A Multiplicative Seasonal Box-Jenkins Model to Nigerian Stock Prices

|

|

|

- Everett Burke

- 9 years ago

- Views:

Transcription

1 A Multiplicative Seasonal Box-Jenkins Model to Nigerian Stock Prices Ette Harrison Etuk Department of Mathematics/Computer Science, Rivers State University of Science and Technology, Nigeria ABSTRACT Time series analysis of Nigerian Stock Prices Data is done. The data used is monthly from 1987 to The time plot reveals a negative trend and no clear seasonality. A multiplicative seasonal model is suggestive given seasonality that tends to increase with time. Seasonal differencing once produced a series with a slightly positive trend but still with no discernible stationarity. A non-seasonal differencing of the seasonal differences yielded a series with no trend but with a correlogram revealing stationarity of order 12 and a seasonal moving average component. A multiplicative seasonal autoregressive integrated moving average (ARIMA) model, (0, 1, 1)x(0, 1, 1) 12, is fitted to the series. Keywords: Stock Prices, Seasonal Time Series, ARIMA model, Nigeria 1. INTRODUCTION A time series is defined as a set of data collected sequentially in time. It has the property that neighbouring values are correlated. This tendency is called autocorrelation. A time series is said to be stationary if it has a constant mean and variance. Moreover the autocorrelation is a function of the lag separating the correlated values and called the autocorrelation function (ACF). A stationary time series {X t } is said to follow an autoregressive moving average model of orders p and q (designated ARMA(p, q)) if it satisfies the following difference equation Or X t - 1 X t-1-2 X t p X t-p = t + 1 t t q t-q (1) A(L)X t = B(L) t (2) where { t }is a sequence of uncorrelated random variables with zero mean and constant variance, called a white noise process, and the i s and j s constants; A(L) = 1-1 L - 2 L p L p and B(L) = L + 2 L q L q and L the backward shift operator defined by L k X t = X t-k. If p = 0, the model (1) becomes a moving average model of order q (designated MA(q)). If, however, q = 0 it becomes an autoregressive process of order p (designated AR(p)). An AR(p) model may be defined as a model whereby a current value of the time series X t depends on the immediate past p values: X t-1, X t-2,, X t-p. On the other hand an MA(q) model is such that the current value X t is a linear combination of immediate past values of the white noise process: t-1, t-2,, t-q. Apart from stationarity, invertibility is another important requirement for a time series. It refers to the property whereby the covariance structure of the series is unique (Priestley, 1981). Moreover it allows for meaningful association of current events with past history of the series (Box and Jenkins, 1976). An AR(p) model may be more specifically written as X t + p1 X t-1 + p2 X t pp X t-p = t Then the sequence of the last coefficients { ii } is called the partial autocorrelation function (PACF) of {Xt}. The ACF of an MA(q) model cuts off after lag q whereas that of an AR(p) model is a combination of sinusoidals dying off slowly. On the other hand the PACF of an MA(q) model dies off slowly whereas that of an AR(p) model cuts off after lag p. AR and MA models are known to exhibit some duality relationships. These include: 1. A finite order AR model is equivalent to an infinite order MA model. 2. A finite order MA model is equivalent to an infinite order AR model. 1

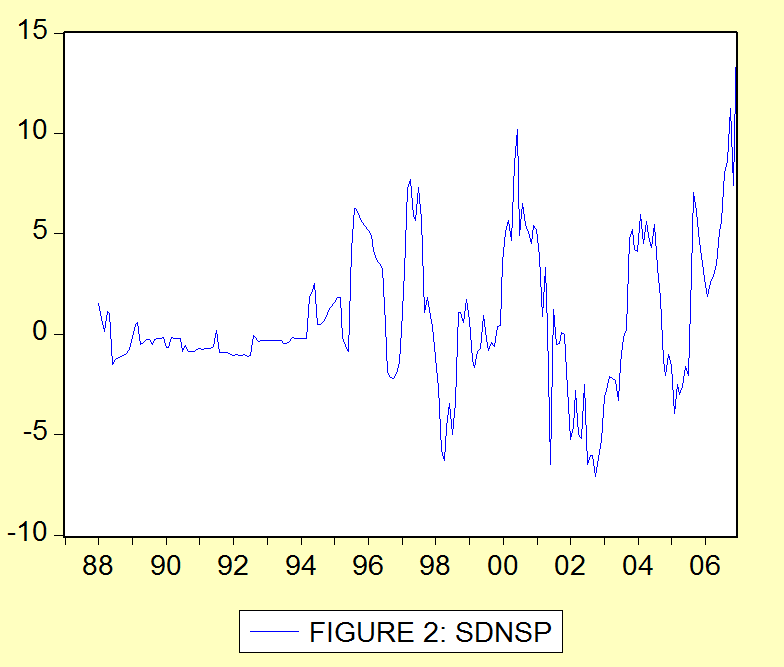

2 3. The ACF of an AR model exhibits the same behaviour as the PACF of an MA model. 4. The PACF of an AR model exhibits the same behaviour as the ACF of an MA model. 5. An AR model is always invertible but is stationary if A(L) = 0 has zeros outside the unit circle. 6. An MA model is always stationary but is invertible if B(L) = 0 has zeros outside the unit circle. Parametric parsimony consideration in model building entails preference for the mixed ARMA fit to either the pure AR or the pure MA fit. Stationarity and invertibility conditions for model (1) or (2) are that the equations A(L) = 0 and B(L) = 0 should have roots outside the unit circle respectively. Often, in practice, a time series is non-stationary. Box and Jenkins (1976) proposed that differencing of appropriate order could render a non-stationary series {Xt} stationary. Let degree of differencing necessary for stationarity be d. Such a series {Xt} may be modeled as A(L) d X t = B(L) t (3) where = 1 - L and in which case A(L) d = 0 shall have unit roots d times. Then differencing to degree d renders the series stationary.the model (3) is said to be an autoregressive integrated moving average model of orders p, d and q and designated ARIMA(p, d, q). 2. SEASONAL ARIMA MODELS A time series is said to be seasonal of order d if there exists a tendency for the series to exhibit periodic behaviour after every time interval d. Traditional time series methods involve the identification, unscrambling and estimation of the traditional components: secular trend, seasonal component, cyclical component and the irregular movement. For forecasting purpose, they are reintegrated. Such techniques could be quite misleading. The time series {X t } is said to follow a multiplicative (p, d, q)x(p, D, Q) s seasonal ARIMA model if A(L) (L s ) d D sx t = B(L) (B s ) t (4) where and are polynomials of order P and Q respectively. That is, (L s ) = L s + + P L sp (5) (L s ) = L s + + q L sq (6) where the i and the j are constants such that the zeros of the equations (5) and (6) are all outside the unit circle for stationarity or invertibility respectively. Equation (5) represents the autoregressive operator whereas (6) represents the moving average operator. Existence of a seasonal nature is often evident from the time plot. Moreover for a seasonal series the ACF or correlogram exhibits a spike at the seasonal lag. Box and Jenkins (1976) and Madsen (2008) are a few authors that have written extensively on such models. A knowledge of the theoretical properties of the models provides basis for their identification and estimation. The purpose of this paper is to fit a seasonal ARIMA model to the Nigerian Stock Prices (NSP). 3. MATERIALS AND METHODS The data for this work are monthly Stock Prices from 1987 to 2006 obtainable from the Nigerian Stock Exchange Office, Port Harcourt, Nigeria Determination of the orders d, D, P, q and Q: Seasonal differencing is necessary to remove the seasonal trend. If there is secular trend non-seasonal differencing will be necessary. To avoid undue model complexity it has been advised that orders of differencing d and D should add up to at most 2 (i.e. d + D < 3). If the ACF of the differenced series has a positive spike at the seasonal lag then a seasonal AR component is suggestive; if it has a negative spike then a seasonal MA term is suggestive 2

3 As already mentioned above, an AR(p) model has a PACF that truncates at lag p and an MA(q) has an ACF that truncates at lag q. In practice 2/ n where n is the sample size are the non-significance limits for both functions Model Estimation The involvement of the white noise process in an ARIMA model entails a nonlinear iterative process in the estimation of the parameters. An optimization criterion like least error sum of squares, maximum likelihood or maximum entropy is used. An initial estimate is usually used. Each iteration is expected to be an improvement of the last one until the estimate converges to an optimal one. However, for pure AR and pure MA models linear optimization techniques exist (See for example, Box and Jenkins(1976), Oyetunji(1985)). There are attempts to adopt linear methods to estimate ARMA models (See for example, Etuk(1987, 1998)). We shall use Eviews software which employs the least squares approach involving nonlinear iterative techniques Diagnostic Checking The model that is fitted to the data should be tested for goodness-of-fit. We shall do some analysis of the residuals of the model. If the model is correct, the residuals would be uncorrelated and would follow a normal distribution with mean zero and constant variance. The autocorrelations of the residuals should not be significantly different from zero. 4. RESULTS AND DISCUSSION The time plot of the original series NSP in Figure 1 shows a slightly positive trend and no clear seasonality. However the seasonality increases with time indicating a multiplicative seasonal model. Seasonal (i.e. 12- month) differencing of the series produces a series SDNSP with a slightly positive trend but with no clear seasonality (see Figure 2). Non-seasonal differencing of SDNSP yields a series DSDNSP with no trend and no clear seasonality (See Figure 3). However, its ACF in Figure 4 has a negative spike at lag 12 revealing a seasonality of lag 12 and a seasonal MA component of order one to the model. We propose the (0, 1, 1)x(0, 1, 1) 12 model DSDNSP t = 1 t t t-13 (7) The model as summarized in Table 1 is given by DSDNSP t = t t t-13 + t (8) ( ) ( ) ( ) The estimation involved 28 iterations. Only the last two coefficients are significantly different from zero, each being larger than twice its standard error. The correlogram of the residuals in Figure 5 depicts the adequacy of the model. Virtually all the residual autocorrelations are not significantly different from zero. Moreover the histogram of the residuals in Figure 6 shows that they are normally distributed with zero mean further indicating model adequacy. 5. CONCLUSION We conclude that Nigerian Stock Price Data follow an adequate (0, 1, 1)x(0, 1, 1) 12 model. REFERENCES 1. Box, G. E. P. and Jenkins, G. M. (1976). Time Series Analysis, Forecasting and Control, Holden-Day, San Francisco. 2. Etuk, E. H. (1987). On the Selection of Autoregressive Moving Average Models. An unpublished Ph. D. Thesis, Department of Statistics, University of Ibadan, Nigeria. 3. Etuk, E. H. (1998). An Autoregressive Integrated Moving Average (ARIMA) Simulation Model: A Case Study. Discovery and Innovation, Volume 10, Nos. 1 & 2: pp Madsen, H. (2008). Time Series Analysis, Chapman & Hall/CRC, London. 5. Oyetunji, O. B. (1985). Inverse Autocorrelations and Moving Average Time Series Modelling. Journal of Official Statistics, Volume : pp Priestley, M. B. (1981). Spectral Analysis and Time Series. Academic Press, London. 3

4 4

5 FIGURE 4: CORRELOGRAM OF DSDNSP 5

6 TABLE 1: MODEL ESTIMATION FIGURE 5: CORRELOGRAM OF RESIDUALS 6

7 FIGURE 6: HISTOGRAM OF RESIDUALS 7

Application of Seasonal Box-Jenkins Techniques for Modelling Monthly Internally Generated Revenue of Rivers State of Nigeria

Application of Seasonal Box-Jenkins Techniques for Modelling Monthly Internally Generated Revenue of Rivers State of Nigeria Ette Harrison Etuk 1, Innocent Uchenna Amadi 2, Igboye Simon Aboko 3, Mazi Yellow

Application of Seasonal Box-Jenkins Techniques for Modelling Monthly Internally Generated Revenue of Rivers State of Nigeria Ette Harrison Etuk 1, Innocent Uchenna Amadi 2, Igboye Simon Aboko 3, Mazi Yellow

TIME SERIES ANALYSIS

TIME SERIES ANALYSIS L.M. BHAR AND V.K.SHARMA Indian Agricultural Statistics Research Institute Library Avenue, New Delhi-0 02 [email protected]. Introduction Time series (TS) data refers to observations

TIME SERIES ANALYSIS L.M. BHAR AND V.K.SHARMA Indian Agricultural Statistics Research Institute Library Avenue, New Delhi-0 02 [email protected]. Introduction Time series (TS) data refers to observations

Time Series - ARIMA Models. Instructor: G. William Schwert

APS 425 Fall 25 Time Series : ARIMA Models Instructor: G. William Schwert 585-275-247 [email protected] Topics Typical time series plot Pattern recognition in auto and partial autocorrelations

APS 425 Fall 25 Time Series : ARIMA Models Instructor: G. William Schwert 585-275-247 [email protected] Topics Typical time series plot Pattern recognition in auto and partial autocorrelations

TIME SERIES ANALYSIS

TIME SERIES ANALYSIS Ramasubramanian V. I.A.S.R.I., Library Avenue, New Delhi- 110 012 [email protected] 1. Introduction A Time Series (TS) is a sequence of observations ordered in time. Mostly these

TIME SERIES ANALYSIS Ramasubramanian V. I.A.S.R.I., Library Avenue, New Delhi- 110 012 [email protected] 1. Introduction A Time Series (TS) is a sequence of observations ordered in time. Mostly these

Univariate and Multivariate Methods PEARSON. Addison Wesley

Time Series Analysis Univariate and Multivariate Methods SECOND EDITION William W. S. Wei Department of Statistics The Fox School of Business and Management Temple University PEARSON Addison Wesley Boston

Time Series Analysis Univariate and Multivariate Methods SECOND EDITION William W. S. Wei Department of Statistics The Fox School of Business and Management Temple University PEARSON Addison Wesley Boston

Some useful concepts in univariate time series analysis

Some useful concepts in univariate time series analysis Autoregressive moving average models Autocorrelation functions Model Estimation Diagnostic measure Model selection Forecasting Assumptions: 1. Non-seasonal

Some useful concepts in univariate time series analysis Autoregressive moving average models Autocorrelation functions Model Estimation Diagnostic measure Model selection Forecasting Assumptions: 1. Non-seasonal

Time Series Analysis

JUNE 2012 Time Series Analysis CONTENT A time series is a chronological sequence of observations on a particular variable. Usually the observations are taken at regular intervals (days, months, years),

JUNE 2012 Time Series Analysis CONTENT A time series is a chronological sequence of observations on a particular variable. Usually the observations are taken at regular intervals (days, months, years),

Sales forecasting # 2

Sales forecasting # 2 Arthur Charpentier [email protected] 1 Agenda Qualitative and quantitative methods, a very general introduction Series decomposition Short versus long term forecasting

Sales forecasting # 2 Arthur Charpentier [email protected] 1 Agenda Qualitative and quantitative methods, a very general introduction Series decomposition Short versus long term forecasting

Time Series Analysis

Time Series Analysis Identifying possible ARIMA models Andrés M. Alonso Carolina García-Martos Universidad Carlos III de Madrid Universidad Politécnica de Madrid June July, 2012 Alonso and García-Martos

Time Series Analysis Identifying possible ARIMA models Andrés M. Alonso Carolina García-Martos Universidad Carlos III de Madrid Universidad Politécnica de Madrid June July, 2012 Alonso and García-Martos

Advanced Forecasting Techniques and Models: ARIMA

Advanced Forecasting Techniques and Models: ARIMA Short Examples Series using Risk Simulator For more information please visit: www.realoptionsvaluation.com or contact us at: [email protected]

Advanced Forecasting Techniques and Models: ARIMA Short Examples Series using Risk Simulator For more information please visit: www.realoptionsvaluation.com or contact us at: [email protected]

Luciano Rispoli Department of Economics, Mathematics and Statistics Birkbeck College (University of London)

") Luciano Rispoli Department of Economics, Mathematics and Statistics Birkbeck College (University of London) 1 Forecasting: definition Forecasting is the process of making statements about events whose

Luciano Rispoli Department of Economics, Mathematics and Statistics Birkbeck College (University of London) 1 Forecasting: definition Forecasting is the process of making statements about events whose

Graphical Tools for Exploring and Analyzing Data From ARIMA Time Series Models

Graphical Tools for Exploring and Analyzing Data From ARIMA Time Series Models William Q. Meeker Department of Statistics Iowa State University Ames, IA 50011 January 13, 2001 Abstract S-plus is a highly

Graphical Tools for Exploring and Analyzing Data From ARIMA Time Series Models William Q. Meeker Department of Statistics Iowa State University Ames, IA 50011 January 13, 2001 Abstract S-plus is a highly

Using JMP Version 4 for Time Series Analysis Bill Gjertsen, SAS, Cary, NC

Using JMP Version 4 for Time Series Analysis Bill Gjertsen, SAS, Cary, NC Abstract Three examples of time series will be illustrated. One is the classical airline passenger demand data with definite seasonal

Using JMP Version 4 for Time Series Analysis Bill Gjertsen, SAS, Cary, NC Abstract Three examples of time series will be illustrated. One is the classical airline passenger demand data with definite seasonal

Forecasting of Paddy Production in Sri Lanka: A Time Series Analysis using ARIMA Model

Tropical Agricultural Research Vol. 24 (): 2-3 (22) Forecasting of Paddy Production in Sri Lanka: A Time Series Analysis using ARIMA Model V. Sivapathasundaram * and C. Bogahawatte Postgraduate Institute

Tropical Agricultural Research Vol. 24 (): 2-3 (22) Forecasting of Paddy Production in Sri Lanka: A Time Series Analysis using ARIMA Model V. Sivapathasundaram * and C. Bogahawatte Postgraduate Institute

How To Model A Series With Sas

Chapter 7 Chapter Table of Contents OVERVIEW...193 GETTING STARTED...194 TheThreeStagesofARIMAModeling...194 IdentificationStage...194 Estimation and Diagnostic Checking Stage...... 200 Forecasting Stage...205

Chapter 7 Chapter Table of Contents OVERVIEW...193 GETTING STARTED...194 TheThreeStagesofARIMAModeling...194 IdentificationStage...194 Estimation and Diagnostic Checking Stage...... 200 Forecasting Stage...205

Threshold Autoregressive Models in Finance: A Comparative Approach

University of Wollongong Research Online Applied Statistics Education and Research Collaboration (ASEARC) - Conference Papers Faculty of Informatics 2011 Threshold Autoregressive Models in Finance: A Comparative

University of Wollongong Research Online Applied Statistics Education and Research Collaboration (ASEARC) - Conference Papers Faculty of Informatics 2011 Threshold Autoregressive Models in Finance: A Comparative

9th Russian Summer School in Information Retrieval Big Data Analytics with R

9th Russian Summer School in Information Retrieval Big Data Analytics with R Introduction to Time Series with R A. Karakitsiou A. Migdalas Industrial Logistics, ETS Institute Luleå University of Technology

9th Russian Summer School in Information Retrieval Big Data Analytics with R Introduction to Time Series with R A. Karakitsiou A. Migdalas Industrial Logistics, ETS Institute Luleå University of Technology

Time Series Analysis

Time Series Analysis Forecasting with ARIMA models Andrés M. Alonso Carolina García-Martos Universidad Carlos III de Madrid Universidad Politécnica de Madrid June July, 2012 Alonso and García-Martos (UC3M-UPM)

Time Series Analysis Forecasting with ARIMA models Andrés M. Alonso Carolina García-Martos Universidad Carlos III de Madrid Universidad Politécnica de Madrid June July, 2012 Alonso and García-Martos (UC3M-UPM)

Time Series Analysis

Time Series 1 April 9, 2013 Time Series Analysis This chapter presents an introduction to the branch of statistics known as time series analysis. Often the data we collect in environmental studies is collected

Time Series 1 April 9, 2013 Time Series Analysis This chapter presents an introduction to the branch of statistics known as time series analysis. Often the data we collect in environmental studies is collected

Time Series Analysis

Time Series Analysis Autoregressive, MA and ARMA processes Andrés M. Alonso Carolina García-Martos Universidad Carlos III de Madrid Universidad Politécnica de Madrid June July, 212 Alonso and García-Martos

Time Series Analysis Autoregressive, MA and ARMA processes Andrés M. Alonso Carolina García-Martos Universidad Carlos III de Madrid Universidad Politécnica de Madrid June July, 212 Alonso and García-Martos

Lecture 2: ARMA(p,q) models (part 3)

models (part 3)") Lecture 2: ARMA(p,q) models (part 3) Florian Pelgrin University of Lausanne, École des HEC Department of mathematics (IMEA-Nice) Sept. 2011 - Jan. 2012 Florian Pelgrin (HEC) Univariate time series Sept.

Lecture 2: ARMA(p,q) models (part 3) Florian Pelgrin University of Lausanne, École des HEC Department of mathematics (IMEA-Nice) Sept. 2011 - Jan. 2012 Florian Pelgrin (HEC) Univariate time series Sept.

Analysis and Computation for Finance Time Series - An Introduction

ECMM703 Analysis and Computation for Finance Time Series - An Introduction Alejandra González Harrison 161 Email: [email protected] Time Series - An Introduction A time series is a sequence of observations

ECMM703 Analysis and Computation for Finance Time Series - An Introduction Alejandra González Harrison 161 Email: [email protected] Time Series - An Introduction A time series is a sequence of observations

Energy Load Mining Using Univariate Time Series Analysis

Energy Load Mining Using Univariate Time Series Analysis By: Taghreed Alghamdi & Ali Almadan 03/02/2015 Caruth Hall 0184 Energy Forecasting Energy Saving Energy consumption Introduction: Energy consumption.

Energy Load Mining Using Univariate Time Series Analysis By: Taghreed Alghamdi & Ali Almadan 03/02/2015 Caruth Hall 0184 Energy Forecasting Energy Saving Energy consumption Introduction: Energy consumption.

Time Series Analysis and Forecasting

Time Series Analysis and Forecasting Math 667 Al Nosedal Department of Mathematics Indiana University of Pennsylvania Time Series Analysis and Forecasting p. 1/11 Introduction Many decision-making applications

Time Series Analysis and Forecasting Math 667 Al Nosedal Department of Mathematics Indiana University of Pennsylvania Time Series Analysis and Forecasting p. 1/11 Introduction Many decision-making applications

Time Series Analysis of Aviation Data

Time Series Analysis of Aviation Data Dr. Richard Xie February, 2012 What is a Time Series A time series is a sequence of observations in chorological order, such as Daily closing price of stock MSFT in

Time Series Analysis of Aviation Data Dr. Richard Xie February, 2012 What is a Time Series A time series is a sequence of observations in chorological order, such as Daily closing price of stock MSFT in

TIME-SERIES ANALYSIS, MODELLING AND FORECASTING USING SAS SOFTWARE

TIME-SERIES ANALYSIS, MODELLING AND FORECASTING USING SAS SOFTWARE Ramasubramanian V. IA.S.R.I., Library Avenue, Pusa, New Delhi 110 012 [email protected] 1. Introduction Time series (TS) data refers

TIME-SERIES ANALYSIS, MODELLING AND FORECASTING USING SAS SOFTWARE Ramasubramanian V. IA.S.R.I., Library Avenue, Pusa, New Delhi 110 012 [email protected] 1. Introduction Time series (TS) data refers

The SAS Time Series Forecasting System

The SAS Time Series Forecasting System An Overview for Public Health Researchers Charles DiMaggio, PhD College of Physicians and Surgeons Departments of Anesthesiology and Epidemiology Columbia University

The SAS Time Series Forecasting System An Overview for Public Health Researchers Charles DiMaggio, PhD College of Physicians and Surgeons Departments of Anesthesiology and Epidemiology Columbia University

Promotional Forecast Demonstration

Exhibit 2: Promotional Forecast Demonstration Consider the problem of forecasting for a proposed promotion that will start in December 1997 and continues beyond the forecast horizon. Assume that the promotion

Exhibit 2: Promotional Forecast Demonstration Consider the problem of forecasting for a proposed promotion that will start in December 1997 and continues beyond the forecast horizon. Assume that the promotion

Readers will be provided a link to download the software and Excel files that are used in the book after payment. Please visit http://www.xlpert.

Readers will be provided a link to download the software and Excel files that are used in the book after payment. Please visit http://www.xlpert.com for more information on the book. The Excel files are

Readers will be provided a link to download the software and Excel files that are used in the book after payment. Please visit http://www.xlpert.com for more information on the book. The Excel files are

1 Short Introduction to Time Series

ECONOMICS 7344, Spring 202 Bent E. Sørensen January 24, 202 Short Introduction to Time Series A time series is a collection of stochastic variables x,.., x t,.., x T indexed by an integer value t. The

ECONOMICS 7344, Spring 202 Bent E. Sørensen January 24, 202 Short Introduction to Time Series A time series is a collection of stochastic variables x,.., x t,.., x T indexed by an integer value t. The

Lecture 4: Seasonal Time Series, Trend Analysis & Component Model Bus 41910, Time Series Analysis, Mr. R. Tsay

Lecture 4: Seasonal Time Series, Trend Analysis & Component Model Bus 41910, Time Series Analysis, Mr. R. Tsay Business cycle plays an important role in economics. In time series analysis, business cycle

Lecture 4: Seasonal Time Series, Trend Analysis & Component Model Bus 41910, Time Series Analysis, Mr. R. Tsay Business cycle plays an important role in economics. In time series analysis, business cycle

Rob J Hyndman. Forecasting using. 11. Dynamic regression OTexts.com/fpp/9/1/ Forecasting using R 1

Rob J Hyndman Forecasting using 11. Dynamic regression OTexts.com/fpp/9/1/ Forecasting using R 1 Outline 1 Regression with ARIMA errors 2 Example: Japanese cars 3 Using Fourier terms for seasonality 4

Rob J Hyndman Forecasting using 11. Dynamic regression OTexts.com/fpp/9/1/ Forecasting using R 1 Outline 1 Regression with ARIMA errors 2 Example: Japanese cars 3 Using Fourier terms for seasonality 4

Univariate Time Series Analysis; ARIMA Models

Econometrics 2 Spring 25 Univariate Time Series Analysis; ARIMA Models Heino Bohn Nielsen of4 Outline of the Lecture () Introduction to univariate time series analysis. (2) Stationarity. (3) Characterizing

Econometrics 2 Spring 25 Univariate Time Series Analysis; ARIMA Models Heino Bohn Nielsen of4 Outline of the Lecture () Introduction to univariate time series analysis. (2) Stationarity. (3) Characterizing

Analysis of algorithms of time series analysis for forecasting sales

SAINT-PETERSBURG STATE UNIVERSITY Mathematics & Mechanics Faculty Chair of Analytical Information Systems Garipov Emil Analysis of algorithms of time series analysis for forecasting sales Course Work Scientific

SAINT-PETERSBURG STATE UNIVERSITY Mathematics & Mechanics Faculty Chair of Analytical Information Systems Garipov Emil Analysis of algorithms of time series analysis for forecasting sales Course Work Scientific

ITSM-R Reference Manual

ITSM-R Reference Manual George Weigt June 5, 2015 1 Contents 1 Introduction 3 1.1 Time series analysis in a nutshell............................... 3 1.2 White Noise Variance.....................................

ITSM-R Reference Manual George Weigt June 5, 2015 1 Contents 1 Introduction 3 1.1 Time series analysis in a nutshell............................... 3 1.2 White Noise Variance.....................................

FORECAST MODEL USING ARIMA FOR STOCK PRICES OF AUTOMOBILE SECTOR. Aloysius Edward. 1, JyothiManoj. 2

FORECAST MODEL USING ARIMA FOR STOCK PRICES OF AUTOMOBILE SECTOR Aloysius Edward. 1, JyothiManoj. 2 Faculty, Kristu Jayanti College, Autonomous, Bengaluru. Abstract There has been a growing interest in

FORECAST MODEL USING ARIMA FOR STOCK PRICES OF AUTOMOBILE SECTOR Aloysius Edward. 1, JyothiManoj. 2 Faculty, Kristu Jayanti College, Autonomous, Bengaluru. Abstract There has been a growing interest in

Forecasting model of electricity demand in the Nordic countries. Tone Pedersen

Forecasting model of electricity demand in the Nordic countries Tone Pedersen 3/19/2014 Abstract A model implemented in order to describe the electricity demand on hourly basis for the Nordic countries.

Forecasting model of electricity demand in the Nordic countries Tone Pedersen 3/19/2014 Abstract A model implemented in order to describe the electricity demand on hourly basis for the Nordic countries.

IBM SPSS Forecasting 22

IBM SPSS Forecasting 22 Note Before using this information and the product it supports, read the information in Notices on page 33. Product Information This edition applies to version 22, release 0, modification

IBM SPSS Forecasting 22 Note Before using this information and the product it supports, read the information in Notices on page 33. Product Information This edition applies to version 22, release 0, modification

COMP6053 lecture: Time series analysis, autocorrelation. [email protected]

COMP6053 lecture: Time series analysis, autocorrelation [email protected] Time series analysis The basic idea of time series analysis is simple: given an observed sequence, how can we build a model that

COMP6053 lecture: Time series analysis, autocorrelation [email protected] Time series analysis The basic idea of time series analysis is simple: given an observed sequence, how can we build a model that

JOHANNES TSHEPISO TSOKU NONOFO PHOKONTSI DANIEL METSILENG FORECASTING SOUTH AFRICAN GOLD SALES: THE BOX-JENKINS METHODOLOGY

DOI: 0.20472/IAC.205.08.3 JOHANNES TSHEPISO TSOKU North West University, South Africa NONOFO PHOKONTSI North West University, South Africa DANIEL METSILENG Department of Health, South Africa FORECASTING

DOI: 0.20472/IAC.205.08.3 JOHANNES TSHEPISO TSOKU North West University, South Africa NONOFO PHOKONTSI North West University, South Africa DANIEL METSILENG Department of Health, South Africa FORECASTING

Discrete Time Series Analysis with ARMA Models

Discrete Time Series Analysis with ARMA Models Veronica Sitsofe Ahiati ([email protected]) African Institute for Mathematical Sciences (AIMS) Supervised by Tina Marquardt Munich University of Technology,

Discrete Time Series Analysis with ARMA Models Veronica Sitsofe Ahiati ([email protected]) African Institute for Mathematical Sciences (AIMS) Supervised by Tina Marquardt Munich University of Technology,

USE OF ARIMA TIME SERIES AND REGRESSORS TO FORECAST THE SALE OF ELECTRICITY

Paper PO10 USE OF ARIMA TIME SERIES AND REGRESSORS TO FORECAST THE SALE OF ELECTRICITY Beatrice Ugiliweneza, University of Louisville, Louisville, KY ABSTRACT Objectives: To forecast the sales made by

Paper PO10 USE OF ARIMA TIME SERIES AND REGRESSORS TO FORECAST THE SALE OF ELECTRICITY Beatrice Ugiliweneza, University of Louisville, Louisville, KY ABSTRACT Objectives: To forecast the sales made by

Forecasting areas and production of rice in India using ARIMA model

International Journal of Farm Sciences 4(1) :99-106, 2014 Forecasting areas and production of rice in India using ARIMA model K PRABAKARAN and C SIVAPRAGASAM* Agricultural College and Research Institute,

International Journal of Farm Sciences 4(1) :99-106, 2014 Forecasting areas and production of rice in India using ARIMA model K PRABAKARAN and C SIVAPRAGASAM* Agricultural College and Research Institute,

Univariate Time Series Analysis; ARIMA Models

Econometrics 2 Fall 25 Univariate Time Series Analysis; ARIMA Models Heino Bohn Nielsen of4 Univariate Time Series Analysis We consider a single time series, y,y 2,..., y T. We want to construct simple

Econometrics 2 Fall 25 Univariate Time Series Analysis; ARIMA Models Heino Bohn Nielsen of4 Univariate Time Series Analysis We consider a single time series, y,y 2,..., y T. We want to construct simple

Studying Achievement

Journal of Business and Economics, ISSN 2155-7950, USA November 2014, Volume 5, No. 11, pp. 2052-2056 DOI: 10.15341/jbe(2155-7950)/11.05.2014/009 Academic Star Publishing Company, 2014 http://www.academicstar.us

Journal of Business and Economics, ISSN 2155-7950, USA November 2014, Volume 5, No. 11, pp. 2052-2056 DOI: 10.15341/jbe(2155-7950)/11.05.2014/009 Academic Star Publishing Company, 2014 http://www.academicstar.us

Time Series Analysis 1. Lecture 8: Time Series Analysis. Time Series Analysis MIT 18.S096. Dr. Kempthorne. Fall 2013 MIT 18.S096

Lecture 8: Time Series Analysis MIT 18.S096 Dr. Kempthorne Fall 2013 MIT 18.S096 Time Series Analysis 1 Outline Time Series Analysis 1 Time Series Analysis MIT 18.S096 Time Series Analysis 2 A stochastic

Lecture 8: Time Series Analysis MIT 18.S096 Dr. Kempthorne Fall 2013 MIT 18.S096 Time Series Analysis 1 Outline Time Series Analysis 1 Time Series Analysis MIT 18.S096 Time Series Analysis 2 A stochastic

MGT 267 PROJECT. Forecasting the United States Retail Sales of the Pharmacies and Drug Stores. Done by: Shunwei Wang & Mohammad Zainal

MGT 267 PROJECT Forecasting the United States Retail Sales of the Pharmacies and Drug Stores Done by: Shunwei Wang & Mohammad Zainal Dec. 2002 The retail sale (Million) ABSTRACT The present study aims

MGT 267 PROJECT Forecasting the United States Retail Sales of the Pharmacies and Drug Stores Done by: Shunwei Wang & Mohammad Zainal Dec. 2002 The retail sale (Million) ABSTRACT The present study aims

Time Series in Mathematical Finance

Instituto Superior Técnico (IST, Portugal) and CEMAT [email protected] European Summer School in Industrial Mathematics Universidad Carlos III de Madrid July 2013 Outline The objective of this short

Instituto Superior Técnico (IST, Portugal) and CEMAT [email protected] European Summer School in Industrial Mathematics Universidad Carlos III de Madrid July 2013 Outline The objective of this short

Forecasting Using Eviews 2.0: An Overview

Forecasting Using Eviews 2.0: An Overview Some Preliminaries In what follows it will be useful to distinguish between ex post and ex ante forecasting. In terms of time series modeling, both predict values

Forecasting Using Eviews 2.0: An Overview Some Preliminaries In what follows it will be useful to distinguish between ex post and ex ante forecasting. In terms of time series modeling, both predict values

Time Series Analysis: Basic Forecasting.

Time Series Analysis: Basic Forecasting. As published in Benchmarks RSS Matters, April 2015 http://web3.unt.edu/benchmarks/issues/2015/04/rss-matters Jon Starkweather, PhD 1 Jon Starkweather, PhD [email protected]

Time Series Analysis: Basic Forecasting. As published in Benchmarks RSS Matters, April 2015 http://web3.unt.edu/benchmarks/issues/2015/04/rss-matters Jon Starkweather, PhD 1 Jon Starkweather, PhD [email protected]

Time Series Analysis and Forecasting Methods for Temporal Mining of Interlinked Documents

Time Series Analysis and Forecasting Methods for Temporal Mining of Interlinked Documents Prasanna Desikan and Jaideep Srivastava Department of Computer Science University of Minnesota. @cs.umn.edu

Time Series Analysis and Forecasting Methods for Temporal Mining of Interlinked Documents Prasanna Desikan and Jaideep Srivastava Department of Computer Science University of Minnesota. @cs.umn.edu

3.1 Stationary Processes and Mean Reversion

3. Univariate Time Series Models 3.1 Stationary Processes and Mean Reversion Definition 3.1: A time series y t, t = 1,..., T is called (covariance) stationary if (1) E[y t ] = µ, for all t Cov[y t, y t

3. Univariate Time Series Models 3.1 Stationary Processes and Mean Reversion Definition 3.1: A time series y t, t = 1,..., T is called (covariance) stationary if (1) E[y t ] = µ, for all t Cov[y t, y t

APPLICATION OF THE VARMA MODEL FOR SALES FORECAST: CASE OF URMIA GRAY CEMENT FACTORY

APPLICATION OF THE VARMA MODEL FOR SALES FORECAST: CASE OF URMIA GRAY CEMENT FACTORY DOI: 10.2478/tjeb-2014-0005 Ramin Bashir KHODAPARASTI 1 Samad MOSLEHI 2 To forecast sales as reliably as possible is

APPLICATION OF THE VARMA MODEL FOR SALES FORECAST: CASE OF URMIA GRAY CEMENT FACTORY DOI: 10.2478/tjeb-2014-0005 Ramin Bashir KHODAPARASTI 1 Samad MOSLEHI 2 To forecast sales as reliably as possible is

PITFALLS IN TIME SERIES ANALYSIS. Cliff Hurvich Stern School, NYU

PITFALLS IN TIME SERIES ANALYSIS Cliff Hurvich Stern School, NYU The t -Test If x 1,..., x n are independent and identically distributed with mean 0, and n is not too small, then t = x 0 s n has a standard

PITFALLS IN TIME SERIES ANALYSIS Cliff Hurvich Stern School, NYU The t -Test If x 1,..., x n are independent and identically distributed with mean 0, and n is not too small, then t = x 0 s n has a standard

Turkey s Energy Demand

Current Research Journal of Social Sciences 1(3): 123-128, 2009 ISSN: 2041-3246 Maxwell Scientific Organization, 2009 Submitted Date: September 28, 2009 Accepted Date: October 12, 2009 Published Date:

Current Research Journal of Social Sciences 1(3): 123-128, 2009 ISSN: 2041-3246 Maxwell Scientific Organization, 2009 Submitted Date: September 28, 2009 Accepted Date: October 12, 2009 Published Date:

Software Review: ITSM 2000 Professional Version 6.0.

Lee, J. & Strazicich, M.C. (2002). Software Review: ITSM 2000 Professional Version 6.0. International Journal of Forecasting, 18(3): 455-459 (June 2002). Published by Elsevier (ISSN: 0169-2070). http://0-

Lee, J. & Strazicich, M.C. (2002). Software Review: ITSM 2000 Professional Version 6.0. International Journal of Forecasting, 18(3): 455-459 (June 2002). Published by Elsevier (ISSN: 0169-2070). http://0-

Traffic Safety Facts. Research Note. Time Series Analysis and Forecast of Crash Fatalities during Six Holiday Periods Cejun Liu* and Chou-Lin Chen

Traffic Safety Facts Research Note March 2004 DOT HS 809 718 Time Series Analysis and Forecast of Crash Fatalities during Six Holiday Periods Cejun Liu* and Chou-Lin Chen Summary This research note uses

Traffic Safety Facts Research Note March 2004 DOT HS 809 718 Time Series Analysis and Forecast of Crash Fatalities during Six Holiday Periods Cejun Liu* and Chou-Lin Chen Summary This research note uses

Chapter 9: Univariate Time Series Analysis

Chapter 9: Univariate Time Series Analysis In the last chapter we discussed models with only lags of explanatory variables. These can be misleading if: 1. The dependent variable Y t depends on lags of

Chapter 9: Univariate Time Series Analysis In the last chapter we discussed models with only lags of explanatory variables. These can be misleading if: 1. The dependent variable Y t depends on lags of

IBM SPSS Forecasting 21

IBM SPSS Forecasting 21 Note: Before using this information and the product it supports, read the general information under Notices on p. 107. This edition applies to IBM SPSS Statistics 21 and to all

IBM SPSS Forecasting 21 Note: Before using this information and the product it supports, read the general information under Notices on p. 107. This edition applies to IBM SPSS Statistics 21 and to all

THE SVM APPROACH FOR BOX JENKINS MODELS

REVSTAT Statistical Journal Volume 7, Number 1, April 2009, 23 36 THE SVM APPROACH FOR BOX JENKINS MODELS Authors: Saeid Amiri Dep. of Energy and Technology, Swedish Univ. of Agriculture Sciences, P.O.Box

REVSTAT Statistical Journal Volume 7, Number 1, April 2009, 23 36 THE SVM APPROACH FOR BOX JENKINS MODELS Authors: Saeid Amiri Dep. of Energy and Technology, Swedish Univ. of Agriculture Sciences, P.O.Box

Application of ARIMA models in soybean series of prices in the north of Paraná

78 Application of ARIMA models in soybean series of prices in the north of Paraná Reception of originals: 09/24/2012 Release for publication: 10/26/2012 Israel José dos Santos Felipe Mestrando em Administração

78 Application of ARIMA models in soybean series of prices in the north of Paraná Reception of originals: 09/24/2012 Release for publication: 10/26/2012 Israel José dos Santos Felipe Mestrando em Administração

Time Series Analysis

Time Series Analysis Lecture Notes for 475.726 Ross Ihaka Statistics Department University of Auckland April 14, 2005 ii Contents 1 Introduction 1 1.1 Time Series.............................. 1 1.2 Stationarity

Time Series Analysis Lecture Notes for 475.726 Ross Ihaka Statistics Department University of Auckland April 14, 2005 ii Contents 1 Introduction 1 1.1 Time Series.............................. 1 1.2 Stationarity

Forecasting the US Dollar / Euro Exchange rate Using ARMA Models

Forecasting the US Dollar / Euro Exchange rate Using ARMA Models LIUWEI (9906360) - 1 - ABSTRACT...3 1. INTRODUCTION...4 2. DATA ANALYSIS...5 2.1 Stationary estimation...5 2.2 Dickey-Fuller Test...6 3.

Forecasting the US Dollar / Euro Exchange rate Using ARMA Models LIUWEI (9906360) - 1 - ABSTRACT...3 1. INTRODUCTION...4 2. DATA ANALYSIS...5 2.1 Stationary estimation...5 2.2 Dickey-Fuller Test...6 3.

ARMA, GARCH and Related Option Pricing Method

ARMA, GARCH and Related Option Pricing Method Author: Yiyang Yang Advisor: Pr. Xiaolin Li, Pr. Zari Rachev Department of Applied Mathematics and Statistics State University of New York at Stony Brook September

ARMA, GARCH and Related Option Pricing Method Author: Yiyang Yang Advisor: Pr. Xiaolin Li, Pr. Zari Rachev Department of Applied Mathematics and Statistics State University of New York at Stony Brook September

Introduction to Time Series Analysis. Lecture 1.

Introduction to Time Series Analysis. Lecture 1. Peter Bartlett 1. Organizational issues. 2. Objectives of time series analysis. Examples. 3. Overview of the course. 4. Time series models. 5. Time series

Introduction to Time Series Analysis. Lecture 1. Peter Bartlett 1. Organizational issues. 2. Objectives of time series analysis. Examples. 3. Overview of the course. 4. Time series models. 5. Time series

Predicting Indian GDP. And its relation with FMCG Sales

Predicting Indian GDP And its relation with FMCG Sales GDP A Broad Measure of Economic Activity Definition The monetary value of all the finished goods and services produced within a country's borders

Predicting Indian GDP And its relation with FMCG Sales GDP A Broad Measure of Economic Activity Definition The monetary value of all the finished goods and services produced within a country's borders

Analysis of the Volatility of the Electricity Price in Kenya Using Autoregressive Integrated Moving Average Model

Science Journal of Applied Mathematics and Statistics 2015; 3(2): 47-57 Published online March 28, 2015 (http://www.sciencepublishinggroup.com/j/sjams) doi: 10.11648/j.sjams.20150302.14 ISSN: 2376-9491

Science Journal of Applied Mathematics and Statistics 2015; 3(2): 47-57 Published online March 28, 2015 (http://www.sciencepublishinggroup.com/j/sjams) doi: 10.11648/j.sjams.20150302.14 ISSN: 2376-9491

Agenda. Managing Uncertainty in the Supply Chain. The Economic Order Quantity. Classic inventory theory

Agenda Managing Uncertainty in the Supply Chain TIØ485 Produkjons- og nettverksøkonomi Lecture 3 Classic Inventory models Economic Order Quantity (aka Economic Lot Size) The (s,s) Inventory Policy Managing

Agenda Managing Uncertainty in the Supply Chain TIØ485 Produkjons- og nettverksøkonomi Lecture 3 Classic Inventory models Economic Order Quantity (aka Economic Lot Size) The (s,s) Inventory Policy Managing

Performing Unit Root Tests in EViews. Unit Root Testing

Página 1 de 12 Unit Root Testing The theory behind ARMA estimation is based on stationary time series. A series is said to be (weakly or covariance) stationary if the mean and autocovariances of the series

Página 1 de 12 Unit Root Testing The theory behind ARMA estimation is based on stationary time series. A series is said to be (weakly or covariance) stationary if the mean and autocovariances of the series

AUTOMATION OF ENERGY DEMAND FORECASTING. Sanzad Siddique, B.S.

AUTOMATION OF ENERGY DEMAND FORECASTING by Sanzad Siddique, B.S. A Thesis submitted to the Faculty of the Graduate School, Marquette University, in Partial Fulfillment of the Requirements for the Degree

AUTOMATION OF ENERGY DEMAND FORECASTING by Sanzad Siddique, B.S. A Thesis submitted to the Faculty of the Graduate School, Marquette University, in Partial Fulfillment of the Requirements for the Degree

16 : Demand Forecasting

16 : Demand Forecasting 1 Session Outline Demand Forecasting Subjective methods can be used only when past data is not available. When past data is available, it is advisable that firms should use statistical

16 : Demand Forecasting 1 Session Outline Demand Forecasting Subjective methods can be used only when past data is not available. When past data is available, it is advisable that firms should use statistical

Forecasting the PhDs-Output of the Higher Education System of Pakistan

Forecasting the PhDs-Output of the Higher Education System of Pakistan Ghani ur Rehman, Dr. Muhammad Khalil Shahid, Dr. Bakhtiar Khan Khattak and Syed Fiaz Ahmed Center for Emerging Sciences, Engineering

Forecasting the PhDs-Output of the Higher Education System of Pakistan Ghani ur Rehman, Dr. Muhammad Khalil Shahid, Dr. Bakhtiar Khan Khattak and Syed Fiaz Ahmed Center for Emerging Sciences, Engineering

ADVANCED FORECASTING MODELS USING SAS SOFTWARE

ADVANCED FORECASTING MODELS USING SAS SOFTWARE Girish Kumar Jha IARI, Pusa, New Delhi 110 012 [email protected] 1. Transfer Function Model Univariate ARIMA models are useful for analysis and forecasting

ADVANCED FORECASTING MODELS USING SAS SOFTWARE Girish Kumar Jha IARI, Pusa, New Delhi 110 012 [email protected] 1. Transfer Function Model Univariate ARIMA models are useful for analysis and forecasting

Time-Series Analysis CHAPTER. 18.1 General Purpose and Description 18-1

CHAPTER 8 Time-Series Analysis 8. General Purpose and Description Time-series analysis is used when observations are made repeatedly over 5 or more time periods. Sometimes the observations are from a single

CHAPTER 8 Time-Series Analysis 8. General Purpose and Description Time-series analysis is used when observations are made repeatedly over 5 or more time periods. Sometimes the observations are from a single

Time series Forecasting using Holt-Winters Exponential Smoothing

Time series Forecasting using Holt-Winters Exponential Smoothing Prajakta S. Kalekar(04329008) Kanwal Rekhi School of Information Technology Under the guidance of Prof. Bernard December 6, 2004 Abstract

Time series Forecasting using Holt-Winters Exponential Smoothing Prajakta S. Kalekar(04329008) Kanwal Rekhi School of Information Technology Under the guidance of Prof. Bernard December 6, 2004 Abstract

Regression and Time Series Analysis of Petroleum Product Sales in Masters. Energy oil and Gas

Regression and Time Series Analysis of Petroleum Product Sales in Masters Energy oil and Gas 1 Ezeliora Chukwuemeka Daniel 1 Department of Industrial and Production Engineering, Nnamdi Azikiwe University

Regression and Time Series Analysis of Petroleum Product Sales in Masters Energy oil and Gas 1 Ezeliora Chukwuemeka Daniel 1 Department of Industrial and Production Engineering, Nnamdi Azikiwe University

Promotional Analysis and Forecasting for Demand Planning: A Practical Time Series Approach Michael Leonard, SAS Institute Inc.

Promotional Analysis and Forecasting for Demand Planning: A Practical Time Series Approach Michael Leonard, SAS Institute Inc. Cary, NC, USA Abstract Many businesses use sales promotions to increase the

Promotional Analysis and Forecasting for Demand Planning: A Practical Time Series Approach Michael Leonard, SAS Institute Inc. Cary, NC, USA Abstract Many businesses use sales promotions to increase the

JetBlue Airways Stock Price Analysis and Prediction

JetBlue Airways Stock Price Analysis and Prediction Team Member: Lulu Liu, Jiaojiao Liu DSO530 Final Project JETBLUE AIRWAYS STOCK PRICE ANALYSIS AND PREDICTION 1 Motivation Started in February 2000, JetBlue

JetBlue Airways Stock Price Analysis and Prediction Team Member: Lulu Liu, Jiaojiao Liu DSO530 Final Project JETBLUE AIRWAYS STOCK PRICE ANALYSIS AND PREDICTION 1 Motivation Started in February 2000, JetBlue

4. Simple regression. QBUS6840 Predictive Analytics. https://www.otexts.org/fpp/4

4. Simple regression QBUS6840 Predictive Analytics https://www.otexts.org/fpp/4 Outline The simple linear model Least squares estimation Forecasting with regression Non-linear functional forms Regression

4. Simple regression QBUS6840 Predictive Analytics https://www.otexts.org/fpp/4 Outline The simple linear model Least squares estimation Forecasting with regression Non-linear functional forms Regression

Chapter 4: Vector Autoregressive Models

Chapter 4: Vector Autoregressive Models 1 Contents: Lehrstuhl für Department Empirische of Wirtschaftsforschung Empirical Research and und Econometrics Ökonometrie IV.1 Vector Autoregressive Models (VAR)...

Chapter 4: Vector Autoregressive Models 1 Contents: Lehrstuhl für Department Empirische of Wirtschaftsforschung Empirical Research and und Econometrics Ökonometrie IV.1 Vector Autoregressive Models (VAR)...

SPSS TRAINING SESSION 3 ADVANCED TOPICS (PASW STATISTICS 17.0) Sun Li Centre for Academic Computing [email protected]

Sun Li Centre for Academic Computing lsun@smu.edu.sg") SPSS TRAINING SESSION 3 ADVANCED TOPICS (PASW STATISTICS 17.0) Sun Li Centre for Academic Computing [email protected] IN SPSS SESSION 2, WE HAVE LEARNT: Elementary Data Analysis Group Comparison & One-way

SPSS TRAINING SESSION 3 ADVANCED TOPICS (PASW STATISTICS 17.0) Sun Li Centre for Academic Computing [email protected] IN SPSS SESSION 2, WE HAVE LEARNT: Elementary Data Analysis Group Comparison & One-way

FORECASTING AND TIME SERIES ANALYSIS USING THE SCA STATISTICAL SYSTEM

FORECASTING AND TIME SERIES ANALYSIS USING THE SCA STATISTICAL SYSTEM VOLUME 2 Expert System Capabilities for Time Series Modeling Simultaneous Transfer Function Modeling Vector Modeling by Lon-Mu Liu

FORECASTING AND TIME SERIES ANALYSIS USING THE SCA STATISTICAL SYSTEM VOLUME 2 Expert System Capabilities for Time Series Modeling Simultaneous Transfer Function Modeling Vector Modeling by Lon-Mu Liu

3. Regression & Exponential Smoothing

3. Regression & Exponential Smoothing 3.1 Forecasting a Single Time Series Two main approaches are traditionally used to model a single time series z 1, z 2,..., z n 1. Models the observation z t as a

3. Regression & Exponential Smoothing 3.1 Forecasting a Single Time Series Two main approaches are traditionally used to model a single time series z 1, z 2,..., z n 1. Models the observation z t as a

In this paper we study how the time-series structure of the demand process affects the value of information

MANAGEMENT SCIENCE Vol. 51, No. 6, June 25, pp. 961 969 issn 25-199 eissn 1526-551 5 516 961 informs doi 1.1287/mnsc.15.385 25 INFORMS Information Sharing in a Supply Chain Under ARMA Demand Vishal Gaur

MANAGEMENT SCIENCE Vol. 51, No. 6, June 25, pp. 961 969 issn 25-199 eissn 1526-551 5 516 961 informs doi 1.1287/mnsc.15.385 25 INFORMS Information Sharing in a Supply Chain Under ARMA Demand Vishal Gaur

2.2 Elimination of Trend and Seasonality

26 CHAPTER 2. TREND AND SEASONAL COMPONENTS 2.2 Elimination of Trend and Seasonality Here we assume that the TS model is additive and there exist both trend and seasonal components, that is X t = m t +

26 CHAPTER 2. TREND AND SEASONAL COMPONENTS 2.2 Elimination of Trend and Seasonality Here we assume that the TS model is additive and there exist both trend and seasonal components, that is X t = m t +

Exam Solutions. X t = µ + βt + A t,

Exam Solutions Please put your answers on these pages. Write very carefully and legibly. HIT Shenzhen Graduate School James E. Gentle, 2015 1. 3 points. There was a transcription error on the registrar

Exam Solutions Please put your answers on these pages. Write very carefully and legibly. HIT Shenzhen Graduate School James E. Gentle, 2015 1. 3 points. There was a transcription error on the registrar

Monitoring the SARS Epidemic in China: A Time Series Analysis

Journal of Data Science 3(2005), 279-293 Monitoring the SARS Epidemic in China: A Time Series Analysis Dejian Lai The University of Texas and Jiangxi University of Finance and Economics Abstract: In this

Journal of Data Science 3(2005), 279-293 Monitoring the SARS Epidemic in China: A Time Series Analysis Dejian Lai The University of Texas and Jiangxi University of Finance and Economics Abstract: In this

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate?

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate? Emily Polito, Trinity College In the past two decades, there have been many empirical studies both in support of and opposing

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate? Emily Polito, Trinity College In the past two decades, there have been many empirical studies both in support of and opposing

Estimating an ARMA Process

Statistics 910, #12 1 Overview Estimating an ARMA Process 1. Main ideas 2. Fitting autoregressions 3. Fitting with moving average components 4. Standard errors 5. Examples 6. Appendix: Simple estimators

Statistics 910, #12 1 Overview Estimating an ARMA Process 1. Main ideas 2. Fitting autoregressions 3. Fitting with moving average components 4. Standard errors 5. Examples 6. Appendix: Simple estimators

Time Series Analysis in WinIDAMS

Time Series Analysis in WinIDAMS P.S. Nagpaul, New Delhi, India April 2005 1 Introduction A time series is a sequence of observations, which are ordered in time (or space). In electrical engineering literature,

Time Series Analysis in WinIDAMS P.S. Nagpaul, New Delhi, India April 2005 1 Introduction A time series is a sequence of observations, which are ordered in time (or space). In electrical engineering literature,

How To Plan A Pressure Container Factory

ScienceAsia 27 (2) : 27-278 Demand Forecasting and Production Planning for Highly Seasonal Demand Situations: Case Study of a Pressure Container Factory Pisal Yenradee a,*, Anulark Pinnoi b and Amnaj Charoenthavornying

ScienceAsia 27 (2) : 27-278 Demand Forecasting and Production Planning for Highly Seasonal Demand Situations: Case Study of a Pressure Container Factory Pisal Yenradee a,*, Anulark Pinnoi b and Amnaj Charoenthavornying

Trend and Seasonal Components

Chapter 2 Trend and Seasonal Components If the plot of a TS reveals an increase of the seasonal and noise fluctuations with the level of the process then some transformation may be necessary before doing

Chapter 2 Trend and Seasonal Components If the plot of a TS reveals an increase of the seasonal and noise fluctuations with the level of the process then some transformation may be necessary before doing

A FULLY INTEGRATED ENVIRONMENT FOR TIME-DEPENDENT DATA ANALYSIS

A FULLY INTEGRATED ENVIRONMENT FOR TIME-DEPENDENT DATA ANALYSIS Version 1.4 July 2007 First edition Intended for use with Mathematica 6 or higher Software and manual: Yu He, John Novak, Darren Glosemeyer

A FULLY INTEGRATED ENVIRONMENT FOR TIME-DEPENDENT DATA ANALYSIS Version 1.4 July 2007 First edition Intended for use with Mathematica 6 or higher Software and manual: Yu He, John Novak, Darren Glosemeyer

Search Marketing Cannibalization. Analytical Techniques to measure PPC and Organic interaction

Search Marketing Cannibalization Analytical Techniques to measure PPC and Organic interaction 2 Search Overview How People Use Search Engines Navigational Research Health/Medical Directions News Shopping

Search Marketing Cannibalization Analytical Techniques to measure PPC and Organic interaction 2 Search Overview How People Use Search Engines Navigational Research Health/Medical Directions News Shopping