Student loans and homeownership

|

|

|

- Thomasina Tate

- 8 years ago

- Views:

Transcription

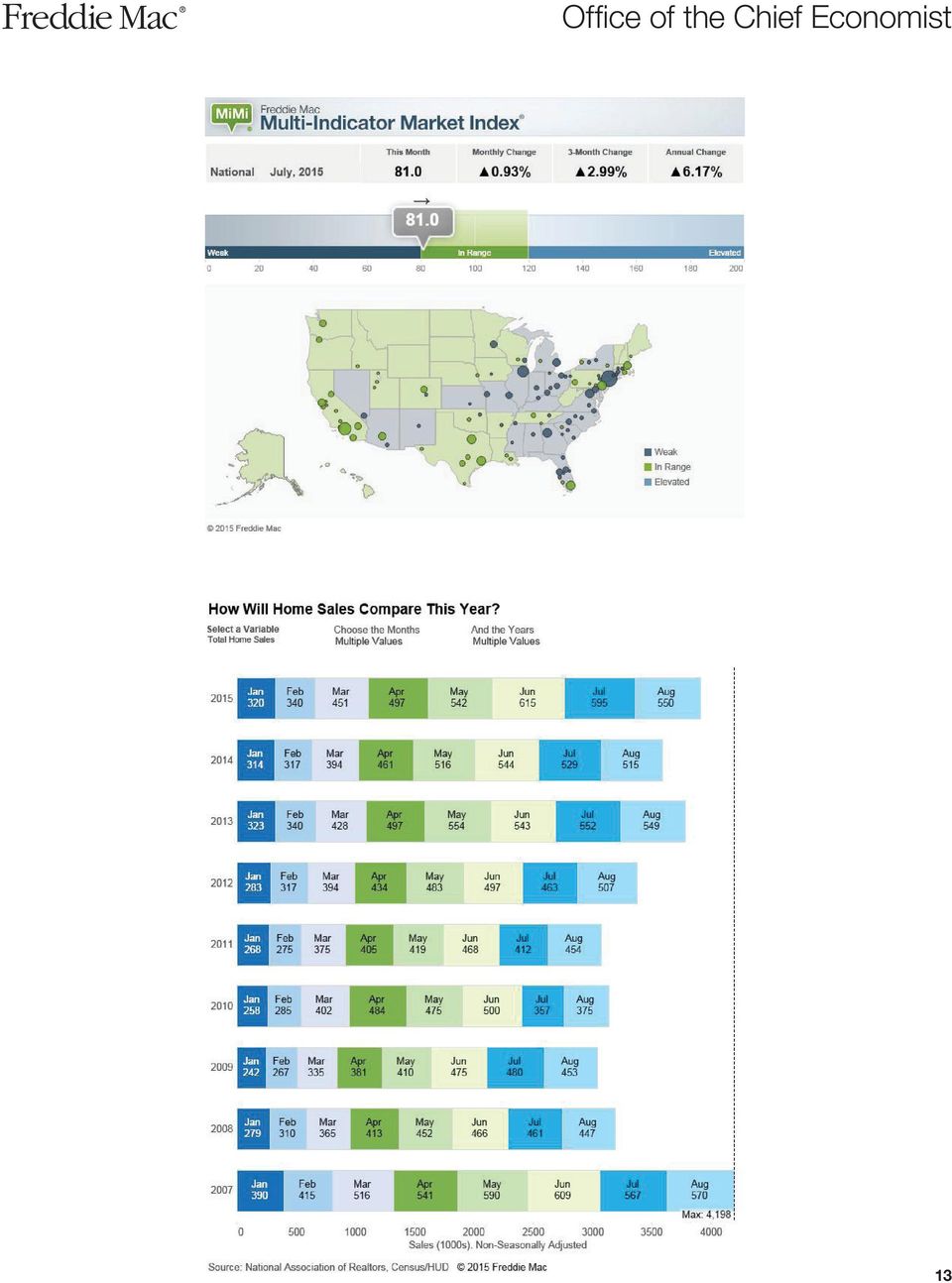

1 Insight & Outlook September 30, 2015 In this Edition: Insight: Student loans and homeownership (P. 1) Outlook: A tale of two economies (P. 7) Housing Snapshot: A selection of key indicators (P. 11) In Closing: In Closing: What were they thinking? (P. 14) Forecast Summary Real GDP Growth (%) Year Fixed Mtg. Rate (%) FMHPI House Price Appreciation (%) 1-4 Family Mortgage Originations ($ Billions) ,530 1,400 Student loans and homeownership Many housing experts expected the homeownership rate which has been declining since 2004 to rebound as Millennials entered the housing market. Instead, the homeownership rate has continued to decline. Even the homeownership rate for the under-35-year-old segment of the market has declined (Exhibit 1). Exhibit 1: Causation or Coincidence? Many theories have been advanced for the slower-than-average entry into homeownership of Millennials. Some analysts argue that the financial crisis reduced employment opportunities just as Millennials entered the labor force, delaying and perhaps permanently reducing the career development and financial accumulation of this 1

2 cohort. Other analysts have relied on sociological theories, arguing that Millennials have different attitudes towards marriage, family, and renting than prior generations. One tempting potential explanation is the rapid growth of student loan debt in recent years. College attendance often increases during recessions, as limited job opportunities reduce the opportunity cost of education. During the Great Recession, many high school graduates who might not otherwise have gone to college decided to invest in a college education in hopes of enjoying higher wages once the recession ended. Similarly, some college graduates, failing to find adequate employment, went back for a graduate degree (with the added benefit of deferring repayment of the student loans from their undergraduate years). These decisions generated explosive growth in student debt during the Great Recession. The overhang of this debt may be making it harder for Millennials to accumulate down payments and to qualify for a mortgage. In addition, many students have been disappointed in the types of jobs and wages available to them post-college. At least in some cases, the expected returns on investment in education have failed to materialize. Finally, student loans have exhibited high delinquency and default rates, damaging the credit scores of many borrowers, thus raising an additional hurdle to homeownership for these borrowers. Are the simultaneous growth in student loan debt and the decline in the Millennial homeownership rate just a coincidence, or is the burden of student debt a significant factor in the lower homeownership rates? While we can t answer that question definitively, there are some tantalizing clues in the data. The recent history of student loan debt A little over a decade ago in the fourth quarter of 2004, aggregate student loan debt stood at $346 billion dollars less than home equity lending, credit card debt, and auto loans (Exhibit 2). Exhibit 2: Non-Mortgage Balances At the onset of the Great Recession, outstanding home equity debt, credit card debt, and auto loans declined, and only auto loans have returned to pre-recession levels. In contrast, student debt tripled over ten years, reaching 2

3 $1.2 trillion in the fourth quarter of While aggregate student debt expanded for all age groups, the balances were concentrated among those under 30 years old and those between 30 and 39 years old (Exhibit 3). Exhibit 3: Total student loan balances by age group The distribution of student loan debt is very uneven (Exhibit 4). Many households have no student loan debt, and among those households with student loan debt many have very little. For others the debt burden is significant. At the end of 2014, over half of those with student debt had outstanding balances greater than $10,000. Nearly two million borrowers owed more than $100,000. Exhibit 4: Distribution of student loan borrowers by 2014Q4 balance 1 Federal Reserve Bank of New York, Consumer Credit Panel: 3

4 Student loans exhibit extraordinarily high rates of delinquency and default, and credit performance has gotten worse in recent years default rates doubled between 2000 and This poor credit performance has led to frequent headlines about the student debt crisis (Exhibit 5). In June of this year, Moody s and Fitch put several securitized student loan issues on watch for ratings downgrades, citing signs of continued poor credit performance. 3 Poor performance on student loan repayment will affect a borrower s credit score and make it more difficult to qualify for a home mortgage. Exhibit 5 Impact of student loan debt on homeownership College graduates historically have enjoyed higher incomes than those who did not graduate from college. For instance, the University of California, Berkeley web site states that a Berkeley education earns our graduates an additional $26,333 each year in income over those who did not go to college. 4 These higher incomes typically support a higher rate of homeownership. And prior to the Great Recession, the associated student loans did not appear to depress the homeownership rate. Before the crisis, homeownership rates of 27-to-30-year-olds with student loans (evidence of at least some college education) were 2 to 3 percent higher than homeownership rates of those with no student loans (Exhibit 6). That gap began to close during the recession and reversed in By 2014 the homeownership rate of student loan borrowers was about one percentage point lower than the rate of non-borrowers. 2 Brookings conference paper by Looney and Yannelis. 3 Interestingly the loans backing the securities in question are guaranteed by the Federal government for a minimum 97 percent of defaulted principal and accrued interest. However, the combination of policies for deferring payments can extend the repayment of the original 10-year loans to as much as 25 years, significantly affecting the yield earned by investors in the securities

5 Exhibit 6: Proportion with home-secured debt at age 30 Note that student loan debt alone can t explain the low homeownership rate among Millennials. After all, the homeownership rate in this cohort has dropped 5 to 6 percentage points for student loan borrowers and nonborrowers alike. Others have questioned the current impact of student loan debt on homeownership. A recent report by Zillow notes that student loan debt has only a small impact on the probability of homeownership for those who completed their degree. 5 For instance, a couple in their early 30s with no student loan debt and at least one bachelor s degree between them have a 70 percent chance of owning a home. A couple with $30,000 in student debt and at least one bachelor s degree have a 68 percent chance. A recent Brookings Institution conference paper by Adam Looney of the U.S. Treasury and Constantine Yannelis of Stanford University helps make sense of these conflicting signals. Using recently released data from the Department of Education, they found that most of the increase in student loan defaults is associated with the rise in the number of borrowers at for-profit schools and, to a lesser-extent, two-year colleges, and certain other non-selective schools. In contrast, default rates have remained low among borrowers attending four-year public and non-profit private colleges. This also holds true for most graduate borrowers despite the recession and relatively high loan balances. This low-default-rate group comprises the vast majority of the federal student loan portfolio (Exhibit 7). Exhibit 7 5-Year Cohort Default Rates All For Profit 2-Year Non- Selective Some Selective Selective Grad % 47% 38% 27% 18% 10% 5% 5 5

6 These patterns of credit performance align with the homeownership patterns highlighted by Zillow. The probability of home ownership is associated with the type of degree (Exhibit 8). Advanced and professional degree holders have a greater than 65 percent chance of owning a home. Those with no degree have a probability of home ownership less than half that. Zillow also found that higher student loan debt balances reduced the probability of homeownership, especially for those who did not complete their studies. The Zillow report noted that accumulating a down payment remains a challenge for first-time home buyers, even those with advanced degrees. Exhibit 8: Homeownership rate by degree Implications for mortgage lending These findings suggest that it may be useful to think of student loan borrowers as being divided into three groups: Successful investors: Borrowers who completed their degrees and found that their post-college earnings are matching their expectations. Unless they are challenged to accumulate a down payment, student loan debt is not a significant deterrent to purchasing their first home. However, they may be delaying for other reasons; Disappointed earners: Graduates of four-year institutions whose return on their education investment is lessthan-expected. They may not be able to find a job in their field and their wage income is lower than originally anticipated. Some of these borrowers took highly-specialized instruction in fields that deteriorated during their period of studies (for example, petroleum engineers graduating now). Their relatively low earnings and student debt burden may hinder homeownership for this group. At-risk borrowers: These are the borrowers identified by Looney and Yannelis in their analysis of the Department of Education data. Many of these borrowers are from less affluent groups. They may be economically worse off than before they started school they have no improvement in their job prospects but they have significant student debts to repay. Delinquency and default on their student loans has hurt their credit scores. This last group is a particular focus for Freddie Mac s efforts to support prudent, affordable lending to low-andmoderate income borrowers. The impact on credit scores of poor repayment performance may make it particularly difficult to assist some members of this group. For the Disappointed Earners and even some of the Successful Investors Freddie Mac s Home Possible Advantage SM program, with its option to pay as little as 3 percent down, may provide help in purchasing that first home. 6

7 A change just this month in Federal Housing Administration (FHA) policy will make it more difficult for some student loan borrowers to qualify for a mortgage. In the past, FHA did not take student debt into account in qualifying a borrower if the debt payments had been temporarily deferred for at least 12 months (a common practice). This policy may have been too generous; Freddie Mac takes a percentage of the debt into account when calculating an applicant s monthly debt-to-income (DTI) ratio. However, FHA s new policy uses a percentage that is twice as large as Freddie Mac s. Conclusion The low homeownership rate among Millennials is still something of a puzzle it cannot be explained solely by the increase in student loan debt. However student debt plays a role higher balances are associated with a lower probability of homeownership at every level of college and graduate education. And recent data has confirmed that student borrowers are not alike. Students who attended schools with less-certain educational benefits have not fared well. Borrowers who did not complete their studies have fared worst of all. These groups are likely to continue to affect the pattern of homeownership among Millennials. Outlook: A tale of two economies The macroeconomic engine has not kicked into gear yet, and the Fed s recent decision to defer increasing short-term interest rates suggests they share this view. At the same time, the housing market is on the way to having its best year since the recovery began. Keep in mind though that the housing sector is coming back from rock bottom and housing activity remains weak compared to historical norms. Macroeconomy Fed watchers must feel they are watching a revival of Waiting for Godot. Approaching every meeting of the Federal Open Market Committee (FOMC), the market braces itself for a Fed tightening, only to watch the FOMC delay any action for at least one more meeting. Freddie Mac s support for student housing The cost of student housing comprises a significant component of the overall cost of attending college. The University of California at Berkeley publishes estimates of the all-in cost of attendance to help students prepare for the financial burden of attending Cal. For the academic year, the tuition for an in-state resident is $13,432. Cal estimates the cost of living in a campus residence hall (room and board) at $14,388 almost a thousand dollars more than tuition and over 40 percent of the total estimated cost of attendance. Most people are aware of Freddie Mac s support for affordable workforce rental housing. However many are unaware that Freddie Mac also provides financing for student housing through its multifamily division. So far in 2015, Freddie Mac has funded over $1.5 billion in loans for student housing providing over 30,000 units at colleges and universities across the country. Student housing is a growing sector of the multifamily market. Freddie Mac s participation in this sector plays a role in making college affordable for more students. 7

8 For some time, the Fed has been signaling they will increase the Federal funds rate just as soon as the data persuade the FOMC that labor markets have recovered and inflation is reliably expected to be at or above 2 percent. The unemployment rate dipped to 5.1 percent in August, a level that many consider consistent with full employment. We remain cautious on this front a sharp decline in labor force participation accounts for essentially all the improvement in the unemployment rate since the end of the recession. Moreover, wage growth has been disappointing in this expansion. In contrast, the inflation rate has not yet reached the Fed s 2 percent threshold. Arguably part of the shortfall can be attributed to the collapse in energy prices and the strengthening of the dollar. Fed comments at the Jackson Hole conference in August suggested the FOMC is looking beyond these transitory influences. However, according to the recent Atlanta Fed Business Inflation Expectations survey, firms have lowered their inflation projections for the coming 12 months, from 1.8 to 1.7 percent. This mixed bag of economic indicators has left the FOMC divided. It is likely, however, that the recent turbulence emanating from China tipped the balance at the September meeting of the FOMC. In the absence of a clear economic signal, the Fed may have wanted to avoid adding any additional volatility to already skittish financial markets. Housing: Best year in home sales since 2007, but The Good At the current pace, home sales this year are expected to be the highest since Existing home sales in August fell a little short of expectations, but the inventory of existing homes for sale remained below the 6 month mark. The faster-than-expected decline in the unemployment rate is boosting demand for homes. A more significant contributor is likely the continued low level of mortgage rates, which has kept affordability high despite impressive gains in house prices. The interest rate on 30-year fixed rate mortgages averaged 3.90 percent in August, and the rate on 15-year fixed rate mortgages averaged 3.12 percent. Mortgage rates have remained relatively stable in recent weeks despite the wide swings in the stock market (Exhibit 9). Exhibit 9: Total Home Sales 8

9 Increased credit availability is another factor supporting the demand for housing. The Mortgage Credit Availability Index (MCAI) published by the Mortgage Bankers Association increased 0.5 percent in August on top of a larger increase in July. Lastly, foreign demand for housing in the US remains strong. According to the National Association of Realtors 2015 Profile of International Home Buying Activity, from April 2014 through March 2015, total international home sales were about $104 billion and represented 8 percent of existing home sales. The Not So Good Housing remains relatively affordable in most of the country. However, at some point soon, the economic outlook will firm up enough for the Fed to begin raising short-term interest rates. Any increase in mortgage rates in response to the Fed tightening will chip away at affordability. As a rough rule of thumb, a quarter-point increase in mortgage rates is the financial equivalent of increasing house prices by 3 percent. For example, an increase in the 30-year mortgage rate from 4 to 5 percent has the same impact on affordability as increasing the price of a house from $200,000 to $225,000. Forecast Updates Economy: Our view on the near-term trajectory of the macroeconomy is largely unchanged from last month. While interest rates are expected to rise more slowly than we projected last month (see below), the effect on the general economy will be muted. Our economic growth and unemployment projections are largely unchanged from last month. Our outlook for inflation remains subdued, largely due to the lingering effects of declining oil prices. We expect inflation to rise gradually to a long-term average of about 2 percent. Based on the Fed s decision last week to defer an increase in the Federal funds rate, we lowered our 2015 and 2016 interest rate forecasts by 0.1 percent for both the 10-year constant maturity Treasury (CMT) and the 30-year fixed rate mortgage (FRM). The 10-year CMT forecasts for 2015 and 2016 are 2.2 percent and 2.9 percent, respectively. The 30-year FRM forecasts for 2015 and 2016 are 3.9 percent and 4.8 percent respectively. In light of the Fed s inaction, we revised down our short-term interest rate forecasts as well. Our 1-year CMT forecasts for 2015 and 2016 stand at 0.4 percent and 1.4 percent, respectively, down from 0.5 percent and 1.9 percent in our August forecast. Housing: The Home Mortgage Disclosure Act (HMDA) data on mortgage originations was released in late September. Preliminary estimates indicate that origination volume was about $100 billion higher than we previously expected. We now estimate that total market originations in 2014 were $1,350 billion. Due to the upward revision to 2014 and stronger-than-expected housing activity in the first half of 2015, we ve increased our estimate of 2015 mortgage originations to $1.53 trillion and 2016 originations to $1.4 trillion. We ve also increased our projection of 2015 home sales to 5.74 million units, which would be the best year since And we ve revised the 2015 refinance share up to 48 percent of all single family mortgage originations. 9

10 Housing Snapshot A selection of key indicators 11

11 12

12 13

13 In Closing: What Were They Thinking? House prices nationally have recovered to within 5 percent of their June 2006 peak. And in some states and metro areas, house prices are significantly higher than their June 2006 levels. In contrast, the post-2009 expansion has been marked by relatively weak growth in income. As a result, the relatively high ratio of house prices to incomes in some metro areas has caught our attention. Should we be concerned, or are current house prices sustainable? In last month s Insight & Outlook, we pointed out that statistics alone can t identify whether housing is overvalued or undervalued. We displayed four reasonable, but different, measures of housing valuation for ten metro areas (repeated as Exhibit 10 below). The results were disheartening the metrics frequently disagreed. By one measure, homes in the Houston metro area were overvalued by 15 percent in March of this year. By another equally-intuitive measure, the same homes were undervalued by 16 percent. The valuation metrics weren t much better at pinpointing the sustainability of prices in other metro areas (Exhibit 10). Exhibit 10 Even when expert human judgment is added to the mix, it s still tough to tell whether housing is overvalued. As an example, the Federal Reserve couldn t come to a consensus about house prices in the bubble years leading up to the financial crisis. Researchers from Swarthmore College reviewed transcripts from the meetings of the Federal Open Market Committee (FOMC) to ascertain the Fed s view of house prices prior to the Great Recession. 6 Despite their access to extensive data and analysis, the members of the FOMC were divided. While some warned of a potential housing bubble, others argued just as vigorously that house prices could be supported on the basis of economic fundamentals. In mid-2005, one bubble skeptic on the FOMC went so far as to say just for the hell of it, 6 Golub, Stephen, Ayse Kaya and Michael Reay. What were they thinking? The Federal Reserve in the run-up to the 2008 financial crisis, Review of International Political Economy, The FOMC is the Fed committee that meets eight times a year to set monetary policy. The FOMC transcripts are made public after a five-year lag. The authors reviewed a wide range of Fed documents in addition to the FOMC transcripts. 14

14 I would like to offer the hypothesis that property values are too low rather than too high. And even those members worried about a bubble did not appear to foresee any systemic risk from a possible collapse of house prices. This historical example and the information in our previous article should make everyone cautious about relying too heavily on statistical measures of housing valuation. However, in the interest of full disclosure, we have to admit that we have added our own metric to the mix. MiMi (Multi-Indicator Market Index ) combines several indicators of current market conditions and compares the result to the long-term value of that combination to identify whether a market is currently weak, stable, or elevated. We find MiMi useful in developing a view of the overall stability of specific markets, but even MiMi isn t a replacement for a broader-ranging analysis with a heavy dose of judgment (and humility). Despite the difficulties, we have an inescapable responsibility to make our best effort at assessing the sustainability of current house prices. The unpaid balance of Freddie Mac mortgage-backed securities currently stands at just over $1.5 trillion and our retained portfolio, while steadily declining, remains between $350 and $400 billion. That s a lot of mortgage credit risk. During the Great Recession, falling house prices inflicted enormous losses on the GSEs and on other holders of mortgage credit risk. To manage our risk exposure, we have to do the best job we can to spot warning signs of overvalued markets. Sean Becketti, Chief Economist Leonard Kiefer, Deputy Chief Economist Penka Trentcheva, Statistician Travell Williams, Statistician Matthew Reyes, Financial Analyst chief_economist@freddiemac.com Opinions, estimates, forecasts and other views contained in this document are those of Freddie Mac s Office of the Chief Economist, do not necessarily represent the views of Freddie Mac or its management, should not be construed as indicating Freddie Mac s business prospects or expected results, and are subject to change without notice. Although the Office of the Chief Economist attempts to provide reliable, useful information, it does not guarantee that the information is accurate, current or suitable for any particular purpose. The information is therefore provided on an as is basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution. Alteration of this document is strictly prohibited. 15

15 September 2015 Economic and Housing Market Outlook Revised 9/29/ Annual Totals Indicator Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q Real GDP (%) Consumer Prices (%) a Unemployment Rate (%) b Year Fixed Mtg. Rate (%) b /1 Hybrid Treas. Indexed ARM Rate (%) b Year Treas. Indexed ARM Rate (%) b Year Const. Mat. Treas. Rate (%) b Year Const. Mat. Treas. Rate (%) b Annual Totals Indicator Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q Housing Starts c Total Home Sales d FMHPI House Price Appreciation (%) e S&P/Case-Shiller Home Price Index (%) f Family Mortgage Originations g. Conventional $200 $284 $306 $301 $290 $379 $320 $240 $224 $340 $336 $220 $1,206 $1,750 $1,570 $1,091 $1,229 $1,120 FHA & VA $52 $63 $71 $73 $80 $81 $80 $60 $56 $85 $84 $55 $286 $372 $355 $259 $301 $280 Total $252 $347 $377 $374 $370 $460 $400 $300 $280 $425 $420 $275 $1,492 $2,122 $1,925 $1,350 $1,530 $1,400 ARM Share (%) h Refinancing Share - Applications (%) i Refinancing Share - Originations (%) j Residential Mortgage Debt (%) k Note: Quarterly and annual forecasts are shown in shaded areas; totals may not add due to rounding; quarterly data expressed as annual rates. Annual forecast data are averages of quarterly values; annual historical data are reported as Q4 over Q4. a. Calculations based on quarterly average of monthly index levels; index levels based on the seasonally-adjusted, all-urban consumer price index. b. Quarterly average of monthly unemployment rates (seasonally-adjusted); Quarterly average of monthly interest rates. c. Millions of housing units; quarterly averages of monthly, seasonally-adjusted levels (reported at an annual rate). d. Millions of housing units; total sales are the sum of new and existing single-family homes;quarterly averages of monthly, seasonally-adjusted levels (reported at an annual rate). e. Quarterly growth rate of Freddie Mac's House Price Index; seasonally-adjusted; annual rates for yearly data. f. National composite index (quarterly growth rate), seasonally-adjusted; annual rates for yearly data. Prepared by Office of the Chief Economist and reflects views as of 9/29/2015 (GTW); Send comments and questions to chief_economist@freddiemac.com. Opinions, estimates, forecasts and other views contained in this document are those of Freddie Mac's Office of the Chief Economist, do not necessarily represent the views of Freddie Mac or its management, should not be construed as indicating Freddie Mac's business prospects or expected results, and are subject to change without notice. Although the Office of the Chief Economist attempts to provide reliable, useful information, it does not guarantee that the information is accurate, current or suitable for any particular purpose. The information is therefore provided on an "as is" basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution. Alteration of this document is strictly prohibited by Freddie Mac. g. Billions of dollars (not seasonally-adjusted); conventional for 2014 are Freddie Mac estimates. h. Federal Housing Finance Agency (FHFA); quarterly averages of monthly shares of number of loans of conventional, home-purchase mortgage closings (not seasonally-adjusted). i. MBA Applications Survey: activity by dollars, total market refi share percent for United States (not seasonally-adjusted). j. Home Mortgage Disclosure Act for all single-family mortgages (not seasonally-adjusted); annual share is dollar-weighted average of quarterly shares (2014 estimated). k. Federal Reserve Board; growth rate of residential mortgage debt, the sum of single-family and multifamily mortgages

b. 2.5 2.4 2.4 2.4 2.4 2.5 2.5 2.6 2.7 2.8 3.0 3.2 3.0 2.7 2.6 2.4 2.5 2.9 10-Year Const.")

Preparing for 2015 Housing Market Opportunities

January U.S. Economic & Housing Market Outlook Preparing for 2015 Housing Market Opportunities As we enter 2015, the U.S. economy and housing markets are prepared for a robust start. Unlike one year ago,

January U.S. Economic & Housing Market Outlook Preparing for 2015 Housing Market Opportunities As we enter 2015, the U.S. economy and housing markets are prepared for a robust start. Unlike one year ago,

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation

August 2014 Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook for factors that typically impact

August 2014 Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook for factors that typically impact

More than Just Curb Appeal Factors that affect the Housing Market

Insight. Education. Analysis. M a r c h 2 0 1 5 More than Just Curb Appeal Factors that affect the Housing Market By Kevin Chambers Not only is buying a house usually the largest purchase anyone will make,

Insight. Education. Analysis. M a r c h 2 0 1 5 More than Just Curb Appeal Factors that affect the Housing Market By Kevin Chambers Not only is buying a house usually the largest purchase anyone will make,

MBA Forecast Commentary Joel Kan, jkan@mba.org

Jun 20, 2014 MBA Forecast Commentary Joel Kan, jkan@mba.org Improving Job Market, Weak Housing Market, Lower Mortgage Originations MBA Economic and Mortgage Finance Commentary: June 2014 Key highlights

Jun 20, 2014 MBA Forecast Commentary Joel Kan, jkan@mba.org Improving Job Market, Weak Housing Market, Lower Mortgage Originations MBA Economic and Mortgage Finance Commentary: June 2014 Key highlights

2014 Fourth Quarter & Full Year Refinance Report Borrowers Who Refinanced in 2014 to Save Approximately $5 Billion in Interest Payments

2014 Fourth Quarter & Full Year Refinance Report Borrowers Who Refinanced in 2014 to Save Approximately $5 Billion in Interest Payments As the origination market evolves from a refinance boom to a purchasemoney

2014 Fourth Quarter & Full Year Refinance Report Borrowers Who Refinanced in 2014 to Save Approximately $5 Billion in Interest Payments As the origination market evolves from a refinance boom to a purchasemoney

MBA Forecast Commentary Joel Kan, jkan@mba.org

MBA Forecast Commentary Joel Kan, jkan@mba.org Weak First Quarter, But Growth Expected to Recover MBA Economic and Mortgage Finance Commentary: May 2015 Broad economic growth in the US got off to a slow

MBA Forecast Commentary Joel Kan, jkan@mba.org Weak First Quarter, But Growth Expected to Recover MBA Economic and Mortgage Finance Commentary: May 2015 Broad economic growth in the US got off to a slow

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners July 2014 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners July 2014 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners March 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners March 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

OBSERVATION. TD Economics SCHOOL S OUT SOFTER TREND IN U.S. HIGHER-ED ENROLLMENT TO PERSIST

OBSERVATION TD Economics SCHOOL S OUT SOFTER TREND IN U.S. HIGHER-ED ENROLLMENT TO PERSIST Highlights Student debt currently sits at $966 billion. This is the second largest outstanding liability on the

OBSERVATION TD Economics SCHOOL S OUT SOFTER TREND IN U.S. HIGHER-ED ENROLLMENT TO PERSIST Highlights Student debt currently sits at $966 billion. This is the second largest outstanding liability on the

Salt Lake Housing Forecast

2015 Salt Lake Housing Forecast A Sustainable Housing Market By James Wood Director of the Bureau of Economic and Business Research Commissioned by the Salt Lake Board of REALTORS By year-end 2013 home

2015 Salt Lake Housing Forecast A Sustainable Housing Market By James Wood Director of the Bureau of Economic and Business Research Commissioned by the Salt Lake Board of REALTORS By year-end 2013 home

Mortgage Retention: Predicting Refinance Motivations

Mortgage Retention: Predicting Refinance Motivations Nothing endures but change - Heraclitus (540 BC 480 BC) Changing Trends in the Mortgage Industry In 2001, at the dawn of the new millennium, long term

Mortgage Retention: Predicting Refinance Motivations Nothing endures but change - Heraclitus (540 BC 480 BC) Changing Trends in the Mortgage Industry In 2001, at the dawn of the new millennium, long term

Obama Administration Efforts to Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners March 21 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners March 21 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

Household Debt and Credit: Student Debt

Household Debt and Credit: Student Debt February 28, 2013 Donghoon Lee The views presented here are those of the author and do not necessarily reflect those of the Federal Reserve Bank of New York, or

Household Debt and Credit: Student Debt February 28, 2013 Donghoon Lee The views presented here are those of the author and do not necessarily reflect those of the Federal Reserve Bank of New York, or

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2014 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2014 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners June 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners June 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

Student Debt Being Smart about Student Loans

Insight. Education. Analysis. S e p t e m b e r 2 0 1 4 Student Debt Being Smart about Student Loans By Kevin Chambers During the 2008 crisis, total American household debt fell. The amount of money borrowed

Insight. Education. Analysis. S e p t e m b e r 2 0 1 4 Student Debt Being Smart about Student Loans By Kevin Chambers During the 2008 crisis, total American household debt fell. The amount of money borrowed

MBA Forecast Commentary Joel Kan

MBA Forecast Commentary Joel Kan Mortgage Originations Estimates Revised Higher MBA Economic and Mortgage Finance Commentary: February 2016 In our most recent forecast, we presented revisions to our mortgage

MBA Forecast Commentary Joel Kan Mortgage Originations Estimates Revised Higher MBA Economic and Mortgage Finance Commentary: February 2016 In our most recent forecast, we presented revisions to our mortgage

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

THE POTENTIAL MACROECONOMIC EFFECT OF DEBT CEILING BRINKMANSHIP

OCTOBER 2013 THE POTENTIAL MACROECONOMIC EFFECT OF DEBT CEILING BRINKMANSHIP Introduction The United States has never defaulted on its obligations, and the U. S. dollar and Treasury securities are at the

OCTOBER 2013 THE POTENTIAL MACROECONOMIC EFFECT OF DEBT CEILING BRINKMANSHIP Introduction The United States has never defaulted on its obligations, and the U. S. dollar and Treasury securities are at the

Student Loan Borrowing and Repayment Trends, 2015

Student Loan Borrowing and Repayment Trends, 2015 April 16, 2015 Andrew Haughwout, Donghoon Lee, Joelle Scally, Wilbert van der Klaauw The views presented here are those of the authors and do not necessarily

Student Loan Borrowing and Repayment Trends, 2015 April 16, 2015 Andrew Haughwout, Donghoon Lee, Joelle Scally, Wilbert van der Klaauw The views presented here are those of the authors and do not necessarily

Investment Symposium March 14-15, 2013 New York, NY. Session E5, U.S. Economic Conditions and the Housing/Mortgage Market

Investment Symposium March 1-15, 213 New York, NY Session E5, U.S. Economic Conditions and the Housing/Mortgage Market Moderator: Jonathan Glowacki Presenter: David Berson Housing & Mortgage Market Outlook

Investment Symposium March 1-15, 213 New York, NY Session E5, U.S. Economic Conditions and the Housing/Mortgage Market Moderator: Jonathan Glowacki Presenter: David Berson Housing & Mortgage Market Outlook

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners July 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners July 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners August 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners August 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 2011-22 July 18, 2011 Securitization and Small Business BY JAMES A. WILCOX Small businesses have relied considerably on securitized markets for credit. The recent financial crisis

FRBSF ECONOMIC LETTER 2011-22 July 18, 2011 Securitization and Small Business BY JAMES A. WILCOX Small businesses have relied considerably on securitized markets for credit. The recent financial crisis

FOR IMMEDIATE RELEASE November 7, 2013 MEDIA CONTACT: Lisa Gagnon 703-903-3385 INVESTOR CONTACT: Robin Phillips 571-382-4732

FOR IMMEDIATE RELEASE MEDIA CONTACT: Lisa Gagnon 703-903-3385 INVESTOR CONTACT: Robin Phillips 571-382-4732 FREDDIE MAC REPORTS PRE-TAX INCOME OF $6.5 BILLION FOR THIRD QUARTER 2013 Release of Valuation

FOR IMMEDIATE RELEASE MEDIA CONTACT: Lisa Gagnon 703-903-3385 INVESTOR CONTACT: Robin Phillips 571-382-4732 FREDDIE MAC REPORTS PRE-TAX INCOME OF $6.5 BILLION FOR THIRD QUARTER 2013 Release of Valuation

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 01-1 April, 01 Commercial Real Estate and Low Interest Rates BY JOHN KRAINER Commercial real estate construction faltered during the 00 recession and has improved only slowly during

FRBSF ECONOMIC LETTER 01-1 April, 01 Commercial Real Estate and Low Interest Rates BY JOHN KRAINER Commercial real estate construction faltered during the 00 recession and has improved only slowly during

INTEREST RATES: WHAT GOES UP MUST COME DOWN

3 INTEREST RATES: WHAT GOES UP MUST COME DOWN John M. Petersen Melvin Mark Capital Group, LLC What an interesting time to be asked to write something about interest rates! Our practice emphasis is commercial

3 INTEREST RATES: WHAT GOES UP MUST COME DOWN John M. Petersen Melvin Mark Capital Group, LLC What an interesting time to be asked to write something about interest rates! Our practice emphasis is commercial

July 2015 U.S. Housing Market Insight & Outlook. Insight: It is different this time (p. 2) Forecast update (p. 6) Outlook: Midyear update (p.

Forecast update (p. 6) Outlook: Midyear update (p.") July 2015 U.S. Housing Market Insight & Outlook Insight: It is different this time (p. 2) Affordability initiatives that allow low down payments like Freddie Mac s Home Possible Advantage (SM) have raised

July 2015 U.S. Housing Market Insight & Outlook Insight: It is different this time (p. 2) Affordability initiatives that allow low down payments like Freddie Mac s Home Possible Advantage (SM) have raised

Late, Not Lost: The Economic Drag From the Millennial Generation

Late, Not Lost: The Economic Drag From the Millennial Generation September 2, 2014 by Joshua Anderson, Emmanuel Sharef, Jason Mandinach of PIMCO We believe concerns of a student debt "bubble" and perpetual

Late, Not Lost: The Economic Drag From the Millennial Generation September 2, 2014 by Joshua Anderson, Emmanuel Sharef, Jason Mandinach of PIMCO We believe concerns of a student debt "bubble" and perpetual

Revisiting the Canadian Mortgage Market Risk is Small and Contained

Revisiting the Canadian Mortgage Market Risk is Small and Contained January 2010 Prepared for: Canadian Association of Accredited Mortgage Professionals By: Will Dunning CAAMP Chief Economist Revisiting

Revisiting the Canadian Mortgage Market Risk is Small and Contained January 2010 Prepared for: Canadian Association of Accredited Mortgage Professionals By: Will Dunning CAAMP Chief Economist Revisiting

Lecture 4: The Aftermath of the Crisis

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

DEUTSCHE ASSET & WEALTH MANAGEMENT REAL ESTATE OUTLOOK

Research Report DEUTSCHE ASSET & WEALTH MANAGEMENT REAL ESTATE OUTLOOK Second Quarter 2013 Economic Outlook Business and consumer spending to drive recovery Quantitative easing beginning its expected unwinding

Research Report DEUTSCHE ASSET & WEALTH MANAGEMENT REAL ESTATE OUTLOOK Second Quarter 2013 Economic Outlook Business and consumer spending to drive recovery Quantitative easing beginning its expected unwinding

Wisconsin's Great Cost Shift

Dēmos Wisconsin's Great Cost Shift HOW HIGHER EDUCATION CUTS UNDERMINE THE STATE'S FUTURE MIDDLE CLASS I n today s economy, a college education is essential for getting a good job and entering the middle

Dēmos Wisconsin's Great Cost Shift HOW HIGHER EDUCATION CUTS UNDERMINE THE STATE'S FUTURE MIDDLE CLASS I n today s economy, a college education is essential for getting a good job and entering the middle

The U.S. Outlook and Monetary Policy. Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City

The U.S. Outlook and Monetary Policy Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City February 2, 2016 Central Exchange Kansas City, Mo. The views expressed by

The U.S. Outlook and Monetary Policy Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City February 2, 2016 Central Exchange Kansas City, Mo. The views expressed by

Underutilization in U.S. Labor Markets

EMBARGOED UNTIL Thursday, February 6, 2014 at 5:45 PM Eastern Time OR UPON DELIVERY Underutilization in U.S. Labor Markets Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of

EMBARGOED UNTIL Thursday, February 6, 2014 at 5:45 PM Eastern Time OR UPON DELIVERY Underutilization in U.S. Labor Markets Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of

http://www.ritholtz.com/blog/2014/11/housing-market-headwin...

Page 1 of 5 - The Big Picture - http://www.ritholtz.com/blog - Housing Market Headwinds Posted By Guest Author On November 10, 2014 @ 5:00 am In Real Estate,Think Tank 3 Comments Housing Market Headwinds

Page 1 of 5 - The Big Picture - http://www.ritholtz.com/blog - Housing Market Headwinds Posted By Guest Author On November 10, 2014 @ 5:00 am In Real Estate,Think Tank 3 Comments Housing Market Headwinds

A mortgage is a loan that is used to finance the purchase of your home. It consists of 5 parts: collateral, principal, interest, taxes, and insurance.

A mortgage is a loan that is used to finance the purchase of your home. It consists of 5 parts: collateral, principal, interest, taxes, and insurance. When you agree to a mortgage, you enter into a legal

A mortgage is a loan that is used to finance the purchase of your home. It consists of 5 parts: collateral, principal, interest, taxes, and insurance. When you agree to a mortgage, you enter into a legal

US HOUSING MARKET MONTHLY

US HOUSING MARKET MONTHLY th Oct. Editor: Ed Stansfield New build sales finally making some headway Overview: The drop in mortgage rates towards the end of September has given mortgage applications a boost,

US HOUSING MARKET MONTHLY th Oct. Editor: Ed Stansfield New build sales finally making some headway Overview: The drop in mortgage rates towards the end of September has given mortgage applications a boost,

A. Volume and Share of Mortgage Originations

Section IV: Characteristics of the Fiscal Year 2006 Book of Business This section takes a closer look at the characteristics of the FY 2006 book of business. The characteristic descriptions include: the

Section IV: Characteristics of the Fiscal Year 2006 Book of Business This section takes a closer look at the characteristics of the FY 2006 book of business. The characteristic descriptions include: the

LIST OF MAJOR LEADING & LAGGING ECONOMIC INDICATORS

APRIL 2014 LIST OF MAJOR LEADING & LAGGING ECONOMIC INDICATORS Most economists talk about where the economy is headed it s what they do. Paying attention to economic indicators can give you an idea of

APRIL 2014 LIST OF MAJOR LEADING & LAGGING ECONOMIC INDICATORS Most economists talk about where the economy is headed it s what they do. Paying attention to economic indicators can give you an idea of

The Aftermath of the Housing Bubble

The Aftermath of the Housing Bubble James Bullard President and CEO, FRB-St. Louis Housing in America: Innovative Solutions to Address the Needs of Tomorrow 5 June 2012 The Bipartisan Policy Center St.

The Aftermath of the Housing Bubble James Bullard President and CEO, FRB-St. Louis Housing in America: Innovative Solutions to Address the Needs of Tomorrow 5 June 2012 The Bipartisan Policy Center St.

U.S. and Regional Housing Markets

U.S. and Regional Housing Markets House Prices Boom, Bust and Rebound Index, 1991: Q1=1* 3 CoreLogic house price index Real FHFA house price index 25 2 15 1 5 1991 199 1997 2 23 26 29 212 215 *Seasonally

U.S. and Regional Housing Markets House Prices Boom, Bust and Rebound Index, 1991: Q1=1* 3 CoreLogic house price index Real FHFA house price index 25 2 15 1 5 1991 199 1997 2 23 26 29 212 215 *Seasonally

Federal Reserve Bank of Kansas City: Consumer Credit Report

Federal Reserve Bank of Kansas City: Consumer Credit Report Tenth District Consumer Credit Report May 29, 2015 By Kelly Edmiston, Senior Economist and Mwai Malindi, Research Associate FIRST QUARTER 2015

Federal Reserve Bank of Kansas City: Consumer Credit Report Tenth District Consumer Credit Report May 29, 2015 By Kelly Edmiston, Senior Economist and Mwai Malindi, Research Associate FIRST QUARTER 2015

THE STATE OF THE ECONOMY

THE STATE OF THE ECONOMY CARLY HARRISON Portland State University Following data revisions, the economy continues to grow steadily, but slowly, in line with expectations. Gross domestic product has increased,

THE STATE OF THE ECONOMY CARLY HARRISON Portland State University Following data revisions, the economy continues to grow steadily, but slowly, in line with expectations. Gross domestic product has increased,

Our $1.3 Trillion Government-Assisted Student Loan Crisis June 3, 2015 by Gary Halbert of Halbert Wealth Management

Our $1.3 Trillion Government-Assisted Student Loan Crisis June 3, 2015 by Gary Halbert of Halbert Wealth Management Page 1, 2016 Advisor Perspectives, Inc. All rights reserved. IN THIS ISSUE: 1. US 1Q

Our $1.3 Trillion Government-Assisted Student Loan Crisis June 3, 2015 by Gary Halbert of Halbert Wealth Management Page 1, 2016 Advisor Perspectives, Inc. All rights reserved. IN THIS ISSUE: 1. US 1Q

BERYL Credit Pulse on High Yield Corporates

BERYL Credit Pulse on High Yield Corporates This paper will summarize Beryl Consulting 2010 outlook and hedge fund portfolio construction for the high yield corporate sector in light of the events of the

BERYL Credit Pulse on High Yield Corporates This paper will summarize Beryl Consulting 2010 outlook and hedge fund portfolio construction for the high yield corporate sector in light of the events of the

Historically, employment in financial

Employment in financial activities: double billed by housing and financial crises The housing market crash, followed by the financial crisis of the 2007-09 recession, helped depress financial activities

Employment in financial activities: double billed by housing and financial crises The housing market crash, followed by the financial crisis of the 2007-09 recession, helped depress financial activities

Student Loans Know Your Options

Student Loans Know Your Options Sam Hewitt Director, Political & Grassroots Advocacy, GRPP Samuel J. Hewitt Sam Hewitt is the director of political and grassroots advocacy at the American Speech-Language-Hearing

Student Loans Know Your Options Sam Hewitt Director, Political & Grassroots Advocacy, GRPP Samuel J. Hewitt Sam Hewitt is the director of political and grassroots advocacy at the American Speech-Language-Hearing

The GSEs Are Helping to Stabilize an Unstable Mortgage Market

Update on the Single-Family Credit Guarantee Business Rick Padilla Director, Corporate Relations & Housing Outreach The Changing Economy: The New Community Lending Environment June 1, 29 The GSEs Are Helping

Update on the Single-Family Credit Guarantee Business Rick Padilla Director, Corporate Relations & Housing Outreach The Changing Economy: The New Community Lending Environment June 1, 29 The GSEs Are Helping

Insight: Mass Production and Mortgages

Insight & Outlook November 23, 2015 In this Edition: Insight: Mass Production and Mortgages Henry Ford is justly-celebrated for his application of mass production techniques to automobiles. Breaking the

Insight & Outlook November 23, 2015 In this Edition: Insight: Mass Production and Mortgages Henry Ford is justly-celebrated for his application of mass production techniques to automobiles. Breaking the

Federal Housing Finance Agency

Fourth Quarter 20 FHFA Federal Property Manager's Report This report contains data on foreclosure prevention activity, refinance and MHA program activity of Fannie Mae and Freddie Mac (the Enterprises)

Fourth Quarter 20 FHFA Federal Property Manager's Report This report contains data on foreclosure prevention activity, refinance and MHA program activity of Fannie Mae and Freddie Mac (the Enterprises)

A Strong Housing Recovery Fuels Growth

Chapman University A. Gary Anderson Center for Economic Research FOR RELEASE: ONLINE: June 12, 2013; 10:00 a.m. PRINT: June 13, 2013 CONTACT: James Doti, President and Donald Bren Distinguished Chair of

Chapman University A. Gary Anderson Center for Economic Research FOR RELEASE: ONLINE: June 12, 2013; 10:00 a.m. PRINT: June 13, 2013 CONTACT: James Doti, President and Donald Bren Distinguished Chair of

Mounting Student Debt Is Reshaping The U.S. Student Loan Market

STRUCTURED FINANCE RESEARCH Mounting Student Debt Is Reshaping The U.S. Student Loan Market Primary Credit Analyst: Erkan Erturk, PhD, New York (1) 212-438-2450; erkan_erturk@standardandpoors.com Business

STRUCTURED FINANCE RESEARCH Mounting Student Debt Is Reshaping The U.S. Student Loan Market Primary Credit Analyst: Erkan Erturk, PhD, New York (1) 212-438-2450; erkan_erturk@standardandpoors.com Business

Making Home Affordable: New Challenges, New Tools

Making Home Affordable: New Challenges, New Tools Todd Hempstead Senior Vice President, Single-Family Mortgage Business Fannie Mae June 2009 1 What I ll cover today Challenges facing our communities Fannie

Making Home Affordable: New Challenges, New Tools Todd Hempstead Senior Vice President, Single-Family Mortgage Business Fannie Mae June 2009 1 What I ll cover today Challenges facing our communities Fannie

18 ECB STYLISED FACTS OF MONEY AND CREDIT OVER THE BUSINESS CYCLE

Box 1 STYLISED FACTS OF MONEY AND CREDIT OVER THE BUSINESS CYCLE Over the past three decades, the growth rates of MFI loans to the private sector and the narrow monetary aggregate M1 have displayed relatively

Box 1 STYLISED FACTS OF MONEY AND CREDIT OVER THE BUSINESS CYCLE Over the past three decades, the growth rates of MFI loans to the private sector and the narrow monetary aggregate M1 have displayed relatively

Bond Market Insights October 10, 2014

Bond Market Insights October 10, 2014 by John Simms, CFA and Jerry Wiesner, CFA General Bond Market Treasury yields rose in September as prices fell. Yields in the belly of the curve (5- to 7-year maturities)

Bond Market Insights October 10, 2014 by John Simms, CFA and Jerry Wiesner, CFA General Bond Market Treasury yields rose in September as prices fell. Yields in the belly of the curve (5- to 7-year maturities)

The U.S. Economy after September 11. 1. pushing us from sluggish growth to an outright contraction. b and there s a lot of uncertainty.

Presentation to the University of Washington Business School For delivery November 15, 2001 at approximately 8:05 AM Pacific Standard Time (11:05 AM Eastern) By Robert T. Parry, President and CEO of the

Presentation to the University of Washington Business School For delivery November 15, 2001 at approximately 8:05 AM Pacific Standard Time (11:05 AM Eastern) By Robert T. Parry, President and CEO of the

Facts and Figures on the Middle-Class Squeeze in Idaho

Facts and Figures on the Middle-Class Squeeze in Idaho For hard-working, middle-class families all over the country, life during the Bush presidency has grown less affordable and less secure. President

Facts and Figures on the Middle-Class Squeeze in Idaho For hard-working, middle-class families all over the country, life during the Bush presidency has grown less affordable and less secure. President

Homeownership. b y B R A D S H U ST E R

INDUSTRY TRENDS Millennials AND Homeownership b y B R A D S H U ST E R Homeownership is not as out of reach as millennials may think. Many misperceptions abound that the industry could help dispel. In

INDUSTRY TRENDS Millennials AND Homeownership b y B R A D S H U ST E R Homeownership is not as out of reach as millennials may think. Many misperceptions abound that the industry could help dispel. In

OCC Mortgage Metrics Report Disclosure of National Bank and Federal Savings Association Mortgage Loan Data

OCC Mortgage Metrics Report Disclosure of National Bank and Federal Savings Association Mortgage Loan Data First Quarter 2014 Office of the Comptroller of the Currency Washington, D.C. June 2014 Contents

OCC Mortgage Metrics Report Disclosure of National Bank and Federal Savings Association Mortgage Loan Data First Quarter 2014 Office of the Comptroller of the Currency Washington, D.C. June 2014 Contents

Statement by. Janet L. Yellen. Chair. Board of Governors of the Federal Reserve System. before the. Committee on Financial Services

For release at 8:30 a.m. EST February 10, 2016 Statement by Janet L. Yellen Chair Board of Governors of the Federal Reserve System before the Committee on Financial Services U.S. House of Representatives

For release at 8:30 a.m. EST February 10, 2016 Statement by Janet L. Yellen Chair Board of Governors of the Federal Reserve System before the Committee on Financial Services U.S. House of Representatives

2014 Survey of Credit Underwriting Practices

2014 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. December 2014 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

2014 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. December 2014 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

The Key to Stabilizing House Prices: Bring Them Down

The Key to Stabilizing House Prices: Bring Them Down Dean Baker December 2008 Center for Economic and Policy Research 1611 Connecticut Avenue, NW, Suite 400 Washington, D.C. 20009 202-293-5380 www.cepr.net

The Key to Stabilizing House Prices: Bring Them Down Dean Baker December 2008 Center for Economic and Policy Research 1611 Connecticut Avenue, NW, Suite 400 Washington, D.C. 20009 202-293-5380 www.cepr.net

Fannie Mae Reports Pre-Tax Income of $8.1 Billion for First Quarter 2013

Resource Center: 1-800-732-6643 Contact: Pete Bakel 202-752-2034 Date: May 9, 2013 Fannie Mae Reports Pre-Tax Income of $8.1 Billion for First Quarter 2013 Release of Valuation Allowance on Deferred Tax

Resource Center: 1-800-732-6643 Contact: Pete Bakel 202-752-2034 Date: May 9, 2013 Fannie Mae Reports Pre-Tax Income of $8.1 Billion for First Quarter 2013 Release of Valuation Allowance on Deferred Tax

Documeent title on one or two lines in Gustan Book 24pt Commercial mortgages are HOT!

TIAA-CREF Asset Management Documeent title on one or two lines in Gustan Book pt Commercial mortgages are HOT! Martha Peyton, Ph.D., Managing Director TIAA-CREF Global Real Estate, Strategy & Research

TIAA-CREF Asset Management Documeent title on one or two lines in Gustan Book pt Commercial mortgages are HOT! Martha Peyton, Ph.D., Managing Director TIAA-CREF Global Real Estate, Strategy & Research

Fixed-income securities have had an extraordinary run, but don t call it a bubble

Wells Fargo Advantage Funds January 2011 Fixed-income securities have had an extraordinary run, but don t call it a bubble Jim Kochan, Chief Fixed-Income Strategist Jim Fuson, CFA Christopher Kennedy Wells

Wells Fargo Advantage Funds January 2011 Fixed-income securities have had an extraordinary run, but don t call it a bubble Jim Kochan, Chief Fixed-Income Strategist Jim Fuson, CFA Christopher Kennedy Wells

TIMING YOUR INVESTMENT STRATEGIES USING BUSINESS CYCLES AND STOCK SECTORS. Developed by Peter Dag & Associates, Inc.

TIMING YOUR INVESTMENT STRATEGIES USING BUSINESS CYCLES AND STOCK SECTORS Developed by Peter Dag & Associates, Inc. 5 4 6 7 3 8 3 1 2 Fig. 1 Introduction The business cycle goes through 4 major growth

TIMING YOUR INVESTMENT STRATEGIES USING BUSINESS CYCLES AND STOCK SECTORS Developed by Peter Dag & Associates, Inc. 5 4 6 7 3 8 3 1 2 Fig. 1 Introduction The business cycle goes through 4 major growth

Q1 1990 Q1 1996 Q1 2002 Q1 2008 Q1

August 2015 Canada s debt burden By Richard J. Wylie, CFA Vice-President, Investment Strategy, Assante Wealth Management Much ink has been spilled over the past several years regarding the extent of the

August 2015 Canada s debt burden By Richard J. Wylie, CFA Vice-President, Investment Strategy, Assante Wealth Management Much ink has been spilled over the past several years regarding the extent of the

MBS in 2013: More of the same, with a slight twist

213 MBS in 213: More of the same, with a slight twist Jason Callan, Senior Portfolio Manager Agency mortgage-backed securities (MBS) should continue to offer an attractive risk-adjusted return opportunity

213 MBS in 213: More of the same, with a slight twist Jason Callan, Senior Portfolio Manager Agency mortgage-backed securities (MBS) should continue to offer an attractive risk-adjusted return opportunity

MACROECONOMIC AND INDUSTRY ANALYSIS VALUATION PROCESS

MACROECONOMIC AND INDUSTRY ANALYSIS VALUATION PROCESS BUSINESS ANALYSIS INTRODUCTION To determine a proper price for a firm s stock, security analyst must forecast the dividend & earnings that can be expected

MACROECONOMIC AND INDUSTRY ANALYSIS VALUATION PROCESS BUSINESS ANALYSIS INTRODUCTION To determine a proper price for a firm s stock, security analyst must forecast the dividend & earnings that can be expected

UK Economic Forecast Q3 2014

UK Economic Forecast Q3 2014 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

UK Economic Forecast Q3 2014 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

Clint M. Hanni Partner Corporate Section of the Business Services Group

How to Negotiate Effectively with Your to Restructure a Loan PRESENTED BY: Clint M. Hanni Partner Corporate Section of the Business Services Group May 26, 2010 11:30 a.m. 1 p.m. Stoel Rives LLP One Utah

How to Negotiate Effectively with Your to Restructure a Loan PRESENTED BY: Clint M. Hanni Partner Corporate Section of the Business Services Group May 26, 2010 11:30 a.m. 1 p.m. Stoel Rives LLP One Utah

2012 Survey of Credit Underwriting Practices

2012 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. June 2012 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

2012 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. June 2012 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

Update on Market Challenges

Update on Market Challenges Charlottesville Area Association of Realtors August 6, 2009 Virginia Housing Development Authority Four inter-related factors continue to hold back recovery in the Charlottesville

Update on Market Challenges Charlottesville Area Association of Realtors August 6, 2009 Virginia Housing Development Authority Four inter-related factors continue to hold back recovery in the Charlottesville

CREDIT UNION TRENDS REPORT

$ in Billions CREDIT UNION TRENDS REPORT CUNA Mutual Group Economics July 216 (May 216 Data) Highlights During May, credit unions picked-up 431, in new memberships, loan and savings balances grew at an

$ in Billions CREDIT UNION TRENDS REPORT CUNA Mutual Group Economics July 216 (May 216 Data) Highlights During May, credit unions picked-up 431, in new memberships, loan and savings balances grew at an

The Housing and Mortgage Market Problem: A Set of Policy Options

Fisher Center for Real Estate & Urban Economics University of California, Berkeley (510) 643-6105 The Housing and Mortgage Market Problem: A Set of Policy Options Author: Kenneth T. Rosen, Chairman, Fisher

Fisher Center for Real Estate & Urban Economics University of California, Berkeley (510) 643-6105 The Housing and Mortgage Market Problem: A Set of Policy Options Author: Kenneth T. Rosen, Chairman, Fisher

The U.S. and Midwest Economy in 2016: Implications for Supply Chain Firms

The U.S. and Midwest Economy in 2016: Implications for Supply Chain Firms Rick Mattoon Senior Economist and Economic Advisor Federal Reserve Bank of Chicago Right Place Supply Chain Management Conference

The U.S. and Midwest Economy in 2016: Implications for Supply Chain Firms Rick Mattoon Senior Economist and Economic Advisor Federal Reserve Bank of Chicago Right Place Supply Chain Management Conference

Spotlight on the Housing Market in the Orlando-Kissimmee-Sanford, FL MSA

Spotlight on in Orlando-Kissimmee-Sanford, FL MSA The Orlando-Kissimmee-Sanford, FL Metropolitan Statistical Area (Orlando MSA) is located in central Florida and includes four counties: Lake, Orange, Osceola,

Spotlight on in Orlando-Kissimmee-Sanford, FL MSA The Orlando-Kissimmee-Sanford, FL Metropolitan Statistical Area (Orlando MSA) is located in central Florida and includes four counties: Lake, Orange, Osceola,

Summary of the Housing and Economic Recovery Act of 2008

Summary of the Housing and Economic Recovery Act of 2008 On July 30, President Bush signed major housing legislation, HR 3221, the Housing and Economic Recovery Act of 2008. The bill restructures regulation

Summary of the Housing and Economic Recovery Act of 2008 On July 30, President Bush signed major housing legislation, HR 3221, the Housing and Economic Recovery Act of 2008. The bill restructures regulation

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 2010-03 February 1, 2010 Mortgage Choice and the Pricing of Fixed-Rate and Adjustable-Rate Mortgages BY JOHN KRAINER In the United States throughout 2009, the share of adjustable-rate

FRBSF ECONOMIC LETTER 2010-03 February 1, 2010 Mortgage Choice and the Pricing of Fixed-Rate and Adjustable-Rate Mortgages BY JOHN KRAINER In the United States throughout 2009, the share of adjustable-rate

The Unsweet Sixteen. The Top 10 Factors Impacting the Economy in 2016. 2007 We are here > Treasury notes. Cash

The Unsweet Sixteen The Top 10 Factors Impacting the Economy in 2016 Ben Miller, CEO 2007 We are here > 2008 2009 Peak Best-Performing Asset Classes Commodities Recession Bottoming Recovery Expansion Treasury

The Unsweet Sixteen The Top 10 Factors Impacting the Economy in 2016 Ben Miller, CEO 2007 We are here > 2008 2009 Peak Best-Performing Asset Classes Commodities Recession Bottoming Recovery Expansion Treasury

Chapter 10 6/16/2010. Mortgage Types and Borrower Decisions: Overview Role of the secondary market. Mortgage types:

Mortgage Types and Borrower Decisions: Overview Role of the secondary market Chapter 10 Residential Mortgage Types and Borrower Decisions Mortgage types: Conventional mortgages FHA mortgages VA mortgages

Mortgage Types and Borrower Decisions: Overview Role of the secondary market Chapter 10 Residential Mortgage Types and Borrower Decisions Mortgage types: Conventional mortgages FHA mortgages VA mortgages

Yukon Wealth Management, Inc.

This summary reflects our views as of 12/15/08. Merrill Lynch High Yield Master Index effective yield at 23%. Asset Class Review: High-Yield Bonds Executive Summary High-yield bonds have had a terrible

This summary reflects our views as of 12/15/08. Merrill Lynch High Yield Master Index effective yield at 23%. Asset Class Review: High-Yield Bonds Executive Summary High-yield bonds have had a terrible

THE ECONOMIC PLIGHT OF MILLENNIALS

THE ECONOMIC PLIGHT OF MILLENNIALS 6 EconSouth January April 2014 A demographic cohort is never monolithic, but the group that recently entered the labor force had one trait in common: they watched as

THE ECONOMIC PLIGHT OF MILLENNIALS 6 EconSouth January April 2014 A demographic cohort is never monolithic, but the group that recently entered the labor force had one trait in common: they watched as

Pioneer Bond Fund. Performance Analysis & Commentary September 2015. Fund Ticker Symbols: PIOBX (Class A); PICYX (Class Y) us.pioneerinvestments.

; PICYX (Class Y) us.pioneerinvestments.") Pioneer Bond Fund COMMENTARY Performance Analysis & Commentary September 2015 Fund Ticker Symbols: PIOBX (Class A); PICYX (Class Y) us.pioneerinvestments.com Third Quarter Review Pioneer Bond Fund s Class

Pioneer Bond Fund COMMENTARY Performance Analysis & Commentary September 2015 Fund Ticker Symbols: PIOBX (Class A); PICYX (Class Y) us.pioneerinvestments.com Third Quarter Review Pioneer Bond Fund s Class

Trends in portfolio management

Trends in portfolio management An Experian white paper credit strategies Market Insight from Experian Page 1 Executive summary The economy is slowly accelerating, although economists, government officials

Trends in portfolio management An Experian white paper credit strategies Market Insight from Experian Page 1 Executive summary The economy is slowly accelerating, although economists, government officials

Bond Outlook. Third Quarter 2014. Waiting on the Fed. 10-Year Treasury Yields. Treasury Bonds. Break-even Inflation Rate

Third Quarter 21 Waiting on the Fed Despite a strong rebound in domestic economic activity with gross domestic production accelerating toward %, persistent low inflationary pressures and dramatically lower

Third Quarter 21 Waiting on the Fed Despite a strong rebound in domestic economic activity with gross domestic production accelerating toward %, persistent low inflationary pressures and dramatically lower

Defining Housing Equity Withdrawal

Housing Reserve Equity Bank of Australia Bulletin February 23 Housing Equity The increase in housing prices in recent years has contributed to rising household wealth and has helped to underpin continued

Housing Reserve Equity Bank of Australia Bulletin February 23 Housing Equity The increase in housing prices in recent years has contributed to rising household wealth and has helped to underpin continued

SHOPPING FOR A MORTGAGE

SHOPPING FOR A MORTGAGE The Traditional Fixed-Rate Mortgage Key characteristics: Level payments, fixed interest rate, fixed term. This mortgage is the one which most of us know, and it is still the loan

SHOPPING FOR A MORTGAGE The Traditional Fixed-Rate Mortgage Key characteristics: Level payments, fixed interest rate, fixed term. This mortgage is the one which most of us know, and it is still the loan

FREDDIE MAC REPORTS THIRD QUARTER 2015 FINANCIAL RESULTS

FOR IMMEDIATE RELEASE MEDIA CONTACT: Lisa Gagnon 703-903-3385 INVESTOR CONTACT: Robin Phillips 571-382-4732 FREDDIE MAC REPORTS THIRD QUARTER 2015 FINANCIAL RESULTS $475 Million Net Loss and $501 Million

FOR IMMEDIATE RELEASE MEDIA CONTACT: Lisa Gagnon 703-903-3385 INVESTOR CONTACT: Robin Phillips 571-382-4732 FREDDIE MAC REPORTS THIRD QUARTER 2015 FINANCIAL RESULTS $475 Million Net Loss and $501 Million

Monthly Economic Dashboard

RETIREMENT INSTITUTE SM Economic perspective Monthly Economic Dashboard Modest acceleration in economic growth appears in store for 2016 as the inventory-caused soft patch ends, while monetary policy moves

RETIREMENT INSTITUTE SM Economic perspective Monthly Economic Dashboard Modest acceleration in economic growth appears in store for 2016 as the inventory-caused soft patch ends, while monetary policy moves

Mortgage Defaults. Shane M. Sherlund. Board of Governors of the Federal Reserve System. March 8, 2010

Mortgage Defaults Shane M. Sherlund Board of Governors of the Federal Reserve System March 8, 2010 The analysis and conclusions contained herein reflect those of the author and do not necessarily reflect

Mortgage Defaults Shane M. Sherlund Board of Governors of the Federal Reserve System March 8, 2010 The analysis and conclusions contained herein reflect those of the author and do not necessarily reflect

The Consumer and Business Lending Initiative

March 3, 2009 The Consumer and Business Lending Initiative A Note on Efforts to Address Securitization Markets and Increase Lending Overview The Obama administration along with the Federal Reserve, the

March 3, 2009 The Consumer and Business Lending Initiative A Note on Efforts to Address Securitization Markets and Increase Lending Overview The Obama administration along with the Federal Reserve, the

Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2009 and 2010 estimates)

") Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2009 and 2010 estimates) Emmanuel Saez March 2, 2012 What s new for recent years? Great Recession 2007-2009 During the

Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2009 and 2010 estimates) Emmanuel Saez March 2, 2012 What s new for recent years? Great Recession 2007-2009 During the

Home-Mortgage Lending Trends in New England in 2010

January 212 No. 212-1 Home-Mortgage Lending Trends in New England in 21 Ana Patricia Muñoz The views expressed in this paper are solely those of the author and do not necessarily represent those of the

January 212 No. 212-1 Home-Mortgage Lending Trends in New England in 21 Ana Patricia Muñoz The views expressed in this paper are solely those of the author and do not necessarily represent those of the

Summary. Abbas P. Grammy 1 Professor of Economics California State University, Bakersfield

The State of the Economy: Kern County, California Summary Abbas P. Grammy 1 Professor of Economics California State University, Bakersfield Kern County households follow national trends. They turned less

The State of the Economy: Kern County, California Summary Abbas P. Grammy 1 Professor of Economics California State University, Bakersfield Kern County households follow national trends. They turned less

44 ECB STOCK MARKET DEVELOPMENTS IN THE LIGHT OF THE CURRENT LOW-YIELD ENVIRONMENT

Box STOCK MARKET DEVELOPMENTS IN THE LIGHT OF THE CURRENT LOW-YIELD ENVIRONMENT Stock market developments are important for the formulation of monetary policy for several reasons. First, changes in stock

Box STOCK MARKET DEVELOPMENTS IN THE LIGHT OF THE CURRENT LOW-YIELD ENVIRONMENT Stock market developments are important for the formulation of monetary policy for several reasons. First, changes in stock

Better domestic economy but lower rates

ZACH PANDL, PORTFOLIO MANAGER AND STRATEGIST 215 PERSPECTIVES INTEREST RATES: FAREWELL, LIQUIDITY TRAP With continued growth and further improvement in labor markets, the Federal Reserve (the Fed) looks

ZACH PANDL, PORTFOLIO MANAGER AND STRATEGIST 215 PERSPECTIVES INTEREST RATES: FAREWELL, LIQUIDITY TRAP With continued growth and further improvement in labor markets, the Federal Reserve (the Fed) looks