Welcome to the financial reports topic

|

|

|

- Marianna Mason

- 9 years ago

- Views:

Transcription

1 Welcome to the financial reports topic

2 We will explore the effect of standard processes in SAP Business One on Financial Reports: such as the Balance Sheet, the Trial Balance, and the Profit and Loss report. We describe when to use each report and how to interpret typical report data

3 Imagine that you are reviewing the Financial Reports with Maria the company accountant of OEC Computers: Maria mentions that you discussed the influence of Period-End Closing on the Balance Sheet and Profit and Loss reports. This is because you usually issue the Financial Reports for the last day of each financial year or period to get the financial status of the company. You demonstrate the financial reports in SAP Business One. Note that the company usually gets last year s related documents after the end of the financial year or period. Therefore, they also issue the reports for the closing period, during the following period

4 We start by talking about the strong connection between the chart of accounts structure and the different financial reports

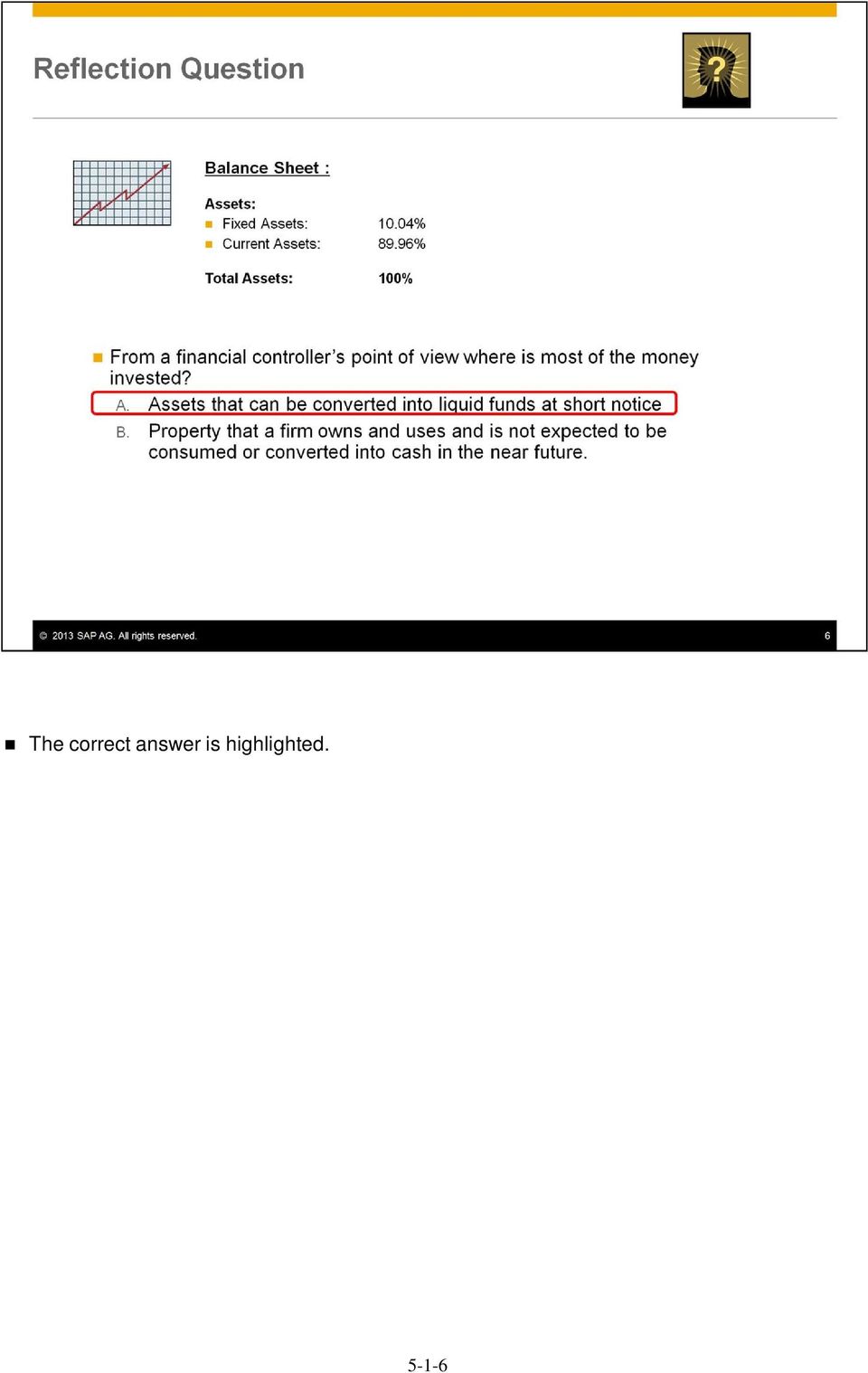

5 At the end of the year you issue the Balance Sheet report. You present the report in a summarized form. For the Assets Drawer you see the following result. From a financial controller s point of view where is most of the money invested? Are they assets that can be converted into liquid funds at short notice or property that a firm owns and uses that is not expected to be consumed or converted into cash in the near future? 5-1-5

6 The correct answer is highlighted

7 Let us go back and examine the Chart of Accounts Structure in association with Financial Reports. This subject is discussed in the Manage the Chart of Accounts topic. Although the chart of accounts will vary according to a company s localization, the structures are very similar around the world. Remember how in the General Ledger you distinguish between Balance Sheet Accounts and Income Statement Accounts, which are also called Profit and Loss Accounts

8 The different reports run on the account balances relevant to a selected date or date range and the reports present them according to their drawer, level and type. For example, the balance sheet report is based on the balance sheet accounts, and similarly the profit and loss statement is based on profit and loss accounts. The trial balance shows all the account types. All these reports are typically issued for the last day of each financial year or period. Let us look closely on each report: 5-1-8

9 All financial reports will appear in the Financials Reports menu which is found in the Financials module 5-1-9

10 The Balance Sheet presents the financial position of a business, the company s value

11 You run the Balance Sheet up to a certain date, that is from the beginning of the company until that date

12 The Balance Sheet presents all Balance Sheet Accounts: Assets, liabilities, and owner s equity

13 When you issue the report, the system runs the report on the account balances of the Balance Sheet accounts and summarizes their values according to the formula: Total Assets equals Total Liabilities plus Equity. In addition, the relative percentage of each balance in the company s assets, liabilities, and equity is presented. The equity section includes the profit period. This amount is calculated while the report is being composed, to represent the summary of the profit and loss of the period

14 Some examples of documents and their related accounts which affect the report are: Accounts receivables and the Sales tax accounts in an A/R Invoice. The bank account in an Outgoing Payment, and The Inventory account in a Goods Receipt PO

15 5-1-15

16 The Trial Balance displays a summary of all accounts and/or business partner balances. The report can comprise a particular cross section of accounts and business partners

17 You can issue the report for a selected posting period or periods

18 The Trial Balance presents all selected accounts (Balance Sheet and Profit and Loss) and business partners master data. If you include business partners in the report, those will be shown at the end, after the list of accounts. The total balance for customers and vendors is represented in the list of accounts, through the control accounts balances

19 When you issue the report, for each account the system presents the total debit and credit amounts, and the ending balance which is calculated as the debit amount minus the credit amount. For the entire report: if the trial balance includes all the accounts in a complete period, the debit and credit side totals must be equal. That is, the total report balance should be zero

20 Here is an example of a document and its related accounts which affect the trial balance report: An A/P Invoice includes the Vendor, the Accounts Payable account, a clearing account or an inventory account, and the Input Tax account

21 5-1-21

22 The Profit and Loss Statement shows the profit (or loss) of your business for the fiscal year or the selected period. It explains the change in the company s value

23 You run the report for a selected period

24 The Profit and Loss Statement presents all the accounts located in the 5 Profit and Loss drawers: Revenues, Cost of Sales, Expenses, Financing and the Other Revenues and Expenses

25 When you run the report, the system calculates the profit or the loss for the fiscal year or the selected period according to this calculation: The balances of the Expense accounts will be subtracted from the balances of the Revenue accounts

26 And here are some examples of documents and their related accounts which affect the report: The income account in an A/R Invoice. And the expense account in an A/P Invoice

27 5-1-27

28 Here is a question for those of you with accounting backgrounds: The Balance Sheet calculation is: Total Assets equals Total Liabilities plus Equity. How is the calculation balanced if the report considers only the Balance Sheet accounts?

29 The profit or loss accumulator is included in the Balance Sheet report and will either increase or decrease the equity on the balance sheet

30 The Statement of Cash Flow is a legal document that is required by many localizations just like the profit and loss and the balance sheet. You need to configure initial settings in the General Settings window and to set defaults for assigning transactions to relevant items in the Statement of Cash Flow. For more details on how to configure the Statement of Cash Flow refer to the on-line help. Note that the Cash Flow is a different report than the Statement of Cash Flow. The Cash Flow report is an internal management tool which is used to help the business manage its cash reserves and to anticipate future periods when it may need to borrow to cover a cash deficit. We will discuss the Cash Flow report in the Cash Management Reports topic

31 Here are some key points to take away: In the General Ledger, you distinguish between Balance Sheet Accounts and Income Statement Accounts, which are also called Profit and Loss Accounts. The different financial reports run on the account balances. The financial reports present the account balances according to a selected date or range and their drawer, level and type

32 The balance sheet report is based on the balance sheet accounts. It presents the company s value using the formula: Total Assets = Total Liabilities + Equity. The report displays the relative percentage of each balance. The profit and loss statement is based on all profit and loss accounts. It presents the profit or loss of your business. The profit or loss for the selected period equals the difference between the balances of the revenue accounts and the balances of the expense accounts. The trial balance is based on all account types. This report presents a summary of all accounts and/or business partner balances. For each account, the report shows the total debit and credit amounts and the ending balance. If the trial balance includes all the accounts in a complete period, the report balance will be zero

33 You have completed the financial reports topic. Thank you for your time

34 5-1-34

Welcome to the course on accounting for the sales and purchasing processes.

Welcome to the course on accounting for the sales and purchasing processes. 1-1 In this topic, we will cover some general accounting conventions and give examples of the automatic journal entries that

Welcome to the course on accounting for the sales and purchasing processes. 1-1 In this topic, we will cover some general accounting conventions and give examples of the automatic journal entries that

Welcome to the internal reconciliation topic. 4-2-1

Welcome to the internal reconciliation topic. 4-2-1 In this topic, we discuss how to utilize the process of internal reconciliation, both system and user reconciliations, in G/L accounts and business partners.

Welcome to the internal reconciliation topic. 4-2-1 In this topic, we discuss how to utilize the process of internal reconciliation, both system and user reconciliations, in G/L accounts and business partners.

Glossary of Accounting Terms

Glossary of Accounting Terms Account - Something to which transactions are assigned. Accounts in MYOB are in one of eight categories: Asset Liability Equity Income Cost of sales Expense Other income Other

Glossary of Accounting Terms Account - Something to which transactions are assigned. Accounts in MYOB are in one of eight categories: Asset Liability Equity Income Cost of sales Expense Other income Other

COMPLETION OF THE ACCOUNTING CYCLE - Closing Entries -

COMPLETION OF THE ACCOUNTING CYCLE - Closing Entries - Worksheet Overview Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance Sheet Account Titles Debit Credit Debit Credit Debit

COMPLETION OF THE ACCOUNTING CYCLE - Closing Entries - Worksheet Overview Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance Sheet Account Titles Debit Credit Debit Credit Debit

Using T Accounts to post journal entries

Using T Accounts to post journal entries Debits Credits This is a T account which is used to analyze posting of double entry accounting Both the right hand column T and the left must have equal totals.

Using T Accounts to post journal entries Debits Credits This is a T account which is used to analyze posting of double entry accounting Both the right hand column T and the left must have equal totals.

Closing the Books Section 7 Accounting 11

Closing the Books At the end of a fiscal year once all the transactions for the entity have been recorded, the revenue and expense accounts must be closed out to a zero balance. These accounts have been

Closing the Books At the end of a fiscal year once all the transactions for the entity have been recorded, the revenue and expense accounts must be closed out to a zero balance. These accounts have been

Accounting Self Study Guide for Staff of Micro Finance Institutions

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 5 Summarizing Changes in Financial Position OBJECTIVES The purpose of this lesson is to show how to summarize the transactions

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 5 Summarizing Changes in Financial Position OBJECTIVES The purpose of this lesson is to show how to summarize the transactions

Basic Accounting Principles

Basic Accounting Principles Basic Accounting Model The basic accounting model represents the relationship between assets (what the company owns), liabilities (what the company owes), and owner s equity

Basic Accounting Principles Basic Accounting Model The basic accounting model represents the relationship between assets (what the company owns), liabilities (what the company owes), and owner s equity

Welcome to the handling payments topic. 2-1

Welcome to the handling payments topic. 2-1 After completing this topic, you will be able to: List the steps of the payment process and perform them in SAP Business One including: Incoming Payments, Outgoing

Welcome to the handling payments topic. 2-1 After completing this topic, you will be able to: List the steps of the payment process and perform them in SAP Business One including: Incoming Payments, Outgoing

Welcome to the topic on purchasing items.

Welcome to the topic on purchasing items. In this topic, we will perform the basic steps for purchasing items. As we go through the process, we will explain the consequences of each process step on inventory

Welcome to the topic on purchasing items. In this topic, we will perform the basic steps for purchasing items. As we go through the process, we will explain the consequences of each process step on inventory

CENTRAL SUSQUEHANNA INTERMEDIATE UNIT Application: Fund Accounting. Account Classes Directory Set Up Learning Guide

CENTRAL SUSQUEHANNA INTERMEDIATE UNIT Application: Fund Accounting Account Classes Directory Set Up Learning Guide 2009 Central Susquehanna Intermediate Unit, USA Table of Contents INTRODUCTION...3 Account

CENTRAL SUSQUEHANNA INTERMEDIATE UNIT Application: Fund Accounting Account Classes Directory Set Up Learning Guide 2009 Central Susquehanna Intermediate Unit, USA Table of Contents INTRODUCTION...3 Account

Changing from Cash to Accrual Accounting

Changing from Cash to Accrual Accounting Contents About Changing the Accounting Method Creating a Client Disb Recov (1210) Account Contacting LexisNexis PCLaw Technical Support Adjusting Disbursements

Changing from Cash to Accrual Accounting Contents About Changing the Accounting Method Creating a Client Disb Recov (1210) Account Contacting LexisNexis PCLaw Technical Support Adjusting Disbursements

Changing from Accrual to Cash Accounting

Changing from Accrual to Cash Accounting Contents About Changing from Accrual to Cash Accounting Description of Accounting Methods Creating a Client Disb Expense (5010) Account Adjusting GST/Vat and Sales

Changing from Accrual to Cash Accounting Contents About Changing from Accrual to Cash Accounting Description of Accounting Methods Creating a Client Disb Expense (5010) Account Adjusting GST/Vat and Sales

Year End Closing 2013 Procedures for Sage 100 ERP. Martin & Associates

Year End Closing 2013 Procedures for Sage 100 ERP Martin & Associates MENU MAS 90 MAS 200 Order of Closing Order Own Closed Module 1 System Wide Backup 2 B/M Bill of materials 3 W/o Work order processing

Year End Closing 2013 Procedures for Sage 100 ERP Martin & Associates MENU MAS 90 MAS 200 Order of Closing Order Own Closed Module 1 System Wide Backup 2 B/M Bill of materials 3 W/o Work order processing

Changing from Accrual to Modified Cash Accounting

Changing from Accrual to Modified Cash Accounting Contents About Changing from Accrual to Modified Cash Accounting Adjusting GST/Vat and Sales Tax Adjusting Accounts Receivable Adjusting Receive Payments

Changing from Accrual to Modified Cash Accounting Contents About Changing from Accrual to Modified Cash Accounting Adjusting GST/Vat and Sales Tax Adjusting Accounts Receivable Adjusting Receive Payments

The following options under the Financial area will be available on the Web as of the February 2016 Release.

The following options under the Financial area will be available on the Web as of the February 2016 Release. Please Note: They will not be going away on PaC. Bank Reconciliation Overview Check Reconciliation

The following options under the Financial area will be available on the Web as of the February 2016 Release. Please Note: They will not be going away on PaC. Bank Reconciliation Overview Check Reconciliation

SAP Note 1825734 Optimization of Financial Processes for China: Account Balance, Aging, and GR/IR

SAP Library Documentation Changes SAP Note 1825734 Optimization of Financial Processes for China: Account Balance, Aging, and GR/IR CUSTOMER April, 2013 (C) SAP AG SAP Note: 1825734 1 Copyright Copyright

SAP Library Documentation Changes SAP Note 1825734 Optimization of Financial Processes for China: Account Balance, Aging, and GR/IR CUSTOMER April, 2013 (C) SAP AG SAP Note: 1825734 1 Copyright Copyright

Reference Document Month-End Closing

Overview Each individual company according to their own business practices establishes month end closing procedures. Typically, a company will create a monthly accounting calendar, which sets the dates

Overview Each individual company according to their own business practices establishes month end closing procedures. Typically, a company will create a monthly accounting calendar, which sets the dates

Amicus Small Firm Accounting: Migrating from Another Accounting System

Amicus Small Firm Accounting: Migrating from Another Accounting System Contents A. Selecting the conversion date... 1 B. Setting up your Firm Settings, accounting method, and users... 1 C. Preparing your

Amicus Small Firm Accounting: Migrating from Another Accounting System Contents A. Selecting the conversion date... 1 B. Setting up your Firm Settings, accounting method, and users... 1 C. Preparing your

Unit 2 The Basic Accounting Cycle

Unit 2 The Basic Accounting Cycle Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Business Transactions and the Accounting Equation Transactions That Affect Assets, Liabilities, and

Unit 2 The Basic Accounting Cycle Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Business Transactions and the Accounting Equation Transactions That Affect Assets, Liabilities, and

SMALL BUSINESS ACCOUNTING. User Guide

SMALL BUSINESS ACCOUNTING User Guide Welcome to QuickBooks We're going to help you get paid, pay others, and see how your business is doing. Use this guide to learn key tasks and get up and running as

SMALL BUSINESS ACCOUNTING User Guide Welcome to QuickBooks We're going to help you get paid, pay others, and see how your business is doing. Use this guide to learn key tasks and get up and running as

TRANSACTIONS ANALYSIS EXAMPLE. Maxwell Partners Medical Diagnostic Services report the following information for 2011, their first year of operations:

TRANSACTIONS ANALYSIS EXAMPLE Maxwell Partners Medical Diagnostic Services report the following information for 2011, their first year of operations: 1. Billings to clients for services provided: $350,000

TRANSACTIONS ANALYSIS EXAMPLE Maxwell Partners Medical Diagnostic Services report the following information for 2011, their first year of operations: 1. Billings to clients for services provided: $350,000

SAP Analytical Fiori Apps for SAP Simple Finance, on-premise edition 1503

SAP Fiori s for SAP Simple Finance, on-premise edition 1503 This document provides you additional information about backend configuration requirement for SAP analytical Fiori s for SAP Simple Finance,

SAP Fiori s for SAP Simple Finance, on-premise edition 1503 This document provides you additional information about backend configuration requirement for SAP analytical Fiori s for SAP Simple Finance,

Welcome to the fixed assets topic. 6-2-1

Welcome to the fixed assets topic. 6-2-1 After completing this topic, you will be able to: Explain the process of managing fixed asset items. Recognize key terms in the Fixed Assets solution. Identify

Welcome to the fixed assets topic. 6-2-1 After completing this topic, you will be able to: Explain the process of managing fixed asset items. Recognize key terms in the Fixed Assets solution. Identify

Welcome to the topic on managing delivery issues with Goods Receipt POs.

Welcome to the topic on managing delivery issues with Goods Receipt POs. In this topic, we will explore how to receive incorrect shipments from a vendor in a goods receipt PO document. Sometimes your supplier

Welcome to the topic on managing delivery issues with Goods Receipt POs. In this topic, we will explore how to receive incorrect shipments from a vendor in a goods receipt PO document. Sometimes your supplier

How To Calculate A Trial Balance For A Company

THE BASIC MODEL The accounting information system is designed to collect and organize data into information that is useful for stakeholders. The Accounting Equation The basic accounting equation is what

THE BASIC MODEL The accounting information system is designed to collect and organize data into information that is useful for stakeholders. The Accounting Equation The basic accounting equation is what

Processing Accounts Payable

Processing Accounts Payable Recurring Payables: Account Source ce Hierarchy Account (Multiple Distribution) Account (overrides Vendor Type Master) Account (overrides Vendor Type Master) ACP.21 Processing

Processing Accounts Payable Recurring Payables: Account Source ce Hierarchy Account (Multiple Distribution) Account (overrides Vendor Type Master) Account (overrides Vendor Type Master) ACP.21 Processing

QuickBooks Interface for Almyta Control System Contents

QuickBooks Interface for Almyta Control System Contents QuickBooks Interface for Almyta Control System... 1 Introduction... 2 Configuring the Interface... 4 Account Description... 6 Export Receipts and

QuickBooks Interface for Almyta Control System Contents QuickBooks Interface for Almyta Control System... 1 Introduction... 2 Configuring the Interface... 4 Account Description... 6 Export Receipts and

Billing Matters Accounting Sunset

WHITE PAPER Billing Matters Accounting Sunset May 2013 Introduction... 2 Key Differences in Process... 2 How to Transition... 3 QuickBooks Setup... 4 What Do I Need... 4 QuickBooks Installation and Creation

WHITE PAPER Billing Matters Accounting Sunset May 2013 Introduction... 2 Key Differences in Process... 2 How to Transition... 3 QuickBooks Setup... 4 What Do I Need... 4 QuickBooks Installation and Creation

Inaugurating your books with QuickBooks is a breeze if you ve just started a business:

Setting Up Existing Records in a New Company File APPENDIX I Inaugurating your books with QuickBooks is a breeze if you ve just started a business: your opening account balances are zero and you build

Setting Up Existing Records in a New Company File APPENDIX I Inaugurating your books with QuickBooks is a breeze if you ve just started a business: your opening account balances are zero and you build

Learn Accounting Understand Business: Course Review Answers

Learn Accounting Understand Business: Course Review Answers 1. What type of accounting measures the activity of the company by looking at economic events regardless of when cash transactions occur? A.

Learn Accounting Understand Business: Course Review Answers 1. What type of accounting measures the activity of the company by looking at economic events regardless of when cash transactions occur? A.

Welcome to the topic on valuation methods.

Welcome to the topic on valuation methods. In this topic, we will look at the three valuation methods used in perpetual inventory in SAP Business One We describe how each valuation method works. Additionally,

Welcome to the topic on valuation methods. In this topic, we will look at the three valuation methods used in perpetual inventory in SAP Business One We describe how each valuation method works. Additionally,

Introductory Governmental Accounting Part I. For State and Local Governments

Introductory Governmental Accounting Part I For State and Local Governments FINANCIAL MANAGEMENT CERTIFICATE TRAINING PROGRAM INTRODUCTORY GOVERNMENTAL ACCOUNTING PART I COURSE OBJECTIVES Upon completion

Introductory Governmental Accounting Part I For State and Local Governments FINANCIAL MANAGEMENT CERTIFICATE TRAINING PROGRAM INTRODUCTORY GOVERNMENTAL ACCOUNTING PART I COURSE OBJECTIVES Upon completion

National Association of Certified Public Bookkeepers. Accounting Basics for QuickBooks Proficiency Test

National Association of Certified Public Bookkeepers Accounting Basics for QuickBooks Proficiency Test Accounting Basics for QuickBooks Proficiency Test Table of Contents Accounting Basics for QuickBooks

National Association of Certified Public Bookkeepers Accounting Basics for QuickBooks Proficiency Test Accounting Basics for QuickBooks Proficiency Test Table of Contents Accounting Basics for QuickBooks

Accounting Notes. Cash - includes money and any medium of exchange that a bank accepts at face value

Asset Accounts: Cash - includes money and any medium of exchange that a bank accepts at face value Accounts Receivable - a record of an oral or implied promise of future cash receipts in exchange for goods

Asset Accounts: Cash - includes money and any medium of exchange that a bank accepts at face value Accounts Receivable - a record of an oral or implied promise of future cash receipts in exchange for goods

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting Lecture Note: Financial Statement Basics, Transaction Recording, and Terminology I. The Financial Reporting Package

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting Lecture Note: Financial Statement Basics, Transaction Recording, and Terminology I. The Financial Reporting Package

Oracle ERP Cloud Period Close Procedures O R A C L E W H I T E P A P E R J U N E 2 0 1 5

Oracle ERP Cloud Period Close Procedures O R A C L E W H I T E P A P E R J U N E 2 0 1 5 Table of Contents Introduction 7 Chapter 1 Period Close Dependencies 8 Chapter 2 Subledger Accounting Overview 9

Oracle ERP Cloud Period Close Procedures O R A C L E W H I T E P A P E R J U N E 2 0 1 5 Table of Contents Introduction 7 Chapter 1 Period Close Dependencies 8 Chapter 2 Subledger Accounting Overview 9

Sage MAS 500 Year-End Processing. Michael Schmitt, BKD December 2011

Sage MAS 500 Year-End Processing Michael Schmitt, BKD December 2011 Welcome / Introductions Michael Schmitt Senior Consultant [email protected] Agenda Welcome / Introductions Order of closing Helpful hints

Sage MAS 500 Year-End Processing Michael Schmitt, BKD December 2011 Welcome / Introductions Michael Schmitt Senior Consultant [email protected] Agenda Welcome / Introductions Order of closing Helpful hints

204 Reports Included with Version 7.0!

204 Reports Included with Version 7.0! Accounts Payable Aged A/P summary by name Aged A/P summary by number Detailed A/P activity by name Detailed A/P activity by number Detailed aged A/P by name Detailed

204 Reports Included with Version 7.0! Accounts Payable Aged A/P summary by name Aged A/P summary by number Detailed A/P activity by name Detailed A/P activity by number Detailed aged A/P by name Detailed

CHAPTER 10 Financial Statements NOTE

NOTE In practice, accruals accounts and prepayments accounts are implied rather than drawn up. It is common for expense accounts to show simply a balance c/d and a balance b/d. The accrual or prepayment

NOTE In practice, accruals accounts and prepayments accounts are implied rather than drawn up. It is common for expense accounts to show simply a balance c/d and a balance b/d. The accrual or prepayment

Chapter 07 - Accounts and Notes Receivable. Chapter Outline

Chapter 07 - Accounts and Receivable I. Accounts Receivable A receivable is an amount due from another party. Accounts Receivable are amounts due from customers for credit sales. A. Recognizing Accounts

Chapter 07 - Accounts and Receivable I. Accounts Receivable A receivable is an amount due from another party. Accounts Receivable are amounts due from customers for credit sales. A. Recognizing Accounts

Introducing the Acowin Accounts Payable Module!

Introducing the Acowin Accounts Payable Module! This quick reference sheet will help you get up and running with the new Acowin Accounts Payable system. For more detailed information about Accounts Payable,

Introducing the Acowin Accounts Payable Module! This quick reference sheet will help you get up and running with the new Acowin Accounts Payable system. For more detailed information about Accounts Payable,

Chapter 7. Special Journals and Subsidiary Ledgers

1 Chapter 7 Special Journals and Subsidiary Ledgers 2 Learning objectives 1. Explain the purpose of special journals 2. Explain the purpose of control accounts and subsidiary ledgers 3. Journalize transactions

1 Chapter 7 Special Journals and Subsidiary Ledgers 2 Learning objectives 1. Explain the purpose of special journals 2. Explain the purpose of control accounts and subsidiary ledgers 3. Journalize transactions

for Sage 100 ERP Accounts Payable Overview Document

for Sage 100 ERP Accounts Payable Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

for Sage 100 ERP Accounts Payable Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

Copyright 2006 Business Management Systems. Web Based ERP/CRM Software

Web Based ERP/CRM Software INTRODUCTION...8 Features... 9 Services... 10 INSTALLATION...11 CUSTOMER FILE...12 Add Customer... 12 Modify Customer... 14 Add Ship To... 15 Modify Ship To... 16 Reports...

Web Based ERP/CRM Software INTRODUCTION...8 Features... 9 Services... 10 INSTALLATION...11 CUSTOMER FILE...12 Add Customer... 12 Modify Customer... 14 Add Ship To... 15 Modify Ship To... 16 Reports...

for Sage 100 ERP General Ledger Overview Document

for Sage 100 ERP General Ledger Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

for Sage 100 ERP General Ledger Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

Assignment 6: Adjusting Journal Entries and

Name: Due Date: December 12, 2011 Score: out of a possible 47 Course value: 7.5% Assignment 6: Adjusting Journal Entries and Worksheets A series of transactions are presented and their journal entries

Name: Due Date: December 12, 2011 Score: out of a possible 47 Course value: 7.5% Assignment 6: Adjusting Journal Entries and Worksheets A series of transactions are presented and their journal entries

ACS 1803 Accounting SUPPLEMENTARY NOTES prepared by E. Kaluzniacky & K. Augustine. Computerized Accounting - The General Ledger System

ACS 1803 Accounting SUPPLEMENTARY NOTES prepared by E. Kaluzniacky & K. Augustine Computerized Accounting - The General Ledger System Every business must keep track of financial information that relates

ACS 1803 Accounting SUPPLEMENTARY NOTES prepared by E. Kaluzniacky & K. Augustine Computerized Accounting - The General Ledger System Every business must keep track of financial information that relates

Year End Closing Procedures for Sage 100 ERP. Martin & Associates

Year End Closing Procedures for Sage 100 ERP 2014 Martin & Associates Period End/Year End FAQs Page 1 of 2 Period End/Year End FAQs Home FAQs & Troubleshooting Show/Hide All Click a question below to

Year End Closing Procedures for Sage 100 ERP 2014 Martin & Associates Period End/Year End FAQs Page 1 of 2 Period End/Year End FAQs Home FAQs & Troubleshooting Show/Hide All Click a question below to

Table of Contents. How to Process Expense Accruals in Umoja. Job Aid. Overview... 2. Objectives... 2. Enterprise Roles... 2

Table of Contents Overview... 2 Objectives... 2 Enterprise Roles... 2 Chapter 1 Process Accrual entry... 2 Chapter 3 Batch program for the Reversal of the Accrual Documents... 13 Chapter 4 How to Reverse

Table of Contents Overview... 2 Objectives... 2 Enterprise Roles... 2 Chapter 1 Process Accrual entry... 2 Chapter 3 Batch program for the Reversal of the Accrual Documents... 13 Chapter 4 How to Reverse

1. Invoice Maintenance

1. Invoice Maintenance Table of Contents Invoice Maintenance... 2 The Invoice tab... 3 The General Ledger Reference Accounts tab... 6 Click on 1. Invoice Maintenance from the Main Menu and the following

1. Invoice Maintenance Table of Contents Invoice Maintenance... 2 The Invoice tab... 3 The General Ledger Reference Accounts tab... 6 Click on 1. Invoice Maintenance from the Main Menu and the following

SAP FI - Automatic Payment Program (Configuration and Run)

") SAP FI - Automatic Payment Program (Configuration and Run) Applies to: SAP ECC 6.0. For more information, visit the Financial Excellence homepage. Summary This document helps you to configure and run Automatic

SAP FI - Automatic Payment Program (Configuration and Run) Applies to: SAP ECC 6.0. For more information, visit the Financial Excellence homepage. Summary This document helps you to configure and run Automatic

Marist College ACCT 203 Financial Accounting Quiz Prep Chapter 3

Marist College ACCT 203 Financial Accounting Quiz Prep Chapter 3 The Accounting Cycle: Capturing Economic Events Peter Rivera August 2011 Disclaimer This Quiz Prep is provided as an outline of the key

Marist College ACCT 203 Financial Accounting Quiz Prep Chapter 3 The Accounting Cycle: Capturing Economic Events Peter Rivera August 2011 Disclaimer This Quiz Prep is provided as an outline of the key

Financial Accounting (FI) Case Study

Case Study") Financial Accounting (FI) Case Study This case study explains an integrated financial accounting process in detail and thus fosters a thorough understanding of each process step and underlying SAP functionality.

Financial Accounting (FI) Case Study This case study explains an integrated financial accounting process in detail and thus fosters a thorough understanding of each process step and underlying SAP functionality.

STUDIO DESIGNER. Accounting 4 Participant

Accounting 4 Participant Thank you for enrolling in Accounting 4 for Studio Designer and Studio Showroom. Please feel free to ask questions as they arise. If we start running short on time, we may hold

Accounting 4 Participant Thank you for enrolling in Accounting 4 for Studio Designer and Studio Showroom. Please feel free to ask questions as they arise. If we start running short on time, we may hold

Coffeyville Community College #07.1543 COURSE SYLLABUS FOR COMPUTERIZED ACCOUNTING. Taasha Viets Instructor

Coffeyville Community College #07.1543 COURSE SYLLABUS FOR COMPUTERIZED ACCOUNTING Taasha Viets Instructor COURSE NUMBER: 07.1543 COURSE TITLE: Computerized Accounting CREDIT HOURS: 3 INSTRUCTOR: OFFICE

Coffeyville Community College #07.1543 COURSE SYLLABUS FOR COMPUTERIZED ACCOUNTING Taasha Viets Instructor COURSE NUMBER: 07.1543 COURSE TITLE: Computerized Accounting CREDIT HOURS: 3 INSTRUCTOR: OFFICE

Glossary of Accounting Terms Peter Baskerville

Glossary of Accounting Terms Peter Baskerville Account for or 'bring to account': An accounting phrase used to describe the recording of a financial transaction that is required under the generally accepted

Glossary of Accounting Terms Peter Baskerville Account for or 'bring to account': An accounting phrase used to describe the recording of a financial transaction that is required under the generally accepted

Cutover Considerations & ERP Migration Best Practices. General Ledger & Inventory

Cutover Considerations & ERP Migration Best Practices 2525 South Lamar Blvd. Suite 10 Austin, TX 78704 512.299.9170 www.cetecerp.com General Ledger & Inventory 1. Cease transactional activity in legacy

Cutover Considerations & ERP Migration Best Practices 2525 South Lamar Blvd. Suite 10 Austin, TX 78704 512.299.9170 www.cetecerp.com General Ledger & Inventory 1. Cease transactional activity in legacy

Managing Company Credit Cards

Managing Company Credit Cards Contents About Managing Company Credit Cards Managing Credit Cards as Vendors Managing Credit Cards as Short Term Liabilities Paying by General Check Without Posting the Statement

Managing Company Credit Cards Contents About Managing Company Credit Cards Managing Credit Cards as Vendors Managing Credit Cards as Short Term Liabilities Paying by General Check Without Posting the Statement

CHAPTER 2 ACCOUNTING FOR TRANSACTIONS

CHAPTER 2 ACCOUNTING FOR TRANSACTIONS Key Terms and Concepts to Know Double entry accounting: Debits and Credits Total debits must always equal total credits Accounting Books: Accounts General Journal

CHAPTER 2 ACCOUNTING FOR TRANSACTIONS Key Terms and Concepts to Know Double entry accounting: Debits and Credits Total debits must always equal total credits Accounting Books: Accounts General Journal

Epicor ERP Epicor ERP Accounts Payable Transaction Hierarchy

Epicor ERP Epicor ERP Accounts Payable Transaction Hierarchy 10 Disclaimer This document is for informational purposes only and is subject to change without notice. This document and its contents, including

Epicor ERP Epicor ERP Accounts Payable Transaction Hierarchy 10 Disclaimer This document is for informational purposes only and is subject to change without notice. This document and its contents, including

Business Intelligence Inquiry Dashboard Job Aid

Business Intelligence Inquiry Dashboard Job Aid DASHBOARD AND DASHBOARD PAGES: DASHBOARD: Inquiry DATA: The data in the Inquiry dashboard is from the Cardinal Financial System General Ledger, Accounts

Business Intelligence Inquiry Dashboard Job Aid DASHBOARD AND DASHBOARD PAGES: DASHBOARD: Inquiry DATA: The data in the Inquiry dashboard is from the Cardinal Financial System General Ledger, Accounts

Objective Evidence. Unit of Measurement. Accounting Period Cycle. Business Entity. Going Concern. Adequate Disclosure. Matching Expenses with Revenue

Accounting Concept: A source document is prepared for each transaction Objective Evidence Accounting Concept: Business transactions are stated in numbers that have common values; that is, using a common

Accounting Concept: A source document is prepared for each transaction Objective Evidence Accounting Concept: Business transactions are stated in numbers that have common values; that is, using a common

In the event of a tie, the score on the last ten questions will be used as a tie-breaker.

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING I 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING I 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

M O N T H E N D / Q U A R T E R L Y / Y E A R E N D C H E C K L I S T S & P R O C E D U R E S ACCOUNTS RECEIVABLE ACCOUNTS PAYABLE

M O N T H E N D / Q U A R T E R L Y / Y E A R E N D C H E C K L I S T S & P R O C E D U R E S ACCOUNTS RECEIVABLE ACCOUNTS PAYABLE PAYROLL GENERAL LEDGER PROCOM SOLUTIONS, INC. OAKLAND CENTER 8980-A ROUTE

M O N T H E N D / Q U A R T E R L Y / Y E A R E N D C H E C K L I S T S & P R O C E D U R E S ACCOUNTS RECEIVABLE ACCOUNTS PAYABLE PAYROLL GENERAL LEDGER PROCOM SOLUTIONS, INC. OAKLAND CENTER 8980-A ROUTE

Welcome to the topic on creating key performance indicators in SAP Business One, release 9.1 version for SAP HANA.

Welcome to the topic on creating key performance indicators in SAP Business One, release 9.1 version for SAP HANA. 1 In this topic, you will learn how to: Use Key Performance Indicators (also known as

Welcome to the topic on creating key performance indicators in SAP Business One, release 9.1 version for SAP HANA. 1 In this topic, you will learn how to: Use Key Performance Indicators (also known as

Navigating within QuickBooks

Navigating within QuickBooks The simplest way to navigate within QuickBooks is to work from the home page. Looking at the home page, you will notice the most common functions within QuickBooks are represented

Navigating within QuickBooks The simplest way to navigate within QuickBooks is to work from the home page. Looking at the home page, you will notice the most common functions within QuickBooks are represented

Welcome to the course on the Bank Statement Processing setup. 2-1

Welcome to the course on the Bank Statement Processing setup. 2-1 In this topic, we install the Bank Statement Processing. We also configure the initial settings for the Bank Statement Processing. 2-2

Welcome to the course on the Bank Statement Processing setup. 2-1 In this topic, we install the Bank Statement Processing. We also configure the initial settings for the Bank Statement Processing. 2-2

Year-End Closing Procedures for Modules in Dynamics GP

Year-End Closing Procedures for Modules in Dynamics GP Page: 1 Welcome! Important Web Seminar Notes Page: 2 To Receive CPE Credit Page: 3 To Receive Group CPE Credit Page: 4 Course Materials Page: 5 McGladrey

Year-End Closing Procedures for Modules in Dynamics GP Page: 1 Welcome! Important Web Seminar Notes Page: 2 To Receive CPE Credit Page: 3 To Receive Group CPE Credit Page: 4 Course Materials Page: 5 McGladrey

Chapter 8. Describe an effective accounting information system. Learning Objectives. Objective 1. Accounting Information Systems

PowerPoint to accompany Chapter 8 Accounting Information Systems Learning Objectives 1. Describe an effective accounting information system 2. Understand both computerised and manual accounting systems

PowerPoint to accompany Chapter 8 Accounting Information Systems Learning Objectives 1. Describe an effective accounting information system 2. Understand both computerised and manual accounting systems

MUNIS HOW TO UTILIZE PURCHASE ORDER INQUIRY

MUNIS HOW TO UTILIZE PURCHASE ORDER INQUIRY Implementation Tyler Technologies, Inc. MUNIS Division 370 U.S. Route One Falmouth, Maine 04105 Web: www.tyler-munis.com HOW TO UTILIZE PURCHASE ORDER INQUIRY

MUNIS HOW TO UTILIZE PURCHASE ORDER INQUIRY Implementation Tyler Technologies, Inc. MUNIS Division 370 U.S. Route One Falmouth, Maine 04105 Web: www.tyler-munis.com HOW TO UTILIZE PURCHASE ORDER INQUIRY

Ratios from the Statement of Financial Position

For The Year Ended 31 March 2007 Ratios from the Statement of Financial Position Profitability Ratios Return on Sales Ratio (%) This is the difference between what a business takes in and what it spends

For The Year Ended 31 March 2007 Ratios from the Statement of Financial Position Profitability Ratios Return on Sales Ratio (%) This is the difference between what a business takes in and what it spends

Unit 2 The Basic Accounting Cycle

Unit 2 The Basic Accounting Cycle Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Business Transactions and the Accounting Equation Transactions That Affect Assets, Liabilities, and

Unit 2 The Basic Accounting Cycle Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Business Transactions and the Accounting Equation Transactions That Affect Assets, Liabilities, and

Chapter 4. Completing the accounting cycle. Appendix 4A: Reversing entries

1 Chapter 4 Completing the accounting cycle Appendix 4A: Reversing entries 2 Learning objective 1. Prepare reversing entries and describe their purpose 3 Reversing entries Reversing entries are optional

1 Chapter 4 Completing the accounting cycle Appendix 4A: Reversing entries 2 Learning objective 1. Prepare reversing entries and describe their purpose 3 Reversing entries Reversing entries are optional

Completing the Accounting Cycle

C H A P T E R 4 Completing the Accounting Cycle Financial Accounting 14e Warren Reeve Duchac human/istock/360/getty Images Flow of Accounting Information (slide 1 of 5) End-of-Period Spreadsheet (Work

C H A P T E R 4 Completing the Accounting Cycle Financial Accounting 14e Warren Reeve Duchac human/istock/360/getty Images Flow of Accounting Information (slide 1 of 5) End-of-Period Spreadsheet (Work

EasyPC Training. Accounting Basics

EasyPC Training Accounting Basics Contents Accounting Basics... 3 The Accounting Equation... 3 Assets... 3 Liabilities... 3 Owner s Equity... 3 The Balance Sheet... 5 Double Entry Bookkeeping... 6 Ledger

EasyPC Training Accounting Basics Contents Accounting Basics... 3 The Accounting Equation... 3 Assets... 3 Liabilities... 3 Owner s Equity... 3 The Balance Sheet... 5 Double Entry Bookkeeping... 6 Ledger

Business Intelligence Accounts Payable Dashboard Job Aid

Business Intelligence Accounts Payable Dashboard Job Aid DASHBOARD AND DASHBOARD PAGES: DASHBOARD: Accounts Payable The data in the Accounts Payable dashboard is from the Cardinal Financial System Accounts

Business Intelligence Accounts Payable Dashboard Job Aid DASHBOARD AND DASHBOARD PAGES: DASHBOARD: Accounts Payable The data in the Accounts Payable dashboard is from the Cardinal Financial System Accounts

Accounting 101 you don t have to be an accountant to run MYOB Your Daily Lives Cash vs. Accrual Accounting

MYOB US, Inc. April 2002 Accounting 101 Like all small business owners, you went into business with a dream: to sell your unique product or services and make a living for you, your family, and your employees.

MYOB US, Inc. April 2002 Accounting 101 Like all small business owners, you went into business with a dream: to sell your unique product or services and make a living for you, your family, and your employees.

Preparing Financial Statements

Carroll_CH03_023-040.qxd 8/10/06 4:37 PM Page 23 CHAPTER 3 Preparing Financial Statements OBJECTIVES F After reading this chapter, the student should be able to: 1. Describe the general process by which

Carroll_CH03_023-040.qxd 8/10/06 4:37 PM Page 23 CHAPTER 3 Preparing Financial Statements OBJECTIVES F After reading this chapter, the student should be able to: 1. Describe the general process by which

CONSOLIDATIONS. Either the full amount or a specified percentage of a particular company's financial information

CONSOLIDATIONS Consolidation means combining the financial statements of two or more separate companies into consolidated financial statements. In the program, each individual company involved in a consolidation

CONSOLIDATIONS Consolidation means combining the financial statements of two or more separate companies into consolidated financial statements. In the program, each individual company involved in a consolidation

for Sage 100 ERP Purchase Order Overview Document

for Sage 100 ERP Purchase Order Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

for Sage 100 ERP Purchase Order Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

Advanced Accounting. Chapter 4: Financial Reporting for a Departmentalized Business

Advanced Accounting Chapter 4: Financial Reporting for a Departmentalized Business Financial statements are used to summarize financial info and then are used to evaluate the financial position and progress

Advanced Accounting Chapter 4: Financial Reporting for a Departmentalized Business Financial statements are used to summarize financial info and then are used to evaluate the financial position and progress

Statement of Cash Flows

HOSP 2110 (Management Acct) Learning Centre Statement of Cash Flows The Statement of Cash Flows (or cash flow statement) is one of the main financial statements used by investors. It shows the cash generated

HOSP 2110 (Management Acct) Learning Centre Statement of Cash Flows The Statement of Cash Flows (or cash flow statement) is one of the main financial statements used by investors. It shows the cash generated

Collaborative SIG: SLA Accounting in R12: Procure to Pay Process

Collaborative SIG: SLA Accounting in R12: Procure to Pay Process Mohan Iyer Principal Consultant FSCP Solutions Inc [email protected] September 22 nd, 2011 Agenda About the Presenter Procure to Pay

Collaborative SIG: SLA Accounting in R12: Procure to Pay Process Mohan Iyer Principal Consultant FSCP Solutions Inc [email protected] September 22 nd, 2011 Agenda About the Presenter Procure to Pay

Accrual Accounting Process

Accrual Accounting Process 15.501 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology Feb 17/18, 2004 1 An accountant s functions include Classifying

Accrual Accounting Process 15.501 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology Feb 17/18, 2004 1 An accountant s functions include Classifying

Accounting I & Accounting II

Accounting I & Accounting II 2011 User Conference Convergence: Better Together Configuring the Tigerpaw Accounting Interface The Configure Accounting dialog box is one of the main areas setup in Tigerpaw

Accounting I & Accounting II 2011 User Conference Convergence: Better Together Configuring the Tigerpaw Accounting Interface The Configure Accounting dialog box is one of the main areas setup in Tigerpaw

Automatic Journal Entries

WRITE-UP CS Automatic Journal Entries version 2008.x.x TL20189 (01/02/09) Copyright Information Text copyright 1998 2008 by Thomson Reuters/Tax & Accounting. All rights reserved. Video display images copyright

WRITE-UP CS Automatic Journal Entries version 2008.x.x TL20189 (01/02/09) Copyright Information Text copyright 1998 2008 by Thomson Reuters/Tax & Accounting. All rights reserved. Video display images copyright

Financial Basics for Non-Financial Managers

Financial Basics for Non-Financial Managers Presented By: Amy Gil of the Jessup Group [email protected] May 13, 2015 Discussion Items Role of finance in organization Basic Accounting Concepts Accounting

Financial Basics for Non-Financial Managers Presented By: Amy Gil of the Jessup Group [email protected] May 13, 2015 Discussion Items Role of finance in organization Basic Accounting Concepts Accounting

Chapter 14. 1 Copyright 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Chapter 14 1 Identify the purposes of the statement of cash flows Distinguish among operating, investing, and financing cash flows Prepare the statement of cash flows by the indirect method Identify noncash

Chapter 14 1 Identify the purposes of the statement of cash flows Distinguish among operating, investing, and financing cash flows Prepare the statement of cash flows by the indirect method Identify noncash

Century 21 Accounting, 8e General Journal Chapter Outlines

Century 21 Accounting, 8e General Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Century 21 Accounting, 8e General Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

There are two basic types of cost accounting systems:

CHAPTER 2 JOB ORDER COSTING Managerial Accounting, Fourth Edition 2-1 Cost Accounting Systems There are two basic types of cost accounting systems: 2-2 LO 1: Explain the characteristics and purposes of

CHAPTER 2 JOB ORDER COSTING Managerial Accounting, Fourth Edition 2-1 Cost Accounting Systems There are two basic types of cost accounting systems: 2-2 LO 1: Explain the characteristics and purposes of

Learning Objectives: Quick answer key: Question # Multiple Choice True/False. 14.1 Describe the important of accounting and financial information.

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

Credit Card Accounts

Table Of Contents Credit Card Register Accounts... 3 Creating a Credit Card Account... 3 Making Payments Using Your Credit Card Account... 4 Making Payments to Your Credit Card Account or Another Register

Table Of Contents Credit Card Register Accounts... 3 Creating a Credit Card Account... 3 Making Payments Using Your Credit Card Account... 4 Making Payments to Your Credit Card Account or Another Register

Choosing the Correct GL Code

Table of Contents Table of Contents 1 Basic GL Information 2 Capitalizing Assets 3 4-10 Category Items List 5 OSF OEC 6 Grants GL Account to Budgetary Category 7 Example 8 General Ledger Fund Listing 9-10

Table of Contents Table of Contents 1 Basic GL Information 2 Capitalizing Assets 3 4-10 Category Items List 5 OSF OEC 6 Grants GL Account to Budgetary Category 7 Example 8 General Ledger Fund Listing 9-10

A - D. Account ChartField

A - D Account ChartField The Account ChartField is used to specify the balance sheet account or operating account on financial transactions. Each ChartField is assigned an account type which indicates

A - D Account ChartField The Account ChartField is used to specify the balance sheet account or operating account on financial transactions. Each ChartField is assigned an account type which indicates

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions