Establishing Credit Smart library Series

|

|

|

- Ezra Shelton

- 8 years ago

- Views:

Transcription

1 4 Establishing Credit Credit is the opportunity to borrow money to use now and then repay over time at an agreed upon cost. It s a convenience and an important financial tool if used wisely. Smart investing@your library Series This initiative is administered jointly by the Reference and User Services Association - a division of the American Library Association - and the FINRA Investor Education Foundation. The program funds library efforts to provide patrons with effective, unbiased financial education resources. Martin County Cooperative Establishing Credit Smart investing@your library Extension 1 Service

2 18% Minimum Payment 87 7 $1,516 What do you find most useful about having a credit card? Payments Credit Cards Buy now, pay later. Debit Cards Buy now, pay now. Good for emergencies Pay for big-ticket items and stretch out the payments over time Establish a credit history Insurance or replacement for purchases Safer than carrying large amounts of cash Airline miles or other rewards Protection from fraud Not managing your credit wisely can lead to: Increased annual percentage rates (APRs) Unnecessary fees A decline in your credit score Denials of future credit, employment or insurance Interest Charges Other Potential Benefits Other Potential Concerns Yes, if you carry a balance or your card offers no grace period. Freebies, such as cash rebates and bonus points good for travel deals. Some purchase protections. Fees and penalties. Also not all cards offer grace periods (time to repay without incurring interest). Over-spending can cause debt problems. No. Easier and faster than writing a check. Avoid debt problems. More cards now offering freebies. Some purchase protections. Fees on certain transactions. You may overdraw your account if you don t record debit card transactions into your check register and balance your checkbook. Benefits of Making More Than The Minimum Payment 18% Minimum Payment (MP) $3,915 18% MP + $ $3,258 18% MP + $ $2,839 This chart assumes you are not making additional purchases, and you are making your payments on time. The minimum payment rate is 4 percent. Of course, the best way to save money and avoid paying interest charges is to pay off your balance in full when you first get your bill. Establishing Credit Smart investing@your library 2

3 Sample Truth in Lending Disclosure Statement Look at the other fees that may be involved (here s an example): $20.00 Late payment fee (if you forgot to mail your check before the due date on the statement) $20.00 Over-the-limit fee (Example: Your credit card limit for spending is $1, and you spent $1, or more.) $20.00 Returned check fee $ 2.00 ATM transaction fee (this is also a cash advance) The grace period does not apply to cash advances. (grace period = 25 days to mail your payment to the credit card company to pay this month s bill before it is late) The annual percentage rate for cash advances (like getting cash at the local ATM) is 24%. (The 19.4% rate listed above, would be for purchases.) Credit Cards Comparison Chart Credit Card 1 Credit Card 2 Credit Card 3 Name of credit card issuer/card What is the annual percentage rate (APR)? Introductory APR? Penalty APR? What is the finance charge? What is the annual fee? What are other fees (late fees, over-the-limit fees, closing fees, etc.)? Is there a grace period? What are other benefits (points earned, etc.)? What is my credit limit? Other? (for example, customer service hours; online access; can you talk to a real person?) Establishing Credit Smart investing@your library 3

The annual percentage rate for cash advances (like getting cash at the local ATM)")

4 Types of Credit Check off the types of credit you have: Revolving credit the type of credit agreement used by most credit cards. It allows consumers to pay all or part of the outstanding balance in each billing cycle. As credit is paid off, it becomes available again to use for another purchase or cash advance. Charge cards cards that are not subject to interest, but you cannot carry a balance you must pay your bill in full each month. Charge cards often have annual fees. There is no set credit limit because cardholders agree to pay the full amount they owe every month. Secured credit cards obtained only after you have deposited money in a savings account to guarantee that you will pay for your credit card charges. Secured cards look like and are used just like unsecured cards. Secured credit cards are an option for people who have no credit history or have a poor one. Subprime cards are marketed to people with poor or damaged credit. Subprime credit is high-interest credit offered to borrowers who may not qualify for any other credit. Stored value cards cards that look like credit cards and use the same magnetic stripe to retain account information. Payroll cards, electronic benefits transfer cards, travel funds cards and store gift cards are examples of stored value cards. Retail (store) credit cards cards issued by department stores, national chain retailers and gasoline companies as a convenience for their customers. These cards are more limited in their use as compared to general purpose credit cards issued by banks and financial services companies (bank cards). Store cards cannot be used to purchase goods and services from other merchants or service providers. Tips on how to use your credit card responsibly Check off things you do: Protect your credit card and account numbers to prevent unauthorized use. Draw a line through blank spaces on charge slips so the amount cannot be changed. Tear up carbon copies of your receipts. Keep a record of your account numbers, expiration dates, and the phone numbers of each credit card issuer in a safe place, separate from your credit card, to quickly report a loss. Carry only the credit cards you think you will use. Pay off your total balance each month. If you cannot pay the total balance, try to pay more than the minimum amount. Read the fine print. Low advertised interest rates might not last as long as you think. You might not have a grace period with balances you have transferred from other credit cards. After you have established a good credit history, ask the credit card issuer to waive the fee or lower the interest rate. Do not keep more than two or three credit cards. Too many cards make overspending tempting. There are, however, good reasons to have more than one card, especially if your credit limit is not high enough on one card to cover an emergency. Many financially responsible people can become overwhelmed by expenses or reduced income triggered by a serious illness, a job loss, or some other unexpected event. To seek help call toll free Establishing Credit Smart investing@your library 4

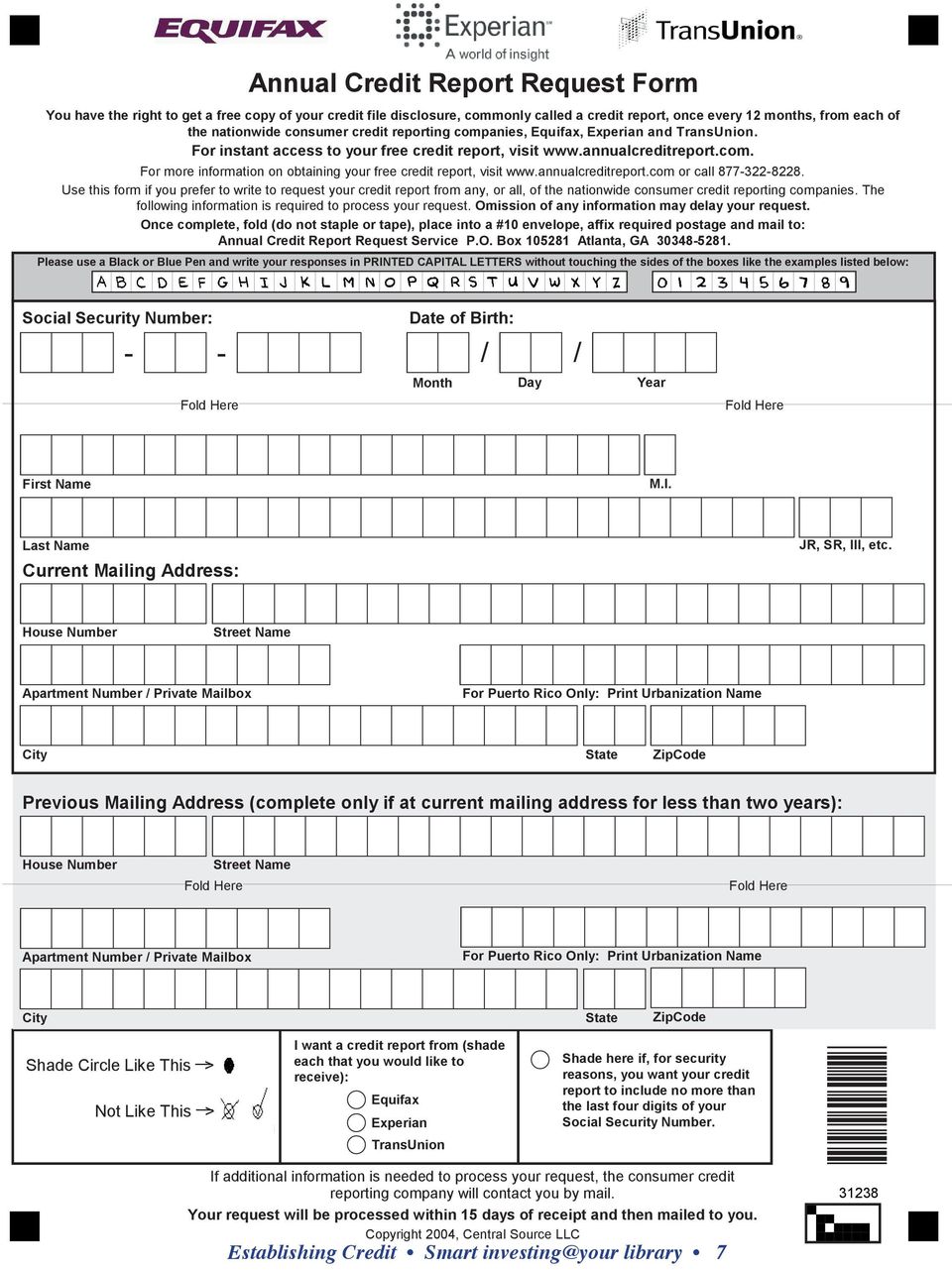

5 How to get a free copy of your credit report once a year from each of 3 reporting agencies To order your free annual report from one or all of the credit reporting agencies, do not contact the three nationwide consumer reporting companies individually. You can obtain FREE annual credit reports by doing ONE of the following: Submit a request online at Call toll-free: Complete the Annual Credit Report Request Form in this booklet on page 7 and mail it to: Annual Credit Report Request Service P. O. Box Atlanta, GA You can print a copy of the Annual Credit Report Request Form (same as on page 7) from or You need to provide your name, address, Social Security number, and date of birth. If you have moved in the last 2 years, you may have to provide your previous address. To maintain the security of your file, each credit reporting agency may ask you for some information that only you would know, like the amount of your monthly mortgage payment. Each company may ask you for different information because the information each has in your file may come from different sources. Remember, you may also be able to obtain a free credit report if: Your application for credit, insurance, or employment is denied based on information in your credit report. You are unemployed and plan to look for a job within 60 days. You are receiving public assistance. Your report is inaccurate because of fraud, including identity theft. If you are not eligible for a free annual credit report, a credit reporting agency may charge you up to $10.00 for each copy. To buy a copy of your report, contact one of the following credit reporting agencies: Equifax: or Experian: 888-EXPERIAN ( ) or TransUnion: or Every 4 months, try getting your free credit report from a different credit reporting agency (Equifax, Experion or Trans Union), to keep track of how you are doing througout the year. Establishing Credit Smart investing@your library 5

from http://www.annualcreditreport.com or http://www.ftc.")

6 Penny Parker Establishing Credit Smart library 6

7 Establishing Credit Smart library 7

8 6 ways to kill your Credit Score Lenders, insurers, landlords and others will charge you more or flat-out reject you if you show up with a low FICO score. Here s how you may be doing yourself harm. By Jeanne Sahadi, CNNMoney.com senior writer Find out your credit score Know how lenders see you. Take seven minutes to download a free credit report at annualcreditreport. com or calling For year-round monitoring, get a report from one of the three major credit bureaus every four months. If you spot an error, notify the bureau (online, by phone or by mail) and the creditor (call and also send a letter). You won t find your credit score here, so when you request a report from Equifax, pay $7.95 for your FICO score, the most commonly used score. The range is 300 to 850, with 700 and above being good. 30 percent of your credit limit. It s always good to pay off your balances every month. But creditors may take a few weeks or even a couple of months to report your payment to the credit bureaus. To boost your score: Don t charge anything for at least 60 days before applying for a loan. That way it s likely that all the payments you ve made to date will be reflected in your credit score by the time a lender requests it. If you can t pay off your total balance in full, at least keep it under 30 percent of your total credit limit. 2 - Be a payment-slacker Sending in your loan or credit card payments late can really hurt. When you re 30 days past due and your balance is still unpaid, your score could take a 60-point hit. That kind of drop could mean a much higher interest rate on loans you take out. Late payments from your past that you have since paid off will have less and less of a negative effect on your score as time goes on. On average, past delinquencies that have since been resolved, might cost you 15 to 20 points. To boost your score: Pay your bill in full and mail it as soon as it arrives, or at the very least the minimum due. Set up automatic online bill payments so you ll never be late. Or, if you are late one month, be sure to pay off what you owe as soon as possible. 3 - Be too thin When it comes to your credit record, fat is good, emaciated bad. Even if you re the most responsible, on-time, in-full bill payer on the planet, your credit score won t be as high as it could be if you have just one credit account. The reason: Your credit profile is too thin and lenders ideally like to see a potential borrower responsibly managing a mix of revolving debt (such as credit cards, where you can reuse the credit after paying it back) and installment debt (such as a car loan or most mortgages, where you pay the same amount every month for a certain period). 1 - Big spender at the wrong time The bigger your total balance as a percent of your total credit limit across all your credit cards, the lower your score will be. You lose 1 point for every percent of your credit limit that you use. So if you have a total credit limit of $10,000 and have an outstanding balance of $4,000 (40%), your score would be 40 points lower than if you had a $0 balance. Ideally, credit experts say, your never want your balance to exceed Establishing Credit Smart investing@your library 8

and the creditor (call and also send a letter).")

9 To boost your score: Consider opening another credit-card account or two, or taking out a car loan or small bank loan. 4 - Be too young and eager Old credit accounts count more than young ones in your credit score. Lenders prefer borrowers who have responsibly managed the same accounts for years. That s a more reliable indicator of creditworthiness than a few months of exemplary behavior on a new account. Accounts open less than six months will hurt your score somewhat. Those open six months or more won t, while those open at least two years will help your score. Lenders also don t like to see a borrower who s gone on a credit binge, applying for a lot of new accounts or loans in a short period. Every time you apply for new credit, your score may be dinged by 5 points. That s not the case, though, if a broker shops around for the best loans on your behalf. In that case, if they approach multiple lenders who all pull your credit report, that will only count as one inquiry so long as they all do so within a two-week window. To boost your score: Avoid applying on your own for a lot of loans and credit cards, particularly in a short period. And avoid excessive card-hopping. 5 - Be too tidy The bigger your balance relative to your credit limit, the lower your score. But while it may be tempting to close out a credit card account when you transfer the balance to a lower-rate card, you may inadvertently hurt your score. That s because your total balance stays the same but your credit limit goes down when you close an account. Say you have three credit cards with a combined credit limit of $24,000 ($8,000 each) and you owe $6,000 total. Your balance represents 25% of your credit limit. If you then close out one of your accounts, your credit limit goes down to $16,000 but your debt is still $6,000, which now represents 37.5% of your credit limit. To boost your score: Don t close unused accounts when you transfer debt. 6 - Be too nonchalant You may be a great credit risk, but your score won t reflect that if there are errors in your credit report. The last thing you need is to have someone else s delinquencies wrongly assigned to you. Or you may think you ve got great credit, but don t realize that your spouse has been hiding debt from you, and killing your score in the meanwhile. Unless you make yourself aware of what s in your credit report a few months before applying for a loan, you ll have no idea how a lender will perceive you, rightly or wrongly. And you won t give yourself the opportunity to improve your score. To boost your score: Order a free credit report once a year from each of the three major credit bureaus, and make sure they re accurate. Order one every four months by going to annualcreditreport.com or calling Two annoying but true facts: Credit scores aren t free, and the credit bureaus don t share information on you, so your credit reports and the scores based on them may vary. So if you re planning on applying for a mortgage or other big loan, you might do well to order a the 3-in-1 deluxe package from myfico.com for $ That will include your credit reports from all three credit bureaus as well as the FICO scores based on those reports. Raise your credit score in 8 minutes Both will lower the size of your outstanding debt as a percentage of your total borrowing power. 1. Pay down a balance. 2. Call your issuer and ask for a higher credit limit. And don t spend it. Establishing Credit Smart investing@your library 9

10 By paying your credit card bill late not only will you face a late payment charge (which could be higher than your minimum payment), your tardiness will show up on your credit report, damage your FICO score and make it harder to get better terms for future loans and accounts. Make sure you send your check in plenty of time, or set up an automatic payment via your bank at least a week before the due date. Martin County s Smart investing@your library Series: 1 - Your Financial Fitness 2 - Designing Your Budget 3 - Banking Basics 4 - Establishing Credit 5 - Credit & Identity Theft 6 - Controlling Debt 7 - Tips for Daily Savings 8 - Saving for the Future Credits: This booklet was designed by Chris Kilbride, University of Florida - Martin County Cooperative Extension Service for the Martin County Library System s Smart investing@your library Series. For details about Smart investing@your library, visit To learn more about the Martin County Library System, visit We would like to acknowledge the original educational outreach material: Credit Cards: What You Need to Know - an educational partnership between Consumer Action and American Express. Charge It Right FDIC Money Smart and To Your Credit FDIC Money Smart Financial Education Curriculum Participant Guide The mission of the FINRA Investor Education Foundation, a nonprofit organization, is to provide underserved Americans with the knowledge, skills and tools necessary for financial success throughout life. The FINRA Foundation envisions a society characterized by universal financial literacy. For more information and financial literacy resources, visit: Establishing Credit Smart investing@your library 10

Participant Guide Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum

Charge It Right Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Credit Cards and Debit Cards 1 Other Cards 2 Sample Truth in Lending Disclosure Statement

Charge It Right Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Credit Cards and Debit Cards 1 Other Cards 2 Sample Truth in Lending Disclosure Statement

Instructor Guide Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum

Charge It Right Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Module Overview 1 Purpose 1 Objectives 1 Time 1 Materials and Equipment Needed to Present

Charge It Right Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Module Overview 1 Purpose 1 Objectives 1 Time 1 Materials and Equipment Needed to Present

Credit: The Good and the Bad

Managing Your Credit Effectively Credit can be a valuable addition to your financial toolbox if you use it carefully and sensibly. Credit means someone is willing to loan you money called Principal in

Managing Your Credit Effectively Credit can be a valuable addition to your financial toolbox if you use it carefully and sensibly. Credit means someone is willing to loan you money called Principal in

Credit Cards: Advantages & Disadvantages

Credit Cards: Advantages & Disadvantages Latino Community Credit Union & Latino Community Development Center CREDIT CARDS: BUILDING A better FUTURE ADVANTAGES AND DISADVANTAGES Latino Community Credit

Credit Cards: Advantages & Disadvantages Latino Community Credit Union & Latino Community Development Center CREDIT CARDS: BUILDING A better FUTURE ADVANTAGES AND DISADVANTAGES Latino Community Credit

Understanding Credit Cards

Understanding Credit Cards INTRODUCTION This brochure can help you understand how credit cards work, become familiar with common terms offered with a credit card, and avoid the dangers of using credit

Understanding Credit Cards INTRODUCTION This brochure can help you understand how credit cards work, become familiar with common terms offered with a credit card, and avoid the dangers of using credit

How do I get good credit?

Slide 1 Credit The information provided in this e-course is intended for educational purposes only and does not constitute specific advice for you as an individual. When evaluating your particular needs,

Slide 1 Credit The information provided in this e-course is intended for educational purposes only and does not constitute specific advice for you as an individual. When evaluating your particular needs,

Chapter 06. What is Consumer Credit? Chapter 6 Learning Objectives. Introduction to Consumer Credit

Chapter 06 Introduction to Consumer Credit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 6-1 Chapter 6 Learning Objectives 1. Define consumer credit and analyze

Chapter 06 Introduction to Consumer Credit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 6-1 Chapter 6 Learning Objectives 1. Define consumer credit and analyze

Understanding Credit BY Sallie Mae and FICO

Understanding Credit BY Sallie Mae and FICO Lisa Mitchell, Sallie Mae Brad Riebel, Sallie Mae April 2015 Session Focus Overview FICO and Sallie Mae partnership on ways to help students understand why credit

Understanding Credit BY Sallie Mae and FICO Lisa Mitchell, Sallie Mae Brad Riebel, Sallie Mae April 2015 Session Focus Overview FICO and Sallie Mae partnership on ways to help students understand why credit

Understanding Credit. The Three C s of Credit. What is a Credit Bureau?

Understanding Credit By definition, the word credit has to do with trust. This is why credit impacts so many financial issues in our lives including the extension of a loan or credit card, how high an

Understanding Credit By definition, the word credit has to do with trust. This is why credit impacts so many financial issues in our lives including the extension of a loan or credit card, how high an

Exercise 4A: What Info Do You Need for a Loan?

Exercise 4A: What Info Do You Need for a Loan? What information do you think is needed to get a loan? Review several samples of loan applications to see what The Cost of Using Credit As mentioned earlier,

Exercise 4A: What Info Do You Need for a Loan? What information do you think is needed to get a loan? Review several samples of loan applications to see what The Cost of Using Credit As mentioned earlier,

Brought to you by PEPCO FCU. Seminar objectives

Take Charge: Wise Use of Credit Cards Brought to you by PEPCO FCU Seminar objectives Learn: Benefits and costs of credit cards How to build a good credit history Warning signs of too much debt How to figure

Take Charge: Wise Use of Credit Cards Brought to you by PEPCO FCU Seminar objectives Learn: Benefits and costs of credit cards How to build a good credit history Warning signs of too much debt How to figure

Credit Workshop. What I need to know about credit and lending products of financial institutions. Financial Education Supported by:

Credit Workshop What I need to know about credit and lending products of financial institutions. Financial Education Supported by: Concept Checklist What will I learn today? [ ] What is Credit? [ ] Advantages/

Credit Workshop What I need to know about credit and lending products of financial institutions. Financial Education Supported by: Concept Checklist What will I learn today? [ ] What is Credit? [ ] Advantages/

GET CREDITWISE SM SM

GET CREDITWISE SM SM Table Of Contents October, 2006 Credit Matters 1 An introduction Establishing Credit 3 Begin building a solid financial base Using Credit Wisely 5 Narrowing your options Monitoring

GET CREDITWISE SM SM Table Of Contents October, 2006 Credit Matters 1 An introduction Establishing Credit 3 Begin building a solid financial base Using Credit Wisely 5 Narrowing your options Monitoring

Slide 3 - When you get a new credit card, activate and sign your card.

Five Keys to Credit for Today Notes for PowerPoint Slide 2 - There are many reasons to know what s in your wallet. We all carry many records, cards, identification, health cards and more in our wallets.

Five Keys to Credit for Today Notes for PowerPoint Slide 2 - There are many reasons to know what s in your wallet. We all carry many records, cards, identification, health cards and more in our wallets.

Use and Misuse of Credit. Chapter 6. Advantages of Credit. What is Consumer Credit?

Chapter 6 Use and Misuse of Credit Introduction to Consumer Credit Before you use credit for a major purchase, ask yourself some questions. Do I have the cash for the down payment? Do I want to use my

Chapter 6 Use and Misuse of Credit Introduction to Consumer Credit Before you use credit for a major purchase, ask yourself some questions. Do I have the cash for the down payment? Do I want to use my

Improve Your Credit Put Bad Credit Behind You

Improve Your Credit Put Bad Credit Behind You Improve your credit While it s possible to get by without credit, access to credit is essential for buying a home, financing a car or getting a credit card.

Improve Your Credit Put Bad Credit Behind You Improve your credit While it s possible to get by without credit, access to credit is essential for buying a home, financing a car or getting a credit card.

Using Credit to Your Advantage.

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

What s in My Credit Report?... 1. Taking Care of Your Score... 3. How Do I Get Credit?... 4. Understanding Credit Cards... 5

The Credit 411 Contents What s in My Credit Report?... 1 Taking Care of Your Score... How Do I Get Credit?... 4 Understanding Credit Cards... 5 Protecting Your Credit... Thinking About Filing Bankruptcy?...

The Credit 411 Contents What s in My Credit Report?... 1 Taking Care of Your Score... How Do I Get Credit?... 4 Understanding Credit Cards... 5 Protecting Your Credit... Thinking About Filing Bankruptcy?...

STUDENT MODULE 8.1 ONLINE SHOPPING AND CREDIT CARDS PAGE 1

STUDENT MODULE 8.1 ONLINE SHOPPING AND CREDIT CARDS PAGE 1 Standard 8: The student will describe and explain interest, credit cards, and online commerce. Credit Cards: More Than Plastic Austin receives

STUDENT MODULE 8.1 ONLINE SHOPPING AND CREDIT CARDS PAGE 1 Standard 8: The student will describe and explain interest, credit cards, and online commerce. Credit Cards: More Than Plastic Austin receives

Using Credit to Your Advantage

Hands on Banking Using Credit to Your Advantage Credit Reports, Credit Scores and Dealing with Debt The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the

Hands on Banking Using Credit to Your Advantage Credit Reports, Credit Scores and Dealing with Debt The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the

Your Financial Fitness

1 Your Financial Fitness Consider Financial Fitness to be just like physical fitness. Why? Because your physical health and your financial health are often the most important factors affecting your wellbeing,

1 Your Financial Fitness Consider Financial Fitness to be just like physical fitness. Why? Because your physical health and your financial health are often the most important factors affecting your wellbeing,

Update: On November 4, 2009, the day that this revised brochure was to go to print,

In May 2009, President Obama signed into law the Credit Card Accountability Responsibility and Disclosure Act (CARD Act) to strengthen consumer credit card protections. The bulk of the new law becomes

In May 2009, President Obama signed into law the Credit Card Accountability Responsibility and Disclosure Act (CARD Act) to strengthen consumer credit card protections. The bulk of the new law becomes

In July 2010, credit card rules will change. In the meantime, here is a guide to current rules, with information about the changes to come, to help

2 In July 2010, credit card rules will change. In the meantime, here is a guide to current rules, with information about the changes to come, to help you when you consider which credit card offer you might

2 In July 2010, credit card rules will change. In the meantime, here is a guide to current rules, with information about the changes to come, to help you when you consider which credit card offer you might

Personal Banking 101 Interested in learning about how to manage your money? Personal Banking 101 will help you understand the financial fundamentals.

Personal Banking 101 Interested in learning about how to manage your money? Personal Banking 101 will help you understand the financial fundamentals. Checking Account If you need a safe place to keep your

Personal Banking 101 Interested in learning about how to manage your money? Personal Banking 101 will help you understand the financial fundamentals. Checking Account If you need a safe place to keep your

Revolving credit: A consumer line of credit that can be used up to a certain limit or paid down at any time.

TEACHER GUIDE 8.1 CREDIT CARDS AND ONLINE SHOPPING PAGE 1 Standard 8: The student will describe and explain interest, credit cards, and online commerce. Credit Cards: More Than Plastic Priority Academic

TEACHER GUIDE 8.1 CREDIT CARDS AND ONLINE SHOPPING PAGE 1 Standard 8: The student will describe and explain interest, credit cards, and online commerce. Credit Cards: More Than Plastic Priority Academic

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Through financial knowledge and expertise, we provide high-quality products and services that enable people to enjoy a better

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Through financial knowledge and expertise, we provide high-quality products and services that enable people to enjoy a better

Office of Student Financial Management

February 2015 Office of Student Financial Management Kasia Palm: Director of Student Financial Management What is Credit? - The ability to obtain goods/services before payment based on the trust that a

February 2015 Office of Student Financial Management Kasia Palm: Director of Student Financial Management What is Credit? - The ability to obtain goods/services before payment based on the trust that a

Growing Dollars and $ense: Personal Financial Planning Seminar

Growing Dollars and $ense: Personal Financial Planning Seminar The Coalition for Debtor Education Kimberly Allman www.debtoreducati0n.org Email: cde@law.fordham.edu This program is made possible by a grant

Growing Dollars and $ense: Personal Financial Planning Seminar The Coalition for Debtor Education Kimberly Allman www.debtoreducati0n.org Email: cde@law.fordham.edu This program is made possible by a grant

Managing Your Credit Report and Scores. Apprisen. 800.355.2227 www.apprisen.com

Managing Your Credit Report and Scores Apprisen 800.355.2227 www.apprisen.com Managing Your Credit Report and Scores Your credit score is one of the most important aspects of your personal finances. From

Managing Your Credit Report and Scores Apprisen 800.355.2227 www.apprisen.com Managing Your Credit Report and Scores Your credit score is one of the most important aspects of your personal finances. From

GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 1. Give Yourself Some Credit! A Greylock Federal Credit Union Financial Literacy Guide

GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 1 Give Yourself Some Credit! A Greylock Federal Credit Union Financial Literacy Guide GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 2 Contents How Does

GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 1 Give Yourself Some Credit! A Greylock Federal Credit Union Financial Literacy Guide GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 2 Contents How Does

Chapter Objectives. Chapter 6. Short Term Credit Management. Major Topics. Reasons for Using Credit. How to Get Credit. Disadvantages of Using Credit

Chapter Objectives Chapter 6. Short Term Credit Management To evaluate reasons for and against using credit and decide whether or not credit is appropriate for you. To be able to take the necessary steps

Chapter Objectives Chapter 6. Short Term Credit Management To evaluate reasons for and against using credit and decide whether or not credit is appropriate for you. To be able to take the necessary steps

MODULE 3 // CREDIT, DEBIT & PREPAID CARDS HALL OF FAME: AGES 18+

MODULE 3 // CREDIT, DEBIT & PREPAID CARDS HALL OF FAME: AGES 18+ MODULE 3 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial

MODULE 3 // CREDIT, DEBIT & PREPAID CARDS HALL OF FAME: AGES 18+ MODULE 3 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial

Credit arrangements can be formal or informal. The three most common types of credit used by consumers are described below.

1-888-842-6328 For toll-free numbers when overseas, visit Collect internationally 1-703-255-8837 TDD for hearing impaired 1-888-869-5863 Credit Wise Credit: a Useful Tool Most of us use consumer credit

1-888-842-6328 For toll-free numbers when overseas, visit Collect internationally 1-703-255-8837 TDD for hearing impaired 1-888-869-5863 Credit Wise Credit: a Useful Tool Most of us use consumer credit

Understanding Credit. Megan Stearns, Credit Counselor

Understanding Credit Megan Stearns, Credit Counselor Obtaining your free credit report will lower your credit score. Closing old accounts can help your credit score. Paying off the balances on your credit

Understanding Credit Megan Stearns, Credit Counselor Obtaining your free credit report will lower your credit score. Closing old accounts can help your credit score. Paying off the balances on your credit

1 Identify your goal. What is it that you want to buy. 2 Gather information. What are the terms of the credit

Be a Savvy Credit User About 40% of credit card holders carry individual balances of less than $1,000, while about 15% individually carry total card balances of more than $10,000. Forty-eight percent of

Be a Savvy Credit User About 40% of credit card holders carry individual balances of less than $1,000, while about 15% individually carry total card balances of more than $10,000. Forty-eight percent of

A crash course in credit

A crash course in credit Ever get the feeling that you re being watched? That someone s keeping an eye on how you handle your money? Well, you re not just imagining things. Banks, credit card companies,

A crash course in credit Ever get the feeling that you re being watched? That someone s keeping an eye on how you handle your money? Well, you re not just imagining things. Banks, credit card companies,

Understanding your Credit Score

Understanding your Credit Score Understanding Your Credit Score Fair, Isaac and Co. is the San Rafael, California Company founded in 1956 by Bill Fair and Earl Isaac. They pioneered the field of credit

Understanding your Credit Score Understanding Your Credit Score Fair, Isaac and Co. is the San Rafael, California Company founded in 1956 by Bill Fair and Earl Isaac. They pioneered the field of credit

Take Charge of Credit Cards

Take Charge of Credit Cards Get Ready to Take Charge of Your Finances Introductory Level What is Credit? Credit- something is received in exchange for a promise to pay back money in the future Borrower

Take Charge of Credit Cards Get Ready to Take Charge of Your Finances Introductory Level What is Credit? Credit- something is received in exchange for a promise to pay back money in the future Borrower

Data Security. New to Credit. Published April 2010. Sponsored by. published X date

Data Security Made Simpler Sponsored by New to Credit Published April 2010 published X date Introduction redit can be a strong financial Ctool to help consumers and small business owners manage their money.

Data Security Made Simpler Sponsored by New to Credit Published April 2010 published X date Introduction redit can be a strong financial Ctool to help consumers and small business owners manage their money.

Credit Scoring and Wealth

the Problem In most games, it is wise to understand the rules before you begin to play. What if you weren t aware that you were playing a game? What if you had not choice whether to play or not? Everyone

the Problem In most games, it is wise to understand the rules before you begin to play. What if you weren t aware that you were playing a game? What if you had not choice whether to play or not? Everyone

How to Use Credit. Latino Community Credit Union & Latino Community Development Center

How to Use Credit Latino Community Credit Union & Latino Community Development Center How to Use Credit Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright

How to Use Credit Latino Community Credit Union & Latino Community Development Center How to Use Credit Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright

CreditAbility: Build a Strong Credit History. Brought to you by Duke University FCU

: Build a Strong Credit History Brought to you by Duke University FCU Seminar Objectives Learn: Who needs to build good credit, and why Significance of credit report and score How to establish credit if

: Build a Strong Credit History Brought to you by Duke University FCU Seminar Objectives Learn: Who needs to build good credit, and why Significance of credit report and score How to establish credit if

Credit Reports and Credit Scores

Credit Reports and Credit Scores This program is made possible by a grant from the FINRA Investor Education Foundation through Smart Investing@Your Library, a partnership with the American Library Association.

Credit Reports and Credit Scores This program is made possible by a grant from the FINRA Investor Education Foundation through Smart Investing@Your Library, a partnership with the American Library Association.

Understanding and managing your credit

Understanding and managing your credit Overview Understanding how credit works and how it affects your chances of getting approved for a loan is important. In this presentation, you ll learn helpful ways

Understanding and managing your credit Overview Understanding how credit works and how it affects your chances of getting approved for a loan is important. In this presentation, you ll learn helpful ways

CREDIT IN A NEW COUNTRY:

CREDIT IN A NEW COUNTRY: A GUIDE TO CREDIT IN CANADA A free publication provided by Consolidated Credit Counseling Services of Canada, Inc., a registered charitable credit counselling and debt management

CREDIT IN A NEW COUNTRY: A GUIDE TO CREDIT IN CANADA A free publication provided by Consolidated Credit Counseling Services of Canada, Inc., a registered charitable credit counselling and debt management

Credit Matters ICAN. Be a Smart Credit Consumer. Iowa College Access Network. Iowa College Access Network

Credit Matters Be a Smart Credit Consumer ICAN Iowa College Access Network Iowa College Access Network ICAN Iowa College Access Network The Iowa College Access Network (ICAN) helps individuals attain their

Credit Matters Be a Smart Credit Consumer ICAN Iowa College Access Network Iowa College Access Network ICAN Iowa College Access Network The Iowa College Access Network (ICAN) helps individuals attain their

Earning Extra Credit. Understanding what it takes to maintain and manage good credit now and for your future

Credit 101 Why Credit is Important 3 Your Credit Score 5 FICO Scoring - From Good to Bad 7 Credit Bureaus 8 Credit-Worthy vs. Credit-Ready 9 Are you Drowning in Debt? 10 2 Why Credit is Important College

Credit 101 Why Credit is Important 3 Your Credit Score 5 FICO Scoring - From Good to Bad 7 Credit Bureaus 8 Credit-Worthy vs. Credit-Ready 9 Are you Drowning in Debt? 10 2 Why Credit is Important College

Credit Scores. www.howtogainwealth.com. Copyright 2009 How to Gain Wealth. All rights reserved.

Credit Scores Why is my Credit Score important? Lenders, such as banks and credit card companies, use credit scores to evaluate the potential risk posed by lending money to consumers and to mitigate losses

Credit Scores Why is my Credit Score important? Lenders, such as banks and credit card companies, use credit scores to evaluate the potential risk posed by lending money to consumers and to mitigate losses

Solving the Credit Puzzle. L G & W Federal Credit Union

Solving the Credit Puzzle L G & W Federal Credit Union Knowledge Check How much do you already know about credit scoring? Sample Credit Report Credit Bureaus Equifax TransUnion Experian Who Can Pull Your

Solving the Credit Puzzle L G & W Federal Credit Union Knowledge Check How much do you already know about credit scoring? Sample Credit Report Credit Bureaus Equifax TransUnion Experian Who Can Pull Your

Make the most of your credit score

Make the most of your credit score Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org Congratulations on taking this important step to learn

Make the most of your credit score Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org Congratulations on taking this important step to learn

Questions and Answers

C r e d i t T r a i n i n g m a n u a l Questions and Answers Q& A About Obtaining and Managing Credit A Consumer Action Publication Table of Contents 1 Introduction 2 Types of Credit 3 Uses of Credit

C r e d i t T r a i n i n g m a n u a l Questions and Answers Q& A About Obtaining and Managing Credit A Consumer Action Publication Table of Contents 1 Introduction 2 Types of Credit 3 Uses of Credit

Office of Student Financial Management

September 2013 Office of Student Financial Management Kasia Palm: Director of Student Financial Management What is Credit? - The ability to obtain goods/services before payment based on the trust that

September 2013 Office of Student Financial Management Kasia Palm: Director of Student Financial Management What is Credit? - The ability to obtain goods/services before payment based on the trust that

How To Check Your Credit Report For Not Credit History

Your Credit Report P.O. Box 15128 Spokane Valley, WA 99215 800.852.5316 www.hzcu.org You may not think about them every day, but your credit report and the three little digits that make up your credit

Your Credit Report P.O. Box 15128 Spokane Valley, WA 99215 800.852.5316 www.hzcu.org You may not think about them every day, but your credit report and the three little digits that make up your credit

Choosing and Using Credit Cards

A WorkLife4You Guide Choosing and Using Credit Cards Chances are you ve gotten your share of preapproved credit card offers in the mail, some with low introductory rates and other perks. Many of these

A WorkLife4You Guide Choosing and Using Credit Cards Chances are you ve gotten your share of preapproved credit card offers in the mail, some with low introductory rates and other perks. Many of these

Your Credit Report What It Says about You

Your Credit Report Your Credit Report What It Says about You Most people finance their homes with mortgages and pay for their cars with loans. Young people often obtain loans to pay for college. And, of

Your Credit Report Your Credit Report What It Says about You Most people finance their homes with mortgages and pay for their cars with loans. Young people often obtain loans to pay for college. And, of

MANAGING CREDIT101 TM %*'9 [[[ EPXEREJGY SVK i

MANAGING CREDIT101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

MANAGING CREDIT101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

Topic 3 Credit Report

Topic 3 Credit Report Questions to Think About: What are the different types of credit and why is credit important? What are its advantages and disadvantages? What is a credit report? How do you read it

Topic 3 Credit Report Questions to Think About: What are the different types of credit and why is credit important? What are its advantages and disadvantages? What is a credit report? How do you read it

Build a Strong Credit History. Brought to you by The New York University Federal Credit Union

Build a Strong Credit History Brought to you by The New York University Federal Credit Union Seminar Objectives Learn: Who needs to build good credit, and why Significance of credit report and score How

Build a Strong Credit History Brought to you by The New York University Federal Credit Union Seminar Objectives Learn: Who needs to build good credit, and why Significance of credit report and score How

A Credit Smart Start. Michael Trecek Sr. Risk Analyst Commerce Bank Retail Lending

A Credit Smart Start Michael Trecek Sr. Risk Analyst Commerce Bank Retail Lending Agenda Credit Score vs. Credit Report Credit Score Components How Credit Scoring Helps You 10 Things that Hurt Your Credit

A Credit Smart Start Michael Trecek Sr. Risk Analyst Commerce Bank Retail Lending Agenda Credit Score vs. Credit Report Credit Score Components How Credit Scoring Helps You 10 Things that Hurt Your Credit

Understanding Your Credit Report

Understanding Your Credit Report What is credit? Credit is the use of someone else s money in exchange for a promise to pay it back on a given date. There are two major types of credit: Revolving and Installment.

Understanding Your Credit Report What is credit? Credit is the use of someone else s money in exchange for a promise to pay it back on a given date. There are two major types of credit: Revolving and Installment.

Getting Smart about Credit

Getting Smart about Credit LESSON PREPARATION AND TEACHER INFORMATION Lesson Summary: This lesson is intended for high school students during a 40 minute time period. The lesson teaches students about

Getting Smart about Credit LESSON PREPARATION AND TEACHER INFORMATION Lesson Summary: This lesson is intended for high school students during a 40 minute time period. The lesson teaches students about

Participant Guide Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum

To Your Credit Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Who Poses the Most Credit Risk? 1 How to Get a Free Credit Report Once a Year 2 Annual

To Your Credit Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Who Poses the Most Credit Risk? 1 How to Get a Free Credit Report Once a Year 2 Annual

Why Credit is Important

Page 1 Why Credit is Important Page 6 How to Protect Yourself from Identity Theft Page 7 Cosigning and Money Lending Tips Page 8 How to Avoid Credit Card Interest Why Credit is Important Learning to build

Page 1 Why Credit is Important Page 6 How to Protect Yourself from Identity Theft Page 7 Cosigning and Money Lending Tips Page 8 How to Avoid Credit Card Interest Why Credit is Important Learning to build

Understanding Your Credit Report

What Is a Credit Report? Understanding Your Credit Report A credit report is a record of your history of credit-card debt and other loan repayment. It shows how much debt you have and if you pay on or

What Is a Credit Report? Understanding Your Credit Report A credit report is a record of your history of credit-card debt and other loan repayment. It shows how much debt you have and if you pay on or

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account.

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

JUST BEGINNING. Your financial life is. I m Buying a Car!

Your financial life is JUST BEGINNING. The decisions you make now will put a steering wheel and a credit card in your hands. But they will also affect your financial future. Your choices may even prevent

Your financial life is JUST BEGINNING. The decisions you make now will put a steering wheel and a credit card in your hands. But they will also affect your financial future. Your choices may even prevent

ATTORNEY ADVERTISING

ATTORNEY ADVERTISING Some jobs are best not delegated. Improving your credit score and putting your finances in shape are best handled by you not by an ill-informed, uncaring, and heavily-marketed debt-settlement

ATTORNEY ADVERTISING Some jobs are best not delegated. Improving your credit score and putting your finances in shape are best handled by you not by an ill-informed, uncaring, and heavily-marketed debt-settlement

How to Use Credit Cards to Help You

How to Use Credit Cards to Help You Pay credit card balance every month Pay credit card bills on time Apply for credit only when needed Keep track of all charges- keep receipts Check monthly credit card

How to Use Credit Cards to Help You Pay credit card balance every month Pay credit card bills on time Apply for credit only when needed Keep track of all charges- keep receipts Check monthly credit card

CreditAbility: Build a Strong Credit History. Brought to you by Duke University FCU

: Build a Strong Credit History Brought to you by Duke University FCU Seminar Objectives Learn: Who needs to build good credit, and why Significance of credit report and score How to establish credit if

: Build a Strong Credit History Brought to you by Duke University FCU Seminar Objectives Learn: Who needs to build good credit, and why Significance of credit report and score How to establish credit if

MOBILOIL FCU 1810 N Major Dr Beaumont, TX 77713 CREDIT CARD AGREEMENT AND DISCLOSURE STATEMENT

MOBILOIL FCU 1810 N Major Dr Beaumont, TX 77713 CREDIT CARD AGREEMENT AND DISCLOSURE STATEMENT Annual Percentage Rate (APR) for purchases and cash advances 2.99% fixed rate (purchases and/or cash advances)

MOBILOIL FCU 1810 N Major Dr Beaumont, TX 77713 CREDIT CARD AGREEMENT AND DISCLOSURE STATEMENT Annual Percentage Rate (APR) for purchases and cash advances 2.99% fixed rate (purchases and/or cash advances)

PRACTICAL MONEY GUIDES CREDIT HISTORY. Your credit history and how it affects your future

PRACTICAL MONEY GUIDES CREDIT HISTORY Your credit history and how it affects your future YOUR CREDIT HISTORY THE RECORD OF HOW WELL YOU HANDLE CREDIT To get a glimpse of your financial future, many businesses

PRACTICAL MONEY GUIDES CREDIT HISTORY Your credit history and how it affects your future YOUR CREDIT HISTORY THE RECORD OF HOW WELL YOU HANDLE CREDIT To get a glimpse of your financial future, many businesses

UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor

By Bill Taylor") UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor Most studies about consumer debt have only focused on credit cards and mortgages. However, personal debt also may include medical expenses, school

UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor Most studies about consumer debt have only focused on credit cards and mortgages. However, personal debt also may include medical expenses, school

Understanding, managing, and rebuilding your credit

Understanding, managing, and rebuilding your credit Objective Bank of America is committed to providing information that will help you understand the effect credit can have on lending, and what you can

Understanding, managing, and rebuilding your credit Objective Bank of America is committed to providing information that will help you understand the effect credit can have on lending, and what you can

Financial payment profile Fair Isaac Corporation (FICO) 300 to 850 the higher, the better

300 to 850 the higher, the better") What is a credit score? Financial payment profile Fair Isaac Corporation (FICO) 300 to 850 the higher, the better National distribution of FICO scores What a low score could cost you? Tens of thousands

What is a credit score? Financial payment profile Fair Isaac Corporation (FICO) 300 to 850 the higher, the better National distribution of FICO scores What a low score could cost you? Tens of thousands

Personal Money Management. Why and How we spend money and potential impacts to personal credit.

Personal Money Management Why and How we spend money and potential impacts to personal credit. Presentation Objectives Understanding Your Financial Personality Personal Credit Scores, impacts, tips, your

Personal Money Management Why and How we spend money and potential impacts to personal credit. Presentation Objectives Understanding Your Financial Personality Personal Credit Scores, impacts, tips, your

Financial Management

I. Banking landscape today In the past year alone, banks have taken many actions to make up for lost profits, including eliminating free checking, raising fees, and pushing customers to buy more financial

I. Banking landscape today In the past year alone, banks have taken many actions to make up for lost profits, including eliminating free checking, raising fees, and pushing customers to buy more financial

Lesson Module 3: Defensive Spending Tackling Credit & Debit Cards

Lesson Module 3: Defensive Spending Tackling Credit & Debit Cards Module 3 Overview Debit cards can be a very safe and convenient way to make purchases. But since money spent on a debit card comes right

Lesson Module 3: Defensive Spending Tackling Credit & Debit Cards Module 3 Overview Debit cards can be a very safe and convenient way to make purchases. But since money spent on a debit card comes right

Participant Guide Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum

Check It Out Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Determining Your Checking Account Needs 1 Checking Account Fees 2 Practice Exercise: Choosing

Check It Out Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Determining Your Checking Account Needs 1 Checking Account Fees 2 Practice Exercise: Choosing

New Direction. Within Your Reach! A Financial Literacy Training Presentation for our Members by:

New Direction Within Your Reach! A Financial Literacy Training Presentation for our Members by: Maintaining a Checking Account Keeping track of Deposits and Withdrawals Why Should I Keep a Check Register?

New Direction Within Your Reach! A Financial Literacy Training Presentation for our Members by: Maintaining a Checking Account Keeping track of Deposits and Withdrawals Why Should I Keep a Check Register?

Table of Contents. Money Smart for Adults Curriculum Page 2 of 21

Table of Contents Checking In... 3 Pre-Test... 4 What Is Credit?... 6 Collateral... 6 Types of Loans... 7 Activity 1: Which Loan Is Best?... 8 The Cost of Credit... 9 Activity 2: Borrowing Money Responsibly...

Table of Contents Checking In... 3 Pre-Test... 4 What Is Credit?... 6 Collateral... 6 Types of Loans... 7 Activity 1: Which Loan Is Best?... 8 The Cost of Credit... 9 Activity 2: Borrowing Money Responsibly...

NOTES. 12 Your Credit Score Your Credit Score 1 CONTENTS:

12 Your Credit Score Your Credit Score 1 NOTES CONTENTS: Introduction...2 The History of Credit Scoring...2 Why Your Credit Score is So Important...3 The Five Factors of Credit Scoring...3 How Does a Low

12 Your Credit Score Your Credit Score 1 NOTES CONTENTS: Introduction...2 The History of Credit Scoring...2 Why Your Credit Score is So Important...3 The Five Factors of Credit Scoring...3 How Does a Low

Be Credit Wise Credit is a way of having something now and paying for it later. Many

Be Credit Wise Credit is a way of having something now and paying for it later. Many of us want to take advantage of flexibility in our spending plans by using credit. Credit isn t free; it s paid for

Be Credit Wise Credit is a way of having something now and paying for it later. Many of us want to take advantage of flexibility in our spending plans by using credit. Credit isn t free; it s paid for

Credit ~ The Basics Participant s Guide

1 Credit ~ The Basics Participant s Guide Table of Contents Welcome Pre-Test What is Credit & Why is it Important? Types of Loans The Cost of Credit The Four C s of Credit Credit Reports Credit Scores

1 Credit ~ The Basics Participant s Guide Table of Contents Welcome Pre-Test What is Credit & Why is it Important? Types of Loans The Cost of Credit The Four C s of Credit Credit Reports Credit Scores

Financial Empowerment Curriculum. Moving Ahead Through Financial Management. Module Three: Mastering Credit Basics

Financial Empowerment Curriculum Moving Ahead Through Financial Management Mastering Credit Basics Reviewing, Understanding and Improving Your Credit Module 3: Mastering Credit Basics Time Clock: 11:00-12:00

Financial Empowerment Curriculum Moving Ahead Through Financial Management Mastering Credit Basics Reviewing, Understanding and Improving Your Credit Module 3: Mastering Credit Basics Time Clock: 11:00-12:00

Facts On Credit Bureaus

Facts On Credit Bureaus The following information relates to the understanding and use of a credit score. Listed are details regarding the determination of a credit score, how you can find out what your

Facts On Credit Bureaus The following information relates to the understanding and use of a credit score. Listed are details regarding the determination of a credit score, how you can find out what your

Designing Your Budget

2 Designing Your Budget Budgeting is needed to get the most mileage out of your income. It is your road map for managing your money. Planning your spending is called Budgeting. Smart investing@your library

2 Designing Your Budget Budgeting is needed to get the most mileage out of your income. It is your road map for managing your money. Planning your spending is called Budgeting. Smart investing@your library

Financial Empowerment Curriculum Moving Ahead Through Financial Management. Workshop Credit Overview

Financial Empowerment Curriculum Moving Ahead Through Financial Management Workshop Credit Overview 1 Workshop Objectives Explain why credit is important. Access and read a copy of your credit report.

Financial Empowerment Curriculum Moving Ahead Through Financial Management Workshop Credit Overview 1 Workshop Objectives Explain why credit is important. Access and read a copy of your credit report.

Keys to Your Financial Future Step 2.5: Credit Repair or Building Plan

46 MODULE 2: Good credit Keys to Your Financial Future Step 2.5: Credit Repair or Building Plan Use the questions to develop your credit repair or building plan. Do you need to repair your credit history?

46 MODULE 2: Good credit Keys to Your Financial Future Step 2.5: Credit Repair or Building Plan Use the questions to develop your credit repair or building plan. Do you need to repair your credit history?

Your Credit Report. 595 Market Street, 16th Floor San Francisco, CA 94105 888.456.2227 www.balancepro.net

Your Credit Report 750. 670. 620. 575. You may not think about them every day, but your credit report and the three little digits that make up your credit score probably influence your life in many ways.

Your Credit Report 750. 670. 620. 575. You may not think about them every day, but your credit report and the three little digits that make up your credit score probably influence your life in many ways.

Volume 1 Taking the first steps

Volume 1 Taking the first steps Welcome to Your Money A guide to managing Take the first step in changing your financial future. Call InCharge Debt Solutions today at 1.877.544.7766 or visit www.incharge.org

Volume 1 Taking the first steps Welcome to Your Money A guide to managing Take the first step in changing your financial future. Call InCharge Debt Solutions today at 1.877.544.7766 or visit www.incharge.org

Drowning in the Sea of Credit Card Debt Tips for Getting Out of Debt and Staying Out 19 TAC Chapter 74.34 (b) (1)

(1)") Drowning in the Sea of Credit Card Debt Tips for Getting Out of Debt and Staying Out 19 TAC Chapter 74.34 (b) (1) Millions of Americans have set sail on the Sea of Credit Card Debt with good intentions

Drowning in the Sea of Credit Card Debt Tips for Getting Out of Debt and Staying Out 19 TAC Chapter 74.34 (b) (1) Millions of Americans have set sail on the Sea of Credit Card Debt with good intentions

Understanding a Credit Report! April 21, 2011. New York City Department of Consumer Affairs. All rights reserved.

Understanding a Credit Report! Questions to Think About What are the different types of credit and why is credit important? What is a credit report? How does credit impact future financial goals? 3 What

Understanding a Credit Report! Questions to Think About What are the different types of credit and why is credit important? What is a credit report? How does credit impact future financial goals? 3 What

Familiarize yourself with laws that authorize and regulate vehicle dealership financing and leasing.

W ith prices averaging more than $28,000 for a new vehicle and $15,000 for a used vehicle, most consumers need financing or leasing to acquire a vehicle. In some cases, buyers use direct lending: they

W ith prices averaging more than $28,000 for a new vehicle and $15,000 for a used vehicle, most consumers need financing or leasing to acquire a vehicle. In some cases, buyers use direct lending: they

It lets you pay for expenses you could not afford with cash, such as a college education, a new vehicle, furniture or a home.

USING CREDIT WISELY Credit Is An Important Financial Tool It lets you pay for expenses you could not afford with cash, such as a college education, a new vehicle, furniture or a home.

USING CREDIT WISELY Credit Is An Important Financial Tool It lets you pay for expenses you could not afford with cash, such as a college education, a new vehicle, furniture or a home.

WHAT IS A CREDIT CARD?

WHAT IS A CREDIT CARD? A credit card allows you to make purchases based on your promise to pay for the good and/or services. Credit cards allow the holder to get something today and pay for it later. BEFORE

WHAT IS A CREDIT CARD? A credit card allows you to make purchases based on your promise to pay for the good and/or services. Credit cards allow the holder to get something today and pay for it later. BEFORE

The Truth About Credit Repair

The Truth About Credit Repair Discover The Insider Secrets Of How The Credit System Really Works and How To Beat The Credit Bureaus At Their Own Game. David Shapiro Esq. Applied Credit Repair Solutions

The Truth About Credit Repair Discover The Insider Secrets Of How The Credit System Really Works and How To Beat The Credit Bureaus At Their Own Game. David Shapiro Esq. Applied Credit Repair Solutions

Your Credit Repair Solution

Your Credit Repair Solution Introduction Your Credit Report Solution will help you understand that there is help available for fixing your credit. Even though you might feel as though you are alone and

Your Credit Repair Solution Introduction Your Credit Report Solution will help you understand that there is help available for fixing your credit. Even though you might feel as though you are alone and

CREDIT BASICS About your credit score

CREDIT BASICS About your credit score Your credit score influences the credit that s available to you and the terms (interest rate, etc.) that lenders offer you. It s a vital part of your credit health.

CREDIT BASICS About your credit score Your credit score influences the credit that s available to you and the terms (interest rate, etc.) that lenders offer you. It s a vital part of your credit health.

Introduction. Purpose. Student Introductions. Agenda and Ground Rules. Objectives

Introduction Instructor and student introductions. Module overview. 1 2 Your name. Student Introductions Your expectations, questions, and concerns about credit. Purpose will: Show you how to read a credit

Introduction Instructor and student introductions. Module overview. 1 2 Your name. Student Introductions Your expectations, questions, and concerns about credit. Purpose will: Show you how to read a credit