Department of Taxation

|

|

|

- Jocelin Booth

- 8 years ago

- Views:

Transcription

1 Department of Taxation Commerce Tax Presentation Deonne E. Contine, Executive Director Sumiko Maser, Chief Deputy Executive Director Paulina Oliver, Deputy Executive Director

2 What do I need to do to determine my Commerce Tax liability. 1) Determine if you are a business entity subject to the Commerce Tax. 2) Determine your Nevada Gross Revenue (NGR). 3) Determine your NAICS code. The NAICS code is necessary to determine the tax rate. 4) Subtract $4,000,000 from your NGR to determine your taxable revenue, then multiply that number by your tax rate.

3 Business Entity Subject To Commerce Tax: Sec. 4 of SB 483 Each entity engaged in a business is subject to the tax, whether they are corporations including S corporations, partnerships, proprietorships, limited liability companies, business associations, joint stock companies, holding companies, and business trusts. Engaged in business broadly defined (Sec. 6): Commencing, conducting or continuing a business The exercise of corporate or franchise powers regarding a business Liquidation of business when entity was conducting the business

4 Business Not Subject To Commerce Tax: Sec. 4(2) of SB 483 Natural person unless it is required to file a 1040 form C, E or F Governmental entity 501(c) or Chapter 82 or 84 non profit Credit Union Certain non business trusts including REITs and REMICs as defined in IRS Code Passive entities Entities organized solely to manage intangible investments Entity participating in exhibition in Nevada that is not required to obtain a business license pursuant to NRS

5 Commerce Tax - Who Must File All business entities subject to the Commerce Tax even if there is no tax liability All corporations required to file an initial or annual list with the Secretary of State even if there is no tax liability

6 Commerce Tax Filing Returns Annual filing Frequency: Due date is 45 th date after June 30, starting August 15, 2016 based on actual revenue for July 1-June 30. A business entity must use the same accounting method as it uses for federal income tax purposes. SB483 allows for a grace period until February 15, 2017 whereby no interest or penalty will be assessed for failure to comply with the Commerce Tax unless the failure was intentional or due to willful neglect. In subsequent years, a taxpayer may request an extension to file for up to 30 days. No penalty will be assessed if approved, but interest will accumulate.

7 Gross Revenue Defined Section 8 or SB 483 The total amount realized by a business entity from engaging in a business in this State without deduction for: cost of goods sold other expenses incurred in operating the business

8 Gross Revenue Does Not Include Section 8(3) of SB 483 Intellectual property revenue from the sale or exchange of the right to use trademarks, trade names, patents, copyrights, or other similar property. Value of Cash discounts Value of goods and services to a customer on a complimentary basis Amounts realized from certain tax free transactions under IRC 118, 331, 332, 336, 337, 338, 351, 355, 368,721, 731, 1031 and 1033 Amounts indirectly realized from a reduction of an expense The value of property or service donated to an organization under IRC 501(c)(3) Amounts not considered revenue under GAAP

9 Deductions from Gross Revenue Section 21 of SB 483 Dividends and distributions Industry Specific Deductions Gaming, Mining, Liquor Suppliers, Insurance Companies, Health Care, Employee Leasing Companies, Entity that manages or operates a property owned or leased by Federal Government or that houses military personnel. Receipts from a passive entity in which the business entity has an ownership interest Pass-through revenue (defined in Sec. 11 of SB 483) Dividends and interest from federal and state bonds or securities Bad debts, returns or refunds to customers, sale of accounts receivable if the underlying debts were included in revenue calculation

Dividends and interest from federal and state bonds or securities Bad debts, returns or refunds to customers, sale of accounts receivable if the")

10 Deductions from Gross Revenue Section 21 of SB 483 Pass-through revenue (defined in Sec. 11 of SB 483) Revenue required by law or fiduciary duty to be distributed to another person or governmental entity Taxes collected from 3 rd party and remitted to taxing authority Reimbursements for advances that are made but not related to sale of goods or services Amounts mandated by contract to be paid to others in specific circumstances Sales commissions paid to non employees (like real estate) contractors payments to sub contractors are not included in revenue calculation for contractor but would be included in revenue of subcontractors. Amounts lawyers hold in trust accounts or amounts paid to another attorney who provided legal services and who is not part of the firm and reimbursements from a claimant for expenses of the claimant s case. Affiliated group revenue transfers. An affiliated group has two or more businesses controlled by (50% ownership/possession)one or more common owners or members of the group.

contractors payments to sub contractors are not included in revenue calculation for contractor but would be included in revenue of subcontractors.")

11 Nevada Gross Revenue Revenue related to your Nevada transaction Tangible personal property sold to a consumer who is in Nevada - it is where it is received by the customer in Nevada (similar to sales tax rules) For revenue related to the sale of services, it is the location where the benefit is received by the purchaser. (i.e. is the purchaser located in Nevada, is the service provided by a Nevada business for a Nevada benefit.) For real property if the real property is located in Nevada.

For real property if the real property is located in Nevada.")

12 Commerce Tax: Gross Revenue includes Gross revenue from the sales of property or services Gross revenue from transportation services if both the origin and destination points are in Nevada Gross royalty income from property located in Nevada Gross receipts from any other business function in Nevada

13 Tax Rates based on NAICS Code 26 different NAICS categories for purposes of the Commerce Tax each with a different tax rate. A business entity s category depends on the type of business it is primarily engaged in. If an entity has more than one type of business activity, it is the category where the highest percentage of the revenue comes from. The business entity must report their NAICS category on the annual Commerce tax return.

14 Sections of SB 483 set forth the rate of the Commerce Tax for the industry in which a business entity is primarily engaged as follows: NAICS Category INDUSTRY Tax Rate 11 Agriculture, Forestry, Hunting.063% 21 Mining, Quarrying, Oil and Gas Extraction.051% 22/517 Utilities and Telecommunications.136% 23 Construction.083% Manufacturing.091% 42 Wholesale Trade.101% Retail Trade.111% 481 Air Transportation.058% 484 Truck Transportation.202%

15 NAICS Category INDUSTRY Tax Rate 482 Rail Transportation.331% 483, , Other Transportation.129% Warehousing and Storage.128% 511, 512, Publishing, Software, Data Processing.253% 515, Finance and Insurance.111% 53 Rental & Leasing.25% 54 Professional, Scientific or Technical.181% Services 55 Management of Companies and.137% Enterprises 561 Administrative and Support Services.154% 562 Waste Management and Remediation Services.261%

16 NAICS Category INDUSTRY Tax Rate 61 Education Services.281% 62 Health Care and Social Assistance.190% 71 Arts, Entertainment and Recreation.24% 721 Accommodations.20% 722 Food Services and Drinking Places.194% 81 Other Services.142% Unclassified Unclassified Business.128%

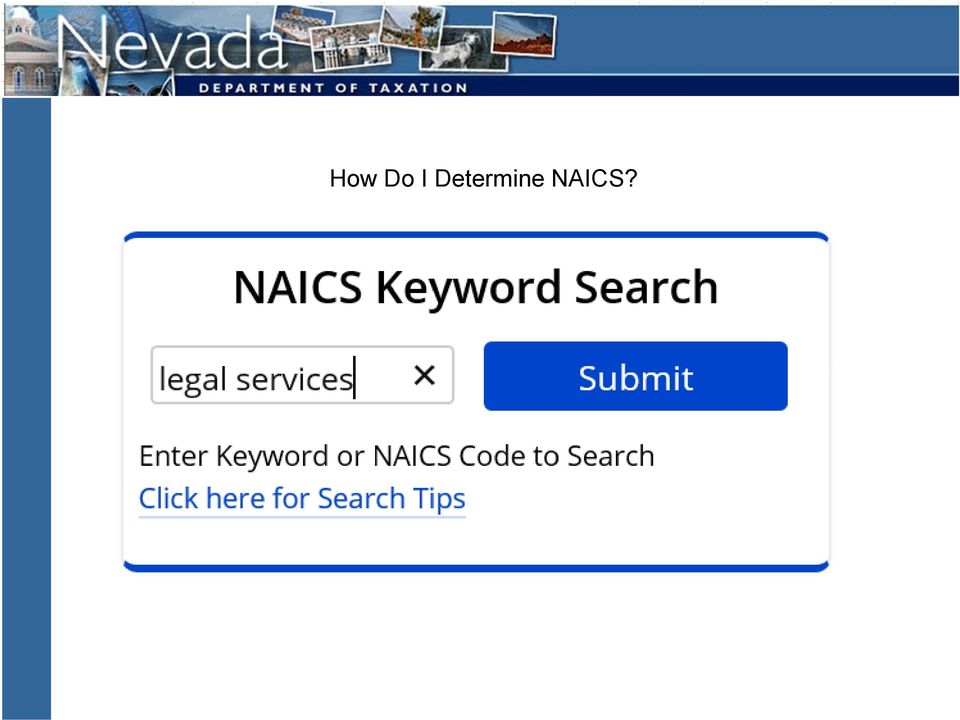

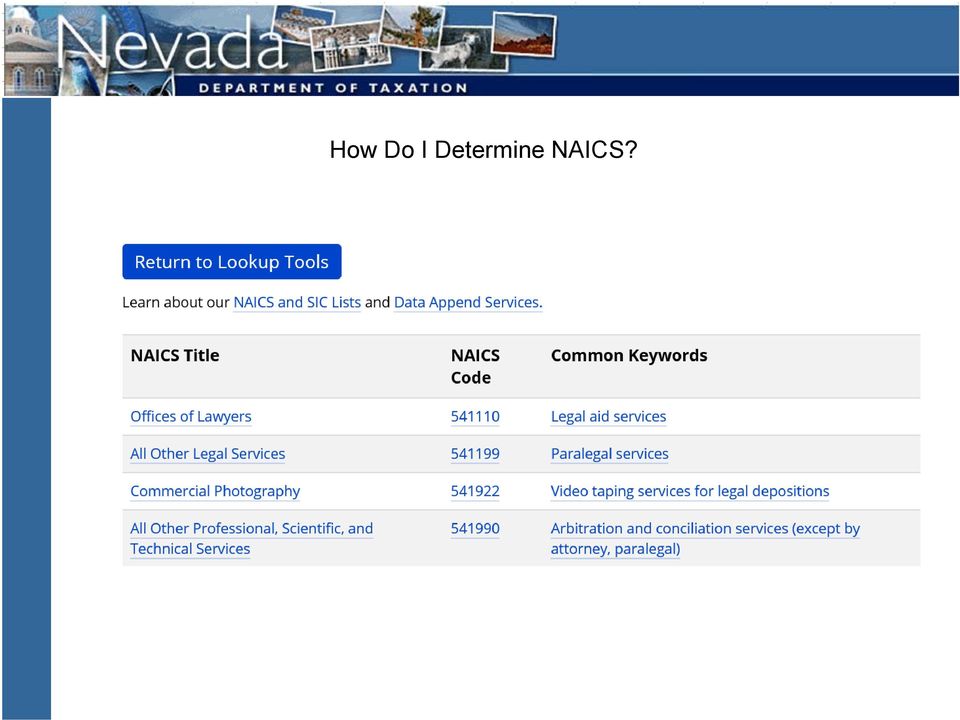

17 How Do I Determine My NAICS? Taxpayers use NAICS codes currently NAICS search tool at

18 How Do I Determine NAICS?

19 How Do I Determine NAICS?

20 Other SB 483 Changes Related to the Commerce Tax Sec. 68 of SB 438 Effective July 1, 2016: An MBT deduction of 50% of the Commerce Tax paid is allowed against the Modified Business Tax liability by the entity that paid the Commerce Tax. Credit good for 4 calendar quarters following payment of the Commerce Tax Credit cannot be more than the MBT liability

21 Please visit our Web Site at or one of our offices at the following locations: Main Office 1550 College Parkway, Suite 100 Carson City NV Phone: (775) Fax: (775) Las Vegas District Office Grant Sawyer Office Building 555 E. Washington Ave, Suite 1300 Las Vegas, Nevada Phone: (702) Fax: (702) Northern Nevada: Southern Nevada: Reno District Office Kietzke Plaza 4600 Kietzke Lane, Bldg L, Suite 235 Reno, NV Phone: (775) Fax: (775) Henderson District Office 2550 Paseo Verde Pkwy, Suite 180 Henderson, Nevada Phone: (702) Fax: (702) Taxpayer Call Center: (866)

2015 NEVADA TAX REFORMS. Commerce Tax, Modified Business Tax, Business License Fee

Joshua J. Hicks Attorney at Law 775.622.9450 tel 775.622.9554 fax jhicks@bhfs.com 2015 NEVADA TAX REFORMS Commerce Tax, Modified Business Tax, Business License Fee Current as of June 10, 2015 A. Commerce

Joshua J. Hicks Attorney at Law 775.622.9450 tel 775.622.9554 fax jhicks@bhfs.com 2015 NEVADA TAX REFORMS Commerce Tax, Modified Business Tax, Business License Fee Current as of June 10, 2015 A. Commerce

Nevada enacts Commerce Tax effective July 1, 2015

from State and Local Tax Services Nevada enacts Commerce Tax effective July 1, 2015 June 10, 2015 In brief Signed on June 10, 2015, and effective July 1, 2015, S.B. 483 imposes an annual commerce tax on

from State and Local Tax Services Nevada enacts Commerce Tax effective July 1, 2015 June 10, 2015 In brief Signed on June 10, 2015, and effective July 1, 2015, S.B. 483 imposes an annual commerce tax on

State & Local Tax Alert

State & Local Tax Alert Breaking state and local tax developments from Grant Thornton LLP Nevada Enacts Budget Bill Including New Commerce Tax On June 9, 2015, Nevada Governor Brian Sandoval signed legislation

State & Local Tax Alert Breaking state and local tax developments from Grant Thornton LLP Nevada Enacts Budget Bill Including New Commerce Tax On June 9, 2015, Nevada Governor Brian Sandoval signed legislation

FAST FACTS. The current State annual business license is replaced by a quarterly State Business Licence Tax.

DATE: March 16, 2015 TO: NTA Members The following five pages contain a section by section summary of SB 252, the Governor s major tax bill. The link to the bill is http://www.leg.state.nv.us/session/78th2015/bills/sb/sb252.pdf,

DATE: March 16, 2015 TO: NTA Members The following five pages contain a section by section summary of SB 252, the Governor s major tax bill. The link to the bill is http://www.leg.state.nv.us/session/78th2015/bills/sb/sb252.pdf,

LICENSING & PERMITS LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY

LICENSING & PERMITS LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY These are the suggested steps along with a listing and a brief description of each of the forms and filings

LICENSING & PERMITS LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY These are the suggested steps along with a listing and a brief description of each of the forms and filings

SAN FRANCISCO S NEW GROSS RECEIPTS TAX AND BUSINESS REGISTRATION FEES

SAN FRANCISCO S NEW GROSS RECEIPTS TAX AND BUSINESS REGISTRATION FEES This summary provides basic information regarding San Francisco Business and Tax Regulations Code ( Code ), Article 12-A-1, Gross Receipts

SAN FRANCISCO S NEW GROSS RECEIPTS TAX AND BUSINESS REGISTRATION FEES This summary provides basic information regarding San Francisco Business and Tax Regulations Code ( Code ), Article 12-A-1, Gross Receipts

LICENSING & PERMITS IN LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY

www.nsbdc.org (800) 240-7094 LICENSING & PERMITS IN LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY These are the suggested steps along with a listing and a brief description

www.nsbdc.org (800) 240-7094 LICENSING & PERMITS IN LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY These are the suggested steps along with a listing and a brief description

Out of Town Business Registration Fee $35.00 per year

Out of Town Business Registration Fee $35.00 per year City Ordinance #1172-81 requires that all businesses apply for and obtain a business registration prior to engaging in business. Please fill out the

Out of Town Business Registration Fee $35.00 per year City Ordinance #1172-81 requires that all businesses apply for and obtain a business registration prior to engaging in business. Please fill out the

Senate Bill No. 483 Committee on Revenue and Economic Development

Senate Bill No. 483 Committee on Revenue and Economic Development CHAPTER... AN ACT relating to governmental financial administration; providing for the imposition, administration and payment of a commerce

Senate Bill No. 483 Committee on Revenue and Economic Development CHAPTER... AN ACT relating to governmental financial administration; providing for the imposition, administration and payment of a commerce

STEP ONE: Create a Corporation, Limited Liability Company, Partnership or Sole Proprietorship Legal Organization

LICENSING & PERMITS VIRGINIA CITY AND STOREY COUNTY These are the suggested steps along with a listing and a brief description of each of the forms and filings necessary for business operations in Lyon

LICENSING & PERMITS VIRGINIA CITY AND STOREY COUNTY These are the suggested steps along with a listing and a brief description of each of the forms and filings necessary for business operations in Lyon

NEVADA TAX NOTES Official Newsletter of the Department of Taxation

N E V A D A D E P A R T M E N T O F T A X A T I O N NEVADA TAX NOTES Official Newsletter of the Department of Taxation OCTOBER 2012 h t t p : / /www.t a x. s t a t e. n v. u s ISSUE NO. 180 Register, File

N E V A D A D E P A R T M E N T O F T A X A T I O N NEVADA TAX NOTES Official Newsletter of the Department of Taxation OCTOBER 2012 h t t p : / /www.t a x. s t a t e. n v. u s ISSUE NO. 180 Register, File

San Francisco Business Tax Reform: Summary of Gross Receipts Tax Legislation Introduced on June 12, 2012

San Francisco Business Tax Reform: Summary of Gross Receipts Tax Legislation Introduced on June 12, 2012 Ben Rosenfield, Controller Ted Egan, Chief Economist Background At the request of the Mayor and

San Francisco Business Tax Reform: Summary of Gross Receipts Tax Legislation Introduced on June 12, 2012 Ben Rosenfield, Controller Ted Egan, Chief Economist Background At the request of the Mayor and

Tax Reform in Texas: Was it the Perfect Storm? Karey Barton Principal

Tax Reform in Texas: Was it the Perfect Storm? Karey Barton Principal December 15, 2008 Agenda The background: What was the emphasis driving tax reform? How did the process work? The basics: Who is subject

Tax Reform in Texas: Was it the Perfect Storm? Karey Barton Principal December 15, 2008 Agenda The background: What was the emphasis driving tax reform? How did the process work? The basics: Who is subject

U.S. Tax Benefits for Exporting

U.S. Tax Benefits for Exporting By Richard S. Lehman, Esq. TAX ATTORNEY www.lehmantaxlaw.com Richard S. Lehman Esq. International Tax Attorney LehmanTaxLaw.com 6018 S.W. 18th Street, Suite C-1 Boca Raton,

U.S. Tax Benefits for Exporting By Richard S. Lehman, Esq. TAX ATTORNEY www.lehmantaxlaw.com Richard S. Lehman Esq. International Tax Attorney LehmanTaxLaw.com 6018 S.W. 18th Street, Suite C-1 Boca Raton,

Nebraska Department of Economic Development. Angel Investment Tax Credit. Qualified Small Business Certification Application Form.

Form NDEDQSB Nebraska Department of Economic Development Angel Investment Tax Credit Qualified Small Business Certification Application Form Section I. Business name and identifying information Legal Name

Form NDEDQSB Nebraska Department of Economic Development Angel Investment Tax Credit Qualified Small Business Certification Application Form Section I. Business name and identifying information Legal Name

CHECK THE MATH ON THE TEXAS MARGINS KAREY W. BARTON PRINCIPAL RYAN, INC.

CHECK THE MATH ON THE TEXAS MARGINS KAREY W. BARTON PRINCIPAL RYAN, INC. TEXAS MARGIN TAX A. Margin Tax Basics 1. Overview The margin tax applies to all entities that enjoy the privilege of liability protection,

CHECK THE MATH ON THE TEXAS MARGINS KAREY W. BARTON PRINCIPAL RYAN, INC. TEXAS MARGIN TAX A. Margin Tax Basics 1. Overview The margin tax applies to all entities that enjoy the privilege of liability protection,

BRIEF OVERVIEW OF PENNSYLVANIA PERSONAL INCOME TAX

CHAPTER 6: BRIEF OVERVIEW OF PENNSYLVANIA PERSONAL INCOME TAX TABLE OF CONTENTS I. OVERVIEW 2 II. TAX RATE...3 III. EIGHT CLASSES OF INCOME 3 A. Gross Compensation... 3 B. Interest... 4 C. Dividends...

CHAPTER 6: BRIEF OVERVIEW OF PENNSYLVANIA PERSONAL INCOME TAX TABLE OF CONTENTS I. OVERVIEW 2 II. TAX RATE...3 III. EIGHT CLASSES OF INCOME 3 A. Gross Compensation... 3 B. Interest... 4 C. Dividends...

Tax Rates. For personal income tax purposes, for tax years beginning after 2014, the tax rates are as follows:

October 2014 District of Columbia Reduced Tax Rates, Single Sales Factor, Other Changes Adopted Permanent District of Columbia budget legislation makes numerous significant changes to the corporation franchise

October 2014 District of Columbia Reduced Tax Rates, Single Sales Factor, Other Changes Adopted Permanent District of Columbia budget legislation makes numerous significant changes to the corporation franchise

1. Nonresident Alien or Resident Alien?

U..S.. Tax Guiide for Non-Resiidents Table of Contents A. U.S. INCOME TAXES ON NON-RESIDENTS 1. Nonresident Alien or Resident Alien? o Nonresident Aliens o Resident Aliens Green Card Test Substantial Presence

U..S.. Tax Guiide for Non-Resiidents Table of Contents A. U.S. INCOME TAXES ON NON-RESIDENTS 1. Nonresident Alien or Resident Alien? o Nonresident Aliens o Resident Aliens Green Card Test Substantial Presence

Michigan Business Tax Frequently Asked Questions

NOTICE: The MBT was amended by 145 PA 2007 on December 1, 2007. Act 145 imposes an annual surcharge to taxpayers' MBT liability, as well as makes other changes. Some of the FAQs below have revised answers

NOTICE: The MBT was amended by 145 PA 2007 on December 1, 2007. Act 145 imposes an annual surcharge to taxpayers' MBT liability, as well as makes other changes. Some of the FAQs below have revised answers

State of Wisconsin Department of Revenue Limited Liability Companies (LLCs)

") State of Wisconsin Department of Revenue Limited Liability Companies (LLCs) Publication 119 (2/15) Table of Contents 2 Page I. INTRODUCTION... 4 II. DEFINITIONS APPLICABLE TO LLCS... 4 III. FORMATION OF

State of Wisconsin Department of Revenue Limited Liability Companies (LLCs) Publication 119 (2/15) Table of Contents 2 Page I. INTRODUCTION... 4 II. DEFINITIONS APPLICABLE TO LLCS... 4 III. FORMATION OF

2015 Texas Franchise Tax Report Information and Instructions

2015 Texas Franchise Tax Report Information and Instructions Form 05-902 (Rev.1-15/2) Topics covered in this booklet: Amended Reports... 10 Annual Reports... 4 Annualized Total Revenue... 3 Change in Accounting

2015 Texas Franchise Tax Report Information and Instructions Form 05-902 (Rev.1-15/2) Topics covered in this booklet: Amended Reports... 10 Annual Reports... 4 Annualized Total Revenue... 3 Change in Accounting

DRAFT. All NAICS. 3-Digit NAICS BP C 3 P 76 X 0 BP C 0 P 0 X 2 OC C 29 P 44 X 35 OC C 0 P 0 X 2 MH C 96 MH C 8 P 37 X 62 P 1107 X 587

All NAICS 3-Digit NAICS BP C 3 P 76 X 0 OC C 29 P 44 X 35 MH C 96 P 1107 X 587 BP C 0 P 0 X 2 OC C 0 P 0 X 2 MH C 8 P 37 X 62 ML C 66 P 958 X 772 ML C 4 P 34 X 69 A. Resource Uses. 11 Agriculture, Forestry,

All NAICS 3-Digit NAICS BP C 3 P 76 X 0 OC C 29 P 44 X 35 MH C 96 P 1107 X 587 BP C 0 P 0 X 2 OC C 0 P 0 X 2 MH C 8 P 37 X 62 ML C 66 P 958 X 772 ML C 4 P 34 X 69 A. Resource Uses. 11 Agriculture, Forestry,

APPLICATION CONTINUES ON THE NEXT PAGE

CITY & COUNTY OF SAN FRANCISCO OFFICE OF THE TREASURER & TAX COLLECTOR JOSÉ CISNEROS, TREASURER Taxpayer Assistance, City Hall Room 140 #1 Dr. Carlton B. Goodlett Place, San Francisco, CA 94102 Customer

CITY & COUNTY OF SAN FRANCISCO OFFICE OF THE TREASURER & TAX COLLECTOR JOSÉ CISNEROS, TREASURER Taxpayer Assistance, City Hall Room 140 #1 Dr. Carlton B. Goodlett Place, San Francisco, CA 94102 Customer

GROSS RECEIPTS TAX AND BUSINESS REGISTRATION FEES ORDINANCE 2014

GROSS RECEIPTS TAX AND BUSINESS REGISTRATION FEES ORDINANCE 2014 CHANGE IS COMING! If there are three things you take away from this presentation 1Registration Fees for All Businesses are Increasing in

GROSS RECEIPTS TAX AND BUSINESS REGISTRATION FEES ORDINANCE 2014 CHANGE IS COMING! If there are three things you take away from this presentation 1Registration Fees for All Businesses are Increasing in

GENERAL INSTRUCTIONS FOR COMPLETING YOUR RETURN

GENERAL INSTRUCTIONS FOR COMPLETING YOUR RETURN PITTSBURGH CITY & SCHOOL DISTRICT The City of Pittsburgh Earned Income Tax is levied at the rate of 1% under ACT 511. The Pittsburgh School District Earned

GENERAL INSTRUCTIONS FOR COMPLETING YOUR RETURN PITTSBURGH CITY & SCHOOL DISTRICT The City of Pittsburgh Earned Income Tax is levied at the rate of 1% under ACT 511. The Pittsburgh School District Earned

U.S. Income Tax Return for an S Corporation

Form 1120S U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is attaching Form 2553 to elect to be an S corporation. Information about Form 1120S and

Form 1120S U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is attaching Form 2553 to elect to be an S corporation. Information about Form 1120S and

The New and Evolving Texas Margin Tax, Part I

The New and Evolving Texas Margin Tax, Part I Charles D. Pulman, J.D., LL.M., CPA Meadows, Collier, Reed, Cousins & Blau, LLP Dallas, Texas David E. Colmenero, J.D., LL.M., CPA Meadows, Collier, Reed,

The New and Evolving Texas Margin Tax, Part I Charles D. Pulman, J.D., LL.M., CPA Meadows, Collier, Reed, Cousins & Blau, LLP Dallas, Texas David E. Colmenero, J.D., LL.M., CPA Meadows, Collier, Reed,

ARTICLE 12-A-1: GROSS RECEIPTS TAX ORDINANCE

ARTICLE 12-A-1: GROSS RECEIPTS TAX ORDINANCE 950. 951. 952. 952.1. 952.2. 952.3. 952.4. 952.5. 952.6. 953. 953.1. 953.2. 953.3. 953.4. 953.5. 953.6. 953.7. 953.8. 953.9. 954. 954.1. 955. 956. 956.1. 956.2.

ARTICLE 12-A-1: GROSS RECEIPTS TAX ORDINANCE 950. 951. 952. 952.1. 952.2. 952.3. 952.4. 952.5. 952.6. 953. 953.1. 953.2. 953.3. 953.4. 953.5. 953.6. 953.7. 953.8. 953.9. 954. 954.1. 955. 956. 956.1. 956.2.

SALES AND USE TAX TECHNICAL BULLETINS SECTION 17

SECTION 17 - NONPROFIT ENTITIES - HOSPITALS, EDUCATIONAL INSTITUTIONS, CHURCHES, ORPHANAGES AND OTHER CHARITABLE OR RELIGIOUS INSTITUTIONS AND ORGANIZATIONS AND QUALIFIED RETIREMENT FACILITIES WHOSE PROPERTY

SECTION 17 - NONPROFIT ENTITIES - HOSPITALS, EDUCATIONAL INSTITUTIONS, CHURCHES, ORPHANAGES AND OTHER CHARITABLE OR RELIGIOUS INSTITUTIONS AND ORGANIZATIONS AND QUALIFIED RETIREMENT FACILITIES WHOSE PROPERTY

INTERNATIONAL TAX COMPLIANCE FOR GOVERNMENT CONTRACTORS

INTERNATIONAL TAX COMPLIANCE FOR GOVERNMENT CONTRACTORS Mark T. Gossart Alison N. Dougherty September 26, 2012 2012 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland 20850 301.231.6200

INTERNATIONAL TAX COMPLIANCE FOR GOVERNMENT CONTRACTORS Mark T. Gossart Alison N. Dougherty September 26, 2012 2012 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland 20850 301.231.6200

2016 Texas Franchise Tax Report Information and Instructions Form 05-903 (11-15)

") 2016 Texas Franchise Tax Report Information and Instructions Form 05-903 (11-15) Topics covered in this booklet: Amended Reports... 10 Annual Reports... 4 Annualized Total Revenue... 3 Change in Accounting

2016 Texas Franchise Tax Report Information and Instructions Form 05-903 (11-15) Topics covered in this booklet: Amended Reports... 10 Annual Reports... 4 Annualized Total Revenue... 3 Change in Accounting

Statutes & Regulations

Corporation Income & Franchise Taxes Statutes & Regulations R-6600 August 2008 A publication of the Louisiana Department of Revenue Foreword This publication contains general information on the corporation

Corporation Income & Franchise Taxes Statutes & Regulations R-6600 August 2008 A publication of the Louisiana Department of Revenue Foreword This publication contains general information on the corporation

Instructions for 2013 Form 4A-1: Wisconsin Apportionment Data for Single Factor Formulas

Instructions for 2013 Form 4A-1: Wisconsin Apportionment Data for Single Factor Formulas Purpose of Form 4A-1 Corporations, partnerships, tax-option (S) corporations and nonresident estates, trusts, and

Instructions for 2013 Form 4A-1: Wisconsin Apportionment Data for Single Factor Formulas Purpose of Form 4A-1 Corporations, partnerships, tax-option (S) corporations and nonresident estates, trusts, and

Internal Revenue Service

Internal Revenue Service Department of the Treasury Number: 200327029 Release Date: 7/3/2003 Index Number: 1362.02-03 Washington, DC 20224 Person to Contact: Telephone Number: Refer Reply To: CC:PSI:2

Internal Revenue Service Department of the Treasury Number: 200327029 Release Date: 7/3/2003 Index Number: 1362.02-03 Washington, DC 20224 Person to Contact: Telephone Number: Refer Reply To: CC:PSI:2

2. Adjustments to Federal Taxable Income The following additions to Federal taxable income must be made in determining State net income:

C. Computation of Net Income (G.S. 105-130.3, G.S. 105-130.5) 1. Preliminary Statement To compute State net income or net loss, a corporation uses its Federal taxable income as defined in the Internal

C. Computation of Net Income (G.S. 105-130.3, G.S. 105-130.5) 1. Preliminary Statement To compute State net income or net loss, a corporation uses its Federal taxable income as defined in the Internal

2013 Ohio Small Business Investor Income Deduction

2013 Ohio Small Business Investor Income Deduction Instructions for Apportioning Business Income Solely for Purposes of Computing the Small Business Investor Income Deduction hio Department of Taxation

2013 Ohio Small Business Investor Income Deduction Instructions for Apportioning Business Income Solely for Purposes of Computing the Small Business Investor Income Deduction hio Department of Taxation

LAWS GOVERNING AUTO INDUSTRY

Automobile LAWS GOVERNING AUTO INDUSTRY Two of the main chapters of the Nevada Revised Statutes and Nevada Administrative Code discussed today are: Chapter 372: Sales and Use Taxes Chapter 482: Motor Vehicles

Automobile LAWS GOVERNING AUTO INDUSTRY Two of the main chapters of the Nevada Revised Statutes and Nevada Administrative Code discussed today are: Chapter 372: Sales and Use Taxes Chapter 482: Motor Vehicles

2007 Utah Corporate Income Tax Statistics

2007 Utah Corporate Income Tax Statistics The data in this publication give a fairly complete picture of the corporate franchise tax in Utah. Corporate income taxes are not only complicated by their logic,

2007 Utah Corporate Income Tax Statistics The data in this publication give a fairly complete picture of the corporate franchise tax in Utah. Corporate income taxes are not only complicated by their logic,

BUSINESS ENTITIES AND ECONOMIC DEVELOPMENT

BUSINESS ENTITIES AND ECONOMIC DEVELOPMENT In support of business and economic development, the State of Nevada and its units of local government endeavor to maintain fair competition, promote growth,

BUSINESS ENTITIES AND ECONOMIC DEVELOPMENT In support of business and economic development, the State of Nevada and its units of local government endeavor to maintain fair competition, promote growth,

These data were developed in cooperation with, and partially funded by, the Office of Advocacy of the U.S. Small Business Administration (SBA)

") Introduction Statistics of U.S. Businesses (SUSB) is an annual series that provides national and subnational data on the distribution of economic data by enterprise size and industry. SUSB covers most

Introduction Statistics of U.S. Businesses (SUSB) is an annual series that provides national and subnational data on the distribution of economic data by enterprise size and industry. SUSB covers most

2014 Ohio IT 1140. Pass-Through Entity and Trust Withholding Tax Return Instructions. hio. Department of Taxation. For taxable year beginning in

For taxable year beginning in 2014 Ohio IT 1140 Pass-Through Entity and Trust Withholding Tax Return Instructions hio tax. hio.gov Department of Taxation 2014 Ohio Form IT 1140 General Instructions Note:

For taxable year beginning in 2014 Ohio IT 1140 Pass-Through Entity and Trust Withholding Tax Return Instructions hio tax. hio.gov Department of Taxation 2014 Ohio Form IT 1140 General Instructions Note:

FYI For Your Information

TAXPAYER SERVICE DIVISION FYI For Your Information Apportionment of Income C CORPORATIONS A C Corporation doing business only in Colorado will compute its tax on 100% of the Colorado taxable income. However,

TAXPAYER SERVICE DIVISION FYI For Your Information Apportionment of Income C CORPORATIONS A C Corporation doing business only in Colorado will compute its tax on 100% of the Colorado taxable income. However,

ENGROSSED HOUSE By: Deutschendorf of the House. ( revenue and taxation amending 68 O.S., Section. 1352 definitions - Sales Tax Code effective

ENGROSSED HOUSE BILL NO. 2736 By: Deutschendorf of the House and Robinson of the Senate ( revenue and taxation amending 68 O.S., Section 1352 definitions - Sales Tax Code effective date emergency ) BE

ENGROSSED HOUSE BILL NO. 2736 By: Deutschendorf of the House and Robinson of the Senate ( revenue and taxation amending 68 O.S., Section 1352 definitions - Sales Tax Code effective date emergency ) BE

San Francisco Voters Pass New Gross Receipts Tax; Current Payroll Expense Tax To Be Phased Out January 22, 2013

Multistate Tax EXTERNAL ALERT San Francisco Voters Pass New Gross Receipts Tax; Current Payroll Expense Tax To Be Phased Out January 22, 2013 Overview The voters of San Francisco (the City ) recently approved

Multistate Tax EXTERNAL ALERT San Francisco Voters Pass New Gross Receipts Tax; Current Payroll Expense Tax To Be Phased Out January 22, 2013 Overview The voters of San Francisco (the City ) recently approved

FEDERAL TAXATION OF INTERNATIONAL TRANSACTIONS

Chapter 10 FEDERAL TAXATION OF INTERNATIONAL TRANSACTIONS Daniel Cassidy 1 10.1 INTRODUCTION Foreign companies with U.S. business transactions face various layers of taxation. These include income, sales,

Chapter 10 FEDERAL TAXATION OF INTERNATIONAL TRANSACTIONS Daniel Cassidy 1 10.1 INTRODUCTION Foreign companies with U.S. business transactions face various layers of taxation. These include income, sales,

Overview. Texas Tax Code Chapter 171. Teresa Bostick, Claire Jamal, Jerry Oxford, Martha Preston, Nat Robberson & Jennifer Specchio

Overview Texas Tax Code Chapter 171 Presented by: Organizer: Panelists: Franchise Tax Policy Staff Janet Spies Teresa Bostick, Claire Jamal, Jerry Oxford, Martha Preston, Nat Robberson & Jennifer Specchio

Overview Texas Tax Code Chapter 171 Presented by: Organizer: Panelists: Franchise Tax Policy Staff Janet Spies Teresa Bostick, Claire Jamal, Jerry Oxford, Martha Preston, Nat Robberson & Jennifer Specchio

MBT FAQ Index. Updated 9/19/2008 1

*Words surrounded by quotation marks are defined in the MBT statute* A Accounting Methods Actual or Annual A8, A11, A31, C33, U28, M55 Cash or Accrual C32, C40, M16, M33, U17, U21 Accounts Receivable Factoring

*Words surrounded by quotation marks are defined in the MBT statute* A Accounting Methods Actual or Annual A8, A11, A31, C33, U28, M55 Cash or Accrual C32, C40, M16, M33, U17, U21 Accounts Receivable Factoring

LLC ENTITY FORMATION. This is a Questionnaire. The purpose of this Limited Liability Company questionnaire is

LLC ENTITY FORMATION This is a Questionnaire. The purpose of this Limited Liability Company questionnaire is for us to determine what must be done to form a proper LLC for you. Its purpose is to fully

LLC ENTITY FORMATION This is a Questionnaire. The purpose of this Limited Liability Company questionnaire is for us to determine what must be done to form a proper LLC for you. Its purpose is to fully

CHAPTER 8 CABLE TELEVISION ARTICLE I CABLE/VIDEO SERVICE PROVIDER FEE

CABLE TELEVISION 8-1-1 CHAPTER 8 CABLE TELEVISION ARTICLE I CABLE/VIDEO SERVICE PROVIDER FEE 8-1-1 DEFINITIONS. As used in this Chapter, the following terms shall have the following meanings: (A) Cable

CABLE TELEVISION 8-1-1 CHAPTER 8 CABLE TELEVISION ARTICLE I CABLE/VIDEO SERVICE PROVIDER FEE 8-1-1 DEFINITIONS. As used in this Chapter, the following terms shall have the following meanings: (A) Cable

Audit Division Statistical Study

Audit Division Statistical Study The Audit Division Statistical Study addresses the requirements set forth by IC 6-8.1-14-4 (2). The information is based on 100 percent of the audits completed, taxpayers

Audit Division Statistical Study The Audit Division Statistical Study addresses the requirements set forth by IC 6-8.1-14-4 (2). The information is based on 100 percent of the audits completed, taxpayers

2. Taxpayer Name (print or type) 7. Federal Employer Identification Number (FEIN) or TR Number. 8. Organization Type (LLC or Trust, see instructions)

7. Federal Employer Identification Number (FEIN) or TR Number. 8. Organization Type (LLC or Trust, see instructions)") Michigan Department of Treasury 4567 (Rev. 02-14), Page 1 Check if this is an 2014 MICHIGAN Business Tax Annual Return Issued under authority of Public Act 36 of 2007. MM-DD-YYYY amended return. Attach

Michigan Department of Treasury 4567 (Rev. 02-14), Page 1 Check if this is an 2014 MICHIGAN Business Tax Annual Return Issued under authority of Public Act 36 of 2007. MM-DD-YYYY amended return. Attach

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased.

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

NEVADA BUSINESS REGISTRATION FORM INSTRUCTIONS

NEVADA BUSINESS REGISTRATION FORM INSTRUCTIONS Completion of this form will provide the common information needed and/or required by participating state and local government agencies. Important details

NEVADA BUSINESS REGISTRATION FORM INSTRUCTIONS Completion of this form will provide the common information needed and/or required by participating state and local government agencies. Important details

Budget Introduction Proposed Budget

Budget Introduction Proposed Budget INTRO - 1 INTRO - 2 Summary of the Budget and Accounting Structure The City of Beverly Hills uses the same basis for budgeting as for accounting. Governmental fund financial

Budget Introduction Proposed Budget INTRO - 1 INTRO - 2 Summary of the Budget and Accounting Structure The City of Beverly Hills uses the same basis for budgeting as for accounting. Governmental fund financial

Supplier Diversity Program. Ensure a diversity of small businesses work with the Smithsonian to accomplish the Institution s mission.

SDP Goals Supplier Diversity Program Ensure a diversity of small businesses work with the Smithsonian to accomplish the Institution s mission. Accomplish success through each museum, research institute

SDP Goals Supplier Diversity Program Ensure a diversity of small businesses work with the Smithsonian to accomplish the Institution s mission. Accomplish success through each museum, research institute

Business-Facts: 3 Digit NAICS Summary 2014

Business-Facts: 3 Digit Summary 4 County (see appendix for geographies), Agriculture, Forestry, Fishing and Hunting 64 4.6 Crop Production 8.8 Animal Production and Aquaculture. 3 Forestry and Logging

Business-Facts: 3 Digit Summary 4 County (see appendix for geographies), Agriculture, Forestry, Fishing and Hunting 64 4.6 Crop Production 8.8 Animal Production and Aquaculture. 3 Forestry and Logging

Tax Return Questionnaire - 2013 Tax Year

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

3. If you received any interest from a "Seller Financed" mortgage, provide: Name and Address of Payer Social Security Number Amount

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

International Tax. Las Vegas, Nevada December 4-5, 2012

International Tax 4 th Annual Southwest Tax Conference Las Vegas, Nevada December 4-5, 2012 Brian Phillip Lau Cindy Hsieh br@rowbotham.com plau@rowbotham.com chsieh@rowbotham.com 101 2 nd Street, Suite

International Tax 4 th Annual Southwest Tax Conference Las Vegas, Nevada December 4-5, 2012 Brian Phillip Lau Cindy Hsieh br@rowbotham.com plau@rowbotham.com chsieh@rowbotham.com 101 2 nd Street, Suite

SALE BY TRUSTEE IN BANKRUPTCY 1003.10

SALE BY TRUSTEE IN BANKRUPTCY 1003.10 Sales by a trustee in bankruptcy are subject to the tax if made during the operation of the business of the debtor to the same extent as sales by other retailers.

SALE BY TRUSTEE IN BANKRUPTCY 1003.10 Sales by a trustee in bankruptcy are subject to the tax if made during the operation of the business of the debtor to the same extent as sales by other retailers.

Margin Tax Initiative

Margin Tax Initiative Presented By: Curt Anderson, CPA June 9, 2014 1 Do you not know, my son, with how little wisdom the world is governed? -17th century Swedish statesman Count Oxenstierna in a letter

Margin Tax Initiative Presented By: Curt Anderson, CPA June 9, 2014 1 Do you not know, my son, with how little wisdom the world is governed? -17th century Swedish statesman Count Oxenstierna in a letter

[Business and Tax Regulations Code Enact Gross Receipts Tax and Phase Out Payroll Expense Tax]

![[Business and Tax Regulations Code Enact Gross Receipts Tax and Phase Out Payroll Expense Tax]](/thumbs/27/9549983.jpg "[Business and Tax Regulations Code Enact Gross Receipts Tax and Phase Out Payroll Expense Tax]") FILE NO. MOTION NO. 1 [Business and Tax Regulations Code Enact Gross Receipts Tax and Phase Out Payroll Expense Tax] Motion ordering submitted to the voters an: "Ordinance amending the Business and Tax

FILE NO. MOTION NO. 1 [Business and Tax Regulations Code Enact Gross Receipts Tax and Phase Out Payroll Expense Tax] Motion ordering submitted to the voters an: "Ordinance amending the Business and Tax

Wages of Employed Texans Who Attended Texas Public Schools

Wage Comparision by Educational Attainment for Texans Age 25 to 30 Median 4th Quarter Wages Number Employed Earnings Year 2010 2011 2012 2010 2011 2012 Educational Attainment Advanced Bachelor's Associate

Wage Comparision by Educational Attainment for Texans Age 25 to 30 Median 4th Quarter Wages Number Employed Earnings Year 2010 2011 2012 2010 2011 2012 Educational Attainment Advanced Bachelor's Associate

Taxation of Nonresidents and Individuals Who Change Residency

State of California Franchise Tax Board Taxation of Nonresidents and Individuals Who Change Residency FTB Publication 1100 (REV 04-2014) For forms and information, go to ftb.ca.gov and search for forms

State of California Franchise Tax Board Taxation of Nonresidents and Individuals Who Change Residency FTB Publication 1100 (REV 04-2014) For forms and information, go to ftb.ca.gov and search for forms

Chapter 27 CABLE/VIDEO SERVICE PROVIDER FEE

Chapter 27 CABLE/VIDEO SERVICE PROVIDER FEE 27.01 Definitions 27.02 Cable/Video Service Provider Fee Imposed 27.03 Applicable Principles 27.04 No Impact on Other Taxes Due from Holder 27.05 Audits of Cable/Video

Chapter 27 CABLE/VIDEO SERVICE PROVIDER FEE 27.01 Definitions 27.02 Cable/Video Service Provider Fee Imposed 27.03 Applicable Principles 27.04 No Impact on Other Taxes Due from Holder 27.05 Audits of Cable/Video

STATE BOARD OF EQUALIZATION STAFF LEGISLATIVE BILL ANALYSIS

STATE BOARD OF EQUALIZATION STAFF LEGISLATIVE BILL ANALYSIS Date Amended: 03/23/11 Bill No: Senate Bill 530 Tax Program: Satellite TV Author: Wright Sponsor: Author Code Sections: Part 14.5 (commencing

STATE BOARD OF EQUALIZATION STAFF LEGISLATIVE BILL ANALYSIS Date Amended: 03/23/11 Bill No: Senate Bill 530 Tax Program: Satellite TV Author: Wright Sponsor: Author Code Sections: Part 14.5 (commencing

Calgary Small Businesses: Fact Sheet

Calgary Small Businesses: Fact Sheet Calgary small businesses account for nearly 95 per cent of all businesses they are a driving force within the city s business community. Small business owners have

Calgary Small Businesses: Fact Sheet Calgary small businesses account for nearly 95 per cent of all businesses they are a driving force within the city s business community. Small business owners have

Business-Facts: 3 Digit NAICS Summary 2015

Business-Facts: Digit Summary 5 5 Demographics Radius : 9 CHAPEL ST, NEW HAVEN, CT 65-8,. -.5 Miles, Agriculture, Forestry, Fishing and Hunting Crop Production Animal Production and Aquaculture Forestry

Business-Facts: Digit Summary 5 5 Demographics Radius : 9 CHAPEL ST, NEW HAVEN, CT 65-8,. -.5 Miles, Agriculture, Forestry, Fishing and Hunting Crop Production Animal Production and Aquaculture Forestry

SALES AND USE TAX TECHNICAL BULLETINS SECTION 18

SECTION 18 - CERTAIN GOVERNMENTAL ENTITIES - THE STATE, COUNTIES, CITIES AND OTHER POLITICAL SUBDIVISIONS 18-1 PURCHASES AND SALES BY AND DONATIONS TO GOVERNMENTAL ENTITIES A. Purchases By Governmental

SECTION 18 - CERTAIN GOVERNMENTAL ENTITIES - THE STATE, COUNTIES, CITIES AND OTHER POLITICAL SUBDIVISIONS 18-1 PURCHASES AND SALES BY AND DONATIONS TO GOVERNMENTAL ENTITIES A. Purchases By Governmental

The Business Organization: Choosing an Entity

The Business Organization: Choosing an Entity The subject matter is divided into two sections: 1. Section A shows direct comparison of different types of organizational structures. 2. Section B details

The Business Organization: Choosing an Entity The subject matter is divided into two sections: 1. Section A shows direct comparison of different types of organizational structures. 2. Section B details

Direct Investment Concepts

76 Direct Investment Concepts In this section: Basic concepts and definitions Direct investment Direct investor Affiliates Exclusions U.S. direct investment abroad (USDIA) U.S. parent U.S. direct investment

76 Direct Investment Concepts In this section: Basic concepts and definitions Direct investment Direct investor Affiliates Exclusions U.S. direct investment abroad (USDIA) U.S. parent U.S. direct investment

City and County of San Francisco Office of the Treasurer & Tax Collector

City and County of San Francisco Office of the Treasurer & Tax Collector Gross Receipts Tax & Payroll Expense Tax Online Filing Instructions Tax Year 2014 R e v i s e d 2/19/2015 Table of Contents A Guide

City and County of San Francisco Office of the Treasurer & Tax Collector Gross Receipts Tax & Payroll Expense Tax Online Filing Instructions Tax Year 2014 R e v i s e d 2/19/2015 Table of Contents A Guide

Sales and Use Taxes: Texas

Jay M. Chadha, Fulbright & Jaworski LLP A Q&A guide to sales and use tax law in Texas. This Q&A addresses key areas of sales and use tax law such as tax scope, multi-state transactions and collecting taxes

Jay M. Chadha, Fulbright & Jaworski LLP A Q&A guide to sales and use tax law in Texas. This Q&A addresses key areas of sales and use tax law such as tax scope, multi-state transactions and collecting taxes

U.S.A. Chapter I. Scope of the Convention

U.S.A. Convention between the Kingdom of the Netherlands and the United States of America for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income Done

U.S.A. Convention between the Kingdom of the Netherlands and the United States of America for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income Done

U.S. Corporation Income Tax Return For calendar year 2015 or tax year beginning, 2015, ending, 20

Form 1120 Department of the Treasury Internal Revenue Service A Check if: 1a Consolidated return (attach Form 851). b Life/nonlife consolidated return... 2 Personal holding co. (attach Sch. PH).. 3 Personal

Form 1120 Department of the Treasury Internal Revenue Service A Check if: 1a Consolidated return (attach Form 851). b Life/nonlife consolidated return... 2 Personal holding co. (attach Sch. PH).. 3 Personal

Small Business Data Assess Your Competition Define Your Customers

Small Business Data Assess Your Competition Define Your Customers Census Bureau Data Can Answer Many Questions What Is Census Bureau Data? Economic / business data Economic Census County Business Patterns

Small Business Data Assess Your Competition Define Your Customers Census Bureau Data Can Answer Many Questions What Is Census Bureau Data? Economic / business data Economic Census County Business Patterns

Collection Information Statement for Wage Earners and Self-Employed Individuals

Form 433-A (Rev. December 2012) Department of the Treasury Internal Revenue Service Collection Information Statement for Wage Earners and Self-Employed Individuals Wage Earners Complete Sections 1, 2,

Form 433-A (Rev. December 2012) Department of the Treasury Internal Revenue Service Collection Information Statement for Wage Earners and Self-Employed Individuals Wage Earners Complete Sections 1, 2,

Business Finance: Will I Make a Profit?

By: Michael Brown Business Finance: Will I Make a Profit? FOCUS: Overview: Students analyze the financial information from two business plans to learn how revenues can be increased or costs decreased in

By: Michael Brown Business Finance: Will I Make a Profit? FOCUS: Overview: Students analyze the financial information from two business plans to learn how revenues can be increased or costs decreased in

Martin County - Stuart Employment Center Census Block Groups Selected for Analysis. Prepared by the South Florida Regional Planning Council.

Census Block Groups Selected for Analysis Prepared by the South Florida Regional Planning Council. Page 1 Work Area Profile Report This map is for demonstration purposes only. For a more detailed and customizable

Census Block Groups Selected for Analysis Prepared by the South Florida Regional Planning Council. Page 1 Work Area Profile Report This map is for demonstration purposes only. For a more detailed and customizable

Corporations: FAQ's. Is my Corporate Name Available?

Is my Corporate Name Available? Corporations: FAQ's Money Matters Tax Service will perform a non-binding name check for name availability within the state of incorporation. We perform the name check at

Is my Corporate Name Available? Corporations: FAQ's Money Matters Tax Service will perform a non-binding name check for name availability within the state of incorporation. We perform the name check at

North Bay Industry Sector Rankings (By County) October 2015 Jim Cassio

October 2015 Jim Cassio") North Bay Rankings (By County) October 2015 Jim Cassio North Bay Rankings (By County) Source: EMSI (Economic Modeling Specialists, Intl.) Contents Lake County... 3 Jobs... 3 Job Growth (Projected)...

North Bay Rankings (By County) October 2015 Jim Cassio North Bay Rankings (By County) Source: EMSI (Economic Modeling Specialists, Intl.) Contents Lake County... 3 Jobs... 3 Job Growth (Projected)...

------------------------- ---------------------- c,ab; sþibi sarebibn Law on Taxation

RksYgesdækic nig hirbaøvtßú RBHraCaNacRkkm

RksYgesdækic nig hirbaøvtßú RBHraCaNacRkkm

VERMONT UNEMPLOYMENT INSURANCE WAGES, BENEFITS, CONTRIBUTIONS AND EMPLOYMENT BY INDUSTRY CALENDAR YEAR 2014

WAGES, BENEFITS, CONTRIBUTIONS AND EMPLOYMENT BY INDUSTRY Vermont Department of Labor VERMONT UNEMPLOYMENT INSURANCE PROGRAM WAGES, BENEFITS, CONTRIBUTIONS AND EMPLOYMENT BY INDUSTRY Visit us at our web

WAGES, BENEFITS, CONTRIBUTIONS AND EMPLOYMENT BY INDUSTRY Vermont Department of Labor VERMONT UNEMPLOYMENT INSURANCE PROGRAM WAGES, BENEFITS, CONTRIBUTIONS AND EMPLOYMENT BY INDUSTRY Visit us at our web

Filing Claims for Refund of Sales or Use Tax

State of Wisconsin Department of Revenue Important Change The football stadium district tax in Brown County ends on September 30, 2015. Filing Claims for Refund of Sales or Use Tax Includes information

State of Wisconsin Department of Revenue Important Change The football stadium district tax in Brown County ends on September 30, 2015. Filing Claims for Refund of Sales or Use Tax Includes information

North Carolina s Reference to the Internal Revenue Code Updated - Impact on 2015 North Carolina Corporate and Individual income Tax Returns

June 3 2016 North Carolina s Reference to the Internal Revenue Code Updated - Impact on 2015 North Carolina Corporate and Individual income Tax Returns Governor McCrory signed into law Session Law 2016-6

June 3 2016 North Carolina s Reference to the Internal Revenue Code Updated - Impact on 2015 North Carolina Corporate and Individual income Tax Returns Governor McCrory signed into law Session Law 2016-6

Choice of Entity. Paul E. Costantino, CPA, MST Costantino Richards Rizzo, LLP, Wakefield

Choice of Entity Paul E. Costantino, CPA, MST Costantino Richards Rizzo, LLP, Wakefield I. Overview of Entities The entity selection process is one of the first steps in the formation of any business,

Choice of Entity Paul E. Costantino, CPA, MST Costantino Richards Rizzo, LLP, Wakefield I. Overview of Entities The entity selection process is one of the first steps in the formation of any business,

2012 GRAND RAPIDS CORPORATION INCOME TAX FORM AND INSTRUCTIONS For use by corporations doing business in the City of Grand Rapids

Grand Rapids Income Tax Department P.O. Box 109 Grand Rapids, Michigan 49501-0109 2012 GRAND RAPIDS CORPORATION INCOME TAX FORM AND INSTRUCTIONS For use by corporations doing business in the City of Grand

Grand Rapids Income Tax Department P.O. Box 109 Grand Rapids, Michigan 49501-0109 2012 GRAND RAPIDS CORPORATION INCOME TAX FORM AND INSTRUCTIONS For use by corporations doing business in the City of Grand

SENATE BILL No. 372 page 2

SENATE BILL No. 372 AN ACT relating to sales taxation; concerning the sourcing of mobile telecommunications services; amending K.S.A. 2001 Supp. 79-3603 and repealing the existing section; also repealing

SENATE BILL No. 372 AN ACT relating to sales taxation; concerning the sourcing of mobile telecommunications services; amending K.S.A. 2001 Supp. 79-3603 and repealing the existing section; also repealing

I Virginia retail sales and use tax or Federal and State excise tax on motor vehicle fuel Account Number Assigned by State:

EXCLUSION WORKSHEET FOR USE WITH THE FAIRFAX COUNTY BPOL (Tax Year) This worksheet should be used to identify all exclusions claimed on the business license applications to include forms: 8TA-FF, 8TA-E1,

EXCLUSION WORKSHEET FOR USE WITH THE FAIRFAX COUNTY BPOL (Tax Year) This worksheet should be used to identify all exclusions claimed on the business license applications to include forms: 8TA-FF, 8TA-E1,

Reg. 1.5833-1 (Effective for tax years beginning on and after January 1, 1998) Allocation and apportionment of Vermont net income by corporations

Allocation and apportionment of Vermont net income by corporations") Reg. 1.5833 ALLOCATION AND APPORTIONMENT OF INCOME Reg. 1.5833-1 (Effective for tax years beginning on and after January 1, 1998) Allocation and apportionment of Vermont net income by corporations (a)

Reg. 1.5833 ALLOCATION AND APPORTIONMENT OF INCOME Reg. 1.5833-1 (Effective for tax years beginning on and after January 1, 1998) Allocation and apportionment of Vermont net income by corporations (a)

Willamette Management Associates

Valuation Analyst Considerations in the C Corporation Conversion to Pass-Through Entity Tax Status Robert F. Reilly, CPA For a variety of economic and taxation reasons, this year may be a particularly

Valuation Analyst Considerations in the C Corporation Conversion to Pass-Through Entity Tax Status Robert F. Reilly, CPA For a variety of economic and taxation reasons, this year may be a particularly

2013 ATHENS INSTRUCTIONS

2013 ATHENS INSTRUCTIONS WHO MUST FILE CITY OF ATHENS INCOME TAX RETURN Non Mandatory Filing: If your only income is from W-2 wages and your employer has withheld 100% of the Athens tax due, you are not

2013 ATHENS INSTRUCTIONS WHO MUST FILE CITY OF ATHENS INCOME TAX RETURN Non Mandatory Filing: If your only income is from W-2 wages and your employer has withheld 100% of the Athens tax due, you are not

The North American Industry Classification System (NAICS)

") The North American Industry Classification System (NAICS) 1 The North American Industry Classification System (NAICS) has replaced the U.S. Standard Industrial Classification (SIC) system http://www.census.gov/epcd/www/naics.html

The North American Industry Classification System (NAICS) 1 The North American Industry Classification System (NAICS) has replaced the U.S. Standard Industrial Classification (SIC) system http://www.census.gov/epcd/www/naics.html

2. Corporations Fully Exempt These corporations qualify for the full income tax exemption:

T. Exempt Corporations (G.S. 105-125, G.S. 105-130.11, G.S. 105-130.12) 1. Preliminary Statement Some types of corporations are fully exempt from income and franchise taxes, whereas others are conditionally

T. Exempt Corporations (G.S. 105-125, G.S. 105-130.11, G.S. 105-130.12) 1. Preliminary Statement Some types of corporations are fully exempt from income and franchise taxes, whereas others are conditionally

RETURN FORM GUIDANcE NOTES

RETURN FORM GUIDANcE NOTES IMPORTANT INFORMATION TO ASSIST WITH THE COMPLETION OF COMPANY RETURN FORMS (R1C) This booklet is for your use and is not required to be returned to the Income Tax Division.

RETURN FORM GUIDANcE NOTES IMPORTANT INFORMATION TO ASSIST WITH THE COMPLETION OF COMPANY RETURN FORMS (R1C) This booklet is for your use and is not required to be returned to the Income Tax Division.

Changing the Way Your Dirt Is Taxed Texas Margin Tax Pitfalls for Real Estate Practitioners. By Benjamin Miller 1

Changing the Way Your Dirt Is Taxed Texas Margin Tax Pitfalls for Real Estate Practitioners By Benjamin Miller 1 In 2006, the Texas Legislature passed the first version of its successor to the Texas franchise

Changing the Way Your Dirt Is Taxed Texas Margin Tax Pitfalls for Real Estate Practitioners By Benjamin Miller 1 In 2006, the Texas Legislature passed the first version of its successor to the Texas franchise

Presents: The Solo 401(k) Plan The Ultimate Retirement Solution for the Self Employed January 2012

Plan The Ultimate Retirement Solution for the Self Employed January 2012") Presents: The Solo 401(k) Plan The Ultimate Retirement Solution for the Self Employed January 2012 Disclaimer: The information provided in this presentation/document is not legal advice, but general information

Presents: The Solo 401(k) Plan The Ultimate Retirement Solution for the Self Employed January 2012 Disclaimer: The information provided in this presentation/document is not legal advice, but general information

Assessing Industry Codes on the IRS Business Master File Paul B. McMahon, Internal Revenue Service

Assessing Industry Codes on the IRS Business Master File Paul B. McMahon, Internal Revenue Service An early process in the development of any business survey is the construction of a sampling frame, and

Assessing Industry Codes on the IRS Business Master File Paul B. McMahon, Internal Revenue Service An early process in the development of any business survey is the construction of a sampling frame, and

Texas - Franchise tax relief, R&D incentives, sales and use tax exemptions for telecommunication, internet providers

No. 2013-301 June 17, 2013 Texas - Franchise tax relief, R&D incentives, sales and use tax exemptions for telecommunication, internet providers June 17: Texas Governor Rick Perry on June 14 signed three

No. 2013-301 June 17, 2013 Texas - Franchise tax relief, R&D incentives, sales and use tax exemptions for telecommunication, internet providers June 17: Texas Governor Rick Perry on June 14 signed three