Functions 3.1 Introduction In previous section, we used 1.03) # of years as the accumulation factor. This section looks at other accumulation factors, including various

3 More on Accumulation and Discount Functions 3.1 Introduction In previous section, we used 1.03) # of years as the accumulation factor. This section looks at other accumulation factors, including various

Solving Exponential Equations

Solving Exponential Equations Deciding How to Solve Exponential Equations When asked to solve an exponential equation such as x + 6 = or x = 18, the first thing we need to do is to decide which way is

Solving Exponential Equations Deciding How to Solve Exponential Equations When asked to solve an exponential equation such as x + 6 = or x = 18, the first thing we need to do is to decide which way is

About Compound Interest

About Compound Interest TABLE OF CONTENTS About Compound Interest... 1 What is COMPOUND INTEREST?... 1 Interest... 1 Simple Interest... 1 Compound Interest... 1 Calculations... 3 Calculating How Much to

About Compound Interest TABLE OF CONTENTS About Compound Interest... 1 What is COMPOUND INTEREST?... 1 Interest... 1 Simple Interest... 1 Compound Interest... 1 Calculations... 3 Calculating How Much to

PowerPoint. to accompany. Chapter 5. Interest Rates

PowerPoint to accompany Chapter 5 Interest Rates 5.1 Interest Rate Quotes and Adjustments To understand interest rates, it s important to think of interest rates as a price the price of using money. When

PowerPoint to accompany Chapter 5 Interest Rates 5.1 Interest Rate Quotes and Adjustments To understand interest rates, it s important to think of interest rates as a price the price of using money. When

14 ARITHMETIC OF FINANCE

4 ARITHMETI OF FINANE Introduction Definitions Present Value of a Future Amount Perpetuity - Growing Perpetuity Annuities ompounding Agreement ontinuous ompounding - Lump Sum - Annuity ompounding Magic?

4 ARITHMETI OF FINANE Introduction Definitions Present Value of a Future Amount Perpetuity - Growing Perpetuity Annuities ompounding Agreement ontinuous ompounding - Lump Sum - Annuity ompounding Magic?

Bank: The bank's deposit pays 8 % per year with annual compounding. Bond: The price of the bond is $75. You will receive $100 five years later.

ü 4.4 lternative Discounted Cash Flow Decision Rules ü Three Decision Rules (1) Net Present Value (2) Future Value (3) Internal Rate of Return, IRR ü (3) Internal Rate of Return, IRR Internal Rate of Return

ü 4.4 lternative Discounted Cash Flow Decision Rules ü Three Decision Rules (1) Net Present Value (2) Future Value (3) Internal Rate of Return, IRR ü (3) Internal Rate of Return, IRR Internal Rate of Return

Chapter 4 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 4 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 4-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

Chapter 4 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 4-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

n k=1 k=0 1/k! = e. Example 6.4. The series 1/k 2 converges in R. Indeed, if s n = n then k=1 1/k, then s 2n s n = 1 n + 1 +...

6 Series We call a normed space (X, ) a Banach space provided that every Cauchy sequence (x n ) in X converges. For example, R with the norm = is an example of Banach space. Now let (x n ) be a sequence

6 Series We call a normed space (X, ) a Banach space provided that every Cauchy sequence (x n ) in X converges. For example, R with the norm = is an example of Banach space. Now let (x n ) be a sequence

Dick Schwanke Finite Math 111 Harford Community College Fall 2013

Annuities and Amortization Finite Mathematics 111 Dick Schwanke Session #3 1 In the Previous Two Sessions Calculating Simple Interest Finding the Amount Owed Computing Discounted Loans Quick Review of

Annuities and Amortization Finite Mathematics 111 Dick Schwanke Session #3 1 In the Previous Two Sessions Calculating Simple Interest Finding the Amount Owed Computing Discounted Loans Quick Review of

4.3 Lagrange Approximation

206 CHAP. 4 INTERPOLATION AND POLYNOMIAL APPROXIMATION Lagrange Polynomial Approximation 4.3 Lagrange Approximation Interpolation means to estimate a missing function value by taking a weighted average

206 CHAP. 4 INTERPOLATION AND POLYNOMIAL APPROXIMATION Lagrange Polynomial Approximation 4.3 Lagrange Approximation Interpolation means to estimate a missing function value by taking a weighted average

Thnkwell s Homeschool Precalculus Course Lesson Plan: 36 weeks

Thnkwell s Homeschool Precalculus Course Lesson Plan: 36 weeks Welcome to Thinkwell s Homeschool Precalculus! We re thrilled that you ve decided to make us part of your homeschool curriculum. This lesson

Thnkwell s Homeschool Precalculus Course Lesson Plan: 36 weeks Welcome to Thinkwell s Homeschool Precalculus! We re thrilled that you ve decided to make us part of your homeschool curriculum. This lesson

Chapter The Time Value of Money

Chapter The Time Value of Money PPT 9-2 Chapter 9 - Outline Time Value of Money Future Value and Present Value Annuities Time-Value-of-Money Formulas Adjusting for Non-Annual Compounding Compound Interest

Chapter The Time Value of Money PPT 9-2 Chapter 9 - Outline Time Value of Money Future Value and Present Value Annuities Time-Value-of-Money Formulas Adjusting for Non-Annual Compounding Compound Interest

Chapter 1. Theory of Interest 1. The measurement of interest 1.1 Introduction

Chapter 1. Theory of Interest 1. The measurement of interest 1.1 Introduction Interest may be defined as the compensation that a borrower of capital pays to lender of capital for its use. Thus, interest

Chapter 1. Theory of Interest 1. The measurement of interest 1.1 Introduction Interest may be defined as the compensation that a borrower of capital pays to lender of capital for its use. Thus, interest

Payment streams and variable interest rates

Chapter 4 Payment streams and variable interest rates In this chapter we consider two extensions of the theory Firstly, we look at payment streams A payment stream is a payment that occurs continuously,

Chapter 4 Payment streams and variable interest rates In this chapter we consider two extensions of the theory Firstly, we look at payment streams A payment stream is a payment that occurs continuously,

Module 1: Corporate Finance and the Role of Venture Capital Financing TABLE OF CONTENTS

1.0 ALTERNATIVE SOURCES OF FINANCE Module 1: Corporate Finance and the Role of Venture Capital Financing Alternative Sources of Finance TABLE OF CONTENTS 1.1 Short-Term Debt (Short-Term Loans, Line of

1.0 ALTERNATIVE SOURCES OF FINANCE Module 1: Corporate Finance and the Role of Venture Capital Financing Alternative Sources of Finance TABLE OF CONTENTS 1.1 Short-Term Debt (Short-Term Loans, Line of

rate nper pmt pv Interest Number of Payment Present Future Rate Periods Amount Value Value 12.00% 1 0 $100.00 $112.00

In Excel language, if the initial cash flow is an inflow (positive), then the future value must be an outflow (negative). Therefore you must add a negative sign before the FV (and PV) function. The inputs

In Excel language, if the initial cash flow is an inflow (positive), then the future value must be an outflow (negative). Therefore you must add a negative sign before the FV (and PV) function. The inputs

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY Answers to Concepts Review and Critical Thinking Questions 1. The four parts are the present value (PV), the future value (FV), the discount

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY Answers to Concepts Review and Critical Thinking Questions 1. The four parts are the present value (PV), the future value (FV), the discount

Partial Fractions. p(x) q(x)

q(x)") Partial Fractions Introduction to Partial Fractions Given a rational function of the form p(x) q(x) where the degree of p(x) is less than the degree of q(x), the method of partial fractions seeks to break

Partial Fractions Introduction to Partial Fractions Given a rational function of the form p(x) q(x) where the degree of p(x) is less than the degree of q(x), the method of partial fractions seeks to break

BUSI 121 Foundations of Real Estate Mathematics

Real Estate Division BUSI 121 Foundations of Real Estate Mathematics SESSION 2 By Graham McIntosh Sauder School of Business University of British Columbia Outline Introduction Cash Flow Problems Cash Flow

Real Estate Division BUSI 121 Foundations of Real Estate Mathematics SESSION 2 By Graham McIntosh Sauder School of Business University of British Columbia Outline Introduction Cash Flow Problems Cash Flow

The Institute of Chartered Accountants of India

CHAPTER 4 SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY APPLICATIONS SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY- APPLICATIONS LEARNING OBJECTIVES After studying this chapter students will be able

CHAPTER 4 SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY APPLICATIONS SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY- APPLICATIONS LEARNING OBJECTIVES After studying this chapter students will be able

Probability Generating Functions

page 39 Chapter 3 Probability Generating Functions 3 Preamble: Generating Functions Generating functions are widely used in mathematics, and play an important role in probability theory Consider a sequence

page 39 Chapter 3 Probability Generating Functions 3 Preamble: Generating Functions Generating functions are widely used in mathematics, and play an important role in probability theory Consider a sequence

Representation of functions as power series

Representation of functions as power series Dr. Philippe B. Laval Kennesaw State University November 9, 008 Abstract This document is a summary of the theory and techniques used to represent functions

Representation of functions as power series Dr. Philippe B. Laval Kennesaw State University November 9, 008 Abstract This document is a summary of the theory and techniques used to represent functions

Key Concepts and Skills. Multiple Cash Flows Future Value Example 6.1. Chapter Outline. Multiple Cash Flows Example 2 Continued

6 Calculators Discounted Cash Flow Valuation Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

6 Calculators Discounted Cash Flow Valuation Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Bond valuation. Present value of a bond = present value of interest payments + present value of maturity value

Bond valuation A reading prepared by Pamela Peterson Drake O U T L I N E 1. Valuation of long-term debt securities 2. Issues 3. Summary 1. Valuation of long-term debt securities Debt securities are obligations

Bond valuation A reading prepared by Pamela Peterson Drake O U T L I N E 1. Valuation of long-term debt securities 2. Issues 3. Summary 1. Valuation of long-term debt securities Debt securities are obligations

CALCULATOR TUTORIAL. Because most students that use Understanding Healthcare Financial Management will be conducting time

CALCULATOR TUTORIAL INTRODUCTION Because most students that use Understanding Healthcare Financial Management will be conducting time value analyses on spreadsheets, most of the text discussion focuses

CALCULATOR TUTORIAL INTRODUCTION Because most students that use Understanding Healthcare Financial Management will be conducting time value analyses on spreadsheets, most of the text discussion focuses