Global Currency Hedging

|

|

|

- Rodger Lee

- 10 years ago

- Views:

Transcription

1 Global Currency Hedging John Y. Campbell Harvard University Arrowstreet Capital, L.P. May 16, 2010

2 Global Currency Hedging Joint work with Karine Serfaty-de Medeiros of OC&C Strategy Consultants and Luis Viceira of Harvard Business School Published in Journal of Finance, February

3 Global Currency Hedging Investment in foreign equity requires an implicit currency position that can be hedged in any desired proportion using forward contracts. What is the optimal hedging policy for an international investor? How can currencies be used to manage portfolio risks? Think of currencies as assets that can be added to a global equity (or bond) portfolio. Assume zero expected excess currency returns to calculate risk management (RM) demand for currencies. The optimal weights are determined by the betas of currency returns with the equity (or bond) returns. These weights imply an optimal currency hedging policy 2

demand for currencies.")

4 Classifying Currencies The bottom line: A classification of currencies Reserve currencies (e.g. US dollar, the euro and Swiss franc) strengthen when world equity markets go down. Commodity-dependent currencies (e.g. Australian dollar, Canadian dollar) strengthen when world equity markets go up. Neutral currencies (e.g. Japanese yen, British pound) are close to uncorrelated with equity markets. 3

are close to uncorrelated with equity markets.")

5 Our Findings Optimal RM currency demands Equity investors should hold reserve currencies Currencies are largely uncorrelated with bonds, so bond market investors should hold their base currency Currency risk and return Reserve currencies have had lower average interest rates and average returns But the return differences are modest Risk management and the carry trade Movements in interest differentials predict currency returns and hence speculative currency demands: the carry trade They predict risks and RM currency demands in, if anything, the same direction: the super carry trade 4

6 Our Data IMF s IFS database: Exchange rates Nominal interest rates, mostly three-month rates Long-term bond yields. MSCI database: Stock returns. We report results for seven countries (or regions): Euroland : Germany, France, Italy, and the Netherlands i.e. 78% to 92% of the market value of the 1999 euro countries Australia, Canada, Japan, Switzerland, UK and US. Monthly data, 1975:7 2005:12. 5

7 Single-Country Stock Portfolios 6

8 7

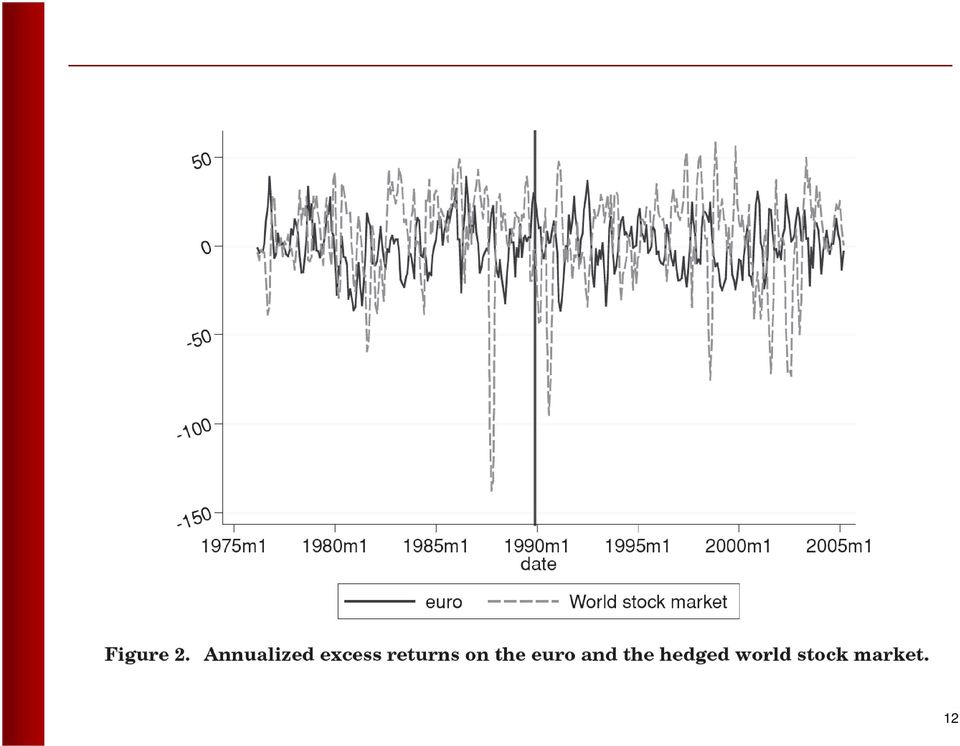

9 Equal-Weighted Global Stock Portfolio 7 countries: 14% invested in each country stock market. The investor can use the full array of currencies to manage risk. What currency exposure minimizes the volatility of this portfolio? In this case, when hedging using the full range of available currencies, the vector of optimal currency positions is independent of the base country. 8

10 9

11 Have Things Changed Over Time? In the 1990 s the euro started to move more strongly against world equity markets, making it a reserve currency. The Swiss franc moves with the euro, so it also became a reserve currency. The negative comovement of the dollar with world equity markets appears to have weakened. But what about the global financial crisis? Hold that thought. 10

12 11

13 12

14 Equal-Weighted Global Bond Portfolio 13

15 5 14

16 Currency Returns in Equilibrium Currencies systematically differ in their comovements with global stock markets. In equilibrium investors must be willing to hold all currencies (Black, 1990). Are currencies priced so that normal currencies offer higher average returns than reserve currencies? If so, governments with reserve currencies benefit from lower funding costs: the exorbitant privilege 15

17 Currency Returns in Equilibrium Reserve currencies do tend to have lower average interest rates than other currencies, with the exception of the Japanese yen Average interest rates also correlate cross-sectionally with average currency returns (an aspect of the forward premium puzzle) We plot average excess returns against betas with a value-weighted currency-hedged world index 16

We plot average excess returns against betas with a value-weighted currency-hedged")

18 Figure 3 R 2 = 48%; Slope = 3.2% 17

19 Figure 4 18

20 Currency Returns in Equilibrium Overall, there exist differences in average realized currency returns that correlate with currency risks. However, these average realized returns have been modest particularly so in the case of the US dollar and the euro 19

21 Conditional Currency Risk Management The ability of interest differentials to predict excess currency returns is well known Forward premium puzzle for academics Carry trade for FX market participants Part of this ability comes from long-run average differences in interest rates and excess currency returns But part of it comes from common time-series variation in interest rates and excess currency returns Do temporary movements in interest rates predict similar movements in covariances of currencies with equities? Do currency hedgers take the opposite side of the carry trade? 20

22 The Super Carry Trade In fact, when the base currency is a reserve currency, RM demands reinforce the carry trade rather than offsetting it One way to see this is to introduce a synthetic carrytrade currency Long the three currencies with highest interest rates Short the three currencies with lowest interest rates The synthetic currency has negative RM demand on its own, but positive RM demand in combination with other currencies 21

23 22

24 How Much Is Volatility Reduced? Table 7 reports standard deviations for global equity and bond portfolios hedged in alternative ways Equity portfolios: Large volatility reductions from full hedging when base currency is a reserve currency, small reductions or even increases when base currency is commodity-dependent Further substantial volatility reductions from optimal unconditional hedging Little benefit from conditional hedging strategies Bond portfolios: Large volatility reductions from full hedging 23

25 Table 7 24

26 Currencies in the Financial Crisis Dollar falls on doubts for its safe-haven status. By Peter Garnham. The dollar suffered yesterday as coordinated action from global central banks to ease liquidity tension in the world's money markets dented its newly found status as a safe-haven currency. Analysts said the dollar had previously benefited as worries over the state of the global financial system heightened risk aversion, prompting US investors to repatriate funds that had been invested in global equities, while lower inflation expectations had supported demand for US bonds. "In a world where cross-border equity investing collapses and bond flows remain stable, there is a net inflow back into the dollar", said Michael Metcalfe of State Street Global Markets. However, analysts said the decision by global central banks to inject $180bn of emergency dollar liquidity into the market had helped boost risk appetite and damp demand for the dollar... The dollar's losses were largest against the high-yielding Australian and New Zealand dollars, which had been the worst hit among leading currencies during the recent market turmoil. Financial Times, September 19,

27 Currencies in the Financial Crisis Several aspects of the financial crisis are consistent with the message of our paper Strong US dollar Weak Australian dollar Failure of the carry trade as low-interest-rate funding currencies strengthened The major exception is the weakness of the euro Probably reflects the fiscal strain on the eurozone implied by the magnitude of the crisis Market lacked faith that eurozone institutions could handle Greece and other weak sovereigns 26

28 Open Questions Why are reserve currencies attractive stores of value for equity investors? Macroeconomic fundamentals, e.g. stable long-term inflation expectations which keep inflation procyclical (Campbell, Sunderam, and Viceira 2008) Financial fundamentals, e.g. liquidity provision Amplification as flight to quality creates endogenous negative correlation of currency and equity returns Will these correlations change? Concern about the risk of a dollar crisis if investors lose faith in the US fiscal position (Rogoff) Possibility that aggressive monetary policy will destabilize inflation expectations. 27

How To Get A Better Return From International Bonds

International fixed income: The investment case Why international fixed income? International bonds currently make up the largest segment of the securities market Ever-increasing globalization and access

International fixed income: The investment case Why international fixed income? International bonds currently make up the largest segment of the securities market Ever-increasing globalization and access

Vanguard research July 2014

The Understanding buck stops here: the hedge return : Vanguard The impact money of currency market hedging funds in foreign bonds Vanguard research July 214 Charles Thomas, CFA; Paul M. Bosse, CFA Hedging

The Understanding buck stops here: the hedge return : Vanguard The impact money of currency market hedging funds in foreign bonds Vanguard research July 214 Charles Thomas, CFA; Paul M. Bosse, CFA Hedging

Discussion of Global Liquidity and Procyclicality by Hyun Song Shin

International Monetary Fund Discussion of Global Liquidity and Procyclicality by Hyun Song Shin Maurice Obstfeld Economic Counsellor June 8, 2015 World Bank Washington DC Main themes: U.S. financial conditions

International Monetary Fund Discussion of Global Liquidity and Procyclicality by Hyun Song Shin Maurice Obstfeld Economic Counsellor June 8, 2015 World Bank Washington DC Main themes: U.S. financial conditions

CHAPTER 15 INTERNATIONAL PORTFOLIO INVESTMENT SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 15 INTERNATIONAL PORTFOLIO INVESTMENT SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. What factors are responsible for the recent surge in international portfolio

CHAPTER 15 INTERNATIONAL PORTFOLIO INVESTMENT SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. What factors are responsible for the recent surge in international portfolio

How Hedging Can Substantially Reduce Foreign Stock Currency Risk

Possible losses from changes in currency exchange rates are a risk of investing unhedged in foreign stocks. While a stock may perform well on the London Stock Exchange, if the British pound declines against

Possible losses from changes in currency exchange rates are a risk of investing unhedged in foreign stocks. While a stock may perform well on the London Stock Exchange, if the British pound declines against

Purer return and reduced volatility: Hedging currency risk in international-equity portfolios

Purer return and reduced volatility: Hedging currency risk in international-equity portfolios Currency-hedged exchange-traded funds (ETFs) may offer investors a compelling way to more precisely access

Purer return and reduced volatility: Hedging currency risk in international-equity portfolios Currency-hedged exchange-traded funds (ETFs) may offer investors a compelling way to more precisely access

KEY INFORMATION DOCUMENT

KEY INFORMATION DOCUMENT PSG WEALTH CURRENCY FUTURES TRADING ACCOUNT TRADING ACCOUNT PAGE 0 This document is a summary of key information about the PSG Wealth currency futures trading account. It will

KEY INFORMATION DOCUMENT PSG WEALTH CURRENCY FUTURES TRADING ACCOUNT TRADING ACCOUNT PAGE 0 This document is a summary of key information about the PSG Wealth currency futures trading account. It will

96 97 98 99 00 01 02 03 04 05 06 07 08* FDI Portfolio Investment Other investment

Chartbook Contact: Sebastian Becker +49 69 91-3664 Global Risk Analysis The unwinding of Yen carry trades Some empirical evidence 3 2 1-1 -2-3 -4 October 31, 28 Many years before the sub-prime crisis hit

Chartbook Contact: Sebastian Becker +49 69 91-3664 Global Risk Analysis The unwinding of Yen carry trades Some empirical evidence 3 2 1-1 -2-3 -4 October 31, 28 Many years before the sub-prime crisis hit

The foreign exchange and derivatives markets in Hong Kong

The foreign exchange and derivatives markets in Hong Kong by the Banking Supervision Department The results of the latest triennial global survey of turnover in the markets for foreign exchange (FX) and

The foreign exchange and derivatives markets in Hong Kong by the Banking Supervision Department The results of the latest triennial global survey of turnover in the markets for foreign exchange (FX) and

Why has FX trading surged? Explaining the 2004 triennial survey 1

Gabriele Galati +41 61 280 8923 [email protected] Michael Melvin +1 480 965 6860 [email protected] Why has FX trading surged? Explaining the 2004 triennial survey 1 The 2004 survey shows a surge in

Gabriele Galati +41 61 280 8923 [email protected] Michael Melvin +1 480 965 6860 [email protected] Why has FX trading surged? Explaining the 2004 triennial survey 1 The 2004 survey shows a surge in

Purer return and reduced volatility: Hedging currency risk in international-equity portfolios

Purer return and reduced volatility: Hedging currency risk in international-equity portfolios Currency-hedged exchange-traded funds (ETFs) offer investors a compelling way to access international-equity

Purer return and reduced volatility: Hedging currency risk in international-equity portfolios Currency-hedged exchange-traded funds (ETFs) offer investors a compelling way to access international-equity

The foreign-exchange and derivatives markets in Hong Kong

The foreign-exchange and derivatives markets in Hong Kong by the Banking Policy Department The results of the latest triennial global survey of turnover in the markets for foreign-exchange (FX) and over-the-counter

The foreign-exchange and derivatives markets in Hong Kong by the Banking Policy Department The results of the latest triennial global survey of turnover in the markets for foreign-exchange (FX) and over-the-counter

GMO White Paper. The Case for Not Currency Hedging Foreign Equity Investments: A U.S. Investor s Perspective EXECUTIVE SUMMARY.

GMO White Paper The Case for Not Currency Hedging Foreign Equity Investments: A U.S. Investor s Perspective Catherine LeGraw Apr 2015 EXECUTIVE SUMMARY Investors often ask about GMO s approach to currency

GMO White Paper The Case for Not Currency Hedging Foreign Equity Investments: A U.S. Investor s Perspective Catherine LeGraw Apr 2015 EXECUTIVE SUMMARY Investors often ask about GMO s approach to currency

FUNDS TM. G10 Currencies: White Paper. A Monetary Policy Analysis FUNDS. The Authority on Currencies

FUNDS White Paper The Authority on Currencies Merk Investments LLC Research MAY 2012 G10 Currencies: A Monetary Policy Analysis Merk Monetary Score favors currencies of, and Canada; disfavors currencies

FUNDS White Paper The Authority on Currencies Merk Investments LLC Research MAY 2012 G10 Currencies: A Monetary Policy Analysis Merk Monetary Score favors currencies of, and Canada; disfavors currencies

Vanguard research July 2014

The Understanding buck stops here: the hedge return : Vanguard The impact money of currency market hedging funds in foreign bonds Vanguard research July 214 Charles Thomas, CFA; Paul M. Bosse, CFA Hedging

The Understanding buck stops here: the hedge return : Vanguard The impact money of currency market hedging funds in foreign bonds Vanguard research July 214 Charles Thomas, CFA; Paul M. Bosse, CFA Hedging

Managing Risk/Reward in Fixed Income

INSIGHTS Managing Risk/Reward in Fixed Income Using Global Currency-Hedged Indices as Benchmarks In the pursuit of alpha, is it better to use a global hedged or unhedged index as a benchmark for measuring

INSIGHTS Managing Risk/Reward in Fixed Income Using Global Currency-Hedged Indices as Benchmarks In the pursuit of alpha, is it better to use a global hedged or unhedged index as a benchmark for measuring

Introductory remarks by Jean-Pierre Danthine

abcdefg News conference Berne, 15 December 2011 Introductory remarks by Jean-Pierre Danthine I would like to address three main issues today. These are the acute market volatility experienced this summer,

abcdefg News conference Berne, 15 December 2011 Introductory remarks by Jean-Pierre Danthine I would like to address three main issues today. These are the acute market volatility experienced this summer,

Online appendix to paper Downside Market Risk of Carry Trades

Online appendix to paper Downside Market Risk of Carry Trades A1. SUB-SAMPLE OF DEVELOPED COUNTRIES I study a sub-sample of developed countries separately for two reasons. First, some of the emerging countries

Online appendix to paper Downside Market Risk of Carry Trades A1. SUB-SAMPLE OF DEVELOPED COUNTRIES I study a sub-sample of developed countries separately for two reasons. First, some of the emerging countries

Assignment 10 (Chapter 11)

") Assignment 10 (Chapter 11) 1. Which of the following tends to cause the U.S. dollar to appreciate in value? a) An increase in U.S. prices above foreign prices b) Rapid economic growth in foreign countries

Assignment 10 (Chapter 11) 1. Which of the following tends to cause the U.S. dollar to appreciate in value? a) An increase in U.S. prices above foreign prices b) Rapid economic growth in foreign countries

Staying alive: Bond strategies for a normalising world

Staying alive: Bond strategies for a normalising world Dr Peter Westaway Chief Economist, Europe Vanguard Asset Management November 2013 This document is directed at investment professionals and should

Staying alive: Bond strategies for a normalising world Dr Peter Westaway Chief Economist, Europe Vanguard Asset Management November 2013 This document is directed at investment professionals and should

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

The Long-Run Performance of the New Zealand Stock Markets: 1899-2012

The Long-Run Performance of the New Zealand Stock Markets: 1899-2012 Bart Frijns * & Alireza Tourani-Rad Auckland Centre for Financial Research (ACFR) Department of Finance, Faculty of Business and Law,

The Long-Run Performance of the New Zealand Stock Markets: 1899-2012 Bart Frijns * & Alireza Tourani-Rad Auckland Centre for Financial Research (ACFR) Department of Finance, Faculty of Business and Law,

Real Estate as a Strategic Asset Class. Less is More: Private Equity Investments` Benefits. How to Invest in Real Estate?

Real Estate as a Strategic Asset Class The Benefits of Illiquid Investments Real estate, a key asset class in a portfolio, can offer stable income returns, partial protection against inflation, and good

Real Estate as a Strategic Asset Class The Benefits of Illiquid Investments Real estate, a key asset class in a portfolio, can offer stable income returns, partial protection against inflation, and good

Global Investing: The Importance of Currency Returns and Currency Hedging

Global Investing: The Importance of Currency Returns and Currency Hedging There is a continuing trend for investors to reduce their home bias in equity allocation and increase the allocation to international

Global Investing: The Importance of Currency Returns and Currency Hedging There is a continuing trend for investors to reduce their home bias in equity allocation and increase the allocation to international

Understanding Currency

Understanding Currency Overlay July 2010 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract As portfolios have expanded to include international investments, investors must be aware of

Understanding Currency Overlay July 2010 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract As portfolios have expanded to include international investments, investors must be aware of

STATE STREET INVESTOR CONFIDENCE INDEX SUMMARY

STATE STREET INVESTOR CONFIDENCE INDEX SUMMARY state street investor confidence index Measuring Investor Confidence on a Quantitative Basis The State Street Investor Confidence Index (the index) provides

STATE STREET INVESTOR CONFIDENCE INDEX SUMMARY state street investor confidence index Measuring Investor Confidence on a Quantitative Basis The State Street Investor Confidence Index (the index) provides

Theories of Exchange rate determination

Theories of Exchange rate determination INTRODUCTION By definition, the Foreign Exchange Market is a market 1 in which different currencies can be exchanged at a specific rate called the foreign exchange

Theories of Exchange rate determination INTRODUCTION By definition, the Foreign Exchange Market is a market 1 in which different currencies can be exchanged at a specific rate called the foreign exchange

Why Currency Returns and Currency Hedging Matters

Research Insight Why Currency Returns and Currency Hedging Matters An Update on the MSCI Hedged Indices Jennifer Bender, Roman Kouzmenko, and Zoltan Nagy msci.com Overview With the growth of international

Research Insight Why Currency Returns and Currency Hedging Matters An Update on the MSCI Hedged Indices Jennifer Bender, Roman Kouzmenko, and Zoltan Nagy msci.com Overview With the growth of international

TREASURY AND FEDERAL RESERVE FOREIGN EXCHANGE OPERATIONS

EMBARGOED: FOR RELEASE AT 4:00 P.M. EST, THURSDAY, FEBRUARY 10, 2011 TREASURY AND FEDERAL RESERVE FOREIGN EXCHANGE OPERATIONS October December 2010 During the fourth quarter of 2010, the U.S. dollar s

EMBARGOED: FOR RELEASE AT 4:00 P.M. EST, THURSDAY, FEBRUARY 10, 2011 TREASURY AND FEDERAL RESERVE FOREIGN EXCHANGE OPERATIONS October December 2010 During the fourth quarter of 2010, the U.S. dollar s

The relationship between exchange rates, interest rates. In this lecture we will learn how exchange rates accommodate equilibrium in

The relationship between exchange rates, interest rates In this lecture we will learn how exchange rates accommodate equilibrium in financial markets. For this purpose we examine the relationship between

The relationship between exchange rates, interest rates In this lecture we will learn how exchange rates accommodate equilibrium in financial markets. For this purpose we examine the relationship between

Foreign Exchange Trading Managers

Foreign Exchange Trading Managers Quantum Leap Capital (abbreviated as QLC ) is a Forex Trading Manager which focuses on trading worldwide foreign currencies on behalf of institutions, corporates and individual

Foreign Exchange Trading Managers Quantum Leap Capital (abbreviated as QLC ) is a Forex Trading Manager which focuses on trading worldwide foreign currencies on behalf of institutions, corporates and individual

What Are the Best Times to Trade for Individual Currency Pairs?

What Are the Best Times to Trade for Individual Currency Pairs? By: Kathy Lien The foreign exchange market operates 24 hours a day and as a result it is impossible for a trader to track every single market

What Are the Best Times to Trade for Individual Currency Pairs? By: Kathy Lien The foreign exchange market operates 24 hours a day and as a result it is impossible for a trader to track every single market

René Garcia Professor of finance

Liquidity Risk: What is it? How to Measure it? René Garcia Professor of finance EDHEC Business School, CIRANO Cirano, Montreal, January 7, 2009 The financial and economic environment We are living through

Liquidity Risk: What is it? How to Measure it? René Garcia Professor of finance EDHEC Business School, CIRANO Cirano, Montreal, January 7, 2009 The financial and economic environment We are living through

Introduction, Forwards and Futures

Introduction, Forwards and Futures Liuren Wu Zicklin School of Business, Baruch College Fall, 2007 (Hull chapters: 1,2,3,5) Liuren Wu Introduction, Forwards & Futures Option Pricing, Fall, 2007 1 / 35

Introduction, Forwards and Futures Liuren Wu Zicklin School of Business, Baruch College Fall, 2007 (Hull chapters: 1,2,3,5) Liuren Wu Introduction, Forwards & Futures Option Pricing, Fall, 2007 1 / 35

Chapter Review and Self-Test Problems

CHAPTER 22 International Corporate Finance 771 3. The fundamental relationships between international financial variables: a. Absolute and relative purchasing power parity, PPP b. Interest rate parity,

CHAPTER 22 International Corporate Finance 771 3. The fundamental relationships between international financial variables: a. Absolute and relative purchasing power parity, PPP b. Interest rate parity,

Business. Insights. When cash is king. Investec Editorials

Business Insights Investec Editorials When cash is king Shelter from the storm Where do investors turn in times of uncertainty? What investment options can provide shelter from the ongoing volatility?

Business Insights Investec Editorials When cash is king Shelter from the storm Where do investors turn in times of uncertainty? What investment options can provide shelter from the ongoing volatility?

Seminar. Global Foreign Exchange Markets Chapter 9. Copyright 2013 Pearson Education. 20 Kasım 13 Çarşamba

Seminar Global Foreign Exchange Markets Chapter 9 9- Learning Objectives To learn the fundamentals of foreign exchange To identify the major characteristics of the foreign-exchange market and how governments

Seminar Global Foreign Exchange Markets Chapter 9 9- Learning Objectives To learn the fundamentals of foreign exchange To identify the major characteristics of the foreign-exchange market and how governments

Consolidated Quarterly Report of Baader Bank AG as at 31.03.2015

Consolidated Quarterly Report of Baader Bank AG as at 31.03.2015 OVERVIEW OF KEY FIGURES RESULTS OF OPERATIONS Q1 2015 Q1 2014 Change in % Net interest income EUR thousand -95 869 >-100.0 Current income

Consolidated Quarterly Report of Baader Bank AG as at 31.03.2015 OVERVIEW OF KEY FIGURES RESULTS OF OPERATIONS Q1 2015 Q1 2014 Change in % Net interest income EUR thousand -95 869 >-100.0 Current income

Quantitative Portfolio Strategy

Quantitative Portfolio Strategy Lev Dynkin 201-524-2839 [email protected] Tony Gould, CFA 212-526-2821 [email protected] CURRENCY HEDGING IN FIXED INCOME PORTFOLIOS Introduction Portfolio managers typically

Quantitative Portfolio Strategy Lev Dynkin 201-524-2839 [email protected] Tony Gould, CFA 212-526-2821 [email protected] CURRENCY HEDGING IN FIXED INCOME PORTFOLIOS Introduction Portfolio managers typically

Universal Hedging: Optimizing Currency Risk and Reward in International Equity Portfolios

Universal Hedging: Optimizing Currency Risk and Reward in International Equity Portfolios Fischer Black n a world where everyone can hedge against changes in the value of real exchange rates (the relative

Universal Hedging: Optimizing Currency Risk and Reward in International Equity Portfolios Fischer Black n a world where everyone can hedge against changes in the value of real exchange rates (the relative

Current account deficit -10. Private sector Other public* Official reserve assets

Australian Capital Flows and the financial Crisis Introduction For many years, Australia s high level of investment relative to savings has been supported by net foreign capital inflow. This net capital

Australian Capital Flows and the financial Crisis Introduction For many years, Australia s high level of investment relative to savings has been supported by net foreign capital inflow. This net capital

CHAPTER 22: FUTURES MARKETS

CHAPTER 22: FUTURES MARKETS 1. a. The closing price for the spot index was 1329.78. The dollar value of stocks is thus $250 1329.78 = $332,445. The closing futures price for the March contract was 1364.00,

CHAPTER 22: FUTURES MARKETS 1. a. The closing price for the spot index was 1329.78. The dollar value of stocks is thus $250 1329.78 = $332,445. The closing futures price for the March contract was 1364.00,

AN INTRODUCTION TO TRADING CURRENCIES

The ins and outs of trading currencies AN INTRODUCTION TO TRADING CURRENCIES A FOREX.com educational guide K$ $ kr HK$ $ FOREX.com is a trading name of GAIN Capital - FOREX.com Canada Limited is a member

The ins and outs of trading currencies AN INTRODUCTION TO TRADING CURRENCIES A FOREX.com educational guide K$ $ kr HK$ $ FOREX.com is a trading name of GAIN Capital - FOREX.com Canada Limited is a member

Investment Insight Diversified Factor Premia Edward Qian PhD, CFA, Bryan Belton, CFA, and Kun Yang PhD, CFA PanAgora Asset Management August 2013

Investment Insight Diversified Factor Premia Edward Qian PhD, CFA, Bryan Belton, CFA, and Kun Yang PhD, CFA PanAgora Asset Management August 2013 Modern Portfolio Theory suggests that an investor s return

Investment Insight Diversified Factor Premia Edward Qian PhD, CFA, Bryan Belton, CFA, and Kun Yang PhD, CFA PanAgora Asset Management August 2013 Modern Portfolio Theory suggests that an investor s return

Chapter 17. Fixed Exchange Rates and Foreign Exchange Intervention. Copyright 2003 Pearson Education, Inc.

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slide 17-1 Chapter 17 Learning Goals How a central bank must manage monetary policy so as to fix its currency's value in the foreign exchange

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slide 17-1 Chapter 17 Learning Goals How a central bank must manage monetary policy so as to fix its currency's value in the foreign exchange

Continuously excessive exchangerate fluctuations

July - No. Continuously excessive exchangerate fluctuations In this Flash, we will look at the currencies of major OECD countries (dollar, euro, yen, pound sterling, Swiss franc, Australian dollar) and

July - No. Continuously excessive exchangerate fluctuations In this Flash, we will look at the currencies of major OECD countries (dollar, euro, yen, pound sterling, Swiss franc, Australian dollar) and

PROTECTING YOUR PORTFOLIO WITH BONDS

Your Global Investment Authority PROTECTING YOUR PORTFOLIO WITH BONDS Bond strategies for an evolving market Market uncertainty has left many investors wondering how to protect their portfolios during

Your Global Investment Authority PROTECTING YOUR PORTFOLIO WITH BONDS Bond strategies for an evolving market Market uncertainty has left many investors wondering how to protect their portfolios during

New data on financial derivatives 1 for the UK National Accounts and Balance of Payments

New data on financial derivatives 1 for the UK National Accounts and Balance of Payments By Andrew Grice Tel: 020 7601 3149 Email: [email protected] This article introduces the first publication

New data on financial derivatives 1 for the UK National Accounts and Balance of Payments By Andrew Grice Tel: 020 7601 3149 Email: [email protected] This article introduces the first publication

Chapter 11. International Economics II: International Finance

Chapter 11 International Economics II: International Finance The other major branch of international economics is international monetary economics, also known as international finance. Issues in international

Chapter 11 International Economics II: International Finance The other major branch of international economics is international monetary economics, also known as international finance. Issues in international

The Foreign Exchange Market Not As Liquid As You May Think

06.09.2012 Seite 1 / 5 The Foreign Exchange Market Not As Liquid As You May Think September 6 2012 1 23 AM GMT By Loriano Mancini Angelo Ranaldo and Jan Wrampelmeyer The foreign exchange market facilitates

06.09.2012 Seite 1 / 5 The Foreign Exchange Market Not As Liquid As You May Think September 6 2012 1 23 AM GMT By Loriano Mancini Angelo Ranaldo and Jan Wrampelmeyer The foreign exchange market facilitates

Does an Optimal Static Policy Foreign Currency Hedge Ratio Exist?

May 2015 Does an Optimal Static Policy Foreign Currency Hedge Ratio Exist? FQ Perspective DORI LEVANONI Partner, Investments ANNA SUPERA-KUC CFA Director Investing in foreign assets comes with the additional

May 2015 Does an Optimal Static Policy Foreign Currency Hedge Ratio Exist? FQ Perspective DORI LEVANONI Partner, Investments ANNA SUPERA-KUC CFA Director Investing in foreign assets comes with the additional

THE LOW INTEREST RATE ENVIRONMENT AND ITS IMPACT ON INSURANCE MARKETS. Mamiko Yokoi-Arai

THE LOW INTEREST RATE ENVIRONMENT AND ITS IMPACT ON INSURANCE MARKETS Mamiko Yokoi-Arai Current macro economic environment is of Low interest rate Low inflation and nominal wage growth Slow growth Demographic

THE LOW INTEREST RATE ENVIRONMENT AND ITS IMPACT ON INSURANCE MARKETS Mamiko Yokoi-Arai Current macro economic environment is of Low interest rate Low inflation and nominal wage growth Slow growth Demographic

How To Beat The Currency Market Without (Much) Skill

Skill") How To Beat The Currency Market Without (Much) Skill January 2010 FQ Perspective by Dori Levanoni and Juliana Bambaci We ve written about rebalancing strategies for nearly two decades. 1 We ve done so

How To Beat The Currency Market Without (Much) Skill January 2010 FQ Perspective by Dori Levanoni and Juliana Bambaci We ve written about rebalancing strategies for nearly two decades. 1 We ve done so

EQUINOX PERFORMANCE REPORT SEPTEMBER QUARTER 2006 MACQUARIE EQUINOX LIMITED PARTICIPATING SHARES ARBN 105 989 231

PERFORMANCE REPORT SEPTEMBER QUARTER 2006 MACQUARIE LIMITED PARTICIPATING SHARES ARBN 105 989 231 Market Commentary Hedge Fund Industry The direction of financial markets in the third quarter was broadly

PERFORMANCE REPORT SEPTEMBER QUARTER 2006 MACQUARIE LIMITED PARTICIPATING SHARES ARBN 105 989 231 Market Commentary Hedge Fund Industry The direction of financial markets in the third quarter was broadly

Portfolio Series Portfolio Review Second Quarter 2010

Portfolio Series Portfolio Review Second Quarter 2010 We are pleased to introduce Portfolio Review, a new quarterly report on Portfolio Series. 3 Portfolio Series Income Fund 7 Portfolio Series Conservative

Portfolio Series Portfolio Review Second Quarter 2010 We are pleased to introduce Portfolio Review, a new quarterly report on Portfolio Series. 3 Portfolio Series Income Fund 7 Portfolio Series Conservative

General Forex Glossary

General Forex Glossary A ADR American Depository Receipt Arbitrage The simultaneous buying and selling of a security at two different prices in two different markets, with the aim of creating profits without

General Forex Glossary A ADR American Depository Receipt Arbitrage The simultaneous buying and selling of a security at two different prices in two different markets, with the aim of creating profits without

Solutions: Sample Exam 2: FINA 5500

Short Questions / Problems Section: (88 points) Solutions: Sample Exam 2: INA 5500 Q1. (8 points) The following are direct quotes from the spot and forward markets for pounds, yens and francs, for two

Short Questions / Problems Section: (88 points) Solutions: Sample Exam 2: INA 5500 Q1. (8 points) The following are direct quotes from the spot and forward markets for pounds, yens and francs, for two

FLEXIBLE EXCHANGE RATES

FLEXIBLE EXCHANGE RATES Along with globalization has come a high degree of interdependence. Central to this is a flexible exchange rate system, where exchange rates are determined each business day by

FLEXIBLE EXCHANGE RATES Along with globalization has come a high degree of interdependence. Central to this is a flexible exchange rate system, where exchange rates are determined each business day by

How Smaller Stocks May Offer Larger Returns

Strategic Advisory Solutions April 2015 How Smaller Stocks May Offer Larger Returns In an environment where the US continues to be the growth engine of the developed world, investors may find opportunity

Strategic Advisory Solutions April 2015 How Smaller Stocks May Offer Larger Returns In an environment where the US continues to be the growth engine of the developed world, investors may find opportunity

CHAPTER 12 CHAPTER 12 FOREIGN EXCHANGE

CHAPTER 12 CHAPTER 12 FOREIGN EXCHANGE CHAPTER OVERVIEW This chapter discusses the nature and operation of the foreign exchange market. The chapter begins by describing the foreign exchange market and

CHAPTER 12 CHAPTER 12 FOREIGN EXCHANGE CHAPTER OVERVIEW This chapter discusses the nature and operation of the foreign exchange market. The chapter begins by describing the foreign exchange market and

Why a Floating Exchange Rate Regime Makes Sense for Canada

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Chambre de commerce du Montréal métropolitain Montreal, Quebec 4 December 2000 Why a Floating Exchange Rate Regime Makes Sense for Canada

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Chambre de commerce du Montréal métropolitain Montreal, Quebec 4 December 2000 Why a Floating Exchange Rate Regime Makes Sense for Canada

MGE#12 The Balance of Payments

MGE#12 The Balance of Payments The Current Account, the Capital Account and the Balance of Payments Introduction to the Foreign Exchange Market Savings, Investment and the Current Account 1 From last session

MGE#12 The Balance of Payments The Current Account, the Capital Account and the Balance of Payments Introduction to the Foreign Exchange Market Savings, Investment and the Current Account 1 From last session

Turnover of the foreign exchange and derivatives market in Hong Kong

Turnover of the foreign exchange and derivatives market in Hong Kong by the Banking Policy Department Hong Kong advanced one place to rank sixth in the global foreign exchange market and seventh when taking

Turnover of the foreign exchange and derivatives market in Hong Kong by the Banking Policy Department Hong Kong advanced one place to rank sixth in the global foreign exchange market and seventh when taking

Bank of Japan Review. Global correlation among government bond markets and Japanese banks' market risk. February 2012. Introduction 2012-E-1

Bank of Japan Review 212-E-1 Global correlation among government bond markets and Japanese banks' market risk Financial System and Bank Examination Department Yoshiyuki Fukuda, Kei Imakubo, Shinichi Nishioka

Bank of Japan Review 212-E-1 Global correlation among government bond markets and Japanese banks' market risk Financial System and Bank Examination Department Yoshiyuki Fukuda, Kei Imakubo, Shinichi Nishioka

B.3. Robustness: alternative betas estimation

Appendix B. Additional empirical results and robustness tests This Appendix contains additional empirical results and robustness tests. B.1. Sharpe ratios of beta-sorted portfolios Fig. B1 plots the Sharpe

Appendix B. Additional empirical results and robustness tests This Appendix contains additional empirical results and robustness tests. B.1. Sharpe ratios of beta-sorted portfolios Fig. B1 plots the Sharpe

CAN INVESTORS PROFIT FROM DEVALUATIONS? THE PERFORMANCE OF WORLD STOCK MARKETS AFTER DEVALUATIONS. Bryan Taylor

CAN INVESTORS PROFIT FROM DEVALUATIONS? THE PERFORMANCE OF WORLD STOCK MARKETS AFTER DEVALUATIONS Introduction Bryan Taylor The recent devaluations in Asia have drawn attention to the risk investors face

CAN INVESTORS PROFIT FROM DEVALUATIONS? THE PERFORMANCE OF WORLD STOCK MARKETS AFTER DEVALUATIONS Introduction Bryan Taylor The recent devaluations in Asia have drawn attention to the risk investors face

SAMPLE MID-TERM QUESTIONS

SAMPLE MID-TERM QUESTIONS William L. Silber HOW TO PREPARE FOR THE MID- TERM: 1. Study in a group 2. Review the concept questions in the Before and After book 3. When you review the questions listed below,

SAMPLE MID-TERM QUESTIONS William L. Silber HOW TO PREPARE FOR THE MID- TERM: 1. Study in a group 2. Review the concept questions in the Before and After book 3. When you review the questions listed below,

The foreign exchange market operates 24 hours a day and as a result it

CHAPTER 5 What Are the Best Times to Trade for Individual Currency Pairs? The foreign exchange market operates 24 hours a day and as a result it is impossible for a trader to track every single market

CHAPTER 5 What Are the Best Times to Trade for Individual Currency Pairs? The foreign exchange market operates 24 hours a day and as a result it is impossible for a trader to track every single market

Answers to Concepts in Review

Answers to Concepts in Review 1. A portfolio is simply a collection of investments assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected return

Answers to Concepts in Review 1. A portfolio is simply a collection of investments assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected return

Currency Derivatives Guide

Currency Derivatives Guide What are Futures? In finance, a futures contract (futures) is a standardised contract between two parties to buy or sell a specified asset of standardised quantity and quality

Currency Derivatives Guide What are Futures? In finance, a futures contract (futures) is a standardised contract between two parties to buy or sell a specified asset of standardised quantity and quality

The global economy Banco de Portugal Lisbon, 24 September 2013 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

Chapter 4.1. Intermarket Relationships

1 Chapter 4.1 Intermarket Relationships 0 Contents INTERMARKET RELATIONSHIPS The forex market is the largest global financial market. While no other financial market can compare to the size of the forex

1 Chapter 4.1 Intermarket Relationships 0 Contents INTERMARKET RELATIONSHIPS The forex market is the largest global financial market. While no other financial market can compare to the size of the forex

Diversify portfolios with U.S. and international bonds

Diversify portfolios with U.S. and international bonds Investing broadly across asset classes such as stocks, bonds and cash can help reduce volatility and risk within a portfolio. Canadian investors have

Diversify portfolios with U.S. and international bonds Investing broadly across asset classes such as stocks, bonds and cash can help reduce volatility and risk within a portfolio. Canadian investors have

CHAPTER 5 THE MARKET FOR FOREIGN EXCHANGE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 5 THE MARKET FOR FOREIGN EXCHANGE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Give a full definition of the market for foreign exchange. Answer: Broadly

CHAPTER 5 THE MARKET FOR FOREIGN EXCHANGE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Give a full definition of the market for foreign exchange. Answer: Broadly

Global Markets Update Signature Global Advisors

SIGNATURE GLOBAL ADVISORS MARKETS UPDATE AUGUST 3, 2011 The following comments come from an internal interview with Chief Investment Officer, Eric Bushell. They represent Signature s current market views

SIGNATURE GLOBAL ADVISORS MARKETS UPDATE AUGUST 3, 2011 The following comments come from an internal interview with Chief Investment Officer, Eric Bushell. They represent Signature s current market views

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. How would you define transaction exposure? How is it different from economic

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. How would you define transaction exposure? How is it different from economic

THE US DOLLAR, THE EURO, THE JAPANESE YEN AND THE CHINESE YUAN IN THE FOREIGN EXCHANGE MARKET A COMPARATIVE ANALYSIS

THE US DOLLAR, THE EURO, THE JAPANESE YEN AND THE CHINESE YUAN IN THE FOREIGN EXCHANGE MARKET A COMPARATIVE ANALYSIS ORASTEAN Ramona Lucian Blaga University of Sibiu, Romania Abstract: This paper exposes

THE US DOLLAR, THE EURO, THE JAPANESE YEN AND THE CHINESE YUAN IN THE FOREIGN EXCHANGE MARKET A COMPARATIVE ANALYSIS ORASTEAN Ramona Lucian Blaga University of Sibiu, Romania Abstract: This paper exposes

AN INTRODUCTION TO THE FOREIGN EXCHANGE MARKET

DUKASCOPY BANK SA AN INTRODUCTION TO THE FOREIGN EXCHANGE MARKET DUKASCOPY BANK EDUCATIONAL GUIDE AN INTRODUCTION TO THE FOREIGN EXCHANGE MARKET www.dukascopy.com CONTENTS INTRODUCTION TO FOREX CURRENCY

DUKASCOPY BANK SA AN INTRODUCTION TO THE FOREIGN EXCHANGE MARKET DUKASCOPY BANK EDUCATIONAL GUIDE AN INTRODUCTION TO THE FOREIGN EXCHANGE MARKET www.dukascopy.com CONTENTS INTRODUCTION TO FOREX CURRENCY

Global bond investing

Global bond investing Todd Schlanger, CFA Investment Strategy Group Vanguard Asset Management, Limited This document is directed at professional investors and should not be distributed to, or relied upon

Global bond investing Todd Schlanger, CFA Investment Strategy Group Vanguard Asset Management, Limited This document is directed at professional investors and should not be distributed to, or relied upon

2. Discuss the implications of the interest rate parity for the exchange rate determination.

CHAPTER 6 INTERNATIONAL PARITY RELATIONSHIPS AND FORECASTING FOREIGN EXCHANGE RATES SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Give a full definition of arbitrage.

CHAPTER 6 INTERNATIONAL PARITY RELATIONSHIPS AND FORECASTING FOREIGN EXCHANGE RATES SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Give a full definition of arbitrage.

Futures Price d,f $ 0.65 = (1.05) (1.04)

(1.04)") 24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

Oxford University Business Economics Programme

The Open Economy Gavin Cameron Tuesday 10 July 2001 Oxford University Business Economics Programme the exchange rate The nominal exchange rate is simply the price of one currency in terms of another pounds

The Open Economy Gavin Cameron Tuesday 10 July 2001 Oxford University Business Economics Programme the exchange rate The nominal exchange rate is simply the price of one currency in terms of another pounds

Condensed Interim Consolidated Financial Statements of. Canada Pension Plan Investment Board

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board September 30, 2015 Condensed Interim Consolidated Balance Sheet As at September 30, 2015 As at September 30,

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board September 30, 2015 Condensed Interim Consolidated Balance Sheet As at September 30, 2015 As at September 30,

Currency Futures trade on the JSE s Currency Derivatives Trading Platform

Currency Futures trade on the JSE s Currency Derivatives Trading Platform DERIVATIVE MARKET Currency Derivatives Currency Futures www.jse.co.za Johannesburg Stock Exchange Currency Futures & Options trade

Currency Futures trade on the JSE s Currency Derivatives Trading Platform DERIVATIVE MARKET Currency Derivatives Currency Futures www.jse.co.za Johannesburg Stock Exchange Currency Futures & Options trade

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate?

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate? Emily Polito, Trinity College In the past two decades, there have been many empirical studies both in support of and opposing

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate? Emily Polito, Trinity College In the past two decades, there have been many empirical studies both in support of and opposing

The Canadian Dollar as a Reserve Currency

1 Lukasz Pomorski, Francisco Rivadeneyra and Eric Wolfe, Funds Management and Banking Department Over the past five years, central banks and monetary authorities have started adding Canadian-dollar assets

1 Lukasz Pomorski, Francisco Rivadeneyra and Eric Wolfe, Funds Management and Banking Department Over the past five years, central banks and monetary authorities have started adding Canadian-dollar assets

Index Solutions A Matter of Weight

Index Solutions A Matter of Weight Newsletter No. 11 Our current newsletter is about weight, or more precisely the weighting of equities in an index. Non-market capitalization weighted indices are at present

Index Solutions A Matter of Weight Newsletter No. 11 Our current newsletter is about weight, or more precisely the weighting of equities in an index. Non-market capitalization weighted indices are at present