立 法 會. Legislative Council. Bills Committee on Inland Revenue (Amendment) (No.3) Bill Background brief

|

|

|

- Ella Page

- 8 years ago

- Views:

Transcription

1 立 法 會 Legislative Council LC Paper No. CB(1)790/13-14(02) Ref : CB1/BC/3/13 Bills Committee on Inland Revenue (Amendment) (No.3) Bill 2013 Background brief Purpose 1. This paper provides background information on the Inland Revenue (Amendment) (No. 3) Bill 2013 ("the Bill"). It also summarizes the major views and suggestions raised by Members on issues relating to the proposals in the Bill. Proposed tax concession for captive insurers under the Budget 2. Captive insurance is a form of self-insurance by companies. A company may wish to set up a captive insurer to provide coverage of specific risks that is not readily available in the market. As a captive insurer 1 can operate with a lower overhead (e.g. no marketing expenses and commission to insurance intermediaries) and profit margin, it may charge a lower premium and the parent company can also share the underwriting profits of the captive insurer. At present, there are two captive insurers in Hong Kong 2. A number of regulatory concessions are currently offered to captive insurance companies, e.g. lower capital, solvency margin requirements and fees. The concessions currently provided to captive insurance companies and comparison with non-life insurance companies on regulatory requirements are given in Appendix I. 1 2 In Hong Kong, a captive insurer is legally defined under the Insurance Companies Ordinance (Cap. 41) as an insurer which carries on general business only and is restricted to underwriting insurance and reinsurance of risks of the companies within the same group of companies to which the captive insurer belongs. CNOOC Insurance Limited (authorized on 5 December 2000) and Sinopec Insurance Limited (authorized on 31 October 2013).

2 As one of the measures to foster cooperation between the Mainland and Hong Kong, the State Council of the Central People's Government promulgated in June 2012 the policy to encourage Mainland enterprises to form captive insurers in Hong Kong to enhance their risk management. In the Budget, the Financial Secretary proposed to reduce the profits tax on the offshore insurance business of captive insurance companies so that they would enjoy the same tax concessions under the Inland Revenue Ordinance (Cap. 112) ("IRO") as those currently applicable to reinsurance companies (i.e. one-half of the normal tax rate of 16.5% for corporations). According to the Administration, it has consulted the Insurance Advisory Committee on the tax concession proposal in August 2013 and obtained its support. Increasing the deduction ceiling for contributions to recognized retirement schemes 4. Section 16AA of IRO provides for the deduction of mandatory contribution by self-employed persons ("SEPs") for the purpose of calculating their tax payable under profits tax. Section 26G of IRO provides for the deduction of contribution to recognized occupational retirement schemes and mandatory contribution to the Mandatory Provident Fund ("MPF") Schemes by employees for the purposes of calculating tax payable under salaries tax or tax under personal assessment. The maximum amount of allowable deduction under section 16AA or 26G of IRO for each year of assessment is prescribed in Schedule 3B to IRO. It is currently set at $15,000 (i.e. $25,000 x 5% x 12 months). 5. On commencement of the Mandatory Provident Fund Schemes Ordinance (Amendment of Schedule 3) Notice 2013 on 1 June , the maximum relevant income ("Max RI") under the Mandatory Provident Fund Schemes Ordinance (Cap. 485) ("MPFSO") will be increased from $25,000 to $30,000 per month. Following this, the Administration proposes to increase the deduction ceiling for contributions 4 to recognized retirement schemes from $15,000 to $17,500 5 for the 2014/15 year of assessment, and $18,000 6 from the 2015/16 year of assessment onwards The Legislative Council ("LegCo") has set up a subcommittee to study the Mandatory Provident Fund Schemes Ordinance (Amendment of Schedule 3) Notice At the meeting of 17 July 2013, the LegCo passed a resolution to approve the Schedule 3 Notice to enable the implementation of the new maximum relevant income of $30,000 on I June Contributions include: (a) mandatory contributions by a SEP under MPFSO; (b) the lesser of the amount of the contributions paid by a person as an employee to a recognized occupational retirement scheme or the amount he would have been required to pay if at all times whilst an employee during the relevant year of assessment he had contributed as a participant in a mandatory provident fund scheme; and (c) mandatory contributions by an employee to a mandatory provident fund scheme under MPFSO. $25,000 x 5% x 2 months + $30,000 x 5% x 10 months $30,000 x 5% x 12 months

3 - 3 - The Bill 6. The Bill, for the purpose of implementing the two proposals in paragraphs 3 and 5 above, was published in the Gazette on 27 December 2013 and received First Reading in LegCo on 8 January The main provisions of the Bill are as follows (a) (b) (c) (d) Clause 3: provides that the profits tax concession for qualifying captive insurers applies to the year of assessment commencing on 1 April 2013 and to all subsequent years of assessment; Clause 4: amends section 14B of IRO to allow a corporation's assessable profits that are derived from the business of insurance of offshore risks as a captive insurer to be chargeable to profits tax at one-half of the normal rate; Clause 6: amends section 23A IRO to provide for the formula for ascertaining a captive insurer's assessable profits that are derived from the business of insurance of offshore risks; Clause 7: amends Schedule 3B to IRO to raise the maximum amount deductible from assessment income for the following contributions (i) (ii) mandatory contributions paid by any SEP under MPFSO; and certain contributions paid by any person to a recognized retirement scheme as an employee; and (e) Clauses 8 and 9: adds a new Schedule 30 to IRO to provide for the transitional arrangements relating to the holding over payment of provisional salaries tax and provisional profits tax, on the ground of the taxpayer's entitlement to the rise in deduction ceiling for contributions to recognized retirement schemes, for the years of assessment 2014/15 and 2015/ The Bill, if passed, would come into operation on the day on which it is published in the Gazette. 8. At the House Committee meeting held on 10 January 2014, Members agreed to form a bills committee to study the Bill.

4 - 4 - Major views and concerns expressed by Members 9. Members have raised matters relating to the development of captive insurance and the proposed profits tax concessions during the session on financial services of the special meeting of the Finance Committee held on 8 April 2013 for the examination of the Estimates of Expenditure The Administration consulted the Panel on Financial Affairs on the two proposals under the Bill at the meeting on 4 November Panel members were generally in support of the two proposals. The major views and concerns raised by Members at the above meetings are summarized in the ensuing paragraphs. Proposed tax concession for captive insurers Attracting more companies to set up captive insurers in Hong Kong 10. Noting that some jurisdictions in Asia had offered more tax concessions for captive insurers, including Singapore which had exempted captive insurers from all profits tax, some Members considered that the proposed tax concessions might not be competitive enough in attracting foreign captive insurers to establish in Hong Kong. There was a suggestion that the Administration should consider offering more incentives, for example, by exempting the captive insurers from all profits tax in their first two years of operation in Hong Kong. The Administration advised that the Government had granted other regulatory concessions for promoting captive insurance business, e.g. lowering their capital and solvency margin requirements, exempting them from the requirement of maintaining assets in Hong Kong, etc. The tax concessions proposed in the Budget would act as a further impetus in attracting captive insurers to domicile in Hong Kong. The Administration would review the measure after one or two years of implementation, and consider whether further concessions would be necessary with due regard to the impact on tax revenue. 11. On Members' enquiries about the major considerations of captive insurers to set up business in Hong Kong besides tax concessions, the Administration responded that the sound legal system, robust regulatory regime and availability of a wide range of professional services were major incentives for setting up business in Hong Kong. Moreover, the proximity of Hong Kong to major Mainland cities and the policy support from the Central People's Government were also instrumental in making Hong Kong an attractive domicile for captive insurers. Given that the concept of captive insurance was still novel to many enterprises in Asia, the Government would accord priority to working with the industry in increasing market awareness and promoting utilization of captive insurance. As regards the benefits for the local job

5 - 5 - market, the Administration advised that it might not be necessary for captive insurers to employ a large workforce of its own as they could outsource captive insurance management services to insurance broker firms. Nevertheless, with the establishment of more captive insurers in Hong Kong, it was envisaged that the pool of local professionals of related business (e.g. reinsurance, legal and actuarial services) would expand in future. 12. In providing incentives for enterprises to set up captive insurance companies in Hong Kong, there was a view from Members that the Administration should balance the interests between large foreign insurance companies and small and medium-sized local insurance companies. The Administration advised that both foreign and local insurance companies, regardless of their size, had all along been competing on a level playing field in Hong Kong. Encouraging foreign enterprises to set up their captive insurance companies in Hong Kong would have minimal impact on the interests of small and medium-sized local insurance companies because captive insurance companies exclusively underwrote the risks of their parent companies, group companies or other affiliated companies. Those risks were mostly outside Hong Kong which were not the target business of small and medium-sized local insurance companies. 13. Upon request by Members, the Administration had provided information on the insurance sector, including the number of captive insurance companies and professional reinsurance companies authorized in Hong Kong in recent years, the revenues from profits tax generated from these companies, and the percentage of contribution of insurance business to the Gross Domestic Product of Hong Kong. The information is in Appendix II. Avoidance of double taxation 14. Members have enquired about the measures to avoid double taxation on Mainland-based companies setting up captive insurance business in Hong Kong. The Administration advised that under the Arrangement between the Mainland of China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income ("the Arrangement"), the profits of a Mainland enterprise carrying on business through a permanent establishment in Hong Kong would be subject to Hong Kong tax but the Mainland enterprise would be entitled to a tax credit in the Mainland. As Hong Kong adopted the territorial basis of taxation, the profits of a Hong Kong enterprise derived from a permanent establishment in the Mainland would not normally be subject to profits tax in Hong Kong, and hence there would be no double taxation. The Arrangement would help avoid levying double taxation in respect of profits tax of captive insurers set up by Mainland companies in Hong Kong.

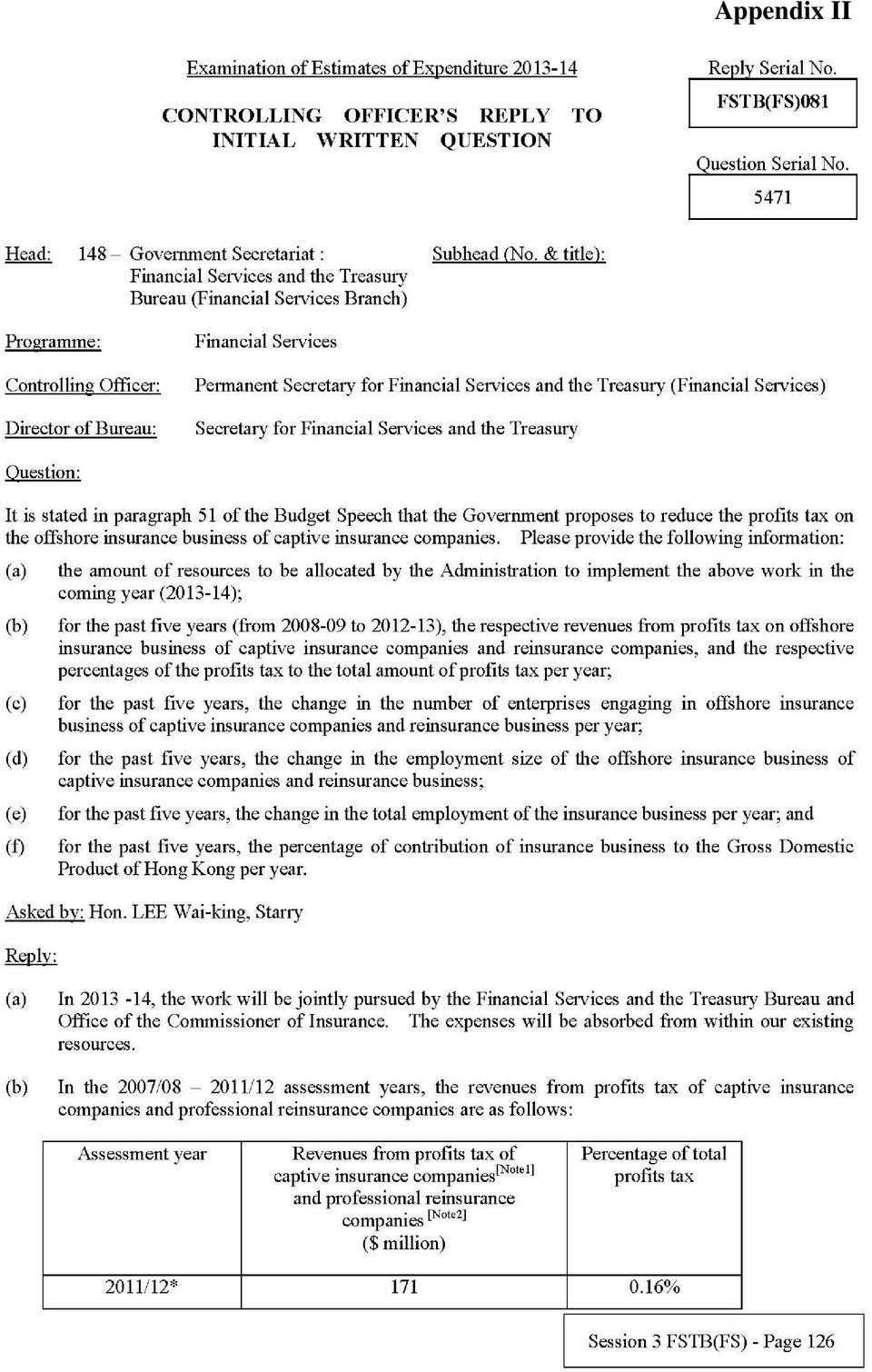

6 - 6 - Proposed increase in the deduction ceiling for contributions to recognized retirement schemes 15. In the light of the ageing population in Hong Kong, a Member suggested that the Administration should consider granting more tax concessions to encourage employees and SEP to increase the voluntary contributions to their retirement schemes so as to enhance their personal savings for better retirement protection. The Member considered that such tax concessions would be particularly useful for MPF schemes, as under such schemes the employers' mandatory contributions would be used to offset the severance payment or the long service payment which would reduce the savings for MPF scheme members. The Administration was urged to consider the suggestion in the context of the 2014 Policy Address and the Budget. Relevant papers 16. A list of the relevant papers on the LegCo website is in Appendix III. Council Business Division 1 Legislative Council Secretariat 27 January 2014

7 Appendix I Concessions currently granted by the Government to captive insurance companies and comparison with non-life insurance companies on regulatory requirements Item Captive Insurer Non-life Insurance Company Minimum Requirement Capital HK$2 million HK$10 million Minimum Margin Solvency The greatest of: a. 5% of the premium income; or b. 5% of the claims outstanding; or c. HK$2 million The greatest of: a. generally 20% of the premium b. generally 20%of the claims outstanding; or c. HK$10 million Requirement for Assets in Hong Kong Valuation Regulation Exempted Assets and liabilities to be valued on the basis of Generally Accepted Accounting Principles To maintain assets in Hong Kong of an amount not less than 80% of its Hong Kong net liabilities plus solvency margin Assets and liabilities to be valued according to the Insurance Companies (General Business) (Valuation) Regulation Authorization Annual Fee and HK$22,600 HK$227,300 (Source: Extract from the Administration's reply to a written question raised by Hon LEUNG Kwok-hung during the examination of Estimates of Expenditure (Reply Serial No. FSTB(FS)086))

8 Appendix II

9 - 2 -

10 Appendix III List of relevant papers Date Event Paper/Minutes of meeting April 2013 July 2013 Special meeting of the Finance Committee for examination of Estimates of Expenditure Report of the Subcommittee on Mandatory Provident Fund Schemes Ordinance (Amendment of Schedule 2) Notice 2013 and Mandatory Provident Fund Schemes Ordinance (Amendment of Schedule 3) Notice 2013 ("the Notices") Written questions raised by members on issues relating to captive insurance business (Reply Serial Nos: FSTB(FS)022, 055, 081 and 086) Report (LC Paper No. CB(1)1478/12-13) 17 July 2013 Council meeting Hansard (Relevant proceedings of the proposed resolutions moved by the Administration in relation to the Notices in pages ) 4 November 2013 Meeting of the Panel on Financial Affairs Discussion paper (LC Paper No. CB(1)155/13-14(02)) Minutes (paragraphs 8 to 17) (LC Paper No. CB(1)626/13-14)

1478/12-13) 17 July 2013 Council meeting Hansard (Relevant proceedings of the proposed resolutions moved by the Administration in relation to the Notices in pages 249-305) 4 November 2013")

11 - 2 - Date Event Paper/Minutes of meeting 8 January 2014 Introduction of the Inland Revenue (Amendment) (No. 3) Bill 2013 into the Legislative Council The Bill Legislative Council Brief on Inland Revenue (Amendment) (No. 3) Bill 2013 (L/M(19) in G6/90/4C(2011) Pt.5) Legal Service Division report on the Bill (LC Paper No. LS22/13-14)

Bill 2013 (L/M(19) in G6/90/4C(2011) Pt.")

Legislative Council Panel on Financial Affairs. Proposal to Attract Enterprises to Establish Corporate Treasury Centres in Hong Kong

CB(1)870/14-15(04) For discussion on 1 June 2015 Legislative Council Panel on Financial Affairs Proposal to Attract Enterprises to Establish Corporate Treasury Centres in Hong Kong PURPOSE In his 2015-16

CB(1)870/14-15(04) For discussion on 1 June 2015 Legislative Council Panel on Financial Affairs Proposal to Attract Enterprises to Establish Corporate Treasury Centres in Hong Kong PURPOSE In his 2015-16

立 法 會 Legislative Council

Ref : CB2/BC/3/12 立 法 會 Legislative Council LC Paper No. CB(2)1092/12-13(05) Bills Committee on Betting Duty (Amendment) Bill 2013 Background brief prepared by the Legislative Council Secretariat Purpose

Ref : CB2/BC/3/12 立 法 會 Legislative Council LC Paper No. CB(2)1092/12-13(05) Bills Committee on Betting Duty (Amendment) Bill 2013 Background brief prepared by the Legislative Council Secretariat Purpose

立 法 會 Legislative Council

立 法 會 Legislative Council Paper for the House Committee Meeting on 16 October 2015 Legal Service Division Report on Companies (Winding Up and Miscellaneous Provisions) (Amendment) Bill 2015 LC Paper No.

立 法 會 Legislative Council Paper for the House Committee Meeting on 16 October 2015 Legal Service Division Report on Companies (Winding Up and Miscellaneous Provisions) (Amendment) Bill 2015 LC Paper No.

Legislative Council Panel on Home Affairs. Two-way Commingling

LC Paper No. CB(2)612/12-13(03) For discussion on 18 February 2013 Legislative Council Panel on Home Affairs Two-way Commingling Purpose This paper briefs Members on the legislative proposals on the Betting

LC Paper No. CB(2)612/12-13(03) For discussion on 18 February 2013 Legislative Council Panel on Home Affairs Two-way Commingling Purpose This paper briefs Members on the legislative proposals on the Betting

Proposal to Attract Enterprises to Establish Corporate Treasury Centres ( CTCs ) in Hong Kong

in Hong Kong") CB(1)931/14-15(03) Proposal to Attract Enterprises to Establish Corporate Treasury Centres ( CTCs ) in Hong Kong LegCo Panel on Financial Affairs Meeting on 1 June 2015 2015 16 Budget To attract multinational

CB(1)931/14-15(03) Proposal to Attract Enterprises to Establish Corporate Treasury Centres ( CTCs ) in Hong Kong LegCo Panel on Financial Affairs Meeting on 1 June 2015 2015 16 Budget To attract multinational

A GUIDE TO THE OCCUPATIONAL RETIREMENT SCHEMES ORDINANCE

A GUIDE TO THE OCCUPATIONAL RETIREMENT SCHEMES ORDINANCE Issued by THE REGISTRAR OF OCCUPATIONAL RETIREMENT SCHEMES Level 16, International Commerce Centre, 1 Austin Road West, Kowloon, Hong Kong. ORS/C/5

A GUIDE TO THE OCCUPATIONAL RETIREMENT SCHEMES ORDINANCE Issued by THE REGISTRAR OF OCCUPATIONAL RETIREMENT SCHEMES Level 16, International Commerce Centre, 1 Austin Road West, Kowloon, Hong Kong. ORS/C/5

Thinking Beyond Borders

INTERNATIONAL EXECUTIVE SERVICES Thinking Beyond Borders Hong Kong kpmg.com Hong Kong Introduction There is no general income tax in Hong Kong. For income to be subject to tax, it must fall under one of

INTERNATIONAL EXECUTIVE SERVICES Thinking Beyond Borders Hong Kong kpmg.com Hong Kong Introduction There is no general income tax in Hong Kong. For income to be subject to tax, it must fall under one of

Deductibility of contributions for. employees and. self-employed persons

Deductibility of contributions for employees and self-employed persons Mandatory Provident Fund Scheme or Recognized Occupational Retirement Scheme Mandatory Provident Fund Scheme (MPFS) Employees (full-time

Deductibility of contributions for employees and self-employed persons Mandatory Provident Fund Scheme or Recognized Occupational Retirement Scheme Mandatory Provident Fund Scheme (MPFS) Employees (full-time

DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 23 (REVISED) RECOGNIZED RETIREMENT SCHEMES

RECOGNIZED RETIREMENT SCHEMES") Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 23 (REVISED) RECOGNIZED RETIREMENT SCHEMES These notes are issued for the information of taxpayers and their tax representatives.

Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 23 (REVISED) RECOGNIZED RETIREMENT SCHEMES These notes are issued for the information of taxpayers and their tax representatives.

Life and Non-Life Insurance (2)

") Life and Non-Life Insurance (2) Life and Non-Life Business in Hong Kong Regulations and Actuarial Guidelines Regulatory Framework The principal regulation for the regulation of the insurance industry in

Life and Non-Life Insurance (2) Life and Non-Life Business in Hong Kong Regulations and Actuarial Guidelines Regulatory Framework The principal regulation for the regulation of the insurance industry in

LEGISLATIVE COUNCIL BRIEF. Inland Revenue Ordinance (Chapter 112)

") File Ref: TsyB R 183/800-1-1/38/0 (C) LEGISLATIVE COUNCIL BRIEF Inland Revenue Ordinance (Chapter 112) INLAND REVENUE (DOUBLE TAXATION RELIEF AND PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME)

File Ref: TsyB R 183/800-1-1/38/0 (C) LEGISLATIVE COUNCIL BRIEF Inland Revenue Ordinance (Chapter 112) INLAND REVENUE (DOUBLE TAXATION RELIEF AND PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME)

Arrangement between the Mainland of China and the HKSAR for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion

Arrangement between the Mainland of China and the HKSAR for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion INCOME FROM PERSONAL SERVICES Inland Revenue Department Hong Kong Special

Arrangement between the Mainland of China and the HKSAR for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion INCOME FROM PERSONAL SERVICES Inland Revenue Department Hong Kong Special

Retirement Benefits in Hong Kong

Retirement Benefits in Hong Kong Introduction In Hong Kong, there are several types of retirement benefits sponsored by different parties as shown below. Government-sponsor - Old Age Allowances from the

Retirement Benefits in Hong Kong Introduction In Hong Kong, there are several types of retirement benefits sponsored by different parties as shown below. Government-sponsor - Old Age Allowances from the

立 法 會 Legislative Council

立 法 會 Legislative Council Ref : CB1/PL/FA LC Paper No. CB(1)1401/12-13(03) Panel on Financial Affairs Meeting on 5 July 2013 Background brief on proposed establishment of an independent Insurance Authority

立 法 會 Legislative Council Ref : CB1/PL/FA LC Paper No. CB(1)1401/12-13(03) Panel on Financial Affairs Meeting on 5 July 2013 Background brief on proposed establishment of an independent Insurance Authority

H O N G K O N G. International Comparison of Insurance Taxation March 2007

H O N G K O N G International Comparison of Insurance International Comparison of Insurance Hong Kong General Insurance 1 Definition Definition of property and casualty insurance company A company authorised

H O N G K O N G International Comparison of Insurance International Comparison of Insurance Hong Kong General Insurance 1 Definition Definition of property and casualty insurance company A company authorised

Application of Insurer Authorisation in Hong Kong

www.pwchk.com Application of Insurer Authorisation in Hong Kong Highlights of the Regulatory Requirements Updated as of January 2012 1. Introduction Under the Hong Kong regulatory regime, institutions

www.pwchk.com Application of Insurer Authorisation in Hong Kong Highlights of the Regulatory Requirements Updated as of January 2012 1. Introduction Under the Hong Kong regulatory regime, institutions

News Flash Hong Kong Tax. November 2015 Issue 10. In brief. In detail. www.pwchk.com

News Flash Hong Kong Tax Understanding the IRD s views on emerging corporate tax issues, in particular the practice on processing Hong Kong tax resident certificate applications November 2015 Issue 10

News Flash Hong Kong Tax Understanding the IRD s views on emerging corporate tax issues, in particular the practice on processing Hong Kong tax resident certificate applications November 2015 Issue 10

Hong Kong International Comparison of Insurance Taxation

Hong Kong International Comparison of Insurance March 2009 Hong Kong General Insurance Definition Definition of property and casualty insurance company A company authorised under the Insurance Companies

Hong Kong International Comparison of Insurance March 2009 Hong Kong General Insurance Definition Definition of property and casualty insurance company A company authorised under the Insurance Companies

A guide to Profits Tax for unincorporated businesses (1) The need-to-know for new businesses and commonly asked questions

The need-to-know for new businesses and commonly asked questions") A guide to Profits Tax for unincorporated businesses (1) The need-to-know for new businesses and commonly asked questions Foreword This guide will help answer some of the questions that owners of small

A guide to Profits Tax for unincorporated businesses (1) The need-to-know for new businesses and commonly asked questions Foreword This guide will help answer some of the questions that owners of small

立 法 會 Legislative Council

立 法 會 Legislative Council LC Paper No. CB(1) 239/11-12 Ref. : CB1/SS/16/10 Paper for the House Committee Subcommittee on Securities and Futures (Contracts Limits and Reportable Positions) (Amendment) Rules

立 法 會 Legislative Council LC Paper No. CB(1) 239/11-12 Ref. : CB1/SS/16/10 Paper for the House Committee Subcommittee on Securities and Futures (Contracts Limits and Reportable Positions) (Amendment) Rules

p r o v i d i n g c o n f i d e n c e t h r o u g h p e r f o r m a n c e

Hong Kong Services p r o v i d i n g c o n f i d e n c e t h r o u g h p e r f o r m a n c e HOW TRIDENT TRUST CAN ASSIST YOU IN HONG KONG Trident Trust has had a multilingual presence in Hong Kong for

Hong Kong Services p r o v i d i n g c o n f i d e n c e t h r o u g h p e r f o r m a n c e HOW TRIDENT TRUST CAN ASSIST YOU IN HONG KONG Trident Trust has had a multilingual presence in Hong Kong for

Legislative Council Panel on Financial Affairs. Proposed Enhancements to the Deposit Protection Scheme

CB(1)780/14-15(05) For discussion on 4 May 2015 Legislative Council Panel on Financial Affairs Proposed Enhancements to the Deposit Protection Scheme PURPOSE This paper briefs Members on the legislative

CB(1)780/14-15(05) For discussion on 4 May 2015 Legislative Council Panel on Financial Affairs Proposed Enhancements to the Deposit Protection Scheme PURPOSE This paper briefs Members on the legislative

Supplementary information on reform to betting duty system of horse race betting

Supplementary information on reform to betting duty system of horse race betting LC Paper No. CB(2)1880/04-05(01) (a) The turnover and betting duty of football betting, lotteries, horse race betting for

Supplementary information on reform to betting duty system of horse race betting LC Paper No. CB(2)1880/04-05(01) (a) The turnover and betting duty of football betting, lotteries, horse race betting for

A guide to Salaries Tax (2) which income is assessable and which deductions are allowable

which income is assessable and which deductions are allowable") A guide to Salaries Tax (2) which income is assessable and which deductions are allowable Foreword This guide helps you understand what income is assessable and what deductions are allowable under Salaries

A guide to Salaries Tax (2) which income is assessable and which deductions are allowable Foreword This guide helps you understand what income is assessable and what deductions are allowable under Salaries

Da Cheng CSI China Mainland Consumer Tracker* (Stock Code: 3071) (the Sub-Fund ) (*This is a synthetic ETF)

(the Sub-Fund ) (*This is a synthetic ETF)") THIS ANNOUNCEMENT AND NOTICE IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION AND DOES NOT CONSTITUTE AN INVITATION OR OFFER TO ACQUIRE, PURCHASE OR SUBSCRIBE FOR UNITS OF THE EXCHANGE TRADED FUND NAMED

THIS ANNOUNCEMENT AND NOTICE IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION AND DOES NOT CONSTITUTE AN INVITATION OR OFFER TO ACQUIRE, PURCHASE OR SUBSCRIBE FOR UNITS OF THE EXCHANGE TRADED FUND NAMED

立 法 會 Legislative Council

立 法 會 Legislative Council LC Paper No. CB(1)1338/05-06(09) Ref: CB1/PL/FA Panel on Financial Affairs Meeting on 4 May 2006 Background Brief on the policies on post-termination employment of senior executives

立 法 會 Legislative Council LC Paper No. CB(1)1338/05-06(09) Ref: CB1/PL/FA Panel on Financial Affairs Meeting on 4 May 2006 Background Brief on the policies on post-termination employment of senior executives

Stamp Duties Consolidation Act 1999

Stamp Duties Consolidation Act 1999 Part 9: Levies 9.1 SECTION 123B OF THE SDCA...1 9.2 SECTION 124 OF THE SDCA...2 9.3 SECTION 124B OF THE SDCA...2 9.4 SECTION 125 OF THE SDCA...2 9.5 SECTION 125A OF

Stamp Duties Consolidation Act 1999 Part 9: Levies 9.1 SECTION 123B OF THE SDCA...1 9.2 SECTION 124 OF THE SDCA...2 9.3 SECTION 124B OF THE SDCA...2 9.4 SECTION 125 OF THE SDCA...2 9.5 SECTION 125A OF

FSDC Research Paper No. 06. Synopsis Paper Proposing Tax Exemptions and Anti avoidance Measures on Private Equity Funds in the 2013 14 Budget

FSDC Research Paper No. 06 Synopsis Paper Proposing Tax Exemptions and Anti avoidance Measures on Private Equity s in the 2013 14 Budget November 2013 Synopsis Paper Proposing Tax Exemptions and Anti-avoidance

FSDC Research Paper No. 06 Synopsis Paper Proposing Tax Exemptions and Anti avoidance Measures on Private Equity s in the 2013 14 Budget November 2013 Synopsis Paper Proposing Tax Exemptions and Anti-avoidance

Doing business in Hong Kong

I. INTRODUCTION Doing business in Hong Kong Tim Drew Partner timdrew@robertwang.com Karen Yan Associate karenyan@robertwang.com Robert Wang Solicitors 1 On 1 July 1997, sovereignty over Hong Kong transferred

I. INTRODUCTION Doing business in Hong Kong Tim Drew Partner timdrew@robertwang.com Karen Yan Associate karenyan@robertwang.com Robert Wang Solicitors 1 On 1 July 1997, sovereignty over Hong Kong transferred

ACCA 香 港 分 會 2016/17 年 度 財 政 預 算 案 建 議. ACCA Hong Kong Budget Submission 2016/17

ACCA 香 港 分 會 2016/17 年 度 財 政 預 算 案 建 議 ACCA Hong Kong Budget Submission 2016/17 EXECUTIVE SUMMARY... 1 PROPOSALS... 4 1 Business Enabling Environment... 4 1.1 One-Belt-One-Road Initiative... 4 1.1.1 Implementation

ACCA 香 港 分 會 2016/17 年 度 財 政 預 算 案 建 議 ACCA Hong Kong Budget Submission 2016/17 EXECUTIVE SUMMARY... 1 PROPOSALS... 4 1 Business Enabling Environment... 4 1.1 One-Belt-One-Road Initiative... 4 1.1.1 Implementation

Paper in response to the issues raised in the Panel on Administration of Justice and Legal Services meeting on 26 April 2004

LC Paper No. CB(2)2582/03-04(01) Paper in response to the issues raised in the Panel on Administration of Justice and Legal Services meeting on 26 April 2004 Review of Professional Indemnity Scheme of

LC Paper No. CB(2)2582/03-04(01) Paper in response to the issues raised in the Panel on Administration of Justice and Legal Services meeting on 26 April 2004 Review of Professional Indemnity Scheme of

Macau SAR Tax Profile

Macau SAR Tax Profile Produced in conjunction with the KPMG Asia Pacific Tax Centre Updated: June 2015 Contents 1 Corporate Income Tax 1 2 Income Tax Treaties for the Avoidance of Double Taxation 5 3 Indirect

Macau SAR Tax Profile Produced in conjunction with the KPMG Asia Pacific Tax Centre Updated: June 2015 Contents 1 Corporate Income Tax 1 2 Income Tax Treaties for the Avoidance of Double Taxation 5 3 Indirect

Hong Kong Expands Existing Offshore Funds Tax Exemption to Benefit Private Equity Funds

Hong Kong Expands Existing Offshore Funds Tax Exemption to Benefit Private Equity Funds By Jeremy Leifer, Partner, Proskauer Rose, Hong Kong Introduction On 17 July, 2015 Hong Kong enacted legislation

Hong Kong Expands Existing Offshore Funds Tax Exemption to Benefit Private Equity Funds By Jeremy Leifer, Partner, Proskauer Rose, Hong Kong Introduction On 17 July, 2015 Hong Kong enacted legislation

The Hong Kong and Australian Pension Systems : An Overview

RP03/PLC The Hong Kong and Australian Pension Systems : 5 December 1997 Prepared by Miss Eva LIU Mr Joseph LEE Research and Library Services Division Provisional Legislative Council Secretariat 5th Floor,

RP03/PLC The Hong Kong and Australian Pension Systems : 5 December 1997 Prepared by Miss Eva LIU Mr Joseph LEE Research and Library Services Division Provisional Legislative Council Secretariat 5th Floor,

COUNTRY PROFILE HONG KONG

COUNTRY PROFILE HONG KONG 1. Economy and foreign investments 2. Tax Rates 3. Tax Treaties 4. Tax Credits 5. Property Tax 6. Excise Tax 7. Stamp Duty 8. Capital Duty 9. Estate Duty 10. Other duties, fees

COUNTRY PROFILE HONG KONG 1. Economy and foreign investments 2. Tax Rates 3. Tax Treaties 4. Tax Credits 5. Property Tax 6. Excise Tax 7. Stamp Duty 8. Capital Duty 9. Estate Duty 10. Other duties, fees

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES. Suggested Answers

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES Suggested Answers Level : Professional Subject : Hong Kong Taxation Diet : June 2007 The suggested answers are published for the purpose of assisting students

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES Suggested Answers Level : Professional Subject : Hong Kong Taxation Diet : June 2007 The suggested answers are published for the purpose of assisting students

DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 34 (REVISED) EXEMPTION FROM PROFITS TAX (INTEREST INCOME) ORDER 1998

EXEMPTION FROM PROFITS TAX (INTEREST INCOME) ORDER 1998") Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 34 (REVISED) EXEMPTION FROM PROFITS TAX (INTEREST INCOME) ORDER 1998 These notes are issued for the information and

Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 34 (REVISED) EXEMPTION FROM PROFITS TAX (INTEREST INCOME) ORDER 1998 These notes are issued for the information and

16 LC 37 2118ER A BILL TO BE ENTITLED AN ACT BE IT ENACTED BY THE GENERAL ASSEMBLY OF GEORGIA:

Senate Bill 347 By: Senator Bethel of the 54th A BILL TO BE ENTITLED AN ACT 1 2 3 4 5 6 To amend Title 33 of the Official Code of Georgia Annotated, relating to insurance, so as to provide for extensive

Senate Bill 347 By: Senator Bethel of the 54th A BILL TO BE ENTITLED AN ACT 1 2 3 4 5 6 To amend Title 33 of the Official Code of Georgia Annotated, relating to insurance, so as to provide for extensive

Open-ended Fund Companies New Initiative to Further Develop HK s Asset Management Industry

Open-ended Fund Companies New Initiative to Further Develop HK s Asset Management Industry Introduction Asset management has become increasingly prominent in the international financial landscape, and

Open-ended Fund Companies New Initiative to Further Develop HK s Asset Management Industry Introduction Asset management has become increasingly prominent in the international financial landscape, and

CLIENT FACT SHEET. If you are under age 65 you may make personal contributions to superannuation on your own behalf.

CLIENT FACT SHEET July 2010 Understanding superannuation and superannuation contributions Superannuation is an investment vehicle designed to assist Australians in saving for their retirement. The Government

CLIENT FACT SHEET July 2010 Understanding superannuation and superannuation contributions Superannuation is an investment vehicle designed to assist Australians in saving for their retirement. The Government

Legislative Council Panel on Manpower

LC Paper No. CB(2)958/09-10(03) For information on 23 February 2010 Legislative Council Panel on Manpower Review of the Levels of Compensation under the Employees Compensation Ordinance and the Pneumoconiosis

LC Paper No. CB(2)958/09-10(03) For information on 23 February 2010 Legislative Council Panel on Manpower Review of the Levels of Compensation under the Employees Compensation Ordinance and the Pneumoconiosis

1. Changes in PRC withholding income tax provisioning policy in relation to CSI RMB Income Fund and CSI RMB Short Maturity Bond Fund

和 CSI Alpha Fund Series (the Trust ) - CSI China-Hong Kong Leaders Fund - CSI RMB Income Fund - CSI RMB Short Maturity Bond Fund (each a "Fund", collectively the Funds ) CITIC Securities International

和 CSI Alpha Fund Series (the Trust ) - CSI China-Hong Kong Leaders Fund - CSI RMB Income Fund - CSI RMB Short Maturity Bond Fund (each a "Fund", collectively the Funds ) CITIC Securities International

OECD-Asia Regional Seminar: Enhancing Transparency and Monitoring of Insurance Markets

OECD-Asia Regional Seminar: Enhancing Transparency and Monitoring of Insurance Markets Regional Experience: Hong Kong Office of the Commissioner of Insurance Financial Services and the Treasury Bureau

OECD-Asia Regional Seminar: Enhancing Transparency and Monitoring of Insurance Markets Regional Experience: Hong Kong Office of the Commissioner of Insurance Financial Services and the Treasury Bureau

Tax Compliance in Greater China

m is,cch a Wolters Kiuwer business Tax Compliance in Greater China China, Hong Kong and Taiwan B363170 EXPANDED TABLE OF CONTENTS IX Chapter 1 INVESTMENT FRAMEWORK CHINA Introduction 4 Overview of the

m is,cch a Wolters Kiuwer business Tax Compliance in Greater China China, Hong Kong and Taiwan B363170 EXPANDED TABLE OF CONTENTS IX Chapter 1 INVESTMENT FRAMEWORK CHINA Introduction 4 Overview of the

British Virgin Islands Insurance Companies

British Virgin Islands Insurance Companies Foreword This memorandum has been prepared for the assistance of those who are considering the formation of insurance companies in the British Virgin Islands.

British Virgin Islands Insurance Companies Foreword This memorandum has been prepared for the assistance of those who are considering the formation of insurance companies in the British Virgin Islands.

LegCo Panel on Manpower. A proposal to make mesothelioma a compensable disease under the Pneumoconiosis (Compensation) Ordinance

Ordinance") LC Paper No. CB(2)310/07-08(03) For discussion on 15 November 2007 LegCo Panel on Manpower A proposal to make mesothelioma a compensable disease under the Pneumoconiosis (Compensation) Ordinance Purpose

LC Paper No. CB(2)310/07-08(03) For discussion on 15 November 2007 LegCo Panel on Manpower A proposal to make mesothelioma a compensable disease under the Pneumoconiosis (Compensation) Ordinance Purpose

services system Reports Act 1988 (Cth) Australia has a sophisticated and stable banking and financial services system.

Australia has a sophisticated and stable banking and financial services system.") FINANCIAL SERVICES Australia has a sophisticated and stable banking and financial services system Australia has a sophisticated and stable banking and financial services system. The banking system is prudentially

FINANCIAL SERVICES Australia has a sophisticated and stable banking and financial services system Australia has a sophisticated and stable banking and financial services system. The banking system is prudentially

Introduction individual 1 April 1998 1 July 1998

Introduction 1. This booklet provides a brief explanation of how The Arrangement between the Mainland of China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation on Income

Introduction 1. This booklet provides a brief explanation of how The Arrangement between the Mainland of China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation on Income

DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 14 (REVISED) PROPERTY TAX

PROPERTY TAX") Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 14 (REVISED) PROPERTY TAX These notes are issued for the information of taxpayers and their tax representatives. They

Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 14 (REVISED) PROPERTY TAX These notes are issued for the information of taxpayers and their tax representatives. They

Commonly Asked Questions on Departmental Interpretation and Practice Notes ( DIPN ) No. 40 Profits Tax: Prepaid or Deferred Revenue Expenses

No. 40 Profits Tax: Prepaid or Deferred Revenue Expenses") Commonly Asked Questions on Departmental Interpretation and Practice Notes ( DIPN ) No. 40 Profits Tax: Prepaid or Deferred Revenue Expenses Foreword The following questions and answers have been prepared

Commonly Asked Questions on Departmental Interpretation and Practice Notes ( DIPN ) No. 40 Profits Tax: Prepaid or Deferred Revenue Expenses Foreword The following questions and answers have been prepared

Subcommittee on Proposed Resolutions under Section 29 of the Public Finance Ordinance (Cap. 2) and Section 3 of the Loans Ordinance (Cap.

and Section 3 of the Loans Ordinance (Cap.") CB(1)1662/08-09(02) Subcommittee on Proposed Resolutions under Section 29 of the Public Finance Ordinance (Cap. 2) and Section 3 of the Loans Ordinance (Cap. 61) Supplementary Information Purpose This

CB(1)1662/08-09(02) Subcommittee on Proposed Resolutions under Section 29 of the Public Finance Ordinance (Cap. 2) and Section 3 of the Loans Ordinance (Cap. 61) Supplementary Information Purpose This

CHAPTER 26.1-35 STANDARD VALUATION LAW

CHAPTER 26.1-35 STANDARD VALUATION LAW 26.1-35-00.1. (Contingent effective date - See note) Definitions. In this chapter, the following definitions apply on or after the operative date of the valuation

CHAPTER 26.1-35 STANDARD VALUATION LAW 26.1-35-00.1. (Contingent effective date - See note) Definitions. In this chapter, the following definitions apply on or after the operative date of the valuation

Legislative Council Panel on Health Services Subcommittee on Health Protection Scheme

LC Paper No. CB(2)855/13-14(02) For information on 18 February 2014 PURPOSE Legislative Council Panel on Health Services Subcommittee on Health Protection Scheme Detailed Proposal on the Setting up of

LC Paper No. CB(2)855/13-14(02) For information on 18 February 2014 PURPOSE Legislative Council Panel on Health Services Subcommittee on Health Protection Scheme Detailed Proposal on the Setting up of

Enhancing Life Insurance Regulatory Regimes in ASIA

International Symposium Enhancing Life Insurance Regulatory Regimes in ASIA Multilateral agencies and regulatory changes in life insurance and pension systems Mr H.Y.Mok, Assistant Commissioner of Insurance,

International Symposium Enhancing Life Insurance Regulatory Regimes in ASIA Multilateral agencies and regulatory changes in life insurance and pension systems Mr H.Y.Mok, Assistant Commissioner of Insurance,

LEGISLATIVE COUNCIL BRIEF. Resolution of the Legislative Council under Section 48A of the Employees Compensation Ordinance, Cap 282

LEGISLATIVE COUNCIL BRIEF Resolution of the Legislative Council under Section 48A of the Employees Compensation Ordinance, Cap 282 Resolution of the Legislative Council under Section 40 of the Pneumoconiosis

LEGISLATIVE COUNCIL BRIEF Resolution of the Legislative Council under Section 48A of the Employees Compensation Ordinance, Cap 282 Resolution of the Legislative Council under Section 40 of the Pneumoconiosis

A guide to Salaries Tax for people coming to work in Hong Kong. HK or non-hk office HK or non-hk employment the days-in-days-out basis of assessment

A guide to Salaries Tax for people coming to work in Hong Kong HK or non-hk office HK or non-hk employment the days-in-days-out basis of assessment Foreword This leaflet provides general guidance to people

A guide to Salaries Tax for people coming to work in Hong Kong HK or non-hk office HK or non-hk employment the days-in-days-out basis of assessment Foreword This leaflet provides general guidance to people

A Brief Guide to Personal Assessment. Whether Tax may be Reduced through Election for Personal Assessment

A Brief Guide to Personal Assessment Whether Tax may be Reduced through Election for Personal Assessment Foreword This leaflet explains 1. what Personal Assessment is, 2. how Personal Assessment may reduce

A Brief Guide to Personal Assessment Whether Tax may be Reduced through Election for Personal Assessment Foreword This leaflet explains 1. what Personal Assessment is, 2. how Personal Assessment may reduce

Hong Kong * 505 IBFD. * Contributed by Ying Zhang, IBFD.

* 1. Tax Authority And Law The tax administration agency in Hong Kong is the Inland Revenue Department of Hong Kong (HKIRD). Hong Kong does not have specific legislation to regulate transfer pricing although

* 1. Tax Authority And Law The tax administration agency in Hong Kong is the Inland Revenue Department of Hong Kong (HKIRD). Hong Kong does not have specific legislation to regulate transfer pricing although

Insurance Companies (Amendment) Bill 2014 Debate and voting arrangements

Bill 2014 Debate and voting arrangements") LC Paper No. CB(3) 852/14-15(01) Insurance Companies (Amendment) Bill 2014 Debate and voting arrangements First debate : Clauses with no amendment Clauses 1 to 4, 6 to 10, 12, 13, 14, 16 to 22, 27, 28,

LC Paper No. CB(3) 852/14-15(01) Insurance Companies (Amendment) Bill 2014 Debate and voting arrangements First debate : Clauses with no amendment Clauses 1 to 4, 6 to 10, 12, 13, 14, 16 to 22, 27, 28,

RECENT INCOME TAX CHANGES

RECENT INCOME TAX CHANGES Increased Medicare Levy Low Income Thresholds The Medicare Levy low-income thresholds for families and dependent child-student component of the threshold have been changed to

RECENT INCOME TAX CHANGES Increased Medicare Levy Low Income Thresholds The Medicare Levy low-income thresholds for families and dependent child-student component of the threshold have been changed to

Briefing for Bills Committee

CB(1)504/12-13(01) Briefing for Bills Committee Inland Revenue and Stamp Duty Legislation (Alternative Bond Schemes) (Amendment) Bill 2012 1 Why developing Islamic finance? Among the fastest growing segments

CB(1)504/12-13(01) Briefing for Bills Committee Inland Revenue and Stamp Duty Legislation (Alternative Bond Schemes) (Amendment) Bill 2012 1 Why developing Islamic finance? Among the fastest growing segments

003.02 Act means Intergovernmental Risk Management Act.

Title 210 - NEBRASKA DEPARTMENT OF INSURANCE Chapter 85 - GROUP HEALTH, DENTAL, ACCIDENT, AND LIFE INSURANCE UNDER THE INTERGOVERNMENTAL RISK MANAGEMENT ACT 001. Authority. This rule is promulgated pursuant

Title 210 - NEBRASKA DEPARTMENT OF INSURANCE Chapter 85 - GROUP HEALTH, DENTAL, ACCIDENT, AND LIFE INSURANCE UNDER THE INTERGOVERNMENTAL RISK MANAGEMENT ACT 001. Authority. This rule is promulgated pursuant

INLAND REVENUE BOARD OF REVIEW DECISIONS. Case No. D51/88

Case No. D51/88 Profits tax insurance company (non-life) interest received from offshore deposits whether subject to profits tax s 23A of the Inland Revenue Ordinance. Profits tax insurance company (non-life)

Case No. D51/88 Profits tax insurance company (non-life) interest received from offshore deposits whether subject to profits tax s 23A of the Inland Revenue Ordinance. Profits tax insurance company (non-life)

DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 20 (REVISED) MUTUAL FUNDS, UNIT TRUSTS AND SIMILAR INVESTMENT SCHEMES

MUTUAL FUNDS, UNIT TRUSTS AND SIMILAR INVESTMENT SCHEMES") Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 20 (REVISED) MUTUAL FUNDS, UNIT TRUSTS AND SIMILAR INVESTMENT SCHEMES These notes are issued for the information of

Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 20 (REVISED) MUTUAL FUNDS, UNIT TRUSTS AND SIMILAR INVESTMENT SCHEMES These notes are issued for the information of

DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 35 (REVISED) CONCESSIONARY DEDUCTIONS: SECTIONS 26E AND 26F HOME LOAN INTEREST

CONCESSIONARY DEDUCTIONS: SECTIONS 26E AND 26F HOME LOAN INTEREST") Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 35 (REVISED) CONCESSIONARY DEDUCTIONS: SECTIONS 26E AND 26F HOME LOAN INTEREST These notes are issued for the information

Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 35 (REVISED) CONCESSIONARY DEDUCTIONS: SECTIONS 26E AND 26F HOME LOAN INTEREST These notes are issued for the information

Inland Revenue (Amendment) Bill 2015. Extending Profits Tax Exemption for Offshore Funds to Private Equity Funds

Bill 2015. Extending Profits Tax Exemption for Offshore Funds to Private Equity Funds") CB(1)800/14-15(01) Inland Revenue (Amendment) Bill 2015 Extending Profits Tax Exemption for Offshore Funds to Private Equity Funds 28 April 2015 Asset management industry in Hong Kong Combined fund management

CB(1)800/14-15(01) Inland Revenue (Amendment) Bill 2015 Extending Profits Tax Exemption for Offshore Funds to Private Equity Funds 28 April 2015 Asset management industry in Hong Kong Combined fund management

[05.05.19] Payments on Termination of an Office or Employment or a Change in its Functions

![[05.05.19] Payments on Termination of an Office or Employment or a Change in its Functions](/thumbs/26/8602141.jpg "[05.05.19] Payments on Termination of an Office or Employment or a Change in its Functions") [05.05.19] Payments on Termination of an Office or Employment or a Change in its Functions Contents Sections 123 and 201, and Schedule 3 of the Taxes Consolidation Act, 1997 Updated April 2014 1. Introduction...3

[05.05.19] Payments on Termination of an Office or Employment or a Change in its Functions Contents Sections 123 and 201, and Schedule 3 of the Taxes Consolidation Act, 1997 Updated April 2014 1. Introduction...3

Mexico. Rodolfo Trampe, Jorge Díaz, José Palomar and Carlos López. Von Wobeser y Sierra, S.C.

Mexico Rodolfo Trampe, Jorge Díaz, José Palomar and Carlos López Market overview 1 What kinds of outsourcing take place in your jurisdiction? In Mexico, a subcontracting regime (understood as the regime

Mexico Rodolfo Trampe, Jorge Díaz, José Palomar and Carlos López Market overview 1 What kinds of outsourcing take place in your jurisdiction? In Mexico, a subcontracting regime (understood as the regime

Double Taxation Relief

CHAPTER 15 Double Taxation Relief Some Key Points Bilateral relief Under this method, the Government of two countries can enter into an agreement to provide relief against double taxation by mutually working

CHAPTER 15 Double Taxation Relief Some Key Points Bilateral relief Under this method, the Government of two countries can enter into an agreement to provide relief against double taxation by mutually working

MINIMUM SURRENDER VALUES AND PAID-UP VALUES

MARCH 2002 Actuarial Standard 4.02 MINIMUM SURRENDER VALUES AND PAID-UP VALUES Life Insurance Actuarial Standards Board TABLE OF CONTENTS INTRODUCTION PAGE The Standard 2 Application of the Surrender Value

MARCH 2002 Actuarial Standard 4.02 MINIMUM SURRENDER VALUES AND PAID-UP VALUES Life Insurance Actuarial Standards Board TABLE OF CONTENTS INTRODUCTION PAGE The Standard 2 Application of the Surrender Value

US Foreign Account Tax Compliance Act Intergovernmental Agreement. Frequently Asked Questions

US Foreign Account Tax Compliance Act Intergovernmental Agreement Frequently Asked Questions This document aims to provide background information regarding the intergovernmental agreement ( IGA ) to be

US Foreign Account Tax Compliance Act Intergovernmental Agreement Frequently Asked Questions This document aims to provide background information regarding the intergovernmental agreement ( IGA ) to be

CPD Information Sheet (Nov 2014)

") CPD Information Sheet (Nov 2014) Insurance Intermediaries Quality Assurance Scheme Continuing Professional Development Programme The Programme 1. Insurance agents/brokers, their chief executives/responsible

CPD Information Sheet (Nov 2014) Insurance Intermediaries Quality Assurance Scheme Continuing Professional Development Programme The Programme 1. Insurance agents/brokers, their chief executives/responsible

Paper F6 (HKG) Taxation (Hong Kong) Tuesday 2 June 2015. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (Hong Kong) Tuesday 2 June 2015. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (Hong Kong) Tuesday 2 June 2015 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections: Section A ALL 15 questions

Fundamentals Level Skills Module Taxation (Hong Kong) Tuesday 2 June 2015 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections: Section A ALL 15 questions

Response of the Administration. I. Employees Compensation Insurance Market-related Matters

Response of the Administration CB(1)1742/02-03(01) I. Employees Compensation Insurance Market-related Matters (a) Soaring premium As explained in the Information Paper entitled Insurance coverage for various

Response of the Administration CB(1)1742/02-03(01) I. Employees Compensation Insurance Market-related Matters (a) Soaring premium As explained in the Information Paper entitled Insurance coverage for various

How Canada Taxes Foreign Income

- 1 - How Canada Taxes Foreign Income (Summary) Purpose of the book The purpose of writing this book, entitled How Canada Taxes Foreign Income is particularly for the benefit of foreign tax lawyers, accountants,

- 1 - How Canada Taxes Foreign Income (Summary) Purpose of the book The purpose of writing this book, entitled How Canada Taxes Foreign Income is particularly for the benefit of foreign tax lawyers, accountants,

HONG KONG Corporate information:

HONG KONG Corporate information: Hong Kong is the richest city in China, its economy is one of the most liberal in the world. It is a financial and commercial hub of global significance. Hong Kong is a

HONG KONG Corporate information: Hong Kong is the richest city in China, its economy is one of the most liberal in the world. It is a financial and commercial hub of global significance. Hong Kong is a

CHAPTER 4 - TAX PREFERENCES FOR SUPERANNUATION AND LIFE INSURANCE SAVINGS

45 CHAPTER 4 - TAX PREFERENCES FOR SUPERANNUATION AND LIFE INSURANCE SAVINGS 4.1 Introduction In general, superannuation and life insurance have not been subject to the normal income tax treatment for

45 CHAPTER 4 - TAX PREFERENCES FOR SUPERANNUATION AND LIFE INSURANCE SAVINGS 4.1 Introduction In general, superannuation and life insurance have not been subject to the normal income tax treatment for

Property and casualty insurance companies are those that insure the assets of the insured party.

International comparison of insurance taxation Argentina General insurance overview Definition Definition of property and casualty insurance company Property and casualty insurance companies are those

International comparison of insurance taxation Argentina General insurance overview Definition Definition of property and casualty insurance company Property and casualty insurance companies are those

TAXATION AND FOREIGN EXCHANGE

TAXATION OF EQUITY HOLDERS The following is a summary of certain PRC and Hong Kong tax consequences of the ownership of H Shares by an investor that purchases such H Shares in the Global Offering and holds

TAXATION OF EQUITY HOLDERS The following is a summary of certain PRC and Hong Kong tax consequences of the ownership of H Shares by an investor that purchases such H Shares in the Global Offering and holds

ITEM FOR FINANCE COMMITTEE

For discussion on 7 December 2012 FCR(2012-13)59 ITEM FOR FINANCE COMMITTEE HEAD 94 LEGAL AID DEPARTMENT Subhead 700 General non-recurrent New Item Injection into the Supplementary Legal Aid Fund Members

For discussion on 7 December 2012 FCR(2012-13)59 ITEM FOR FINANCE COMMITTEE HEAD 94 LEGAL AID DEPARTMENT Subhead 700 General non-recurrent New Item Injection into the Supplementary Legal Aid Fund Members

NEW ZEALAND International Comparison of Insurance Taxation January 2005

International Comparison of Insurance International Comparison of Insurance New Zealand General Insurance 1 Definition Definition of property and casualty insurance company A company to which insurance

International Comparison of Insurance International Comparison of Insurance New Zealand General Insurance 1 Definition Definition of property and casualty insurance company A company to which insurance

An Overview of Florida s Insurance Premium Tax

An Overview of Florida s Insurance Premium Tax Report Number 2007-122 October 2006 Prepared for The Florida Senate Prepared by Committee on Finance and Tax Table of Contents Summary... separate document

An Overview of Florida s Insurance Premium Tax Report Number 2007-122 October 2006 Prepared for The Florida Senate Prepared by Committee on Finance and Tax Table of Contents Summary... separate document

Cayman Islands Insurance and Reinsurance Companies

Cayman Islands Insurance and Reinsurance Companies Introduction All companies carrying on insurance business in or from within the Cayman Islands must be licensed by the Cayman Islands Monetary Authority

Cayman Islands Insurance and Reinsurance Companies Introduction All companies carrying on insurance business in or from within the Cayman Islands must be licensed by the Cayman Islands Monetary Authority

Public Consultation on New Strategy of Innovation and Technology Development

Public Consultation on New Strategy of Innovation and Technology Development Preamble Over the years, the Federation has been a strong advocate of promoting Hong Kong s innovation and technology development.

Public Consultation on New Strategy of Innovation and Technology Development Preamble Over the years, the Federation has been a strong advocate of promoting Hong Kong s innovation and technology development.

DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 13 (REVISED) PROFITS TAX TAXATION OF INTEREST RECEIVED

PROFITS TAX TAXATION OF INTEREST RECEIVED") Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 13 (REVISED) PROFITS TAX TAXATION OF INTEREST RECEIVED These notes are issued for the information and guidance of

Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 13 (REVISED) PROFITS TAX TAXATION OF INTEREST RECEIVED These notes are issued for the information and guidance of

CONSULTATION PAPER. Insurance (Fees) Regulations 2013 Registered Schemes Administrators (Fees) Order 2013

Regulations 2013 Registered Schemes Administrators (Fees) Order 2013") CONSULTATION PAPER Insurance (Fees) Regulations 2013 Registered Schemes Administrators (Fees) Order 2013 This document is relevant to all entities regulated by the Insurance and Pensions Authority under

CONSULTATION PAPER Insurance (Fees) Regulations 2013 Registered Schemes Administrators (Fees) Order 2013 This document is relevant to all entities regulated by the Insurance and Pensions Authority under

TAXATION OF INCOME FROM SALARY TAX YEAR 2012. (1 st July 11-30 th June 12)

") . (1 st July 11-30 th June 12) The Computation of Tax of a Salaried Person has been defined under section 12, 13 and 14 of the Income Tax Ordinance, 2001 read with rules 2 to 7 of the Income Tax Rules,

. (1 st July 11-30 th June 12) The Computation of Tax of a Salaried Person has been defined under section 12, 13 and 14 of the Income Tax Ordinance, 2001 read with rules 2 to 7 of the Income Tax Rules,

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO. Update as of 15 February 2013

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO Report 1 issued on September 2011, validated by the Central Bank of Trinidad and Tobago Update as of 15 February 2013 1 This

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO Report 1 issued on September 2011, validated by the Central Bank of Trinidad and Tobago Update as of 15 February 2013 1 This

Building the Entrepreneurs Colony: Hong Kong Vs Singapore By Cora Cheung

Building the Entrepreneurs Colony: Hong Kong Vs Singapore By Cora Cheung Start-ups have been the buzz words in recent years and it is believed to be the driver of the next economic boom; sharing the spotlight

Building the Entrepreneurs Colony: Hong Kong Vs Singapore By Cora Cheung Start-ups have been the buzz words in recent years and it is believed to be the driver of the next economic boom; sharing the spotlight

Pilot Programme to Enhance Talent Training for the Insurance Sector and the Asset and Wealth Management Sector

Financial Services and the Treasury Bureau Financial Services Branch CB(1)931/14-15(02) Pilot Programme to Enhance Talent Training for the Insurance Sector and the Asset and Wealth Management Sector Legislative

Financial Services and the Treasury Bureau Financial Services Branch CB(1)931/14-15(02) Pilot Programme to Enhance Talent Training for the Insurance Sector and the Asset and Wealth Management Sector Legislative

Solvency Standard for Captive Insurers Transacting Non-life Insurance Business 2014

Solvency Standard for Captive Insurers Transacting Non-life Insurance Business 2014 Prudential Supervision Department Issued: December 2014 2 1. Introduction 1.1. Authority 1. This solvency standard is

Solvency Standard for Captive Insurers Transacting Non-life Insurance Business 2014 Prudential Supervision Department Issued: December 2014 2 1. Introduction 1.1. Authority 1. This solvency standard is

Legislative Council Panel on Transport and Panel on Financial Affairs

LC Paper No. CB(2)150/11-12(02) For information on 31 October 2011 Legislative Council Panel on Transport and Panel on Financial Affairs Joint Subcommittee on Issues Relating to Insurance Coverage for

LC Paper No. CB(2)150/11-12(02) For information on 31 October 2011 Legislative Council Panel on Transport and Panel on Financial Affairs Joint Subcommittee on Issues Relating to Insurance Coverage for

立 法 會 Legislative Council

立 法 會 Legislative Council LC Paper No. CB(1)108/14-15 (These minutes have been seen by the ) Ref : CB1/BC/10/13 Bills Committee on Mandatory Provident Fund Schemes (Amendment) Bill 2014 Minutes of second

立 法 會 Legislative Council LC Paper No. CB(1)108/14-15 (These minutes have been seen by the ) Ref : CB1/BC/10/13 Bills Committee on Mandatory Provident Fund Schemes (Amendment) Bill 2014 Minutes of second

Hong Kong Companies Accounting Issues & Declaration of Offshore Income. TAI Kwok Yin Aileen ACCA (HK)

") Hong Kong Companies Accounting Issues & Declaration of Offshore Income TAI Kwok Yin Aileen ACCA (HK) 1 Contents I. Accounting Issues of Hong Kong Companies When the company need to prepare the accounts

Hong Kong Companies Accounting Issues & Declaration of Offshore Income TAI Kwok Yin Aileen ACCA (HK) 1 Contents I. Accounting Issues of Hong Kong Companies When the company need to prepare the accounts

Legislative Council Panel on Health Services Subcommittee on Health Protection Scheme

LC Paper No. CB(2)855/13-14(03) For information on 18 February 2014 PURPOSE Legislative Council Panel on Health Services Subcommittee on Health Protection Scheme Proposed Claims Dispute Resolution Mechanism

LC Paper No. CB(2)855/13-14(03) For information on 18 February 2014 PURPOSE Legislative Council Panel on Health Services Subcommittee on Health Protection Scheme Proposed Claims Dispute Resolution Mechanism

58-58-50. Standard Valuation Law.

58-58-50. Standard Valuation Law. (a) This section shall be known as the Standard Valuation Law. (b) Each year the Commissioner shall value or cause to be valued the reserve liabilities ("reserves") for

58-58-50. Standard Valuation Law. (a) This section shall be known as the Standard Valuation Law. (b) Each year the Commissioner shall value or cause to be valued the reserve liabilities ("reserves") for

Thailand. Thailand General Insurance. International Comparison of Insurance Taxation* May 2009. *connectedthinking. Definition Accounting Taxation

Thailand International Comparison of Insurance * May 2009 Thailand General Insurance Definition Definition of property and casualty insurance company Companies having been licensed to engage in the non-life

Thailand International Comparison of Insurance * May 2009 Thailand General Insurance Definition Definition of property and casualty insurance company Companies having been licensed to engage in the non-life

LEGISLATIVE COUNCIL BRIEF. Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Chapter 615)

Ordinance (Chapter 615)") File Ref: G13/21C LEGISLATIVE COUNCIL BRIEF Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Chapter 615) Anti-Money Laundering and Counter-Terrorist Financing

File Ref: G13/21C LEGISLATIVE COUNCIL BRIEF Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Chapter 615) Anti-Money Laundering and Counter-Terrorist Financing

Insurance Newsletter Number 03 Year 2004

Insurance Newsletter Number 03 Year 2004 Solvency I Directives Introduction The Solvency I Directives for life insurers (2002/12/EC) and non-life insurers (2002/13/EC) update some of the requirements of

Insurance Newsletter Number 03 Year 2004 Solvency I Directives Introduction The Solvency I Directives for life insurers (2002/12/EC) and non-life insurers (2002/13/EC) update some of the requirements of

Comparison of Provisions and Schemes of Employees Protection in Hong Kong and other Jurisdictions

LC Paper No. CB(1)259/01-02(06) Comparison of Provisions and Schemes of Employees Protection in Hong Kong and other Jurisdictions Severance payment/ 1 Hong Kong Severance payment (for dismissal by reason

LC Paper No. CB(1)259/01-02(06) Comparison of Provisions and Schemes of Employees Protection in Hong Kong and other Jurisdictions Severance payment/ 1 Hong Kong Severance payment (for dismissal by reason