Some Observations on Variance and Risk

|

|

|

- Rudolf Cain

- 10 years ago

- Views:

Transcription

1 Some Observations on Variance and Risk 1 Introduction By K.K.Dharni Pradip Kumar 1.1 In most actuarial contexts some or all of the cash flows in a contract are uncertain and depend on the death or survival or possibly the state of health of a life. 1.2 The income to a life insurer comes from the payments made by policyholders, which are called as the premium. There is further addition due to return earned on the fund. The outgo of an insurer is as benefits and expenses. 1.3 For various purposes, the assumptions may not be the best estimates of the individual basic elements but may be more cautious than best estimates. If we expect to earn an interest rate of 7% p.a. on the invested fund we may calculate the premiums assuming that we may earn 5% p.a. As we are assuming that we will earn less rate of interest that we expect on best estimate basis, the premiums so calculated will be higher than that would need to be if expected rate of 7% were actually earned. 2 General Aspects 2.1 The premiums are generally paid in one of the following ways: A single premium contract In this case the amount of premium is certain and there is need to calculate the expected value of payment A regular (annual) premium contract The premiums are paid by a regular (annual) payment of a level amount, the first premium is due at the time the contract is effected. The premiums continue to be paid until the end of some agreed maximum premium term which may be the same as the contract term, limited for certain period less than the contract term or until the life dies if the same occurs earlier. 254

2 2.1.3 However, instead of annual premiums, premiums may be paid in instalments on monthly, quarterly or half-yearly basis. In such a case, in the event of death of a life assured, the premium is payable for the full policy year in which the death takes place. 2.2 A net premium is the amount of premium required to meet the expected cost of the assurance or annuity benefits under a contract when mortality and interest assumptions are given. It is also referred as the pure premium or risk premium. 2.3 In a life insurance contract, we are concerned with the time value of money and uncertainty attached to payment to be made in the future. 2.4 A life insurance company may price products by any of the following three approaches: Assuming a constant interest rate for each future year Using a deterministic approach where interest rates are assumed to change in a predetermined way Using a stochastic approach 2.5 We may calculate the expected value and variance of a benefit which is a random variable (the benefit amount may be fixed but the time value may make it different) 2.6 The office premium for a contract on the basis of suitable mortality, interest and expense assumptions can be calculated by equating the expected present value as under: The expected value of the office premium income = The expected value of the outgo on benefits + The expected value of the outgo on expenses 2.7 The loss incurred by the insurer on a particular policy will depend on the future lifetime of the policyholder. From the equation of value, we can calculate the premium that sets the expected present value of the insurer s loss equal to zero. For any level of premium, we can calculate the expectation and variance of the present value of loss if the relevant assumptions are given. 3 Assumptions 3.1 We propose to consider the following plans for our study: 255

3 Whole life Term Assurance 15, 20 & 25 years Endowment Assurance 15, 20 & 25 years 3.2 In whole life assurance, the sum assured (benefit) is paid on the death of the life assured. The premium may be paid as single premium or as annual premium. The premium may be calculated taking into account the following: Mortality to be expected on the lives to be insured Investment return which could be earned on the fund Expenses which would be incurred in procuring, servicing and making final payment under the contract The further items could be considered such as: i. Bonus for with profit policies ii. Margin for adverse deviations iii. Provision to profit for shareholders / return on capital employed 3.3 We propose to calculate the values of benefit provided and its variance under same assumptions. The basis are as under: Mortality Table : LIC Ultimate Rates of interest : 5% p.a., 6% p.a., 7% p.a., 8% p.a. and 9% p.a. Sum assured : Rs. 1,00,000/- 4 Explanations 4.1 Whole life : Single Premium We are considering the business under without profit policies only. Further we are ignoring expense and margin for adverse deviation and provision for profit for shareholders / return on capital employed. The policies are assumed to join on exact age and sum assured is paid at the end of the year of death The without profit whole life policies may be issued to lives aged between 18 & 60 years of age. At age 18 years, the single premium Ax (value of the benefit) is Rs. 8, on the assumption of 5% rate of interest and Rs. 2, on the assumption of 9% rate of interest. The single premium at age 60 years at 5% rate of interest is Rs. 44, and at 9% rate of interest is Rs. 26, The single premium at age

4 years as compared to age 18 years has increased by 4.24 times at 5% rate of interest and times at 9% rate of interest. We know it is due to increasing mortality with increase in age and effect of increase in rate of interest The variance of single premium under without profit whole life policy can be calculated by using the formula as under: (SA)^2 [ 2Ax (Ax)^2 ] where SA is sum assured and for our purpose it is Rs. 1,00,000. Ax is value of the benefit under whole life insurance at rate of interest say i and 2Ax is value of the benefit under whole life insurance at rate of interest (1+i)^2-1. We would be using value of Ax at 5%, 6%, 7%, 8% & 9% and thus value of 2Ax would be arrived at 10.25%, 12.36%, 14.49%, 16.64% & 18.81% The value of variance of single premium of Rs. 8, at age 18 years at 5% rate of interest is Rs. 9,67,99,324. The sum assured is Rs. 1 lac and the variance is thus about 968 times the sum assured and about 11,503 times the single premium. The corresponding figure at age 60 years for single premium of Rs. 44, is Rs 34,47,66,252 which is about 3,448 times the sum assured and about 7,813 times single premium. The variance at age 60 years is 3.56 times the variance at age 18 years while the single premium at age 60 years is 5.24 times the single premium at age 18 years. 4.2 Whole life : Annual Premium For whole life policies, the premium may be for whole life or limited to some age and / or number of premiums. However for the purpose of this paper we are assuming that the premium are payable for whole of life and are paid annually in advance. The annual premium would be arrived at by the following formula:.. Ax / ax at different ages and at different rates of interest. The annual premium at ages 18 years at 5% rate of interest is Rs and at 9% rate of interest is Rs The annual premium at age 60 years at rate of interest of 5% is Rs. 3, and at rate of interest of 9% is Rs. 2, The annual premium at age 60 years is 8.60 times annual premium at age 18 years at 5% rate of interest and times annual premium at age 18 years at 9% rate of interest. 257

![3 The variance of single premium under without profit whole life policy can be calculated by using the formula as under: (SA)^2 [ 2Ax (Ax)^2 ] where SA is sum assured and for our purpose it is Rs.](/docs-images/53/11132466/images/page_4.jpg "1,00,000. Ax is value of the benefit under whole life insurance at rate of interest say i and 2Ax is value of the benefit under whole life insurance at rate of interest (1+i)^2-1.")

5 4.2.2 The variance of annual premium under Without Profit Whole Life Policy can be calculated by using the formula as under: (SA)^2 [(Px / d) + 1]^2 [ 2Ax (Ax)^2 ] where, Px is the annual premium for unit sum assured under whole life policy at a particular rate of interest i and d is the discount rate equivalent to rate of interest i and SA, 2Ax and Ax have the same meaning as for the single premium formula given earlier The value of variance of annual premium of Rs at age of 18 years at 5% rate of interest is Rs.11,54,05,427. The sum assured being Rs.1 lac, the variance is about 1,154 times the sum assured. Further, the variance is about 2,63,784 times the annual premium. As compared to variance under single premium at age of 18 years, variance under annual premium has increased by about 19%. The value of variance of annual premium of Rs.3, at age of 60 years at 5% rate of interest is Rs.110,49,82,178. As compared to sum assured of Rs.1 lac, the variance is about 11,050 times and as compared to annual premium of Rs.3,763.10, the variance is about 2,93,636 times The value of variance for whole-life without profit policy of annual premium at age of 18 years of Rs for whole-life without profit policy of Rs.1 lac at rate of interest of 9% is 5,69,31,945. The value of variance is about 569 times the sum assured of Rs.1 lac and about 3,01,546 times the amount of annual premium of Rs The value of variance of annual premium for age of 60 years (Rs.2,955.30) at 9% rate of interest is Rs.72,82,10,436. Thus, the value of variance at age of 60 years is about 7,282 times the value of sum assured of Rs.1 lac and about 2,46,408 times the annual premium. 4.3 Term Issurance : Single Premium We may now take up Term Insurance Without Profits. Terms being considered are 15 years, 20 years and 25 years. The value of the single premium for a sum assured of Rs.1 lac taking into account the mortality and interest would be as per the formula: where, 1,00,000 Ax:n I I 258

6 x is the exact age at entry n is the term during which benefit is payable if death occurs during the period. I Ax:n I is the value of benefit for a unit sum if a person at age x dies within a period of n years At 18 years of age, the single premium for 15 years term insurance at rate of interest of 5% is Rs.1, The single premium for 18 years of age and at 5% rate of interest for terms of 20 years and 25 years are Rs.1, and Rs.1, respectively. At the age of 60 years, the single premium at 5% rate of interest are Rs.23,348.20, Rs.32, and Rs.39, for terms of 15 years, 20 years and 25 years respectively. Thus, there is an increase of 1,992%, 2,198% and 2,165% in the single premium between 18 years and 60 years of age for Temporary Assurance of 15 years, 20 years and 25 years respectively The value of the variance for single premium of policy of Rs.1 lac term insurance is as under: where, I I (1,00,000)^2 [ 2Ax:n I ( Ax:n I )^2] 2Ax:n I is the value of term insurance of unit amount age at age x for a period of n years at rate of interest (1 + I)^2 1 I where i is the rate of interest assumed in the calculation of Ax:n I The value of variance of single premium of Rs.1, for term insurance for 15 years at age 18 years at 5% rate of interest is Rs.7,81,89,634. The sum assured is Rs.1 lac and the variance is thus about 782 times the sum assured and about 70,050 times the single premium of Rs.1, The single premium at age 18 years for term insurance of 20 years and 25 years are Rs.1, and Rs.1, and the corresponding value of variance are Rs.8,93,27,667 and Rs.9,88,63,699 respectively. The variances for term insurance of 20 years and 25 years are about 893 and 989 times the sum assured of Rs.1 lac and about 63,755 and 57,296 times the respective single premiums The value of variance of single premium of Rs for term assurance of Rs.1 lac at age of 18 years at rate of interest of 9% is Rs.5,01,95,714. The variance is thus about I 259

7 502 times the sum assured and about 58,578 times the single premium. The single premium at the same age for 20 years and 25 years term insurance at 9% rate of interest are Rs.1, and Rs.1, while the corresponding values of variance are Rs.5,30,45,876 and Rs.5,46,55,955 respectively. Thus, the variances are about 530 and 547 times the sum assured and about 52,924 and 47,965 times the respective single premium for term insurance policies of 20 and 25 years The value of variation of single premium of Rs.23, for term insurance of 15 years at 5% rate of interest at 60 years of age is Rs.102,88,87,233. The sum assured is Rs.1 lac and the variance is thus about 10,289 times the sum assured and about 44,067 times the single premium. The single premium for term insurance of 20 and 25 years at 5% rate of interest at 60 years of age are Rs.32, and Rs.39, respectively. The values of variation at age 60 years for term insurances for 20 and 25 years are Rs.90,67,50,101 and Rs.64,27,72,382 respectively. The variance for 20 years term insurance policies are about 9068 times the sum assured and about 28,162 times the value of single premium. The variances for 25 years term insurance policies are about 6,428 times the sum assured and about 16,449 times the value of the single premium for the policy The value of variation at age 60 years of single premium of Rs.17, at 9% rate of interest for term insurance of 15 years is Rs.64,02,95,182 which is about 6,403 times the value of sum insurance of Rs.1 lac and about 37,244 times the value of single premium. The corresponding values of variation for term insurance of 20 years and 25 years are Rs.56,17,88,518 and Rs.46,73,07,527. The variance values for 20 and 25 years term insurance are about 5,618 and 4,673 times the sum assured of Rs.1 lac and about 25,865 times and 18,955 times the value of single premiums of Rs.21, and Rs.24, respectively. 4.4 Term Issurance : Annual Premium We may now take up annual premium under term insurance plans and the values for the annual premium and variance under the annual premiums may be calculated as under: I I.. Expected value of annual premium (Px:n I )= SA * ( Ax:n I / ax:n I ) I I I Variance value of annual premium = (SA)^2 [(Px:n I/d) + 1]^2 [ 2Ax:n I (Ax:n I)^2] 260

8 4.4.2 At 18 years of age, the annual premium for sum assured of Rs.1 lac for 15 years term insurance at rate of interest of 5% is Rs and the variance of annual premium is Rs.8,16,10,954. The variance is about 816 times the sum assured and about 7,91,571 times the annual premium. The variance of annual premium at rate of interest of 5% at 18 years of age for term insurance for 20 years and 25 years are Rs.9,34,24,974 and Rs.10,38,17,460 against annual premium of Rs and Rs Thus, the variance for 20 and 25 years term insurance policies are about 934 and 1,038 times the sum insured and about 8,65,046 and about 8,81,303 times the respective annual premiums under the policies The annual premium for sum assured of Rs.1 lac for 15 years term insurance at the age of 60 years at 5% rate of interest is Rs.2, and the variance of annual premium is Rs.234,01,07,607. Thus, the variance is about 23,401 times the sum assured and about 9,67,146 times the annual premium. The corresponding variances for 20 years and 25 years term insurance are Rs.238,51,49,235 and Rs.189,29,41,618 against the annual premiums of Rs.2, and Rs.3, respectively. Thus, the variances for 20 and 25 years term policy at age of 60 years at 5% rate of interest are about and 18,929 times the sum assured and about 8,05,467 times and 5,55,115 times the respective annual premiums under the policy At 9% rate of interest and the age of 18 years, the annual premium for sum assured of Rs.1 lac for 15 years term insurance is Rs and the variance of annual premium is Rs.5,13,95,270. Thus, the variance is about 514 times the sum assured and about 5,23,907 times the annual premium. The variances of annual premiums at 9% rate of interest at the age of 18 years for term insurance policies of 20 and 25 years terms are Rs.5,43,57,560 and Rs.5,60,86,262 against the annual premiums of Rs and Rs respectively. Thus, the variances at 20 and 25 years term insurance policies are about 544 and 561 times the sum assured and about 5,35,542 and 5,22,705 times their respective annual premium At 9% rate of interest and the age of 60 years, the annual premium for a sum assured of Rs.1 lac for term insurance of 15 years is Rs.2, and the variance of annual premium is Rs.102,19,10,580. Thus, the variance is about 10,219 times the sum assured and about 4,69,995 times the annual premium. The variances of annual premiums at 9% rate of interest at the age of 60 years for term insurance policies 20 and 25 years term are 96,00,44,363 and 83,71,12,840 which are about 9,600 and 8,371 times the sum assured of Rs.1 lac and about 3,78,432 times and 2,99,589 times the annual premium of Rs.2, and Rs.2, respectively. 261

9 4.5 Endowment Assurance : Single Premium We would now take up the Endowment Assurance Without Profit policy with terms 15, 20 and 25 years. The sum assured is payable at death during the term of insurance and on survival at the end of the term. We would first consider single premium policy and the premium would be 1,00,000 * Ax:n I where the symbol Ax:n I denotes the value of unit sum payable on death during the term of n years and on survival to the end of the term (if the death has not taken place) during the term at age x of the life assured at a particular rate of interest The value of the variance for single premium of Rs.1 lac sum assured is as under: (1,00,000)^2 [ 2Ax:n I (Ax:n I)^2 ] where, 2Ax:n I is the value of Endowment Assurance of unit amount at age x for a period of n years at rate of interest (1+i)^2 1 where i is the assumed rate in the calculation of Ax:n I At 5% rate of interest and age of 18 years, the single premium for Endowment Assurance Without Profit policy for Rs.1 lac sum assured for term of 15 years is Rs.48, and the corresponding variance of single premium is Rs.98,18,682. Accordingly, the variance is about 98 times the sum assured and about 203 times the single premium. The variances for terms 20 years and 25 years for Rs.1 lac sum assured at age of 18 years are Rs.1,84,26,372 and Rs.2,83,92,515 against the single premium of Rs.38, and Rs.30, respectively. Thus, the variances are about 184 and 284 times the sum assured and about 482 and 938 times their respective single premiums At 5% rate of interest and age of 60 years, the single premium for Endowment Assurance Without Profit policy for Rs.1 lac sum assured for term of 15 years is Rs.54, and the variance of single premium is Rs.12,94,83,111. Accordingly, the variance is about 1,295 times the sum assured and about 2,396 times the single premium. The variances for terms of 20 years and 25 years for Rs.1 lac sum assured at age of 60 years are Rs.22,18,43,292 and Rs.29,34,12,447 against the single premium of Rs.48, and Rs.45, Thus, the variances are about 2,218 and 2,934 times the sum assured and about 4,600 and 6,458 times their respective single premiums. 262

during the term at age x of the life assured at a particular rate of interest. 4.5.")

10 4.5.5 At 9% rate of interest and age of 18 years, the single premium for Endowment Assurance Without Profit policy of Rs.1 lac sum assured for term of 15 years is Rs.27, and the corresponding variance of single premium is Rs.1,60,51,127. Accordingly, the variance is about 161 times the sum assured and about 576 times the single premium. The variances for terms of 20 years and 25 years for Rs.1 lac sum assured at age of 18 years are Rs.2,53,37,871 and Rs.3,34,33,031 against single premium of Rs.18, and Rs,12, respectively. Thus, the variances are about 253 and 334 times the sum assured and 1,375 and 2,707 times their respective single premiums At 9% rate of interest and age of 60 years, the single premium for Endowment Assurance Without Profits for Rs.1 lac sum assured for term of 15 years is Rs.34,714 and the corresponding variance of single premium is Rs.21,18,39,604. Accordingly, the variance is about 2,118 times the sum assured and about 6,102 times the single premium. The variances for terms of 20 and 25 years for Rs.1 lac sum assured at age of 60 years are Rs.30,99,79,847 and Rs.36,69,71,890 against single premium of Rs.29, and Rs.27, respectively. Thus, the variances are about 3,100 times and 3,670 times the sum assured and about 10,577 and 13,517 times their respective single premiums. 4.6 Endowment Assurance : Annual Premium We would now take up annual premiums under Endowment Assurance Without Profit policy for terms of 15, 20 and 25 years. The annual premium can be derived from the value of the benefit (single premium) divided by the immediate annuity ȧ. x:n I as per the definition given in the term insurance annual premium contract The value of the variance for annual premium of Rs.1 lac sum assured is calculated by using the formula as under: (SA)^2 [(Px:n I/d) + 1]^2 [ 2Ax:n I (Ax:n I)^2 ] where, Px:n I is the Endowment Assurance Without Profit premium for term of n years for unit sum assured. Other symbols have similar definitions as per term insurance contract At 5% rate of interest and age of 18 years, the annual premium for Endowment Assurance Without Profit policy of Rs.1 lac sum assured for term of 15 years is Rs.4, and 263

11 the corresponding variance of annual premium is Rs.3,69,20,582. Accordingly, the variance is about 369 times the sum assured and about 8,256 times the amount of annual premium. The variance for terms of 20 years and 25 years for Rs.1 lac sum assured at age of 18 years are Rs.4,82,67,764 and Rs.5,83,98,982 against annual premium of Rs.2, and Rs.2, respectively. Thus, the variances are about 483 and 584 times the sum assured and 16,389 and 28,246 times their respective annual premiums At 5% rate of interest and age of 60 years, the annual premium for Endowment Assurance Without Profit policy of Rs.1 lac sum assured for term of 15 years is Rs.5, and the corresponding variance of annual premium is Rs.61,32,33,751. Accordingly, the variance is about 6,132 times the sum assured and about 1,09,485 times the amount of annual premium. The variance for terms of 20 years and 25 years for Rs.1 lac sum assured at age of 60 years are Rs.82,75,63,787 and Rs.98,53,40,079 against annual premium of Rs.4, and Rs.3, respectively. Thus, the variances are about 8,276 and 9,853 times of the sum assured and 1,86,582 and 2,48,541 times their respective annual premium At 9% rate of interest and age of 18 years, the annual premium for Endowment Assurance Without Profit policy of Rs.1 lac sum assured for term of 15 years is Rs.3, and the corresponding variance of annual premium is Rs.3,08,43,899. Accordingly, the variance is about 308 times the sum assured and about 9,672 times the amount of annual premium. The variances for terms of 20 years and 25 years for Rs.1 lac sum assured at age of 18 years are Rs.3,80,81,620 and Rs.435,18,680 against annual premiums of Rs.1, and Rs respectively. Thus, the variances are about 381 and 435 times the sum assured and 20,412 and 37,406 times their respective annual premiums At 9% rate of interest and age of 60 years, the annual premium for Endowment Assurance Without Profit policy of Rs.1 lac sum assured for term of 15 years is Rs.4, and the corresponding variance of annual premium is Rs.49,70,12,852. Accordingly, the variance is about 4,970 times the sum assured and about 1,13,204 times the amount of annual premium. The variances for terms of 20 years and 25 years for Rs.1 lac sum assured at age of 60 years are Rs.62,02,90,114 and Rs.69,14,56,607 against annual premiums of Rs.3, and Rs.3, respectively. Thus, the variances are about 6,203 times and 6,915 times of the sum assured and 1,81,202 and 2,24,710 times their respective annual premiums. 264

12 5 Observations 5.1 We attach the annexures - 1 & 2 showing the variance of single premium at 5% and 9% rates of interest respectively. While going through the same, we may make the following observations on the values of variance: The variance for single premium for Whole Life policies is increasing with increase in age. The variance at age 60 years is about 4 times the variance at age 14 years at 5% rate of interest The variance for single premium for Whole Life policies becomes less with increase in rate of interest upto certain ages and then increasing thereafter. For increase in rate of interest from 5% to 6%, the variance upto age 48 years is less at 6% rate of interest as compared to 5% rate of interest and then from age 49 years onwards, the variance at 6% is more than variance at 5%. While comparing the rates of 5% and 9%, the variance at 9% is less upto age 54 years but is more at age 55 years and onwards The variance under Term Insurance policy is more for all terms of 15 years, 20 years and 25 years as compared to the variance under Whole Life policy after age 35 years at 5% rate of interest and after age 38 years at 9% rate of interest At 5% rate of interest, the variance under Term Insurance policy increases with increase in term from 15 years to 20 years from age of 14 years to 56 years and then decreases. The position for term from 20 years to 25 years is that the variance is more for 25 years upto age of 49 years and is then less for the age of 50 years and onwards At 9% rate of interest, the variance under Term Insurance policy increases with increase in term from 15 years to 20 years from age of 14 years to 52 years and then decreases. The position for term from 20 years to 25 years is that the variance is more for 25 years upto age of 45 years and is then less for the age of 46 years and onwards The variance under Endowment Assurance is much less as compared to Term Assurance and Whole Life policies. This is due to the provision of payment of benefit on the survival to the end of the term The variance under Endowment Assurance at all ages increases with the increase in term from 15 years to 25 years. 265

13 5.2 We attach the annexures 3 & 4 showing the variance of annual premiums at rates of interest of 5% and 9%. While going through the same, we may make the following observations on the values of variance: Variance under annual premium is always more than the variance under single premium. Incidentally, the single premium is always more than the annual premium Variance is increasing with age (both at 5% and 9%) At 5% rate of interest, variance under Term Insurance for 20 years is always more than the variance under 15 years term insurance for all ages. However, if we compare variance for 25 years term insurance with 20 years term insurance, the same is more upto 53 years of age and is then less from age 54 onwards Both at 5% and 9% rate of interest for all ages, the variance under 20 years Endowment Assurance policy is higher than the variance under 15 years Endowment policy. Same is the position of Endowment Assurance policy for 25 years term as compared to 20 years Endowment Assurance policy At 9% rate of interest, the variance under term insurance for 20 years is more upto 56 years of age but is less from age 57 years onwards as compared to the variance under term insurance of 15 years. Further, the variance under term insurance for 25 years is more upto 48 years of age and is less from age 49 years onwards as compared to the variance under term insurance of 20 years. 5.3 The variances under Endowment Assurance Without Profit are lowest and the variances under term insurance for 25 years are generally higher than the variance under Whole Life without Profit. The premiums under Endowment Assurances are much more than the term assurances as Endowment Assurances contain the additional payment of sum assured on survival to the end of term. The premium under Whole Life is lower than the premium under Endowment Assurance but is more than the term assurance as the mortality at higher ages is more. 6 General Observations 6.1 The premiums are calculated taking into account the mortality and a fixed rate of interest for the entire term. The variance is for a single policy and it is due to a small probability of a policy becoming a claim due to death every year during the term of the policy 266

. 5.2.3 At 5% rate of interest, variance under Term Insurance for 20 years is always more than the variance under 15 years term insurance for all ages.")

14 under Term Insurance, Endowment Assurance and Whole Life except at very high ages under the Whole Life. Although under Whole Life and Endowment Assurances, we are sure that the benefit is payable but is distributed with a probability distribution as per mortality table which gives rise to variance as a fixed rate of interest is involved which makes the present value of the benefits differ according to the time of payment. Under Term Insurance, there is no payment on survival to the end of the term but the payment of benefit is distributed with a probability distribution as per the mortality table. 6.2 The risk we have covered is primarily the mortality risk. We know that if there are n lives of the same age, the variance of the group of n lives is n times the variance of the individual policy (life) considering the various lives as independent. The standard deviation is the positive square root of the variance and thus the standard deviation of the group of n independent lives at the same age and with same sum assured and under the same plan and term will reduce by the square root of n. Thus, if there is a large number of independent lives, the standard deviation for a certain age, plan, term and sum assured would reduce in proportion substantially (in proportion to square root of the number of lives). 7 Number of Lives 7.1 We propose to consider the minimum number of lives so that the probability of the experience exceeding the charged annual premium which we may consider it as 110% of annual premium is 1%. 7.2 For Whole Life Assurance, the annual premium at age 18 for Rs.1 lac sum assured at 5% rate of interest is Rs and the standard deviation is Rs.10, We want the standard deviation reduced to such an extent that times (assuming normal distribution) of the standard deviation for the group of n lives is 10% of the annual premium. The formula for this may be given as under : * Standard Deviation of individual policy = 10% of annual premium (n)^(1/2) or (n)^(1/2) = * Standard Deviation of individual policy 10% of annual premium 7.3 The number of independent lives at age of 18 years required for the probability of loss exceeding 10% of annual premium being 1% is 3,26,204. This is the position for Whole Life Insurance at age of 18 years. 267

15 7.4 On the above basis, the number of independent lives required for the probability of loss exceeding 10% of annual premium being 1% for term insurance of 15 years term at age 18 is 41,53,849. The relevant figures for 20 and 25 years are 38,12,157 and 40,47,619 lives. 7.5 Similarly, the number of independent lives required for the probability of loss exceeding 10% of annual premium being 1% for Endowment Assurance Without Profit for term of 15 years at age 18 is 999. The relevant figures for terms of 20 and 25 years at age 18 are 3,011 and 7,392 lives. 7.6 The charging for margin for adverse deviation at a flat rate for all the plans may not be appropriate. However, for the purpose of our study, we have chosen the margin at 5% and probability level also at 5%. The formula for the number of independent lives required on this basis is as under: (1.96 * Standard Deviation of individual policy / 5% of annual premium)^2 7.7 We attach annexure - 5 giving the single premiums, standard deviations and minimum number of lives required under Whole Life, Term Assurances with terms 15, 20 and 25 years and Endowment Assurance with terms 15, 20 and 25 years at rates of interest 5%, 6%, 7%, 8% and 9% for ages 20, 30, 40, 50 and 60 years. The Annexure - 6 gives the above information for annual premium. 7.8 On the basis of Annexure 5 & 6, we may observe as under: The minimum lives are 7 under single premium Endowment Assurance for 15 years at age 20. The maximum lives are under annual premium Term Insurance for 20 years where the number of lives are 1,15,25,236. However, the term insurance annual premium for 15 years term is Rs only and if we increase it by 50% instead of 5% as assumed in the calculation, the number of lives would be reduced to 1,15, The figure of minimum number of lives is reducing with the increase in age from 20 to 60 years under Whole Life and Term Insurance plans at all the rates of interest viz. 5%, 6%, 7%, 8% and 9%. This is the position for both the single premium and annual premium policies The figure of minimum number of lives is increasing with increase in age for Endowment Assurance under the term of 15, 20 and 25 years both under Single premium and Annual premium and at all rates of interest viz. 5%, 6%, 7%, 8% and 9%. 268

16 7.8.4 The figures of minimum number of lives generally decreases with increase in terms from 15 years to 20 years and from 20 years to 25 years both under single premium and annual premium except that the figure for annual premium term insurance for 20 years is more than the figure of term insurance for 15 years at age of 20 years The figures of minimum number of lives under Endowment Assurance are increasing with increase in term from 15 years to 20 years and from 20 years to 25 years both under single premium and annual premiums and at all rates of interest viz. 5%, 6%, 7%, 8% and 9%. 8 Conclusions 8.1 We may conclude that we need to be more careful under Term Insurance plan as far as mortality is concerned. However, we should have a large portfolio of business so that the homogeneity is increased and variance is reduced. 8.2 We have not considered the effect of variation in sum assured and duplicate policies (multiple policies on single life). However, normally companies would be having reinsurance arrangement so that the policies beyond certain sum assured are reinsured. 8.3 The variance of Endowment Assurance would be more affected by the probable distribution of interest rate assumption rather than uniform rate of interest. 269

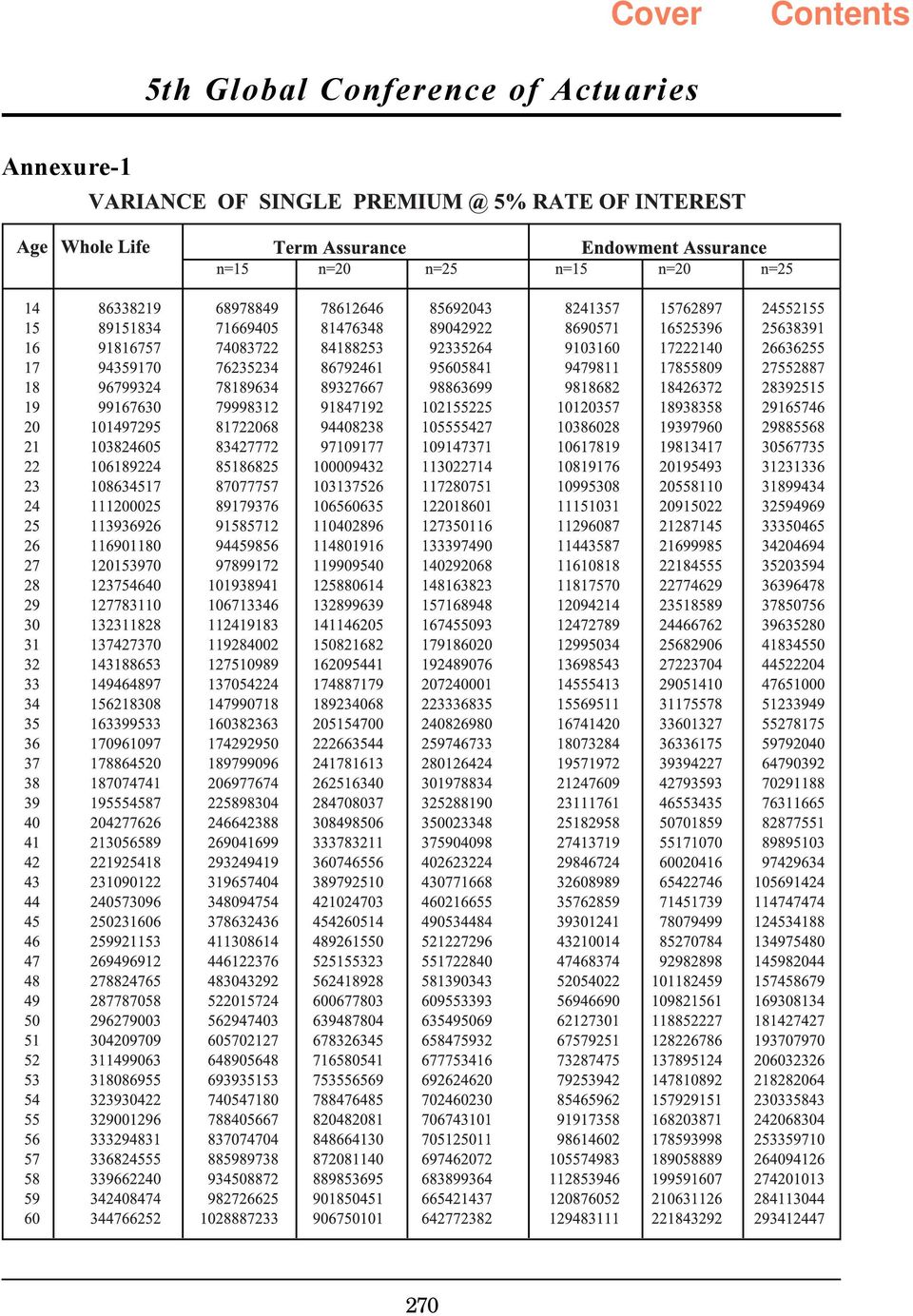

17 Annexure-1 270

18 Annexure-2 271

19 Annexure-3 272

20 Annexure-4 273

21 Annexure-5 Minimum Number of Lives required for 5% probability (Single Premium) of loss not exceeding 5% of Single Premium 274

22 Annexure-6 Minimum Number of Lives required for 5% probability (Annual Premium) of loss not exceeding 5% of Annual Premium 275

23 About the Author : K. K. Dharni Name : Kewal Krishan Dharni Date of Birth : 13 th March 1942 Current position : Consultant with Sahara India Life Insurance Co. Ltd. Professional Qualification : Associate of Insititute of Actuaries, London Fellow of Actuarial Society of India, Mumbai Past Experience : Worked in LIC of India from December 1962 to July Retired as Regional Manager (Actuarial) which position was held for about 9 years. Has experience in New Business, Actuarial, Pension & Group Schemes and Training. [email protected] 276

24 About the Author : Pradip Kumar Name : Pradip Kumar Current position : Deputy Secretary (Actuarial/Valuation), LIC of India, Central Office, Mumbai Professional Qualification : DAT of Insititute of Actuaries, London Associate of Actuarial Society of India, Mumbai Academic : Master s degree in Physics Bachelor degree in Science Past Experience : Working in LIC of India since Has experience in Product Development in Central Office, Actuarial. Pension & Group Schemes both in Administration and Marketing. LIC Housing Finance as Area Manager. Conventional Branch as Sr./ Branch Manager. [email protected] 277

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 17 th November 2011 Subject CT5 General Insurance, Life and Health Contingencies Time allowed: Three Hours (10.00 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 17 th November 2011 Subject CT5 General Insurance, Life and Health Contingencies Time allowed: Three Hours (10.00 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO

JANUARY 2016 EXAMINATIONS. Life Insurance I

PAPER CODE NO. MATH 273 EXAMINER: Dr. C. Boado-Penas TEL.NO. 44026 DEPARTMENT: Mathematical Sciences JANUARY 2016 EXAMINATIONS Life Insurance I Time allowed: Two and a half hours INSTRUCTIONS TO CANDIDATES:

PAPER CODE NO. MATH 273 EXAMINER: Dr. C. Boado-Penas TEL.NO. 44026 DEPARTMENT: Mathematical Sciences JANUARY 2016 EXAMINATIONS Life Insurance I Time allowed: Two and a half hours INSTRUCTIONS TO CANDIDATES:

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION 8 October 2015 (pm) Subject CT5 Contingencies Core Technical

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION 8 October 2015 (pm) Subject CT5 Contingencies Core Technical

O MIA-009 (F2F) : GENERAL INSURANCE, LIFE AND

: GENERAL INSURANCE, LIFE AND") No. of Printed Pages : 11 MIA-009 (F2F) kr) ki) M.Sc. ACTUARIAL SCIENCE (MSCAS) N December, 2012 0 O MIA-009 (F2F) : GENERAL INSURANCE, LIFE AND HEALTH CONTINGENCIES Time : 3 hours Maximum Marks : 100

No. of Printed Pages : 11 MIA-009 (F2F) kr) ki) M.Sc. ACTUARIAL SCIENCE (MSCAS) N December, 2012 0 O MIA-009 (F2F) : GENERAL INSURANCE, LIFE AND HEALTH CONTINGENCIES Time : 3 hours Maximum Marks : 100

Further Topics in Actuarial Mathematics: Premium Reserves. Matthew Mikola

Further Topics in Actuarial Mathematics: Premium Reserves Matthew Mikola April 26, 2007 Contents 1 Introduction 1 1.1 Expected Loss...................................... 2 1.2 An Overview of the Project...............................

Further Topics in Actuarial Mathematics: Premium Reserves Matthew Mikola April 26, 2007 Contents 1 Introduction 1 1.1 Expected Loss...................................... 2 1.2 An Overview of the Project...............................

Heriot-Watt University. BSc in Actuarial Mathematics and Statistics. Life Insurance Mathematics I. Extra Problems: Multiple Choice

Heriot-Watt University BSc in Actuarial Mathematics and Statistics Life Insurance Mathematics I Extra Problems: Multiple Choice These problems have been taken from Faculty and Institute of Actuaries exams.

Heriot-Watt University BSc in Actuarial Mathematics and Statistics Life Insurance Mathematics I Extra Problems: Multiple Choice These problems have been taken from Faculty and Institute of Actuaries exams.

EXAMINATION. 6 April 2005 (pm) Subject CT5 Contingencies Core Technical. Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE

Subject CT5 Contingencies Core Technical. Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE") Faculty of Actuaries Institute of Actuaries EXAMINATION 6 April 2005 (pm) Subject CT5 Contingencies Core Technical Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate and

Faculty of Actuaries Institute of Actuaries EXAMINATION 6 April 2005 (pm) Subject CT5 Contingencies Core Technical Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate and

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION 27 April 2015 (pm) Subject CT5 Contingencies Core Technical Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate and examination

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION 27 April 2015 (pm) Subject CT5 Contingencies Core Technical Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate and examination

PREMIUM AND BONUS. MODULE - 3 Practice of Life Insurance. Notes

4 PREMIUM AND BONUS 4.0 INTRODUCTION A insurance policy needs to be bought. This comes at a price which is known as premium. Premium is the consideration for covering of the risk of the insured. The insured

4 PREMIUM AND BONUS 4.0 INTRODUCTION A insurance policy needs to be bought. This comes at a price which is known as premium. Premium is the consideration for covering of the risk of the insured. The insured

Actuarial Society of India

Actuarial Society of India EXAMINATION 30 th October 2006 Subject ST1 Health and Care Insurance Specialist Technical Time allowed: Three hours (14.15* pm 17.30 pm) INSTRUCTIONS TO THE CANDIDATE 1. Enter

Actuarial Society of India EXAMINATION 30 th October 2006 Subject ST1 Health and Care Insurance Specialist Technical Time allowed: Three hours (14.15* pm 17.30 pm) INSTRUCTIONS TO THE CANDIDATE 1. Enter

Solution. Let us write s for the policy year. Then the mortality rate during year s is q 30+s 1. q 30+s 1

Solutions to the May 213 Course MLC Examination by Krzysztof Ostaszewski, http://wwwkrzysionet, krzysio@krzysionet Copyright 213 by Krzysztof Ostaszewski All rights reserved No reproduction in any form

Solutions to the May 213 Course MLC Examination by Krzysztof Ostaszewski, http://wwwkrzysionet, krzysio@krzysionet Copyright 213 by Krzysztof Ostaszewski All rights reserved No reproduction in any form

1 st December 2014. Taxability of Life Insurance Benefits An Actuarial View

1 st December 2014 Taxability of Life Insurance Benefits An Actuarial View 1) The Finance Act 2014, has introduced Section 194 (DA) in the Income tax Act, 1961, requiring deduction of tax at source at

1 st December 2014 Taxability of Life Insurance Benefits An Actuarial View 1) The Finance Act 2014, has introduced Section 194 (DA) in the Income tax Act, 1961, requiring deduction of tax at source at

Premium Calculation. Lecture: Weeks 12-14. Lecture: Weeks 12-14 (STT 455) Premium Calculation Fall 2014 - Valdez 1 / 31

Premium Calculation Fall 2014 - Valdez 1 / 31") Premium Calculation Lecture: Weeks 12-14 Lecture: Weeks 12-14 (STT 455) Premium Calculation Fall 2014 - Valdez 1 / 31 Preliminaries Preliminaries An insurance policy (life insurance or life annuity) is

Premium Calculation Lecture: Weeks 12-14 Lecture: Weeks 12-14 (STT 455) Premium Calculation Fall 2014 - Valdez 1 / 31 Preliminaries Preliminaries An insurance policy (life insurance or life annuity) is

Premium Calculation. Lecture: Weeks 12-14. Lecture: Weeks 12-14 (Math 3630) Annuities Fall 2015 - Valdez 1 / 32

Annuities Fall 2015 - Valdez 1 / 32") Premium Calculation Lecture: Weeks 12-14 Lecture: Weeks 12-14 (Math 3630) Annuities Fall 2015 - Valdez 1 / 32 Preliminaries Preliminaries An insurance policy (life insurance or life annuity) is funded

Premium Calculation Lecture: Weeks 12-14 Lecture: Weeks 12-14 (Math 3630) Annuities Fall 2015 - Valdez 1 / 32 Preliminaries Preliminaries An insurance policy (life insurance or life annuity) is funded

Annuities. Lecture: Weeks 9-11. Lecture: Weeks 9-11 (STT 455) Annuities Fall 2014 - Valdez 1 / 43

Annuities Fall 2014 - Valdez 1 / 43") Annuities Lecture: Weeks 9-11 Lecture: Weeks 9-11 (STT 455) Annuities Fall 2014 - Valdez 1 / 43 What are annuities? What are annuities? An annuity is a series of payments that could vary according to:

Annuities Lecture: Weeks 9-11 Lecture: Weeks 9-11 (STT 455) Annuities Fall 2014 - Valdez 1 / 43 What are annuities? What are annuities? An annuity is a series of payments that could vary according to:

How To Perform The Mathematician'S Test On The Mathematically Based Test

MATH 3630 Actuarial Mathematics I Final Examination - sec 001 Monday, 10 December 2012 Time Allowed: 2 hours (6:00-8:00 pm) Room: MSB 411 Total Marks: 120 points Please write your name and student number

MATH 3630 Actuarial Mathematics I Final Examination - sec 001 Monday, 10 December 2012 Time Allowed: 2 hours (6:00-8:00 pm) Room: MSB 411 Total Marks: 120 points Please write your name and student number

How To Become A Life Insurance Specialist

Institute of Actuaries of India Subject ST2 Life Insurance For 2015 Examinations Aim The aim of the Life Insurance Specialist Technical subject is to instil in successful candidates principles of actuarial

Institute of Actuaries of India Subject ST2 Life Insurance For 2015 Examinations Aim The aim of the Life Insurance Specialist Technical subject is to instil in successful candidates principles of actuarial

Glossary of insurance terms

Glossary of insurance terms I. Insurance Products Annuity is a life insurance policy where an insurance company pays an income stream to an individual, usually until death, in exchange for the payment

Glossary of insurance terms I. Insurance Products Annuity is a life insurance policy where an insurance company pays an income stream to an individual, usually until death, in exchange for the payment

The Internal Rate of Return Model for Life Insurance Policies

The Internal Rate of Return Model for Life Insurance Policies Abstract Life insurance policies are no longer seen solely as a means of insuring life. Due to many new features introduced by life insurers,

The Internal Rate of Return Model for Life Insurance Policies Abstract Life insurance policies are no longer seen solely as a means of insuring life. Due to many new features introduced by life insurers,

May 2012 Course MLC Examination, Problem No. 1 For a 2-year select and ultimate mortality model, you are given:

Solutions to the May 2012 Course MLC Examination by Krzysztof Ostaszewski, http://www.krzysio.net, [email protected] Copyright 2012 by Krzysztof Ostaszewski All rights reserved. No reproduction in any

Solutions to the May 2012 Course MLC Examination by Krzysztof Ostaszewski, http://www.krzysio.net, [email protected] Copyright 2012 by Krzysztof Ostaszewski All rights reserved. No reproduction in any

Chapter 2. 1. You are given: 1 t. Calculate: f. Pr[ T0

Chapter 2 1. You are given: 1 5 t F0 ( t) 1 1,0 t 125 125 Calculate: a. S () t 0 b. Pr[ T0 t] c. Pr[ T0 t] d. S () t e. Probability that a newborn will live to age 25. f. Probability that a person age

Chapter 2 1. You are given: 1 5 t F0 ( t) 1 1,0 t 125 125 Calculate: a. S () t 0 b. Pr[ T0 t] c. Pr[ T0 t] d. S () t e. Probability that a newborn will live to age 25. f. Probability that a person age

TABLE OF CONTENTS. 4. Daniel Markov 1 173

TABLE OF CONTENTS 1. Survival A. Time of Death for a Person Aged x 1 B. Force of Mortality 7 C. Life Tables and the Deterministic Survivorship Group 19 D. Life Table Characteristics: Expectation of Life

TABLE OF CONTENTS 1. Survival A. Time of Death for a Person Aged x 1 B. Force of Mortality 7 C. Life Tables and the Deterministic Survivorship Group 19 D. Life Table Characteristics: Expectation of Life

1 Cash-flows, discounting, interest rate models

Assignment 1 BS4a Actuarial Science Oxford MT 2014 1 1 Cash-flows, discounting, interest rate models Please hand in your answers to questions 3, 4, 5 and 8 for marking. The rest are for further practice.

Assignment 1 BS4a Actuarial Science Oxford MT 2014 1 1 Cash-flows, discounting, interest rate models Please hand in your answers to questions 3, 4, 5 and 8 for marking. The rest are for further practice.

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 13 th May 2015 Subject CT5 General Insurance, Life and Health Contingencies Time allowed: Three Hours (10.30 13.30 Hrs) Total Marks: 100 INSTRUCTIONS TO THE

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 13 th May 2015 Subject CT5 General Insurance, Life and Health Contingencies Time allowed: Three Hours (10.30 13.30 Hrs) Total Marks: 100 INSTRUCTIONS TO THE

1. Datsenka Dog Insurance Company has developed the following mortality table for dogs:

1 Datsenka Dog Insurance Company has developed the following mortality table for dogs: Age l Age l 0 2000 5 1200 1 1950 6 1000 2 1850 7 700 3 1600 8 300 4 1400 9 0 Datsenka sells an whole life annuity

1 Datsenka Dog Insurance Company has developed the following mortality table for dogs: Age l Age l 0 2000 5 1200 1 1950 6 1000 2 1850 7 700 3 1600 8 300 4 1400 9 0 Datsenka sells an whole life annuity

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION 30 April 2015 (am) Subject SA2 Life Insurance Specialist Applications Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate and

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION 30 April 2015 (am) Subject SA2 Life Insurance Specialist Applications Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate and

SBI LIFE -PRODUCT FEATURES

SBI LIFE -PRODUCT FEATURES KEYMAN INSURANCE Why a keyman policy? Person covered Min. & Max. at entry Maximum Cover Age Minimum Term To protect the Corporate against the financial consequences due to the

SBI LIFE -PRODUCT FEATURES KEYMAN INSURANCE Why a keyman policy? Person covered Min. & Max. at entry Maximum Cover Age Minimum Term To protect the Corporate against the financial consequences due to the

Manual for SOA Exam MLC.

Chapter 6. Benefit premiums. Extract from: Arcones Fall 2010 Edition, available at http://www.actexmadriver.com/ 1/77 Fully discrete benefit premiums In this section, we will consider the funding of insurance

Chapter 6. Benefit premiums. Extract from: Arcones Fall 2010 Edition, available at http://www.actexmadriver.com/ 1/77 Fully discrete benefit premiums In this section, we will consider the funding of insurance

November 2012 Course MLC Examination, Problem No. 1 For two lives, (80) and (90), with independent future lifetimes, you are given: k p 80+k

and (90), with independent future lifetimes, you are given: k p 80+k") Solutions to the November 202 Course MLC Examination by Krzysztof Ostaszewski, http://www.krzysio.net, [email protected] Copyright 202 by Krzysztof Ostaszewski All rights reserved. No reproduction in

Solutions to the November 202 Course MLC Examination by Krzysztof Ostaszewski, http://www.krzysio.net, [email protected] Copyright 202 by Krzysztof Ostaszewski All rights reserved. No reproduction in

ACTUARIAL MATHEMATICS FOR LIFE CONTINGENT RISKS

ACTUARIAL MATHEMATICS FOR LIFE CONTINGENT RISKS DAVID C. M. DICKSON University of Melbourne MARY R. HARDY University of Waterloo, Ontario V HOWARD R. WATERS Heriot-Watt University, Edinburgh CAMBRIDGE

ACTUARIAL MATHEMATICS FOR LIFE CONTINGENT RISKS DAVID C. M. DICKSON University of Melbourne MARY R. HARDY University of Waterloo, Ontario V HOWARD R. WATERS Heriot-Watt University, Edinburgh CAMBRIDGE

Rule 9 On Prescribing Reserve Requirements of Insurance Companies

Banking and Payments Authority of Kosovo Pursuant to the authority given under Section 17.b of UNMIK Regulation No. 2001/24 date of October 1, 2001 on Amending UNMIK Regulation No. 1999/20, on Banking

Banking and Payments Authority of Kosovo Pursuant to the authority given under Section 17.b of UNMIK Regulation No. 2001/24 date of October 1, 2001 on Amending UNMIK Regulation No. 1999/20, on Banking

Annuities and decumulation phase of retirement. Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA

Annuities and decumulation phase of retirement Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA CASH LUMP SUM AT RETIREMENT CASH INSTEAD OF PENSION > popular with pension scheme members

Annuities and decumulation phase of retirement Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA CASH LUMP SUM AT RETIREMENT CASH INSTEAD OF PENSION > popular with pension scheme members

Chapter 9 Experience rating

0 INTRODUCTION 1 Chapter 9 Experience rating 0 Introduction The rating process is the process of deciding on an appropriate level of premium for a particular class of insurance business. The contents of

0 INTRODUCTION 1 Chapter 9 Experience rating 0 Introduction The rating process is the process of deciding on an appropriate level of premium for a particular class of insurance business. The contents of

- LIFE INSURANCE CORPORATION OF INDIA CENTRAL OFFICE. Dept.: Product Development Jeevan Bima Marg, Mumbai 400 021

- LIFE INSURANCE CORPORATION OF INDIA CENTRAL OFFICE Dept.: Product Development Yogakshema, Jeevan Bima Marg, Mumbai 400 021 Ref: CO/PD/66 3 rd March, 2015 All HODs of Central Office All Zonal Offices

- LIFE INSURANCE CORPORATION OF INDIA CENTRAL OFFICE Dept.: Product Development Yogakshema, Jeevan Bima Marg, Mumbai 400 021 Ref: CO/PD/66 3 rd March, 2015 All HODs of Central Office All Zonal Offices

Premium calculation. summer semester 2013/2014. Technical University of Ostrava Faculty of Economics department of Finance

Technical University of Ostrava Faculty of Economics department of Finance summer semester 2013/2014 Content 1 Fundamentals Insurer s expenses 2 Equivalence principles Calculation principles 3 Equivalence

Technical University of Ostrava Faculty of Economics department of Finance summer semester 2013/2014 Content 1 Fundamentals Insurer s expenses 2 Equivalence principles Calculation principles 3 Equivalence

HOW WE MANAGE THE PHOENIX LIFE LIMITED SPI WITH-PROFITS FUND

HOW WE MANAGE THE PHOENIX LIFE LIMITED SPI WITH-PROFITS FUND A guide for trustees with Simplified Pension Investment deposit administration policies invested in this fund The aims of this guide The guide

HOW WE MANAGE THE PHOENIX LIFE LIMITED SPI WITH-PROFITS FUND A guide for trustees with Simplified Pension Investment deposit administration policies invested in this fund The aims of this guide The guide

A chapter on Valuation basis covering the following minimum criteria should also be displayed on the web-site of the Insurers.

L-42 42- Valuation Basis (Life Insurance) A chapter on Valuation basis covering the following minimum criteria should also be displayed on the web-site of the Insurers. Data The company maintains the Policy

L-42 42- Valuation Basis (Life Insurance) A chapter on Valuation basis covering the following minimum criteria should also be displayed on the web-site of the Insurers. Data The company maintains the Policy

Life Assurance (Provision of Information) Regulations, 2001

Regulations, 2001") ACTUARIAL STANDARD OF PRACTICE LA-8 LIFE ASSURANCE PRODUCT INFORMATION Classification Mandatory MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE CODE OF PROFESSIONAL CONDUCT AND THAT ACTUARIAL

ACTUARIAL STANDARD OF PRACTICE LA-8 LIFE ASSURANCE PRODUCT INFORMATION Classification Mandatory MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE CODE OF PROFESSIONAL CONDUCT AND THAT ACTUARIAL

MATH 3630 Actuarial Mathematics I Class Test 2 Wednesday, 17 November 2010 Time Allowed: 1 hour Total Marks: 100 points

MATH 3630 Actuarial Mathematics I Class Test 2 Wednesday, 17 November 2010 Time Allowed: 1 hour Total Marks: 100 points Please write your name and student number at the spaces provided: Name: Student ID:

MATH 3630 Actuarial Mathematics I Class Test 2 Wednesday, 17 November 2010 Time Allowed: 1 hour Total Marks: 100 points Please write your name and student number at the spaces provided: Name: Student ID:

SOCIETY OF ACTUARIES. EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE QUESTIONS

SOCIETY OF ACTUARIES EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE QUESTIONS The following questions or solutions have been modified since this document was prepared to use with the syllabus effective

SOCIETY OF ACTUARIES EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE QUESTIONS The following questions or solutions have been modified since this document was prepared to use with the syllabus effective

Abbey Life Assurance Company Limited Participating Business Fund

Abbey Life Assurance Company Limited Participating Business Fund Principles and of Financial Management (PPFM) 1 General... 2 1.1 Introduction... 2 1.2 The With-Profits Policies... 2 2 Structure of these

Abbey Life Assurance Company Limited Participating Business Fund Principles and of Financial Management (PPFM) 1 General... 2 1.1 Introduction... 2 1.2 The With-Profits Policies... 2 2 Structure of these

2 Policy Values and Reserves

2 Policy Values and Reserves [Handout to accompany this section: reprint of Life Insurance, from The Encyclopaedia of Actuarial Science, John Wiley, Chichester, 2004.] 2.1 The Life Office s Balance Sheet

2 Policy Values and Reserves [Handout to accompany this section: reprint of Life Insurance, from The Encyclopaedia of Actuarial Science, John Wiley, Chichester, 2004.] 2.1 The Life Office s Balance Sheet

TABLE OF CONTENTS. GENERAL AND HISTORICAL PREFACE iii SIXTH EDITION PREFACE v PART ONE: REVIEW AND BACKGROUND MATERIAL

TABLE OF CONTENTS GENERAL AND HISTORICAL PREFACE iii SIXTH EDITION PREFACE v PART ONE: REVIEW AND BACKGROUND MATERIAL CHAPTER ONE: REVIEW OF INTEREST THEORY 3 1.1 Interest Measures 3 1.2 Level Annuity

TABLE OF CONTENTS GENERAL AND HISTORICAL PREFACE iii SIXTH EDITION PREFACE v PART ONE: REVIEW AND BACKGROUND MATERIAL CHAPTER ONE: REVIEW OF INTEREST THEORY 3 1.1 Interest Measures 3 1.2 Level Annuity

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014

Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014") Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial year from 1 January 2014 to 31 December 2014

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial year from 1 January 2014 to 31 December 2014

Premium Calculation - continued

Premium Calculation - continued Lecture: Weeks 1-2 Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring 2015 - Valdez 1 / 16 Recall some preliminaries Recall some preliminaries An insurance policy (life

Premium Calculation - continued Lecture: Weeks 1-2 Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring 2015 - Valdez 1 / 16 Recall some preliminaries Recall some preliminaries An insurance policy (life

A chapter on Valuation basis covering the following minimum criteria should also be displayed on the web-site of the Insurers.

L-42 42- Valuation Basis (Life Insurance) A chapter on Valuation basis covering the following minimum criteria should also be displayed on the web-site of the Insurers. Data The company maintains the Policy

L-42 42- Valuation Basis (Life Insurance) A chapter on Valuation basis covering the following minimum criteria should also be displayed on the web-site of the Insurers. Data The company maintains the Policy

NEDGROUP LIFE FINANCIAL MANAGEMENT PRINCIPLES AND PRACTICES OF ASSURANCE COMPANY LIMITED. A member of the Nedbank group

NEDGROUP LIFE ASSURANCE COMPANY LIMITED PRINCIPLES AND PRACTICES OF FINANCIAL MANAGEMENT A member of the Nedbank group We subscribe to the Code of Banking Practice of The Banking Association South Africa

NEDGROUP LIFE ASSURANCE COMPANY LIMITED PRINCIPLES AND PRACTICES OF FINANCIAL MANAGEMENT A member of the Nedbank group We subscribe to the Code of Banking Practice of The Banking Association South Africa

INSTRUCTIONS TO CANDIDATES

Society of Actuaries Canadian Institute of Actuaries Exam MLC Models for Life Contingencies Friday, October 31, 2014 8:30 a.m. 12:45 p.m. MLC General Instructions 1. Write your candidate number here. Your

Society of Actuaries Canadian Institute of Actuaries Exam MLC Models for Life Contingencies Friday, October 31, 2014 8:30 a.m. 12:45 p.m. MLC General Instructions 1. Write your candidate number here. Your

Actuarial Report. On the Proposed Transfer of the Life Insurance Business from. Asteron Life Limited. Suncorp Life & Superannuation Limited

Actuarial Report On the Proposed Transfer of the Life Insurance Business from Asteron Life Limited to Suncorp Life & Superannuation Limited Actuarial Report Page 1 of 47 1. Executive Summary 1.1 Background

Actuarial Report On the Proposed Transfer of the Life Insurance Business from Asteron Life Limited to Suncorp Life & Superannuation Limited Actuarial Report Page 1 of 47 1. Executive Summary 1.1 Background

4. Life Insurance. 4.1 Survival Distribution And Life Tables. Introduction. X, Age-at-death. T (x), time-until-death

, time-until-death") 4. Life Insurance 4.1 Survival Distribution And Life Tables Introduction X, Age-at-death T (x), time-until-death Life Table Engineers use life tables to study the reliability of complex mechanical and

4. Life Insurance 4.1 Survival Distribution And Life Tables Introduction X, Age-at-death T (x), time-until-death Life Table Engineers use life tables to study the reliability of complex mechanical and

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013

Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013") Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial period from 1 January 2013 to 31 December 2013

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial period from 1 January 2013 to 31 December 2013

> How does our With-Profits Fund work? > What are bonuses? > How are regular bonuses worked out?

Your With-Profits Plan a guide to how we manage the Fund Conventional With-Profits Plans originally issued by Scottish Amicable Life Assurance Society (SALAS) Your With-Profits Plan is a medium to long-term

Your With-Profits Plan a guide to how we manage the Fund Conventional With-Profits Plans originally issued by Scottish Amicable Life Assurance Society (SALAS) Your With-Profits Plan is a medium to long-term

GLOSSARY. A contract that provides for periodic payments to an annuitant for a specified period of time, often until the annuitant s death.

The glossary contains explanations of certain terms and definitions used in this prospectus in connection with us and our business. The terms and their meanings may not correspond to standard industry

The glossary contains explanations of certain terms and definitions used in this prospectus in connection with us and our business. The terms and their meanings may not correspond to standard industry

Featured article: Evaluating the Cost of Longevity in Variable Annuity Living Benefits

Featured article: Evaluating the Cost of Longevity in Variable Annuity Living Benefits By Stuart Silverman and Dan Theodore This is a follow-up to a previous article Considering the Cost of Longevity Volatility

Featured article: Evaluating the Cost of Longevity in Variable Annuity Living Benefits By Stuart Silverman and Dan Theodore This is a follow-up to a previous article Considering the Cost of Longevity Volatility

How To Value Royal Life With Profits

Bonus Rates Royal London - Life Business Regular Bonus Rates: Regular Premium Single Premium 0.5% 0.5% 2011 0.5% 0.5% For policies taken out after 2004 the regular bonus rates are greater than 0.5% Final

Bonus Rates Royal London - Life Business Regular Bonus Rates: Regular Premium Single Premium 0.5% 0.5% 2011 0.5% 0.5% For policies taken out after 2004 the regular bonus rates are greater than 0.5% Final

SURRENDER VALUE AND PAID-UP VALUE STANDARD FOR LIFE INSURANCE

Actuarial Society of Malaysia (ASM) SURRENDER VALUE AND PAID-UP VALUE STANDARD FOR LIFE INSURANCE Prepared by: Life Insurance Sub-Committee of Actuarial Society of Malaysia TABLE OF CONTENTS CONTENTS PAGE

Actuarial Society of Malaysia (ASM) SURRENDER VALUE AND PAID-UP VALUE STANDARD FOR LIFE INSURANCE Prepared by: Life Insurance Sub-Committee of Actuarial Society of Malaysia TABLE OF CONTENTS CONTENTS PAGE

Standard Life Assurance Limited OCTOBER 2013. Principles and Practices of Financial Management for the Heritage With Profits Fund

Standard Life Assurance Limited OCTOBER 2013 Principles and Practices of Financial Management for the Heritage With Profits Fund Preface... 3 Background to the Principles and Practices of Financial Management...

Standard Life Assurance Limited OCTOBER 2013 Principles and Practices of Financial Management for the Heritage With Profits Fund Preface... 3 Background to the Principles and Practices of Financial Management...

Taxation of Life Insurance Companies

Taxation of Life Insurance Companies Taxation of Life Insurance Companies R. Ramakrishnan Consultant Actuary [email protected] Section 1 : Basis of Assessment 1.1) The total salary earned during a

Taxation of Life Insurance Companies Taxation of Life Insurance Companies R. Ramakrishnan Consultant Actuary [email protected] Section 1 : Basis of Assessment 1.1) The total salary earned during a

MONEY BACK PLANS. For the year 2004-05 the two rates of investment return declared by the Life Insurance Council are 6% and 10% per annum.

MONEY BACK PLANS 1. Money Back with Profit Unlike ordinary endowment insurance plans where the survival benefits are payable only at the end of the endowment period, this scheme provides for periodic payments

MONEY BACK PLANS 1. Money Back with Profit Unlike ordinary endowment insurance plans where the survival benefits are payable only at the end of the endowment period, this scheme provides for periodic payments

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 15 th November 2010 Subject CT1 Financial Mathematics Time allowed: Three Hours (15.00 18.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1. Please

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 15 th November 2010 Subject CT1 Financial Mathematics Time allowed: Three Hours (15.00 18.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1. Please

How To Get A Health Insurance Plan In Munich

L-42- Valuation Basis (Life Insurance - Individual ) A chapter on Valuation basis covering the following minimum criteria should also be displayed on the web-site of the Insurers. a. How the policy data

L-42- Valuation Basis (Life Insurance - Individual ) A chapter on Valuation basis covering the following minimum criteria should also be displayed on the web-site of the Insurers. a. How the policy data

LIFE INSURANCE AND PENSIONS by Peter Tryfos York University

LIFE INSURANCE AND PENSIONS by Peter Tryfos York University Introduction Life insurance is the business of insuring human life: in return for a premium payable in one sum or installments, an insurance

LIFE INSURANCE AND PENSIONS by Peter Tryfos York University Introduction Life insurance is the business of insuring human life: in return for a premium payable in one sum or installments, an insurance

A Primer for Calculating the Swiss Solvency Test Cost of Capital for a Market Value Margin

A Primer for Calculating the Swiss Solvency Test Cost of Capital for a Market Value Margin 26. April 2006 Philipp Keller Federal Office of Private Insurance [email protected] 1. Introduction

A Primer for Calculating the Swiss Solvency Test Cost of Capital for a Market Value Margin 26. April 2006 Philipp Keller Federal Office of Private Insurance [email protected] 1. Introduction

Valuation Report on Prudential Annuities Limited as at 31 December 2003. The investigation relates to 31 December 2003.

PRUDENTIAL ANNUITIES LIMITED Returns for the year ended 31 December 2003 SCHEDULE 4 Valuation Report on Prudential Annuities Limited as at 31 December 2003 1. Date of investigation The investigation relates

PRUDENTIAL ANNUITIES LIMITED Returns for the year ended 31 December 2003 SCHEDULE 4 Valuation Report on Prudential Annuities Limited as at 31 December 2003 1. Date of investigation The investigation relates

Accounting of Long Term Employee Benefits context and perspective

Accounting of Long Term Employee Benefits context and perspective By S. N. Bhattacharya Abstract : The latest revision of the Indian Accounting Standard of employee benefits (AS 15 revised 2005) has brought

Accounting of Long Term Employee Benefits context and perspective By S. N. Bhattacharya Abstract : The latest revision of the Indian Accounting Standard of employee benefits (AS 15 revised 2005) has brought

Insurance Benefits. Lecture: Weeks 6-8. Lecture: Weeks 6-8 (STT 455) Insurance Benefits Fall 2014 - Valdez 1 / 36

Insurance Benefits Fall 2014 - Valdez 1 / 36") Insurance Benefits Lecture: Weeks 6-8 Lecture: Weeks 6-8 (STT 455) Insurance Benefits Fall 2014 - Valdez 1 / 36 An introduction An introduction Central theme: to quantify the value today of a (random)

Insurance Benefits Lecture: Weeks 6-8 Lecture: Weeks 6-8 (STT 455) Insurance Benefits Fall 2014 - Valdez 1 / 36 An introduction An introduction Central theme: to quantify the value today of a (random)

LIFE INSURANCE. and INVESTMENT

INVESTMENT SAVINGS & INSURANCE ASSOCIATION OF NZ INC GLOSSARY OF LIFE INSURANCE and INVESTMENT TERMS 2 Accident Benefit A benefit payable should death occur as the result of an accident. It may be a stand-alone

INVESTMENT SAVINGS & INSURANCE ASSOCIATION OF NZ INC GLOSSARY OF LIFE INSURANCE and INVESTMENT TERMS 2 Accident Benefit A benefit payable should death occur as the result of an accident. It may be a stand-alone

Sanlam Life Insurance Limited Principles and Practices of Financial Management (PPFM) for Sanlam Life Participating Annuity Products

for Sanlam Life Participating Annuity Products") Sanlam Life Insurance Limited Principles and Practices of Financial Management (PPFM) for Sanlam Life Participating Annuity Products Table of Contents Section 1 - Information 1.1 Background 2 1.2 Purpose

Sanlam Life Insurance Limited Principles and Practices of Financial Management (PPFM) for Sanlam Life Participating Annuity Products Table of Contents Section 1 - Information 1.1 Background 2 1.2 Purpose

LIA Guidelines on Benefit Illustrations

LIA Guidelines on Benefit Illustrations CONTENTS 1 Purpose 2 Basis for illustrating policy benefits 3 Basis for illustrating policy charges 4 Format of main benefit illustrations 5 Other requirements on

LIA Guidelines on Benefit Illustrations CONTENTS 1 Purpose 2 Basis for illustrating policy benefits 3 Basis for illustrating policy charges 4 Format of main benefit illustrations 5 Other requirements on

Institute of Actuaries of India

Institute of Actuaries of India Liyaquat Khan November 22, 2003 President To, All fellow members, Dear All, Re: Actuarial Practice Standard 12 (APS 12) - Investigations of Retirement Benefit Schemes: Choice

Institute of Actuaries of India Liyaquat Khan November 22, 2003 President To, All fellow members, Dear All, Re: Actuarial Practice Standard 12 (APS 12) - Investigations of Retirement Benefit Schemes: Choice

Case Study Modeling Longevity Risk for Solvency II

Case Study Modeling Longevity Risk for Solvency II September 8, 2012 Longevity 8 Conference Waterloo, Ontario Presented by Stuart Silverman Principal & Consulting Actuary Background SOLVENCY II New Minimum

Case Study Modeling Longevity Risk for Solvency II September 8, 2012 Longevity 8 Conference Waterloo, Ontario Presented by Stuart Silverman Principal & Consulting Actuary Background SOLVENCY II New Minimum

HOW WE MANAGE THE PHOENIX LIFE LIMITED PHOENIX WITH-PROFITS FUND

HOW WE MANAGE THE PHOENIX LIFE LIMITED PHOENIX WITH-PROFITS FUND A guide for policyholders with unitised with-profits policies (except for Profit Plus Fund policies) invested in this fund The aims of this

HOW WE MANAGE THE PHOENIX LIFE LIMITED PHOENIX WITH-PROFITS FUND A guide for policyholders with unitised with-profits policies (except for Profit Plus Fund policies) invested in this fund The aims of this

Longevity risk. What do South African and UK retirement frameworks have in common??

Longevity risk Over the past 50 years life expectancy in the UK has increased by up to 10 years Longevity is the result of a complex interaction of various factors such as increased prosperity, changes

Longevity risk Over the past 50 years life expectancy in the UK has increased by up to 10 years Longevity is the result of a complex interaction of various factors such as increased prosperity, changes

Principles and Practices Of Financial Management

Principles and Practices Of Financial Management Wesleyan Assurance Society (Open Fund) Effective from 1 August 2008 Wesleyan Assurance Society Head Office: Colmore Circus, Birmingham B4 6AR Telephone:

Principles and Practices Of Financial Management Wesleyan Assurance Society (Open Fund) Effective from 1 August 2008 Wesleyan Assurance Society Head Office: Colmore Circus, Birmingham B4 6AR Telephone:

GUIDELINES CONTINGENCY PLAN FOR INSURERS

GUIDELINES ON CONTINGENCY PLAN FOR INSURERS (Issued under section 7 (1) (a) of the Financial Services Act 2007 and section 130 of the Insurance Act 2005) February 2008 1 1. INTRODUCTION 1.1. The Insurance

GUIDELINES ON CONTINGENCY PLAN FOR INSURERS (Issued under section 7 (1) (a) of the Financial Services Act 2007 and section 130 of the Insurance Act 2005) February 2008 1 1. INTRODUCTION 1.1. The Insurance

LIC S KOMAL JEEVAN VS. ICICI S SMART KID & TATA AIG S MAHALIFE JR.

38 THE JOURNAL A COMPARATIVE ANALYSIS : LIC S KOMAL JEEVAN VS. ICICI S SMART KID & TATA AIG S MAHALIFE JR. By: Shri Sekhar Chandra Sahoo Manager (Sales), MDO-1, Mumbai. L Life s aspirations come in the

38 THE JOURNAL A COMPARATIVE ANALYSIS : LIC S KOMAL JEEVAN VS. ICICI S SMART KID & TATA AIG S MAHALIFE JR. By: Shri Sekhar Chandra Sahoo Manager (Sales), MDO-1, Mumbai. L Life s aspirations come in the

6 th GLOBAL CONFERENCE OF ACTUARIES 18 19 February, 2004, New Delhi. By Walter de Oude. (Subject Code 01 Subject Group : Life Insurance)

") 6 th GLOBAL CONFERENCE OF ACTUARIES 18 19 February, 2004, New Delhi By Walter de Oude (Subject Code 01 Subject Group : Life Insurance) 1 Cashflow Pricing Walter de Oude 5th GCA Feb 2004 Cashflow pricing

6 th GLOBAL CONFERENCE OF ACTUARIES 18 19 February, 2004, New Delhi By Walter de Oude (Subject Code 01 Subject Group : Life Insurance) 1 Cashflow Pricing Walter de Oude 5th GCA Feb 2004 Cashflow pricing

GLOSSARY. A contract that provides for periodic payments to an annuitant for a specified period of time, often until the annuitant s death.

The glossary contains explanations of certain terms and definitions used in this prospectus in connection with the Group and its business. The terms and their meanings may not correspond to standard industry

The glossary contains explanations of certain terms and definitions used in this prospectus in connection with the Group and its business. The terms and their meanings may not correspond to standard industry

Manual for SOA Exam MLC.

Chapter 6. Benefit premiums Extract from: Arcones Fall 2010 Edition, available at http://www.actexmadriver.com/ 1/90 (#4, Exam M, Spring 2005) For a fully discrete whole life insurance of 100,000 on (35)

Chapter 6. Benefit premiums Extract from: Arcones Fall 2010 Edition, available at http://www.actexmadriver.com/ 1/90 (#4, Exam M, Spring 2005) For a fully discrete whole life insurance of 100,000 on (35)

Practice Exam 1. x l x d x 50 1000 20 51 52 35 53 37

Practice Eam. You are given: (i) The following life table. (ii) 2q 52.758. l d 5 2 5 52 35 53 37 Determine d 5. (A) 2 (B) 2 (C) 22 (D) 24 (E) 26 2. For a Continuing Care Retirement Community, you are given

Practice Eam. You are given: (i) The following life table. (ii) 2q 52.758. l d 5 2 5 52 35 53 37 Determine d 5. (A) 2 (B) 2 (C) 22 (D) 24 (E) 26 2. For a Continuing Care Retirement Community, you are given

Start small. Save big.

Start small. Save big. PRODUCT BROCHURE A long term savings plan with bonuses, guaranteed additions and insurance protection* *Terms and Conditions apply. Your life is full of responsibilities. As a responsible

Start small. Save big. PRODUCT BROCHURE A long term savings plan with bonuses, guaranteed additions and insurance protection* *Terms and Conditions apply. Your life is full of responsibilities. As a responsible

Basics of Corporate Pension Plan Funding

Basics of Corporate Pension Plan Funding A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all figures are based in USD. 1 Introduction In general, a pension plan is a promise

Basics of Corporate Pension Plan Funding A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all figures are based in USD. 1 Introduction In general, a pension plan is a promise

Institute of Actuaries of India

Institute of Actuaries of India INDICATIVE SOLUTION May 2012 Examination Subject SA2 Life Insurance Introduction The indicative solution has been written by the Examiners with the aim of helping candidates.

Institute of Actuaries of India INDICATIVE SOLUTION May 2012 Examination Subject SA2 Life Insurance Introduction The indicative solution has been written by the Examiners with the aim of helping candidates.

Happily Ever After. Enjoy Guaranteed Income Even After Your Retirement.

Happily Ever After. Enjoy Guaranteed Income Even After Your Retirement. Exide Life New Immediate Annuity with Return of Purchase Price Lifelong Annuity Payouts Guaranteed for Life Flexible Payout Options

Happily Ever After. Enjoy Guaranteed Income Even After Your Retirement. Exide Life New Immediate Annuity with Return of Purchase Price Lifelong Annuity Payouts Guaranteed for Life Flexible Payout Options

Windsor Life Assurance Company Limited. Windsor Life With-Profit Fund. Principles and Practices of Financial Management

Windsor Life Assurance Company Limited Windsor Life With-Profit Fund Principles and Practices of Financial Management July 2011 Registered in England No. 754167. Registered Office: Windsor House, Telford

Windsor Life Assurance Company Limited Windsor Life With-Profit Fund Principles and Practices of Financial Management July 2011 Registered in England No. 754167. Registered Office: Windsor House, Telford

EXAMINATION. 22 April 2010 (pm) Subject ST2 Life Insurance Specialist Technical. Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE

Subject ST2 Life Insurance Specialist Technical. Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE") Faculty of Actuaries Institute of Actuaries EXAMINATION 22 April 2010 (pm) Subject ST2 Life Insurance Specialist Technical Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate

Faculty of Actuaries Institute of Actuaries EXAMINATION 22 April 2010 (pm) Subject ST2 Life Insurance Specialist Technical Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate

Your With-Profits Plan a guide to how we manage the Fund Prudential Conventional With-Profits Plans

Your With-Profits Plan a guide to how we manage the Fund Prudential Conventional With-Profits Plans Your With-Profits Plan is a medium to long-term investment that: > combines your money with money from

Your With-Profits Plan a guide to how we manage the Fund Prudential Conventional With-Profits Plans Your With-Profits Plan is a medium to long-term investment that: > combines your money with money from