Investment risk - questioning your way to more effective risk management

|

|

|

- Rebecca Morrison

- 8 years ago

- Views:

Transcription

1 Investment risk - questioning your way to more effective risk management Ravi Rastogi, Towers Watson Neil Chapman, Towers Watson September 2013, Brussels 2013 Towers Watson. All rights reserved.

2 The new normal greater complexity and interconnectivity Insurance crisis Banking crisis Major sovereign default War Climate change Fracking GM food Cyber terrorism Nanotechnology Energy Water shortage Food shortage Rare earths Endogenous risk Macro factors Killer pandemic Sustainability Insurance crisis Complexity New beliefs Technology Environment Self-inflicted disease Finance Capital Markets Society Minor sovereign default Debt Demographics Ageing Underfunded pensions Healthcare Currency crisis Economics Imbalances Hyperinflation Inflation Protectionism End of fiat money Politics Short-termism Fairness Two-tier economy Depression Emerging wealth Double dip Two-speed world Political crisis Future of Euro End of capitalism Social unrest Default War Multipolar world

3 The same old problem all models are flawed Unknown model limitations Reality Known model limitations Accurately modelled risks

4 Our agenda for today market risk questions risk managers should be asking in the new normal 1 Can we make more efficient investment decisions? Questions 2 Can we better quantify risk? 3 Are there new and emerging asset risks?

5 Good investment decisions should be based on a coherent and consistent framework Strategic Principles Know Why IM Excellence (Portfolio Construction) Enablers Know What, Where, Know How When Execution Know What, Who Mission and goals Values and beliefs Governance and resources Asset allocation and risk Culture Value chain Manager capability Often static and not a focus area Client delivery Actions and decisions Measurement and Often the review main focus areas Proprietary and Confidential. For Towers Watson and Towers Watson client use only. 5

6 Common issues and outcomes that separate the good from the great Dysfunctional organisation 1 Ignoring assets because they are HARD-to-model Sub-optimal processes Roles and responsibilities unclear Slow decision making The impact of suboptimal investment beliefs and processes 2 3 Chase (eg) LIQUIDITY to the detriment of (eg) YIELD Capturing emerging trends after they have emerged

LIQUIDITY to the detriment of (eg) YIELD Capturing emerging trends after they have")

7 Encouraging good investment behaviours Allocation of capital and diversification Rewarding diversification Good investment behaviours Understanding of limitations Expert holistic risk assessment Link to remuneration

8 Better risk quantification 2013 Towers Watson. All rights reserved.

9 Fit for purpose models and calibrations are required Spectrum of model sophistication Standard Formula 80/20 point Average point Leading pack Best-in-class Best-of-breed Bank prop desk Theoretical zone of acceptability for internal models A consistent and coherent calibration framework is needed combined with appropriate expertise Risk type Data Analysis Expert Judgement Benchmarking Market/credit risk Insurance/ operational Investment professionals are the experts of choice for investment (market and credit) risk Actuaries are the experts of choice for insurance and operational risk

risk Actuaries are the experts of choice for insurance and")

10 When calibrating beware of regime changes Per cent Euro Spreads over 10yr German Bunds Ireland Italy Portugal Spain Debt to GDP ratio for different US borrower types (%) Household Sector Financial Sector Non-Financial Business Sector Government Sector 6 4 Finland France Greece (rhs) Source: Bloomberg Source: DataStream 1 2 3

11 and future trends Historic sovereign default and restructuring rates Prospective sovereign credit rating distribution % default/restructuring # of countries (rhs) Hard currency Local currency Hundreds % of DM sovereign countries 100% 90% 80% 70% 60% BBB Speculative grade Source: Reinhardt/Rogoff, Towers Watson % 40% 30% A 20% 10% AAA AA 0% Source: Standard and Poors

12 Case Study: modelling complex asset classes Challenges Carrying out an independent review of an EC model Capturing different hedge fund styles in the model Challenging client assumptions around the use of equities to represent hedge funds in their model Approach Key risk analysis extensive modelling of equity and hedge funds relationships in different market conditions Use of left tail multipliers based on 2008 experience Separation of market sensitivity(beta) and manager skill(alpha) to enhance use of benchmarks in the model Application of subjective judgement to further improve market distribution vs blind benchmark approach Beneficial outcomes The client had a higher level of confidence that risks were appropriately captured and modelled in economic capital We shared the findings of the review with the regulator, who accepted the conclusions confirming the adequacy of the firm s capital requirements Breakdown of sensitivity of hedge fund returns to global equities Alpha (manager skill) Beta (HF index)

13 New and emerging asset risks 2013 Towers Watson. All rights reserved.

14 Asset managers are always looking for better opportunities ECA loans Infrastructure debt Insurance linked securities Direct Lending Social Housing Loans Equity release mortgages Hedge Funds Structured credit which results in new assets and risks that risk managers need to understand and quantify

15 Case Study: Investing in new asset classes Challenges for the risk manager Understand, managing and monitor new classes Upgrading economic capital models for new classes Limited data and role of expert judgement Excess return Excess return vs risk/capital 3.0% 2.5% 2.0% 1.5% 1.0% Current Portfolio A 0.5% Portfolio B Portfolio C 0.0% 12.4% 12.6% 12.8% 13.0% 13.2% 13.4% 13.6% VaR 99.5 inc LP, % of best estimate liabilities (adjusted for LP) Beneficial outcomes Return enhancements of 50+ bps Reduced economic capital Suitable illiquid / alternative credit assets identified Assets to be transitioned over time as opportunities emerge Empirical Fitted Fitted CDF KS test central KS test upper and lower bounds 15

16 Investing in more illiquid assets will require more robust liquidity management Liquidity risk limits and tolerances e.g. coverage ratio and extent of loss Governance, processes and controls Aligning investment strategy, liquidity facilities and management actions with limits and tolerances Monitoring, MI and scenario testing Understanding cash outflows, encumbrances, price sensitivities and asset sale criteria / order

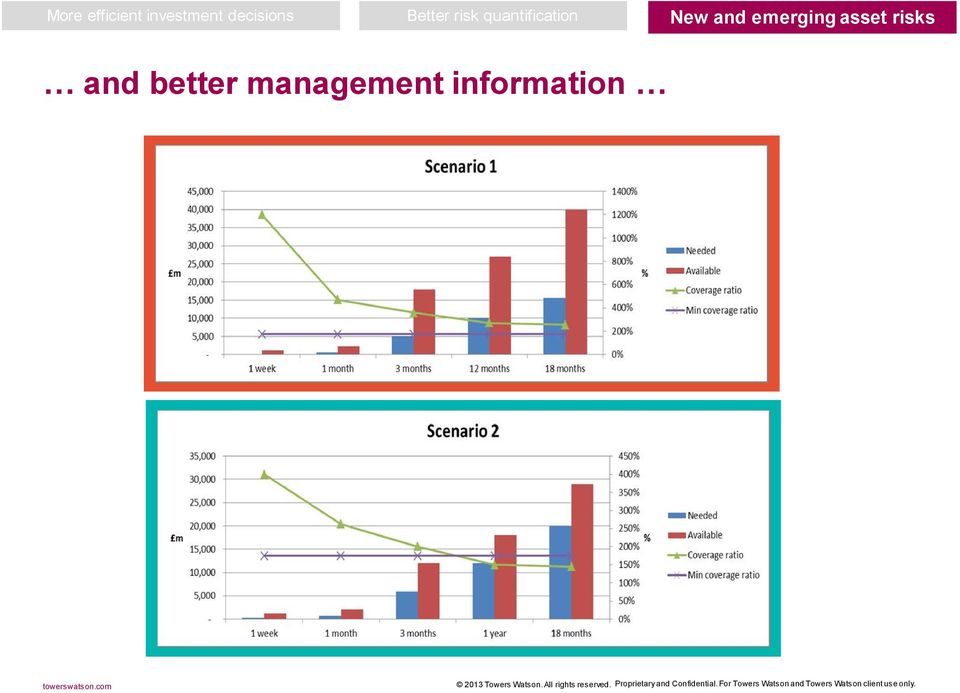

17 and better management information

18 and an understanding of emerging liquidity risks European Markets Infrastructure Regulation (EMIR) EXPECTED CHANGES FOR OTC DERIVATIVES CASH REQUIRED FOR VARIATION MARGIN for derivatives traded by central counterparties BILLATERAL COLLATERALISATION REQUIRED for derivatives not centrally cleared IMPACT Derivatives with a long duration may further INCREASE LIQUIDITY REQUIREMENTS or require arrangements to access liquidity at short notice GREATEST IMPACT ON: Annuity writers that make use of interest rate swaps With-profits funds that use OTC derivatives to hedge guarantees and options

19 Conclusion: the new normal will present risk managers with new market risk challenges and questions they need to ask IMPROVING Investment decision taking BETTER USE OF EXPERT JUDGEMENT Improve risk quantification UNDERSTAND New/emerging asset risks e.g. liquidity C H A L L E N G E S

20 Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

up to 1 year 2,391 3.27 1 to 5 years 3,441 4.70 6 to 10 years 3,554 4.86 11 to 20 years 1,531 2.09 over 20 years 62,226 85.08 TOTAL 73,143 100.

SECTION 2 RISKS OF INSURANCE COMPANIES 2.1 INSURANCE RISKS QUALITATIVE AND QUANTITATIVE INFORMATION Life business The typical risks of the life insurance portfolio (managed by Intesa Sanpaolo Vita, Intesa

SECTION 2 RISKS OF INSURANCE COMPANIES 2.1 INSURANCE RISKS QUALITATIVE AND QUANTITATIVE INFORMATION Life business The typical risks of the life insurance portfolio (managed by Intesa Sanpaolo Vita, Intesa

Investment Risk Management Under New Regulatory Framework. Steven Yang Yu Muqiu Liu Redington Ltd

Investment Risk Management Under New Regulatory Framework Steven Yang Yu Muqiu Liu Redington Ltd 06 May 2015 Premiums written in billion RMB Dramatic growth of insurance market 2,500 Direct premium written

Investment Risk Management Under New Regulatory Framework Steven Yang Yu Muqiu Liu Redington Ltd 06 May 2015 Premiums written in billion RMB Dramatic growth of insurance market 2,500 Direct premium written

Diversified Growth Funds & implications for actuarial assumptions

Diversified Growth Funds & implications for actuarial assumptions Part 1: Actuarial return and discount rate assumptions Subtitle: But Mother, look! The Emperor isn t wearing any clothes! Is it reasonable

Diversified Growth Funds & implications for actuarial assumptions Part 1: Actuarial return and discount rate assumptions Subtitle: But Mother, look! The Emperor isn t wearing any clothes! Is it reasonable

Notes to the consolidated financial statements Part E Information on risks and relative hedging policies

SECTION 2 RISKS OF INSURANCE COMPANIES 2.1 INSURANCE RISKS Life branch The typical risks of the life insurance portfolio (managed by EurizonVita, EurizonLife, SudPoloVita and CentroVita) may be divided

SECTION 2 RISKS OF INSURANCE COMPANIES 2.1 INSURANCE RISKS Life branch The typical risks of the life insurance portfolio (managed by EurizonVita, EurizonLife, SudPoloVita and CentroVita) may be divided

CPBI Saskatchewan Regional Council Alternative Investments - Worth the Effort?

CPBI Saskatchewan Regional Council Alternative Investments - Worth the Effort? PREPARED BY: Brendan George, Partner, George & Bell Consulting Inc. November 18 and 19, 2015 Agenda Current Economic Environment

CPBI Saskatchewan Regional Council Alternative Investments - Worth the Effort? PREPARED BY: Brendan George, Partner, George & Bell Consulting Inc. November 18 and 19, 2015 Agenda Current Economic Environment

THE LOW INTEREST RATE ENVIRONMENT AND ITS IMPACT ON INSURANCE MARKETS. Mamiko Yokoi-Arai

THE LOW INTEREST RATE ENVIRONMENT AND ITS IMPACT ON INSURANCE MARKETS Mamiko Yokoi-Arai Current macro economic environment is of Low interest rate Low inflation and nominal wage growth Slow growth Demographic

THE LOW INTEREST RATE ENVIRONMENT AND ITS IMPACT ON INSURANCE MARKETS Mamiko Yokoi-Arai Current macro economic environment is of Low interest rate Low inflation and nominal wage growth Slow growth Demographic

The Credit Analysis Process: From In-Depth Company Research to Selecting the Right Instrument

Featured Solution May 2015 Your Global Investment Authority The Credit Analysis Process: From In-Depth Company Research to Selecting the Right Instrument In today s low yield environment, an active investment

Featured Solution May 2015 Your Global Investment Authority The Credit Analysis Process: From In-Depth Company Research to Selecting the Right Instrument In today s low yield environment, an active investment

Uncertainty and Financial Regulation. Myron S. Scholes Frank E. Buck Professor of Finance, Emeritus, Stanford University 30 August, 2011

Uncertainty and Financial Regulation Myron S. Scholes Frank E. Buck Professor of Finance, Emeritus, Stanford University 30 August, 2011 1 Six Functions of a Financial System Goal is to enhance communication

Uncertainty and Financial Regulation Myron S. Scholes Frank E. Buck Professor of Finance, Emeritus, Stanford University 30 August, 2011 1 Six Functions of a Financial System Goal is to enhance communication

Liquidity and the Development of Robust Corporate Bond Markets

Liquidity and the Development of Robust Corporate Bond Markets Marti G. Subrahmanyam Stern School of Business New York University For presentation at the CAMRI Executive Roundtable Luncheon Talk National

Liquidity and the Development of Robust Corporate Bond Markets Marti G. Subrahmanyam Stern School of Business New York University For presentation at the CAMRI Executive Roundtable Luncheon Talk National

ALM in UK Life. DRAFT 12 January 2011 V1

ALM in UK Life WP & Annuity strategy t John Lister DRAFT 12 January 2011 V1 1 ALM in UK Life Summary Asset and Liability management is at the core of what we do This combined with the quality of our credit

ALM in UK Life WP & Annuity strategy t John Lister DRAFT 12 January 2011 V1 1 ALM in UK Life Summary Asset and Liability management is at the core of what we do This combined with the quality of our credit

Agenda. Introduction Re pricing Gap Analysis and Earnings Risk Modeling Implementation Sample Reports Governance and Market Risk Exposure

Interest Rate Earnings Risk Analysis for Insurers Repricing Gap Approach Mark Scanlon, Ikwhan Oh, Joonghee Huh Agenda Introduction Re pricing Gap Analysis and Earnings Risk Modeling Implementation Sample

Interest Rate Earnings Risk Analysis for Insurers Repricing Gap Approach Mark Scanlon, Ikwhan Oh, Joonghee Huh Agenda Introduction Re pricing Gap Analysis and Earnings Risk Modeling Implementation Sample

Investment Strategies for Pension Funds. Christopher Nichols Investment Director, Multi Asset Investing Standard Life Investments (UK)

") Investment Strategies for Pension Funds Christopher Nichols Investment Director, Multi Asset Investing Standard Life Investments (UK) Pensions need consistency but markets deliver chaos Discrete Yearly

Investment Strategies for Pension Funds Christopher Nichols Investment Director, Multi Asset Investing Standard Life Investments (UK) Pensions need consistency but markets deliver chaos Discrete Yearly

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc.

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc. Introduction Basel II is an international framework on capital that applies to deposit taking institutions in many countries, including Canada.

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc. Introduction Basel II is an international framework on capital that applies to deposit taking institutions in many countries, including Canada.

Actuarial Risk Management

ARA syllabus Actuarial Risk Management Aim: To provide the technical skills to apply the principles and methodologies studied under actuarial technical subjects for the identification, quantification and

ARA syllabus Actuarial Risk Management Aim: To provide the technical skills to apply the principles and methodologies studied under actuarial technical subjects for the identification, quantification and

ERM-2: Introduction to Economic Capital Modeling

ERM-2: Introduction to Economic Capital Modeling 2011 Casualty Loss Reserve Seminar, Las Vegas, NV A presentation by François Morin September 15, 2011 2011 Towers Watson. All rights reserved. INTRODUCTION

ERM-2: Introduction to Economic Capital Modeling 2011 Casualty Loss Reserve Seminar, Las Vegas, NV A presentation by François Morin September 15, 2011 2011 Towers Watson. All rights reserved. INTRODUCTION

Alternative Investments Insurance Company Strategies

Alternative Investments Insurance Company Strategies Gareth Mee and Richard McIntyre 10 th November 2014 Agenda Introduction insurance company considerations Themes and case studies Annuity funds General

Alternative Investments Insurance Company Strategies Gareth Mee and Richard McIntyre 10 th November 2014 Agenda Introduction insurance company considerations Themes and case studies Annuity funds General

Rating Methodology for Domestic Life Insurance Companies

Rating Methodology for Domestic Life Insurance Companies Introduction ICRA Lanka s Claim Paying Ability Ratings (CPRs) are opinions on the ability of life insurance companies to pay claims and policyholder

Rating Methodology for Domestic Life Insurance Companies Introduction ICRA Lanka s Claim Paying Ability Ratings (CPRs) are opinions on the ability of life insurance companies to pay claims and policyholder

What alternative investments are of interest to life companies?

Life Conference 2011 Scott Robertson and Niall Clifford, KPMG LLP What alternative investments are of interest to life companies? 21 November 2011 Contents 1. What alternative assets have low correlation

Life Conference 2011 Scott Robertson and Niall Clifford, KPMG LLP What alternative investments are of interest to life companies? 21 November 2011 Contents 1. What alternative assets have low correlation

EIOPA Stress Test 2011. Press Briefing Frankfurt am Main, 4 July 2011

EIOPA Stress Test 2011 Press Briefing Frankfurt am Main, 4 July 2011 Topics 1. Objectives 2. Initial remarks 3. Framework 4. Participation 5. Results 6. Summary 7. Follow up 2 Objectives Overall objective

EIOPA Stress Test 2011 Press Briefing Frankfurt am Main, 4 July 2011 Topics 1. Objectives 2. Initial remarks 3. Framework 4. Participation 5. Results 6. Summary 7. Follow up 2 Objectives Overall objective

Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries

and Bond Yield Spreads in Selected EU 1 Countries") LIST OF CHARTS Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries Chart I.2. Gross Debt Stock and Budget Deficits of Selected Countries as of 2010 1 Chart

LIST OF CHARTS Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries Chart I.2. Gross Debt Stock and Budget Deficits of Selected Countries as of 2010 1 Chart

2013 GSAM Insurance Survey & Industry Investment Trends

Global Insurance Asset Management AASCIF Annual Workshop Fall 23 23 GSAM Insurance Survey & Industry Investment Trends Michael Siegel, PhD Global Head of GSAM Insurance Asset Management September 3, 23

Global Insurance Asset Management AASCIF Annual Workshop Fall 23 23 GSAM Insurance Survey & Industry Investment Trends Michael Siegel, PhD Global Head of GSAM Insurance Asset Management September 3, 23

ERM from a Small Insurance Company Perspective

ERM from a Small Insurance Company Perspective NABRICO Sept 30, 2011 Agenda Section 1 Section 2 Section 3 Section 4 ERM Introduction Key Risks Streamlined Quantitative Process Other Influences 1 1 Section

ERM from a Small Insurance Company Perspective NABRICO Sept 30, 2011 Agenda Section 1 Section 2 Section 3 Section 4 ERM Introduction Key Risks Streamlined Quantitative Process Other Influences 1 1 Section

SEMINAR ON CREDIT RISK MANAGEMENT AND SME BUSINESS RENATO MAINO. Turin, June 12, 2003. Agenda

SEMINAR ON CREDIT RISK MANAGEMENT AND SME BUSINESS RENATO MAINO Head of Risk assessment and management Turin, June 12, 2003 2 Agenda Italian market: the peculiarity of Italian SMEs in rating models estimation

SEMINAR ON CREDIT RISK MANAGEMENT AND SME BUSINESS RENATO MAINO Head of Risk assessment and management Turin, June 12, 2003 2 Agenda Italian market: the peculiarity of Italian SMEs in rating models estimation

HOUSING FINANCE IN TRANSITION ECONOMIES

HOUSING FINANCE IN TRANSITION ECONOMIES OECD Workshop Warsaw, Poland December 5-6, 5 2002 Loïc Chiquier The World Bank 1 Challenge in Transition Economies! Key for growth, poverty, wealth (75 wealth),

HOUSING FINANCE IN TRANSITION ECONOMIES OECD Workshop Warsaw, Poland December 5-6, 5 2002 Loïc Chiquier The World Bank 1 Challenge in Transition Economies! Key for growth, poverty, wealth (75 wealth),

QUARTERLY FINANCIAL STATEMENTS AS AT 30 SEPTEMBER 2011

QUARTERLY FINANCIAL STATEMENTS AS AT 30 SEPTEMBER Media telephone conference 8 November Agenda Overview Financial highlights Jörg Schneider 2 Munich Re (Group) Jörg Schneider 4 Torsten Oletzky 13 Torsten

QUARTERLY FINANCIAL STATEMENTS AS AT 30 SEPTEMBER Media telephone conference 8 November Agenda Overview Financial highlights Jörg Schneider 2 Munich Re (Group) Jörg Schneider 4 Torsten Oletzky 13 Torsten

Multi Asset Credit. Reviewing your credit exposure is it time to consider a multi-asset approach?

It seems that whoever you talk to in the pensions industry about their current hot topic, the answer is Multi-Asset Credit (MAC). But what does this term really mean? The answer, it appears, depends who

It seems that whoever you talk to in the pensions industry about their current hot topic, the answer is Multi-Asset Credit (MAC). But what does this term really mean? The answer, it appears, depends who

Bonds - Strategic S fixed Income Portfolio Management

OPTIMIZING YOUR BOND PORTFOLIO THROUGH RISK FACTOR MODELING FIXED INCOME INVESTMENTS SPAN A BROAD RANGE OF SENSITIVITIES TO CHANGES IN YIELDS AND CREDIT SPREADS. Understanding how different types of fixed

OPTIMIZING YOUR BOND PORTFOLIO THROUGH RISK FACTOR MODELING FIXED INCOME INVESTMENTS SPAN A BROAD RANGE OF SENSITIVITIES TO CHANGES IN YIELDS AND CREDIT SPREADS. Understanding how different types of fixed

Risk Practitioner Conference

Risk Practitioner Conference Introducing RiskFrontier for Portfolio Management DOY CHARNSUPHARINDR, Director VANESSA WU, Managing Director October 2011 Agenda 1. What is RiskFrontier? 2. How is RiskFrontier

Risk Practitioner Conference Introducing RiskFrontier for Portfolio Management DOY CHARNSUPHARINDR, Director VANESSA WU, Managing Director October 2011 Agenda 1. What is RiskFrontier? 2. How is RiskFrontier

Understanding Fixed Income

Understanding Fixed Income 2014 AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 Understanding Fixed Income About fixed income at AMP Capital Our global presence helps us deliver outstanding

Understanding Fixed Income 2014 AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 Understanding Fixed Income About fixed income at AMP Capital Our global presence helps us deliver outstanding

Investment Strategy for Pensions Actuaries A Multi Asset Class Approach

Investment Strategy for Pensions Actuaries A Multi Asset Class Approach 16 January 2007 Representing Schroders: Neil Walton Head of Strategic Solutions Tel: 020 7658 2486 Email: Neil.Walton@Schroders.com

Investment Strategy for Pensions Actuaries A Multi Asset Class Approach 16 January 2007 Representing Schroders: Neil Walton Head of Strategic Solutions Tel: 020 7658 2486 Email: Neil.Walton@Schroders.com

Effective Techniques for Stress Testing and Scenario Analysis

Effective Techniques for Stress Testing and Scenario Analysis Om P. Arya Federal Reserve Bank of New York November 4 th, 2008 Mumbai, India The views expressed here are not necessarily of the Federal Reserve

Effective Techniques for Stress Testing and Scenario Analysis Om P. Arya Federal Reserve Bank of New York November 4 th, 2008 Mumbai, India The views expressed here are not necessarily of the Federal Reserve

Financial Statements

PROVINCIAL JUDGES AND MASTERS IN CHAMBERS RESERVE FUND Financial Statements Year Ended March 31, 2015 Independent Auditor s Report.... 204 Statement of Financial Position..................... 205 Statement

PROVINCIAL JUDGES AND MASTERS IN CHAMBERS RESERVE FUND Financial Statements Year Ended March 31, 2015 Independent Auditor s Report.... 204 Statement of Financial Position..................... 205 Statement

List of legislative acts

List of legislative acts BRRd : d irective 2014/59/EU of the European Parliament and of the Council of 15 May 2014 establishing a framework for the recovery and resolution of credit institutions and investment

List of legislative acts BRRd : d irective 2014/59/EU of the European Parliament and of the Council of 15 May 2014 establishing a framework for the recovery and resolution of credit institutions and investment

Fiscal Consolidation During a Depression

NIESR Fiscal Consolidation During a Depression Nitika Bagaria*, Dawn Holland** and John van Reenen* *London School of Economics **National Institute of Economic and Social Research October 2012 Project

NIESR Fiscal Consolidation During a Depression Nitika Bagaria*, Dawn Holland** and John van Reenen* *London School of Economics **National Institute of Economic and Social Research October 2012 Project

Financial Statements

LONG TERM DISABILITY INCOME CONTINUANCE PLAN - BARGAINING UNIT Financial Statements Year Ended March 31, 2015 Independent Auditor s Report.... 542 Statement of Financial Position.... 543 Statement of Changes

LONG TERM DISABILITY INCOME CONTINUANCE PLAN - BARGAINING UNIT Financial Statements Year Ended March 31, 2015 Independent Auditor s Report.... 542 Statement of Financial Position.... 543 Statement of Changes

The EU Stress Test and Sovereign Debt Exposures

Please cite this paper as: Blundell-Wignall, A. and P. Slovik (2010), The EU Stress Test and Sovereign Debt Exposures, OECD Working Papers on Finance, Insurance and Private Pensions, No. 4, OECD Financial

Please cite this paper as: Blundell-Wignall, A. and P. Slovik (2010), The EU Stress Test and Sovereign Debt Exposures, OECD Working Papers on Finance, Insurance and Private Pensions, No. 4, OECD Financial

Analyzing Risk in an Investment Portfolio

Introduction Analyzing Risk in an Investment Portfolio October 16, 2012 PUBLIC TRUST ADVISORS Neil Waud, CFA Director Portfolio Management neil.waud@publictrustadvisors.com (303) 244-0468 Matthew Tight

Introduction Analyzing Risk in an Investment Portfolio October 16, 2012 PUBLIC TRUST ADVISORS Neil Waud, CFA Director Portfolio Management neil.waud@publictrustadvisors.com (303) 244-0468 Matthew Tight

FIXED INCOME INVESTORS HAVE OPTIONS TO INCREASE RETURNS, LOWER RISK

1 FIXED INCOME INVESTORS HAVE OPTIONS TO INCREASE RETURNS, LOWER RISK By Michael McMurray, CFA Senior Consultant As all investors are aware, fixed income yields and overall returns generally have been

1 FIXED INCOME INVESTORS HAVE OPTIONS TO INCREASE RETURNS, LOWER RISK By Michael McMurray, CFA Senior Consultant As all investors are aware, fixed income yields and overall returns generally have been

ROYAL LONDON ABSOLUTE RETURN GOVERNMENT BOND FUND

ROYAL LONDON ABSOLUTE RETURN GOVERNMENT BOND FUND For professional investors only A NEW OPPORTUNITY Absolute return funds offer an attractive, alternative source of alpha outright or as part of a balanced

ROYAL LONDON ABSOLUTE RETURN GOVERNMENT BOND FUND For professional investors only A NEW OPPORTUNITY Absolute return funds offer an attractive, alternative source of alpha outright or as part of a balanced

Bank of America Merrill Lynch Banking & Insurance CEO Conference Bob Diamond

4 October 2011 Bank of America Merrill Lynch Banking & Insurance CEO Conference Bob Diamond Thank you and good morning. It s a pleasure to be here and I d like to thank our hosts for the opportunity to

4 October 2011 Bank of America Merrill Lynch Banking & Insurance CEO Conference Bob Diamond Thank you and good morning. It s a pleasure to be here and I d like to thank our hosts for the opportunity to

RISK FACTORS AND RISK MANAGEMENT

Bangkok Bank Public Company Limited 044 RISK FACTORS AND RISK MANAGEMENT Bangkok Bank recognizes that effective risk management is fundamental to good banking practice. Accordingly, the Bank has established

Bangkok Bank Public Company Limited 044 RISK FACTORS AND RISK MANAGEMENT Bangkok Bank recognizes that effective risk management is fundamental to good banking practice. Accordingly, the Bank has established

Course Syllabus For Banking and Financial Management Department

For Banking and Financial Management Department School Year First Year First year Second year Third year Fifth year Fifth year Fifth year Fifth year Name of course Financial Accounting principles Intermediate

For Banking and Financial Management Department School Year First Year First year Second year Third year Fifth year Fifth year Fifth year Fifth year Name of course Financial Accounting principles Intermediate

Fixed Income Investor Presentation. July 2012

Fixed Income Investor Presentation July 2012 Cautionary Note on Forward Looking Statements Today s presentation may include forward-looking statements. These statements represent the Firm s belief regarding

Fixed Income Investor Presentation July 2012 Cautionary Note on Forward Looking Statements Today s presentation may include forward-looking statements. These statements represent the Firm s belief regarding

BELIEF INTERPRETATION IMPLICATIONS FOR DECISION MAKING

SKILLS AND COMPETENCIES Investment Belief 1 The Investment Committee should have access to appropriate skills sets. Voting members of the Committee, the Executive Team and investment advisers, and representatives

SKILLS AND COMPETENCIES Investment Belief 1 The Investment Committee should have access to appropriate skills sets. Voting members of the Committee, the Executive Team and investment advisers, and representatives

Risk Management. Did you know? What is Risk Management?

Risk Did you know? Financial services organizations help people buy houses, build businesses and protect their families financially. Banks, insurance companies, asset managers, pension administrators and

Risk Did you know? Financial services organizations help people buy houses, build businesses and protect their families financially. Banks, insurance companies, asset managers, pension administrators and

Case study: Making the move into investment grade corporates

National Asset-Liability Management Europe Case study: Making the move into investment grade corporates Tomas Garbaravičius 3 March 2016 London Outline The reasoning behind the decision to corporate bonds

National Asset-Liability Management Europe Case study: Making the move into investment grade corporates Tomas Garbaravičius 3 March 2016 London Outline The reasoning behind the decision to corporate bonds

Capital preservation strategy update

Client Education Summit 2012 Capital preservation strategy update Head of Institutional Fixed Income Investments, Americas October 9, 2012 Topics for discussion 1 Capital preservation strategies 2 3 4

Client Education Summit 2012 Capital preservation strategy update Head of Institutional Fixed Income Investments, Americas October 9, 2012 Topics for discussion 1 Capital preservation strategies 2 3 4

seic.com/institutions

Nonprofit Management Research Panel Liquidity Pool Management for U.S. Colleges and Universities Gain a better understanding of your school s financial risks and the benefits of integrating the investment

Nonprofit Management Research Panel Liquidity Pool Management for U.S. Colleges and Universities Gain a better understanding of your school s financial risks and the benefits of integrating the investment

THE INSURANCE BUSINESS (SOLVENCY) RULES 2015

RULES 2015") THE INSURANCE BUSINESS (SOLVENCY) RULES 2015 Table of Contents Part 1 Introduction... 2 Part 2 Capital Adequacy... 4 Part 3 MCR... 7 Part 4 PCR... 10 Part 5 - Internal Model... 23 Part 6 Valuation... 34

THE INSURANCE BUSINESS (SOLVENCY) RULES 2015 Table of Contents Part 1 Introduction... 2 Part 2 Capital Adequacy... 4 Part 3 MCR... 7 Part 4 PCR... 10 Part 5 - Internal Model... 23 Part 6 Valuation... 34

Danish mortgage bonds provide attractive yields and low risk

JANUARY 2015 Danish mortgage bonds provide attractive yields and low risk New European Union legislation favours Danish mortgage bonds KEY CONCEPTS New legislation favours Danish mortgage bonds Attractive

JANUARY 2015 Danish mortgage bonds provide attractive yields and low risk New European Union legislation favours Danish mortgage bonds KEY CONCEPTS New legislation favours Danish mortgage bonds Attractive

Solutions for Balance Sheet Management

ENTERPRISE RISK SOLUTIONS Solutions for Balance Sheet Management Moody s Analytics offers a powerful combination of software and advisory services for essential balance sheet and liquidity risk management.

ENTERPRISE RISK SOLUTIONS Solutions for Balance Sheet Management Moody s Analytics offers a powerful combination of software and advisory services for essential balance sheet and liquidity risk management.

Featured article: Evaluating the Cost of Longevity in Variable Annuity Living Benefits

Featured article: Evaluating the Cost of Longevity in Variable Annuity Living Benefits By Stuart Silverman and Dan Theodore This is a follow-up to a previous article Considering the Cost of Longevity Volatility

Featured article: Evaluating the Cost of Longevity in Variable Annuity Living Benefits By Stuart Silverman and Dan Theodore This is a follow-up to a previous article Considering the Cost of Longevity Volatility

Autumn Investor Seminar. Workshops. Managing Variable Annuity Risk

Autumn Investor Seminar Workshops Managing Variable Annuity Risk Jean-Christophe Menioux Kevin Byrne Denis Duverne Group CRO CIO AXA Equitable Chief Financial Officer Paris November 25, 2008 Cautionary

Autumn Investor Seminar Workshops Managing Variable Annuity Risk Jean-Christophe Menioux Kevin Byrne Denis Duverne Group CRO CIO AXA Equitable Chief Financial Officer Paris November 25, 2008 Cautionary

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Standard No. 13 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS STANDARD ON ASSET-LIABILITY MANAGEMENT OCTOBER 2006 This document was prepared by the Solvency and Actuarial Issues Subcommittee in consultation

Standard No. 13 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS STANDARD ON ASSET-LIABILITY MANAGEMENT OCTOBER 2006 This document was prepared by the Solvency and Actuarial Issues Subcommittee in consultation

The package of measures to avoid artificial volatility and pro-cyclicality

The package of measures to avoid artificial volatility and pro-cyclicality Explanation of the measures and the need to include them in the Solvency II framework Contents 1. Key messages 2. Why the package

The package of measures to avoid artificial volatility and pro-cyclicality Explanation of the measures and the need to include them in the Solvency II framework Contents 1. Key messages 2. Why the package

The Ratio of Leverage. When you combine ignorance and leverage, you get some pretty interesting results. Warren Buffett

The Ratio of Leverage When you combine ignorance and leverage, you get some pretty interesting results. Warren Buffett 1 What is leverage? definition of leverage: debt to equity ratio Basel Commitee: One

The Ratio of Leverage When you combine ignorance and leverage, you get some pretty interesting results. Warren Buffett 1 What is leverage? definition of leverage: debt to equity ratio Basel Commitee: One

(Part.1) FOUNDATIONS OF RISK MANAGEMENT

FOUNDATIONS OF RISK MANAGEMENT") (Part.1) FOUNDATIONS OF RISK MANAGEMENT 1 : Risk Taking: A Corporate Governance Perspective Delineating Efficient Portfolios 2: The Standard Capital Asset Pricing Model 1 : Risk : A Helicopter View 2:

(Part.1) FOUNDATIONS OF RISK MANAGEMENT 1 : Risk Taking: A Corporate Governance Perspective Delineating Efficient Portfolios 2: The Standard Capital Asset Pricing Model 1 : Risk : A Helicopter View 2:

DCF and WACC calculation: Theory meets practice

www.pwc.com DCF and WACC calculation: Theory meets practice Table of contents Section 1. Fair value and company valuation page 3 Section 2. The DCF model: Basic assumptions and the expected cash flows

www.pwc.com DCF and WACC calculation: Theory meets practice Table of contents Section 1. Fair value and company valuation page 3 Section 2. The DCF model: Basic assumptions and the expected cash flows

ING Insurance Economic Capital Framework

ING Insurance Economic Capital Framework Thomas C. Wilson Chief Insurance Risk Officer Kent University, September 5, 2007 www.ing.com Objectives of this session ING has been using economic capital internally

ING Insurance Economic Capital Framework Thomas C. Wilson Chief Insurance Risk Officer Kent University, September 5, 2007 www.ing.com Objectives of this session ING has been using economic capital internally

Objectives and key requirements of this Prudential Standard

Prudential Standard LPS 001 Definitions Objectives and key requirements of this Prudential Standard This Prudential Standard defines key terms referred to in other Prudential Standards applicable to life

Prudential Standard LPS 001 Definitions Objectives and key requirements of this Prudential Standard This Prudential Standard defines key terms referred to in other Prudential Standards applicable to life

Investment insight. Fixed income the what, when, where, why and how TABLE 1: DIFFERENT TYPES OF FIXED INCOME SECURITIES. What is fixed income?

Fixed income investments make up a large proportion of the investment universe and can form a significant part of a diversified portfolio but investors are often much less familiar with how fixed income

Fixed income investments make up a large proportion of the investment universe and can form a significant part of a diversified portfolio but investors are often much less familiar with how fixed income

Homework Solutions - Lecture 2

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1286.12 and the treasury rate is 3.43%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1286.12 and the treasury rate is 3.43%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

Recommendations on the Ortec Finance AG asset liability management review of the After-Service Medical Coverage Scheme

Document: EB 2014/111/R.17 Agenda: 9(d) Date: 12 March 2014 Distribution: Public Original: English E Recommendations on the Ortec Finance AG asset liability management review of the After-Service Medical

Document: EB 2014/111/R.17 Agenda: 9(d) Date: 12 March 2014 Distribution: Public Original: English E Recommendations on the Ortec Finance AG asset liability management review of the After-Service Medical

Absolute return: The search for positive returns in changing markets

Absolute return: The search for positive returns in changing markets Tuesday, 7 June 2011 Portfolio Manager for Global Fixed Income and Absolute Return Funds www.dbadvisors.com Topics for discussion What

Absolute return: The search for positive returns in changing markets Tuesday, 7 June 2011 Portfolio Manager for Global Fixed Income and Absolute Return Funds www.dbadvisors.com Topics for discussion What

DEBT MANAGEMENT OFFICE NIGERIA

DEBT MANAGEMENT OFFICE NIGERIA MANAGING NIGERIA S DEBT STOCK Presentation at the Investor/Issuer Education Outreach Programme Organised by Securities and Exchange Commission on July 27, 2011 By Patience

DEBT MANAGEMENT OFFICE NIGERIA MANAGING NIGERIA S DEBT STOCK Presentation at the Investor/Issuer Education Outreach Programme Organised by Securities and Exchange Commission on July 27, 2011 By Patience

Jornadas Economicas del Banco de Guatemala. Managing Market Risk. Max Silberberg

Managing Market Risk Max Silberberg Defining Market Risk Market risk is exposure to an adverse change in value of financial instrument caused by movements in market variables. Market risk exposures are

Managing Market Risk Max Silberberg Defining Market Risk Market risk is exposure to an adverse change in value of financial instrument caused by movements in market variables. Market risk exposures are

The value of liquidity

INVESTMENT MANAGEMENT The value of liquidity Implications for global debt instruments INVESTMENT PERSPECTIVES AUGUST 2014 A Contents Contents Executive summary 1 1. What is liquidity? 2 2. Modelling liquidity

INVESTMENT MANAGEMENT The value of liquidity Implications for global debt instruments INVESTMENT PERSPECTIVES AUGUST 2014 A Contents Contents Executive summary 1 1. What is liquidity? 2 2. Modelling liquidity

Good Practice Checklist

Investment Governance Good Practice Checklist Governance Structure 1. Existence of critical decision-making bodies e.g. Board of Directors, Investment Committee, In-House Investment Team, External Investment

Investment Governance Good Practice Checklist Governance Structure 1. Existence of critical decision-making bodies e.g. Board of Directors, Investment Committee, In-House Investment Team, External Investment

Business Reviews - Prudential plc Annual Report 2012

68 Business review Prudential plc Annual Report 2012 Risk and capital management As a provider of financial services, including insurance, the management of risk lies at the heart of Prudential s business.

68 Business review Prudential plc Annual Report 2012 Risk and capital management As a provider of financial services, including insurance, the management of risk lies at the heart of Prudential s business.

How To Improve Profits At Bmoi

Bank of America Merrill Lynch Banking and Insurance CEO Conference London, 29 September 2009 Good morning. I d like to thank Bank of America Merrill Lynch for letting us speak this morning. Before I talk

Bank of America Merrill Lynch Banking and Insurance CEO Conference London, 29 September 2009 Good morning. I d like to thank Bank of America Merrill Lynch for letting us speak this morning. Before I talk

Sberbank Group s IFRS Results for 6 Months 2013. August 2013

Sberbank Group s IFRS Results for 6 Months 2013 August 2013 Summary of 6 Months 2013 performance: Income Statement Net profit reached RUB 174.5 bn (or RUB 7.95 per ordinary share), a 0.5% decrease on RUB

Sberbank Group s IFRS Results for 6 Months 2013 August 2013 Summary of 6 Months 2013 performance: Income Statement Net profit reached RUB 174.5 bn (or RUB 7.95 per ordinary share), a 0.5% decrease on RUB

For further information UBI Banca Investor Relations Tel.+ 39 0353922217 Email: investor.relations@ubibanca.it UBI Banca Press relations Tel.

- - - For further information UBI Banca Investor Relations Tel.+ 39 0353922217 Email: investor.relations@ubibanca.it UBI Banca Press relations Tel.+ 39 0302433591 +39 3358268310 Email: relesterne@ubibanca.it

- - - For further information UBI Banca Investor Relations Tel.+ 39 0353922217 Email: investor.relations@ubibanca.it UBI Banca Press relations Tel.+ 39 0302433591 +39 3358268310 Email: relesterne@ubibanca.it

Society of Actuaries in Ireland

Society of Actuaries in Ireland Information and Assistance Note LA-1: Actuaries involved in the Own Risk & Solvency Assessment (ORSA) under Solvency II Life Assurance and Life Reinsurance Business Issued

Society of Actuaries in Ireland Information and Assistance Note LA-1: Actuaries involved in the Own Risk & Solvency Assessment (ORSA) under Solvency II Life Assurance and Life Reinsurance Business Issued

ICAAP for Asset Managers: Risk Control Limited

ICAAP for Asset Managers: Risk Control Limited March 2015 Copyright Risk Control Limited 2015 1 Contents Risk Control Limited Overview Pillar II ICAAP: Overview Pillar II ICAAP: Step by Step What we can

ICAAP for Asset Managers: Risk Control Limited March 2015 Copyright Risk Control Limited 2015 1 Contents Risk Control Limited Overview Pillar II ICAAP: Overview Pillar II ICAAP: Step by Step What we can

Valuation Report on Prudential Annuities Limited as at 31 December 2003. The investigation relates to 31 December 2003.

PRUDENTIAL ANNUITIES LIMITED Returns for the year ended 31 December 2003 SCHEDULE 4 Valuation Report on Prudential Annuities Limited as at 31 December 2003 1. Date of investigation The investigation relates

PRUDENTIAL ANNUITIES LIMITED Returns for the year ended 31 December 2003 SCHEDULE 4 Valuation Report on Prudential Annuities Limited as at 31 December 2003 1. Date of investigation The investigation relates

AXA s approach to Asset Liability Management. HELVEA Insurance Capital Adequacy and Solvency Day April 28th, 2005

AXA s approach to Asset Liability Management HELVEA Insurance Capital Adequacy and Solvency Day April 28th, 2005 ALM in AXA has always been based on a long-term view Even though Solvency II framework is

AXA s approach to Asset Liability Management HELVEA Insurance Capital Adequacy and Solvency Day April 28th, 2005 ALM in AXA has always been based on a long-term view Even though Solvency II framework is

Condensed Interim Consolidated Financial Statements of. Canada Pension Plan Investment Board

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board December 31, 2015 Condensed Interim Consolidated Balance Sheet As at December 31, 2015 (CAD millions) As at December

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board December 31, 2015 Condensed Interim Consolidated Balance Sheet As at December 31, 2015 (CAD millions) As at December

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2008 Answers 1 (a) Rights issue price = 2 5 x 0 8 = $2 00 per share Theoretical ex rights price = ((2 50 x 4) + (1 x 2 00)/5=$2

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2008 Answers 1 (a) Rights issue price = 2 5 x 0 8 = $2 00 per share Theoretical ex rights price = ((2 50 x 4) + (1 x 2 00)/5=$2

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective Paul Thornton International Actuarial Association Presentation to OECD Insurance and Pensions Committee June 2010

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective Paul Thornton International Actuarial Association Presentation to OECD Insurance and Pensions Committee June 2010

Greek banks and corporate funding costs

NATIONAL BANK OF GREECE Greek banks and corporate funding costs January 214 Paul Mylonas CRO & Chief Economist National Bank of Greece NBG: ECONOMIC ANALYSIS DEPARTMENT Economic Analysis Department Roadmap

NATIONAL BANK OF GREECE Greek banks and corporate funding costs January 214 Paul Mylonas CRO & Chief Economist National Bank of Greece NBG: ECONOMIC ANALYSIS DEPARTMENT Economic Analysis Department Roadmap

Morgan Stanley 10th Annual European Financials Conference. Mark Wilson Chief Executive Officer. March 2014

Morgan Stanley 10th Annual European Financials Conference Mark Wilson Chief Executive Officer March 2014 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed

Morgan Stanley 10th Annual European Financials Conference Mark Wilson Chief Executive Officer March 2014 1 Disclaimer Cautionary statements: This should be read in conjunction with the documents filed

Research. What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields?

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

Trade Finance Update for Multinationals and Financial Institutions

Trade Finance Update for Multinationals and Financial Institutions A Discussion on Recent Developments in Trade Finance Presented by: Ricardo Martinez, Partner, New York Lloyd Winans, Partner, New York

Trade Finance Update for Multinationals and Financial Institutions A Discussion on Recent Developments in Trade Finance Presented by: Ricardo Martinez, Partner, New York Lloyd Winans, Partner, New York

Public consultation on Building a Capital Markets Union

Case Id: 6793f8c7-c6ef-45dd-8987-665fe5775337 Date: 13/05/2015 23:30:38 Public consultation on Building a Capital Markets Union Fields marked with * are mandatory. Introduction The purpose of the Green

Case Id: 6793f8c7-c6ef-45dd-8987-665fe5775337 Date: 13/05/2015 23:30:38 Public consultation on Building a Capital Markets Union Fields marked with * are mandatory. Introduction The purpose of the Green

Finance for growth, the role of the insurance industry

Finance for growth, the role of the insurance industry Dario Focarelli Director General ANIA Visiting Professor, Risk Management and Insurance, 'La Sapienza' Roma Adjunct Professor, 'Tanaka Business School',

Finance for growth, the role of the insurance industry Dario Focarelli Director General ANIA Visiting Professor, Risk Management and Insurance, 'La Sapienza' Roma Adjunct Professor, 'Tanaka Business School',

Condensed Interim Consolidated Financial Statements of. Canada Pension Plan Investment Board

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board September 30, 2015 Condensed Interim Consolidated Balance Sheet As at September 30, 2015 As at September 30,

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board September 30, 2015 Condensed Interim Consolidated Balance Sheet As at September 30, 2015 As at September 30,

How credit analysts view and use the financial statements

How credit analysts view and use the financial statements Introduction Traditionally it is viewed that equity investment is high risk and bond investment low risk. Bondholders look at companies for creditworthiness,

How credit analysts view and use the financial statements Introduction Traditionally it is viewed that equity investment is high risk and bond investment low risk. Bondholders look at companies for creditworthiness,

Investment Portfolio Management and Effective Asset Allocation for Institutional and Private Banking Clients

Investment Portfolio Management and Effective Asset Allocation for Institutional and Private Banking Clients www.mce-ama.com/2396 Senior Managers Days 4 www.mce-ama.com 1 WHY attend this programme? This

Investment Portfolio Management and Effective Asset Allocation for Institutional and Private Banking Clients www.mce-ama.com/2396 Senior Managers Days 4 www.mce-ama.com 1 WHY attend this programme? This

Practical guide to IFRS

pwc.com/ifrs Practical guide to IFRS Financial reporting considerations arising from current market conditions in Europe Background There continue to be significant economic concerns in some European countries

pwc.com/ifrs Practical guide to IFRS Financial reporting considerations arising from current market conditions in Europe Background There continue to be significant economic concerns in some European countries

CONSTRUCTING A GROWTH FIXED INCOME PORTFOLIO MAY 2013

CONSTRUCTING A GROWTH FIXED INCOME PORTFOLIO MAY 2013 Context Currently developed market sovereign bonds are not appealing from an investment perspective. They offer negative or low real returns and are

CONSTRUCTING A GROWTH FIXED INCOME PORTFOLIO MAY 2013 Context Currently developed market sovereign bonds are not appealing from an investment perspective. They offer negative or low real returns and are

European real estate debt The case for senior commercial mortgage investment September 2015

Spread (bps) European real estate debt The case for senior commercial mortgage investment September 2015 For fixed income investors, the case for senior commercial mortgage lending remains strong, with

Spread (bps) European real estate debt The case for senior commercial mortgage investment September 2015 For fixed income investors, the case for senior commercial mortgage lending remains strong, with

Ten reasons to be invested in European Listed Real Estate

Ten reasons to be invested in European Listed Real Estate Executive Summary At Petercam Institutional Asset, we are convinced that investing part of one s assets in European listed real estate makes sense.

Ten reasons to be invested in European Listed Real Estate Executive Summary At Petercam Institutional Asset, we are convinced that investing part of one s assets in European listed real estate makes sense.

LDI Fundamentals: Is Our Strategy Working? A survey of pension risk management metrics

LDI Fundamentals: Is Our Strategy Working? A survey of pension risk management metrics Pension plan sponsors have increasingly been considering liability-driven investment (LDI) strategies as an approach

LDI Fundamentals: Is Our Strategy Working? A survey of pension risk management metrics Pension plan sponsors have increasingly been considering liability-driven investment (LDI) strategies as an approach

iii. Risk Report Management's Assessment on Risk Profile

Management Discussion and Analysis, Risk Report and Financial Control Reconciliations, Risk Report 149 Risk Report and Financial Control iii. Risk Report the allianz risk management approach is designed

Management Discussion and Analysis, Risk Report and Financial Control Reconciliations, Risk Report 149 Risk Report and Financial Control iii. Risk Report the allianz risk management approach is designed

Lecture 2 Bond pricing. Hedging the interest rate risk

Lecture 2 Bond pricing. Hedging the interest rate risk IMQF, Spring Semester 2011/2012 Module: Derivatives and Fixed Income Securities Course: Fixed Income Securities Lecturer: Miloš Bo ović Lecture outline

Lecture 2 Bond pricing. Hedging the interest rate risk IMQF, Spring Semester 2011/2012 Module: Derivatives and Fixed Income Securities Course: Fixed Income Securities Lecturer: Miloš Bo ović Lecture outline

DACT autumn diner workshop. Risk management, valuation and accounting

DACT autumn diner workshop Risk management, valuation and accounting Agenda 1. Risk management - mitigate risk Cost of hedging Risk mitigants Risk management policy 2. Valuation & accounting - mitigate

DACT autumn diner workshop Risk management, valuation and accounting Agenda 1. Risk management - mitigate risk Cost of hedging Risk mitigants Risk management policy 2. Valuation & accounting - mitigate

Asset-Liability Management

Asset-Liability Management in today s insurance world Presentation to the Turkish Actuarial Society Jeremy Kent FIA Dominic Clark FIA Thanos Moulovasilis FIA 27 November 2013 Agenda ALM some definitions

Asset-Liability Management in today s insurance world Presentation to the Turkish Actuarial Society Jeremy Kent FIA Dominic Clark FIA Thanos Moulovasilis FIA 27 November 2013 Agenda ALM some definitions

& Embedded value 2009

First quarter 2010 results & Embedded value 2009 Jan Nooitgedagt, CFO Analyst & Investor presentation May 12, 2010 Key messages o Further improvement of underlying earnings o Continued execution of strategy

First quarter 2010 results & Embedded value 2009 Jan Nooitgedagt, CFO Analyst & Investor presentation May 12, 2010 Key messages o Further improvement of underlying earnings o Continued execution of strategy

Are Unconstrained Bond Funds a Substitute for Core Bonds?

TOPICS OF INTEREST Are Unconstrained Bond Funds a Substitute for Core Bonds? By Peter Wilamoski, Ph.D. Director of Economic Research Philip Schmitt, CIMA Senior Research Associate AUGUST 2014 The problem

TOPICS OF INTEREST Are Unconstrained Bond Funds a Substitute for Core Bonds? By Peter Wilamoski, Ph.D. Director of Economic Research Philip Schmitt, CIMA Senior Research Associate AUGUST 2014 The problem

THE USE OF FIXED INCOME DERIVATIVES AT TAL GLOBAL ASSET MANAGEMENT

GLOBAL ASSET MANAGEMENT INC. THE USE OF FIXED INCOME DERIVATIVES AT TAL GLOBAL ASSET MANAGEMENT Paul Bourdeau, CFA Page 1 September 2002 AGENDA Overview of TAL Overview of the Use of Derivatives at Use

GLOBAL ASSET MANAGEMENT INC. THE USE OF FIXED INCOME DERIVATIVES AT TAL GLOBAL ASSET MANAGEMENT Paul Bourdeau, CFA Page 1 September 2002 AGENDA Overview of TAL Overview of the Use of Derivatives at Use