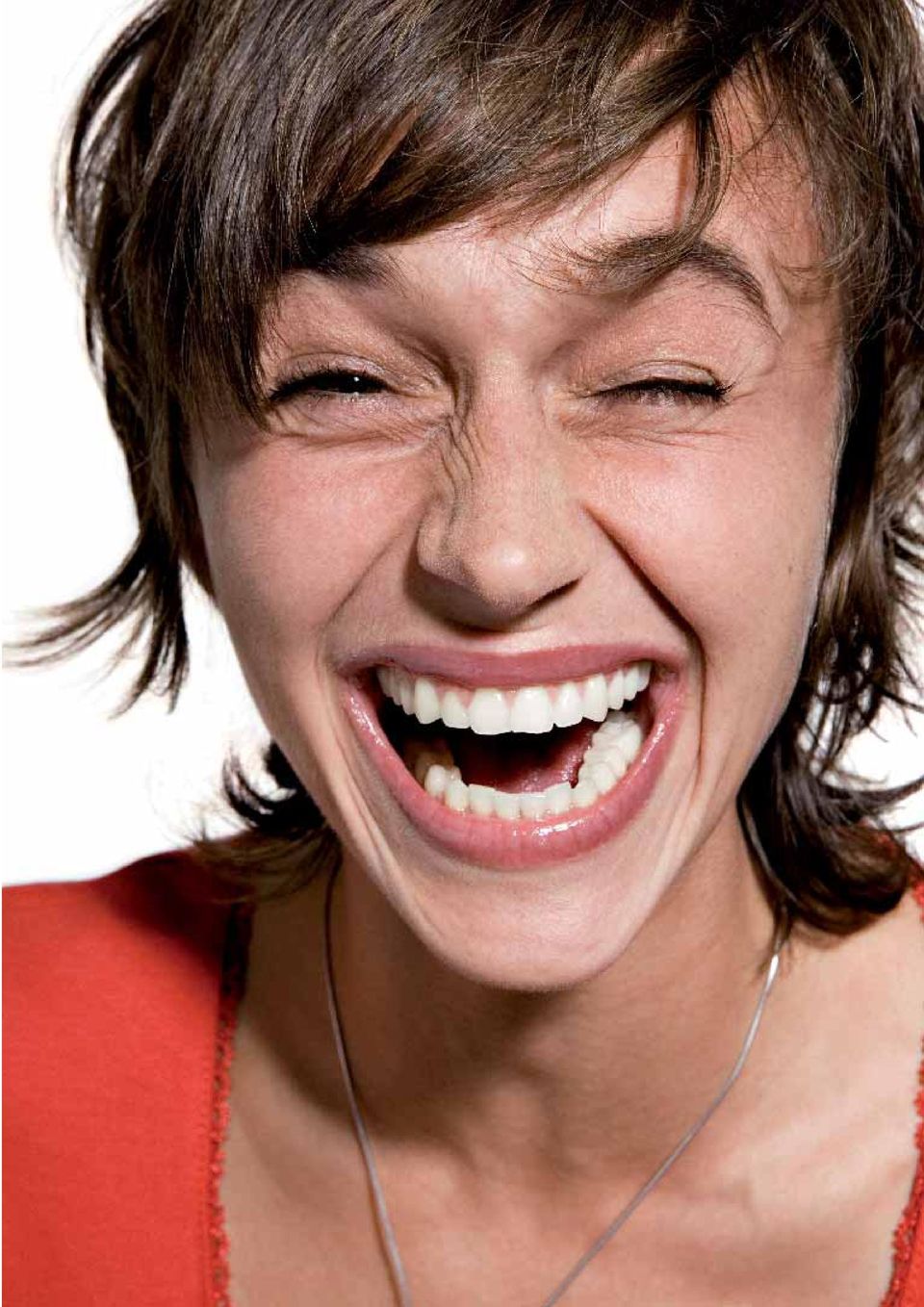

LAUGH AND THE WORLD SEES ALL YOUR TEETH. YOUR EYES NARROW, YOUR NOSTRILS FLARE AND YOUR TEETH BECOME THE FOCAL ATTRACTION OF

|

|

|

- Miles Simon

- 8 years ago

- Views:

Transcription

1 ANNUAL REPORT 2006 STRAUMANN Straumann is a global leader in implant dentistry and oral tissue regeneration. For a brief overview of our company, our vision, mission, and core beliefs, please see pp COMMITTED TO SIMPLY DOING MORE FOR DENTAL PROFESSIONALS LAUGH AND THE WORLD SEES ALL YOUR TEETH. YOUR EYES NARROW, YOUR NOSTRILS FLARE AND YOUR TEETH BECOME THE FOCAL ATTRACTION OF Simply doing more is the guiding principle we use to position our products and services and to highlight our day-to-day operations in the interest of dental professionals and patients. Having pioneered many of the most influential technologies and techniques in our field, we have a tradition of doing more to advance oral implantology and patient care. As this annual report demonstrates, 2006 was no exception in this respect. YOUR FACE. THE BEAUTY OF CONFIDENT LAUGHTER ANNUAL REPORT 2006 DIES WHEN TEETH ARE LOST. STRAUMANN DENTAL IMPLANTS RESTORE MORE THAN TEETH AND MORE THAN A SMILE: THEY PUT NATURAL ATTRACTION BACK INTO A LAUGHING FACE. THE PORTRAITS IN Straumann Holding AG Peter Merian-Weg Basel Switzerland THIS REPORT SHOW JUST HOW VALUABLE THAT IS.

2 NET REVENUE (in CHF million) OPERATING AND NET PROFIT (in CHF million) Operating profi t Net profi t REVENUES BY REGION KEY FACTS & FIGURES Rest of World 2% Asia/Pacific 10% North America 25% CASH FLOW AND INVESTMENTS Europe 63% (in CHF million) Cash fl ow Investments NET REVENUE CLIMBS 18% TO CHF 599 MILLION NET PROFIT RISES 11% TO CHF 142 MILLION (23.7% MARGIN) FREE CASH FLOW INCREASES FIVEFOLD TO CHF 126 MILLION NEW PRODUCTS LAUNCHED; FULL PIPELINE TO DRIVE FUTURE GROWTH MARKET POSITION MAINTAINED; EXPANSION OF DIRECT DISTRIBUTION CONTINUES COMPETENCIES ENHANCED; ALMOST 200 JOBS CREATED KEY FIGURES (in CHF million) Change (in %) Net revenue Operating result before depreciation and amortization (EBITDA) Operating profi t (EBIT) Net profi t Cash generated from operating activities Investments/Acquisitions (59) Free cash fl ow Value added (economic profi t) CONCERNING FORWARD-LOOKING STATEMENTS This report contains certain forward-looking statements, which can be identified by the use of terminology such as scheduled, to plan, will, expected, consider, anticipate, forecast, expectation, improve, maintain, believe or similar wording. Such forward-looking statements reflect the current views of management and are subject to known and unknown risks, uncertainties and other factors that may cause actual results, performance or achievements of the Straumann Group ( Group ) to differ materially from those expressed or implied. These include risks related to the success of and demand for the Group s products, the potential for the Group s products to become obsolete, the Group s ability to defend its intellectual property, the Group s ability to develop and commercialize new products in a timely manner, the dynamic and competitive environment in which the Group operates, the regulatory environment, changes in currency exchange rates, the Group s ability to generate revenues and profitability, the Group s ability to realize expansion projects or projects to establish subsidiaries in a timely manner, and the Group s ability to recruit and retain key employees. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in this report. Straumann is providing the information in this report as of this date and does not undertake any obligation to update any forward-looking statements contained in it as a result of new information, future events or otherwise. TRADEMARKS Straumann Emdogain, Straumann Emdogain PLUS, Straumann BoneCeramic, Straumann CARES, SLA, SLActive, Straumann Dental Implant System, Straumann TempImplant, synocta, Straumann Membrane are either registered trademarks or trademarks of Straumann Holding AG and/or its affiliated companies. EMPLOYEES SHARE PRICE HEADCOUNT (in %) Straumann SPI Change 2005 (in %) Employees at 31 December PROFITABILITY (in CHF) Return on assets (ROA) Return on equity (ROE) Return on capital employed (ROCE) SHARE INFORMATION (in CHF) Change (in %) Ordinary dividend paid per share Share price at year-end (2) FTSE4GOOD INDEX FTSE Group confirms that Straumann Holding AG has been independently assessed according to the FTSE4Good criteria, and has satisfied the requirements to become a constituent of the FTSE4Good Index Series. Created by the global index company FTSE Group, FTSE4Good is an equity index series that is designed to facilitate investment in companies that meet globally recognised corporate responsibility standards. Companies in the FTSE4Good Index Series have met stringent social, ethical and environmental criteria, and are positioned to capitalise on the benefits of responsible business practice. IMPRESSUM Published by: Institut Straumann AG, Basel Layout concept and realization: Eclat AG, Erlenbach/Zurich Consultant on sustainability chapter: sustainserv, Zurich and Boston Independent expert interviews: Abbott Chrisman, Oliver Klaffke Photography: Board, Management, locations: Derek Li Wan Po, Howard Brundrett Print: Neidhart + Schön AG, Zurich Basel, 1 February CHF 3.00 proposed for 2006, payable in 2007 subject to shareholder approval.

FREE CASH FLOW INCREASES FIVEFOLD TO CHF 126 MILLION NEW PRODUCTS LAUNCHED; FULL PIPELINE TO DRIVE FUTURE GROWTH MARKET POSITION MAINTAINED; EXPANSION OF DIRECT DISTRIBUTION CONTINUES")

3 CONTENTS ANNUAL REPORT 2006 OPERATIONAL REVIEW Letter to shareholders 4 Straumann in brief 8 Markets and regions 14 Products and services 24 Production and logistics 34 Innovation and partnership 38 Research and development 38 Partnership 42 Sustainability 46 Our responsibility 46 Employees 50 Customers 52 Communities 54 Environmental protection 56 INDEPENDENT EXPERT OPINIONS Access to treatment 63 Building implant practices 64 Education in implant dentistry 65 New materials 66 Regulatory developments 67 CORPORATE GOVERNANCE Principles 69 Group structure and shareholders 69 Capital structure 73 Board of Directors 75 Executive Management 79 Compensation Shareholders rights of participation 84 Changes in control and defense measures 84 Auditors 84 Information policy 85 FINANCIAL REPORT APPENDIX 159

4 4 Straumann Annual Report 2006 Operational Review LETTER TO SHAREHOLDERS LETTER TO SHAREHOLDERS Gilbert Achermann, President and CEO; Dr h.c. Rudolf Maag, Chairman DEAR SHAREHOLDER, After several years of continual dynamic growth and substantial expansion, our company made significant progress in 2006 towards becoming a medium-sized international company MORE THAN A YEAR OF TRANSITION Some observers have described the year as one of transition for Straumann. We believe it was more: over the past 12 months we have established a base and set the stage for superior performance and future growth. At the same time, we have continued to do our homework by delivering peace of mind to our customers through proven reliable and simple product concepts coupled with service excellence. We underpinned our leadership position in Europe, our main region. We tackled the issues and worked on the fundamentals for achieving our ambitions in North America, and we started to focus more on the emerging opportunities in Asia. We generated solid growth throughout 2006, with full-year net revenue increasing 16% in local currencies (18% in Swiss francs) to CHF 599 million, while operating and net profits reached CHF 175 million and CHF 143 million, respectively. After substantial infrastructure and capacity expansion in the past years, we expect a phase of normal capital expenditure going forward. However, the absorption of these costs, especially those related to the build-up of manufacturing in Andover and the production of new technologies, obviously affected our ability to expand margins further. REGIONAL PERFORMANCE AND STRATEGY From a regional perspective, Europe contributed some 63% of net revenues and grew 19% in local currencies to CHF 381 million. With the integration of our Danish distributor, we completed our strategic aspiration to gain direct access to all customers in Western Europe. While some European markets such as Switzerland, Sweden and Italy have higher penetration levels, other countries such as France and the UK still have tremendous treatment-substitution potential. This is evident from the fact that the European dental implant and oral tissue regeneration market which we have continued to outpace continues to yield high-teen growth rates. In the continuing absence of reimbursement, our future growth will be supported by the overall strengthening of Europe s economy and improving consumer sentiments in the European region. Hence, we will continue to invest in the expansion of our European sales and marketing organizations.

5 Straumann Annual Report 2006 Operational Review LETTER TO SHAREHOLDERS 5 Our North American franchise has not yet developed in line have created a new position at the Executive Board level for with our ambitious expectations, yet we achieved full-year a Head of Global Sales, who will be appointed in We revenue growth of 12% in local currencies to CHF 149 million. have also created an additional sales region in Europe, and Despite this, we maintained our position in this important have continued to recruit and train new sales personnel in market and continued to improve our profitability. While all regions. These improvements will help us to implement we are confident that we will be able to further accelerate global strategies consistently, to become more effective at growth, it will be difficult to close the gap on the local market leader in the foreseeable future by organic growth alone. master processes efficiently throughout the organization. the operational level, to further improve productivity, and to We are therefore open to considering strategic options for extrinsic growth in the North American market provided AN APPROPRIATE MIX OF SKILLS they make sense and enhance shareholder value. For the second consecutive year we have been ranked among In the Asia/Pacific region, full-year revenues grew 12% to the top 100 companies in the Europe s 500 survey published CHF 57 million. We continue to experience volatile quarterly by BusinessWeek magazine. With our workforce expanding sales development there owing to the lack of direct market to 1534, we have continued to create jobs and career opportunities. In addition to attracting new talent, we have provided presence. The exception, of course, is Australia, which has performed well and has now been complemented by direct more training for our employees and managers to help them distribution in New Zealand. Our strategic goal is still to secure direct ac- of future growth. Clearly we will have advance and to master the challenges WE HAVE CONTINUED TO CREATE JOBS AND CAREER OPPORTUNITIES cess to customers in all key markets to continue to import talent and competencies from other industries and larger organizations, throughout the region in the coming years. At the beginning of 2007, we signed a memorandum of understanding that but we are nonetheless committed to developing our own paves the way for us to acquire the Straumann-related business of our Japanese distributor. Once completed, the trans- Change and rapid growth place high demands on the energy people to ensure consistency and an appropriate mix. action will give us direct access to our customers in Japan and flexibility of our staff and managers. On behalf of our as of the second-half of this year. It is important to achieve stakeholders, we would like to thank all our employees for transitions seamlessly in order to maintain the leadership their continued contributions, initiative, commitment and position that has been built up over the years by our trusted loyalty throughout the past year. partners. SHAPING A UNIQUE CULTURE ORGANIZING FOR GROWTH At the outset of 2006, we formalized and published five core Globally expanding businesses require continuous organizational and structural adaptation to ensure scalability, ef- in the future. We also launched our new corporate visual beliefs that will shape our company culture and our business fectiveness, consistency and quality. In the fourth quarter, identity to further strengthen the power of the Straumann Straumann carried out a reorganization program groupwide to streamline processes and improve operational ex- train our entire organization about our beliefs, our brand, brand. We then initiated a corporate alignment initiative to cellence. As a result, we began 2007 with a consolidated and other factors that make us stand above an increasingly divisional structure and a more focused leadership team. crowded marketplace. We consider that cultural alignment Importantly, we have defined responsibilities more clearly and consistency have a key part in the execution of strategy. for: the innovation and sales processes, lifecycle management, finances and operations. To boost our sales power, we cal training. Similarly, all our staff have received All newcomers to Straumann worldwide will receive identi- instruction

6 6 Straumann Annual Report 2006 Operational Review LETTER TO SHAREHOLDERS on ethical business behavior in our Code of Conduct, which we began to implement in The Code is designed to ensure that we do things ethically, legally and properly wherever we operate. Our business success has enabled us to continue our commitment to making dental treatment available to the underprivileged through a variety of projects in developing regions and in our own neighborhoods. These and our other efforts towards long-term sustainability are some of the factors that have contributed to our continued inclusion in the FTSE4Good index. INNOVATION FROM THE LABORATORY BENCH TO THE FACTORY FLOOR As always, simplicity and reliability continue to be our main philosophies when bringing products and services to our customers. For us, service excellence means being a trusted, consistent partner for customers around the world. It involves helping them to grow their practices and to deliver better treatment outcomes to their patients. Strong demand for our products placed considerable challenges on our production capability in Whilst our build-up in Andover continues ahead of target, we were challenged to meet demand for SLActive for much of This has driven innovation on the factory floor and prompted our engineers to develop new high-volume equipment that will boost output and ensure the highest standards of qual- The changing dynamics and challenges underline the importance of innovation and service orientation. We maintained ity. Not only will this enable us to step up our production and marketing initiatives for SLActive, it will also prepare us our leadership in scientific innovation for the forthcoming introduction of an WE MAINTAINED OUR LEADERand we are proud to report that, here exciting new implant line extension. SHIP IN SCIENTIFIC INNOVATION too, we continued to do our homework The core of this project is a bone-level diligently in Nowhere is this better illustrated than with our unrivalled implant surface technology SLActive, which brings a new standard of care to patients. Throughout the year, our extensive clinical program continued to generate remarkable, strong data that further confirm the predictability and reliability of SLActive. Independent experts now suggest that up to eight in ten patients have one or more risk factors and could benefit from SLActive 1. This, and the fact that despite high overall success rates every four minutes an implant fails somewhere, emphasizes the need for genuine improvements like SLActive. As a result, more and more leading clinicians implant that will offer additional treatment options to clinicians. It is already undergoing initial clinical development and will give us access to a significant market segment in This is just one of the exciting projects in our pipeline, which is the richest in the history of the company. It will allow us to deliver state-of-the-art solutions for any customer franchise and product category in the coming years. These projects and other initiatives give Straumann an excellent basis for continued growth in an attractive market provided, of course, that they offer evidence-based benefits for customers and patients. worldwide are adopting this technology as their product of choice. This was exemplified in the successful North American launch of SLActive and its continued roll-out in Europe. Apart from introducing numerous small but nonetheless significant improvements to our existing range, we also continued the roll-out of our fully-synthetic bone substitute Straumann BoneCeramic, which we also launched as a combination with Straumann Emdogain, called Emdogain PLUS. 1 Barter, S. Make a difference in your most challenging cases. Data presented at European Association for Osseointegration 15th Annual Scientifi c Meeting, 5 7 October 2006, Zurich, Switzerland. 2 Based on an implant success rate of 97% and an estimated 4.8 million implants placed in 2005.

7 Straumann Annual Report 2006 Operational Review LETTER TO SHAREHOLDERS 7 STRONG PARTNERSHIPS WITH ACADEMIA Our activities in research and education are driven through the International Team for Implantology (ITI), an independent global network that includes prominent academics at the world s leading universities and dental schools. This ensures high standards in education, treatment quality and patient care. It also links Straumann closely with leading universities and academia. The ITI staged numerous highly successful scientific congresses around the globe throughout 2006, and increased its membership dramatically. to include the opinions of leading independent experts to provide you with an even broader view of what is happening in our extremely exciting environment. Finally, we want to thank you, our shareholders, and our other stakeholders for the continued support and confidence in Straumann. Basel, 1 February 2007 OUTLOOK Our many achievements in 2006 were driven by our commitment to simply doing more for dental professionals. We have begun 2007 mindful of our core belief achieving more is our future. Looking ahead, we remain very optimistic about the inherent growth opportunities in the field of implant dentistry and oral tissue regeneration. We believe that the global market will prosper further and grow in the mid-teen range over the coming years. By virtue of our innovation and service leadership, we are confident that, in the coming years, we will be able to grow above market in terms of revenue, while expanding our margins thanks to further improvements in operational excellence. In 2006, the first dental implant in an outreach program was placed in Alaska. It was part of our sponsorship of the American Prosthodontics Society s Teeth for Alaska mission. A few months later, kilometers away, we began serving customers directly in New Zealand. These two events at opposite ends of the earth illustrate the breadth of our continuing efforts to bring a better standard of care to patients around the world. This Annual Report provides details and insights to give you a fuller picture. In preparing it we followed the reporting guidelines of the Global Reporting Initiative (GRI), reflecting the importance we attach to sustainability. For the third year running, we are privileged Dr h.c. Rudolf Maag Chairman Gilbert Achermann President and Chief Executive Officer

8 8 Straumann Annual Report 2006 Operational Review STRAUMANN IN BRIEF STRAUMANN IN BRIEF WHO WE ARE, WHAT WE STAND FOR, WHERE WE ARE HEADED, AND WHAT MAKES US SPECIAL OUR COMPANY OUR CORE BELIEFS Headquartered in Basel, Switzerland, the Straumann Group is a global leader in implant dentistry and oral tissue regeneration. In collaboration with leading clinics, research institutes and universities, the Group researches and develops implants, instruments, and tissue regeneration products for use in tooth replacement solutions or to prevent tooth loss. The Group manufactures implant system components and instruments in Switzerland and the US, and oral tissue regeneration products in Sweden. Straumann also offers comprehensive services to the dental profession worldwide, including training and education, which is provided in collaboration with the International Team for Implantology (ITI). Altogether, Straumann employs 1534 people worldwide, and its products and services are available in more than 60 countries through the Group s 18 distribution subsidiaries and broad network of distribution partners. More about the company structure, organization and management can be found in the Corporate Governance chapter (pp ). OUR VISION To be the partner of choice in implant dentistry and oral tissue regeneration. OUR MISSION SPECIALIZATION IS OUR SOUL For more than half a century we have concentrated our scientific expertise and our passion for excellence on researching and delivering superior solutions. Our success comes from a clear strategic focus in implant dentistry. SIMPLICITY IS OUR STRENGTH We translate complex technology and procedures into userfriendly solutions to improve the standard of patient care. For us, simplicity also means being straightforward in all our relationships to build trust and respect. CUSTOMERS ARE OUR INSPIRATION We are dedicated to the success of every customer and the well-being of every patient. That is why we always seek to understand the customer s perspective and deliver more than implants. RELIABILITY IS OUR TRADEMARK We deliver peace of mind. Our customers and patients rely on us for thoroughly researched, predictable solutions. We never compromise on quality. ACHIEVING MORE IS OUR FUTURE We strive relentlessly to provide better solutions and to create higher value for our stakeholders and employees. We must always believe in our ability to achieve more. We are committed to creating success for customers in implant dentistry and tissue regeneration. By simply doing more, we deliver superior solutions that enable dental professionals to provide the best possible care to patients.

9 Straumann Annual Report 2006 Operational Review STRAUMANN IN BRIEF 9 OUR STRATEGY BUSINESS FOCUS Our strategy is to maintain our focus on implant dentistry and tissue regeneration and related fields where we want to become the partner of choice. While market dynamics and our own range of products and services provide potential for continued attractive organic growth, we are carefully monitoring trends and evaluating opportunities in implant dentistry, tissue regeneration and closely related fields, with the goal of complementing our portfolio, exploiting synergies, and enabling us to bring further meaningful innovations and benefits to customers and patients. Our objective is to capitalize on the market growth potential by increasing awareness for our solutions among dental professionals and patients, continuing to introduce product innovations with proven clinical benefits, and building unparalleled brand awareness. INNOVATIONS WITH PROVEN BENEFITS We believe that continued product and service innovation, tailored to the different customer segments and skill levels, is key to our future success. Innovations must deliver genuine benefits to patients and customers, and an acceptable cost-benefit ratio. The benefits need to be compelling and substantiated by clinical evidence, which in turn is the basis for our proposition of value creation. SOLID FINANCIAL BASE AND FOCUS ON LONG-TERM SHAREHOLDER VALUE Straumann has a solid financial base and strategic financial flexibility. We have signaled our intention to return excess liquidity to our shareholders in the absence of major strategic undertakings, such as operational expansion or value enhancing acquisitions. DIRECT ACCESS TO CUSTOMERS AND BROAD GEOGRAPHIC FOCUS We continue to believe that, in order to serve our customers best, it is essential to have direct access to them. Our intention, therefore, is to continue to gain greater control over our distribution channels, wherever possible and appropriate, allowing us to offer superior solutions and service based on closeness to customers. We are committed to maintaining and solidifying our leading position in Europe through continued investments in sales, marketing, and education. In addition, we will develop selected Eastern European markets in the coming years. In North America, we are continuing our efforts to strengthen our current presence, not ruling out extrinsic growth opportunities to increase our share of voice. In Asia/Pacific, we aim to establish a direct presence in all key markets and to open an Asian regional office in the near future.

10 10 Straumann Annual Report 2006 Operational Review STRAUMANN IN BRIEF OUR HISTORY The history of the Straumann Group has three distinct eras and spans more than half a century. It began in the Swiss village of Waldenburg in 1954 with the foundation of a research institute bearing the name of its founder, Dr Ing. Reinhardt Straumann. Between 1954 and 1970 the company specialized in alloys used in timing instruments and in materials testing. Among Straumann s renowned inventions in this period were special alloys that are still used in watch springs today. A breakthrough in the use of non-corroding alloys for treating bone fractures prompted Dr Fritz Straumann, the founder s son, to enter the fields of orthopedics and dental implantology, which began the second phase of the company s history. Between 1970 and 1990, Straumann became a leading manufacturer of osteosynthesis implants. A management buy-out of the osteosynthesis division in 1990 led to the creation of Stratec (subsequently Synthes) as a separate company. Thus, 1990 marked the beginning of the Straumann Group as it is known today. Thomas Straumann, grandson of the founder, headed the remaining part of the firm, which employed just 25 people focused exclusively on dental implants. In 1998, Straumann Holding AG became a publicly traded company on the Swiss Exchange. Through the acquisition of Kuros Therapeutics (2002) and Biora (2003), Straumann entered the promising field of oral tissue regeneration. Another major milestone in the company s history was in 1980 when Straumann established a partnership with the International Team for Implantology, forming a symbiosis of research expertise and industrial know-how. The 1980s also marked the company s geographic expansion, with subsidiaries in Germany (1980) and the US (1989). The following are examples of the groundbreaking achievements that have established Straumann as a leading innovator in implant dentistry: 1974 The one-stage surgical procedure, the rough implant surface, and an implant design that respects biologic width The Morse taper connection, still widely used today SLA, the first macro- and microtextured rough surface, which reduced implant osseointegration time by half SLActive, the first hydrophilic surface, which cuts healing times by half again. OUR BRAND Research has shown that the great majority of consumer/ purchasing decisions are driven by emotional factors, e.g. brand association, rather than rational considerations. 3 With several hundred implant manufacturers around the world competing for the trust of customers, strong branding and corporate identity are assets that differentiate Straumann in an increasingly crowded and competitive marketplace. Furthermore, brand awareness is more important at the professional level than among consumers, because the selection of the implant system is made by the dentist, not the patient. In 2005 and 2006, Straumann conducted customer surveys in key markets, which confirmed that brand recognition by dental professionals is one of the three main criteria that influence the choice of implant system. In two surveys, customers told us that we should be bolder in adopting a more emotional approach in our branding without compromising our reasoned and scientific values. Using this and other findings, we revised and developed our branding strategy and corporate identity to leverage the power of our brand according to market-relevant criteria, and to differentiate Straumann from the competition. 3 Kenning, Deppe M, Schwindt W, Kugel H, Plassmann H. Wie eine starke Marke wirkt. Harvard Business Manager 2005; 3:53-57.

11 Straumann Annual Report 2006 Operational Review STRAUMANN IN BRIEF 11 The surveys confirmed that customers expect continued service excellence, expert support for instance, in education/ training and sales/marketing, and they expect to gain from networking with experts and colleagues through platforms such as the International Team for Implantology. This endorses our philosophy of providing more than implants with our guiding principle of simply doing more. This is not merely a catchphrase; it is our company culture, and should be expressed in every interaction with customers. Hence, branding is not the initiative of a single department, it has to be supported by all our staff. To this end we initiated a Corporate Alignment Program throughout the company in 2006 to ensure that all Straumann employees are committed to simply doing more for dental professionals. The program also provided instruction on our strategy, company focus, history, and core beliefs, in addition to understanding the importance of consistency in branding. In mid-year, we introduced a new Straumann Brand Design to support and communicate our company values and brand. The white background represents simplicity, while the rich green background, which is closely connected to Straumann s tradition and identity, symbolizes reliability. The implant icon is a further symbol of Straumann s history, commitment and specialization in implant dentistry. PROTECTING THE STRAUMANN BRAND It is a priority for the company not only to enhance but also to protect the value of the Straumann brand. For this reason, we have increased our trademark protection activities and have built up a broad and strong trademark portfolio. In 2006, a number of warning letters were sent to infringing parties. One legal action for trademark infringement was pursued by Straumann in 2006 against a major competitor and is currently in progress. The Group regularly scrutinizes competitor products, materials and activities, and will continue to defend its trademark position vigorously wherever appropriate. Elements in Straumann s new corporate visual identity

12 LAUGHTER SHIFTS THE BODY INTO TOP GEAR, STIMULATING 17 MUSCLES IN THE FACE AND 80 THROUGHOUT THE BODY. AIR IS FORCED THROUGH THE LUNGS AT 60 MILES PER HOUR, AND THE HEART BEATS AS FAST AS IT DOES IN A SPRINT. LAUGHTER IS FOLLOWED BY A PHASE OF RELAXATION. LAUGHING FOR A SINGLE MINUTE IS JUST AS RELAXING AS 45 MINUTES OF WHOLE-BODY RELAXATION EXERCISES. STRAUMANN PRODUCTS RESTORE LAUGHTER AND ARE MEDICINE FOR THE SOUL.

13

14 14 Straumann Annual Report 2006 Operational Review MARKETS AND REGIONS MARKETS AND REGIONS AS A LEADER IN ALL OUR ESTABLISHED MARKETS AND A PIONEER IN EMERGING MARKETS, WE ARE DEDICATED TO THE SUCCESS OF CUSTOMERS AND THE WELL-BEING OF PATIENTS ALL OVER THE WORLD. DENTAL IMPLANTS: A LASTING SOLUTION TO A GROWING NEED Implant-borne tooth restorations closely mirror natural teeth and offer distinct advantages over conventional treatments. One of the major benefits of dental implants is that they provide a stable foundation for replacement teeth and help preserve the neighboring teeth and bone structure. The survival rates of implants are very high and are based on extensive clinical data. 4 In addition, long-term overall costs are lower than with conventional treatment. 5 Furthermore, implants have been shown in clinical studies to improve the quality of life and well-being of patients. 6 Implants can be used to replace individual teeth (by securing a crown to a single implant) or multiple teeth (bridges or dentures secured to multiple implants). TREATMENT OPTIONS FOR TOOTH LOSS Single-tooth replacement with conventional crowns and bridge (left) and with an implant-based solution (right) that preserves the neighboring teeth The most common cause of tooth loss is not accidents but periodontal disease, which affects the majority of adults. In fact, 5 20% of any population suffers from severe forms of the disease. 7 Despite their proven advantages over conventional treatment, implant-based restorations are generally not reimbursed by insurance schemes. TO REFER, OR NOT TO REFER The global implant dentistry market can be generally categorized according to two models depending on the extent to which patients are referred. In the referral system, implants are predominantly placed by specialists or oral surgeons, and the referring doctor or generalist completes the prosthetic restoration. By contrast, in the non-referral model, both procedures are more commonly performed by the same doctor. The world s largest single market, the US, is predominantly referral-based. In Europe, countries such as Germany, the Netherlands, and Sweden are characterized by the referral system, whereas Italy, Spain, France and others are predominantly non-referral. In countries where referrals are less common, Straumann offers a surgical support service to ensure that practitioners get off to a successful start in implant techniques. Elsewhere, in places where the referral model predominates, our marketing efforts are geared towards building and supporting the corresponding referral networks. The aim is to connect dentists who are starting out in implant prosthetics with experienced surgeons who can offer effective support during diagnosis, treatment planning and prosthetic restoration. In addition, we provide local support through medical product specialists and regional training courses tailored to all levels, particularly the less experienced, helping to ensure that first cases are successful and result in patient satisfaction. Implant solutions for multiple-tooth replacement, including full dentures

15 Straumann Annual Report 2006 Operational Review MARKETS AND REGIONS 15 MARKET SIZE AND GROWTH GLOBAL IMPLANT MARKET BY REGION It is difficult to determine the size and growth of the overall market accurately because distribution models, product portfolios and disclosure levels vary widely within the sector. According to recent estimates, the global implant dentistry market was worth CHF 2.4 billion in 2006 and is thought to have grown 16 17% in Europe accounts for roughly half the market, while North America represents about a third. Taking into account the numerous small local manufacturers, particularly in Asia/Pacific and in the rest of the world, the overall market is probably somewhat larger. Rest of World approx. 5% Asia/Pacific 10 15% North America 30 35% Europe 50 55% Source: Straumann estimates (based on business intelligence and end-market revenues where available) MARKET PENETRATION Europe North America RoW* Population 380 million 330 million 410 million Prevalence of tooth loss 45 50% 45 50% 60 65% Affected people 180 million 155 million 265 million Annual treatment rate 10 12% 9 11% 6 8% People seeking treatment 20 million 15 million 21 million Exclusion for medical/other reasons 40 60% 40 60% 40 60% People eligible for implant treatment 10 million 8 million 11 million Implant treatment rate 12 14% 6 8% 5 7% People treated with implants 1.3 million 0.5 million 0.8 million Estimated prevalence of tooth loss and treatment rates in the industrialized world * Australia, Japan, South Korea, Taiwan, Brazil Source: Straumann estimates 4 Schwartz-Arad D, Herzberg R, Levin L. Evaluation of long-term implant success. J Periodontol 2005; 76: Bragger U, Krenander P, Lang NP. Economic aspects of single-tooth replacement. Clin Oral Implants Res 2005; 16: Heydecke G, Thomason J, Lund J, Feine J. The impact of conventional and implant-supported prostheses on social and sexual activities in edentulous adults: Results from a randomized trial 2 months after treatment. J Dent Res 2005; 33: Epidemiology of Periodontal Diseases. American Academy of Periodontology report. J Periodontol 2005; 76:

16 16 Straumann Annual Report 2006 Operational Review MARKETS AND REGIONS Implant dentistry is predominantly a substitution market, and despite the double-digit market growth over the past years, market penetration remains remarkably low. Of more than 600 million people affected by tooth loss in the developed world, less than 60 million seek treatment every year (see table on previous page). About half of these would be eligible for implant treatment based on their medical and financial status, but it is estimated that less than 1 in 10 eligible patients is treated with implants. In Europe, the implant treatment rate is about 13%, in contrast to North America and the rest of the developed world where the comparative rates are only about 7% and 6%, respectively. MARKET SHARE The market continues to be dominated by a small number of major players, with the top five companies accounting for around 85% of the total market. Apart from the established global players, numerous smaller suppliers are trying to enter or further penetrate this highly attractive growth market. Most of them have little clinical documentation, or lack a broad, in-depth service offering. Often, they compete on a local level only. Straumann maintained its global number two position in 2006, controlling around a quarter of the market, while Nobel Biocare continues to lead the market with a market share of more than 30%. Other major global players are Biomet/3i, Zimmer, Dentsply, Astra Tech and Osstem. ESTIMATED GLOBAL IMPLANT MARKET BY SHARE Others 14% Dentsply 5% Zimmer 9% Biomet/3i 13% Source: Straumann estimates (based on market intelligence and end-market revenues for the first 9 months of 2006, where available) GROWTH DRIVERS AND TRENDS Nobel Biocare 33% Straumann 26% The main driver for market growth is the increasing acceptance of implants due to their advantages over conventional tooth replacement. In addition, demographic trends, such as the aging population and increasing wealth, further support market growth. Furthermore, dental implant training and education of dental practitioners remains a key prerequisite for meeting patient demands and driving market growth. Indeed, the limited number of dentists currently offering dental implant treatment, especially in North America and Asia, underpins the huge growth opportunity in these markets. Lastly, most suppliers currently focus their activities on developed countries, leaving a huge untapped potential in the emerging economies over the medium-term. The success of implants has increased the expectations of patients and practitioners. Consequently, patients expectations have moved beyond impeccable function to include lasting esthetic quality, fast and painless replacement procedures, and good value for money. However, in the discussion of treatment prices, it is often overlooked that implant components account for only about 15 20% of overall

17 Straumann Annual Report 2006 Operational Review MARKETS AND REGIONS 17 treatment costs. Furthermore, consumers and customers are not always mindful of the fact that overall lifetime costs of implant-based solutions are more favorable than conventional alternative treatments in most cases. OUTLOOK Over the next few years, we expect the global market to continue to grow at least at 15%. Straumann s goal is to continue to grow above this by virtue of innovation and our superior service offering. STRAUMANN SALES IN 2006 BY REGION Rest of World 2% Asia/Pacific 10% North America 25% Europe 63% STRAUMANN S EXPANDING GLOBAL PRESENCE EUROPE In 2006, a team supported by Straumann placed the first dental implant in an outreach program in Alaska. Shortly after, at the other end of the world, we began serving customers directly in New Zealand. Between these latitudes our products and services are sold in over 60 countries through 18 sales and marketing subsidiaries (see p. 166) and a broad network of distributors. In 2006, Europe continued to be the largest market region in terms of sales, followed by North America and Asia/Pacific. Based on available data, we estimate that the European dental implant and oral tissue regeneration market grew in the low-teens in By contrast, Straumann sustained the strong growth achieved in the previous year, with revenues up 19% in local currencies (20% in CHF) to CHF 381 million. While Germany continued to be the main contributor to European sales, a good performance was posted by Straumann Iberia, the Group s third largest subsidiary in Europe after Italy, and ahead of Switzerland. The UK and France also posted the most dynamic regional growth rates, and performances elsewhere were generally solid with all countries yielding double-digit underlying growth. The performance was lifted by the successful introduction/ roll-out of new products. Our third-generation implant surface technology SLActive became available throughout Europe on all our main implant types. We also extended Straumann CARES, our individualized abutment service, broadly in Europe, and we completed the roll-out of our fully-synthetic bone augmentation product, Straumann BoneCeramic, which was also launched as a convenient product combination under the brandname Emdogain PLUS.

18 18 Straumann Annual Report 2006 Operational Review MARKETS AND REGIONS Our share of voice among dental professionals was amplified through highly successful ITI congresses in Europe, which attracted some 4000 participants. We also initiated a pilot project in Austria to help increase patient information through the national media. If the results are promising, the campaign will be broadened to other countries. With the acquisition of our Danish distributor, which became effective at the beginning of 2006, we achieved our ambition of controlling all our distribution channels in Western Europe. A CHANGING HEALTHCARE ENVIRONMENT The frequency of implant-based procedures varies from country to country. Treatment with implants is for example about 10 times more common in Switzerland than in the UK based on implants per population. The reasons for the disparity lie mainly in the number of dentists offering implant treatment, the education level of dentists, patient awareness, and factors such as average income, oral hygiene, and, finally, the various healthcare and reimbursement systems. Following changes in healthcare reimbursement in Sweden in 2005 and the Netherlands in 2006, Straumann enjoyed positive growth in those countries. In the UK, changes in the National Health Service did not have a negative impact on our sales. On the contrary, the UK has become one of our fastest growing European markets, enabling us to relocate its headquarters and combine it with a new training center close to London s Gatwick hub. Straumann UK s new headquarters and training center in the Pegasus building near London s Gatwick airport The debate about healthcare insurance and reimbursement in Germany continues, but no prognosis can be made in the current absence of details regarding proposed legislation. It is also difficult to gauge what effect the increase in VAT will have on German consumer spending and whether this in turn will affect implant dentistry. OUTLOOK (EUROPE) Although market penetration rates measured in the annual number of treated patients are higher in Europe than elsewhere, the European dental implant market is estimated by independent sources to grow annually in the low to mid teens over the coming years. Our goal is to maintain market leadership through continued investment in sales, marketing and education. We believe that we have the basis to outpace the market over the coming years. Having achieved our ambition of gaining direct distribution in all major Western European countries, we will seek continuous operating improvements in all our established markets. Furthermore, we shall take advantage of the expansion of the European Union and work towards further developing emerging Eastern European markets.

19 Straumann Annual Report 2006 Operational Review MARKETS AND REGIONS 19 EXECUTIVE INTERVIEW FOCUS: MARKET USA Jim Frontero, President & CEO Straumann USA WHAT IS THE MOST DIFFICULT CHALLENGE FOR STRAUMANN USA NORTH AMERICA The North American market for dental implants continues to grow strongly due to increased awareness through media coverage, dental meetings, and the broader inclusion of implant dentistry into dental school curricula. Furthermore, the market upside continues to be extraordinary, as it is estimated that only around 7% of the North American dental implant market is currently served. In addition to the growing number of professionals placing implants, patient demand continues to rise driven by increasing attention paid to personal esthetics and a healthy, active life-style particularly among the wealthier aging population. These positive market factors helped us increase North American revenues by 12% (in l.c.) in 2006 to CHF 149 million, which corresponds to 25% of Group revenues. For the US, which is the world s largest single market, 2006 was marked by many achievements and challenges for Straumann. We continued to settle into our new North American headquarters in Andover, Massachusetts. The build-up of production moved ahead faster than planned, with more than components produced to our high precision standards (see p. 34 for further details). Our new state-of-the-art training facility in Andover hosted a significant portion of the thousands of customer education and training events countrywide. We increased our US sales force and began 2007 with double the team we had at the outset of Importantly, we have improved our structure, territory planning and customer coverage, and the training of our sales representatives. During the year, talent retention became particularly important, prompting us to review our incentive program and reward system for performance and loyalty. We also refined our hiring standards. TODAY? Dynamic growth and competition compel us to differentiate Straumann from our rivals through superior technology and service. We made significant progress on this in 2006 with the successful introduction of SLActive, the systematic upgrade of personnel and improved business processes. Harmonizing these changes to drive above-market growth and productivity gains in 2007 is our biggest challenge today. HAVE CUSTOMER- AND STAFF-LOYALTY BEEN A PROBLEM? In 2006, we earned the trust and business of new customers and we established an attractive loyalty program. In the near term, new products and a bone-level implant line will further strengthen our competitiveness. Our requirements for higher performance, dedication to organizational development, utmost integrity and commitment have led to personnel changes. These are not due to an underlying problem, but are the result of thoughtful preparation for future success. I am pleased to observe renewed spirit and energy throughout our US operation. IS MORE AGGRESSIVE MARKETING TO GENERAL DENTISTS AND PATIENTS THE ANSWER? With only some 15% of dental professionals surgically active in placing implants, the US dental implant market is underpenetrated and offers huge potential. Targeted initiatives to raise awareness among generalists and patients are positive. To ensure sustainable treatment success, our strategy uses a team approach with the surgical specialist, the restorative generalist and the dental technician. This approach is supported through educational events and programs to build referral relationships. CAN YOU NARROW THE GAP ON THE MARKET LEADER BY ORGANIC GROWTH? I believe we can. How quickly depends on our execution of three specific growth strategies: Leading the market with needed, scientifically proven technologies; partnering with specialists and referring practitioners, and investing more aggressively in the future generation of surgical dentists. The first two will secure short- and mid-term market share gains. The latter will expand the marketplace and seed it with key clinicians who view our dental implant system as the reference standard.

20 20 Straumann Annual Report 2006 Operational Review MARKETS AND REGIONS Two highly experienced managers with impressive track records in the healthcare industry were appointed to lead our ASIA/PACIFIC AND REST OF THE WORLD efforts in North America. Jim Frontero was nominated CEO With the exception of Australia and New Zealand, Straumann serves the Asia/Pacific (APAC) region through dis- and President of Straumann USA, LLC in October, and Alain Laroche was hired in August to head our Canadian organization. At year-end, we employed more than 300 people in sales. tributors and thus reports only a portion of the total market North America. In 2006, our revenues in the APAC region increased 12% (in One of the most important initiatives was the regional CHF) to CHF 57 million. While consistent strong growth was launch of SLActive. Its rapid adoption by existing and new posted by the new Australian subsidiary, the main developed customers alike revealed that the North markets (Japan, Korea and Taiwan) experienced slower growth ONE OF THE MOST IMPORTANT American market values scientifically documented innovation with genuine benefits. than in the previous year, due in INITIATIVES WAS THE REGIONAL Greater-than-anticipated demand combined INTRODUCTION OF SLActive part to the aggressive tactics of with limited supply in the first six months prompted us to competitors, particularly copycats. This, and the strong fluctuations in ordering patterns reinforces our resolve to gain restrict sales to early adopters, thus constraining full-year revenues. We have since been able to broaden supply. direct market presence in these areas in order to ward off competition and own our customer relationships. OUTLOOK (NORTH AMERICA) A small but significant move in this direction was taken in Based on the favorable substitution potential, low penetration level and particularly interesting referral market oppor- 2007, having discontinued the existing agreement. We also New Zealand, where we took over distribution in January tunities, the North American implant market is expected to succeeded in taking over the existing sales personnel, making the transfer seamless. grow favorably in the high teens. Despite our past investment and operational efforts, we have not yet captured significantly greater share of voice in the US. One approach to 12 million, Straumann also operates through distributors, In the rest of the world, where revenues rose 12% to CHF this would be to explore opportunities for extrinsic growth. with the exception of Brazil. Although the latter is the largest market in the region, it is characterized by numerous However, our immediate approach in 2007 will be to continue our internal initiatives to accelerate sales growth, focusing particularly on leadership, sales productivity and ed- spite of this, we achieved very strong growth there in low-price local manufacturers, making business difficult. In ucation initiatives. Optimized resource alignment, improved business processes, and efficiency increases in our sales organization, combined with full availability of SLActive, will help drive growth in 2007 and beyond.

2014 First-quarter revenue

29.04. First-quarter revenue Conference Call Basel, 30 April Disclaimer This presentation contains certain forward-looking statements that reflect the current views of management. Such statements are subject

29.04. First-quarter revenue Conference Call Basel, 30 April Disclaimer This presentation contains certain forward-looking statements that reflect the current views of management. Such statements are subject

Straumann posts 5% growth in local currencies (l.c.) in the first nine months of 2011, lifted by strong sales in North America

in the first nine months of 2011, lifted by strong sales in North America") Media release Straumann posts 5% growth in local currencies (l.c.) in the first nine months of 2011, lifted by strong sales in North America Net revenue reaches CHF 518 million, driven by growth across

Media release Straumann posts 5% growth in local currencies (l.c.) in the first nine months of 2011, lifted by strong sales in North America Net revenue reaches CHF 518 million, driven by growth across

2012 Full-year results

2012 Full-year results Analysts & Media Conference Basel, 21 February 2013 Disclaimer This presentation contains certain forward-looking statements, which can be identified by the use of terminology such

2012 Full-year results Analysts & Media Conference Basel, 21 February 2013 Disclaimer This presentation contains certain forward-looking statements, which can be identified by the use of terminology such

2013 First-quarter results

2013 First-quarter results Analysts & Media Conference Call Basel, 30 April 2013 Disclaimer This presentation contains certain forward-looking statements, which can be identified by the use of terminology

2013 First-quarter results Analysts & Media Conference Call Basel, 30 April 2013 Disclaimer This presentation contains certain forward-looking statements, which can be identified by the use of terminology

2013 Half-year results

Half-year results Analysts & Media Conference Basel, 20 August Disclaimer This presentation contains certain forward-looking statements, which can be identified by the use of terminology such as will,

Half-year results Analysts & Media Conference Basel, 20 August Disclaimer This presentation contains certain forward-looking statements, which can be identified by the use of terminology such as will,

World leading in innovative restorative and esthetic dental solutions.

World leading in innovative restorative and esthetic dental solutions. Individualized crowns, bridges, veneers and abutments Standardized implants and abutments TiUnite surface At a glance Nobel Biocare

World leading in innovative restorative and esthetic dental solutions. Individualized crowns, bridges, veneers and abutments Standardized implants and abutments TiUnite surface At a glance Nobel Biocare

MarketsandMarkets. http://www.marketresearch.com/marketsandmarkets-v3719/ Publisher Sample

MarketsandMarkets http://www.marketresearch.com/marketsandmarkets-v3719/ Publisher Sample Phone: 800.298.5699 (US) or +1.240.747.3093 or +1.240.747.3093 (Int'l) Hours: Monday - Thursday: 5:30am - 6:30pm

MarketsandMarkets http://www.marketresearch.com/marketsandmarkets-v3719/ Publisher Sample Phone: 800.298.5699 (US) or +1.240.747.3093 or +1.240.747.3093 (Int'l) Hours: Monday - Thursday: 5:30am - 6:30pm

Company information for patients. More than Swiss precision. A better quality of life.

Company information for patients More than Swiss precision. A better quality of life. More than the latest technology. Long-lasting satisfaction. FEW COMPANIES HAVE SO MUCH TO OFFER More than 35 years

Company information for patients More than Swiss precision. A better quality of life. More than the latest technology. Long-lasting satisfaction. FEW COMPANIES HAVE SO MUCH TO OFFER More than 35 years

Caring, one person at a time.

JOHNSON & JOHNSON STRATEGIC FRAMEWORK Caring, one person at a time. STRATEG IC FRAM EWOR K 1 Nothing is more important than the health and well-being of those we love. That s why the Johnson & Johnson

JOHNSON & JOHNSON STRATEGIC FRAMEWORK Caring, one person at a time. STRATEG IC FRAM EWOR K 1 Nothing is more important than the health and well-being of those we love. That s why the Johnson & Johnson

2012 Letter from Our Chief Executive Officer

2012 Letter from Our Chief Executive Officer Our strong performance in fiscal 2012 demonstrates that our growth strategy enabled us to further differentiate Accenture in the marketplace and deliver significant

2012 Letter from Our Chief Executive Officer Our strong performance in fiscal 2012 demonstrates that our growth strategy enabled us to further differentiate Accenture in the marketplace and deliver significant

Medium-term Business Plan

Mitsubishi UFJ Financial Group, Inc. Medium-term Business Plan Tokyo, May 15, 2015 --- Mitsubishi UFJ Financial Group, Inc. (MUFG) announced today that it has formulated its medium-term business plan for

Mitsubishi UFJ Financial Group, Inc. Medium-term Business Plan Tokyo, May 15, 2015 --- Mitsubishi UFJ Financial Group, Inc. (MUFG) announced today that it has formulated its medium-term business plan for

To Our Shareholders A Message from the CEO

To Our Shareholders A Message from the CEO Overview of Fiscal 2007 Performance Looking at consolidated performance during fiscal 2007, or the year ended March 31, 2007, ORIX achieved an 18% rise in net

To Our Shareholders A Message from the CEO Overview of Fiscal 2007 Performance Looking at consolidated performance during fiscal 2007, or the year ended March 31, 2007, ORIX achieved an 18% rise in net

Dental Implants and Prosthetics Market by Material, Stage, Connectors & Product Type - Global Forecast to 2020

Brochure More information from http://www.researchandmarkets.com/reports/3288512/ Dental Implants and Prosthetics Market by Material, Stage, Connectors & Product Type - Global Forecast to 2020 Description:

Brochure More information from http://www.researchandmarkets.com/reports/3288512/ Dental Implants and Prosthetics Market by Material, Stage, Connectors & Product Type - Global Forecast to 2020 Description:

AXA INVESTMENT MANAGERS

AXA INVESTMENT MANAGERS Entering a new phase of growth Investor Day November 20, 2014 Andrea ROSSI CEO AXA Investment Managers Member of the AXA Group Executive Committee Certain statements contained herein

AXA INVESTMENT MANAGERS Entering a new phase of growth Investor Day November 20, 2014 Andrea ROSSI CEO AXA Investment Managers Member of the AXA Group Executive Committee Certain statements contained herein

How international expansion is a driver of performance for insurers in uncertain times

How international expansion is a driver of performance for insurers in uncertain times Accenture Global Multi-Country Operating Model Survey May 2009 Copyright 2009 Accenture. All rights reserved. Accenture,

How international expansion is a driver of performance for insurers in uncertain times Accenture Global Multi-Country Operating Model Survey May 2009 Copyright 2009 Accenture. All rights reserved. Accenture,

Agreement to Acquire 100% Ownership of Protective Life Corporation

[Unofficial Translation] June 4, 2014 Koichiro Watanabe President and Representative Director The Dai-ichi Life Insurance Company, Limited Code: 8750 (TSE First section) Agreement to Acquire 100% Ownership

[Unofficial Translation] June 4, 2014 Koichiro Watanabe President and Representative Director The Dai-ichi Life Insurance Company, Limited Code: 8750 (TSE First section) Agreement to Acquire 100% Ownership

TO OUR SHAREHOLDERS A MESSAGE FROM THE CEO. shareholders equity ratio and ROE both rose to over 10%.

TO OUR SHAREHOLDERS A MESSAGE FROM THE CEO During the fiscal year ended March 31, 2004, attained record-high total revenues, income before income taxes, and net income. We also made steady progress in

TO OUR SHAREHOLDERS A MESSAGE FROM THE CEO During the fiscal year ended March 31, 2004, attained record-high total revenues, income before income taxes, and net income. We also made steady progress in

How will dentistry look in 2020?

How will dentistry look in 2020? Gilbert Achermann, Chairman Capital Markets Day Amsterdam, 16 May 2012 Methodology To complement existing research, we conducted more than 40 interviews with KOLs and dental

How will dentistry look in 2020? Gilbert Achermann, Chairman Capital Markets Day Amsterdam, 16 May 2012 Methodology To complement existing research, we conducted more than 40 interviews with KOLs and dental

Herzogenaurach, Germany, July 27, 2004 PUMA AG announces its consolidated nd

P Quarter P Half-Year For immediate release MEDIA CONTACT: INVESTOR CONTACT: U.S.A.: Lisa Beachy, Tel. +1 617 488 2945 Europe: Ulf Santjer, Tel. +49 9132 81 2489 Dieter Bock, Tel. +49 9132 81 2261 Herzogenaurach,

P Quarter P Half-Year For immediate release MEDIA CONTACT: INVESTOR CONTACT: U.S.A.: Lisa Beachy, Tel. +1 617 488 2945 Europe: Ulf Santjer, Tel. +49 9132 81 2489 Dieter Bock, Tel. +49 9132 81 2261 Herzogenaurach,

Remarks by George Quinn (slides 2 to 12), Chief Financial Officer of Zurich Insurance Group.

, Chief Financial Officer of Zurich Insurance Group.") Q1 Results 2015 Remarks by George Quinn (slides 2 to 12), Chief Financial Officer of Zurich Insurance Group. May 7, 2015 Slide 2: Key highlights Good morning or good afternoon. My name is George Quinn

Q1 Results 2015 Remarks by George Quinn (slides 2 to 12), Chief Financial Officer of Zurich Insurance Group. May 7, 2015 Slide 2: Key highlights Good morning or good afternoon. My name is George Quinn

More than a fixed rehabilitation.

More than a fixed rehabilitation. A reason to smile. In combination with: Patient expectations drive dental treatments for fixed edentulous immediate restorations. Patients today have increasingly high

More than a fixed rehabilitation. A reason to smile. In combination with: Patient expectations drive dental treatments for fixed edentulous immediate restorations. Patients today have increasingly high

Management s Discussion and Analysis

Management s Discussion and Analysis 6 Financial Policy Sysmex regards increasing its market capitalization to maximize corporate value an important management objective and pays careful attention to stable

Management s Discussion and Analysis 6 Financial Policy Sysmex regards increasing its market capitalization to maximize corporate value an important management objective and pays careful attention to stable

Strategic Plan 2013-2017

Strategic Plan 2013-2017 2 P age Presidents Welcome It is my great pleasure to present the European Federation of Periodontology s strategy for 2013-2017. This is the European Federation of Periodontology

Strategic Plan 2013-2017 2 P age Presidents Welcome It is my great pleasure to present the European Federation of Periodontology s strategy for 2013-2017. This is the European Federation of Periodontology

Straumann Dental Implants Confident smiles

Straumann Dental Implants Confident smiles STRAUMANN DENTAL IMPLANTS - DESIGNED TO LAST A LIFETIME Dental Implants The decision to replace missing teeth with dental implants is an excellent investment

Straumann Dental Implants Confident smiles STRAUMANN DENTAL IMPLANTS - DESIGNED TO LAST A LIFETIME Dental Implants The decision to replace missing teeth with dental implants is an excellent investment

PRESS RELEASE. Ana Botín: Santander is well positioned to face the challenges. We will lead change GENERAL SHAREHOLDERS MEETING

PRESS RELEASE GENERAL SHAREHOLDERS MEETING Ana Botín: Santander is well positioned to face the challenges. We will lead change Banco Santander has room for growth within our customer base and in our ten

PRESS RELEASE GENERAL SHAREHOLDERS MEETING Ana Botín: Santander is well positioned to face the challenges. We will lead change Banco Santander has room for growth within our customer base and in our ten

Zurich Insurance Group. Our people 2015

Zurich Insurance Group Our people 2015 Zurich Insurance Group 1 Our people 2015 People play a crucial role in delivering Zurich s strategy and ambition to be the best insurer for our customers, the best

Zurich Insurance Group Our people 2015 Zurich Insurance Group 1 Our people 2015 People play a crucial role in delivering Zurich s strategy and ambition to be the best insurer for our customers, the best

Analysts and press conference for the financial year 2010. March 16, 2011

Analysts and press conference for the financial year 2010 March 16, 2011 Welcome Walter Gränicher Jost Sigrist Werner Schmidli Chairman of the Board of Directors Chief Executive Officer Chief Financial

Analysts and press conference for the financial year 2010 March 16, 2011 Welcome Walter Gränicher Jost Sigrist Werner Schmidli Chairman of the Board of Directors Chief Executive Officer Chief Financial

PATIENT INFORMATION. A new quality of life with dental implants. www.straumann.com

PATIENT INFORMATION A new quality of life with dental implants www.straumann.com A N E W Q U A L I T Y O F L I F E W I T H D E N T A L I M P L A N T S Contents Page 3 4 7 7 8 11 12 14 15 17 18 The beauty

PATIENT INFORMATION A new quality of life with dental implants www.straumann.com A N E W Q U A L I T Y O F L I F E W I T H D E N T A L I M P L A N T S Contents Page 3 4 7 7 8 11 12 14 15 17 18 The beauty

Management Commentary. Second Quarter 2015 Results

Management Commentary Second Quarter 2015 Results The RetailMeNot, Inc. ( RetailMeNot ) earnings call will begin on August 5, 2015 at 7:00am central time (8:00am eastern time) and will include prepared

Management Commentary Second Quarter 2015 Results The RetailMeNot, Inc. ( RetailMeNot ) earnings call will begin on August 5, 2015 at 7:00am central time (8:00am eastern time) and will include prepared

Straumann Dental Implant System. Implant Selection Guide.

Straumann Dental Implant System. Implant Selection Guide. STRAUMANN's IMPLANT PORTFOLIO The Straumann Dental Implant System offers two implant lines with diverse body and neck designs ranging from the

Straumann Dental Implant System. Implant Selection Guide. STRAUMANN's IMPLANT PORTFOLIO The Straumann Dental Implant System offers two implant lines with diverse body and neck designs ranging from the

People Strategy in Action

People Strategy in Action Welcome to Our People Strategy 2 The Bausch + Lomb People Strategy The Bausch + Lomb People Strategy 3 Introduction Transforming our company through our people Our transformation

People Strategy in Action Welcome to Our People Strategy 2 The Bausch + Lomb People Strategy The Bausch + Lomb People Strategy 3 Introduction Transforming our company through our people Our transformation

TIGroup Shareholder Update: Fiscal 2008 Major Goals Met or Exceeded. Revenue Run Rate Reaches $40M. Positive 2009 Outlook

News Release: FOR IMMEDIATE RELEASE TIGroup Shareholder Update: Fiscal 2008 Major Goals Met or Exceeded. Revenue Run Rate Reaches $40M. Positive 2009 Outlook BEVERLY HILLS, Calif. January 13, 2009 -- Tri-Isthmus

News Release: FOR IMMEDIATE RELEASE TIGroup Shareholder Update: Fiscal 2008 Major Goals Met or Exceeded. Revenue Run Rate Reaches $40M. Positive 2009 Outlook BEVERLY HILLS, Calif. January 13, 2009 -- Tri-Isthmus

For personal use only

Attention ASX Company Announcements Platform Lodgement of Open Briefing ASX ANNOUNCEMENT: 8 February 2012 CEO and CFO on Half Year Results and Outlook Open Briefing with and CFO Martin Brooke Talent2 International

Attention ASX Company Announcements Platform Lodgement of Open Briefing ASX ANNOUNCEMENT: 8 February 2012 CEO and CFO on Half Year Results and Outlook Open Briefing with and CFO Martin Brooke Talent2 International

Patient information on dental implants. More than just beautiful teeth. A comprehensive guide to dental implants.

Patient information on dental implants More than just beautiful teeth. A comprehensive guide to dental implants. 1 2 My implants have become a part of me. I don t even think about them. There s no discomfort

Patient information on dental implants More than just beautiful teeth. A comprehensive guide to dental implants. 1 2 My implants have become a part of me. I don t even think about them. There s no discomfort

2015 Russian Nanotechnology Investment Enabling Technology Leadership Award

2015 Russian Nanotechnology Investment Enabling Technology Leadership Award 2015 Contents Background and Company Performance... 3 Technology Leverage and Customer Impact of OJSC RUSNANO... 3-5 Conclusion...

2015 Russian Nanotechnology Investment Enabling Technology Leadership Award 2015 Contents Background and Company Performance... 3 Technology Leverage and Customer Impact of OJSC RUSNANO... 3-5 Conclusion...

2013 Letter from Our Chairman & CEO

2013 Letter from Our Chairman & CEO In fiscal 2013, we extended our track record of creating exceptional shareholder value. Pierre Nanterme Chairman & CEO Delivering in fiscal 2013 In fiscal 2013, Accenture

2013 Letter from Our Chairman & CEO In fiscal 2013, we extended our track record of creating exceptional shareholder value. Pierre Nanterme Chairman & CEO Delivering in fiscal 2013 In fiscal 2013, Accenture

Annual General Meeting of Beiersdorf AG, Hamburg March 31, 2015

Annual General Meeting of Beiersdorf AG, Hamburg March 31, 2015 Speech by Stefan F. Heidenreich Chairman of the Executive Board Check against delivery Page 1 / 9 Dear shareholders, ladies and gentlemen,

Annual General Meeting of Beiersdorf AG, Hamburg March 31, 2015 Speech by Stefan F. Heidenreich Chairman of the Executive Board Check against delivery Page 1 / 9 Dear shareholders, ladies and gentlemen,

We love what we do at RIM and it shows.

21 getting it right. The following discussion contains forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 15 and applicable Canadian securities laws,

21 getting it right. The following discussion contains forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 15 and applicable Canadian securities laws,

FOR IMMEDIATE RELEASE

FOR IMMEDIATE RELEASE O-I REPORTS FULL YEAR AND FOURTH QUARTER 2014 RESULTS O-I generates second highest free cash flow in the Company s history PERRYSBURG, Ohio (February 2, 2015) Owens-Illinois, Inc.

FOR IMMEDIATE RELEASE O-I REPORTS FULL YEAR AND FOURTH QUARTER 2014 RESULTS O-I generates second highest free cash flow in the Company s history PERRYSBURG, Ohio (February 2, 2015) Owens-Illinois, Inc.

Berenberg Bank European Conference 2011

Dirk W. Kirsten, CFO Süha Demokan, Head of IR 30 November 2011 Surrey, UK Disclaimer This presentation contains forward-looking statements based on beliefs of Nobel Biocare's management. When used in this

Dirk W. Kirsten, CFO Süha Demokan, Head of IR 30 November 2011 Surrey, UK Disclaimer This presentation contains forward-looking statements based on beliefs of Nobel Biocare's management. When used in this

Kuoni to focus on its core business as a service provider to the global travel industry

INFORMATION Zurich, 14 January 2015 Kuoni to focus on its core business as a service provider to the global travel industry Exit from tour operating activities Strategic initiatives to accelerate growth

INFORMATION Zurich, 14 January 2015 Kuoni to focus on its core business as a service provider to the global travel industry Exit from tour operating activities Strategic initiatives to accelerate growth

Global Dental Industry: An Analysis

Brochure More information from http://www.researchandmarkets.com/reports/1145728/ Global Dental Industry: An Analysis Description: The dental industry is one of the most attractive segments of the healthcare

Brochure More information from http://www.researchandmarkets.com/reports/1145728/ Global Dental Industry: An Analysis Description: The dental industry is one of the most attractive segments of the healthcare

Like natural teeth. Treatment with dental implants is a safe, reliable and well-proven solution for permanently replacing one or more missing teeth.

Implants for life 2 IMPLANTS FOR LIFE Like natural teeth Treatment with dental implants is a safe, reliable and well-proven solution for permanently replacing one or more missing teeth. Millions of people

Implants for life 2 IMPLANTS FOR LIFE Like natural teeth Treatment with dental implants is a safe, reliable and well-proven solution for permanently replacing one or more missing teeth. Millions of people

Every year, I look forward to the Annual General Meeting and to presenting the Board's report on Coloplast for the past financial year.

Chairman's report 2014-15 Annex 1 Michael Pram Rasmussen: 1. A challenging year for Coloplast Every year, I look forward to the Annual General Meeting and to presenting the Board's report on Coloplast

Chairman's report 2014-15 Annex 1 Michael Pram Rasmussen: 1. A challenging year for Coloplast Every year, I look forward to the Annual General Meeting and to presenting the Board's report on Coloplast

Personal and Commercial Client Group Canada

Management s Discussion and Analysis Personal and Commercial Client Group Canada Robert W. Pearce President and Chief Executive Officer, Personal and Commercial Client Group Canada Group Description Personal

Management s Discussion and Analysis Personal and Commercial Client Group Canada Robert W. Pearce President and Chief Executive Officer, Personal and Commercial Client Group Canada Group Description Personal

FTI Consulting +44 (0)20 3727 1340 Richard Mountain / Susanne Yule

20 3727 1340 Richard Mountain / Susanne Yule") 13 October 2015 THIRD QUARTER 2015 INTERIM MANAGEMENT STATEMENT Highlights* 10.2% Group gross profit growth, good contributions from all four regions FX lowered gross profit by c. 7m (c. 18m YTD) Double-digit

13 October 2015 THIRD QUARTER 2015 INTERIM MANAGEMENT STATEMENT Highlights* 10.2% Group gross profit growth, good contributions from all four regions FX lowered gross profit by c. 7m (c. 18m YTD) Double-digit

Financial Information

Financial Information Solid results with in all key financial metrics of 23.6 bn, up 0.4% like-for like Adjusted EBITA margin up 0.3 pt on organic basis Net profit up +4% to 1.9 bn Record Free Cash Flow

Financial Information Solid results with in all key financial metrics of 23.6 bn, up 0.4% like-for like Adjusted EBITA margin up 0.3 pt on organic basis Net profit up +4% to 1.9 bn Record Free Cash Flow

ROFIN-SINAR REPORTS RESULTS FOR THE FIRST QUARTER OF FISCAL YEAR 2016

- PRESS RELEASE - Contact: Katharina Manok ROFIN-SINAR 011-49-40-733-63-4256 - or - 734-416-0206 ROFIN-SINAR REPORTS RESULTS FOR THE FIRST QUARTER OF FISCAL YEAR 2016 Quarterly earnings per share increased

- PRESS RELEASE - Contact: Katharina Manok ROFIN-SINAR 011-49-40-733-63-4256 - or - 734-416-0206 ROFIN-SINAR REPORTS RESULTS FOR THE FIRST QUARTER OF FISCAL YEAR 2016 Quarterly earnings per share increased

How To Sell An Investment Bank

RESULTS PRESENTATION Half year ended 30 November 2013 IG H1 FY14 RESULTS PRESENTATION P1 DISCLAIMER This presentation, prepared by IG Group Holdings plc (the Company ), may contain forward-looking statements

RESULTS PRESENTATION Half year ended 30 November 2013 IG H1 FY14 RESULTS PRESENTATION P1 DISCLAIMER This presentation, prepared by IG Group Holdings plc (the Company ), may contain forward-looking statements

Topic 1 Wealth Management

Topic 1 Wealth Management 1. Background Moderator: Hansjörg Germann, As Head of Strategy Development at Zurich, Mr. Germann is responsible for all aspects of the strategic asset allocation for the group

Topic 1 Wealth Management 1. Background Moderator: Hansjörg Germann, As Head of Strategy Development at Zurich, Mr. Germann is responsible for all aspects of the strategic asset allocation for the group

Annual Press Conference 2015. 18 March 2015

Annual Press Conference 2015 18 March 2015 AGENDA Annual Press Conference 2015 Topic Speaker Time 1. Welcome Hubertus Spethmann 10.00 am 2. 2014 at a glance 2.1. Highlights Steven Holland 2.2. Financial

Annual Press Conference 2015 18 March 2015 AGENDA Annual Press Conference 2015 Topic Speaker Time 1. Welcome Hubertus Spethmann 10.00 am 2. 2014 at a glance 2.1. Highlights Steven Holland 2.2. Financial

The ReThink Group plc ( ReThink Group or the Group ) Unaudited Interim Results. Profits double as strategy delivers continued improved performance

Unaudited Interim Results. Profits double as strategy delivers continued improved performance") The ReThink Group plc ( ReThink Group or the Group ) Unaudited Interim Results Profits double as strategy delivers continued improved performance The Group (AIM: RTG), one of the UK s leading recruitment

The ReThink Group plc ( ReThink Group or the Group ) Unaudited Interim Results Profits double as strategy delivers continued improved performance The Group (AIM: RTG), one of the UK s leading recruitment

WE ARE. SHOWROOMPRIVE.com FY2015 RESULTS February, 16 th 2016

WE ARE SHOWROOMPRIVE.com FY2015 RESULTS February, 16 th 2016 I BUSINESS UPDATE AND 2015 RESULTS HIGHLIGHTS 2015: A YEAR FULL OF ACHIEVEMENTS A STRONG AND PROFITABLE GROWTH 443m net sales and 24m EBITDA

WE ARE SHOWROOMPRIVE.com FY2015 RESULTS February, 16 th 2016 I BUSINESS UPDATE AND 2015 RESULTS HIGHLIGHTS 2015: A YEAR FULL OF ACHIEVEMENTS A STRONG AND PROFITABLE GROWTH 443m net sales and 24m EBITDA

Willis makes firm offer to buy Gras Savoye at year-end 2015, to expand its fully integrated multinational offering to clients

News Release Contact: Media: Investors: Paul Platt (Willis) +44 20 3124 7659 Paul.Platt@willis.com Céline Meslier (Gras Savoye) +33 (0)1 41 3 55 02 celine.meslier@grassavoye.com Peter Poillon +1 212 915

News Release Contact: Media: Investors: Paul Platt (Willis) +44 20 3124 7659 Paul.Platt@willis.com Céline Meslier (Gras Savoye) +33 (0)1 41 3 55 02 celine.meslier@grassavoye.com Peter Poillon +1 212 915

Zurich Insurance Group. Our people 2014

Zurich Insurance Group Our people 2014 Zurich Insurance Group 1 Our people 2014 We aim to create sustainable value for all our stakeholders, in line with our values as set out in Zurich Basics, our code

Zurich Insurance Group Our people 2014 Zurich Insurance Group 1 Our people 2014 We aim to create sustainable value for all our stakeholders, in line with our values as set out in Zurich Basics, our code

No. 1 Choice for Europe s Leading Brands e-recruitment

Recognised as a leader in e-recruitment software by: No. 1 Choice for Europe s Leading Brands e-recruitment StepStone is the world s leading provider of Total Talent Management solutions. Every day StepStone

Recognised as a leader in e-recruitment software by: No. 1 Choice for Europe s Leading Brands e-recruitment StepStone is the world s leading provider of Total Talent Management solutions. Every day StepStone

Nokia Conference Call Third Quarter 2004 Financial Results. Jorma Ollila Chairman and CEO Rick Simonson Senior Vice President and CFO

Nokia Conference Call Third Quarter 2004 Financial Results Jorma Ollila Chairman and CEO Rick Simonson Senior Vice President and CFO Ulla James Vice President, Investor Relations October 14, 2004 15.00