FINANCIAL ACCOUNTING

|

|

|

- Dinah Parker

- 10 years ago

- Views:

Transcription

1 FINANCIAL ACCOUNTING FORMATION 2 EXAMINATION - AUGUST 2012 NOTES: You are required to answer Question 1. You are also required to answer any three out of Questions 2 to 5. (If you provide answers to all of Questions 2 to 5, you must draw a clearly distinguishable line through the answer not to be marked. Otherwise, only the first three answers to hand for Questions 2 to 5 will be marked.) Note: Students have optional use of the Extended Trial Balance, which if used, must be included in the answer booklet. PRO-FORMA STATEMENT OF COMPREHENSIVE INCOME BY NATURE, STATEMENT OF COMPREHENSIVE INCOME BY FUNCTION AND STATEMENT OF FINANCIAL POSITION ARE PROVIDED. TIME ALLOWED: 3.5 hours, plus 10 minutes to read the paper. INSTRUCTIONS: During the reading time you may write notes on the examination paper but you may not commence writing in your answer book. Marks for each question are shown. The pass mark required is 50% in total over the whole paper. Start your answer to each question on a new page. You are reminded to pay particular attention to your communication skills and care must be taken regarding the format and literacy of the solutions. The marking system will take into account the content of your answers and the extent to which answers are supported with relevant legislation, case law or examples where appropriate. List on the cover of each answer booklet, in the space provided, the number of each question(s) attempted. The Institute of Certified Public Accountants in Ireland, 17 Harcourt Street, Dublin 2.

Note: Students have optional use of the Extended Trial Balance, which if used, must be included in the answer booklet.")

2 THE INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS IN IRELAND FINANCIAL ACCOUNTING FORMATION 2 EXAMINATION - AUGUST 2012 Time allowed: 3.5 hours plus 10 minutes to read the paper. Answer Question 1 and three of the remaining four questions. Note: Students have optional use of the Extended Trial Balance, which if used, must be included in the answer booklet. 1. (a) A company is deciding how to measure the value of a motor vehicle in their accounts. At a recent meeting, the following alternatives were considered: i) Value the motor vehicle at 10,000. This is based on the cost of the motor vehicle when purchased two years ago; ii) Value the motor vehicle at 12,000. This is based on the cost of a similar motor vehicle if purchased today; iii) Value the motor vehicle at 7,000. This is based on the sales price of a similar motor vehicle if sold today; iv) Value the motor vehicle at 8,000. This is based on an estimate of what a similar motor vehicle will return to them in cash from its use and which has been discounted into what the cash will be worth in today s money. For i) to iv) above outline which measurement base is being used and discuss any three (3) of these measurement bases in relation to measuring assets. (10 marks) Page1

Value the motor vehicle at 12,000.")

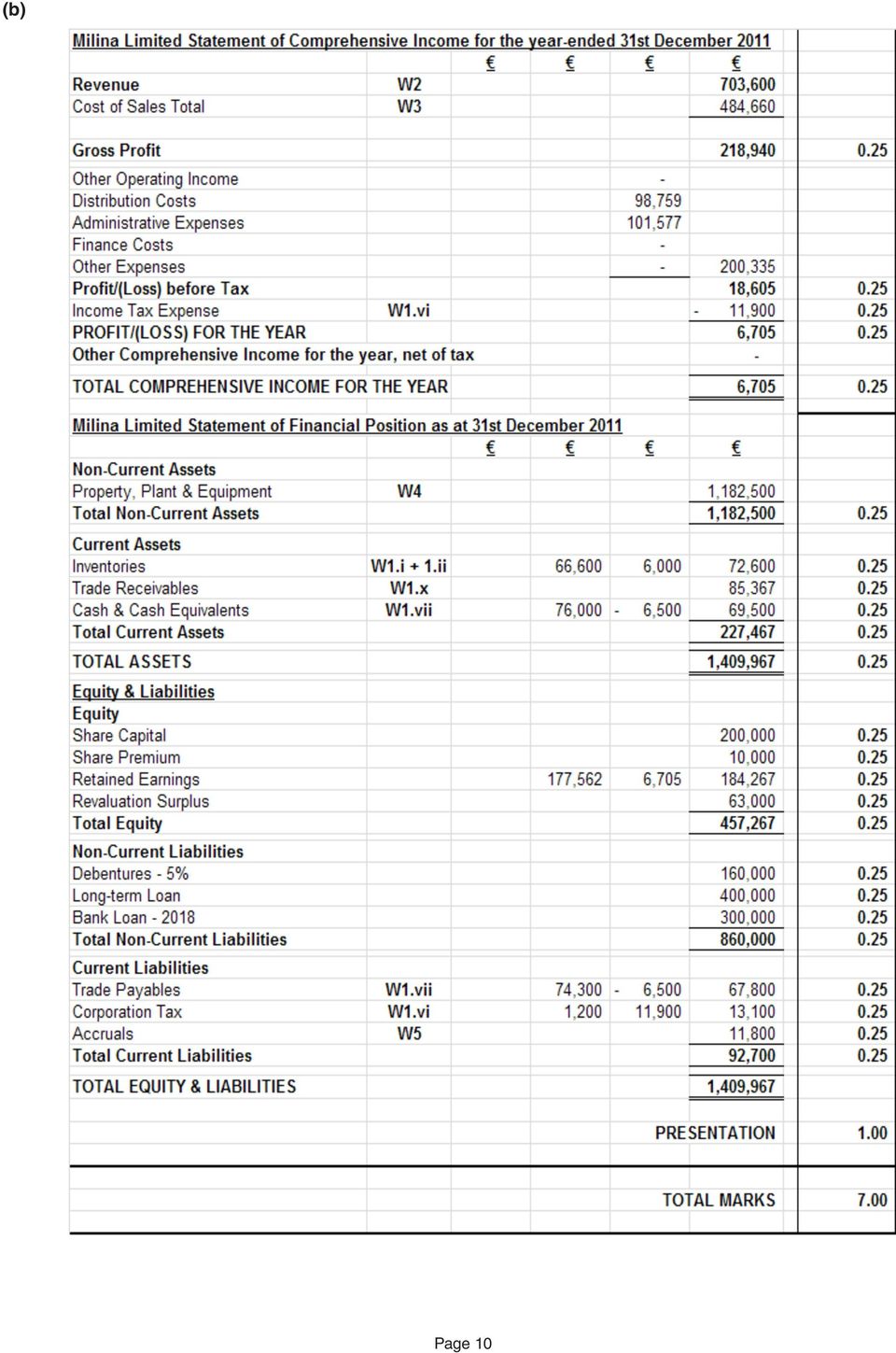

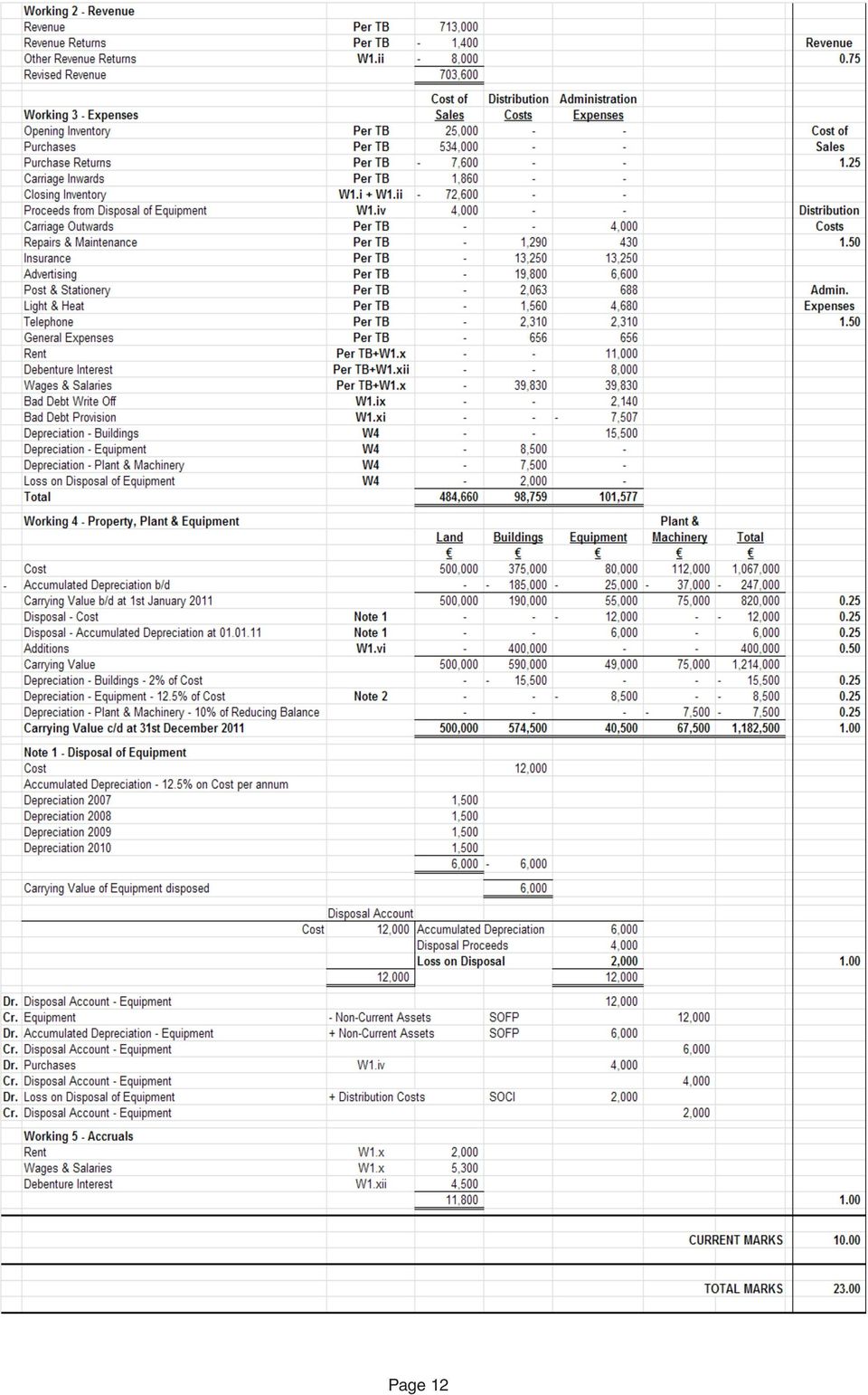

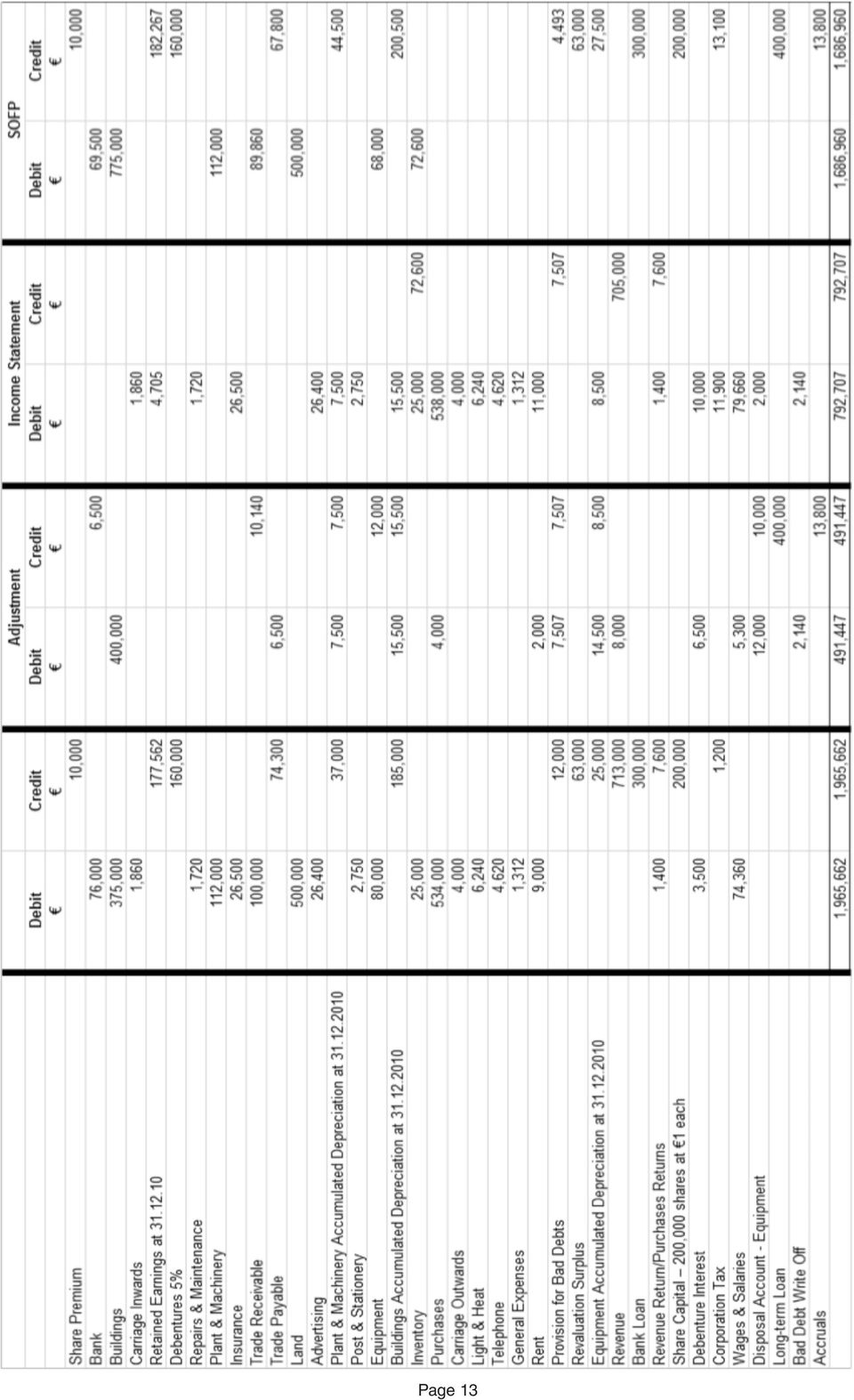

3 (b) The following trial balance was extracted from the books of Milina Limited as at 30 June 2012: Debit Credit Share Premium 10,000 Repairs & Maintenance 1,720 Buildings 375,000 Carriage Outwards 4,000 Debentures 5% 160,000 Bank Loan ,000 Revenue Returns/Purchases Returns 1,400 7,600 Plant & Machinery 112,000 Bank 76,000 Insurance 26,500 Revenue 713,000 Provision for Bad Debts 12,000 Trade Receivables/Trade Payables 100,000 74,300 Land 500,000 Advertising 26,400 Plant & Machinery Accumulated Depreciation at ,000 Post & Stationery 2,750 Equipment 80,000 Buildings Accumulated Depreciation at ,000 Opening Inventory 25,000 Light & Heat 6,240 Telephone 4,620 Revaluation Surplus 63,000 Equipment Accumulated Depreciation at ,000 General Expenses 1,312 Rent 9,000 Share Capital 200,000 shares at 1 each 200,000 Debenture Interest 3,500 Retained Earnings at ,562 Carriage Inwards 1,860 Corporation Tax 1,200 Purchases 534,000 Wages & Salaries 74,360 1,965,662 1,965,662 The following information, based on your investigations, has also come to your attention: (i) Milina Limited had counted the original cost of inventories at the year-end and they amounted to 68,000. However, some inventory items that originally cost 4,800 were damaged prior to the year-end and will require repair work that will cost an estimated 600. When repaired, these items could then be sold for 4,000. ii) iii) Included in Revenue is an amount of 10,000 for goods sold on a sale or return basis to a customer. One the 5 July 2012, 8,000 of the goods sold was returned. The margin on these goods when they are sold is 25%. Depreciation is to be charged as follows: Buildings 2% on Cost (100% to Administration Expenses) Equipment 12.5% on Cost (100% to Distribution Costs) Plant & Machinery 10% Reducing Balance (100% to Distribution Costs) Depreciation is charged in full in year of purchase and none in year of sale and this year s depreciation has not been included in the above trial balance. iv) Included in Purchases is 4,000 which is the proceeds from the disposal of equipment. This equipment was purchased for 12,000 on 1 February Page 2

4 v) No revaluation of any Property, Plant or Equipment took place in the year-ended 30 June vi) vii) viii) A building was purchased on 30 June 2012 for 400,000. This purchase was financed by a long-term loan. This transaction has yet to be included in the above trial balance. A payment for insurance of 6,500 has been credited to Trade Payables by mistake. The Corporation tax bill for the year ending 30 June 2012 is estimated at 11,900 and this has not been provided for in the above trial balance. ix) A customer has gone into liquidation and you are advised to write off the full balance owing 2,140. x) There are closing accruals for Rent and Wages & Salaries amounting to 2,000 and 5,300 respectively which have not yet been included in the above trial balance. xi) xii) xiii) The Provision for Bad Debts should be changed to 5% of Trade Receivables. Provide for the Debenture Interest outstanding at the year-end. The following expenses are to be allocated in the following proportions; Distribution Costs Administration Costs Repairs & Maintenance 75% 25% Insurance 50% 50% Advertising 75% 25% Post & Stationery 75% 25% Light & Heat 25% 75% Telephone 50% 50% General Expenses 50% 50% Rent 0% 100% Debenture Interest 0% 100% Wages & Salaries 50% 50% Carriage Outwards 0% 100% Bad Debts Write Off 0% 100% Bad Debt Provision 0% 100% REQUIREMENT: Prepare, in a form suitable for publication, a Statement of Comprehensive Income and Statement of Financial Position for Milina Limited for the financial year-ending 30 June Show all workings. The workings for an adjustment should be in the form of a double entry or a journal. There is not any need for a narrative. (30 marks) [Total: 40 Marks] Page 3

A customer has gone into liquidation and you are advised to write off the full balance owing 2,140.")

5 2. (a) Explain what is meant by the following: i) a prepayment. ii) an accrual. Use an example of each to help support your answer. (4 Marks) (b) Matthew is a sole trader who maintains a combined insurance and rent ledger account. He rents out an office on 1 December 2010 at an annual rent of 168,000 payable quarterly in advance. The insurance, which starts on1 October 2010, is paid twice a year one month in arrears and amounts to 72,000 for a year. The following were the payments made by Matthew during the year to 31 December Date Details Rent 42, Rent 42, Insurance 36, Rent 42, Rent 45, Insurance 36, Rent 45,000 Additional Information: i) Rent of 42,000 was paid on 1 December 2010 for the quarter to 28 February ii) A rent review took place on 1 December 2011 and the annual rent has now increased to 180,000 per annum from that date. iii) Insurance for the year-ending 30 September 2012 amounts to 84,000. REQUIREMENT: Prepare the Insurance and Rent ledger account for Matthew for the year-ending 31 December (7 Marks) (c) (d) In the context of IAS 16 Property, Plant & Equipment, explain what is meant by the terms Capital Expenditure and Revenue Expenditure. (4 Marks) State, with reasons, whether each of the following items should be classified as capital or revenue expenditure. i) Purchase of a van; ii) Painting of the van in the company colours on purchase of the van; iii) Repainting of the van three years later; iv) Servicing the van on a six month basis; v) Replacing the engine of the van after 2 years with a similar engine. (5 Marks) [Total: 20 Marks] Page 4

6 3. Walter Johnson, a local business person is starting to import goods from various countries abroad and has asked you, a trainee financial accountant, for advice on how to account for the effects of changes in foreign exchange rates for his company Translate Limited. Translate Limited s year-end is 31 December and its reporting or functional currency is the euro ( ). REQUIREMENT: Walter Johnson has asked you to prepare a report which addresses the following: (a) In accordance with IAS 21 Changes in Foreign Exchange Rates, describe what is meant by the following: i) A foreign currency transaction. ii) An exchange difference. (4 Marks) (b) In reporting a foreign currency transaction in the functional currency, how should the transaction be recognised: i) On initial recognition; ii) At the end of the reporting period. (6 Marks) (c) Translate Limited entered into the following foreign currency transaction: Purchased goods from the US for $120, Paid for the goods purchased on the The exchange rates are as follows: 1 US Dollars $ equals in REQUIREMENT: Record the above transactions in the books of Translate Limited for the years ended 31 December 2010 and 31 December (10 Marks) [Total: 20 Marks] Page 5

A foreign currency transaction. ii) An exchange difference.")

7 4. (a) Mr. Twiddle is a sole trader who has asked you, as his financial accountant, to prepare his trade receivables and trade payables ledger control accounts for the month of January 2012 and ascertain what the net balances of the respective ledgers should be on 31 January Balances on 1 January 2012 Trade Receivables Ledger Dr 58,145 Cr 12,843 Trade Payables Ledger Dr 13,751 Cr 47,485 Total for the Month to 31 January 2012 Purchases 98,658 Sales 138,039 Purchases Returns 14,471 Trade Receivables Accounts settled by contra accounts with Trade Payables 12,682 Bad Debt Written Off 13,987 Discounts and Allowances to Customers 12,791 Cash Received from Customers 132,216 Cash Discount Received 13,873 Cash Paid to Trade Payables 82,157 Cash Paid to Customers 12,653 REQUIREMENT: (i) Prepare the Trade Receivables and the Trade Payables Control Accounts for the month-ended 31 January (10 Marks) (ii) Provide possible reconcilable items for a Trade Payables Control Account Reconciliation. (5 Marks) (b) Mr. Twiddle sends out a Trade Receivables Statement to his customers at the end of every month. A customer of Mr. Twiddle s has contacted him complaining to him that there is a difference between Mr. Twiddle s statement and what the customer claims that he owes Mr. Twiddle. REQUIREMENT: Explain how differences can arise between Mr. Twiddle s Trade Receivables Statement that he sends to his customers showing the amount due to him and the amount that the customer is saying is owing to Mr. Twiddle. (5 Marks) [Total: 20 Marks] Page 6

8 5. Caherame Limited is a manufacturer of plastic troughs for the farming industry and its accounts are as follows: Caherame Limited Statement of Financial Position as at 31 December Non-Current Assets Property, Plant & Equipment 1,820 1,496 Development Expenditure Total Non-Current Assets 2,080 1,733 Current Assets Inventories Trade Receivables Cash Total Current Assets Total Assets 2,769 2,313 Equity & Liabilities Equity Share Capital 1, Share Premium Retained Earnings Revaluation Surplus Total Equity 2,046 1,452 Non-Current Liabilities Debentures 10% Total Non-Current Liabilities Current Liabilities Trade Payables Bank Overdraft Corporation Tax Total Current Liabilities Total Equity & Liabilities 2,769 2,313 Caherame Limited Statement of Comprehensive Income for the year-ended 31 December Revenue 6,400 Cost of Sales 5,800 Gross Profit 600 Distribution Costs (235) Administration Expenses (145) Interest Costs (30) Investment Income - Profit before Tax 190 Income Tax Expense (30) Profit for the Year 160 Other Comprehensive Income Gains on Property Revaluations 100 Total Other Comprehensive Income for the year, net of tax 100 Total Comprehensive Income for the year, net of tax 260 (Question 5 continued on Next Page) Page 7

9 (Question 5 Continued) Notes: i. Property, Plant & Equipment with a carrying value of 80,000 was sold for 110,000. This asset had originally cost 150,000. ii. Depreciation of Property, Plant & Equipment during the year amounted to 85,000. iii. Amortisation of Development Expenditure during the year amounted to 15,000. iv. Dividends paid during the year amounted to 30,000 and are reported in the Statement of Changes in Equity. v. Debentures were redeemed on the 30 September REQUIREMENT: Prepare a Statement of Cash Flows for the year-ended 31 December 2011 for Caherame Limited. [Total: 20 Marks] END OF PAPER Page 8

10 SUGGESTED SOLUTIONS THE INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS IN IRELAND FINANCIAL ACCOUNTING FORMATION 2 EXAMINATION - AUGUST 2012 SOLUTION 1 (a) i) Historical cost ii) Current cost iii) Realisable (settlement) value iv) Present value (4 Marks) Historical cost Per the conceptual framework, under historical cost, assets are recorded at the amount of cash or cash equivalents paid or the fair value of the consideration given to acquire them at the time of their acquisition. Current cost Assets are recorded at the amount of cash or cash equivalents that would have to be paid if the same or an equivalent asset was acquired currently. Realisable (settlement) value Assets are carried at the amount of cash or cash equivalents that could currently be obtained by selling the asset in an orderly disposal. Present value Assets are carried at the present discounted value of the future net cash inflows that the item is expected to generate in the normal course of business. Discuss any 3 of the above measurement bases in relation to assets (6 Marks) Page 9

11 (b) Page 10

12 Working - Journal Entries Working - Closing Inventory Total Inventories at Cost per Inventory Count 68,000 Damaged Inventories - Cost 4,800 NRV - Selling Price less costs to sell (4, ) -3,400 Inventory Write Down 1,400 Value of Closing Inventories 66,600 '000 '000 1.i Dr. Inventory + Current Assets SOFP 66, Cr. Closing Inventory - Cost of Sales SOCI 66,600 1.ii Dr. Revenue - Revenue SOCI 8, Cr. Trade Receivable - Current Assets SOFP 8,000 Dr. Closing Inventory + Current Assets SOFP 6, Cr. Closing Inventory - Cost of Sales SOCI 6,000 1.iv Dr. Purchases - Cost of Sales SOCI 4, Cr. Disposal Account 4,000 1.vi Dr. Buildings + Non-Current Assets SOFP 400, Cr. Long-term Loan + Non-Current Liabilities SOFP 400,000 1.vii Dr. Trade Payables - Current Liabilities SOFP 6, Cr. Bank - Current Asset SOFP 6,500 1.viii Dr. Corporation Tax + Expenses SOCI 11, Cr. Corporation Tax Due + Current Liabilities SOFP 11,900 1.ix Dr. Bad Debt Write Off + Expenses SOCI 2, Cr. Trade Receivables - Current Assets SOFP 2,140 1.x Dr. Rent + Expenses SOCI 2, Dr. Wages & Salaries + Expenses SOCI 5,300 Cr. Accruals + Current Liabilities SOFP 7,300 1.xi Dr. Trade Receivables + Current Assets SOFP 7, Cr. Decrease in Bad Debt Provision + Other Income SOCI 7,507 Trade Receivables Balance per TB 100,000 Less Goods Returned W1.ii -8,000 - Bad Debt Write Off W1.vii -2,140 89,860 - Bad Debt Provision - 5% -4,493 Revised Trade Receivable 85,367 Current Bad Debt Provision TB 12,000 New Bad Debt Provision See Above 4,493 Decrease in Bad Debt Provision -7,507 1.xii Dr. Debenture Interest + Expenses SOCI 4,500 Cr. Debenture Interest Due + Current Liabilities SOFP 4, Debentures Per TB 160,000 Interest for the year at 5% 8,000 Already Paid Per TB -3,500 Amount due at the year-end 4,500 CURRENT MARKS Page 11

13 Page 12

14 Page 13

15 SOLUTION 2 a) Prepayments are items of expense that relate to future periods but which have already been paid for and are shown in expenses of the current period. They must be excluded from this year s expenses as they relate to a future period. Examples of Prepayments could include Rent Prepaid, Phone Credit Prepaid etc. Accruals are expenses which have not been included in expenses in this period as they have not been paid for in this period but which must be included as they have been incurred in this period as per the accruals concept. Examples of Accruals could include Wages owing at the end of a period, Light & Heat Due etc. (4 Marks) b) Calculation of the Insurance and Rent for the year-ending 31st December 2011 through the form of a ledger account including the closing accrual and prepayment. c) Capital Expenditure is expenditure which results in the acquisition of non-current assets or an improvement in their earning capacity. Revenue Expenditure is expenditure incurred for the purpose of the trade or to maintain non-current assets. (4 Marks) d) i) Capital Expenditure; ii) Capital Expenditure; iii) Revenue Expenditure; iv) Revenue Expenditure; v) Revenue Expenditure. (5 Marks) Page 14 [Total: 20 Marks]

16 SOLUTION 3 REPORT To: Mr. Walter Johnson, Managing Director Translate Limited From: Financial Accountant Re: IAS 21 Changes in Foreign Exchange Rates Date: September 2012 a) i) Per paragraph 20 of IAS 21, a foreign currency transaction is a transaction that is denominated or requires settlement in a foreign currency, including transactions arising when an entity; (a) Buys or sells goods or services whose price is denominated in a foreign currency; (b) Borrows or lends funds when the amounts payable or receivable are denominated in a foreign currency; or (c) Otherwise acquires or disposes of assets, or incurs or settles liabilities, denominated in a foreign currency. (2 Marks) ii) Per paragraph 8 of IAS 21, an exchange difference is the difference resulting from translating a given number of units of one currency into another currency at different exchange rates. (2 Marks) b) i) Per paragraph 21 of IAS 21, on initial a foreign currency transaction shall be recorded by applying to the foreign currency amount the spot exchange rate between the functional currency and foreign currency at the date of the transaction. For practical reasons, a rate that approximates the actual rate at the date of transaction is often used, for example, an average rate for a week or a month might be used for all transactions in each foreign currency occurring during that period. However, if exchange rates fluctuate significantly, the use of the average rate for a period is inappropriate. (3 Marks) ii) Per paragraph 23 of IAS 21, at the end of each reporting period; (a) foreign currency monetary items shall be translated using the closing exchange rate; (b) Non-monetary items that are measured in terms of historical cost in a foreign currency shall be translated using the exchange rate at the date of the transaction; and (c) Non-monetary items that are measured at fair value in a foreign currency shall be translated using the exchange rates at the date when the fair value was determined. (3 Marks) c) The accounting treatment for the transactions for the year-ending 31st December 2010 and 2011 is as follows: Dr. Purchases SOCI 100,000 ($120,000/1.20) Cr. Trade Payables SOFP 100, Dr. Trade Payables SOFP 4,000 Cr. Expense SOCI 4,000 The 4,000 is an exchange difference that arises due to the change in the exchange rates from the to the i.e. $120,000/1.25 = 96,000. The difference between 100,000 and 96,000 is 4, Dr. Trade Payables SOFP 96,000 Dr. Expense SOCI 24,000 Cr. Bank SOFP 120,000 ($120,000/1.00) (10 Marks) I hope that the above responses clarify and answer your queries. If you have any further queries, please do not hesitate to contact me. Yours sincerely, Financial Accountant Page 15 [Total: 20 Marks]

Borrows or lends funds when the amounts payable or receivable are denominated in a foreign currency; or (c) Otherwise acquires or disposes of assets, or incurs")

17 SOLUTION 4 a) The solution for the trade receivable and trade payable control accounts for Mr. Twiddle for January 2012 are as follows: (10 Marks) Dr. Mr. Twiddle Trade Receivables Control Account Cr. Balance B/d 58,145 Balance B/d 12, Sales 138,039 Contras 12, Cash Paid to Customers 12,653 Bad Debt Written Off 13, Discount Allowed 12, Cash Received from Customers 132, Balance C/d 24, , , Balance B/d 24, Dr. Mr. Twiddle Trade Payables Control Account Cr. Balance B/d 13,751 Balance B/d 47, Contras 12,682 Purchases 98, Purchases Returns 14, Discount Received 13, Cash Paid to Trade Payables 82, Balance C/d 9, , , Balance B/d 9, (10.50 Marks to a Total of 10 Marks) TOTAL MARKS b) Possible reasons for reconcilable items for a trade payable control account reconciliation are as follows: i. Invoice omitted from the control account but entered in the trade payables ledger; ii. Supplier balance excluded from the trade payables ledger total because the account had been included in the trade receivables ledger by mistake; iii. Credit sale posted in error to the debit of a trade payables ledger account instead of the debit of an account in the trade receivables ledger; iv. Under-casting error in calculation of total end of period trade payables balances; v. Customer account with a credit balance included in the trade payables ledger that should have been included in the trade receivables ledger; vi. Sales return posted in error to the credit of a trade payables ledger instead of the credit of an account in the trade receivables ledger. (5 Marks) c) Possible explanations for differences between Mr. Twiddle s trade receivable statement and the amount that the customer is saying is owing to Mr. Twiddle are as follows: i) A sale has been omitted from the books of either the seller or the trade receivables ii) A sale has been incorrectly entered in the books of either the seller or the trade receivables; iii) A sale has been made at the end of the month but only entered in the books or either the seller or the trade receivables in the following month; iv) Goods returned had been entered in the books of the seller but not in the books of the trade receivables; v) Goods returned have been incorrectly entered in the books of either the seller of the trade receivables; vi) The trade receivables had entered goods as having been returned in their books when in fact, the goods were not returned by the seller; Page 16

18 vii) A sale has been recorded in the books of the seller in the trade receivables account when it should been entered in the account of another customer; viii) A sale has been recorded in the books of the trade receivables in the sellers account when it should been entered in the account of another seller; ix) A payment made to the supplier and entered in the books of the trade receivables had not been received by the seller; x) Goods had been dispatched by the seller and entered in the books of the seller but had not yet been received by the trade receivables (5 Marks) [Total: 20 Marks] Page 17

[Total: 20")

19 SOLUTION 5 Caherame Limited Statement of Cash flows for the year ended 31st December 2011 Cash flows from Operating Activities '000 '000 Profit before Taxation Adjustments for Depreciation Amortisation Profit on Sale of PPE (110-80) Interest Expense Decrease in Trade Receivables Increase in Inventory Increase in Trade Payables Cash Generated from Operations Interest Paid Income Taxes Paid Net Cash from Operating Activities Cash flows from Investing Activities Payments to Acquire Property, Plant & Equipment Receipts from Sale of Property, Plant & Equipment Payments to Acquire Development Expenditure Net Cash used in Investing Activities Cash flows from Financing Activities Proceeds from Issue of Shares Debentures Redeemed Dividends Paid Net Cash from Financing Activities Net Increase in Cash & Cash Equivalents Cash & Cash Equivalents at beginning of Year Note Cash & Cash Equivalents at end of Year Note Note '000 '000 Cash on hand and balances with bank Bank Overdraft Cash and Cash Equivalents OVERALL MARKS Page 18

20 Cash Flow Workings Calculation of Debenture Interest 400,000 for 9 Months at 8% Interest ,000 for 3 Months at 8% Interest 6 Interest 30 Interest Account Balance b/d - Expense - SOCI 30 Interest Paid 30 Balance c/d Corporation Tax Account Corporation Tax Paid 21 Balance b/d 35 Balance c/d 44 Expense - SOCI Share Capital Account Balance b/d - S. Capital 900 Balance b/d - S. Premium 20 Balance c/d - S. Capital 1,200 Balance c/d - S. Premium 84 Proceeds from Issue of S. Capital 364 1,284 1,284 Property, Plant & Equipment Account Balance b/d 1,496 Depreciation 85 Revaluation Surplus 100 Disposal 80 Purchase of PPE 389 Balance c/d 1,820 1,985 1,985 Development Expenditure Account Balance b/d 237 Amortisation 15 Purchase of Dev. Expend. 38 Balance c/d [Total: 20 Marks] Page 19

21 Marking Scheme Q1 a) 4 x 1 Marks each 4 Discuss 3 of the methods x 2 Marks each 6 b) Workings 18 Statement of Comprehensive Income 6 Statement of Financial Position 5 Presentation of SOCI + SOFP 1 Total Marks Q1 40 Q2 a) Definition of Prepayments 1 Definition of Accruals 1 Example of a Prepayment 1 Example of an Accrual 1 b) Opening Balances of Rent & Insurance 1 7 Payments x 0.25 marks each 2 Rent expense for the year 1 Insurance expense for the year 1 Closing Balances of Rent & Insurance 2 c) Capital Expenditure definition 2 Revenue Expenditure definition 2 d) 5 answers x 1 mark each 5 Total Marks Q2 20 Q3 a) Foreign Currency Transaction definition 2 Exchange Difference 2 b) Initial Recognition At the end of the Reporting Period 3 c) Accounting Treatment for transactions At the At the At the Total Marks Q3 20 Page 20

22 Q4 a) Trade Receivables Control Account Opening Balances 1 Sales 0.5 Contras 0.5 Cash Paid to Customers 0.5 Bad Debt Written Off 0.5 Discount Allowed 0.5 Cash Received from Customers 0.5 Balance carried down 0.5 Totals 0.5 Closing Balances 0.5 Trade Payables Control Account Opening Balances 1 Purchases 0.5 Contras 0.5 Purchase Returns 0.5 Discount Received 0.5 Cash Received to Suppliers 0.5 Balance carried down 0.5 Totals 0.5 Closing Balances Marks to a Total of 10 Marks b) Possible Reasons 4 x 1.25 marks each 5 c) Possible Explanations 5 x 1 mark each 5 Total Marks Q4 20 Q5 Operating Activities 10.5 Investing Activities 4 Financing Activities 3 Cash & Cash Equivalents 2.5 Total Marks Q5 20 Page 21

FINANCIAL ACCOUNTING

FINANCIAL ACCOUNTING FORMATION 2 EXAMINATION - APRIL 2012 NOTES: You are required to answer Question 1. You are also required to answer any three out of Questions 2 to 5. (If you provide answers to all

FINANCIAL ACCOUNTING FORMATION 2 EXAMINATION - APRIL 2012 NOTES: You are required to answer Question 1. You are also required to answer any three out of Questions 2 to 5. (If you provide answers to all

Paper F3. Financial Accounting. Specimen Exam applicable from June 2014. Fundamentals Level Knowledge Module

Fundamentals Level Knowledge Module Financial Accounting Specimen Exam applicable from June 2014 Time allowed: 2 hours This paper is divided into two sections: Section A ALL 35 questions are compulsory

Fundamentals Level Knowledge Module Financial Accounting Specimen Exam applicable from June 2014 Time allowed: 2 hours This paper is divided into two sections: Section A ALL 35 questions are compulsory

Cork Institute of Technology. Autumn 2006 Advanced Financial Accounting (Time: 3 Hours)

") Cork Institute of Technology Bachelor of Business in Accounting Award Bachelor of Business in Management - Award Instructions Answer FOUR questions Answer all THREE questions in Section A and ONE question

Cork Institute of Technology Bachelor of Business in Accounting Award Bachelor of Business in Management - Award Instructions Answer FOUR questions Answer all THREE questions in Section A and ONE question

6. Show all your workings. icpar

CERTIFIED PUBLIC ACCOUNTANT FOUNDATION LEVEL 1 EXAMINATION F1.3: FINANCIAL ACCOUNTING MONDAY: 10 JUNE 2013 INSTRUCTIONS: 1. Time Allowed: 3 hours 15 minutes (15 minutes reading and 3 hours writing). 2.

CERTIFIED PUBLIC ACCOUNTANT FOUNDATION LEVEL 1 EXAMINATION F1.3: FINANCIAL ACCOUNTING MONDAY: 10 JUNE 2013 INSTRUCTIONS: 1. Time Allowed: 3 hours 15 minutes (15 minutes reading and 3 hours writing). 2.

SUGGESTED LAYOUTS FOR FINANCIAL STATEMENTS

Appendix 2 SUGGESTED LAYOUTS FOR FINANCIAL STATEMENTS These layouts are suggestions only and are not prescriptive. Other suitable alternatives which conform to the general principles of FRS 102 will be

Appendix 2 SUGGESTED LAYOUTS FOR FINANCIAL STATEMENTS These layouts are suggestions only and are not prescriptive. Other suitable alternatives which conform to the general principles of FRS 102 will be

INSTITUTE OF FINANCIAL ACCOUNTANTS JUNE 2011 EXAMINATION. D1. Financial Accounting

1 INSTITUTE OF FINANCIAL ACCOUNTANTS JUNE 2011 EXAMINATION D1. Financial Accounting Instructions to candidates 1. Time allowed is 3 hours and 10 minutes, which includes 10 minutes reading time. 2. This

1 INSTITUTE OF FINANCIAL ACCOUNTANTS JUNE 2011 EXAMINATION D1. Financial Accounting Instructions to candidates 1. Time allowed is 3 hours and 10 minutes, which includes 10 minutes reading time. 2. This

(a) (i) Marking Scheme: 1 mark for definition and 1 mark for example.

(i) Marking Scheme: 1 mark for definition and 1 mark for example.") T A S M A N I A N Accounting C E R T I F I C A T E Subject Code ACC5C O F E D U C A T I O N Question 1 T A S M A N I A N Q U A L I F I C A T I O N S A U T H O R I T Y (a) (i) Marking Scheme: 1 mark for

T A S M A N I A N Accounting C E R T I F I C A T E Subject Code ACC5C O F E D U C A T I O N Question 1 T A S M A N I A N Q U A L I F I C A T I O N S A U T H O R I T Y (a) (i) Marking Scheme: 1 mark for

(AA11) FINANCIAL ACCOUNTING BASICS

FINANCIAL ACCOUNTING BASICS") All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA1 EXAMINATION - JANUARY 2016 (AA11) FINANCIAL ACCOUNTING BASICS Instructions to candidates (Please Read Carefully): (1) Time allowed:

All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA1 EXAMINATION - JANUARY 2016 (AA11) FINANCIAL ACCOUNTING BASICS Instructions to candidates (Please Read Carefully): (1) Time allowed:

PREPARING FINAL ACCOUNTS. part

15_1312MH_CH09 27/1/05 8:38 am Page 87 PREPARING part 3 FINAL ACCOUNTS 9 The final accounts of sole traders 10 Accounting principles, concepts and policies 11 Depreciation and fixed assets 12 Bad debts

15_1312MH_CH09 27/1/05 8:38 am Page 87 PREPARING part 3 FINAL ACCOUNTS 9 The final accounts of sole traders 10 Accounting principles, concepts and policies 11 Depreciation and fixed assets 12 Bad debts

INTERNATIONAL ACCOUNTING STANDARDS. CIE Guidance for teachers of. 7110 Principles of Accounts and. 0452 Accounting

www.xtremepapers.com INTERNATIONAL ACCOUNTING STANDARDS CIE Guidance for teachers of 7110 Principles of Accounts and 0452 Accounting 1 CONTENTS Introduction...3 Use of this document... 3 Users of financial

www.xtremepapers.com INTERNATIONAL ACCOUNTING STANDARDS CIE Guidance for teachers of 7110 Principles of Accounts and 0452 Accounting 1 CONTENTS Introduction...3 Use of this document... 3 Users of financial

Assessment Schedule 2013 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176)

") NCEA Level 2 Accounting (91176) 2013 Page 1 of 7 Assessment Schedule 2013 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Evidence Part A Question One

NCEA Level 2 Accounting (91176) 2013 Page 1 of 7 Assessment Schedule 2013 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Evidence Part A Question One

CONTENTS. Kevin O Riordan 2000 ISBN 1841 31 3750. Folens Publishers, Hibernian Industrial Estate, Greenhills Road. Tallaght, Dublin 24.

CONTENTS Chapter 2: Double-Entry Book-keeping and the Trial Balance... 1 Chapter 3: Profit Measurement and Balance Sheet Preparation... 5 Chapter 4: Value Added Tax and Statutory Deductions... 8 Chapter

CONTENTS Chapter 2: Double-Entry Book-keeping and the Trial Balance... 1 Chapter 3: Profit Measurement and Balance Sheet Preparation... 5 Chapter 4: Value Added Tax and Statutory Deductions... 8 Chapter

Chapter. Statement of Cash Flows For Single Company

Chapter 4 Statement of Cash Flows For Single Company 4.1 Single company statement of cash flows Statement of cash flows are primary financial statements and are required along side the income statement

Chapter 4 Statement of Cash Flows For Single Company 4.1 Single company statement of cash flows Statement of cash flows are primary financial statements and are required along side the income statement

B. Division of Costs The purpose of a Manufacturing Account is to ascertain Cost of Production ( ).

.") Manufacturing Accounts ( ) S5 Manufacturing Account/LWL A. Function of a Manufacturing Acccount For those businesses which deal with manufacturing products. It is common in today s business to act both

Manufacturing Accounts ( ) S5 Manufacturing Account/LWL A. Function of a Manufacturing Acccount For those businesses which deal with manufacturing products. It is common in today s business to act both

PART 5. External Reporting and Performance Evaluation. Statements of financial performance and position. Statement of cash flows 19

PART 5 External Reporting and Performance Evaluation Statements of financial performance and position 18 Statement of cash flows 19 Analysis and interpretation of financial statements 20 CHAPTER 18 Statements

PART 5 External Reporting and Performance Evaluation Statements of financial performance and position 18 Statement of cash flows 19 Analysis and interpretation of financial statements 20 CHAPTER 18 Statements

Mustafa Khuwaja - CAT Finalist

1 Run through the Flashcards as often as you can during your final revision period. The day before the exam, try to go through the Flashcards again. You will be well on your way to passing your exams.

1 Run through the Flashcards as often as you can during your final revision period. The day before the exam, try to go through the Flashcards again. You will be well on your way to passing your exams.

Coimisiún na Scrúduithe Stáit State Examinations Commission. Leaving Certificate 2014. Marking Scheme. Accounting. Higher Level

Coimisiún na Scrúduithe Stáit State Examinations Commission Leaving Certificate 2014 Marking Scheme Accounting Higher Level Note to teachers and students on the use of published marking schemes Marking

Coimisiún na Scrúduithe Stáit State Examinations Commission Leaving Certificate 2014 Marking Scheme Accounting Higher Level Note to teachers and students on the use of published marking schemes Marking

Accruals and prepayments

5 Accruals and prepayments this chapter covers... In the last chapter we have looked at the preparation of financial statements or final accounts using the extended trial balance, or spreadsheet, approach.

5 Accruals and prepayments this chapter covers... In the last chapter we have looked at the preparation of financial statements or final accounts using the extended trial balance, or spreadsheet, approach.

SOLE TRADER FINAL ACCOUNTS

6 SOLE TRADER FINAL ACCOUNTS CASE STUDY Starting out in business Olivia Boulton used to work as a buyer of kitchen and cookware goods for a large department store in central London. She was good at her

6 SOLE TRADER FINAL ACCOUNTS CASE STUDY Starting out in business Olivia Boulton used to work as a buyer of kitchen and cookware goods for a large department store in central London. She was good at her

BUSINESS ACCOUNTS. sample documents. sourced from www.osbornebooks.co.uk

BUSINESS ACCOUNTS sample documents sourced from www.osbornebooks.co.uk Sample documents document page invoice 3 statement 4 double-entry accounts 5 cash book 6 petty cash book 7 extended trial balance

BUSINESS ACCOUNTS sample documents sourced from www.osbornebooks.co.uk Sample documents document page invoice 3 statement 4 double-entry accounts 5 cash book 6 petty cash book 7 extended trial balance

Large Company Limited. Report and Accounts. 31 December 2009

Registered number 123456 Large Company Limited Report and Accounts 31 December 2009 Report and accounts Contents Page Company information 1 Directors' report 2 Statement of directors' responsibilities

Registered number 123456 Large Company Limited Report and Accounts 31 December 2009 Report and accounts Contents Page Company information 1 Directors' report 2 Statement of directors' responsibilities

Transition to International Financial Reporting Standards

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates

International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates Objective 1 An entity may carry on foreign activities in two ways. It may have transactions in foreign currencies or

International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates Objective 1 An entity may carry on foreign activities in two ways. It may have transactions in foreign currencies or

TRADING ACCOUNT (Horizontal Format) for the year ended. Particulars. Rs.

for the year ended. Particulars. Rs.") Dr. To Opening Stock To Purchases Less: Returns outwards () To Frieght & Carriage To Customs & Insurance To Wages To Gas, Water & Fuel To Factory Expenses To Royalty on Production To Cargo Expenses To

Dr. To Opening Stock To Purchases Less: Returns outwards () To Frieght & Carriage To Customs & Insurance To Wages To Gas, Water & Fuel To Factory Expenses To Royalty on Production To Cargo Expenses To

Trading Profit and Loss Account

Trading Profit and Loss Account Trading Account The trading account shows the income from sales and the direct costs of making those sales. It includes the balance of stocks at the start and end of the

Trading Profit and Loss Account Trading Account The trading account shows the income from sales and the direct costs of making those sales. It includes the balance of stocks at the start and end of the

5 BUSINESS ACCOUNTING STANDARD CASH FLOW STATEMENT I. GENERAL PROVISIONS II. KEY DEFINITIONS

APPROVED by Resolution No. 1 of 18 December 2003 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania 5 BUSINESS ACCOUNTING STANDARD CASH FLOW STATEMENT

APPROVED by Resolution No. 1 of 18 December 2003 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania 5 BUSINESS ACCOUNTING STANDARD CASH FLOW STATEMENT

Double entry bookkeeping

ACCOUNTS PREPARATION I Double entry bookkeeping Introduction A sound knowledge of double entry underpins many of the learning outcomes and skills required for Accounts Preparation I. A sound understanding

ACCOUNTS PREPARATION I Double entry bookkeeping Introduction A sound knowledge of double entry underpins many of the learning outcomes and skills required for Accounts Preparation I. A sound understanding

Financial Accounting 1 st Year Examination

Financial Accounting 1 st Year Examination May 2012 Paper, Solutions & Examiner s Report NOTES TO USERS ABOUT THESE SOLUTIONS The solutions in this document are published by Accounting Technicians Ireland.

Financial Accounting 1 st Year Examination May 2012 Paper, Solutions & Examiner s Report NOTES TO USERS ABOUT THESE SOLUTIONS The solutions in this document are published by Accounting Technicians Ireland.

UNIVERSITY EXAMINATIONS COURSE TITLE: FINANCIAL ACCOUNTING DATE: 19/08/2010

KABARAK UNIVERSITY UNIVERSITY EXAMINATIONS /2010 ACADEMIC YEAR FOR THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION COURSE CODE: ACCT 510 COURSE TITLE: FINANCIAL ACCOUNTING STREAM: DAY: TIME: MBA THURSDAY

KABARAK UNIVERSITY UNIVERSITY EXAMINATIONS /2010 ACADEMIC YEAR FOR THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION COURSE CODE: ACCT 510 COURSE TITLE: FINANCIAL ACCOUNTING STREAM: DAY: TIME: MBA THURSDAY

Accounting for Branches Including Foreign Branch Accounts

9 Accounting for Branches Including Foreign Branch Accounts BASIC CONCEPTS Types of branches Dependent branches Independent branches Based on accounting point of view, branches may be classified as follows:

9 Accounting for Branches Including Foreign Branch Accounts BASIC CONCEPTS Types of branches Dependent branches Independent branches Based on accounting point of view, branches may be classified as follows:

Suggested layouts for financial statements in Accounting Courses National 5 and Higher

Suggested layouts for financial statements in Accounting Courses National 5 and Higher The following suggested layouts may be used when presenting financial statements in the Accounting Courses for National

Suggested layouts for financial statements in Accounting Courses National 5 and Higher The following suggested layouts may be used when presenting financial statements in the Accounting Courses for National

Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates

21 The Effects of Changes in Foreign Exchange Rates") Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates Contents Paragraph OBJECTIVE 1-2 SCOPE 3-7 DEFINITIONS 8-16 Elaboration on the definitions 9-16 Functional currency

Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates Contents Paragraph OBJECTIVE 1-2 SCOPE 3-7 DEFINITIONS 8-16 Elaboration on the definitions 9-16 Functional currency

Small Company Limited. Report and Accounts. 31 December 2007

Registered number 123456 Small Company Limited Report and Accounts 31 December 2007 Report and accounts Contents Page Company information 1 Directors' report 2 Accountants' report 3 Profit and loss account

Registered number 123456 Small Company Limited Report and Accounts 31 December 2007 Report and accounts Contents Page Company information 1 Directors' report 2 Accountants' report 3 Profit and loss account

Foreign Currency Translation

Statement of Accounting Standards Foreign Currency Translation Prepared by the Accounting Standards Board and the Public Sector Accounting Standards Board of the Australian Accounting Research Foundation

Statement of Accounting Standards Foreign Currency Translation Prepared by the Accounting Standards Board and the Public Sector Accounting Standards Board of the Australian Accounting Research Foundation

Advanced Financial Accounting

Advanced Financial Accounting Sample Paper 2 Questions & Suggested Solutions Page 1 of 27 INSTRUCTIONS TO CANDIDATES PLEASE READ CAREFULLY Candidates must indicate clearly whether they are answering the

Advanced Financial Accounting Sample Paper 2 Questions & Suggested Solutions Page 1 of 27 INSTRUCTIONS TO CANDIDATES PLEASE READ CAREFULLY Candidates must indicate clearly whether they are answering the

CENTRE FOR CONTINUING EDUCATION BBA (AVIATION OPERATION)

") CENTRE FOR CONTINUING EDUCATION BBA (AVIATION OPERATION) BATCH: SEMESTER: NAME: ROLL NO: ASSIGNMENT 1 & 2 FOR BUSINESS ACCOUNTING BBCF 131 UNIVERSITY OF PETROLEUM & ENERGY STUDIES Assignment-1 Note: All

CENTRE FOR CONTINUING EDUCATION BBA (AVIATION OPERATION) BATCH: SEMESTER: NAME: ROLL NO: ASSIGNMENT 1 & 2 FOR BUSINESS ACCOUNTING BBCF 131 UNIVERSITY OF PETROLEUM & ENERGY STUDIES Assignment-1 Note: All

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education

*0018636067* UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education ACCOUNTING 0452/13 Paper 1 October/November 2013 Candidates answer on the Question

*0018636067* UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education ACCOUNTING 0452/13 Paper 1 October/November 2013 Candidates answer on the Question

CHAPTER 25 ACCOUNTING FOR INTRAGROUP TRANSACTIONS

CHAPTER 25 ACCOUNTING FOR INTRAGROUP TRANSACTIONS LEARNING OBJECTIVES Upon completing this chapter readers should be able to: LO1 explain the nature of intragroup transactions; LO2 describe how and why

CHAPTER 25 ACCOUNTING FOR INTRAGROUP TRANSACTIONS LEARNING OBJECTIVES Upon completing this chapter readers should be able to: LO1 explain the nature of intragroup transactions; LO2 describe how and why

Cash budget Predict the movements of cash received and paid for over a period of time. Financial statements

Achievement Standard 90976 Demonstrate understanding of accounting concepts for small entities ACCOUNTING. Externally assessed 3 credits Accounting 90976 (Accounting.) involves the recognition, definition

Achievement Standard 90976 Demonstrate understanding of accounting concepts for small entities ACCOUNTING. Externally assessed 3 credits Accounting 90976 (Accounting.) involves the recognition, definition

16 BUSINESS ACCOUNTING STANDARD CONSOLIDATED FINANCIAL STATEMENTS AND INVESTMENTS IN SUBSIDIARIES I. GENERAL PROVISIONS

APPROVED by Resolution No. 10 of 10 December 2003 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania 16 BUSINESS ACCOUNTING STANDARD CONSOLIDATED

APPROVED by Resolution No. 10 of 10 December 2003 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania 16 BUSINESS ACCOUNTING STANDARD CONSOLIDATED

ACCOUNTING 1 (ACN101- M)

") 1 ACCOUNTING 1 (ACN101- M) STUDY UNIT 1: THE NATURE AND FUNCTION OF ACCOUNTING DEFINITION: Accounting can be defined as the orderly & systematic recording of the monetary values of financial transactions

1 ACCOUNTING 1 (ACN101- M) STUDY UNIT 1: THE NATURE AND FUNCTION OF ACCOUNTING DEFINITION: Accounting can be defined as the orderly & systematic recording of the monetary values of financial transactions

DO NOT OPEN THIS QUESTION PAPER UNTIL YOU ARE TOLD TO DO SO. Financial Pillar. F1 Financial Operations. 21 November 2013 Thursday Morning Session

DO NOT OPEN THIS QUESTION PAPER UNTIL YOU ARE TOLD TO DO SO. Financial Pillar F1 Financial Operations 21 November 2013 Thursday Morning Session Instructions to candidates You are allowed three hours to

DO NOT OPEN THIS QUESTION PAPER UNTIL YOU ARE TOLD TO DO SO. Financial Pillar F1 Financial Operations 21 November 2013 Thursday Morning Session Instructions to candidates You are allowed three hours to

CASH FLOW STATEMENT. MODULE - 6A Analysis of Financial Statements. Cash Flow Statement. Notes

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

Level 3 Accounting Solutions Booklet. For further information contact us: Tel. +44 (0) 8707 202909 Email. [email protected] www.lcci.org.

8707 202909 Email. enquiries@ediplc.com www.lcci.org.") Level 3 Accounting Solutions Booklet For further information contact us: Tel. +44 (0) 8707 202909 Email. [email protected] www.lcci.org.uk London Chamber of Commerce and Industry (LCCI) International

Level 3 Accounting Solutions Booklet For further information contact us: Tel. +44 (0) 8707 202909 Email. [email protected] www.lcci.org.uk London Chamber of Commerce and Industry (LCCI) International

CHAPTER 10 Financial Statements NOTE

NOTE In practice, accruals accounts and prepayments accounts are implied rather than drawn up. It is common for expense accounts to show simply a balance c/d and a balance b/d. The accrual or prepayment

NOTE In practice, accruals accounts and prepayments accounts are implied rather than drawn up. It is common for expense accounts to show simply a balance c/d and a balance b/d. The accrual or prepayment

The Effects of Changes in Foreign Exchange Rates

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 21 The Effects of Changes in Foreign Exchange Rates SB-FRS 21 The Effects of Changes in Foreign Exchange Rates was operative for Statutory Boards financial

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 21 The Effects of Changes in Foreign Exchange Rates SB-FRS 21 The Effects of Changes in Foreign Exchange Rates was operative for Statutory Boards financial

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

CHAPTER 4. Final Accounts

CHAPTER 4 Final Accounts Meaning Preparation of final account is the last stage of the accounting cycle. The basic objective of every concern maintaining the book of accounts is to find out the profit

CHAPTER 4 Final Accounts Meaning Preparation of final account is the last stage of the accounting cycle. The basic objective of every concern maintaining the book of accounts is to find out the profit

IFRS IN PRACTICE. IAS 7 Statement of Cash Flows

IFRS IN PRACTICE IAS 7 Statement of Cash Flows 2 IFRS IN PRACTICE - IAS 7 STATEMENT OF CASH FLOWS TABLE OF CONTENTS 1. Introduction 3 2. Definition of cash and cash equivalents 4 2.1. Demand deposits 4

IFRS IN PRACTICE IAS 7 Statement of Cash Flows 2 IFRS IN PRACTICE - IAS 7 STATEMENT OF CASH FLOWS TABLE OF CONTENTS 1. Introduction 3 2. Definition of cash and cash equivalents 4 2.1. Demand deposits 4

FINANCIAL STATEMENTS-II

MODULE - 3 15 FINANCIAL STATEMENTS-II You have learnt that Income Statement i.e. Trading & Profit and Loss Account and Position Statement i.e., Balance Sheet are two financial statements, which are prepared

MODULE - 3 15 FINANCIAL STATEMENTS-II You have learnt that Income Statement i.e. Trading & Profit and Loss Account and Position Statement i.e., Balance Sheet are two financial statements, which are prepared

C02-Fundamentals of financial accounting

Sample Exam Paper Question 1 The difference between an income statement and an income and expenditure account is that: A. An income and expenditure account is an international term for an Income statement.

Sample Exam Paper Question 1 The difference between an income statement and an income and expenditure account is that: A. An income and expenditure account is an international term for an Income statement.

FINANCIAL STATEMENTS-I

14 FINANCIAL STATEMENTS-I You have learnt the meaning of the financial statements and the need to prepare these for the business organisations. You have also learnt the format of these statements and the

14 FINANCIAL STATEMENTS-I You have learnt the meaning of the financial statements and the need to prepare these for the business organisations. You have also learnt the format of these statements and the

NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

Preparing a Successful Financial Plan

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

STATUTORY BOARD SB-FRS 32 FINANCIAL REPORTING STANDARD. Financial Instruments: Presentation Illustrative Examples

STATUTORY BOARD SB-FRS 32 FINANCIAL REPORTING STANDARD Financial Instruments: Presentation Illustrative Examples CONTENTS Paragraphs ACCOUNTING FOR CONTRACTS ON EQUITY INSTRUMENTS OF AN ENTITY Example

STATUTORY BOARD SB-FRS 32 FINANCIAL REPORTING STANDARD Financial Instruments: Presentation Illustrative Examples CONTENTS Paragraphs ACCOUNTING FOR CONTRACTS ON EQUITY INSTRUMENTS OF AN ENTITY Example

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 32. Financial Instruments: Presentation Illustrative Examples

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 32 Financial Instruments: Presentation Illustrative Examples CONTENTS Paragraphs ACCOUNTING FOR CONTRACTS ON EQUITY INSTRUMENTS OF AN ENTITY Example

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 32 Financial Instruments: Presentation Illustrative Examples CONTENTS Paragraphs ACCOUNTING FOR CONTRACTS ON EQUITY INSTRUMENTS OF AN ENTITY Example

Exam 1 chapters 1-4 Needles 10ed

Exam 1 chapters 1-4 Needles 10ed Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Which of the following is the most appropriate definition of accounting?

Exam 1 chapters 1-4 Needles 10ed Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Which of the following is the most appropriate definition of accounting?

SAMPLE QUESTION PAPER IN ACCOUNTANCY. Time: Three Hours Maximum Marks: 100

SAMPLE QUESTION PAPER IN ACCOUNTANCY Time: Three Hours Maximum Marks: 100 Note: The question paper is divided into two sections A and B. Attempt all questions of Section A and any one question of Section

SAMPLE QUESTION PAPER IN ACCOUNTANCY Time: Three Hours Maximum Marks: 100 Note: The question paper is divided into two sections A and B. Attempt all questions of Section A and any one question of Section

Assessment Schedule 2010 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224)

") NCEA Level 2 Accounting (90224) 2010 page 1 of 7 Assessment Schedule 2010 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224) Evidence Statement ONE Part

NCEA Level 2 Accounting (90224) 2010 page 1 of 7 Assessment Schedule 2010 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224) Evidence Statement ONE Part

EXPLANATORY NOTES. 1. Summary of accounting policies

1. Summary of accounting policies Reporting Entity Taranaki Regional Council is a regional local authority governed by the Local Government Act 2002. The Taranaki Regional Council group (TRC) consists

1. Summary of accounting policies Reporting Entity Taranaki Regional Council is a regional local authority governed by the Local Government Act 2002. The Taranaki Regional Council group (TRC) consists

Summary of Significant Accounting Policies FOR THE FINANCIAL YEAR ENDED 31 MARCH 2014

46 Unless otherwise stated, the following accounting policies have been applied consistently in dealing with items which are considered material in relation to the financial statements. The Company and

46 Unless otherwise stated, the following accounting policies have been applied consistently in dealing with items which are considered material in relation to the financial statements. The Company and

Sri Lanka Accounting Standard-LKAS 7. Statement of Cash Flows

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Accounts of the sole trader

Unit 1 Accounts of the sole trader This unit consists of one section only: Section 1: Final accounts Section 1 Final accounts By the end of this section you should be able to: explain the position of a

Unit 1 Accounts of the sole trader This unit consists of one section only: Section 1: Final accounts Section 1 Final accounts By the end of this section you should be able to: explain the position of a

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

MARK SCHEME for the October/November 2010 question paper for the guidance of teachers 0452 ACCOUNTING. 0452/22 Paper 2, maximum raw mark 120

www.xtremepapers.com UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education MARK SCHEME for the October/November 2010 question paper for the guidance

www.xtremepapers.com UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education MARK SCHEME for the October/November 2010 question paper for the guidance

IPSAS 2 CASH FLOW STATEMENTS

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

Statement of Cash Flows

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

ACCT1115. Review Package - Midterm SOLUTION Fall 2013

ACCT1115 Review Package - Midterm SOLUTION Fall 2013 Part I Multiple Choice 1) How should you record the purchase of an expensive automobile? a) Decrease cash, increase assets b) Decrease cash, increase

ACCT1115 Review Package - Midterm SOLUTION Fall 2013 Part I Multiple Choice 1) How should you record the purchase of an expensive automobile? a) Decrease cash, increase assets b) Decrease cash, increase

International Accounting Standard 7 Statement of cash flows *

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

Statement of Cash Flows

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 7 Statement of Cash Flows This version of SB-FRS 7 does not include amendments that are effective for annual periods beginning after 1 January 2014.

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 7 Statement of Cash Flows This version of SB-FRS 7 does not include amendments that are effective for annual periods beginning after 1 January 2014.

AUDIT PLAN: RECEIVABLES

Audit procedures for receivables AUDIT PLAN: RECEIVABLES Completeness Agree the balance from the individual sales ledger accounts to the aged receivables listing and vice versa. Match the total of the

Audit procedures for receivables AUDIT PLAN: RECEIVABLES Completeness Agree the balance from the individual sales ledger accounts to the aged receivables listing and vice versa. Match the total of the

Detailed competency map: Knowledge requirements. (AAT examination)

") Detailed competency map: Knowledge requirements (AAT examination) Fields of competency The items listed are shown with an indicator of the minimum acceptable level of competency, based on a three-point

Detailed competency map: Knowledge requirements (AAT examination) Fields of competency The items listed are shown with an indicator of the minimum acceptable level of competency, based on a three-point

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

The Effects of Changes in Foreign Exchange Rates

Compiled Accounting Standard AASB 121 The Effects of Changes in Foreign Exchange Rates This compiled Standard applies to annual reporting periods ending on or after 28 February 2007. Early application

Compiled Accounting Standard AASB 121 The Effects of Changes in Foreign Exchange Rates This compiled Standard applies to annual reporting periods ending on or after 28 February 2007. Early application

PRINCIPLES FOR PRODUCING AND SUBMITTING REPORTS

December 2014 PRINCIPLES FOR PRODUCING AND SUBMITTING REPORTS (1) The balance sheet and income statement are in euros, rounded up to integers. Amounts recorded in foreign currencies must be converted into

December 2014 PRINCIPLES FOR PRODUCING AND SUBMITTING REPORTS (1) The balance sheet and income statement are in euros, rounded up to integers. Amounts recorded in foreign currencies must be converted into

IFRS Foundation: Training Material for the IFRS for SMEs. Module 30 Foreign Currency Translation

2009 IFRS Foundation: Training Material for the IFRS for SMEs Module 30 Foreign Currency Translation IFRS Foundation: Training Material for the IFRS for SMEs including the full text of Section 30 Foreign

2009 IFRS Foundation: Training Material for the IFRS for SMEs Module 30 Foreign Currency Translation IFRS Foundation: Training Material for the IFRS for SMEs including the full text of Section 30 Foreign

Cambridge International Examinations Cambridge International General Certificate of Secondary Education

Cambridge International Examinations Cambridge International General Certificate of Secondary Education *0123456789* ACCOUNTING 0452/01 Paper 1 For Examination from 2014 SPECIMEN PAPER 1 hour 45 minutes

Cambridge International Examinations Cambridge International General Certificate of Secondary Education *0123456789* ACCOUNTING 0452/01 Paper 1 For Examination from 2014 SPECIMEN PAPER 1 hour 45 minutes

Paper 2 Accounting (Syllabus 2008)

") Section A- FINANCIAL ACCOUNTING 1. Which of the following is not a Fixed Asset? (a) Building (b) Bank balance (c) Plant (d) Goodwill [Hints: (b) Fixed asset is an asset held with the intention of being

Section A- FINANCIAL ACCOUNTING 1. Which of the following is not a Fixed Asset? (a) Building (b) Bank balance (c) Plant (d) Goodwill [Hints: (b) Fixed asset is an asset held with the intention of being

The Effects of Changes in Foreign Exchange Rates

Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority.

Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority.

IPSAS 4 THE EFFECTS OF CHANGES IN FOREIGN EXCHANGE RATES ACKNOWLEDGMENT

THE EFFECTS OF CHANGES IN FOREIGN EXCHANGE RATES ACKNOWLEDGMENT This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 21 (revised

THE EFFECTS OF CHANGES IN FOREIGN EXCHANGE RATES ACKNOWLEDGMENT This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 21 (revised

18 BUSINESS ACCOUNTING STANDARD FINANCIAL ASSETS AND FINANCIAL LIABILITIES I. GENERAL PROVISIONS

APPROVED by Resolution No. 11 of 27 October 2004 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania 18 BUSINESS ACCOUNTING STANDARD FINANCIAL ASSETS

APPROVED by Resolution No. 11 of 27 October 2004 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania 18 BUSINESS ACCOUNTING STANDARD FINANCIAL ASSETS

(These incorporate the June 2011 amendments to IAS 1 and are effective for annual periods commencing on, or after, 1 July 2012).

.") This booklet contains pro-forma: a) Statement of Comprehensive Income By Nature (page 1), Statement of Comprehensive Income By Function (page 2), and Statement of Financial Position (page 3). AND (IAS

This booklet contains pro-forma: a) Statement of Comprehensive Income By Nature (page 1), Statement of Comprehensive Income By Function (page 2), and Statement of Financial Position (page 3). AND (IAS

AAT LEVEL 2 LESSON 2. Association of Accounting Technicians (AAT) Example Course Materials

Example Course Materials") LESSON 2 Double Entry Processing On completing this lesson you should be able to: Identify and explain the accounting concepts which underpin the double entry system of processing business transactions

LESSON 2 Double Entry Processing On completing this lesson you should be able to: Identify and explain the accounting concepts which underpin the double entry system of processing business transactions

Teacher Resource Bank

Teacher Resource Bank GCE Accounting Other Guidance: ACCN2 Update on IAS ACCN3 Updates on IAS (July 2012). The Assessment and Qualifications Alliance (AQA) is a company limited by guarantee registered

Teacher Resource Bank GCE Accounting Other Guidance: ACCN2 Update on IAS ACCN3 Updates on IAS (July 2012). The Assessment and Qualifications Alliance (AQA) is a company limited by guarantee registered

how to prepare a cash flow statement

business builder 4 how to prepare a cash flow statement zions business resource center zions business resource center 2 how to prepare a cash flow statement A cash flow statement is important to your business

business builder 4 how to prepare a cash flow statement zions business resource center zions business resource center 2 how to prepare a cash flow statement A cash flow statement is important to your business

Residual carrying amounts and expected useful lives are reviewed at each reporting date and adjusted if necessary.

87 Accounting Policies Intangible assets a) Goodwill Goodwill represents the excess of the cost of an acquisition over the fair value of identifiable net assets and liabilities of the acquired company

87 Accounting Policies Intangible assets a) Goodwill Goodwill represents the excess of the cost of an acquisition over the fair value of identifiable net assets and liabilities of the acquired company

Accumulated depreciation is eliminated against the gross carrying value of the asset and the net amount restated to the revalued amount of the asset.

IAS 16 Property, Plant & Equipment Revaluations. By: Conor Foley, B. Comm., MAcc., ACA, Dip IFR. Lecturer in Accounting Limerick Institute of Technology. Examiner: Formation 2 Financial Accounting. This

IAS 16 Property, Plant & Equipment Revaluations. By: Conor Foley, B. Comm., MAcc., ACA, Dip IFR. Lecturer in Accounting Limerick Institute of Technology. Examiner: Formation 2 Financial Accounting. This

Level 3 Accounting, 2010

9 0 5 0 3 R 3 Level 3 Accounting, 2010 90503 Prepare financial statements for partnerships and companies Credits: Six 9.30 am Thursday 25 November 2010 RESOURCE BOOKLET Refer to this booklet to answer

9 0 5 0 3 R 3 Level 3 Accounting, 2010 90503 Prepare financial statements for partnerships and companies Credits: Six 9.30 am Thursday 25 November 2010 RESOURCE BOOKLET Refer to this booklet to answer

MARK SCHEME for the May/June 2011 question paper for the guidance of teachers 0452 ACCOUNTING. 0452/21 Paper 2, maximum raw mark 120

www.xtremepapers.com UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education MARK SCHEME for the May/June question paper for the guidance of teachers

www.xtremepapers.com UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education MARK SCHEME for the May/June question paper for the guidance of teachers

Financial Accounting (F3/FFA) February 2014 to August 2015

February 2014 to August 2015") Financial Accounting (F3/FFA) February 2014 to August 2015 This syllabus and study guide are designed to help with teaching and learning and is intended to provide detailed information on what could be

Financial Accounting (F3/FFA) February 2014 to August 2015 This syllabus and study guide are designed to help with teaching and learning and is intended to provide detailed information on what could be

Process Accounts Payable and Receivable

Process Accounts Payable and Receivable UNIT PURPOSE On successful completion of this unit the learner will be able to maintain financial records of a business using both manual accounting processes and

Process Accounts Payable and Receivable UNIT PURPOSE On successful completion of this unit the learner will be able to maintain financial records of a business using both manual accounting processes and

Accounting and Reporting Policy FRS 102. Staff Education Note 1 Cash flow statements

Staff Education Note 1: Cash flow Statements Accounting and Reporting Policy FRS 102 Staff Education Note 1 Cash flow statements Disclaimer This Education Note has been prepared by FRC staff for the convenience

Staff Education Note 1: Cash flow Statements Accounting and Reporting Policy FRS 102 Staff Education Note 1 Cash flow statements Disclaimer This Education Note has been prepared by FRC staff for the convenience

Abbey plc ( Abbey or the Company ) Interim Statement for the six months ended 31 October 2007

Interim Statement for the six months ended 31 October 2007") Abbey plc ( Abbey or the Company ) Interim Statement for the six months ended 31 October 2007 The Board of Abbey plc reports a profit before taxation of 18.20m which compares with a profit of 22.57m for

Abbey plc ( Abbey or the Company ) Interim Statement for the six months ended 31 October 2007 The Board of Abbey plc reports a profit before taxation of 18.20m which compares with a profit of 22.57m for

SHIRE OF CARNARVON POLICY

SHIRE OF CARNARVON POLICY POLICY NO C010 POLICY SIGNIFICANT ACCOUNTING POLICIES RESPONSIBLE DIRECTORATE CORPORATE COUNCIL ADOPTION Date: 27.5.14 Resolution No. FC 5/5/14 REVIEWED/MODIFIED Date: Resolution

SHIRE OF CARNARVON POLICY POLICY NO C010 POLICY SIGNIFICANT ACCOUNTING POLICIES RESPONSIBLE DIRECTORATE CORPORATE COUNCIL ADOPTION Date: 27.5.14 Resolution No. FC 5/5/14 REVIEWED/MODIFIED Date: Resolution

MARK SCHEME for the October/November 2014 series 0452 ACCOUNTING. 0452/23 Paper 2, maximum raw mark 120

CAMBRIDGE INTERNATIONAL EXAMINATIONS Cambridge International General Certificate of Secondary Education MARK SCHEME for the October/November series 0452 ACCOUNTING 0452/23 Paper 2, maximum raw mark 120

CAMBRIDGE INTERNATIONAL EXAMINATIONS Cambridge International General Certificate of Secondary Education MARK SCHEME for the October/November series 0452 ACCOUNTING 0452/23 Paper 2, maximum raw mark 120

PAPER F1 FINANCIAL OPERATIONS

PAPER F1 FINANCIAL OPERATIONS CONSOLIDATED ACCOUNTS PART TWO By Jo Amos, F1 tutor and marker In the previous article we looked at the general principle of consolidated accounts, in particular the consolidated

PAPER F1 FINANCIAL OPERATIONS CONSOLIDATED ACCOUNTS PART TWO By Jo Amos, F1 tutor and marker In the previous article we looked at the general principle of consolidated accounts, in particular the consolidated

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS 0452 ACCOUNTING. 0452/01 Paper 1 (Multiple Choice), maximum mark 40

, maximum mark 40") www.xtremepapers.com UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education MARK SCHEME for the June 2004 question papers 0452 ACCOUNTING 0452/01 Paper

www.xtremepapers.com UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education MARK SCHEME for the June 2004 question papers 0452 ACCOUNTING 0452/01 Paper

The Examiner's Answers F1 - Financial Operations May 2013

The Examiner's Answers F1 - Financial Operations May 2013 Some of the answers that follow are fuller and more comprehensive than would be expected from a wellprepared candidate. They have been written

The Examiner's Answers F1 - Financial Operations May 2013 Some of the answers that follow are fuller and more comprehensive than would be expected from a wellprepared candidate. They have been written

RANBAXY EGYPT COMPANY (L.L.C.) FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2015 TOGETHER WITH AUDITOR S REPORT

FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2015 TOGETHER WITH AUDITOR S REPORT") FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2015 TOGETHER WITH AUDITOR S REPORT Translation of Auditor s report AUDITOR S REPORT TO THE SHAREHOLDERS OF Report on the Financial Statements We have audited

FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2015 TOGETHER WITH AUDITOR S REPORT Translation of Auditor s report AUDITOR S REPORT TO THE SHAREHOLDERS OF Report on the Financial Statements We have audited