Validating Market Risk Models: A Practical Approach

|

|

|

- Richard Beasley

- 9 years ago

- Views:

Transcription

1 Validating Market Risk Models: A Practical Approach Doug Gardner Wells Fargo November 2010 The views expressed in this presentation are those of the author and do not necessarily reflect the position of Wells Fargo. The examples, methods, approaches, and explanations are intended to reflect perceived best practices and do not necessarily represent methods or approaches as implemented or used by Wells Fargo.

2 Outline Market risk models Components of market risk models Validation of market risk model components Risk factor identification and distributions Pricing models Statistical measures Validation tips Page 2

3 Market Risk Definitions Market risk The risk of an increase or decrease in the market price of a financial instrument or portfolio May be due to changes in stock prices, interest rates, credit spreads, foreign exchange rates, commodity prices, implied volatilities Regulatory classification General market risk: due to systemic or general market factors (e.g., FX rates, equity indices, benchmark prices) Specific risk: due to idiosyncratic factors unique to a financial instrument Incremental risk: market risk arising from credit-related factors (rating downgrades or defaults) Page 3

4 Market Risk Measurement Predict the distribution of possible change in value of an instrument over a given time horizon Summary statistics Moments: volatility (standard deviation), skewness, kurtosis Value at Risk (VaR) the maximum amount that can be lost over a given time horizon with a specified degree of confidence Banks calculate regulatory capital based on a 99% confidence level over a 10 day time horizon CVaR (aka Expected Shortfall, Tail VaR) Expected loss in the distribution tail (e.g., in worst 5% of outcomes) Unlike VaR, CVAR is a coherent risk measure Page 4

Expected loss in the distribution tail (e.g.")

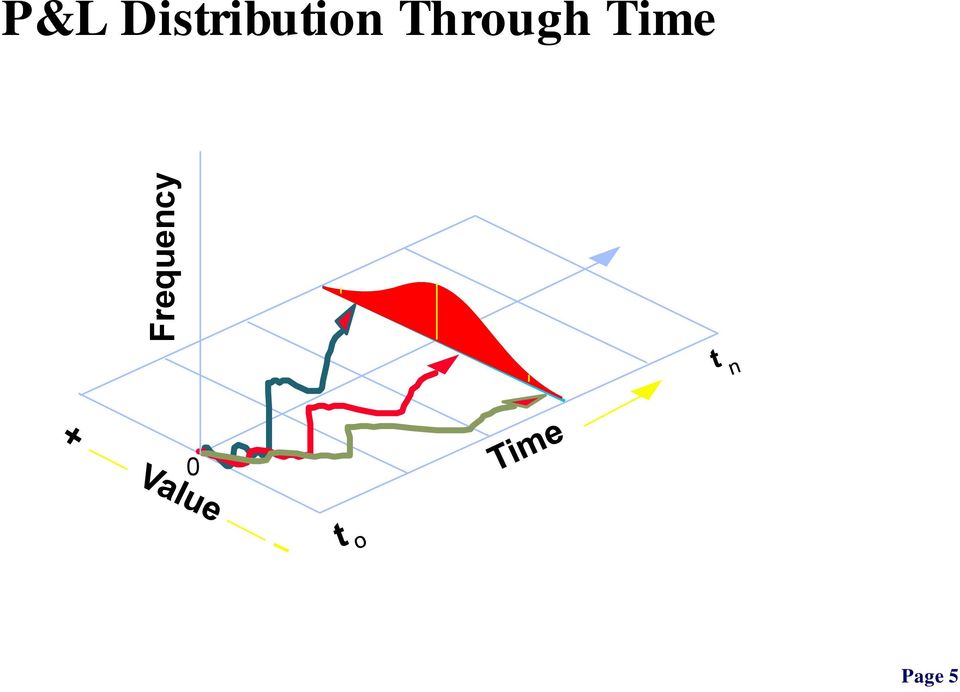

5 Frequency P&L Distribution Through Time 0 Page 5

6 Market Risk Models Model components Risk factor multivariate distribution (more generally, process) Instrument price distribution (as function of risk factors) Risk factor distributions Parametric (e.g., multivariate normal) Nonparametric (e.g., historical simulation) Semi-parametric (e.g., historical simulation with volatility updating) Instrument pricing Taylor series (e.g., delta, delta/partial gamma, delta/full gamma) Full revaluation Pricing grids Page 6

Semi-parametric (e.g.")

7 Risk Factor Selection RF selection is portfolio dependent Requires in-depth knowledge of portfolio and products Basis risk - modeled/ignored? Bucketing for curves/surfaces Risk reports may reveal portfolio concentrations (e.g., large OTM positions), and hence suggest the need for additional granularity Proxies New products often lack relevant historical data A particular problem for historical stress scenarios and stressed VaR General market risk versus specific risk Which risk factors where? Page 7

8 Risk Factor Properties Distributional assumption: Normal/lognormal/other an issue even with historical simulation Volatility clustering Fat tails leptokurtosis Time-varying correlations (?) Other considerations Frequency of risk factor updates (daily/monthly/quarterly) Curve/surface interpolation and extrapolation Dealing with poor/missing data (particular issue with specific risk) Overlapping intervals Observations no longer independent Sun et al. (2009) examine impact on price change percentiles Page 8

Overlapping intervals Observations no longer independent")

9 Pricing Model Validation Pricing models used for market risk purposes should be validated to similar standard as models used for marking Theoretical review Review of key assumptions Comparison to alternative models (including models used for marking if different) Implementation review Page 9

Implementation")

10 Backtesting Pricing Models Compare model predicted P&L (using actual risk factor changes) to actual P&L Clean (frozen portfolio, exclude fee income and ad-hoc adjustments) versus dirty (i.e., actual) P&L Significant differences can reveal a number of possible issues Model implementation errors Missing risk factors Inadequate pricing model approximations (portfolio nonlinearity) Lack of granularity in curve bucketing For general market risk, some differences are to be expected for instruments subject to specific risk Page 10

11 Backtesting VaR: Unconditional Coverage Kupiec (1995) Coverage test: compare actual VaR exceptions to predicted Example: P&L is expected to exceed a 95% VaR 5 days out of 100 (on average) Under the null hypothesis (model is correctly specified), the number of exceptions follows a binomial distribution (which can be approximated by a normal distribution for large number of observations) Basis for regulatory backtesting (99% 1-day VaR) Page 11

Basis for regulatory backtesting (99% 1-day VaR) Page 11")

12 Hypothesis Testing Model Decision Correct Incorrect Accept OK Type 2 error Reject Type 1 error OK Type 1 error : reject a correct model Type 2 error: accept an incorrect model Page 12

13 Regulatory Exception Zones Zone Exceptions Penalty K Type 1 Error Green Yellow % % % % % Red % Exceptions based on 99% 1-day VaR over past year Within the yellow zone, regulators apply discretion Page 13

14 Type 1/2 Error Tradeoffs Ideally, a test would have both low type 1 (reject a correct model) and type 2 (accept an incorrect model) errors In practice, need to balance these through choice of exception threshold: to reduce type 2 errors, must increase type 1 errors Regulators are most concerned about type 2 errors 99% confidence level produces an unreliable test due to the relative paucity of exceptions Using a lower confidence level (say 95%) produces a more reliable test (lower type 2 error rate for a given type 1 error rate), and thus can be a useful supplement A number of institutions entered the red zone in 2008 (RISK, Jan-2010) Page 14

, and thus can be a useful supplement A number of institutions entered the red zone in 2008 (RISK,")

15 Conditional Coverage Testing Exceptions should be serially independent (i.e., not bunch ) The model should have the correct conditional coverage as well as the correct unconditional coverage Christoffersen (1998) proposes a test that tests individually for unconditional coverage and independence Lack of independence may suggest a model that fails to properly account for volatility clustering, or a poorly modeled portfolio with time-varying risk profile

16 Testing the Entire Distribution Rosenblatt transformation: Let X(t) = F(Y(t)) where F is the model-predicted P&L cdf, Y(t) is the P&L on day t X(t) should be uniformly distributed and iid May examine this graphically as well as formally test statistically Berkowitz (2001) suggests using Z(t) = N(X(t)) where N is the inverse of the standard normal Z(t) should then be distributed normally and iid May then apply standard tests of normality May also construct a test that focuses only on the tail of the distribution rather than the entire distribution

17 Multivariate Coverage Testing Perignon and Smith (2008) suggest a multivariate generalization of the unconditional coverage test of Kupiec First select a set of coverage probabilities and associated K buckets (e.g., 0-1%, 1-5%, 5-10%, %) Compare the expected frequency of observations X(t) falling in each bucket (1%, 4%, 5%, 90% in this example) to the observed frequency The associated test statistic is chi-square distributed with K-1 degrees of freedom This procedure is commonly applied in other areas including the evaluation of the calibration of credit scoring models (Hosmer- Lemeshow 2000)

Compare the expected frequency of observations X(t) falling in each bucket (1%, 4%, 5%, 90% in this example) to the")

18 Validation Tips Model validation, like model building, must start with a strong understanding of the phenomenon being modeled Build a strong relationship with trading, finance and risk oversight Validate based on model usage For example, evaluate model performance in stress scenarios if this is a possible use Use multiple methods Examine each key model component individually, as well as together Use a full range of tests Evaluate model performance at multiple levels (product, desk, trading area, firm)

Contents. List of Figures. List of Tables. List of Examples. Preface to Volume IV

Contents List of Figures List of Tables List of Examples Foreword Preface to Volume IV xiii xvi xxi xxv xxix IV.1 Value at Risk and Other Risk Metrics 1 IV.1.1 Introduction 1 IV.1.2 An Overview of Market

Contents List of Figures List of Tables List of Examples Foreword Preface to Volume IV xiii xvi xxi xxv xxix IV.1 Value at Risk and Other Risk Metrics 1 IV.1.1 Introduction 1 IV.1.2 An Overview of Market

CALYPSO ENTERPRISE RISK SYSTEM

1 CALYPSO ENTERPRISE RISK SYSTEM Dr Philip Symes Introduction 2 Calypso's Enterprise Risk Service (ERS) is part of their Front-to-Back software system. Calypso ERS provides the Middle Office risk function.

1 CALYPSO ENTERPRISE RISK SYSTEM Dr Philip Symes Introduction 2 Calypso's Enterprise Risk Service (ERS) is part of their Front-to-Back software system. Calypso ERS provides the Middle Office risk function.

Dr Christine Brown University of Melbourne

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

CONTENTS. List of Figures List of Tables. List of Abbreviations

List of Figures List of Tables Preface List of Abbreviations xiv xvi xviii xx 1 Introduction to Value at Risk (VaR) 1 1.1 Economics underlying VaR measurement 2 1.1.1 What is VaR? 4 1.1.2 Calculating VaR

List of Figures List of Tables Preface List of Abbreviations xiv xvi xviii xx 1 Introduction to Value at Risk (VaR) 1 1.1 Economics underlying VaR measurement 2 1.1.1 What is VaR? 4 1.1.2 Calculating VaR

The Best of Both Worlds:

The Best of Both Worlds: A Hybrid Approach to Calculating Value at Risk Jacob Boudoukh 1, Matthew Richardson and Robert F. Whitelaw Stern School of Business, NYU The hybrid approach combines the two most

The Best of Both Worlds: A Hybrid Approach to Calculating Value at Risk Jacob Boudoukh 1, Matthew Richardson and Robert F. Whitelaw Stern School of Business, NYU The hybrid approach combines the two most

Calculating VaR. Capital Market Risk Advisors CMRA

Calculating VaR Capital Market Risk Advisors How is VAR Calculated? Sensitivity Estimate Models - use sensitivity factors such as duration to estimate the change in value of the portfolio to changes in

Calculating VaR Capital Market Risk Advisors How is VAR Calculated? Sensitivity Estimate Models - use sensitivity factors such as duration to estimate the change in value of the portfolio to changes in

CITIGROUP INC. BASEL II.5 MARKET RISK DISCLOSURES AS OF AND FOR THE PERIOD ENDED MARCH 31, 2013

CITIGROUP INC. BASEL II.5 MARKET RISK DISCLOSURES AS OF AND FOR THE PERIOD ENDED MARCH 31, 2013 DATED AS OF MAY 15, 2013 Table of Contents Qualitative Disclosures Basis of Preparation and Review... 3 Risk

CITIGROUP INC. BASEL II.5 MARKET RISK DISCLOSURES AS OF AND FOR THE PERIOD ENDED MARCH 31, 2013 DATED AS OF MAY 15, 2013 Table of Contents Qualitative Disclosures Basis of Preparation and Review... 3 Risk

An introduction to Value-at-Risk Learning Curve September 2003

An introduction to Value-at-Risk Learning Curve September 2003 Value-at-Risk The introduction of Value-at-Risk (VaR) as an accepted methodology for quantifying market risk is part of the evolution of risk

An introduction to Value-at-Risk Learning Curve September 2003 Value-at-Risk The introduction of Value-at-Risk (VaR) as an accepted methodology for quantifying market risk is part of the evolution of risk

How To Test For Significance On A Data Set

Non-Parametric Univariate Tests: 1 Sample Sign Test 1 1 SAMPLE SIGN TEST A non-parametric equivalent of the 1 SAMPLE T-TEST. ASSUMPTIONS: Data is non-normally distributed, even after log transforming.

Non-Parametric Univariate Tests: 1 Sample Sign Test 1 1 SAMPLE SIGN TEST A non-parametric equivalent of the 1 SAMPLE T-TEST. ASSUMPTIONS: Data is non-normally distributed, even after log transforming.

II. DISTRIBUTIONS distribution normal distribution. standard scores

Appendix D Basic Measurement And Statistics The following information was developed by Steven Rothke, PhD, Department of Psychology, Rehabilitation Institute of Chicago (RIC) and expanded by Mary F. Schmidt,

Appendix D Basic Measurement And Statistics The following information was developed by Steven Rothke, PhD, Department of Psychology, Rehabilitation Institute of Chicago (RIC) and expanded by Mary F. Schmidt,

Effective Techniques for Stress Testing and Scenario Analysis

Effective Techniques for Stress Testing and Scenario Analysis Om P. Arya Federal Reserve Bank of New York November 4 th, 2008 Mumbai, India The views expressed here are not necessarily of the Federal Reserve

Effective Techniques for Stress Testing and Scenario Analysis Om P. Arya Federal Reserve Bank of New York November 4 th, 2008 Mumbai, India The views expressed here are not necessarily of the Federal Reserve

The Ten Great Challenges of Risk Management. Carl Batlin* and Barry Schachter** March, 2000

The Ten Great Challenges of Risk Management Carl Batlin* and Barry Schachter** March, 2000 *Carl Batlin has been the head of Quantitative Research at Chase Manhattan Bank and its predecessor banks, Chemical

The Ten Great Challenges of Risk Management Carl Batlin* and Barry Schachter** March, 2000 *Carl Batlin has been the head of Quantitative Research at Chase Manhattan Bank and its predecessor banks, Chemical

Stress Testing Trading Desks

Stress Testing Trading Desks Michael Sullivan Office of the Comptroller of the Currency Paper presented at the Expert Forum on Advanced Techniques on Stress Testing: Applications for Supervisors Hosted

Stress Testing Trading Desks Michael Sullivan Office of the Comptroller of the Currency Paper presented at the Expert Forum on Advanced Techniques on Stress Testing: Applications for Supervisors Hosted

Quantitative Methods for Finance

Quantitative Methods for Finance Module 1: The Time Value of Money 1 Learning how to interpret interest rates as required rates of return, discount rates, or opportunity costs. 2 Learning how to explain

Quantitative Methods for Finance Module 1: The Time Value of Money 1 Learning how to interpret interest rates as required rates of return, discount rates, or opportunity costs. 2 Learning how to explain

Risk Management for Fixed Income Portfolios

Risk Management for Fixed Income Portfolios Strategic Risk Management for Credit Suisse Private Banking & Wealth Management Products (SRM PB & WM) August 2014 1 SRM PB & WM Products Risk Management CRO

Risk Management for Fixed Income Portfolios Strategic Risk Management for Credit Suisse Private Banking & Wealth Management Products (SRM PB & WM) August 2014 1 SRM PB & WM Products Risk Management CRO

Financial Assets Behaving Badly The Case of High Yield Bonds. Chris Kantos Newport Seminar June 2013

Financial Assets Behaving Badly The Case of High Yield Bonds Chris Kantos Newport Seminar June 2013 Main Concepts for Today The most common metric of financial asset risk is the volatility or standard

Financial Assets Behaving Badly The Case of High Yield Bonds Chris Kantos Newport Seminar June 2013 Main Concepts for Today The most common metric of financial asset risk is the volatility or standard

Fundamental Review of the Trading Book: A Revised Market Risk Framework Second Consultative Document by the Basel Committee on Banking Supervision

An Insight Paper by CRISIL GR&A ANALYSIS Fundamental Review of the Trading Book: A Revised Market Risk Framework Second Consultative Document by the Basel Committee on Banking Supervision The Basel Committee

An Insight Paper by CRISIL GR&A ANALYSIS Fundamental Review of the Trading Book: A Revised Market Risk Framework Second Consultative Document by the Basel Committee on Banking Supervision The Basel Committee

Jornadas Economicas del Banco de Guatemala. Managing Market Risk. Max Silberberg

Managing Market Risk Max Silberberg Defining Market Risk Market risk is exposure to an adverse change in value of financial instrument caused by movements in market variables. Market risk exposures are

Managing Market Risk Max Silberberg Defining Market Risk Market risk is exposure to an adverse change in value of financial instrument caused by movements in market variables. Market risk exposures are

Regulatory and Economic Capital

Regulatory and Economic Capital Measurement and Management Swati Agiwal November 18, 2011 What is Economic Capital? Capital available to the bank to absorb losses to stay solvent Probability Unexpected

Regulatory and Economic Capital Measurement and Management Swati Agiwal November 18, 2011 What is Economic Capital? Capital available to the bank to absorb losses to stay solvent Probability Unexpected

Parametric Value at Risk

April 2013 by Stef Dekker Abstract With Value at Risk modelling growing ever more complex we look back at the basics: parametric value at risk. By means of simulation we show that the parametric framework

April 2013 by Stef Dekker Abstract With Value at Risk modelling growing ever more complex we look back at the basics: parametric value at risk. By means of simulation we show that the parametric framework

Risk Based Capital Guidelines; Market Risk. The Bank of New York Mellon Corporation Market Risk Disclosures. As of December 31, 2013

Risk Based Capital Guidelines; Market Risk The Bank of New York Mellon Corporation Market Risk Disclosures As of December 31, 2013 1 Basel II.5 Market Risk Annual Disclosure Introduction Since January

Risk Based Capital Guidelines; Market Risk The Bank of New York Mellon Corporation Market Risk Disclosures As of December 31, 2013 1 Basel II.5 Market Risk Annual Disclosure Introduction Since January

Northern Trust Corporation

Northern Trust Corporation Market Risk Disclosures June 30, 2014 Market Risk Disclosures Effective January 1, 2013, Northern Trust Corporation (Northern Trust) adopted revised risk based capital guidelines

Northern Trust Corporation Market Risk Disclosures June 30, 2014 Market Risk Disclosures Effective January 1, 2013, Northern Trust Corporation (Northern Trust) adopted revised risk based capital guidelines

APPROACHES TO COMPUTING VALUE- AT-RISK FOR EQUITY PORTFOLIOS

APPROACHES TO COMPUTING VALUE- AT-RISK FOR EQUITY PORTFOLIOS (Team 2b) Xiaomeng Zhang, Jiajing Xu, Derek Lim MS&E 444, Spring 2012 Instructor: Prof. Kay Giesecke I. Introduction Financial risks can be

APPROACHES TO COMPUTING VALUE- AT-RISK FOR EQUITY PORTFOLIOS (Team 2b) Xiaomeng Zhang, Jiajing Xu, Derek Lim MS&E 444, Spring 2012 Instructor: Prof. Kay Giesecke I. Introduction Financial risks can be

How To Know Market Risk

Chapter 6 Market Risk for Single Trading Positions Market risk is the risk that the market value of trading positions will be adversely influenced by changes in prices and/or interest rates. For banks,

Chapter 6 Market Risk for Single Trading Positions Market risk is the risk that the market value of trading positions will be adversely influenced by changes in prices and/or interest rates. For banks,

Basel Committee on Banking Supervision. Explanatory note on the revised minimum capital requirements for market risk

Basel Committee on Banking Supervision Explanatory note on the revised minimum capital requirements for market risk January 2016 This publication is available on the BIS website (www.bis.org). Bank for

Basel Committee on Banking Supervision Explanatory note on the revised minimum capital requirements for market risk January 2016 This publication is available on the BIS website (www.bis.org). Bank for

Chapter 3 RANDOM VARIATE GENERATION

Chapter 3 RANDOM VARIATE GENERATION In order to do a Monte Carlo simulation either by hand or by computer, techniques must be developed for generating values of random variables having known distributions.

Chapter 3 RANDOM VARIATE GENERATION In order to do a Monte Carlo simulation either by hand or by computer, techniques must be developed for generating values of random variables having known distributions.

Risk Based Capital Guidelines; Market Risk. The Bank of New York Mellon Corporation Market Risk Disclosures. As of June 30, 2014

Risk Based Capital Guidelines; Market Risk The Bank of New York Mellon Corporation Market Risk Disclosures As of June 30, 2014 1 Basel II.5 Market Risk Quarterly Disclosure Introduction Since January 1,

Risk Based Capital Guidelines; Market Risk The Bank of New York Mellon Corporation Market Risk Disclosures As of June 30, 2014 1 Basel II.5 Market Risk Quarterly Disclosure Introduction Since January 1,

Discussion Paper On the validation and review of Credit Rating Agencies methodologies

Discussion Paper On the validation and review of Credit Rating Agencies methodologies 17 November 2015 ESMA/2015/1735 Responding to this paper The European Securities and Markets Authority (ESMA) invites

Discussion Paper On the validation and review of Credit Rating Agencies methodologies 17 November 2015 ESMA/2015/1735 Responding to this paper The European Securities and Markets Authority (ESMA) invites

COMMITTEE OF EUROPEAN SECURITIES REGULATORS. Date: December 2009 Ref.: CESR/09-1026

COMMITTEE OF EUROPEAN SECURITIES REGULATORS Date: December 009 Ref.: CESR/09-06 Annex to CESR s technical advice on the level measures related to the format and content of Key Information Document disclosures

COMMITTEE OF EUROPEAN SECURITIES REGULATORS Date: December 009 Ref.: CESR/09-06 Annex to CESR s technical advice on the level measures related to the format and content of Key Information Document disclosures

Third Edition. Philippe Jorion GARP. WILEY John Wiley & Sons, Inc.

2008 AGI-Information Management Consultants May be used for personal purporses only or by libraries associated to dandelon.com network. Third Edition Philippe Jorion GARP WILEY John Wiley & Sons, Inc.

2008 AGI-Information Management Consultants May be used for personal purporses only or by libraries associated to dandelon.com network. Third Edition Philippe Jorion GARP WILEY John Wiley & Sons, Inc.

HYPOTHESIS TESTING: POWER OF THE TEST

HYPOTHESIS TESTING: POWER OF THE TEST The first 6 steps of the 9-step test of hypothesis are called "the test". These steps are not dependent on the observed data values. When planning a research project,

HYPOTHESIS TESTING: POWER OF THE TEST The first 6 steps of the 9-step test of hypothesis are called "the test". These steps are not dependent on the observed data values. When planning a research project,

Measuring Exchange Rate Fluctuations Risk Using the Value-at-Risk

Journal of Applied Finance & Banking, vol.2, no.3, 2012, 65-79 ISSN: 1792-6580 (print version), 1792-6599 (online) International Scientific Press, 2012 Measuring Exchange Rate Fluctuations Risk Using the

Journal of Applied Finance & Banking, vol.2, no.3, 2012, 65-79 ISSN: 1792-6580 (print version), 1792-6599 (online) International Scientific Press, 2012 Measuring Exchange Rate Fluctuations Risk Using the

LDA at Work: Deutsche Bank s Approach to Quantifying Operational Risk

LDA at Work: Deutsche Bank s Approach to Quantifying Operational Risk Workshop on Financial Risk and Banking Regulation Office of the Comptroller of the Currency, Washington DC, 5 Feb 2009 Michael Kalkbrener

LDA at Work: Deutsche Bank s Approach to Quantifying Operational Risk Workshop on Financial Risk and Banking Regulation Office of the Comptroller of the Currency, Washington DC, 5 Feb 2009 Michael Kalkbrener

Copula Simulation in Portfolio Allocation Decisions

Copula Simulation in Portfolio Allocation Decisions Gyöngyi Bugár Gyöngyi Bugár and Máté Uzsoki University of Pécs Faculty of Business and Economics This presentation has been prepared for the Actuaries

Copula Simulation in Portfolio Allocation Decisions Gyöngyi Bugár Gyöngyi Bugár and Máté Uzsoki University of Pécs Faculty of Business and Economics This presentation has been prepared for the Actuaries

Basel Committee on Banking Supervision. Fundamental review of the trading book interim impact analysis

Basel Committee on Banking Supervision Fundamental review of the trading book interim impact analysis November 2015 This publication is available on the BIS website (www.bis.org). Bank for International

Basel Committee on Banking Supervision Fundamental review of the trading book interim impact analysis November 2015 This publication is available on the BIS website (www.bis.org). Bank for International

Implied Volatility Surface

Implied Volatility Surface Liuren Wu Zicklin School of Business, Baruch College Options Markets (Hull chapter: 16) Liuren Wu Implied Volatility Surface Options Markets 1 / 18 Implied volatility Recall

Implied Volatility Surface Liuren Wu Zicklin School of Business, Baruch College Options Markets (Hull chapter: 16) Liuren Wu Implied Volatility Surface Options Markets 1 / 18 Implied volatility Recall

How To Check For Differences In The One Way Anova

MINITAB ASSISTANT WHITE PAPER This paper explains the research conducted by Minitab statisticians to develop the methods and data checks used in the Assistant in Minitab 17 Statistical Software. One-Way

MINITAB ASSISTANT WHITE PAPER This paper explains the research conducted by Minitab statisticians to develop the methods and data checks used in the Assistant in Minitab 17 Statistical Software. One-Way

Descriptive Statistics

Descriptive Statistics Primer Descriptive statistics Central tendency Variation Relative position Relationships Calculating descriptive statistics Descriptive Statistics Purpose to describe or summarize

Descriptive Statistics Primer Descriptive statistics Central tendency Variation Relative position Relationships Calculating descriptive statistics Descriptive Statistics Purpose to describe or summarize

Financial Risk Forecasting Chapter 8 Backtesting and stresstesting

Financial Risk Forecasting Chapter 8 Backtesting and stresstesting Jon Danielsson London School of Economics 2015 To accompany Financial Risk Forecasting http://www.financialriskforecasting.com/ Published

Financial Risk Forecasting Chapter 8 Backtesting and stresstesting Jon Danielsson London School of Economics 2015 To accompany Financial Risk Forecasting http://www.financialriskforecasting.com/ Published

Validation of Internal Rating and Scoring Models

Validation of Internal Rating and Scoring Models Dr. Leif Boegelein Global Financial Services Risk Management [email protected] 07.09.2005 2005 EYGM Limited. All Rights Reserved. Agenda 1. Motivation

Validation of Internal Rating and Scoring Models Dr. Leif Boegelein Global Financial Services Risk Management [email protected] 07.09.2005 2005 EYGM Limited. All Rights Reserved. Agenda 1. Motivation

A comparison of Value at Risk methods for measurement of the financial risk 1

A comparison of Value at Risk methods for measurement of the financial risk 1 Mária Bohdalová, Faculty of Management, Comenius University, Bratislava, Slovakia Abstract One of the key concepts of risk

A comparison of Value at Risk methods for measurement of the financial risk 1 Mária Bohdalová, Faculty of Management, Comenius University, Bratislava, Slovakia Abstract One of the key concepts of risk

INTERPRETING THE ONE-WAY ANALYSIS OF VARIANCE (ANOVA)

") INTERPRETING THE ONE-WAY ANALYSIS OF VARIANCE (ANOVA) As with other parametric statistics, we begin the one-way ANOVA with a test of the underlying assumptions. Our first assumption is the assumption of

INTERPRETING THE ONE-WAY ANALYSIS OF VARIANCE (ANOVA) As with other parametric statistics, we begin the one-way ANOVA with a test of the underlying assumptions. Our first assumption is the assumption of

Stochastic Analysis of Long-Term Multiple-Decrement Contracts

Stochastic Analysis of Long-Term Multiple-Decrement Contracts Matthew Clark, FSA, MAAA, and Chad Runchey, FSA, MAAA Ernst & Young LLP Published in the July 2008 issue of the Actuarial Practice Forum Copyright

Stochastic Analysis of Long-Term Multiple-Decrement Contracts Matthew Clark, FSA, MAAA, and Chad Runchey, FSA, MAAA Ernst & Young LLP Published in the July 2008 issue of the Actuarial Practice Forum Copyright

Developments in Risk Attribution

Singapore 2004 Developments in Risk Attribution Investment Managers Association of Singapore September 23, 2004 Alex Carmichael Director Risk Solutions & Operations RiskMetrics Group Asia Pacific [email protected]

Singapore 2004 Developments in Risk Attribution Investment Managers Association of Singapore September 23, 2004 Alex Carmichael Director Risk Solutions & Operations RiskMetrics Group Asia Pacific [email protected]

STA-201-TE. 5. Measures of relationship: correlation (5%) Correlation coefficient; Pearson r; correlation and causation; proportion of common variance

Correlation coefficient; Pearson r; correlation and causation; proportion of common variance") Principles of Statistics STA-201-TE This TECEP is an introduction to descriptive and inferential statistics. Topics include: measures of central tendency, variability, correlation, regression, hypothesis

Principles of Statistics STA-201-TE This TECEP is an introduction to descriptive and inferential statistics. Topics include: measures of central tendency, variability, correlation, regression, hypothesis

Non Linear Dependence Structures: a Copula Opinion Approach in Portfolio Optimization

Non Linear Dependence Structures: a Copula Opinion Approach in Portfolio Optimization Jean- Damien Villiers ESSEC Business School Master of Sciences in Management Grande Ecole September 2013 1 Non Linear

Non Linear Dependence Structures: a Copula Opinion Approach in Portfolio Optimization Jean- Damien Villiers ESSEC Business School Master of Sciences in Management Grande Ecole September 2013 1 Non Linear

(Part.1) FOUNDATIONS OF RISK MANAGEMENT

FOUNDATIONS OF RISK MANAGEMENT") (Part.1) FOUNDATIONS OF RISK MANAGEMENT 1 : Risk Taking: A Corporate Governance Perspective Delineating Efficient Portfolios 2: The Standard Capital Asset Pricing Model 1 : Risk : A Helicopter View 2:

(Part.1) FOUNDATIONS OF RISK MANAGEMENT 1 : Risk Taking: A Corporate Governance Perspective Delineating Efficient Portfolios 2: The Standard Capital Asset Pricing Model 1 : Risk : A Helicopter View 2:

MANAGE RISK WITH CONFIDENCE

>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>> ENTERPRISE RISK Bloomberg Trading Solutions MANAGE RISK WITH CONFIDENCE >>>>> SHARPEN YOUR VIEW Managing risk is more critical than ever. And more

>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>> ENTERPRISE RISK Bloomberg Trading Solutions MANAGE RISK WITH CONFIDENCE >>>>> SHARPEN YOUR VIEW Managing risk is more critical than ever. And more

RISK MANAGEMENT PRACTICES RISK FRAMEWORKS MARKET RISK OPERATIONAL RISK CREDIT RISK LIQUIDITY RISK, ALM & FTP

T H E P RO F E SS I O N A L R I S K M A N AG E R ( P R M ) D E S I G N AT I O N P RO G R A M PRM TM SELF STUDY GUIDE EXAM III RISK MANAGEMENT PRACTICES RISK FRAMEWORKS MARKET RISK OPERATIONAL RISK CREDIT

T H E P RO F E SS I O N A L R I S K M A N AG E R ( P R M ) D E S I G N AT I O N P RO G R A M PRM TM SELF STUDY GUIDE EXAM III RISK MANAGEMENT PRACTICES RISK FRAMEWORKS MARKET RISK OPERATIONAL RISK CREDIT

Credit Risk Stress Testing

1 Credit Risk Stress Testing Stress Testing Features of Risk Evaluator 1. 1. Introduction Risk Evaluator is a financial tool intended for evaluating market and credit risk of single positions or of large

1 Credit Risk Stress Testing Stress Testing Features of Risk Evaluator 1. 1. Introduction Risk Evaluator is a financial tool intended for evaluating market and credit risk of single positions or of large

ARMS Counterparty Credit Risk

ARMS Counterparty Credit Risk PFE - Potential Future Exposure & CVA - Credit Valuation Adjustment An introduction to the ARMS CCR module EXECUTIVE SUMMARY The ARMS CCR Module combines market proven financial

ARMS Counterparty Credit Risk PFE - Potential Future Exposure & CVA - Credit Valuation Adjustment An introduction to the ARMS CCR module EXECUTIVE SUMMARY The ARMS CCR Module combines market proven financial

APT Integrated risk management for the buy-side

APT Integrated risk management for the buy-side SUNGARD S APT: INTEGRATED RISK MANAGEMENT FOR THE BUY-SIDE SunGard APT helps your business to effectively monitor and manage its investment risks. Whatever

APT Integrated risk management for the buy-side SUNGARD S APT: INTEGRATED RISK MANAGEMENT FOR THE BUY-SIDE SunGard APT helps your business to effectively monitor and manage its investment risks. Whatever

POINT Innovative Multi-Asset Portfolio Analysis

Index, Portfolio and Risk Solutions POINT Innovative Multi-Asset Portfolio Analysis The Difference Is Clear POINT: Dynamic Decision Support Flexible portfolio and index reporting Draw from our vast database

Index, Portfolio and Risk Solutions POINT Innovative Multi-Asset Portfolio Analysis The Difference Is Clear POINT: Dynamic Decision Support Flexible portfolio and index reporting Draw from our vast database

Subject ST9 Enterprise Risk Management Syllabus

Subject ST9 Enterprise Risk Management Syllabus for the 2015 exams 1 June 2014 Aim The aim of the Enterprise Risk Management (ERM) Specialist Technical subject is to instil in successful candidates the

Subject ST9 Enterprise Risk Management Syllabus for the 2015 exams 1 June 2014 Aim The aim of the Enterprise Risk Management (ERM) Specialist Technical subject is to instil in successful candidates the

Tail-Dependence an Essential Factor for Correctly Measuring the Benefits of Diversification

Tail-Dependence an Essential Factor for Correctly Measuring the Benefits of Diversification Presented by Work done with Roland Bürgi and Roger Iles New Views on Extreme Events: Coupled Networks, Dragon

Tail-Dependence an Essential Factor for Correctly Measuring the Benefits of Diversification Presented by Work done with Roland Bürgi and Roger Iles New Views on Extreme Events: Coupled Networks, Dragon

Market Risk Capital Disclosures Report. For the Quarter Ended March 31, 2013

MARKET RISK CAPITAL DISCLOSURES REPORT For the quarter ended March 31, 2013 Table of Contents Section Page 1 Morgan Stanley... 1 2 Risk-based Capital Guidelines: Market Risk... 1 3 Market Risk... 1 3.1

MARKET RISK CAPITAL DISCLOSURES REPORT For the quarter ended March 31, 2013 Table of Contents Section Page 1 Morgan Stanley... 1 2 Risk-based Capital Guidelines: Market Risk... 1 3 Market Risk... 1 3.1

INCORPORATION OF LIQUIDITY RISKS INTO EQUITY PORTFOLIO RISK ESTIMATES. Dan dibartolomeo September 2010

INCORPORATION OF LIQUIDITY RISKS INTO EQUITY PORTFOLIO RISK ESTIMATES Dan dibartolomeo September 2010 GOALS FOR THIS TALK Assert that liquidity of a stock is properly measured as the expected price change,

INCORPORATION OF LIQUIDITY RISKS INTO EQUITY PORTFOLIO RISK ESTIMATES Dan dibartolomeo September 2010 GOALS FOR THIS TALK Assert that liquidity of a stock is properly measured as the expected price change,

Effective Stress Testing in Enterprise Risk Management

Effective Stress Testing in Enterprise Risk Management Lijia Guo, Ph.D., ASA, MAAA *^ Copyright 2008 by the Society of Actuaries. All rights reserved by the Society of Actuaries. Permission is granted

Effective Stress Testing in Enterprise Risk Management Lijia Guo, Ph.D., ASA, MAAA *^ Copyright 2008 by the Society of Actuaries. All rights reserved by the Society of Actuaries. Permission is granted

GN47: Stochastic Modelling of Economic Risks in Life Insurance

GN47: Stochastic Modelling of Economic Risks in Life Insurance Classification Recommended Practice MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND THAT

GN47: Stochastic Modelling of Economic Risks in Life Insurance Classification Recommended Practice MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND THAT

Projects Involving Statistics (& SPSS)

") Projects Involving Statistics (& SPSS) Academic Skills Advice Starting a project which involves using statistics can feel confusing as there seems to be many different things you can do (charts, graphs,

Projects Involving Statistics (& SPSS) Academic Skills Advice Starting a project which involves using statistics can feel confusing as there seems to be many different things you can do (charts, graphs,

Summary of Formulas and Concepts. Descriptive Statistics (Ch. 1-4)

") Summary of Formulas and Concepts Descriptive Statistics (Ch. 1-4) Definitions Population: The complete set of numerical information on a particular quantity in which an investigator is interested. We assume

Summary of Formulas and Concepts Descriptive Statistics (Ch. 1-4) Definitions Population: The complete set of numerical information on a particular quantity in which an investigator is interested. We assume

How To Write A New Capital Charge On Trading Books

Incremental Risk Capital (IRC) and Comprehensive Risk Measure (CRM): Modelling Challenges in a Bank-wide System Jean-Baptiste Brunac BNP Paribas Risk Methodology and Analytics Group Risk Management EIFR

Incremental Risk Capital (IRC) and Comprehensive Risk Measure (CRM): Modelling Challenges in a Bank-wide System Jean-Baptiste Brunac BNP Paribas Risk Methodology and Analytics Group Risk Management EIFR

Market Risk Management

Market Risk Management Hamish Treleaven, Executive General Manager, Market Risk Management 17 November 2010 The quantum of Market Risk at CBA Current Economic Capital attribution Current Market Risk Economic

Market Risk Management Hamish Treleaven, Executive General Manager, Market Risk Management 17 November 2010 The quantum of Market Risk at CBA Current Economic Capital attribution Current Market Risk Economic

Normality Testing in Excel

Normality Testing in Excel By Mark Harmon Copyright 2011 Mark Harmon No part of this publication may be reproduced or distributed without the express permission of the author. [email protected]

Normality Testing in Excel By Mark Harmon Copyright 2011 Mark Harmon No part of this publication may be reproduced or distributed without the express permission of the author. [email protected]

Sample Size and Power in Clinical Trials

Sample Size and Power in Clinical Trials Version 1.0 May 011 1. Power of a Test. Factors affecting Power 3. Required Sample Size RELATED ISSUES 1. Effect Size. Test Statistics 3. Variation 4. Significance

Sample Size and Power in Clinical Trials Version 1.0 May 011 1. Power of a Test. Factors affecting Power 3. Required Sample Size RELATED ISSUES 1. Effect Size. Test Statistics 3. Variation 4. Significance

1) What kind of risk on settlements is covered by 'Herstatt Risk' for which BCBS was formed?

What kind of risk on settlements is covered by 'Herstatt Risk' for which BCBS was formed?") 1) What kind of risk on settlements is covered by 'Herstatt Risk' for which BCBS was formed? a) Exchange rate risk b) Time difference risk c) Interest rate risk d) None 2) Which of the following is not

1) What kind of risk on settlements is covered by 'Herstatt Risk' for which BCBS was formed? a) Exchange rate risk b) Time difference risk c) Interest rate risk d) None 2) Which of the following is not

Business Statistics. Successful completion of Introductory and/or Intermediate Algebra courses is recommended before taking Business Statistics.

Business Course Text Bowerman, Bruce L., Richard T. O'Connell, J. B. Orris, and Dawn C. Porter. Essentials of Business, 2nd edition, McGraw-Hill/Irwin, 2008, ISBN: 978-0-07-331988-9. Required Computing

Business Course Text Bowerman, Bruce L., Richard T. O'Connell, J. B. Orris, and Dawn C. Porter. Essentials of Business, 2nd edition, McGraw-Hill/Irwin, 2008, ISBN: 978-0-07-331988-9. Required Computing

ERM-2: Introduction to Economic Capital Modeling

ERM-2: Introduction to Economic Capital Modeling 2011 Casualty Loss Reserve Seminar, Las Vegas, NV A presentation by François Morin September 15, 2011 2011 Towers Watson. All rights reserved. INTRODUCTION

ERM-2: Introduction to Economic Capital Modeling 2011 Casualty Loss Reserve Seminar, Las Vegas, NV A presentation by François Morin September 15, 2011 2011 Towers Watson. All rights reserved. INTRODUCTION

Working Paper No. 525 Filtered historical simulation Value-at-Risk models and their competitors Pedro Gurrola-Perez and David Murphy

Working Paper No. 525 Filtered historical simulation Value-at-Risk models and their competitors Pedro Gurrola-Perez and David Murphy March 2015 Working papers describe research in progress by the author(s)

Working Paper No. 525 Filtered historical simulation Value-at-Risk models and their competitors Pedro Gurrola-Perez and David Murphy March 2015 Working papers describe research in progress by the author(s)

Ten key points from Basel s Fundamental Review of the Trading Book

First January 19, 2016 take A publication of PwC s financial services regulatory practice Ten key points from Basel s Fundamental Review of the Trading Book On January 14 th, the Basel Committee on Banking

First January 19, 2016 take A publication of PwC s financial services regulatory practice Ten key points from Basel s Fundamental Review of the Trading Book On January 14 th, the Basel Committee on Banking

REGULATORY CAPITAL DISCLOSURES MARKET RISK PILLAR 3 REPORT

REGULATORY CAPITAL DISCLOSURES MARKET RISK PILLAR 3 REPORT For the quarterly period ended June 30, 2013 Table of Contents I. Executive Summary 1 Introduction 1 Basel II Overview 1 Basel 2.5 Market Risk

REGULATORY CAPITAL DISCLOSURES MARKET RISK PILLAR 3 REPORT For the quarterly period ended June 30, 2013 Table of Contents I. Executive Summary 1 Introduction 1 Basel II Overview 1 Basel 2.5 Market Risk

12.5: CHI-SQUARE GOODNESS OF FIT TESTS

125: Chi-Square Goodness of Fit Tests CD12-1 125: CHI-SQUARE GOODNESS OF FIT TESTS In this section, the χ 2 distribution is used for testing the goodness of fit of a set of data to a specific probability

125: Chi-Square Goodness of Fit Tests CD12-1 125: CHI-SQUARE GOODNESS OF FIT TESTS In this section, the χ 2 distribution is used for testing the goodness of fit of a set of data to a specific probability

Basel Committee on Banking Supervision. Analysis of the trading book hypothetical portfolio exercise

Basel Committee on Banking Supervision Analysis of the trading book hypothetical portfolio exercise September 2014 This publication is available on the BIS website (www.bis.org). Grey underlined text in

Basel Committee on Banking Supervision Analysis of the trading book hypothetical portfolio exercise September 2014 This publication is available on the BIS website (www.bis.org). Grey underlined text in

Understanding Volatility

Options Trading Forum October 2 nd, 2002 Understanding Volatility Sheldon Natenberg Chicago Trading Co. 440 S. LaSalle St. Chicago, IL 60605 (312) 863-8004 [email protected] exercise price time to expiration

Options Trading Forum October 2 nd, 2002 Understanding Volatility Sheldon Natenberg Chicago Trading Co. 440 S. LaSalle St. Chicago, IL 60605 (312) 863-8004 [email protected] exercise price time to expiration

A Primer on Mathematical Statistics and Univariate Distributions; The Normal Distribution; The GLM with the Normal Distribution

A Primer on Mathematical Statistics and Univariate Distributions; The Normal Distribution; The GLM with the Normal Distribution PSYC 943 (930): Fundamentals of Multivariate Modeling Lecture 4: September

A Primer on Mathematical Statistics and Univariate Distributions; The Normal Distribution; The GLM with the Normal Distribution PSYC 943 (930): Fundamentals of Multivariate Modeling Lecture 4: September

Java Modules for Time Series Analysis

Java Modules for Time Series Analysis Agenda Clustering Non-normal distributions Multifactor modeling Implied ratings Time series prediction 1. Clustering + Cluster 1 Synthetic Clustering + Time series

Java Modules for Time Series Analysis Agenda Clustering Non-normal distributions Multifactor modeling Implied ratings Time series prediction 1. Clustering + Cluster 1 Synthetic Clustering + Time series

How To Write A Credit Risk Book

CRM validation Jérôme BRUN, Head of model validation (market risk) June 2011 Introduction and agenda 1 3 amendments on the trading book to be implemented in 2011 Incremental Risk Charge (IRC) & Comprehensive

CRM validation Jérôme BRUN, Head of model validation (market risk) June 2011 Introduction and agenda 1 3 amendments on the trading book to be implemented in 2011 Incremental Risk Charge (IRC) & Comprehensive

EDF CEA Inria School Systemic Risk and Quantitative Risk Management

C2 RISK DIVISION EDF CEA Inria School Systemic Risk and Quantitative Risk Management EDF CEA INRIA School Systemic Risk and Quantitative Risk Management Regulatory rules evolutions and internal models

C2 RISK DIVISION EDF CEA Inria School Systemic Risk and Quantitative Risk Management EDF CEA INRIA School Systemic Risk and Quantitative Risk Management Regulatory rules evolutions and internal models

EBF response to Basel Fundamental Review of the Trading Book: A revised market risk framework

Ref.:EBF_005704 Brussels, 31 January 2014 Launched in 1960, the European Banking Federation is the voice of the European banking sector from the European Union and European Free Trade Association countries.

Ref.:EBF_005704 Brussels, 31 January 2014 Launched in 1960, the European Banking Federation is the voice of the European banking sector from the European Union and European Free Trade Association countries.

Citigroup Inc. Basel II.5 Market Risk Disclosures As of and For the Period Ended March 31, 2014

Citigroup Inc. Basel II.5 Market Risk Disclosures and For the Period Ended TABLE OF CONTENTS OVERVIEW 3 Organization 3 Capital Adequacy 3 Basel II.5 Covered Positions 3 Valuation and Accounting Policies

Citigroup Inc. Basel II.5 Market Risk Disclosures and For the Period Ended TABLE OF CONTENTS OVERVIEW 3 Organization 3 Capital Adequacy 3 Basel II.5 Covered Positions 3 Valuation and Accounting Policies

VALUE AT RISK: PHILIPPE JORION

VALUE AT RISK: The New Benchmark for Managing Financial Risk THIRD EDITION Answer Key to End-of-Chapter Exercises PHILIPPE JORION McGraw-Hill c 2006 Philippe Jorion VAR: Answer Key to End-of-Chapter Exercises

VALUE AT RISK: The New Benchmark for Managing Financial Risk THIRD EDITION Answer Key to End-of-Chapter Exercises PHILIPPE JORION McGraw-Hill c 2006 Philippe Jorion VAR: Answer Key to End-of-Chapter Exercises

ERM Exam Core Readings Fall 2015. Table of Contents

i ERM Exam Core Readings Fall 2015 Table of Contents Section A: Risk Categories and Identification The candidate will understand the types of risks faced by an entity and be able to identify and analyze

i ERM Exam Core Readings Fall 2015 Table of Contents Section A: Risk Categories and Identification The candidate will understand the types of risks faced by an entity and be able to identify and analyze

by Maria Heiden, Berenberg Bank

Dynamic hedging of equity price risk with an equity protect overlay: reduce losses and exploit opportunities by Maria Heiden, Berenberg Bank As part of the distortions on the international stock markets

Dynamic hedging of equity price risk with an equity protect overlay: reduce losses and exploit opportunities by Maria Heiden, Berenberg Bank As part of the distortions on the international stock markets

SENSITIVITY ANALYSIS AND INFERENCE. Lecture 12

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike License. Your use of this material constitutes acceptance of that license and the conditions of use of materials on this

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike License. Your use of this material constitutes acceptance of that license and the conditions of use of materials on this

IMPLEMENTATION NOTE. Validating Risk Rating Systems at IRB Institutions

IMPLEMENTATION NOTE Subject: Category: Capital No: A-1 Date: January 2006 I. Introduction The term rating system comprises all of the methods, processes, controls, data collection and IT systems that support

IMPLEMENTATION NOTE Subject: Category: Capital No: A-1 Date: January 2006 I. Introduction The term rating system comprises all of the methods, processes, controls, data collection and IT systems that support

The Volcker Rule 13 considerations for calculating and reporting quantitative measures

The Volcker Rule 13 considerations for calculating and reporting quantitative measures Introduction On December 10, 2013 three Federal banking agencies as well the U.S. Securities and Exchange Commission

The Volcker Rule 13 considerations for calculating and reporting quantitative measures Introduction On December 10, 2013 three Federal banking agencies as well the U.S. Securities and Exchange Commission

PROVIDING RETIREMENT INCOME WITH STRUCTURED PRODUCTS

PROVIDING RETIREMENT INCOME WITH STRUCTURED PRODUCTS CUBE INVESTING David Stuff [email protected] ABSTRACT Structured products are an attractive type of investment for income seeking investors.

PROVIDING RETIREMENT INCOME WITH STRUCTURED PRODUCTS CUBE INVESTING David Stuff [email protected] ABSTRACT Structured products are an attractive type of investment for income seeking investors.

Additional sources Compilation of sources: http://lrs.ed.uiuc.edu/tseportal/datacollectionmethodologies/jin-tselink/tselink.htm

Mgt 540 Research Methods Data Analysis 1 Additional sources Compilation of sources: http://lrs.ed.uiuc.edu/tseportal/datacollectionmethodologies/jin-tselink/tselink.htm http://web.utk.edu/~dap/random/order/start.htm

Mgt 540 Research Methods Data Analysis 1 Additional sources Compilation of sources: http://lrs.ed.uiuc.edu/tseportal/datacollectionmethodologies/jin-tselink/tselink.htm http://web.utk.edu/~dap/random/order/start.htm

Financial Modeling using Microsoft Excel

Module 1A: Valuation modeling Part 1 Introduction to valuation modeling Understanding integrated financial models - Basic valuation techniques: accounting-based, market-based and cash-flow based - Revenue

Module 1A: Valuation modeling Part 1 Introduction to valuation modeling Understanding integrated financial models - Basic valuation techniques: accounting-based, market-based and cash-flow based - Revenue

Course Text. Required Computing Software. Course Description. Course Objectives. StraighterLine. Business Statistics

Course Text Business Statistics Lind, Douglas A., Marchal, William A. and Samuel A. Wathen. Basic Statistics for Business and Economics, 7th edition, McGraw-Hill/Irwin, 2010, ISBN: 9780077384470 [This

Course Text Business Statistics Lind, Douglas A., Marchal, William A. and Samuel A. Wathen. Basic Statistics for Business and Economics, 7th edition, McGraw-Hill/Irwin, 2010, ISBN: 9780077384470 [This

March 2016. Stress testing the UK banking system: guidance on the traded risk methodology for participating banks and building societies

March 2016 Stress testing the UK banking system: guidance on the traded risk methodology for participating banks and building societies 1 Overview 3 1.1 Introduction 3 1.2 Key design features 3 2 Preliminaries

March 2016 Stress testing the UK banking system: guidance on the traded risk methodology for participating banks and building societies 1 Overview 3 1.1 Introduction 3 1.2 Key design features 3 2 Preliminaries

Chapter 8 Hypothesis Testing Chapter 8 Hypothesis Testing 8-1 Overview 8-2 Basics of Hypothesis Testing

Chapter 8 Hypothesis Testing 1 Chapter 8 Hypothesis Testing 8-1 Overview 8-2 Basics of Hypothesis Testing 8-3 Testing a Claim About a Proportion 8-5 Testing a Claim About a Mean: s Not Known 8-6 Testing

Chapter 8 Hypothesis Testing 1 Chapter 8 Hypothesis Testing 8-1 Overview 8-2 Basics of Hypothesis Testing 8-3 Testing a Claim About a Proportion 8-5 Testing a Claim About a Mean: s Not Known 8-6 Testing