FIN 413 Corporate Finance. Capital Structure, Taxes, and Bankruptcy

|

|

|

- Edwina Doyle

- 10 years ago

- Views:

Transcription

1 FIN 413 Corporate Finance Capital Structure, Taxes, and Bankruptcy Evgeny Lyandres Fall

2 Relaxing the M-M Assumptions E D T Interest payments to bondholders are deductible for tax purposes while payments to equityholders are not. V (levered firm) = V(unlevered firm) + PV(tax shields) 2

= V(unlevered firm) + PV(tax")

3 3

4 Consider the following income statements Income Statements Firm U Firm L EBIT $1000 $1000 Interest payments at 8% $0 $80 Pretax income $1000 $920 Taxes $340 $312.8 Net shareholders income $660 $607.2 Total net income $660 $687.2 Interest tax shield $0 $27.2 4

5 The tax bill of L is $T C r D D less than that of U This is the tax shield provided by the debt of L The value of this tax shield is PV tax shield = Tax rate * Return on Debt * Amount borrowed Return on Debt We thus have: V L = V U + T C D or V(levered firm) = V(unlevered firm) + PV(tax shields) 5

= V(unlevered firm) + PV(tax shields) 5")

6 According to this analysis, all firms should be 100% debt-financed Two reasons can explain the difference between empirical evidence and this argument - personal taxes - bankruptcy costs 6

7 Taxes and Bankruptcy Costs D E T Bankruptcy Costs V (levered firm) = The optimal capital structure balances the gains from lower taxes with the increased expected costs of bankruptcy. 7

8 U.S. bankruptcy code Chapter 7 bankruptcy - Absolute priority Chapter 11 bankruptcy - Debtholders and equityholders get new claims instead of the old ones - Reorganization plan 8

9 Costs of bankruptcy Direct costs - Management time - Legal expenses and advisors fees - Court costs Indirect costs - Conflicts of interests between equityholders and debtholders (agency problems) 9

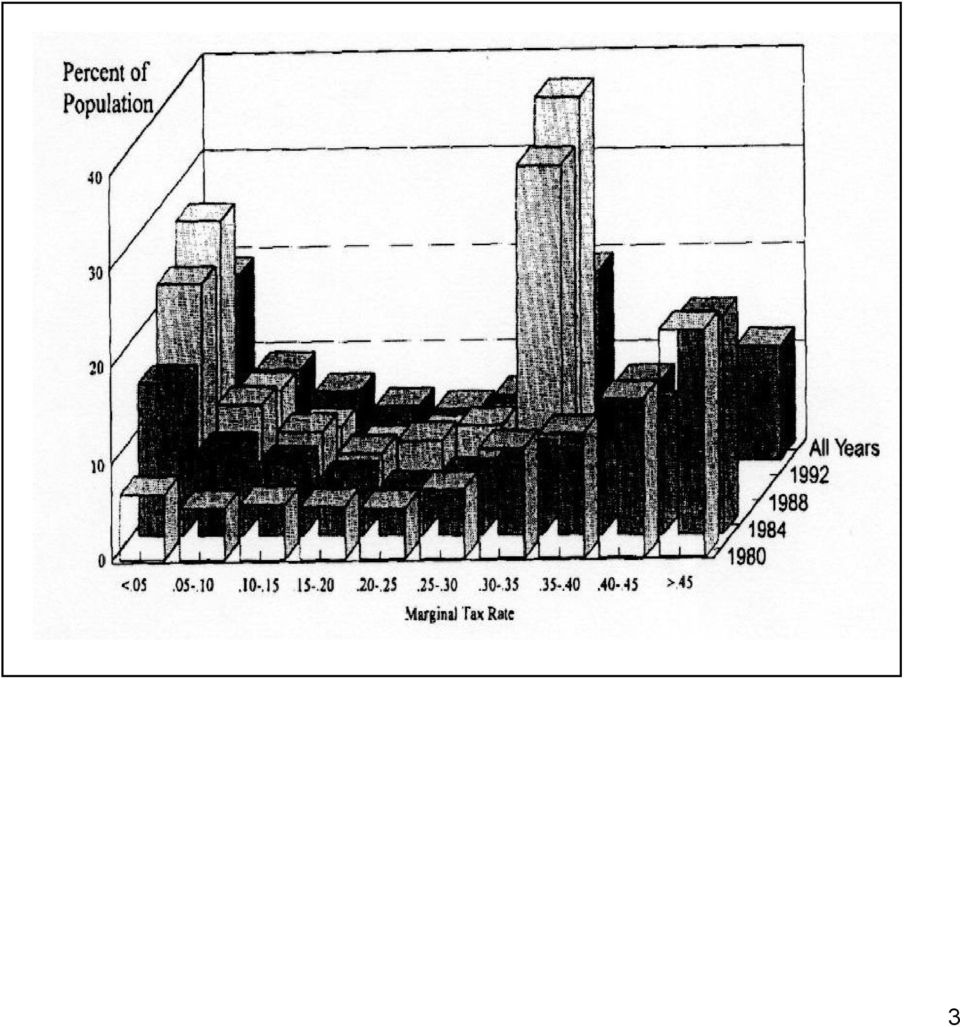

10 Trade-off between tax shield and cost of financial distress Market Value PV Tax Shields PV of costs of financial distress Value if all equity financed Debt Ratio Optimal Debt Ratio Value of the firm = Value of all equity financed + PV tax shield - PV costs of financial distress 10

11 Bankruptcy Costs Jerry Warner examined bankruptcies of 11 railroads to estimate the costs of bankruptcy The bankruptcy proceedings typical lasted many years. The average was 13 years, and the longest was 23 years On average, these firms spent approximately $2M on the bankruptcy proceedings 11

12 Bankruptcy Costs Several academic studies have examined the direct costs of bankruptcy: BC = T t= 0 BC V 0 BC V 5 BC t = $2M = 5.3% = 1.4% BC E( ) V 5 is even lower 12

13 Taxes and bankruptcy Costs Merton Miller - A case of horse and rabbit s stew - Analysis so far ignores personal taxes and the effect of the equilibrium in the bond market 13

14 Miller's Debt and Taxes Both corporations and individuals pay taxes. When corporations pay interest on debt, they reduce their own taxes, but increase the taxes of individuals. Ultimately, the corporation must bear all of the taxes associated with its activities either directly, or indirectly through higher required rates of return on the securities that it issues. 14

15 Miller's Debt and Taxes D E T Personal Taxes Increase the amount of debt in the capital structure until the marginal corporate tax saving is equal to the marginal personal tax cost. 15

16 The Tax Advantage of Debt Financing After-tax cash flow from $1 of interest After-tax cash flow from $1 of equity income (1-Tb) (1-Tc) (1-Te) Net savings from $1 of interest: T* = (1-Tb) - (1-Tc) (1-Te) 16

- (1-Tc)")

17 17

18 Return on debt 10% After-corporate tax return on riskless equity 8% Investor A B Tax rate on equity 20% 20% Marginal tax rate on income 40% 20% Net return on equity 6.4% 6.4% Net return on debt 6% 8% 18

19 DeAngelo and Masulis Debt and Taxes As corporations increase their debt, they reduce the probability that they will pay the highest marginal tax rate and be able to fully utilize all tax credits and deductions. Default Zero taxes, deductions not fully utilized Positive taxes, tax credits not fully utilized Taxes paid at the highest marginal rate Income 19

20 DeAngelo and Masulis Debt and Taxes Comparative statics for optimal leverage Non-interest tax shields Bankruptcy costs Corporate marginal tax rate Personal marginal tax rate 20

21 DeAngelo and Masulis Debt and Taxes Holding other things constant, the logic of the model is sound, and provides useful information However, large industrial firms typically have many non-interest deductions (depreciation), large tax credit (investment tax credit), and also high leverage What s wrong with DeAngelo/ Masulis story? 21

Chapter 15: Debt Policy

FIN 302 Class Notes Chapter 15: Debt Policy Two Cases: Case one: NO TAX All Equity Half Debt Number of shares 100,000 50,000 Price per share $10 $10 Equity Value $1,000,000 $500,000 Debt Value $0 $500,000

FIN 302 Class Notes Chapter 15: Debt Policy Two Cases: Case one: NO TAX All Equity Half Debt Number of shares 100,000 50,000 Price per share $10 $10 Equity Value $1,000,000 $500,000 Debt Value $0 $500,000

CHAPTER 15 Capital Structure: Basic Concepts

Multiple Choice Questions: CHAPTER 15 Capital Structure: Basic Concepts I. DEFINITIONS HOMEMADE LEVERAGE a 1. The use of personal borrowing to change the overall amount of financial leverage to which an

Multiple Choice Questions: CHAPTER 15 Capital Structure: Basic Concepts I. DEFINITIONS HOMEMADE LEVERAGE a 1. The use of personal borrowing to change the overall amount of financial leverage to which an

DUKE UNIVERSITY Fuqua School of Business. FINANCE 351 - CORPORATE FINANCE Problem Set #7 Prof. Simon Gervais Fall 2011 Term 2.

DUKE UNIVERSITY Fuqua School of Business FINANCE 351 - CORPORATE FINANCE Problem Set #7 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Suppose the corporate tax rate is 40%, and investors pay a tax

DUKE UNIVERSITY Fuqua School of Business FINANCE 351 - CORPORATE FINANCE Problem Set #7 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Suppose the corporate tax rate is 40%, and investors pay a tax

CAPITAL STRUCTURE [Chapter 15 and Chapter 16]

![CAPITAL STRUCTURE [Chapter 15 and Chapter 16]](/thumbs/34/17057255.jpg "CAPITAL STRUCTURE [Chapter 15 and Chapter 16]") Capital Structure [CHAP. 15 & 16] -1 CAPITAL STRUCTURE [Chapter 15 and Chapter 16] CONTENTS I. Introduction II. Capital Structure & Firm Value WITHOUT Taxes III. Capital Structure & Firm Value WITH Corporate

Capital Structure [CHAP. 15 & 16] -1 CAPITAL STRUCTURE [Chapter 15 and Chapter 16] CONTENTS I. Introduction II. Capital Structure & Firm Value WITHOUT Taxes III. Capital Structure & Firm Value WITH Corporate

Chapter 1: The Modigliani-Miller Propositions, Taxes and Bankruptcy Costs

Chapter 1: The Modigliani-Miller Propositions, Taxes and Bankruptcy Costs Corporate Finance - MSc in Finance (BGSE) Albert Banal-Estañol Universitat Pompeu Fabra and Barcelona GSE Albert Banal-Estañol

Chapter 1: The Modigliani-Miller Propositions, Taxes and Bankruptcy Costs Corporate Finance - MSc in Finance (BGSE) Albert Banal-Estañol Universitat Pompeu Fabra and Barcelona GSE Albert Banal-Estañol

SOLUTIONS. Practice questions. Multiple Choice

Practice questions Multiple Choice 1. XYZ has $25,000 of debt outstanding and a book value of equity of $25,000. The company has 10,000 shares outstanding and a stock price of $10. If the unlevered beta

Practice questions Multiple Choice 1. XYZ has $25,000 of debt outstanding and a book value of equity of $25,000. The company has 10,000 shares outstanding and a stock price of $10. If the unlevered beta

Ch. 18: Taxes + Bankruptcy cost

Ch. 18: Taxes + Bankruptcy cost If MM1 holds, then Financial Management has little (if any) impact on value of the firm: If markets are perfect, transaction cost (TAC) and bankruptcy cost are zero, no

Ch. 18: Taxes + Bankruptcy cost If MM1 holds, then Financial Management has little (if any) impact on value of the firm: If markets are perfect, transaction cost (TAC) and bankruptcy cost are zero, no

THE FINANCING DECISIONS BY FIRMS: IMPACT OF CAPITAL STRUCTURE CHOICE ON VALUE

IX. THE FINANCING DECISIONS BY FIRMS: IMPACT OF CAPITAL STRUCTURE CHOICE ON VALUE The capital structure of a firm is defined to be the menu of the firm's liabilities (i.e, the "right-hand side" of the

IX. THE FINANCING DECISIONS BY FIRMS: IMPACT OF CAPITAL STRUCTURE CHOICE ON VALUE The capital structure of a firm is defined to be the menu of the firm's liabilities (i.e, the "right-hand side" of the

MM1 - The value of the firm is independent of its capital structure (the proportion of debt and equity used to finance the firm s operations).

.") Teaching Note Miller Modigliani Consider an economy for which the Efficient Market Hypothesis holds and in which all financial assets are possibly traded (abusing words we call this The Complete Markets

Teaching Note Miller Modigliani Consider an economy for which the Efficient Market Hypothesis holds and in which all financial assets are possibly traded (abusing words we call this The Complete Markets

Chapter 7. . 1. component of the convertible can be estimated as 1100-796.15 = 303.85.

Chapter 7 7-1 Income bonds do share some characteristics with preferred stock. The primary difference is that interest paid on income bonds is tax deductible while preferred dividends are not. Income bondholders

Chapter 7 7-1 Income bonds do share some characteristics with preferred stock. The primary difference is that interest paid on income bonds is tax deductible while preferred dividends are not. Income bondholders

DUKE UNIVERSITY Fuqua School of Business. FINANCE 351 - CORPORATE FINANCE Problem Set #4 Prof. Simon Gervais Fall 2011 Term 2.

DUK UNIRSITY Fuqua School of Business FINANC 351 - CORPORAT FINANC Problem Set #4 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Suppose the corporate tax rate is 40%. Consider a firm that earns $1,000

DUK UNIRSITY Fuqua School of Business FINANC 351 - CORPORAT FINANC Problem Set #4 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Suppose the corporate tax rate is 40%. Consider a firm that earns $1,000

Tax-adjusted discount rates with investor taxes and risky debt

Tax-adjusted discount rates with investor taxes and risky debt Ian A Cooper and Kjell G Nyborg October 2004 Abstract This paper derives tax-adjusted discount rate formulas with Miles-Ezzell leverage policy,

Tax-adjusted discount rates with investor taxes and risky debt Ian A Cooper and Kjell G Nyborg October 2004 Abstract This paper derives tax-adjusted discount rate formulas with Miles-Ezzell leverage policy,

WACC and a Generalized Tax Code

WACC and a Generalized Tax Code Sven Husmann, Lutz Kruschwitz and Andreas Löffler version from 10/06/2001 ISSN 0949 9962 Abstract We extend the WACC approach to a tax system having a firm income tax and

WACC and a Generalized Tax Code Sven Husmann, Lutz Kruschwitz and Andreas Löffler version from 10/06/2001 ISSN 0949 9962 Abstract We extend the WACC approach to a tax system having a firm income tax and

Chapter 17 Capital Structure Limits to the Use of Debt

University of Science and Technology Beijing Dongling School of Economics and management Chapter 17 Capital Structure Limits to the Use of Debt Dec. 2012 Dr. Xiao Ming USTB 1 Key Concepts and Skills Define

University of Science and Technology Beijing Dongling School of Economics and management Chapter 17 Capital Structure Limits to the Use of Debt Dec. 2012 Dr. Xiao Ming USTB 1 Key Concepts and Skills Define

The Adjusted Present Value Approach to Valuing Leveraged Buyouts 1

Chapter 17 Valuation and Capital Budgeting for the Levered Firm 17A-1 Appendix 17A The Adjusted Present Value Approach to Valuing Leveraged Buyouts 1 Introduction A leveraged buyout (LBO) is the acquisition

Chapter 17 Valuation and Capital Budgeting for the Levered Firm 17A-1 Appendix 17A The Adjusted Present Value Approach to Valuing Leveraged Buyouts 1 Introduction A leveraged buyout (LBO) is the acquisition

U + PV(Interest Tax Shield)

") CHAPTER 15 Debt and Taxes Chapter Synopsis 15.1 The Interest Tax Deduction A C-Corporation pays taxes on proits ater interest payments are deducted, but it pays dividends rom ater-tax net income. Thus,

CHAPTER 15 Debt and Taxes Chapter Synopsis 15.1 The Interest Tax Deduction A C-Corporation pays taxes on proits ater interest payments are deducted, but it pays dividends rom ater-tax net income. Thus,

The Adjusted Present Value Approach to Valuing Leveraged Buyouts 1 Introduction

Chapter 18 Valuation and Capital Budgeting for the Levered Firm 18A-1 Appendix 18A The Adjusted Present Value Approach to Valuing Leveraged Buyouts 1 Introduction A leveraged buyout (LBO) is the acquisition

Chapter 18 Valuation and Capital Budgeting for the Levered Firm 18A-1 Appendix 18A The Adjusted Present Value Approach to Valuing Leveraged Buyouts 1 Introduction A leveraged buyout (LBO) is the acquisition

Problem 1 Problem 2 Problem 3

Problem 1 (1) Book Value Debt/Equity Ratio = 2500/2500 = 100% Market Value of Equity = 50 million * $ 80 = $4,000 Market Value of Debt =.80 * 2500 = $2,000 Debt/Equity Ratio in market value terms = 2000/4000

Problem 1 (1) Book Value Debt/Equity Ratio = 2500/2500 = 100% Market Value of Equity = 50 million * $ 80 = $4,000 Market Value of Debt =.80 * 2500 = $2,000 Debt/Equity Ratio in market value terms = 2000/4000

Financial Markets and Valuation - Tutorial 6: SOLUTIONS. Capital Structure and Cost of Funds

Financial Markets and Valuation - Tutorial 6: SOLUTIONS Capital Structure and Cost of Funds (*) denotes those problems to be covered in detail during the tutorial session (*) Problem 1. (Ross, Westerfield

Financial Markets and Valuation - Tutorial 6: SOLUTIONS Capital Structure and Cost of Funds (*) denotes those problems to be covered in detail during the tutorial session (*) Problem 1. (Ross, Westerfield

Leverage and Capital Structure

Leverage and Capital Structure Ross Chapter 16 Spring 2005 10.1 Leverage Financial Leverage Financial leverage is the use of fixed financial costs to magnify the effect of changes in EBIT on EPS. Fixed

Leverage and Capital Structure Ross Chapter 16 Spring 2005 10.1 Leverage Financial Leverage Financial leverage is the use of fixed financial costs to magnify the effect of changes in EBIT on EPS. Fixed

Numbers 101: Taxes, Investment, and Depreciation

The Anderson School at UCLA POL 2000-20 Numbers 101: Taxes, Investment, and Depreciation Copyright 2002 by Richard P. Rumelt. In the Note on Cost and Value over Time (POL 2000-09), we introduced the basic

The Anderson School at UCLA POL 2000-20 Numbers 101: Taxes, Investment, and Depreciation Copyright 2002 by Richard P. Rumelt. In the Note on Cost and Value over Time (POL 2000-09), we introduced the basic

Chapter 17 Does Debt Policy Matter?

Chapter 17 Does Debt Policy Matter? Multiple Choice Questions 1. When a firm has no debt, then such a firm is known as: (I) an unlevered firm (II) a levered firm (III) an all-equity firm D) I and III only

Chapter 17 Does Debt Policy Matter? Multiple Choice Questions 1. When a firm has no debt, then such a firm is known as: (I) an unlevered firm (II) a levered firm (III) an all-equity firm D) I and III only

The Adjusted-Present-Value Approach to Valuing Leveraged Buyouts 1)

") IE Aufgabe 4 The Adjusted-Present-Value Approach to Valuing Leveraged Buyouts 1) Introduction A leveraged buyout (LBO) is the acquisition by a small group of equity investors of a public or private company

IE Aufgabe 4 The Adjusted-Present-Value Approach to Valuing Leveraged Buyouts 1) Introduction A leveraged buyout (LBO) is the acquisition by a small group of equity investors of a public or private company

Corporate Finance & Options: MGT 891 Homework #6 Answers

Corporate Finance & Options: MGT 891 Homework #6 Answers Question 1 A. The APV rule states that the present value of the firm equals it all equity value plus the present value of the tax shield. In this

Corporate Finance & Options: MGT 891 Homework #6 Answers Question 1 A. The APV rule states that the present value of the firm equals it all equity value plus the present value of the tax shield. In this

EMBA in Management & Finance. Corporate Finance. Eric Jondeau

EMBA in Management & Finance Corporate Finance EMBA in Management & Finance Lecture 4: Capital Structure Limits to the Use of Debt Outline 1. Costs of Financial Distress 2. Description of Costs 3. Can

EMBA in Management & Finance Corporate Finance EMBA in Management & Finance Lecture 4: Capital Structure Limits to the Use of Debt Outline 1. Costs of Financial Distress 2. Description of Costs 3. Can

FIN 423/523 Recapitalizations

FIN 423/523 Recapitalizations Debt-for-Equity Swaps Equity-for-Debt Swaps Calls of Convertible Securities to Force Conversion optimal conversion policy Asymmetric Information What Is a Recapitalization

FIN 423/523 Recapitalizations Debt-for-Equity Swaps Equity-for-Debt Swaps Calls of Convertible Securities to Force Conversion optimal conversion policy Asymmetric Information What Is a Recapitalization

How To Decide If A Firm Should Borrow Money Or Not

Global Markets January 2006 Corporate Capital Structure Authors Henri Servaes Professor of Finance London Business School Peter Tufano Sylvan C. Coleman Professor of Financial Management Harvard Business

Global Markets January 2006 Corporate Capital Structure Authors Henri Servaes Professor of Finance London Business School Peter Tufano Sylvan C. Coleman Professor of Financial Management Harvard Business

WACC and APV. The Big Picture: Part II - Valuation

WACC and APV 1 The Big Picture: Part II - Valuation A. Valuation: Free Cash Flow and Risk April 1 April 3 Lecture: Valuation of Free Cash Flows Case: Ameritrade B. Valuation: WACC and APV April 8 April

WACC and APV 1 The Big Picture: Part II - Valuation A. Valuation: Free Cash Flow and Risk April 1 April 3 Lecture: Valuation of Free Cash Flows Case: Ameritrade B. Valuation: WACC and APV April 8 April

EMBA in Management & Finance. Corporate Finance. Eric Jondeau

EMBA in Management & Finance Corporate Finance EMBA in Management & Finance Lecture 5: Capital Budgeting For the Levered Firm Prospectus Recall that there are three questions in corporate finance. The

EMBA in Management & Finance Corporate Finance EMBA in Management & Finance Lecture 5: Capital Budgeting For the Levered Firm Prospectus Recall that there are three questions in corporate finance. The

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.)

") Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

Discount rates for project appraisal

Discount rates for project appraisal We know that we have to discount cash flows in order to value projects We can identify the cash flows BUT What discount rate should we use? 1 The Discount Rate and

Discount rates for project appraisal We know that we have to discount cash flows in order to value projects We can identify the cash flows BUT What discount rate should we use? 1 The Discount Rate and

The Cost of Capital and Optimal Financing Policy in a. Dynamic Setting

The Cost of Capital and Optimal Financing Policy in a Dynamic Setting February 18, 2014 Abstract This paper revisits the Modigliani-Miller propositions on the optimal financing policy and cost of capital

The Cost of Capital and Optimal Financing Policy in a Dynamic Setting February 18, 2014 Abstract This paper revisits the Modigliani-Miller propositions on the optimal financing policy and cost of capital

A Test Of The M&M Capital Structure Theories Richard H. Fosberg, William Paterson University, USA

A Test Of The M&M Capital Structure Theories Richard H. Fosberg, William Paterson University, USA ABSTRACT Modigliani and Miller (1958, 1963) predict two very specific relationships between firm value

A Test Of The M&M Capital Structure Theories Richard H. Fosberg, William Paterson University, USA ABSTRACT Modigliani and Miller (1958, 1963) predict two very specific relationships between firm value

Chapter 7: Capital Structure: An Overview of the Financing Decision

Chapter 7: Capital Structure: An Overview of the Financing Decision 1. Income bonds are similar to preferred stock in several ways. Payment of interest on income bonds depends on the availability of sufficient

Chapter 7: Capital Structure: An Overview of the Financing Decision 1. Income bonds are similar to preferred stock in several ways. Payment of interest on income bonds depends on the availability of sufficient

] (3.3) ] (1 + r)t (3.4)

![] (3.3) ] (1 + r)t (3.4)](/thumbs/39/18539117.jpg "] (3.3) ] (1 + r)t (3.4)") Present value = future value after t periods (3.1) (1 + r) t PV of perpetuity = C = cash payment (3.2) r interest rate Present value of t-year annuity = C [ 1 1 ] (3.3) r r(1 + r) t Future value of annuity

Present value = future value after t periods (3.1) (1 + r) t PV of perpetuity = C = cash payment (3.2) r interest rate Present value of t-year annuity = C [ 1 1 ] (3.3) r r(1 + r) t Future value of annuity

Practice Exam (Solutions)

") Practice Exam (Solutions) June 6, 2008 Course: Finance for AEO Length: 2 hours Lecturer: Paul Sengmüller Students are expected to conduct themselves properly during examinations and to obey any instructions

Practice Exam (Solutions) June 6, 2008 Course: Finance for AEO Length: 2 hours Lecturer: Paul Sengmüller Students are expected to conduct themselves properly during examinations and to obey any instructions

COSTS OF FINANCIAL DISTRESS AND CAPITAL STRUCTURE OF FIRMS AYDIN OZKAN. Thesis presented for the degree of D.PHIL UNIVERSITY OF YORK

COSTS OF FINANCIAL DISTRESS AND CAPITAL STRUCTURE OF FIRMS AYDIN OZKAN Thesis presented for the degree of D.PHIL UNIVERSITY OF YORK DEPARTMENT OF ECONOMICS AND RELATED STUDIES March 1996 CONTENTS Acknowledgements

COSTS OF FINANCIAL DISTRESS AND CAPITAL STRUCTURE OF FIRMS AYDIN OZKAN Thesis presented for the degree of D.PHIL UNIVERSITY OF YORK DEPARTMENT OF ECONOMICS AND RELATED STUDIES March 1996 CONTENTS Acknowledgements

Chapter 14 Assessing Long-Term Debt, Equity, and Capital Structure

I. Capital Structure (definitions) II. MM without Taxes (1958) III. MM with Taxes (1963) Chapter 14 Assessing Long-Term Debt, Equity, and Capital Structure IV. Financial Distress V. Business Risk VI. Financial

I. Capital Structure (definitions) II. MM without Taxes (1958) III. MM with Taxes (1963) Chapter 14 Assessing Long-Term Debt, Equity, and Capital Structure IV. Financial Distress V. Business Risk VI. Financial

CHAPTER 16. Financial Distress, Managerial Incentives, and Information. Chapter Synopsis

CHAPTER 16 Financial Distress, Managerial Incentives, and Information Chapter Synopsis In the previous two chapters it was shown that, in an otherwise perfect capital market in which firms pay taxes, the

CHAPTER 16 Financial Distress, Managerial Incentives, and Information Chapter Synopsis In the previous two chapters it was shown that, in an otherwise perfect capital market in which firms pay taxes, the

Wrap-up of Financing. Katharina Lewellen Finance Theory II March 11, 2003

Wrap-up of Financing Katharina Lewellen Finance Theory II March 11, 2003 Overview of Financing Financial forecasting Short-run forecasting General dynamics: Sustainable growth. Capital structure Describing

Wrap-up of Financing Katharina Lewellen Finance Theory II March 11, 2003 Overview of Financing Financial forecasting Short-run forecasting General dynamics: Sustainable growth. Capital structure Describing

1. What is a recapitalization? Why is this considered a pure capital structure change?

CHAPTER 12 CONCEPT REVIEW QUESTIONS 1. What is a recapitalization? Why is this considered a pure capital structure change? Recapitalization is an alteration of a company s capital structure to change the

CHAPTER 12 CONCEPT REVIEW QUESTIONS 1. What is a recapitalization? Why is this considered a pure capital structure change? Recapitalization is an alteration of a company s capital structure to change the

Discount Rates and Tax

Discount Rates and Tax Ian A Cooper and Kjell G Nyborg London Business School First version: March 1998 This version: August 2004 Abstract This note summarises the relationships between values, rates of

Discount Rates and Tax Ian A Cooper and Kjell G Nyborg London Business School First version: March 1998 This version: August 2004 Abstract This note summarises the relationships between values, rates of

The value of tax shields is NOT equal to the present value of tax shields

The value of tax shields is NOT equal to the present value of tax shields Pablo Fernández * IESE Business School. University of Navarra. Madrid, Spain ABSTRACT We show that the value of tax shields is

The value of tax shields is NOT equal to the present value of tax shields Pablo Fernández * IESE Business School. University of Navarra. Madrid, Spain ABSTRACT We show that the value of tax shields is

Leverage. FINANCE 350 Global Financial Management. Professor Alon Brav Fuqua School of Business Duke University. Overview

Leverage FINANCE 35 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University Overview Capital Structure does not matter! Modigliani & Miller propositions Implications for

Leverage FINANCE 35 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University Overview Capital Structure does not matter! Modigliani & Miller propositions Implications for

Corporate Finance: Final Exam

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. For partial credit, when discounting, please show the discount rate

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. For partial credit, when discounting, please show the discount rate

Cost of Capital. Katharina Lewellen Finance Theory II April 9, 2003

Cost of Capital Katharina Lewellen Finance Theory II April 9, 2003 What Next? We want to value a project that is financed by both debt and equity Our approach: Calculate expected Free Cash Flows (FCFs)

Cost of Capital Katharina Lewellen Finance Theory II April 9, 2003 What Next? We want to value a project that is financed by both debt and equity Our approach: Calculate expected Free Cash Flows (FCFs)

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II + III

SOLUTIONS RE-EXAMS 2014 II + III") TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

Financial Distress EC 1745. Borja Larrain

Financial Distress EC 1745 Borja Larrain Today: 1. Costs of financial distress. 2. Trade-off theory of capital structure. 3. Empirical estimates of the costs of financial distress. 4. Bankruptcy. Readings:

Financial Distress EC 1745 Borja Larrain Today: 1. Costs of financial distress. 2. Trade-off theory of capital structure. 3. Empirical estimates of the costs of financial distress. 4. Bankruptcy. Readings:

30-1. CHAPTER 30 Financial Distress. Multiple Choice Questions: I. DEFINITIONS

CHAPTER 30 Financial Distress Multiple Choice Questions: I. DEFINITIONS FINANCIAL DISTRESS c 1. Financial distress can be best described by which of the following situations in which the firm is forced

CHAPTER 30 Financial Distress Multiple Choice Questions: I. DEFINITIONS FINANCIAL DISTRESS c 1. Financial distress can be best described by which of the following situations in which the firm is forced

NORTHWESTERN UNIVERSITY J.L. KELLOGG GRADUATE SCHOOL OF MANAGEMENT

NORTHWESTERN UNIVERSITY J.L. KELLOGG GRADUATE SCHOOL OF MANAGEMENT Tim Thompson Finance D42 Fall, 1997 Teaching Note: Valuation Using the Adjusted Present Value (APV) Method vs. Adjusted Discount Rate

NORTHWESTERN UNIVERSITY J.L. KELLOGG GRADUATE SCHOOL OF MANAGEMENT Tim Thompson Finance D42 Fall, 1997 Teaching Note: Valuation Using the Adjusted Present Value (APV) Method vs. Adjusted Discount Rate

Part 9. The Basics of Corporate Finance

Part 9. The Basics of Corporate Finance The essence of business is to raise money from investors to fund projects that will return more money to the investors. To do this, there are three financial questions

Part 9. The Basics of Corporate Finance The essence of business is to raise money from investors to fund projects that will return more money to the investors. To do this, there are three financial questions

Cost of Capital and Project Valuation

Cost of Capital and Project Valuation 1 Background Firm organization There are four types: sole proprietorships partnerships limited liability companies corporations Each organizational form has different

Cost of Capital and Project Valuation 1 Background Firm organization There are four types: sole proprietorships partnerships limited liability companies corporations Each organizational form has different

The Assumptions and Math Behind WACC and APV Calculations

The Assumptions and Math Behind WACC and APV Calculations Richard Stanton U.C. Berkeley Mark S. Seasholes U.C. Berkeley This Version October 27, 2005 Abstract We outline the math and assumptions behind

The Assumptions and Math Behind WACC and APV Calculations Richard Stanton U.C. Berkeley Mark S. Seasholes U.C. Berkeley This Version October 27, 2005 Abstract We outline the math and assumptions behind

Chapter 9. Year Revenue COGS Depreciation S&A Taxable Income After-tax Operating Income 1 $20.60 $12.36 $1.00 $2.06 $5.18 $3.11

Chapter 9 9-1 We assume that revenues and selling & administrative expenses will increase at the rate of inflation. Year Revenue COGS Depreciation S&A Taxable Income After-tax Operating Income 1 $20.60

Chapter 9 9-1 We assume that revenues and selling & administrative expenses will increase at the rate of inflation. Year Revenue COGS Depreciation S&A Taxable Income After-tax Operating Income 1 $20.60

Internal Equity, Taxes, and Capital Structure

Internal Equity, Taxes, and Capital Structure Jonathan Lewellen Dartmouth College and NBER [email protected] Katharina Lewellen Dartmouth College [email protected] Revision: March

Internal Equity, Taxes, and Capital Structure Jonathan Lewellen Dartmouth College and NBER [email protected] Katharina Lewellen Dartmouth College [email protected] Revision: March

GESTÃO FINANCEIRA II PROBLEM SET 5 SOLUTIONS (FROM BERK AND DEMARZO S CORPORATE FINANCE ) LICENCIATURA UNDERGRADUATE COURSE

LICENCIATURA UNDERGRADUATE COURSE") GESTÃO FINANCEIRA II PROBLEM SET 5 SOLUTIONS (FROM BERK AND DEMARZO S CORPORATE FINANCE ) LICENCIATURA UNDERGRADUATE COURSE 1 ST SEMESTER 2010-2011 Chapter 18 Capital Budgeting and Valuation with Leverage

GESTÃO FINANCEIRA II PROBLEM SET 5 SOLUTIONS (FROM BERK AND DEMARZO S CORPORATE FINANCE ) LICENCIATURA UNDERGRADUATE COURSE 1 ST SEMESTER 2010-2011 Chapter 18 Capital Budgeting and Valuation with Leverage

t = 1 2 3 1. Calculate the implied interest rates and graph the term structure of interest rates. t = 1 2 3 X t = 100 100 100 t = 1 2 3

MØA 155 PROBLEM SET: Summarizing Exercise 1. Present Value [3] You are given the following prices P t today for receiving risk free payments t periods from now. t = 1 2 3 P t = 0.95 0.9 0.85 1. Calculate

MØA 155 PROBLEM SET: Summarizing Exercise 1. Present Value [3] You are given the following prices P t today for receiving risk free payments t periods from now. t = 1 2 3 P t = 0.95 0.9 0.85 1. Calculate

CHAPTER 8. Problems and Questions

CHAPTER 8 Problems and Questions 1. Plastico, a manufacturer of consumer plastic products, is evaluating its capital structure. The balance sheet of the company is as follows (in millions): Assets Liabilities

CHAPTER 8 Problems and Questions 1. Plastico, a manufacturer of consumer plastic products, is evaluating its capital structure. The balance sheet of the company is as follows (in millions): Assets Liabilities

The Debt-Equity Trade Off: The Capital Structure Decision

The Debt-Equity Trade Off: The Capital Structure Decision Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable

The Debt-Equity Trade Off: The Capital Structure Decision Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable

1. CFI Holdings is a conglomerate listed on the Zimbabwe Stock Exchange (ZSE) and has three operating divisions as follows:

and has three operating divisions as follows:") NATIONAL UNIVERSITY OF SCIENCE AND TECHNOLOGY FACULTY OF COMMERCE DEPARTMENT OF FINANCE BACHELOR OF COMMERCE HONOURS DEGREE IN FINANCE PART II 2 ND SEMESTER FINAL EXAMINATION MAY 2005 CORPORATE FINANCE

NATIONAL UNIVERSITY OF SCIENCE AND TECHNOLOGY FACULTY OF COMMERCE DEPARTMENT OF FINANCE BACHELOR OF COMMERCE HONOURS DEGREE IN FINANCE PART II 2 ND SEMESTER FINAL EXAMINATION MAY 2005 CORPORATE FINANCE

University of Waterloo Midterm Examination

Student number: Student name: ANONYMOUS Instructor: Dr. Hongping Tan Duration: 1.5 hours AFM 371/2 Winter 2011 4:30-6:00 Tuesday, March 1 This exam has 12 pages including this page. Important Information:

Student number: Student name: ANONYMOUS Instructor: Dr. Hongping Tan Duration: 1.5 hours AFM 371/2 Winter 2011 4:30-6:00 Tuesday, March 1 This exam has 12 pages including this page. Important Information:

CHAPTER 13 Capital Structure and Leverage

CHAPTER 13 Capital Structure and Leverage Business and financial risk Optimal capital structure Operating Leverage Capital structure theory 1 What s business risk? Uncertainty about future operating income

CHAPTER 13 Capital Structure and Leverage Business and financial risk Optimal capital structure Operating Leverage Capital structure theory 1 What s business risk? Uncertainty about future operating income

Chapter 12. Preferred Stocks - 1. Preferred Stocks and Convertibles

Preferred Stocks - 1 Chapter 12 Preferred Stocks and Convertibles Preferred Stocks Valuing and Investing in Preferreds Convertibles Valuing and Investing in Convertibles Preferred stocks have preference

Preferred Stocks - 1 Chapter 12 Preferred Stocks and Convertibles Preferred Stocks Valuing and Investing in Preferreds Convertibles Valuing and Investing in Convertibles Preferred stocks have preference

Use the table for the questions 18 and 19 below.

Use the table for the questions 18 and 19 below. The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 1 3 4 5 Price

Use the table for the questions 18 and 19 below. The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 1 3 4 5 Price

Chapter 17: Financial Statement Analysis

FIN 301 Class Notes Chapter 17: Financial Statement Analysis INTRODUCTION Financial ratio: is a relationship between different accounting items that tells something about the firm s activities. Purpose

FIN 301 Class Notes Chapter 17: Financial Statement Analysis INTRODUCTION Financial ratio: is a relationship between different accounting items that tells something about the firm s activities. Purpose

Estimating Cash Flows

Estimating Cash Flows DCF Valuation 1 Steps in Cash Flow Estimation Estimate the current earnings of the firm If looking at cash flows to equity, look at earnings after interest expenses - i.e. net income

Estimating Cash Flows DCF Valuation 1 Steps in Cash Flow Estimation Estimate the current earnings of the firm If looking at cash flows to equity, look at earnings after interest expenses - i.e. net income

CHAPTER 20. Hybrid Financing: Preferred Stock, Warrants, and Convertibles

CHAPTER 20 Hybrid Financing: Preferred Stock, Warrants, and Convertibles 1 Topics in Chapter Types of hybrid securities Preferred stock Warrants Convertibles Features and risk Cost of capital to issuers

CHAPTER 20 Hybrid Financing: Preferred Stock, Warrants, and Convertibles 1 Topics in Chapter Types of hybrid securities Preferred stock Warrants Convertibles Features and risk Cost of capital to issuers

Finding the Right Financing Mix: The Capital Structure Decision. Aswath Damodaran 1

Finding the Right Financing Mix: The Capital Structure Decision Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate

Finding the Right Financing Mix: The Capital Structure Decision Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate

Homework Assignment #1: Answer Key

Econ 497 Economics of the Financial Crisis Professor Ickes Spring 2012 Homework Assignment #1: Answer Key 1. Consider a firm that has future payoff.supposethefirm is unlevered, call the firm and its shares

Econ 497 Economics of the Financial Crisis Professor Ickes Spring 2012 Homework Assignment #1: Answer Key 1. Consider a firm that has future payoff.supposethefirm is unlevered, call the firm and its shares

UNIVERSITY OF WAH Department of Management Sciences

BBA-330: FINANCIAL MANAGEMENT UNIVERSITY OF WAH COURSE DESCRIPTION/OBJECTIVES The module aims at building competence in corporate finance further by extending the coverage in Business Finance module to

BBA-330: FINANCIAL MANAGEMENT UNIVERSITY OF WAH COURSE DESCRIPTION/OBJECTIVES The module aims at building competence in corporate finance further by extending the coverage in Business Finance module to

Financial Statement Analysis!

Financial Statement Analysis! The raw data for investing Aswath Damodaran! 1! Questions we would like answered! Assets Liabilities What are the assets in place? How valuable are these assets? How risky

Financial Statement Analysis! The raw data for investing Aswath Damodaran! 1! Questions we would like answered! Assets Liabilities What are the assets in place? How valuable are these assets? How risky

Lecture 6. Forecasting Cash Flow Statement

Lecture 6 Forecasting Cash Flow Statement Takeaways from income statement and balance sheet forecasting Elias Rantapuska / Aalto BIZ Finance 2 Note on our discussion today Discussion today: Rather high-level

Lecture 6 Forecasting Cash Flow Statement Takeaways from income statement and balance sheet forecasting Elias Rantapuska / Aalto BIZ Finance 2 Note on our discussion today Discussion today: Rather high-level

HEALTHCARE FINANCE: AN INTRODUCTION TO ACCOUNTING AND FINANCIAL MANAGEMENT. Online Appendix A Financial Ratios

HEALTHCARE FINANCE: AN INTRODUCTION TO ACCOUNTING AND FINANCIAL MANAGEMENT Online Appendix A Financial Ratios INTRODUCTION In Chapter 17, we indicated that ratio analysis is a technique commonly used to

HEALTHCARE FINANCE: AN INTRODUCTION TO ACCOUNTING AND FINANCIAL MANAGEMENT Online Appendix A Financial Ratios INTRODUCTION In Chapter 17, we indicated that ratio analysis is a technique commonly used to

Cash Flow, Taxes, and Project Evaluation. Remember Income versus Cashflow

Cash Flow, Taxes, and Project Evaluation Of the four steps in calculating NPV, the most difficult is the first: Forecasting cash flows. We now focus on this problem, with special attention to What is cash

Cash Flow, Taxes, and Project Evaluation Of the four steps in calculating NPV, the most difficult is the first: Forecasting cash flows. We now focus on this problem, with special attention to What is cash

The Impact of Capital Structure Determinants on Small and Medium size Enterprise Leverage

Södertörn University Institution for Social Science Master Thesis 30 hp Economics Spring Semester 2013 The Impact of Capital Structure Determinants on Small and Medium size Enterprise Leverage An Empirical

Södertörn University Institution for Social Science Master Thesis 30 hp Economics Spring Semester 2013 The Impact of Capital Structure Determinants on Small and Medium size Enterprise Leverage An Empirical

E. V. Bulyatkin CAPITAL STRUCTURE

E. V. Bulyatkin Graduate Student Edinburgh University Business School CAPITAL STRUCTURE Abstract. This paper aims to analyze the current capital structure of Lufthansa in order to increase market value

E. V. Bulyatkin Graduate Student Edinburgh University Business School CAPITAL STRUCTURE Abstract. This paper aims to analyze the current capital structure of Lufthansa in order to increase market value

Module 1: Corporate Finance and the Role of Venture Capital Financing TABLE OF CONTENTS

1.0 FINANCING PRINCIPLES Module 1: Corporate Finance and the Role of Venture Capital Financing Financing Principles 1.01 Introduction to Financing Principles 1.02 Capitalization of a Business 1.03 Capital

1.0 FINANCING PRINCIPLES Module 1: Corporate Finance and the Role of Venture Capital Financing Financing Principles 1.01 Introduction to Financing Principles 1.02 Capitalization of a Business 1.03 Capital

BA 351 CORPORATE FINANCE. John R. Graham Adapted from S. Viswanathan LECTURE 10 THE ADJUSTED NET PRESENT VALUE METHOD

BA 351 CORPORATE FINANCE John R. Graham Adapted from S. Viswanathan LECTURE 10 THE ADJUSTED NET PRESENT VALUE METHOD FUQUA SCHOOL OF BUSINESS DUKE UNIVERSITY 1 THE ADJUSTED NET PRESENT VALUE METHOD COPING

BA 351 CORPORATE FINANCE John R. Graham Adapted from S. Viswanathan LECTURE 10 THE ADJUSTED NET PRESENT VALUE METHOD FUQUA SCHOOL OF BUSINESS DUKE UNIVERSITY 1 THE ADJUSTED NET PRESENT VALUE METHOD COPING

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

Homework Solutions - Lecture 2

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1286.12 and the treasury rate is 3.43%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1286.12 and the treasury rate is 3.43%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

On the Applicability of WACC for Investment Decisions

On the Applicability of WACC for Investment Decisions Jaime Sabal Department of Financial Management and Control ESADE. Universitat Ramon Llull Received: December, 2004 Abstract Although WACC is appropriate

On the Applicability of WACC for Investment Decisions Jaime Sabal Department of Financial Management and Control ESADE. Universitat Ramon Llull Received: December, 2004 Abstract Although WACC is appropriate

SELECTING DISCOUNT RATES FOR CASH FLOWS AND REVENUE REQUIREMENTS

SELECTING DISCOUNT RATES FOR CASH FLOWS AND REVENUE REQUIREMENTS David E. Eckmann Florida Power and Light Company and Louis C. Gapenski University of Florida AGA/EEI Presented at the Budgeting and Financial

SELECTING DISCOUNT RATES FOR CASH FLOWS AND REVENUE REQUIREMENTS David E. Eckmann Florida Power and Light Company and Louis C. Gapenski University of Florida AGA/EEI Presented at the Budgeting and Financial

Chapter 13, ROIC and WACC

Chapter 13, ROIC and WACC Lakehead University Winter 2005 Role of the CFO The Chief Financial Officer (CFO) is involved in the following decisions: Management Decisions Financing Decisions Investment Decisions

Chapter 13, ROIC and WACC Lakehead University Winter 2005 Role of the CFO The Chief Financial Officer (CFO) is involved in the following decisions: Management Decisions Financing Decisions Investment Decisions

CHAPTER 14 COST OF CAPITAL

CHAPTER 14 COST OF CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. It is the minimum rate of return the firm must earn overall on its existing assets. If it earns more than this,

CHAPTER 14 COST OF CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. It is the minimum rate of return the firm must earn overall on its existing assets. If it earns more than this,

Appendix B Weighted Average Cost of Capital

Appendix B Weighted Average Cost of Capital The inclusion of cost of money within cash flow analyses in engineering economics and life-cycle costing is a very important (and in many cases dominate) contributing

Appendix B Weighted Average Cost of Capital The inclusion of cost of money within cash flow analyses in engineering economics and life-cycle costing is a very important (and in many cases dominate) contributing

Finding the Right Financing Mix: The Capital Structure Decision

Finding the Right Financing Mix: The Capital Structure Decision Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum

Finding the Right Financing Mix: The Capital Structure Decision Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum

Copyright 2009 Pearson Education Canada

The consequence of failing to adjust the discount rate for the risk implicit in projects is that the firm will accept high-risk projects, which usually have higher IRR due to their high-risk nature, and

The consequence of failing to adjust the discount rate for the risk implicit in projects is that the firm will accept high-risk projects, which usually have higher IRR due to their high-risk nature, and

Chapter 16 Financial Distress, Managerial Incentives, and Information

Chapter 16 Financial Distress, Managerial Incentives, and Information 16-1. Gladstone Corporation is about to launch a new product. Depending on the success of the new product, Gladstone may have one of

Chapter 16 Financial Distress, Managerial Incentives, and Information 16-1. Gladstone Corporation is about to launch a new product. Depending on the success of the new product, Gladstone may have one of

CHAPTER 2 ACCOUNTING STATEMENTS, TAXES, AND CASH FLOW

CHAPTER 2 ACCOUNTING STATEMENTS, TAXES, AND CASH FLOW Answers to Concepts Review and Critical Thinking Questions 1. True. Every asset can be converted to cash at some price. However, when we are referring

CHAPTER 2 ACCOUNTING STATEMENTS, TAXES, AND CASH FLOW Answers to Concepts Review and Critical Thinking Questions 1. True. Every asset can be converted to cash at some price. However, when we are referring

DETERMINANTS OF THE CAPITAL STRUCTURE: EMPIRICAL STUDY FROM THE KOREAN MARKET

DETERMINANTS OF THE CAPITAL STRUCTURE: EMPIRICAL STUDY FROM THE KOREAN MARKET Doug S. Choi Metropolitan State University of Denver INTRODUCTION This study intends to examine the important determinants

DETERMINANTS OF THE CAPITAL STRUCTURE: EMPIRICAL STUDY FROM THE KOREAN MARKET Doug S. Choi Metropolitan State University of Denver INTRODUCTION This study intends to examine the important determinants

Capital Structure II

Capital Structure II Introduction In the previous lecture we introduced the subject of capital gearing. Gearing occurs when a company is financed partly through fixed return finance (e.g. loans, loan stock

Capital Structure II Introduction In the previous lecture we introduced the subject of capital gearing. Gearing occurs when a company is financed partly through fixed return finance (e.g. loans, loan stock

The Relationship Between Debt Financing and Market Value of Company: Empirical Study of Listed Real Estate Company of China

Proceedings of the 7th International Conference on Innovation & Management 2043 The Relationship Between Debt Financing and Market Value of Company: Empirical Study of Listed Real Estate Company of China

Proceedings of the 7th International Conference on Innovation & Management 2043 The Relationship Between Debt Financing and Market Value of Company: Empirical Study of Listed Real Estate Company of China

Capital Structure. Itay Goldstein. Wharton School, University of Pennsylvania

Capital Structure Itay Goldstein Wharton School, University of Pennsylvania 1 Debt and Equity There are two main types of financing: debt and equity. Consider a two-period world with dates 0 and 1. At

Capital Structure Itay Goldstein Wharton School, University of Pennsylvania 1 Debt and Equity There are two main types of financing: debt and equity. Consider a two-period world with dates 0 and 1. At