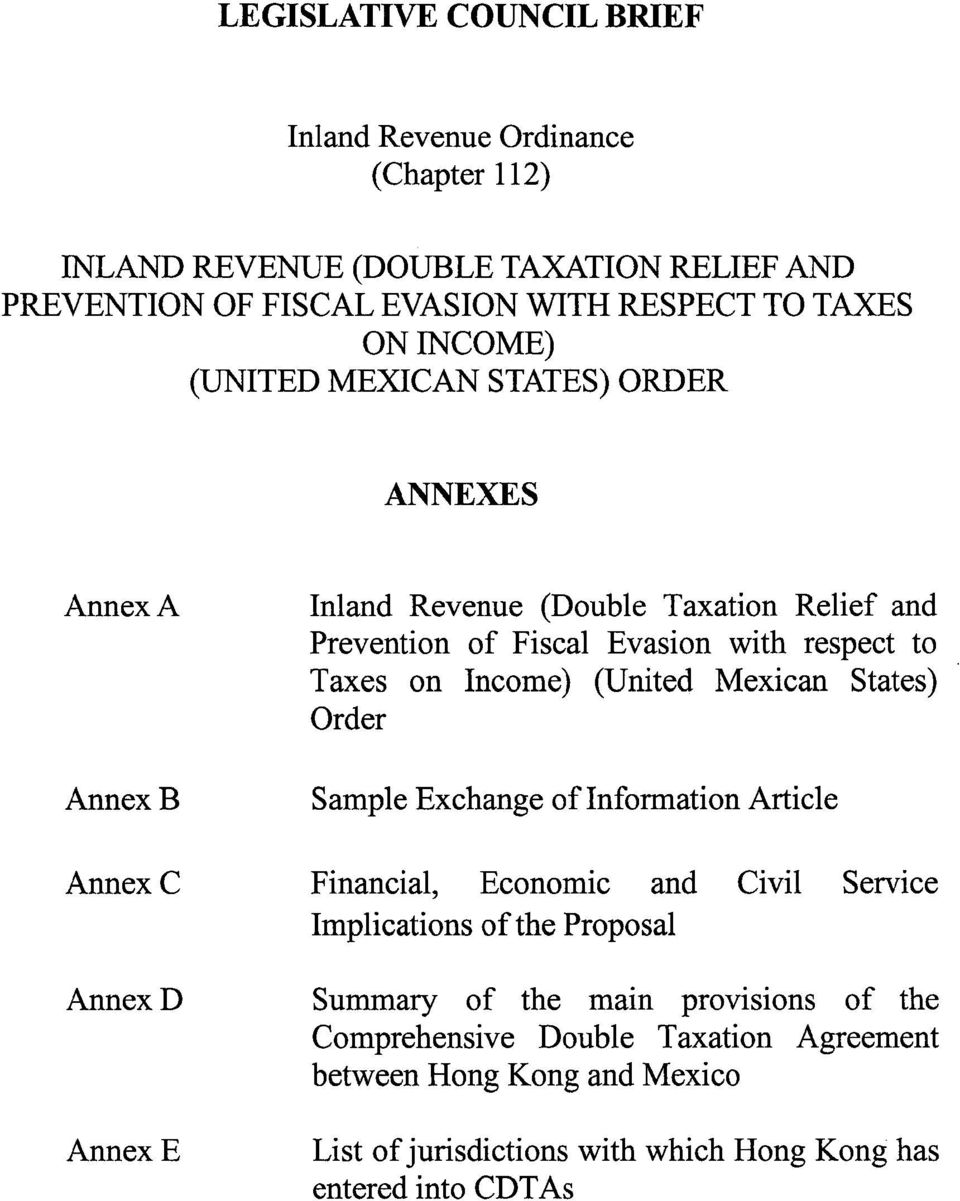

LEGISLATIVE COUNCIL BRIEF. Inland Revenue Ordinance (Chapter 112)

|

|

|

- Noah Wade

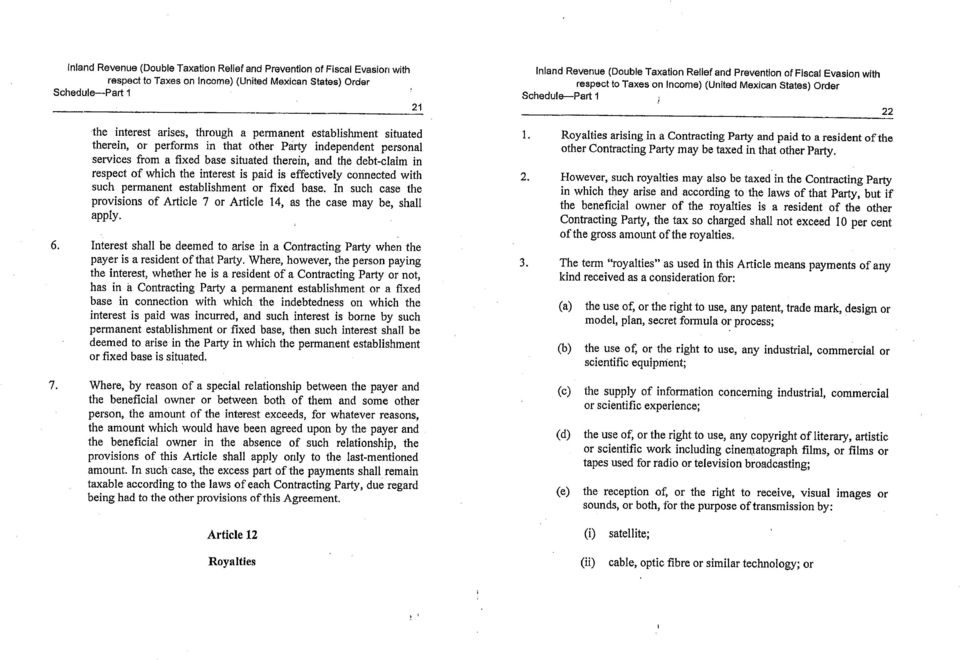

- 10 years ago

- Views:

Transcription

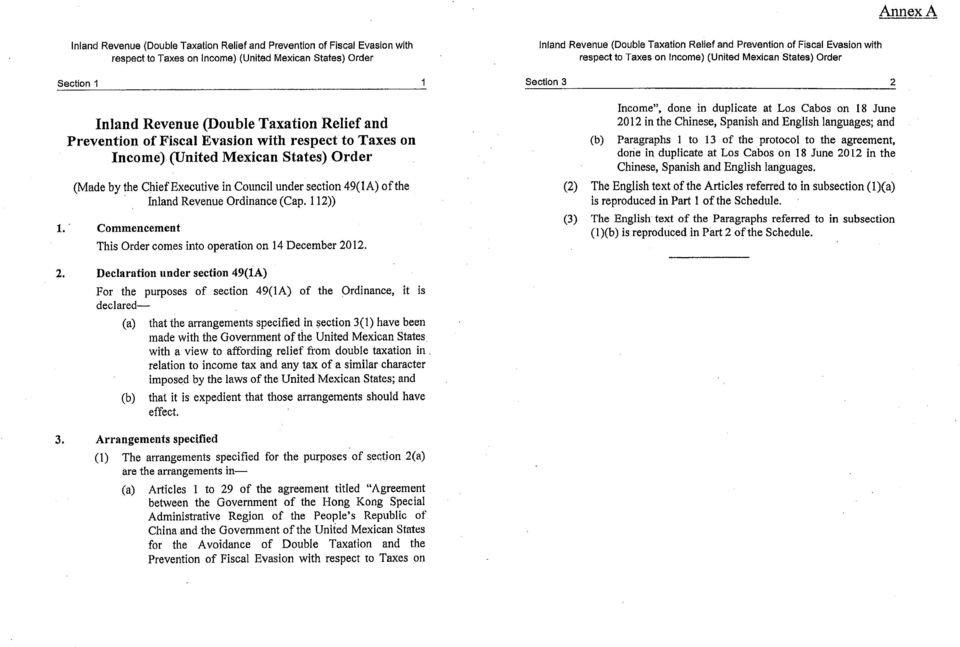

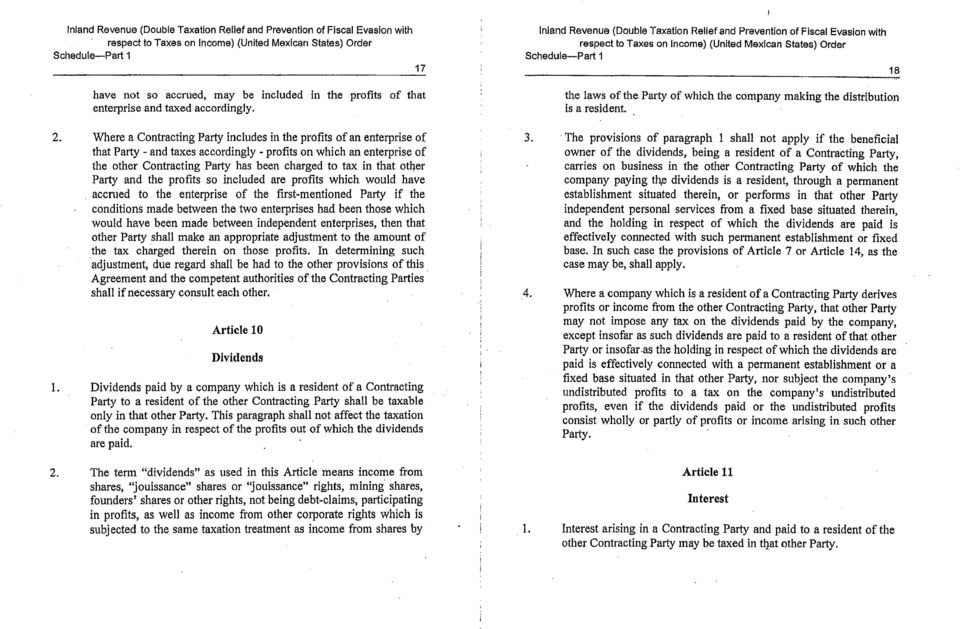

1 File Ref: TsyB R 183/ /38/0 (C) LEGISLATIVE COUNCIL BRIEF Inland Revenue Ordinance (Chapter 112) INLAND REVENUE (DOUBLE TAXATION RELIEF AND PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME) (UNITED MEXICAN STATES) ORDER INTRODUCTION A At the meeting of the Executive Council on 9 October 2012, the Council ADVISED and the Chief Executive ORDERED that the Inland Revenue (Double Taxation Relief and Prevention of Fiscal Evasion with respect to Taxes on Income) (United Mexican States) Order (the Order), at Annex A, should be made under section 49(1A) of the Inland Revenue Ordinance, Cap. 112 (the Ordinance). The Order implements the Agreement between the Hong Kong Special Administrative Region (HKSAR) and Mexico for the Avoidance of Double Taxation with respect to Taxes on Income signed on 18 June 2012 (the Mexican Agreement). JUSTIFICATIONS Benefits of Comprehensive Agreements for Avoidance of Double Taxation 2. Double taxation refers to the imposition of comparable taxes in more than one tax jurisdiction in respect of the same source of income. The international community generally recognises that double taxation hinders the exchange of goods and services, movements of capital, technology and human resources, and poses an obstacle to the development of economic relations between economies. As a business facilitation initiative, it is our policy to enter into Comprehensive Agreements for Avoidance of Double

.")

2 Taxation (CDTAs) with our trading and investment partners so as to minimise double taxation. 3. Hong Kong adopts the territorial concept of taxation whereby only income sourced from Hong Kong is subject to tax. A local resident s income derived from sources outside Hong Kong would not be taxed in Hong Kong and hence would not be subject to double taxation. Double taxation may occur where a foreign jurisdiction taxes its own residents income derived from Hong Kong. Although many jurisdictions do provide their residents with unilateral tax relief for the Hong Kong tax they paid on income derived therefrom, the existence of a CDTA will provide enhanced certainty and stability in respect of the elimination of double taxation. Besides, the tax relief provided under a CDTA may exceed the level provided unilaterally by a tax jurisdiction. Benefits of the Mexican Agreement 4. In the absence of a CDTA, income earned by Mexican residents in Hong Kong is subject to both Hong Kong and Mexican income tax. Under the Mexican Agreement, tax paid in Hong Kong will be allowed as credit against tax payable in Mexico. 5. In the absence of a CDTA, Hong Kong residents receiving interest from Mexico are subject to Mexico s withholding tax, which is in general 30% at present. Under the Mexican Agreement, such withholding tax will be capped at 10%. The interest withholding tax rate will be further reduced to 4.9% if the beneficial owner is a bank. The Mexican withholding tax on royalties, currently at 25% in general, will be capped at 10% under the Mexican Agreement. 6. Upon its coming into effect, the Mexican Agreement will supersede the existing provisions in the air services agreement with Mexico on limited double taxation avoidance and provide the same level of benefits as those provisions in respect of taxes on air income, i.e. Hong Kong airlines operating flights to Mexico will be taxed at Hong Kong s corporation tax rate of 16.5% (which is lower than that of Mexico at 30%) and will not be taxed in Mexico. Profits from international shipping transport earned by Hong Kong residents that arise in Mexico, which are currently subject to tax there, will not be taxed in Mexico under the Mexican Agreement. 7. In the absence of a CDTA, the profits of Hong Kong companies doing business through a permanent establishment in Mexico may be taxed in both places if the income is Hong Kong sourced. Under the Mexican Agreement, double taxation will be avoided in that any Mexican tax paid by Page 2

3 the companies will be allowed as a credit against the tax payable in Hong Kong in respect of the income, subject to the provisions of the tax laws of Hong Kong. 8. Under the Mexican Agreement, the income derived by a Hong Kong resident, which is not paid by (or on behalf of) and borne by a Mexican entity, from employment exercised in Mexico will be exempted from Mexican income tax if his or her aggregate stay in Mexico in any relevant 12-month period does not exceed 183 days. 9. Overall speaking, the Mexican Agreement sets out clearly the allocation of taxing rights between the two jurisdictions and the relief on tax rates on different types of income. It will help investors of the two economies to better assess their potential tax liabilities from cross-border economic activities, foster closer economic and trade links between the two places, and provide added incentives for enterprises of Mexico to do business with or invest in Hong Kong, and vice versa. B Exchange of Information Article under the Mexican Agreement 10. The Inland Revenue (Amendment) Ordinance 2010, which enables Hong Kong to adopt the Organisation for Economic Co-operation and Development (OECD) 2004 version of the Exchange of Information (EoI) Article in our CDTAs, came into operation in March During the scrutiny of the relevant Amendment Bill, the Government presented a sample EoI Article (Annex B) to the Bills Committee and undertook to highlight any deviation from the text in any CDTA that we have signed when we submit the CDTA for vetting. 11. The Mexican Agreement, which contains an EoI Article (the Article) based on the OECD 2004 version, has adopted all the safeguards in the sample EoI Article, in particular - (a) the Article only obliges the Contracting Parties to exchange information upon receipt of specific request. It does not require the Contracting Parties to exchange information on an automatic or spontaneous basis; (b) the scope of information exchange is confined to taxes covered by the Mexican Agreement; (c) the information sought should be foreseeably relevant, i.e. there will be no fishing expedition; (d) confidentiality requirements and restrictions on the usage of the information exchanged are as set out in the sample EoI Article; Page 3

4 Legal Basis (e) information will only be disclosed to the tax authorities and not for release to their oversight body; (f) the information requested shall not be disclosed to a third jurisdiction; and (g) there is no obligation to supply information under certain circumstances as set out in the sample EoI Article. 12. Under section 49(1A) of the Ordinance, the Chief Executive in Council may, by order, declare that arrangements have been made with the government of any territory outside Hong Kong with a view to affording relief from double taxation in relation to income tax and any tax of a similar character imposed by the laws of that territory. Following the signing of the Mexican Agreement, it is necessary for the Chief Executive in Council to declare by order that arrangements with the United Mexican States on double taxation relief have been made so as to bring the Mexican Agreement into effect. OTHER OPTIONS 13. An Order made by the Chief Executive in Council under section 49(1A) of the Ordinance is the only way to give effect to the Mexican Agreement. There is no other option. THE ORDER 14. Section 2 of the Order declares that the arrangements specified in section 3 for double taxation relief in relation to income tax and any tax of a similar character imposed by the laws of the United Mexican States have been made and that those arrangements should take effect. Section 3 states that the arrangements are those in Articles 1 to 29 of the Mexican Agreement as well as Paragraphs 1 to 13 of the Protocol to the Mexican Agreement, the text of which Articles and Paragraphs is set out in the Schedule to the Order. LEGISLATIVE TIMETABLE 15. The legislative timetable is as follows Publication in the Gazette 19 October 2012 Tabling at Legislative Council 24 October 2012 Commencement of the Order 14 December 2012 Page 4

5 C IMPLICATIONS OF THE PROPOSAL 16. The proposal has financial, economic and civil service implications as set out in Annex C. The proposal is in conformity with the Basic Law, including the provisions concerning human rights. The proposal will not affect the binding effect of the existing provisions of the Ordinance and its subsidiary legislation. It has no productivity, environmental or sustainability implications. PUBLIC CONSULTATION 17. The business and professional sectors have all along supported our policy to conclude more CDTAs with our trading and investment partners. PUBLICITY 18. We issued a press release on 19 June 2012 on the signing of the Mexican Agreement. A spokesman will be available to answer media and public enquiries. D E BACKGROUND 19. The Mexican Agreement is the twenty-fifth CDTA concluded by Hong Kong with another jurisdiction. A summary of the main provisions of the Agreement is at Annex D. 20. As at end September 2012, we have entered into CDTAs with 25 jurisdictions. A list of these jurisdictions is at Annex E. ENQUIRY 21. In case of enquiries about this Brief, please contact Ms Shirley Kwan, Principal Assistant Secretary for Financial Services and the Treasury (Treasury), at Financial Services and the Treasury Bureau 17 October 2012 Page 5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

Hong Kong s Double Tax Treaty Network

TAX FLASH July 2010 TAX FLASH July 2010 Hong Kong s Double Tax Treaty Network To remain as an international financial and commercial centre, it has become important for Hong Kong to promote its transparency

TAX FLASH July 2010 TAX FLASH July 2010 Hong Kong s Double Tax Treaty Network To remain as an international financial and commercial centre, it has become important for Hong Kong to promote its transparency

LEGISLATIVE COUNCIL BRIEF. Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Chapter 615)

Ordinance (Chapter 615)") File Ref: G13/21C LEGISLATIVE COUNCIL BRIEF Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Chapter 615) Anti-Money Laundering and Counter-Terrorist Financing

File Ref: G13/21C LEGISLATIVE COUNCIL BRIEF Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Chapter 615) Anti-Money Laundering and Counter-Terrorist Financing

Inland Revenue (Double Taxation Relief and Prevention of Fiscal Evasion with respect to Taxes on Income) (Socialist Republic of Vietnam) (Amendment)

(Socialist Republic of Vietnam) (Amendment)") Section1 B2773 L.N. 120 of 2014 Inland Revenue (Double Taxation Relief and Prevention of Fiscal Evasion with respect to Taxes on Income) (Socialist Republic of Vietnam) (Amendment) Order 2014 (Made by

Section1 B2773 L.N. 120 of 2014 Inland Revenue (Double Taxation Relief and Prevention of Fiscal Evasion with respect to Taxes on Income) (Socialist Republic of Vietnam) (Amendment) Order 2014 (Made by

立 法 會. Legislative Council. Bills Committee on Inland Revenue (Amendment) (No.3) Bill 2013. Background brief

(No.3) Bill 2013. Background brief") 立 法 會 Legislative Council LC Paper No. CB(1)790/13-14(02) Ref : CB1/BC/3/13 Bills Committee on Inland Revenue (Amendment) (No.3) Bill 2013 Background brief Purpose 1. This paper provides background information

立 法 會 Legislative Council LC Paper No. CB(1)790/13-14(02) Ref : CB1/BC/3/13 Bills Committee on Inland Revenue (Amendment) (No.3) Bill 2013 Background brief Purpose 1. This paper provides background information

Arrangement between the Mainland of China and the HKSAR for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion

Arrangement between the Mainland of China and the HKSAR for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion INCOME FROM PERSONAL SERVICES Inland Revenue Department Hong Kong Special

Arrangement between the Mainland of China and the HKSAR for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion INCOME FROM PERSONAL SERVICES Inland Revenue Department Hong Kong Special

Declaration of Change of Titles (Communications and Technology Branch and Secretaries of Communications and Technology Branch) Notice 2015

Notice 2015") Declaration of Change of Titles Technology Branch and Section 1 B4949 Declaration of Change of Titles Technology Branch and Secretaries of Communications and Technology Branch) Notice 2015 (Made by the

Declaration of Change of Titles Technology Branch and Section 1 B4949 Declaration of Change of Titles Technology Branch and Secretaries of Communications and Technology Branch) Notice 2015 (Made by the

1. Changes in PRC withholding income tax provisioning policy in relation to CSI RMB Income Fund and CSI RMB Short Maturity Bond Fund

和 CSI Alpha Fund Series (the Trust ) - CSI China-Hong Kong Leaders Fund - CSI RMB Income Fund - CSI RMB Short Maturity Bond Fund (each a "Fund", collectively the Funds ) CITIC Securities International

和 CSI Alpha Fund Series (the Trust ) - CSI China-Hong Kong Leaders Fund - CSI RMB Income Fund - CSI RMB Short Maturity Bond Fund (each a "Fund", collectively the Funds ) CITIC Securities International

News Flash Hong Kong Tax. November 2015 Issue 10. In brief. In detail. www.pwchk.com

News Flash Hong Kong Tax Understanding the IRD s views on emerging corporate tax issues, in particular the practice on processing Hong Kong tax resident certificate applications November 2015 Issue 10

News Flash Hong Kong Tax Understanding the IRD s views on emerging corporate tax issues, in particular the practice on processing Hong Kong tax resident certificate applications November 2015 Issue 10

Macau SAR Tax Profile

Macau SAR Tax Profile Produced in conjunction with the KPMG Asia Pacific Tax Centre Updated: June 2015 Contents 1 Corporate Income Tax 1 2 Income Tax Treaties for the Avoidance of Double Taxation 5 3 Indirect

Macau SAR Tax Profile Produced in conjunction with the KPMG Asia Pacific Tax Centre Updated: June 2015 Contents 1 Corporate Income Tax 1 2 Income Tax Treaties for the Avoidance of Double Taxation 5 3 Indirect

CLEARING AND SETTLEMENT SYSTEMS BILL

C1881 CLEARING AND SETTLEMENT SYSTEMS BILL CONTENTS Clause Page PART 1 PRELIMINARY 1. Short title and commencement... C1887 2. Interpretation... C1887 PART 2 DESIGNATION AND OVERSIGHT Division 1 Designation

C1881 CLEARING AND SETTLEMENT SYSTEMS BILL CONTENTS Clause Page PART 1 PRELIMINARY 1. Short title and commencement... C1887 2. Interpretation... C1887 PART 2 DESIGNATION AND OVERSIGHT Division 1 Designation

COUNTRY PROFILE HONG KONG

COUNTRY PROFILE HONG KONG 1. Economy and foreign investments 2. Tax Rates 3. Tax Treaties 4. Tax Credits 5. Property Tax 6. Excise Tax 7. Stamp Duty 8. Capital Duty 9. Estate Duty 10. Other duties, fees

COUNTRY PROFILE HONG KONG 1. Economy and foreign investments 2. Tax Rates 3. Tax Treaties 4. Tax Credits 5. Property Tax 6. Excise Tax 7. Stamp Duty 8. Capital Duty 9. Estate Duty 10. Other duties, fees

US Foreign Account Tax Compliance Act Intergovernmental Agreement. Frequently Asked Questions

US Foreign Account Tax Compliance Act Intergovernmental Agreement Frequently Asked Questions This document aims to provide background information regarding the intergovernmental agreement ( IGA ) to be

US Foreign Account Tax Compliance Act Intergovernmental Agreement Frequently Asked Questions This document aims to provide background information regarding the intergovernmental agreement ( IGA ) to be

A GUIDE TO THE OCCUPATIONAL RETIREMENT SCHEMES ORDINANCE

A GUIDE TO THE OCCUPATIONAL RETIREMENT SCHEMES ORDINANCE Issued by THE REGISTRAR OF OCCUPATIONAL RETIREMENT SCHEMES Level 16, International Commerce Centre, 1 Austin Road West, Kowloon, Hong Kong. ORS/C/5

A GUIDE TO THE OCCUPATIONAL RETIREMENT SCHEMES ORDINANCE Issued by THE REGISTRAR OF OCCUPATIONAL RETIREMENT SCHEMES Level 16, International Commerce Centre, 1 Austin Road West, Kowloon, Hong Kong. ORS/C/5

LEGISLATIVE COUNCIL BRIEF. Insurance Companies Ordinance (Chapter 41) INSURANCE COMPANIES (AMENDMENT) ORDINANCE 2015 (COMMENCEMENT) NOTICE 2015

INSURANCE COMPANIES (AMENDMENT) ORDINANCE 2015 (COMMENCEMENT) NOTICE 2015") File Ref.: INS/2/3C(2015) LEGISLATIVE COUNCIL BRIEF Insurance Companies Ordinance (Chapter 41) INSURANCE COMPANIES (AMENDMENT) ORDINANCE 2015 (COMMENCEMENT) NOTICE 2015 INTRODUCTION The Secretary for Financial

File Ref.: INS/2/3C(2015) LEGISLATIVE COUNCIL BRIEF Insurance Companies Ordinance (Chapter 41) INSURANCE COMPANIES (AMENDMENT) ORDINANCE 2015 (COMMENCEMENT) NOTICE 2015 INTRODUCTION The Secretary for Financial

LEGISLATIVE COUNCIL BRIEF. Clearing and Settlement Systems (Amendment) Bill 2015

Bill 2015") File Ref: B&M/2/1/20C LEGISLATIVE COUNCIL BRIEF Clearing and Settlement Systems Ordinance (Chapter 584) Clearing and Settlement Systems (Amendment) Bill 2015 INTRODUCTION At the meeting of the Executive

File Ref: B&M/2/1/20C LEGISLATIVE COUNCIL BRIEF Clearing and Settlement Systems Ordinance (Chapter 584) Clearing and Settlement Systems (Amendment) Bill 2015 INTRODUCTION At the meeting of the Executive

DTA HONG KONG - SWITZERLAND: INPUTS AND COMMENTS BY EIGER LAW

DTA HONG KONG - SWITZERLAND: INPUTS AND COMMENTS BY EIGER LAW Kristian OLENIK Nathan KAISER August 2012 www.eigerlaw.com Page - 2 INPUTS AND COMMENTS 1 CONTENTS: DTA Hong Kong Switzerland: Inputs and Comments

DTA HONG KONG - SWITZERLAND: INPUTS AND COMMENTS BY EIGER LAW Kristian OLENIK Nathan KAISER August 2012 www.eigerlaw.com Page - 2 INPUTS AND COMMENTS 1 CONTENTS: DTA Hong Kong Switzerland: Inputs and Comments

Hong Kong Taxation of Non- Residents

www.pwc.com Hong Kong Taxation of Non- Residents Fergus Wong National Tax Policy Services PricewaterhouseCoopers 28 August 2012 Agenda Treaty developments in Hong Kong Taxation issues of Treaty resident

www.pwc.com Hong Kong Taxation of Non- Residents Fergus Wong National Tax Policy Services PricewaterhouseCoopers 28 August 2012 Agenda Treaty developments in Hong Kong Taxation issues of Treaty resident

LEGISLATIVE COUNCIL BRIEF. Legal Aid Ordinance (Chapter 91) PROPOSED RESOLUTION UNDER THE LEGAL AID ORDINANCE

PROPOSED RESOLUTION UNDER THE LEGAL AID ORDINANCE") File Ref: HAB/CR 19/1/2 LEGISLATIVE COUNCIL BRIEF Legal Aid Ordinance (Chapter 91) PROPOSED RESOLUTION UNDER THE LEGAL AID ORDINANCE INTRODUCTION Annex Pursuant to section 7(b) of the Legal Aid Ordinance

File Ref: HAB/CR 19/1/2 LEGISLATIVE COUNCIL BRIEF Legal Aid Ordinance (Chapter 91) PROPOSED RESOLUTION UNDER THE LEGAL AID ORDINANCE INTRODUCTION Annex Pursuant to section 7(b) of the Legal Aid Ordinance

香 港 特 別 行 政 區 政 府. The Government of the Hong Kong Special Administrative Region. Development Bureau Technical Circular (Works) No.

No.") 政 府 總 部 發 展 局 工 務 科 香 港 特 別 行 政 區 政 府 The Government of the Hong Kong Special Administrative Region Works Branch Development Bureau Government Secretariat 香 港 添 馬 添 美 道 2 號 政 府 總 部 西 翼 1 8 樓 18/F, West

政 府 總 部 發 展 局 工 務 科 香 港 特 別 行 政 區 政 府 The Government of the Hong Kong Special Administrative Region Works Branch Development Bureau Government Secretariat 香 港 添 馬 添 美 道 2 號 政 府 總 部 西 翼 1 8 樓 18/F, West

Legislative Council Panel on Financial Affairs. Proposal to Attract Enterprises to Establish Corporate Treasury Centres in Hong Kong

CB(1)870/14-15(04) For discussion on 1 June 2015 Legislative Council Panel on Financial Affairs Proposal to Attract Enterprises to Establish Corporate Treasury Centres in Hong Kong PURPOSE In his 2015-16

CB(1)870/14-15(04) For discussion on 1 June 2015 Legislative Council Panel on Financial Affairs Proposal to Attract Enterprises to Establish Corporate Treasury Centres in Hong Kong PURPOSE In his 2015-16

THE TAXATION INSTITUTE OF HONG KONG CTA QUALIFYING EXAMINATION PILOT PAPER PAPER 5 ADVANCED TAXATION PRACTICE

THE TAXATION INSTITUTE OF HONG KONG CTA QUALIFYING EXAMINATION PILOT PAPER PAPER 5 ADVANCED TAXATION PRACTICE Advance Tax- pilot_1007_q&a_jy R28/3/2013 1 QUESTIONS Section A Case Answer Question 1 in this

THE TAXATION INSTITUTE OF HONG KONG CTA QUALIFYING EXAMINATION PILOT PAPER PAPER 5 ADVANCED TAXATION PRACTICE Advance Tax- pilot_1007_q&a_jy R28/3/2013 1 QUESTIONS Section A Case Answer Question 1 in this

Implementation of the EU tax directives in Poland

Bartosz Bacia Implementation of the EU tax directives in Poland Since Poland joined the EU on May 1 2004, Polish tax law need to be adapted to the EU Council directives for the member states. The new legal

Bartosz Bacia Implementation of the EU tax directives in Poland Since Poland joined the EU on May 1 2004, Polish tax law need to be adapted to the EU Council directives for the member states. The new legal

Conflicts and Issues under The U.S. - India Tax Treaty

TAX TREATIES Conflicts and Issues under The U.S. - India Tax Treaty Shefali Goradia*, Carol P. Tello** When the income tax treaty between India and the United States ( Treaty ) was negotiated in the late

TAX TREATIES Conflicts and Issues under The U.S. - India Tax Treaty Shefali Goradia*, Carol P. Tello** When the income tax treaty between India and the United States ( Treaty ) was negotiated in the late

BASIC APPROACHES TO TAX TREATY NEGOTIATION 1

Introduction BASIC APPROACHES TO TAX TREATY NEGOTIATION 1 Income tax treaties (technically conventions ) begin with the recitation that they are entered into between countries for the purposes of avoiding

Introduction BASIC APPROACHES TO TAX TREATY NEGOTIATION 1 Income tax treaties (technically conventions ) begin with the recitation that they are entered into between countries for the purposes of avoiding

The Government of the Kingdom of the Netherlands, The Government of the Hong Kong Special Administrative Region of the People s Republic of China,

AGREEMENT BETWEEN THE KINGDOM OF THE NETHERLANDS AND THE HONG KONG SPECIAL ADMINISTRATIVE REGION OF THE PEOPLE S REPUBLIC OF CHINA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION

AGREEMENT BETWEEN THE KINGDOM OF THE NETHERLANDS AND THE HONG KONG SPECIAL ADMINISTRATIVE REGION OF THE PEOPLE S REPUBLIC OF CHINA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION

p r o v i d i n g c o n f i d e n c e t h r o u g h p e r f o r m a n c e

Hong Kong Services p r o v i d i n g c o n f i d e n c e t h r o u g h p e r f o r m a n c e HOW TRIDENT TRUST CAN ASSIST YOU IN HONG KONG Trident Trust has had a multilingual presence in Hong Kong for

Hong Kong Services p r o v i d i n g c o n f i d e n c e t h r o u g h p e r f o r m a n c e HOW TRIDENT TRUST CAN ASSIST YOU IN HONG KONG Trident Trust has had a multilingual presence in Hong Kong for

TOTAL A PRO PR SER SER CES LTD Secure your future

TOTALPRO SERVICES LTD Secure your future International Tax Planning Company Formation and Administration Legal Services Banking Services Accounting and Audit Services Virtual Office Services About us Established

TOTALPRO SERVICES LTD Secure your future International Tax Planning Company Formation and Administration Legal Services Banking Services Accounting and Audit Services Virtual Office Services About us Established

CYPRUS INTERNATIONAL TRUSTS. A. THEORETICAL BACKGROUND Cyprus International Trusts very much follow the way UK trusts operate.

CYPRUS INTERNATIONAL TRUSTS Cypriot trust law has been shaped on the basis of UK law and the Cyprus Trustee Law Cap.193 emulates the English Trustee Act 1925. Concerning the current Cyprus legislative

CYPRUS INTERNATIONAL TRUSTS Cypriot trust law has been shaped on the basis of UK law and the Cyprus Trustee Law Cap.193 emulates the English Trustee Act 1925. Concerning the current Cyprus legislative

LEGISLATIVE COUNCIL PANEL ON COMMERCE AND INDUSTRY. Proposed amendments to the Import and Export (Registration) Regulations (Cap. 60 sub. leg.

Regulations (Cap. 60 sub. leg.") CB(1)278/06-07(06) For information On 21 November 2006 LEGISLATIVE COUNCIL PANEL ON COMMERCE AND INDUSTRY Proposed amendments to the Import and Export (Registration) Regulations (Cap. 60 sub. leg. E) Introduction

CB(1)278/06-07(06) For information On 21 November 2006 LEGISLATIVE COUNCIL PANEL ON COMMERCE AND INDUSTRY Proposed amendments to the Import and Export (Registration) Regulations (Cap. 60 sub. leg. E) Introduction

MERCHANT SHIPPING (LIMITATION OF SHIPOWNERS LIABILITY) (AMENDMENT) ORDINANCE 2005

(AMENDMENT) ORDINANCE 2005") A7 MERCHANT SHIPPING (LIMITATION OF SHIPOWNERS 2005 CONTENTS Section Page 1. Short title and commencement... A9 2. Interpretation... A9 3. Convention to have force of law... A11 4. Application... A13 5.

A7 MERCHANT SHIPPING (LIMITATION OF SHIPOWNERS 2005 CONTENTS Section Page 1. Short title and commencement... A9 2. Interpretation... A9 3. Convention to have force of law... A11 4. Application... A13 5.

Belgium in international tax planning

Belgium in international tax planning Presented by Bernard Peeters and Mieke Van Zandweghe, tax division at Tiberghien Belgium has improved its tax climate considerably in recent years. This may be illustrated

Belgium in international tax planning Presented by Bernard Peeters and Mieke Van Zandweghe, tax division at Tiberghien Belgium has improved its tax climate considerably in recent years. This may be illustrated

Individual income tax in China

Individual income tax in China Individual income tax ( IIT ) is a complicated tax framework and many expatriates are confused about how to determine their tax liability in China. It is strongly recommended

Individual income tax in China Individual income tax ( IIT ) is a complicated tax framework and many expatriates are confused about how to determine their tax liability in China. It is strongly recommended

Tax Issues in Employment and Remuneration. BDO Richfield Advisory Ltd Tax & Legal Services

Tax Issues in Employment and Remuneration Andrew Jackomos Senior Partner BDO Richfield Advisory Limited 13 February 2009 Taxes are what we pay for civilised society. Oliver Wendell Holmes, Jr, Compania

Tax Issues in Employment and Remuneration Andrew Jackomos Senior Partner BDO Richfield Advisory Limited 13 February 2009 Taxes are what we pay for civilised society. Oliver Wendell Holmes, Jr, Compania

Legislative Council Panel on Home Affairs. Two-way Commingling

LC Paper No. CB(2)612/12-13(03) For discussion on 18 February 2013 Legislative Council Panel on Home Affairs Two-way Commingling Purpose This paper briefs Members on the legislative proposals on the Betting

LC Paper No. CB(2)612/12-13(03) For discussion on 18 February 2013 Legislative Council Panel on Home Affairs Two-way Commingling Purpose This paper briefs Members on the legislative proposals on the Betting

立 法 會 Legislative Council

立 法 會 Legislative Council Paper for the House Committee Meeting on 16 October 2015 Legal Service Division Report on Companies (Winding Up and Miscellaneous Provisions) (Amendment) Bill 2015 LC Paper No.

立 法 會 Legislative Council Paper for the House Committee Meeting on 16 October 2015 Legal Service Division Report on Companies (Winding Up and Miscellaneous Provisions) (Amendment) Bill 2015 LC Paper No.

Legislative Council Panel on Financial Affairs

For information Legislative Council Panel on Financial Affairs Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Amendment of Schedule 2) Notice 2015 PURPOSE This

For information Legislative Council Panel on Financial Affairs Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Amendment of Schedule 2) Notice 2015 PURPOSE This

Income Tax Guide on E-Commerce

INLAND REVENUE AUTHORITY OF SINGAPORE Income Tax Guide on E-Commerce This guide is meant to assist businesses in understanding the Income Tax treatment on E- Commerce. Published 3rd Edition 23 February

INLAND REVENUE AUTHORITY OF SINGAPORE Income Tax Guide on E-Commerce This guide is meant to assist businesses in understanding the Income Tax treatment on E- Commerce. Published 3rd Edition 23 February

BANK LEVY DOUBLE TAXATION AGREEMENT BETWEEN THE UNITED KINGDOM AND THE FEDERAL REPUBLIC OF GERMANY

BANK LEVY DOUBLE TAXATION AGREEMENT BETWEEN THE UNITED KINGDOM AND THE FEDERAL REPUBLIC OF GERMANY The Agreement, which was signed in London on 7 December 2011, entered into force on 21 February 2013.

BANK LEVY DOUBLE TAXATION AGREEMENT BETWEEN THE UNITED KINGDOM AND THE FEDERAL REPUBLIC OF GERMANY The Agreement, which was signed in London on 7 December 2011, entered into force on 21 February 2013.

Trust is built with consistency.

Trust is built with consistency. by Lincoln Chafee About Döhle Döhle Corporate and Trust Services Limited (DCTS) is a leading independent corporate and fiduciary service provider specialising in managing

Trust is built with consistency. by Lincoln Chafee About Döhle Döhle Corporate and Trust Services Limited (DCTS) is a leading independent corporate and fiduciary service provider specialising in managing

FSDC Research Paper No. 06. Synopsis Paper Proposing Tax Exemptions and Anti avoidance Measures on Private Equity Funds in the 2013 14 Budget

FSDC Research Paper No. 06 Synopsis Paper Proposing Tax Exemptions and Anti avoidance Measures on Private Equity s in the 2013 14 Budget November 2013 Synopsis Paper Proposing Tax Exemptions and Anti-avoidance

FSDC Research Paper No. 06 Synopsis Paper Proposing Tax Exemptions and Anti avoidance Measures on Private Equity s in the 2013 14 Budget November 2013 Synopsis Paper Proposing Tax Exemptions and Anti-avoidance

Bosera ETFs. Bosera FTSE China A50 Index ETF

Important: If you are in any doubt about the contents of this Addendum, you should consult your stockbroker, bank manager, solicitor, accountant or other financial adviser. This Addendum forms an integral

Important: If you are in any doubt about the contents of this Addendum, you should consult your stockbroker, bank manager, solicitor, accountant or other financial adviser. This Addendum forms an integral

Double Taxation Relief

CHAPTER 15 Double Taxation Relief Some Key Points Bilateral relief Under this method, the Government of two countries can enter into an agreement to provide relief against double taxation by mutually working

CHAPTER 15 Double Taxation Relief Some Key Points Bilateral relief Under this method, the Government of two countries can enter into an agreement to provide relief against double taxation by mutually working

UNITED KINGDOM LIMITED LIABILITY PARTNERSHIPS

UNITED KINGDOM LIMITED LIABILITY PARTNERSHIPS Background A United Kingdom Limited Liability Partnership (LLP) has become a very popular vehicle for international commercial activity. This is because the

UNITED KINGDOM LIMITED LIABILITY PARTNERSHIPS Background A United Kingdom Limited Liability Partnership (LLP) has become a very popular vehicle for international commercial activity. This is because the

MALTA Jurisdictional Guide

MALTA Jurisdictional Guide GENERAL INFORMATION The Republic of Malta is situated in the centre of the Mediterranean, south of Sicily, east of Tunisia and north of Libya. Malta gained its independence from

MALTA Jurisdictional Guide GENERAL INFORMATION The Republic of Malta is situated in the centre of the Mediterranean, south of Sicily, east of Tunisia and north of Libya. Malta gained its independence from

Explanatory notes VAT invoicing rules

Explanatory notes VAT invoicing rules (Council Directive 2010/45/EU) Why explanatory notes? Explanatory notes aim at providing a better understanding of legislation adopted at EU level and in this case

Explanatory notes VAT invoicing rules (Council Directive 2010/45/EU) Why explanatory notes? Explanatory notes aim at providing a better understanding of legislation adopted at EU level and in this case

The Government of Ireland and the Government of the Hong Kong Special Administrative Region of the People s Republic of China;

AGREEMENT BETWEEN THE GOVERNMENT OF IRELAND AND THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION OF THE PEOPLE S REPUBLIC OF CHINA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF

AGREEMENT BETWEEN THE GOVERNMENT OF IRELAND AND THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION OF THE PEOPLE S REPUBLIC OF CHINA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF

IRAS e-tax Guide. Tax Exemption for Foreign-Sourced Income (Second edition)

") IRAS e-tax Guide Tax Exemption for Foreign-Sourced Income (Second edition) Published by Inland Revenue Authority of Singapore Published on 31 May 2013 First edition on 6 Sep 2011 Disclaimers IRAS shall

IRAS e-tax Guide Tax Exemption for Foreign-Sourced Income (Second edition) Published by Inland Revenue Authority of Singapore Published on 31 May 2013 First edition on 6 Sep 2011 Disclaimers IRAS shall

JOINT COUNCIL OF EUROPE/OECD CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS

JOINT COUNCIL OF EUROPE/OECD CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS 1 TABLE OF CONTENTS TEXT OF THE CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS4 PREAMBLE... 4 CHAPTER

JOINT COUNCIL OF EUROPE/OECD CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS 1 TABLE OF CONTENTS TEXT OF THE CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS4 PREAMBLE... 4 CHAPTER

Financial Advisers (Amendment) Bill

Bill") Financial Advisers (Amendment) Bill Bill No. 15/2015. Read the first time on 11 May 2015. A BILL intituled An Act to amend the Financial Advisers Act (Chapter 110 of the 2007 Revised Edition). Be it enacted

Financial Advisers (Amendment) Bill Bill No. 15/2015. Read the first time on 11 May 2015. A BILL intituled An Act to amend the Financial Advisers Act (Chapter 110 of the 2007 Revised Edition). Be it enacted

PROTOCOL ARTICLE 1. Paragraph 3 of Article II (Taxes Covered) of the Convention shall be deleted and replaced by the following paragraph:

of the Convention shall be deleted and replaced by the following paragraph:") PROTOCOL BETWEEN THE KINGDOM OF SPAIN AND CANADA AMENDING THE CONVENTION BETWEEN SPAIN AND CANADA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME

PROTOCOL BETWEEN THE KINGDOM OF SPAIN AND CANADA AMENDING THE CONVENTION BETWEEN SPAIN AND CANADA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME

HONG KONG Corporate information:

HONG KONG Corporate information: Hong Kong is the richest city in China, its economy is one of the most liberal in the world. It is a financial and commercial hub of global significance. Hong Kong is a

HONG KONG Corporate information: Hong Kong is the richest city in China, its economy is one of the most liberal in the world. It is a financial and commercial hub of global significance. Hong Kong is a

Amendments to the Tax Treatment of Financing Costs and Income (Debt Cap)

") Amendments to the Tax Treatment of Financing Costs and Income (Debt Cap) Who is likely to be affected? Large groups of companies that are subject to the debt cap. General description of the measure This

Amendments to the Tax Treatment of Financing Costs and Income (Debt Cap) Who is likely to be affected? Large groups of companies that are subject to the debt cap. General description of the measure This

Proposal to Attract Enterprises to Establish Corporate Treasury Centres ( CTCs ) in Hong Kong

in Hong Kong") CB(1)931/14-15(03) Proposal to Attract Enterprises to Establish Corporate Treasury Centres ( CTCs ) in Hong Kong LegCo Panel on Financial Affairs Meeting on 1 June 2015 2015 16 Budget To attract multinational

CB(1)931/14-15(03) Proposal to Attract Enterprises to Establish Corporate Treasury Centres ( CTCs ) in Hong Kong LegCo Panel on Financial Affairs Meeting on 1 June 2015 2015 16 Budget To attract multinational

UK/HONG KONG DOUBLE TAXATION AGREEMENT AND PROTOCOL SIGNED 21 JUNE 2010 Entered into force 20 December 2010

UK/HONG KONG DOUBLE TAXATION AGREEMENT AND PROTOCOL SIGNED 21 JUNE 2010 Entered into force 20 December 2010 Effective in the United Kingdom from 1 April 2011 for corporation tax and from 6 April 2011 for

UK/HONG KONG DOUBLE TAXATION AGREEMENT AND PROTOCOL SIGNED 21 JUNE 2010 Entered into force 20 December 2010 Effective in the United Kingdom from 1 April 2011 for corporation tax and from 6 April 2011 for

MANUAL ON EFFECTIVE MUTUAL AGREEMENT PROCEDURES (MEMAP)

") ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT MANUAL ON EFFECTIVE MUTUAL AGREEMENT PROCEDURES (MEMAP) February 2007 Version CENTRE FOR TAX POLICY AND ADMINISTRATION MANUAL ON EFFECTIVE MUTUAL

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT MANUAL ON EFFECTIVE MUTUAL AGREEMENT PROCEDURES (MEMAP) February 2007 Version CENTRE FOR TAX POLICY AND ADMINISTRATION MANUAL ON EFFECTIVE MUTUAL

Private Company: SWEDEN

Private Company: SWEDEN Limited Liability Company [Aktiebolag /AB] Partnership [Handelsbolag / HB] Limited Partnership [Kommanditbolag / KB] Formation and Registration Bank Accounts Professional Administration

Private Company: SWEDEN Limited Liability Company [Aktiebolag /AB] Partnership [Handelsbolag / HB] Limited Partnership [Kommanditbolag / KB] Formation and Registration Bank Accounts Professional Administration

MALTA: A JURISDICTION OF CHOICE

MALTA: A JURISDICTION OF CHOICE LONDON - September 2012 Doing business from Malta can make a huge difference for your business UHY BUSINESS ADVISORY SERVICES LIMITED Updated September, 2012 An attractive

MALTA: A JURISDICTION OF CHOICE LONDON - September 2012 Doing business from Malta can make a huge difference for your business UHY BUSINESS ADVISORY SERVICES LIMITED Updated September, 2012 An attractive

UNSOLICITED PROPOSALS

UNSOLICITED PROPOSALS GUIDE FOR SUBMISSION AND ASSESSMENT January 2012 CONTENTS 1 PREMIER S STATEMENT 3 2 INTRODUCTION 3 3 GUIDING PRINCIPLES 5 3.1 OPTIMISE OUTCOMES 5 3.2 ASSESSMENT CRITERIA 5 3.3 PROBITY

UNSOLICITED PROPOSALS GUIDE FOR SUBMISSION AND ASSESSMENT January 2012 CONTENTS 1 PREMIER S STATEMENT 3 2 INTRODUCTION 3 3 GUIDING PRINCIPLES 5 3.1 OPTIMISE OUTCOMES 5 3.2 ASSESSMENT CRITERIA 5 3.3 PROBITY

35. Hong Kong. International Transfer Pricing 2013/14

35. Hong Kong Introduction The increasing cross-border activities of Hong Kong businesses with those in mainland China and the expansion of the Hong Kong treaty network have made transfer pricing a real

35. Hong Kong Introduction The increasing cross-border activities of Hong Kong businesses with those in mainland China and the expansion of the Hong Kong treaty network have made transfer pricing a real

Having amended the Convention by an Additional Protocol that Modifies the Convention, signed at Mexico City on September 8, 1994;

SECOND ADDITIONAL PROTOCOL THAT MODIFIES THE CONVENTION BETWEEN THE GOVERNMENT OF THE UNITED STATES OF AMERICA AND THE GOVERNMENT OF THE UNITED MEXICAN STATES FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE

SECOND ADDITIONAL PROTOCOL THAT MODIFIES THE CONVENTION BETWEEN THE GOVERNMENT OF THE UNITED STATES OF AMERICA AND THE GOVERNMENT OF THE UNITED MEXICAN STATES FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE

SSAP 32 STATEMENT OF STANDARD ACCOUNTING PRACTICE 32 CONSOLIDATED FINANCIAL STATEMENTS AND ACCOUNTING FOR INVESTMENTS IN SUBSIDIARIES

SSAP 32 STATEMENT OF STANDARD ACCOUNTING PRACTICE 32 CONSOLIDATED FINANCIAL STATEMENTS AND ACCOUNTING FOR INVESTMENTS IN SUBSIDIARIES (Issued January 2001) The standards, which have been set in bold italic

SSAP 32 STATEMENT OF STANDARD ACCOUNTING PRACTICE 32 CONSOLIDATED FINANCIAL STATEMENTS AND ACCOUNTING FOR INVESTMENTS IN SUBSIDIARIES (Issued January 2001) The standards, which have been set in bold italic

Communication between the Auditor and the Insurance Authority

PN 620.2 Revised February 2013 Practice Note 620.2 Communication between the Auditor and the Insurance Authority PRACTICE NOTE 620.2 COMMUNICATION BETWEEN THE AUDITOR AND THE INSURANCE AUTHORITY (Issued

PN 620.2 Revised February 2013 Practice Note 620.2 Communication between the Auditor and the Insurance Authority PRACTICE NOTE 620.2 COMMUNICATION BETWEEN THE AUDITOR AND THE INSURANCE AUTHORITY (Issued

TAXATION AND FOREIGN EXCHANGE

TAXATION OF EQUITY HOLDERS The following is a summary of certain PRC and Hong Kong tax consequences of the ownership of H Shares by an investor that purchases such H Shares in the Global Offering and holds

TAXATION OF EQUITY HOLDERS The following is a summary of certain PRC and Hong Kong tax consequences of the ownership of H Shares by an investor that purchases such H Shares in the Global Offering and holds

25*$1,6$7,21)25(&2120,&&223(5$7,21$1''(9(/230(17

25(&2120,&&223(5$7,21$1''(9(/230(17") 25*$1,6$7,21)25(&2120,&&223(5$7,21$1''(9(/230(17 &URVVERUGHU,QFRPH7D[,VVXHV$ULVLQJIURP (PSOR\HH6WRFN2SWLRQ3ODQV &(175()257$;32/,&

25*$1,6$7,21)25(&2120,&&223(5$7,21$1''(9(/230(17 &URVVERUGHU,QFRPH7D[,VVXHV$ULVLQJIURP (PSOR\HH6WRFN2SWLRQ3ODQV &(175()257$;32/,&

CLSA ASIA-PACIFIC SECURITIES DEALING SERVICES: AUSTRALIA MARKET ANNEX

CLSA ASIA-PACIFIC SECURITIES DEALING SERVICES: AUSTRALIA MARKET ANNEX IMPORTANT NOTICE CLSA Singapore Pte Ltd (ARBN 125 288 271, a company incorporated in Singapore) is permitted to provide certain financial

CLSA ASIA-PACIFIC SECURITIES DEALING SERVICES: AUSTRALIA MARKET ANNEX IMPORTANT NOTICE CLSA Singapore Pte Ltd (ARBN 125 288 271, a company incorporated in Singapore) is permitted to provide certain financial

IMPROVING THE RESOLUTION OF TAX TREATY DISPUTES

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT IMPROVING THE RESOLUTION OF TAX TREATY DISPUTES (Report adopted by the Committee on Fiscal Affairs on 30 January 2007) February 2007 CENTRE FOR TAX

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT IMPROVING THE RESOLUTION OF TAX TREATY DISPUTES (Report adopted by the Committee on Fiscal Affairs on 30 January 2007) February 2007 CENTRE FOR TAX

Implementing a Diverted Profits Tax

Implementing a Diverted Profits Tax May 2016 Commonwealth of Australia 2016 ISBN 978-1-925220-92-6 This publication is available for your use under a Creative Commons Attribution 3.0 Australia licence,

Implementing a Diverted Profits Tax May 2016 Commonwealth of Australia 2016 ISBN 978-1-925220-92-6 This publication is available for your use under a Creative Commons Attribution 3.0 Australia licence,

15 Double Taxation Relief

15 Double Taxation Relief 15.1 Concept of Double Taxation Relief In the present era of cross-border transactions across the globe, the effect of taxation is one of the important considerations for any

15 Double Taxation Relief 15.1 Concept of Double Taxation Relief In the present era of cross-border transactions across the globe, the effect of taxation is one of the important considerations for any

Requirements made under the Intermediaries Byelaw

Chapter 2 Requirements made under the Intermediaries Byelaw Section 1 Delegated Underwriting Registers of coverholders and registered binding authorities Part B of the Intermediaries Byelaw Format and

Chapter 2 Requirements made under the Intermediaries Byelaw Section 1 Delegated Underwriting Registers of coverholders and registered binding authorities Part B of the Intermediaries Byelaw Format and

GLOBAL GUIDE TO M&A TAX

Quality tax advice, globally GLOBAL GUIDE TO M&A TAX 2013 EDITION www.taxand.com CYPRUS Cyprus From a Buyer s Perspective 1. What are the main differences among acquisitions made through a share deal versus

Quality tax advice, globally GLOBAL GUIDE TO M&A TAX 2013 EDITION www.taxand.com CYPRUS Cyprus From a Buyer s Perspective 1. What are the main differences among acquisitions made through a share deal versus

Part 3. Company Formation and Related Matters, and Re-registration of Company

Part 3 Division 1 Subdivision 1 Section 66 A3491 Part 3 Company Formation and Related Matters, and Re-registration of Company Division 1 Company Formation Subdivision 1 General Requirements for Formation

Part 3 Division 1 Subdivision 1 Section 66 A3491 Part 3 Company Formation and Related Matters, and Re-registration of Company Division 1 Company Formation Subdivision 1 General Requirements for Formation

MODEL CONVENTION WITH RESPECT TO TAXES ON INCOME AND ON CAPITAL

WITH RESPECT TO TAXES ON INCOME AND ON CAPITAL SUMMARY OF THE CONVENTION Title and Preamble Chapter I SCOPE OF THE CONVENTION Article 1 Article 2 Persons covered Taxes covered Chapter II DEFINITIONS Article

WITH RESPECT TO TAXES ON INCOME AND ON CAPITAL SUMMARY OF THE CONVENTION Title and Preamble Chapter I SCOPE OF THE CONVENTION Article 1 Article 2 Persons covered Taxes covered Chapter II DEFINITIONS Article

How To Get A Small Business License In Australia

1 L.R.O. 2007 Small Business Development CAP. 318C CHAPTER 318C SMALL BUSINESS DEVELOPMENT ARRANGEMENT OF SECTIONS SECTION 1. Short title. 2. Interpretation. 3. Small business. 4. Approved small business

1 L.R.O. 2007 Small Business Development CAP. 318C CHAPTER 318C SMALL BUSINESS DEVELOPMENT ARRANGEMENT OF SECTIONS SECTION 1. Short title. 2. Interpretation. 3. Small business. 4. Approved small business

Rules for the admission of shares to stock exchange listing (Listing Rules)

") Rules for the admission of shares to stock exchange listing (Listing Rules) TABLE OF CONTENTS: 1. GENERAL... 3 2. CONDITIONS FOR ADMISSION TO LISTING... 3 2.1 GENERAL CONDITIONS... 3 2.1.1 Public interest,

Rules for the admission of shares to stock exchange listing (Listing Rules) TABLE OF CONTENTS: 1. GENERAL... 3 2. CONDITIONS FOR ADMISSION TO LISTING... 3 2.1 GENERAL CONDITIONS... 3 2.1.1 Public interest,

GUIDELINES ON TAXATION OF ELECTRONIC COMMERCE

IRB MALAYSIA E-COMMERCE GUIDELINES INLAND REVENUE BOARD OF MALAYSIA GUIDELINES ON TAXATION OF ELECTRONIC COMMERCE TABLE OF CONTENTS Page 1. Introduction 1 2. Terminology 1 3. Scope of Charge 2 4. Scope

IRB MALAYSIA E-COMMERCE GUIDELINES INLAND REVENUE BOARD OF MALAYSIA GUIDELINES ON TAXATION OF ELECTRONIC COMMERCE TABLE OF CONTENTS Page 1. Introduction 1 2. Terminology 1 3. Scope of Charge 2 4. Scope

International Assignment Services Taxation of International Assignees Country Hong Kong

www.pwc.com/globalmobility International Assignment Services Taxation of International Assignees Country Hong Kong Human Resources Services International Assignment Taxation Folio Last Updated: December

www.pwc.com/globalmobility International Assignment Services Taxation of International Assignees Country Hong Kong Human Resources Services International Assignment Taxation Folio Last Updated: December

INCOME TAX PRACTICES MAINTAINED BY BELGIUM. Report of the Panel presented to the Council of Representatives on 12 November 1976 (L/4424-23S/127)

") 2 November 1976 INCOME TAX PRACTICES MAINTAINED BY BELGIUM Report of the Panel presented to the Council of Representatives on 12 November 1976 (L/4424-23S/127) 1. The Panel's terms of reference were established

2 November 1976 INCOME TAX PRACTICES MAINTAINED BY BELGIUM Report of the Panel presented to the Council of Representatives on 12 November 1976 (L/4424-23S/127) 1. The Panel's terms of reference were established

LEGISLATIVE COUNCIL BRIEF. Resolution of the Legislative Council under Section 48A of the Employees Compensation Ordinance, Cap 282

LEGISLATIVE COUNCIL BRIEF Resolution of the Legislative Council under Section 48A of the Employees Compensation Ordinance, Cap 282 Resolution of the Legislative Council under Section 40 of the Pneumoconiosis

LEGISLATIVE COUNCIL BRIEF Resolution of the Legislative Council under Section 48A of the Employees Compensation Ordinance, Cap 282 Resolution of the Legislative Council under Section 40 of the Pneumoconiosis

Thinking Beyond Borders

INTERNATIONAL EXECUTIVE SERVICES Thinking Beyond Borders Hong Kong kpmg.com Hong Kong Introduction There is no general income tax in Hong Kong. For income to be subject to tax, it must fall under one of

INTERNATIONAL EXECUTIVE SERVICES Thinking Beyond Borders Hong Kong kpmg.com Hong Kong Introduction There is no general income tax in Hong Kong. For income to be subject to tax, it must fall under one of

It is further notified in terms of paragraph 1 of Article 27 of the Convention, that the date of entry into force is 17 December 2002.

NEW CONVENTION BETWEEN THE GOVERNMENT OF THE REPUBLIC OF SOUTH AFRICA AND THE GOVERNMENT OF THE UNITED KINGDOM OF GREAT BRITAIN AND NORTHERN IRELAND FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION

NEW CONVENTION BETWEEN THE GOVERNMENT OF THE REPUBLIC OF SOUTH AFRICA AND THE GOVERNMENT OF THE UNITED KINGDOM OF GREAT BRITAIN AND NORTHERN IRELAND FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION

15. 2. 2. 2. Is Section 10d of the Corporate Income Tax Act consistent with Article 9 of the OECD Model Tax Convention?

CHAPTER 15. SUMMARY AND CONCLUSIONS 15. 1. Introduction The main question addressed in this PhD thesis is whether the restrictions placed by Dutch law on deducting interest for corporate income tax purposes

CHAPTER 15. SUMMARY AND CONCLUSIONS 15. 1. Introduction The main question addressed in this PhD thesis is whether the restrictions placed by Dutch law on deducting interest for corporate income tax purposes

TITLE VIII PAYMENT, CLEARING AND SETTLEMENT SUPERVISION

1 0 1 TITLE VIII PAYMENT, CLEARING AND SETTLEMENT SUPERVISION SEC. 01. SHORT TITLE. This title may be cited as the Payment, Clearing, and Settlement Supervision Act of 00. SEC. 0. FINDINGS AND PURPOSES.

1 0 1 TITLE VIII PAYMENT, CLEARING AND SETTLEMENT SUPERVISION SEC. 01. SHORT TITLE. This title may be cited as the Payment, Clearing, and Settlement Supervision Act of 00. SEC. 0. FINDINGS AND PURPOSES.

Income tax for individuals is computed on a monthly basis by applying the above progressive tax rates to employment income.

Worldwide personal tax guide 2013 2014 China Local information Tax Authority Website Tax Year Tax Return due date Is joint filing possible Are tax return extensions possible State Administration of Taxation

Worldwide personal tax guide 2013 2014 China Local information Tax Authority Website Tax Year Tax Return due date Is joint filing possible Are tax return extensions possible State Administration of Taxation

Income in the Netherlands is categorised into boxes. The above table relates to Box 1 income.

Worldwide personal tax guide 2013 2014 The Netherlands Local information Tax Authority Website Tax Year Tax Return due date Is joint filing possible Are tax return extensions possible Belastingdienst www.belastingdienst.nl

Worldwide personal tax guide 2013 2014 The Netherlands Local information Tax Authority Website Tax Year Tax Return due date Is joint filing possible Are tax return extensions possible Belastingdienst www.belastingdienst.nl