Price Discrimination: Part 2. Sotiris Georganas

|

|

|

- Jeffrey Luke Jacobs

- 10 years ago

- Views:

Transcription

1 Price Discrimination: Part 2 Sotiris Georganas

2 1 More pricing techniques We will look at some further pricing techniques Non-linear pricing (2nd degree price discrimination) 2. Bundling

3 2 Non-linear pricing Definition 1 With a non-linear price a consumer s total expenditure on a good does not increase linearly (proportionately) with the number of unit purchased. Useful when 1. a monopolist faces unobserved heterogeneity in demand, and 2. the monopolist can prevent resale (no arbitrage) Think of the monopolist as designing offers (or bundles ) each consisting of a quantity and a total payment for each type of consumer.

Think of the monopolist as designing offers (or bundles )")

4 2.1 A Graphical Representation Consider a monopolist who sells to two types of consumers: highwillingness-to-pay consumers and low-willingness-to-pay consumers. Assume: one consumer of each type. the monopolist cannot tell the consumers apart he does not know who is the high- and the low-willingness-to-pay consumer respectively. the monopolist s marginal cost is zero (for simplicity): the monopolist maximizes his revenue. The demands for both consumers are displayed in Fig 1.

: the monopolist maximizes his revenue.")

5 If the monopolist could observe who is who, he could price discriminate perfectly: he would then sell q1 0 to person 1 (the low-demander) at price A, and q2 0 to person 2 (the high-demander) at price A + B + C. No consumer surplus for the consumers. However, this will not work if the monopolist cannot observe the demand type for each consumer. The high-willingness-to-pay consumer will have an incentive to pretend to be a low-willingness-to-pay consumer; by buying q 0 1 at price A, he can obtain a surplus equal to B.

6

7 What can the monopolist do then? Design price-quantity packages targeted at each type. Making sure that each consumer chooses the package intended for her. In other words: the consumer are induced to self-select: each consumer must prefer the bundle designed for her over that designed for the other type. The perfect price discrimination solution does not induce self-selection (it is not in high-willingness-to-pay consumer s interest to choose q 0 2 at price A + B + C).

8 A first attempt One possibility is to: Offer to sell q 0 1 at price A, and q0 2 at price A + C. The consumers then self-select (the low-willingness-to-pay consumer strictly prefers the low-quantity package; the high-willingnessto-pay consumer is indifferent between the two packages, gaining a surplus of B from each package). Total revenues are 2A + C (A from type 1 and A + C from type 2) But the monopolist can do even better than that!!!

.")

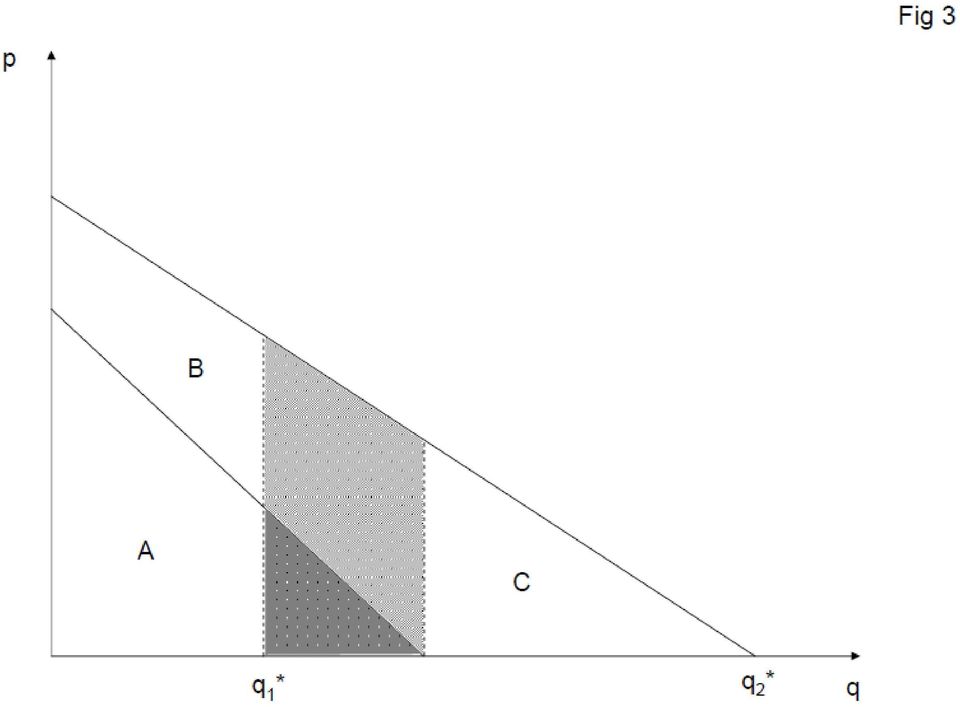

9 The solution The monopolist can reduce the quantity intended for the low-willingnessto-pay consumer from q1 0, at the same time reducing the price. This reduces the profit on the low-willingness-to-pay consumer by the small black triangle. Fig 2. However, it also makes the low-quantity package less attractive for the high-willingness-to-pay consumer. The monopolist can then charge more for the high quantity q 0 2 : the area C has grown. At the optimum, 2A + C is maximized. Fig. 3.

10

11

12 Properties of the solution The low-willingness-to-pay consumer obtains zero surplus The high-willingness-to-pay consumer obtains a positive surplus The quantity sold to the low-willingness-to-pay consumer is lower than the efficient level q 0 1. The monopolist offers quantity discounts: the average price paid for q 0 1 is higher than that for q0 2.

13 2.2 Formal Analysis A monopoly firm produces a single good. Constant average (and marginal) cost of production: c. There is a set consumers, each with the following utility: θv (q) T when buying a quantity q > 0 and paying T. V ( ) is a differentiable function, with V (q) > 0, V (q) < 0 and V (0) = 0.

14 Hence if I don t buy anything (q = 0) and don t pay anything (T = 0), my utility is zero. θ is a taste parameter the strenght of preferences for the good. A given consumer s taste parameter θ is either high or low: θ {θ 1, θ 2 }, with 0 < θ 1 < θ 2. Assumption 1 Asymmetric information: The consumer knows his own θ, but the firm does not know it. The firm only knows that a fraction λ of all consumers are of type θ 1, and the others (a fraction 1 λ) are of type θ 2.

15 The firm offers two price-quantity bundles to the consumers: (q 1, T 1 ) is directed to the type-θ 1 consumers. (q 2, T 2 ) is directed to the type-θ 2 consumers. We assume that the parameters are such that it is optimal for the firm to sell to both consumer types, rather than focusing on only the high valuation consumers.

16 Analysis The firm chooses q 1, q 2, T 1, and T 2 so as to maximize its profit, Π m = λ (T 1 cq 1 ) + (1 λ) (T 2 cq 2 ), subject to four constraints: Two individual rationality constraints and two incentive compatibility constraints. Type-θ 1 consumers must prefer their bundle to not trading at all: θ 1 V (q 1 ) T 1 0. (IR-1) Type-θ 2 consumers must prefer their bundle to not trading at all: θ 2 V (q 2 ) T 2 0. (IR-2)

T 1 0.")

17 Type-θ 1 consumers must prefer their bundle to the bundle directed to the type-θ 2 consumers: θ 1 V (q 1 ) T 1 θ 1 V (q 2 ) T 2. (IC-1) Type-θ 2 consumers must prefer their bundle to the bundle directed to the type-θ 1 consumers: θ 2 V (q 2 ) T 2 θ 2 V (q 1 ) T 1. (IC-2)

T 2 θ 2 V (q 1 ) T")

18 We can simplify the problem by making two observations: If IR-1 and IC-2 are satisfied, so is IR-2. We can therefore ignore IR-2. To see this, note that By IC-2: θ 2 V (q 2 ) T 2 θ 2 V (q 1 ) T 1 By θ 2 > θ 1 : θ 2 V (q 1 ) T 1 θ 1 V (q 1 ) T 1 By IR-1: θ 1 V (q 1 ) T 1 0 Hence, completing the chain: θ 2 V (q 2 ) T 2 0, i.e. IR-2 is satisfied.

T 1 θ 1 V (q 1 ) T 1 By IR-1: θ 1 V (q 1 ) T 1 0 Hence, completing the chain: θ")

19 At the optimum, IC-1 is not binding. We can t ignore IC-1 just like that: we must prove that it is not binding. One can do this as follows: 1. Ignore IC-1 and solve for the solution. 2. Check whether IC-1 is satisfied at this solution. 3. If it is satisfied, we can conclude that the solution we found must solve also the problem with the constraint IC-1.

20 The simplified problem: choose q 1, q 2, T 1, and T 2 so as to maximize subject to Π m = λ (T 1 cq 1 ) + (1 λ) (T 2 cq 2 ), (1) θ 1 V (q 1 ) T 1 0 (IR-1) and θ 2 V (q 2 ) T 2 θ 2 V (q 1 ) T 1. (IC-2)

and θ 2 V (q 2 ) T 2 θ 2 V (q 1 ) T 1.")

21 Note that since Π m is increasing in T 1 and T 2, both constraints must bind at the optimum. We thus have and T 1 = θ 1 V (q 1 ) (2) T 2 = θ 2 V (q 2 ) θ 2 V (q 1 ) + T 1 = θ 2 V (q 2 ) θ 2 V (q 1 ) + θ 1 V (q 1 ) = θ 2 V (q 2 ) (θ 2 θ 1 ) V (q 1 ). (3) We can now simplify the problem further, transforming it into an unconstrained problem by substituting in the objective function.

22 By plugging (2) and (3) into (1), we get Π m = λ [θ 1 V (q 1 ) cq 1 ] + (1 λ) [θ 2 V (q 2 ) (θ 2 θ 1 ) V (q 1 ) cq 2 ]. The problem now amounts to maximizing this expression for Π m w.r.t. q 1 and q 2 (without having to take any constraints into account). The FOC w.r.t. q 1 : Πm q 1 = λ [ θ 1 V (q 1 ) c ] (1 λ) (θ 2 θ 1 ) V (q 1 ) = 0 or θ 1 V (q 1 ) [ 1 (1 λ) (θ 2 θ 1 ) λ θ 1 ] = c (4)

23 where the term in brackets is positive but less than one! The FOC w.r.t. q 2 : Π m = (1 λ) [ θ 2 V (q 2 ) c ] = 0 q 2 or θ 2 V (q2 ) = c (5)

24 Conclusions 1. The high-demand consumers buy the socially optimal quantity: marginal utility/willingness to pay equals marginal cost. [By (5).] Intuition: Suppose e.g. that the monopolist sold a smaller quantity. Then by increasing the quantity q 2 up to the points where type 2 s marginal willingness to pay is equal to c and charging the type s willingness to pay for the additional quantity, lead to higher profits but leaves the consumer s utility unaffected. 2. The low-demand consumers buy less than the socially optimal quantity: marginal utility > marginal cost. [By (4).] Intuition:

25 The monopolist wants to extract the high-demand consumer s large surplus. An obstacle to this: If the high type gets too little surplus, he can choose the low type bundle instead. To prevent this, the monopolist makes the low-type s bundle less attractive by offering those consumers less. This works because high-demand consumers suffer more from a reduction in consumption than do low-demand consumers. (4) and (5) also imply that q 2 > q Low-demand consumers derive no surplus, while high-demand consumers derive a positive surplus.

26 4. The relevant personal arbitrage constraint is to prevent high-demand consumers from choosing the low-demand consumers bundle.

27 3 Commodity bundling A pricing strategy available for a monopolist who is selling more than one product. Definition 2 A monopolist firm is bundling if it offers to sell packages of related goods together. Examples include: (computer software, vacations, films etc.) So why bundle? Less expensive to sell together (cheaper production \ distribution) Complementarities in consumption.

28 3.1 Bundling to reduce variability in willingness to pay However, we will focus on a third possibility: Claim 1 Bundling may be an optimal pricing strategy when there is a high variability in the willingness to pay for the individual goods, but low variability in the willingness to pay for a package of the goods.

29 An example (Varian, Intermediate Microeconomics) A monopolist sell two software products: word processor and spreadsheet. Marginal cost is zero (for simplicity): revenues are maximized. Each consumer buys at most one unit of each product. There are two types of consumers: A and B whose willingness to pay are as follows:

30 Willingness to pay for products Type of consumer Word processor Spreadsheet Type A consumer Type B consumer Assumption 2 No complementaries in consumption a consumer s willingness to pay for package equals the sum of his willingness to pay for the individual components.

31 Pricing options 1. Sell each good separately: revenues maximized when each product is sold at $100 (the smallest willingness to pay) total revenues are then $ Sell a bundle: each consumer is willing to pay $220 for the bundle: set the price for the bundle at $220 Total revenues are $440.

32 3.2 General rule If the monopolist cannot price discriminate, he has to set the price for each individual product equal to the lowest willingness-to-pay. Thus if there is high variability in the willingness to pay, the price for each individual product will be low. If the variability in the willingness to pay for a bundle is low, then the monopolist can charge a fairly high price for the bundle. In the above case, there was no variability at all in the willingness to pay for the bundle. In this case, the monopolist can actually replicate perfect price discrimination by using the bundling technique.

33 4 What to remember from this lecture What is a non-linear pricing scheme. When might a monopolist use a non-linear pricing scheme. Properties of an optimal non-linear pricing scheme (that the lowquantity is held back to make it unattractive to the high-willingnessto-pay consumers, that the low-willingness-to-pay consumers obtain no consumer surplus, but the high-willingness-to-pay consumers do, that the solution involves quantity discounts). That a multi-product monopolist may be able to increase its profits by using a bundling strategy when the variability in the willingness to pay for the individual products is high but the variability in the willingness to pay for a bundle is low.

3 Price Discrimination

Joe Chen 26 3 Price Discrimination There is no universally accepted definition for price discrimination (PD). In most cases, you may consider PD as: producers sell two units of the same physical good at

Joe Chen 26 3 Price Discrimination There is no universally accepted definition for price discrimination (PD). In most cases, you may consider PD as: producers sell two units of the same physical good at

Lecture 6: Price discrimination II (Nonlinear Pricing)

") Lecture 6: Price discrimination II (Nonlinear Pricing) EC 105. Industrial Organization. Fall 2011 Matt Shum HSS, California Institute of Technology November 14, 2012 EC 105. Industrial Organization. Fall

Lecture 6: Price discrimination II (Nonlinear Pricing) EC 105. Industrial Organization. Fall 2011 Matt Shum HSS, California Institute of Technology November 14, 2012 EC 105. Industrial Organization. Fall

Second degree price discrimination

Bergals School of Economics Fall 1997/8 Tel Aviv University Second degree price discrimination Yossi Spiegel 1. Introduction Second degree price discrimination refers to cases where a firm does not have

Bergals School of Economics Fall 1997/8 Tel Aviv University Second degree price discrimination Yossi Spiegel 1. Introduction Second degree price discrimination refers to cases where a firm does not have

ADVANCED MICROECONOMICS (TUTORIAL)

") ELMAR G. WOLFSTETTER, MAY 12, 214 ADVANCED MICROECONOMICS (TUTORIAL) EXERCISE SHEET 4 - ANSWERS AND HINTS We appreciate any comments and suggestions that may help to improve these solution sets. Exercise

ELMAR G. WOLFSTETTER, MAY 12, 214 ADVANCED MICROECONOMICS (TUTORIAL) EXERCISE SHEET 4 - ANSWERS AND HINTS We appreciate any comments and suggestions that may help to improve these solution sets. Exercise

Problem Set 9 Solutions

Problem Set 9 s 1. A monopoly insurance company provides accident insurance to two types of customers: low risk customers, for whom the probability of an accident is 0.25, and high risk customers, for

Problem Set 9 s 1. A monopoly insurance company provides accident insurance to two types of customers: low risk customers, for whom the probability of an accident is 0.25, and high risk customers, for

SECOND-DEGREE PRICE DISCRIMINATION

SECOND-DEGREE PRICE DISCRIMINATION FIRST Degree: The firm knows that it faces different individuals with different demand functions and furthermore the firm can tell who is who. In this case the firm extracts

SECOND-DEGREE PRICE DISCRIMINATION FIRST Degree: The firm knows that it faces different individuals with different demand functions and furthermore the firm can tell who is who. In this case the firm extracts

2.2 Price Discrimination

2.2 Price Discrimination Matilde Machado Download the slides from: http://www.eco.uc3m.es/~mmachado/teaching/oi-i-mei/index.html 1 2.2 Price Discrimination Everyday situations where price discrimination

2.2 Price Discrimination Matilde Machado Download the slides from: http://www.eco.uc3m.es/~mmachado/teaching/oi-i-mei/index.html 1 2.2 Price Discrimination Everyday situations where price discrimination

Chapter 11 Pricing Strategies for Firms with Market Power

Managerial Economics & Business Strategy Chapter 11 Pricing Strategies for Firms with Market Power McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. Basic

Managerial Economics & Business Strategy Chapter 11 Pricing Strategies for Firms with Market Power McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. Basic

1.4 Hidden Information and Price Discrimination 1

1.4 Hidden Information and Price Discrimination 1 To be included in: Elmar Wolfstetter. Topics in Microeconomics: Industrial Organization, Auctions, and Incentives. Cambridge University Press, new edition,

1.4 Hidden Information and Price Discrimination 1 To be included in: Elmar Wolfstetter. Topics in Microeconomics: Industrial Organization, Auctions, and Incentives. Cambridge University Press, new edition,

PRICE DISCRIMINATION Industrial Organization B

PRICE DISCRIMINATION Industrial Organization B THIBAUD VERGÉ Autorité de la Concurrence and CREST-LEI Master of Science in Economics - HEC Lausanne (2009-2010) THIBAUD VERGÉ (AdlC, CREST-LEI) Price Discrimination

PRICE DISCRIMINATION Industrial Organization B THIBAUD VERGÉ Autorité de la Concurrence and CREST-LEI Master of Science in Economics - HEC Lausanne (2009-2010) THIBAUD VERGÉ (AdlC, CREST-LEI) Price Discrimination

First degree price discrimination ECON 171

First degree price discrimination Introduction Annual subscriptions generally cost less in total than one-off purchases Buying in bulk usually offers a price discount these are price discrimination reflecting

First degree price discrimination Introduction Annual subscriptions generally cost less in total than one-off purchases Buying in bulk usually offers a price discount these are price discrimination reflecting

Part IV. Pricing strategies and market segmentation

Part IV. Pricing strategies and market segmentation Chapter 9. Menu pricing Slides Industrial Organization: Markets and Strategies Paul Belleflamme and Martin Peitz Cambridge University Press 2010 Chapter

Part IV. Pricing strategies and market segmentation Chapter 9. Menu pricing Slides Industrial Organization: Markets and Strategies Paul Belleflamme and Martin Peitz Cambridge University Press 2010 Chapter

2.4 Multiproduct Monopoly. 2.4 Multiproduct Monopoly

.4 Multiproduct Monopoly Matilde Machado Slides available from: http://www.eco.uc3m.es/oi-i-mei/.4 Multiproduct Monopoly The firm is a monopoly in all markets where it operates i=,.n goods sold by the

.4 Multiproduct Monopoly Matilde Machado Slides available from: http://www.eco.uc3m.es/oi-i-mei/.4 Multiproduct Monopoly The firm is a monopoly in all markets where it operates i=,.n goods sold by the

2. Price Discrimination

The theory of Industrial Organization Ph. D. Program in Law and Economics Session 5: Price Discrimination J. L. Moraga 2. Price Discrimination Practise of selling the same product to distinct consumers

The theory of Industrial Organization Ph. D. Program in Law and Economics Session 5: Price Discrimination J. L. Moraga 2. Price Discrimination Practise of selling the same product to distinct consumers

KEELE UNIVERSITY MID-TERM TEST, 2007 BA BUSINESS ECONOMICS BA FINANCE AND ECONOMICS BA MANAGEMENT SCIENCE ECO 20015 MANAGERIAL ECONOMICS II

KEELE UNIVERSITY MID-TERM TEST, 2007 Thursday 22nd NOVEMBER, 12.05-12.55 BA BUSINESS ECONOMICS BA FINANCE AND ECONOMICS BA MANAGEMENT SCIENCE ECO 20015 MANAGERIAL ECONOMICS II Candidates should attempt

KEELE UNIVERSITY MID-TERM TEST, 2007 Thursday 22nd NOVEMBER, 12.05-12.55 BA BUSINESS ECONOMICS BA FINANCE AND ECONOMICS BA MANAGEMENT SCIENCE ECO 20015 MANAGERIAL ECONOMICS II Candidates should attempt

A Detailed Price Discrimination Example

A Detailed Price Discrimination Example Suppose that there are two different types of customers for a monopolist s product. Customers of type 1 have demand curves as follows. These demand curves include

A Detailed Price Discrimination Example Suppose that there are two different types of customers for a monopolist s product. Customers of type 1 have demand curves as follows. These demand curves include

Market Power and Efficiency in Card Payment Systems: A Comment on Rochet and Tirole

Market Power and Efficiency in Card Payment Systems: A Comment on Rochet and Tirole Luís M. B. Cabral New York University and CEPR November 2005 1 Introduction Beginning with their seminal 2002 paper,

Market Power and Efficiency in Card Payment Systems: A Comment on Rochet and Tirole Luís M. B. Cabral New York University and CEPR November 2005 1 Introduction Beginning with their seminal 2002 paper,

p, we suppress the wealth arguments in the aggregate demand function. We can thus state the monopolist s problem as follows: max pq (p) c (q (p)).

c (q (p)).") Chapter 9 Monopoly As you will recall from intermediate micro, monopoly is the situation where there is a single seller of a good. Because of this, it has the power to set both the price and quantity of

Chapter 9 Monopoly As you will recall from intermediate micro, monopoly is the situation where there is a single seller of a good. Because of this, it has the power to set both the price and quantity of

MICROECONOMICS II PROBLEM SET III: MONOPOLY

MICROECONOMICS II PROBLEM SET III: MONOPOLY EXERCISE 1 Firstly, we analyze the equilibrium under the monopoly. The monopolist chooses the quantity that maximizes its profits; in particular, chooses the

MICROECONOMICS II PROBLEM SET III: MONOPOLY EXERCISE 1 Firstly, we analyze the equilibrium under the monopoly. The monopolist chooses the quantity that maximizes its profits; in particular, chooses the

Economics 431 Fall 2003 1st midterm Answer Key

Economics 431 Fall 003 1st midterm Answer Key 1) (7 points) Consider an industry that consists of a large number of identical firms. In the long run competitive equilibrium, a firm s marginal cost must

Economics 431 Fall 003 1st midterm Answer Key 1) (7 points) Consider an industry that consists of a large number of identical firms. In the long run competitive equilibrium, a firm s marginal cost must

Part IV. Pricing strategies and market segmentation. Chapter 8. Group pricing and personalized pricing

Part IV. Pricing strategies and market segmentation Chapter 8. Group pricing and personalized pricing Slides Industrial Organization: Markets and Strategies Paul Belleflamme and Martin Peitz Cambridge

Part IV. Pricing strategies and market segmentation Chapter 8. Group pricing and personalized pricing Slides Industrial Organization: Markets and Strategies Paul Belleflamme and Martin Peitz Cambridge

Sustainable Energy Systems

Theory of Regulation PhD, DFA M. Victor M. Martins Semester 2 2008/2009 2. 1 Natural monopoly regulation 2. 1 Natural monopoly regulation: efficient pricing, linear, non linear pricing and Ramsey pricing.

Theory of Regulation PhD, DFA M. Victor M. Martins Semester 2 2008/2009 2. 1 Natural monopoly regulation 2. 1 Natural monopoly regulation: efficient pricing, linear, non linear pricing and Ramsey pricing.

Solution to Homework Set 7

Solution to Homework Set 7 Managerial Economics Fall 011 1. An industry consists of five firms with sales of $00 000, $500 000, $400 000, $300 000, and $100 000. a) points) Calculate the Herfindahl-Hirschman

Solution to Homework Set 7 Managerial Economics Fall 011 1. An industry consists of five firms with sales of $00 000, $500 000, $400 000, $300 000, and $100 000. a) points) Calculate the Herfindahl-Hirschman

Lecture 2: Consumer Theory

Lecture 2: Consumer Theory Preferences and Utility Utility Maximization (the primal problem) Expenditure Minimization (the dual) First we explore how consumers preferences give rise to a utility fct which

Lecture 2: Consumer Theory Preferences and Utility Utility Maximization (the primal problem) Expenditure Minimization (the dual) First we explore how consumers preferences give rise to a utility fct which

All these models were characterized by constant returns to scale technologies and perfectly competitive markets.

Economies of scale and international trade In the models discussed so far, differences in prices across countries (the source of gains from trade) were attributed to differences in resources/technology.

Economies of scale and international trade In the models discussed so far, differences in prices across countries (the source of gains from trade) were attributed to differences in resources/technology.

Figure 1, A Monopolistically Competitive Firm

The Digital Economist Lecture 9 Pricing Power and Price Discrimination Many firms have the ability to charge prices for their products consistent with their best interests even thought they may not be

The Digital Economist Lecture 9 Pricing Power and Price Discrimination Many firms have the ability to charge prices for their products consistent with their best interests even thought they may not be

Managerial Economics Prof. Trupti Mishra S.J.M. School of Management Indian Institute of Technology, Bombay. Lecture - 13 Consumer Behaviour (Contd )

") (Refer Slide Time: 00:28) Managerial Economics Prof. Trupti Mishra S.J.M. School of Management Indian Institute of Technology, Bombay Lecture - 13 Consumer Behaviour (Contd ) We will continue our discussion

(Refer Slide Time: 00:28) Managerial Economics Prof. Trupti Mishra S.J.M. School of Management Indian Institute of Technology, Bombay Lecture - 13 Consumer Behaviour (Contd ) We will continue our discussion

1. Supply and demand are the most important concepts in economics.

Page 1 1. Supply and demand are the most important concepts in economics. 2. Markets and Competition a. Market is a group of buyers and sellers of a particular good or service. P. 66. b. These individuals

Page 1 1. Supply and demand are the most important concepts in economics. 2. Markets and Competition a. Market is a group of buyers and sellers of a particular good or service. P. 66. b. These individuals

1. Briefly explain what an indifference curve is and how it can be graphically derived.

Chapter 2: Consumer Choice Short Answer Questions 1. Briefly explain what an indifference curve is and how it can be graphically derived. Answer: An indifference curve shows the set of consumption bundles

Chapter 2: Consumer Choice Short Answer Questions 1. Briefly explain what an indifference curve is and how it can be graphically derived. Answer: An indifference curve shows the set of consumption bundles

-1- Worked Solutions 5. Lectures 9 and 10. Question Lecture 1. L9 2. L9 3. L9 4. L9 5. L9 6. L9 7. L9 8. L9 9. L9 10. L9 11. L9 12.

-1- Worked Solutions 5 Lectures 9 and 10. Question Lecture 1. L9 2. L9 3. L9 4. L9 5. L9 6. L9 7. L9 8. L9 9. L9 10. L9 11. L9 12. L10 Unit 5 solutions Exercise 1 There may be practical difficulties in

-1- Worked Solutions 5 Lectures 9 and 10. Question Lecture 1. L9 2. L9 3. L9 4. L9 5. L9 6. L9 7. L9 8. L9 9. L9 10. L9 11. L9 12. L10 Unit 5 solutions Exercise 1 There may be practical difficulties in

Lecture Notes. 1 What is Asymmetric Information and why it matters for Economics?

Lecture Notes The most important development in economics in the last forty years has been the study of incentives to achieve potential mutual gain when the parties have different degrees of knowledge.

Lecture Notes The most important development in economics in the last forty years has been the study of incentives to achieve potential mutual gain when the parties have different degrees of knowledge.

A. a change in demand. B. a change in quantity demanded. C. a change in quantity supplied. D. unit elasticity. E. a change in average variable cost.

1. The supply of gasoline changes, causing the price of gasoline to change. The resulting movement from one point to another along the demand curve for gasoline is called A. a change in demand. B. a change

1. The supply of gasoline changes, causing the price of gasoline to change. The resulting movement from one point to another along the demand curve for gasoline is called A. a change in demand. B. a change

How To Price Bundle On Cable Television

K. Bundling Brown and in Cable P. J. Alexander Television Bundling in Cable Television: A Pedagogical Note With a Policy Option Keith Brown and Peter J. Alexander Federal Communications Commission, USA

K. Bundling Brown and in Cable P. J. Alexander Television Bundling in Cable Television: A Pedagogical Note With a Policy Option Keith Brown and Peter J. Alexander Federal Communications Commission, USA

1 Monopoly Why Monopolies Arise? Monopoly is a rm that is the sole seller of a product without close substitutes. The fundamental cause of monopoly is barriers to entry: A monopoly remains the only seller

1 Monopoly Why Monopolies Arise? Monopoly is a rm that is the sole seller of a product without close substitutes. The fundamental cause of monopoly is barriers to entry: A monopoly remains the only seller

2. Information Economics

2. Information Economics In General Equilibrium Theory all agents had full information regarding any variable of interest (prices, commodities, state of nature, cost function, preferences, etc.) In many

2. Information Economics In General Equilibrium Theory all agents had full information regarding any variable of interest (prices, commodities, state of nature, cost function, preferences, etc.) In many

ANOTHER PERVERSE EFFECT OF MONOPOLY POWER

ANOTHER PERVERSE EFFECT OF MONOPOLY POWER Jean J. Gabszewicz and Xavier Y. Wauthy November 2000 Abstract We show that the simple fact that a monopolist sells a good in units which are indivisible may well

ANOTHER PERVERSE EFFECT OF MONOPOLY POWER Jean J. Gabszewicz and Xavier Y. Wauthy November 2000 Abstract We show that the simple fact that a monopolist sells a good in units which are indivisible may well

Marginal cost. Average cost. Marginal revenue 10 20 40

Economics 101 Fall 2011 Homework #6 Due: 12/13/2010 in lecture Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework

Economics 101 Fall 2011 Homework #6 Due: 12/13/2010 in lecture Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework

Chapter 15: Monopoly WHY MONOPOLIES ARISE HOW MONOPOLIES MAKE PRODUCTION AND PRICING DECISIONS

Chapter 15: While a competitive firm is a taker, a monopoly firm is a maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

Chapter 15: While a competitive firm is a taker, a monopoly firm is a maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

Examples on Monopoly and Third Degree Price Discrimination

1 Examples on Monopoly and Third Degree Price Discrimination This hand out contains two different parts. In the first, there are examples concerning the profit maximizing strategy for a firm with market

1 Examples on Monopoly and Third Degree Price Discrimination This hand out contains two different parts. In the first, there are examples concerning the profit maximizing strategy for a firm with market

Lecture 9: Price Discrimination

Lecture 9: Price Discrimination EC 105. Industrial Organization. Fall 2011 Matt Shum HSS, California Institute of Technology September 9, 2011 September 9, 2011 1 / 23 Outline Outline 1 Perfect price discrimination

Lecture 9: Price Discrimination EC 105. Industrial Organization. Fall 2011 Matt Shum HSS, California Institute of Technology September 9, 2011 September 9, 2011 1 / 23 Outline Outline 1 Perfect price discrimination

Business Ethics Concepts & Cases

Business Ethics Concepts & Cases Manuel G. Velasquez Chapter Four Ethics in the Marketplace Definition of Market A forum in which people come together to exchange ownership of goods; a place where goods

Business Ethics Concepts & Cases Manuel G. Velasquez Chapter Four Ethics in the Marketplace Definition of Market A forum in which people come together to exchange ownership of goods; a place where goods

Answers to Chapter 6 Exercises

Answers to Chapter 6 Exercises Review and practice exercises 6.1. Perfect price discrimination. Consider a monopolist with demand D = 10 p and marginal cost MC = 40. Determine profit, consumer surplus,

Answers to Chapter 6 Exercises Review and practice exercises 6.1. Perfect price discrimination. Consider a monopolist with demand D = 10 p and marginal cost MC = 40. Determine profit, consumer surplus,

Advertising. Sotiris Georganas. February 2013. Sotiris Georganas () Advertising February 2013 1 / 32

Advertising February 2013 1 / 32") Advertising Sotiris Georganas February 2013 Sotiris Georganas () Advertising February 2013 1 / 32 Outline 1 Introduction 2 Main questions about advertising 3 How does advertising work? 4 Persuasive advertising

Advertising Sotiris Georganas February 2013 Sotiris Georganas () Advertising February 2013 1 / 32 Outline 1 Introduction 2 Main questions about advertising 3 How does advertising work? 4 Persuasive advertising

Problem Set #5-Key. Economics 305-Intermediate Microeconomic Theory

Problem Set #5-Key Sonoma State University Economics 305-Intermediate Microeconomic Theory Dr Cuellar (1) Suppose that you are paying your for your own education and that your college tuition is $200 per

Problem Set #5-Key Sonoma State University Economics 305-Intermediate Microeconomic Theory Dr Cuellar (1) Suppose that you are paying your for your own education and that your college tuition is $200 per

Why do merchants accept payment cards?

Why do merchants accept payment cards? Julian Wright National University of Singapore Abstract This note explains why merchants accept expensive payment cards when merchants are Cournot competitors. The

Why do merchants accept payment cards? Julian Wright National University of Singapore Abstract This note explains why merchants accept expensive payment cards when merchants are Cournot competitors. The

Price Dispersion. Ed Hopkins Economics University of Edinburgh Edinburgh EH8 9JY, UK. November, 2006. Abstract

Price Dispersion Ed Hopkins Economics University of Edinburgh Edinburgh EH8 9JY, UK November, 2006 Abstract A brief survey of the economics of price dispersion, written for the New Palgrave Dictionary

Price Dispersion Ed Hopkins Economics University of Edinburgh Edinburgh EH8 9JY, UK November, 2006 Abstract A brief survey of the economics of price dispersion, written for the New Palgrave Dictionary

Name. Final Exam, Economics 210A, December 2011 Here are some remarks to help you with answering the questions.

Name Final Exam, Economics 210A, December 2011 Here are some remarks to help you with answering the questions. Question 1. A firm has a production function F (x 1, x 2 ) = ( x 1 + x 2 ) 2. It is a price

Name Final Exam, Economics 210A, December 2011 Here are some remarks to help you with answering the questions. Question 1. A firm has a production function F (x 1, x 2 ) = ( x 1 + x 2 ) 2. It is a price

Pricing to Mass Markets. Simple Monopoly Pricing, Price Discrimination and the Losses from Monopoly

Pricing to Mass Markets Simple Monopoly Pricing, Price Discrimination and the Losses from Monopoly Many Buyers Costly to set individual prices to each consumer to extract their individual willingness-to-pay.

Pricing to Mass Markets Simple Monopoly Pricing, Price Discrimination and the Losses from Monopoly Many Buyers Costly to set individual prices to each consumer to extract their individual willingness-to-pay.

INTRODUCTORY MICROECONOMICS

INTRODUCTORY MICROECONOMICS UNIT-I PRODUCTION POSSIBILITIES CURVE The production possibilities (PP) curve is a graphical medium of highlighting the central problem of 'what to produce'. To decide what

INTRODUCTORY MICROECONOMICS UNIT-I PRODUCTION POSSIBILITIES CURVE The production possibilities (PP) curve is a graphical medium of highlighting the central problem of 'what to produce'. To decide what

Product Differentiation In homogeneous goods markets, price competition leads to perfectly competitive outcome, even with two firms Price competition

Product Differentiation In homogeneous goods markets, price competition leads to perfectly competitive outcome, even with two firms Price competition with differentiated products Models where differentiation

Product Differentiation In homogeneous goods markets, price competition leads to perfectly competitive outcome, even with two firms Price competition with differentiated products Models where differentiation

SUPPLY AND DEMAND : HOW MARKETS WORK

SUPPLY AND DEMAND : HOW MARKETS WORK Chapter 4 : The Market Forces of and and demand are the two words that economists use most often. and demand are the forces that make market economies work. Modern

SUPPLY AND DEMAND : HOW MARKETS WORK Chapter 4 : The Market Forces of and and demand are the two words that economists use most often. and demand are the forces that make market economies work. Modern

Economics 2020a / HBS 4010 / HKS API-111 FALL 2010 Solutions to Practice Problems for Lectures 1 to 4

Economics 00a / HBS 4010 / HKS API-111 FALL 010 Solutions to Practice Problems for Lectures 1 to 4 1.1. Quantity Discounts and the Budget Constraint (a) The only distinction between the budget line with

Economics 00a / HBS 4010 / HKS API-111 FALL 010 Solutions to Practice Problems for Lectures 1 to 4 1.1. Quantity Discounts and the Budget Constraint (a) The only distinction between the budget line with

Economics 335, Spring 1999 Problem Set #7

Economics 335, Spring 1999 Problem Set #7 Name: 1. A monopolist has two sets of customers, group 1 and group 2. The inverse demand for group 1 may be described by P 1 = 200? Q 1, where P 1 is the price

Economics 335, Spring 1999 Problem Set #7 Name: 1. A monopolist has two sets of customers, group 1 and group 2. The inverse demand for group 1 may be described by P 1 = 200? Q 1, where P 1 is the price

Price Discrimination and Two Part Tariff

Sloan School of Management 15.010/15.011 Massachusetts Institute of Technology RECITATION NOTES #6 Price Discrimination and Two Part Tariff Friday - October 29, 2004 OUTLINE OF TODAY S RECITATION 1. Conditions

Sloan School of Management 15.010/15.011 Massachusetts Institute of Technology RECITATION NOTES #6 Price Discrimination and Two Part Tariff Friday - October 29, 2004 OUTLINE OF TODAY S RECITATION 1. Conditions

Chapter 21: Consumer Behavior and Utility Maximization

Chapter : Consumer Behavior and Utility Maximization ANSWERS TO END-OF-CHAPTER QUESTIONS - Explain the law of demand through the income and substitution effects, using a price increase as a point of departure

Chapter : Consumer Behavior and Utility Maximization ANSWERS TO END-OF-CHAPTER QUESTIONS - Explain the law of demand through the income and substitution effects, using a price increase as a point of departure

Competition between Apple and Samsung in the smartphone market introduction into some key concepts in managerial economics

Competition between Apple and Samsung in the smartphone market introduction into some key concepts in managerial economics Dr. Markus Thomas Münter Collège des Ingénieurs Stuttgart, June, 03 SNORKELING

Competition between Apple and Samsung in the smartphone market introduction into some key concepts in managerial economics Dr. Markus Thomas Münter Collège des Ingénieurs Stuttgart, June, 03 SNORKELING

Economics of Insurance

Economics of Insurance In this last lecture, we cover most topics of Economics of Information within a single application. Through this, you will see how the differential informational assumptions allow

Economics of Insurance In this last lecture, we cover most topics of Economics of Information within a single application. Through this, you will see how the differential informational assumptions allow

Do not open this exam until told to do so.

Do not open this exam until told to do so. Department of Economics College of Social and Applied Human Sciences K. Annen, Winter 004 Final (Version ): Intermediate Microeconomics (ECON30) Solutions Final

Do not open this exam until told to do so. Department of Economics College of Social and Applied Human Sciences K. Annen, Winter 004 Final (Version ): Intermediate Microeconomics (ECON30) Solutions Final

Chapter 21: The Discounted Utility Model

Chapter 21: The Discounted Utility Model 21.1: Introduction This is an important chapter in that it introduces, and explores the implications of, an empirically relevant utility function representing intertemporal

Chapter 21: The Discounted Utility Model 21.1: Introduction This is an important chapter in that it introduces, and explores the implications of, an empirically relevant utility function representing intertemporal

Oligopoly and Strategic Pricing

R.E.Marks 1998 Oligopoly 1 R.E.Marks 1998 Oligopoly Oligopoly and Strategic Pricing In this section we consider how firms compete when there are few sellers an oligopolistic market (from the Greek). Small

R.E.Marks 1998 Oligopoly 1 R.E.Marks 1998 Oligopoly Oligopoly and Strategic Pricing In this section we consider how firms compete when there are few sellers an oligopolistic market (from the Greek). Small

Pricing and Persuasive Advertising in a Differentiated Market

Pricing and Persuasive Advertising in a Differentiated Market Baojun Jiang Olin Business School, Washington University in St. Louis, St. Louis, MO 63130, [email protected] Kannan Srinivasan Tepper

Pricing and Persuasive Advertising in a Differentiated Market Baojun Jiang Olin Business School, Washington University in St. Louis, St. Louis, MO 63130, [email protected] Kannan Srinivasan Tepper

Pricing in a Competitive Market with a Common Network Resource

Pricing in a Competitive Market with a Common Network Resource Daniel McFadden Department of Economics, University of California, Berkeley April 8, 2002 I. This note is concerned with the economics of

Pricing in a Competitive Market with a Common Network Resource Daniel McFadden Department of Economics, University of California, Berkeley April 8, 2002 I. This note is concerned with the economics of

Using Revenue Management in Multiproduct Production/Inventory Systems: A Survey Study

Using Revenue Management in Multiproduct Production/Inventory Systems: A Survey Study Master s Thesis Department of Production economics Linköping Institute of Technology Hadi Esmaeili Ahangarkolaei Mohammad

Using Revenue Management in Multiproduct Production/Inventory Systems: A Survey Study Master s Thesis Department of Production economics Linköping Institute of Technology Hadi Esmaeili Ahangarkolaei Mohammad

Why is Insurance Good? An Example Jon Bakija, Williams College (Revised October 2013)

") Why is Insurance Good? An Example Jon Bakija, Williams College (Revised October 2013) Introduction The United States government is, to a rough approximation, an insurance company with an army. 1 That is

Why is Insurance Good? An Example Jon Bakija, Williams College (Revised October 2013) Introduction The United States government is, to a rough approximation, an insurance company with an army. 1 That is

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

Common in European countries government runs telephone, water, electric companies.

Public ownership Common in European countries government runs telephone, water, electric companies. US: Postal service. Because delivery of mail seems to be natural monopoly. Private ownership incentive

Public ownership Common in European countries government runs telephone, water, electric companies. US: Postal service. Because delivery of mail seems to be natural monopoly. Private ownership incentive

Answers to Text Questions and Problems. Chapter 22. Answers to Review Questions

Answers to Text Questions and Problems Chapter 22 Answers to Review Questions 3. In general, producers of durable goods are affected most by recessions while producers of nondurables (like food) and services

Answers to Text Questions and Problems Chapter 22 Answers to Review Questions 3. In general, producers of durable goods are affected most by recessions while producers of nondurables (like food) and services

Module 7: Debt Contracts & Credit Rationing

Module 7: Debt Contracts & Credit ationing Information Economics (Ec 515) George Georgiadis Two Applications of the principal-agent model to credit markets An entrepreneur (E - borrower) has a project.

Module 7: Debt Contracts & Credit ationing Information Economics (Ec 515) George Georgiadis Two Applications of the principal-agent model to credit markets An entrepreneur (E - borrower) has a project.

Frequent flyer programs and dynamic contracting with limited commitment

Frequent flyer programs and dynamic contracting with limited commitment Emil Temnyalov March 14, 2015 Abstract I present a novel contract theoretic explanation of the profitability and management of loyalty

Frequent flyer programs and dynamic contracting with limited commitment Emil Temnyalov March 14, 2015 Abstract I present a novel contract theoretic explanation of the profitability and management of loyalty

Monopolistic Competition

Monopolistic Chapter 17 Copyright 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department, Harcourt College

Monopolistic Chapter 17 Copyright 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department, Harcourt College

Monopoly. E. Glen Weyl. Lecture 8 Price Theory and Market Design Fall 2013. University of Chicago

and Pricing Basics E. Glen Weyl University of Chicago Lecture 8 Price Theory and Market Design Fall 2013 Introduction and Pricing Basics Definition and sources of monopoly power Basic monopolistic incentive

and Pricing Basics E. Glen Weyl University of Chicago Lecture 8 Price Theory and Market Design Fall 2013 Introduction and Pricing Basics Definition and sources of monopoly power Basic monopolistic incentive

Moral Hazard. Itay Goldstein. Wharton School, University of Pennsylvania

Moral Hazard Itay Goldstein Wharton School, University of Pennsylvania 1 Principal-Agent Problem Basic problem in corporate finance: separation of ownership and control: o The owners of the firm are typically

Moral Hazard Itay Goldstein Wharton School, University of Pennsylvania 1 Principal-Agent Problem Basic problem in corporate finance: separation of ownership and control: o The owners of the firm are typically

ECON 312: Oligopolisitic Competition 1. Industrial Organization Oligopolistic Competition

ECON 312: Oligopolisitic Competition 1 Industrial Organization Oligopolistic Competition Both the monopoly and the perfectly competitive market structure has in common is that neither has to concern itself

ECON 312: Oligopolisitic Competition 1 Industrial Organization Oligopolistic Competition Both the monopoly and the perfectly competitive market structure has in common is that neither has to concern itself

Lecture 10 Monopoly Power and Pricing Strategies

Lecture 10 Monopoly Power and Pricing Strategies Business 5017 Managerial Economics Kam Yu Fall 2013 Outline 1 Origins of Monopoly 2 Monopolistic Behaviours 3 Limits of Monopoly Power 4 Price Discrimination

Lecture 10 Monopoly Power and Pricing Strategies Business 5017 Managerial Economics Kam Yu Fall 2013 Outline 1 Origins of Monopoly 2 Monopolistic Behaviours 3 Limits of Monopoly Power 4 Price Discrimination

1) If the government sets a price ceiling below the monopoly price, will this reduce deadweight loss in a monopolized market?

If the government sets a price ceiling below the monopoly price, will this reduce deadweight loss in a monopolized market?") Managerial Economics Study Questions With Solutions Monopoly and Price Disrcimination 1) If the government sets a price ceiling below the monopoly price, will this reduce deadweight loss in a monopolized

Managerial Economics Study Questions With Solutions Monopoly and Price Disrcimination 1) If the government sets a price ceiling below the monopoly price, will this reduce deadweight loss in a monopolized

Labor Economics, 14.661. Lecture 3: Education, Selection, and Signaling

Labor Economics, 14.661. Lecture 3: Education, Selection, and Signaling Daron Acemoglu MIT November 3, 2011. Daron Acemoglu (MIT) Education, Selection, and Signaling November 3, 2011. 1 / 31 Introduction

Labor Economics, 14.661. Lecture 3: Education, Selection, and Signaling Daron Acemoglu MIT November 3, 2011. Daron Acemoglu (MIT) Education, Selection, and Signaling November 3, 2011. 1 / 31 Introduction

Pricing with Perfect Competition. Business Economics Advanced Pricing Strategies. Pricing with Market Power. Markup Pricing

Business Economics Advanced Pricing Strategies Thomas & Maurice, Chapter 12 Herbert Stocker [email protected] Institute of International Studies University of Ramkhamhaeng & Department of Economics

Business Economics Advanced Pricing Strategies Thomas & Maurice, Chapter 12 Herbert Stocker [email protected] Institute of International Studies University of Ramkhamhaeng & Department of Economics

Optimal Income Taxation with Multidimensional Types

1 Optimal Income Taxation with Multidimensional Types Kenneth L. Judd Hoover Institution NBER Che-Lin Su Northwestern University (Stanford Ph. D.) PRELIMINARY AND INCOMPLETE November, 2006 2 Introduction

1 Optimal Income Taxation with Multidimensional Types Kenneth L. Judd Hoover Institution NBER Che-Lin Su Northwestern University (Stanford Ph. D.) PRELIMINARY AND INCOMPLETE November, 2006 2 Introduction

CHAPTER 4 Consumer Choice

CHAPTER 4 Consumer Choice CHAPTER OUTLINE 4.1 Preferences Properties of Consumer Preferences Preference Maps 4.2 Utility Utility Function Ordinal Preference Utility and Indifference Curves Utility and

CHAPTER 4 Consumer Choice CHAPTER OUTLINE 4.1 Preferences Properties of Consumer Preferences Preference Maps 4.2 Utility Utility Function Ordinal Preference Utility and Indifference Curves Utility and

Exercises for Industrial Organization Master de Economía Industrial 2012-2013. Matilde Pinto Machado

Exercises for Industrial Organization Master de Economía Industrial 2012-2013 Matilde Pinto Machado September 11, 2012 1 Concentration Measures 1. Imagine two industries A and B with concentration curves

Exercises for Industrial Organization Master de Economía Industrial 2012-2013 Matilde Pinto Machado September 11, 2012 1 Concentration Measures 1. Imagine two industries A and B with concentration curves

Chapter 11. T he economy that we. The World of Oligopoly: Preliminaries to Successful Entry. 11.1 Production in a Nonnatural Monopoly Situation

Chapter T he economy that we are studying in this book is still extremely primitive. At the present time, it has only a few productive enterprises, all of which are monopolies. This economy is certainly

Chapter T he economy that we are studying in this book is still extremely primitive. At the present time, it has only a few productive enterprises, all of which are monopolies. This economy is certainly

LECTURE #15: MICROECONOMICS CHAPTER 17

LECTURE #15: MICROECONOMICS CHAPTER 17 I. IMPORTANT DEFINITIONS A. Oligopoly: a market structure with a few sellers offering similar or identical products. B. Game Theory: the study of how people behave

LECTURE #15: MICROECONOMICS CHAPTER 17 I. IMPORTANT DEFINITIONS A. Oligopoly: a market structure with a few sellers offering similar or identical products. B. Game Theory: the study of how people behave

CHAPTER 8 PROFIT MAXIMIZATION AND COMPETITIVE SUPPLY

CHAPTER 8 PROFIT MAXIMIZATION AND COMPETITIVE SUPPLY TEACHING NOTES This chapter begins by explaining what we mean by a competitive market and why it makes sense to assume that firms try to maximize profit.

CHAPTER 8 PROFIT MAXIMIZATION AND COMPETITIVE SUPPLY TEACHING NOTES This chapter begins by explaining what we mean by a competitive market and why it makes sense to assume that firms try to maximize profit.

A.2 The Prevalence of Transfer Pricing in International Trade

19. Transfer Prices A. The Transfer Price Problem A.1 What is a Transfer Price? 19.1 When there is a international transaction between say two divisions of a multinational enterprise that has establishments

19. Transfer Prices A. The Transfer Price Problem A.1 What is a Transfer Price? 19.1 When there is a international transaction between say two divisions of a multinational enterprise that has establishments

Health Economics. University of Linz & Physicians. Gerald J. Pruckner. Lecture Notes, Summer Term 2009. Gerald J. Pruckner Physicians 1 / 22

Health Economics Physicians University of Linz & Gerald J. Pruckner Lecture Notes, Summer Term 2009 Gerald J. Pruckner Physicians 1 / 22 Physicians in Austria Gerald J. Pruckner Physicians 2 / 22 Resident

Health Economics Physicians University of Linz & Gerald J. Pruckner Lecture Notes, Summer Term 2009 Gerald J. Pruckner Physicians 1 / 22 Physicians in Austria Gerald J. Pruckner Physicians 2 / 22 Resident

Monopoly and Monopsony Labor Market Behavior

Monopoly and Monopsony abor Market Behavior 1 Introduction For the purposes of this handout, let s assume that firms operate in just two markets: the market for their product where they are a seller) and

Monopoly and Monopsony abor Market Behavior 1 Introduction For the purposes of this handout, let s assume that firms operate in just two markets: the market for their product where they are a seller) and

Chapter 7: The Costs of Production QUESTIONS FOR REVIEW

HW #7: Solutions QUESTIONS FOR REVIEW 8. Assume the marginal cost of production is greater than the average variable cost. Can you determine whether the average variable cost is increasing or decreasing?

HW #7: Solutions QUESTIONS FOR REVIEW 8. Assume the marginal cost of production is greater than the average variable cost. Can you determine whether the average variable cost is increasing or decreasing?

Prices versus Exams as Strategic Instruments for Competing Universities

Prices versus Exams as Strategic Instruments for Competing Universities Elena Del Rey and Laura Romero October 004 Abstract In this paper we investigate the optimal choice of prices and/or exams by universities

Prices versus Exams as Strategic Instruments for Competing Universities Elena Del Rey and Laura Romero October 004 Abstract In this paper we investigate the optimal choice of prices and/or exams by universities

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY EXERCISES 3. A monopolist firm faces a demand with constant elasticity of -.0. It has a constant marginal cost of $0 per unit and sets a price to maximize

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY EXERCISES 3. A monopolist firm faces a demand with constant elasticity of -.0. It has a constant marginal cost of $0 per unit and sets a price to maximize

Economics 1011a: Intermediate Microeconomics

Lecture 11: Choice Under Uncertainty Economics 1011a: Intermediate Microeconomics Lecture 11: Choice Under Uncertainty Tuesday, October 21, 2008 Last class we wrapped up consumption over time. Today we

Lecture 11: Choice Under Uncertainty Economics 1011a: Intermediate Microeconomics Lecture 11: Choice Under Uncertainty Tuesday, October 21, 2008 Last class we wrapped up consumption over time. Today we

Capital Structure II

Capital Structure II Introduction In the previous lecture we introduced the subject of capital gearing. Gearing occurs when a company is financed partly through fixed return finance (e.g. loans, loan stock

Capital Structure II Introduction In the previous lecture we introduced the subject of capital gearing. Gearing occurs when a company is financed partly through fixed return finance (e.g. loans, loan stock

Imperfect information Up to now, consider only firms and consumers who are perfectly informed about market conditions: 1. prices, range of products

Imperfect information Up to now, consider only firms and consumers who are perfectly informed about market conditions: 1. prices, range of products available 2. characteristics or relative qualities of

Imperfect information Up to now, consider only firms and consumers who are perfectly informed about market conditions: 1. prices, range of products available 2. characteristics or relative qualities of

The Analysis of the Article Microsoft's Aggressive New Pricing Strategy Using. Microeconomic Theory

2 The Analysis of the Article Microsoft's Aggressive New Pricing Strategy Using Microeconomic Theory I. Introduction: monopolistic power as a means of getting high profits II. The review of the article

2 The Analysis of the Article Microsoft's Aggressive New Pricing Strategy Using Microeconomic Theory I. Introduction: monopolistic power as a means of getting high profits II. The review of the article

Exercises Lecture 8: Trade policies

Exercises Lecture 8: Trade policies Exercise 1, from KOM 1. Home s demand and supply curves for wheat are: D = 100 0 S = 0 + 0 Derive and graph Home s import demand schedule. What would the price of wheat

Exercises Lecture 8: Trade policies Exercise 1, from KOM 1. Home s demand and supply curves for wheat are: D = 100 0 S = 0 + 0 Derive and graph Home s import demand schedule. What would the price of wheat

Problem Set #3 Answer Key

Problem Set #3 Answer Key Economics 305: Macroeconomic Theory Spring 2007 1 Chapter 4, Problem #2 a) To specify an indifference curve, we hold utility constant at ū. Next, rearrange in the form: C = ū

Problem Set #3 Answer Key Economics 305: Macroeconomic Theory Spring 2007 1 Chapter 4, Problem #2 a) To specify an indifference curve, we hold utility constant at ū. Next, rearrange in the form: C = ū