The Valuation of Default Risk in Corporate Bonds and Interest Rate Swaps

|

|

|

- Calvin Stewart

- 10 years ago

- Views:

Transcription

1 Financial Institutions Center The Valuation of Default Risk in Corporate Bonds and Interest Rate Swaps by Soren S. Nielsen Ehud I. Ronn 96-23

2 THE WHARTON FINANCIAL INSTITUTIONS CENTER The Wharton Financial Institutions Center provides a multi-disciplinary research approach to the problems and opportunities facing the financial services industry in its search for competitive excellence. The Center's research focuses on the issues related to managing risk at the firm level as well as ways to improve productivity and performance. The Center fosters the development of a community of faculty, visiting scholars and Ph.D. candidates whose research interests complement and support the mission of the Center. The Center works closely with industry executives and practitioners to ensure that its research is informed by the operating realities and competitive demands facing industry participants as they pursue competitive excellence. Copies of the working papers summarized here are available from the Center. If you would like to learn more about the Center or become a member of our research community, please let us know of your interest. Anthony M. Santomero Director The Working Paper Series is made possible by a generous grant from the Alfred P. Sloan Foundation

3 The Valuation of Default Risk in Corporate Bonds and Interest Rate Swaps 1 October 1994 Revised: January 15, 1996 Abstract : This paper implements a model for the valuation of the default risk implicit in the prices of corporate bonds. The analytical approach considers the two essential ingredients in the valuation of corporate bonds: interest rate uncertainty and default risk. The former is modeled as a diffusion process. The latter is modeled as a spread following a diffusion process, with the magnitude of this spread impacting on the probability of a Poisson process governing the arrival of the default event. We apply two variants of this model to the valuation of fixed-for-floating swaps. In the first, the swap is default-free, and the spread represents the appropriate discounted expected value of the instantaneous TED spread; in the second, we allow the swap to incorporate default risk. We propose to test our models using the entire term structure of corporate bonds prices for different ratings and industry categories, as well as the term structure of fixed-for-floating swaps. 1 Soren S. Nielsen is at the Department of Management Science and Information Systems of the University of Texas at Austin. Ehud I. Ronn is at the Department of Finance of the University of Texas at Austin. Correspondence should be addressed to Ehud I. Ronn, Department of Finance, College and Graduate School of Business, University of Texas at Austin, Austin, TX Phone: (512) Fax: (512) E- mail: [email protected].

4 The Valuation of Default Risk in Corporate Bonds and Interest Rate Swaps* 1 Introduction The valuation of securities subject to default risk has been of interest in the academic and practitioner literature for some time. Beginning with Merton (1974), a substantial body of literature has modeled the default event as dependent on the value of the firm, F, with prespecified default boundary. For the latter, see, e.g., the recent work of Hull and White (1992) and Longstaff and Schwartz (1994). In contrast, the approach we offer below is silent on the causality of default, and hence does not require specification of the precise events which cause the firm to seek, or be forced into, a state of bankruptcy. Hence, this approach enjoys a greater generality relative to its predecessors. Following Jarrow and Turnbull (1992), Jarrow, Lando and Turnbull (1994), Lando (1994), Madan and Unal (1994) and Duffie and Singleton (1994), the current model abstracts from an explicit dependence on an unobservable firm value. In contrast, our model explicitly models the instantaneous default spread on risky bonds, correlates that spread to the riskfree rate of interest, and links the default intensity to its presumed market-efficient predictor, the prevailing instantaneous credit spread. * The authors acknowledge the helpful comments and suggestions of George Handjinicolaou, Guillaume Fonkenell, Martin Fridson, Dilip Madan, George Morgan and finance seminar participants at the University of Maryland, the University of Texas at Austin and Southern Methodist University. Earlier drafts of this paper were presented at the April 1994 Derivatives and Systemic Risk Conference, the April 1995 Cornell University/Queen s University Derivative Conference, and the May 1995 Conference of the Society for Computational Economics. The authors would also like to thank Merrill Lynch & Co. for providing data in support of this project. The authors remain solely responsible for any errors contained herein.

5 The approach we suggest leads to directly testable results in the valuation of corporate bonds. We submit our model to rigorous econometric testing using a data base composed of the entire term structures of corporate bonds for different ratings and industry classifications. Practitioners have of late become interested in models of default risk for several reasons. First, understanding the default event permits a more accurate modeling of issues subject to default in general, and corporate bonds in particular. Second, the modeling of the default event permits the construction and valuation of alternative securities whose payoff is triggered by the default event (or lack thereof), which go by the generic name credit derivatives. 1 The valuation of interest rate swaps has attracted significant attention. One strand of literature, including Evans and Bales (1991), Litzenberger (1992), and Chen and Selender (1994) have reported on the relative insensitivity of swap spreads to default measures, while Grinblatt (1995) has modeled the swap spread as a compensation for illiquidity relative to Treasuries. In contrast, the works of Cooper and Mello (1991) and Longstaff and Schwartz (1995) have attributed swap spreads to default risk, while Bhasin (1995) has recently reported on the increasing cross-sectional credit-quality variety of OTC-derivative or where

6 counterparties. Swap contracts are natural candidates for two-factor modeling, and in this paper we present two such models: in the first, the swap spread is simply the riskfree discounted expected present value of the TED (LIBOR Treasury) spread, whereas the second model generalizes the first to admit default risk. The paper is organized as follows. Section 2 proposes the two-factor corporate-bond model. Section 3 discusses the data and methodology, with Section 4 reporting on the model s empirical results. Section 5 presents default-free as well as risky two-factor swaps models, and their attendant empirical estimates. Section 6 concludes. 2 A Two-Factor Model of Default Risk 2.1 Model The two-factor model of the default risk assumes the following process: (1) where 3

7 instantaneous default spread s and the after-default recovery rate D. Specifically, given our notation, consider the par value of an instantaneously-maturing risky debt issue promisvaluation, this value is equal to the discounted expected value of the payoffs: The intuition for this model incorporates the following aspects: 1. The corporation s bond prices are presumed to drift downward as default becomes increasingly likely (e.g., as they are downgraded). 2. Given the default event has occurred, the bond sells at a post-default price of D, some fraction of face value We allow for a correlation in changes between r and s, and perform period-by-period discounting using riskless rates of interest. 4. Over the next interval, if the instantaneously-maturing security does not default, it will pay a return in excess of the riskfree rate; otherwise, it will sell at a price D. 2.2 Implementation equations (1) specify joint lognormal diffusions we require a lattice implementation: 3 In a more general model, the fraction D would not be a constant but presumably depend on the prevailing term structure of interest rates. 4

8 process is: 4 (2) The system (2) results in an efficient, recombining tree; see Appendix A for details. ance and covariance conditions implied in equations (1). 5 Specifically, we require that, under the risk-neutral probability measure, (3) (4) (5) Appendix A demonstrates that these conditions give rise to 10 equations in 12 variables, 4 The quadrinomial lattice contains the minimal number of nodes required to satisfy the firstand second-moment restrictions specified in eqs. (1). 5

9 and hence is underidentified. That appendix also demonstrates that the quadrinomial tree This choice of parameters satisfies the constraints that all probabilities be positive so long Note that the above tree is not a true quadrinomial, for whenever a default occurs, that branch of the tree terminates. In fact, for the postulated constant u s, we obtain a simple recombining tree. 7 3 Data: Term Structures of Treasury Bonds, Corporate Bonds and Swaps The data for our analysis consists of the term structures of interest rates for alternatecategories ratings Merrill Lynch & Co. bond indices, specified in Appendix B: these bond indices constitute examples wherein we observe an entire term structure of Treasury and corporate credit spreads through a 10-year maturity; with semi-annually separated intervals, this implies data on 20 par bonds with maturities ranging from one-half year to ten years. An interesting component of this data is the swap curve, which in turn permits the application of this methodology to the calculation of the default risk implicit in these important securities. Our data includes observations on the par rates for Treasury and corporate bonds including standard fixed-for-floating-libor swap rates at maturities of two, three, respectively. From this data, we can extract the zero-coupon Treasury and corporate rates A, which imply fewer restrictions on parameter values in order to assure positive state prices; the resulting empirical magnitudes did not change substantially. step of the tree. 6

10 through a bootstrap technique which complements the observable bonds by linearly interpolating the par rates for each semi-annually separated maturity from six months through ten years. The technique uses the postulated twenty par rates and sequentially solves for the zero-coupon rate that would give rise to the observable par rates. The analytical details of this technique are described in Appendix C. Figure 1 displays an example of the Treasury and corporate par rate curve for several ratings categories, including the swap curve. 4 Default-Risk Parameter Estimation for Corporate Bonds 4.1 Methodology Using this data, our analysis determines the implicit values of the parameters which explain the cross-sectional term structures of interest rates for alternate ratings categories. Specifically, assume that we observe the term structure of the riskless rate of interest, and the term structure of credit spreads for a given ratings category. This data is conveyed the market prices of the Treasury corporate securities, respectively, for maturity t, t = 0.5, 1,..., 8 The valuation of swaps is perforce different, since the widening/tightening of the swap spread does not necessarily imply a concomitant increase/decrease in the probability of a swap countervalue of the swap at a given point in time. 7

11

12 process for the default spread is then time-homogeneous and entirely determined by the Ideally, one would implement an empirical procedure to estimate the value of the pais immediate default, but with full recovery. While this is a feasible empirical solution, it is clearly an unintuitive one. In order to preclude such a solution, we fix D at two arbitrary values, D = 0 and D =.5. distributed, then the estimation problem is we have 20 data points and three parameters to estimate. In calibration estimations such as these, we infrequently encounter the possibility of estimating an implied correlation coefficient. In the current case, objective (6) permits the The estimation procedure can be ratings category-specific or it can be market-wide: ries. Thus, the objective function (6) could be estimated with and without imposing the identical parameter values across different ratings categories. 9 variables.

13 4.2 Statistical Properties of the Estimates The above model is amenable to non-linear least squares estimation. If where = 4.3 Empirical Results For 12/29/94, Table 1 reports the following set of parameter estimates: 9

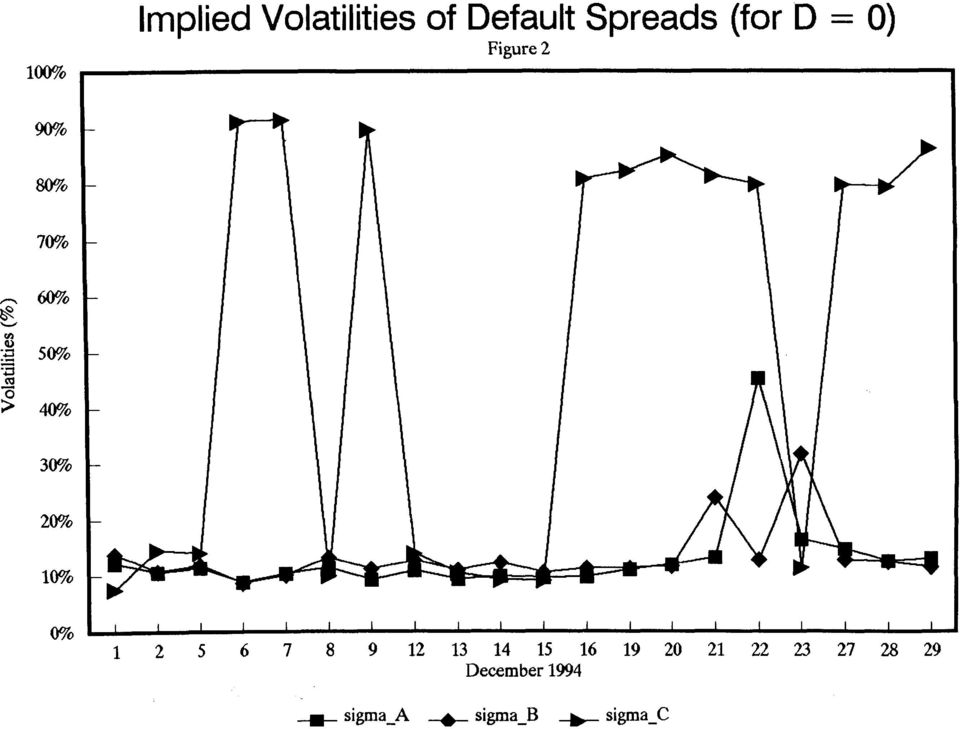

14 Table 1 Parameter Estimates for 12/29/94 Note: Numbers in parentheses represent standard errors. For D = 0, Panel A of Table 1 reports the separate-category estimates of implied volaon 12/29/94 as equal to {.130,.115,.862}. Figure 2 contains a perspective on these values by presenting the time-series estimates of these parameters for the entire month of December For D = 0.5, Figure 3 displays the time-series of implied volatility for the riskless rate remarkable stability for the fourth quarter of Similar results also obtain for D = 0. We performed sensitivity analyses on the parameter estimates and observed the follow- 10

15

16

17 ing effects: Interestingly, the impact of the correlation effect was negative, but only weakly so. Our model s empirical result thus contrasts with the finding of Longstaff and Schwartz (1994), who find that the correlation of a firm s assets with changes in the level of the interest rate can have significant effects on the value of risky fixed-income securities (p. 23). 5 A Two-Factor Model for the Swap Curve 5.1 A Two-Factor Default-Free Model for the Swap Curve As noted above, swap contracts are natural candidates for two-factor modeling. Thus, our first approach models the swap spread as the riskfree discounted expected present value of the TED spread. to-market value of an interest rate swap receiving fixed and paying floating LIBOR on a 11

18 Now consider the valuation of put swaptions. notional amount) of a put swaption with time to expiration t, swap-maturity T and exercise rate K. The value of the put swaption is the discounted expected value of the payoff, put swaptions prices P (t, T, K), we can obtain empirical estimates of the model s parathen the estimation procedure is order to place emphasis on the higher-order volatility-dependence of swaption prices. 5.2 A Two-Factor Risk Model for the Swap Curve A default-risk approach to the valuation of the swap curve requires a modification of the corporate bond-default model. Specifically, if the swap is the sole contract existing between the two parties, and the two parties currently have identical credit rating, then the probability of default increases with the absolute value of the mark-to-market on the swap. We require this assumption of default symmetry, since our empirical swap rates mark-to-market value of an interest rate swap receiving fixed and paying floating LIBOR 10 For a modeling of the swap contract with asymmetric default assumptions, see Duffie and Huang (1995). 12

19 partial-recovery-rate parameter k < 1, (7) where occurring over the next interval 11 specified in the system (2). 13

20 assume that in the region of interest, we can write the linear relationship In this case, the values of the put swaptions are once again since the short side of the put swaption has no incentive to default prior to the exercise of the put. However, the arguments of the value 5.3 Empirical Results Using the above data, the estimation problem is now of the model s coefficients, as well as the test of whether the incorporation of default risk residuals, the relevant test statistic for the nested test becomes 14

21 Table 2 reports the empirical tests based on vanilla fixed-for-floating swap rates out to a ten year maturity, and 17 put swaption prices for each of eight dates over the period Jan. 18, 1993 May 3,

22

23 Several results from Table 2 are noteworthy: 1. At the 5% level, the sum of squared residuals on each observation date is significantly reduced through the addition of the possibility of default. If we posit the identical parameter values throughout the sample period, then the significance of default risk can be established at the 1% level. of riskfree rates of interest. 6 Summary This paper has derived a two-factor risk model for corporate bonds and interest rate swaps. The model is parsimonious in its assumptions, uses readily-observable inputs and is estimated empirically from the observable spreads of defaultable bonds and fixed-for-floating interest rate swaps. The empirical results suggest the importance of explicit modeling of the default event for both sets of securities. Further, we believe subsequent work should be focused on modeling the relevant stochastic processes so as to elicit the implied after-default values of corporate bonds and interest-rate swaps. 17

24 A Construction of the Quadrinomial Tree Equation (2) in the text specifies the quadrinomial lattice to be used for corporate bond valuation. This appendix demonstrates the numerical validity of that specification in fulfilling the first and second moment requirements of the joint process eqs. (1). Consider first the first-moment conditions (3). For i = 1, 2, we require that (8) (9) to produce the following two conditions: which implies Finally, the covariance condition (5) is 18

25 which implies We now demonstrate the tree can be constructed to satisfy all requirements under the equations in six unknowns: (10) (11) (12) (13) (14) (15) The solution to this system can be seen by inspection as follows. Equations (11) and the solution to the system is The non-uniqueness of this system can be resolved by appeal to the economics of the 19

26 20

27 B Data The data consists of the term structures of interest rates for alternate ratings-categories Merrill Lynch & Co. bond indices.

28 C Bootstrapping the Yield Curve from Par Rates For a unit par bond, consider the relation (16) (17) (18) From eq. (18), on-the-run points 2, 3, 7 and 10 yrs. 22

29 References 1. Bhasin, Vijay, On the Credit Risk of OTC Derivative Users, Working Paper, Federal Reserve Board of Governors, Chen, Andrew and Arthur K. Selender, Determination of Swap Spreads: An Empirical Analysis, Working Paper, Southern Methodist University, Cooper, Ian and Antonio Mello, The Default Risk of Swaps, Journal of Finance, 46, 1991, pp item Duffie, Darrell and Ming Huang, Swap Rates and Credit Quality, Working Paper, Stanford University, Evans, E. and Giola Parente Bales, What Drives Interest Rate Swap Spreads? in Interest Rate Swaps, Carl Beidleman (ed.), 1991, pp Grinblatt, Mark, An Analytic Solution for Interest Rate Swap Spreads, Working Paper, Anderson Graduate School of Management, April Hull, John and Alan White, The Impact of Default Risk on the Prices of Options and Other Derivative Securities, Working Paper, Faculty of Management, University of Toronto, Jarrow, Robert A. and Stuart Turnbull, Pricing Options on Financial Securities Subject to Credit Risk, Working Paper, Graduate School of Management, Cornell University, Jarrow, Robert A., David Lando and Stuart Turnbull, A Markov Model for the Term Structure of Credit Risk Spreads, Working Paper, Cornell University and Queen s University, Lando, David, A Continuous-Time Markov Model of the Term Structure of Credit Spreads, Working Paper, Graduate School of Management, Cornell University,

30 10. Leland, Hayne E. and Klaus B. Toft, Optimal Capital Structure, Endogenous Bankruptcy, and the Term Structure of Credit Spreads, Working Paper, University of California, Berkeley, December Litzenberger, Robert H., Swaps: Plain and Fanciful, Journal of Finance, 1992, pp Longstaff, Francis and Eduardo Schwartz, A Simple Approach to Valuing Risky Fixed and Floating Rate Debt, Journal of Finance, 50, pp Madan, Dilip B. and Haluk Unal, Pricing the Risks of Default, Working Paper, College of Business, University of Maryland, Merton, Robert C., On the Pricing of Corporate Debt: The Risk Structure of Interest Rates, Journal of Finance, 1974, pp

Pricing Interest-Rate- Derivative Securities

Pricing Interest-Rate- Derivative Securities John Hull Alan White University of Toronto This article shows that the one-state-variable interest-rate models of Vasicek (1977) and Cox, Ingersoll, and Ross

Pricing Interest-Rate- Derivative Securities John Hull Alan White University of Toronto This article shows that the one-state-variable interest-rate models of Vasicek (1977) and Cox, Ingersoll, and Ross

Valuation of the Minimum Guaranteed Return Embedded in Life Insurance Products

Financial Institutions Center Valuation of the Minimum Guaranteed Return Embedded in Life Insurance Products by Knut K. Aase Svein-Arne Persson 96-20 THE WHARTON FINANCIAL INSTITUTIONS CENTER The Wharton

Financial Institutions Center Valuation of the Minimum Guaranteed Return Embedded in Life Insurance Products by Knut K. Aase Svein-Arne Persson 96-20 THE WHARTON FINANCIAL INSTITUTIONS CENTER The Wharton

MULTIPLE DEFAULTS AND MERTON'S MODEL L. CATHCART, L. EL-JAHEL

ISSN 1744-6783 MULTIPLE DEFAULTS AND MERTON'S MODEL L. CATHCART, L. EL-JAHEL Tanaka Business School Discussion Papers: TBS/DP04/12 London: Tanaka Business School, 2004 Multiple Defaults and Merton s Model

ISSN 1744-6783 MULTIPLE DEFAULTS AND MERTON'S MODEL L. CATHCART, L. EL-JAHEL Tanaka Business School Discussion Papers: TBS/DP04/12 London: Tanaka Business School, 2004 Multiple Defaults and Merton s Model

Spread-Based Credit Risk Models

Spread-Based Credit Risk Models Paul Embrechts London School of Economics Department of Accounting and Finance AC 402 FINANCIAL RISK ANALYSIS Lent Term, 2003 c Paul Embrechts and Philipp Schönbucher, 2003

Spread-Based Credit Risk Models Paul Embrechts London School of Economics Department of Accounting and Finance AC 402 FINANCIAL RISK ANALYSIS Lent Term, 2003 c Paul Embrechts and Philipp Schönbucher, 2003

Innovations in Mortgage Modeling: An Introduction

2005 V33 4: pp. 587 593 REAL ESTATE ECONOMICS Innovations in Mortgage Modeling: An Introduction Nancy Wallace This special issue presents a selection of recent methodological advances in the academic literature

2005 V33 4: pp. 587 593 REAL ESTATE ECONOMICS Innovations in Mortgage Modeling: An Introduction Nancy Wallace This special issue presents a selection of recent methodological advances in the academic literature

Fixed-Income Securities. Assignment

FIN 472 Professor Robert B.H. Hauswald Fixed-Income Securities Kogod School of Business, AU Assignment Please be reminded that you are expected to use contemporary computer software to solve the following

FIN 472 Professor Robert B.H. Hauswald Fixed-Income Securities Kogod School of Business, AU Assignment Please be reminded that you are expected to use contemporary computer software to solve the following

Risk and Return in the Canadian Bond Market

Risk and Return in the Canadian Bond Market Beyond yield and duration. Ronald N. Kahn and Deepak Gulrajani (Reprinted with permission from The Journal of Portfolio Management ) RONALD N. KAHN is Director

Risk and Return in the Canadian Bond Market Beyond yield and duration. Ronald N. Kahn and Deepak Gulrajani (Reprinted with permission from The Journal of Portfolio Management ) RONALD N. KAHN is Director

A Unified Model of Equity Risk, Credit Risk & Convertibility Using Dual Binomial Trees

A Unified Model of Equity Risk, Credit Risk & Convertibility Using Dual Binomial Trees Nick Wade Northfield Information Services 2002, European Seminar Series 14-October-2002, London 16-October-2002, Amsterdam

A Unified Model of Equity Risk, Credit Risk & Convertibility Using Dual Binomial Trees Nick Wade Northfield Information Services 2002, European Seminar Series 14-October-2002, London 16-October-2002, Amsterdam

Modeling correlated market and credit risk in fixed income portfolios

Journal of Banking & Finance 26 (2002) 347 374 www.elsevier.com/locate/econbase Modeling correlated market and credit risk in fixed income portfolios Theodore M. Barnhill Jr. a, *, William F. Maxwell b

Journal of Banking & Finance 26 (2002) 347 374 www.elsevier.com/locate/econbase Modeling correlated market and credit risk in fixed income portfolios Theodore M. Barnhill Jr. a, *, William F. Maxwell b

Asymmetry and the Cost of Capital

Asymmetry and the Cost of Capital Javier García Sánchez, IAE Business School Lorenzo Preve, IAE Business School Virginia Sarria Allende, IAE Business School Abstract The expected cost of capital is a crucial

Asymmetry and the Cost of Capital Javier García Sánchez, IAE Business School Lorenzo Preve, IAE Business School Virginia Sarria Allende, IAE Business School Abstract The expected cost of capital is a crucial

DETERMINING THE VALUE OF EMPLOYEE STOCK OPTIONS. Report Produced for the Ontario Teachers Pension Plan John Hull and Alan White August 2002

DETERMINING THE VALUE OF EMPLOYEE STOCK OPTIONS 1. Background Report Produced for the Ontario Teachers Pension Plan John Hull and Alan White August 2002 It is now becoming increasingly accepted that companies

DETERMINING THE VALUE OF EMPLOYEE STOCK OPTIONS 1. Background Report Produced for the Ontario Teachers Pension Plan John Hull and Alan White August 2002 It is now becoming increasingly accepted that companies

INTEREST RATE SWAPS September 1999

INTEREST RATE SWAPS September 1999 INTEREST RATE SWAPS Definition: Transfer of interest rate streams without transferring underlying debt. 2 FIXED FOR FLOATING SWAP Some Definitions Notational Principal:

INTEREST RATE SWAPS September 1999 INTEREST RATE SWAPS Definition: Transfer of interest rate streams without transferring underlying debt. 2 FIXED FOR FLOATING SWAP Some Definitions Notational Principal:

Modeling Correlated Interest Rate, Exchange Rate, and Credit Risk in Fixed Income Portfolios

Modeling Correlated Interest Rate, Exchange Rate, and Credit Risk in Fixed Income Portfolios Theodore M. Barnhill, Jr. and William F. Maxwell* Corresponding Author: William F. Maxwell, Assistant Professor

Modeling Correlated Interest Rate, Exchange Rate, and Credit Risk in Fixed Income Portfolios Theodore M. Barnhill, Jr. and William F. Maxwell* Corresponding Author: William F. Maxwell, Assistant Professor

Master Thesis in Financial Economics

Master Thesis in Financial Economics Pricing Credit Derivatives Using Hull-White Two-Factor Model DRAFT - VERSION 3 [email protected] Supervisor: Alexander Herbertsson January 17, 2007 Abstract

Master Thesis in Financial Economics Pricing Credit Derivatives Using Hull-White Two-Factor Model DRAFT - VERSION 3 [email protected] Supervisor: Alexander Herbertsson January 17, 2007 Abstract

T HE P RICING OF O PTIONS ON C REDIT-S ENSITIVE B ONDS

Schmalenbach Business Review Vol. 55 July 2003 pp. 178 193 Sandra Peterson/Richard C. Stapleton* T HE P RICING OF O PTIONS ON C REDIT-S ENSITIVE B ONDS A BSTRACT We build a three-factor term-structure

Schmalenbach Business Review Vol. 55 July 2003 pp. 178 193 Sandra Peterson/Richard C. Stapleton* T HE P RICING OF O PTIONS ON C REDIT-S ENSITIVE B ONDS A BSTRACT We build a three-factor term-structure

ON THE VALUATION OF CORPORATE BONDS

ON THE VALUATION OF CORPORATE BONDS by Edwin J. Elton,* Martin J. Gruber,* Deepak Agrawal** and Christopher Mann** * Nomura Professors, New York University ** Doctoral students, New York University 43

ON THE VALUATION OF CORPORATE BONDS by Edwin J. Elton,* Martin J. Gruber,* Deepak Agrawal** and Christopher Mann** * Nomura Professors, New York University ** Doctoral students, New York University 43

The Valuation of Currency Options

The Valuation of Currency Options Nahum Biger and John Hull Both Nahum Biger and John Hull are Associate Professors of Finance in the Faculty of Administrative Studies, York University, Canada. Introduction

The Valuation of Currency Options Nahum Biger and John Hull Both Nahum Biger and John Hull are Associate Professors of Finance in the Faculty of Administrative Studies, York University, Canada. Introduction

Master of Mathematical Finance: Course Descriptions

Master of Mathematical Finance: Course Descriptions CS 522 Data Mining Computer Science This course provides continued exploration of data mining algorithms. More sophisticated algorithms such as support

Master of Mathematical Finance: Course Descriptions CS 522 Data Mining Computer Science This course provides continued exploration of data mining algorithms. More sophisticated algorithms such as support

Market Value of Insurance Contracts with Profit Sharing 1

Market Value of Insurance Contracts with Profit Sharing 1 Pieter Bouwknegt Nationale-Nederlanden Actuarial Dept PO Box 796 3000 AT Rotterdam The Netherlands Tel: (31)10-513 1326 Fax: (31)10-513 0120 E-mail:

Market Value of Insurance Contracts with Profit Sharing 1 Pieter Bouwknegt Nationale-Nederlanden Actuarial Dept PO Box 796 3000 AT Rotterdam The Netherlands Tel: (31)10-513 1326 Fax: (31)10-513 0120 E-mail:

LECTURE 10.1 Default risk in Merton s model

LECTURE 10.1 Default risk in Merton s model Adriana Breccia March 12, 2012 1 1 MERTON S MODEL 1.1 Introduction Credit risk is the risk of suffering a financial loss due to the decline in the creditworthiness

LECTURE 10.1 Default risk in Merton s model Adriana Breccia March 12, 2012 1 1 MERTON S MODEL 1.1 Introduction Credit risk is the risk of suffering a financial loss due to the decline in the creditworthiness

Hedging Illiquid FX Options: An Empirical Analysis of Alternative Hedging Strategies

Hedging Illiquid FX Options: An Empirical Analysis of Alternative Hedging Strategies Drazen Pesjak Supervised by A.A. Tsvetkov 1, D. Posthuma 2 and S.A. Borovkova 3 MSc. Thesis Finance HONOURS TRACK Quantitative

Hedging Illiquid FX Options: An Empirical Analysis of Alternative Hedging Strategies Drazen Pesjak Supervised by A.A. Tsvetkov 1, D. Posthuma 2 and S.A. Borovkova 3 MSc. Thesis Finance HONOURS TRACK Quantitative

Explaining the Lehman Brothers Option Adjusted Spread of a Corporate Bond

Fixed Income Quantitative Credit Research February 27, 2006 Explaining the Lehman Brothers Option Adjusted Spread of a Corporate Bond Claus M. Pedersen Explaining the Lehman Brothers Option Adjusted Spread

Fixed Income Quantitative Credit Research February 27, 2006 Explaining the Lehman Brothers Option Adjusted Spread of a Corporate Bond Claus M. Pedersen Explaining the Lehman Brothers Option Adjusted Spread

Chapter 22 Credit Risk

Chapter 22 Credit Risk May 22, 2009 20.28. Suppose a 3-year corporate bond provides a coupon of 7% per year payable semiannually and has a yield of 5% (expressed with semiannual compounding). The yields

Chapter 22 Credit Risk May 22, 2009 20.28. Suppose a 3-year corporate bond provides a coupon of 7% per year payable semiannually and has a yield of 5% (expressed with semiannual compounding). The yields

Credit Implied Volatility

Credit Implied Volatility Bryan Kelly* Gerardo Manzo Diogo Palhares University of Chicago & NBER University of Chicago AQR Capital Management January 2015 PRELIMINARY AND INCOMPLETE Abstract We introduce

Credit Implied Volatility Bryan Kelly* Gerardo Manzo Diogo Palhares University of Chicago & NBER University of Chicago AQR Capital Management January 2015 PRELIMINARY AND INCOMPLETE Abstract We introduce

On Estimating the Relation Between Corporate Bond Yield Spreads and Treasury Yields

On Estimating the Relation Between Corporate Bond Yield Spreads and Treasury Yields Gady Jacoby I.H. Asper School of Business The University of Manitoba Current Draft: October 2002 Dept. of Accounting

On Estimating the Relation Between Corporate Bond Yield Spreads and Treasury Yields Gady Jacoby I.H. Asper School of Business The University of Manitoba Current Draft: October 2002 Dept. of Accounting

LIFE INSURANCE AND WEALTH MANAGEMENT PRACTICE COMMITTEE AND GENERAL INSURANCE PRACTICE COMMITTEE

LIFE INSURANCE AND WEALTH MANAGEMENT PRACTICE COMMITTEE AND GENERAL INSURANCE PRACTICE COMMITTEE Information Note: Discount Rates for APRA Capital Standards Contents 1. Status of Information Note 3 2.

LIFE INSURANCE AND WEALTH MANAGEMENT PRACTICE COMMITTEE AND GENERAL INSURANCE PRACTICE COMMITTEE Information Note: Discount Rates for APRA Capital Standards Contents 1. Status of Information Note 3 2.

Valuation of Razorback Executive Stock Options: A Simulation Approach

Valuation of Razorback Executive Stock Options: A Simulation Approach Joe Cheung Charles J. Corrado Department of Accounting & Finance The University of Auckland Private Bag 92019 Auckland, New Zealand.

Valuation of Razorback Executive Stock Options: A Simulation Approach Joe Cheung Charles J. Corrado Department of Accounting & Finance The University of Auckland Private Bag 92019 Auckland, New Zealand.

LOS 56.a: Explain steps in the bond valuation process.

The following is a review of the Analysis of Fixed Income Investments principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: Introduction

The following is a review of the Analysis of Fixed Income Investments principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: Introduction

Structural Recovery of Face Value at Default

Structural Recovery of Face Value at Default Rajiv Guha and Alessandro Sbuelz First Version: December 2002 This Version: December 2005 Abstract A Recovery of Face Value at Default (RFV) means receiving

Structural Recovery of Face Value at Default Rajiv Guha and Alessandro Sbuelz First Version: December 2002 This Version: December 2005 Abstract A Recovery of Face Value at Default (RFV) means receiving

LIBOR vs. OIS: The Derivatives Discounting Dilemma

LIBOR vs. OIS: The Derivatives Discounting Dilemma John Hull PRMIA May 2012 1 Agenda OIS and LIBOR CVA and DVA The Main Result Potential Sources of Confusion FVA and DVA See John Hull and Alan White: LIBOR

LIBOR vs. OIS: The Derivatives Discounting Dilemma John Hull PRMIA May 2012 1 Agenda OIS and LIBOR CVA and DVA The Main Result Potential Sources of Confusion FVA and DVA See John Hull and Alan White: LIBOR

Derivatives: Principles and Practice

Derivatives: Principles and Practice Rangarajan K. Sundaram Stern School of Business New York University New York, NY 10012 Sanjiv R. Das Leavey School of Business Santa Clara University Santa Clara, CA

Derivatives: Principles and Practice Rangarajan K. Sundaram Stern School of Business New York University New York, NY 10012 Sanjiv R. Das Leavey School of Business Santa Clara University Santa Clara, CA

Credit Swap Valuation

Credit Swap Valuation Darrell Duffie Graduate School of Business, Stanford University Draft: November 6, 1998 Forthcoming: Financial Analyst s Journal Abstract: This 1 article explains the basics of pricing

Credit Swap Valuation Darrell Duffie Graduate School of Business, Stanford University Draft: November 6, 1998 Forthcoming: Financial Analyst s Journal Abstract: This 1 article explains the basics of pricing

STRUCTURAL VERSUS REDUCED FORM MODELS: A NEW INFORMATION BASED PERSPECTIVE

JOIM JOURNAL OF INVESTMENT MANAGEMENT, Vol. 2, No. 2, (2004), pp. 1 10 JOIM 2004 www.joim.com STRUCTURAL VERSUS REDUCED FORM MODELS: A NEW INFORMATION BASED PERSPECTIVE Robert A. Jarrow a, and Philip Protter

JOIM JOURNAL OF INVESTMENT MANAGEMENT, Vol. 2, No. 2, (2004), pp. 1 10 JOIM 2004 www.joim.com STRUCTURAL VERSUS REDUCED FORM MODELS: A NEW INFORMATION BASED PERSPECTIVE Robert A. Jarrow a, and Philip Protter

Caput Derivatives: October 30, 2003

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Schonbucher Chapter 9: Firm Value and Share Priced-Based Models Updated 07-30-2007

Schonbucher Chapter 9: Firm alue and Share Priced-Based Models Updated 07-30-2007 (References sited are listed in the book s bibliography, except Miller 1988) For Intensity and spread-based models of default

Schonbucher Chapter 9: Firm alue and Share Priced-Based Models Updated 07-30-2007 (References sited are listed in the book s bibliography, except Miller 1988) For Intensity and spread-based models of default

Eurodollar Futures, and Forwards

5 Eurodollar Futures, and Forwards In this chapter we will learn about Eurodollar Deposits Eurodollar Futures Contracts, Hedging strategies using ED Futures, Forward Rate Agreements, Pricing FRAs. Hedging

5 Eurodollar Futures, and Forwards In this chapter we will learn about Eurodollar Deposits Eurodollar Futures Contracts, Hedging strategies using ED Futures, Forward Rate Agreements, Pricing FRAs. Hedging

Black-Scholes-Merton approach merits and shortcomings

Black-Scholes-Merton approach merits and shortcomings Emilia Matei 1005056 EC372 Term Paper. Topic 3 1. Introduction The Black-Scholes and Merton method of modelling derivatives prices was first introduced

Black-Scholes-Merton approach merits and shortcomings Emilia Matei 1005056 EC372 Term Paper. Topic 3 1. Introduction The Black-Scholes and Merton method of modelling derivatives prices was first introduced

Interest Rate Swaps. Key Concepts and Buzzwords. Readings Tuckman, Chapter 18. Swaps Swap Spreads Credit Risk of Swaps Uses of Swaps

Interest Rate Swaps Key Concepts and Buzzwords Swaps Swap Spreads Credit Risk of Swaps Uses of Swaps Readings Tuckman, Chapter 18. Counterparty, Notional amount, Plain vanilla swap, Swap rate Interest

Interest Rate Swaps Key Concepts and Buzzwords Swaps Swap Spreads Credit Risk of Swaps Uses of Swaps Readings Tuckman, Chapter 18. Counterparty, Notional amount, Plain vanilla swap, Swap rate Interest

IASB/FASB Meeting Week beginning 11 April 2011. Top down approaches to discount rates

IASB/FASB Meeting Week beginning 11 April 2011 IASB Agenda reference 5A FASB Agenda Staff Paper reference 63A Contacts Matthias Zeitler [email protected] +44 (0)20 7246 6453 Shayne Kuhaneck [email protected]

IASB/FASB Meeting Week beginning 11 April 2011 IASB Agenda reference 5A FASB Agenda Staff Paper reference 63A Contacts Matthias Zeitler [email protected] +44 (0)20 7246 6453 Shayne Kuhaneck [email protected]

OR/MS Today - June 2007. Financial O.R. A Pointer on Points

OR/MS Today - June 2007 Financial O.R. A Pointer on Points Given the array of residential mortgage products, should a homebuyer pay upfront points in order to lower the annual percentage rate? Introducing

OR/MS Today - June 2007 Financial O.R. A Pointer on Points Given the array of residential mortgage products, should a homebuyer pay upfront points in order to lower the annual percentage rate? Introducing

C(t) (1 + y) 4. t=1. For the 4 year bond considered above, assume that the price today is 900$. The yield to maturity will then be the y that solves

(1 + y) 4. t=1. For the 4 year bond considered above, assume that the price today is 900$. The yield to maturity will then be the y that solves") Economics 7344, Spring 2013 Bent E. Sørensen INTEREST RATE THEORY We will cover fixed income securities. The major categories of long-term fixed income securities are federal government bonds, corporate

Economics 7344, Spring 2013 Bent E. Sørensen INTEREST RATE THEORY We will cover fixed income securities. The major categories of long-term fixed income securities are federal government bonds, corporate

FIN 472 Fixed-Income Securities Forward Rates

FIN 472 Fixed-Income Securities Forward Rates Professor Robert B.H. Hauswald Kogod School of Business, AU Interest-Rate Forwards Review of yield curve analysis Forwards yet another use of yield curve forward

FIN 472 Fixed-Income Securities Forward Rates Professor Robert B.H. Hauswald Kogod School of Business, AU Interest-Rate Forwards Review of yield curve analysis Forwards yet another use of yield curve forward

Learning Curve September 2005. Understanding the Z-Spread Moorad Choudhry*

Learning Curve September 2005 Understanding the Z-Spread Moorad Choudhry* A key measure of relative value of a corporate bond is its swap spread. This is the basis point spread over the interest-rate swap

Learning Curve September 2005 Understanding the Z-Spread Moorad Choudhry* A key measure of relative value of a corporate bond is its swap spread. This is the basis point spread over the interest-rate swap

Equity-index-linked swaps

Equity-index-linked swaps Equivalent to portfolios of forward contracts calling for the exchange of cash flows based on two different investment rates: a variable debt rate (e.g. 3-month LIBOR) and the

Equity-index-linked swaps Equivalent to portfolios of forward contracts calling for the exchange of cash flows based on two different investment rates: a variable debt rate (e.g. 3-month LIBOR) and the

MONEY MARKET SUBCOMMITEE(MMS) FLOATING RATE NOTE PRICING SPECIFICATION

FLOATING RATE NOTE PRICING SPECIFICATION") MONEY MARKET SUBCOMMITEE(MMS) FLOATING RATE NOTE PRICING SPECIFICATION This document outlines the use of the margin discounting methodology to price vanilla money market floating rate notes as endorsed

MONEY MARKET SUBCOMMITEE(MMS) FLOATING RATE NOTE PRICING SPECIFICATION This document outlines the use of the margin discounting methodology to price vanilla money market floating rate notes as endorsed

Article from: Risk Management. June 2009 Issue 16

Article from: Risk Management June 2009 Issue 16 CHAIRSPERSON S Risk quantification CORNER Structural Credit Risk Modeling: Merton and Beyond By Yu Wang The past two years have seen global financial markets

Article from: Risk Management June 2009 Issue 16 CHAIRSPERSON S Risk quantification CORNER Structural Credit Risk Modeling: Merton and Beyond By Yu Wang The past two years have seen global financial markets

Part V: Option Pricing Basics

erivatives & Risk Management First Week: Part A: Option Fundamentals payoffs market microstructure Next 2 Weeks: Part B: Option Pricing fundamentals: intrinsic vs. time value, put-call parity introduction

erivatives & Risk Management First Week: Part A: Option Fundamentals payoffs market microstructure Next 2 Weeks: Part B: Option Pricing fundamentals: intrinsic vs. time value, put-call parity introduction

BINOMIAL OPTION PRICING

Darden Graduate School of Business Administration University of Virginia BINOMIAL OPTION PRICING Binomial option pricing is a simple but powerful technique that can be used to solve many complex option-pricing

Darden Graduate School of Business Administration University of Virginia BINOMIAL OPTION PRICING Binomial option pricing is a simple but powerful technique that can be used to solve many complex option-pricing

Published in Journal of Investment Management, Vol. 13, No. 1 (2015): 64-83

: 64-83") Published in Journal of Investment Management, Vol. 13, No. 1 (2015): 64-83 OIS Discounting, Interest Rate Derivatives, and the Modeling of Stochastic Interest Rate Spreads John Hull and Alan White Joseph

Published in Journal of Investment Management, Vol. 13, No. 1 (2015): 64-83 OIS Discounting, Interest Rate Derivatives, and the Modeling of Stochastic Interest Rate Spreads John Hull and Alan White Joseph

Option Valuation. Chapter 21

Option Valuation Chapter 21 Intrinsic and Time Value intrinsic value of in-the-money options = the payoff that could be obtained from the immediate exercise of the option for a call option: stock price

Option Valuation Chapter 21 Intrinsic and Time Value intrinsic value of in-the-money options = the payoff that could be obtained from the immediate exercise of the option for a call option: stock price

VALUATION OF PLAIN VANILLA INTEREST RATES SWAPS

Graduate School of Business Administration University of Virginia VALUATION OF PLAIN VANILLA INTEREST RATES SWAPS Interest-rate swaps have grown tremendously over the last 10 years. With this development,

Graduate School of Business Administration University of Virginia VALUATION OF PLAIN VANILLA INTEREST RATES SWAPS Interest-rate swaps have grown tremendously over the last 10 years. With this development,

FORWARDS AND EUROPEAN OPTIONS ON CDO TRANCHES. John Hull and Alan White. First Draft: December, 2006 This Draft: March 2007

FORWARDS AND EUROPEAN OPTIONS ON CDO TRANCHES John Hull and Alan White First Draft: December, 006 This Draft: March 007 Joseph L. Rotman School of Management University of Toronto 105 St George Street

FORWARDS AND EUROPEAN OPTIONS ON CDO TRANCHES John Hull and Alan White First Draft: December, 006 This Draft: March 007 Joseph L. Rotman School of Management University of Toronto 105 St George Street

Measuring and marking counterparty risk

Chapter 9 Measuring and marking counterparty risk Eduardo Canabarro Head of Credit Quantitative Risk Modeling, Goldman Sachs Darrell Duffie Professor, Stanford University Graduate School of Business Introduction

Chapter 9 Measuring and marking counterparty risk Eduardo Canabarro Head of Credit Quantitative Risk Modeling, Goldman Sachs Darrell Duffie Professor, Stanford University Graduate School of Business Introduction

What Drives Interest Rate Swap Spreads?

What Drives Interest Rate Swap Spreads? An Empirical Analysis of Structural Changes and Implications for Modeling the Dynamics of the Swap Term Structure Kodjo M. Apedjinou Job Market Paper First Draft:

What Drives Interest Rate Swap Spreads? An Empirical Analysis of Structural Changes and Implications for Modeling the Dynamics of the Swap Term Structure Kodjo M. Apedjinou Job Market Paper First Draft:

Extending Factor Models of Equity Risk to Credit Risk and Default Correlation. Dan dibartolomeo Northfield Information Services September 2010

Extending Factor Models of Equity Risk to Credit Risk and Default Correlation Dan dibartolomeo Northfield Information Services September 2010 Goals for this Presentation Illustrate how equity factor risk

Extending Factor Models of Equity Risk to Credit Risk and Default Correlation Dan dibartolomeo Northfield Information Services September 2010 Goals for this Presentation Illustrate how equity factor risk

Black and Scholes - A Review of Option Pricing Model

CAPM Option Pricing Sven Husmann a, Neda Todorova b a Department of Business Administration, European University Viadrina, Große Scharrnstraße 59, D-15230 Frankfurt (Oder, Germany, Email: [email protected],

CAPM Option Pricing Sven Husmann a, Neda Todorova b a Department of Business Administration, European University Viadrina, Große Scharrnstraße 59, D-15230 Frankfurt (Oder, Germany, Email: [email protected],

How Much of the Corporate-Treasury Yield Spread is Due to Credit Risk? 1

How Much of the Corporate-Treasury Yield Spread is Due to Credit Risk? 1 Jing-zhi Huang 2 Penn State University and New York University and Ming Huang 3 Stanford University This draft: May, 2003 1 We thank

How Much of the Corporate-Treasury Yield Spread is Due to Credit Risk? 1 Jing-zhi Huang 2 Penn State University and New York University and Ming Huang 3 Stanford University This draft: May, 2003 1 We thank

American and European. Put Option

American and European Put Option Analytical Finance I Kinda Sumlaji 1 Table of Contents: 1. Introduction... 3 2. Option Style... 4 3. Put Option 4 3.1 Definition 4 3.2 Payoff at Maturity... 4 3.3 Example

American and European Put Option Analytical Finance I Kinda Sumlaji 1 Table of Contents: 1. Introduction... 3 2. Option Style... 4 3. Put Option 4 3.1 Definition 4 3.2 Payoff at Maturity... 4 3.3 Example

CREATING A CORPORATE BOND SPOT YIELD CURVE FOR PENSION DISCOUNTING DEPARTMENT OF THE TREASURY OFFICE OF ECONOMIC POLICY WHITE PAPER FEBRUARY 7, 2005

CREATING A CORPORATE BOND SPOT YIELD CURVE FOR PENSION DISCOUNTING I. Introduction DEPARTMENT OF THE TREASURY OFFICE OF ECONOMIC POLICY WHITE PAPER FEBRUARY 7, 2005 Plan sponsors, plan participants and

CREATING A CORPORATE BOND SPOT YIELD CURVE FOR PENSION DISCOUNTING I. Introduction DEPARTMENT OF THE TREASURY OFFICE OF ECONOMIC POLICY WHITE PAPER FEBRUARY 7, 2005 Plan sponsors, plan participants and

FIXED-INCOME SECURITIES. Chapter 10. Swaps

FIXED-INCOME SECURITIES Chapter 10 Swaps Outline Terminology Convention Quotation Uses of Swaps Pricing of Swaps Non Plain Vanilla Swaps Terminology Definition Agreement between two parties They exchange

FIXED-INCOME SECURITIES Chapter 10 Swaps Outline Terminology Convention Quotation Uses of Swaps Pricing of Swaps Non Plain Vanilla Swaps Terminology Definition Agreement between two parties They exchange

Zero-Coupon Bonds (Pure Discount Bonds)

") Zero-Coupon Bonds (Pure Discount Bonds) The price of a zero-coupon bond that pays F dollars in n periods is F/(1 + r) n, where r is the interest rate per period. Can meet future obligations without reinvestment

Zero-Coupon Bonds (Pure Discount Bonds) The price of a zero-coupon bond that pays F dollars in n periods is F/(1 + r) n, where r is the interest rate per period. Can meet future obligations without reinvestment

Constructing Portfolios of Constant-Maturity Fixed- Income ETFs

Constructing Portfolios of Constant-Maturity Fixed- Income ETFs Newfound Research LLC December 2013 For more information about Newfound Research call us at +1-617-531-9773, visit us at www.thinknewfound.com

Constructing Portfolios of Constant-Maturity Fixed- Income ETFs Newfound Research LLC December 2013 For more information about Newfound Research call us at +1-617-531-9773, visit us at www.thinknewfound.com

Pricing European and American bond option under the Hull White extended Vasicek model

1 Academic Journal of Computational and Applied Mathematics /August 2013/ UISA Pricing European and American bond option under the Hull White extended Vasicek model Eva Maria Rapoo 1, Mukendi Mpanda 2

1 Academic Journal of Computational and Applied Mathematics /August 2013/ UISA Pricing European and American bond option under the Hull White extended Vasicek model Eva Maria Rapoo 1, Mukendi Mpanda 2

One Period Binomial Model

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 One Period Binomial Model These notes consider the one period binomial model to exactly price an option. We will consider three different methods of pricing

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 One Period Binomial Model These notes consider the one period binomial model to exactly price an option. We will consider three different methods of pricing

Option pricing. Vinod Kothari

Option pricing Vinod Kothari Notation we use this Chapter will be as follows: S o : Price of the share at time 0 S T : Price of the share at time T T : time to maturity of the option r : risk free rate

Option pricing Vinod Kothari Notation we use this Chapter will be as follows: S o : Price of the share at time 0 S T : Price of the share at time T T : time to maturity of the option r : risk free rate

Application of Quantitative Credit Risk Models in Fixed Income Portfolio Management

Application of Quantitative Credit Risk Models in Fixed Income Portfolio Management Ron D Vari, Ph.D., Kishore Yalamanchili, Ph.D., and David Bai, Ph.D. State Street Research and Management September 26-3,

Application of Quantitative Credit Risk Models in Fixed Income Portfolio Management Ron D Vari, Ph.D., Kishore Yalamanchili, Ph.D., and David Bai, Ph.D. State Street Research and Management September 26-3,

How To Sell A Callable Bond

1.1 Callable bonds A callable bond is a fixed rate bond where the issuer has the right but not the obligation to repay the face value of the security at a pre-agreed value prior to the final original maturity

1.1 Callable bonds A callable bond is a fixed rate bond where the issuer has the right but not the obligation to repay the face value of the security at a pre-agreed value prior to the final original maturity

Options: Valuation and (No) Arbitrage

Arbitrage") Prof. Alex Shapiro Lecture Notes 15 Options: Valuation and (No) Arbitrage I. Readings and Suggested Practice Problems II. Introduction: Objectives and Notation III. No Arbitrage Pricing Bound IV. The Binomial

Prof. Alex Shapiro Lecture Notes 15 Options: Valuation and (No) Arbitrage I. Readings and Suggested Practice Problems II. Introduction: Objectives and Notation III. No Arbitrage Pricing Bound IV. The Binomial

Analytical Research Series

EUROPEAN FIXED INCOME RESEARCH Analytical Research Series INTRODUCTION TO ASSET SWAPS Dominic O Kane January 2000 Lehman Brothers International (Europe) Pub Code 403 Summary An asset swap is a synthetic

EUROPEAN FIXED INCOME RESEARCH Analytical Research Series INTRODUCTION TO ASSET SWAPS Dominic O Kane January 2000 Lehman Brothers International (Europe) Pub Code 403 Summary An asset swap is a synthetic

Fair Value Measurement

Indian Accounting Standard (Ind AS) 113 Fair Value Measurement (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type

Indian Accounting Standard (Ind AS) 113 Fair Value Measurement (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type

Pricing Interest Rate Derivatives Using Black-Derman-Toy Short Rate Binomial Tree

Pricing Interest Rate Derivatives Using Black-Derman-Toy Short Rate Binomial Tree Shing Hing Man http://lombok.demon.co.uk/financialtap/ 3th August, 0 Abstract This note describes how to construct a short

Pricing Interest Rate Derivatives Using Black-Derman-Toy Short Rate Binomial Tree Shing Hing Man http://lombok.demon.co.uk/financialtap/ 3th August, 0 Abstract This note describes how to construct a short

Tutorial: Structural Models of the Firm

Tutorial: Structural Models of the Firm Peter Ritchken Case Western Reserve University February 16, 2015 Peter Ritchken, Case Western Reserve University Tutorial: Structural Models of the Firm 1/61 Tutorial:

Tutorial: Structural Models of the Firm Peter Ritchken Case Western Reserve University February 16, 2015 Peter Ritchken, Case Western Reserve University Tutorial: Structural Models of the Firm 1/61 Tutorial:

How To Understand A Rates Transaction

International Swaps and Derivatives Association, Inc. Disclosure Annex for Interest Rate Transactions This Annex supplements and should be read in conjunction with the General Disclosure Statement. NOTHING

International Swaps and Derivatives Association, Inc. Disclosure Annex for Interest Rate Transactions This Annex supplements and should be read in conjunction with the General Disclosure Statement. NOTHING

Global Financial Management

Global Financial Management Bond Valuation Copyright 999 by Alon Brav, Campbell R. Harvey, Stephen Gray and Ernst Maug. All rights reserved. No part of this lecture may be reproduced without the permission

Global Financial Management Bond Valuation Copyright 999 by Alon Brav, Campbell R. Harvey, Stephen Gray and Ernst Maug. All rights reserved. No part of this lecture may be reproduced without the permission

Bond valuation and bond yields

RELEVANT TO ACCA QUALIFICATION PAPER P4 AND PERFORMANCE OBJECTIVES 15 AND 16 Bond valuation and bond yields Bonds and their variants such as loan notes, debentures and loan stock, are IOUs issued by governments

RELEVANT TO ACCA QUALIFICATION PAPER P4 AND PERFORMANCE OBJECTIVES 15 AND 16 Bond valuation and bond yields Bonds and their variants such as loan notes, debentures and loan stock, are IOUs issued by governments

Interest Rate and Currency Swaps

Interest Rate and Currency Swaps Eiteman et al., Chapter 14 Winter 2004 Bond Basics Consider the following: Zero-Coupon Zero-Coupon One-Year Implied Maturity Bond Yield Bond Price Forward Rate t r 0 (0,t)

Interest Rate and Currency Swaps Eiteman et al., Chapter 14 Winter 2004 Bond Basics Consider the following: Zero-Coupon Zero-Coupon One-Year Implied Maturity Bond Yield Bond Price Forward Rate t r 0 (0,t)

Beyond preferred stock valuation of complex equity and hybrid instruments

Beyond preferred stock valuation of complex equity and hybrid instruments ASA Advanced Business Valuation Conference October 2015 Amanda A. Miller, Ph.D. 4 June 2015 Amanda A. Miller, Ph.D. ([email protected])

Beyond preferred stock valuation of complex equity and hybrid instruments ASA Advanced Business Valuation Conference October 2015 Amanda A. Miller, Ph.D. 4 June 2015 Amanda A. Miller, Ph.D. ([email protected])