A three dimensional stochastic Model for Claim Reserving

|

|

|

- Jared Ryan

- 10 years ago

- Views:

Transcription

1 A three dimensional stochastic Model for Claim Reserving Magda Schiegl Haydnstr. 6, D Neufahrn, [email protected] and Cologne University of Applied Sciences Claudiusstr. 1, D Köln Abstract Within the Solvency II framework the insurance industry requires a realistic modelling of the risk processes relevant for its business. Every insurance company should be capable of running a holistic risk management process to meet this challenge. For property and casualty (P&C) insurance companies the risk adequate modelling of the claim reserves is a very important topic as this liabilities determine up to 70% percent of the balance sum. We propose a three dimensional (3D) stochastic model for claim reserving. It meets the necessary number of degrees of freedom to model a realistic claim process that consists of occurrence, reporting and run-off. The model delivers consistently the reserve s distribution function as well as the distributions of all parts of it that are needed for accounting and controlling. The calibration methods for the model are well known from data analysis and they are applicable in an practitioner environment. We evaluate the model numerically by the help of Monte Carlo (MC) simulation. Classical actuarial reserve models are two dimensional (2D). They lead to an estimation algorithm that is applied on a 2D matrix, the run off triangle. Those methods (for instance the Chain Ladder or the Bornhuetter Ferguson method) are widely used in practice nowadays and give rise to several problems: They estimate the reserves expectation and some of them - under very restriction assumptions - the variance. They provide no information about the tail of the reserve s distribution, what would be most important for risk calculation, for assessing the insurance company s financial stability and economic situation. Additionally, due to the projection of the claim process into a two dimensional space the results are very often distorted and dependent on the kind of projection. Therefore we extend the classical 2D models to a 3D space because we find inconsistencies generated by inadequate projections into the 2D spaces. Keywords: Claim reserving, IBNR reserve, collective model of risk theory, Monte Carlo simulation, stochastic model. 1

insurance companies the risk adequate modelling of the claim reserves is a very important topic as this liabilities determine up to 70% percent of the balance sum.")

2 1. Introduction In the framework of Solvency II holistic risk management became very important for insurance business. It is going to implement a new, efficient supervisory basis that enables the risk - orientated and principle based calculation of the economic capital. In P&C insurance companies the claim reserves are the most important liability position in the balance sheet. They determine up to 70% of the balance sum, of course depending on product mix and capitalisation of the company. Claim reserves are necessary to cover the liabilities arising from insurance contracts written in the presence and the past. Therefore claim reserving is decisive for regulatory and accounting issues as well as for product pricing and reporting. The claim reserves are calculated for homogeneous portfolios of insurance contracts via actuarial methods which are well known form literature. The basis of the classic reserving methods is built by two dimensional matrices, the run - off triangles. They are generated via accumulation of claim data. Details are given in section 2 of this paper. An overview on claim reserving and its classical methods can be found in Taylor [12, 13] and in Radtke, Schmidt [7]. The main problem of the classical methods is the fact that a complex stochastic process with many degrees of freedom is transformed to a two dimensional structure the run-off matrix. This means that the real world is projected to a 2D model and it is expected that on this basis one gets a convenient forecast of the future. This is only true under very special assumptions. Additionally most of the classic methods do only estimate the reserves expectation value. For very few of them, for instance the Chain Ladder method, the second moment of the distribution is know under very restrictive assumptions posed on the underlying stochastic model (see [3]). The point however is that the classical methods give no estimate of the reserve distribution s tail which is of great importance for risk calculation. In reality the claim process consists of claims occurrence (first), reporting (second) and run off (third). Therefore a 3D model structure is very natural and adequate for this problem. We introduce a 3D stochastic model for claim reserves. The variables of the model are: The number of active claims and the claim payments. The expectation value and the variance of the reserve are given as an analytical function of the model parameters. The reserve distribution can be calculated numerically. To calculate them we perform Monte Carlo (MC) simulations on the basis of this model. There exists already experience on MC simulation techniques for reserve model evaluation, see [8]. The results of the MC simulation are the reserves probability distributions. The model can be calibrated to real world data (claim portfolio data) via standard methods of data analysis (see [9]). Notice that reserves in this context severs as a placeholder for the total reserve, the INBR reserve, the number of IBNR claims or any other quantity relevant for managing and reporting the reserve process. The distributions are the basis for further risk calculation and management in P&C insurance companies. For instance this makes accessible risk measures as VaR or expected shortfall. 2

3 2. The connection between the 2D and the 3D models As was stated in the introduction the classic models project the claim process to a 2D world, operate on cumulated 2D data structures and calculate only the expectation of the reserve. The typical data structures for payments that build the basis for reserve estimation are shown in figure 1. The claim payments are accumulated according to occurrence versus run off years in the one case and reporting versus runoff years in the other case. The formal relation between these two 2D matrices with the tensors of our 3D model is given at the end of this section: ( 1) ( 2) S mn are the components of the occurrence versus run off year matrix and S mn are the components of the reporting versus run off year matrix. The matrices upper left triangles are filled with (known) figures. They represent the past. The figures in the lower right triangle have to be estimated by the application of mathematical, statistical methods. There exists quite a zoo of actuarial methods for such calculations. (see for example [1, 2, 3, 6, 7]). Depending on the kind of the used data triangle the result of this calculations is either the total reserve (the sum of reported claims and IBNR reserves; see left side of figure 1) or two separate results for both parts of the total reserves (see right side of figure 1). In practice one is often faced with the following problem: Appling both methods to the same data set delivers inconsistent results. This is well known and up to now this insufficiency was ascribed to properties of the estimators, particularly the bias (see for instance [10, 11]). To our knowledge up to now nobody asked, if the dimension of the state space underlying the description of the problem is appropriate or not. The claim process is shown schematically in figure 2. After the occurrence of a claim it is reported to the insurance company. The time between occurrence and reporting, the lag, depends on the line of business and can vary from one day to several years. As an example: For motor car insurance the lag is typically very short, for other lines of third party liability insurance it can be much longer up to several years. After having been reported the claims are paid either at once or with several payments. Several payments are typical in the case of injured persons for instance. The time between the reporting of the claim and the final run off can differ from several days up to years or even decades (lifelong annuity payments for injured persons for instance). Having in mind this three step nature of the claim process (occurrence reporting payment) the extension from the classic 2D model to a 3D model is quite natural in the sense that it follows the imperative of reality. We therefore propose as a basis for further analysis to aggregate the claim data to a three dimensional structure: The first dimension is the relative (to the oldest) occurrence year, the second is the number of years between occurrence and reporting and the third dimension is the difference (in years) between claim s reporting and payment. Claim reserves are modelled stochastically within the above defined 3D framework. It is assumed that the parameters of the microscopic claim process are known or can be measured. This is a quite realistic assumption provided the insurance company is ready to collect claim data over a relevant time horizon. We model a set of claims stochastically, including their projection into the future. We do this by the help of Monte Carlo simulation and get as a result the statistical properties (distribution) of the macroscopic quantities (reserves). We model the following microscopic quantities: The number of active claims N occurred in year i, reported j years after occurrence and still active k years after reporting. Still active means that the claim is not closed and therefore it can be the source of further payments. The second quantity to be modelled is Z. This is the 3

( 2) S mn are the components of the occurrence versus run off year matrix")

4 total amount paid for the N claims of occurrence year i with reporting delay j years in the kth year after reporting. In the following we connect the quantities of the 3D model to those of the 2D model which is used by the standard reserving methods. We visualise this circumstances additionally in figure 3. The up to now reported claims are found in the run off triangle: i + j I N ij0 with This triangle (occurrence versus. reporting year) is used in practice to estimate the ultimate number of claims per occurrence year. The boundary I is given by the claim portfolio s total run-off time (number of years). The estimation of the ultimate claim number consists of the sum of already reported claims and the incurred but not reported (IBNR) claims (see figure 3a). The table of active claims in the presence is given by the set (see figure 3b): { N i + j + k = I } Below and on this plain lie all known numbers: Number of claims (left side of figure 3) as well as payments for claims(see right hand side of figure 3). The numbers above the plain have to be estimated and give an economic evaluation of the future claim numbers and payments respectively. The IBNR reserve can be written as: R ˆ = ˆ IBNR Z. { i, j, k i+ j+ k> I i+ j< I } The number of IBNR claims is given by: N ˆ = ˆ { i, j i+ j> I } IBNR N ij 0 The total reserve evaluates as (sum of reserves for known and unknown claims): R ˆ = ˆ + ˆ total RIBNR Z. { i, j, k i+ j> I } The visualisation of these reserves can be seen in figure 3 on the right hand side: For the IBNR reserve see figure 3d), for the total reserve figure 3c) and d). In both cubes the plain separating the known from the unknown numbers is drawn with sketched lines. By aggregating the components of the Z tensor (payments) in the following way the run off triangles used by standard 2D reserving methods can be generated: The run off triangle payments: occurrence versus run off year, well known in the 2D world, can be generated from the 3D according to: 4

is used in practice to estimate the ultimate number of claims per occurrence year. The boundary I is given by the claim portfolio s total run-off time (number of years).")

5 ( 1) S mn = Z mjk { j, k j+ k= n m+ j+ k I } This triangle is used in the context of standard reserving methods for estimating the total reserve. The 2D run off triangle payment: reporting versus run off year is generated via: ( 2) S mn = Z ijn { i, j i+ j= m i+ j+ n I } This triangle is used in the context of standard reserving methods for business lines with very long reporting times to estimate the total reserve. It should deliver reasonable results in the case of constant portfolio volumes and a stationary claim process. Insurance companies think currently about setting automatic single claim reserves for some lines of business as for instance motor car insurance. For this purpose they need values for the mean future claim size contingent on the claim history. This automatic procedure does only make sense for claims with small or medium sized expectations. Our model has the advantage to deliver such estimators for the mean claim size depending on the reporting lag j and on the number of years k for which the claim has been active: MCS jk = i, l k i Z N ijl. The dependence on k and j is so important because it is expected that the mean claim size grows with both, k and j. 5

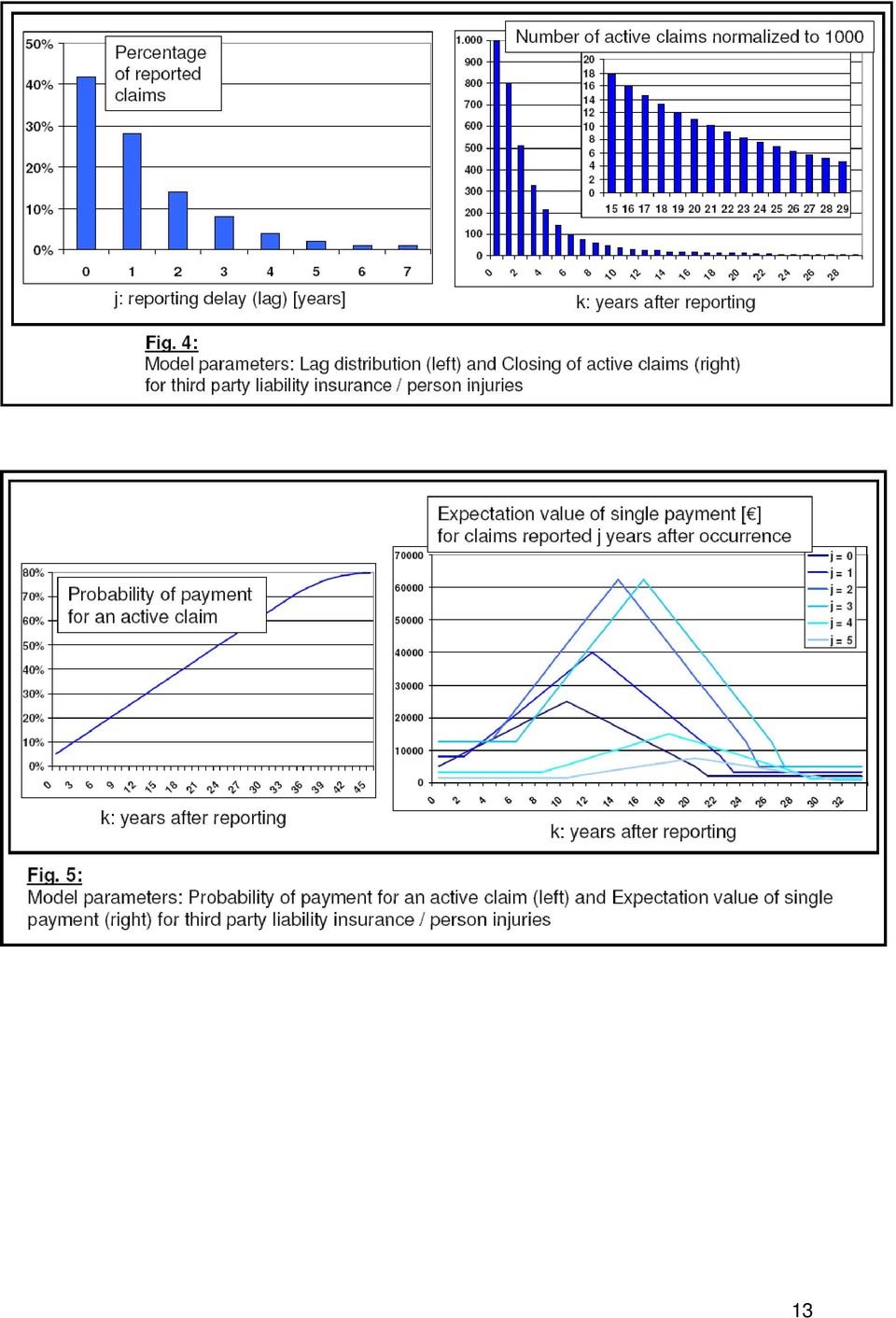

6 3. The 3D Model and its Application In this section we define the stochastic 3D model. We introduce the necessary distributions determining the single claim process on a microscopic level and its parameters. We introduce one example for a realistic claim process and set the parameter values according to this example. This enables us to demonstrate our model in a real world scenario. We implement our model in a Monte Carlo simulation program and calculate the empirical distributions of IBNR claim numbers, IBNR reserve and total reserve The 3D Model As described in section 2 we model the number of active claims N occurred in year i, reported j years after occurrence and still active k years after reporting as well as Z, the total amount paid for the N claims of occurrence year i with reporting delay j years in the kth year after reporting. The ultimate number of claims in occurrence year i is: N i = N ij 0 j It is modelled as Poisson distributed with (given) parameter N Poisson ( ) i N i The claim numbers obey a multinomial distribution along the years of reporting delays according to the parameters { 1,2 I } N i. λ j j,.., with λ =. j j 1 Where the parameter I is the claim portfolio s total run-off time (number of years). For convenience we have chosen I = J. This is a suitable assumption if the claim history of the company is known for a long time, minimum as long as the run off time. Other conventions are possible. Therefore the claim numbers for k = 0 are distributed according to: N [, λ, λ,.., λ λ ] ij0 MultNom N i 1 2 j,.., The closing of active claims along the years after reporting is described by the parameters { 1,2 K } Im ax η k k,.., with η = 0 1 and η k < ηk +1. Where the boundary K is the imum number of years a reported claim needs for the run off to be completed. 6

7 The fact that an open claim is not closed in year k can be modelled as a survival process resulting in a binomial distribution with survival probability η k : N [ η ] BiNom N, 1 Therefore the expectation of the active number of claims can be written as: E [ N ] N i λ j ηk =. The claim payments are modelled according the collective model of risk theory: k ν Z = X l where the number of single claim payments ν is binomially distributed l= 1 ( ) ν [ N p ] BiNom, ik with parameters N, the active number of claims, and p ik, the probability that an active claim produces a payment. The X are the payments for single claims. Applying the model to Monte Carlo simulations (section 3.1) we assume them to be Gamma distributed with parameters depending on i, j, and k: [ EW Var ] X Γ, This completes the setting of our model. The choice of the distributions for claim numbers and payments is of course a matter of best fit to the data. We made here the assumptions characterised above, being not too far from real world claim data, in order to apply the model to a concrete simulation example. We deal with some aspects concerning the problem of model selection in section The Monte Carlos (MC) Simulation and Results We apply the model described in section 3.1 by the help of MC simulation. We simulate a set of claims in its microscopic environment. Every element of the set (i.e. claim) obeys the stochastic process (3D model) of section 3.1. The parameters of the process are known from data analysis of claim databases containing single claim information. The formulas in section 2 give the connection between the microscopic and the macroscopic world, i.e. the reserves for the total claim portfolio. Due to the ansatz of our model we are able to gain knowledge of the macroscopic world s statistical properties, particularly the empirical distributions of the reserves (total and IBNR) and the number of IBNR claims. We have chosen the model s parameter values in a way that they contain some typical features of real life claim portfolios. They are, of course, no one to one values from an existing portfolio. 7

![The claim payments are modelled according the collective model of risk theory: k ν Z = X l where the number of single claim payments ν is binomially distributed l= 1 ( ) ν [ N p ] BiNom, ik with](/docs-images/45/7774225/images/page_7.jpg "parameters N, the active number of claims, and p ik, the probability that an active claim produces a payment. The X are the payments for single claims.")

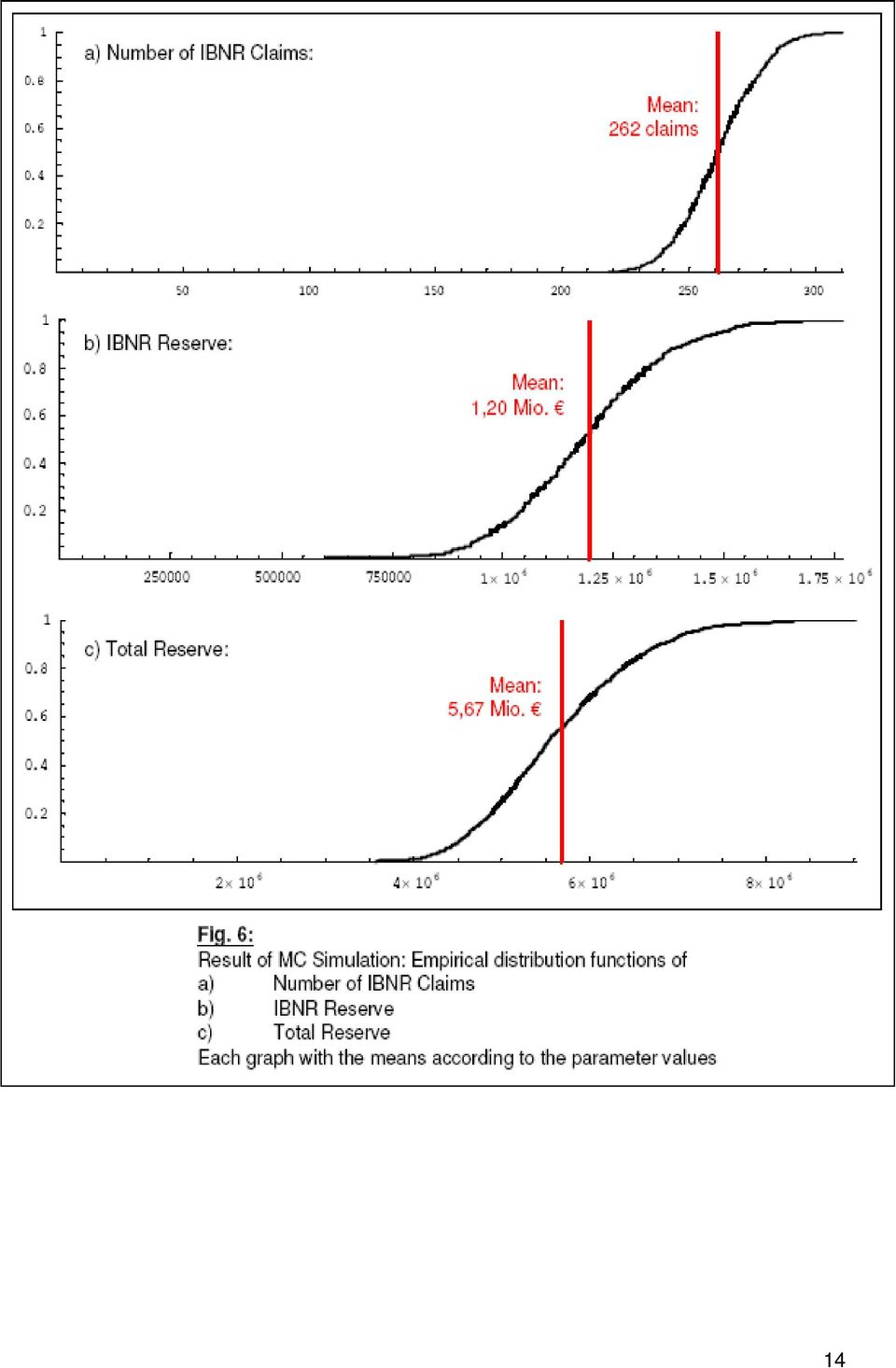

8 Now the description of the model parameter values follows: They are displayed in figures 4 and 5. All parameters show typical features as they can be found in third party liability portfolios with person injuries. The lag distribution parameters λ j can be seen in figure 4 on the left side. They are monotonically falling in j, the delay time in years. This is similar in all lines of business, whereas the width of the distribution varies substantially from line to line. In our example some 40% of the claims are reported in the occurrence year and less than 30% one year later. In figure 4 on the right the closing down of active claims is plotted, normalised to 1000 claims at the beginning. From this follow the parameter values for η k. Due to the definition it is a monotonically falling function in k, the number of years after reporting. The rate of decrease depends very much of the kind of insurance portfolio. For portfolios with person injuries it is quite typical that even after a very long time 30 years as in our example or even longer there are still open claims. This is for instance due to accident caused, disabled persons that have to be cared for until they die. For our example we assume that the probability of payment for an active claim p ik depends only on k not on i. Active claims, although not fully regulated, do not generate a payment every year. The probability for payment is plotted in figure 5 on the left side. This parameters depends very much on the line of business. In our case there is a rise in probability from a few percent in the early years after reporting up to 80% some 40 years after reporting. In other lines probabilities that decrease with the number of years after reporting can be observed. For the expectation value of a single payment EW we assume homogeneity over occurrence time. Therefore it does not depend on i but on j and k. The expectation value of a single payment is depicted in figure 5 on the right side. The parameter values underlie stylized assumptions as one can see in figure 5. However several typical features are included in this parameter values: The overall size, the fact that there is a imum in payments some years after the claim was reported and the fact, that this imum is the higher the longer the time lag between occurrence and reporting was. This can be understood as follows: Claims that are discovered not earlier than a few years after occurrence carry a higher risk than claims having been discovered immediately after occurrence. This is only true for the first few years (in our example 3 years). If the claim is discovered / reported later, the claim size decreases very rapidly. This is of course, one example in any case the right expectation profile has to be found out via data analysis of the claim portfolio. Further we assumed: Var = 4EW. The variance is proportional to the expectation with a constant that is very typical to that kind of claim portfolio. Overdispersed payment distributions are found very often in third party liability insurance. For our MC simulation we set the initial mean number of claims to N = 150 and assume an annual growth of 3%. This is for example a realistic assumption in the case of an insurance portfolio with 3% growing volume (contracts) and a stationary claim frequency. We considered 15 occurrence years. For the MC simulation we used the MATHEMATICA package. The results of MC simulation can be seen in figure 6: The distributions for a) the number of claims, b) the IBNR reserve and c) the total reserve. We used 1000 MC samples in this case. In each part of the plot the mean value, depending analytically on the model parameters, is given as a numeric value and is plotted into the graph. From these distributions risk measures as the standard deviation VaR, TailVar or expected shortfall can be calculated. The new regulatory and accounting standards do ask for them. i 8

9 4. Overview and Outlook This paper proposes a 3D model for claim reserving. It shows the connection to the classical actuarial 2 D models and clarifies that the 3D model can be understood as an extension of the 2D ones. In this way wrong reserve estimations due to inadequate projections on 2D space can be avoided. The 3D model can be calibrated to claim portfolio data via standard methods of data analysis. The expectation and variance of the reserve are an analytical function of the model parameters. The reserve distribution can be calculated by Monte Carlos Simulation techniques. This makes all measures of risk accessible for calculation. There are many interesting questions that can be investigated as the 3D model implies a new way of analysing claim data: First of all: What is the performance of 3D models compared with classical actuarial 2D methods. In which situations are 2D methods appropriate? Can quantitative rules be formulated to define regimes in the parameter space where 3D modelling is necessary? Our framework of the 3D models enables us to answer this questions on a quantitative basis. This questions can be investigated via analytical and / or numerical methods. For numerics we are about to set up a MC simulation experiment to compare the 2D and the 3D results for a given microscopic claim process according to the model of section 3.1. Another aim is to put up robust estimation methods for the model parameters from a given claim portfolio. We have already given a first answers to this topic (see [9]): We detected the structure of the claim data set necessary to proceed with the estimation. The estimation has to be consistent in the sense that the estimates of the different parameters do not influence one another. As we have some knowledge of the parameters properties (see section 3.2) we used a Bayes inference method for parameter estimation. Further practical application would be quite interesting to be done, especially in connection with the points to be investigated as noted above. After all a further extension of our model to a single claim reserve process would be possible. In an insurance company there are not only claim number and claim payment data available on a single claim level, but also reserve data. The single claim reserves are expert estimations on the final claim size after run off. This estimation is adjusted over the lifetime of the claim to its present state. This could be modelled as a (stochastic) reserve process analogously to the payment process in the present model. The reserve process could also be calibrated on single claim data. The applicability of the extended model in practice has to be analysed carefully due to the following reason: An improved prediction in macroscopic portfolio reserve will only be achieved, if the insurance company s real world reserving process can be modelled consistently over the past. All practitioners know that this assumption is not trivial at all! So the success of the model extension depends very much on the peculiarities of the insurance company. Extensions of that kind have been worked out for the 2D methods during the last years (see [5]). 9

10 Literature 1. R. L. Bornhuetter R. E. and Ferguson CAS 59, 181 (1972). 2. Th. Mack, ASTIN Bulletin 21, 93 (1991). 3. Th. Mack, ASTIN Bulletin 23, 213 (1993). 4. Th. Mack, ASTIN Bulletin 30, 333 (2000). 5. Th. Mack and G. Quarg, Blätter DGVFM Deutsche Gesellschaft für Versicherungs- und Finanzmathematik e.v. Germany, XXVI, 597 (2004). 6. W. Neuhaus, Scand. Actuar. J., 151 (1992). 7. M. Radtke and K.D. Schmidt (eds.), Handbuch zur Schadenreservierung, (Verlag Versicherungswirtschaft, Karlsruhe, 2004). 8. M. Schiegl, On the Safety Loading for Chain Ladder Estimates: A Monte Carlo Simulation Study, ASTIN Bulletin 32, 107 (2002). 9. M. Schiegl, Parameter estimation for a stochastic claim reserving model, DPG Conference, Berlin (2008). 10. K.D. Schmidt and A. Schnaus, ASTIN Bulletin 26, 247 (1996). 11. K.D. Schmidt and A. Wünsche DGVM Blätter XXIII, 267 (1998). 12. G.C. Taylor, Claims Reserving in Non-Life Insurance, (North-Holland, Amsterdam,1986). 13. G.C. Taylor, Loss Reserving, (Kluwer Academic Publishers, Boston, 2000). 10

. 9. M. Schiegl, Parameter estimation for a stochastic claim reserving model, DPG Conference, Berlin (2008).")

11 11

12 12

13 13

14 14

Runoff of the Claims Reserving Uncertainty in Non-Life Insurance: A Case Study

1 Runoff of the Claims Reserving Uncertainty in Non-Life Insurance: A Case Study Mario V. Wüthrich Abstract: The market-consistent value of insurance liabilities consists of the best-estimate prediction

1 Runoff of the Claims Reserving Uncertainty in Non-Life Insurance: A Case Study Mario V. Wüthrich Abstract: The market-consistent value of insurance liabilities consists of the best-estimate prediction

A credibility method for profitable cross-selling of insurance products

Submitted to Annals of Actuarial Science manuscript 2 A credibility method for profitable cross-selling of insurance products Fredrik Thuring Faculty of Actuarial Science and Insurance, Cass Business School,

Submitted to Annals of Actuarial Science manuscript 2 A credibility method for profitable cross-selling of insurance products Fredrik Thuring Faculty of Actuarial Science and Insurance, Cass Business School,

Towards the strengthening and moderinsation of insurance and surety regulation

Non-Life Insurance Technical Provisions i Towards the strengthening and moderinsation of insurance and surety regulation XXI International Seminar on Insurance and Surety, November 2010, Mexico City Olaf

Non-Life Insurance Technical Provisions i Towards the strengthening and moderinsation of insurance and surety regulation XXI International Seminar on Insurance and Surety, November 2010, Mexico City Olaf

The Study of Chinese P&C Insurance Risk for the Purpose of. Solvency Capital Requirement

The Study of Chinese P&C Insurance Risk for the Purpose of Solvency Capital Requirement Xie Zhigang, Wang Shangwen, Zhou Jinhan School of Finance, Shanghai University of Finance & Economics 777 Guoding

The Study of Chinese P&C Insurance Risk for the Purpose of Solvency Capital Requirement Xie Zhigang, Wang Shangwen, Zhou Jinhan School of Finance, Shanghai University of Finance & Economics 777 Guoding

Treatment of technical provisions under Solvency II

Treatment of technical provisions under Solvency II Quantitative methods, qualitative requirements and disclosure obligations Authors Martin Brosemer Dr. Susanne Lepschi Dr. Katja Lord Contact [email protected]

Treatment of technical provisions under Solvency II Quantitative methods, qualitative requirements and disclosure obligations Authors Martin Brosemer Dr. Susanne Lepschi Dr. Katja Lord Contact [email protected]

Methodology. Discounting. MVM Methods

Methodology In this section, we describe the approaches taken to calculate the fair value of the insurance loss reserves for the companies, lines, and valuation dates in our study. We also describe a variety

Methodology In this section, we describe the approaches taken to calculate the fair value of the insurance loss reserves for the companies, lines, and valuation dates in our study. We also describe a variety

Matching Investment Strategies in General Insurance Is it Worth It? Aim of Presentation. Background 34TH ANNUAL GIRO CONVENTION

Matching Investment Strategies in General Insurance Is it Worth It? 34TH ANNUAL GIRO CONVENTION CELTIC MANOR RESORT, NEWPORT, WALES Aim of Presentation To answer a key question: What are the benefit of

Matching Investment Strategies in General Insurance Is it Worth It? 34TH ANNUAL GIRO CONVENTION CELTIC MANOR RESORT, NEWPORT, WALES Aim of Presentation To answer a key question: What are the benefit of

How To Calculate Multi-Year Horizon Risk Capital For Non-Life Insurance Risk

The Multi-Year Non-Life Insurance Risk Dorothea Diers, Martin Eling, Christian Kraus und Marc Linde Preprint Series: 2011-11 Fakultät für Mathematik und Wirtschaftswissenschaften UNIVERSITÄT ULM The Multi-Year

The Multi-Year Non-Life Insurance Risk Dorothea Diers, Martin Eling, Christian Kraus und Marc Linde Preprint Series: 2011-11 Fakultät für Mathematik und Wirtschaftswissenschaften UNIVERSITÄT ULM The Multi-Year

How To Become A Life Insurance Specialist

Institute of Actuaries of India Subject ST2 Life Insurance For 2015 Examinations Aim The aim of the Life Insurance Specialist Technical subject is to instil in successful candidates principles of actuarial

Institute of Actuaries of India Subject ST2 Life Insurance For 2015 Examinations Aim The aim of the Life Insurance Specialist Technical subject is to instil in successful candidates principles of actuarial

A Model of Optimum Tariff in Vehicle Fleet Insurance

A Model of Optimum Tariff in Vehicle Fleet Insurance. Bouhetala and F.Belhia and R.Salmi Statistics and Probability Department Bp, 3, El-Alia, USTHB, Bab-Ezzouar, Alger Algeria. Summary: An approach about

A Model of Optimum Tariff in Vehicle Fleet Insurance. Bouhetala and F.Belhia and R.Salmi Statistics and Probability Department Bp, 3, El-Alia, USTHB, Bab-Ezzouar, Alger Algeria. Summary: An approach about

Central Bank of Ireland Guidelines on Preparing for Solvency II Pre-application for Internal Models

2013 Central Bank of Ireland Guidelines on Preparing for Solvency II Pre-application for Internal Models 1 Contents 1 Context... 1 2 General... 2 3 Guidelines on Pre-application for Internal Models...

2013 Central Bank of Ireland Guidelines on Preparing for Solvency II Pre-application for Internal Models 1 Contents 1 Context... 1 2 General... 2 3 Guidelines on Pre-application for Internal Models...

AISAM-ACME study on non-life long tail liabilities

AISAM-ACME study on non-life long tail liabilities Reserve risk and risk margin assessment under Solvency II 17 October 2007 Page 3 of 48 AISAM-ACME study on non-life long tail liabilities Reserve risk

AISAM-ACME study on non-life long tail liabilities Reserve risk and risk margin assessment under Solvency II 17 October 2007 Page 3 of 48 AISAM-ACME study on non-life long tail liabilities Reserve risk

Actuarial Risk Management

ARA syllabus Actuarial Risk Management Aim: To provide the technical skills to apply the principles and methodologies studied under actuarial technical subjects for the identification, quantification and

ARA syllabus Actuarial Risk Management Aim: To provide the technical skills to apply the principles and methodologies studied under actuarial technical subjects for the identification, quantification and

Quantitative Impact Study 1 (QIS1) Summary Report for Belgium. 21 March 2006

Summary Report for Belgium. 21 March 2006") Quantitative Impact Study 1 (QIS1) Summary Report for Belgium 21 March 2006 1 Quantitative Impact Study 1 (QIS1) Summary Report for Belgium INTRODUCTORY REMARKS...4 1. GENERAL OBSERVATIONS...4 1.1. Market

Quantitative Impact Study 1 (QIS1) Summary Report for Belgium 21 March 2006 1 Quantitative Impact Study 1 (QIS1) Summary Report for Belgium INTRODUCTORY REMARKS...4 1. GENERAL OBSERVATIONS...4 1.1. Market

One-year reserve risk including a tail factor : closed formula and bootstrap approaches

One-year reserve risk including a tail factor : closed formula and bootstrap approaches Alexandre Boumezoued R&D Consultant Milliman Paris [email protected] Yoboua Angoua Non-Life Consultant

One-year reserve risk including a tail factor : closed formula and bootstrap approaches Alexandre Boumezoued R&D Consultant Milliman Paris [email protected] Yoboua Angoua Non-Life Consultant

THE MULTI-YEAR NON-LIFE INSURANCE RISK

THE MULTI-YEAR NON-LIFE INSURANCE RISK MARTIN ELING DOROTHEA DIERS MARC LINDE CHRISTIAN KRAUS WORKING PAPERS ON RISK MANAGEMENT AND INSURANCE NO. 96 EDITED BY HATO SCHMEISER CHAIR FOR RISK MANAGEMENT AND

THE MULTI-YEAR NON-LIFE INSURANCE RISK MARTIN ELING DOROTHEA DIERS MARC LINDE CHRISTIAN KRAUS WORKING PAPERS ON RISK MANAGEMENT AND INSURANCE NO. 96 EDITED BY HATO SCHMEISER CHAIR FOR RISK MANAGEMENT AND

Marketing Mix Modelling and Big Data P. M Cain

1) Introduction Marketing Mix Modelling and Big Data P. M Cain Big data is generally defined in terms of the volume and variety of structured and unstructured information. Whereas structured data is stored

1) Introduction Marketing Mix Modelling and Big Data P. M Cain Big data is generally defined in terms of the volume and variety of structured and unstructured information. Whereas structured data is stored

LDA at Work: Deutsche Bank s Approach to Quantifying Operational Risk

LDA at Work: Deutsche Bank s Approach to Quantifying Operational Risk Workshop on Financial Risk and Banking Regulation Office of the Comptroller of the Currency, Washington DC, 5 Feb 2009 Michael Kalkbrener

LDA at Work: Deutsche Bank s Approach to Quantifying Operational Risk Workshop on Financial Risk and Banking Regulation Office of the Comptroller of the Currency, Washington DC, 5 Feb 2009 Michael Kalkbrener

Non-Life Insurance Mathematics

Thomas Mikosch Non-Life Insurance Mathematics An Introduction with the Poisson Process Second Edition 4y Springer Contents Part I Collective Risk Models 1 The Basic Model 3 2 Models for the Claim Number

Thomas Mikosch Non-Life Insurance Mathematics An Introduction with the Poisson Process Second Edition 4y Springer Contents Part I Collective Risk Models 1 The Basic Model 3 2 Models for the Claim Number

Contents. List of Figures. List of Tables. List of Examples. Preface to Volume IV

Contents List of Figures List of Tables List of Examples Foreword Preface to Volume IV xiii xvi xxi xxv xxix IV.1 Value at Risk and Other Risk Metrics 1 IV.1.1 Introduction 1 IV.1.2 An Overview of Market

Contents List of Figures List of Tables List of Examples Foreword Preface to Volume IV xiii xvi xxi xxv xxix IV.1 Value at Risk and Other Risk Metrics 1 IV.1.1 Introduction 1 IV.1.2 An Overview of Market

S T O C H A S T I C C L A I M S R E S E R V I N G O F A S W E D I S H L I F E I N S U R A N C E P O R T F O L I O

S T O C H A S T I C C L A I M S R E S E R V I N G O F A S W E D I S H L I F E I N S U R A N C E P O R T F O L I O DIPLOMA THESIS PRESENTED FOR THE. FOR SWEDISH ACTUARIAL SO CIETY PETER NIMAN 2007 ABSTRACT

S T O C H A S T I C C L A I M S R E S E R V I N G O F A S W E D I S H L I F E I N S U R A N C E P O R T F O L I O DIPLOMA THESIS PRESENTED FOR THE. FOR SWEDISH ACTUARIAL SO CIETY PETER NIMAN 2007 ABSTRACT

Actuarial Methods in Health Insurance Provisioning, Pricing and Forecasting

Actuarial Methods in Health Insurance Provisioning, Pricing and Forecasting Prepared by Peter Lurie Presented to the Institute of Actuaries of Australia Biennial Convention 23-26 September 2007 Christchurch,

Actuarial Methods in Health Insurance Provisioning, Pricing and Forecasting Prepared by Peter Lurie Presented to the Institute of Actuaries of Australia Biennial Convention 23-26 September 2007 Christchurch,

Decomposition of life insurance liabilities into risk factors theory and application

Decomposition of life insurance liabilities into risk factors theory and application Katja Schilling University of Ulm March 7, 2014 Joint work with Daniel Bauer, Marcus C. Christiansen, Alexander Kling

Decomposition of life insurance liabilities into risk factors theory and application Katja Schilling University of Ulm March 7, 2014 Joint work with Daniel Bauer, Marcus C. Christiansen, Alexander Kling

UNIVERSITY OF OSLO. The Poisson model is a common model for claim frequency.

UNIVERSITY OF OSLO Faculty of mathematics and natural sciences Candidate no Exam in: STK 4540 Non-Life Insurance Mathematics Day of examination: December, 9th, 2015 Examination hours: 09:00 13:00 This

UNIVERSITY OF OSLO Faculty of mathematics and natural sciences Candidate no Exam in: STK 4540 Non-Life Insurance Mathematics Day of examination: December, 9th, 2015 Examination hours: 09:00 13:00 This

Micro-level stochastic loss reserving for general insurance

Faculty of Business and Economics Micro-level stochastic loss reserving for general insurance Katrien Antonio, Richard Plat DEPARTMENT OF ACCOUNTANCY, FINANCE AND INSURANCE (AFI) AFI_1270 Micro level stochastic

Faculty of Business and Economics Micro-level stochastic loss reserving for general insurance Katrien Antonio, Richard Plat DEPARTMENT OF ACCOUNTANCY, FINANCE AND INSURANCE (AFI) AFI_1270 Micro level stochastic

PREDICTIVE DISTRIBUTIONS OF OUTSTANDING LIABILITIES IN GENERAL INSURANCE

PREDICTIVE DISTRIBUTIONS OF OUTSTANDING LIABILITIES IN GENERAL INSURANCE BY P.D. ENGLAND AND R.J. VERRALL ABSTRACT This paper extends the methods introduced in England & Verrall (00), and shows how predictive

PREDICTIVE DISTRIBUTIONS OF OUTSTANDING LIABILITIES IN GENERAL INSURANCE BY P.D. ENGLAND AND R.J. VERRALL ABSTRACT This paper extends the methods introduced in England & Verrall (00), and shows how predictive

Stochastic Analysis of Long-Term Multiple-Decrement Contracts

Stochastic Analysis of Long-Term Multiple-Decrement Contracts Matthew Clark, FSA, MAAA, and Chad Runchey, FSA, MAAA Ernst & Young LLP Published in the July 2008 issue of the Actuarial Practice Forum Copyright

Stochastic Analysis of Long-Term Multiple-Decrement Contracts Matthew Clark, FSA, MAAA, and Chad Runchey, FSA, MAAA Ernst & Young LLP Published in the July 2008 issue of the Actuarial Practice Forum Copyright

Modelling the Claims Development Result for Solvency Purposes

Modelling the Claims Development Result for Solvency Purposes Michael Merz, Mario V. Wüthrich Version: June 10, 008 Abstract We assume that the claims liability process satisfies the distribution-free

Modelling the Claims Development Result for Solvency Purposes Michael Merz, Mario V. Wüthrich Version: June 10, 008 Abstract We assume that the claims liability process satisfies the distribution-free

Best Estimate of the Technical Provisions

Best Estimate of the Technical Provisions FSI Regional Seminar for Supervisors in Africa on Risk Based Supervision Mombasa, Kenya, 14-17 September 2010 Leigh McMahon BA FIAA GAICD Senior Manager, Diversified

Best Estimate of the Technical Provisions FSI Regional Seminar for Supervisors in Africa on Risk Based Supervision Mombasa, Kenya, 14-17 September 2010 Leigh McMahon BA FIAA GAICD Senior Manager, Diversified

Representing Uncertainty by Probability and Possibility What s the Difference?

Representing Uncertainty by Probability and Possibility What s the Difference? Presentation at Amsterdam, March 29 30, 2011 Hans Schjær Jacobsen Professor, Director RD&I Ballerup, Denmark +45 4480 5030

Representing Uncertainty by Probability and Possibility What s the Difference? Presentation at Amsterdam, March 29 30, 2011 Hans Schjær Jacobsen Professor, Director RD&I Ballerup, Denmark +45 4480 5030

A linear algebraic method for pricing temporary life annuities

A linear algebraic method for pricing temporary life annuities P. Date (joint work with R. Mamon, L. Jalen and I.C. Wang) Department of Mathematical Sciences, Brunel University, London Outline Introduction

A linear algebraic method for pricing temporary life annuities P. Date (joint work with R. Mamon, L. Jalen and I.C. Wang) Department of Mathematical Sciences, Brunel University, London Outline Introduction

CEIOPS-DOC-33/09. (former CP 39) October 2009

October 2009") CEIOPS-DOC-33/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Technical provisions Article 86 a Actuarial and statistical methodologies to calculate the best estimate (former CP 39)

CEIOPS-DOC-33/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Technical provisions Article 86 a Actuarial and statistical methodologies to calculate the best estimate (former CP 39)

Stochastic Solvency Testing in Life Insurance. Genevieve Hayes

Stochastic Solvency Testing in Life Insurance Genevieve Hayes Deterministic Solvency Testing Assets > Liabilities In the insurance context, the values of the insurer s assets and liabilities are uncertain.

Stochastic Solvency Testing in Life Insurance Genevieve Hayes Deterministic Solvency Testing Assets > Liabilities In the insurance context, the values of the insurer s assets and liabilities are uncertain.

Guidelines on the valuation of technical provisions

EIOPA-BoS-14/166 EN Guidelines on the valuation of technical provisions EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20; Fax. + 49 69-951119-19; email: [email protected]

EIOPA-BoS-14/166 EN Guidelines on the valuation of technical provisions EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20; Fax. + 49 69-951119-19; email: [email protected]

Pricing Alternative forms of Commercial insurance cover. Andrew Harford

Pricing Alternative forms of Commercial insurance cover Andrew Harford Pricing alternative covers Types of policies Overview of Pricing Approaches Total claim cost distribution Discounting Cash flows Adjusting

Pricing Alternative forms of Commercial insurance cover Andrew Harford Pricing alternative covers Types of policies Overview of Pricing Approaches Total claim cost distribution Discounting Cash flows Adjusting

Quantitative Methods for Finance

Quantitative Methods for Finance Module 1: The Time Value of Money 1 Learning how to interpret interest rates as required rates of return, discount rates, or opportunity costs. 2 Learning how to explain

Quantitative Methods for Finance Module 1: The Time Value of Money 1 Learning how to interpret interest rates as required rates of return, discount rates, or opportunity costs. 2 Learning how to explain

STOCHASTIC CLAIMS RESERVING IN GENERAL INSURANCE. By P. D. England and R. J. Verrall. abstract. keywords. contact address. ".

B.A.J. 8, III, 443-544 (2002) STOCHASTIC CLAIMS RESERVING IN GENERAL INSURANCE By P. D. England and R. J. Verrall [Presented to the Institute of Actuaries, 28 January 2002] abstract This paper considers

B.A.J. 8, III, 443-544 (2002) STOCHASTIC CLAIMS RESERVING IN GENERAL INSURANCE By P. D. England and R. J. Verrall [Presented to the Institute of Actuaries, 28 January 2002] abstract This paper considers

Pricing Alternative forms of Commercial Insurance cover

Pricing Alternative forms of Commercial Insurance cover Prepared by Andrew Harford Presented to the Institute of Actuaries of Australia Biennial Convention 23-26 September 2007 Christchurch, New Zealand

Pricing Alternative forms of Commercial Insurance cover Prepared by Andrew Harford Presented to the Institute of Actuaries of Australia Biennial Convention 23-26 September 2007 Christchurch, New Zealand

Approximation of Aggregate Losses Using Simulation

Journal of Mathematics and Statistics 6 (3): 233-239, 2010 ISSN 1549-3644 2010 Science Publications Approimation of Aggregate Losses Using Simulation Mohamed Amraja Mohamed, Ahmad Mahir Razali and Noriszura

Journal of Mathematics and Statistics 6 (3): 233-239, 2010 ISSN 1549-3644 2010 Science Publications Approimation of Aggregate Losses Using Simulation Mohamed Amraja Mohamed, Ahmad Mahir Razali and Noriszura

Institute of Actuaries of India Subject CT3 Probability and Mathematical Statistics

Institute of Actuaries of India Subject CT3 Probability and Mathematical Statistics For 2015 Examinations Aim The aim of the Probability and Mathematical Statistics subject is to provide a grounding in

Institute of Actuaries of India Subject CT3 Probability and Mathematical Statistics For 2015 Examinations Aim The aim of the Probability and Mathematical Statistics subject is to provide a grounding in

SOA Health 2007 Spring Meeting Valuation and Reserving Techniques

SOA Health 2007 Spring Meeting Valuation and Reserving Techniques Property & Casualty Reserving Techniques Theresa Bourdon, FCAS, MAAA CAS Statement of Principles Regarding P&C Loss and Loss Adjustment

SOA Health 2007 Spring Meeting Valuation and Reserving Techniques Property & Casualty Reserving Techniques Theresa Bourdon, FCAS, MAAA CAS Statement of Principles Regarding P&C Loss and Loss Adjustment

Solution. Let us write s for the policy year. Then the mortality rate during year s is q 30+s 1. q 30+s 1

Solutions to the May 213 Course MLC Examination by Krzysztof Ostaszewski, http://wwwkrzysionet, krzysio@krzysionet Copyright 213 by Krzysztof Ostaszewski All rights reserved No reproduction in any form

Solutions to the May 213 Course MLC Examination by Krzysztof Ostaszewski, http://wwwkrzysionet, krzysio@krzysionet Copyright 213 by Krzysztof Ostaszewski All rights reserved No reproduction in any form

Cover. Optimal Retentions with Ruin Probability Target in The case of Fire. Insurance in Iran

Cover Optimal Retentions with Ruin Probability Target in The case of Fire Insurance in Iran Ghadir Mahdavi Ass. Prof., ECO College of Insurance, Allameh Tabataba i University, Iran Omid Ghavibazoo MS in

Cover Optimal Retentions with Ruin Probability Target in The case of Fire Insurance in Iran Ghadir Mahdavi Ass. Prof., ECO College of Insurance, Allameh Tabataba i University, Iran Omid Ghavibazoo MS in

Development Period 1 2 3 4 5 6 7 8 9 Observed Payments

Pricing and reserving in the general insurance industry Solutions developed in The SAS System John Hansen & Christian Larsen, Larsen & Partners Ltd 1. Introduction The two business solutions presented

Pricing and reserving in the general insurance industry Solutions developed in The SAS System John Hansen & Christian Larsen, Larsen & Partners Ltd 1. Introduction The two business solutions presented

Dr Christine Brown University of Melbourne

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

ING Insurance Economic Capital Framework

ING Insurance Economic Capital Framework Thomas C. Wilson Chief Insurance Risk Officer Kent University, September 5, 2007 www.ing.com Objectives of this session ING has been using economic capital internally

ING Insurance Economic Capital Framework Thomas C. Wilson Chief Insurance Risk Officer Kent University, September 5, 2007 www.ing.com Objectives of this session ING has been using economic capital internally

Practical Calculation of Expected and Unexpected Losses in Operational Risk by Simulation Methods

Practical Calculation of Expected and Unexpected Losses in Operational Risk by Simulation Methods Enrique Navarrete 1 Abstract: This paper surveys the main difficulties involved with the quantitative measurement

Practical Calculation of Expected and Unexpected Losses in Operational Risk by Simulation Methods Enrique Navarrete 1 Abstract: This paper surveys the main difficulties involved with the quantitative measurement

Property Casualty Insurer Economic Capital using a VAR Model Thomas Conway and Mark McCluskey

Property Casualty Insurer Economic Capital using a VAR Model Thomas Conway and Mark McCluskey Concept The purpose of this paper is to build a bridge between the traditional methods of looking at financial

Property Casualty Insurer Economic Capital using a VAR Model Thomas Conway and Mark McCluskey Concept The purpose of this paper is to build a bridge between the traditional methods of looking at financial

Tail-Dependence an Essential Factor for Correctly Measuring the Benefits of Diversification

Tail-Dependence an Essential Factor for Correctly Measuring the Benefits of Diversification Presented by Work done with Roland Bürgi and Roger Iles New Views on Extreme Events: Coupled Networks, Dragon

Tail-Dependence an Essential Factor for Correctly Measuring the Benefits of Diversification Presented by Work done with Roland Bürgi and Roger Iles New Views on Extreme Events: Coupled Networks, Dragon

Institute of Actuaries of India. ST7 General Insurance : Reserving & Capital Modelling

Institute of Actuaries of India ST7 General Insurance : Reserving & Capital Modelling November 2012 Examinations INDICATIVE SOLUTIONS Solution 1 : The different types of inflation affecting claim payment

Institute of Actuaries of India ST7 General Insurance : Reserving & Capital Modelling November 2012 Examinations INDICATIVE SOLUTIONS Solution 1 : The different types of inflation affecting claim payment

Intermediate Track II

Intermediate Track II September 2000 Minneapolis, Minnesota 1 This Session Will Discuss 1. Bornhuetter-Ferguson Method 2. Average Hindsight Method 3. Average Incremental Paid Method 2 BORNHUETTER- FERGUSON

Intermediate Track II September 2000 Minneapolis, Minnesota 1 This Session Will Discuss 1. Bornhuetter-Ferguson Method 2. Average Hindsight Method 3. Average Incremental Paid Method 2 BORNHUETTER- FERGUSON

Bodily Injury Thematic Review

2015 Bodily Injury Thematic Review ii Central Bank of Ireland Insurance Directorate 2015 BODILY INJURY THEMATIC REVIEW 1 Introduction 1.1 Overview and Context 4 1.2 Summary of Findings 5 1.3 Observations

2015 Bodily Injury Thematic Review ii Central Bank of Ireland Insurance Directorate 2015 BODILY INJURY THEMATIC REVIEW 1 Introduction 1.1 Overview and Context 4 1.2 Summary of Findings 5 1.3 Observations

Embedded Value Report

Embedded Value Report 2012 ACHMEA EMBEDDED VALUE REPORT 2012 Contents Management summary 3 Introduction 4 Embedded Value Results 5 Value Added by New Business 6 Analysis of Change 7 Sensitivities 9 Impact

Embedded Value Report 2012 ACHMEA EMBEDDED VALUE REPORT 2012 Contents Management summary 3 Introduction 4 Embedded Value Results 5 Value Added by New Business 6 Analysis of Change 7 Sensitivities 9 Impact

Bayesian prediction of disability insurance frequencies using economic indicators

Bayesian prediction of disability insurance frequencies using economic indicators Catherine Donnelly Heriot-Watt University, Edinburgh, UK Mario V. Wüthrich ETH Zurich, RisLab, Department of Mathematics,

Bayesian prediction of disability insurance frequencies using economic indicators Catherine Donnelly Heriot-Watt University, Edinburgh, UK Mario V. Wüthrich ETH Zurich, RisLab, Department of Mathematics,

Case Study Modeling Longevity Risk for Solvency II

Case Study Modeling Longevity Risk for Solvency II September 8, 2012 Longevity 8 Conference Waterloo, Ontario Presented by Stuart Silverman Principal & Consulting Actuary Background SOLVENCY II New Minimum

Case Study Modeling Longevity Risk for Solvency II September 8, 2012 Longevity 8 Conference Waterloo, Ontario Presented by Stuart Silverman Principal & Consulting Actuary Background SOLVENCY II New Minimum

Operations and Supply Chain Management Prof. G. Srinivasan Department of Management Studies Indian Institute of Technology, Madras

Operations and Supply Chain Management Prof. G. Srinivasan Department of Management Studies Indian Institute of Technology, Madras Lecture - 36 Location Problems In this lecture, we continue the discussion

Operations and Supply Chain Management Prof. G. Srinivasan Department of Management Studies Indian Institute of Technology, Madras Lecture - 36 Location Problems In this lecture, we continue the discussion

Projection of the With-Profits Balance Sheet under ICA+ John Lim (KPMG) & Richard Taylor (AEGON) 11 November 2013

& Richard Taylor (AEGON) 11 November 2013") Projection of the With-Profits Balance Sheet under ICA+ John Lim (KPMG) & Richard Taylor (AEGON) 11 November 2013 Introduction Projecting the with-profits business explicitly is already carried out by

Projection of the With-Profits Balance Sheet under ICA+ John Lim (KPMG) & Richard Taylor (AEGON) 11 November 2013 Introduction Projecting the with-profits business explicitly is already carried out by

Replicating Life Insurance Liabilities

Replicating Life Insurance Liabilities O. Khomenko Jena, 23 March 2011 1 Solvency II New Regulation for Insurance Industry Solvency II is a new regulation for European insurance industry. It is expected

Replicating Life Insurance Liabilities O. Khomenko Jena, 23 March 2011 1 Solvency II New Regulation for Insurance Industry Solvency II is a new regulation for European insurance industry. It is expected

BEL best estimate liability, deduced from the mean loss as a present value of mean loss,

Calculations of SCR, Technical Provisions, Market Value Margin (MVM) using the Cost of Capital method, for a one-year risk horizon, based on an ICRFS-Plus single composite model and associated forecast

Calculations of SCR, Technical Provisions, Market Value Margin (MVM) using the Cost of Capital method, for a one-year risk horizon, based on an ICRFS-Plus single composite model and associated forecast

Further Topics in Actuarial Mathematics: Premium Reserves. Matthew Mikola

Further Topics in Actuarial Mathematics: Premium Reserves Matthew Mikola April 26, 2007 Contents 1 Introduction 1 1.1 Expected Loss...................................... 2 1.2 An Overview of the Project...............................

Further Topics in Actuarial Mathematics: Premium Reserves Matthew Mikola April 26, 2007 Contents 1 Introduction 1 1.1 Expected Loss...................................... 2 1.2 An Overview of the Project...............................

DECISION MAKING UNDER UNCERTAINTY:

DECISION MAKING UNDER UNCERTAINTY: Models and Choices Charles A. Holloway Stanford University TECHNISCHE HOCHSCHULE DARMSTADT Fachbereich 1 Gesamtbibliothek Betrtebswirtscrtaftslehre tnventar-nr. :...2>2&,...S'.?S7.

DECISION MAKING UNDER UNCERTAINTY: Models and Choices Charles A. Holloway Stanford University TECHNISCHE HOCHSCHULE DARMSTADT Fachbereich 1 Gesamtbibliothek Betrtebswirtscrtaftslehre tnventar-nr. :...2>2&,...S'.?S7.

GN47: Stochastic Modelling of Economic Risks in Life Insurance

GN47: Stochastic Modelling of Economic Risks in Life Insurance Classification Recommended Practice MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND THAT

GN47: Stochastic Modelling of Economic Risks in Life Insurance Classification Recommended Practice MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND THAT

ESTIMATION OF CLAIM NUMBERS IN AUTOMOBILE INSURANCE

Annales Univ. Sci. Budapest., Sect. Comp. 42 (2014) 19 35 ESTIMATION OF CLAIM NUMBERS IN AUTOMOBILE INSURANCE Miklós Arató (Budapest, Hungary) László Martinek (Budapest, Hungary) Dedicated to András Benczúr

Annales Univ. Sci. Budapest., Sect. Comp. 42 (2014) 19 35 ESTIMATION OF CLAIM NUMBERS IN AUTOMOBILE INSURANCE Miklós Arató (Budapest, Hungary) László Martinek (Budapest, Hungary) Dedicated to András Benczúr

Society of Actuaries in Ireland

Society of Actuaries in Ireland Information and Assistance Note LA-1: Actuaries involved in the Own Risk & Solvency Assessment (ORSA) under Solvency II Life Assurance and Life Reinsurance Business Issued

Society of Actuaries in Ireland Information and Assistance Note LA-1: Actuaries involved in the Own Risk & Solvency Assessment (ORSA) under Solvency II Life Assurance and Life Reinsurance Business Issued

CAPITAL ALLOCATION FOR INSURANCE COMPANIES WHAT GOOD IS IT? H e l m u t G r ü n d l, Berlin* and H a t o S c h m e i s e r, Berlin*

CAPITAL ALLOCATION FOR INSURANCE COMPANIES WHAT GOOD IS IT? By H e l m u t G r ü n d l, Berlin* and H a t o S c h m e i s e r, Berlin* SEPTEMBER 23, SECOND DRAFT JEL-KLASSIFICATION: G22, G3, G32 *Institut

CAPITAL ALLOCATION FOR INSURANCE COMPANIES WHAT GOOD IS IT? By H e l m u t G r ü n d l, Berlin* and H a t o S c h m e i s e r, Berlin* SEPTEMBER 23, SECOND DRAFT JEL-KLASSIFICATION: G22, G3, G32 *Institut

The Voices of Influence iijournals.com PENSION & LONGEVITY RISK TRANSFER. for INSTITUTIONAL INVESTORS

The Voices of Influence iijournals.com PENSION & LONGEVITY RISK TRANSFER for INSTITUTIONAL INVESTORS FALL 2013 Quantifying the Mortality Longevity Offset Peter Nakada and Chris Hornsby Peter Nakada is

The Voices of Influence iijournals.com PENSION & LONGEVITY RISK TRANSFER for INSTITUTIONAL INVESTORS FALL 2013 Quantifying the Mortality Longevity Offset Peter Nakada and Chris Hornsby Peter Nakada is

One-year projection of run-off conditional tail expectation (CTE) reserves

reserves") MARCH 2013 ENTERPRISE RISK SOLUTIONS B&H RESEARCH ESG MARCH 2013 DOCUMENTATION PACK Steven Morrison PhD Laura Tadrowski PhD Craig Turnbull FIA Moody's Analytics Research Contact Us Americas +1.212.553.1658

MARCH 2013 ENTERPRISE RISK SOLUTIONS B&H RESEARCH ESG MARCH 2013 DOCUMENTATION PACK Steven Morrison PhD Laura Tadrowski PhD Craig Turnbull FIA Moody's Analytics Research Contact Us Americas +1.212.553.1658

Risk aggregation in insurance

THESIS FOR THE DEGREE OF LICENTIATE OF ENGINEERING Risk aggregation in insurance Jonas Alm Department of Mathematical Sciences Division of Mathematical Statistics Chalmers University of Technology and

THESIS FOR THE DEGREE OF LICENTIATE OF ENGINEERING Risk aggregation in insurance Jonas Alm Department of Mathematical Sciences Division of Mathematical Statistics Chalmers University of Technology and

Credit Risk Models: An Overview

Credit Risk Models: An Overview Paul Embrechts, Rüdiger Frey, Alexander McNeil ETH Zürich c 2003 (Embrechts, Frey, McNeil) A. Multivariate Models for Portfolio Credit Risk 1. Modelling Dependent Defaults:

Credit Risk Models: An Overview Paul Embrechts, Rüdiger Frey, Alexander McNeil ETH Zürich c 2003 (Embrechts, Frey, McNeil) A. Multivariate Models for Portfolio Credit Risk 1. Modelling Dependent Defaults:

Financial Simulation Models in General Insurance

Financial Simulation Models in General Insurance By - Peter D. England Abstract Increases in computer power and advances in statistical modelling have conspired to change the way financial modelling is

Financial Simulation Models in General Insurance By - Peter D. England Abstract Increases in computer power and advances in statistical modelling have conspired to change the way financial modelling is

A liability driven approach to asset allocation

A liability driven approach to asset allocation Xinliang Chen 1, Jan Dhaene 2, Marc Goovaerts 2, Steven Vanduffel 3 Abstract. We investigate a liability driven methodology for determining optimal asset

A liability driven approach to asset allocation Xinliang Chen 1, Jan Dhaene 2, Marc Goovaerts 2, Steven Vanduffel 3 Abstract. We investigate a liability driven methodology for determining optimal asset

INTEGRATED OPTIMIZATION OF SAFETY STOCK

INTEGRATED OPTIMIZATION OF SAFETY STOCK AND TRANSPORTATION CAPACITY Horst Tempelmeier Department of Production Management University of Cologne Albertus-Magnus-Platz D-50932 Koeln, Germany http://www.spw.uni-koeln.de/

INTEGRATED OPTIMIZATION OF SAFETY STOCK AND TRANSPORTATION CAPACITY Horst Tempelmeier Department of Production Management University of Cologne Albertus-Magnus-Platz D-50932 Koeln, Germany http://www.spw.uni-koeln.de/

Stochastic Claims Reserving Methods in Non-Life Insurance

Stochastic Claims Reserving Methods in Non-Life Insurance Mario V. Wüthrich 1 Department of Mathematics ETH Zürich Michael Merz 2 Faculty of Economics University Tübingen Version 1.1 1 ETH Zürich, CH-8092

Stochastic Claims Reserving Methods in Non-Life Insurance Mario V. Wüthrich 1 Department of Mathematics ETH Zürich Michael Merz 2 Faculty of Economics University Tübingen Version 1.1 1 ETH Zürich, CH-8092

Quantitative Operational Risk Management

Quantitative Operational Risk Management Kaj Nyström and Jimmy Skoglund Swedbank, Group Financial Risk Control S-105 34 Stockholm, Sweden September 3, 2002 Abstract The New Basel Capital Accord presents

Quantitative Operational Risk Management Kaj Nyström and Jimmy Skoglund Swedbank, Group Financial Risk Control S-105 34 Stockholm, Sweden September 3, 2002 Abstract The New Basel Capital Accord presents

Fundamentals of Actuarial Mathematics. 3rd Edition

Brochure More information from http://www.researchandmarkets.com/reports/2866022/ Fundamentals of Actuarial Mathematics. 3rd Edition Description: - Provides a comprehensive coverage of both the deterministic

Brochure More information from http://www.researchandmarkets.com/reports/2866022/ Fundamentals of Actuarial Mathematics. 3rd Edition Description: - Provides a comprehensive coverage of both the deterministic

Capital Requirements for Variable Annuities - Discussion Paper. August 2009. Insurance Supervision Department

Capital Requirements for Variable Annuities - Discussion Paper August 2009 Insurance Supervision Department Contents Introduction... 2 Suggested Methodology... 3 Basic Principle... 3 Basic Guarantee Liabilities...

Capital Requirements for Variable Annuities - Discussion Paper August 2009 Insurance Supervision Department Contents Introduction... 2 Suggested Methodology... 3 Basic Principle... 3 Basic Guarantee Liabilities...

Master of Mathematical Finance: Course Descriptions

Master of Mathematical Finance: Course Descriptions CS 522 Data Mining Computer Science This course provides continued exploration of data mining algorithms. More sophisticated algorithms such as support

Master of Mathematical Finance: Course Descriptions CS 522 Data Mining Computer Science This course provides continued exploration of data mining algorithms. More sophisticated algorithms such as support

STATISTICAL METHODS IN GENERAL INSURANCE. Philip J. Boland National University of Ireland, Dublin [email protected]

STATISTICAL METHODS IN GENERAL INSURANCE Philip J. Boland National University of Ireland, Dublin [email protected] The Actuarial profession appeals to many with excellent quantitative skills who aspire

STATISTICAL METHODS IN GENERAL INSURANCE Philip J. Boland National University of Ireland, Dublin [email protected] The Actuarial profession appeals to many with excellent quantitative skills who aspire

Solvency II and Predictive Analytics in LTC and Beyond HOW U.S. COMPANIES CAN IMPROVE ERM BY USING ADVANCED

Solvency II and Predictive Analytics in LTC and Beyond HOW U.S. COMPANIES CAN IMPROVE ERM BY USING ADVANCED TECHNIQUES DEVELOPED FOR SOLVENCY II AND EMERGING PREDICTIVE ANALYTICS METHODS H o w a r d Z

Solvency II and Predictive Analytics in LTC and Beyond HOW U.S. COMPANIES CAN IMPROVE ERM BY USING ADVANCED TECHNIQUES DEVELOPED FOR SOLVENCY II AND EMERGING PREDICTIVE ANALYTICS METHODS H o w a r d Z

Life Cycle Asset Allocation A Suitable Approach for Defined Contribution Pension Plans

Life Cycle Asset Allocation A Suitable Approach for Defined Contribution Pension Plans Challenges for defined contribution plans While Eastern Europe is a prominent example of the importance of defined

Life Cycle Asset Allocation A Suitable Approach for Defined Contribution Pension Plans Challenges for defined contribution plans While Eastern Europe is a prominent example of the importance of defined

Bootstrap Modeling: Beyond the Basics

Mark R. Shapland, FCAS, ASA, MAAA Jessica (Weng Kah) Leong, FIAA, FCAS, MAAA Abstract Motivation. Bootstrapping is a very versatile model for estimating a distribution of possible outcomes for the unpaid

Mark R. Shapland, FCAS, ASA, MAAA Jessica (Weng Kah) Leong, FIAA, FCAS, MAAA Abstract Motivation. Bootstrapping is a very versatile model for estimating a distribution of possible outcomes for the unpaid

A reserve risk model for a non-life insurance company

A reserve risk model for a non-life insurance company Salvatore Forte 1, Matteo Ialenti 1, and Marco Pirra 2 1 Department of Actuarial Sciences, Sapienza University of Roma, Viale Regina Elena 295, 00185

A reserve risk model for a non-life insurance company Salvatore Forte 1, Matteo Ialenti 1, and Marco Pirra 2 1 Department of Actuarial Sciences, Sapienza University of Roma, Viale Regina Elena 295, 00185

ON THE PREDICTION ERROR IN SEVERAL CLAIMS RESERVES ESTIMATION METHODS IEVA GEDIMINAITĖ

ON THE PREDICTION ERROR IN SEVERAL CLAIMS RESERVES ESTIMATION METHODS IEVA GEDIMINAITĖ MASTER THESIS STOCKHOLM, 2009 Royal Institute of Technology School of Engineering Sciences Dept. of Mathematics Master

ON THE PREDICTION ERROR IN SEVERAL CLAIMS RESERVES ESTIMATION METHODS IEVA GEDIMINAITĖ MASTER THESIS STOCKHOLM, 2009 Royal Institute of Technology School of Engineering Sciences Dept. of Mathematics Master

EDUCATION AND EXAMINATION COMMITTEE SOCIETY OF ACTUARIES RISK AND INSURANCE. Copyright 2005 by the Society of Actuaries

EDUCATION AND EXAMINATION COMMITTEE OF THE SOCIET OF ACTUARIES RISK AND INSURANCE by Judy Feldman Anderson, FSA and Robert L. Brown, FSA Copyright 25 by the Society of Actuaries The Education and Examination

EDUCATION AND EXAMINATION COMMITTEE OF THE SOCIET OF ACTUARIES RISK AND INSURANCE by Judy Feldman Anderson, FSA and Robert L. Brown, FSA Copyright 25 by the Society of Actuaries The Education and Examination

Modelling Uncertainty in Claims Experience to Price General Insurance Contracts

Modelling Uncertainty in Claims Experience to Price General Insurance Contracts Vanita Duggal Actuary Palisade Risk Conference, Mumbai January 13, 2015 What is Insurance? Coverage by contract whereby one

Modelling Uncertainty in Claims Experience to Price General Insurance Contracts Vanita Duggal Actuary Palisade Risk Conference, Mumbai January 13, 2015 What is Insurance? Coverage by contract whereby one