Tax Implications of Significant PFRS Standards

|

|

|

- Dominick Wells

- 8 years ago

- Views:

Transcription

1 Tax Implications of Significant PFRS Standards Ma. Victoria C. Españo PICPA National Annual Convention Iloilo City, 2010

2 PFRS and Tax Laws Philippine Financial Reporting Standards (PFRS) set of rules to govern the recognition, measurement and reporting of financial transactions of an entity Philippine National Internal Revenue Code (Tax Code) set of laws governing the taxes imposed in the Philippines

set of laws governing the taxes imposed in the")

3 PFRS and Tax Laws For tax purposes, revenue and expenses are generally determined based on the accounting method followed by the taxpayer (Sec. 43) Exception If accounting method is not reflective of true income, a different method may be used. If the NIRC provides for specific treatment of income or expenses, this should be followed.

4 What BIR says about the new accounting standards.. Generally accepted accounting principles (GAAP) and Generally accepted accounting standards (GAAS) approved by the Accounting Standards Council (ASC) may, from time to time, differ from the provisions of the Tax Code of 1997 and its implementing regulations. In such cases, the provisions of the Tax Code and its implementing rules and regulations shall prevail. - Rev. Memorandum Circular

5 What BIR says about the new accounting standards.. Taxpayers must maintain books and records that would show clearly the reconciling items or differences between the amounts shown in a taxpayer s financial statements and the figures reported in its income tax return. - Rev. Regulations No

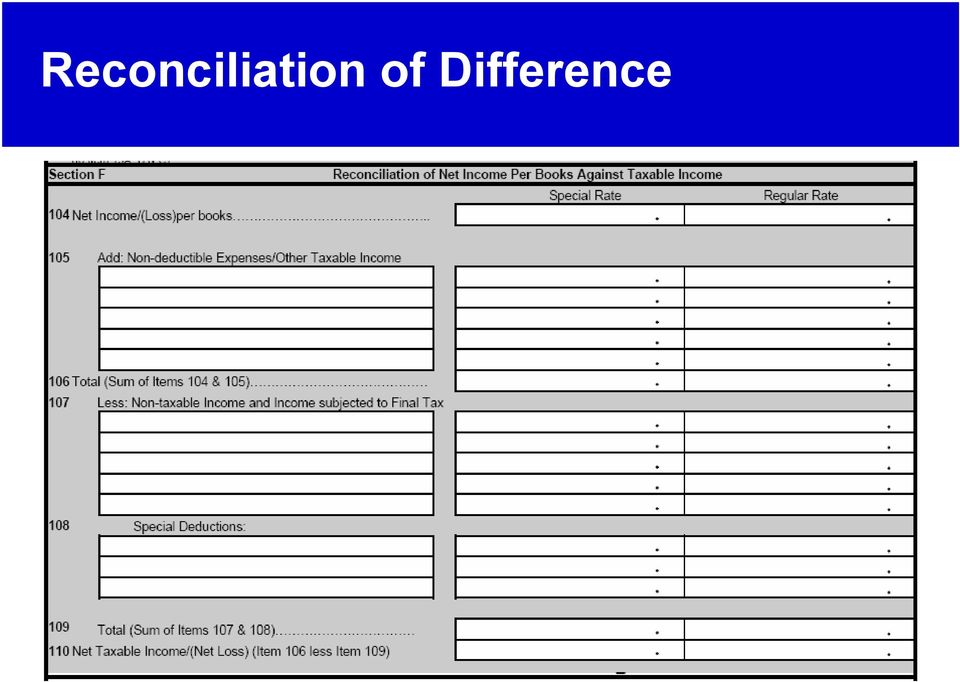

6 Reconciliation of Difference

7 Importance of Financial Records Audited financial statements are required to be submitted with ITR. Financial records are reviewed during tax examination Courts also rely on financial records in evaluating the completeness and correctness of tax information.

8 What should taxpayers do Understand changes brought about by these standards and evaluate if they are contrary to existing tax rules If not contrary and will reflect true income, adopt them. Comply with requirements relating to the adoption of such change! 1. Approval for changes in accounting methods 2. Tax ruling to confirm acceptability of accounting treatment for tax purposes

9 What should taxpayers do If contrary, recognize that information shall be treated differently for tax purposes. Difference should be reported as reconciling accounts between tax and book income. Establish system to track and capture the differences - Track differences for every affected transaction - Calculate differences at the end of the year

10 New Standards Effective 2005 PAS 1 PAS 2 PAS 8 PAS 10 PAS 16 PAS 17 PAS 19 PAS 21 PAS 24 PAS 27 PAS 29 Presentation in Financial Statements Inventories Changes in Accounting Policy, Prior Period Error s & Estimates Events After Balance Sheet Date Property, Plant and Equipment Leases Employee Benefits Effects of Changes in Foreign Exchange Rates Related Party Transactions Consolidated and Separate Financial Statements Investment in Associates

11 New Standards Effective 2005 PAS 31 PAS 32 PAS 33 PAS 36 PAS 38 PAS 39 PAS 40 PFRS 2 PFRS 3 PFRS 5 Interest in Joint Ventures Financial Instruments: Presentation and Disclosures Earnings Per Share Impairment of Assets Intangible Assets Financial Instruments: Recognition and Measurements Investment Properties Share-based Payments Business Combinations Non-current assets held for sales

12 After 2005 Additional standards and interpretations issued by the IASB and the IFRIC 37 standards (8 x PFRSs; 29 x PASs) 24 interpretations (13 x IFRICs; 11 x SICs)

24 interpretations (13 x IFRICs;")

13 Understanding Differences ACCOUNTING Fair value Substance Matching Income and Expenses Accounting Standards TAX Cost Form Contractual Rights and Obligations Legal Provisions

14

15 PAS 2 : Inventories Inventories are required to be stated at the lower of: Cost or Net realizable value NRV = Estimated selling price Less: Estimated cost to sell

16 PAS 2 : Inventories Accounting Inventory shall be adjusted to NRV if the latter is lower than cost. Tax Inventory shall remain to be valued at cost Write-down to NRV expense during the period Not valid additions to Cost of Sales. Reversal of write-down reduction in inventories recognized as expense during the period Reversals should not decrease COS.

17 PAS 36: Impairment of Assets Accounting Policy Tax Treatment / Issues Impairment loss is charged as an expense. Losses recognized due to impairment are not deductible. A reversal of an impairment loss for an asset shall be recognized immediately As income (or reduction of expense). Gains from reversal of impairment loss are not taxable. Any reversal of an impairment loss of a revalued asset is credited directly to equity under the heading revaluation surplus.

18 PAS 40 : Investment Property Applies to property (land or building) used to Earn rentals or For capital appreciation or Both Rather than for use in the production or supply of goods or for administrative purposes, or sale in the ordinary course of business.

19 PAS 40 : Investment Property An entity is given the option to choose either: a fair value model, under which an investment property is measured at fair value with changes in fair value recognized in profit or loss a cost model, which requires an investment property to be measured after initial measurement at depreciated cost.

20 PAS 36 : Investment Property Accounting Fair value model Increase in FV property is reported as income Decrease in FV is reported as expense Tax For tax, property shall be valued at cost. Income/expense recognized due to changes in the value of the property will not be considered as taxable income /deductible expense. If a property is used in business, taxpayer can claim deduction for depreciation. Depreciation shall be based on cost. If the property is sold, gains or losses to be considered shall be based on the unadjusted carrying value (without adjustment of fair value effects).

21

22 Fundamental Principle - Accounting Inventories are required to be stated at the lower of: Cost or Net realizable value

23 Measurement of Cost - Accounting Includes: Cost of purchase Cost of conversion Other costs to bring inventories to present location and condition Excludes: Abnormal waste Storage Cost Unrelated administrative overhead Selling costs Deferred Payment cost Foreign exchange differences

24 Example - Deferred payment Buyer Side Product was invoiced for P100, payable after a year. If cash payment, price will be P90. Purchases 90 Deferred Interest Expense 10 Accounts Payable 100 Accounts Payable 100 Interest Expense 10 Cash 100 Deferred Interest Expense 10

25 PAS 2 : Inventories Accounting Cash discounts and Settlement discounts are recognized when the purchase is booked. Contractual discounts shall be recognized once probable. Tax If the discount has not been granted at the time of purchase, the purchase price shall be recorded based on the invoice amount Only actual discounts are reported as reduction from gross sales. Cash discount time of purchase Settlement discount when received Rebates when granted

26 PAS 2 : Inventories Accounting If not availed, the foregone discount is recognized as finance cost. Tax Such finance cost shall not be deductible. Useful to use a different account title to record discounts recognized upon purchase but not yet granted under a different account title finance costs relating to unavailed discounts.

27 PAS 18 : Revenue Recognition Goods Transfer of risks & rewards Management involvement Substance of the transaction Recognize revenue when: 1. Measured reliably 2. Flow of economic benefits probable 3. Costs measured reliably Services Performance of obligations Percentage of completion method PAS 11 construction contracts

28 PAS 18 : Revenue Recognition Multiple Element Arrangements (MEA) - Arrangements involving the supply of multiple goods or services at different points in time Examples of MEAs include Supply of goods with subsequent servicing Certain customer loyalty/incentive schemes

29 PAS 18 : Revenue Recognition Accounting Revenues shall be accounted for separately. Tax Treat the components of a transaction separately if - Amount for subsequent servicing that is identifiable from the selling price is deferred and recognized as revenue over the period during which the service is performed. the contract explicitly describes these components and the stipulated payments are broken down according to the various parts of what is being provided under the contract.

30 Substance vs. Form - MEA Example : Supply of goods with subsequent servicing Entity G runs a promotion in which customers sign a twelve month airtime contract with minimum monthly spend of P 30 per month, entitling them to 60 minutes of usage each month, and receive a "free" phone. The phone is also sold separately for P100 (assume there are regular sales at this price). Under the promotion customers also pay a one-off connection fee of P50.

31 Substance vs. Form - MEA Analysis: The arrangement includes two separately identifiable components - the phone and the airtime service. The total consideration for the arrangement is P410 ( x30). The fair value of the phone is P100. The fair value of the airtime revenue is P360. Using a relative fair value approach, the total revenue of P410 is allocated proportionately to the fair values of the two separately identifiable components as follows: Phone: P410 x (100/460) = 89 Airtime: P410 x (360/460) = 321

32 PAS 18 : Revenue Recognition Accounting Recognized as sale of goods: The phone revenue of P89 is recognized on delivery of the phone, along with associated costs. Recognized as sale of services: The airtime revenue of P321 is recognized on a straight line basis over the 12 month contract period. Tax Recognized as sale of services Income tax : VAT: Connection fee of P50 is recognized as revenue in the first year. Airtime revenue of P360 is recognized over the 12 month contract period. Taxable sales is the amount actually received during the year.

33 PAS 17 : Leases Classification of Leases 1. Finance Lease is a lease that transfers substantially all the risks and rewards incident to ownership of an asset. Title may or may not eventually be transferred. 2. Operating Lease is a lease other than the finance lease.

34 Definition Tax (RR 19-86) 1. Lease an agreement between the lessor and lessee giving lessee possession and use of a specific property upon payment of rentals over a period of time. 2. Conditional Sale one of the parties obligates himself or transfer ownership of and deliver a determinate thing while the other pays a price certain.

35 PAS 17 : Leases Accounting Tax Operating Lease Operating Lease Finance Lease Operating Lease Finance Lease Conditional Sale

36 PAS 32: Financial Instruments: Presentation and Disclosures Financial Liability Equity Instrument When issuer is or can be required to deliver either cash or another financial asset to the holder (presence of contractual obligation) When it represents a residual interest in the net asset of the issuer

37 PAS 18 : Revenue Recognition Accounting Tax The substance of a financial instrument governs its classification rather than its legal form Based on LEGAL FORM Treated as obligation if covered by PN, Loan agreements and etc. Treated as equity if representing ownership in company. Normally covered by shares of stocks.

38 Financial Liabilities vs. Equity Instruments Instrument Classification For Accounting Treatment For Tax Payout Common shares Equity Equity Dividends Redeemable preferred shares with 50% fixed dividend each year subject to availability of distributable profits Liability Equity Accounting: Interest Tax: Dividends Convertible bond which converts into fixed number of shares Liability for bond and equity for option Liability Accounting: Interest and Dividend Tax: Interest Convertible bond which converts into shares to the value of the liability Liability Liability until converted to shares Interest

39 PAS 32: Financial Instruments Presentation and Disclosures Financial Liabilities vs. Equity Instruments Example: Company A issued on May 5, 2005 preferred shares with 10% dividend per year and are redeemable in May Accounting: The preferred shares are to be presented in the B/S of Company A as liabilities because they represent contractual obligations of the company to deliver cash at a fixed maturity date. Tax: The preferred shares are treated as equity. Payout is dividend not interest.

40 Tax Treatment: Interest vs. Dividend Interest Dividend Deductibility Deductible Non-deductible Withholding Tax Interest paid to foreign creditor is subject to 20% FT or tax treaty rate, if applicable -0% if intercorporate -32% if NRFC unless Treaty rate - 15% if Resident if tax-sparing provision applies

41 Tax Rules Thin capitalization BIR to examine whether there is a true debtor-creditor relationship. Excessively large liabilities in relation to capital stock (especially in the case of a new company) may indicate a thin capitalization situation. In the absence of rules prescribing guidelines and presumptions as to what constitute thin capitalization (unlike other countries), there is a necessity to determine the reasonable ratio of debt over equity considering all factors surrounding the case. - Rev Audit Memo Order 1-98

42

43 PAS 18 : Revenue Recognition Fair value of consideration received or receivable If consideration is receivable in the future, use present value and recognize interest income as discount unwinds

44 PAS 18 : Revenue Recognition Example: Seller Side Product was invoiced for P100, payable after 18 months. If cash payment, price will be P90. Accounts Receivable 100 Sales 90 Deferred Interest Income 10 Cash 100 Deferred Interest income 10 Accounts Receivable 100 Interest Income 10

45 PAS 18 : Revenue Recognition Accounting When inventories are sold with deferred settlement terms, the difference between the sales price for normal credit terms and the amount received is recognized as interest income over the period of financing. Tax Taxpayer should report as sales the full invoice amount, both for income and VAT purposes. Implicit interest income on transaction is not taxable. For tracking purposes, a different account may be used to record this type of interest.

46 PAS 16: Property, Plant and Equipment PPE are initially measured at cost. Components of the cost of PPE: Purchase price, including import duties Directly attributable costs Initial estimate of the costs of dismantling and removing the item and restoring the site Excludes interest and financing cost to acquire property, except for qualifying assets.

47 PAS 16: Property, Plant and Equipment Accounting Cost shall include initial estimate of cost of dismantlement or removal or cost of restoration incurred to install an item. Tax Not qualified as part of the cost of PPE. This difference affects: - Depreciation - Book value of PPE when disposed Such costs are deductible only when actually incurred (upon dismantling, restoration)

48 PAS 16: Property, Plant and Equipment Accounting Cost shall include initial estimate of cost of dismantlement or removal or Tax Withholding tax - based on actual acquisition cost of PPE. VAT - purchase should be reported at acquisition cost. cost of restoration incurred to install an item.

49 Example: Accounting for Estimated Dismantling and Restoration Costs FS Tax Acquisition cost: Purchase price Installation cost PV Est. dismantling cost P 1,500, , ,000 P 1,500, ,000 - Total Acquisition Cost P 1,850,000 P 1,600,000 Annual Depreciation P 370,000 P 320,000 *Useful life = 5 years

50 PAS 17: Leases Operating Lease : Lessor Accounting Policy Lease income from operating leases shall be recognized as income on a straight-line basis over the lease term, even if the receipts are not on such a basis. Tax Treatment / Issues Income to be reported shall be the amount to be received by the Lessor based on the provisions of the agreement. Hence, the income to be reported by the lessor is just the rent actually earned.

51 Operating Lease with unequal rental payments Year 1 Lessor s Books Lessee s Books Dr. Cash P1,000 Dr. Rent Expense P1,150 Dr. Receivable 150 Cr. Payable 150 Cr. Rent Income 1,150 Cr. Cash P1,000 Year 2 Annual rental: Y1 - P1,000; Y2 - P1,100; Y3 - P1,200; Y4 - P1,300; Lease term = 4 yrs Total rent for 4 years = P4,600; Average annual rent = P1,150 Accounting entry upon receipt/payment of rent: Years 1 and 2 Dr. Cash P1,000 Dr. Rent Expense P1,150 Dr. Receivable 150 Cr. Payable 150 Cr. Rent Income 1,150 Cr. Cash P1,000

52

53 PAS 8 : Changes in Accounting Policy Accounting Accounting error should be adjusted retrospectively. Tax Tax return in affected year should be amended to report true income or expense. However, this can only be done within three years from the date of filing of such return and provided no notice for audit or investigation has been served to the taxpayer. - Sec. 6, NIRC, as amended

54 PAS 16 : Property, Plant and Equipment Interest and financing charges relating to acquisition of property are treated as period expense, unless said interest are opted to be capitalized for being related to acquisition of qualifying assets. Qualifying asset pertain to a property that necessarily takes a substantial period of time to get ready for its intended use or sale. o Manufacturing plant o Power generation facilities o Buildings o Warehouse

55 PAS 16: Property, Plant and Equipment Accounting Interest and financing charges relating to acquisition of property Non-qualifying treated as an expense Qualifying option to either recognize as period expense or to capitalize as part of the cost of the asset. Tax If incurred in connection with the acquisition of property used in business, taxpayer is given the option to either : Treat interest as part of the cost of the property (and thereof be part of the depreciable base) or Claim interest as deduction in the year incurred. - Sec. 34(B)(1), NIRC as amended

56 PAS 36 : Impairment of Assets Accounting Impairment loss Charged to profit and loss. Tax Gain or loss is recognized only when the asset is sold or disposed. - Sec. 96, Rev. Regs. 2 Non-deductible losses. Gains from reversal of impairment loss are not taxable. - BIR Ruling DA , Nov. 10, 2003

57 PAS 38 : Intangible Assets Accounting Tax Expenditure on research - Recognized as an expense when it is incurred. Development expenditures Option to - Expense in the year incurred, or - Capitalize as an intangible asset. Option to Deduct in the year incurred or Deferred expenses and claim as deduction ratably distributed over a period of not less than 60 months, beginning with the month in which the taxpayer first realizes benefits from such expenditures. -Sec. 34(I), NIRC as amended

58 Example Impact of Impairment on Depreciation Calculation of the Impairment loss at the end of 2005 Carrying amount before impairment loss P 150,000 Impairment loss (P 28,872) Recoverable amount P 121,128 Depreciation each year (straight line basis) P 12,113 Deductible depreciation P 15,000

59 PAS 19: Employee Benefits Accounting DCP = expense / accrued liability is the amount of required contribution under the plan. DBP = use of actuarial assumptions to measure the net expense (income) and the retirement benefit obligation (asset). Tax Only contributions paid during the year to a BIR-qualified trusteed plan are deductible Rule on deductibility: Contributions for present service cost full deductible; Contributions for past service cost, 1/10th of the contribution paid. - Sec 34(J), NIRC

60 Reconciling Tax and Book Income

61 Reconciling Items to be shown in ITR Non-deductible loss on write-down of inventory to net realizable value (PAS 2) Non-deductible/non-taxable implicit interest expense/income recognized on purchase of inventory on deferred installment term (PAS 2) Non-taxable/non-deductible gains/losses arising from the recognition of biological assets/agricultural produce at FV less point-of-sale costs (PAS 41) Difference between the gains/loss on disposal of biological assets/agricultural produce computed using stated at FV less point-ofsale costs vs. unadjusted costs (PAS 41) Non-deductible depreciation on dismantlement, restoration costs and/or revaluation increment (PAS16) Non-deductible impairment losses (PAS 16,38,17,36,40,PFRS 5)

62 Reconciling Items - Additional Non-deductible depreciation on dismantlement, restoration costs and/or revaluation increment (PAS16) Non-deductible impairment losses (PAS 16,38,17,36,40,PFRS 5) Non-taxable gain on reversal of impairment loss (PAS 16, 38, 17, 36, 40, PFRS 5) Additional depreciation on proceeds from samples deducted from the cost of equipment (PAS 16) Difference between the gain/loss on disposal of property computed using the carrying value vs. BV based on cost (PAS 16,17,36,40, PFRS 5) Non-deductible loss on assets de-recognized (PAS 16,36,40, PFRS 5) Amortization of research costs capitalized for tax purposes (PAS 38)

63 Reconciling Items - Additional Loss on write-off of research costs (PAS 38) Difference between the lease expense per contract and per expense recorded (PAS 17) Difference in depreciation expense per accounting and per tax on capitalized leased assets (PAS 17) Gain/loss on assets sold through sale-leaseback agreement (PAS 17) Amortization of gain/loss on assets sold through sale-leaseback agreement (PAS 17) Non-taxable/non-deductible revaluation gains/loss (PAS 38,32)

64 Reconciling Items - Additional Non-deductible/non-taxable implicit interest expenses/income recognized on financial instruments (PAS 32) Interest expense financial instrument recorded as dividends (PAS 32) Non-deductible/non-taxable interest expense/income pertaining to dividends declared/received (PAS 32) Non-taxable/non-deductible gains/losses in changes in faire value of financial assets at FVTPL (PAS 32) Non-taxable/non-deductible gains/losses on remeasurement of derivatives/hedging (PAS 32) Non-deductible accrual of employee benefits (PAS 19, PFRS 2) Employee benefits paid in the current taxable year bur accrued in previous year/s (PAS 19, PFRS 2)

65 Challenge for business entities Are their accounting personnel familiar with the differences with tax and accounting rules to be able to make valuable suggestions to management? Did their employees who are responsible for the preparation of income tax return undergo training on the impact of the new accounting standards on tax reporting? Has the entity reviewed its information system to determine if it effectively captures the relevant tax and accounting differences to ensure availability of correct information when required? Does the entity maintain records to support these differences are retained and will be readily available in case of a BIR tax audit?

66 Thank You...

EXPLANATORY NOTES. 1. Summary of accounting policies

1. Summary of accounting policies Reporting Entity Taranaki Regional Council is a regional local authority governed by the Local Government Act 2002. The Taranaki Regional Council group (TRC) consists

1. Summary of accounting policies Reporting Entity Taranaki Regional Council is a regional local authority governed by the Local Government Act 2002. The Taranaki Regional Council group (TRC) consists

Consolidated financial statements

Summary of significant accounting policies Basis of preparation DSM s consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted

Summary of significant accounting policies Basis of preparation DSM s consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted

Transition to International Financial Reporting Standards

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

Jollibee Foods Corporation and Subsidiaries

Jollibee Foods Corporation and Subsidiaries Consolidated Financial Statements December 31, 2013 and 2012 and Years Ended December 31, 2013, 2012 and 2011 and Independent Auditors Report SyCip Gorres Velayo

Jollibee Foods Corporation and Subsidiaries Consolidated Financial Statements December 31, 2013 and 2012 and Years Ended December 31, 2013, 2012 and 2011 and Independent Auditors Report SyCip Gorres Velayo

CONSOLIDATED STATEMENT OF INCOME

CONSOLIDATED STATEMENT OF INCOME Notes Sales 1) 5,429,574 5,169,545 Cost of Goods Sold 2) 3,041,622 2,824,771 Gross Profit 2,387,952 2,344,774 Selling Expenses 3) 1,437,010 1,381,132 General and Administrative

CONSOLIDATED STATEMENT OF INCOME Notes Sales 1) 5,429,574 5,169,545 Cost of Goods Sold 2) 3,041,622 2,824,771 Gross Profit 2,387,952 2,344,774 Selling Expenses 3) 1,437,010 1,381,132 General and Administrative

STATEMENT OF COMPLIANCE AND BASIS OF MEASUREMENT

Accounting policies REPORTING ENTITY The Waikato Regional Council is a territorial local authority governed by the Local Government Act 2002, and is domiciled in New Zealand. The main purpose of prospective

Accounting policies REPORTING ENTITY The Waikato Regional Council is a territorial local authority governed by the Local Government Act 2002, and is domiciled in New Zealand. The main purpose of prospective

Residual carrying amounts and expected useful lives are reviewed at each reporting date and adjusted if necessary.

87 Accounting Policies Intangible assets a) Goodwill Goodwill represents the excess of the cost of an acquisition over the fair value of identifiable net assets and liabilities of the acquired company

87 Accounting Policies Intangible assets a) Goodwill Goodwill represents the excess of the cost of an acquisition over the fair value of identifiable net assets and liabilities of the acquired company

Philippine Financial Reporting Standards (Adopted by SEC as of December 31, 2011)

") Standards (Adopted by SEC as of December 31, 2011) Philippine Financial Reporting Framework for the Preparation and Presentation of Financial Statements Conceptual Framework Phase A: Objectives and qualitative

Standards (Adopted by SEC as of December 31, 2011) Philippine Financial Reporting Framework for the Preparation and Presentation of Financial Statements Conceptual Framework Phase A: Objectives and qualitative

Summary of Significant Accounting Policies FOR THE FINANCIAL YEAR ENDED 31 MARCH 2014

46 Unless otherwise stated, the following accounting policies have been applied consistently in dealing with items which are considered material in relation to the financial statements. The Company and

46 Unless otherwise stated, the following accounting policies have been applied consistently in dealing with items which are considered material in relation to the financial statements. The Company and

International Accounting Standard 40 Investment Property

International Accounting Standard 40 Investment Property Objective 1 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

International Accounting Standard 40 Investment Property Objective 1 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

LEASES SCOPE/EXCLUSIONS

LEASES SCOPE/EXCLUSIONS What is a lease? A lease is an agreement whereby the lessor conveys to the lessee in return for a payment or series of payments the right to use an asset for an agreed period of

LEASES SCOPE/EXCLUSIONS What is a lease? A lease is an agreement whereby the lessor conveys to the lessee in return for a payment or series of payments the right to use an asset for an agreed period of

SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS. Year ended December 31, 2011

SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS Year ended SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS For the year ended The information contained in

SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS Year ended SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS For the year ended The information contained in

Acal plc. Accounting policies March 2006

Acal plc Accounting policies March 2006 Basis of preparation The consolidated financial statements of Acal plc and all its subsidiaries have been prepared in accordance with International Financial Reporting

Acal plc Accounting policies March 2006 Basis of preparation The consolidated financial statements of Acal plc and all its subsidiaries have been prepared in accordance with International Financial Reporting

Consolidated Statement of Financial Position Sumitomo Corporation and Subsidiaries As of March 31, 2016 and 2015. Millions of U.S.

Consolidated Statement of Financial Position Sumitomo Corporation and Subsidiaries As of March 31, 2016 and 2015 ASSETS Current assets: Cash and cash equivalents 868,755 895,875 $ 7,757 Time deposits 11,930

Consolidated Statement of Financial Position Sumitomo Corporation and Subsidiaries As of March 31, 2016 and 2015 ASSETS Current assets: Cash and cash equivalents 868,755 895,875 $ 7,757 Time deposits 11,930

Note 2 SIGNIFICANT ACCOUNTING

Note 2 SIGNIFICANT ACCOUNTING POLICIES BASIS FOR THE PREPARATION OF THE FINANCIAL STATEMENTS The consolidated financial statements have been prepared in accordance with International Financial Reporting

Note 2 SIGNIFICANT ACCOUNTING POLICIES BASIS FOR THE PREPARATION OF THE FINANCIAL STATEMENTS The consolidated financial statements have been prepared in accordance with International Financial Reporting

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS TABLE OF CONTENTS MANAGEMENT S STATEMENT OF RESPONSIBILITY FOR FINANCIAL REPORTING 65 INDEPENDENT AUDITOR S REPORT 66 CONSOLIDATED FINANCIAL STATEMENTS 67 Consolidated

CONSOLIDATED FINANCIAL STATEMENTS TABLE OF CONTENTS MANAGEMENT S STATEMENT OF RESPONSIBILITY FOR FINANCIAL REPORTING 65 INDEPENDENT AUDITOR S REPORT 66 CONSOLIDATED FINANCIAL STATEMENTS 67 Consolidated

Income Taxes STATUTORY BOARD SB-FRS 12 FINANCIAL REPORTING STANDARD

STATUTORY BOARD SB-FRS 12 FINANCIAL REPORTING STANDARD Income Taxes This version of the Statutory Board Financial Reporting Standard does not include amendments that are effective for annual periods beginning

STATUTORY BOARD SB-FRS 12 FINANCIAL REPORTING STANDARD Income Taxes This version of the Statutory Board Financial Reporting Standard does not include amendments that are effective for annual periods beginning

How To Account For Property, Plant And Equipment

International Accounting Standard 16 Property, Plant and Equipment Objective 1 The objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of

International Accounting Standard 16 Property, Plant and Equipment Objective 1 The objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of

Investments in Associates and Joint Ventures

International Accounting Standard 28 Investments in Associates and Joint Ventures In April 2001 the International Accounting Standards Board (IASB) adopted IAS 28 Accounting for Investments in Associates,

International Accounting Standard 28 Investments in Associates and Joint Ventures In April 2001 the International Accounting Standards Board (IASB) adopted IAS 28 Accounting for Investments in Associates,

Volex Group plc. Transition to International Financial Reporting Standards Supporting document for 2 October 2005 Interim Statement. 1.

Volex Group plc Transition to International Financial Reporting Standards Supporting document for 2 October 2005 Interim Statement 1. Introduction The consolidated financial statements of Volex Group plc

Volex Group plc Transition to International Financial Reporting Standards Supporting document for 2 October 2005 Interim Statement 1. Introduction The consolidated financial statements of Volex Group plc

Fixed Assets. Name: SudhirJain M. No.: 213157

Fixed Assets Name: SudhirJain M. No.: 213157 Agenda AS- 10 Accounting for Fixed Assets Introduction & Scope Definitions and other relevant provisions Relevant provisions of other Accounting Standards applicable

Fixed Assets Name: SudhirJain M. No.: 213157 Agenda AS- 10 Accounting for Fixed Assets Introduction & Scope Definitions and other relevant provisions Relevant provisions of other Accounting Standards applicable

Property, Plant and Equipment

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 16 Property, Plant and Equipment SB-FRS 16 Property, Plant and Equipment applies to Statutory Boards for annual periods beginning on or after 1 January

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 16 Property, Plant and Equipment SB-FRS 16 Property, Plant and Equipment applies to Statutory Boards for annual periods beginning on or after 1 January

ACCOUNTING POLICY 1.1 FINANCIAL REPORTING. Policy Statement. Definitions. Area covered. This Policy is University-wide.

POLICY Area covered ACCOUNTING POLICY This Policy is University-wide Approval date 5 May 2016 Policy Statement Intent Scope Effective date 5 May 2016 Next review date 5 May 2019 To establish decisions,

POLICY Area covered ACCOUNTING POLICY This Policy is University-wide Approval date 5 May 2016 Policy Statement Intent Scope Effective date 5 May 2016 Next review date 5 May 2019 To establish decisions,

Consolidated financial statements of MTY Food Group Inc. November 30, 2015 and 2014

Consolidated financial statements of MTY Food Group Inc. Independent auditor s report...1 2 Consolidated statements of income... 3 Consolidated statements of comprehensive income... 4 Consolidated statements

Consolidated financial statements of MTY Food Group Inc. Independent auditor s report...1 2 Consolidated statements of income... 3 Consolidated statements of comprehensive income... 4 Consolidated statements

Contents. 3 Group Financial Statements. 68 Financial Statements of Schindler Holding Ltd. 84 Compensation Report. 102 Corporate Governance

Investing in people and technology. Financial Statements 2014 Contents 3 Group Financial Statements 68 Financial Statements of Schindler Holding Ltd. 84 Compensation Report 102 Corporate Governance The

Investing in people and technology. Financial Statements 2014 Contents 3 Group Financial Statements 68 Financial Statements of Schindler Holding Ltd. 84 Compensation Report 102 Corporate Governance The

Muhammad Asif Iqbal Technical Advisor, SOCPA. March 7, 2012

Saudi Accounting Framework in comparison with Framework Muhammad Asif Iqbal Technical Advisor, SOCPA ICAP KSA Chapter, Khobar March 7, 2012 Agenda Status of Accounting Standards in Saudi Arabia SOCPA Convergence

Saudi Accounting Framework in comparison with Framework Muhammad Asif Iqbal Technical Advisor, SOCPA ICAP KSA Chapter, Khobar March 7, 2012 Agenda Status of Accounting Standards in Saudi Arabia SOCPA Convergence

DESIGNIT OSLO A/S STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2016

DESIGNIT OSLO A/S STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2016 Payables include balances due to Micro & Small Enterprises ` NIL as on 31 st March 2016. *Trade 1. Company

DESIGNIT OSLO A/S STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2016 Payables include balances due to Micro & Small Enterprises ` NIL as on 31 st March 2016. *Trade 1. Company

Summary of Certain Differences between SFRS and US GAAP

Summary of Certain Differences between and SUMMARY OF CERTAIN DIFFERENCES BETWEEN AND The combined financial statements and the pro forma consolidated financial information of our Group included in this

Summary of Certain Differences between and SUMMARY OF CERTAIN DIFFERENCES BETWEEN AND The combined financial statements and the pro forma consolidated financial information of our Group included in this

UNCONTROLLED IF PRINTED ACCOUNTING POLICY

UNCONTROLLED IF PRINTED NAVY CANTEENS ACCOUNTING POLICY Applicability: This procedure is applicable to all RANCCB directors and Navy Canteens, managers and staff in all Navy Canteens business units. Legislation:

UNCONTROLLED IF PRINTED NAVY CANTEENS ACCOUNTING POLICY Applicability: This procedure is applicable to all RANCCB directors and Navy Canteens, managers and staff in all Navy Canteens business units. Legislation:

NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS

NAS 21 NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2-14 Identifying a business combination 5-10 Business combinations involving entities under common control

NAS 21 NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2-14 Identifying a business combination 5-10 Business combinations involving entities under common control

Transition to International Financial Reporting Standards (IFRS)

") Transition to International Financial Reporting Standards (IFRS) Contents Page Foreword... 4 IFRS consolidated balance sheet as at January 1, 2004, and December 31, 2004 and IFRS consolidated income statement

Transition to International Financial Reporting Standards (IFRS) Contents Page Foreword... 4 IFRS consolidated balance sheet as at January 1, 2004, and December 31, 2004 and IFRS consolidated income statement

Sri Lanka Accounting Standard for Smaller Enterprises

Sri Lanka Accounting Standard for Smaller Enterprises The Sri Lanka Accounting Standards for Smaller Enterprises (SLASSE) was published in Year 2003. This needs to be revised to be in line with the revisions

Sri Lanka Accounting Standard for Smaller Enterprises The Sri Lanka Accounting Standards for Smaller Enterprises (SLASSE) was published in Year 2003. This needs to be revised to be in line with the revisions

Accounting and reporting by charities EXPOSURE DRAFT

10. Balance sheet Introduction 10.1. All charities preparing accruals accounts must prepare a balance sheet at the end of each reporting period which gives a true and fair view of their financial position.

10. Balance sheet Introduction 10.1. All charities preparing accruals accounts must prepare a balance sheet at the end of each reporting period which gives a true and fair view of their financial position.

Brussels, March 2014 Summary of significant accounting policies

Brussels, March 2014 Summary of significant accounting policies Tessenderlo Chemie NV (hereafter referred to as the "company"), the parent company, is domiciled in Belgium. The consolidated financial statements

Brussels, March 2014 Summary of significant accounting policies Tessenderlo Chemie NV (hereafter referred to as the "company"), the parent company, is domiciled in Belgium. The consolidated financial statements

JGAAP-IFRS comparison. English version 3.0 [equivalent of Japanese version 4.0]

![JGAAP-IFRS comparison. English version 3.0 [equivalent of Japanese version 4.0]](/thumbs/24/3831703.jpg "JGAAP-IFRS comparison. English version 3.0 [equivalent of Japanese version 4.0]") - comparison English version 3.0 [equivalent of Japanese version 4.0] Contents Contents... 2 Introduction... 3 Presentation of Financial Statements, Accounting Policies, Changes in Accounting Estimates

- comparison English version 3.0 [equivalent of Japanese version 4.0] Contents Contents... 2 Introduction... 3 Presentation of Financial Statements, Accounting Policies, Changes in Accounting Estimates

A&W Food Services of Canada Inc. Consolidated Financial Statements December 30, 2012 and January 1, 2012 (in thousands of dollars)

") A&W Food Services of Canada Inc. Consolidated Financial Statements December 30, and January 1, (in thousands of dollars) February 12, 2013 Independent Auditor s Report To the Shareholders of A&W Food Services

A&W Food Services of Canada Inc. Consolidated Financial Statements December 30, and January 1, (in thousands of dollars) February 12, 2013 Independent Auditor s Report To the Shareholders of A&W Food Services

SIGNIFICANT GROUP ACCOUNTING POLICIES

SIGNIFICANT GROUP ACCOUNTING POLICIES Basis of consolidation Subsidiaries Subsidiaries are all entities over which the Group has the sole right to exercise control over the operations and govern the financial

SIGNIFICANT GROUP ACCOUNTING POLICIES Basis of consolidation Subsidiaries Subsidiaries are all entities over which the Group has the sole right to exercise control over the operations and govern the financial

FEDERATED CO-OPERATIVES LIMITED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME year ended October 31, 2012

CONSOLIDATED Financial Statements Federated Co-operatives Limited / OCTOBER 31, 2012 In Millions of CAD $ FEDERATED CO-OPERATIVES LIMITED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME year ended October

CONSOLIDATED Financial Statements Federated Co-operatives Limited / OCTOBER 31, 2012 In Millions of CAD $ FEDERATED CO-OPERATIVES LIMITED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME year ended October

Content. 3 Group Financial Statements. 68 Financial Statements of Schindler Holding Ltd. 86 Compensation Report. 102 Corporate Governance

Each day Schindler moves one billion people. Financial Statements 2013 Content 3 Group Financial Statements 68 Financial Statements of Schindler Holding Ltd. 86 Compensation Report 102 Corporate Governance

Each day Schindler moves one billion people. Financial Statements 2013 Content 3 Group Financial Statements 68 Financial Statements of Schindler Holding Ltd. 86 Compensation Report 102 Corporate Governance

International Accounting Standard 17 Leases

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

Profit/loss attributable to: (w7) Owners of the parent 60 21 Non-controlling interest 11 8 72 01

Owners of the parent 60 21 Non-controlling interest 11 8 72 01") Answers Professional Level Essentials Module, Paper P2 (IRL) Corporate Reporting (Irish) June 2014 Answers 1 (a) (i) Marchant Group: Statement of profit or loss and other comprehensive income for the year

Answers Professional Level Essentials Module, Paper P2 (IRL) Corporate Reporting (Irish) June 2014 Answers 1 (a) (i) Marchant Group: Statement of profit or loss and other comprehensive income for the year

Investments and advances... 313,669

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

G8 Education Limited ABN: 95 123 828 553. Accounting Policies

G8 Education Limited ABN: 95 123 828 553 Accounting Policies Table of Contents Note 1: Summary of significant accounting policies... 3 (a) Basis of preparation... 3 (b) Principles of consolidation... 3

G8 Education Limited ABN: 95 123 828 553 Accounting Policies Table of Contents Note 1: Summary of significant accounting policies... 3 (a) Basis of preparation... 3 (b) Principles of consolidation... 3

IFRS IN PRACTICE. IAS 7 Statement of Cash Flows

IFRS IN PRACTICE IAS 7 Statement of Cash Flows 2 IFRS IN PRACTICE - IAS 7 STATEMENT OF CASH FLOWS TABLE OF CONTENTS 1. Introduction 3 2. Definition of cash and cash equivalents 4 2.1. Demand deposits 4

IFRS IN PRACTICE IAS 7 Statement of Cash Flows 2 IFRS IN PRACTICE - IAS 7 STATEMENT OF CASH FLOWS TABLE OF CONTENTS 1. Introduction 3 2. Definition of cash and cash equivalents 4 2.1. Demand deposits 4

International Accounting Standard 12 Income Taxes. Objective. Scope. Definitions IAS 12

International Accounting Standard 12 Income Taxes Objective The objective of this Standard is to prescribe the accounting treatment for income taxes. The principal issue in accounting for income taxes

International Accounting Standard 12 Income Taxes Objective The objective of this Standard is to prescribe the accounting treatment for income taxes. The principal issue in accounting for income taxes

WIPRO DOHA LLC FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED MARCH 31, 2016

WIPRO DOHA LLC FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED MARCH 31, 2016 WIPRO DOHA LLC BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated) As at March 31, 2016

WIPRO DOHA LLC FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED MARCH 31, 2016 WIPRO DOHA LLC BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated) As at March 31, 2016

Investments in Associates and Joint Ventures

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 28 Investments in Associates and Joint Ventures This standard applies for annual periods beginning on or after 1 January 2013. Earlier application is

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 28 Investments in Associates and Joint Ventures This standard applies for annual periods beginning on or after 1 January 2013. Earlier application is

2 This Standard shall be applied by all entities that are investors with joint control of, or significant influence over, an investee.

International Accounting Standard 28 Investments in Associates and Joint Ventures Objective 1 The objective of this Standard is to prescribe the accounting for investments in associates and to set out

International Accounting Standard 28 Investments in Associates and Joint Ventures Objective 1 The objective of this Standard is to prescribe the accounting for investments in associates and to set out

KOREAN AIR LINES CO., LTD. AND SUBSIDIARIES. Consolidated Financial Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

INGENICO GROUP Consolidated Financial Statements

INGENICO GROUP Consolidated Financial Statements December 31, 2014 Ingenico Consolidated Financial Statements December 31, 2014 I. CONSOLIDATED INCOME STATEMENTS For the years ended December 31, 2014 and

INGENICO GROUP Consolidated Financial Statements December 31, 2014 Ingenico Consolidated Financial Statements December 31, 2014 I. CONSOLIDATED INCOME STATEMENTS For the years ended December 31, 2014 and

[7] Accounting policies

![[7] Accounting policies](/thumbs/39/20265557.jpg "[7] Accounting policies") 121 [7] Accounting policies The Group financial statements have been prepared under the historical cost convention, with the exception of derivative financial instruments, available-for-sale financial

121 [7] Accounting policies The Group financial statements have been prepared under the historical cost convention, with the exception of derivative financial instruments, available-for-sale financial

Principal Accounting Policies

1. Basis of Preparation The accounts have been prepared in accordance with Hong Kong Financial Reporting Standards ( HKFRS ). The accounts have been prepared under the historical cost convention as modified

1. Basis of Preparation The accounts have been prepared in accordance with Hong Kong Financial Reporting Standards ( HKFRS ). The accounts have been prepared under the historical cost convention as modified

Indian Accounting Standard (Ind AS) 12. Income Taxes

12. Income Taxes") Indian Accounting Standard (Ind AS) 12 Contents Income Taxes Paragraphs Objective Scope 1 4 Definitions 5 11 Tax base 7 11 Recognition of current tax liabilities and current tax assets 12 14 Recognition

Indian Accounting Standard (Ind AS) 12 Contents Income Taxes Paragraphs Objective Scope 1 4 Definitions 5 11 Tax base 7 11 Recognition of current tax liabilities and current tax assets 12 14 Recognition

Sri Lanka Accounting Standard LKAS 17. Leases

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 3 DEFINITIONS 4 6 CLASSIFICATION OF LEASES 7 19 LEASES IN THE FINANCIAL

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 3 DEFINITIONS 4 6 CLASSIFICATION OF LEASES 7 19 LEASES IN THE FINANCIAL

Investments and advances... 344,499

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

The only way is forward

Neste Oil in 2014 The only way is forward Financial statements 2 FINANCIAL STATEMENTS 3 Key financial indicators 3 Calculation of key financial indicators 4 Consolidated financial statements 6 Consolidated

Neste Oil in 2014 The only way is forward Financial statements 2 FINANCIAL STATEMENTS 3 Key financial indicators 3 Calculation of key financial indicators 4 Consolidated financial statements 6 Consolidated

Sri Lanka Accounting Standard LKAS 12. Income Taxes

Sri Lanka Accounting Standard LKAS 12 Income Taxes CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD-LKAS 12 INCOME TAXES OBJECTIVE SCOPE 1 4 DEFINITIONS 5 11 Tax base 7 11 RECOGNITION OF CURRENT TAX LIABILITIES

Sri Lanka Accounting Standard LKAS 12 Income Taxes CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD-LKAS 12 INCOME TAXES OBJECTIVE SCOPE 1 4 DEFINITIONS 5 11 Tax base 7 11 RECOGNITION OF CURRENT TAX LIABILITIES

Shin Kong Investment Trust Co., Ltd. Financial Statements for the Years Ended December 31, 2014 and 2013 and Independent Auditors Report

Shin Kong Investment Trust Co., Ltd. Financial Statements for the Years Ended, 2014 and 2013 and Independent Auditors Report INDEPENDENT AUDITORS REPORT The Board of Directors and stockholder Shin Kong

Shin Kong Investment Trust Co., Ltd. Financial Statements for the Years Ended, 2014 and 2013 and Independent Auditors Report INDEPENDENT AUDITORS REPORT The Board of Directors and stockholder Shin Kong

POLICY MANUAL. Financial Management Significant Accounting Policies (July 2015)

") POLICY 1. Objective To adopt Full Accrual Accounting and all other applicable Accounting Standards. 2. Local Government Reference Local Government Act 1995 Local Government (Financial Management) Regulations

POLICY 1. Objective To adopt Full Accrual Accounting and all other applicable Accounting Standards. 2. Local Government Reference Local Government Act 1995 Local Government (Financial Management) Regulations

Statutory Financial Reporting Policy

Statutory Financial Reporting Policy Reference Number: 3.15 12/270185 Type: Council Category: Corporate Services Relevant Community Plan Outcome: Demonstrate effective leadership with strong community

Statutory Financial Reporting Policy Reference Number: 3.15 12/270185 Type: Council Category: Corporate Services Relevant Community Plan Outcome: Demonstrate effective leadership with strong community

Area Standard AIFRS impact Management action First time Adoption of Australian Equivalents to IFRS

First time Adoption of Australian Equivalents to IFRS AASB 1 An entity s first Australian-equivalents-to-IFRS (AIFRS) financial report applies for reporting periods beginning on or after 1 January 2005

First time Adoption of Australian Equivalents to IFRS AASB 1 An entity s first Australian-equivalents-to-IFRS (AIFRS) financial report applies for reporting periods beginning on or after 1 January 2005

HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2013

HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2013 HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED BALANCE SHEETS ASSETS

HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2013 HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED BALANCE SHEETS ASSETS

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES (Issued April 1999) The standards, which have been set in bold italic type, should be read in the context of

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES (Issued April 1999) The standards, which have been set in bold italic type, should be read in the context of

ACCOUNTING POLICIES. for the year ended 30 June 2014

ACCOUNTING POLICIES REPORTING ENTITIES City Lodge Hotels Limited (the company) is a company domiciled in South Africa. The group financial statements of the company as at and comprise the company and its

ACCOUNTING POLICIES REPORTING ENTITIES City Lodge Hotels Limited (the company) is a company domiciled in South Africa. The group financial statements of the company as at and comprise the company and its

Consolidated Financial Statements

Consolidated Financial Statements For the year ended February 20, 2016 Nitori Holdings Co., Ltd. Consolidated Balance Sheet Nitori Holdings Co., Ltd. and consolidated subsidiaries As at February 20, 2016

Consolidated Financial Statements For the year ended February 20, 2016 Nitori Holdings Co., Ltd. Consolidated Balance Sheet Nitori Holdings Co., Ltd. and consolidated subsidiaries As at February 20, 2016

INTERNATIONAL ACCOUNTING STANDARDS. CIE Guidance for teachers of. 7110 Principles of Accounts and. 0452 Accounting

www.xtremepapers.com INTERNATIONAL ACCOUNTING STANDARDS CIE Guidance for teachers of 7110 Principles of Accounts and 0452 Accounting 1 CONTENTS Introduction...3 Use of this document... 3 Users of financial

www.xtremepapers.com INTERNATIONAL ACCOUNTING STANDARDS CIE Guidance for teachers of 7110 Principles of Accounts and 0452 Accounting 1 CONTENTS Introduction...3 Use of this document... 3 Users of financial

The consolidated financial statements of

Our 2014 financial statements The consolidated financial statements of plc and its subsidiaries (the Group) for the year ended 31 December 2014 have been prepared in accordance with International Financial

Our 2014 financial statements The consolidated financial statements of plc and its subsidiaries (the Group) for the year ended 31 December 2014 have been prepared in accordance with International Financial

In addition, Outokumpu has adopted the following amended standards as of January 1, 2009:

1. Corporate information Outokumpu Oyj is a Finnish public limited liability company organised under the laws of Finland and domiciled in Espoo. The parent company, Outokumpu Oyj, has been listed on the

1. Corporate information Outokumpu Oyj is a Finnish public limited liability company organised under the laws of Finland and domiciled in Espoo. The parent company, Outokumpu Oyj, has been listed on the

Significant Accounting Policies

Apart from the accounting policies presented within the corresponding notes to the financial statements, other significant accounting policies are set out below. These policies have been consistently applied

Apart from the accounting policies presented within the corresponding notes to the financial statements, other significant accounting policies are set out below. These policies have been consistently applied

ANNUAL FINANCIAL RESULTS

ANNUAL FINANCIAL RESULTS Directors Statement The directors of Air New Zealand Limited are pleased to present to shareholders the Annual Report* and financial statements for Air New Zealand and its controlled

ANNUAL FINANCIAL RESULTS Directors Statement The directors of Air New Zealand Limited are pleased to present to shareholders the Annual Report* and financial statements for Air New Zealand and its controlled

Condensed Consolidated Statement of Operations and Comprehensive Income (Loss) 3. Condensed Consolidated Balance Sheet 4

3. Condensed Consolidated Balance Sheet 4") CONSOLIDATED FINANCIAL STATEMENTS For the fiscal year ended March 31, 2014 INDEX Page Condensed Consolidated Statement of Operations and Comprehensive Income (Loss) 3 Condensed Consolidated Balance Sheet

CONSOLIDATED FINANCIAL STATEMENTS For the fiscal year ended March 31, 2014 INDEX Page Condensed Consolidated Statement of Operations and Comprehensive Income (Loss) 3 Condensed Consolidated Balance Sheet

Assuming office supplies are charged to the Office Supplies inventory account when purchased:

Adjusting Entries Prepaid Expenses Second Bullet Example - Assuming office supplies are charged to the Office Supplies inventory account when purchased: Office supplies expense 7,800 Office supplies 7,800

Adjusting Entries Prepaid Expenses Second Bullet Example - Assuming office supplies are charged to the Office Supplies inventory account when purchased: Office supplies expense 7,800 Office supplies 7,800

IFrS. Disclosure checklist. July 2011. kpmg.com/ifrs

IFrS Disclosure checklist July 2011 kpmg.com/ifrs Contents What s new? 1 1. General presentation 2 1.1 Presentation of financial statements 2 1.2 Changes in equity 12 1.3 Statement of cash flows 13 1.4

IFrS Disclosure checklist July 2011 kpmg.com/ifrs Contents What s new? 1 1. General presentation 2 1.1 Presentation of financial statements 2 1.2 Changes in equity 12 1.3 Statement of cash flows 13 1.4

Notes to the Consolidated Financial Statements

Notes to the Consolidated Financial Statements Basic information Vaisala is a global leader in environmental and industrial measurement. Building on over 75 years of experience, Vaisala contributes to

Notes to the Consolidated Financial Statements Basic information Vaisala is a global leader in environmental and industrial measurement. Building on over 75 years of experience, Vaisala contributes to

Consolidated Financial Statements Notes to the Consolidated Financial Statements for Fiscal Year 2014

171 The most important exchange rates applied in the consolidated financial statements developed as follows in relation to the euro: Currency Average rate Closing rate Country 1 EUR = 2014 2013 2014 2013

171 The most important exchange rates applied in the consolidated financial statements developed as follows in relation to the euro: Currency Average rate Closing rate Country 1 EUR = 2014 2013 2014 2013

NAS 09 NEPAL ACCOUNTING STANDARDS ON INCOME TAXES

NAS 09 NEPAL ACCOUNTING STANDARDS ON INCOME TAXES CONTENTS Paragraphs OBJECTIVE SCOPE 1-4 DEFINITIONS 5-11 Tax Base 7-11 RECOGNITION OF CURRENT TAX LIABILITIES AND CURRENT TAX ASSETS 12-14 RECOGNITION

NAS 09 NEPAL ACCOUNTING STANDARDS ON INCOME TAXES CONTENTS Paragraphs OBJECTIVE SCOPE 1-4 DEFINITIONS 5-11 Tax Base 7-11 RECOGNITION OF CURRENT TAX LIABILITIES AND CURRENT TAX ASSETS 12-14 RECOGNITION

Profit/loss attributable to: (w7) Owners of the parent 60 21 Non-controlling interest 11 8 72 01

Owners of the parent 60 21 Non-controlling interest 11 8 72 01") Answers Professional Level Essentials Module, Paper P2 (SGP) Corporate Reporting (Singapore) June 2014 Answers 1 (a) (i) Marchant Group: Statement of profit or loss and other comprehensive income for the

Answers Professional Level Essentials Module, Paper P2 (SGP) Corporate Reporting (Singapore) June 2014 Answers 1 (a) (i) Marchant Group: Statement of profit or loss and other comprehensive income for the

Consolidated Extended Financial Statements of Echo Investment Capital Group for the 1st half of 2009

SEMI-ANNUAL REPORT 2009 Consolidated Extended Financial Statements of Echo Investment Capital Group for the 1st half of 2009 August 31, 2009 Semi-annual Report for the 1st half of 2009 1 I. Consolidated

SEMI-ANNUAL REPORT 2009 Consolidated Extended Financial Statements of Echo Investment Capital Group for the 1st half of 2009 August 31, 2009 Semi-annual Report for the 1st half of 2009 1 I. Consolidated

NOTES TO THE FINANCIAL STATEMENTS

NOTES TO THE FINANCIAL STATEMENTS 1 SIGNIFICANT ACCOUNTING POLICIES (a) Statement of compliance These financial statements have been prepared in accordance with all applicable Hong Kong Financial Reporting

NOTES TO THE FINANCIAL STATEMENTS 1 SIGNIFICANT ACCOUNTING POLICIES (a) Statement of compliance These financial statements have been prepared in accordance with all applicable Hong Kong Financial Reporting

Abbey plc ( Abbey or the Company ) Interim Statement for the six months ended 31 October 2007

Interim Statement for the six months ended 31 October 2007") Abbey plc ( Abbey or the Company ) Interim Statement for the six months ended 31 October 2007 The Board of Abbey plc reports a profit before taxation of 18.20m which compares with a profit of 22.57m for

Abbey plc ( Abbey or the Company ) Interim Statement for the six months ended 31 October 2007 The Board of Abbey plc reports a profit before taxation of 18.20m which compares with a profit of 22.57m for

ANNUAL FINANCIAL RESULTS FOR THE YEAR ENDED 31 JULY 2014 FONTERRA ANNUAL FINANCIAL RESULTS 2014 A

ANNUAL FINANCIAL RESULTS FOR THE YEAR ENDED 31 JULY 2014 FONTERRA ANNUAL FINANCIAL RESULTS 2014 A CONTENTS DIRECTORS STATEMENT 1 INCOME STATEMENT 2 STATEMENT OF COMPREHENSIVE INCOME 3 STATEMENT OF FINANCIAL

ANNUAL FINANCIAL RESULTS FOR THE YEAR ENDED 31 JULY 2014 FONTERRA ANNUAL FINANCIAL RESULTS 2014 A CONTENTS DIRECTORS STATEMENT 1 INCOME STATEMENT 2 STATEMENT OF COMPREHENSIVE INCOME 3 STATEMENT OF FINANCIAL

VASSETI (UK) PLC CONSOLIDATED FINANCIAL STATEMENTS FOR THE SIX MONTHS ENDED 30 JUNE 2013

PLC CONSOLIDATED FINANCIAL STATEMENTS FOR THE SIX MONTHS ENDED 30 JUNE 2013") CONSOLIDATED FINANCIAL STATEMENTS FOR THE SIX MONTHS ENDED 30 JUNE 2013 INTERIM MANAGEMENT REPORT (UNAUDITED) FOR THE 6 MONTHS ENDED 30 JUNE 2013 1. Key Risks and uncertainties Risks and uncertainties

CONSOLIDATED FINANCIAL STATEMENTS FOR THE SIX MONTHS ENDED 30 JUNE 2013 INTERIM MANAGEMENT REPORT (UNAUDITED) FOR THE 6 MONTHS ENDED 30 JUNE 2013 1. Key Risks and uncertainties Risks and uncertainties

Canadian GAAP - IFRS Comparison Series Issue 8 Leases

- Comparison Series Issue 8 Leases Both and are principle-based frameworks and, from a conceptual standpoint, many of the general principles are the same. However, the application of those general principles

- Comparison Series Issue 8 Leases Both and are principle-based frameworks and, from a conceptual standpoint, many of the general principles are the same. However, the application of those general principles

Financial Statements 2014

Financial Statements 2014 This financial statement is part of Heijmans annual report 2014. The complete English version of the annual report will be published a number of weeks after the publication of

Financial Statements 2014 This financial statement is part of Heijmans annual report 2014. The complete English version of the annual report will be published a number of weeks after the publication of

Tax implications on application of New UK GAAP, FRS 101. FRS 101 Overview Paper. Tax implications

FRS 101 Overview Paper Tax implications Date of publication: 22 January 2014 Contents INTRODUCTION 1 BACKGROUND 2 Summary of the changes to the accounting standards 2 Interaction of these changes with

FRS 101 Overview Paper Tax implications Date of publication: 22 January 2014 Contents INTRODUCTION 1 BACKGROUND 2 Summary of the changes to the accounting standards 2 Interaction of these changes with

ANNUAL FINANCIAL RESULTS

ANNUAL FINANCIAL RESULTS For the year ended 31 July 2013 ANNUAL FINANCIAL RESULTS 2013 FONTERRA CO-OPERATIVE GROUP LIMITED Contents: DIRECTORS STATEMENT... 1 INCOME STATEMENT... 2 STATEMENT OF COMPREHENSIVE

ANNUAL FINANCIAL RESULTS For the year ended 31 July 2013 ANNUAL FINANCIAL RESULTS 2013 FONTERRA CO-OPERATIVE GROUP LIMITED Contents: DIRECTORS STATEMENT... 1 INCOME STATEMENT... 2 STATEMENT OF COMPREHENSIVE

ABN 17 006 852 820 PTY LTD (FORMERLY KNOWN AS AQUAMAX PTY LTD) DIRECTORS REPORT FOR THE YEAR ENDED 30 SEPTEMBER 2015

DIRECTORS REPORT FOR THE YEAR ENDED 30 SEPTEMBER 2015") DIRECTORS REPORT FOR THE YEAR ENDED 30 SEPTEMBER 2015 In accordance with a resolution of the Directors dated 16 December 2015, the Directors of the Company have pleasure in reporting on the Company for

DIRECTORS REPORT FOR THE YEAR ENDED 30 SEPTEMBER 2015 In accordance with a resolution of the Directors dated 16 December 2015, the Directors of the Company have pleasure in reporting on the Company for

PKF International Limited administers a network of legally independent member firms which carry on separate businesses under the PKF Name.

IFRS Summary 2010 PKF International Limited administers a network of legally independent member firms which carry on separate businesses under the PKF Name. PKF International Limited is not responsible

IFRS Summary 2010 PKF International Limited administers a network of legally independent member firms which carry on separate businesses under the PKF Name. PKF International Limited is not responsible

Illustrative Financial Statements Prepared Using the Financial Reporting Framework for Small- and Medium-Entities

Illustrative Financial Statements Prepared Using the Financial Reporting Framework for Small- and Medium-Entities Illustrative Financial Statements This component of the toolkit contains sample financial

Illustrative Financial Statements Prepared Using the Financial Reporting Framework for Small- and Medium-Entities Illustrative Financial Statements This component of the toolkit contains sample financial

Accounting Standard AASB 1020 December 1999. Income Taxes. Issued by the Australian Accounting Standards Board

Accounting Standard AASB 1020 December 1999 Income Taxes Issued by the Australian Accounting Standards Board Obtaining a Copy of this Accounting Standard Copies of this Standard are available for purchase

Accounting Standard AASB 1020 December 1999 Income Taxes Issued by the Australian Accounting Standards Board Obtaining a Copy of this Accounting Standard Copies of this Standard are available for purchase

The statements are presented in pounds sterling and have been prepared under IFRS using the historical cost convention.

Note 1 to the financial information Basis of accounting ITE Group Plc is a UK listed company and together with its subsidiary operations is hereafter referred to as the Company. The Company is required

Note 1 to the financial information Basis of accounting ITE Group Plc is a UK listed company and together with its subsidiary operations is hereafter referred to as the Company. The Company is required

International Accounting Standard 1 Presentation of Financial Statements

IAS 1 Presentation of Financial Statements International Accounting Standard 1 Presentation of Financial Statements Objective 1 This Standard prescribes the basis for presentation of general purpose financial

IAS 1 Presentation of Financial Statements International Accounting Standard 1 Presentation of Financial Statements Objective 1 This Standard prescribes the basis for presentation of general purpose financial

EKO FAKTORİNG A.Ş. FINANCIAL STATEMENTS AT 31 DECEMBER 2013 TOGETHER WITH INDEPENDENT AUDITOR S REPORT

FINANCIAL STATEMENTS TOGETHER WITH INDEPENDENT AUDITOR S REPORT FINANCIAL STATEMENTS CONTENTS PAGES BALANCE SHEET (STATEMENT OF FINANCIAL POSITION)... 1 STATEMENT OF COMPREHENSIVE INCOME... 2 STATEMENT

FINANCIAL STATEMENTS TOGETHER WITH INDEPENDENT AUDITOR S REPORT FINANCIAL STATEMENTS CONTENTS PAGES BALANCE SHEET (STATEMENT OF FINANCIAL POSITION)... 1 STATEMENT OF COMPREHENSIVE INCOME... 2 STATEMENT

International Accounting Standard 12 Income Taxes

EC staff consolidated version as of 21 June 2012, EN IAS 12 FOR INFORMATION PURPOSES ONLY International Accounting Standard 12 Income Taxes Objective The objective of this Standard is to prescribe the

EC staff consolidated version as of 21 June 2012, EN IAS 12 FOR INFORMATION PURPOSES ONLY International Accounting Standard 12 Income Taxes Objective The objective of this Standard is to prescribe the

Summary of significant accounting policies

1 (14) Summary of significant accounting policies The principal accounting policies applied in the preparation of Neste's consolidated financial statements are set out below. These policies have been consistently

1 (14) Summary of significant accounting policies The principal accounting policies applied in the preparation of Neste's consolidated financial statements are set out below. These policies have been consistently

ASPE at a Glance. Standards Included in Topic

ASPE AT A GLANCE ASPE AT A GLANCE This publication has been compiled to assist users in gaining a high level overview of Accounting Standards for Private Enterprises (ASPE) included in Part II of the CPA

ASPE AT A GLANCE ASPE AT A GLANCE This publication has been compiled to assist users in gaining a high level overview of Accounting Standards for Private Enterprises (ASPE) included in Part II of the CPA

NOTES TO THE COMPANY FINANCIAL STATEMENTS

FINANCIAL S 78 79 80 81 82 CONSOLIDATED INCOME CONSOLIDATED OF COMPREHENSIVE INCOME CONSOLIDATED OF FINANCIAL POSITION CONSOLIDATED OF CONSOLIDATED OF CHANGES IN EQUITY 83 NOTES TO THE CONSOLIDATED FINANCIAL

FINANCIAL S 78 79 80 81 82 CONSOLIDATED INCOME CONSOLIDATED OF COMPREHENSIVE INCOME CONSOLIDATED OF FINANCIAL POSITION CONSOLIDATED OF CONSOLIDATED OF CHANGES IN EQUITY 83 NOTES TO THE CONSOLIDATED FINANCIAL

International Accounting Standard 7 Statement of cash flows *

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

Sri Lanka Accounting Standard -LKAS 40. Investment Property

Sri Lanka Accounting Standard -LKAS 40 Investment Property -1088- 85-1089- 4 This Standard does not apply to: biological assets related to agricultural activity (seelkas 41 Agriculture); and mineral rights

Sri Lanka Accounting Standard -LKAS 40 Investment Property -1088- 85-1089- 4 This Standard does not apply to: biological assets related to agricultural activity (seelkas 41 Agriculture); and mineral rights

PART III. Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Independent Auditors Report 47

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March