Accounts. Checking. Name Block Date

|

|

|

- Diane Hubbard

- 10 years ago

- Views:

Transcription

1 Name Block Date Checking Accounts Tasks Checking Accounts Notes... page 5 Debit Card Questions... page 7 Writing a Check Activity... page 8 Checking Simulation #1... pages 9-19 Checking Simulation #2... pages Responsible Checking Project... page 30 1

2 Introduction to Checking Accounts People generally use checking accounts to store money in the short term until it is needed for day to day expenses like gas or groceries or to pay bills, and they can usually deposit or withdraw any amount of money in their account as many times as they like. Checking accounts also come with convenient ways to deposit and withdraw money from the account, such as checks and ATM cards. However, people with checking accounts must be careful when using them, since some banks charge fees for certain actions, such as using another bank's ATM, withdrawing more money from your account than the amount in it, or not maintaining a minimum balance. On the other hand, a savings account is used to set money aside for use in the future and allow the money to collect interest. Many people regularly place some of their money into savings accounts rather than spending it in order to achieve financial goals, such as buying the latest gadget or game, without having to go into debt to do it. Compound interest is interest paid on both the money you put into your account and the interest already earned. For example, if you put $100 into an account that earns 10% interest, you will initially earn $10, which will result in a total account balance of $110. The next time your account earns 10% it will be based on $110 instead of just $100, giving you a total account balance of $121. You can earn even more in compound interest if you stretch to put as much money as you can into your account and leave it untouched. See the chart below, which is based on a savings account started with $50 and earning interest at a rate of 3.5% each month. If you add just $10 each month, the account can grow nicely to $714 after five years. If you instead put in a slightly higher amount $15 each month you'd have a balance of $1,042 after five years. But if you had increased your deposits to $50 a month, those extra dollars plus the compounding of interest would give you a balance of $3,333 after five years. There are many banks that offer special accounts for kids and teens, so talk to your parents if you'd like to open an account of your own and start learning how to manage money. But you don't need a bank account to start the habit of saving a simple piggy bank will do! 2

3 Choose the Account That Is Best for You When it comes to finding a safe place to put your money, there are a lot of options. Savings accounts, checking accounts, certificates of deposit and money market accounts are popular choices. Each has different rules and benefits that fit different needs. When choosing the one that is right for you, consider: 1. Minimum deposit requirements- Some accounts can only be set up with a minimum dollar amount. If your account goes below the minimum the bank may not pay you interest on the money you deposited and you may be charged extra fees. 2. Limits on withdrawals- Can you take money out whenever you want? Are there any penalties for doing so? 3. Interest- How much (if anything) is paid and when: Daily, monthly, quarterly, yearly? 4. Deposit insurance- Make sure your bank is a member of the Federal Deposit Insurance Corporation. This organization protects the money in your checking and savings accounts, certificates of deposit and IRA accounts up to $250, Credit unions- A credit union is a nonprofit, cooperative financial institution owned and run by its members. Like the FDIC does for banks, the National Credit Union Share Insurance Fund insures a person's savings up to $250, Convenience- How easy is it to put money in and take it out? Are there tellers or ATM machines close to where you work and live? Or would you receive most of your service via the telephone or Internet? If you are considering a checking account or another type of account with check-writing privileges, add these items to your list of things to think about: Number of checks- Is there a maximum number of checks you can write per month without incurring a charge? Check fees- Is there a monthly fee for the account or a charge for each check you write? Holds on checks- Is there a waiting period for checks to clear before you can withdraw the money from your account? Overdrafts- If you write a check for more money than you have in your account, what happens? You may be able to link your checking account to a savings account to protect yourself. Debit card fees- Are there fees for using your debit card? strong>account fees- Banks can charge fees on your checking or savings account to cover things like maintenance, withdrawals, or minimum balance rules. However, the bank must inform you of the fees up front as part of your account agreement and notify you when changes occur. Practices vary from bank to bank, but each must inform you of the fee change on your statement, in a separate letter, or in a pamphlet. The Federal Reserve has more information about account fees. Bounced checks- It s your responsibility to have sufficient funds in your account to cover the checks you write. If you try to cash a check, withdraw money, or use your debit card for an amount greater than the amount of money in your account, you can face a bounced check or overdraft fee. Your bank may pay for the item, but charge you a fee or deny the purchase and still charge you a fee. In addition, the business to which you wrote the check may charge you an additional returned check fee. Bounced checks can also blemish your credit record, so you may want to talk to your bank about overdraft protection. 3

4 Debit Cards Definition: Debit cards are similar to credit cards, except debit cards only allow you to spend money that you already have -- the money comes out of a checking account linked to the card. Debit cards do not increase your debt burden like credit cards do, although it is possible to borrow small amounts as part of an overdraft line of credit. Where to Use Debit Cards You can use debit cards very much like a plain old credit card. Many retailers will allow you to use a debit card at checkout just like a credit card. You just swipe it and you're done. However, sometimes you have to let the retailer know you're using a debit card instead of credit. You can choose to have your purchase processed as a "debit" or "credit" transaction. Although debit cards can be used almost anywhere, think before you swipe. That card goes directly to your checking account. If your card information is stolen, thieves can drain your account (which will make it difficult to pay expenses). You are somewhat protected against fraud, but avoiding trouble in the first place is much easier. Be especially careful using your debit card online. Debit Cards and the ATM For some people, the main reason to have a debit card is to use it at an ATM. For a while, banks issued "ATM Cards" which were only useful if you were standing in front of an ATM trying to take out cash. Eventually, banks started to add more features so that a debit card can now be used at almost any location. Prepaid Debit Cards Traditionally, debit cards are part of your checking account; they allow you to spend money electronically instead of writing a check. However, newer prepaid cards allow you to pay with plastic (or by punching in your account number online) without the need for a checking account. Many cards can be used without any approval or credit check, and they help you avoid going into debt because you can only spend what you load onto the card. Debit Card Rewards Some debit cards are part of "rewards" programs. Using your card can lead to discounts or accumulating points (which can then be used for travel, gifts, and other goods). If you know how you'll use your debit card, and you know where you plan to spend money in the future, it may pay to pick a debit card that will save you money or help you enjoy perks. 4

5 Checking Accounts Notes Use the information from the articles entitled Introduction to Checking Accounts, Choose the Account That Is Best for You, and Debit Cards to define these terms and answer the questions. Purpose of Checking Account Deposit Vocabulary Withdraw ATM Minimum Balance Interest Minimum Deposit Requirement Deposit Insurance Credit Union Check Check Fee Bounced Check Debit Card Debit Card Fee Overdraft How can you earn money on the money in your checking or savings account? When will you use a debit card? Questions What is the difference between a debit card and a prepaid debit card? 5

6 9 best practices for debit card use Debit cards are useful financial tools as they offer the convenience of plastic -- without the risk of racking up debt. Just like credit cards, though, debit cards can lead to trouble if not used wisely. Here are experts' nine best tips for managing your debit card. 1. Know yourself. Do you have bad money habits, such as not balancing your checkbook, losing receipts and getting hit with overdraft charges? If so, avoid pulling out your debit card every time you crave a latte, and pay cash for everyday purchases. "The debit card is a great tool, but it's not for everyone," says Susan Tiffany, director of consumer periodicals for the Credit Union National Association. "Just ask yourself upfront: 'Am I the kind of person who's going to run into trouble with this?'" 2. Keep track of transactions. Keep good records to avoid bounced checks, overdraft fees and stress. "Write down every purchase right away in your check register," says Gail Cunningham, spokeswoman for the National Foundation for Credit Counseling. This goes double for those who have joint accounts, according to Catherine Williams, vice president of financial literacy for Money Management International, a national credit counseling firm. "It's really important that you both record all your transactions and be in close communication with each other," Williams says. 3. Don't automatically "opt in." This summer, new federal regulations prohibit banks from allowing customers to overdraft with debit cards unless they opt in. Banks are urging customers to do so, but Leslie Parrish, a senior researcher at the Center for Responsible Lending, says 80 percent of consumers would rather have their card declined at the checkout counter than get hit with a $30 or more overdraft fee. "Your debit card could become your most expensive credit card if you don't have enough money in your account and are extended credit," Parrish says. Instead of opting in, Linda Sherry, national priorities director for Consumer Action, recommends you set up your own overdraft protection by linking your card to a savings account or a line of credit. 4. Watch out for holds. Before using your debit card to make hotel reservations, rent a car or even buy gas, ask whether any holds will be placed on your account -- and how much and how long those funds will be held. If you don't want your money tied up for what could be as long as a month, consider using a credit card for hotels and rentals instead, Tiffany recommends. (Or, make the reservation with a credit card and pay the final bill with your debit card.) "If you're traveling and don't have the balance to cover the holds they've placed, you could go to buy dinner and have your card declined," Tiffany says. Your debit card could become your most expensive credit card if you don't have enough money in your account and are extended credit. -- Leslie Parrish Center for Responsible Lending 5. Know the difference: debit versus credit. You've just swiped your card to pay for a new pair of jeans, and the clerk asks, "Debit or credit?" If you choose "debit" and punch in your PIN, the transaction happens online and is processed right away. If you choose "credit" and sign instead, the transaction may hit your account several days later, leaving you to think you have more money in your account when you don't. 6

7 6. Be smart about choosing a PIN number. Try to choose a random combination of numbers that you can remember easily, and avoid choosing a PIN that a criminal could guess, such as your initials, your kid's birthday, the last four digits of your Social Security number or numbers in sequence, recommends Greg Meyer, community relations manager for Meriwest Credit Union. "You wouldn't believe the number of people who want to choose 0000 or 1111," Meyer says. "That's just asking, 'Please rip me off.'" 7. Go online daily to check your account. Stay on top of every transaction to find out right away about unexpected fees or holds, accidental double charges or fraud. This is especially important with debit cards because any money you lose is your own -- not the bank's, says Tom Harkins, chief strategy officer for Secure Identity Systems and former vice president of security and risk for MasterCard International. By federal law, your losses from fraudulent activity on your debit card are limited to $50 -- but only if you notify your bank within two days of noticing a problem. 8. Be careful when linking accounts. If you're going to link your debit card checking account to a savings account, avoid exposing too much of your money to fraud, Harkins says. "The more accounts you link, the more you're giving fraudsters free rein," Harkins says. Your liability might be limited, but it could take days or weeks for the bank to reimburse you. "That's the risky part -- your money is gone, and the mortgage is due tomorrow, you're going to start bouncing checks and you can't even make an ATM withdrawal," he warns. 9. Use a credit card for big purchases. The bottom line: Debit cards don't offer as many consumer protections as credit cards. Cunningham recommends making large purchases -- such as stoves, refrigerators or plane tickets -- with a credit card. "You might want that product protection in case there's a dispute down the road," Cunningham says. A real-life example: When Steve Rhode, a consumer debt expert at GetOutOfDebt.org, lived in England, he used his credit card to buy plane tickets to fly his family back to the United States, but the airline went out of business before his trip. "I was able to file a claim with the credit card company and they wiped off the charge," Rhode says. "If I had used a debit card, that money would have been gone for good." Questions 1. How can you avoid overspending with your debit card? 2. Why is it important to record your transactions? 3. Why might you use your card as credit instead of debit? 4. What should you NOT use to make your PIN? 5. If you could give one piece of advice to someone about using a debit card, what would it be? 7

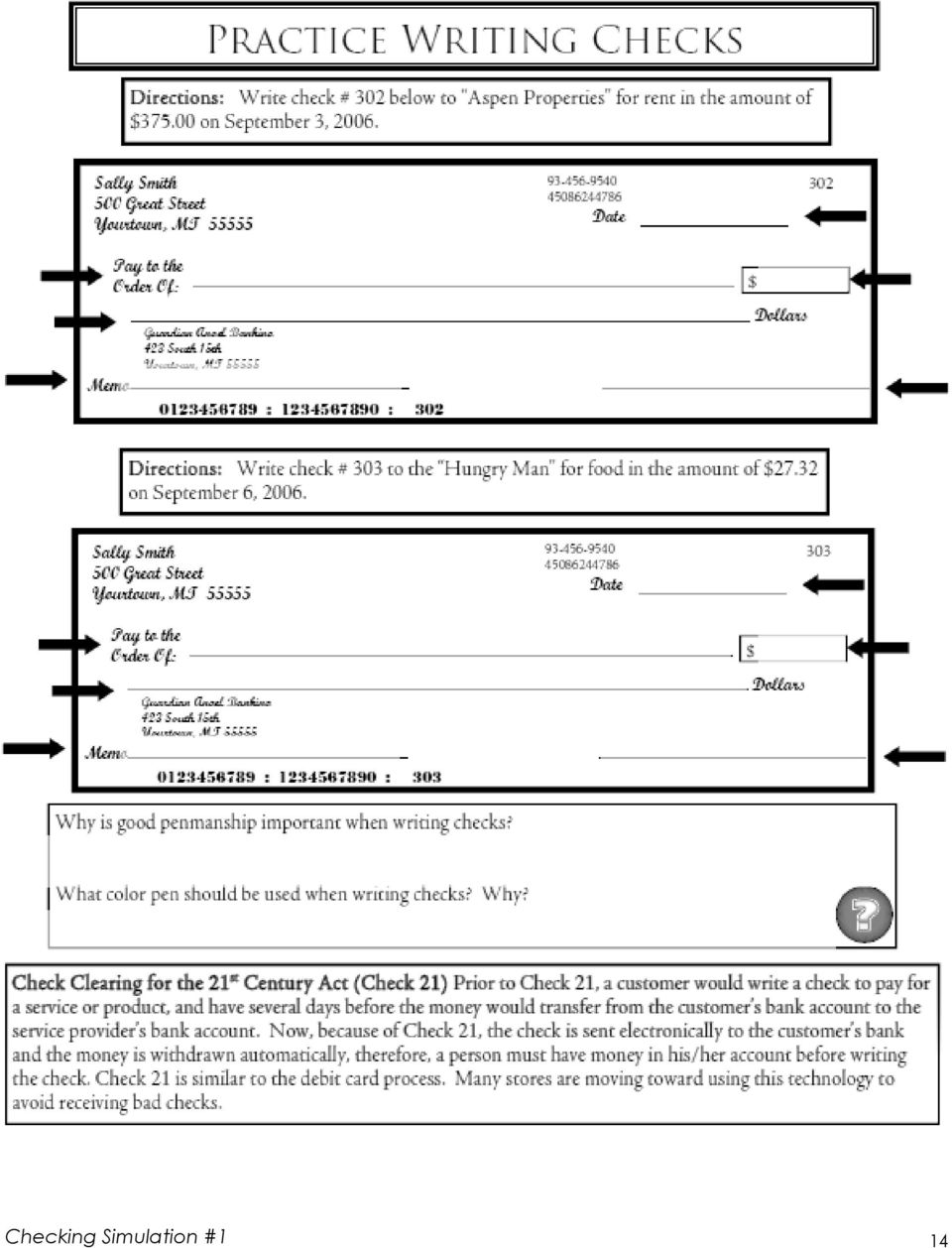

8 Writing a Check Activity To spend money held a in a checking account, people can use their debit cards at ATMs, online, or in stores, or they can write checks to make payments for goods and services. When you open a checking account, the bank will supply you with a checkbook full of blank checks and a checking register to record your transactions. It is important to know how to properly write a check so they do not bounce and leave you paying fees! For this activity, follow these instructions in order to write a check from Joe C. Dollar to pay his rent for March On line 1, write today s date. 2. On line 2, the Pay to the Order of line, write Hackettstown Central Apartments. This line tells the bank who can cash the check. 3. On line 3, in the box next to the dollar sign, write You will always write the numerical amount to be paid in this box. 4. On line 4, write out Nine hundred fifty and xx/100 and then draw a line in all remaining space up to where Dollars is typed. It is important to always write out the amount in case your numbers are illegible, and you must draw the line across in empty space so nobody can add to what you originally wrote. 5. On line 5, the memo, write Rent. This is to remind you and the person you re paying what the money is for. 6. On line 6, sign Joe C. Dollar. If you don t sign a check, nobody can cash it! 8

9 Checking Simulation #1 9

10 Checking Simulation #1 10

11 Checking Simulation #1 11

12 Checking Simulation #1 12

13 Checking Simulation #1 13

14 Checking Simulation #1 14

15 Checking Simulation #1 15

16 Checking Simulation #1 16

17 Checking Simulation #1 17

18 Checking Simulation #1 18

19 Checking Simulation #1 19

20 Checking Simulation #2 Checking Simulation #2 20

21 Checking Simulation #2 21

22 Checking Simulation #2 22

23 Checking Simulation #2 23

24 Checking Simulation #2 24

25 Checking Simulation #2 25

26 Checking Simulation #2 26

27 Checking Simulation #2 27

28 Checking Simulation #2 28

29 Checking Simulation #2 29

30 Responsible Checking Project Over the course of this unit on checking, you have learned the purpose of checking accounts, how to write checks, how to use a debit card, and how to use these tools responsibly. Now, you will create a pamphlet demonstrating what you ve learned. Each page needs the following information: 1. Cover Page 1. Title 2. Your Name 3. Block # 2. Vocabulary 1. Checking Account 2. Deposit 3. Withdrawal 4. Check 5. Checkbook 6. Check Register 7. Debit Card 8. ATM 9. PIN 3. Purpose of Checking Accounts 1. Answer: Why do people have checking accounts? 2. Answer: What are 2 ways to make payments with checking accounts? 4. Checks 1. Explain why a check could be used 2. Include a picture of a completed check 5. Depositing a Check 1. Write how to deposit a check sign the back, fill out a deposit slip at the bank, etc. 6. Debit Cards 1. Explain what a debit card is used for 2. Include a picture of a debit card 7. Debit Card Tips 1. Write at least 2 tips for people to responsibly use their debit cards or how to use an ATM Each page is worth 10 points [10 points x 7 pages = 70 points] 10 Points can be earned in the last 2 categories as well: Mechanics correct spelling, grammar, punctuation, & word usage 21 st Century Skills completed on time; appropriate use of class time; neat & creative overall appearance TOTAL = 100 POINTS 30

Share Draft/Checking Account Basics

Goals Share Draft/Checking Account Basics By the end of this session, students will be able to explain and understand: How and why checks are used What factors to compare when shopping for an account How

Goals Share Draft/Checking Account Basics By the end of this session, students will be able to explain and understand: How and why checks are used What factors to compare when shopping for an account How

Savings and Bank Accounts

LESSON 2 Savings Savings and Bank Accounts Quick Write Suppose a relative gives you a generous gift of $1,000 for your sixteenth birthday. Your parent or guardian says that you can spend $50 on things

LESSON 2 Savings Savings and Bank Accounts Quick Write Suppose a relative gives you a generous gift of $1,000 for your sixteenth birthday. Your parent or guardian says that you can spend $50 on things

CHECKING BASICS101. 701.255.0042 www.capcu.org

CHECKING BASICS101 701.255.0042 www.capcu.org This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended,

CHECKING BASICS101 701.255.0042 www.capcu.org This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended,

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account.

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Anytime Adviser Checking Account Coach

Anytime Adviser Checking Account Coach Welcome. This interactive guide coaches you in managing your checking account. You may move from chapter to chapter by selecting headings from the left. Click on

Anytime Adviser Checking Account Coach Welcome. This interactive guide coaches you in managing your checking account. You may move from chapter to chapter by selecting headings from the left. Click on

Prepaid Cards. An alternative to credit and debit cards. When choosing how to pay for their purchases, consumers have many options.

General-purpose reloadable prepaid cards Prepaid Cards An alternative to credit and debit cards When choosing how to pay for their purchases, consumers have many options. Cash, check, debit and credit

General-purpose reloadable prepaid cards Prepaid Cards An alternative to credit and debit cards When choosing how to pay for their purchases, consumers have many options. Cash, check, debit and credit

Standard 4: The student will demonstrate the ability to balance a checkbook and reconcile financial accounts. Standard 4.

STUDENT MODULE 4.1 MANAGING A BANK ACCOUNT PAGE 1 Standard 4: The student will demonstrate the ability to balance a checkbook and reconcile financial accounts. Standard 4. Tracking Your Money Alexis stops

STUDENT MODULE 4.1 MANAGING A BANK ACCOUNT PAGE 1 Standard 4: The student will demonstrate the ability to balance a checkbook and reconcile financial accounts. Standard 4. Tracking Your Money Alexis stops

Standard 4: The student will demonstrate the ability to balance a checkbook and reconcile financial accounts. Standard 4.

TEACHER GUIDE 4.1 MANAGING A BANK ACCOUNT PAGE 1 Standard 4: The student will demonstrate the ability to balance a checkbook and reconcile financial accounts. Standard 4. Tracking Your Money Priority Academic

TEACHER GUIDE 4.1 MANAGING A BANK ACCOUNT PAGE 1 Standard 4: The student will demonstrate the ability to balance a checkbook and reconcile financial accounts. Standard 4. Tracking Your Money Priority Academic

Basic Banking. 2) Money that a bank allows you to borrow and pay back with interest

Money that a bank allows you to borrow and pay back with interest") Basic Banking When choosing a bank, you should look for a bank that offers the type of accounts and services you are looking for. You might look for convenience of branch locations, great customer service,

Basic Banking When choosing a bank, you should look for a bank that offers the type of accounts and services you are looking for. You might look for convenience of branch locations, great customer service,

Credit Cards: Advantages & Disadvantages

Credit Cards: Advantages & Disadvantages Latino Community Credit Union & Latino Community Development Center CREDIT CARDS: BUILDING A better FUTURE ADVANTAGES AND DISADVANTAGES Latino Community Credit

Credit Cards: Advantages & Disadvantages Latino Community Credit Union & Latino Community Development Center CREDIT CARDS: BUILDING A better FUTURE ADVANTAGES AND DISADVANTAGES Latino Community Credit

PRACTICAL MONEY GUIDES DEBIT CARD BASICS. What you need to know about using your debit card

PRACTICAL MONEY GUIDES DEBIT CARD BASICS What you need to know about using your debit card MONEY IN THE BANK If credit cards mean pay later, debit cards mean pay now. These cards are issued by your bank,

PRACTICAL MONEY GUIDES DEBIT CARD BASICS What you need to know about using your debit card MONEY IN THE BANK If credit cards mean pay later, debit cards mean pay now. These cards are issued by your bank,

GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 1. Give Yourself Some Credit! A Greylock Federal Credit Union Financial Literacy Guide

GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 1 Give Yourself Some Credit! A Greylock Federal Credit Union Financial Literacy Guide GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 2 Contents How Does

GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 1 Give Yourself Some Credit! A Greylock Federal Credit Union Financial Literacy Guide GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 2 Contents How Does

MODULE 3 // CREDIT, DEBIT & PREPAID CARDS HALL OF FAME: AGES 18+

MODULE 3 // CREDIT, DEBIT & PREPAID CARDS HALL OF FAME: AGES 18+ MODULE 3 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial

MODULE 3 // CREDIT, DEBIT & PREPAID CARDS HALL OF FAME: AGES 18+ MODULE 3 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial

Checking 101. Property of Penn State Federal Credit Union

Checking 101 Checking 101 Checking Account Basics A check is a written order that represents cash Credit Union checking accounts are also called SHARE DRAFT accounts A share draft is equivalent to a check,

Checking 101 Checking 101 Checking Account Basics A check is a written order that represents cash Credit Union checking accounts are also called SHARE DRAFT accounts A share draft is equivalent to a check,

Checking 101. Checking Out Checking Accounts

Checking 101 Checking Out Checking Accounts Checking Account Basics A check is a written order that represents cash Credit Union checking accounts are also called SHARE DRAFT accounts A share draft is

Checking 101 Checking Out Checking Accounts Checking Account Basics A check is a written order that represents cash Credit Union checking accounts are also called SHARE DRAFT accounts A share draft is

Participant Guide Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum

Check It Out Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Determining Your Checking Account Needs 1 Checking Account Fees 2 Practice Exercise: Choosing

Check It Out Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Determining Your Checking Account Needs 1 Checking Account Fees 2 Practice Exercise: Choosing

1.4. Will my Social Security and Supplemental Security Income benefits be safe?

1. OVERVIEW 1.1. What is the Direct Express card? The Direct Express card is a prepaid debit card available to Social Security and Supplemental Security Income check recipients who wish to receive their

1. OVERVIEW 1.1. What is the Direct Express card? The Direct Express card is a prepaid debit card available to Social Security and Supplemental Security Income check recipients who wish to receive their

Getting and Keeping A Checking Account

Getting and Keeping A Checking Account You've decided to get a checking account. That's a good idea. Your money will be safe and you'll have a record of what you've paid for. You'll know how much you have

Getting and Keeping A Checking Account You've decided to get a checking account. That's a good idea. Your money will be safe and you'll have a record of what you've paid for. You'll know how much you have

How to manage manage your your checking checking account. account.

How How to manage to manage your your checking checking account. account. Introduction Welcome to Desert Schools Federal Credit Union. Congratulations on your first checking account! It s the perfect time

How How to manage to manage your your checking checking account. account. Introduction Welcome to Desert Schools Federal Credit Union. Congratulations on your first checking account! It s the perfect time

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

Dimes to Riches Money Management for Teens in Grades 7-12

Dimes to Riches Money Management for Teens in Grades 7-12 s e e r t n o row g t n s e o yd e n o M t a! h k t n a w b o n a k t u n By now yo Your parents are & Life is getting busy and you need cash for

Dimes to Riches Money Management for Teens in Grades 7-12 s e e r t n o row g t n s e o yd e n o M t a! h k t n a w b o n a k t u n By now yo Your parents are & Life is getting busy and you need cash for

Math 8.1: Mathematical Process Standards

Lesson Description Texas Essential Knowledge and Skills (Target standards) Texas Essential Knowledge and Skills (Prerequisite standards) National Standards (Supporting standards) CEE Council for Economic

Lesson Description Texas Essential Knowledge and Skills (Target standards) Texas Essential Knowledge and Skills (Prerequisite standards) National Standards (Supporting standards) CEE Council for Economic

A card built to put your money to work. Welcome to your Citi Dividend World MasterCard.

WELCOME Citi Dividend World MasterCard Cash Back. Security. Convenience. SMART A card built to put your money to work. Welcome to your Citi Dividend World MasterCard. Here s how it works: Earn at least

WELCOME Citi Dividend World MasterCard Cash Back. Security. Convenience. SMART A card built to put your money to work. Welcome to your Citi Dividend World MasterCard. Here s how it works: Earn at least

Banking Basics 101. How to Manage Your Finances and Still Have Money Left Over For Pizza. Course objectives learn about:

Banking Basics 101 Course objectives learn about: Using a checking account Various types of payment vehicles Benefits of a savings account How to Manage Your Finances and Still Have Money Left Over For

Banking Basics 101 Course objectives learn about: Using a checking account Various types of payment vehicles Benefits of a savings account How to Manage Your Finances and Still Have Money Left Over For

lesson six using banking services teacher s guide

lesson six using banking services teacher s guide using banking services web sites web sites for banking services The Internet is probably the most extensive and dynamic source of information in our society.

lesson six using banking services teacher s guide using banking services web sites web sites for banking services The Internet is probably the most extensive and dynamic source of information in our society.

Uneasy about getting started? Not to worry. SageLink Credit Union has trained employees to help you every step of the way.

Checking If you re like most young adults, you spend a lot of time thinking about money. How to get money? What to spend your money on? Where to keep your money in between? A MoneyLink Checking account

Checking If you re like most young adults, you spend a lot of time thinking about money. How to get money? What to spend your money on? Where to keep your money in between? A MoneyLink Checking account

Personal Financial Literacy: Checking

Personal Financial Literacy: Checking Overview In this lesson, students will learn the benefits of checking accounts, as well as precautions one must take with these accounts. They will practice using

Personal Financial Literacy: Checking Overview In this lesson, students will learn the benefits of checking accounts, as well as precautions one must take with these accounts. They will practice using

Checking Account Management

Checking Account Management 595 Market Street, 16th Floor San Francisco, CA 94105 888.456.2227 www.balancepro.net Whether you have a history of overdraft or nonsufficient funds charges or you just want

Checking Account Management 595 Market Street, 16th Floor San Francisco, CA 94105 888.456.2227 www.balancepro.net Whether you have a history of overdraft or nonsufficient funds charges or you just want

How To Understand How To Get A Bank Account

Opening a Bank Account Section Objectives A basic component in establishing financial independence is Opening a Bank Account. Banking services are essential tools for managing personal finances and building

Opening a Bank Account Section Objectives A basic component in establishing financial independence is Opening a Bank Account. Banking services are essential tools for managing personal finances and building

Using Banking Services

Teacher's Guide $ Lesson Six Using Banking Services 04/09 using banking services websites websites for banking services The internet is probably the most extensive and dynamic source of information in

Teacher's Guide $ Lesson Six Using Banking Services 04/09 using banking services websites websites for banking services The internet is probably the most extensive and dynamic source of information in

Using Credit to Your Advantage Credit Cards and Loans Participant Guide

Hands on Banking Using Credit to Your Advantage The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the program anytime at www.handsonbanking.org & www.elfuturoentusmanos.org

Hands on Banking Using Credit to Your Advantage The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the program anytime at www.handsonbanking.org & www.elfuturoentusmanos.org

CHECKING 101 EDUCATION. Practice & Reference Material

CHECKING 101 EDUCATION Practice & Reference Material BOOKLET INFORMATION Thank you for your willingness to learn more about managing your checking account and how to better use the tools Academy Bank offers

CHECKING 101 EDUCATION Practice & Reference Material BOOKLET INFORMATION Thank you for your willingness to learn more about managing your checking account and how to better use the tools Academy Bank offers

Checking Account and Debit Card Simulation

Checking Account and Debit Card Simulation Student Instructions and Worksheets Introductory Level Take Charge Today May 2006 Checking Account & Debit Card Simulation Page 1 Checking Account Student Instructions

Checking Account and Debit Card Simulation Student Instructions and Worksheets Introductory Level Take Charge Today May 2006 Checking Account & Debit Card Simulation Page 1 Checking Account Student Instructions

Checking Account & Debit Card Simulation and Student Worksheet. Understanding Checking Accounts and Debit Card Transactions

Checking Account & Debit Card Simulation and Student Worksheet Understanding Checking Accounts and Debit Card Transactions What is a Checking Account? Common financial service used by many consumers Funds

Checking Account & Debit Card Simulation and Student Worksheet Understanding Checking Accounts and Debit Card Transactions What is a Checking Account? Common financial service used by many consumers Funds

What is a Checking Account? Checking Account & Debit Card Simulation. What is a Check? Bouncing a Check. Other Checking Components

Checking Account & Debit Card Simulation Understanding Checking Accounts and Debit Card Transactions What is a Checking Account? Common financial service used by many consumers Funds are easily accessed

Checking Account & Debit Card Simulation Understanding Checking Accounts and Debit Card Transactions What is a Checking Account? Common financial service used by many consumers Funds are easily accessed

WHY YOUR CREDIT HISTORY MATTERS AND HOW TO IMPROVE IT.

WHY YOUR CREDIT HISTORY MATTERS AND HOW TO IMPROVE IT. CONTENTS. 1 WHY YOUR CREDIT HISTORY MATTERS 1 2 WHAT S CREDIT? 2 3 WHAT IS A CREDIT REPORT? 3 4 CHECKING YOUR CREDIT REPORT 4 5 IMPROVING YOUR CREDIT

WHY YOUR CREDIT HISTORY MATTERS AND HOW TO IMPROVE IT. CONTENTS. 1 WHY YOUR CREDIT HISTORY MATTERS 1 2 WHAT S CREDIT? 2 3 WHAT IS A CREDIT REPORT? 3 4 CHECKING YOUR CREDIT REPORT 4 5 IMPROVING YOUR CREDIT

transfer money by check or electronic payment to a person or organization that you designate as payee

Bank Products 1. Introduction For many people, the first financial institution they deal with, and the one they use most often, is a bank or credit union. That s because banks and credit unions provide

Bank Products 1. Introduction For many people, the first financial institution they deal with, and the one they use most often, is a bank or credit union. That s because banks and credit unions provide

Checking Account and Debit Card Simulation

Checking Account and Debit Card Simulation Student Instructions and Worksheets Get Ready to Take Charge of Your Finances Family Economics & Financial Education May 2006 Get Ready to Take Charge of Your

Checking Account and Debit Card Simulation Student Instructions and Worksheets Get Ready to Take Charge of Your Finances Family Economics & Financial Education May 2006 Get Ready to Take Charge of Your

Choosing and Using a Checking Account

LESSON 8 Choosing and Using a Checking Account LESSON DESCRIPTION AND BACKGROUND The students learn the fundamentals of maintaining a checking account. They examine electronic banking methods, the writing

LESSON 8 Choosing and Using a Checking Account LESSON DESCRIPTION AND BACKGROUND The students learn the fundamentals of maintaining a checking account. They examine electronic banking methods, the writing

Introducing the Credit Card

Introducing the Credit Card This program was designed with high school students in mind. It goes over everything you need to know before you get your first credit card so you can manage it wisely.» Key

Introducing the Credit Card This program was designed with high school students in mind. It goes over everything you need to know before you get your first credit card so you can manage it wisely.» Key

Checking Account. Money Smarts for Kids. Money Skills for Life. Member FDIC. Welcome! What Is a Checking Account? Why Is a Checking Account So Great?

Checking Account Welcome! Welcome to Young Americans Bank, the only bank in the world designed specifically for young people! Mr. Bill Daniels started Young Americans Bank in 1987 because he thought it

Checking Account Welcome! Welcome to Young Americans Bank, the only bank in the world designed specifically for young people! Mr. Bill Daniels started Young Americans Bank in 1987 because he thought it

Banking Procedures. Online Resources CHAPTER 5

CHAPTER 5 Banking Procedures Getty Images/PhotoDisc C hapter 5 discusses banking activities for consumers and banking in the United States. Many benefits and services for consumers are available from financial

CHAPTER 5 Banking Procedures Getty Images/PhotoDisc C hapter 5 discusses banking activities for consumers and banking in the United States. Many benefits and services for consumers are available from financial

Personal Banking 101 Interested in learning about how to manage your money? Personal Banking 101 will help you understand the financial fundamentals.

Personal Banking 101 Interested in learning about how to manage your money? Personal Banking 101 will help you understand the financial fundamentals. Checking Account If you need a safe place to keep your

Personal Banking 101 Interested in learning about how to manage your money? Personal Banking 101 will help you understand the financial fundamentals. Checking Account If you need a safe place to keep your

Overdraft Education Practice & Reference Materials

Overdraft Education Practice & Reference Materials 2011 IN-Focus Digital Booklet Instructions 2 This booklet is designed for use with the First Financial Bank Overdraft Education video. Any unauthorized

Overdraft Education Practice & Reference Materials 2011 IN-Focus Digital Booklet Instructions 2 This booklet is designed for use with the First Financial Bank Overdraft Education video. Any unauthorized

u.s. bank focus card Frequently Asked Questions The Focus Card What is the Focus Card? How does the Focus Card work?

Frequently Asked Questions What is the Focus Card? The Focus Card is a reloadable, prepaid debit card issued by U.S. Bank. It provides an electronic option for receiving your pay. It is not a credit card,

Frequently Asked Questions What is the Focus Card? The Focus Card is a reloadable, prepaid debit card issued by U.S. Bank. It provides an electronic option for receiving your pay. It is not a credit card,

Vocabulary Financial Institutions Student Worksheet

Vocabulary Student Worksheet Page 1 Name Period Primary 1. Bounced Check: Vocabulary Financial Institutions Student Worksheet 2. ATM Charge: 3. Stop Payment Fee: 4. Travelers Checks: 5. ATM: 6. FDIC: 7.

Vocabulary Student Worksheet Page 1 Name Period Primary 1. Bounced Check: Vocabulary Financial Institutions Student Worksheet 2. ATM Charge: 3. Stop Payment Fee: 4. Travelers Checks: 5. ATM: 6. FDIC: 7.

Lesson Description. Concepts. Objectives. Content Standards. Cards, Cars and Currency Lesson 3: Banking on Debit Cards

Lesson Description After discussing basic information about debit cards, students work in pairs to balance a bank account statement and calculate the costs of using a debit card irresponsibly. The students

Lesson Description After discussing basic information about debit cards, students work in pairs to balance a bank account statement and calculate the costs of using a debit card irresponsibly. The students

Checking Account & Debit Card Simulation. Understanding Checking Accounts and Debit Card Transactions

Checking Account & Debit Card Simulation Understanding Checking Accounts and Debit Card Transactions What is a Checking Account? Common financial service used by many consumers Funds are easily accessed

Checking Account & Debit Card Simulation Understanding Checking Accounts and Debit Card Transactions What is a Checking Account? Common financial service used by many consumers Funds are easily accessed

Bank Products. 3.1 Introduction

Bank Products Bank Products For many people, the first financial institution they deal with, and the one they use most often, is a bank or credit union. That s because banks and credit unions provide a

Bank Products Bank Products For many people, the first financial institution they deal with, and the one they use most often, is a bank or credit union. That s because banks and credit unions provide a

Arab Bank Cards User Guide

Arab Bank Cards User Guide 4600900 arabbank.jo A card to suit every lifestyle Coming to you from the largest Arab banking network, Arab Bank Cards entitle you to a host of benefits designed to offer you

Arab Bank Cards User Guide 4600900 arabbank.jo A card to suit every lifestyle Coming to you from the largest Arab banking network, Arab Bank Cards entitle you to a host of benefits designed to offer you

TALKING POINTS COLLEGE STUDENTS PRESENTED BY JEAN CHATZKY AND PASS FROM AMERICAN EXPRESS SM

INTRODUCTION Give your kids a heads-up that tonight you re going to make some time to talk about money. It won t take all night, but they should clear their schedule. If your kid is away at college, and

INTRODUCTION Give your kids a heads-up that tonight you re going to make some time to talk about money. It won t take all night, but they should clear their schedule. If your kid is away at college, and

Teacher's Guide. Lesson Six. Banking Services 04/09

Teacher's Guide $ Lesson Six Banking Services 04/09 banking services websites Students will make wise choices about their banking services once they understand such fundamentals as: selecting and managing

Teacher's Guide $ Lesson Six Banking Services 04/09 banking services websites Students will make wise choices about their banking services once they understand such fundamentals as: selecting and managing

Why do you need my Social Security Number and other personal information when I enroll for an I.C.E. card?

ABOUT THE ICE MasterCard Prepaid CARD What is the I.C.E MasterCard Prepaid CARD? Is the I.C.E. Card like a checking or savings account? Are funds loaded on to the I.C.E. Card FDIC insured? Are there age

ABOUT THE ICE MasterCard Prepaid CARD What is the I.C.E MasterCard Prepaid CARD? Is the I.C.E. Card like a checking or savings account? Are funds loaded on to the I.C.E. Card FDIC insured? Are there age

PAYROLL CARD FREQUENTLY ASKED QUESTIONS

The following document provides answers to frequently asked questions regarding the Umpqua Bank Payroll Card. Contact Customer Care at 800-650-7141 with questions. Card Basics Q. How does the Payroll Card

The following document provides answers to frequently asked questions regarding the Umpqua Bank Payroll Card. Contact Customer Care at 800-650-7141 with questions. Card Basics Q. How does the Payroll Card

TOP TRUMPS Comparisons of how to pay for goods and services online

Cash Cash is legal tender in the form of bank notes and coins Small value purchases e.g. cafes, shops Pocket money Repaying friends Cash is physically transferred from one person to the next, usually face-to-face

Cash Cash is legal tender in the form of bank notes and coins Small value purchases e.g. cafes, shops Pocket money Repaying friends Cash is physically transferred from one person to the next, usually face-to-face

PRACTICAL MONEY GUIDES PREPAID CARD BASICS. What you should know about using prepaid cards

PRACTICAL MONEY GUIDES PREPAID CARD BASICS What you should know about using prepaid cards PREPAID CARDS AN ALTERNATIVE TO CASH A prepaid card is a card you load with money to make purchases anywhere a

PRACTICAL MONEY GUIDES PREPAID CARD BASICS What you should know about using prepaid cards PREPAID CARDS AN ALTERNATIVE TO CASH A prepaid card is a card you load with money to make purchases anywhere a

Checking Account FINANCIAL INSTITUTION WITHDRAWAL. Should I Be Banking? Checking Account. Taking Charge of Your Own. And More!

TEEN GUIDE moneytalks4teens.org Checking Account Crossword Puzzle Should I Be Banking? Taking Charge of Your Own Checking Account Choosing Your FINANCIAL INSTITUTION Opening Your Checking Account Making

TEEN GUIDE moneytalks4teens.org Checking Account Crossword Puzzle Should I Be Banking? Taking Charge of Your Own Checking Account Choosing Your FINANCIAL INSTITUTION Opening Your Checking Account Making

Adults Version. Instructor guide. 2003, 2012 Wells Fargo Bank, N.A. All rights reserved. Member FDIC. ECG-714394

Adults Version Instructor guide 2003, 2012 Wells Fargo Bank, N.A. All rights reserved. Member FDIC. ECG-714394 Welcome to Wells Fargo s Hands on Banking program! This fun, interactive, and engaging financial

Adults Version Instructor guide 2003, 2012 Wells Fargo Bank, N.A. All rights reserved. Member FDIC. ECG-714394 Welcome to Wells Fargo s Hands on Banking program! This fun, interactive, and engaging financial

FINANCIAL/BANKING LITERACY ASSISTANCE FOR LATINO AMERICANS

FINANCIAL/BANKING LITERACY ASSISTANCE FOR LATINO AMERICANS REASONS WHY YOU SHOULD OPEN A BANK ACCOUNT Safety Carrying cash on payday or keeping large amounts of money at home or in your wallet can make

FINANCIAL/BANKING LITERACY ASSISTANCE FOR LATINO AMERICANS REASONS WHY YOU SHOULD OPEN A BANK ACCOUNT Safety Carrying cash on payday or keeping large amounts of money at home or in your wallet can make

The Merchant. Skimming is No Laughing Matter. A hand held skimming device. These devices can easily be purchased online.

1 February 2010 Volume 2, Issue 1 The Merchant Serving Florida State University s Payment Card Community Individual Highlights: Skimming Scam 1 Skimming at Work 2 Safe at Home 3 Read your Statement 4 Useful

1 February 2010 Volume 2, Issue 1 The Merchant Serving Florida State University s Payment Card Community Individual Highlights: Skimming Scam 1 Skimming at Work 2 Safe at Home 3 Read your Statement 4 Useful

Cash Management. Cash management. Two key aspects of cash mgt. Checking Accounts Savings Accounts Debit cards and overdraft protection

Cash Management Checking Accounts Savings Accounts Debit cards and overdraft protection Cash management Getting a handle on your cash and other liquid assets Cash is the money in your wallet plus what

Cash Management Checking Accounts Savings Accounts Debit cards and overdraft protection Cash management Getting a handle on your cash and other liquid assets Cash is the money in your wallet plus what

Your Money Matters! Financial Literacy Teacher Guide. Thanks to TD for helping us bring this resource to schools for free.

Your Money Matters! Financial Literacy Teacher Guide 2 Table of Contents: Introduction...3 Toronto Star epaper...4 Financial Awareness Inventory...5 SPENDING To Spend or Not to Spend Activity...6 I Need

Your Money Matters! Financial Literacy Teacher Guide 2 Table of Contents: Introduction...3 Toronto Star epaper...4 Financial Awareness Inventory...5 SPENDING To Spend or Not to Spend Activity...6 I Need

February 11, 2015. Megabyte Money.notebook. Megabyte Money. Electronic "money" that replaces currency & checks. Sep 18-8:51 PM

Megabyte Money Electronic "money" that replaces currency & checks. Sep 18-8:51 PM 1 With the Internet, electronic transfers, payments, & banking have been made easier and more popular. Electronic Funds

Megabyte Money Electronic "money" that replaces currency & checks. Sep 18-8:51 PM 1 With the Internet, electronic transfers, payments, & banking have been made easier and more popular. Electronic Funds

Budget Main Window (Single Bank Account) Budget Main Window (Multiple Bank Accounts)

Budget Main Window (Multiple Bank Accounts)") Budget Main Window (Single Bank Account) Budget Main Window (Multiple Bank Accounts) Page 1 of 136 Using Budget Help Budget has extensive help features. To get help use Budget's Help > Budget Help menu

Budget Main Window (Single Bank Account) Budget Main Window (Multiple Bank Accounts) Page 1 of 136 Using Budget Help Budget has extensive help features. To get help use Budget's Help > Budget Help menu

Choosing and Using a Checking Account

LESSON 8 Choosing and Using a Checking Account Introduction Buying a new mp3 player is not a snap decision. You have to know the storage capacity of the player the larger the capacity, the more music and

LESSON 8 Choosing and Using a Checking Account Introduction Buying a new mp3 player is not a snap decision. You have to know the storage capacity of the player the larger the capacity, the more music and

How to Use a Financial Institution

How to Use a Financial Institution Latino Community Credit Union & Latino Community Development Center HOW TO USE A FINANCIAL INSTITUTION LATINO COMMUNITY CREDIT UNION & LATINO COMMUNITY DEVELOPMENT CENTER

How to Use a Financial Institution Latino Community Credit Union & Latino Community Development Center HOW TO USE A FINANCIAL INSTITUTION LATINO COMMUNITY CREDIT UNION & LATINO COMMUNITY DEVELOPMENT CENTER

Unit 5: Banking Options

Read Chapter 5 in the text. Unit 5: Banking Options Read this unit including websites. Suggestions: you may want to write down some key points. This information will be very basic for some of you. For

Read Chapter 5 in the text. Unit 5: Banking Options Read this unit including websites. Suggestions: you may want to write down some key points. This information will be very basic for some of you. For

Instructor Guide Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum

Check It Out Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Module Overview 1 Purpose 1 Objectives 1 Time 1 Materials and Equipment Needed to Present

Check It Out Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Module Overview 1 Purpose 1 Objectives 1 Time 1 Materials and Equipment Needed to Present

How do I get good credit?

Slide 1 Credit The information provided in this e-course is intended for educational purposes only and does not constitute specific advice for you as an individual. When evaluating your particular needs,

Slide 1 Credit The information provided in this e-course is intended for educational purposes only and does not constitute specific advice for you as an individual. When evaluating your particular needs,

10 Steps to Financial Freedom in Your Twenties and Thirties

1 Steps to Financial Freedom in Your Twenties and Thirties On our journey to obtain independence and achieve financial success, we usually prioritize having good educational experiences, a sound resume

1 Steps to Financial Freedom in Your Twenties and Thirties On our journey to obtain independence and achieve financial success, we usually prioritize having good educational experiences, a sound resume

Independent Bank 230 W Main St Ionia, MI 48846 800.300.3193 www.independentbank.com ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE

230 W Main St Ionia, MI 48846 800.300.3193 www.independentbank.com ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE For purposes of this disclosure and agreement the terms "we", "us" and "our" refer to

230 W Main St Ionia, MI 48846 800.300.3193 www.independentbank.com ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE For purposes of this disclosure and agreement the terms "we", "us" and "our" refer to

Learn about. How to deposit money. How to make withdrawals and write checks. How to keep track of your money

Cumberland Security Bank s Checking School Learn about How to deposit money How to make withdrawals and write checks How to keep track of your money Depositing Money You can deposit cash and/or checks

Cumberland Security Bank s Checking School Learn about How to deposit money How to make withdrawals and write checks How to keep track of your money Depositing Money You can deposit cash and/or checks

Money Math for Teens. Before You Choose a Credit Card

Money Math for Teens Before You Choose a Credit Card This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education

Money Math for Teens Before You Choose a Credit Card This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education

Checking Accounts. Open, Manage, and Reconcile

Checking Accounts Open, Manage, and Reconcile 1. What is a checking account? A checking account is opened at a bank or other financial institution. Banks offer several different types of checking accounts.

Checking Accounts Open, Manage, and Reconcile 1. What is a checking account? A checking account is opened at a bank or other financial institution. Banks offer several different types of checking accounts.

Tips and Answers: Banking Basics Case Studies Case Study: The Piggy Bank

Tips and Answers: Banking Basics Case Studies Case Study: The Piggy Bank Twins Emma and Emmett are excited to be starting college next year. Emma is leaving home behind and heading to college in Florida

Tips and Answers: Banking Basics Case Studies Case Study: The Piggy Bank Twins Emma and Emmett are excited to be starting college next year. Emma is leaving home behind and heading to college in Florida

Participant Guide Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum

Bank On It Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Banking Basics 1 Opening and Maintaining a Bank Account 2 Choosing a Bank Checklist 3 Practice

Bank On It Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Banking Basics 1 Opening and Maintaining a Bank Account 2 Choosing a Bank Checklist 3 Practice

Jump$tart Washington Curriculum Unit 1 Chapter 1 Contents

Jump$tart Washington Curriculum Unit 1 Chapter 1 Contents Jump$tart... 1 UNIT ONE: PLANNING AND MONEY MANAGEMENT... 2 Chapter One: Financial Literacy... 2 Chapter Learning Objectives... 2 Episode 301 Synopsis...

Jump$tart Washington Curriculum Unit 1 Chapter 1 Contents Jump$tart... 1 UNIT ONE: PLANNING AND MONEY MANAGEMENT... 2 Chapter One: Financial Literacy... 2 Chapter Learning Objectives... 2 Episode 301 Synopsis...

How a Teen can use "Budget" to manage their money

How a Teen can use "Budget" to manage their money Parents, you can use "Budget" to teach your teen how to manage their allowance and/or part-time job income, and eventually to manage a checking account.

How a Teen can use "Budget" to manage their money Parents, you can use "Budget" to teach your teen how to manage their allowance and/or part-time job income, and eventually to manage a checking account.

BUILDING YOUR MONEY PYRAMID: FINANCIAL PLANNING CFE 3218V

BUILDING YOUR MONEY PYRAMID: FINANCIAL PLANNING CFE 3218V OPEN CAPTIONED MERIDIAN EDUCATION CORP. 1994 Grade Levels: 10-13+ 14 minutes 1 Instructional Graphic Enclosed DESCRIPTION Most people will earn

BUILDING YOUR MONEY PYRAMID: FINANCIAL PLANNING CFE 3218V OPEN CAPTIONED MERIDIAN EDUCATION CORP. 1994 Grade Levels: 10-13+ 14 minutes 1 Instructional Graphic Enclosed DESCRIPTION Most people will earn

1 Identify your goal. What is it that you want to buy. 2 Gather information. What are the terms of the credit

Be a Savvy Credit User About 40% of credit card holders carry individual balances of less than $1,000, while about 15% individually carry total card balances of more than $10,000. Forty-eight percent of

Be a Savvy Credit User About 40% of credit card holders carry individual balances of less than $1,000, while about 15% individually carry total card balances of more than $10,000. Forty-eight percent of

Table of Contents. Money Smart for Adults Curriculum Page 2 of 21

Table of Contents Checking In... 3 Pre-Test... 4 What Is Credit?... 6 Collateral... 6 Types of Loans... 7 Activity 1: Which Loan Is Best?... 8 The Cost of Credit... 9 Activity 2: Borrowing Money Responsibly...

Table of Contents Checking In... 3 Pre-Test... 4 What Is Credit?... 6 Collateral... 6 Types of Loans... 7 Activity 1: Which Loan Is Best?... 8 The Cost of Credit... 9 Activity 2: Borrowing Money Responsibly...

The Webster Visa Prepaid Debit Card Frequently Asked Questions

Contact Us Welcome to Webster Bank. Please contact our Card Services support line at 866.242.0861 with any questions or concerns, 24/7. Thank you for being a valued Webster Customer! The Webster Visa Prepaid

Contact Us Welcome to Webster Bank. Please contact our Card Services support line at 866.242.0861 with any questions or concerns, 24/7. Thank you for being a valued Webster Customer! The Webster Visa Prepaid

Credit cards explained

Credit cards explained What is a credit card? As its name suggests, a credit card lets you buy things on credit meaning that you don t need to have the money upfront to pay for your purchases. If large,

Credit cards explained What is a credit card? As its name suggests, a credit card lets you buy things on credit meaning that you don t need to have the money upfront to pay for your purchases. If large,

TABLE OF CONTENTS. Introduction 3. General Guidelines for Successful Account Management 3. Managing Your Checking Account. 1.

TABLE OF CONTENTS Introduction 3 General Guidelines for Successful Account Management 3 Managing Your Checking Account 1. Check Register 2. Planning 3. Recording Your Transactions 4. Balancing Your Account

TABLE OF CONTENTS Introduction 3 General Guidelines for Successful Account Management 3 Managing Your Checking Account 1. Check Register 2. Planning 3. Recording Your Transactions 4. Balancing Your Account

Cardholder Frequently Asked Questions

Skip to Content Cardholder Frequently Asked Questions Close this browser window to return to session. TOTALPAY Card by ADP FAQs CARD BASICS 1. Is my TOTALPAY Card ready to use when I receive it? 2. When

Skip to Content Cardholder Frequently Asked Questions Close this browser window to return to session. TOTALPAY Card by ADP FAQs CARD BASICS 1. Is my TOTALPAY Card ready to use when I receive it? 2. When

BANKING 101. Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org

BANKING 101 Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org Congratulations on taking this important step to learn about issues dealing

BANKING 101 Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org Congratulations on taking this important step to learn about issues dealing

Your new checking account Getting started guide

Your new checking account Getting started guide Welcome to checking made easy At Wells Fargo, our checking accounts are designed to simplify your everyday finances so you can enjoy more of life. To make

Your new checking account Getting started guide Welcome to checking made easy At Wells Fargo, our checking accounts are designed to simplify your everyday finances so you can enjoy more of life. To make

Travel Card. Cardholder Frequently Asked Questions. June 2014 T.FQ.S.20141.E

Travel Card Cardholder Frequently Asked Questions Travel Card (1) Where can I use my card? Your card may be used anywhere debit cards are accepted. The brand marks on your card indicate where the card

Travel Card Cardholder Frequently Asked Questions Travel Card (1) Where can I use my card? Your card may be used anywhere debit cards are accepted. The brand marks on your card indicate where the card

TABLE OF CONTENTS. Introduction 3. General Guidelines for Successful Account Management 3. Managing Your Checking Account. 1.

TABLE OF CONTENTS Introduction 3 General Guidelines for Successful Account Management 3 Managing Your Checking Account 1. Check Register 2. Planning 3. Recording Your Transactions 4. Balancing Your Account

TABLE OF CONTENTS Introduction 3 General Guidelines for Successful Account Management 3 Managing Your Checking Account 1. Check Register 2. Planning 3. Recording Your Transactions 4. Balancing Your Account

FBFCU VISA PREPAID DEBIT CARD FREQUENTLY ASKED QUESTIONS (FAQs)

") ABOUT THE FORT BRAGG FEDERAL CREDIT UNION VISA PREPAID CARD What is the FORT BRAGG FEDERAL CREDIT UNION Visa Prepaid Card? Is the FORT BRAGG FEDERAL CREDIT UNION Card like a checking or savings account?

ABOUT THE FORT BRAGG FEDERAL CREDIT UNION VISA PREPAID CARD What is the FORT BRAGG FEDERAL CREDIT UNION Visa Prepaid Card? Is the FORT BRAGG FEDERAL CREDIT UNION Card like a checking or savings account?

Introductions. Student Introductions. Purpose. Objectives (Continued) Objectives

Objectives") Introductions Instructor and student introductions Module overview 1 2 Your name Student Introductions Your expectations, questions, and concerns about checking accounts Purpose will teach you how to use

Introductions Instructor and student introductions Module overview 1 2 Your name Student Introductions Your expectations, questions, and concerns about checking accounts Purpose will teach you how to use

Your new checking account

Your new checking account Getting started guide The information in this disclosure may not be entirely accessible to screen readers. Please call the Phone Bank at 1-800-TO-WELLS if you would like to obtain

Your new checking account Getting started guide The information in this disclosure may not be entirely accessible to screen readers. Please call the Phone Bank at 1-800-TO-WELLS if you would like to obtain