Financial Risk Management Exam Sample Questions

|

|

|

- Simon Cunningham

- 9 years ago

- Views:

Transcription

1 Financial Risk Management Exam Sample Questions Prepared by Daniel HERLEMONT 1

2 PART I - QUANTITATIVE ANALYSIS 3 Chapter 1 - Bunds Fundamentals 3 Chapter 2 - Fundamentals of Probability 7 Chapter 3 Fundamentals of Statistics 11 Chapter 4 - Monte Carlo Methods 13 PART I - CAPITAL MARKETS 17 Chapter 5 - Introduction to Derivatives 17 Chapter 6 - Options 18 Chapter 7 - Fixed Income Securities 22 Chapter 8 - Fixed Income Derivatives 28 Chapter 9 - Equity Market 31 Chapter 10 - Currency and Commodities Markets 33 PART III - MARKET RISK MANAGEMENT 36 Chapter 11 - Introduction to Risk Measurement 36 Chapter 12 - Identification of Risk Factors 38 Chapter 13 - Sources of Risk 40 Chapter 14 - Hedging Linear Risk 44 Chapter 15 - Non Linear Risk: Options 47 Chapter 16 - Modelling Risk Factors 52 Chapter 17 - VaR Methods 53 PART IV - Credit Risk Management 55 Chapter 18 - Introduction to Credit Risk 55 Chapter 19 - Measuring Actuarial Default Risk 58 Chapter 20 - Measuring Default Risk from Market Prices 63 Chapter 21 - Credit Exposure 65 Chapter 22 - Credit Derivatives 71 Chapter 23 - Managing Credit Risk 75 PART V - OERATIONAL AND INTEGRATED RISK MANAGEMENT 79 Chapter 24 - Operational Risk 79 Chapter 25 - Risk Capital and RAROC 82 Chapter 26 - Best Practices Reports 84 Chapter 27 - Firmwide Risk Management 84 Chapter 31 - The Basle Accord 89 Chapter 32 - The Basle Risk Charge 91 2

3 PART I - QUANTITATIVE ANALYSIS Chapter 1 - Bunds Fundamentals 3

4 4

5 5

6 6

7 Chapter 2 - Fundamentals of Probability 7

8 8

9 9

10 10

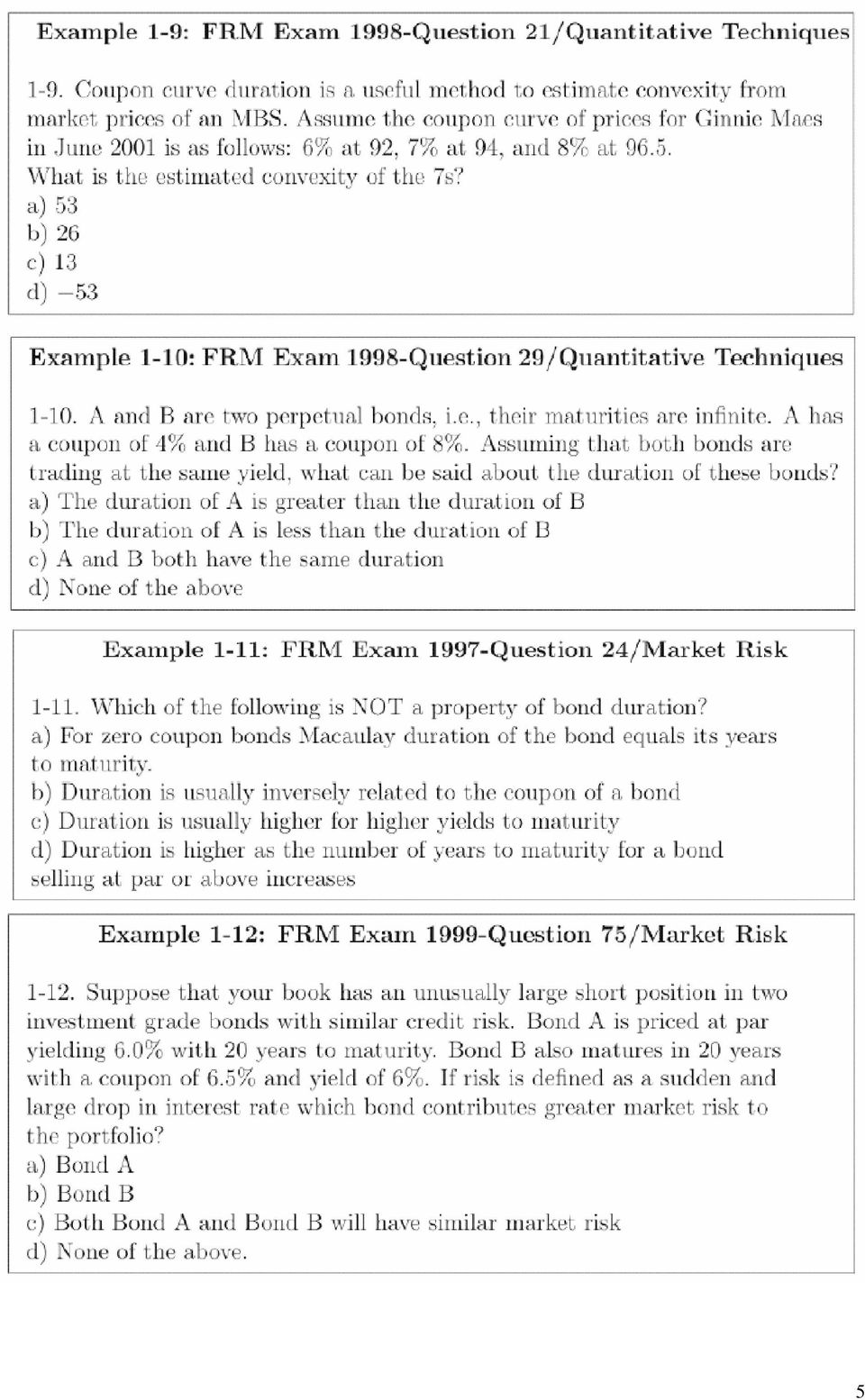

11 Chapter 3 Fundamentals of Statistics FRM-99, Question 4 Random walk assumes that returns from one time period are statistically independent from another period. This implies: A. Returns on 2 time periods can not be equal. B. Returns on 2 time periods are uncorrelated. C. Knowledge of the returns from one period does not help in predicting returns from another period D. Both b and c. FRM-99, Question 14 Suppose returns are uncorrelated over time. You are given that the volatility over 2 days is 1.2%. What is the volatility over 20 days? A. 0.38% B. 1.2% C. 3.79% D. 12.0% FRM-98, Question 7 Assume an asset price variance increases linearly with time. Suppose the expected asset price volatility for the next 2 months is 15% (annualized), and for the 1 month that follows, the expected volatility is 35% (annualized). What is the average expected volatility over the next 3 months? A. 22% B. 24% C. 25% D. 35% FRM-97, Question 15 The standard VaR calculation for extension to multiple periods assumes that returns are serially uncorrelated. If prices display trend, the true VaR will be: A. the same as standard VaR B. greater than the standard VaR C. less than the standard VaR D. unable to be determined FRM-99, Question 2 Under what circumstances could the explanatory power of regression analysis be overstated? A. The explanatory variables are not correlated with one another. B. The variance of the error term decreases as the value of the dependent variable increases. C. The error term is normally distributed. D. An important explanatory variable is excluded. FRM-99, Question 20 What is the covariance between populations a and b: a b A B C D FRM-99, Question 6 Daily returns on spot positions of the Euro against USD are highly correlated with returns on spot holdings of Yen against USD. This implies that: A. When Euro strengthens against USD, the yen also tends to strengthens, but returns are not necessarily equal. B. The two sets of returns tend to be almost equal C. The two sets of returns tend to be almost equal in magnitude but opposite in sign. D. None of the above. 11

12 FRM-99, Question 10 You want to estimate correlation between stocks in Frankfurt and Tokyo. You have prices of selected securities. How will time discrepancy bias the computed volatilities for individual stocks and correlations between these two markets? A. Increased volatility with correlation unchanged. B. Lower volatility with lower correlation. C. Volatility unchanged with lower correlation. D. Volatility unchanged with correlation unchanged. FRM-00, Question 125 If the F-test shows that the set of X variables explains a significant amount of variation in the Y variable, then: A. Another linear regression model should be tried. B. A t-test should be used to test which of the individual X variables can be discarded. C. A transformation of Y should be made. D. Another test could be done using an indicator variable to test significance of the model. FRM-00, Question 112 Positive autocorrelation of prices can be defined as: A. An upward movement in price is more likely to be followed by another upward movement in price. B. A downward movement in price is more likely to be followed by another downward movement. C. Both A and B. D. Historic prices have no correlation with future prices. FRM-00, Question 112 Positive autocorrelation of prices can be defined as: A. An upward movement in price is more likely to be followed by another upward movement in price. B. A downward movement in price is more likely to be followed by another downward movement. C. Both A and B. D. Historic prices have no correlation with future prices. 12

13 Chapter 4 - Monte Carlo Methods 13

14 14

15 15

16 16

17 PART I - CAPITAL MARKETS Chapter 5 - Introduction to Derivatives 17

18 Chapter 6 - Options 18

19 19

20 20

21 21

22 Chapter 7 - Fixed Income Securities 22

23 23

24 24

25 25

26 26

27 27

28 Chapter 8 - Fixed Income Derivatives 28

29 29

30 30

31 Chapter 9 - Equity Market 31

32 32

33 Chapter 10 - Currency and Commodities Markets 33

34 34

35 35

36 PART III - MARKET RISK MANAGEMENT Chapter 11 - Introduction to Risk Measurement 36

37 37

38 Chapter 12 - Identification of Risk Factors 38

39 39

40 Chapter 13 - Sources of Risk 40

41 41

42 42

43 43

44 Chapter 14 - Hedging Linear Risk 44

45 45

46 46

47 Chapter 15 - Non Linear Risk: Options 47

48 48

49 49

50 50

51 51

52 Chapter 16 - Modelling Risk Factors 52

53 Chapter 17 - VaR Methods 53

54 54

55 PART IV - Credit Risk Management Chapter 18 - Introduction to Credit Risk 55

56 56

57 57

58 Chapter 19 - Measuring Actuarial Default Risk 58

59 59

60 60

61 61

62 62

63 Chapter 20 - Measuring Default Risk from Market Prices 63

64 64

65 Chapter 21 - Credit Exposure 65

66 66

67 67

68 68

69 69

70 70

71 Chapter 22 - Credit Derivatives 71

72 72

73 73

74 74

75 Chapter 23 - Managing Credit Risk 75

76 76

77 77

78 78

79 PART V - OERATIONAL AND INTEGRATED RISK MANAGEMENT Chapter 24 - Operational Risk 79

80 80

81 81

82 Chapter 25 - Risk Capital and RAROC 82

83 83

84 Chapter 26 - Best Practices Reports Chapter 27 - Firmwide Risk Management 84

85 85

86 86

87 87

88 88

89 Chapter 31 - The Basle Accord 89

90 90

91 Chapter 32 - The Basle Risk Charge 91

92 92

93 93

94 94

95 95

96 96

Financial Risk Management Exam Sample Questions/Answers

Financial Risk Management Exam Sample Questions/Answers Prepared by Daniel HERLEMONT 1 2 3 4 5 6 Chapter 3 Fundamentals of Statistics FRM-99, Question 4 Random walk assumes that returns from one time period

Financial Risk Management Exam Sample Questions/Answers Prepared by Daniel HERLEMONT 1 2 3 4 5 6 Chapter 3 Fundamentals of Statistics FRM-99, Question 4 Random walk assumes that returns from one time period

Third Edition. Philippe Jorion GARP. WILEY John Wiley & Sons, Inc.

2008 AGI-Information Management Consultants May be used for personal purporses only or by libraries associated to dandelon.com network. Third Edition Philippe Jorion GARP WILEY John Wiley & Sons, Inc.

2008 AGI-Information Management Consultants May be used for personal purporses only or by libraries associated to dandelon.com network. Third Edition Philippe Jorion GARP WILEY John Wiley & Sons, Inc.

CHAPTER 9 MANAGEMENT OF ECONOMIC EXPOSURE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 9 MANAGEMENT OF ECONOMIC EXPOSURE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. How would you define economic exposure to exchange risk? Answer: Economic

CHAPTER 9 MANAGEMENT OF ECONOMIC EXPOSURE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. How would you define economic exposure to exchange risk? Answer: Economic

Updated Stress Testing Features in RiskMetrics

Updated Stress Testing Features in RiskMetrics RiskManager Historical Scenarios for Fall 2008, Treatment of Yield Curve Shocks, and a Hectic Day Risk Setting Introduction MSCI has updated RiskMetrics RiskManager

Updated Stress Testing Features in RiskMetrics RiskManager Historical Scenarios for Fall 2008, Treatment of Yield Curve Shocks, and a Hectic Day Risk Setting Introduction MSCI has updated RiskMetrics RiskManager

Jornadas Economicas del Banco de Guatemala. Managing Market Risk. Max Silberberg

Managing Market Risk Max Silberberg Defining Market Risk Market risk is exposure to an adverse change in value of financial instrument caused by movements in market variables. Market risk exposures are

Managing Market Risk Max Silberberg Defining Market Risk Market risk is exposure to an adverse change in value of financial instrument caused by movements in market variables. Market risk exposures are

Risk Based Capital Guidelines; Market Risk. The Bank of New York Mellon Corporation Market Risk Disclosures. As of June 30, 2014

Risk Based Capital Guidelines; Market Risk The Bank of New York Mellon Corporation Market Risk Disclosures As of June 30, 2014 1 Basel II.5 Market Risk Quarterly Disclosure Introduction Since January 1,

Risk Based Capital Guidelines; Market Risk The Bank of New York Mellon Corporation Market Risk Disclosures As of June 30, 2014 1 Basel II.5 Market Risk Quarterly Disclosure Introduction Since January 1,

Calculating VaR. Capital Market Risk Advisors CMRA

Calculating VaR Capital Market Risk Advisors How is VAR Calculated? Sensitivity Estimate Models - use sensitivity factors such as duration to estimate the change in value of the portfolio to changes in

Calculating VaR Capital Market Risk Advisors How is VAR Calculated? Sensitivity Estimate Models - use sensitivity factors such as duration to estimate the change in value of the portfolio to changes in

Asset Liability Management

e-learning and reference solutions for the global finance professional Asset Liability Management A comprehensive e-learning product covering Global Best Practices, Strategic, Operational and Analytical

e-learning and reference solutions for the global finance professional Asset Liability Management A comprehensive e-learning product covering Global Best Practices, Strategic, Operational and Analytical

Global Currency Hedging

Global Currency Hedging John Y. Campbell Harvard University Arrowstreet Capital, L.P. May 16, 2010 Global Currency Hedging Joint work with Karine Serfaty-de Medeiros of OC&C Strategy Consultants and Luis

Global Currency Hedging John Y. Campbell Harvard University Arrowstreet Capital, L.P. May 16, 2010 Global Currency Hedging Joint work with Karine Serfaty-de Medeiros of OC&C Strategy Consultants and Luis

Contents. List of Figures. List of Tables. List of Examples. Preface to Volume IV

Contents List of Figures List of Tables List of Examples Foreword Preface to Volume IV xiii xvi xxi xxv xxix IV.1 Value at Risk and Other Risk Metrics 1 IV.1.1 Introduction 1 IV.1.2 An Overview of Market

Contents List of Figures List of Tables List of Examples Foreword Preface to Volume IV xiii xvi xxi xxv xxix IV.1 Value at Risk and Other Risk Metrics 1 IV.1.1 Introduction 1 IV.1.2 An Overview of Market

Caput Derivatives: October 30, 2003

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Optimal Hedging of Uncertain Foreign Currency Returns. 12/12/2011 SLJ Macro Partners Fatih Yilmaz

Optimal Hedging of Uncertain Foreign Currency Returns 12/12/2011 SLJ Macro Partners Fatih Yilmaz Optimal Hedging of Uncertain Foreign Currency Returns A. Statement of Problem Over- or under-hedging of

Optimal Hedging of Uncertain Foreign Currency Returns 12/12/2011 SLJ Macro Partners Fatih Yilmaz Optimal Hedging of Uncertain Foreign Currency Returns A. Statement of Problem Over- or under-hedging of

An introduction to Value-at-Risk Learning Curve September 2003

An introduction to Value-at-Risk Learning Curve September 2003 Value-at-Risk The introduction of Value-at-Risk (VaR) as an accepted methodology for quantifying market risk is part of the evolution of risk

An introduction to Value-at-Risk Learning Curve September 2003 Value-at-Risk The introduction of Value-at-Risk (VaR) as an accepted methodology for quantifying market risk is part of the evolution of risk

The Tangent or Efficient Portfolio

The Tangent or Efficient Portfolio 1 2 Identifying the Tangent Portfolio Sharpe Ratio: Measures the ratio of reward-to-volatility provided by a portfolio Sharpe Ratio Portfolio Excess Return E[ RP ] r

The Tangent or Efficient Portfolio 1 2 Identifying the Tangent Portfolio Sharpe Ratio: Measures the ratio of reward-to-volatility provided by a portfolio Sharpe Ratio Portfolio Excess Return E[ RP ] r

9 Hedging the Risk of an Energy Futures Portfolio UNCORRECTED PROOFS. Carol Alexander 9.1 MAPPING PORTFOLIOS TO CONSTANT MATURITY FUTURES 12 T 1)

") Helyette Geman c0.tex V - 0//0 :00 P.M. Page Hedging the Risk of an Energy Futures Portfolio Carol Alexander This chapter considers a hedging problem for a trader in futures on crude oil, heating oil and

Helyette Geman c0.tex V - 0//0 :00 P.M. Page Hedging the Risk of an Energy Futures Portfolio Carol Alexander This chapter considers a hedging problem for a trader in futures on crude oil, heating oil and

GRADO EN ECONOMÍA. Is the Forward Rate a True Unbiased Predictor of the Future Spot Exchange Rate?

FACULTAD DE CIENCIAS ECONÓMICAS Y EMPRESARIALES GRADO EN ECONOMÍA Is the Forward Rate a True Unbiased Predictor of the Future Spot Exchange Rate? Autor: Elena Renedo Sánchez Tutor: Juan Ángel Jiménez Martín

FACULTAD DE CIENCIAS ECONÓMICAS Y EMPRESARIALES GRADO EN ECONOMÍA Is the Forward Rate a True Unbiased Predictor of the Future Spot Exchange Rate? Autor: Elena Renedo Sánchez Tutor: Juan Ángel Jiménez Martín

ERM Exam Core Readings Fall 2015. Table of Contents

i ERM Exam Core Readings Fall 2015 Table of Contents Section A: Risk Categories and Identification The candidate will understand the types of risks faced by an entity and be able to identify and analyze

i ERM Exam Core Readings Fall 2015 Table of Contents Section A: Risk Categories and Identification The candidate will understand the types of risks faced by an entity and be able to identify and analyze

Currency Options and Swaps: Hedging Currency Risk

Currency Options and Swaps: Hedging Currency Risk By Louis Morel ECON 826 International Finance Queen s Economics Department January 23, 2004 Table of Contents 1. Introduction...2 2. Currency risk exposure...2

Currency Options and Swaps: Hedging Currency Risk By Louis Morel ECON 826 International Finance Queen s Economics Department January 23, 2004 Table of Contents 1. Introduction...2 2. Currency risk exposure...2

AVANTGARD Treasury, liquidity risk, and cash management. White Paper FINANCIAL RISK MANAGEMENT IN TREASURY

AVANTGARD Treasury, liquidity risk, and cash management White Paper FINANCIAL RISK MANAGEMENT IN TREASURY Contents 1 Introduction 1 Mitigating financial risk: Is there an effective framework in place?

AVANTGARD Treasury, liquidity risk, and cash management White Paper FINANCIAL RISK MANAGEMENT IN TREASURY Contents 1 Introduction 1 Mitigating financial risk: Is there an effective framework in place?

1.2 Structured notes

1.2 Structured notes Structured notes are financial products that appear to be fixed income instruments, but contain embedded options and do not necessarily reflect the risk of the issuing credit. Used

1.2 Structured notes Structured notes are financial products that appear to be fixed income instruments, but contain embedded options and do not necessarily reflect the risk of the issuing credit. Used

Dr Christine Brown University of Melbourne

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

1. Currency Exposure. VaR for currency positions. Hedged and unhedged positions

RISK MANAGEMENT [635-0]. Currency Exposure. ar for currency positions. Hedged and unhedged positions Currency Exposure Currency exposure represents the relationship between stated financial goals and exchange

RISK MANAGEMENT [635-0]. Currency Exposure. ar for currency positions. Hedged and unhedged positions Currency Exposure Currency exposure represents the relationship between stated financial goals and exchange

Lecture 1: Asset pricing and the equity premium puzzle

Lecture 1: Asset pricing and the equity premium puzzle Simon Gilchrist Boston Univerity and NBER EC 745 Fall, 2013 Overview Some basic facts. Study the asset pricing implications of household portfolio

Lecture 1: Asset pricing and the equity premium puzzle Simon Gilchrist Boston Univerity and NBER EC 745 Fall, 2013 Overview Some basic facts. Study the asset pricing implications of household portfolio

Vanguard research July 2014

The Understanding buck stops here: the hedge return : Vanguard The impact money of currency market hedging funds in foreign bonds Vanguard research July 214 Charles Thomas, CFA; Paul M. Bosse, CFA Hedging

The Understanding buck stops here: the hedge return : Vanguard The impact money of currency market hedging funds in foreign bonds Vanguard research July 214 Charles Thomas, CFA; Paul M. Bosse, CFA Hedging

Algorithmic Trading Session 6 Trade Signal Generation IV Momentum Strategies. Oliver Steinki, CFA, FRM

Algorithmic Trading Session 6 Trade Signal Generation IV Momentum Strategies Oliver Steinki, CFA, FRM Outline Introduction What is Momentum? Tests to Discover Momentum Interday Momentum Strategies Intraday

Algorithmic Trading Session 6 Trade Signal Generation IV Momentum Strategies Oliver Steinki, CFA, FRM Outline Introduction What is Momentum? Tests to Discover Momentum Interday Momentum Strategies Intraday

EDF CEA Inria School Systemic Risk and Quantitative Risk Management

C2 RISK DIVISION EDF CEA Inria School Systemic Risk and Quantitative Risk Management EDF CEA INRIA School Systemic Risk and Quantitative Risk Management Regulatory rules evolutions and internal models

C2 RISK DIVISION EDF CEA Inria School Systemic Risk and Quantitative Risk Management EDF CEA INRIA School Systemic Risk and Quantitative Risk Management Regulatory rules evolutions and internal models

Chapter 22 Credit Risk

Chapter 22 Credit Risk May 22, 2009 20.28. Suppose a 3-year corporate bond provides a coupon of 7% per year payable semiannually and has a yield of 5% (expressed with semiannual compounding). The yields

Chapter 22 Credit Risk May 22, 2009 20.28. Suppose a 3-year corporate bond provides a coupon of 7% per year payable semiannually and has a yield of 5% (expressed with semiannual compounding). The yields

10 knacks of using Nikkei Volatility Index Futures

10 knacks of using Nikkei Volatility Index Futures 10 KNACKS OF USING NIKKEI VOLATILITY INDEX FUTURES 1. Nikkei VI is an index indicating how the market predicts the market volatility will be in one month

10 knacks of using Nikkei Volatility Index Futures 10 KNACKS OF USING NIKKEI VOLATILITY INDEX FUTURES 1. Nikkei VI is an index indicating how the market predicts the market volatility will be in one month

Multi-Factor Risk Attribution Concept and Uses. CREDIT SUISSE AG, Mary Cait McCarthy, CFA, FRM August 29, 2012

Multi-Factor Risk Attribution Concept and Uses Introduction Why do we need risk attribution? What are we trying to achieve with it? What is the difference between ex-post and ex-ante risk? What is the

Multi-Factor Risk Attribution Concept and Uses Introduction Why do we need risk attribution? What are we trying to achieve with it? What is the difference between ex-post and ex-ante risk? What is the

The Professional Risk Managers Handbook A Comprehensive Guide to Current Theory and Best Practices

The Professional Risk Managers Handbook A Comprehensive Guide to Current Theory and Best Practices The Official Handbook for the PRM Designation 2015 Edition Table of Contents PRM Exam I FINANCE THEORY,

The Professional Risk Managers Handbook A Comprehensive Guide to Current Theory and Best Practices The Official Handbook for the PRM Designation 2015 Edition Table of Contents PRM Exam I FINANCE THEORY,

Dual Listing of the SGX EURO STOXX 50 Index Futures in Singapore

September 2011 Dual Listing of the SGX EURO STOXX 50 Index Futures in Singapore Mr Tobias Hekster Managing Director, True Partner Education Ltd Senior Strategist, Algorithmic Training Group of Hong Kong

September 2011 Dual Listing of the SGX EURO STOXX 50 Index Futures in Singapore Mr Tobias Hekster Managing Director, True Partner Education Ltd Senior Strategist, Algorithmic Training Group of Hong Kong

OPTIONS EDUCATION GLOBAL

OPTIONS EDUCATION GLOBAL TABLE OF CONTENTS Introduction What are FX Options? Trading 101 ITM, ATM and OTM Options Trading Strategies Glossary Contact Information 3 5 6 8 9 10 16 HIGH RISK WARNING: Before

OPTIONS EDUCATION GLOBAL TABLE OF CONTENTS Introduction What are FX Options? Trading 101 ITM, ATM and OTM Options Trading Strategies Glossary Contact Information 3 5 6 8 9 10 16 HIGH RISK WARNING: Before

SOLUTION1. exercise 1

exercise 1 Stock BBB has a spot price equal to 80$ and a dividend equal to 10$ will be paid in 5 months. The on year interest rate is equal to 8% (c.c). 1. Calculate the 6 month forward price? 2. Calculate

exercise 1 Stock BBB has a spot price equal to 80$ and a dividend equal to 10$ will be paid in 5 months. The on year interest rate is equal to 8% (c.c). 1. Calculate the 6 month forward price? 2. Calculate

Market Risk Capital Disclosures Report. For the Quarter Ended March 31, 2013

MARKET RISK CAPITAL DISCLOSURES REPORT For the quarter ended March 31, 2013 Table of Contents Section Page 1 Morgan Stanley... 1 2 Risk-based Capital Guidelines: Market Risk... 1 3 Market Risk... 1 3.1

MARKET RISK CAPITAL DISCLOSURES REPORT For the quarter ended March 31, 2013 Table of Contents Section Page 1 Morgan Stanley... 1 2 Risk-based Capital Guidelines: Market Risk... 1 3 Market Risk... 1 3.1

Statement of Financial Condition

Financial Report for the 14th Business Year 5-1, Marunouchi 1-Chome, Chiyoda-ku, Tokyo Citigroup Global Markets Japan Inc. Rodrigo Zorrilla, Representative Director, President and CEO Statement of Financial

Financial Report for the 14th Business Year 5-1, Marunouchi 1-Chome, Chiyoda-ku, Tokyo Citigroup Global Markets Japan Inc. Rodrigo Zorrilla, Representative Director, President and CEO Statement of Financial

Measuring Exchange Rate Fluctuations Risk Using the Value-at-Risk

Journal of Applied Finance & Banking, vol.2, no.3, 2012, 65-79 ISSN: 1792-6580 (print version), 1792-6599 (online) International Scientific Press, 2012 Measuring Exchange Rate Fluctuations Risk Using the

Journal of Applied Finance & Banking, vol.2, no.3, 2012, 65-79 ISSN: 1792-6580 (print version), 1792-6599 (online) International Scientific Press, 2012 Measuring Exchange Rate Fluctuations Risk Using the

ERM Learning Objectives

ERM Learning Objectives INTRODUCTION These Learning Objectives are expressed in terms of the knowledge required of an expert * in enterprise risk management (ERM). The Learning Objectives are organized

ERM Learning Objectives INTRODUCTION These Learning Objectives are expressed in terms of the knowledge required of an expert * in enterprise risk management (ERM). The Learning Objectives are organized

Financial Risk Manager (FRM ) Examination. 2011 Practice Exam Part I / Part II

Examination. 2011 Practice Exam Part I / Part II") Financial Risk Manager (FRM ) Examination 2011 Practice Exam Part I / Part II TABLE OF CONTENTS Introduction...............................................................1 2011 FRM Part I Practice Exam

Financial Risk Manager (FRM ) Examination 2011 Practice Exam Part I / Part II TABLE OF CONTENTS Introduction...............................................................1 2011 FRM Part I Practice Exam

MULTIPLE REGRESSION AND ISSUES IN REGRESSION ANALYSIS

MULTIPLE REGRESSION AND ISSUES IN REGRESSION ANALYSIS MSR = Mean Regression Sum of Squares MSE = Mean Squared Error RSS = Regression Sum of Squares SSE = Sum of Squared Errors/Residuals α = Level of Significance

MULTIPLE REGRESSION AND ISSUES IN REGRESSION ANALYSIS MSR = Mean Regression Sum of Squares MSE = Mean Squared Error RSS = Regression Sum of Squares SSE = Sum of Squared Errors/Residuals α = Level of Significance

Test3. Pessimistic Most Likely Optimistic Total Revenues 30 50 65 Total Costs -25-20 -15

Test3 1. The market value of Charcoal Corporation's common stock is $20 million, and the market value of its riskfree debt is $5 million. The beta of the company's common stock is 1.25, and the market

Test3 1. The market value of Charcoal Corporation's common stock is $20 million, and the market value of its riskfree debt is $5 million. The beta of the company's common stock is 1.25, and the market

Investec Gold ETN. What is the Investec Gold ETN? Why invest in Investec Gold ETN?

Gold ETN Investec Gold ETN Product Name Investec Gold ETN Exchange Traded Note Underlying Physical Spot Gold Price (London) Issuer Investec Bank Limited Maturity Date October 2017 Exchange Johannesburg

Gold ETN Investec Gold ETN Product Name Investec Gold ETN Exchange Traded Note Underlying Physical Spot Gold Price (London) Issuer Investec Bank Limited Maturity Date October 2017 Exchange Johannesburg

Introduction to Statistical Computing in Microsoft Excel By Hector D. Flores; [email protected], and Dr. J.A. Dobelman

Introduction to Statistical Computing in Microsoft Excel By Hector D. Flores; [email protected], and Dr. J.A. Dobelman Statistics lab will be mainly focused on applying what you have learned in class with

Introduction to Statistical Computing in Microsoft Excel By Hector D. Flores; [email protected], and Dr. J.A. Dobelman Statistics lab will be mainly focused on applying what you have learned in class with

Foreign Exchange Market INTERNATIONAL FINANCE. Function and Structure of FX Market. Market Characteristics. Market Attributes. Trading in Markets

Foreign Exchange Market INTERNATIONAL FINANCE Chapter 5 Encompasses: Conversion of purchasing power across currencies Bank deposits of foreign currency Credit denominated in foreign currency Foreign trade

Foreign Exchange Market INTERNATIONAL FINANCE Chapter 5 Encompasses: Conversion of purchasing power across currencies Bank deposits of foreign currency Credit denominated in foreign currency Foreign trade

Alternative Investing

Alternative Investing An important piece of the puzzle Improve diversification Manage portfolio risk Target absolute returns Innovation is our capital. Make it yours. Manage Risk and Enhance Performance

Alternative Investing An important piece of the puzzle Improve diversification Manage portfolio risk Target absolute returns Innovation is our capital. Make it yours. Manage Risk and Enhance Performance

Index Volatility Futures in Asset Allocation: A Hedging Framework

Investment Research Index Volatility Futures in Asset Allocation: A Hedging Framework Jai Jacob, Portfolio Manager/Analyst, Lazard Asset Management Emma Rasiel, PhD, Assistant Professor of the Practice

Investment Research Index Volatility Futures in Asset Allocation: A Hedging Framework Jai Jacob, Portfolio Manager/Analyst, Lazard Asset Management Emma Rasiel, PhD, Assistant Professor of the Practice

1. HOW DOES FOREIGN EXCHANGE TRADING WORK?

XV. Important additional information on forex transactions / risks associated with foreign exchange transactions (also in the context of forward exchange transactions) The following information is given

XV. Important additional information on forex transactions / risks associated with foreign exchange transactions (also in the context of forward exchange transactions) The following information is given

Global Investing: The Importance of Currency Returns and Currency Hedging

Global Investing: The Importance of Currency Returns and Currency Hedging There is a continuing trend for investors to reduce their home bias in equity allocation and increase the allocation to international

Global Investing: The Importance of Currency Returns and Currency Hedging There is a continuing trend for investors to reduce their home bias in equity allocation and increase the allocation to international

Introducing the Loan Pool Specific Factor in CreditManager

Technical Note Introducing the Loan Pool Specific Factor in CreditManager A New Tool for Decorrelating Loan Pools Driven by the Same Market Factor Attila Agod, András Bohák, Tamás Mátrai Attila.Agod@ Andras.Bohak@

Technical Note Introducing the Loan Pool Specific Factor in CreditManager A New Tool for Decorrelating Loan Pools Driven by the Same Market Factor Attila Agod, András Bohák, Tamás Mátrai Attila.Agod@ Andras.Bohak@

Disclosure of European Embedded Value as of March 31, 2015

UNOFFICIAL TRANSLATION Although the Company pays close attention to provide English translation of the information disclosed in Japanese, the Japanese original prevails over its English translation in

UNOFFICIAL TRANSLATION Although the Company pays close attention to provide English translation of the information disclosed in Japanese, the Japanese original prevails over its English translation in

Financial Assets Behaving Badly The Case of High Yield Bonds. Chris Kantos Newport Seminar June 2013

Financial Assets Behaving Badly The Case of High Yield Bonds Chris Kantos Newport Seminar June 2013 Main Concepts for Today The most common metric of financial asset risk is the volatility or standard

Financial Assets Behaving Badly The Case of High Yield Bonds Chris Kantos Newport Seminar June 2013 Main Concepts for Today The most common metric of financial asset risk is the volatility or standard

Understanding Managed Futures

Understanding Managed Futures February 2009 Introduction Managed futures have proven their strengths as an investment since the first funds were launched in the early 1970s. For over more than 30 years,

Understanding Managed Futures February 2009 Introduction Managed futures have proven their strengths as an investment since the first funds were launched in the early 1970s. For over more than 30 years,

Use the table for the questions 18 and 19 below.

Use the table for the questions 18 and 19 below. The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 1 3 4 5 Price

Use the table for the questions 18 and 19 below. The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 1 3 4 5 Price

Understanding Currency

Understanding Currency Overlay July 2010 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract As portfolios have expanded to include international investments, investors must be aware of

Understanding Currency Overlay July 2010 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract As portfolios have expanded to include international investments, investors must be aware of

Assignment 10 (Chapter 11)

") Assignment 10 (Chapter 11) 1. Which of the following tends to cause the U.S. dollar to appreciate in value? a) An increase in U.S. prices above foreign prices b) Rapid economic growth in foreign countries

Assignment 10 (Chapter 11) 1. Which of the following tends to cause the U.S. dollar to appreciate in value? a) An increase in U.S. prices above foreign prices b) Rapid economic growth in foreign countries

Makeup Exam MØA 155 Financial Economics February 2010 Permitted Material: Calculator, Norwegian/English Dictionary

University of Stavanger (UiS) Stavanger Masters Program Makeup Exam MØA 155 Financial Economics February 2010 Permitted Material: Calculator, Norwegian/English Dictionary The number in brackets is the

University of Stavanger (UiS) Stavanger Masters Program Makeup Exam MØA 155 Financial Economics February 2010 Permitted Material: Calculator, Norwegian/English Dictionary The number in brackets is the

2) The three categories of forecasting models are time series, quantitative, and qualitative. 2)

The three categories of forecasting models are time series, quantitative, and qualitative. 2)") Exam Name TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) Regression is always a superior forecasting method to exponential smoothing, so regression should be used

Exam Name TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) Regression is always a superior forecasting method to exponential smoothing, so regression should be used

Chapter 3.1. Capital and Trade Flow Drive Currency Values

Chapter 3.1 Capital and Trade Flow Drive Currency Values 0 CAPITAL AND TRADE FLOW DRIVE CURRENCY VALUES Supply and demand are the simple concepts behind all price movement in the forex market, and no two

Chapter 3.1 Capital and Trade Flow Drive Currency Values 0 CAPITAL AND TRADE FLOW DRIVE CURRENCY VALUES Supply and demand are the simple concepts behind all price movement in the forex market, and no two

Module 5: Multiple Regression Analysis

Using Statistical Data Using to Make Statistical Decisions: Data Multiple to Make Regression Decisions Analysis Page 1 Module 5: Multiple Regression Analysis Tom Ilvento, University of Delaware, College

Using Statistical Data Using to Make Statistical Decisions: Data Multiple to Make Regression Decisions Analysis Page 1 Module 5: Multiple Regression Analysis Tom Ilvento, University of Delaware, College

Derivatives, Measurement and Hedge Accounting

Derivatives, Measurement and Hedge Accounting IAS 39 11 June 2008 Contents Derivatives and embedded derivatives Definition Sample of products Accounting treatment Measurement Active market VS Inactive

Derivatives, Measurement and Hedge Accounting IAS 39 11 June 2008 Contents Derivatives and embedded derivatives Definition Sample of products Accounting treatment Measurement Active market VS Inactive

RISK DISCLOSURE FOR FINANCIAL INSTRUMENTS

RISK DISCLOSURE FOR FINANCIAL INSTRUMENTS ROBOOPTION TN / ROBOFOREX (CY) LTD RISK DISCLOSURE FOR FINANCIAL INSTRUMENTS RoboOption is a trade name of RoboForex (CY) Ltd (hereinafter called the Company )

RISK DISCLOSURE FOR FINANCIAL INSTRUMENTS ROBOOPTION TN / ROBOFOREX (CY) LTD RISK DISCLOSURE FOR FINANCIAL INSTRUMENTS RoboOption is a trade name of RoboForex (CY) Ltd (hereinafter called the Company )

KEY INFORMATION DOCUMENT

KEY INFORMATION DOCUMENT PSG WEALTH CURRENCY FUTURES TRADING ACCOUNT TRADING ACCOUNT PAGE 0 This document is a summary of key information about the PSG Wealth currency futures trading account. It will

KEY INFORMATION DOCUMENT PSG WEALTH CURRENCY FUTURES TRADING ACCOUNT TRADING ACCOUNT PAGE 0 This document is a summary of key information about the PSG Wealth currency futures trading account. It will

Statistical Tests for Multiple Forecast Comparison

Statistical Tests for Multiple Forecast Comparison Roberto S. Mariano (Singapore Management University & University of Pennsylvania) Daniel Preve (Uppsala University) June 6-7, 2008 T.W. Anderson Conference,

Statistical Tests for Multiple Forecast Comparison Roberto S. Mariano (Singapore Management University & University of Pennsylvania) Daniel Preve (Uppsala University) June 6-7, 2008 T.W. Anderson Conference,

A Primer on Forecasting Business Performance

A Primer on Forecasting Business Performance There are two common approaches to forecasting: qualitative and quantitative. Qualitative forecasting methods are important when historical data is not available.

A Primer on Forecasting Business Performance There are two common approaches to forecasting: qualitative and quantitative. Qualitative forecasting methods are important when historical data is not available.

Examination II. Fixed income valuation and analysis. Economics

Examination II Fixed income valuation and analysis Economics Questions Foundation examination March 2008 FIRST PART: Multiple Choice Questions (48 points) Hereafter you must answer all 12 multiple choice

Examination II Fixed income valuation and analysis Economics Questions Foundation examination March 2008 FIRST PART: Multiple Choice Questions (48 points) Hereafter you must answer all 12 multiple choice

PROFUNDS GROUP INVESTOR EDUCATION GUIDE 1 GEARED INVESTING. An introduction to leveraged and inverse funds

PROFUNDS GROUP INVESTOR EDUCATION GUIDE 1 GEARED INVESTING An introduction to leveraged and inverse funds GEARED FUNDS have generated a great deal of interest in recent years. Also known as LEVERAGED AND

PROFUNDS GROUP INVESTOR EDUCATION GUIDE 1 GEARED INVESTING An introduction to leveraged and inverse funds GEARED FUNDS have generated a great deal of interest in recent years. Also known as LEVERAGED AND

MBA 8230 Corporation Finance (Part II) Practice Final Exam #2

Practice Final Exam #2") MBA 8230 Corporation Finance (Part II) Practice Final Exam #2 1. Which of the following input factors, if increased, would result in a decrease in the value of a call option? a. the volatility of the company's

MBA 8230 Corporation Finance (Part II) Practice Final Exam #2 1. Which of the following input factors, if increased, would result in a decrease in the value of a call option? a. the volatility of the company's

VARIABLES EXPLAINING THE PRICE OF GOLD MINING STOCKS

VARIABLES EXPLAINING THE PRICE OF GOLD MINING STOCKS Jimmy D. Moss, Lamar University Donald I. Price, Lamar University ABSTRACT The purpose of this study is to examine the relationship between an index

VARIABLES EXPLAINING THE PRICE OF GOLD MINING STOCKS Jimmy D. Moss, Lamar University Donald I. Price, Lamar University ABSTRACT The purpose of this study is to examine the relationship between an index

16 : Demand Forecasting

16 : Demand Forecasting 1 Session Outline Demand Forecasting Subjective methods can be used only when past data is not available. When past data is available, it is advisable that firms should use statistical

16 : Demand Forecasting 1 Session Outline Demand Forecasting Subjective methods can be used only when past data is not available. When past data is available, it is advisable that firms should use statistical

Investment Statistics: Definitions & Formulas

Investment Statistics: Definitions & Formulas The following are brief descriptions and formulas for the various statistics and calculations available within the ease Analytics system. Unless stated otherwise,

Investment Statistics: Definitions & Formulas The following are brief descriptions and formulas for the various statistics and calculations available within the ease Analytics system. Unless stated otherwise,

Northern Trust Corporation

Northern Trust Corporation Market Risk Disclosures June 30, 2014 Market Risk Disclosures Effective January 1, 2013, Northern Trust Corporation (Northern Trust) adopted revised risk based capital guidelines

Northern Trust Corporation Market Risk Disclosures June 30, 2014 Market Risk Disclosures Effective January 1, 2013, Northern Trust Corporation (Northern Trust) adopted revised risk based capital guidelines

VDAX -NEW. Deutsche Börse AG Frankfurt am Main, April 2005

VDAX -NEW Deutsche Börse AG Frankfurt am Main, April 2005 With VDAX -NEW, Deutsche Börse quantifies future market expectations of the German stock market Overview VDAX -NEW Quantifies the expected risk

VDAX -NEW Deutsche Börse AG Frankfurt am Main, April 2005 With VDAX -NEW, Deutsche Börse quantifies future market expectations of the German stock market Overview VDAX -NEW Quantifies the expected risk

Investment Opportunities When Currencies Fluctuate: Taking Advantage of FX Volatility

Investment Opportunities When Currencies Fluctuate: Taking Advantage of FX Volatility Shaun Osborne, TD Securities AGENDA What drives currency markets? What is the outlook for the USD, CAD Appreciation

Investment Opportunities When Currencies Fluctuate: Taking Advantage of FX Volatility Shaun Osborne, TD Securities AGENDA What drives currency markets? What is the outlook for the USD, CAD Appreciation

Generating Random Numbers Variance Reduction Quasi-Monte Carlo. Simulation Methods. Leonid Kogan. MIT, Sloan. 15.450, Fall 2010

Simulation Methods Leonid Kogan MIT, Sloan 15.450, Fall 2010 c Leonid Kogan ( MIT, Sloan ) Simulation Methods 15.450, Fall 2010 1 / 35 Outline 1 Generating Random Numbers 2 Variance Reduction 3 Quasi-Monte

Simulation Methods Leonid Kogan MIT, Sloan 15.450, Fall 2010 c Leonid Kogan ( MIT, Sloan ) Simulation Methods 15.450, Fall 2010 1 / 35 Outline 1 Generating Random Numbers 2 Variance Reduction 3 Quasi-Monte

CITIGROUP INC. BASEL II.5 MARKET RISK DISCLOSURES AS OF AND FOR THE PERIOD ENDED MARCH 31, 2013

CITIGROUP INC. BASEL II.5 MARKET RISK DISCLOSURES AS OF AND FOR THE PERIOD ENDED MARCH 31, 2013 DATED AS OF MAY 15, 2013 Table of Contents Qualitative Disclosures Basis of Preparation and Review... 3 Risk

CITIGROUP INC. BASEL II.5 MARKET RISK DISCLOSURES AS OF AND FOR THE PERIOD ENDED MARCH 31, 2013 DATED AS OF MAY 15, 2013 Table of Contents Qualitative Disclosures Basis of Preparation and Review... 3 Risk

Financial Management in IB. Exercises 1. I. Foreign Exchange Market

Financial Management in IB Exercises 1 1 I. Foreign Exchange Market Locational Arbitrage Paris Interbank market: EUR/USD 1,2548/1,2552 London Interbank market: EUR/USD 1,2543/1,2546 Is locational arbitrage

Financial Management in IB Exercises 1 1 I. Foreign Exchange Market Locational Arbitrage Paris Interbank market: EUR/USD 1,2548/1,2552 London Interbank market: EUR/USD 1,2543/1,2546 Is locational arbitrage

Chapter 9. Forecasting Exchange Rates. Lecture Outline. Why Firms Forecast Exchange Rates

Chapter 9 Forecasting Exchange Rates Lecture Outline Why Firms Forecast Exchange Rates Forecasting Techniques Technical Forecasting Fundamental Forecasting Market-Based Forecasting Mixed Forecasting Forecasting

Chapter 9 Forecasting Exchange Rates Lecture Outline Why Firms Forecast Exchange Rates Forecasting Techniques Technical Forecasting Fundamental Forecasting Market-Based Forecasting Mixed Forecasting Forecasting

Credit Risk Stress Testing

1 Credit Risk Stress Testing Stress Testing Features of Risk Evaluator 1. 1. Introduction Risk Evaluator is a financial tool intended for evaluating market and credit risk of single positions or of large

1 Credit Risk Stress Testing Stress Testing Features of Risk Evaluator 1. 1. Introduction Risk Evaluator is a financial tool intended for evaluating market and credit risk of single positions or of large

PITFALLS IN TIME SERIES ANALYSIS. Cliff Hurvich Stern School, NYU

PITFALLS IN TIME SERIES ANALYSIS Cliff Hurvich Stern School, NYU The t -Test If x 1,..., x n are independent and identically distributed with mean 0, and n is not too small, then t = x 0 s n has a standard

PITFALLS IN TIME SERIES ANALYSIS Cliff Hurvich Stern School, NYU The t -Test If x 1,..., x n are independent and identically distributed with mean 0, and n is not too small, then t = x 0 s n has a standard

Non Linear Dependence Structures: a Copula Opinion Approach in Portfolio Optimization

Non Linear Dependence Structures: a Copula Opinion Approach in Portfolio Optimization Jean- Damien Villiers ESSEC Business School Master of Sciences in Management Grande Ecole September 2013 1 Non Linear

Non Linear Dependence Structures: a Copula Opinion Approach in Portfolio Optimization Jean- Damien Villiers ESSEC Business School Master of Sciences in Management Grande Ecole September 2013 1 Non Linear

U.S. SHORT TERM. Equity Risk Model IDENTIFY ANALYZE QUANTIFY NORTHFIELD

U.S. SHORT TERM Equity Risk Model IDENTIFY ANALYZE QUANTIFY NORTHFIELD FEB-3-2015 U.S. Short Term Equity Risk Model Table of Contents INTRODUCTION... 2 Forecasting Short-Term Risk... 2 Statistical Factor

U.S. SHORT TERM Equity Risk Model IDENTIFY ANALYZE QUANTIFY NORTHFIELD FEB-3-2015 U.S. Short Term Equity Risk Model Table of Contents INTRODUCTION... 2 Forecasting Short-Term Risk... 2 Statistical Factor

Implied Volatility Skews in the Foreign Exchange Market. Empirical Evidence from JPY and GBP: 1997-2002

Implied Volatility Skews in the Foreign Exchange Market Empirical Evidence from JPY and GBP: 1997-2002 The Leonard N. Stern School of Business Glucksman Institute for Research in Securities Markets Faculty

Implied Volatility Skews in the Foreign Exchange Market Empirical Evidence from JPY and GBP: 1997-2002 The Leonard N. Stern School of Business Glucksman Institute for Research in Securities Markets Faculty

up to 1 year 2,391 3.27 1 to 5 years 3,441 4.70 6 to 10 years 3,554 4.86 11 to 20 years 1,531 2.09 over 20 years 62,226 85.08 TOTAL 73,143 100.

SECTION 2 RISKS OF INSURANCE COMPANIES 2.1 INSURANCE RISKS QUALITATIVE AND QUANTITATIVE INFORMATION Life business The typical risks of the life insurance portfolio (managed by Intesa Sanpaolo Vita, Intesa

SECTION 2 RISKS OF INSURANCE COMPANIES 2.1 INSURANCE RISKS QUALITATIVE AND QUANTITATIVE INFORMATION Life business The typical risks of the life insurance portfolio (managed by Intesa Sanpaolo Vita, Intesa

POINT Innovative Multi-Asset Portfolio Analysis

Index, Portfolio and Risk Solutions POINT Innovative Multi-Asset Portfolio Analysis The Difference Is Clear POINT: Dynamic Decision Support Flexible portfolio and index reporting Draw from our vast database

Index, Portfolio and Risk Solutions POINT Innovative Multi-Asset Portfolio Analysis The Difference Is Clear POINT: Dynamic Decision Support Flexible portfolio and index reporting Draw from our vast database

ROBECO MULTI MARKET BOND JUL 03/13, USD

Benchmark: ATTRACTIVE YIELD IN COMBINATION WITH A SOLID FOUNDATION T HE PRO D UC T IN BRIEF : Issuer: Rabobank Nederland Currency: US dollars Nominal value: USD 1,000 Issue price: 100% Issue date: 15 July

Benchmark: ATTRACTIVE YIELD IN COMBINATION WITH A SOLID FOUNDATION T HE PRO D UC T IN BRIEF : Issuer: Rabobank Nederland Currency: US dollars Nominal value: USD 1,000 Issue price: 100% Issue date: 15 July

Exotic Options Trading

Exotic Options Trading Frans de Weert John Wiley & Sons, Ltd Preface Acknowledgements 1 Introduction 2 Conventional Options, Forwards and Greeks 2.1 Call and Put Options and Forwards 2.2 Pricing Calls

Exotic Options Trading Frans de Weert John Wiley & Sons, Ltd Preface Acknowledgements 1 Introduction 2 Conventional Options, Forwards and Greeks 2.1 Call and Put Options and Forwards 2.2 Pricing Calls

Market Risk Analysis. Quantitative Methods in Finance. Volume I. The Wiley Finance Series

Brochure More information from http://www.researchandmarkets.com/reports/2220051/ Market Risk Analysis. Quantitative Methods in Finance. Volume I. The Wiley Finance Series Description: Written by leading

Brochure More information from http://www.researchandmarkets.com/reports/2220051/ Market Risk Analysis. Quantitative Methods in Finance. Volume I. The Wiley Finance Series Description: Written by leading

Facilitating On-Demand Risk and Actuarial Analysis in MATLAB. Timo Salminen, CFA, FRM Model IT

Facilitating On-Demand Risk and Actuarial Analysis in MATLAB Timo Salminen, CFA, FRM Model IT Introduction It is common that insurance companies can valuate their liabilities only quarterly Sufficient

Facilitating On-Demand Risk and Actuarial Analysis in MATLAB Timo Salminen, CFA, FRM Model IT Introduction It is common that insurance companies can valuate their liabilities only quarterly Sufficient

INCORPORATION OF LIQUIDITY RISKS INTO EQUITY PORTFOLIO RISK ESTIMATES. Dan dibartolomeo September 2010

INCORPORATION OF LIQUIDITY RISKS INTO EQUITY PORTFOLIO RISK ESTIMATES Dan dibartolomeo September 2010 GOALS FOR THIS TALK Assert that liquidity of a stock is properly measured as the expected price change,

INCORPORATION OF LIQUIDITY RISKS INTO EQUITY PORTFOLIO RISK ESTIMATES Dan dibartolomeo September 2010 GOALS FOR THIS TALK Assert that liquidity of a stock is properly measured as the expected price change,

Hedge Effectiveness Testing

Hedge Effectiveness Testing Using Regression Analysis Ira G. Kawaller, Ph.D. Kawaller & Company, LLC Reva B. Steinberg BDO Seidman LLP When companies use derivative instruments to hedge economic exposures,

Hedge Effectiveness Testing Using Regression Analysis Ira G. Kawaller, Ph.D. Kawaller & Company, LLC Reva B. Steinberg BDO Seidman LLP When companies use derivative instruments to hedge economic exposures,

Item 7A. Quantitative and Qualitative Disclosures about Market Risk. Risk Management

Item 7A. Quantitative and Qualitative Disclosures about Market Risk. Risk Management Risk Management Policy and Control Structure. Risk is an inherent part of the Company s business and activities. The

Item 7A. Quantitative and Qualitative Disclosures about Market Risk. Risk Management Risk Management Policy and Control Structure. Risk is an inherent part of the Company s business and activities. The

Department of Economics and Related Studies Financial Market Microstructure. Topic 1 : Overview and Fixed Cost Models of Spreads

Session 2008-2009 Department of Economics and Related Studies Financial Market Microstructure Topic 1 : Overview and Fixed Cost Models of Spreads 1 Introduction 1.1 Some background Most of what is taught

Session 2008-2009 Department of Economics and Related Studies Financial Market Microstructure Topic 1 : Overview and Fixed Cost Models of Spreads 1 Introduction 1.1 Some background Most of what is taught

Review Jeopardy. Blue vs. Orange. Review Jeopardy

Review Jeopardy Blue vs. Orange Review Jeopardy Jeopardy Round Lectures 0-3 Jeopardy Round $200 How could I measure how far apart (i.e. how different) two observations, y 1 and y 2, are from each other?

Review Jeopardy Blue vs. Orange Review Jeopardy Jeopardy Round Lectures 0-3 Jeopardy Round $200 How could I measure how far apart (i.e. how different) two observations, y 1 and y 2, are from each other?

MSCI Global Minimum Volatility Indices Methodology

MSCI Global Minimum Volatility Indices Methodology Table of Contents Section 1: Introduction... 3 Section 2: Characteristics of MSCI Minimum Volatility Indices... 3 Section 3: Constructing the MSCI Minimum

MSCI Global Minimum Volatility Indices Methodology Table of Contents Section 1: Introduction... 3 Section 2: Characteristics of MSCI Minimum Volatility Indices... 3 Section 3: Constructing the MSCI Minimum

CHAPTER 15 INTERNATIONAL PORTFOLIO INVESTMENT SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 15 INTERNATIONAL PORTFOLIO INVESTMENT SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. What factors are responsible for the recent surge in international portfolio

CHAPTER 15 INTERNATIONAL PORTFOLIO INVESTMENT SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. What factors are responsible for the recent surge in international portfolio

SYSTEMS OF REGRESSION EQUATIONS

SYSTEMS OF REGRESSION EQUATIONS 1. MULTIPLE EQUATIONS y nt = x nt n + u nt, n = 1,...,N, t = 1,...,T, x nt is 1 k, and n is k 1. This is a version of the standard regression model where the observations

SYSTEMS OF REGRESSION EQUATIONS 1. MULTIPLE EQUATIONS y nt = x nt n + u nt, n = 1,...,N, t = 1,...,T, x nt is 1 k, and n is k 1. This is a version of the standard regression model where the observations

How the Greeks would have hedged correlation risk of foreign exchange options

How the Greeks would have hedged correlation risk of foreign exchange options Uwe Wystup Commerzbank Treasury and Financial Products Neue Mainzer Strasse 32 36 60261 Frankfurt am Main GERMANY [email protected]

How the Greeks would have hedged correlation risk of foreign exchange options Uwe Wystup Commerzbank Treasury and Financial Products Neue Mainzer Strasse 32 36 60261 Frankfurt am Main GERMANY [email protected]

CURRENCY HEDGING IN THE EMERGING MARKETS: ALL PAIN, NO GAIN

March 2016 Tim Atwill, Ph.D., CFA Head of Investment Strategy Parametric 1918 Eighth Avenue Suite 3100 Seattle, WA 98101 T 206 694 5575 F 206 694 5581 www.parametricportfolio.com CURRENCY HEDGING IN THE

March 2016 Tim Atwill, Ph.D., CFA Head of Investment Strategy Parametric 1918 Eighth Avenue Suite 3100 Seattle, WA 98101 T 206 694 5575 F 206 694 5581 www.parametricportfolio.com CURRENCY HEDGING IN THE