Risk and Return. Peachtree Securities, Inc. (A)

|

|

|

- Samuel Roberts

- 9 years ago

- Views:

Transcription

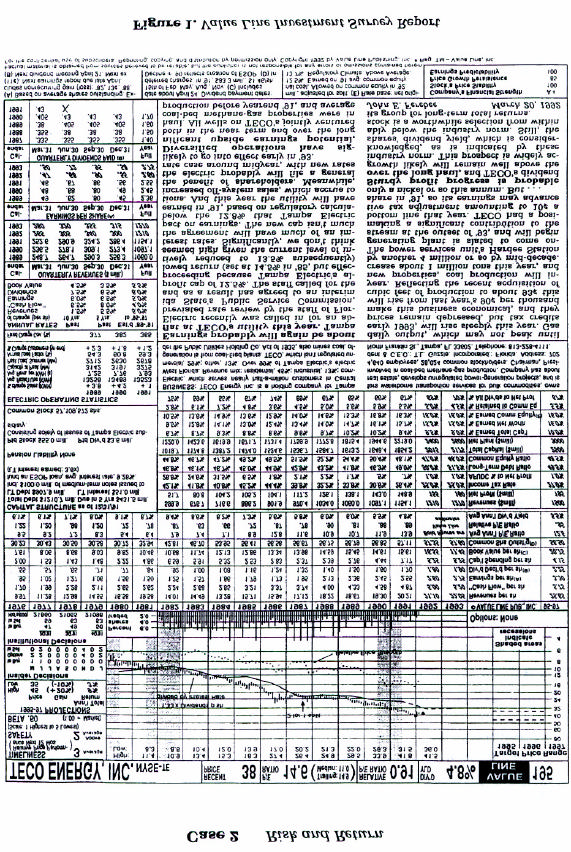

1 2 Risk and Return Peachtree Securities, Inc. (A) Peachtree Securities is a regional brokerage house based in Atlanta. Although the firm is only 20 years old, it has prospered by following a simple goal providing quality personal brokerage services to small investors. Jake Taylor, the firm s founder and president, is well-satisfied with Peachtree s progress. However, he is apprehensive about the future, as more and more of the firm s customers are buying mutual funds rather than individual stocks and bonds. Thus, even though the number of customers per office has been increasing because of population growth, the number of transactions per customer has been decreasing, and hence sales growth has slackened. Taylor believes this trend will continue, so he has been actively expanding his product line in an effort to increase sales volume. As a first step, Peachtree began offering trust and portfolio management services five years ago. Many of the trust clients are retirees who are interested primarily in current income rather than capital gains. Thus, an average portfolio consists mostly of bonds and high yield stocks. The stock component is heavily weighted with electric utilities, an industry that has traditionally paid high dividends. For example, the average electric company s dividend yield was about 6.3 percent in 1992, versus an average stock s yield of 3.1 percent. Until 1993, Peachtree had no in-house security analysts all stock and bond selections were based on research provided by subscription services. However, these services had become very costly, and the volume of portfolio management had reached the point where hiring an in-house analyst was now cost-effective. Because most of its portfolios were heavily weighted with electric utilities, Peachtree created its first analyst position to track this industry. Taylor hired Laura Donahue, a recent graduate of the University of Georgia, to fill the job. Donahue reported to work in early January, 1993, jubilant at having the opportunity to use the skills she had worked so hard to learn. Taylor then informed her that her first task would be to conduct a seminar for a group of Peachtree customers on stock investments, including the effects of different securities on portfolio performance. Donahue was asked to pick an electric utility, assess its riskiness, develop an estimate of its required rate of return on equity, and then present her findings to a group of Peachtree s customers. Donahue s first step choosing the company- was simple. She had been born and raised in Tampa, Florida, so she picked TECO Energy, Inc., the holding company for Tampa Electric. Next, she searched for information on the company. Donahue remembered using the Value Line Investment Survey during her student days, so she turned to this 1

2 source first. (See Figure 1 on the last page of this case.) Then, she spent a few days reviewing industry trends to gain a historical perspective. Electric utilities are granted monopolies to provide electric service in a given geographical area. In exchange for the franchise, the company is subjected to regulation over both the prices it may charge and the quality of its service. In theory, regulation acts to prevent the company from abusing its monopoly position, and its prices are set to mimic those that would occur if the firm were operating under perfect competition. Under such competition, the firm would earn its cost of capital, no more and no less. In the 1950s and much of the 1960s, electric utilities were in an ideal position. Their costs were declining because of technological advances and economies of scale in generation and distribution. This made everyone happy- managers, regulators, stockholders, and customers. However, the situation changed dramatically during the 1970s, when inflation, along with high gas and oil prices, pushed construction and operating costs to levels which were unimaginable just a few years earlier. The result was a massive change in the economics of the industry and in how investors viewed electric utilities. Today, the industry is facing many challenges including cogeneration, diversification, deregulation, and nuclear generation. Cogeneration is the combined production of electricity and thermal power, usually steam. Most electric companies use coal or nuclear energy to generate electricity. In the 1980s, though, oil and gas prices dropped sharply, making it cheaper to generate with gas or oil. However, one cannot burn gas or oil in a coal or nuclear plant. The changed fuel cost situation, combined with a need for steam, made it profitable for many industrial customers to switch to cogeneration. This, in turn, has made it very difficult for utilities to forecast industrial demand. Also, since utilities must buy any surplus power generated by their former customers, companies with cogeneration plants are, in effect, competing with the electric companies. Diversification, or expansion into nonregulated industries, is being evaluated by many utility companies. Due to large depreciation flows following completion of major plant construction programs in the early 1980 s, many companies now have cash flows that exceed immediate needs. Industry officials believe that usage of these cash flows to diversify into nonregulated industries would smooth out the financial risks of the regulated business, while providing companies an opportunity to earn returns above those allowed by regulation. To facilitate diversification, many electric utilities, including TECO, have formed holding companies under which the parent company holds both regulated and nonregulated subsidiaries. Diversification does have some potential downside for both utility customers (ratepayers) and stockholders. Ratepayers are supposed to pay the costs associated with producing and delivering power, plus enough to cover the utility s cost of capital. However, a diversified utility could, theoretically, allocate some corporate costs that should be assigned to the unregulated (diversified) subsidiaries to the regulated utility. This would cause reported profits to be abnormally high for the nonregulated business. In effect, 2

3 ratepayers would be subsidizing the nonregulated businesses. The total corporation s overall rate of return would be excessive, because it would be earning the regulated cost of capital on utility operations and more than a competitive return on nonregulated operations. Of course, regulators are aware of all this, so their auditors are always on the alert to detect and prevent improper cost allocations. There are two significant risks to stockholders from utility diversification programs. First, there is the chance that utility executives, who generally have limited exposure to intense competition, will fail in the competitive, nonregulated, markets they enter. In that case, money that could have been paid out as dividends will have been lost in business ventures that turned out to be unprofitable. Second, if the diversified activities are highly profitable, causing the overall corporation to earn a high rate of return, then regulators might reduce the returns allowed on the utility operations. There is always a question as to what a company s cost of capital really is hence the rate of return the utility commission should allow it to earn-and it is easier for a commission to set the allowed rate of return at the low end of any reasonable range if the company is highly profitable because of successful nonregulated businesses. Thus, it has been argued that diversified utilities might be getting into a can t-win situation. As one analyst put it, a diversified utility s stockholders are in a heads you win, tails I lose situation. There is also much discussion at present about the deregulation of the electricity markets per se, and there is much controversy over the forced use of wheeling, whereby a customer (usually a large industrial customer) buys power from some other party but gets delivery over the transmission lines of the utility in whose service area it operates. This situation has occurred to a large extent in the gas industry, where large customers have contracted directly with producers and then forced (through legal actions) pipeline companies to deliver the gas. Another problem facing many, but not all, electric companies relates to nuclear plants. A few decades ago, nuclear power was thought by many to be the wave of the future in electric generation. It was widely believed that nuclear was cleaner and cheaper than coal, oil, and gas generation. However, the 1979 accident at Three Mile Island almost instantly reversed the future of nuclear power. Many plants that were under construction at that time were canceled, while the costs of completing the remaining plants skyrocketed. Many partially completed plants had to be retrofitted with new safety devices. As a result, the cost of power from new nuclear plants rose dramatically. Further, several states have held referendums to close nuclear plants. With this industry overview in mind, Laura Donahue developed the data in Table 1 on returns expected in the coming year. TECO is the stock of primary interest, Gold Hill is a domestic gold mining company, and the S& P 500 Fund is a mutual fund that invests in the stocks which make up the S&P 500 index. Donahue s final preparatory step was to outline some questions that she believed to be relevant to the task at hand. See if you can answer the questions she developed. 3

4 Table I Estimated Total Returns State of Economy Probability T- Bond Teco Gold Hill S&P 500 Fund Recession 10% 8% -8% 18% -15% Below 20% 8% 2% 23% 0% Average Average 40% 8% 14% 7% 15% Above 20% 8% 25% -3% 30% Average Boom 10% 8% 33% 2% 45% 4

5 Questions 1. a. Why is the T-bond return in Table 1 shown to be independent of the state of the economy? b. Is the return on a 1-year T-bond risk-free? 2. a. Calculate the expected rate of return on each of the four alternatives listed in Table 1. b. Based solely on expected returns, which of the potential investments appears best? 3. Now calculate the standard deviations and coefficients of variation of returns for the four alternatives. a. What type of risk do these statistics measure? b. Is the standard deviation or the coefficient of variation the better measure? c. How do the alternatives compare when risk is considered? (Hint: for the S&P 500, the standard deviation = 16.4%; for Gold Hill, the standard deviation = 9.1%.) 4. Suppose an investor forms a stock portfolio by investing $10,000 in Gold Hill and $10,000 in TECO. a. What would be the portfolio s expected rate of return, standard deviation, and coefficient of variation? b. How does this compare with values for the individual stocks? c. What characteristic of the two investments makes risk reduction possible? d. What do you think would happen to the portfolio s expected rate of return and standard deviation if the portfolio contained 75 percent Gold Hill? If it contained 75 percent TECO? Using excel, construct the portfolio to substantiate your answers. 5. Now consider a portfolio consisting of $10,000 in TECO and $10,000 in the S&P 500 Fund. a. Would this portfolio have the same risk-reducing effect as the Gold Hill-TECO portfolio considered in Question 4? Explain. b.construct a portfolio using TECO and the S&P 500 Fund in excel to substantiate your answer. 5

6 6. Suppose an investor starts with a portfolio consisting of one randomly selected stock. a. What would happen to the portfolio s risk if more and more randomly selected stocks were added? b. What are the implications for investors? c. Do portfolio effects impact the way investors should think about the riskiness of individual securities? d. Would you expect this to affect companies costs of capital? e. Explain the differences between total risk, diversifiable (companyspecific) risk, and market risk. f. Assume that you choose to hold a single stock portfolio. Should you expect to be compensated for all of the risk that you bear? 7. Now change Table 1 by crossing out the state of the economy and probability columns and replacing them with Year 1, Year 2, Year 3, Year 4, and Year 5. Then, plot three lines on a scatter diagram which shows the returns on the S& P 500 (the market) on the X axis and (1) T-bond returns, (2) TECO returns, and (3) Gold Hill returns on the Y axis. What are these lines called? Estimate the slope coefficient of each line. What is the slope coefficient called, and what is its significance? What is the significance of the distance between the plot points and the regression line, i.e. the errors? (Note: If you have a calculator with statistical functions, use linear regression to find the slope coefficients.) 8. Plot the Security Market Line. (Hint: Use Table 1 data to obtain the risk-free rate and the required rate of return on the market.) What is the required rate of return (use CAPM) on TECO s stock using Value Line s beta estimate of 0.6 as reported in Figure 1? Plot Teco s expected rate of return you calculated in 2a. Based on the SML analysis, should investors buy TECO stock? 6

7 9. a. What would happen to TECO s required rate of return if inflation expectations increased by 3 percentage points above the estimate embedded in the 8.0 percent risk-free rate? b. Now go back to the original inflation estimate, where K rf = 8%, and indicate what would happen to TECO s required rate of return if investors risk aversion increased so that the market risk premium rose from 7 percent to 8 percent. c. Now go back to the original conditions (k rf = 8%, RP m = 7%) and assume that TECO s beta rose from 0.6 to 1.0. What effect would this have on the required rate of return? d. What is the efficient markets of hypothesis (EMH)? a. What impact does this theory have on decisions concerning the investment in securities? b. Is it applicable to real assets such as plant and equipment? c. What impact does the EMH have on corporate financing decisions? d. Should Jake Taylor be concerned about the EMH when he considers adding to his staff of security analysts? Explain. 10. Notwithstanding the Value Line report, suppose TECO s long-term debt ratio (Long-term debt/total assets) decreased during the period 1982 through Further, suppose this ratio was projected to continue decreasing in 1993 and beyond. What impact would this have on TECO s riskiness, hence on its beta and required rate of return on equity? 7

8 8

Chapter 5 Risk and Return ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 5 Risk and Return ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 5-1 a. Stand-alone risk is only a part of total risk and pertains to the risk an investor takes by holding only one asset. Risk is

Chapter 5 Risk and Return ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 5-1 a. Stand-alone risk is only a part of total risk and pertains to the risk an investor takes by holding only one asset. Risk is

Review for Exam 2. Instructions: Please read carefully

Review for Exam Instructions: Please read carefully The exam will have 1 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation questions.

Review for Exam Instructions: Please read carefully The exam will have 1 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation questions.

MBA 8230 Corporation Finance (Part II) Practice Final Exam #2

Practice Final Exam #2") MBA 8230 Corporation Finance (Part II) Practice Final Exam #2 1. Which of the following input factors, if increased, would result in a decrease in the value of a call option? a. the volatility of the company's

MBA 8230 Corporation Finance (Part II) Practice Final Exam #2 1. Which of the following input factors, if increased, would result in a decrease in the value of a call option? a. the volatility of the company's

WEB APPENDIX. Calculating Beta Coefficients. b Beta Rise Run Y 7.1 1 8.92 X 10.0 0.0 16.0 10.0 1.6

WEB APPENDIX 8A Calculating Beta Coefficients The CAPM is an ex ante model, which means that all of the variables represent before-thefact, expected values. In particular, the beta coefficient used in

WEB APPENDIX 8A Calculating Beta Coefficients The CAPM is an ex ante model, which means that all of the variables represent before-thefact, expected values. In particular, the beta coefficient used in

Chapter 9. The Valuation of Common Stock. 1.The Expected Return (Copied from Unit02, slide 36)

") Readings Chapters 9 and 10 Chapter 9. The Valuation of Common Stock 1. The investor s expected return 2. Valuation as the Present Value (PV) of dividends and the growth of dividends 3. The investor s required

Readings Chapters 9 and 10 Chapter 9. The Valuation of Common Stock 1. The investor s expected return 2. Valuation as the Present Value (PV) of dividends and the growth of dividends 3. The investor s required

Chapter 5. Conditional CAPM. 5.1 Conditional CAPM: Theory. 5.1.1 Risk According to the CAPM. The CAPM is not a perfect model of expected returns.

Chapter 5 Conditional CAPM 5.1 Conditional CAPM: Theory 5.1.1 Risk According to the CAPM The CAPM is not a perfect model of expected returns. In the 40+ years of its history, many systematic deviations

Chapter 5 Conditional CAPM 5.1 Conditional CAPM: Theory 5.1.1 Risk According to the CAPM The CAPM is not a perfect model of expected returns. In the 40+ years of its history, many systematic deviations

Chapter 5. Risk and Return. Copyright 2009 Pearson Prentice Hall. All rights reserved.

Chapter 5 Risk and Return Learning Goals 1. Understand the meaning and fundamentals of risk, return, and risk aversion. 2. Describe procedures for assessing and measuring the risk of a single asset. 3.

Chapter 5 Risk and Return Learning Goals 1. Understand the meaning and fundamentals of risk, return, and risk aversion. 2. Describe procedures for assessing and measuring the risk of a single asset. 3.

CHAPTER 6. Topics in Chapter. What are investment returns? Risk, Return, and the Capital Asset Pricing Model

CHAPTER 6 Risk, Return, and the Capital Asset Pricing Model 1 Topics in Chapter Basic return concepts Basic risk concepts Stand-alone risk Portfolio (market) risk Risk and return: CAPM/SML 2 What are investment

CHAPTER 6 Risk, Return, and the Capital Asset Pricing Model 1 Topics in Chapter Basic return concepts Basic risk concepts Stand-alone risk Portfolio (market) risk Risk and return: CAPM/SML 2 What are investment

Investing Practice Questions

Investing Practice Questions 1) When interest is calculated only on the principal amount of the investment, it is known as: a) straight interest b) simple interest c) compound interest d) calculated interest

Investing Practice Questions 1) When interest is calculated only on the principal amount of the investment, it is known as: a) straight interest b) simple interest c) compound interest d) calculated interest

Weighted Average Cost of Capital (WACC)

") Financial Modeling Templates (WACC) http://spreadsheetml.com/finance/weightedaveragecostofcapital.shtml Copyright (c) 2009-2014, ConnectCode All Rights Reserved. ConnectCode accepts no responsibility for

Financial Modeling Templates (WACC) http://spreadsheetml.com/finance/weightedaveragecostofcapital.shtml Copyright (c) 2009-2014, ConnectCode All Rights Reserved. ConnectCode accepts no responsibility for

ENERGY ADVISORY COMMITTEE. Electricity Market Review: Return on Investment

ENERGY ADVISORY COMMITTEE Electricity Market Review: Return on Investment The Issue To review the different approaches in determining the return on investment in the electricity supply industry, and to

ENERGY ADVISORY COMMITTEE Electricity Market Review: Return on Investment The Issue To review the different approaches in determining the return on investment in the electricity supply industry, and to

Chapter 11 The Cost of Capital ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 11 The Cost of Capital ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 11-1 a. The weighted average cost of capital, WACC, is the weighted average of the after-tax component costs of capital -debt,

Chapter 11 The Cost of Capital ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 11-1 a. The weighted average cost of capital, WACC, is the weighted average of the after-tax component costs of capital -debt,

Solution: The optimal position for an investor with a coefficient of risk aversion A = 5 in the risky asset is y*:

Problem 1. Consider a risky asset. Suppose the expected rate of return on the risky asset is 15%, the standard deviation of the asset return is 22%, and the risk-free rate is 6%. What is your optimal position

Problem 1. Consider a risky asset. Suppose the expected rate of return on the risky asset is 15%, the standard deviation of the asset return is 22%, and the risk-free rate is 6%. What is your optimal position

Shares Mutual funds Structured bonds Bonds Cash money, deposits

FINANCIAL INSTRUMENTS AND RELATED RISKS This description of investment risks is intended for you. The professionals of AB bank Finasta have strived to understandably introduce you the main financial instruments

FINANCIAL INSTRUMENTS AND RELATED RISKS This description of investment risks is intended for you. The professionals of AB bank Finasta have strived to understandably introduce you the main financial instruments

CHAPTER 10 RISK AND RETURN: THE CAPITAL ASSET PRICING MODEL (CAPM)

") CHAPTER 10 RISK AND RETURN: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concepts Review and Critical Thinking Questions 1. Some of the risk in holding any asset is unique to the asset in question.

CHAPTER 10 RISK AND RETURN: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concepts Review and Critical Thinking Questions 1. Some of the risk in holding any asset is unique to the asset in question.

Review for Exam 2. Instructions: Please read carefully

Review for Exam 2 Instructions: Please read carefully The exam will have 25 multiple choice questions and 5 work problems You are not responsible for any topics that are not covered in the lecture note

Review for Exam 2 Instructions: Please read carefully The exam will have 25 multiple choice questions and 5 work problems You are not responsible for any topics that are not covered in the lecture note

Models of Risk and Return

Models of Risk and Return Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Models of Risk and Return Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Answers to Concepts in Review

Answers to Concepts in Review 1. A portfolio is simply a collection of investments assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected return

Answers to Concepts in Review 1. A portfolio is simply a collection of investments assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected return

The Tangent or Efficient Portfolio

The Tangent or Efficient Portfolio 1 2 Identifying the Tangent Portfolio Sharpe Ratio: Measures the ratio of reward-to-volatility provided by a portfolio Sharpe Ratio Portfolio Excess Return E[ RP ] r

The Tangent or Efficient Portfolio 1 2 Identifying the Tangent Portfolio Sharpe Ratio: Measures the ratio of reward-to-volatility provided by a portfolio Sharpe Ratio Portfolio Excess Return E[ RP ] r

Market Efficiency and Behavioral Finance. Chapter 12

Market Efficiency and Behavioral Finance Chapter 12 Market Efficiency if stock prices reflect firm performance, should we be able to predict them? if prices were to be predictable, that would create the

Market Efficiency and Behavioral Finance Chapter 12 Market Efficiency if stock prices reflect firm performance, should we be able to predict them? if prices were to be predictable, that would create the

Total shares at the end of ten years is 100*(1+5%) 10 =162.9.

10 =162.9.") FCS5510 Sample Homework Problems Unit04 CHAPTER 8 STOCK PROBLEMS 1. An investor buys 100 shares if a $40 stock that pays a annual cash dividend of $2 a share (a 5% dividend yield) and signs up for the

FCS5510 Sample Homework Problems Unit04 CHAPTER 8 STOCK PROBLEMS 1. An investor buys 100 shares if a $40 stock that pays a annual cash dividend of $2 a share (a 5% dividend yield) and signs up for the

One-Stop-Shopping Investment For Retirement Planning

TARGET DATE RETIREMENT FUNDS One-Stop-Shopping Investment For Retirement Planning Investing for retirement can be challenging if you re not an expert. Here s a simple choice for your retirement investing...

TARGET DATE RETIREMENT FUNDS One-Stop-Shopping Investment For Retirement Planning Investing for retirement can be challenging if you re not an expert. Here s a simple choice for your retirement investing...

Practice Set #4 and Solutions.

FIN-469 Investments Analysis Professor Michel A. Robe Practice Set #4 and Solutions. What to do with this practice set? To help students prepare for the assignment and the exams, practice sets with solutions

FIN-469 Investments Analysis Professor Michel A. Robe Practice Set #4 and Solutions. What to do with this practice set? To help students prepare for the assignment and the exams, practice sets with solutions

Chapter 9 The Cost of Capital ANSWERS TO SELEECTED END-OF-CHAPTER QUESTIONS

Chapter 9 The Cost of Capital ANSWERS TO SELEECTED END-OF-CHAPTER QUESTIONS 9-1 a. The weighted average cost of capital, WACC, is the weighted average of the after-tax component costs of capital -debt,

Chapter 9 The Cost of Capital ANSWERS TO SELEECTED END-OF-CHAPTER QUESTIONS 9-1 a. The weighted average cost of capital, WACC, is the weighted average of the after-tax component costs of capital -debt,

Cost of Capital Presentation for ERRA Tariff Committee Dr. Konstantin Petrov / Waisum Cheng / Dr. Daniel Grote April 2009 Experience you can trust.

Cost of Capital Presentation for ERRA Tariff Committee Dr. Konstantin Petrov / Waisum Cheng / Dr. Daniel Grote April 2009 Experience you can trust. Agenda 1.Definition of Cost of Capital a) Concept and

Cost of Capital Presentation for ERRA Tariff Committee Dr. Konstantin Petrov / Waisum Cheng / Dr. Daniel Grote April 2009 Experience you can trust. Agenda 1.Definition of Cost of Capital a) Concept and

DSIP List (Diversified Stock Income Plan)

") Kent A. Newcomb, CFA, Equity Sector Analyst Joseph E. Buffa, Equity Sector Analyst DSIP List (Diversified Stock Income Plan) Commentary from ASG's Equity Sector Analysts January 2014 Concept Review The

Kent A. Newcomb, CFA, Equity Sector Analyst Joseph E. Buffa, Equity Sector Analyst DSIP List (Diversified Stock Income Plan) Commentary from ASG's Equity Sector Analysts January 2014 Concept Review The

ENTREPRENEURIAL FINANCE: Strategy Valuation and Deal Structure

ENTREPRENEURIAL FINANCE: Strategy Valuation and Deal Structure Chapter 9 Valuation Questions and Problems 1. You are considering purchasing shares of DeltaCad Inc. for $40/share. Your analysis of the company

ENTREPRENEURIAL FINANCE: Strategy Valuation and Deal Structure Chapter 9 Valuation Questions and Problems 1. You are considering purchasing shares of DeltaCad Inc. for $40/share. Your analysis of the company

Chapter 13 Composition of the Market Portfolio 1. Capital markets in Flatland exhibit trade in four securities, the stocks X, Y and Z,

Chapter 13 Composition of the arket Portfolio 1. Capital markets in Flatland exhibit trade in four securities, the stocks X, Y and Z, and a riskless government security. Evaluated at current prices in

Chapter 13 Composition of the arket Portfolio 1. Capital markets in Flatland exhibit trade in four securities, the stocks X, Y and Z, and a riskless government security. Evaluated at current prices in

Source of Finance and their Relative Costs F. COST OF CAPITAL

F. COST OF CAPITAL 1. Source of Finance and their Relative Costs 2. Estimating the Cost of Equity 3. Estimating the Cost of Debt and Other Capital Instruments 4. Estimating the Overall Cost of Capital

F. COST OF CAPITAL 1. Source of Finance and their Relative Costs 2. Estimating the Cost of Equity 3. Estimating the Cost of Debt and Other Capital Instruments 4. Estimating the Overall Cost of Capital

Risk and Return. a. 25.3% b. 22.5% c. 23.3% d. 17.1%

Risk and Return 1. The Duncan Company's stock is currently selling for $15. People generally expect its price to rise to $18 by the end of next year and that it will pay a dividend of $.50 per share during

Risk and Return 1. The Duncan Company's stock is currently selling for $15. People generally expect its price to rise to $18 by the end of next year and that it will pay a dividend of $.50 per share during

The Language of the Stock Market

The Language of the Stock Market Family Economics & Financial Education Family Economics & Financial Education Revised November 2004 Investing Unit Language of the Stock Market Slide 1 Why Learn About

The Language of the Stock Market Family Economics & Financial Education Family Economics & Financial Education Revised November 2004 Investing Unit Language of the Stock Market Slide 1 Why Learn About

What Annuities Can (and Can t) Do for Retirees With proper handling and expectations, annuities are powerful retirement income tools

Do for Retirees With proper handling and expectations, annuities are powerful retirement income tools") What Annuities Can (and Can t) Do for Retirees With proper handling and expectations, annuities are powerful retirement income tools Illustration by Enrico Varrasso A 65-year old American male has a 10%

What Annuities Can (and Can t) Do for Retirees With proper handling and expectations, annuities are powerful retirement income tools Illustration by Enrico Varrasso A 65-year old American male has a 10%

Chapter 11, Risk and Return

Chapter 11, Risk and Return 1. A portfolio is. A) a group of assets, such as stocks and bonds, held as a collective unit by an investor B) the expected return on a risky asset C) the expected return on

Chapter 11, Risk and Return 1. A portfolio is. A) a group of assets, such as stocks and bonds, held as a collective unit by an investor B) the expected return on a risky asset C) the expected return on

1. a. (iv) b. (ii) [6.75/(1.34) = 10.2] c. (i) Writing a call entails unlimited potential losses as the stock price rises.

![1. a. (iv) b. (ii) [6.75/(1.34) = 10.2] c. (i) Writing a call entails unlimited potential losses as the stock price rises.](/thumbs/39/20115486.jpg "1. a. (iv) b. (ii) [6.75/(1.34) = 10.2] c. (i) Writing a call entails unlimited potential losses as the stock price rises.") 1. Solutions to PS 1: 1. a. (iv) b. (ii) [6.75/(1.34) = 10.2] c. (i) Writing a call entails unlimited potential losses as the stock price rises. 7. The bill has a maturity of one-half year, and an annualized

1. Solutions to PS 1: 1. a. (iv) b. (ii) [6.75/(1.34) = 10.2] c. (i) Writing a call entails unlimited potential losses as the stock price rises. 7. The bill has a maturity of one-half year, and an annualized

Corporate Finance Sample Exam 2A Dr. A. Frank Thompson

Corporate Finance Sample Exam 2A Dr. A. Frank Thompson True/False Indicate whether the statement is true or false. 1. The market value of any real or financial asset, including stocks, bonds, CDs, coins,

Corporate Finance Sample Exam 2A Dr. A. Frank Thompson True/False Indicate whether the statement is true or false. 1. The market value of any real or financial asset, including stocks, bonds, CDs, coins,

Risk and Return Models: Equity and Debt. Aswath Damodaran 1

Risk and Return Models: Equity and Debt Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Risk and Return Models: Equity and Debt Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Chapter 7 Risk, Return, and the Capital Asset Pricing Model

Chapter 7 Risk, Return, and the Capital Asset Pricing Model MULTIPLE CHOICE 1. Suppose Sarah can borrow and lend at the risk free-rate of 3%. Which of the following four risky portfolios should she hold

Chapter 7 Risk, Return, and the Capital Asset Pricing Model MULTIPLE CHOICE 1. Suppose Sarah can borrow and lend at the risk free-rate of 3%. Which of the following four risky portfolios should she hold

CIS September 2012 Exam Diet. Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis

CIS September 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Corporate Finance (1 13) 1. Assume a firm issues N1 billion in debt

CIS September 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Corporate Finance (1 13) 1. Assume a firm issues N1 billion in debt

RISK AND RETURN WHY STUDY RISK AND RETURN?

66798_c08_306-354.qxd 10/31/03 5:28 PM Page 306 Why Study Risk and Return? The General Relationship between Risk and Return The Return on an Investment Risk A Preliminary Definition Portfolio Theory Review

66798_c08_306-354.qxd 10/31/03 5:28 PM Page 306 Why Study Risk and Return? The General Relationship between Risk and Return The Return on an Investment Risk A Preliminary Definition Portfolio Theory Review

Finance 3130 Corporate Finiance Sample Final Exam Spring 2012

Finance 3130 Corporate Finiance Sample Final Exam Spring 2012 True/False Indicate whether the statement is true or falsewith A for true and B for false. 1. Interest paid by a corporation is a tax deduction

Finance 3130 Corporate Finiance Sample Final Exam Spring 2012 True/False Indicate whether the statement is true or falsewith A for true and B for false. 1. Interest paid by a corporation is a tax deduction

INVESTMENTS IN OFFSHORE OIL AND NATURAL GAS DEPOSITS IN ISRAEL: BASIC PRINCIPLES ROBERT S. PINDYCK

INVESTMENTS IN OFFSHORE OIL AND NATURAL GAS DEPOSITS IN ISRAEL: BASIC PRINCIPLES ROBERT S. PINDYCK Bank of Tokyo-Mitsubishi Professor of Economics and Finance Sloan School of Management Massachusetts Institute

INVESTMENTS IN OFFSHORE OIL AND NATURAL GAS DEPOSITS IN ISRAEL: BASIC PRINCIPLES ROBERT S. PINDYCK Bank of Tokyo-Mitsubishi Professor of Economics and Finance Sloan School of Management Massachusetts Institute

Chapter 10 Capital Markets and the Pricing of Risk

Chapter 10 Capital Markets and the Pricing of Risk 10-1. The figure below shows the one-year return distribution for RCS stock. Calculate a. The expected return. b. The standard deviation of the return.

Chapter 10 Capital Markets and the Pricing of Risk 10-1. The figure below shows the one-year return distribution for RCS stock. Calculate a. The expected return. b. The standard deviation of the return.

Guide to Getting Loans on Investment Properties. Mark Ferguson. Copyright 2013 All rights reserved Invest Four More Proprietary

Guide to Getting Loans on Investment Properties Mark Ferguson Table of Contents Guide to Getting Loans on Investment Properties... 1 Should you get a loan for investment properties?... 3 Why are the returns

Guide to Getting Loans on Investment Properties Mark Ferguson Table of Contents Guide to Getting Loans on Investment Properties... 1 Should you get a loan for investment properties?... 3 Why are the returns

Chapter 5 Uncertainty and Consumer Behavior

Chapter 5 Uncertainty and Consumer Behavior Questions for Review 1. What does it mean to say that a person is risk averse? Why are some people likely to be risk averse while others are risk lovers? A risk-averse

Chapter 5 Uncertainty and Consumer Behavior Questions for Review 1. What does it mean to say that a person is risk averse? Why are some people likely to be risk averse while others are risk lovers? A risk-averse

Cost of Capital Basics

Cost of Capital Basics The corporate cost of capital is a blend (weighted average) of the costs of the financing components. It is used as a benchmark rate of return in new new project evaluations. Key

Cost of Capital Basics The corporate cost of capital is a blend (weighted average) of the costs of the financing components. It is used as a benchmark rate of return in new new project evaluations. Key

The Marginal Cost of Capital and the Optimal Capital Budget

WEB EXTENSION12B The Marginal Cost of Capital and the Optimal Capital Budget If the capital budget is so large that a company must issue new equity, then the cost of capital for the company increases.

WEB EXTENSION12B The Marginal Cost of Capital and the Optimal Capital Budget If the capital budget is so large that a company must issue new equity, then the cost of capital for the company increases.

Chapter 11. Topics Covered. Chapter 11 Objectives. Risk, Return, and Capital Budgeting

Chapter 11 Risk, Return, and Capital Budgeting Topics Covered Measuring Market Risk Portfolio Betas Risk and Return CAPM and Expected Return Security Market Line CAPM and Stock Valuation Chapter 11 Objectives

Chapter 11 Risk, Return, and Capital Budgeting Topics Covered Measuring Market Risk Portfolio Betas Risk and Return CAPM and Expected Return Security Market Line CAPM and Stock Valuation Chapter 11 Objectives

MCDONALD S CORPORATION. Harmony Lynn Lazore ACG 2021-001

MCDONALD S CORPORATION Harmony Lynn Lazore ACG 2021-001 Executive Summary McDonald s Corporation spent 2006 expanding their number of restaurants world wide, disposing of Chipotle Mexican Grill, and converting

MCDONALD S CORPORATION Harmony Lynn Lazore ACG 2021-001 Executive Summary McDonald s Corporation spent 2006 expanding their number of restaurants world wide, disposing of Chipotle Mexican Grill, and converting

RISKS IN MUTUAL FUND INVESTMENTS

RISKS IN MUTUAL FUND INVESTMENTS Classification of Investors Investors can be classified based on their Risk Tolerance Levels : Low Risk Tolerance Moderate Risk Tolerance High Risk Tolerance Fund Classification

RISKS IN MUTUAL FUND INVESTMENTS Classification of Investors Investors can be classified based on their Risk Tolerance Levels : Low Risk Tolerance Moderate Risk Tolerance High Risk Tolerance Fund Classification

Mutual Fund Investing Exam Study Guide

Mutual Fund Investing Exam Study Guide This document contains the questions that will be included in the final exam, in the order that they will be asked. When you have studied the course materials, reviewed

Mutual Fund Investing Exam Study Guide This document contains the questions that will be included in the final exam, in the order that they will be asked. When you have studied the course materials, reviewed

COST OF CAPITAL Compute the cost of debt. Compute the cost of preferred stock.

OBJECTIVE 1 Compute the cost of debt. The method of computing the yield to maturity for bonds will be used how to compute the cost of debt. Because interest payments are tax deductible, only after-tax

OBJECTIVE 1 Compute the cost of debt. The method of computing the yield to maturity for bonds will be used how to compute the cost of debt. Because interest payments are tax deductible, only after-tax

Basic Financial Tools: A Review. 3 n 1 n. PV FV 1 FV 2 FV 3 FV n 1 FV n 1 (1 i)

") Chapter 28 Basic Financial Tools: A Review The building blocks of finance include the time value of money, risk and its relationship with rates of return, and stock and bond valuation models. These topics

Chapter 28 Basic Financial Tools: A Review The building blocks of finance include the time value of money, risk and its relationship with rates of return, and stock and bond valuation models. These topics

Chapter 7 Stocks, Stock Valuation, and Stock Market Equilibrium ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 7 Stocks, Stock Valuation, and Stock Market Equilibrium ANSWERS TO END-OF-CHAPTER QUESTIONS 7-1 a. A proxy is a document giving one person the authority to act for another, typically the power

Chapter 7 Stocks, Stock Valuation, and Stock Market Equilibrium ANSWERS TO END-OF-CHAPTER QUESTIONS 7-1 a. A proxy is a document giving one person the authority to act for another, typically the power

Common Sense Economics Part 4: Twelve Key Elements of Practical Personal Finance Practice Test

Common Sense Economics Part 4: Twelve Key Elements of Practical Personal Finance Practice Test 1. Your comparative advantage in a specific area is determined by a. the market value of the skill relative

Common Sense Economics Part 4: Twelve Key Elements of Practical Personal Finance Practice Test 1. Your comparative advantage in a specific area is determined by a. the market value of the skill relative

FIN 432 Investment Analysis and Management Review Notes for Midterm Exam

FIN 432 Investment Analysis and Management Review Notes for Midterm Exam Chapter 1 1. Investment vs. investments 2. Real assets vs. financial assets 3. Investment process Investment policy, asset allocation,

FIN 432 Investment Analysis and Management Review Notes for Midterm Exam Chapter 1 1. Investment vs. investments 2. Real assets vs. financial assets 3. Investment process Investment policy, asset allocation,

Obligation-based Asset Allocation for Public Pension Plans

Obligation-based Asset Allocation for Public Pension Plans Market Commentary July 2015 PUBLIC PENSION PLANS HAVE a single objective to provide income for a secure retirement for their members. Once the

Obligation-based Asset Allocation for Public Pension Plans Market Commentary July 2015 PUBLIC PENSION PLANS HAVE a single objective to provide income for a secure retirement for their members. Once the

Mutual Fund Expense Information on Quarterly Shareholder Statements

June 2005 Mutual Fund Expense Information on Quarterly Shareholder Statements You may have noticed that beginning with your March 31 quarterly statement from AllianceBernstein, two new sections have been

June 2005 Mutual Fund Expense Information on Quarterly Shareholder Statements You may have noticed that beginning with your March 31 quarterly statement from AllianceBernstein, two new sections have been

COST THEORY. I What costs matter? A Opportunity Costs

COST THEORY Cost theory is related to production theory, they are often used together. However, the question is how much to produce, as opposed to which inputs to use. That is, assume that we use production

COST THEORY Cost theory is related to production theory, they are often used together. However, the question is how much to produce, as opposed to which inputs to use. That is, assume that we use production

International Business 7e

International Business 7e by Charles W.L. Hill McGraw-Hill/Irwin Copyright 2009 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 11 The Global Capital Market Introduction The rapid globalization

International Business 7e by Charles W.L. Hill McGraw-Hill/Irwin Copyright 2009 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 11 The Global Capital Market Introduction The rapid globalization

The CAPM (Capital Asset Pricing Model) NPV Dependent on Discount Rate Schedule

NPV Dependent on Discount Rate Schedule") The CAPM (Capital Asset Pricing Model) Massachusetts Institute of Technology CAPM Slide 1 of NPV Dependent on Discount Rate Schedule Discussed NPV and time value of money Choice of discount rate influences

The CAPM (Capital Asset Pricing Model) Massachusetts Institute of Technology CAPM Slide 1 of NPV Dependent on Discount Rate Schedule Discussed NPV and time value of money Choice of discount rate influences

Financial Planning Newsletter

Financial Planning Newsletter Structuring Your Portfolio for Future Success? Beware of Misleading, Misinterpreted & Out Dated Information Wealth Management Steinberg High Yield Fund Steinberg Equity Fund

Financial Planning Newsletter Structuring Your Portfolio for Future Success? Beware of Misleading, Misinterpreted & Out Dated Information Wealth Management Steinberg High Yield Fund Steinberg Equity Fund

A Basic Introduction to the Methodology Used to Determine a Discount Rate

A Basic Introduction to the Methodology Used to Determine a Discount Rate By Dubravka Tosic, Ph.D. The term discount rate is one of the most fundamental, widely used terms in finance and economics. Whether

A Basic Introduction to the Methodology Used to Determine a Discount Rate By Dubravka Tosic, Ph.D. The term discount rate is one of the most fundamental, widely used terms in finance and economics. Whether

LECTURES ON REAL OPTIONS: PART I BASIC CONCEPTS

LECTURES ON REAL OPTIONS: PART I BASIC CONCEPTS Robert S. Pindyck Massachusetts Institute of Technology Cambridge, MA 02142 Robert Pindyck (MIT) LECTURES ON REAL OPTIONS PART I August, 2008 1 / 44 Introduction

LECTURES ON REAL OPTIONS: PART I BASIC CONCEPTS Robert S. Pindyck Massachusetts Institute of Technology Cambridge, MA 02142 Robert Pindyck (MIT) LECTURES ON REAL OPTIONS PART I August, 2008 1 / 44 Introduction

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

Chapter 11. Topics Covered. Chapter 11 Objectives. Risk, Return, and Capital Budgeting

Chapter 11 Risk, Return, and Capital Budgeting Topics Covered Measuring Market Risk Portfolio Betas Risk and Return CAPM and Expected Return Security Market Line CAPM and Stock Valuation Chapter 11 Objectives

Chapter 11 Risk, Return, and Capital Budgeting Topics Covered Measuring Market Risk Portfolio Betas Risk and Return CAPM and Expected Return Security Market Line CAPM and Stock Valuation Chapter 11 Objectives

CHAPTER 7: OPTIMAL RISKY PORTFOLIOS

CHAPTER 7: OPTIMAL RIKY PORTFOLIO PROLEM ET 1. (a) and (e).. (a) and (c). After real estate is added to the portfolio, there are four asset classes in the portfolio: stocks, bonds, cash and real estate.

CHAPTER 7: OPTIMAL RIKY PORTFOLIO PROLEM ET 1. (a) and (e).. (a) and (c). After real estate is added to the portfolio, there are four asset classes in the portfolio: stocks, bonds, cash and real estate.

Chapter 9. The Valuation of Common Stock. 1.The Expected Return (Copied from Unit02, slide 39)

") Readings Chapters 9 and 10 Chapter 9. The Valuation of Common Stock 1. The investor s expected return 2. Valuation as the Present Value (PV) of dividends and the growth of dividends 3. The investor s required

Readings Chapters 9 and 10 Chapter 9. The Valuation of Common Stock 1. The investor s expected return 2. Valuation as the Present Value (PV) of dividends and the growth of dividends 3. The investor s required

AN OVERVIEW OF FINANCIAL MANAGEMENT

CHAPTER 1 Review Questions AN OVERVIEW OF FINANCIAL MANAGEMENT 1. Management s basic, overriding goal is to create for 2. The same actions that maximize also benefits society 3. If businesses are successful

CHAPTER 1 Review Questions AN OVERVIEW OF FINANCIAL MANAGEMENT 1. Management s basic, overriding goal is to create for 2. The same actions that maximize also benefits society 3. If businesses are successful

Portfolio Performance Measures

Portfolio Performance Measures Objective: Evaluation of active portfolio management. A performance measure is useful, for example, in ranking the performance of mutual funds. Active portfolio managers

Portfolio Performance Measures Objective: Evaluation of active portfolio management. A performance measure is useful, for example, in ranking the performance of mutual funds. Active portfolio managers

Pros and Cons of Different Investment Options

Pros and Cons of Different Investment Options In 2016, new legislation called CRM2 will come to Canada. Once enacted, all financial institutions in Canada will be required to disclose all investment management

Pros and Cons of Different Investment Options In 2016, new legislation called CRM2 will come to Canada. Once enacted, all financial institutions in Canada will be required to disclose all investment management

ST. JAMES S PLACE INTERNATIONAL INTERNATIONAL INVESTMENT BOND

INTRODUCING THE ST. JAMES S PLACE INTERNATIONAL INTERNATIONAL INVESTMENT BOND THE ST. JAMES S PLACE PARTNERSHIP The St. James s Place Partnership is an elite group, made up of many of the most experienced,

INTRODUCING THE ST. JAMES S PLACE INTERNATIONAL INTERNATIONAL INVESTMENT BOND THE ST. JAMES S PLACE PARTNERSHIP The St. James s Place Partnership is an elite group, made up of many of the most experienced,

The cost of capital. A reading prepared by Pamela Peterson Drake. 1. Introduction

The cost of capital A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction... 1 2. Determining the proportions of each source of capital that will be raised... 3 3. Estimating the marginal

The cost of capital A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction... 1 2. Determining the proportions of each source of capital that will be raised... 3 3. Estimating the marginal

Stock Valuation: Gordon Growth Model. Week 2

Stock Valuation: Gordon Growth Model Week 2 Approaches to Valuation 1. Discounted Cash Flow Valuation The value of an asset is the sum of the discounted cash flows. 2. Contingent Claim Valuation A contingent

Stock Valuation: Gordon Growth Model Week 2 Approaches to Valuation 1. Discounted Cash Flow Valuation The value of an asset is the sum of the discounted cash flows. 2. Contingent Claim Valuation A contingent

Pricing Forwards and Futures

Pricing Forwards and Futures Peter Ritchken Peter Ritchken Forwards and Futures Prices 1 You will learn Objectives how to price a forward contract how to price a futures contract the relationship between

Pricing Forwards and Futures Peter Ritchken Peter Ritchken Forwards and Futures Prices 1 You will learn Objectives how to price a forward contract how to price a futures contract the relationship between

Practice Exam (Solutions)

") Practice Exam (Solutions) June 6, 2008 Course: Finance for AEO Length: 2 hours Lecturer: Paul Sengmüller Students are expected to conduct themselves properly during examinations and to obey any instructions

Practice Exam (Solutions) June 6, 2008 Course: Finance for AEO Length: 2 hours Lecturer: Paul Sengmüller Students are expected to conduct themselves properly during examinations and to obey any instructions

John Chaimanis, Co-Founder and Managing Director, Kendall Sustainable Infrastructure (KSI)

") John Chaimanis, Co-Founder and Managing Director, Kendall Sustainable Infrastructure (KSI) United States Where do you see opportunities for powerful, effective investing today? Mr. Chaimanis: Energy. Clean,

John Chaimanis, Co-Founder and Managing Director, Kendall Sustainable Infrastructure (KSI) United States Where do you see opportunities for powerful, effective investing today? Mr. Chaimanis: Energy. Clean,

NPH Fixed Income Research Update. Bob Downing, CFA. NPH Senior Investment & Due Diligence Analyst

White Paper: NPH Fixed Income Research Update Authored By: Bob Downing, CFA NPH Senior Investment & Due Diligence Analyst National Planning Holdings, Inc. Due Diligence Department National Planning Holdings,

White Paper: NPH Fixed Income Research Update Authored By: Bob Downing, CFA NPH Senior Investment & Due Diligence Analyst National Planning Holdings, Inc. Due Diligence Department National Planning Holdings,

Discounted Cash Flow. Alessandro Macrì. Legal Counsel, GMAC Financial Services

Discounted Cash Flow Alessandro Macrì Legal Counsel, GMAC Financial Services History The idea that the value of an asset is the present value of the cash flows that you expect to generate by holding it

Discounted Cash Flow Alessandro Macrì Legal Counsel, GMAC Financial Services History The idea that the value of an asset is the present value of the cash flows that you expect to generate by holding it

CHAPTER 17. Payout Policy. Chapter Synopsis

CHAPTER 17 Payout Policy Chapter Synopsis 17.1 Distributions to Shareholders A corporation s payout policy determines if and when it will distribute cash to its shareholders by issuing a dividend or undertaking

CHAPTER 17 Payout Policy Chapter Synopsis 17.1 Distributions to Shareholders A corporation s payout policy determines if and when it will distribute cash to its shareholders by issuing a dividend or undertaking

A Review of Cross Sectional Regression for Financial Data You should already know this material from previous study

A Review of Cross Sectional Regression for Financial Data You should already know this material from previous study But I will offer a review, with a focus on issues which arise in finance 1 TYPES OF FINANCIAL

A Review of Cross Sectional Regression for Financial Data You should already know this material from previous study But I will offer a review, with a focus on issues which arise in finance 1 TYPES OF FINANCIAL

Risk, Return and Market Efficiency

Risk, Return and Market Efficiency For 9.220, Term 1, 2002/03 02_Lecture16.ppt Student Version Outline 1. Introduction 2. Types of Efficiency 3. Informational Efficiency 4. Forms of Informational Efficiency

Risk, Return and Market Efficiency For 9.220, Term 1, 2002/03 02_Lecture16.ppt Student Version Outline 1. Introduction 2. Types of Efficiency 3. Informational Efficiency 4. Forms of Informational Efficiency

Investment Companies

Mutual Funds Mutual Funds Investment companies Financial intermediaries that collect funds form individual investors and invest those funds in a potentially wide rande of securities or other asstes Polling

Mutual Funds Mutual Funds Investment companies Financial intermediaries that collect funds form individual investors and invest those funds in a potentially wide rande of securities or other asstes Polling

The essentials of investing for retirement.

The essentials of investing for retirement. Fidelity has been helping people invest for retirement for more than 65 years. Some investors use our actively managed and index mutual funds. Some use our powerful

The essentials of investing for retirement. Fidelity has been helping people invest for retirement for more than 65 years. Some investors use our actively managed and index mutual funds. Some use our powerful

any any assistance on on this this examination.

I I ledge on on my honor that I have not given or received any any assistance on on this this examination. Signed: Name: Perm #: TA: This quiz consists of 11 questions and has a total of 6 ages, including

I I ledge on on my honor that I have not given or received any any assistance on on this this examination. Signed: Name: Perm #: TA: This quiz consists of 11 questions and has a total of 6 ages, including

ANSWERS TO END-OF-CHAPTER PROBLEMS WITHOUT ASTERISKS

Part III Answers to End-of-Chapter Problems 97 CHAPTER 1 ANSWERS TO END-OF-CHAPTER PROBLEMS WITHOUT ASTERISKS Why Study Money, Banking, and Financial Markets? 7. The basic activity of banks is to accept

Part III Answers to End-of-Chapter Problems 97 CHAPTER 1 ANSWERS TO END-OF-CHAPTER PROBLEMS WITHOUT ASTERISKS Why Study Money, Banking, and Financial Markets? 7. The basic activity of banks is to accept

Value-Based Management

Value-Based Management Lecture 5: Calculating the Cost of Capital Prof. Dr. Gunther Friedl Lehrstuhl für Controlling Technische Universität München Email: [email protected] Overview 1. Value Maximization

Value-Based Management Lecture 5: Calculating the Cost of Capital Prof. Dr. Gunther Friedl Lehrstuhl für Controlling Technische Universität München Email: [email protected] Overview 1. Value Maximization

Chapter 12: Gross Domestic Product and Growth Section 1

Chapter 12: Gross Domestic Product and Growth Section 1 Key Terms national income accounting: a system economists use to collect and organize macroeconomic statistics on production, income, investment,

Chapter 12: Gross Domestic Product and Growth Section 1 Key Terms national income accounting: a system economists use to collect and organize macroeconomic statistics on production, income, investment,

Econ 422 Summer 2006 Final Exam Solutions

Econ 422 Summer 2006 Final Exam Solutions This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make a computational

Econ 422 Summer 2006 Final Exam Solutions This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make a computational

VOCABULARY INVESTING Student Worksheet

Vocabulary Worksheet Page 1 Name Period VOCABULARY INVESTING Student Worksheet PRIMARY VOCABULARY 1. Savings: 2. Investments: 3. Investing: 4. Risk: 5. Return: 6. Liquidity: 7. Stocks: 8. Bonds: 9. Mutual

Vocabulary Worksheet Page 1 Name Period VOCABULARY INVESTING Student Worksheet PRIMARY VOCABULARY 1. Savings: 2. Investments: 3. Investing: 4. Risk: 5. Return: 6. Liquidity: 7. Stocks: 8. Bonds: 9. Mutual

Modified dividend payout ratio =

15 Modifying the model to include stock buybacks In recent years, firms in the United States have increasingly turned to stock buybacks as a way of returning cash to stockholders. Figure 13.3 presents

15 Modifying the model to include stock buybacks In recent years, firms in the United States have increasingly turned to stock buybacks as a way of returning cash to stockholders. Figure 13.3 presents

CHAPTER 20: OPTIONS MARKETS: INTRODUCTION

CHAPTER 20: OPTIONS MARKETS: INTRODUCTION 1. Cost Profit Call option, X = 95 12.20 10 2.20 Put option, X = 95 1.65 0 1.65 Call option, X = 105 4.70 0 4.70 Put option, X = 105 4.40 0 4.40 Call option, X

CHAPTER 20: OPTIONS MARKETS: INTRODUCTION 1. Cost Profit Call option, X = 95 12.20 10 2.20 Put option, X = 95 1.65 0 1.65 Call option, X = 105 4.70 0 4.70 Put option, X = 105 4.40 0 4.40 Call option, X

Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments.

![Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments.](/thumbs/40/20590846.jpg "Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments.") Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments. Historic economist Benjamin Graham famously said, The essence of investment management is

Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments. Historic economist Benjamin Graham famously said, The essence of investment management is

Fundamentals Level Skills Module, Paper F9. Section B

Answers Fundamentals Level Skills Module, Paper F9 Financial Management September/December 2015 Answers Section B 1 (a) Market value of equity = 15,000,000 x 3 75 = $56,250,000 Market value of each irredeemable

Answers Fundamentals Level Skills Module, Paper F9 Financial Management September/December 2015 Answers Section B 1 (a) Market value of equity = 15,000,000 x 3 75 = $56,250,000 Market value of each irredeemable

Referred to as the statement of financial position provides a snap shot of a company s assets, liabilities and equity at a particular point in time.

Glossary Aggressive investor Balance sheet Bear market Typically has a higher risk appetite. They are prepared or can afford to risk much more and for this they stand to reap the big rewards. Referred

Glossary Aggressive investor Balance sheet Bear market Typically has a higher risk appetite. They are prepared or can afford to risk much more and for this they stand to reap the big rewards. Referred

How to make changes to your annuity income

How to make changes to your annuity income What s inside 2 Is it time to make a change? 3 Your annuity income 5 TIAA Traditional income 7 TIAA and CREF variable income 10 Ways to adjust your annuity income

How to make changes to your annuity income What s inside 2 Is it time to make a change? 3 Your annuity income 5 TIAA Traditional income 7 TIAA and CREF variable income 10 Ways to adjust your annuity income

CFA Examination PORTFOLIO MANAGEMENT Page 1 of 6

PORTFOLIO MANAGEMENT A. INTRODUCTION RETURN AS A RANDOM VARIABLE E(R) = the return around which the probability distribution is centered: the expected value or mean of the probability distribution of possible

PORTFOLIO MANAGEMENT A. INTRODUCTION RETURN AS A RANDOM VARIABLE E(R) = the return around which the probability distribution is centered: the expected value or mean of the probability distribution of possible

Cash flow before tax 1,587 1,915 1,442 2,027 Tax at 28% (444) (536) (404) (568)

(536) (404) (568)") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2014 Answers 1 (a) Calculation of NPV Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 5,670 6,808 5,788 6,928 Variable

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2014 Answers 1 (a) Calculation of NPV Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 5,670 6,808 5,788 6,928 Variable

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided