CSRS and FERS Benefits Calculator and Retirement Income/Expense Analyzer

|

|

|

- Nicholas Gray

- 10 years ago

- Views:

Transcription

1 CSRS and FERS Benefits Calculator and Retirement Income/Expense Analyzer Software Manual Decision Support Software LLC P.O. Box 2368 Granite Bay, CA Page 1 of 156

2 Table of Contents Program: Installation, Activation, and Deactivation (License Transfer Procedure) Getting Started Retirement Annuity (Retirement Benefit Calculations and Projections) Retirement Eligibility Creditable Service High 3 Average Military Service Deposit Redeposit Annuity Calculation FERS Supplement - Social Security CSRS Offset - Social Security WEP Calculation Thrift Savings Plan (TSP) Contributions Growth Withdrawal Insurance Federal Employees Group Life Insurance (FEGLI) Federal Employees Health Benefits Program (FEHBP) Long Term Care Insurance (LTC) Retirement Affordability Analyzer Income Analysis From Other Sources Federal Income and Inflation Analysis Expense Analysis From Other Sources Income and Expense Analysis Income Analysis From Government Sources Only Expense Analysis From Government Sources Only Income and Expense Analysis - From Government Sources Income and Expense Analysis - From Other Sources Income and Expense Analysis - From All Sources Fix Problems Printing Reports Create custom report Print the Federal Employee Benefits Analysis report Import Personal Data from an earlier program Professional Features Data Files Client Data File Operations Place Client Data in a Client Folder Retrieve Client Data from a Client Folder Delete a Client Folder List Client Folders in a Spreadsheet Send Client Folders to Another Office New 2011 Receive Client Folder from Another Office New 2011 Remove Client Data from All Forms View Sample Client Data Import Client Folders from Previous Versions of the Software Customizing Report Cover and Disclaimer Pages Data Collection Form View Advisor Information License Disclaimer and Limitations of Liability Support Page 2 of 156

3 Program Installation, Activation, and Deactivation Installation Note: The program initially runs as the FREE Personal edition. It must be activated (see below) to convert it to the FREE Personal PLUS edition or Professional edition. However, activation is not required to continue to run the FREE Personal edition. 1. To download the FREE Personal edition of the CSRS and FERS Benefits Calculator and Retirement Income/Expense Analyzer program, click here. 2. Next click on the OPEN/RUN button on the File Download message, and 3. Then, follow the directions on the screen as they are presented to install the program. Activation When the program is first installed, it runs in the Free Personal edition. An activation code is not needed to run the FREE Personal edition. However, to convert the FREE edition to the FREE Personal PLUS edition or the Professional edition, you must request a FREE Personal PLUS or Professional activation code using the procedure provided here: Deactivation - License Transfer Procedure The software license is for a single user on a single computer. Please, see the License message under the Legal menu in the Benefits Calculator program. If you would like to deactivate the program license on a computer and move it to a different computer, please send an message to Decision Support Software LLC - and ask for the procedure to do this. Page 3 of 156

4 Getting Started with the CSRS and FERS Benefits Calculator and Retirement Income/Expense Analyzer Welcome to the CSRS and FERS Benefits Calculator and Retirement Income/Expense Analyzer software program. You will find that it is the most powerful federal retirement benefits program available. By using it, you will enter your personal data, analyze your retirement benefits, and plan for an affordable retirement in just a few short hours. This is just the beginning. As you study the reports and become more aware of the details of each of the retirement benefits elements, you will change existing data and view the results to determine the impact on your retirement plan. You will print reports that will provide detailed charts and graphs that reveal the details of initial and yearly changes to your benefits during your working and retirement years. When you change your data, new reports can be printed and you can compare the results with previous reports. You will quickly master the program by following the steps in this, "Getting Started," section. In addition by following the steps here, you will avoid problems encountered when data is not entered in the proper order. Getting Help 1. This full help manual can be found: a. In the Benefits Calculator program - click on HELP ==> Software Manual, or Page 4 of 156

5 b. Click Windows Start Button ==> Programs ==> Federal Retirement Instant help is available on any form. When you need help, select 'Form Help' on the menu while working on a form. 3. Installation or Activation Problems: Support: Page 5 of 156

6 Procedure to Enter your Personal Data Data entered in the CSRS and FERS Benefits Calculator and Retirement Income/Expense Analyzer must be input in the sequence shown on this page and next. This is required as some forms get data from other forms, and failure to follow this sequence will result in data input and reporting errors. Print this page and next and follow the sequence. 1. Gather and enter your personal data on the Federal Benefits Data Collection Form. A blank data collection form can be found here: CSRS and FERS Benefits Calculator 2. Enter Retirement Annuity Data: 3. Enter Thrift Savings Plan Data: A. Contributions B. Growth C. Withdrawal Page 6 of 156

7 4. Enter Insurance Data: Retirement Income/Expense Analyzer 5. Enter Retirement Income/Expense Analyzer Data: Reports Generator 6. Reports: After you have entered all your data in the sequence listed in steps 2 through 5, you are ready to view the report pages. After you enter all your data and you want to make a change (for example change the retirement date entered in Step 2.A.), then you must revisit each form below the form where the change was made (for example, if the retirement date was changed on form 2. A., Retirement Eligibility, then all forms below 2.A. must be revisited) so that the impact of the change is calculated on all following, dependent forms. Page 7 of 156

so that the impact of the change is calculated on all following, dependent forms. Page 7 of 156")

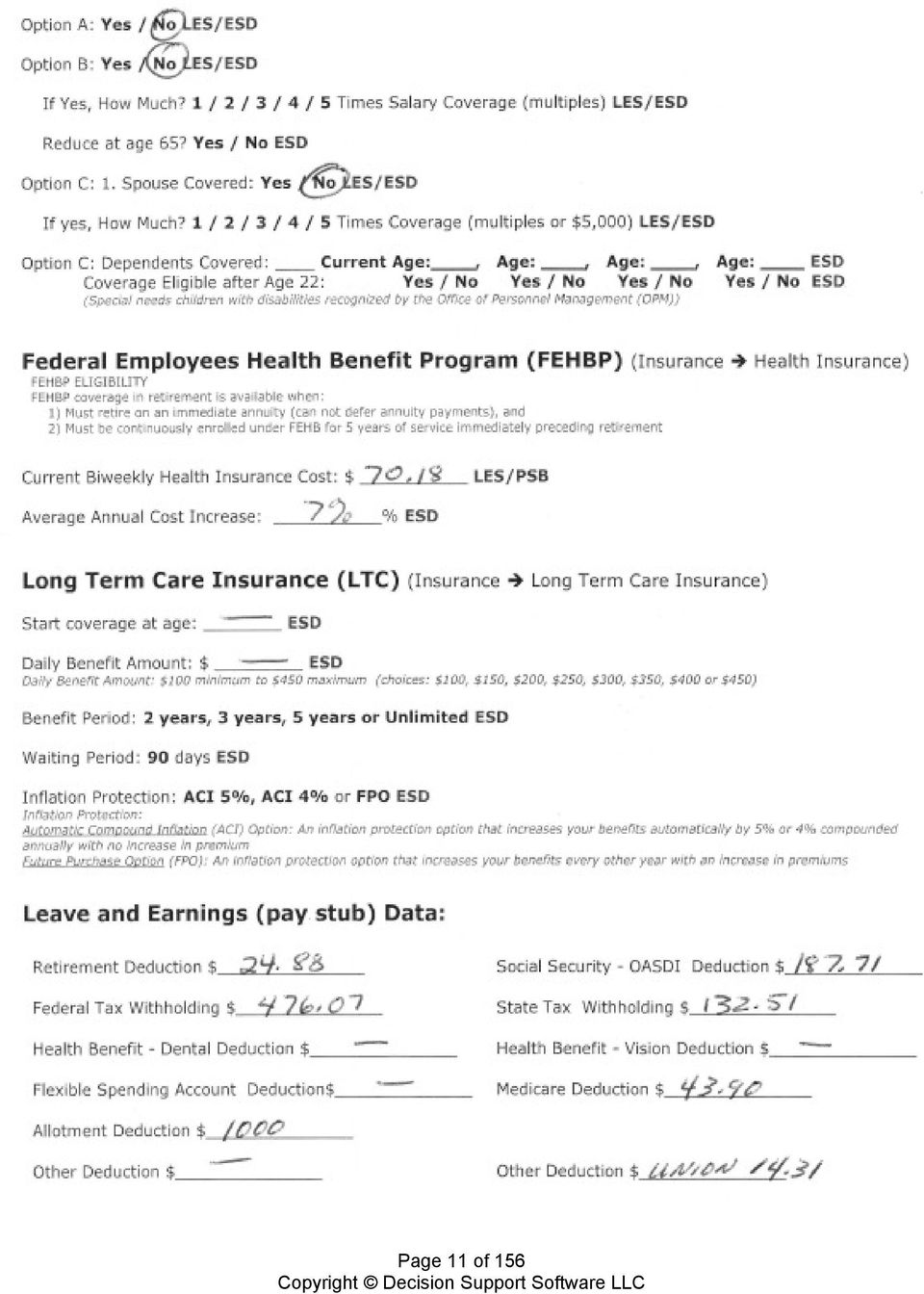

8 Sample Data Collection Form The following four pages contain sample data that will be used in the remainder of this manual. A blank data collection form can be found here: Page 8 of 156

9 Page 9 of 156

10 Page 10 of 156

11 Page 11 of 156

12 Enter Your Data For the Professional user, we have included sample benefits data so that you can view the various forms and print the report pages that you may be interested in. You can get the sample data by selecting "View Sample Data" from the "Professional" menu item. We suggest that you do this first and then read the help pages for each form. Professional edition only Page 12 of 156

13 For the Professional user, when you are ready to enter your first client's data, you must go to the "Professional" menu and select "Remove Client Data from All Forms." This will clean all sample data from all the forms. Professional edition Only If you do not do this, you will mix your first client's data with the sample data, and you will get erroneous results. Professional users must do this each time you begin to enter new client information. If this is not done, you will mix the previous client's data with the current client. Page 13 of 156

14 Benefits Calculator The Benefits Calculator section of the software contains three major sections: Annuity, Thrift Savings Plan, and Insurance The Annuity menu lists ten input forms in the order they must be worked (A. Retirement Eligibility is the first form to be filled in). CSRS must fill in Annuity forms: A. Retirement Eligibility, B. Creditable Service, C. High 3 Average, and D. Annuity Calculation. FERS must fill in Annuity forms: A. Retirement Eligibility, B. Creditable Service, C. High 3 Average, D. Annuity Calculation and E. Social Security - FERS Supplement. Page 14 of 156

15 A. On the Annuity==> Retirement Eligibility form, the following must be entered: Retirement System (CSRS, FERS or xfers (transfer from CSRS to FERS), Employee Type (Regular or Other: Firefighter, Law Enforcement or Air Traffic Controller), Retirement Type: Regular, Optional (early retirement) or Mandatory, Birth Date, Retirement - Service Computation Data (SCD), and Retirement Date (automatically calculated by clicking on "Earliest Retirement Date" button. This data is used on other forms. Personal FREE and FREE Personal PLUS users will be allowed to enter a birth date only once. Make sure it is correct as it cannot be changed. Annuity ==> Retirement Eligibility Form Page 15 of 156

16 Page 16 of 156

17 B. Annuity ==> Creditable Service Sick leave is entered on this form. Optionally, civilian and military leave can be entered on this form for you convenience to store service information for record keeping purposes, however only sick leave is needed on other forms. Military service time and civilian service time (through today) are added together and then subtracted from today's date to estimate the Service Computation Date. This is only a ball-park estimate. Annuity ==> Creditable Service Form Sick leave for CSRS and FERS is entered on this form. For FERS Employees: Creditable service is increased by 50% of the sick leave hours saved at retirement through 2013, and Creditable service is increased by 100% of the sick leave hours saved at retirement starting Page 17 of 156

.")

in the green box labeled High 3 Average, and (2) the")

18 C. On the High 3 Average form fill in your average your Current Annual Salary and your estimated January percent increase in pay (usually cost of living increase, but you should consider: step increases and promotions). Then, click on the Calculate button. Your average high 3 at retirement will be displayed in two places: (1) in the green box labeled High 3 Average, and (2) the top line of the spreadsheet (it also displays your retirement date). Annuity ==> High 3 Average Form Page 18 of 156

in the green box labeled High 3 Average, and (2) the")

19 The Annual Salary and the % Increase in January are sent to the TSP ==> Contributions Form TSP ==> Contributions Form and to the Insurance ==> FEGLI form. Insurance ==> FEGLI Form Page 19 of 156

20 If you are retiring in this calendar year and you have at least three years of salary data (pay increases and dates of increases), then you should enter the historical data in the New Salary and Change Dates windows provided on the form." This will give you a more accurate projection of your High 3 Average. First: Enter your Current Annual Salary and Percent Increase (this data is used on the TSP and FEGLI forms), then click on the RED calculate button. Second: Enter salary history (New Salary and Change Dates) in the area shown. Then, click on the Calculate button at the bottom of the form. Annuity ==> High 3 Average Form Page 20 of 156

in the area shown. Then, click on the Calculate button at the bottom of the form.")

21 D. Select Annuity Calculation from the Annuity menu. The high 3 average will be displayed from the Annuity ==> High 3 Average form. Your years of service and age at retirement will be displayed from the Annuity ==> Retirement Eligibility form. Your projected sick leave will be displayed from the Annuity ==> Creditable Service form. The top line (highlighted in read) of the spreadsheet at the bottom of the form contains your retirement annuity information. Each line below contains delayed retirement annuity information so that you can see what the benefit would be to delay your retirement one or more years (or one or more months). There are two boxes at the top of the form that require additional information that was not entered on any of the other forms: (1) Estimated High 3 Increase / Year - enter your expected percent change in high three average each year (used for projecting your high 3 beyond your chosen retirement date so you can see the effect of delaying your retirement), and (2) Annual Cost of Living Adjustment (COLA) - used to project increases in your retirement income each year after retirement. Finally, enter the Survivor Benefit. Annuity ==> Annuity Calculation Page 21 of 156

.")

.")

22 E. If you are a FERS employee, then you must select the Annuity ==> Social Security - FERS Supplement form. You will enter your projected monthly social security at age 62 that is provided annually to you from the social security administration (SSA). If you don't have your SSA information, you can get an estimate by selecting the SS Quick Calculation button. In addition, you will enter the annual social security COLA (currently averages 2.98%). If you have military service, then you will enter the years and months served. Annuity ==> Social Security - FERS Supplement Form Page 22 of 156

23 6. Now you are ready to enter your TSP data. There are three TSP input forms: Contributions, Growth, and Withdrawal. See the TSP section of this manual for details. You must enter data on all three TSP forms (Contributions, Growth and Withdrawal) or the program will not store your TSP data. Page 23 of 156

24 Page 24 of 156

a. See the respective help pages for these forms. 8. The Retirement Income/Expense Analyzer calculations are integrated with the Benefits Calculator calculations.")

25 7. After entering your TSP information, you are now ready to enter your Insurance data: FEGLI - Federal Employees Group Life Insurance, FEHBP - Federal Employees Health Benefits Program, and LTC - Long Term Care) a. See the respective help pages for these forms. 8. The Retirement Income/Expense Analyzer calculations are integrated with the Benefits Calculator calculations. Therefore, you must visit each form in the Retirement Income/Expense Analyzer before going to the Reports Generator section of the software so that report related calculations can be made. See the Retirement Income/Expense Analyzer section for details. 9. Reports Generator pages: After entering data in the Benefits Calculator and the Retirement Income/Expense Analyzer forms, you can view or print over 50 report pages. See the Report section for more detail. Page 25 of 156

* Creditable Service (Required: CSRS and FERS) High 3 Average (Required: CSRS and FERS) * Military Service Deposit Redeposit Annuity Calculation (Required: CSRS and FERS) Social")

26 Annuity To properly calculate the retirement annuity and survivor benefit, the forms listed under the Annuity menu must be filled-in in the order presented here: Retirement Eligibility (Required: CSRS and FERS) * Creditable Service (Required: CSRS and FERS) High 3 Average (Required: CSRS and FERS) * Military Service Deposit Redeposit Annuity Calculation (Required: CSRS and FERS) Social Security - FERS Supplement (Required: FERS and CSRS to FERS Transfers) Social Security - CSRS Offset (Required CSRS Offset) WEP Calculation (CSRS) If you make a change in one or more of these forms, then you must access all higher numbered forms. For example, if you change a retirement date on the Retirement Eligibility form, then you must re-access the following forms so that the calculations on these forms conform to the new date: Creditable Service (Required: CSRS and FERS) High 3 Average (Required: CSRS and FERS) * Military Service Deposit Redeposit Annuity Calculation (Required: CSRS and FERS) Social Security - FERS Supplement (Required: FERS and CSRS to FERS Transfers) Social Security - CSRS Offset (Required CSRS Offset) * The Retirement Eligibility form and the High 3 Average form must be filled in before selecting the TSP, Insurance, and the Retirement Income/Expense Analyzer forms. Page 26 of 156

, and (3) the type of retirement (Regular, Optional (early out RIF), or Mandatory for Firefighters, Law Enforcement and Air Traffic Controllers")

27 Retirement Eligibility Introduction In addition to entering your name and address information, you will enter: (1) the retirement system (CSRS, FERS, or CSRS to FERS Transfer (xfers)), (2) whether you are a regular or special provisions employee (Other), and (3) the type of retirement (Regular, Optional (early out RIF), or Mandatory for Firefighters, Law Enforcement and Air Traffic Controllers (only special provisions). By entering your birth date, retirement service computation date (SCD), transfer date (if CSRS to FERS transferee (not shown)) and retirement date, you will see if you meet minimum service time and minimum age requirements for the type of retirement you are interested in. You can use the, "Earliest Retirement Date," button to calculate the date that you are first eligible to retire. Reference OPM CSRS: Retirement Eligibility OPM FERS: Retirement Eligibility FederalRetirement.net: CSRS FERS Page 27 of 156

28 Details 1. Enter your personal information: Name, Address, City, State, and Zip code. 2. Next enter: Retirement System (CSRS, FERS or xfers (CSRS to FERS transferee)), Employee Type (Regular or Other), and Retirement Type (Regular, Optional (Early Out RIF), or Mandatory) or click on the, "Earliest," button. 3. Next, enter your: Birth Date*, Retirement - Service Computation Date (SCD) Note: the Retirement - SCD must include all Civil Service time plus Military Time, Transfer Date (if xfers), and Retirement Date or click on the, "Earliest Retirement Date," button. * Note for Personal FREE or FREE Personal PLUS users, the birth date can be entered only once. Please, check to make sure it is accurate as it cannot be changed after it is entered. Example: Page 28 of 156

29 4. Minimum Service - Years and Minimum Retirement Age data are displayed at the bottom of the form. Notice in this situation there are three regular retirement options: Example 1 - FERS Employee a. 5 Minimum Service Years and 62 Minimum Retirement Age, b. 20 Minimum Service Years and 60 Minimum Retirement Age, and c. 30 Minimum Service Years and 56 Years O months Minimum Retirement Age You must meet one of these three conditions (a., b, or c.) in order to be eligible for a regular retirement. You will see a green display at the lower right side of the form that states, Service and Age Requirements Met when the earliest (or later) retirement date is entered. In the example above, the Service at Retirement is 34 years, 0 months and 22 days, (greater than the required Minimum Service - Years) and Age at Retirement is 56 Years and 0 Months (equal to 56 years and 0 months the required Minimum Retirement Age). The Minimum Service requirement (30 years) and Minimum Age Requirement (56 years) have been met. In our next example, change the birth date to The indicator at the lower right side of the screen is now red and states, Service and Age Requirements Not Met. The required Service at Retirement is 30 years, and the requirement is met. The minimum required Age at Retirement is 56 Years and 0 Months. However, the age, in this case is 55 years and 0 months and does not meet the minimum Age at Retirement. Page 29 of 156

retirement is available.")

30 In our last example, change the birth date back to and change the SCD to The Minimum Retirement Age is OK, but the Service at Retirement has not been met for a regular FERS retirement. For a FERS employee, a Minimum Retirement Age + 10 (MRA + 10) retirement is available. In this example, the Minimum Retirement Age and Service at Retirement (10 + years) requirements have been met. However, there is a 5% reduction in annuity penalty for each year the MRA + 10 retiree is under age 62 at retirement. In this example, the retiree is 56 years and 0 months old at retirement and is 6 years and 0 months away from age 62. The penalty is a 6 x 5% = 30.00% reduction in the retirement annuity. 5. BIRTHDATE, RETIREMENT - SERVICE COMPUTATION DATE, TRANSFER DATE (if applicable), RETIREMENT DATE, CURRENT CREDITABLE SERVICE, CURRENT AGE, CSRS SERVICE AT TRANSFER (if applicable not shown), AGE AT TRANSFER (if applicable not shown), SERVICE AT Retirement, and AGE AT RETIREMENT are used by other forms. Page 30 of 156

31 Creditable Service Introduction You should review your personal records to find exact dates of Civilian Service and Military Service. You will then enter dates of service in each category. Your Civilian and Military Service Time will be calculated. You will then use this information to check your Official Personal Folder (OPF) in your personnel office to determine that your Retirement Service Computation Date (SCD) is accurate. You will enter your unused Sick Leave information, historical and planned for the future. The unused sick leave will added to your service time credit that is used to calculate your retirement annuity. Reference OPM CSRS: Creditable Service OPM CSRS Unused Sick Leave: Creditable Sick Leave OPM FERS: Creditable Service FERS Unused Sick Leave: Creditable Service FederalRetirement.net: CSRS FERS Details - Civilian Service and Military Service: Note: The Civilian and Military data entered on this form is not used in any other calculations in this Benefits Calculator or the Retirement Income/Expense Analyzer. It is not necessary to enter this data unless you want to compare your calculations with those of your personnel office or to calculate the SCD. Page 31 of 156

32 1. Start by entering your first Civil Service job at the top of the form. Enter a short description of the job, then enter the starting and ending dates underneath. Next enter your second job description and starting and ending dates. And continue this way down the form. The program requires this order (first job at top, latest job at bottom of list) to accurately calculate total service time. 2. Repeat this process for all your military time. When you have finished, you will observe your total combined civilian and military service time. You can then compare your service times (civilian and military) with those recorded in your OPF. In addition your calculated SCD is displayed this is an approximate date. SCD Calculation Example: Yeas of civilian, full-time creditable, service began on and is calculated through today Four years of military service credit ( to ) is added to civilian service. 3. The Total Creditable Service Time (Civilian + Military) is 24 years, 0 months, and 0 days 4. The Service Computation Date is calculated by subtracting Total Service Time (24 years, 0 months, and 0 days) from today's date = If you don't have your official SCD, you can use the calculated SCD. It is then entered on the Annuity ==> Retirement Eligibility form. Page 32 of 156

33 Details - Unused Sick Leave: Enter sick leave information at the right side of the form. First, enter the proposed sick leave time to be saved for each two week pay period. Enter any amount between 0 and 4 hours per two week period. Next enter the saved sick leave hours to date. Notice that the number of 2 week pay periods until your retirement is calculated (calculated using today s date and the retirement date from the Annuity ==> Retirement Eligibility form), and the sick leave hours to be saved between today and retirement are calculated. Finally, the total number of years, months and days of saved sick leave at retirement is calculated. Use of this Data 1. The Civilian and Military Service information calculated on this form are not used on any other form in this program. It is provided to ensure that your figures agree with those found in your Official Personnel Folder. However, the Civilian and Military service time can be used to calculate the actual Retirement Service Computation Date illustrated above. 2. The Sick Leave data is used by the Annuity ==> Annuity Calculation form to add to the total service time for annuity calculations only and not for minimum service determination. Page 33 of 156

34 High 3 Average Introduction If you will retire after this year, then the High 3 averaged is estimated using your current salary and an estimated increase in annual salary. If you will retire this year, you will review personal records to find dates and amounts of pay increases covering, at least the last three to four years. After entering this information into this form, the High 3 average at retirement will be calculated. Reference OPM Computation Example: High 3 Average OPM CSRS: High 3 Average OPM FERS: High 3 Average FederalRetirement.net: CSRS FERS Details Projection Method - Retirement Next Year or Later: 1. If your retirement date is in the next calendar year or later, you will estimate your Hi 3 average to retirement. 2. Enter your Current Annual Salary. 3. Enter your expected average annual pay Increase (% Increase in January). Consider annual cost-of-living Page 34 of 156

35 adjustments, step increases, and promotions. 4. Click on the Calculate button. Example: Details Current Year Method Retiring this year: 1. Start by entering your Current Annual Salary, and your estimated Percent Increase Each January as described in the previous section. Then click on the RED calculate button towards the top of the form (see step 1 above in the picture). This is entered as this data is needed on the TSP and FEGLI forms. Page 35 of 156

36 2. Next enter the latest pay change date and amount (see above). Then enter previous pay change dates and amounts in chronological order. 3. If dates are not in order, dates are missing, or dates are wrong, the High 3 calculation will be in error. Therefore, extensive date error checking was added to this form to ensure accuracy of date entries. If a mistake is made, an error message will explain the problem. To insert or delete a date and amount, place the mouse cursor on the appropriate date, click the mouse, then click on the Insert Line or Delete Line button. 4. After entering the pay change information, click on the Calculate button located at the bottom of the form. 5. Any errors in the dates will be displayed as stated above. 6. The green, High 3 Average window displays the high 3 average on your retirement date (it is also displayed on the top line of the spreadsheet on the right side of the form). Note, if a pay increase occurs after today but before your retirement date, it will not be reflected in the high 3 average at retirement. To overcome this, you can predict a pay change date and amount and enter this in the latest Date Effective and Annual Pay columns on the form. 7. The spreadsheet lists monthly High 3 averages and changes in High 3 averages from one month to the next. Small variations from one month to the next occur because the number of days in each month are different. Gradual trends up in the monthly High 3 average are a result of larger pay increases or shorter duration Page 36 of 156

37 between pay changes. Gradual trends down in the monthly High 3 average occur due to smaller pay increases or longer duration between pay changes. 8. The calculated High 3 average from this form is sent to the Annuity ==> Annuity Calculation form. Therefore, the information on this form must be entered before working on the Annuity ==> Annuity Calculation form. If you are retiring this calendar year, then you should enter Pay Changes and Dates in the individual boxes provided on the form instead of projecting your high 3. This will give you a more accurate calculation of your High 3 Average. However, you must first use the "Project Hi 3 to Retirement" method first as the data created by it is used in the TSP and FEGLI forms. Page 37 of 156

38 Military Service Introduction You will answer a few questions regarding military service to include dates and Social Security deposits, and you will receive information on deposit requirements, deposit due dates and interest rate information. The data collected on this form is not used on any other form. Reference OPM CSRS: Military Service OPM FERS: Military Service FederalRetirement.net: CSRS - FERS Details CSRS 1. Answer the questions on the left side of the screen by selecting one of the two buttons in two or more of the statement boxes. Depending on how the selections are made, other statement boxes will be enabled or disabled. The general response to the selections made will be displayed at the bottom of the screen in the big box on the left. There will be general information covering: impacts on making (or not making) a deposit for Page 38 of 156

39 military service time. Social security and military credit applied to civil service credit and the type of interest (fixed or variable) to be charged with the deposit will be displayed. FERS 1. Answer the questions on the right side of the screen by selecting one of the two buttons in one or more of the statement boxes. Depending on how selections are made, the bottom statement box will be enabled or disabled. The general response to the statements will be displayed at the bottom of the screen in the big box to the right. There will be general information covering impacts of making (or not making) a deposit for military service time. Military credit applied to civil service credit and whether interest will or will not be charged for the deposit. CSRS and FERS 1. The screen provides only very general information. Please consult your personnel department for specific answers on military service as applied to civil service 2. No data from this form is used by any other form, however a report page is available that provides military service information. Page 39 of 156

. You will review the consequences of not paying the deposit and interest.")

40 Deposit Introduction You will enter the period of time (if any) where deductions from Civil Service income were not deposited in a retirement system (CSRS or FERS). You will determine how much is owed (deposit and interest). You will review the consequences of not paying the deposit and interest. Reference OPM CSRS: Deposit - Performed CSRS service where no retirement deductions were withheld from your pay OPM FERS: Deposit - Performed FERS service where no retirement deductions were withheld from your pay Details 1. Enter the beginning date and ending date when deductions for a retirement system were not withheld. Enter the deposit owed for this period. You will probably need to contact the personnel office for this information. 2. Do not enter a Deposit to be Paid On This Date at this point. 3. Click on the Calculate Deposit button. (a) If the deposit period ended before , the program will calculate the Interest and the Total Deposit owed on the Retirement Date. (b) If the deposit period ended on or after , the program will calculate the Service Time Earned Page 40 of 156

41 during this Period and deduct it from the Total Service at Retirement. (c) Either the Total Deposit Owed (3.a) or Service Time Earned during this period (3.b) will be sent to the Annuity ==> Annuity Calculation form for adjustment of the retirement annuity. 4. If the intent is to make a deposit or a deposit was previously made, enter the deposit date in the Deposit to be Paid On This Date field. Then click on the Calculate Deposit button. 5. General information is provided at the top of this form as to the annuity impacts of making or not making a deposit for non-deduction period of time before and after Caution Make sure that you push the CALCULATE DEPOSIT button before leaving this form. The data displayed on the form is passed to the Annuity ==> Annuity Calculation form. If you make changes or just review this form without pushing the Calculate DEPOSIT button, erroneous data will be processed by the Annuity ==> Annuity Calculation form. Page 41 of 156

42 Redeposit Introduction You will enter the civil service period of time for which a refund of retirement deposits was received. You will determine how much is owed (redeposit and interest). You will review the consequences of not paying the redeposit and interest. Reference OPM CSRS: Redeposit - A redeposit is the repayment of retirement deductions that were previously withheld and refunded to you, plus interest. FERS: Redeposit FederalRetirement.net: CSRS-FERS Details 1. Enter the beginning date and ending date where deductions for the retirement system were made and were later received as a refund of these deductions. Enter the amount refunded for this period. Enter the date the refund was received. You may need to contact the personnel office for this information. 2. Do not enter a Redeposit to be Paid On This Date at this point. Page 42 of 156

If the redeposit period ended on or after 10-01-1990, the program will calculate the Service Time Earned During Refund Period and deduct it from the Total Service at Retirement.")

43 3. Click on the Calculate Redeposit button. (a) If the redeposit period ended before , the program will calculate the Interest and the Total Redeposit Owed on the Retirement Date. (b) If the redeposit period ended on or after , the program will calculate the Service Time Earned During Refund Period and deduct it from the Total Service at Retirement. (c) Either the Total Redeposit Owed (3.a) or Service Time Earned During Refund Period (3.b) will be sent to the Annuity ==> Annuity Calculation form for adjustment of the retirement annuity. 4. If a redeposit will be made or has already been made, enter the redeposit date in the Redeposit to be Paid On This Date field. Then click on the Calculate Redeposit button. 5. General information is provided at the top of this form as to the annuity impacts of making or not making a redeposit for the refund period of time before and after Caution Make sure that you click on the CALCULATE REDEPOSIT button before leaving this form. The data displayed on the form is passed to the Annuity ==> Annuity Calculation form. If you make changes or just review this form without pushing the Calculate REDEPOSIT button, erroneous data will be processed by the Annuity ==> 7 Annuity Calculation form. Example: (taken from FERS: Redeposit) The following example illustrates the total cost of a redeposit including the interest charges: Joseph was a federal employee from 1985 through In November 1998, Joseph left federal service and withdrew all of his FERS contributions -- a total of $8,000. Joseph returned to federal service in Because the redeposit law for FERS employees changed in 2011, Joseph would now like to redeposit his withdrawn FERS contributions. If he does, he will be able to get credit for 13.5 years of service, from 1985 to 1998, for FERS eligibility and FERS annuity computation purposes. The following table summarizes what Joseph owes for his redeposit after withdrawing the $8,000 of FERS contributions when he left federal service in 1998: Joseph therefore owes for his FERS redeposit a total of $14,517 as of the end of By redepositing the full $14,517, Joseph will add 13.5 years to his FERS service. In so doing, Joseph's redeposit is also adding 13.5 percent (13.5 years times 1.0 percent) to his FERS annuity each year if he retires before 62. For example, if Joseph's high-three average salary is $100,000, he will add 13.5 percent of $100,000, or $13,500 a year to his annuity for the rest of his life. In other words, it will take slightly more than one year after Page 43 of 156

44 Joseph retires to be reimbursed for his $14,517 redeposit. The "breakpoint" for Joseph's redeposit is therefore approximately 13 months. If Joseph retires after age 62 with at least 20 years of service, he will add 14.9 (13.5 times 1.1 percent) percent to his FERS annuity with a "breakpoint" of slightly less than one year. Application to Make Service Credit Payment - FERS are available for download at: Page 44 of 156

or 11 years (max.)).")

45 Annuity Calculation Introduction This form calculates the retirement annuity. You will review the interaction of many variables that affect the retirement annuity and the survivor benefit. You will view the change in annuity by delaying the retirement for a period of time (11 months (max.) or 11 years (max.)). Reference: OPM CSRS: Benefits Calculation OPM FERS: Benefits Calculation FederalRetirement.net: CSRS-FERS Details 1. Input Data. This form gets its data from the following sources: Annuity ==> Retirement Eligibility (Age at Retirement (years and months), Service Years and Months at Retirement, Retirement System, Employee Type, Employee Skill, and Retirement Type), Annuity ==> Creditable Service (Sick Leave only), Page 45 of 156

46 Annuity ==> High 3 Average (Hi 3 Average amount), Annuity ==> Deposit (Annual Deposit Penalty - either an amount or years/months), and Annuity ==> Redeposit (Annual Redeposit Penalty - either an amount or years/months). In the data boxes found at the top of the form, the: Estimated High 3 Increase/Year, and (COLA) in Retirement are the only inputs that do not come from other forms. High 3 Average at Retirement, Years and Months of Service at Retirement, and Age at Retirement in Years and Months can be temporarily changed directly on the form but will not be saved. This allows for temporary testing of changes to these inputs. 2. The spreadsheet at the bottom of the form can be scrolled vertically and horizontally. It displays the results of all the calculations made from the inputs listed in paragraph 1. No input can be made on the spreadsheet; it is for the display of data only. The top line of the spreadsheet displays the data on the retirement date (selected on the Annuity ==> Retirement Eligibility Form). The top line of the spreadsheet is the source of data for many report pages: Analysis Summary, Retirement Data, Annuity, Benefits Cost, and Others. 3. By selecting the View Data - Years, projections from the retirement date out 11 years can be reviewed on the spreadsheet. These years appear below the top line (selected Retirement Year on the Annuity ==> Retirement Eligibility form) of the spreadsheet. The spreadsheet lines are presented to show what the impact would be to delay a retirement one or more years. Since the High 3 cannot be accurately calculated (without future pay increase and date information) for the future, you will need to estimate an annual percent increase for projection purposes (see the 3. High 3 Average form for monthly historical averages) and enter it in the Estimated High 3 Increase/Year data box. By selecting the View Data - Months, projections from the retirement date (top line of spreadsheet) out 11 months can be reviewed. This data is presented to show what the impact would be to delay a retirement one or more months. A Change in Hi 3 Average is intentionally not incorporated in the View Data Month option. 4. At times, some of the rows on the spreadsheet may be colored with a red background. This indicates that the Service at Retirement and/or Age at Retirement requirements (see Annuity ==> Retirement Eligibility form) for the Retirement Type selected have not been met (both CSRS and FERS). A yellow background indicates eligibility for a reduced benefit under FERS (MRA + 10 option) only. 5. By clicking on the Clear Form button, you can enter what-if data on the form at the top and observe the results on the spreadsheet. The data that you enter on this form is only temporary and will be lost when you exit the form. When you return to the form data will come from the forms listed in paragraph 1. Page 46 of 156

47 6. The CSRS Survivor control (up and down arrows) can adjust the Survivor Annuity between 0% and 100% in 1% increments. As shown on the form, with the control set to 100% the Survivor Annuity is calculated as 55% of the No Survivor Annuity amount. This control is only visible if the Retirement System is CSRS. Example CSRS Survivor Benefit Selection 7. The FERS Survivor control can be set for a 0%, 25%, or a 50% benefit. This control is only visible if the Retirement System is FERS or xfers (CSRS to FERS transfer employee). Example FERS Survivor Benefit Selection 8. The spreadsheet at the bottom of the screen displays the full Annual and full Monthly Annuity Amounts (No Survivor and With Survivor). Page 47 of 156

48 9. The Annual Cost of Living Adjustment (COLA) is used for projecting increases in the retirement annuity and survivor benefit in the report forms. It is not used in any of the calculations on this form. You can review COLA history by selecting the, "History," button. Cost of Living In Retirement Entry Page 48 of 156

Penalties) for each system are displayed.")

49 10. If the Retirement System is XFERS (CSRS to FERS transfer employee selected on the Annuity ==> Retirement Eligibility form), a Transfer Details button will appear under the Clear Form button. When selected, details are revealed as to Service Time in each Retirement System (CSRS and FERS), Annual Annuity in CSRS and FERS are displayed, and Early Retirement penalties (Annual Under Minimum Retirement Age (MRA) Penalties) for each system are displayed. This form generates data for the following report pages: Analysis Summary, Retirement Data, Retirement Benefit, Annuity, Benefits Cost, and Others Example: Page 49 of 156

50 FERS Supplement - Social Security Introduction The FERS Supplement is a benefit paid until age 62 to certain FERS employees who retire before age 62 and who are entitled to an immediate annuity. The supplement approximates the value of FERS service in a Social Security benefit. The general purpose of the supplement is to provide a level of income before age 62 similar to what the retiree will receive at age 62 as part of a Social Security benefit, if eligible for Social Security at that age. The supplement stops at age 62 even if the FERS retiree is not eligible for Social Security. Reference OPM: FERS Supplement FederalRetirement.net: FERS Supplement Details 1. The FERS Supplement form gets data from the following source forms: Annuity ==> Retirement Eligibility: a. Age at Retirement, and b. FERS Service at Retirement, and Annuity ==> Annuity Calculation: a. FERS Annuity and b. Annual FERS Annuity COLA Page 50 of 156

51 These forms (Annuity ==> Retirement, and Annuity ==> Annuity Calculation) must be filled in before working on the FERS Supplement form. 2. Data is recorded on the FERS Supplement form: a. Monthly Social Security at Age 62 - this is found on the "Your Social Security Statement," sent to you from the IRS. Enter the monthly amount shown on page 2 that states, "At age 62, your payment would be about..." If you don't have your social security statement, you can obtain an estimate by clicking on the Calculator button. b. Annual Social Security COLA - The Social Security Act specifies a formula for determining the COLA. In general, the COLA is equal to the percentage increase in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of one year to the third quarter of the next. The following table was taken from the Social Security Administration, History of Automatic Cost-Of-Living Adjustments fact sheet. From the table below, the average COLA = 2.70% Table from: 3. Enter Years and Months of Military service. 4. The FERS Supplement is calculated: Years of FERS service (minus military service) divided by 40 times the Monthly Social Security at Age 62. For example, from the Figure Above: Years of FERS service = 34 years + 0 months Monthly Social Security at Age 62 = $1,459 Calculation: (34 months) divided by (40) times ($1,459) = $1240 (rounded). 5. The spreadsheet at the bottom of the FERS Supplement form can be scrolled vertically. It displays the results of all the calculations made from the inputs listed in paragraphs 1 and 2. No input can be made on the spreadsheet; it is for display of data only. The spreadsheet data can be printed by selecting the FERS Supplement report page in the menu. Page 51 of 156

, however there is an Annuity COLA and FERS Supplement COLA, starting the second year of retirement. 7.")

52 6. For regular FERS employees, there is no cost-of-living adjustment (COLA) for the FERS annuity until age 62, and no COLA for the FERS supplement. For Special Provisions employees (Firefighters, Law Enforcement, and Air Traffic Controllers), however there is an Annuity COLA and FERS Supplement COLA, starting the second year of retirement. 7. You can waive starting Social Security Benefits at age 62. However, FERS Supplement payments stop at age 62. After you enter the "Monthly Social Security at Age 62, Enter the desired Start Age of Social Security and enter Social Security Amount at Start Age. Example: Page 52 of 156

53 CSRS Offset - Social Security Introduction At retirement, CSRS Offset employee benefits are computed in the same manner as any regular CSRS employee if under age 62. The full CSRS annuity benefit is paid until age 62, when the CSRS Offset retiree is eligible for Social Security. At age 62, the CSRS retirement benefit is recomputed to take into account the years of service the employee was covered under both CSRS Offset and Social Security. At age 62, the CSRS annuity is then permanently reduced (offset) by the portion of the Social Security retirement benefit that is attributable to the period of time the employee was covered by both systems. The CSRS Offset employee will receive Social Security benefits at age 62, however the CSRS annuity will be reduced. The CSRS Offset is the lesser of (1) Social Security earnings attributable to Offset service or (2) the total Social Security benefit multiplied by a fraction (number of CSRS Offset years divided by 40). Reference OPM: CSRS Offset Details Page 53 of 156

54 1. The CSRS Offset form gets data from the following source forms: Annuity ==> Retirement Eligibility a. Age at Retirement, and b. CSRS Service at Retirement Annuity ==> Annuity Calculation. a. CSRS Annuity and b. Annual CSRS Annuity COLA These forms: Annuity ==> Retirement Eligibility, and Annuity ==> Annuity Calculation, must be filled in before working on the CSRS Offset form. 2. Data recorded on the CSRS offset form: a. Monthly Social Security at Age 62 - this is found on the "Your Social Security Statement," sent to you each your from the SSA. Enter the monthly amount shown on page 2 that states, "At age 62, your payment would be about..." If you don't have your social security statement, you can obtain an estimate by clicking on the Calculator button. b. Monthly Social Security - Amount Attributable to Offset at Age 62 - you must contact the Social Security Administration an ask for this amount (however, your are not likely to get it). If the information is not available, then set the amount to zero. c. Annual Social Security COLA - The Social Security Act specifies a formula for determining the COLA. In general, the COLA is equal to the percentage increase in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of one year to the third quarter of the next. The following table was taken from the Social Security Administration, History of Automatic Cost-Of-Living Adjustments fact sheet. From the table below, the average COLA = 2.70% Table from: d. Start Offset Employment - Date that CSRS Offset service began. 3. The spreadsheet at the bottom of the CSRS Offset form displays the results of all the calculations made from the inputs listed in paragraphs 1 and 2. No input can be made on the spreadsheet; it is for display of data only. Page 54 of 156

55 The spreadsheet data can be printed by selecting the CSRS Offset report page on the report form. 4. The CSRS Offset is calculated: Monthly Social Security at Age 62 times Years of CSRS Offset service divided by 40. For example, from the Figure Above: Monthly Social Security at Age 62 = $1,400 Years of Offset service = 27 Calculation: $1,400 x (27 years of CSRS Offset service) divided by 40 = $ The CSRS Offset is subtracted from the CSRS annuity starting at age 62 - at the time social security payments start. From the picture above at age 62: Annuity = $2,759 Minus $945 Adjusted Annuity at age 62 = $1,814 Page 55 of 156

56 Windfall Elimination Provision (WEP Calculation - CSRS) Introduction CSRS employees DO NOT pay Social Security taxes, but they do pay Medicare tax (1.45% of salary). Generally, CSRS employees receive no Social Security retirement benefits, unless they have worked in a position covered by Social Security before or after working as a CSRS employee. Even with other work covered by Social Security, there is a very good chance that Social Security retirement benefits due a CSRS retiree, will be permanently reduced by the Windfall Elimination Provision (WEP). Reference OPM CSRS: Windfall Elimination Provision Social Security Administration: Windfall Elimination Provision FederalRetirement.net: CSRS Details What is the Windfall Elimination Provision of the Social Security Reform Act of 1983? It established that a person would only draw Social Security benefits for the actual work done under the Social Security Act. It established that a person who draws a civil service annuity (or other non-covered annuity) must have at least 30 years of substantial Social Security coverage in order to draw the highest allowed benefits from Social Security. For each year less than 30 years of substantial coverage, your Social Security benefit is reduced by 5% until you reach 40%.That 40% becomes the floor for your Social Security benefits. Page 56 of 156

57 You must have earned the following amounts to be considered substantial earnings: See the Social Security website: for more detailed information. Page 57 of 156

58 Thrift Savings Plan Introduction You will calculate future earnings in one or more of the TSP funds during working and retirement years. You will investigate the monthly increase in each of the funds for any period of time. You will select a month and year in which to start withdrawal of TSP funds. You will compare the three major options for withdrawing funds (lump sum, monthly payments and annuity). The TSP form is separated into three areas (each has a tab): Contributions, Growth, and Withdrawal. Reference TSP: Contributions TSP: Growth TSP: Withdrawal FederalRetirement.net: TSP Details Page 58 of 156

59 The TSP form requires the Retirement System and Retirement Date that are entered on the Annuity ==> Retirement Eligibility form. Annuity ==> Retirement Eligibility form In addition, Annual Salary and Percentage Increase Each January are required and come from the Annuity ==> High 3 Average form. Annuity ==> High 3 Average form You must enter this data on the two Annuity forms before you can work on the TSP form. Page 59 of 156

60 CONTRIBUTIONS (tab): The Retirement System, from the Annuity ==> Retirement Eligibility form, and the Annual Salary and the Percentage Increase Each January, from the Annuity ==> High 3 Average form, appear at the top of the TSP Contributions form. Example: Page 60 of 156

61 1. Begin by entering the Existing TSP Savings on the Contributions Form. Federal employees can view this information at Account Access web page. In addition, federal employees can access the TSP web site directly from the Benefits Calculator HELP menu. You must know the Personal Identification Number and Social Security Number to obtain account information. 2. Enter the percent of the annual salary or the biweekly amount to invest in the funds. 3. The Internal Revenue Service Max Allowed contribution limit cannot be exceeded. If you contribute the max allowed and you are 50 years old or older, then you can contribute an additional sum in the Catchup (yellow) window. 4. Enter the percent of the total contributions to put into the L, C, F, G, I and S funds (Distribute Savings into Funds in Percentages). The entries must total 100%. Page 61 of 156

62 5. Select the L Fund if applicable. 6. After entering all the information above, the program calculates the allocation of the future investments into each of the funds in the percentages you entered in paragraph 4 above. If you are a FERS employee, the government s annual contribution is automatically calculated in-accordancewith the following: You Government TOTAL Contribute Contributes 0% 1% 2% 3% 4% 5% 5% + 1% 2% 3% 4% 4.5% 5% 5% 1% 3% 5% 7% 8.5% 10% 10% + TSP Catch-Up General Information Catch-up contributions are a supplement to the participant s regular employee contributions and do not count against either the statutory contribution percentage or the Internal Revenue Code s elective deferral limit. However, the catch-up contributions have their own annual limit (the annual catch-up contributions limit ) and eligibility criteria. Eligibility for Catch-up Contributions A federal employee is eligible: (1) when the federal employee becomes 50 or older, and (2) if the federal employee is already contributing the maximum amount of regular TSP contributions for which he/she is eligible. Page 62 of 156

on the TSP website. TSP return rates were taken from: https://www.tsp.")

63 GROWTH (tab): 1. Enter the Future Compound Annual Return Rate - Percentages for each fund. You can find historical percentages for the funds (and other information) on the TSP website. TSP return rates were taken from: Example: Page 63 of 156

64 2. Two spreadsheets depict funds growth. The top spreadsheet displays the growth of each individual fund in the future. The bottom spreadsheet displays the future growth of the funds allocated into the selected L fund. 3. Displayed data: (a) The Retirement Date was entered in the, Annuity ==> Retirement Eligibility form. (b) The Retirement Age was calculated in the Annuity ==> Retirement Eligibility form. Annuity ==> Retirement Eligibility form TSP ==> Growth Tab (c) The Withdrawal Age (Year and Month when TSP withdrawals will start. (d) The number of Months from Now when TSP withdrawals start will be displayed, 4. After selecting the Calculate Performance button, calculations are made that fill-in the Funds Growth spread sheets described in 2. above. Page 64 of 156

65 5. The following effects on Existing Savings can be calculated, displayed, and printed: (a) Future growth, of existing savings for any time period, (b) Changing the distribution of existing savings in different funds, (c) Changing the future compound annual return rate of existing savings in different funds, (d) Changing the withdrawal age of existing savings in different funds, 6. The following effects on Future Contributions can be calculated, displayed, and printed in the Funds Growth spread sheet: (a) Future growth, of future contributions for any time period, (b) Changing the distribution of future contributions in different funds, (c) Changing the future compound annual return rate of future contributions in different funds, (d) Changing the withdrawal age of future contributions in different funds, 7. CALCULATIONS: During each month in the working years, the program calculates: (a) The amount deposited in each fund, (b) Increase of each deposit beginning in January each year, and (c) Compounded increases on savings in each fund. During each month in the retirement years, the program calculates: (a) Compounded increases on savings in each fund. The results are viewed in the Funds Growth spreadsheets. Page 65 of 156

in the TSP Booklet, \"Withdrawing Your TSP Account After Leaving Federal Service.")

66 WITHDRAWAL (tab): Start by selecting from one of the three major Withdrawal Options (see figure above): Lump Sum, Monthly Payments or Annuity. You can find information covering these options (and other information) in the TSP Booklet, "Withdrawing Your TSP Account After Leaving Federal Service." Click the Withdrawal HELP button (see figure above) to display this document. Page 66 of 156

.")

67 Example: 1. The Lump Sum selection will produce no further calculation as the lump sum is viewed in the Funds Growth spread sheet (Growth Tab) - in the Balance column on the bottom line. It also appears in the light green information window to the right of Withdrawal Options (shown below). This option is usually selected when you desire to roll the money out of your TSP account into an investment. Be extremely careful if you do this as there could be major tax consequences. Page 67 of 156

68 2. The Monthly Payments selection displays three new options: Life Expectancy (IRS) Number of Payments, and Monthly Amount methods for calculating the monthly withdrawal. See the information window on the form. (a) Select one of the three options: LIfe Expectancy: The number of payments and monthly amount are calculated for you using the Internal Revenue Service (IRS) life expectancy table. The number of payments depends on the age at which the withdrawal will start. The program will deduct the maximum amount from each fund so that each fund will have almost a zero amount after the last payment is made. Number of Payments: Enter the number of payments you want. The monthly amount is calculated by the program, and it will deduct the maximum amount from each fund so that each fund will have almost a zero amount after the last payment is made. Monthly Amount: Enter the number of payments and the monthly amount you want. The program will deduct a portion from each fund determined by the percentages entered in the, "Distribute Savings into the Funds in Percentages Shown," fields. Page 68 of 156

69 (b) Enter Number of Payments (if applicable) and/or Monthly Amount (if applicable) (c) Enter the distribution percentages of the five funds during the withdrawal years by entering percentages in one or more of the Fund fields. You can select the L Income fund allocation by clicking on the L Income Distribution button. The total percentage must equal 100%. Click here to view a short video that covers the three Monthly Payment options. Page 69 of 156

Enter the Current Interest Rate Index. Click on the Annuity Interest Rate Index button.")

70 3. The Annuity selection (a) You will observe Your Age at Start of Annuity that you selected when in the Growth (tab) part of the TSP form (b) If there is a joint annuitant, enter his/her age in the Joint Annuitants Age at Start of Annuity field. (c) Enter the Current Interest Rate Index. Click on the Annuity Interest Rate Index button. This will open the, "Annuity Interest Rate" web page on the TSP website. (d) On the Annuity form (above) you will see three types of Annuity: - SINGLE LIFE with Level or Increasing Payments, - JOINT LIFE WITH SPOUSE with Level or Increasing Payments, and - JOINT LIFE WITH OTHER SPOUSE with Level Payments. (e) Click on the Calculate Annuity button, and observe the various monthly annuity amounts. (f) You can get detailed information on Annuity in the TSP Booklet, "Annuity." Click on the Benefits Calculator HELP menu then click on TSP web site. Look in the Forms and Publications section of the TSP web site. Page 70 of 156

71 Insurance Page 71 of 156

72 Federal Employees Group Life Insurance (FEGLI) Introduction You will review current FEGLI insurance coverage and the biweekly, monthly and annual premiums. You will investigate future changes in coverage and premiums, based on salary and age, before and after retirement. You can change the type and amount of coverage and then view resulting changes in premiums. For each scenario, you will view the long term coverage and accumulated costs. Reference OPM: FEGLI FederalRetirement.net: FEGLI Details Page 72 of 156

73 Example: 1. The FEGLI form gets the Birth Date, Retirement Date, Current Age, and Age at Retirement from the Annuity ==> Retirement Eligibility form. This data must be entered before you can work on the FEGLI form. Annuity ==> Retirement Eligibility form Page 73 of 156

. 4.")

74 2. The FEGLI form gets the Annual Salary, and Jan. Increase, from the Annuity ==> High 3 form. This data must be entered before you can work on the FEGLI form. Annuity ==> High 3 form 3. If you are a Postal Employee, then check the Postal Employee box (postal employees receive free Basic coverage until they retire). 4. Next select insurance coverage by clicking on the appropriate Coverage boxes (see above). Page 74 of 156

75 5. For additional information regarding FEGLI, click on the HELP menu and select FEGLI website. BASIC coverage is equal to the current annual salary rounded up to the next $1,000 plus $2000 if you are 45 years old and over. If you are under 45 years old, then Basic coverage is greater (see the FEGLI website for details). You must select this coverage to be eligible for the optional coverage (A, B, and C). The Basic coverage may be continued after retirement under certain conditions. At age 65 (if retired) there are three options for Basic Coverage: (a) No reduction in Basic coverage, (b) 50% reduction in Basic coverage starting at age 65 reduced by 1% per month until 50% coverage is reached, (c) 75% reduction in Basic coverage starting at age 65 reduced by 2% per month until 25% coverage is reached. Select the reduction desired by clicking on the appropriate entry under the Reduction At Age 65 heading. Option A - Standard coverage is equal to $10,000 dollars. You may continue it after retirement if Basic coverage is continued. Effective at the end of the month after the month in which age 65 is reached or the retirement date (if later than age 65), Option A coverage will be reduced by 2% per month until it reaches 25% ($2,500). Page 75 of 156

76 Option B - Additional coverage is equal to 1 to 5 times the annual salary rounded up to the next $1,000. Select any number between 1 and 5 under the Option B Multiplier heading. This optional coverage continues automatically after retirement if Basic coverage is elected. Effective at the end of the month after the month in which age 65 is reached or the retirement date (if later than age 65), Option B coverage will reduce by 2% of the pre-retirement amount per month for 50 months, at which time the coverage will end. However, if continued coverage after the age of 65 is desired, check the NO Reduction At Age 65 box. Option C - Family coverage covers eligible family members: $5,000 for a spouse and $2,500 for each eligible dependent child. It continues automatically after retirement if Basic coverage is continued. Multiple amounts of coverage for Spouse and Dependents are available from 1 to 5 multiples ($5,000 to $25,000 in $5,000 increments for Spouse and $2,500 to $12,500 for each Dependent). Select the Cover Spouse box and click on the Dependent Information button (if applicable) to enter the number of dependent children. If selected, enter Dependents current age and mark the Yes box if support for the dependent is allowed after age of 22, then push the OK button. Select the C Multiplier for the coverage desired. Effective at the end of the month after the month in which age 65 is reached or the retirement date (if later than age 65), Option C coverage will reduce by 2% of the retirement age amount per month for 50 months, at which time coverage will end. However, if continued coverage after the age of 65 is desired, check the NO Reduction At Age 65 Box. Note: if you have marked one or more boxes under Coverage but you have not marked the Basic Coverage box, then all calculations will be zero and some options will not be displayed. See Basic Coverage. Page 76 of 156

77 6. Next, click on the Calculate button and review the Premiums (biweekly or monthly and annual), the accumulated cost for all coverage over the years, and coverage amounts from current age to display years selected. Click on the third column RED heading above Premium to alternate between the Biweekly and Monthly display of data. 7. Click the FEGLI Codes button to view and/or print the FEGLI Codes. Page 77 of 156

78 Federal Employees Health Benefits Program (FEHBP) Introduction The FEHBP form will help you to project future FEHBP costs with an estimated premium cost increase each year. Reference OPM: FEHBP FederalRetirement.net: FEHBP Details 1. You will enter your current, biweekly FEHBP payment found on your leave and earnings statement (pay stub) and an estimated percentage annual cost increase in your FEHBP payments each year. 2. The Benefits Calculator will then convert your biweekly payment into a monthly payment, and an annual payment. 3. Finally, the program will calculate annually compounded increases in each of these payment amounts (biweekly, monthly and annual) by the percentage annual cost increase you enter. The percentage change each Page 78 of 156

= $2,860.")

79 year is increased by compounding the previous year's increase. For example, assume that the first year's total payments = 26 payments x $100 (biweekly) = $2,600. The second year's annual payment amount is expected to increase by 10%: $2,600 + (10% x $2,600 = $260) = $2,860. In the third year the annual payment amount is expected to increase by 10%: $2,860 + (10% x $2,860 = $286) = $3,146. Example: 4. For additional information regarding Health Insurance, click on the HELP menu and select FEGHB Health Insurance website. Page 79 of 156

80 Long Term Care (LTC) Insurance Introduction Like other Americans, federal employees and retirees are concerned about their long-term care needs. Long term care is something you may need if you can no longer perform everyday tasks by yourself. For example, there may come a time when you need help getting dressed, eating or bathing. It also includes the kind of care you would need if you had a severe cognitive impairment like Alzheimer's disease. You can receive this care in a variety of settings, including your home, an assisted living facility or a nursing home. Reference OPM: LTC FederalRetirement.net: LTC Example: Page 80 of 156

81 Details Figure 1 Page 81 of 156

82 Figure 2 Figure 3 1. Fill-in the following basic data on the LTC website form (see Figure 1): Birth Date, Select Customize Your Plan, Daily Benefit Amount - The maximum amount a plan will pay in any single day, Benefit Period - The amount of time your insurance will last if the full daily benefit is paid every day, Page 82 of 156

83 Waiting Period (is fixed at 90 days) - The amount of time you must pay for covered services before the insurance will begin to pay, and Inflation Protection - three options that will increase benefits to help pay for increased costs of care: (a) Automatic Compound Inflation (ACI) Option- An inflation protection option that increases your benefits automatically by 4% or 5% compounded annually with no increase in premium (at this time), or (b) Future Purchase Option - An inflation protection option that increases your benefits every other year with an increase in premiums. 2. Transfer the Data entered on the LTC Website form to the Entry Form (see Figure 1). 3. Click on the Calculate button (not shown in Figure 1) on the LTC Website form. 4. Transfer the Data calculated on the LTC Website form to the Entry Form (see Figure 2). 5. Click on the Calculate button on the Entry form (see Figure 2). 6. A pop-up message appears (see Figure 3) that calculates 22 years of LTC data. This is a brief listing. A detailed report page displays LTC coverage and premiums from current age through age 90. Page 83 of 156

84 Retirement Affordability Analyzer Page 84 of 156

85 Overview The Retirement Income/Expense Analyzer program was developed to integrate all income and expense data from the Benefits Calculator and other sources in order to present a thorough analysis of income and expenses during each year of retirement. Analyzer Menu Source of Data Calculations A. Income Other Sources Analyzer TSP Rollover, Pensions, Rental Property, Spouse's Income, Jobs after Retirement, and Other Taxable and Non-Taxable Income B. Income Analysis Benefits Calculator Current: and Analyzer All Pay Stub Income & Deductions Retirement: Annuity, FERS Supplement, Social Security, TSP, and Annuity Deductions C. Expense Other Sources Analyzer Living Expense: Summarized or Itemized D. Income + Expense Analysis: 1. Income Gov. Sources Benefits Calculator Salary, Annuity, FERS Supplement, Social Security, and TSP 2. Expenses Gov. Sources Benefits Calculator Retirement Penalties, Survivor Benefit, FEGLI, Health Insurance, Long Term Care (LTC) Insurance, and Federal and State Income Taxes 3. Income & Expenses Gov Sources D.1. & D Income & Expenses Other Sources A. & C. 5. Income & Expenses All Sources Comparison Comparison A. & B. & C. & D.1. & D.2. & D.3 & D.4. Retirement Affordability Federal job and retirement income are thoroughly analyzed: Salary, Retirement Annuity, Social Security / FERS Supplement (if applicable), and TSP. Federal job and retirement expenses are also thoroughly analyzed: Retirement penalties, Survivor Benefit, FEGLI, Health Insurance, Long Term Care (LTC) Insurance, and Page 85 of 156

86 Federal and State Taxes. In addition, to the federal job and retirement related sources of income and expenses listed above, other sources of income and expenses can be listed and projected over time. The primary purpose of the Retirement Income/Expense Analyzer is to investigate future time periods when expenses may be larger than income. With this knowledge, strategies for avoiding this situation can be explored. The Annuity, TSP and Insurance sections of the Benefits Calculator are used to calculate your federal benefits. The Retirement Income/Expense Analyzer will take these calculations and project them into your retirement years. You will view the impact time has on: Annuity, Social Security (FERS and CSRS Offset), TSP, Annuity Penalties (e.g., early retirement), Survivor Benefit, FEGLI, Health Insurance, Long Term Care Insurance, and State and Federal Income Taxes. You will then add other sources of income and expenses that are realized during your retirement years. Other income may include (in part): IRAs Roth IRAs Savings Accounts Part-time Job Rental Income, Reverse Mortgages, and Other Sources Other sources of expenses may include (in part): House Payment, Car Payment, Utilities, Travel, Education, Food, Clothing, and Others Sources. Finally, the government income and expenses and other sources of income and expense are combined so that yearly and monthly projections are calculated from retirement age to age 90. There may be periods of time when income is insufficient to meet expenses. The power of the Benefits Calculator and Retirement Income/Expense Analyzer can then be used to make adjustments in many places so that income is always greater than expenses. Date is entered in the following order: A. Income Other Sources, B. Income Analysis, C. Expense Other Sources, D. Income + Expense Analysis: 1. Income from Government Sources, 2. Expense from Government Sources, 3. Income and Expense from Government Sources, 4. Income and Expense from Other Sources, and 5. Income and Expenses from All Sources. Page 86 of 156

87 Income Analysis - From Other Sources Introduction You will estimate your annual and monthly retirement income from other sources starting the first year of retirement. You will then project your annual and monthly income in retirement to age 90. You can switch from a yearly to a monthly view of all the income data. Details The Income from Other Sources is selected in the menu as shown. Page 87 of 156

88 1. The Income from Other Sources is entered directly on this form - no input comes directly from the Benefits Calculator. 2. Start by selecting the Source of the income as shown above. There are three general categories of income sources: Savings, Job/Retirement Income, and Property. 3. Select a Savings source to calculate a periodic withdrawal from any type of savings or investment. For example in the figure below, a withdrawal from a TSP Rollover investment is shown. In this case, the investment (TSP Rollover) has grown to $443,231 at the start of the withdrawal period (see the TSP section in this manual). The investment is expected to continue to grow 5.00% annually. The initial annual withdrawal is $20,000, and the amount of annual withdrawal will increase 2.00% each year and is taxable ($20,000:Yes see below). Retirement and withdrawal from this savings both begin at age 56, and the annual withdrawal will continue through age 90. Page 88 of 156

and the entry will be displayed on the Income Analysis - Other Sources form. 5. After clicking on the ADD key, the following form appears.")

89 4. After selecting the STOP AGE, press the TAB key on the keyboard. The ADD button will become available. Click on the ADD key (see above) and the entry will be displayed on the Income Analysis - Other Sources form. 5. After clicking on the ADD key, the following form appears. The projection of the amount of Annual Income and the Remaining balance in the savings is calculated and displayed. In the picture above, you can see that the savings will decrease each year (Remaining balance column) even though the annual growth is 5.00%. Because of the level of the starting annual income ($20,000) and the level of annual increases in withdrawals (2.00% each year), the savings balance cannot earn enough to Page 89 of 156

decreasing the initial annual income amount and/or (2) reducing the annual increases in income. 6.")

90 keep up with the increasing annual withdrawals. The Remaining savings balance can remain the same or increase each year by: (1) decreasing the initial annual income amount and/or (2) reducing the annual increases in income. 6. In the example shown above, "Annual income: 20,000:Yes is displayed. The Yes indicates this is a taxable income. Income from a different source may be non-taxable and will be displayed as $4700:No 7. If you want this report page, click on the Print button (shown above). 8. Click on the Monthly Income button to convert the annual amount to monthly amount. Notes: a. You must do this if you want monthly calculations on the Income Analysis - Other Sources report page. Page 90 of 156

part of the Retirement Income/Expense Analyzer.")

91 b. All Taxable and Non-Taxable amounts are combined and sent to the Income Analysis (see next section in this manual) part of the Retirement Income/Expense Analyzer. Page 91 of 156

92 8. Another source of income after retirement could be a part-time job. This can be added to the this form. 9. Select a Job / Retirement Income source to calculate income from a part-time job. For example in the figure above, an income from a part-time job is shown. The annual income is $15,000 to start and it is expected to grow 3% each year. The job duration extends from age 56 through age When the Job / Retirement Income entry is added, the following Annual Job Growth Income chart is displayed and can be printed. Page 92 of 156

93 11. Income from a Property can be added the same way as a Job/Retirement Income. 12. After you make an entry on the Income Analysis - Other Sources form, you can: Recalculate it, Edit it, or Delete it To do one of these, click an entry (for example, TSP Rollover show) and then select one of the three buttons. a. By clicking on the Calculate button you will see the following Page 93 of 156

94 b. The Edit button is used to make changes. After changes are made, press the Tab key to move to the Stop Age field, then click on the ADD button. c. By selecting the Delete button, the highlighted line (TSP Rollover shown here) will be deleted. d. The TSP Rollover is removed as shown here. Page 94 of 156

95 Federal Income and Inflation Analysis Introduction This form in the Retirement Income/Expense Analyzer provides a comparison of today's income and expense with income and expense the first year of retirement. Income and expense sources calculated in the Benefits Calculator are automatically imported into this form. Additional expense found on your earnings and leave statement (biweekly pay stub) can be manually added. The Benefits Calculator projections at retirement are also imported into this form. The form compares Net Pay today with Initial Net income in retirement. An analysis of the impact of inflation on calculated income at retirement is provided. Details 1. Click on Income Analysis on the menu. Page 95 of 156

96 2. The Federal Income Analysis - Monthly form collects data from the Benefits Calculator and displays it in the colored fields on the form. The data in the colored fields cannot be changed on this form, however it can be changed by adjusting entries on various Benefits Calculator forms. 3. Some expense (deductions) data can be entered in the blank, white fields on this form, and it is found on your leave and earnings statement (biweekly pay statement). Page 96 of 156

97 4. The retirement Federal and State income taxes are calculated by clicking on the two Estimate Tax buttons. 5. All Taxable and Non-Taxable entries come from the Income Other Sources form. The Taxable income is used, in part, to calculate the retirement Federal and State income taxes estimation. 6. After entering your data, the Net Pay today can be compared with the monthly Net Income in the first year of retirement. The Difference in Net Pay Today and Net Income in Retirement is displayed at the bottom of the form. If retirement Net Income is less than today's Net Pay income, the field turns red (as shown). This indicates a shortfall in retirement income. 7. To view the impact inflation will have in projected retirement income, click on the, "View Inflation Advisor," button at the bottom of the form (see above). 8. The inflation advisor form appears. Enter an Average Yearly Inflation Rate to view inflation impact on retirement income. 9. The Taxable Income and the Non-Taxable Income from other sources come from the Retirement Income/Expense Analyzer ==> Expense Other Sources form. 10. The data presented on both of these forms is made available to the report section of the program. 11. Calculating Retirement Income Shortfall (example) : 1. The Net Monthly Pay today ($3, shown here) is usually consumed each month on all living expenses. Therefore, it represents your needed income (standard of living) to maintain your lifestyle. 2. The available Net Income ($2, shown here) in retirement is less than the today's standard of living by $1, (income shortfall shown here). 3. However, when inflation is considered, the actual shortfall of needed retirement income is calculated to be $4, (shown here) in order to equal the purchasing power of today's net pay of $3, There is a projected shortfall of $2, (shown here) of income ($4, needed - $2, available at retirement). Page 97 of 156

98 Page 98 of 156

99 Expense Analysis From Other Sources Introduction You will estimate your annual and monthly retirement living expenses starting the first year of retirement. You will then project your annual and monthly expense in retirement to age 90. You can switch from a yearly to a monthly view of all the income data. Details The Expense from Other Sources is selected in the menu as shown here. Page 99 of 156