Calculation Guide Estate Master DF Summary Report Performance Indicators. August 2012

|

|

|

- Jemimah Blankenship

- 9 years ago

- Views:

Transcription

1 Calculation Guide Estate Master DF Summary Report Performance Indicators August 2012

2 Table of Contents Introduction... 3 Summary Report - Performance Indicators Gross Development Profit Net Development Profit Development Margin Residual Land Value (Based on % Development Margin) Net Present Value Benefit Cost Ratio Project Internal Rate of Return Residual Land Value (Based on % NPV) Equity IRR Equity Contribution Peak Debt Exposure Equity to Debt Ratio Weighted Average Cost of Capital (WACC) Breakeven Date for Cumulative Cash Flow Yield on Costs Rent Cover Profit Erosion

3 Introduction Estate Master has put together this document to assist you with working through the different calculations that appear on the developer s Summary report within the Estate Master DF (Development Feasibility) software The objective for this document is to break down any questions you may have regarding how Estate Master calculates each of the different sections within the Summary report itself. The Developers Summary report is broken up into three broad sections which we will investigate further. These are: 1. Total revenue (Including sales and revenue) 2. Total Project costs 3. Performance Indicators: The performance indicators are commonly used to look at how the project is performing with critical business decisions often being made from the information provided by these different indicators. We have provided a summary of the different calculations below. 3

in a given period of time.")

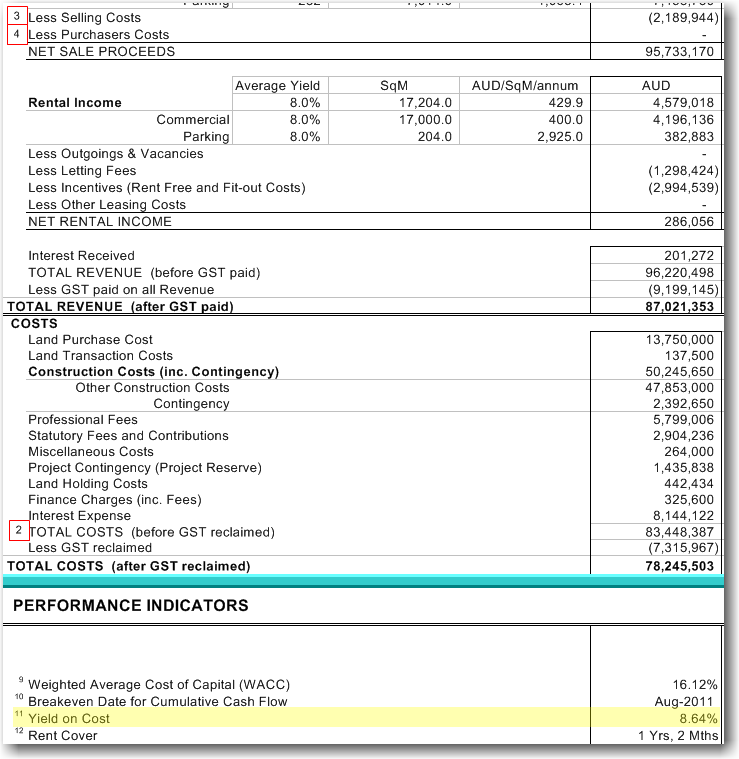

4 Summary Report - Performance Indicators 1. Gross Development Profit This is calculated by subtracting a company's total expenses from total revenue, thus showing what the company has earned (or lost) in a given period of time. This output is only displayed on the Summary report if there are profit distributions payable to the land owner or lenders, otherwise on the Net Development Profit is displayed. Calculation Example Gross Development Profit = 1 Total Revenue 87,021,353 minus - 2 Total Costs 78,245,503 8,775,850 4

5 2. Net Development Profit Often referred to as also net profit, it is similar to Gross Development Profit but also includes any profit share distributions. Calculation Example Net Development Profit = 1 Total Revenue 3,295,475,883 minus - 2 Total Costs 2,698,797,522 minus - 3 Profit Share 59,667, ,010,525 5

6 3. Development Margin Also known as the Profit/Risk Factor, it is commonly used by developers as a reflection of profitability and is the percentage return of net profit over development costs as a standard and common calculation. Estate Master however takes the developers margin one more step and provides five different methods for the margin calculation as shown below. Calculation There are 5 different methods for calculating the Development Margin on the Summary Report, set via the Preferences. In addition to these Preferences, the Development Margin is also impacted by the Preference to display Performance Indicators Before or After Profit Share is paid out (i.e. on Gross or Net Development Profit) If Based on Gross Development Profit is selected, then the numerator in the equation is the Gross Development Profit output on the Summary sheet (only outputted if there are profit share distributions being paid) (item 1 below) If Based on Net Development Profit is selected, then the numerator in the equation is the Net Development Profit output on the Summary sheet (item 2 below) 6

minus - 4 Purchaser s Costs 0 minus - 5 Outgoings & Vacancies 0 minus - 6 Letting Fees (1,298,424) minus - 7 Incentives (2,994,539) minus - 8 Other Leasing Costs ) 0 ) 14.")

7 Preference 1 - On Total Development Costs (inc Selling and Leasing Costs) Example Development Margin = 1 Development Profit (Net or Gross) 11,647,832 Divided by / 2 ( Total Costs ( 76,116,245 minus - 3 Selling Costs (2,205,897) minus - 4 Purchaser s Costs 0 minus - 5 Outgoings & Vacancies 0 minus - 6 Letting Fees (1,298,424) minus - 7 Incentives (2,994,539) minus - 8 Other Leasing Costs ) 0 ) 14.10% 7

minus - 4 Purchaser s Costs 0 plus + GST/VAT on Leasing Costs ) 271,039 ) 14.")

8 Preference 2 - On Total Development Costs (inc Selling Costs) Example Development Margin = 1 Development Profit (Net or Gross) 11,647,832 Divided by / 2 ( Total Costs ( 76,116,245 minus - 3 Selling Costs (2,205,897) minus - 4 Purchaser s Costs 0 plus + GST/VAT on Leasing Costs ) 271,039 ) 14.82% Note: Since we are not factoring Leasing Costs as part of Development Costs in this option, we need to exclude any GST/VAT Reclaim on Leasing Costs from the calculation of 'Total Costs'. This figure is not explicitly displayed on the Summary report. It can be calculated manually by determining the GST/VAT that is reclaimable for items 5, 6,7 and 8 that make up Leasing Costs. 8

271,039 ) 15.")

9 Preference 3 - On Total Development Costs (net of Selling and Leasing Costs) Example Development Margin = 1 Development Profit (Net or Gross) 11,647,832 Divided by / 2 ( Total Costs ( 76,116,245 plus + GST/VAT on Selling Costs 200,536 plus + GST/VAT on Leasing Costs ) 271,039 ) 15.21% Note: Since we are not factoring Selling Costs or Leasing Costs as part of Development Costs in this option, we need to exclude any GST/VAT Reclaim on these from the calculation of 'Total Costs'. This figure is not explicitly displayed on the Summary report. It can be calculated manually by determining the GST/VAT that is reclaimable for items 3,4, 5, 6,7 and 8 that make up Selling and Leasing Costs. 9

(9,274,486) ) 12.")

10 Preference 4 - On Total Revenue (net of Tax) Example Development Margin = 1 Development Profit (Net or Gross) 11,647,832 Divided by / 2 ( Total Sales Revenue ( 98,751,864 plus + 3 Rental Income 4,579,018 plus + 4 Interest Received 206,540 plus + 5 Other Income 0 plus + 6 Tax Paid on all Revenue ) (9,274,486) ) 12.36% 10

8,977,442 ) 13.30% Tax on Sales is not explicitly displayed on the Summary report.")

11 Preference 5 - On Total Sale Proceeds (net of Selling Costs) Example Development Margin = 1 Development Profit (Net or Gross) 11,647,832 Divided by / 2 ( Net Sales Proceeds ( 96,545,966 minus - Tax Paid on Sales ) 8,977,442 ) 13.30% Tax on Sales is not explicitly displayed on the Summary report. It can be calculated manually by determining the GST/VAT/Sales Tax that is reclaimable for all individual Sales Revenue items. 11

12 4. Residual Land Value (Based on % Development Margin) The Residual Land Value based on the Target Development Margin is the maximum price for the land that the developer would pay to make the calculated development margin equal the target hurdle rate. The target hurdle rate is essentially the developer s required profit margin return for the project, also referred to as a Profit and Risk Factor. The Development Margin has been the traditional method of development feasibility analysis in the past and is beneficial for short term projects. However it does have its shortcomings it does not account for the time value of money and its results can be misleading for projects that extended beyond two or more years. Two projects may have the same net profit, but due to differences in the timing of cash inflows and outflows, one project may be realising its profit earlier than the other. Therefore, it you take into account the old adage a bird in the hand is worth two in the bush, then even though the projects have the same profit, a prudent developer/investor would chose the project that achieves its profit earlier. From the example below you can see that the Development Margin for the proposed development project is only achieving 14.10% based on an assumed Land Purchase Price of 13,750,000. In order to achieve the Target Development Margin of 25% the developer would need to purchase the land for a maximum residual land value of 8,921,

13 Calculation There is no specific formula that calculates the Residual Land Value. It is a result that is calculated through undertaking a goal seek - the land price is manipulated up and down until the Development Margin matches the developer s desired Target Development Margin. The Target Development Margin is set on the Input sheet under Hurdle Rates Even though the Residual Land Value calculation is not a formula, it can still be easily recreated and demonstrated using Estate Masters Goal Seek function. Once you have opened the Goal Seek function, set the following parameters: Set Cell: The Development Margin output on the Summary report To Value: The Target Development Margin By Changing Cell: The Land Purchase Price input on the Input sheet Once you press OK on the Goal Seek, it will then calculate an answer in the Land Purchase Price input on the Input sheet. 13

14 5. Net Present Value The Net Present Value (NPV) is the difference between the present value of cash inflows (revenue) and the present value of cash outflows (costs), discounted by a user-defined Discount Rate. NPV compares the value of a dollar today to the value of that same dollar in the future, taking inflation and returns into account. If the NPV of a prospective project is positive, it should be accepted. However, if NPV is negative, the project should probably be rejected because cash flows will also be negative. Calculation The standard Excel function for NPV is used in Estate Master: NPV ( rate, value1, value2,...) + value0 Where: rate = is the rate of discount over the length of one period. Value0 = the first time period (period zero). The first time period in the cash flow is not discounted, and therefore is not added within the NPV function. It is simply added outside of the function. Value1, value2,...= are the arguments representing the payments and income. The cash flow data that is used to calculate the NPV is also summarised in the Project IRR & NPV section of the Cash Flow worksheet. There are 4 different methods for calculating the Net Present Value on the Summary Report, set via the Preferences. They relate to the specific cash flow that is used to calculate the NPV, most notably if it includes financing costs, interest and corporate tax. 14

15 In addition to these Preferences, the Net Present Value is also impacted by the Preference to convert the Discount Rate on either an Effective or Nominal Basis. This is required as the Discount Rate that is entered by the user is an annual rate, however the cash flow that the NPV is calculated on can have monthly, quarterly or half-yearly rests, depending on how the user has decided to set the model up. Example per annum Nominal D/T 18.00% / 12 = 1.5% per month per annum Effective [(D + 1) 1/T ]-1 [(18.00% + 1) 1/12 ]- 1= 1.39% per month Where: D = is the annual discount rate. T = The number of rest periods per annum (i.e Monthly = 12, Quarterly = 4, etc) 15

plus 4 Time period 0 for Net Cash Flow (before Interest & Corporate Tax) plus 5 Time")

16 Preference 1 - On Cash Flow Excluding all Financing Costs, Interest and Corporate Tax NPV = 1 NPV ( Discount Rate entered in Input sheet converted from annual to rest period rate, 2 Time period 1 onwards for Net Cash Flow before Interest & Corporate Tax plus 3 Time period 1 onwards for Financing Costs ) plus 4 Time period 0 for Net Cash Flow (before Interest & Corporate Tax) plus 5 Time period 0 for Financing Costs Note: The above Discount Rate needs to be converted from an annual rate, to a rate equivalent to the rest periods being used in the model, before it is used in the NPV function. 16

plus 4 Time period 0 for Net Cash Flow (before")

17 Preference 2 - On Cash Flow Including Financing Costs but Excluding Interest and Corporate Tax NPV = 1 NPV ( Discount Rate entered in Input sheet converted from annual to rest period rate, 2 Time period 1 onwards for Net Cash Flow before Interest & Corporate Tax plus 3 Time period 1 onwards for Application and Line Fees for Loans 1, 2, 3 and 4 ) plus 4 Time period 0 for Net Cash Flow (before Interest & Corporate Tax) plus 5 Time period 0 for Application and Line Fees for Loans 1, 2, 3 and 4 Note: The above Discount Rate needs to be converted from an annual rate, to a rate equivalent to the rest periods being used in the model, before it is used in the NPV function. 17

plus 3 Time period 1 onwards for Corporate Tax ) plus 4 Time period 0 for Net Cash Flow (after Interest & Corporate Tax) plus 5")

18 Preference 3 - On Cash Flow Including Financing Costs and Interest but Excluding Corporate Tax NPV = 1 NPV ( Discount Rate entered in Input sheet converted from annual to rest period rate, 2 Time period 1 onwards for Net Cash Flow (after Interest & Corporate Tax) plus 3 Time period 1 onwards for Corporate Tax ) plus 4 Time period 0 for Net Cash Flow (after Interest & Corporate Tax) plus 5 Time period 0 for Corporate Tax Note: The above Discount Rate needs to be converted from an annual rate, to a rate equivalent to the rest periods being used in the model, before it is used in the NPV function. 18

19 Preference 4 - On Cash Flow Including Financing Costs, Interest and Corporate Tax NPV = 1 NPV ( Discount Rate entered in Input sheet converted from annual to rest period rate, 2 Time period 1 onwards for Net Cash Flow (after Interest & Corporate Tax) ) plus 4 Time period 0 for Net Cash Flow (after Interest & Corporate Tax) Note: The above Discount Rate needs to be converted from an annual rate, to a rate equivalent to the rest periods being used in the model, before it is used in the NPV function. 19

20 6. Benefit Cost Ratio The Benefit Cost Ratio (BCR) attempts to identify the relationship between the costs of a project and their benefits (revenues) on a current value basis. It is essentially the ratio between the present value of a projects costs and the present value of the projects revenues. A BCR below 1.0 infers that the project s costs outweigh the project s revenues, and therefore is deemed to be not feasible, whereas, a BCR above 1.0 infers that the project s costs are less than the project s revenues, and therefore is deemed to be feasible. The Benefit Cost Ratio is closely related to the NPV, just a different way of representing it. Essentially: When the NPV = 0, the BCR = 1.0 When the NPV < 0, the BCR <1.0 When the NPV > 0, the BCR >1.0 Calculation Basically, the Benefit Cost Ratio is the NPV of Revenue divided by the NPV of Costs Since the Benefit Cost Ratio is looking at the comparison between the present value of costs and revenues, the same Preferences are used when determining what cash flow data is used to calculate the output (i.e. whether Interest, Finance Costs and Corporate Tax are considered as Costs in this calculation), and how the discount rate is converted from an annual rate to a rest period rate. BCR = 1 ( NPV ( Discount Rate entered in Input sheet converted from annual to rest period rate, 2 Time period 1 onwards for Total Net Revenue ) plus 3 Time period 0 for Total Net Revenue ) divided by ( NPV ( Discount Rate entered in Input sheet converted from annual to rest period 1 rate, Time period 1 onwards for Costs ) plus Time period 0 for Costs ) 20

: o Total Costs (4) minus Application and Line Fees for Loans 1, 2, 3 and 4 (6) If Preference 3 (Including Financing Costs and Interest but Excluding Corporate")

21 Where Costs = If Preference 1 (Excluding all Financing Costs, Interest and Corporate Tax): o Total Costs (4) minus Financing Costs (exc Fees) (5) If Preference 2 (Including Financing Costs but Excluding Interest and Corporate Tax): o Total Costs (4) minus Application and Line Fees for Loans 1, 2, 3 and 4 (6) If Preference 3 (Including Financing Costs and Interest but Excluding Corporate Tax): o Total Costs (4) minus Application and Line Fees for Loans 1, 2, 3 and 4 (6) minus Interest Charged/Received for Equity, Surplus Cash and Loans 1, 2, 3 and 4 (7) If Preference 4 (Preference 4 - On Cash Flow Including Financing Costs, Interest and Corporate Tax): o Total Costs (4) minus Application and Line Fees for Loans 1, 2, 3 and 4 (6) minus Interest Charged/Received for Equity, Surplus Cash and Loans 1, 2, 3 and 4 (7) plus Corporate Tax (8) Note: The above Discount Rate needs to be converted from an annual rate, to a rate equivalent to the rest periods being used in the model, before it is used in the NPV function. 21

22 22

from a particular investment equal to zero.")

23 7. Project Internal Rate of Return The Internal Rate of Return (IRR) on an investment or project is the "annualised return rate" or "rate of return" that makes the net present value of all cash flows (both positive and negative) from a particular investment equal to zero. In more specific terms, the IRR of an investment is the discount rate at which the net present value of costs (negative cash flows) of the investment equals the net present value of the benefits (positive cash flows) of the investment. Calculation The standard Excel function for IRR is used in Estate Master: IRR ( values, guess) Where: Values = is an array or a reference to cells that contain numbers for which you want to calculate the internal rate of return. Guess = a number that you guess is close to the result of IRR. The cash flow data that is used to calculate the IRR is also summarised in the Project IRR & NPV section of the Cash Flow worksheet. There are 4 different methods for calculating the IRR on the Summary Report, set via the Preferences. They relate to the specific cash flow that is used to calculate the IRR, most notably if it includes financing costs, interest and corporate tax. 23

24 In addition to these Preferences, the IRR is also impacted by the Preference to convert the Discount Rate on either an Effective or Nominal basis. This is required as the initial IRR that is calculated using the Excel IRR function and the cash flow data is not necessarily always an annual rate for example, if the user is running the model with monthly rest periods, then the initial IRR result would be a rate per month. Since IRR needs to be expressed as an annual rate, the answer provided by the Excel IRR function needs to be converted. Example per annum Nominal D x T 1.5% per month x 12 = 18% p.a per annum Effective [(D + 1) T ]-1 [(1.5% per month + 1) 12 ]- 1= 19.56% p.a Where: D = is the rest period (e.g monthly) IRR T = The number of rest periods per annum (i.e Monthly = 12, Quarterly = 4, etc) The Guess Rate is critical in the IRR function, as it uses an iterative technique for calculating it. Starting with the guess, the IRR function cycles through the calculation until the result is accurate within percent. If the IRR function can't find a result that works after 20 tries, the #NUM! error value is returned. The Guess Rate is set in the Hurdle Rates section of the Input sheet. 24

25 Preference 1 - On Cash Flow Excluding all Financing Costs, Interest and Corporate Tax IRR = 1 IRR (Time period 0 onwards for Net Cash Flow before Interest & Corporate Tax plus 2 Time period 0 onwards for Financing Costs 3, Nominate an estimate of IRR entered in Input sheet converted from annual to rest period rate ) Convert answer to Annual Rate based on Nominal or Effective Preference Note: The above Guess Rate needs to be converted from an annual rate, to a rate equivalent to the rest periods being used in the model, before it is used in the IRR function. 25

26 Preference 2 - On Cash Flow Including Financing Costs but Excluding Interest and Corporate Tax IRR = 1 IRR (Time period 0 onwards for Net Cash Flow before Interest & Corporate Tax plus 2 Time period 0 onwards for Application and Line Fees for Loans 1, 2, 3 and 4 3, Nominate an estimate of IRR entered in Input sheet converted from annual to rest period rate ) Convert answer to Annual Rate based on Nominal or Effective Preference Note: The above Guess Rate needs to be converted from an annual rate, to a rate equivalent to the rest periods being used in the model, before it is used in the IRR function. 26

27 Preference 3 - On Cash Flow Including Financing Costs and Interest but Excluding Corporate Tax IRR = 1 IRR (Time period 0 onwards for Net Cash Flow (after Interest & Corporate Tax) plus 2 Time period 0 onwards for Corporate Tax 3, Nominate an estimate of IRR entered in Input sheet converted from annual to rest period rate ) Convert answer to Annual Rate based on Nominal or Effective Preference Note: The above Guess Rate needs to be converted from an annual rate, to a rate equivalent to the rest periods being used in the model, before it is used in the IRR function. 27

28 Preference 4 - On Cash Flow Including Financing Costs, Interest and Corporate Tax IRR = 1 IRR (Time period 0 onwards for Net Cash Flow (after Interest & Corporate Tax), Nominate an estimate of IRR entered in Input sheet converted from annual to rest 2 period rate ) Convert answer to Annual Rate based on Nominal or Effective Preference Note: The above Guess Rate needs to be converted from an annual rate, to a rate equivalent to the rest periods being used in the model, before it is used in the IRR function. 28

29 8. Residual Land Value (Based on % NPV) The Residual Land Value based on the NPV is the maximum price for the land that the developer would pay to make the calculated NPV equal zero or the calculated IRR equal the Discount Rate. The Discount Rate is essentially the developer s required IRR for the project. Unlike the Development Margin, the NPV and IRR takes into account the dimension of time in its calculation and is used to differentiate projects of different cash flow exposures. It is more effective for longer term projects of more than 2 years, as it can be quite sensitive to small movements in time for short term projects. By adopting a suitable Discount Rate (Target IRR), the cash inflows and outflows are discounted to determine their present value and then added together to form a Net Present Value for ease of comparison between other projects of dissimilar timings. From the example below you can see that the IRR for the proposed development project is only achieving 15.51% based on an assumed Land Purchase Price of 13,750,000. In order to achieve the Target IRR (Discount Rate) of 18% the developer would need to purchase the land for a maximum residual land value of 10,377,

30 Calculation There is no specific formula that calculates the Residual Land Value. It is a result that is calculated through undertaking a goal seek - the land price is manipulated up and down until the NPV equals zero and the IRR matches the developer s desired Target IRR (i.e Discount Rate). The Discount Rate is set on the Input sheet under Hurdle Rates Even though the Residual Land Value calculation is not a formula, it can still be easily recreated and demonstrated using Estate Masters Goal Seek function. Once you have opened the Goal Seek function, set the following parameters: Set Cell: The NPV output on the Summary report To Value: Zero By Changing Cell: The Land Purchase Price input on the Input sheet Once you press OK on the Goal Seek, it will then calculate an answer in the Land Purchase Price input on the Input sheet. 30

31 9. Equity IRR The Equity IRR is different to the Project IRR, as it only looks at the rate of return on the equity contributions and repayments. Calculation Similar to the Project IRR, the following pertains to the Equity IRR: The standard Excel function for IRR is used in Estate Master for the Equity IRR calculation. The Equity IRR is also impacted by the Preference to convert the Discount Rate on either an Effective or Nominal Basis. The initial Equity IRR that is calculated using the Excel IRR function and the cash flow data is not necessarily always an annual rate, and therefore needs to be converted on an Effective or Nominal basis. A Guess Rate is required. Equity IRR = 1 IRR (Time period 0 onwards for Equity Cash Flow, 2 Nominate an estimate of IRR entered in Input sheet ) Convert answer to Annual Rate based on Nominal or Effective Preference Note: The above Guess Rate needs to be converted from an annual rate, to a rate equivalent to the rest periods being used in the model, before it is used in the Equity IRR function. 31

32 10. Equity Contribution This is the total amount of Equity being contributed into the Project Calculation Equity Contribution = 1 Sum of all positive Equity Injections on CashFlow sheet Example 5,500, , , , , , , , , , ,568,499 69,945,602 32

, (67,890,551),")

33 11. Peak Debt Exposure This is where the project overdraft for all debt loans reaches its highest point. Calculation Peak Debt Exposure = 1 Largest Negative Project Overdraft on CashFlow sheet, converted to a positive number Example MIN ( (67,833,974), (67,890,551), (68,187,893), (68,187,893), (68,299,049) ) * -1 68,299,049 33

34 12. Equity to Debt Ratio This is the proportion of equity being contributed to the project compared to debt. Calculation Example Equity to Debt Ratio = 1 Equity Funds Invested 69,945,602 divided by / 2 Total Debt Funds Invested 132,371, % 34

70,924,966 ) multiplied by * 3 Developer's")

35 13. Weighted Average Cost of Capital (WACC) The WACC is a calculation of a firm's cost of capital in which each category of capital (equity and debt) is proportionately weighted. Calculation Example WACC = 1 ( Equity Funds Invested ( 70,924,966 divided by / 2 ( Total Debt Funds Invested ( 132,668,186 plus + 1 Equity Funds Invested ) 70,924,966 ) multiplied by * 3 Developer's Cost of Equity on Input 35% ) Sheet ) plus + 2 ( Total Debt Funds Invested ( 132,668,186 divided by / 2 ( Total Debt Funds Invested ( 132,668,186 plus + 1 Equity Funds Invested ) 70,924,966 ) multiplied by * 4 Total Debt Weighted Average Interest 7.53% ) Rate ) multiplied by * 5 ( 1 Weighted Average Tax Rate on ( 1-20% ) Financials Sheet ) 16.12% 35

36 36

37 14. Breakeven Date for Cumulative Cash Flow This is where the Cumulative Cash Flow After Interest goes from being negative to zero/positive. If there are multiple occasions where this occurs in the project life, then the last time it occurs is reported. If the project does not make a profit (and hence does not break even at any point), this result will show N.A Calculation Breakeven Date for Cumulative Cash Flow = 1 The last period where Cumulative Cash Flow After Interest on CashFlow sheet goes from negative to zero or positive Example May-2011 (76,721,570) Jun-2011 (76,972,339) Jul-2011 (70,467,688) Aug ,074,862 Aug

38 15. Yield on Costs Yield on cost is an investment's annual dividend (i.e rental income) divided by the original cost of the investment. If the project does not have any rental income, this result will show N.A Calculation Example Yield on Costs = Current Net Annual Rent on Tenants 1 7,396,700 sheet Divided by / 2 ( Total Costs Before Tax Reclaimed ( 83,448,387 minus - 3 Selling Costs (2,189,944) minus - 4 Purchaser s Costs ) 0 ) 8.64% 38

39 39

40 16. Rent Cover Rent Cover is the total Net Development Profit divided by the Current Net Annual Rental expressed as a number of years/months. If the project does not have any rental income, this result will show N.A Calculation Example Rent Cover = 1 Net Development Profit 8,775,850 Divided by / 2 Current Net Annual Rent on Tenants 7,396,700 sheet This result is then formatted to express a time period of months/years (rounded down to the nearest month) Years and 2 Months 40

41 17. Profit Erosion Profit Erosion is the period of time post practical completion that the project can remain unsold (but leased out) until finance and land holding costs erodes the profit for the development to zero. If the project does not have any capitalised rental income, this result will show N.A Calculation Rent Cover = 1 Net Development Profit multiplied by -1 Divided by From the month the first Capitalised Sales is due to occur onwards, Sum of the following on the Cash Flow sheet ( Maximum of the 2 Previous Month s Gross Rental Income plus 3 Previous Month s Leasing Costs plus 4 Previous Month s Interest Received or 5 Current Month s Gross Rental Income plus 6 Current Month s Leasing Costs plus 7 Current Month s Interest Received ) minus 8 Current Month s Land Holding Costs plus 9 Current Month s Application and Line Fees for Loans 1, 2, 3 and 4 plus 10 Current Month s Interest Charged for Equity and Loans 1, 2, 3 and 4 This result is then formatted to express a time period of months/years (rounded down to the nearest month). 41

42 42

ICASL - Business School Programme

ICASL - Business School Programme Quantitative Techniques for Business (Module 3) Financial Mathematics TUTORIAL 2A This chapter deals with problems related to investing money or capital in a business

ICASL - Business School Programme Quantitative Techniques for Business (Module 3) Financial Mathematics TUTORIAL 2A This chapter deals with problems related to investing money or capital in a business

INCOME APPROACH Gross Income Estimate - $198,000 Vacancy and Rent Loss - $9,900

INCOME APPROACH The Income Approach considers the return on Investment and is similar to the method that investors typically use to make their investment decisions. It is most directly applicable to income

INCOME APPROACH The Income Approach considers the return on Investment and is similar to the method that investors typically use to make their investment decisions. It is most directly applicable to income

Preparing cash budgets

3 Preparing cash budgets this chapter covers... In this chapter we will examine in detail how a cash budget is prepared. This is an important part of your studies, and you will need to be able to prepare

3 Preparing cash budgets this chapter covers... In this chapter we will examine in detail how a cash budget is prepared. This is an important part of your studies, and you will need to be able to prepare

Calculator and QuickCalc USA

Investit Software Inc. www.investitsoftware.com. Calculator and QuickCalc USA TABLE OF CONTENTS Steps in Using the Calculator Time Value on Money Calculator Is used for compound interest calculations involving

Investit Software Inc. www.investitsoftware.com. Calculator and QuickCalc USA TABLE OF CONTENTS Steps in Using the Calculator Time Value on Money Calculator Is used for compound interest calculations involving

Property Report : House in Dallas

Property Report : House in Dallas Generated on: Jul 6, 2016 Author: Guest Page 1 of 11 Table of Contents Executive Summary 3 Property Description 4 Operational Effectivness 5 Financial Effectivness 6 Financing

Property Report : House in Dallas Generated on: Jul 6, 2016 Author: Guest Page 1 of 11 Table of Contents Executive Summary 3 Property Description 4 Operational Effectivness 5 Financial Effectivness 6 Financing

Table of Contents. Part I Introduction to Estate Master. Part II Installation 11. Part III Introduction to Development Analysis

Operations Manual 2 Estate Master DM Table of Contents 6 Part I Introduction to Estate Master 1 Introduction... 6 2 Program Integrity... 6 3 System Requirements... 7 9 Part II Installation 11 Part III

Operations Manual 2 Estate Master DM Table of Contents 6 Part I Introduction to Estate Master 1 Introduction... 6 2 Program Integrity... 6 3 System Requirements... 7 9 Part II Installation 11 Part III

NSW BOARDING ACCOMODATION CALCULATOR USER GUIDELINES

NSW BOARDING ACCOMODATION CALCULATOR USER GUIDELINES ORIGINALLY PREPARED FOR NSW DEPARTMENT OF HOUSING IN MAY 2007 BY HILL PDA. AMENDED JULY 2010 BY HOUSING NSW 1 WHAT IS THE BOARDING ACCOMMODATION CALCULATOR?

NSW BOARDING ACCOMODATION CALCULATOR USER GUIDELINES ORIGINALLY PREPARED FOR NSW DEPARTMENT OF HOUSING IN MAY 2007 BY HILL PDA. AMENDED JULY 2010 BY HOUSING NSW 1 WHAT IS THE BOARDING ACCOMMODATION CALCULATOR?

Introduction to Real Estate Investment Appraisal

Introduction to Real Estate Investment Appraisal NPV and IRR Pat McAllister INVESTMENT APPRAISAL DISCOUNTED CASFLOW ANALYSIS Investment Mathematics Discounted cash flow to calculate Gross present value

Introduction to Real Estate Investment Appraisal NPV and IRR Pat McAllister INVESTMENT APPRAISAL DISCOUNTED CASFLOW ANALYSIS Investment Mathematics Discounted cash flow to calculate Gross present value

APPENDIX. Interest Concepts of Future and Present Value. Concept of Interest TIME VALUE OF MONEY BASIC INTEREST CONCEPTS

CHAPTER 8 Current Monetary Balances 395 APPENDIX Interest Concepts of Future and Present Value TIME VALUE OF MONEY In general business terms, interest is defined as the cost of using money over time. Economists

CHAPTER 8 Current Monetary Balances 395 APPENDIX Interest Concepts of Future and Present Value TIME VALUE OF MONEY In general business terms, interest is defined as the cost of using money over time. Economists

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

3. Time value of money. We will review some tools for discounting cash flows.

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

Chapter 9. Year Revenue COGS Depreciation S&A Taxable Income After-tax Operating Income 1 $20.60 $12.36 $1.00 $2.06 $5.18 $3.11

Chapter 9 9-1 We assume that revenues and selling & administrative expenses will increase at the rate of inflation. Year Revenue COGS Depreciation S&A Taxable Income After-tax Operating Income 1 $20.60

Chapter 9 9-1 We assume that revenues and selling & administrative expenses will increase at the rate of inflation. Year Revenue COGS Depreciation S&A Taxable Income After-tax Operating Income 1 $20.60

Basic Concept of Time Value of Money

Basic Concept of Time Value of Money CHAPTER 1 1.1 INTRODUCTION Money has time value. A rupee today is more valuable than a year hence. It is on this concept the time value of money is based. The recognition

Basic Concept of Time Value of Money CHAPTER 1 1.1 INTRODUCTION Money has time value. A rupee today is more valuable than a year hence. It is on this concept the time value of money is based. The recognition

The Marginal Cost of Capital and the Optimal Capital Budget

WEB EXTENSION12B The Marginal Cost of Capital and the Optimal Capital Budget If the capital budget is so large that a company must issue new equity, then the cost of capital for the company increases.

WEB EXTENSION12B The Marginal Cost of Capital and the Optimal Capital Budget If the capital budget is so large that a company must issue new equity, then the cost of capital for the company increases.

The key tools of farm business analyses

10 The key tools of farm business analyses This chapter explains the benefits of accurately documenting farm assets and liabilities, as well as farm costs and income, to monitor the business performance

10 The key tools of farm business analyses This chapter explains the benefits of accurately documenting farm assets and liabilities, as well as farm costs and income, to monitor the business performance

Financial Statement and Cash Flow Analysis

Chapter 2 Financial Statement and Cash Flow Analysis Answers to Concept Review Questions 1. What role do the FASB and SEC play with regard to GAAP? The FASB is a nongovernmental, professional standards

Chapter 2 Financial Statement and Cash Flow Analysis Answers to Concept Review Questions 1. What role do the FASB and SEC play with regard to GAAP? The FASB is a nongovernmental, professional standards

Net Present Value (NPV)

") Investment Criteria 208 Net Present Value (NPV) What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value and

Investment Criteria 208 Net Present Value (NPV) What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value and

Table of Contents. Part I Introduction to Estate Master. Part II Installation. Part III Introduction to Development Feasibility Analysis

Operations Manual 2 Estate Master DF Table of Contents 6 Part I Introduction to Estate Master 1 Introduction... 6 2 Program Integrity... 6 3 System Requirements... 7 9 Part II Installation Part III Introduction

Operations Manual 2 Estate Master DF Table of Contents 6 Part I Introduction to Estate Master 1 Introduction... 6 2 Program Integrity... 6 3 System Requirements... 7 9 Part II Installation Part III Introduction

International Valuation Guidance Note No. 9 Discounted Cash Flow Analysis for Market and Non-Market Based Valuations

International Valuation Guidance Note No. 9 Discounted Cash Flow Analysis for Market and Non-Market Based Valuations 1.0 Introduction 1.1 Discounted cash flow (DCF) analysis is a financial modelling technique

International Valuation Guidance Note No. 9 Discounted Cash Flow Analysis for Market and Non-Market Based Valuations 1.0 Introduction 1.1 Discounted cash flow (DCF) analysis is a financial modelling technique

Time Value of Money 1

Time Value of Money 1 This topic introduces you to the analysis of trade-offs over time. Financial decisions involve costs and benefits that are spread over time. Financial decision makers in households

Time Value of Money 1 This topic introduces you to the analysis of trade-offs over time. Financial decisions involve costs and benefits that are spread over time. Financial decision makers in households

Computing the Total Assets, Liabilities, and Owner s Equity

21-1 Assets are the total of your cash, the items that you have purchased, and any money that your customers owe you. Liabilities are the total amount of money that you owe to creditors. Owner s equity,

21-1 Assets are the total of your cash, the items that you have purchased, and any money that your customers owe you. Liabilities are the total amount of money that you owe to creditors. Owner s equity,

Introduction to Real Estate Investment Appraisal

Introduction to Real Estate Investment Appraisal Maths of Finance Present and Future Values Pat McAllister INVESTMENT APPRAISAL: INTEREST Interest is a reward or rent paid to a lender or investor who has

Introduction to Real Estate Investment Appraisal Maths of Finance Present and Future Values Pat McAllister INVESTMENT APPRAISAL: INTEREST Interest is a reward or rent paid to a lender or investor who has

Management Accounting Financial Strategy

PAPER P9 Management Accounting Financial Strategy The Examiner provides a short study guide, for all candidates revising for this paper, to some first principles of finance and financial management Based

PAPER P9 Management Accounting Financial Strategy The Examiner provides a short study guide, for all candidates revising for this paper, to some first principles of finance and financial management Based

Investment Appraisal INTRODUCTION

8 Investment Appraisal INTRODUCTION After reading the chapter, you should: understand what is meant by the time value of money; be able to carry out a discounted cash flow analysis to assess the viability

8 Investment Appraisal INTRODUCTION After reading the chapter, you should: understand what is meant by the time value of money; be able to carry out a discounted cash flow analysis to assess the viability

hp calculators HP 17bII+ Net Present Value and Internal Rate of Return Cash Flow Zero A Series of Cash Flows What Net Present Value Is

HP 17bII+ Net Present Value and Internal Rate of Return Cash Flow Zero A Series of Cash Flows What Net Present Value Is Present Value and Net Present Value Getting the Present Value And Now For the Internal

HP 17bII+ Net Present Value and Internal Rate of Return Cash Flow Zero A Series of Cash Flows What Net Present Value Is Present Value and Net Present Value Getting the Present Value And Now For the Internal

Economic Analysis and Economic Decisions for Energy Projects

Economic Analysis and Economic Decisions for Energy Projects Economic Factors As in any investment project, the following factors should be considered while making the investment decisions in energy investment

Economic Analysis and Economic Decisions for Energy Projects Economic Factors As in any investment project, the following factors should be considered while making the investment decisions in energy investment

Time-Value-of-Money and Amortization Worksheets

2 Time-Value-of-Money and Amortization Worksheets The Time-Value-of-Money and Amortization worksheets are useful in applications where the cash flows are equal, evenly spaced, and either all inflows or

2 Time-Value-of-Money and Amortization Worksheets The Time-Value-of-Money and Amortization worksheets are useful in applications where the cash flows are equal, evenly spaced, and either all inflows or

Choice of Discount Rate

Choice of Discount Rate Discussion Plan Basic Theory and Practice A common practical approach: WACC = Weighted Average Cost of Capital Look ahead: CAPM = Capital Asset Pricing Model Massachusetts Institute

Choice of Discount Rate Discussion Plan Basic Theory and Practice A common practical approach: WACC = Weighted Average Cost of Capital Look ahead: CAPM = Capital Asset Pricing Model Massachusetts Institute

Fundamentals Level Skills Module, Paper F9. Section A. Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6%

![Fundamentals Level Skills Module, Paper F9. Section A. Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6%](/thumbs/40/20831119.jpg "Fundamentals Level Skills Module, Paper F9. Section A. Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6%") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2015 Answers Section A 1 A 2 D 3 D Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6% 4 A 5 D 6 B 7

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2015 Answers Section A 1 A 2 D 3 D Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6% 4 A 5 D 6 B 7

NOTICE: For details of the project history please look under the Work Plan section of this website.

NOTICE: This Exposure Draft is available to show the historic evolution of the project. It does not include changes made by the Board following the consultation process and therefore should not be relied

NOTICE: This Exposure Draft is available to show the historic evolution of the project. It does not include changes made by the Board following the consultation process and therefore should not be relied

FINANCIAL ANALYSIS GUIDE

MAN 4720 POLICY ANALYSIS AND FORMULATION FINANCIAL ANALYSIS GUIDE Revised -August 22, 2010 FINANCIAL ANALYSIS USING STRATEGIC PROFIT MODEL RATIOS Introduction Your policy course integrates information

MAN 4720 POLICY ANALYSIS AND FORMULATION FINANCIAL ANALYSIS GUIDE Revised -August 22, 2010 FINANCIAL ANALYSIS USING STRATEGIC PROFIT MODEL RATIOS Introduction Your policy course integrates information

Compound Interest. Invest 500 that earns 10% interest each year for 3 years, where each interest payment is reinvested at the same rate:

Compound Interest Invest 500 that earns 10% interest each year for 3 years, where each interest payment is reinvested at the same rate: Table 1 Development of Nominal Payments and the Terminal Value, S.

Compound Interest Invest 500 that earns 10% interest each year for 3 years, where each interest payment is reinvested at the same rate: Table 1 Development of Nominal Payments and the Terminal Value, S.

Financial Reporting & Analysis Chapter 17 Solutions Statement of Cash Flows Exercises

Financial Reporting & Analysis Chapter 17 Solutions Statement of Cash Flows Exercises Exercises E17-1. Determining cash flows from operations Using the indirect method, cash flow from operations is computed

Financial Reporting & Analysis Chapter 17 Solutions Statement of Cash Flows Exercises Exercises E17-1. Determining cash flows from operations Using the indirect method, cash flow from operations is computed

( ) ( )( ) ( ) 2 ( ) 3. n n = 100 000 1+ 0.10 = 100 000 1.331 = 133100

( )( ) ( ) 2 ( ) 3. n n = 100 000 1+ 0.10 = 100 000 1.331 = 133100") Mariusz Próchniak Chair of Economics II Warsaw School of Economics CAPITAL BUDGETING Managerial Economics 1 2 1 Future value (FV) r annual interest rate B the amount of money held today Interest is compounded

Mariusz Próchniak Chair of Economics II Warsaw School of Economics CAPITAL BUDGETING Managerial Economics 1 2 1 Future value (FV) r annual interest rate B the amount of money held today Interest is compounded

Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements

Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements TABLE OF CONTENTS 1.0

Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements TABLE OF CONTENTS 1.0

6. Debt Valuation and the Cost of Capital

6. Debt Valuation and the Cost of Capital Introduction Firms rarely finance capital projects by equity alone. They utilise long and short term funds from a variety of sources at a variety of costs. No

6. Debt Valuation and the Cost of Capital Introduction Firms rarely finance capital projects by equity alone. They utilise long and short term funds from a variety of sources at a variety of costs. No

By Tim Berry President, Palo Alto Software Copyright September, 2004. The Business Plan Pro Financial Model

By Tim Berry President, Palo Alto Software Copyright September, 2004 The Business Plan Pro Financial Model Table Of Contents Table Of Contents Introduction... 2 Accounting Principals... 3 Simplifying Assumptions...

By Tim Berry President, Palo Alto Software Copyright September, 2004 The Business Plan Pro Financial Model Table Of Contents Table Of Contents Introduction... 2 Accounting Principals... 3 Simplifying Assumptions...

Capital Investment Analysis and Project Assessment

PURDUE EXTENSION EC-731 Capital Investment Analysis and Project Assessment Michael Boehlje and Cole Ehmke Department of Agricultural Economics Capital investment decisions that involve the purchase of

PURDUE EXTENSION EC-731 Capital Investment Analysis and Project Assessment Michael Boehlje and Cole Ehmke Department of Agricultural Economics Capital investment decisions that involve the purchase of

Land Purchase Analysis

Land Purchase Analysis With this program, the user can evaluate the economic return on a farmland purchase and calculate a maximum bid price The maximum bid price is the purchase price that allows the

Land Purchase Analysis With this program, the user can evaluate the economic return on a farmland purchase and calculate a maximum bid price The maximum bid price is the purchase price that allows the

GUIDANCE NOTE: THE USE OF INTERNAL RATES OF RETURN IN PFI PROJECTS

GUIDANCE NOTE: THE USE OF INTERNAL RATES OF RETURN IN PFI PROJECTS 1 INTRODUCTION 1.1 The Internal Rate of Return (IRR) is most commonly used in PFI Contracts as a measure of the rate of return expected

GUIDANCE NOTE: THE USE OF INTERNAL RATES OF RETURN IN PFI PROJECTS 1 INTRODUCTION 1.1 The Internal Rate of Return (IRR) is most commonly used in PFI Contracts as a measure of the rate of return expected

Chapter 18. Web Extension: Percentage Cost Analysis, Leasing Feedback, and Leveraged Leases

Chapter 18 Web Extension: Percentage Cost Analysis, Leasing Feedback, and Leveraged Leases Percentage Cost Analysis Anderson s lease-versus-purchase decision from Chapter 18 could also be analyzed using

Chapter 18 Web Extension: Percentage Cost Analysis, Leasing Feedback, and Leveraged Leases Percentage Cost Analysis Anderson s lease-versus-purchase decision from Chapter 18 could also be analyzed using

1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084 6,327 6,580 6,844

Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084 6,327 6,580 6,844") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2013 Answers 1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2013 Answers 1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084

CHAPTER 8 INTEREST RATES AND BOND VALUATION

CHAPTER 8 INTEREST RATES AND BOND VALUATION Solutions to Questions and Problems 1. The price of a pure discount (zero coupon) bond is the present value of the par value. Remember, even though there are

CHAPTER 8 INTEREST RATES AND BOND VALUATION Solutions to Questions and Problems 1. The price of a pure discount (zero coupon) bond is the present value of the par value. Remember, even though there are

Breakeven Analysis. Breakeven for Services.

Dollars and Sense Introduction Your dream is to operate a profitable business and make a good living. Before you open, however, you want some indication that your business will be profitable, if not immediately

Dollars and Sense Introduction Your dream is to operate a profitable business and make a good living. Before you open, however, you want some indication that your business will be profitable, if not immediately

Calculation Guide Estate Master DF Summary Report Returns on Funds Invested. Aug 2014

Calculatin Guide Estate Master DF Summary Reprt Returns n Funds Invested Aug 2014 Table f Cntents Intrductin... 3 Summary Reprt Returns n Funds Invested... 4 1. Funds Invested (Cash Outlay)... 4 2. Peak

Calculatin Guide Estate Master DF Summary Reprt Returns n Funds Invested Aug 2014 Table f Cntents Intrductin... 3 Summary Reprt Returns n Funds Invested... 4 1. Funds Invested (Cash Outlay)... 4 2. Peak

GCSE Business Studies. Ratios. For first teaching from September 2009 For first award in Summer 2011

GCSE Business Studies Ratios For first teaching from September 2009 For first award in Summer 2011 Ratios At the end of this unit students should be able to: Interpret and analyse final accounts and balance

GCSE Business Studies Ratios For first teaching from September 2009 For first award in Summer 2011 Ratios At the end of this unit students should be able to: Interpret and analyse final accounts and balance

Real Estate Investment Analysis and Advanced Income Appraisal BUSI 331

Real Estate Division Real Estate Investment Analysis and Advanced Income Appraisal BUSI 331 Presentation by Graham McIntosh Outline 1. Introduction 2. Investment Analysis vs. Appraisal 3. The After Tax

Real Estate Division Real Estate Investment Analysis and Advanced Income Appraisal BUSI 331 Presentation by Graham McIntosh Outline 1. Introduction 2. Investment Analysis vs. Appraisal 3. The After Tax

Capital Budgeting. Financial Modeling Templates

Financial Modeling Templates http://spreadsheetml.com/finance/capitalbudgeting.shtml Copyright (c) 2009-2014, ConnectCode All Rights Reserved. ConnectCode accepts no responsibility for any adverse affect

Financial Modeling Templates http://spreadsheetml.com/finance/capitalbudgeting.shtml Copyright (c) 2009-2014, ConnectCode All Rights Reserved. ConnectCode accepts no responsibility for any adverse affect

CARNEGIE MELLON UNIVERSITY CIO INSTITUTE

CARNEGIE MELLON UNIVERSITY CIO INSTITUTE CAPITAL BUDGETING BASICS Contact Information: Lynne Pastor Email: [email protected] RELATED LEARNGING OBJECTIVES 7.2 LO 3: Compare and contrast the implications

CARNEGIE MELLON UNIVERSITY CIO INSTITUTE CAPITAL BUDGETING BASICS Contact Information: Lynne Pastor Email: [email protected] RELATED LEARNGING OBJECTIVES 7.2 LO 3: Compare and contrast the implications

CIMA F3 Course Notes. Chapter 11. Company valuations

CIMA F3 Course Notes Chapter 11 Company valuations Personal use only - not licensed for use on courses 144 1. Company valuations There are several methods of valuing the equity of a company. The simplest

CIMA F3 Course Notes Chapter 11 Company valuations Personal use only - not licensed for use on courses 144 1. Company valuations There are several methods of valuing the equity of a company. The simplest

BENEFIT-COST ANALYSIS Financial and Economic Appraisal using Spreadsheets

BENEFIT-COST ANALYSIS Financial and Economic Appraisal using Spreadsheets Ch. 4: Project and Private Benefit-Cost Analysis Private Benefit-Cost Analysis Deriving Project and Private cash flows: Project

BENEFIT-COST ANALYSIS Financial and Economic Appraisal using Spreadsheets Ch. 4: Project and Private Benefit-Cost Analysis Private Benefit-Cost Analysis Deriving Project and Private cash flows: Project

IGCSE Business Studies revision notes Finance [email protected]

IGCSE FINANCE REVISION NOTES Table of contents Table of contents... 2 SOURCES OF FINANCE... 3 CASH FLOW... 5 HOW TO CALCULATE THE CASH BALANCE... 5 HOW TO WORK OUT THE CASH AVAILABLE TO THE BUSINESS...

IGCSE FINANCE REVISION NOTES Table of contents Table of contents... 2 SOURCES OF FINANCE... 3 CASH FLOW... 5 HOW TO CALCULATE THE CASH BALANCE... 5 HOW TO WORK OUT THE CASH AVAILABLE TO THE BUSINESS...

MBA Data Analysis Pad John Beasley

1 Marketing Analysis Pad - 1985 Critical Issue: Identify / Define the Problem: Objectives: (Profitability Sales Growth Market Share Risk Diversification Innovation) Company Mission: (Source & Focus for

1 Marketing Analysis Pad - 1985 Critical Issue: Identify / Define the Problem: Objectives: (Profitability Sales Growth Market Share Risk Diversification Innovation) Company Mission: (Source & Focus for

Contribution 787 1,368 1,813 983. Taxable cash flow 682 1,253 1,688 858 Tax liabilities (205) (376) (506) (257)

(376) (506) (257)") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2012 Answers 1 (a) Calculation of net present value (NPV) As nominal after-tax cash flows are to be discounted, the nominal

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2012 Answers 1 (a) Calculation of net present value (NPV) As nominal after-tax cash flows are to be discounted, the nominal

CE Entrepreneurship. Investment decision making

CE Entrepreneurship Investment decision making Cash Flow For projects where there is a need to spend money to develop a product or establish a service which results in cash coming into the business in

CE Entrepreneurship Investment decision making Cash Flow For projects where there is a need to spend money to develop a product or establish a service which results in cash coming into the business in

Finance 445 Practice Exam Chapters 1, 2, 5, and part of Chapter 6. Part One. Multiple Choice Questions.

Finance 445 Practice Exam Chapters 1, 2, 5, and part of Chapter 6 Part One. Multiple Choice Questions. 1. Similar to the example given in class, assume that a corporation has $500 of cash revenue and $300

Finance 445 Practice Exam Chapters 1, 2, 5, and part of Chapter 6 Part One. Multiple Choice Questions. 1. Similar to the example given in class, assume that a corporation has $500 of cash revenue and $300

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting Lecture Note: Financial Statement Basics, Transaction Recording, and Terminology I. The Financial Reporting Package

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting Lecture Note: Financial Statement Basics, Transaction Recording, and Terminology I. The Financial Reporting Package

1 (a) Calculation of net present value (NPV) Year 1 2 3 4 5 6 $000 $000 $000 $000 $000 $000 Sales revenue 1,600 1,600 1,600 1,600 1,600

Calculation of net present value (NPV) Year 1 2 3 4 5 6 $000 $000 $000 $000 $000 $000 Sales revenue 1,600 1,600 1,600 1,600 1,600") Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2011 Answers 1 (a) Calculation of net present value (NPV) Year 1 2 3 4 5 6 $000 $000 $000 $000 $000 $000 Sales revenue 1,600

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2011 Answers 1 (a) Calculation of net present value (NPV) Year 1 2 3 4 5 6 $000 $000 $000 $000 $000 $000 Sales revenue 1,600

Lease Analysis Tools

Lease Analysis Tools 2009 ELFA Lease Accountants Conference Presenter: Bill Bosco, Pres. [email protected] Leasing 101 914-522-3233 Overview Math of Finance Theory Glossary of terms Common calculations

Lease Analysis Tools 2009 ELFA Lease Accountants Conference Presenter: Bill Bosco, Pres. [email protected] Leasing 101 914-522-3233 Overview Math of Finance Theory Glossary of terms Common calculations

User Guide for OPIC Financial Projections Model Builder Tool

User Guide for OPIC Financial Projections Model Builder Tool 4/2/2013 Prepared by: Deborah Howard Document Control Document Information Information Document Owner Deborah Howard Issue Date 4/2/2013 Document

User Guide for OPIC Financial Projections Model Builder Tool 4/2/2013 Prepared by: Deborah Howard Document Control Document Information Information Document Owner Deborah Howard Issue Date 4/2/2013 Document

Southern Africa Syndicated Loans Documentation Training 31 July 2014, Johannesburg. Financial Covenants Edmund Boyo, Partner Clifford Chance

Southern Africa Syndicated Loans Documentation Training 31 July 2014, Johannesburg Financial Covenants Edmund Boyo, Partner Clifford Chance Introduction The LMA financial covenants: LMA leveraged facility

Southern Africa Syndicated Loans Documentation Training 31 July 2014, Johannesburg Financial Covenants Edmund Boyo, Partner Clifford Chance Introduction The LMA financial covenants: LMA leveraged facility

Scott s Real Estate Investment Trust. Interim Consolidated Financial Statements (Unaudited) March 31, 2009 and 2008

March 31, 2009 and 2008") Interim Consolidated Financial Statements March 31, and Interim Consolidated Balance Sheets (in thousands of dollars) Assets March 31, December 31, Income-producing properties (note 3) 172,404 174,135

Interim Consolidated Financial Statements March 31, and Interim Consolidated Balance Sheets (in thousands of dollars) Assets March 31, December 31, Income-producing properties (note 3) 172,404 174,135

WORKBOOK ON PROJECT FINANCE. Prepared by Professor William J. Kretlow University of Houston

WORKBOOK ON PROJECT FINANCE Prepared by Professor William J. Kretlow University of Houston 2002 by Institute for Energy, Law & Enterprise, University of Houston Law Center. All rights reserved. TABLE

WORKBOOK ON PROJECT FINANCE Prepared by Professor William J. Kretlow University of Houston 2002 by Institute for Energy, Law & Enterprise, University of Houston Law Center. All rights reserved. TABLE

380.760: Corporate Finance. Financial Decision Making

380.760: Corporate Finance Lecture 2: Time Value of Money and Net Present Value Gordon Bodnar, 2009 Professor Gordon Bodnar 2009 Financial Decision Making Finance decision making is about evaluating costs

380.760: Corporate Finance Lecture 2: Time Value of Money and Net Present Value Gordon Bodnar, 2009 Professor Gordon Bodnar 2009 Financial Decision Making Finance decision making is about evaluating costs

PERPETUITIES NARRATIVE SCRIPT 2004 SOUTH-WESTERN, A THOMSON BUSINESS

NARRATIVE SCRIPT 2004 SOUTH-WESTERN, A THOMSON BUSINESS NARRATIVE SCRIPT: SLIDE 2 A good understanding of the time value of money is crucial for anybody who wants to deal in financial markets. It does

NARRATIVE SCRIPT 2004 SOUTH-WESTERN, A THOMSON BUSINESS NARRATIVE SCRIPT: SLIDE 2 A good understanding of the time value of money is crucial for anybody who wants to deal in financial markets. It does

10.SHORT-TERM DECISIONS & CAPITAL INVESTMENT APPRAISAL

INDUSTRIAL UNIVERSITY OF HO CHI MINH CITY AUDITING ACCOUNTING FACULTY 10.SHORT-TERM DECISIONS & CAPITAL INVESTMENT APPRAISAL 4 Topic List INDUSTRIAL UNIVERSITY OF HO CHI MINH CITY AUDITING ACCOUNTING FACULTY

INDUSTRIAL UNIVERSITY OF HO CHI MINH CITY AUDITING ACCOUNTING FACULTY 10.SHORT-TERM DECISIONS & CAPITAL INVESTMENT APPRAISAL 4 Topic List INDUSTRIAL UNIVERSITY OF HO CHI MINH CITY AUDITING ACCOUNTING FACULTY

Types of Leases. Lease Financing

Lease Financing Types of leases Tax treatment of leases Effects on financial statements Lessee s analysis Lessor s analysis Other issues in lease analysis Who are the two parties to a lease transaction?

Lease Financing Types of leases Tax treatment of leases Effects on financial statements Lessee s analysis Lessor s analysis Other issues in lease analysis Who are the two parties to a lease transaction?

SU 8: Responsibility Accounting and Performance Measures 415. 8.5 Financial Measures

SU 8: Responsibility Accounting and Performance Measures 415 8.5 Financial Measures 57. A firm earning a profit can increase its return on investment by A. Increasing sales revenue and operating expenses

SU 8: Responsibility Accounting and Performance Measures 415 8.5 Financial Measures 57. A firm earning a profit can increase its return on investment by A. Increasing sales revenue and operating expenses

Financial Statement Analysis!

Financial Statement Analysis! The raw data for investing Aswath Damodaran! 1! Questions we would like answered! Assets Liabilities What are the assets in place? How valuable are these assets? How risky

Financial Statement Analysis! The raw data for investing Aswath Damodaran! 1! Questions we would like answered! Assets Liabilities What are the assets in place? How valuable are these assets? How risky

Learning Objectives: Quick answer key: Question # Multiple Choice True/False. 14.1 Describe the important of accounting and financial information.

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

Financial Statement Consolidation

Financial Statement Consolidation We will consolidate the previously completed worksheets in this financial plan. In order to complete this section of the plan, you must have already completed all of the

Financial Statement Consolidation We will consolidate the previously completed worksheets in this financial plan. In order to complete this section of the plan, you must have already completed all of the

ENTREPRENEURIAL FINANCE: Strategy Valuation and Deal Structure

ENTREPRENEURIAL FINANCE: Strategy Valuation and Deal Structure Chapter 9 Valuation Questions and Problems 1. You are considering purchasing shares of DeltaCad Inc. for $40/share. Your analysis of the company

ENTREPRENEURIAL FINANCE: Strategy Valuation and Deal Structure Chapter 9 Valuation Questions and Problems 1. You are considering purchasing shares of DeltaCad Inc. for $40/share. Your analysis of the company

Large Company Limited. Report and Accounts. 31 December 2009

Registered number 123456 Large Company Limited Report and Accounts 31 December 2009 Report and accounts Contents Page Company information 1 Directors' report 2 Statement of directors' responsibilities

Registered number 123456 Large Company Limited Report and Accounts 31 December 2009 Report and accounts Contents Page Company information 1 Directors' report 2 Statement of directors' responsibilities

Fin 5413 CHAPTER FOUR

Slide 1 Interest Due Slide 2 Fin 5413 CHAPTER FOUR FIXED RATE MORTGAGE LOANS Interest Due is the mirror image of interest earned In previous finance course you learned that interest earned is: Interest

Slide 1 Interest Due Slide 2 Fin 5413 CHAPTER FOUR FIXED RATE MORTGAGE LOANS Interest Due is the mirror image of interest earned In previous finance course you learned that interest earned is: Interest

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods TABLE OF CONTENTS

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

ECONOMIC JUSTIFICATION

ECONOMIC JUSTIFICATION A Manufacturing Engineer s Point of View M. Kevin Nelson, P.E. President Productioneering, Inc. www.roboautotech.com Contents: I. Justification methods a. Net Present Value (NPV)

ECONOMIC JUSTIFICATION A Manufacturing Engineer s Point of View M. Kevin Nelson, P.E. President Productioneering, Inc. www.roboautotech.com Contents: I. Justification methods a. Net Present Value (NPV)

BF 6701 : Financial Management Comprehensive Examination Guideline

BF 6701 : Financial Management Comprehensive Examination Guideline 1) There will be 5 essay questions and 5 calculation questions to be completed in 1-hour exam. 2) The topics included in those essay and

BF 6701 : Financial Management Comprehensive Examination Guideline 1) There will be 5 essay questions and 5 calculation questions to be completed in 1-hour exam. 2) The topics included in those essay and

ITU / BDT- COE workshop. Network Planning. Business Planning. Lecture NP- 3.5. Nairobi, Kenya, 7 11 October 2002

ITU / BDT- COE workshop Nairobi, Kenya, 7 11 October 2002 Network Planning Lecture NP- 3.5 Business Planning October 8th ITU/BDT-COE Network Planning/ Business Planning - O.G.S. Lecture NP - 3.5 - slide

ITU / BDT- COE workshop Nairobi, Kenya, 7 11 October 2002 Network Planning Lecture NP- 3.5 Business Planning October 8th ITU/BDT-COE Network Planning/ Business Planning - O.G.S. Lecture NP - 3.5 - slide

VALUE 11.125%. $100,000 2003 (=MATURITY

NOTES H IX. How to Read Financial Bond Pages Understanding of the previously discussed interest rate measures will permit you to make sense out of the tables found in the financial sections of newspapers

NOTES H IX. How to Read Financial Bond Pages Understanding of the previously discussed interest rate measures will permit you to make sense out of the tables found in the financial sections of newspapers

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS 1997, Roy T. Black REAE 5311, Fall 2005 University of Texas at Arlington J. Andrew Hansz, Ph.D., CFA CONTENTS ITEM ANNUAL COMPOUND INTEREST TABLES AT 10% MATERIALS

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS 1997, Roy T. Black REAE 5311, Fall 2005 University of Texas at Arlington J. Andrew Hansz, Ph.D., CFA CONTENTS ITEM ANNUAL COMPOUND INTEREST TABLES AT 10% MATERIALS

Understanding Cash Flow Statements

Understanding Cash Flow Statements 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Components and Format of the Cash Flow Statement... 3 3. The

Understanding Cash Flow Statements 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Components and Format of the Cash Flow Statement... 3 3. The

Company Financial Plan

Financial Modeling Templates http://spreadsheetml.com/finance/companyfinancialplan.shtml Copyright (c) 2009-2014, ConnectCode All Rights Reserved. ConnectCode accepts no responsibility for any adverse

Financial Modeling Templates http://spreadsheetml.com/finance/companyfinancialplan.shtml Copyright (c) 2009-2014, ConnectCode All Rights Reserved. ConnectCode accepts no responsibility for any adverse

Rate used to accrete interest and calculate the present value of cash flows that unlock the contractual service margin

IASB Agenda ref 2B STAFF PAPER REG IASB Meeting Project Paper topic Insurance contracts July 2014 Rate used to accrete interest and calculate the present value of cash flows that CONTACT(S) Izabela Ruta

IASB Agenda ref 2B STAFF PAPER REG IASB Meeting Project Paper topic Insurance contracts July 2014 Rate used to accrete interest and calculate the present value of cash flows that CONTACT(S) Izabela Ruta

Glossary of Accounting Terms

Glossary of Accounting Terms Account - Something to which transactions are assigned. Accounts in MYOB are in one of eight categories: Asset Liability Equity Income Cost of sales Expense Other income Other

Glossary of Accounting Terms Account - Something to which transactions are assigned. Accounts in MYOB are in one of eight categories: Asset Liability Equity Income Cost of sales Expense Other income Other

How to Calculate Present Values

How to Calculate Present Values Michael Frantz, 2010-09-22 Present Value What is the Present Value The Present Value is the value today of tomorrow s cash flows. It is based on the fact that a Euro tomorrow

How to Calculate Present Values Michael Frantz, 2010-09-22 Present Value What is the Present Value The Present Value is the value today of tomorrow s cash flows. It is based on the fact that a Euro tomorrow

Unit 2: Finance for Business

Unit 2: Finance for Business Level: 1 and 2 Unit type: Core Guided learning hours: 30 Assessment type: External Unit introduction All businesses have to spend money before they can make a profit, and when

Unit 2: Finance for Business Level: 1 and 2 Unit type: Core Guided learning hours: 30 Assessment type: External Unit introduction All businesses have to spend money before they can make a profit, and when

Balance Sheet. Financial Management Series #1 9/2009

Balance Sheet Prepared By: James N. Kurtz, Extension Educator Financial Management Series #1 9/2009 A complete set of financial statements for agriculture include: a Balance Sheet; an Income Statement;

Balance Sheet Prepared By: James N. Kurtz, Extension Educator Financial Management Series #1 9/2009 A complete set of financial statements for agriculture include: a Balance Sheet; an Income Statement;

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION 12 April 2016 (am) Subject CT1 Financial Mathematics Core

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION 12 April 2016 (am) Subject CT1 Financial Mathematics Core

Time Value of Money. 2014 Level I Quantitative Methods. IFT Notes for the CFA exam

Time Value of Money 2014 Level I Quantitative Methods IFT Notes for the CFA exam Contents 1. Introduction...2 2. Interest Rates: Interpretation...2 3. The Future Value of a Single Cash Flow...4 4. The

Time Value of Money 2014 Level I Quantitative Methods IFT Notes for the CFA exam Contents 1. Introduction...2 2. Interest Rates: Interpretation...2 3. The Future Value of a Single Cash Flow...4 4. The

Accounting. Consolidated Balance Sheets [ADVANCED HIGHER] Brian Bennie. abc

![Accounting. Consolidated Balance Sheets [ADVANCED HIGHER] Brian Bennie. abc](/thumbs/40/20534999.jpg "Accounting. Consolidated Balance Sheets [ADVANCED HIGHER] Brian Bennie. abc") Accounting Consolidated Balance Sheets [ADVANCED HIGHER] Brian Bennie abc Acknowledgement Learning and Teaching Scotland gratefully acknowledge this contribution to the National Qualifications support

Accounting Consolidated Balance Sheets [ADVANCED HIGHER] Brian Bennie abc Acknowledgement Learning and Teaching Scotland gratefully acknowledge this contribution to the National Qualifications support

Volex Group plc. Transition to International Financial Reporting Standards Supporting document for 2 October 2005 Interim Statement. 1.

Volex Group plc Transition to International Financial Reporting Standards Supporting document for 2 October 2005 Interim Statement 1. Introduction The consolidated financial statements of Volex Group plc

Volex Group plc Transition to International Financial Reporting Standards Supporting document for 2 October 2005 Interim Statement 1. Introduction The consolidated financial statements of Volex Group plc

ROUND(cell or formula, 2)

") There are many ways to set up an amortization table. This document shows how to set up five columns for the payment number, payment, interest, payment applied to the outstanding balance, and the outstanding

There are many ways to set up an amortization table. This document shows how to set up five columns for the payment number, payment, interest, payment applied to the outstanding balance, and the outstanding

Transition to International Financial Reporting Standards

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

A Basic Introduction to the Methodology Used to Determine a Discount Rate

A Basic Introduction to the Methodology Used to Determine a Discount Rate By Dubravka Tosic, Ph.D. The term discount rate is one of the most fundamental, widely used terms in finance and economics. Whether

A Basic Introduction to the Methodology Used to Determine a Discount Rate By Dubravka Tosic, Ph.D. The term discount rate is one of the most fundamental, widely used terms in finance and economics. Whether

CHAPTER 4. FINANCIAL STATEMENTS

CHAPTER 4. FINANCIAL STATEMENTS Accounting standards require statements that show the financial position, earnings, cash flows, and investment (distribution) by (to) owners. These measurements are reported,

CHAPTER 4. FINANCIAL STATEMENTS Accounting standards require statements that show the financial position, earnings, cash flows, and investment (distribution) by (to) owners. These measurements are reported,

Question 1. Marking scheme. F9 ACCA June 2013 Exam: BPP Answers

Question 1 Text references. NPV is covered in Chapter 8 and real or nominal terms in Chapter 9. Financial objectives are covered in Chapter 1. Top tips. Part (b) requires you to explain the different approaches.

Question 1 Text references. NPV is covered in Chapter 8 and real or nominal terms in Chapter 9. Financial objectives are covered in Chapter 1. Top tips. Part (b) requires you to explain the different approaches.

PROJECT PROFILE ON THE ESTABLISHMENT OF ALUMINIUM FRAMES PRODUCING PLANT

Investment Office ANRS PROJECT PROFILE ON THE ESTABLISHMENT OF ALUMINIUM FRAMES PRODUCING PLANT Development Studies Associates (DSA) October 2008 Addis Ababa Table of Contents 1. Executive Summary...1

Investment Office ANRS PROJECT PROFILE ON THE ESTABLISHMENT OF ALUMINIUM FRAMES PRODUCING PLANT Development Studies Associates (DSA) October 2008 Addis Ababa Table of Contents 1. Executive Summary...1

CHAPTER 7 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 7 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 7 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 25. P.25.16 The following data are furnished by the Hypothetical Leasing Ltd (HLL):

:") CHAPTER 25 Solved Problems P.25.16 The following data are furnished by the Hypothetical Leasing Ltd (HLL): Investment cost Rs 500 lakh Primary lease term 5 years Estimated residual value after the primary

CHAPTER 25 Solved Problems P.25.16 The following data are furnished by the Hypothetical Leasing Ltd (HLL): Investment cost Rs 500 lakh Primary lease term 5 years Estimated residual value after the primary