Premium Calculation - continued

|

|

|

- Stephen Bryan

- 8 years ago

- Views:

Transcription

1 Premium Calculation - continued Lecture: Weeks 1-2 Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 1 / 16

2 Recall some preliminaries Recall some preliminaries An insurance policy (life insurance or life annuity) is funded by contract premiums: once (single premium) made usually at time of policy issue, or a series of payments (usually contingent on survival of policyholder) with first payment made at policy issue to cover for the benefits, expenses associated with initiating/maintaining contract, profit margins, and deviations due to adverse experience. Net premiums (or sometimes called benefit premiums) considers only the benefits provided nothing allocated to pay for expenses, profit or contingency margins Gross premiums (or sometimes called expense-loaded premiums) covers the benefits and includes expenses, profits, and contingency margins Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 2 / 16

considers only the benefits provided nothing allocated to pay for expenses, profit or contingency margins Gross premiums (or sometimes called")

3 Recall some preliminaries Chapter summary - continued Present value of future loss (negative profit) random variable Premium principles the equivalence principle (or actuarial equivalence principle) portfolio percentile premiums Return of premium policies Substandard risks Chapter 6 (sections 6.8, 6.9) of Dickson, et al. Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 3 / 16

of Dickson, et al.")

4 net random future loss Net random future loss An insurance contract is an agreement between two parties: the insurer agrees to pay for insurance benefits; in exchange for insurance premiums to be paid by the insured. The insurer s net random future loss is defined by L n 0 = PVFB 0 PVFP 0. where PVFB 0 is the present value, at time of issue, of future benefits to be paid by the insurer and PVFP 0 is the present value, at time of issue, of future premiums to be paid by the insured. Note: this is also called the present value of future loss random variable (in the book), and if no confusion, we may simply write this as L 0. Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 4 / 16

, and if no confusion, we may simply write this as L 0.")

5 net random future loss equivalence principle The principle of equivalence The net premium, generically denoted by P, may be determined according to the principle of equivalence by setting E [ L n 0 ] = 0. The expected value of the insurer s net random future loss is zero. This is then equivalent to setting E [ PVFB 0 ] = E [ PVFP0 ]. In other words, at issue, we have APV(Future Premiums) = APV(Future Benefits). Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 5 / 16

6 net random future loss gross premiums Gross premium calculations Treat expenses as if they are a part of benefits. The gross random future loss at issue is defined by L g 0 = PVFB 0 + PVFE 0 PVFP 0, where PVFE 0 is the present value random variable associated with future expenses incurred by the insurer. The gross premium, generically denoted by G, may be determined according to the principle of equivalence by setting E [ L g 0] = 0. This is equivalent to setting E [ PVFB 0 ] + E [ PVFE0 ] = E [ PVFP0 ]. In other words, at issue, we have APV(FP 0 ) = APV(FB 0 ) + APV(FE 0 ). Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 6 / 16

![expenses incurred by the insurer. The gross premium, generically denoted by G, may be determined according to the principle of equivalence by setting E [ L g 0] = 0.](/docs-images/42/15043488/images/page_6.jpg "This is equivalent to setting E [ PVFB 0 ] + E [ PVFE0 ] = E [ PVFP0 ]. In other words, at issue, we have APV(FP 0 ) = APV(FB 0 ) + APV(FE 0 ).")

7

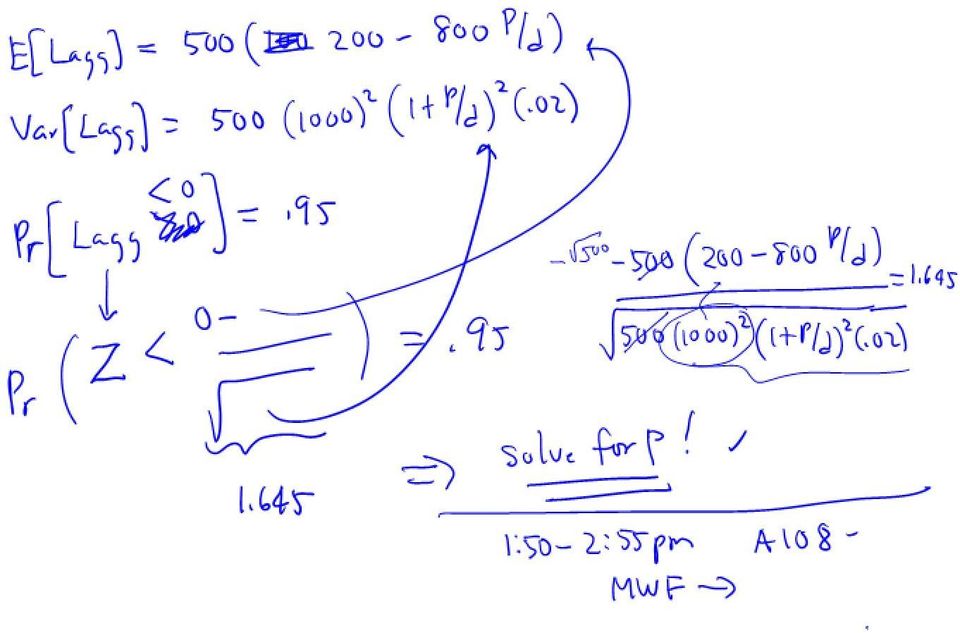

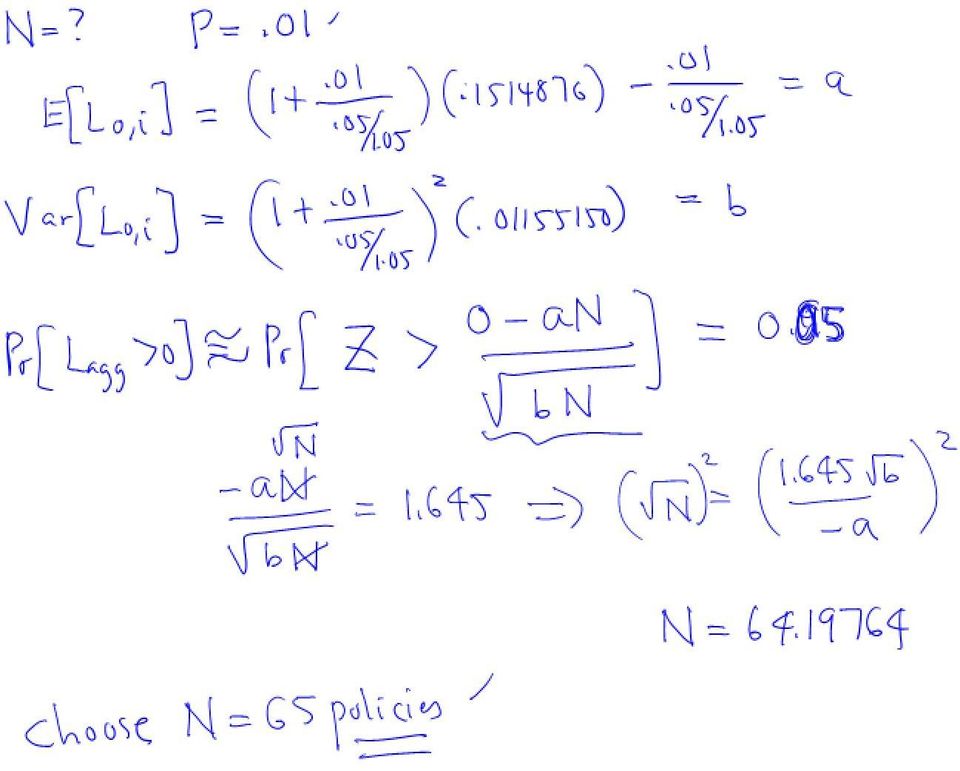

8 Portfolio percentile premiums Portfolio percentile premium principle Suppose insurer issues a portfolio of N identical and independent policies where the PV of loss-at-issue for the i-th policy is L 0,1. The total portfolio (aggregate) future loss is then defined by Its expected value is therefore L agg = L 0,1 + L 0,2 + + L 0,N = N i=1 L 0,i N E[L agg ] = E [ ] L 0,i i=1 and, by independence, the variance is Var[L agg ] = N Var [ ] L 0,i. i=1 Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 7 / 16

9 Portfolio percentile premiums - continued Portfolio percentile premium principle The portfolio percentile premium principle sets the premium P so that there is a probability, say α with 0 < α < 1, of a positive gain from the portfolio. In other words, we set P so that Pr[L agg < 0] = α. Note that loss could include expenses. Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 8 / 16

![1, of a positive gain from the portfolio. In other words, we set P so that Pr[L agg < 0] = α.](/docs-images/42/15043488/images/page_9.jpg "Note that loss could include expenses.")

10

11

12

13

14 Portfolio percentile premiums - continued Example 6.12 Consider Example Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 9 / 16

Premium")

15

16

17 Portfolio percentile premiums illustrative example Illustrative example 1 An insurer sells 100 fully discrete whole life insurance policies of $1, each of the same age 45. You are given: All policies have independent future lifetimes. i = 5% ä 45 = Using the Normal approximation: 1 Calculate the annual contract premium according to the portfolio percentile premium principle with α = Suppose the annual contract premium is set at 0.01 per policy. Determine the smallest number of policies to be sold so that the insurer has at least a 95% probability of a gain from this portfolio of policies. Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 10 / 16

18

19

20 return of premium Return of premium policies Consider a fully discrete whole life insurance to (x) with benefit equal to $B plus return of all premiums accumulated with interest at rate j. The net random future loss in this case can be expressed as L 0 = P s K+1 j v K+1 + B v K+1 P ä K+1, for K = 0, 1,... and s K+1 j is calculated at rate j. All other actuarial functions are calculated at rate i. Consider the following cases: Let j = 0. This implies s K+1 j = (K + 1) and the annual benefit premium will be B A x P =. ä x (IA) x Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 11 / 16

and the annual benefit premium will be B A x P =.")

21

22

23

24

25

26 return of premium - continued - continued Let i = j. In this case, the loss L 0 = B v K+1 because s K+1 j v K+1 = ä K+1. Thus, there is no possible premium because all premiums are returned and yet there is an additional benefit of $B. Let i < j. Then we have L 0 = P ( s K+1 j s K+1 ) v K+1 + B v K+1, which is always positive because s K+1 j > s K+1 when i < j. No possible premium. Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 12 / 16

27 return of premium - continued - continued Let i > j. Then we can write the loss as L 0 = P vk+1 j vk+1 d j + B v K+1 P ä K+1 where d j = 1 [1/(1 + j)] and v j is the corresponding discount rate associated with interest rate j = [(1 + i)/(1 + j)] 1. Here, P = A x ä x (Ax), j Ax d j where (A x ) j is a (discrete) whole life insurance to (x) evaluated at interest rate j. Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 13 / 16

40 = 8.6179 i = 4% Calculate ä 40.")

28 return of premium illustrative examples Illustrative example 2 For a whole life insurance on (40), you are given: Death benefit, payable at the end of the year of death, is equal to $10,000 plus the return of all premiums paid without interest. Annual benefit premium of is payable at the beginning of each year. (IA) 40 = i = 4% Calculate ä 40. Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 14 / 16

29

30 return of premium illustrative examples SOA Question #22 Consider Question #22 from Fall 2012 SOA MLC Exam: You are given the following information about a special fully discrete 2-payment, 2-year term insurance on (80): Mortality follows the Illustrative Life Table. i = The death benefit is 1000 plus a return of all premiums paid without interest. Level premiums are calculated using the equivalence principle. Calculate the benefit premium for this special insurance. For practice: try calculating the benefit premium if the return of all premiums paid comes with an interest of say Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 15 / 16

31

32

33 substandard risks Pricing with extra or substandard risks An impaired individual, or one who suffers from a medical condition, may still be offered an insurance policy but at a rate higher than that of a standard risk. Generally there are three possible approaches: age rating: calculate the premium with the individual at an older age constant addition to the force of mortality: µ s x+t = µ x+t + φ, for φ > 0 constant multiple of mortality rates: q s x+t = min (cq x+t, 1), for c > 1 Read Section 6.9. Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 16 / 18

34

35 substandard risks illustrative example Published SOA question #45 Your company is competing to sell a life annuity-due with an APV of $500,000 to a 50-year-old individual. Based on your company s experience, typical 50-year-old annuitants have a complete life expectancy of 25 years. However, this individual is not as healthy as your company s typical annuitant, and your medical experts estimate that his complete life expectancy is only 15 years. You decide to price the benefit using the issue age that produces a complete life expectancy of 15 years. You also assume: For typical annuitants of all ages, l x = 100(ω x), for 0 x ω. i = 0.06 Calculate the annual benefit premium that your company can offer to this individual. Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 17 / 18

36

37

38 Other terminologies Other terminologies and notations used Expression net random future loss L 0 net premium gross premium equivalence principle Other terms/symbols used loss at issue 0 L benefit premium expense-loaded premium actuarial equivalence principle generic premium G P π substandard may be superscripted with * or s Lecture: Weeks 1-2 (STT 456) Premium Calculation Spring Valdez 16 / 16

Premium Calculation. Lecture: Weeks 12-14. Lecture: Weeks 12-14 (Math 3630) Annuities Fall 2015 - Valdez 1 / 32

Annuities Fall 2015 - Valdez 1 / 32") Premium Calculation Lecture: Weeks 12-14 Lecture: Weeks 12-14 (Math 3630) Annuities Fall 2015 - Valdez 1 / 32 Preliminaries Preliminaries An insurance policy (life insurance or life annuity) is funded

Premium Calculation Lecture: Weeks 12-14 Lecture: Weeks 12-14 (Math 3630) Annuities Fall 2015 - Valdez 1 / 32 Preliminaries Preliminaries An insurance policy (life insurance or life annuity) is funded

Premium Calculation. Lecture: Weeks 12-14. Lecture: Weeks 12-14 (STT 455) Premium Calculation Fall 2014 - Valdez 1 / 31

Premium Calculation Fall 2014 - Valdez 1 / 31") Premium Calculation Lecture: Weeks 12-14 Lecture: Weeks 12-14 (STT 455) Premium Calculation Fall 2014 - Valdez 1 / 31 Preliminaries Preliminaries An insurance policy (life insurance or life annuity) is

Premium Calculation Lecture: Weeks 12-14 Lecture: Weeks 12-14 (STT 455) Premium Calculation Fall 2014 - Valdez 1 / 31 Preliminaries Preliminaries An insurance policy (life insurance or life annuity) is

Annuities. Lecture: Weeks 9-11. Lecture: Weeks 9-11 (STT 455) Annuities Fall 2014 - Valdez 1 / 43

Annuities Fall 2014 - Valdez 1 / 43") Annuities Lecture: Weeks 9-11 Lecture: Weeks 9-11 (STT 455) Annuities Fall 2014 - Valdez 1 / 43 What are annuities? What are annuities? An annuity is a series of payments that could vary according to:

Annuities Lecture: Weeks 9-11 Lecture: Weeks 9-11 (STT 455) Annuities Fall 2014 - Valdez 1 / 43 What are annuities? What are annuities? An annuity is a series of payments that could vary according to:

MATH 3630 Actuarial Mathematics I Class Test 2 Wednesday, 17 November 2010 Time Allowed: 1 hour Total Marks: 100 points

MATH 3630 Actuarial Mathematics I Class Test 2 Wednesday, 17 November 2010 Time Allowed: 1 hour Total Marks: 100 points Please write your name and student number at the spaces provided: Name: Student ID:

MATH 3630 Actuarial Mathematics I Class Test 2 Wednesday, 17 November 2010 Time Allowed: 1 hour Total Marks: 100 points Please write your name and student number at the spaces provided: Name: Student ID:

Premium calculation. summer semester 2013/2014. Technical University of Ostrava Faculty of Economics department of Finance

Technical University of Ostrava Faculty of Economics department of Finance summer semester 2013/2014 Content 1 Fundamentals Insurer s expenses 2 Equivalence principles Calculation principles 3 Equivalence

Technical University of Ostrava Faculty of Economics department of Finance summer semester 2013/2014 Content 1 Fundamentals Insurer s expenses 2 Equivalence principles Calculation principles 3 Equivalence

Insurance Benefits. Lecture: Weeks 6-8. Lecture: Weeks 6-8 (STT 455) Insurance Benefits Fall 2014 - Valdez 1 / 36

Insurance Benefits Fall 2014 - Valdez 1 / 36") Insurance Benefits Lecture: Weeks 6-8 Lecture: Weeks 6-8 (STT 455) Insurance Benefits Fall 2014 - Valdez 1 / 36 An introduction An introduction Central theme: to quantify the value today of a (random)

Insurance Benefits Lecture: Weeks 6-8 Lecture: Weeks 6-8 (STT 455) Insurance Benefits Fall 2014 - Valdez 1 / 36 An introduction An introduction Central theme: to quantify the value today of a (random)

Manual for SOA Exam MLC.

Chapter 4. Life Insurance. Extract from: Arcones Manual for the SOA Exam MLC. Fall 2009 Edition. available at http://www.actexmadriver.com/ 1/14 Level benefit insurance in the continuous case In this chapter,

Chapter 4. Life Insurance. Extract from: Arcones Manual for the SOA Exam MLC. Fall 2009 Edition. available at http://www.actexmadriver.com/ 1/14 Level benefit insurance in the continuous case In this chapter,

November 2012 Course MLC Examination, Problem No. 1 For two lives, (80) and (90), with independent future lifetimes, you are given: k p 80+k

and (90), with independent future lifetimes, you are given: k p 80+k") Solutions to the November 202 Course MLC Examination by Krzysztof Ostaszewski, http://www.krzysio.net, krzysio@krzysio.net Copyright 202 by Krzysztof Ostaszewski All rights reserved. No reproduction in

Solutions to the November 202 Course MLC Examination by Krzysztof Ostaszewski, http://www.krzysio.net, krzysio@krzysio.net Copyright 202 by Krzysztof Ostaszewski All rights reserved. No reproduction in

May 2012 Course MLC Examination, Problem No. 1 For a 2-year select and ultimate mortality model, you are given:

Solutions to the May 2012 Course MLC Examination by Krzysztof Ostaszewski, http://www.krzysio.net, krzysio@krzysio.net Copyright 2012 by Krzysztof Ostaszewski All rights reserved. No reproduction in any

Solutions to the May 2012 Course MLC Examination by Krzysztof Ostaszewski, http://www.krzysio.net, krzysio@krzysio.net Copyright 2012 by Krzysztof Ostaszewski All rights reserved. No reproduction in any

SOCIETY OF ACTUARIES. EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE QUESTIONS

SOCIETY OF ACTUARIES EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE QUESTIONS The following questions or solutions have been modified since this document was prepared to use with the syllabus effective

SOCIETY OF ACTUARIES EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE QUESTIONS The following questions or solutions have been modified since this document was prepared to use with the syllabus effective

Manual for SOA Exam MLC.

Chapter 6. Benefit premiums Extract from: Arcones Fall 2010 Edition, available at http://www.actexmadriver.com/ 1/90 (#4, Exam M, Spring 2005) For a fully discrete whole life insurance of 100,000 on (35)

Chapter 6. Benefit premiums Extract from: Arcones Fall 2010 Edition, available at http://www.actexmadriver.com/ 1/90 (#4, Exam M, Spring 2005) For a fully discrete whole life insurance of 100,000 on (35)

Solution. Let us write s for the policy year. Then the mortality rate during year s is q 30+s 1. q 30+s 1

Solutions to the May 213 Course MLC Examination by Krzysztof Ostaszewski, http://wwwkrzysionet, krzysio@krzysionet Copyright 213 by Krzysztof Ostaszewski All rights reserved No reproduction in any form

Solutions to the May 213 Course MLC Examination by Krzysztof Ostaszewski, http://wwwkrzysionet, krzysio@krzysionet Copyright 213 by Krzysztof Ostaszewski All rights reserved No reproduction in any form

SOCIETY OF ACTUARIES. EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE QUESTIONS

SOCIETY OF ACTUARIES EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE QUESTIONS The following questions or solutions have been modified since this document was prepared to use with the syllabus effective

SOCIETY OF ACTUARIES EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE QUESTIONS The following questions or solutions have been modified since this document was prepared to use with the syllabus effective

Chapter 2. 1. You are given: 1 t. Calculate: f. Pr[ T0

Chapter 2 1. You are given: 1 5 t F0 ( t) 1 1,0 t 125 125 Calculate: a. S () t 0 b. Pr[ T0 t] c. Pr[ T0 t] d. S () t e. Probability that a newborn will live to age 25. f. Probability that a person age

Chapter 2 1. You are given: 1 5 t F0 ( t) 1 1,0 t 125 125 Calculate: a. S () t 0 b. Pr[ T0 t] c. Pr[ T0 t] d. S () t e. Probability that a newborn will live to age 25. f. Probability that a person age

Manual for SOA Exam MLC.

Chapter 5. Life annuities Extract from: Arcones Fall 2009 Edition, available at http://www.actexmadriver.com/ 1/60 (#24, Exam M, Fall 2005) For a special increasing whole life annuity-due on (40), you

Chapter 5. Life annuities Extract from: Arcones Fall 2009 Edition, available at http://www.actexmadriver.com/ 1/60 (#24, Exam M, Fall 2005) For a special increasing whole life annuity-due on (40), you

Manual for SOA Exam MLC.

Chapter 5. Life annuities. Extract from: Arcones Manual for the SOA Exam MLC. Spring 2010 Edition. available at http://www.actexmadriver.com/ 1/114 Whole life annuity A whole life annuity is a series of

Chapter 5. Life annuities. Extract from: Arcones Manual for the SOA Exam MLC. Spring 2010 Edition. available at http://www.actexmadriver.com/ 1/114 Whole life annuity A whole life annuity is a series of

How To Perform The Mathematician'S Test On The Mathematically Based Test

MATH 3630 Actuarial Mathematics I Final Examination - sec 001 Monday, 10 December 2012 Time Allowed: 2 hours (6:00-8:00 pm) Room: MSB 411 Total Marks: 120 points Please write your name and student number

MATH 3630 Actuarial Mathematics I Final Examination - sec 001 Monday, 10 December 2012 Time Allowed: 2 hours (6:00-8:00 pm) Room: MSB 411 Total Marks: 120 points Please write your name and student number

Manual for SOA Exam MLC.

Chapter 6. Benefit premiums. Extract from: Arcones Fall 2010 Edition, available at http://www.actexmadriver.com/ 1/24 Non-level premiums and/or benefits. Let b k be the benefit paid by an insurance company

Chapter 6. Benefit premiums. Extract from: Arcones Fall 2010 Edition, available at http://www.actexmadriver.com/ 1/24 Non-level premiums and/or benefits. Let b k be the benefit paid by an insurance company

Manual for SOA Exam MLC.

Chapter 6. Benefit premiums. Extract from: Arcones Fall 2010 Edition, available at http://www.actexmadriver.com/ 1/77 Fully discrete benefit premiums In this section, we will consider the funding of insurance

Chapter 6. Benefit premiums. Extract from: Arcones Fall 2010 Edition, available at http://www.actexmadriver.com/ 1/77 Fully discrete benefit premiums In this section, we will consider the funding of insurance

SOCIETY OF ACTUARIES. EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE WRITTEN-ANSWER QUESTIONS AND SOLUTIONS

SOCIETY OF ACTUARIES EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE WRITTEN-ANSWER QUESTIONS AND SOLUTIONS Questions February 12, 2015 In Questions 12, 13, and 19, the wording was changed slightly

SOCIETY OF ACTUARIES EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE WRITTEN-ANSWER QUESTIONS AND SOLUTIONS Questions February 12, 2015 In Questions 12, 13, and 19, the wording was changed slightly

JANUARY 2016 EXAMINATIONS. Life Insurance I

PAPER CODE NO. MATH 273 EXAMINER: Dr. C. Boado-Penas TEL.NO. 44026 DEPARTMENT: Mathematical Sciences JANUARY 2016 EXAMINATIONS Life Insurance I Time allowed: Two and a half hours INSTRUCTIONS TO CANDIDATES:

PAPER CODE NO. MATH 273 EXAMINER: Dr. C. Boado-Penas TEL.NO. 44026 DEPARTMENT: Mathematical Sciences JANUARY 2016 EXAMINATIONS Life Insurance I Time allowed: Two and a half hours INSTRUCTIONS TO CANDIDATES:

ACTUARIAL MATHEMATICS FOR LIFE CONTINGENT RISKS

ACTUARIAL MATHEMATICS FOR LIFE CONTINGENT RISKS DAVID C. M. DICKSON University of Melbourne MARY R. HARDY University of Waterloo, Ontario V HOWARD R. WATERS Heriot-Watt University, Edinburgh CAMBRIDGE

ACTUARIAL MATHEMATICS FOR LIFE CONTINGENT RISKS DAVID C. M. DICKSON University of Melbourne MARY R. HARDY University of Waterloo, Ontario V HOWARD R. WATERS Heriot-Watt University, Edinburgh CAMBRIDGE

Manual for SOA Exam MLC.

Chapter 4. Life insurance. Extract from: Arcones Fall 2009 Edition, available at http://www.actexmadriver.com/ (#1, Exam M, Fall 2005) For a special whole life insurance on (x), you are given: (i) Z is

Chapter 4. Life insurance. Extract from: Arcones Fall 2009 Edition, available at http://www.actexmadriver.com/ (#1, Exam M, Fall 2005) For a special whole life insurance on (x), you are given: (i) Z is

INSTRUCTIONS TO CANDIDATES

Society of Actuaries Canadian Institute of Actuaries Exam MLC Models for Life Contingencies Friday, October 31, 2014 8:30 a.m. 12:45 p.m. MLC General Instructions 1. Write your candidate number here. Your

Society of Actuaries Canadian Institute of Actuaries Exam MLC Models for Life Contingencies Friday, October 31, 2014 8:30 a.m. 12:45 p.m. MLC General Instructions 1. Write your candidate number here. Your

Heriot-Watt University. BSc in Actuarial Mathematics and Statistics. Life Insurance Mathematics I. Extra Problems: Multiple Choice

Heriot-Watt University BSc in Actuarial Mathematics and Statistics Life Insurance Mathematics I Extra Problems: Multiple Choice These problems have been taken from Faculty and Institute of Actuaries exams.

Heriot-Watt University BSc in Actuarial Mathematics and Statistics Life Insurance Mathematics I Extra Problems: Multiple Choice These problems have been taken from Faculty and Institute of Actuaries exams.

Practice Exam 1. x l x d x 50 1000 20 51 52 35 53 37

Practice Eam. You are given: (i) The following life table. (ii) 2q 52.758. l d 5 2 5 52 35 53 37 Determine d 5. (A) 2 (B) 2 (C) 22 (D) 24 (E) 26 2. For a Continuing Care Retirement Community, you are given

Practice Eam. You are given: (i) The following life table. (ii) 2q 52.758. l d 5 2 5 52 35 53 37 Determine d 5. (A) 2 (B) 2 (C) 22 (D) 24 (E) 26 2. For a Continuing Care Retirement Community, you are given

Universal Life Insurance

Universal Life Insurance Lecture: Weeks 11-12 Thanks to my friend J. Dhaene, KU Leuven, for ideas here drawn from his notes. Lecture: Weeks 11-12 (STT 456) Universal Life Insurance Spring 2015 - Valdez

Universal Life Insurance Lecture: Weeks 11-12 Thanks to my friend J. Dhaene, KU Leuven, for ideas here drawn from his notes. Lecture: Weeks 11-12 (STT 456) Universal Life Insurance Spring 2015 - Valdez

Manual for SOA Exam MLC.

Chapter 5 Life annuities Extract from: Arcones Manual for the SOA Exam MLC Fall 2009 Edition available at http://wwwactexmadrivercom/ 1/94 Due n year temporary annuity Definition 1 A due n year term annuity

Chapter 5 Life annuities Extract from: Arcones Manual for the SOA Exam MLC Fall 2009 Edition available at http://wwwactexmadrivercom/ 1/94 Due n year temporary annuity Definition 1 A due n year term annuity

Some Observations on Variance and Risk

Some Observations on Variance and Risk 1 Introduction By K.K.Dharni Pradip Kumar 1.1 In most actuarial contexts some or all of the cash flows in a contract are uncertain and depend on the death or survival

Some Observations on Variance and Risk 1 Introduction By K.K.Dharni Pradip Kumar 1.1 In most actuarial contexts some or all of the cash flows in a contract are uncertain and depend on the death or survival

Solution. Because you are not doing business in the state of New York, you only need to do the calculations at the end of each policy year.

Exercises in life and annuity valuation. You are the valuation actuary for the Hard Knocks Life Insurance Company offering life annuities and life insurance to guinea pigs. The valuation interest rate

Exercises in life and annuity valuation. You are the valuation actuary for the Hard Knocks Life Insurance Company offering life annuities and life insurance to guinea pigs. The valuation interest rate

1. Datsenka Dog Insurance Company has developed the following mortality table for dogs:

1 Datsenka Dog Insurance Company has developed the following mortality table for dogs: Age l Age l 0 2000 5 1200 1 1950 6 1000 2 1850 7 700 3 1600 8 300 4 1400 9 0 Datsenka sells an whole life annuity

1 Datsenka Dog Insurance Company has developed the following mortality table for dogs: Age l Age l 0 2000 5 1200 1 1950 6 1000 2 1850 7 700 3 1600 8 300 4 1400 9 0 Datsenka sells an whole life annuity

Mathematics of Life Contingencies MATH 3281

Mathematics of Life Contingencies MATH 3281 Life annuities contracts Edward Furman Department of Mathematics and Statistics York University February 13, 2012 Edward Furman Mathematics of Life Contingencies

Mathematics of Life Contingencies MATH 3281 Life annuities contracts Edward Furman Department of Mathematics and Statistics York University February 13, 2012 Edward Furman Mathematics of Life Contingencies

Manual for SOA Exam MLC.

Chapter 4 Life Insurance Extract from: Arcones Manual for the SOA Exam MLC Fall 2009 Edition available at http://wwwactexmadrivercom/ 1/13 Non-level payments paid at the end of the year Suppose that a

Chapter 4 Life Insurance Extract from: Arcones Manual for the SOA Exam MLC Fall 2009 Edition available at http://wwwactexmadrivercom/ 1/13 Non-level payments paid at the end of the year Suppose that a

TABLE OF CONTENTS. Practice Exam 1 3 Practice Exam 2 15 Practice Exam 3 27 Practice Exam 4 41 Practice Exam 5 53 Practice Exam 6 65

TABLE OF CONTENTS Practice Exam 1 3 Practice Exam 2 15 Practice Exam 3 27 Practice Exam 4 41 Practice Exam 5 53 Practice Exam 6 65 Solutions to Practice Exam 1 79 Solutions to Practice Exam 2 89 Solutions

TABLE OF CONTENTS Practice Exam 1 3 Practice Exam 2 15 Practice Exam 3 27 Practice Exam 4 41 Practice Exam 5 53 Practice Exam 6 65 Solutions to Practice Exam 1 79 Solutions to Practice Exam 2 89 Solutions

4. Life Insurance. 4.1 Survival Distribution And Life Tables. Introduction. X, Age-at-death. T (x), time-until-death

, time-until-death") 4. Life Insurance 4.1 Survival Distribution And Life Tables Introduction X, Age-at-death T (x), time-until-death Life Table Engineers use life tables to study the reliability of complex mechanical and

4. Life Insurance 4.1 Survival Distribution And Life Tables Introduction X, Age-at-death T (x), time-until-death Life Table Engineers use life tables to study the reliability of complex mechanical and

ACTS 4301 FORMULA SUMMARY Lesson 1: Probability Review. Name f(x) F (x) E[X] Var(X) Name f(x) E[X] Var(X) p x (1 p) m x mp mp(1 p)

![ACTS 4301 FORMULA SUMMARY Lesson 1: Probability Review. Name f(x) F (x) E[X] Var(X) Name f(x) E[X] Var(X) p x (1 p) m x mp mp(1 p)](/thumbs/39/20405687.jpg "ACTS 4301 FORMULA SUMMARY Lesson 1: Probability Review. Name f(x) F (x) E[X] Var(X) Name f(x) E[X] Var(X) p x (1 p) m x mp mp(1 p)") ACTS 431 FORMULA SUMMARY Lesson 1: Probability Review 1. VarX)= E[X 2 ]- E[X] 2 2. V arax + by ) = a 2 V arx) + 2abCovX, Y ) + b 2 V ary ) 3. V ar X) = V arx) n 4. E X [X] = E Y [E X [X Y ]] Double expectation

ACTS 431 FORMULA SUMMARY Lesson 1: Probability Review 1. VarX)= E[X 2 ]- E[X] 2 2. V arax + by ) = a 2 V arx) + 2abCovX, Y ) + b 2 V ary ) 3. V ar X) = V arx) n 4. E X [X] = E Y [E X [X Y ]] Double expectation

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION 27 April 2015 (pm) Subject CT5 Contingencies Core Technical Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate and examination

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION 27 April 2015 (pm) Subject CT5 Contingencies Core Technical Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate and examination

O MIA-009 (F2F) : GENERAL INSURANCE, LIFE AND

: GENERAL INSURANCE, LIFE AND") No. of Printed Pages : 11 MIA-009 (F2F) kr) ki) M.Sc. ACTUARIAL SCIENCE (MSCAS) N December, 2012 0 O MIA-009 (F2F) : GENERAL INSURANCE, LIFE AND HEALTH CONTINGENCIES Time : 3 hours Maximum Marks : 100

No. of Printed Pages : 11 MIA-009 (F2F) kr) ki) M.Sc. ACTUARIAL SCIENCE (MSCAS) N December, 2012 0 O MIA-009 (F2F) : GENERAL INSURANCE, LIFE AND HEALTH CONTINGENCIES Time : 3 hours Maximum Marks : 100

SOA EXAM MLC & CAS EXAM 3L STUDY SUPPLEMENT

SOA EXAM MLC & CAS EXAM 3L STUDY SUPPLEMENT by Paul H. Johnson, Jr., PhD. Last Modified: October 2012 A document prepared by the author as study materials for the Midwestern Actuarial Forum s Exam Preparation

SOA EXAM MLC & CAS EXAM 3L STUDY SUPPLEMENT by Paul H. Johnson, Jr., PhD. Last Modified: October 2012 A document prepared by the author as study materials for the Midwestern Actuarial Forum s Exam Preparation

2 Policy Values and Reserves

2 Policy Values and Reserves [Handout to accompany this section: reprint of Life Insurance, from The Encyclopaedia of Actuarial Science, John Wiley, Chichester, 2004.] 2.1 The Life Office s Balance Sheet

2 Policy Values and Reserves [Handout to accompany this section: reprint of Life Insurance, from The Encyclopaedia of Actuarial Science, John Wiley, Chichester, 2004.] 2.1 The Life Office s Balance Sheet

Asset and Liability Composition in Participating Life Insurance: The Impact on Shortfall Risk and Shareholder Value

Asset and Liability Composition in Participating Life Insurance: The Impact on Shortfall Risk and Shareholder Value 7th Conference in Actuarial Science & Finance on Samos June 1, 2012 Alexander Bohnert1,

Asset and Liability Composition in Participating Life Insurance: The Impact on Shortfall Risk and Shareholder Value 7th Conference in Actuarial Science & Finance on Samos June 1, 2012 Alexander Bohnert1,

On Simulation Method of Small Life Insurance Portfolios By Shamita Dutta Gupta Department of Mathematics Pace University New York, NY 10038

On Simulation Method of Small Life Insurance Portfolios By Shamita Dutta Gupta Department of Mathematics Pace University New York, NY 10038 Abstract A new simulation method is developed for actuarial applications

On Simulation Method of Small Life Insurance Portfolios By Shamita Dutta Gupta Department of Mathematics Pace University New York, NY 10038 Abstract A new simulation method is developed for actuarial applications

Manual for SOA Exam MLC.

Chapter 5 Life annuities Extract from: Arcones Manual for the SOA Exam MLC Fall 2009 Edition available at http://wwwactexmadrivercom/ 1/70 Due n year deferred annuity Definition 1 A due n year deferred

Chapter 5 Life annuities Extract from: Arcones Manual for the SOA Exam MLC Fall 2009 Edition available at http://wwwactexmadrivercom/ 1/70 Due n year deferred annuity Definition 1 A due n year deferred

Manual for SOA Exam MLC.

Chapter 4. Life Insurance. c 29. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam MLC. Fall 29 Edition. available at http://www.actexmadriver.com/ c 29. Miguel A. Arcones.

Chapter 4. Life Insurance. c 29. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam MLC. Fall 29 Edition. available at http://www.actexmadriver.com/ c 29. Miguel A. Arcones.

Math 630 Problem Set 2

Math 63 Problem Set 2 1. AN n-year term insurance payable at the moment of death has an actuarial present value (i.e. EPV) of.572. Given µ x+t =.7 and δ =.5, find n. (Answer: 11) 2. Given: Ā 1 x:n =.4275,

Math 63 Problem Set 2 1. AN n-year term insurance payable at the moment of death has an actuarial present value (i.e. EPV) of.572. Given µ x+t =.7 and δ =.5, find n. (Answer: 11) 2. Given: Ā 1 x:n =.4275,

Actuarial Science with

Actuarial Science with 1. life insurance & actuarial notations Arthur Charpentier joint work with Christophe Dutang & Vincent Goulet and Giorgio Alfredo Spedicato s lifecontingencies package Meielisalp

Actuarial Science with 1. life insurance & actuarial notations Arthur Charpentier joint work with Christophe Dutang & Vincent Goulet and Giorgio Alfredo Spedicato s lifecontingencies package Meielisalp

Mortality Risk and its Effect on Shortfall and Risk Management in Life Insurance

Mortality Risk and its Effect on Shortfall and Risk Management in Life Insurance AFIR 2011 Colloquium, Madrid June 22 nd, 2011 Nadine Gatzert and Hannah Wesker University of Erlangen-Nürnberg 2 Introduction

Mortality Risk and its Effect on Shortfall and Risk Management in Life Insurance AFIR 2011 Colloquium, Madrid June 22 nd, 2011 Nadine Gatzert and Hannah Wesker University of Erlangen-Nürnberg 2 Introduction

EDUCATION COMMITTEE OF THE SOCIETY OF ACTUARIES MLC STUDY NOTE SUPPLEMENTARY NOTES FOR ACTUARIAL MATHEMATICS FOR LIFE CONTINGENT RISKS VERSION 2.

EDUCATION COMMITTEE OF THE SOCIETY OF ACTUARIES MLC STUDY NOTE SUPPLEMENTARY NOTES FOR ACTUARIAL MATHEMATICS FOR LIFE CONTINGENT RISKS VERSION 2.0 by Mary R. Hardy, PhD, FIA, FSA, CERA David C. M. Dickson,

EDUCATION COMMITTEE OF THE SOCIETY OF ACTUARIES MLC STUDY NOTE SUPPLEMENTARY NOTES FOR ACTUARIAL MATHEMATICS FOR LIFE CONTINGENT RISKS VERSION 2.0 by Mary R. Hardy, PhD, FIA, FSA, CERA David C. M. Dickson,

Manual for SOA Exam MLC.

Chapter 5. Life annuities. Section 5.7. Computing present values from a life table Extract from: Arcones Manual for the SOA Exam MLC. Spring 2010 Edition. available at http://www.actexmadriver.com/ 1/30

Chapter 5. Life annuities. Section 5.7. Computing present values from a life table Extract from: Arcones Manual for the SOA Exam MLC. Spring 2010 Edition. available at http://www.actexmadriver.com/ 1/30

Living to 100: Survival to Advanced Ages: Insurance Industry Implication on Retirement Planning and the Secondary Market in Insurance

Living to 100: Survival to Advanced Ages: Insurance Industry Implication on Retirement Planning and the Secondary Market in Insurance Jay Vadiveloo, * Peng Zhou, Charles Vinsonhaler, and Sudath Ranasinghe

Living to 100: Survival to Advanced Ages: Insurance Industry Implication on Retirement Planning and the Secondary Market in Insurance Jay Vadiveloo, * Peng Zhou, Charles Vinsonhaler, and Sudath Ranasinghe

EXAMINATION. 6 April 2005 (pm) Subject CT5 Contingencies Core Technical. Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE

Subject CT5 Contingencies Core Technical. Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE") Faculty of Actuaries Institute of Actuaries EXAMINATION 6 April 2005 (pm) Subject CT5 Contingencies Core Technical Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate and

Faculty of Actuaries Institute of Actuaries EXAMINATION 6 April 2005 (pm) Subject CT5 Contingencies Core Technical Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate and

Fair value of insurance liabilities: unit linked / variable business

Fair value of insurance liabilities: unit linked / variable business The fair value treatment of unit linked / variable business differs from that of the traditional policies; below a description of a

Fair value of insurance liabilities: unit linked / variable business The fair value treatment of unit linked / variable business differs from that of the traditional policies; below a description of a

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 17 th November 2011 Subject CT5 General Insurance, Life and Health Contingencies Time allowed: Three Hours (10.00 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 17 th November 2011 Subject CT5 General Insurance, Life and Health Contingencies Time allowed: Three Hours (10.00 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO

TABLE OF CONTENTS. 4. Daniel Markov 1 173

TABLE OF CONTENTS 1. Survival A. Time of Death for a Person Aged x 1 B. Force of Mortality 7 C. Life Tables and the Deterministic Survivorship Group 19 D. Life Table Characteristics: Expectation of Life

TABLE OF CONTENTS 1. Survival A. Time of Death for a Person Aged x 1 B. Force of Mortality 7 C. Life Tables and the Deterministic Survivorship Group 19 D. Life Table Characteristics: Expectation of Life

Analyzing the Surrender Rate of Limited Reimbursement Long-Term Individual Health Insurance

Analyzing the Surrender Rate of Limited Reimbursement Long-Term Individual Health Insurance Chih-Hua Chiao, Shing-Her Juang, Pin-Hsun Chen, Chen-Ting Chueh Department of Financial Engineering and Actuarial

Analyzing the Surrender Rate of Limited Reimbursement Long-Term Individual Health Insurance Chih-Hua Chiao, Shing-Her Juang, Pin-Hsun Chen, Chen-Ting Chueh Department of Financial Engineering and Actuarial

1 Cash-flows, discounting, interest rate models

Assignment 1 BS4a Actuarial Science Oxford MT 2014 1 1 Cash-flows, discounting, interest rate models Please hand in your answers to questions 3, 4, 5 and 8 for marking. The rest are for further practice.

Assignment 1 BS4a Actuarial Science Oxford MT 2014 1 1 Cash-flows, discounting, interest rate models Please hand in your answers to questions 3, 4, 5 and 8 for marking. The rest are for further practice.

Profit Measures in Life Insurance

Profit Measures in Life Insurance Shelly Matushevski Honors Project Spring 2011 The University of Akron 2 Table of Contents I. Introduction... 3 II. Loss Function... 5 III. Equivalence Principle... 7 IV.

Profit Measures in Life Insurance Shelly Matushevski Honors Project Spring 2011 The University of Akron 2 Table of Contents I. Introduction... 3 II. Loss Function... 5 III. Equivalence Principle... 7 IV.

**BEGINNING OF EXAMINATION**

November 00 Course 3 Society of Actuaries **BEGINNING OF EXAMINATION**. You are given: R = S T µ x 0. 04, 0 < x < 40 0. 05, x > 40 Calculate e o 5: 5. (A) 4.0 (B) 4.4 (C) 4.8 (D) 5. (E) 5.6 Course 3: November

November 00 Course 3 Society of Actuaries **BEGINNING OF EXAMINATION**. You are given: R = S T µ x 0. 04, 0 < x < 40 0. 05, x > 40 Calculate e o 5: 5. (A) 4.0 (B) 4.4 (C) 4.8 (D) 5. (E) 5.6 Course 3: November

Manual for SOA Exam MLC.

Manual for SOA Eam MLC. Chapter 4. Life Insurance. Etract from: Arcones Manual for the SOA Eam MLC. Fall 2009 Edition. available at http://www.actemadriver.com/ Manual for SOA Eam MLC. 1/9 Payments at

Manual for SOA Eam MLC. Chapter 4. Life Insurance. Etract from: Arcones Manual for the SOA Eam MLC. Fall 2009 Edition. available at http://www.actemadriver.com/ Manual for SOA Eam MLC. 1/9 Payments at

4.1 4.2 Probability Distribution for Discrete Random Variables

4.1 4.2 Probability Distribution for Discrete Random Variables Key concepts: discrete random variable, probability distribution, expected value, variance, and standard deviation of a discrete random variable.

4.1 4.2 Probability Distribution for Discrete Random Variables Key concepts: discrete random variable, probability distribution, expected value, variance, and standard deviation of a discrete random variable.

1. Revision 2. Revision pv 3. - note that there are other equivalent formulae! 1 pv 16.5 4. A x A 1 x:n A 1

Tutorial 1 1. Revision 2. Revision pv 3. - note that there are other equivalent formulae! 1 pv 16.5 4. A x A 1 x:n A 1 x:n a x a x:n n a x 5. K x = int[t x ] - or, as an approximation: T x K x + 1 2 6.

Tutorial 1 1. Revision 2. Revision pv 3. - note that there are other equivalent formulae! 1 pv 16.5 4. A x A 1 x:n A 1 x:n a x a x:n n a x 5. K x = int[t x ] - or, as an approximation: T x K x + 1 2 6.

REGS 2013: Variable Annuity Guaranteed Minimum Benefits

Department of Mathematics University of Illinois, Urbana-Champaign REGS 2013: Variable Annuity Guaranteed Minimum Benefits By: Vanessa Rivera Quiñones Professor Ruhuan Feng September 30, 2013 The author

Department of Mathematics University of Illinois, Urbana-Champaign REGS 2013: Variable Annuity Guaranteed Minimum Benefits By: Vanessa Rivera Quiñones Professor Ruhuan Feng September 30, 2013 The author

Statistical Analysis of Life Insurance Policy Termination and Survivorship

Statistical Analysis of Life Insurance Policy Termination and Survivorship Emiliano A. Valdez, PhD, FSA Michigan State University joint work with J. Vadiveloo and U. Dias Session ES82 (Statistics in Actuarial

Statistical Analysis of Life Insurance Policy Termination and Survivorship Emiliano A. Valdez, PhD, FSA Michigan State University joint work with J. Vadiveloo and U. Dias Session ES82 (Statistics in Actuarial

Manual for SOA Exam MLC.

Chapter 4. Life Insurance. Extract from: Arcones Manual for the SOA Exam MLC. Fall 2009 Edition. available at http://www.actexmadriver.com/ 1/44 Properties of the APV for continuous insurance The following

Chapter 4. Life Insurance. Extract from: Arcones Manual for the SOA Exam MLC. Fall 2009 Edition. available at http://www.actexmadriver.com/ 1/44 Properties of the APV for continuous insurance The following

EXAMINATIONS. 18 April 2000 (am) Subject 105 Actuarial Mathematics 1. Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE

Subject 105 Actuarial Mathematics 1. Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE") Faculty of Actuaries Institute of Actuaries EXAMINATIONS 18 April 2000 (am) Subject 105 Actuarial Mathematics 1 Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Write your surname in full, the

Faculty of Actuaries Institute of Actuaries EXAMINATIONS 18 April 2000 (am) Subject 105 Actuarial Mathematics 1 Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Write your surname in full, the

Chapter 04 - More General Annuities

Chapter 04 - More General Annuities 4-1 Section 4.3 - Annuities Payable Less Frequently Than Interest Conversion Payment 0 1 0 1.. k.. 2k... n Time k = interest conversion periods before each payment n

Chapter 04 - More General Annuities 4-1 Section 4.3 - Annuities Payable Less Frequently Than Interest Conversion Payment 0 1 0 1.. k.. 2k... n Time k = interest conversion periods before each payment n

Rule 9 On Prescribing Reserve Requirements of Insurance Companies

Banking and Payments Authority of Kosovo Pursuant to the authority given under Section 17.b of UNMIK Regulation No. 2001/24 date of October 1, 2001 on Amending UNMIK Regulation No. 1999/20, on Banking

Banking and Payments Authority of Kosovo Pursuant to the authority given under Section 17.b of UNMIK Regulation No. 2001/24 date of October 1, 2001 on Amending UNMIK Regulation No. 1999/20, on Banking

Math 370/408, Spring 2008 Prof. A.J. Hildebrand. Actuarial Exam Practice Problem Set 2 Solutions

Math 70/408, Spring 2008 Prof. A.J. Hildebrand Actuarial Exam Practice Problem Set 2 Solutions About this problem set: These are problems from Course /P actuarial exams that I have collected over the years,

Math 70/408, Spring 2008 Prof. A.J. Hildebrand Actuarial Exam Practice Problem Set 2 Solutions About this problem set: These are problems from Course /P actuarial exams that I have collected over the years,

THE EMPIRE LIFE INSURANCE COMPANY

THE EMPIRE LIFE INSURANCE COMPANY Condensed Interim Consolidated Financial Statements For the nine months ended September 30, 2013 Unaudited Issue Date: November 6, 2013 These condensed interim consolidated

THE EMPIRE LIFE INSURANCE COMPANY Condensed Interim Consolidated Financial Statements For the nine months ended September 30, 2013 Unaudited Issue Date: November 6, 2013 These condensed interim consolidated

SOCIETY OF ACTUARIES EXAM M ACTUARIAL MODELS EXAM M SAMPLE QUESTIONS

SOCIETY OF ACTUARIES EXAM M ACTUARIAL MODELS EXAM M SAMPLE QUESTIONS Copyright 005 by the Society of Actuaries Some of the questions in this study note are taken from past SOA examinations. M-09-05 PRINTED

SOCIETY OF ACTUARIES EXAM M ACTUARIAL MODELS EXAM M SAMPLE QUESTIONS Copyright 005 by the Society of Actuaries Some of the questions in this study note are taken from past SOA examinations. M-09-05 PRINTED

Aggregate Loss Models

Aggregate Loss Models Chapter 9 Stat 477 - Loss Models Chapter 9 (Stat 477) Aggregate Loss Models Brian Hartman - BYU 1 / 22 Objectives Objectives Individual risk model Collective risk model Computing

Aggregate Loss Models Chapter 9 Stat 477 - Loss Models Chapter 9 (Stat 477) Aggregate Loss Models Brian Hartman - BYU 1 / 22 Objectives Objectives Individual risk model Collective risk model Computing

Session 4: Universal Life

Session 4: Universal Life US GAAP for International Life Insurers Bill Horbatt SFAS 97 Effective 1989 Applicability Limited-Payment Contracts Universal Life-Type Contracts Investment Contracts 2 2 Universal

Session 4: Universal Life US GAAP for International Life Insurers Bill Horbatt SFAS 97 Effective 1989 Applicability Limited-Payment Contracts Universal Life-Type Contracts Investment Contracts 2 2 Universal

Glossary of insurance terms

Glossary of insurance terms I. Insurance Products Annuity is a life insurance policy where an insurance company pays an income stream to an individual, usually until death, in exchange for the payment

Glossary of insurance terms I. Insurance Products Annuity is a life insurance policy where an insurance company pays an income stream to an individual, usually until death, in exchange for the payment

Yanyun Zhu. Actuarial Model: Life Insurance & Annuity. Series in Actuarial Science. Volume I. ir* International Press. www.intlpress.

Yanyun Zhu Actuarial Model: Life Insurance & Annuity Series in Actuarial Science Volume I ir* International Press www.intlpress.com Contents Preface v 1 Interest and Annuity-Certain 1 1.1 Introduction

Yanyun Zhu Actuarial Model: Life Insurance & Annuity Series in Actuarial Science Volume I ir* International Press www.intlpress.com Contents Preface v 1 Interest and Annuity-Certain 1 1.1 Introduction

Health insurance pricing in Spain: Consequences and alternatives

Health insurance pricing in Spain: Consequences and alternatives Anna Castañer, M. Mercè Claramunt and Carmen Ribas Dept. Matemàtica Econòmica, Financera i Actuarial Universitat de Barcelona Abstract For

Health insurance pricing in Spain: Consequences and alternatives Anna Castañer, M. Mercè Claramunt and Carmen Ribas Dept. Matemàtica Econòmica, Financera i Actuarial Universitat de Barcelona Abstract For

TABLE OF CONTENTS. GENERAL AND HISTORICAL PREFACE iii SIXTH EDITION PREFACE v PART ONE: REVIEW AND BACKGROUND MATERIAL

TABLE OF CONTENTS GENERAL AND HISTORICAL PREFACE iii SIXTH EDITION PREFACE v PART ONE: REVIEW AND BACKGROUND MATERIAL CHAPTER ONE: REVIEW OF INTEREST THEORY 3 1.1 Interest Measures 3 1.2 Level Annuity

TABLE OF CONTENTS GENERAL AND HISTORICAL PREFACE iii SIXTH EDITION PREFACE v PART ONE: REVIEW AND BACKGROUND MATERIAL CHAPTER ONE: REVIEW OF INTEREST THEORY 3 1.1 Interest Measures 3 1.2 Level Annuity

Safety margins for unsystematic biometric risk in life and health insurance

Safety margins for unsystematic biometric risk in life and health insurance Marcus C. Christiansen June 1, 2012 7th Conference in Actuarial Science & Finance on Samos Seite 2 Safety margins for unsystematic

Safety margins for unsystematic biometric risk in life and health insurance Marcus C. Christiansen June 1, 2012 7th Conference in Actuarial Science & Finance on Samos Seite 2 Safety margins for unsystematic

EDUCATION AND EXAMINATION COMMITTEE SOCIETY OF ACTUARIES RISK AND INSURANCE. Copyright 2005 by the Society of Actuaries

EDUCATION AND EXAMINATION COMMITTEE OF THE SOCIET OF ACTUARIES RISK AND INSURANCE by Judy Feldman Anderson, FSA and Robert L. Brown, FSA Copyright 25 by the Society of Actuaries The Education and Examination

EDUCATION AND EXAMINATION COMMITTEE OF THE SOCIET OF ACTUARIES RISK AND INSURANCE by Judy Feldman Anderson, FSA and Robert L. Brown, FSA Copyright 25 by the Society of Actuaries The Education and Examination

More on annuities with payments in arithmetic progression and yield rates for annuities

More on annuities with payments in arithmetic progression and yield rates for annuities 1 Annuities-due with payments in arithmetic progression 2 Yield rate examples involving annuities More on annuities

More on annuities with payments in arithmetic progression and yield rates for annuities 1 Annuities-due with payments in arithmetic progression 2 Yield rate examples involving annuities More on annuities

Annuities and decumulation phase of retirement. Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA

Annuities and decumulation phase of retirement Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA CASH LUMP SUM AT RETIREMENT CASH INSTEAD OF PENSION > popular with pension scheme members

Annuities and decumulation phase of retirement Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA CASH LUMP SUM AT RETIREMENT CASH INSTEAD OF PENSION > popular with pension scheme members

Ermanno Pitacco. University of Trieste (Italy) ermanno.pitacco@deams.units.it 1/38. p. 1/38

ermanno.pitacco@deams.units.it 1/38. p. 1/38") p. 1/38 Guarantees and product design in Life & Health Insurance Ermanno Pitacco University of Trieste (Italy) ermanno.pitacco@deams.units.it 1/38 p. 2/38 Agenda Introduction & Motivation Weakening the

p. 1/38 Guarantees and product design in Life & Health Insurance Ermanno Pitacco University of Trieste (Italy) ermanno.pitacco@deams.units.it 1/38 p. 2/38 Agenda Introduction & Motivation Weakening the

Further Topics in Actuarial Mathematics: Premium Reserves. Matthew Mikola

Further Topics in Actuarial Mathematics: Premium Reserves Matthew Mikola April 26, 2007 Contents 1 Introduction 1 1.1 Expected Loss...................................... 2 1.2 An Overview of the Project...............................

Further Topics in Actuarial Mathematics: Premium Reserves Matthew Mikola April 26, 2007 Contents 1 Introduction 1 1.1 Expected Loss...................................... 2 1.2 An Overview of the Project...............................

Stochastic Analysis of Long-Term Multiple-Decrement Contracts

Stochastic Analysis of Long-Term Multiple-Decrement Contracts Matthew Clark, FSA, MAAA, and Chad Runchey, FSA, MAAA Ernst & Young LLP Published in the July 2008 issue of the Actuarial Practice Forum Copyright

Stochastic Analysis of Long-Term Multiple-Decrement Contracts Matthew Clark, FSA, MAAA, and Chad Runchey, FSA, MAAA Ernst & Young LLP Published in the July 2008 issue of the Actuarial Practice Forum Copyright

b g is the future lifetime random variable.

**BEGINNING OF EXAMINATION** 1. Given: (i) e o 0 = 5 (ii) l = ω, 0 ω (iii) is the future lifetime random variable. T Calculate Var Tb10g. (A) 65 (B) 93 (C) 133 (D) 178 (E) 333 COURSE/EXAM 3: MAY 000-1

**BEGINNING OF EXAMINATION** 1. Given: (i) e o 0 = 5 (ii) l = ω, 0 ω (iii) is the future lifetime random variable. T Calculate Var Tb10g. (A) 65 (B) 93 (C) 133 (D) 178 (E) 333 COURSE/EXAM 3: MAY 000-1

Valuation Report on Prudential Annuities Limited as at 31 December 2003. The investigation relates to 31 December 2003.

PRUDENTIAL ANNUITIES LIMITED Returns for the year ended 31 December 2003 SCHEDULE 4 Valuation Report on Prudential Annuities Limited as at 31 December 2003 1. Date of investigation The investigation relates

PRUDENTIAL ANNUITIES LIMITED Returns for the year ended 31 December 2003 SCHEDULE 4 Valuation Report on Prudential Annuities Limited as at 31 December 2003 1. Date of investigation The investigation relates

(Official Gazette of Montenegro, No 01/13 of 3 January 2013) GENERAL PROVISION. Article 1

GENERAL PROVISION. Article 1") Pursuant to Article 83 paragraph 6, Article 87 and Article 177 item 4 of the Law on Insurance (Official Gazette of the Republic of Montenegro, No 78/06 and 19/07 and Official Gazette of Montenegro, No

Pursuant to Article 83 paragraph 6, Article 87 and Article 177 item 4 of the Law on Insurance (Official Gazette of the Republic of Montenegro, No 78/06 and 19/07 and Official Gazette of Montenegro, No

Guardian Investor II SM Variable Annuity Fact Card

THE GUARDIAN INSURANCE & ANNUITY COMPANY, INC. (GIAC) Guardian Investor II SM Variable Annuity Fact Card A Variable Annuity is a long-term financial product for retirement purposes that allows you to accumulate

THE GUARDIAN INSURANCE & ANNUITY COMPANY, INC. (GIAC) Guardian Investor II SM Variable Annuity Fact Card A Variable Annuity is a long-term financial product for retirement purposes that allows you to accumulate

Mathematics of Life Contingencies. Math 3281 3.00 W Instructor: Edward Furman Homework 1

Mathematics of Life Contingencies. Math 3281 3.00 W Instructor: Edward Furman Homework 1 Unless otherwise indicated, all lives in the following questions are subject to the same law of mortality and their

Mathematics of Life Contingencies. Math 3281 3.00 W Instructor: Edward Furman Homework 1 Unless otherwise indicated, all lives in the following questions are subject to the same law of mortality and their

Math 370/408, Spring 2008 Prof. A.J. Hildebrand. Actuarial Exam Practice Problem Set 5 Solutions

Math 370/408, Spring 2008 Prof. A.J. Hildebrand Actuarial Exam Practice Problem Set 5 Solutions About this problem set: These are problems from Course 1/P actuarial exams that I have collected over the

Math 370/408, Spring 2008 Prof. A.J. Hildebrand Actuarial Exam Practice Problem Set 5 Solutions About this problem set: These are problems from Course 1/P actuarial exams that I have collected over the

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 13 th May 2015 Subject CT5 General Insurance, Life and Health Contingencies Time allowed: Three Hours (10.30 13.30 Hrs) Total Marks: 100 INSTRUCTIONS TO THE

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 13 th May 2015 Subject CT5 General Insurance, Life and Health Contingencies Time allowed: Three Hours (10.30 13.30 Hrs) Total Marks: 100 INSTRUCTIONS TO THE

EXAM 3, FALL 003 Please note: On a one-time basis, the CAS is releasing annotated solutions to Fall 003 Examination 3 as a study aid to candidates. It is anticipated that for future sittings, only the

EXAM 3, FALL 003 Please note: On a one-time basis, the CAS is releasing annotated solutions to Fall 003 Examination 3 as a study aid to candidates. It is anticipated that for future sittings, only the

LIFE INSURANCE AND PENSIONS by Peter Tryfos York University

LIFE INSURANCE AND PENSIONS by Peter Tryfos York University Introduction Life insurance is the business of insuring human life: in return for a premium payable in one sum or installments, an insurance

LIFE INSURANCE AND PENSIONS by Peter Tryfos York University Introduction Life insurance is the business of insuring human life: in return for a premium payable in one sum or installments, an insurance

Properties of Future Lifetime Distributions and Estimation

Properties of Future Lifetime Distributions and Estimation Harmanpreet Singh Kapoor and Kanchan Jain Abstract Distributional properties of continuous future lifetime of an individual aged x have been studied.

Properties of Future Lifetime Distributions and Estimation Harmanpreet Singh Kapoor and Kanchan Jain Abstract Distributional properties of continuous future lifetime of an individual aged x have been studied.

Pricing and Risk Management of Variable Annuity Guaranteed Benefits by Analytical Methods Longevity 10, September 3, 2014

Pricing and Risk Management of Variable Annuity Guaranteed Benefits by Analytical Methods Longevity 1, September 3, 214 Runhuan Feng, University of Illinois at Urbana-Champaign Joint work with Hans W.

Pricing and Risk Management of Variable Annuity Guaranteed Benefits by Analytical Methods Longevity 1, September 3, 214 Runhuan Feng, University of Illinois at Urbana-Champaign Joint work with Hans W.

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION 30 April 2015 (am) Subject SA2 Life Insurance Specialist Applications Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate and

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION 30 April 2015 (am) Subject SA2 Life Insurance Specialist Applications Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate and

Featured article: Evaluating the Cost of Longevity in Variable Annuity Living Benefits

Featured article: Evaluating the Cost of Longevity in Variable Annuity Living Benefits By Stuart Silverman and Dan Theodore This is a follow-up to a previous article Considering the Cost of Longevity Volatility

Featured article: Evaluating the Cost of Longevity in Variable Annuity Living Benefits By Stuart Silverman and Dan Theodore This is a follow-up to a previous article Considering the Cost of Longevity Volatility

Multi-state transition models with actuarial applications c

Multi-state transition models with actuarial applications c by James W. Daniel c Copyright 2004 by James W. Daniel Reprinted by the Casualty Actuarial Society and the Society of Actuaries by permission

Multi-state transition models with actuarial applications c by James W. Daniel c Copyright 2004 by James W. Daniel Reprinted by the Casualty Actuarial Society and the Society of Actuaries by permission

Case Study Modeling Longevity Risk for Solvency II

Case Study Modeling Longevity Risk for Solvency II September 8, 2012 Longevity 8 Conference Waterloo, Ontario Presented by Stuart Silverman Principal & Consulting Actuary Background SOLVENCY II New Minimum

Case Study Modeling Longevity Risk for Solvency II September 8, 2012 Longevity 8 Conference Waterloo, Ontario Presented by Stuart Silverman Principal & Consulting Actuary Background SOLVENCY II New Minimum

PREMIUM AND BONUS. MODULE - 3 Practice of Life Insurance. Notes

4 PREMIUM AND BONUS 4.0 INTRODUCTION A insurance policy needs to be bought. This comes at a price which is known as premium. Premium is the consideration for covering of the risk of the insured. The insured

4 PREMIUM AND BONUS 4.0 INTRODUCTION A insurance policy needs to be bought. This comes at a price which is known as premium. Premium is the consideration for covering of the risk of the insured. The insured