Microfinance in Peru: Key Findings and Perspectives

|

|

|

- Horatio Lawson

- 10 years ago

- Views:

Transcription

1 2011/GFPN/WKSP/010 Session 3 Microfinance in Peru: Key Findings and Perspectives Submitted by: Profinanzas Workshop on Microfinance Best Practices Ha Noi, Viet Nam 7-8 April 2011

2 Maria Rosa Morán Member of the Board of Directors of PROFINANZAS Microfinance Leaders Association Asomif Perú 1

3 ABOUT US 2 "MICROFINANCE IN PERÚ: Key Findings And Perspectives Presented by: Maria Rosa Morán APEC Summit, April 2011, Vietnam 2

4 AGENDA 1. The Peruvian Socioeconomic Context 1. The Peruvian Socioeconomic Context 2. The Microfinance Demand 2. The Microfinance Demand 3. The Peru Case Study 3. The Peru Case Study 4. Conclusions and Perspectives 4. Conclusions and Perspectives MACROECONOMIC CONTEXT Peru has been a top performer in LA since In 2008, the Peruvian GDP grew by 9.8%, one of the highest growth rates in the world. Peru s outstanding t indicators and solid fiscal position have prompted several international risk classifiers to grant the country an investment grade. 3

5 MACROECONOMIC CONTEXT GDP Growth 12.00% 10.00% 8.00% 6.00% 4.00% 2.00% 000% 0.00% % MACROECONOMIC CONTEXT Nevertheless: 36.2% of Peru s population lives in poverty, 12.6% in extreme poverty. The country is currently working towards a reduction to 11.5 % by 2015; unfortunately, inequalities between urban and rural areas have increased. The highland and jungle areas register the highest percentages of the population in extreme poverty: 37.4% and 20.7% respectively. 4

6 MACROECONOMIC CONTEXT POVERTY LEVELS ARE DECREASING BUT STILL HIGH PERU: POVERTY INCIDENCE (%) MICROFINANCE DEMAND Micro or Small Company (SME s) By the number of workers, employs to 10 or 100 workers. By annual sales, sells or 170,000 Euros approx. Currently the 98.6% of the total number of business are SME s, approx million; they generate 77% of employment and explain the 42.1% of the Peruvian GDP. However, most of the SMEs (72.6%) are in the informal sector, in particular the micro. 5

7 MICROFINANCE DEMAND Micro or Small Company (SME s) Only 18% have Tax Registration Number and 75% has no operating license. They have low productivity. On annual average, a worker in a micro and small business generates 3,870 Euros and 15,390 Euros, respectively, while the average of the medium and large company is around 27,700 Euros. World Bank: 60% of the Peruvian economy is informal. MICROFINANCE DEMAND TWO DIFFERENT WORLDS TRADITIONAL BANKERS MICROENTREPRENEURS 6

8 PERUVIAN MODEL Is there a Peruvian Microfinance Model? PERUVIAN MODEL OVERALL MICROFINANCE BUSINESS ENVIRONMENT RANKINGS Rank Country Score Score change Perú Philippines Bolivia Ghana Pakistan Ecuador El Salvado India Kenya

9 IMF s CREDIT PORTFOLIO EVOLUTION December 2010 (millions of nuevos soles) Growth 7% 19,258 11,121 15,345 7, Fuente: S.B.S. Elaboración: Área de Estadística Asomif Perú 6 IMF s SAVINGS EVOLUTION December 2010 (millions of nuevos soles) Growth 182%,868 7,413 10,907 5, Fuente: S.B.S. Elaboración: Área de Estadística Asomif Perú 9 8

Growth 182%,868 7,413 10,907 5,273 2010 2009 2008 2007 Fuente: S.B.")

10 IMF s OFFICES GROWT December 2010 (percentage) Fuente: S.B.S. Elaboración: Área de Estadística Asomif Perú 21 IMF S JOBS GROWTH December 2010 (Percentage) 27,122 12,542 16,674 22,423 8,435 39% 10,089 19% 24% 33% 35% 18% Crec Fuente: S.B.S. Elaboración: Área de Estadística Asomif Perú 22 9

27,122 12,542 16,674 22,423 8,435 39% 10,089 19% 24% 33% 35%")

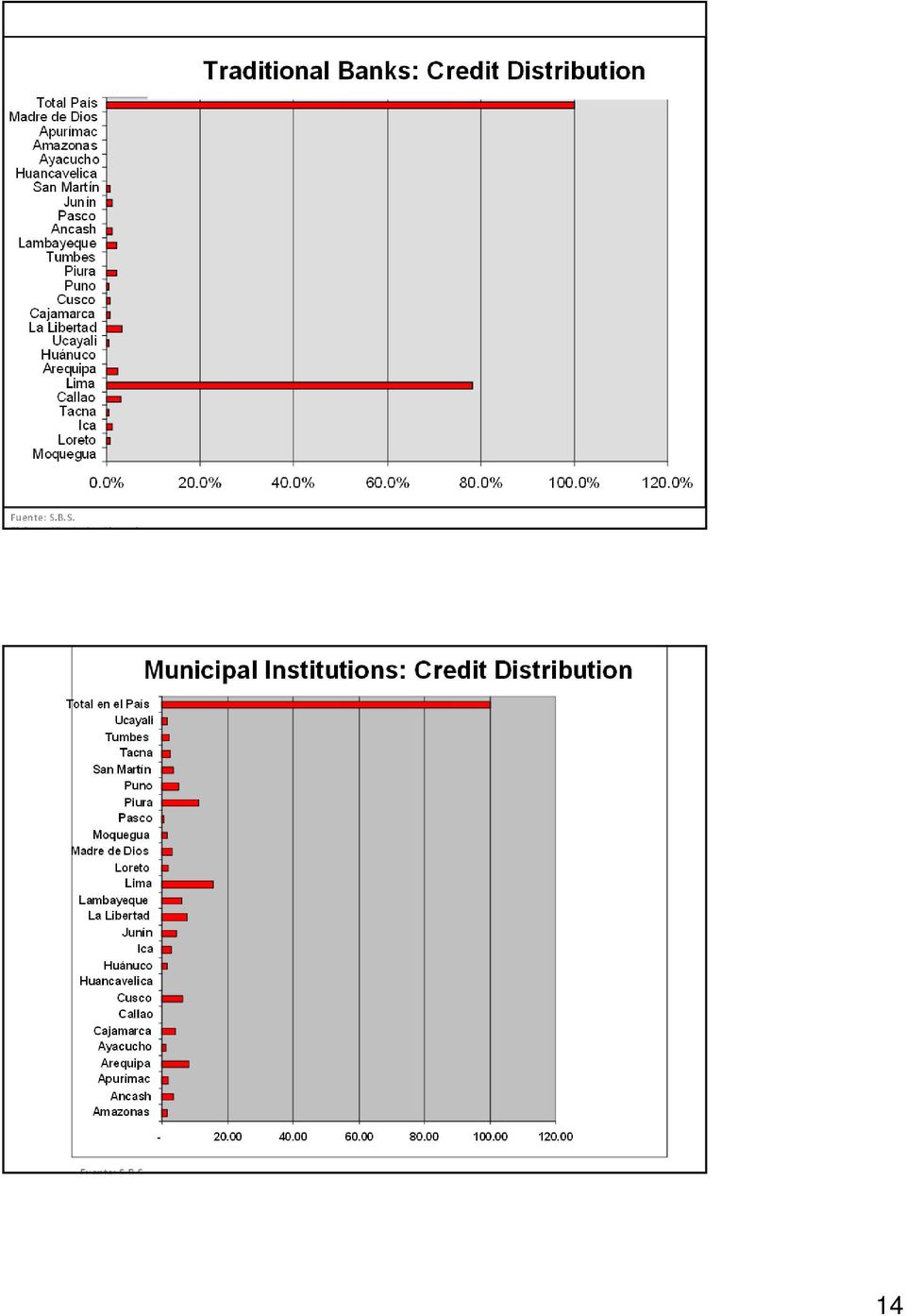

11 PERUVIAN MODEL PERUVIAN FINANCIAL SYSTEM Number of Assets Companies % Traditional Banks Financial Companies Microfinance Companies no Banks Municipal Institutions Rural Institutions Edpymes State Banking Banco de la Nacion Agrobanco Leasing Companies PERUVIAN MODEL PERU: MICROFINANCE MARKET Traditional Banking System: 88.6% of savings and 84.3% of loans. Microfinance System: 11.4% of savings and 15.6% of loans. Number of borrowers in the financial system: 6, microfinance system serves 42.2% of them!!! 10

12 PERUVIAN MODEL WOMEN'S ACCESS TO CREDIT (Dec. 2009) Tradicional Banks: 26% Rural & Municipal Institutions: 38% Edpymes: 58% Fuente: SBS PERUVIAN MODEL 75% OF THE MICROENTREPRENEURS ARE IMFs CLIENTS Deudores por Microcréditos del Sistema Financiero Peruano (%) Junio 2009 Microcredit clients in the Peruvian Finance System Deudores Compartidos 15 % Bancos y financieras no especializadas 11 % Bancos y financieras especializados 24 % Microfinancieras no bancarias 50 % >>Total de deudores por microcréditos del Sistema Financiero Peruano: 1,257,162 Fuente: SBS 11

13 PERUVIAN MODEL Main Features: Commercial approach (self-sustaining), Market Driven Model Individual Credit = Credit Group Urban portfolio (more lucrative) Political Independent No subsides Size of MFIs Products Diversification PERUVIAN MODEL Main Features: Funding Sources Credit culture Enabling regulatory and institutional environment Upgrading & Downscaling Still a unmet demand 12

14 PERUVIAN MODEL Credit Methodology: Analyst Omnipresent Analysis In Situ No collaterals Cash Flow Speed and customer proximity Simple and Friendly Procedures Long Term Relationship 13

15

16 CONCLUSIONS & PERSPECTIVES MAIN THREATS Higher incidence of Administrative costs scale!!. Population Geographically dispersed. Costs in time and resources due to complexity of legal and regulatory framework. Taxes to credit lines (30% + 19% (Income and Sales Tax)). Collateral reduce risk but increase credit cost. High costs in resolving conflicts due to Peruvian judicial system inefficiencies. CONCLUSIONS & PERSPECTIVES MAIN THREATS Traditional banks Downscaling Entry of participants without expertise in the sector..increased competition can lead to overindebtedness of clients Decreased of low-cost funding Excessive regulation can harm smaller entities Increasing government intervention may affect the sector 15

17 CONCLUSIONS & PERSPECTIVES MAIN SUCCESS FACTORS "Double Profit : Profits and social responsibility are compatible!!! Credit portfolio management Products Tailored Decentralized business model Informal sector, tailored to economic swings, flexibility, etc. Atomized portfolio, business model people-intensive, mixed public-private funding CONCLUSIONS & PERSPECTIVES SUCCESS FACTORS " Conservative provisions and uncollectible of default loans Microcredit = Microfinance One stop shop for all finance needs: Microcredit, Savings, Remittances, microinsures Mortgage, vehicles, microleasing, machinery, among others Debit cards, ATM Machines, Micro rural loans Rural structured loans (advised and supervised) Among, others 16

18 CONCLUSIONS & PERSPECTIVES Pervian Microfinance Case Study has shown that supporting Micro and Small enterprises and ensuring broad acces to financial services, is not only a tool to the succes of democratization of credit but also an effective instrument to fight poverty!!! 3 17

19 María Rosa Morán 18

FINANCIAL INCLUSION INDICATORS FOR DEVELOPING COUNTRIES: The Peruvian Case

FINANCIAL INCLUSION INDICATORS FOR DEVELOPING COUNTRIES: The Peruvian Case Mrs. Giovanna Priale Reyes Head of the Office of Products and Services to the Consumer [email protected] Superintendency of Banking,

FINANCIAL INCLUSION INDICATORS FOR DEVELOPING COUNTRIES: The Peruvian Case Mrs. Giovanna Priale Reyes Head of the Office of Products and Services to the Consumer [email protected] Superintendency of Banking,

Microfinance Regulation in Peru: Current State, Lessons Learned and Prospects for the Future

ESSAYS ON REGULATION AND SUPERVISION Microfinance Regulation in Peru: Current State, Lessons Learned and Prospects for the Future ALFREDO EBENTREICH April 2005 ESSAYS ON REGULATION AND SUPERVISION No.4

ESSAYS ON REGULATION AND SUPERVISION Microfinance Regulation in Peru: Current State, Lessons Learned and Prospects for the Future ALFREDO EBENTREICH April 2005 ESSAYS ON REGULATION AND SUPERVISION No.4

Access to Financial Services in Developing Countries: Identification of Obstacles. Liliana Rojas-Suárez July 2006

Access to Financial Services in Developing Countries: Identification of Obstacles Liliana Rojas-Suárez July 2006 Background Even though banks are the most important providers of financial services Evolution

Access to Financial Services in Developing Countries: Identification of Obstacles Liliana Rojas-Suárez July 2006 Background Even though banks are the most important providers of financial services Evolution

THE VALUE OF MICROLENDING IN EMERGING ECONOMIES THE CASE OF BRAZIL

THE VALUE OF MICROLENDING IN EMERGING ECONOMIES THE CASE OF BRAZIL Celson Hupfer Banco Itaú Defining Microlending Credit to poor people or micro-entrepreneurs without access to formal credit sources very

THE VALUE OF MICROLENDING IN EMERGING ECONOMIES THE CASE OF BRAZIL Celson Hupfer Banco Itaú Defining Microlending Credit to poor people or micro-entrepreneurs without access to formal credit sources very

SME Banking-Africa. A Unique Opportunity for the Continent

SME Banking-Africa A Unique Opportunity for the Continent Key Messages More to be done The opportunity Challenges in SME financing Profitable segment A proposed solution 2 SMEs in Africa- The Missing Middle

SME Banking-Africa A Unique Opportunity for the Continent Key Messages More to be done The opportunity Challenges in SME financing Profitable segment A proposed solution 2 SMEs in Africa- The Missing Middle

The Impact of Interest Rate Ceilings on Microfinance Industry

The Impact of Interest Rate Ceilings on Microfinance Industry Ali Saleh Alshebami School of Commerce & Management Science, SRTM University, India E-mail: [email protected] Prof. D. M. Khandare School

The Impact of Interest Rate Ceilings on Microfinance Industry Ali Saleh Alshebami School of Commerce & Management Science, SRTM University, India E-mail: [email protected] Prof. D. M. Khandare School

IMPACT OF MICROINSURANCE REGULATION IN PERU. Carla Chiappe Villegas Superintendency of Banking, Insurance and Private Pensions Funds Administrators

IMPACT OF MICROINSURANCE REGULATION IN PERU Carla Chiappe Villegas Superintendency of Banking, Insurance and Private Pensions Funds Administrators Superficie: 1 285 216 Km2 Población Total: 29 461 933

IMPACT OF MICROINSURANCE REGULATION IN PERU Carla Chiappe Villegas Superintendency of Banking, Insurance and Private Pensions Funds Administrators Superficie: 1 285 216 Km2 Población Total: 29 461 933

Microfinance Institution Life Cycle Case Study

Publication Series Microfinance Institution Life Cycle Case Study Financiera Edyficar, Peru Kathleen Dischner, Treetops Capital Mike Gabriel, Grameen Foundation April 2009 www.grameenfoundation.org i 2009

Publication Series Microfinance Institution Life Cycle Case Study Financiera Edyficar, Peru Kathleen Dischner, Treetops Capital Mike Gabriel, Grameen Foundation April 2009 www.grameenfoundation.org i 2009

SECTOR ASSESSMENT: MICROFINANCE

Microfinance Development Program Cluster (Subprogram 1) (RRP VIE 42235-01) A. Overall Sector Context SECTOR ASSESSMENT: MICROFINANCE 1. Poverty Reduction Objectives and Measures. About 72% of the population

Microfinance Development Program Cluster (Subprogram 1) (RRP VIE 42235-01) A. Overall Sector Context SECTOR ASSESSMENT: MICROFINANCE 1. Poverty Reduction Objectives and Measures. About 72% of the population

Comprise resident commercial banks and other banks functioning as commercial banks that meet the definition of ODCs.

Other depository corporations (ODCs) Comprise commercial banks, credit unions and financial cooperatives, deposit taking microfinance institutions, and other deposit takers. These include all resident

Other depository corporations (ODCs) Comprise commercial banks, credit unions and financial cooperatives, deposit taking microfinance institutions, and other deposit takers. These include all resident

FIRST ANNUAL REPORT ON THE LATIN AMERICA SMALL BUSINESS LENDING INITIATIVE AUGUST 2008

FIRST ANNUAL REPORT ON THE LATIN AMERICA SMALL BUSINESS LENDING INITIATIVE AUGUST 2008 I. OVERVIEW This report summarizes the first year of implementation of the Latin America Small Business Lending Initiative

FIRST ANNUAL REPORT ON THE LATIN AMERICA SMALL BUSINESS LENDING INITIATIVE AUGUST 2008 I. OVERVIEW This report summarizes the first year of implementation of the Latin America Small Business Lending Initiative

ADS Chapter 219 Microenterprise Development

Microenterprise Development Document Quality Check Date: 02/08/2013 Partial Revision Date: 07/08/2011 Responsible Office: E3 File Name: 219_020813 Functional Series 200 Programming Policy Microenterprise

Microenterprise Development Document Quality Check Date: 02/08/2013 Partial Revision Date: 07/08/2011 Responsible Office: E3 File Name: 219_020813 Functional Series 200 Programming Policy Microenterprise

10th ANIVERSARY SULAMERICA INVESTIMENTOS

10th ANIVERSARY SULAMERICA INVESTIMENTOS AGENDA 1. Perú Macro Environment 2. The need for a Pension System Reform 3. The Private Pension System 4. AFP Integra 5. Multifondos 6. The Future 1 1. Peru - Macro

10th ANIVERSARY SULAMERICA INVESTIMENTOS AGENDA 1. Perú Macro Environment 2. The need for a Pension System Reform 3. The Private Pension System 4. AFP Integra 5. Multifondos 6. The Future 1 1. Peru - Macro

Ghana s Legal Framework for Secured Transactions

Ghana s Legal Framework for Secured Transactions M A R E K D U B O V E C M D U B O V E C @ N A T L A W.C O M Organization of the Presentation 1) Current Substantive Legal Framework 2) Assessment against

Ghana s Legal Framework for Secured Transactions M A R E K D U B O V E C M D U B O V E C @ N A T L A W.C O M Organization of the Presentation 1) Current Substantive Legal Framework 2) Assessment against

Microfinance in Cambodia

Microfinance in Cambodia Investors playground or force for financial inclusion? Sanjay Sinha M-CRIL, December 2013 Introduction to the social investors playground Cambodia is one of the smaller countries

Microfinance in Cambodia Investors playground or force for financial inclusion? Sanjay Sinha M-CRIL, December 2013 Introduction to the social investors playground Cambodia is one of the smaller countries

Fine-Tuning Regulation based on Access Indicators

Fine-Tuning Regulation based on Access Indicators Fiorella Arbulú Díaz 1 / Abstract This document highlights the importance of financial inclusion data in the policymaking process. In particular, it describes

Fine-Tuning Regulation based on Access Indicators Fiorella Arbulú Díaz 1 / Abstract This document highlights the importance of financial inclusion data in the policymaking process. In particular, it describes

SBP s Seminar on Housing Microfinance. Low Income Housing and Housing Finance

SBP s Seminar on Housing Microfinance Low Income Housing and Housing Finance Syed Farhan Fasihuddin September 06, 2012 [email protected] Karachi, Pakistan Content 1. Terminology 2. Low Income Housing

SBP s Seminar on Housing Microfinance Low Income Housing and Housing Finance Syed Farhan Fasihuddin September 06, 2012 [email protected] Karachi, Pakistan Content 1. Terminology 2. Low Income Housing

Small Business Banking perspective. Syed Mahbubur Rahman Managing Director & CEO

Small Business Banking perspective Syed Mahbubur Rahman Managing Director & CEO BRAC Bank Beginning of the Journey Small and Medium size Enterprises (SMEs) in Bangladesh did not have access to banks and

Small Business Banking perspective Syed Mahbubur Rahman Managing Director & CEO BRAC Bank Beginning of the Journey Small and Medium size Enterprises (SMEs) in Bangladesh did not have access to banks and

Marketing to the Private Health Sector

Marketing to the Private Health Sector Understanding the Market is a Key to Success This guide s previous section established that the private health sector is growing and offers attractive market opportunities

Marketing to the Private Health Sector Understanding the Market is a Key to Success This guide s previous section established that the private health sector is growing and offers attractive market opportunities

SECTOR ASSESSMENT (SUMMARY): FINANCE

: FINANCE") Microfinance Expansion Project (RRP PNG 44304) Sector Road Map SECTOR ASSESSMENT (SUMMARY): FINANCE 1. Sector Performance, Problems, and Opportunities 1. During 2000 2006, the growth in population in Papua

Microfinance Expansion Project (RRP PNG 44304) Sector Road Map SECTOR ASSESSMENT (SUMMARY): FINANCE 1. Sector Performance, Problems, and Opportunities 1. During 2000 2006, the growth in population in Papua

Contest. Gobernarte: The Art of Good Government. Eduardo Campos Award. 2015 Third Edition

Contest Gobernarte: The Art of Good Government Eduardo Campos Award 2015 Third Edition 1 Gobernarte: The Art of Good Government The purpose of the Gobernarte contest is to identify, reward, document, and

Contest Gobernarte: The Art of Good Government Eduardo Campos Award 2015 Third Edition 1 Gobernarte: The Art of Good Government The purpose of the Gobernarte contest is to identify, reward, document, and

Colloquium on microfinance

Harnessing the power of credit reporting systems UNCITRAL Colloquium on microfinance Vienna, 18 th January 2013 FABRIZIO FRABONI Responsible Finance The Counter Balance More than 2.7 billion people and

Harnessing the power of credit reporting systems UNCITRAL Colloquium on microfinance Vienna, 18 th January 2013 FABRIZIO FRABONI Responsible Finance The Counter Balance More than 2.7 billion people and

Microfinance in Egypt:

The Egyptian financial Supervisory authority Microfinance in Egypt: An Overview Ghada Waly Advisor to the Chairman for Microfinance EFSA Content Definition of Microfinance (MF) Historical Background of

The Egyptian financial Supervisory authority Microfinance in Egypt: An Overview Ghada Waly Advisor to the Chairman for Microfinance EFSA Content Definition of Microfinance (MF) Historical Background of

SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities

: MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities") Small Business and Entrepreneurship Development Project (RRP UZB 42007-014) SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems,

Small Business and Entrepreneurship Development Project (RRP UZB 42007-014) SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems,

FINANCIAL INCLUSION INDICATORS FOR DEVELOPING COUNTRIES: The Peruvian Case

FINANCIAL INCLUSION INDICATORS FOR DEVELOPING COUNTRIES: The Peruvian Case Giovanna Prialé Reyes, SBS Peru,* Luis Daniel Allaín Cañote, SBS Peru, * and Rafe Mazer, CGAP I. Introduction The importance of

FINANCIAL INCLUSION INDICATORS FOR DEVELOPING COUNTRIES: The Peruvian Case Giovanna Prialé Reyes, SBS Peru,* Luis Daniel Allaín Cañote, SBS Peru, * and Rafe Mazer, CGAP I. Introduction The importance of

S.B.S. Resolution Nº 1928-2015 The Head of the Superintendency of Banks, Insurance Companies and Private Pension Fund Administrators

Waiver of Responsibility The law and any other regulation translated into English are only referential. The official language for any legal purposes is Spanish as published in the Official Journal El Peruano.

Waiver of Responsibility The law and any other regulation translated into English are only referential. The official language for any legal purposes is Spanish as published in the Official Journal El Peruano.

MICROFINANCE. Orrick, Herrington & Sutcliffe. Legal guide. Type: Published: Last Updated: Keywords: Microfinance; lending; development.

MICROFINANCE Orrick, Herrington & Sutcliffe Type: Published: Last Updated: Keywords: Legal guide Microfinance; lending; development. This document provides general information and comments on the subject

MICROFINANCE Orrick, Herrington & Sutcliffe Type: Published: Last Updated: Keywords: Legal guide Microfinance; lending; development. This document provides general information and comments on the subject

IFC Secured Transactions Advisory Project in China

IFC Secured Transactions Advisory Project in China 1 Background In 2004, the People s Bank of China (PBOC) recognized wide spread financing difficulties among small and medium enterprises (SMEs) and requested

IFC Secured Transactions Advisory Project in China 1 Background In 2004, the People s Bank of China (PBOC) recognized wide spread financing difficulties among small and medium enterprises (SMEs) and requested

Zurich Venezuela: Providing insurance to Venezuela s low-income population

Zurich Venezuela: Providing insurance to Venezuela s low-income population What once started with a coffee chat between a priest and the President of Zurich Venezuela on a Sunday morning after church service

Zurich Venezuela: Providing insurance to Venezuela s low-income population What once started with a coffee chat between a priest and the President of Zurich Venezuela on a Sunday morning after church service

Global South-South Development EXPO 2014

Global South-South Development EXPO 2014 ILO Solution Forum: Microinsurance Washington DC, 19 November 2014 What do the working poor need? Opportunity: government policy, action Organisation: Co-ops, MFIs,

Global South-South Development EXPO 2014 ILO Solution Forum: Microinsurance Washington DC, 19 November 2014 What do the working poor need? Opportunity: government policy, action Organisation: Co-ops, MFIs,

Developing Kenya s Mortgage Market

Developing Kenya s Mortgage Market Simon Walley Senior Housing Finance Specialist World Bank 17 February, 2011 - Nairobi Outline Rationale for developing the mortgage market Mortgage Market Summary Housing

Developing Kenya s Mortgage Market Simon Walley Senior Housing Finance Specialist World Bank 17 February, 2011 - Nairobi Outline Rationale for developing the mortgage market Mortgage Market Summary Housing

Table 1.1 TOTAL FACTORING VOLUME BY COUNTRY IN THE LAST 10 YEARS (MILLIONS OF EUROS)

") INTRODUCTION Factoring is a financial option for the management of receivables. In simple word it is the conversion of credit sales into cash. In factoring, a financial institution (factor) buys the accounts

INTRODUCTION Factoring is a financial option for the management of receivables. In simple word it is the conversion of credit sales into cash. In factoring, a financial institution (factor) buys the accounts

Liberia Leasing Investment Forum

Finance Leasing in Liberia: Unlocking Accelerated Market and Business Development Adopting Best Practice Models to Make Leasing Work in Liberia Minerva Kotei Monrovia, A 40 Year Commitment to Leasing A

Finance Leasing in Liberia: Unlocking Accelerated Market and Business Development Adopting Best Practice Models to Make Leasing Work in Liberia Minerva Kotei Monrovia, A 40 Year Commitment to Leasing A

Village banks: the new generation. How IFAD helped FINCA set its village banking programmes on the road to commercialization

Village banks: the new generation How IFAD helped FINCA set its village banking programmes on the road to commercialization What is FINCA? FINCA International, Inc. provides financial services to the world

Village banks: the new generation How IFAD helped FINCA set its village banking programmes on the road to commercialization What is FINCA? FINCA International, Inc. provides financial services to the world

Facilitating Remittances to Help Families and Small Businesses

G8 ACTION PLAN: APPLYING THE POWER OF ENTREPRENEURSHIP TO THE ERADICATION OF POVERTY The UN Commission on the Private Sector and Development has stressed that poverty alleviation requires a strong private

G8 ACTION PLAN: APPLYING THE POWER OF ENTREPRENEURSHIP TO THE ERADICATION OF POVERTY The UN Commission on the Private Sector and Development has stressed that poverty alleviation requires a strong private

RURAL AND AGRICULTURE FINANCE Prof. Puneetha Palakurthi School of Community Economic Development Sothern New Hampshire University

RURAL AND AGRICULTURE FINANCE Prof. Puneetha Palakurthi School of Community Economic Development Sothern New Hampshire University DRIVERS OF RURAL DEVELOPMENT High overall economic growth Effective land

RURAL AND AGRICULTURE FINANCE Prof. Puneetha Palakurthi School of Community Economic Development Sothern New Hampshire University DRIVERS OF RURAL DEVELOPMENT High overall economic growth Effective land

4. Conducting performance monitoring and evaluation

60 4. Conducting performance monitoring and evaluation IFAD DECISION TOOLS FOR RURAL FINANCE 4. Conducting performance monitoring and evaluation Action: Effectively conduct ongoing and annual performance

60 4. Conducting performance monitoring and evaluation IFAD DECISION TOOLS FOR RURAL FINANCE 4. Conducting performance monitoring and evaluation Action: Effectively conduct ongoing and annual performance

University meets Microfinance. Do our clients grow? - Microfinance vs. SME Finance

University meets Microfinance Do our clients grow? - Microfinance vs. SME Finance July 2012 Definition(s) of MSME Definitions vary greatly between countries, financial regulators and financial institutions.

University meets Microfinance Do our clients grow? - Microfinance vs. SME Finance July 2012 Definition(s) of MSME Definitions vary greatly between countries, financial regulators and financial institutions.

Chile: Microloans programme (CORFO) (interest rate reduction) 24030 - Financial intermediaries in the formal sector 2002 66 866 (2009 random sample)

(interest rate reduction) 24030 - Financial intermediaries in the formal sector 2002 66 866 (2009 random sample)") Chile: Microloans programme (CORFO) (interest rate reduction) Ex post evaluation report OECD sector BMZ project ID Project executing agency Consultant 24030 - Financial intermediaries in the formal sector

Chile: Microloans programme (CORFO) (interest rate reduction) Ex post evaluation report OECD sector BMZ project ID Project executing agency Consultant 24030 - Financial intermediaries in the formal sector

Financial Services that Clients Need - The 3.0 Business Models - Reconciling Outreach with Sustainability

Financial Services that Clients Need - The 3.0 Business Models - Reconciling Outreach with Sustainability Berlin, 29 November 2012 Robert Peck Christen Maxwell School of Citizenship and Public Affairs,

Financial Services that Clients Need - The 3.0 Business Models - Reconciling Outreach with Sustainability Berlin, 29 November 2012 Robert Peck Christen Maxwell School of Citizenship and Public Affairs,

Contents. 1 Peru: Atractive economy and financial system 2 Organization 3 BBVA Continental vs. Peers 4 Social responsibility and Awards 5 Ratings

March 2013 Disclaimer This document has been elaborated as a part of the information policies and transparency of BBVA Continental and contains public information, own source and provided by third parties,

March 2013 Disclaimer This document has been elaborated as a part of the information policies and transparency of BBVA Continental and contains public information, own source and provided by third parties,

Two trillion and counting

Two trillion and counting Assessing the credit gap for micro, small, and medium-size enterprises in the developing world OCTOBER 2010 Peer Stein International Finance Corporation Tony Goland McKinsey &

Two trillion and counting Assessing the credit gap for micro, small, and medium-size enterprises in the developing world OCTOBER 2010 Peer Stein International Finance Corporation Tony Goland McKinsey &

Central Banks and the Development Agenda The CBN Experience Sadiq Usman 1 Presentation Outline 2 Slide Introduction Brief on Nigeria The recent Banking Crisis CBN Developmental Activities CBN Interventions

Central Banks and the Development Agenda The CBN Experience Sadiq Usman 1 Presentation Outline 2 Slide Introduction Brief on Nigeria The recent Banking Crisis CBN Developmental Activities CBN Interventions

BALANCE SHEET AND INCOME STATEMENT

BANCOLOMBIA S.A. (NYSE: CIB; BVC: BCOLOMBIA, PFBCOLOM) REPORTS CONSOLIDATED NET INCOME OF COP 1,879 BILLION FOR 2014, AN INCREASE OF 24% COMPARED TO 2013. Operating income increased 23.8% during 2014 and

BANCOLOMBIA S.A. (NYSE: CIB; BVC: BCOLOMBIA, PFBCOLOM) REPORTS CONSOLIDATED NET INCOME OF COP 1,879 BILLION FOR 2014, AN INCREASE OF 24% COMPARED TO 2013. Operating income increased 23.8% during 2014 and

Value of information

5th FINANCIAL INFRASTRUCTURE AND RISK MANAGEMENT TRAINING Value of information Mohamed Refaat El-Houshi,MBA Managing Director I-Score Egypt Rabat - 22-25 September, 2014 Session 2. 1 Presentation Content

5th FINANCIAL INFRASTRUCTURE AND RISK MANAGEMENT TRAINING Value of information Mohamed Refaat El-Houshi,MBA Managing Director I-Score Egypt Rabat - 22-25 September, 2014 Session 2. 1 Presentation Content

$100 change. How can. aneconomy. Microfinance and Microcredit. One small loan can change a family.

How can Microfinance and Microcredit $100 change aneconomy? It could be for a new tool, a machine, or a shop in the marketplace millions of the world s poor and low-income people have taken advantage of

How can Microfinance and Microcredit $100 change aneconomy? It could be for a new tool, a machine, or a shop in the marketplace millions of the world s poor and low-income people have taken advantage of

A Business Case for Microinsurance

A Business Case for Microinsurance Munich Re Microinsurance Conference 2010 Presented by Doug Lacey November 2010 Agenda Purpose and methodology Experiences with insurers Framework for assessing profitability

A Business Case for Microinsurance Munich Re Microinsurance Conference 2010 Presented by Doug Lacey November 2010 Agenda Purpose and methodology Experiences with insurers Framework for assessing profitability

Building the Capacity of BMOs: Guiding Principles for Project Managers

Paris, 1-2 February 2006 www.publicprivatedialogue.org RESOURCE BUILDING AND MAINTAINING BUSINESS MEMBERSHIP ORGANIZATIONS Building the Capacity of BMOs: Guiding Principles for Project Managers Andrei

Paris, 1-2 February 2006 www.publicprivatedialogue.org RESOURCE BUILDING AND MAINTAINING BUSINESS MEMBERSHIP ORGANIZATIONS Building the Capacity of BMOs: Guiding Principles for Project Managers Andrei

Ministerie van Toerisme, Economische Zaken, Verkeer en Telecommunicatie Ministry of Tourism, Economic Affairs, Transport and Telecommunication

SME Policy Framework for St. Maarten May, 2014 Department of Economic Affairs, Transportation & P. 1 of 16 TABLE OF CONTENTS 1. Introduction 2. SME Developments in St. Maarten 2.1 Definition 2.2 Government

SME Policy Framework for St. Maarten May, 2014 Department of Economic Affairs, Transportation & P. 1 of 16 TABLE OF CONTENTS 1. Introduction 2. SME Developments in St. Maarten 2.1 Definition 2.2 Government

Thierry Tressel Lead Economist, Research Group, World Bank 2015 High Level Caribbean Forum, Sept. 3-4 2015, St. Kitts

Thierry Tressel Lead Economist, Research Group, World Bank 215 High Level Caribbean Forum, Sept. 3-4 215, St. Kitts Policy issue Focus on SMEs: they are the biggest contributors to employment across countries,

Thierry Tressel Lead Economist, Research Group, World Bank 215 High Level Caribbean Forum, Sept. 3-4 215, St. Kitts Policy issue Focus on SMEs: they are the biggest contributors to employment across countries,

FINANCE AND BUSINESS DEVELOPMENT SERVICES FOR ENTREPRENEURSHIP DEVELOPMENT: (SME lending in Kenya, from microfinance institution to SME bank )

") FINANCE AND BUSINESS DEVELOPMENT SERVICES FOR ENTREPRENEURSHIP DEVELOPMENT: (SME lending in Kenya, from microfinance institution to SME bank ) What is K-Rep Bank Vision - Mission- To be the financial services

FINANCE AND BUSINESS DEVELOPMENT SERVICES FOR ENTREPRENEURSHIP DEVELOPMENT: (SME lending in Kenya, from microfinance institution to SME bank ) What is K-Rep Bank Vision - Mission- To be the financial services

An Inside View of Microcredit in Panama: The Financial Investment in MFIs

Economics World, June 2015, Vol. 3, No. 5-6, 128-136 doi: 10.17265/2328-7144/2015.0506.002 D DAVID PUBLISHING An Inside View of Microcredit in Panama: The Financial Investment in MFIs Anna Paola Micheli

Economics World, June 2015, Vol. 3, No. 5-6, 128-136 doi: 10.17265/2328-7144/2015.0506.002 D DAVID PUBLISHING An Inside View of Microcredit in Panama: The Financial Investment in MFIs Anna Paola Micheli

SECTOR ASSESSMENT (SUMMARY): FINANCE 1. 1. Sector Performance, Problems, and Opportunities

: FINANCE 1. 1. Sector Performance, Problems, and Opportunities") Country Partnership Strategy: Bangladesh, 2011 2015 SECTOR ASSESSMENT (SUMMARY): FINANCE 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. The finance sector in Bangladesh is diverse,

Country Partnership Strategy: Bangladesh, 2011 2015 SECTOR ASSESSMENT (SUMMARY): FINANCE 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. The finance sector in Bangladesh is diverse,

Pricing Disclosure and Truth-in- Lending Policy: International Examples and Standards

Promoting Transparent Pricing in the Microfinance Industry Pricing Disclosure and Truth-in- Lending Policy: International Examples and Standards October 2011 What can we learn from truth-in-lending legislation?

Promoting Transparent Pricing in the Microfinance Industry Pricing Disclosure and Truth-in- Lending Policy: International Examples and Standards October 2011 What can we learn from truth-in-lending legislation?

IOE PERSPECTIVES ON THE POST 2015 DEVELOPMENT AGENDA JANUARY 2013

IOE PERSPECTIVES ON THE POST 2015 DEVELOPMENT AGENDA JANUARY 2013 INTERNATIONAL ORGANISATION OF EMPLOYERS Disclaimer Articles posted on the website are made available by the UNCTAD secretariat in the form

IOE PERSPECTIVES ON THE POST 2015 DEVELOPMENT AGENDA JANUARY 2013 INTERNATIONAL ORGANISATION OF EMPLOYERS Disclaimer Articles posted on the website are made available by the UNCTAD secretariat in the form

THE ACCESS TO FINANCE IN MOLDOVA - BANKING COMPARED TO MICROFINANCE ORGANIZATIONS

THE ACCESS TO FINANCE IN MOLDOVA - BANKING COMPARED TO MICROFINANCE ORGANIZATIONS Viorica POPA, PhD Student Abstract The objective of this article is the comparative analysis of the banking sector with

THE ACCESS TO FINANCE IN MOLDOVA - BANKING COMPARED TO MICROFINANCE ORGANIZATIONS Viorica POPA, PhD Student Abstract The objective of this article is the comparative analysis of the banking sector with

ROLE OF THE BANKING SECTOR IN PROMOTING GROWTH & DEVELOPMENT OF SMALL AND MEDIUM ENTERPRISES ADDRESS DR. C. L. DHLIWAYO ACTING GOVERNOR MARCH 2014

ROLE OF THE BANKING SECTOR IN PROMOTING GROWTH & DEVELOPMENT OF SMALL AND MEDIUM ENTERPRISES ADDRESS BY DR. C. L. DHLIWAYO ACTING GOVERNOR AT THE 2 ND SME BANKING & MICROFINANCE SUMMIT 2014 MARCH 2014

ROLE OF THE BANKING SECTOR IN PROMOTING GROWTH & DEVELOPMENT OF SMALL AND MEDIUM ENTERPRISES ADDRESS BY DR. C. L. DHLIWAYO ACTING GOVERNOR AT THE 2 ND SME BANKING & MICROFINANCE SUMMIT 2014 MARCH 2014

Managing Human Resources in Small and Medium Enterprises (SMEs) in Developing Countries: A Research Agenda for Bangladesh SMEs

in Developing Countries: A Research Agenda for Bangladesh SMEs") DOI: 10.7763/IPEDR. 2012. V55. 43 Managing Human Resources in Small and Medium Enterprises (SMEs) in Developing Countries: A Research Agenda for Bangladesh SMEs Mohammad A Arafat 1 and Dr Ezaz Ahmed 2

DOI: 10.7763/IPEDR. 2012. V55. 43 Managing Human Resources in Small and Medium Enterprises (SMEs) in Developing Countries: A Research Agenda for Bangladesh SMEs Mohammad A Arafat 1 and Dr Ezaz Ahmed 2

Commercialization of Microfinance

8/16/2011 1 13 Commercialization of Microfinance Robert Lensink (RUG/WUR) Presentation for the UMM Conference in Frankfurt Schedule 8/16/2011 2 13 Some preliminary remarks Recent trend: commercialization

8/16/2011 1 13 Commercialization of Microfinance Robert Lensink (RUG/WUR) Presentation for the UMM Conference in Frankfurt Schedule 8/16/2011 2 13 Some preliminary remarks Recent trend: commercialization

Microcredit: A microprimer. Prof. Jay Aronson

Microcredit: A microprimer Prof. Jay Aronson Buzzzzzzzzzzzzzz Microcredit has become a development buzzwork, just like human capacity, structural capacity, or sustainability 2005 was dubbed the International

Microcredit: A microprimer Prof. Jay Aronson Buzzzzzzzzzzzzzz Microcredit has become a development buzzwork, just like human capacity, structural capacity, or sustainability 2005 was dubbed the International

of the microcredit sector in the European Union 2010-11

Overview of the microcredit sector in the European Union 2010-11 Summary For the first time the EMN Overview survey covered Non-EU member states including all potential EU candidate states. A special emphasis

Overview of the microcredit sector in the European Union 2010-11 Summary For the first time the EMN Overview survey covered Non-EU member states including all potential EU candidate states. A special emphasis

World Bank SME Questionnaire December 2006

The World Bank Questionnaire on Bank Financing to SMEs This version: December 8, 2006 Bank: Staff interviewed: Interviewers: Date: This questionnaire is focused on credit to small and medium enterprises

The World Bank Questionnaire on Bank Financing to SMEs This version: December 8, 2006 Bank: Staff interviewed: Interviewers: Date: This questionnaire is focused on credit to small and medium enterprises

Secured Transactions & Collateral Registries: Global Expansion, Global Results

Secured Transactions & Collateral Registries: Global Expansion, Global Results WHY SECURED TRANSACTIONS? CLEAR MARKET FAILURE IN LAC AND BEYOND SME Finance Gap 400 million SMEs in developing world 50%

Secured Transactions & Collateral Registries: Global Expansion, Global Results WHY SECURED TRANSACTIONS? CLEAR MARKET FAILURE IN LAC AND BEYOND SME Finance Gap 400 million SMEs in developing world 50%

World Health Organization 2009

World Health Organization 2009 This document is not a formal publication of the World Health Organization (WHO), and all rights are reserved by the Organization. The document may, however, be freely reviewed,

World Health Organization 2009 This document is not a formal publication of the World Health Organization (WHO), and all rights are reserved by the Organization. The document may, however, be freely reviewed,

Shaping national health financing systems: can micro-banking contribute?

Shaping national health financing systems: can micro-banking contribute? Varatharajan Durairaj, Sidhartha R. Sinha, David B. Evans and Guy Carrin World Health Report (2010) Background Paper, 22 HEALTH

Shaping national health financing systems: can micro-banking contribute? Varatharajan Durairaj, Sidhartha R. Sinha, David B. Evans and Guy Carrin World Health Report (2010) Background Paper, 22 HEALTH

SEMINAR ON CREDIT RISK MANAGEMENT AND SME BUSINESS RENATO MAINO. Turin, June 12, 2003. Agenda

SEMINAR ON CREDIT RISK MANAGEMENT AND SME BUSINESS RENATO MAINO Head of Risk assessment and management Turin, June 12, 2003 2 Agenda Italian market: the peculiarity of Italian SMEs in rating models estimation

SEMINAR ON CREDIT RISK MANAGEMENT AND SME BUSINESS RENATO MAINO Head of Risk assessment and management Turin, June 12, 2003 2 Agenda Italian market: the peculiarity of Italian SMEs in rating models estimation

Q&A Oxfam and Impact Investments. Audience: Entrepreneurs Investors Oxfam + partners General audience (including press) General

General") Q&A Oxfam and Impact Investments Audience: Entrepreneurs Investors Oxfam + partners General audience (including press) General Q: Why is Oxfam active in impact investing? A: Oxfam believes the upcoming

Q&A Oxfam and Impact Investments Audience: Entrepreneurs Investors Oxfam + partners General audience (including press) General Q: Why is Oxfam active in impact investing? A: Oxfam believes the upcoming

UNRAVELLING MICRO UNIT DEVELOPMENT AND REFINANCE AGENCY (MUDRA) Prime M2i Consulting Private Limited

Prime M2i Consulting Private Limited") UNRAVELLING MICRO UNIT DEVELOPMENT AND REFINANCE AGENCY (MUDRA) ABOUT MUDRA MUDRA: A refinancing facility for supporting microenterprises Current legal status: NBFC, a wholly-owned subsidiary of SIDBI

UNRAVELLING MICRO UNIT DEVELOPMENT AND REFINANCE AGENCY (MUDRA) ABOUT MUDRA MUDRA: A refinancing facility for supporting microenterprises Current legal status: NBFC, a wholly-owned subsidiary of SIDBI

FINANCE for the POOR Equipment Leasing and Lending: A Guide for Microfinance 1

FINANCE for the POOR Equipment Leasing and Lending: A Guide for Microfinance 1 GLENN D. WESTLEY Senior Advisor, Micro, Small and Medium Enterprise Division Inter-American Development Bank As microfinance

FINANCE for the POOR Equipment Leasing and Lending: A Guide for Microfinance 1 GLENN D. WESTLEY Senior Advisor, Micro, Small and Medium Enterprise Division Inter-American Development Bank As microfinance

Microfinance and the Role of Policies and Procedures in Saturated Markets and During Periods of Fast Growth

Microfinance and the Role of Policies and Procedures in Saturated Markets and During Periods of Fast Growth Microfinance Information Exchange & Planet Rating An evaluation of the role that lending methodologies,

Microfinance and the Role of Policies and Procedures in Saturated Markets and During Periods of Fast Growth Microfinance Information Exchange & Planet Rating An evaluation of the role that lending methodologies,

COMPANY PRODUCTS AND SERVICES

COMPANY PRODUCTS AND SERVICES THE WORLD IS WAITING. 1 1 Santander Group. With more than 150 years in the business, Santander has become one of the world's largest financial groups. This has been based

COMPANY PRODUCTS AND SERVICES THE WORLD IS WAITING. 1 1 Santander Group. With more than 150 years in the business, Santander has become one of the world's largest financial groups. This has been based

Research Insight Peru - Model Market for Microfinance

Research Insight Peru - Model Market for Microfinance Research Insight is a publication of responsability research. At irregular intervals, responsability research conducts and compiles analyses, studies,

Research Insight Peru - Model Market for Microfinance Research Insight is a publication of responsability research. At irregular intervals, responsability research conducts and compiles analyses, studies,

CASE STORY ON GENDER DIMENSION OF AID FOR TRADE. Banking on Women Pays Off: Creating Opportunities for Women Entrepreneurs

CASE STORY ON GENDER DIMENSION OF AID FOR TRADE Banking on Women Pays Off: Creating Opportunities for Women Entrepreneurs Banking on Women Pays Off Creating Opportunities for Women Entrepreneurs International

CASE STORY ON GENDER DIMENSION OF AID FOR TRADE Banking on Women Pays Off: Creating Opportunities for Women Entrepreneurs Banking on Women Pays Off Creating Opportunities for Women Entrepreneurs International

6 th African Microfinance Conference

6 th African Microfinance Conference Presentation by: Mr. Wilson Twamuhabwa CEO, UGAFODE Microfinance Limited (MDI) President AMFIU- Uganda MFI Network Contact: [email protected] About UGAFODE

6 th African Microfinance Conference Presentation by: Mr. Wilson Twamuhabwa CEO, UGAFODE Microfinance Limited (MDI) President AMFIU- Uganda MFI Network Contact: [email protected] About UGAFODE

MicroVest and Social Impact Scoring Model

Social Impact Report FY 2013 Message from the Chief Executive Officer I am pleased to present our second annual Social Impact Report. In this report, we discuss our various initiatives within the impact

Social Impact Report FY 2013 Message from the Chief Executive Officer I am pleased to present our second annual Social Impact Report. In this report, we discuss our various initiatives within the impact

EUROPEAN SME CAPEX BAROMETER

GE Capital EUROPEAN SME CAPEX BAROMETER SMEs business sentiment and capital investment in Europe s four biggest economies July 2011 www.gecapital.eu Contents Introduction Executive summary Capital investment

GE Capital EUROPEAN SME CAPEX BAROMETER SMEs business sentiment and capital investment in Europe s four biggest economies July 2011 www.gecapital.eu Contents Introduction Executive summary Capital investment

Deploying a MNO s Mobile Banking Solution for the Microfinance Sector:

Deploying a MNO s Mobile Banking Solution for the Microfinance Sector: What are the Key Issues to Address? November, 26 th of 2009 Thierno SECK Director of Mobile Banking Projects, PlaNet Finance AS Glossary

Deploying a MNO s Mobile Banking Solution for the Microfinance Sector: What are the Key Issues to Address? November, 26 th of 2009 Thierno SECK Director of Mobile Banking Projects, PlaNet Finance AS Glossary

THE MULTILATERAL INVESTMENT FUND DEPLOYING VALUE CHAINS FOR DEVELOPMENT. Nancy Lee General Manager MULTILATERAL INVESTMENT FUND

THE MULTILATERAL INVESTMENT FUND DEPLOYING VALUE CHAINS FOR DEVELOPMENT Nancy Lee General Manager MULTILATERAL INVESTMENT FUND 2. TABLE OF CONTENTS Introduction to the Multilateral Investment Fund Evolution

THE MULTILATERAL INVESTMENT FUND DEPLOYING VALUE CHAINS FOR DEVELOPMENT Nancy Lee General Manager MULTILATERAL INVESTMENT FUND 2. TABLE OF CONTENTS Introduction to the Multilateral Investment Fund Evolution

2Q15 Consolidated Earnings Results

2Q15 Consolidated Earnings Results IFRS September 2015 Disclaimer Grupo Aval Acciones y Valores S.A. ( Grupo Aval ) is an issuer of securities in Colombia and in the United States, registered with Colombia

2Q15 Consolidated Earnings Results IFRS September 2015 Disclaimer Grupo Aval Acciones y Valores S.A. ( Grupo Aval ) is an issuer of securities in Colombia and in the United States, registered with Colombia

MicroFinancialOrganization

2011 MicroFinancialOrganization December 2011 LTD MFO Capital Credit Content Business Plan 1. Index of tables and figures 1.1.Georgia........................................................................

2011 MicroFinancialOrganization December 2011 LTD MFO Capital Credit Content Business Plan 1. Index of tables and figures 1.1.Georgia........................................................................

Axis Bank Ltd. Policy for lending to Micro and Small Enterprises (MSEs)

") Axis Bank Ltd. Policy for lending to Micro and Small Enterprises (MSEs) Introduction: The Micro and Small Enterprise (MSE) sector contributes significantly to manufacturing output, employment and exports

Axis Bank Ltd. Policy for lending to Micro and Small Enterprises (MSEs) Introduction: The Micro and Small Enterprise (MSE) sector contributes significantly to manufacturing output, employment and exports

How To Invest In A Farm Business

Impact Investment AFI Summit Discussion August 18, 2015 Catalyzing Investments Over Time Impact Investing S SCALE OF OUTREACH c a l e Institution Building Governance Project-based TA SUSTAINABILITY Why

Impact Investment AFI Summit Discussion August 18, 2015 Catalyzing Investments Over Time Impact Investing S SCALE OF OUTREACH c a l e Institution Building Governance Project-based TA SUSTAINABILITY Why

Research Insight Efficiency is the key to lower interest rates in microfinance. Executive Summery

Research Insight Efficiency is the key to lower interest rates in microfinance Executive Summery March 14 Key findings Microfinance provides hundreds of millions of low-income households with access to

Research Insight Efficiency is the key to lower interest rates in microfinance Executive Summery March 14 Key findings Microfinance provides hundreds of millions of low-income households with access to