Automated Underwriting. Classroom Text

|

|

|

- Mark Crawford

- 9 years ago

- Views:

Transcription

1 Automated Underwriting Classroom Text

2 Chapter Four Page 1 Automated Underwriting The Reasoning Behind Automated Underwriting The mortgage industry is rapidly moving into the automated age. Lead-generation companies that utilize mass-marketing technology; loan origination software that plugs directly into a company s pipeline reporting; internet websites that can originate and pre-approve a loan, these are all examples of how the process of getting a loan into The System has improved. It would be foolhardy to develop methods to increase production on the front end if there were no improved system for getting loans out the back end! Thus, Fannie Mae and Freddie Mac have developed automated underwriting systems that are designed to do just that to utilize technology to reduce costs and streamline processes throughout the mortgage cycle. And it s not just Fannie Mae and Freddie Mac, many portfolio and subprime lenders have developed technology designed to expedite and simplify the approval process. Each entity has its own system; yet despite the different names, are intended to achieve the same goals. Fannie Mae calls her system Desktop Underwriter (DU), while Freddie Mac calls his Loan Prospector (LP). Portfolio and subprime lenders have trade names for theirs, as well. Automated underwriting represents a more sophisticated way of assessing mortgage risk, enabling the tailoring of specific loan data contained in the file based on an individual borrower s risk profile. These flexibilities include: streamlined documentation and appraisals, less stringent mortgage insurance requirements, and expanded LTV ratios and product offerings. The automated systems are currently designed to underwrite the following loan types: Owner Occupied Second Home Non-Owner Occupied Purchase Rate & Term Refinance Cash Out Refinance One to Four Unit Properties First Mortgages Fixed rate, Adjustable rate, Balloon mortgages Construction to Permanent Community Lending Tiered pricing products (Level I, II or III) DU and LP will perform an underwriting analysis using either a completed 1003 or a subset of information from the loan application. The option to underwrite using a lessthan-complete 1003 supports the need for point of sale qualification, where quick, yet conditional, credit recommendations can be made using the information gathered during

3 Chapter Four Page 2 a borrower interview. In situations where a credit recommendation is performed using a partial 1003, the lender and borrower must complete the 1003 prior to closing, with any modified information resubmitted to the AU for approval. Desktop Underwriter and Loan Prospector are designed to evaluate a loan file based on risk layering, as opposed to looking at each individual component. This allows for a more accurate determination of a borrower s likelihood of default. These AUS models have been developed after many years of data being compiled on borrower credit habits, transaction type and their relationship to default rates. This layering of risk concept can provide for more latitude in certain areas of your file, such as debt ratios, or can be more restrictive in other areas, such as transaction type versus LTV. These risk layers generally fall into three categories, and we call them the 3 C s of Underwriting: Credit Capacity Collateral Credit history Credit score Income Assets and Liabilities Debt ratios Collateral Type and LTV Value, Condition and Marketability How to Access Automated Underwriting As a processor working for a mortgage broker, it is not likely that you will have unlimited, unrestricted access to an automated underwriting system. These systems are designed to perform many functions for a wholesale lender, and for Fannie Mae and Freddie Mac. First, the AU systems can and should be utilized as a pre-qualification tool by the mortgage originator. This requires written authorization from a borrower, as their credit report will be pulled by the lending agency. Second, the AU systems are used by the lending agency as a monitor of borrower activity; if the same borrower has applied for two different owner-occupied loans at the same time through two different lenders, the systems will pick it up. Next, many wholesale lenders use their systems to monitor origination activity versus funding activity, and finally, the systems are used as final underwriting and acceptance/eligibility tools by the wholesale lenders. There are different means of reaching these systems, and depending upon your company policy and the wholesale lenders you work with, you may use one or all of these avenues to access DU, LP or other AU systems.

4 Chapter Four Page 3 Agency Direct Access Your company may be set up to access DU or LP by going directly to the agency website and inputting your data into their system. In order to do this, your company will need to have a User ID and a Password, which are now electronically transmitted to you once you have successfully registered as a user with Fannie Mae and/or Freddie Mac. Your company will also be responsible for all fees generated by this direct access method. The biggest advantage to utilizing direct access, however, is that your file will receive a response almost immediately. Both Fannie Mae and Freddie Mac offer training to mortgage industry personnel on how to input 1003 information into their systems to perform underwriting analyses. It is recommended that you take advantage of these training sessions if this is the method of choice for your company to access AU. Lender-Sponsored AU Many wholesale lenders have developed systems that integrate their product offerings with DU and LP credit recommendations. It is necessary to become an approved broker with each wholesale lender in order to access their systems. The information on your borrower will generally be uploaded from your loan origination system (LOS), or processing software, directly into the lender s system. Many lenders have time restrictions that must be met for an approval to be valid, and some will not allow the loan to be locked in with their secondary marketing department until their AU has been completed. Also, you may not receive your underwriting analysis for several minutes. Frequently, the cost of accessing DU or LP for an underwriting decision will be borne by the wholesale lender. Most lenders that offer AU access through their websites also offer training, either on-line or with a manual. Again, it will prove expeditious for you to take advantage of this training. E-Commerce Portals As we mentioned earlier, the mortgage industry is moving rapidly into the lead in e-commerce and business-tobusiness (B2B) technology offerings. There are several broad-based B2B vertical portals through which originators can access products and services sponsored by wholesalers, investors, and vendors, including automated underwriting systems, such as DU and LP. As with the lender-sponsored AU, your borrower information will be

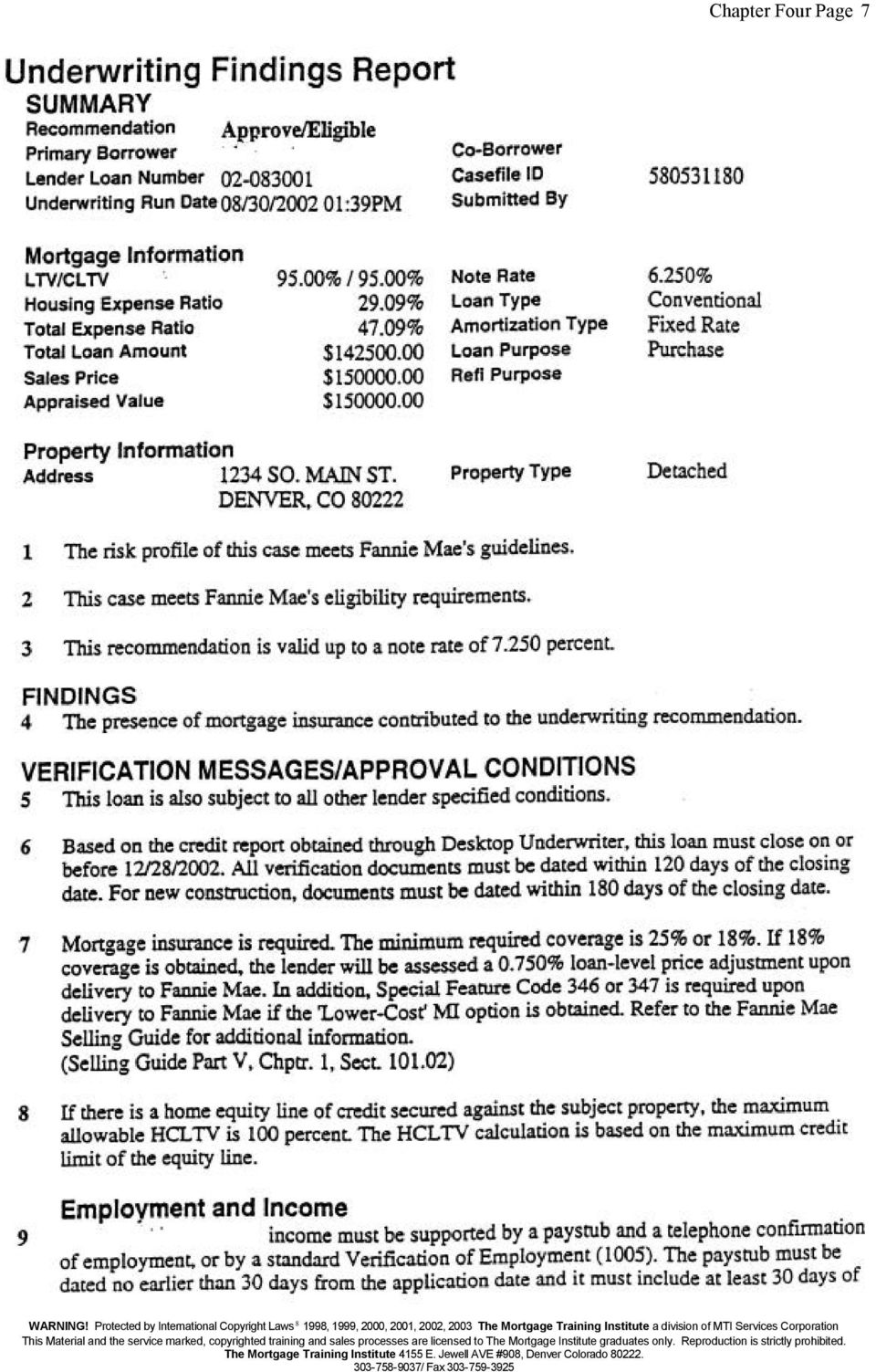

5 Chapter Four Page 4 uploaded directly from your LOS into these portals once you have selected a sponsoring lender. Other services such as flood certificates, appraisals, and mortgage insurance products can be obtained using this method. The Underwriting Recommendation After each loan is submitted for preliminary underwriting analysis, DU or LP will display the underwriting recommendation on the appropriate screen, depending on access venue. In most cases, the recommendation is defined in terms of the credit risk profile of the case and in terms of meeting the requirements of Fannie Mae or Freddie Mac purchase eligibility. These two recommendations will tell you if: 1) the credit risk meets underwriting guidelines, and 2) if the loan is eligible for purchase by either entity. It is possible for your loan to meet the underwriting guidelines, yet not be eligible for purchase. Sometimes the loan is not eligible for purchase, according to the automated system, because of variances in the loan parameters such as LTV or property type. You will need to confirm with your lender if they have a particular commitment that allows for these variances, and if so, you should continue to process the file according to the processing requirements, and submit it to your wholesale lender for manual approval of the variance. It is important to clarify that the AUS models do not make the decision to grant or deny credit that is left up to the wholesale lender. The AUS models are tools that are utilized to enhance a lender s ability to extend mortgage credit by consistently applying requirements and guidelines when evaluating a borrower s creditworthiness. FNMA UNDERWRITING FINDINGS REPORT Fannie Mae will issue its recommendation via an Underwriting Findings report, and issue you Verification Messages/Approval Conditions telling you how to process your loan in order for it to meet approval/eligibility requirements at closing. The Fannie Mae recommendations that could come back are: Approve/Eligible Based on the data submitted to DU, the loan meets credit risk criteria and is eligible for purchase. This is as strong of a preapproval that you can get! Make sure your verified information matches what s on your initial application, and you re sure to go to closing! You must comply with all of the Verification Messages/Approval Conditions listed in the Underwriting Findings report and document the loan file accordingly. And, you must apply due diligence when reviewing the documentation in the loan file to determine if there is any potentially derogatory or contradictory information that is not part of the data analyzed by Desktop Underwriter. Furthermore, you should review the credit report to confirm that the data that Desktop Underwriter evaluated with

6 Chapter Four Page 5 respect to the borrower s credit history was accurate and complete. Any information that you are aware of that appears to have escaped DU notice should be documented in your file in accordance with full Fannie Mae underwriting guidelines. Approve/Ineligible Refer/Eligible Refer/Ineligible The loan meets credit risk requirements based on the underwriting guidelines (such as debt ratios, cash requirements, loan purpose), but does not meet purchase requirements (such as LTV or loan type). You will need to review the reasons listed for the Ineligible finding, and investigate alternative parameters that may alleviate the perceived additional layering of risk in the file. A lender can deliver loans that receive an Approve/Ineligible recommendation to Fannie Mae if the lender has a negotiated variance in its commitment that covers the ineligible condition specific to the loan transaction. The data submitted to DU indicates that the borrower does not meet the credit criteria as set forth in the underwriting guidelines, such as liquid assets, debt ratio, or credit history. Thus, DU cannot recommend approval of the loan, however, Fannie Mae indicates that it would purchase the loan based on other eligibility factors such as LTV and loan type. The Underwriting Findings will outline the main reasons for the Refer recommendation. You must then determine if you have compensating factors to overcome the reason for referral, and know that you will have to document them. This may then allow an underwriter who is manually reviewing your file to make an assessment for approval. Based on the data submitted to DU, the loan does not meet Fannie Mae s credit risk and eligibility requirements. The system will have evaluated a combination of risk factors, including the LTV, debt ratio, liquid assets, each borrower s credit history, employment status, property type, loan type, and the purpose of the loan. Based on the data submitted, DU cannot recommend approval of the loan, and finds that the layering of risk renders it ineligible for purchase. If you can make the loan meet the credit requirements at final approval, a lender can deliver the loan to Fannie Mae if the lender has a negotiated variance in its commitment that covers the ineligible condition specific to the loan transaction. Refer with Caution Based on the data submitted to DU, and after assessing all information, the system cannot recommend an approval. The layering of risk associated with the information contained in the file represents a greater risk of default than those with an Approve or Refer recommendation. The loan may be eligible for sale to Fannie Mae based on loan parameters; however, the perceived degree of

.")

7 Chapter Four Page 6 risk is too high. Certain transactions that contain a high degree of credit risk that receive this recommendation are not allowed to be sold to Fannie Mae, even if they receive an Eligible finding. Among the more common transactions included here are: Limited cash-out refinance mortgages with LTVs greater than 90% (other than fixed-rate mortgages securing one-unit properties). Cash-out refinance mortgages with LTVs greater than 75%. Mortgages secured by investment properties with LTVs greater than 80%. ARMs secured by three- and four-unit investment properties. Mortgages subject to subordinate financing with LTVs greater than 75% and CLTV s greater than 90% to 95%, such as 80/15/5 and 90/5/5 Your documentation requirements will be listed in the Verification Messages/Approval Conditions section, specifically identifying credit issues you should address, employment income docs needed, asset verification required, and type of appraisal needed.

8 Chapter Four Page 7

9 Chapter Four Page 8

10 Chapter Four Page 9

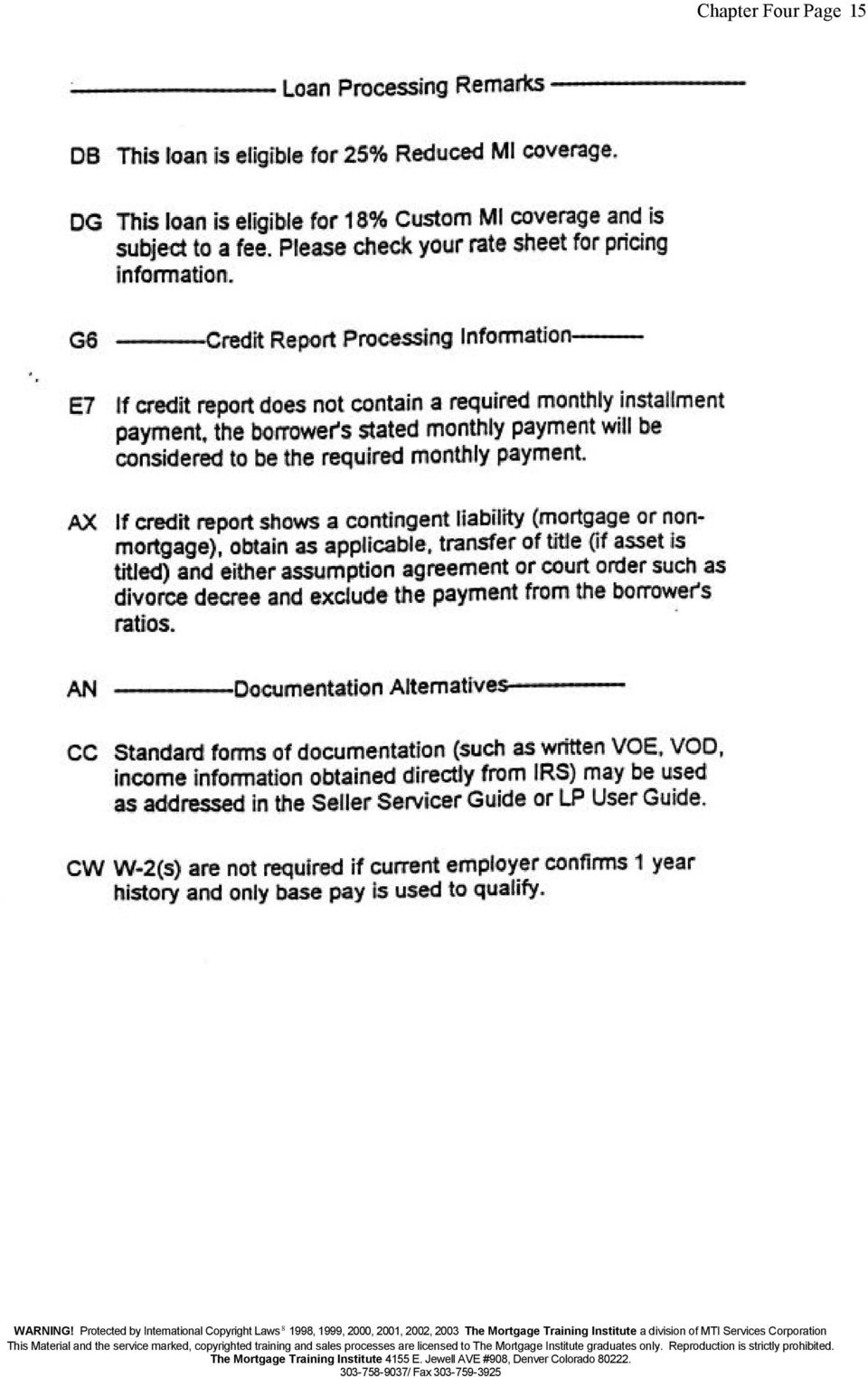

11 Chapter Four Page 10 FHLMC FEEDBACK CERTIFICATE Freddie Mac will issue its recommendations via a Feedback Certificate. After identifying the Evaluation Status of the data submission, it will also provide an assessment for purchase eligibility, credit risk class, documentation class, and minimum collateral assessment. Here are the main components of the Feedback Certificate: Evaluation Status: Complete the AUS has processed the transaction successfully. Invalid - there is information missing or inaccurate that prevents the AUS from processing your request. Refer to the Feedback Certificate for reasons. Ineligible the AUS cannot evaluate your transaction, it does not meet acceptable transaction guidelines (such as five unit property, too many borrowers, etc). Refer to the Feedback Certificate for reasons. Incomplete the AUS was unable to acquire the needed credit data to evaluate the transaction. Refer to the Feedback Certificate for reasons. Purchase Eligibility: Freddie Mac Acceptable the loan is eligible for purchase by Freddie Mac according to their standards as set forth in their Seller/Servicer Guidelines. Freddie Mac Ineligible the loan is eligible for evaluation but not for sale to Freddie Mac as per their standards as set forth in their Seller/Servicer Guidelines. 500 Freddie Mac Eligible the loan receives an A-Minus Offering. It may be eligible for Accept processing subject to specific terms. Credit Risk Class: Accept based on the analysis of credit and other data submitted, the credit risk class is acceptable provided all information is true, correct and complete. Caution the application has serious risks that must be evaluated with a full credit and collateral analysis to determine if it is salable to Freddie Mac. Documentation Class: Accept Plus this is the most expedient processing available. It uses stated income and debt, expanded ratios and only requires a verbal employment verification for salaried borrowers. Self-

12 Chapter Four Page 11 employed borrowers can qualify for Accept Plus regardless of how long they have been self employed. Streamlined Accept there are substantially fewer documentation requirements than full processing. Standard this requires standard, or full processing documentation as identified in the Seller/Servicer Guidelines. Your documentation requirements will be listed on the Documentation Checklist provided with the Feedback Certificate. You should review the Loan Information Section in the Certificate in detail, however, to identify any credit issues you should address, and specifics on employment and income docs needed, asset verification required, and type of appraisal needed. In summary, the concept of using an AUS as a processing tool is simply put: Enter & Review Process & Submit Completed Submit Data Recommendations/ Package Loan Loan to Lender for To AUS. Feedback Info. Accordingly. Final Approval.

13 Chapter Four Page 12

14 Chapter Four Page 13

15 Chapter Four Page 14

16 Chapter Four Page 15

Desktop Originator /Desktop Underwriter Version 5.5

Desktop Originator /Desktop Underwriter Version 5.5 Release Notes May 20, 2005 Updated June 8, 2005 In July 2005, we will implement DU Version 5.5. This new version will contain a number of enhancements

Desktop Originator /Desktop Underwriter Version 5.5 Release Notes May 20, 2005 Updated June 8, 2005 In July 2005, we will implement DU Version 5.5. This new version will contain a number of enhancements

Desktop Originator/Desktop Underwriter Release Notes DU Version 9.2

Desktop Originator/Desktop Underwriter Release Notes DU Version 9.2 October 14, 2014 Last updated December 8, 2014 During the weekend of December 13, 2014, Fannie Mae will implement Desktop Underwriter

Desktop Originator/Desktop Underwriter Release Notes DU Version 9.2 October 14, 2014 Last updated December 8, 2014 During the weekend of December 13, 2014, Fannie Mae will implement Desktop Underwriter

U.S. BANK WHOLESALE DELEGATED UNDERWRITING REQUIREMENTS

U.S. BANK WHOLESALE DELEGATED UNDERWRITING REQUIREMENTS The following information is required by U.S. Bank Wholesale Department to be eligible for consideration of delegated underwriting authority. 1.

U.S. BANK WHOLESALE DELEGATED UNDERWRITING REQUIREMENTS The following information is required by U.S. Bank Wholesale Department to be eligible for consideration of delegated underwriting authority. 1.

ditech BUSINESS LENDING FREDDIE MAC ELIGIBLE ARM PRODUCT CORRESPONDENT ONLY

1. PRODUCT DESCRIPTION Conventional Conforming five year/one year adjustable rate mortgage Servicing retained 30-year term Fully amortizing Non-convertible ARM Plan ID 2725 Manufactured homes not eligible

1. PRODUCT DESCRIPTION Conventional Conforming five year/one year adjustable rate mortgage Servicing retained 30-year term Fully amortizing Non-convertible ARM Plan ID 2725 Manufactured homes not eligible

Multiple Financed Properties Program Fannie Mae/Freddie Mac. Table of Contents

Table of Contents 1. Category... 2 2. High Balance... 2 3. Property Types...2 4. Applying the Multiple Financed property Policy to Manually Underwritten Loans... 2 5. Applying the Multiple Financed property

Table of Contents 1. Category... 2 2. High Balance... 2 3. Property Types...2 4. Applying the Multiple Financed property Policy to Manually Underwritten Loans... 2 5. Applying the Multiple Financed property

Automated Property Service: Frequently Asked Questions

Automated Property Service: Frequently Asked Questions April 2015 APS Overview Q1: What is Fannie Mae s Automated Property Service (APS) Fannie Mae s Automated Property Service (APS) is an automated property

Automated Property Service: Frequently Asked Questions April 2015 APS Overview Q1: What is Fannie Mae s Automated Property Service (APS) Fannie Mae s Automated Property Service (APS) is an automated property

Announcement 09-13 May 11, 2009. Home Affordable Refinance Updates and Clarifications to Announcement 09-04

Announcement 09-13 May 11, 2009 Amends these Guides: Selling Home Affordable Refinance Updates and Clarifications to Announcement 09-04 Introduction On March 4, 2009, Fannie Mae announced two new refinance

Announcement 09-13 May 11, 2009 Amends these Guides: Selling Home Affordable Refinance Updates and Clarifications to Announcement 09-04 Introduction On March 4, 2009, Fannie Mae announced two new refinance

Processing FHA TOTAL and VA Mortgages

This reference contains information to help you process Federal Housing Administration (FHA) mortgages and Department of Veteran Affairs (VA) mortgages using Loan Prospector. Information on FHA TOTAL Mortgage

This reference contains information to help you process Federal Housing Administration (FHA) mortgages and Department of Veteran Affairs (VA) mortgages using Loan Prospector. Information on FHA TOTAL Mortgage

HOME BUYING101 TM %*'9 [[[ EPXEREJGY SVK i

HOME BUYING101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

HOME BUYING101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

Desktop Originator/Desktop Underwriter Release Notes DU Version 9.3

Desktop Originator/Desktop Underwriter Release Notes DU Version 9.3 September 29, 2015 During the weekend of December 12, 2015, Fannie Mae will implement Desktop Underwriter (DU ) Version 9.3, which will

Desktop Originator/Desktop Underwriter Release Notes DU Version 9.3 September 29, 2015 During the weekend of December 12, 2015, Fannie Mae will implement Desktop Underwriter (DU ) Version 9.3, which will

Conforming DU Refi Plus (HARP 2)

") Conforming DU Refi Plus (HARP 2) Investor 04 Retail Only SNMC will accept loan submissions for the Home Affordable Refinance Program - HARP 2. These loan submissions will be subject to the current FNMA

Conforming DU Refi Plus (HARP 2) Investor 04 Retail Only SNMC will accept loan submissions for the Home Affordable Refinance Program - HARP 2. These loan submissions will be subject to the current FNMA

Conventional DU Refi Plus

Endeavor America Loan Services Conventional DU Refi Plus Guidelines Conventional Guidelines... 3 Matrix... 3 Overview... 3 Program Expiration... 3 Loan Purpose... 4 Maximum LTV, CLTV, and HCLTV Ratios

Endeavor America Loan Services Conventional DU Refi Plus Guidelines Conventional Guidelines... 3 Matrix... 3 Overview... 3 Program Expiration... 3 Loan Purpose... 4 Maximum LTV, CLTV, and HCLTV Ratios

1030HARP DU REFI PLUS (6/8/12)

") 1030HARP DU REFI PLUS (6/8/12) DESCRIPTION REQUIRED BORROWER BENEFIT DU Refi Plus is a limited cash-out refinance program that allows for expanded eligibility criteria, as well as reduced documentation

1030HARP DU REFI PLUS (6/8/12) DESCRIPTION REQUIRED BORROWER BENEFIT DU Refi Plus is a limited cash-out refinance program that allows for expanded eligibility criteria, as well as reduced documentation

Processing FHA TOTAL and VA Mortgages

This reference contains information to help you process Federal Housing Administration (FHA) mortgages and Department of Veteran Affairs (VA) mortgages using Loan Prospector. Information on FHA TOTAL Mortgage

This reference contains information to help you process Federal Housing Administration (FHA) mortgages and Department of Veteran Affairs (VA) mortgages using Loan Prospector. Information on FHA TOTAL Mortgage

Maximum loan amounts, LTV, CLTV & HCLTV per Desktop Underwriter (DU) or Loan Prospector (LP) guidelines

or Loan Prospector (LP) guidelines") Section 500 Loan Products 500.01 Product Overview In general, Loans eligible for purchase by LAKE MICHIGAN FINCIAL must meet the standards and guidelines of Fannie Mae and Freddie Mac (Agencies), dependent

Section 500 Loan Products 500.01 Product Overview In general, Loans eligible for purchase by LAKE MICHIGAN FINCIAL must meet the standards and guidelines of Fannie Mae and Freddie Mac (Agencies), dependent

EFFECTIVE FOR FHA CASE NUMBER ASSIGNMENTS ON AND AFTER SEPTEMBER 14, 2015 OVERLAY MATRIX: GOVERNMENT

Appraisals Attached PUDs Automated Findings Condominiums Credit History VA: Form 2055 Appraisal dated prior to the Note Date required on IRRRLs if current VA loan is not serviced by BB&T. FHA: Property

Appraisals Attached PUDs Automated Findings Condominiums Credit History VA: Form 2055 Appraisal dated prior to the Note Date required on IRRRLs if current VA loan is not serviced by BB&T. FHA: Property

Multiple (5-10) Financed Properties Retail and Wholesale

Financed Properties Retail and Wholesale") Multiple (5-10) Financed Properties Retail and Wholesale Revisions Date Revisions 2/3/15 Updated Sections: Overview, Subject Property is Second Home or Investment Property, Delayed Financing Exception,

Multiple (5-10) Financed Properties Retail and Wholesale Revisions Date Revisions 2/3/15 Updated Sections: Overview, Subject Property is Second Home or Investment Property, Delayed Financing Exception,

Desktop Originator/Desktop Underwriter Release Notes DU Version 9.1

Desktop Originator/Desktop Underwriter Release Notes DU Version 9.1 August 20, 2013 During the weekend of November 16, 2013, Fannie Mae will implement Desktop Underwriter (DU ) Version 9.1, which will

Desktop Originator/Desktop Underwriter Release Notes DU Version 9.1 August 20, 2013 During the weekend of November 16, 2013, Fannie Mae will implement Desktop Underwriter (DU ) Version 9.1, which will

Agency Conforming Fixed Rate Products. Agency 20 Year Fixed

Agency Conforming Fixed Rate Products Agency 30 Year Fixed Agency 20 Year Fixed APR APR Non-Escrowed Loans ***No charge for non-escrowed loans*** 3.250 1.000 3.445 State Adjustment Zone 1: 3.375 0.250

Agency Conforming Fixed Rate Products Agency 30 Year Fixed Agency 20 Year Fixed APR APR Non-Escrowed Loans ***No charge for non-escrowed loans*** 3.250 1.000 3.445 State Adjustment Zone 1: 3.375 0.250

What to Look For in a Pre-Approval

What to Look For in a Pre-Approval Authored by Keith Bergfeld, Network Funding, LP And the ongoing focus group dedicated to improving the efficiency of real estate transactions. Alan Anderson First American

What to Look For in a Pre-Approval Authored by Keith Bergfeld, Network Funding, LP And the ongoing focus group dedicated to improving the efficiency of real estate transactions. Alan Anderson First American

Announcement 08-22 September 5, 2008. Miscellaneous Eligibility, Policy, and Pricing Updates

Announcement 08-22 September 5, 2008 Amends these Guides: Selling Miscellaneous Eligibility, Policy, and Pricing Updates Introduction This Announcement contains updates and clarifications to Fannie Mae

Announcement 08-22 September 5, 2008 Amends these Guides: Selling Miscellaneous Eligibility, Policy, and Pricing Updates Introduction This Announcement contains updates and clarifications to Fannie Mae

HOME BUYING101. 701.255.0042 www.capcu.org i

HOME BUYING101 701.255.0042 www.capcu.org i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended,

HOME BUYING101 701.255.0042 www.capcu.org i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended,

Example 1 of 3 Accept Feedback Certificate Primary Residence

Example 1 of 3 Accept Feedback Certificate Primary Residence ***** This loan is subject to one or more fees. Please refer to the Delivery Fees Information section of the Full Feedback Certificate for details.

Example 1 of 3 Accept Feedback Certificate Primary Residence ***** This loan is subject to one or more fees. Please refer to the Delivery Fees Information section of the Full Feedback Certificate for details.

E MORTGAGE MANAGEMENT, LLC 704 VA

E MORTGAGE MANAGEMENT, LLC 704 VA IRRRLs PRODUCT GUIDELINES 1/26/2015 Mortgage Eligibility Product Code Short Long Description Description Description VF15IRL VA 15 YR IRRRL VF15IRL - VA 15 YR IRRRL VF30IRL

E MORTGAGE MANAGEMENT, LLC 704 VA IRRRLs PRODUCT GUIDELINES 1/26/2015 Mortgage Eligibility Product Code Short Long Description Description Description VF15IRL VA 15 YR IRRRL VF15IRL - VA 15 YR IRRRL VF30IRL

E MORTGAGE MANAGEMENT, LLC 702 VA ARMS PRODUCT GUIDELINES

E MORTGAGE MANAGEMENT, LLC 702 VA ARMS PRODUCT GUIDELINES 2/24/2015 Mortgage Eligibility Product Code Short Description Long Description Description VF31 VA 3 YR ARM VF31 - VA 3-1 ARM VF51 VA 5 YR ARM

E MORTGAGE MANAGEMENT, LLC 702 VA ARMS PRODUCT GUIDELINES 2/24/2015 Mortgage Eligibility Product Code Short Description Long Description Description VF31 VA 3 YR ARM VF31 - VA 3-1 ARM VF51 VA 5 YR ARM

Texas Home Equity Program Guide Fixed Rate

Fixed Rate Wholesale Lending July 20, 2015 Table of Contents Texas Home Equity Program Guide... 1 Fixed Rate... 1 Program Overview... 2 Employee Loan Policy... 2 Credit Philosophy... 2 Ability to Repay

Fixed Rate Wholesale Lending July 20, 2015 Table of Contents Texas Home Equity Program Guide... 1 Fixed Rate... 1 Program Overview... 2 Employee Loan Policy... 2 Credit Philosophy... 2 Ability to Repay

DU User s Guide for FHA Loans

DU User s Guide for FHA Loans 2003, 2005 Fannie Mae. All rights reserved. Desktop Originator, DO, Desktop Underwriter, and DU are registered trademarks of Fannie Mae. FICO is a registered trademark of

DU User s Guide for FHA Loans 2003, 2005 Fannie Mae. All rights reserved. Desktop Originator, DO, Desktop Underwriter, and DU are registered trademarks of Fannie Mae. FICO is a registered trademark of

Oaktree Funding Corporation

Freddie Mac s Relief Refinance Open Access Agenda What is Relief Refinance Mortgages Open Access? AUS and Qualifications FAQ s Questions 2 What is Relief Refinance Mortgages Open Access? The Freddie Mac

Freddie Mac s Relief Refinance Open Access Agenda What is Relief Refinance Mortgages Open Access? AUS and Qualifications FAQ s Questions 2 What is Relief Refinance Mortgages Open Access? The Freddie Mac

FHA Standard Refinance Cash Out

This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

E MORTGAGE MANAGEMENT, LLC 701 VA FIXED PRODUCT GUIDELINES

E MORTGAGE MANAGEMENT, LLC 70 VA FIXED PRODUCT GUIDELINES 2/24/205 Mortgage Eligibility Product Code Short Description Long Description Description VF5 VA 5 YR VF5 - VA FIXED 5 YEAR VF20 VA 20 YR VF20

E MORTGAGE MANAGEMENT, LLC 70 VA FIXED PRODUCT GUIDELINES 2/24/205 Mortgage Eligibility Product Code Short Description Long Description Description VF5 VA 5 YR VF5 - VA FIXED 5 YEAR VF20 VA 20 YR VF20

Lending Guide. Section 400 Loan Submission & Standards

General Brokers have the option to submit loans to Rushmore Home Loans, a division of Rushmore Loan Management Services LLC (Rushmore) for underwriting via e-mail, Rushmore s IQ2 System, or courier/mail

General Brokers have the option to submit loans to Rushmore Home Loans, a division of Rushmore Loan Management Services LLC (Rushmore) for underwriting via e-mail, Rushmore s IQ2 System, or courier/mail

Home Affordable Refinance Program (HARP) 2.0 DU Refi Plus and Freddie Mac Relief Refinance-Open Access Training Updated - May 4, 2012

2.0 DU Refi Plus and Freddie Mac Relief Refinance-Open Access Training Updated - May 4, 2012") Home Affordable Refinance Program (HARP) 2.0 DU Refi Plus and Freddie Mac Relief Refinance-Open Access Training Updated - May 4, 2012 The Federal Housing Finance Agency (FHFA) announced changes to the

Home Affordable Refinance Program (HARP) 2.0 DU Refi Plus and Freddie Mac Relief Refinance-Open Access Training Updated - May 4, 2012 The Federal Housing Finance Agency (FHFA) announced changes to the

PRODUCT MATRIX 7/25/2012

PRODUCT MATRIX 7/25/2012 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing, registration and closing

PRODUCT MATRIX 7/25/2012 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing, registration and closing

Fannie Mae DU Refi Plus Helping borrowers efficiently refinance Fannie Mae loans

Why DU Refi Plus Fannie Mae DU Refi Plus Helping borrowers efficiently refinance Fannie Mae loans 2 Why DU Refi Plus Provides a competitively-priced, streamline refinance option to qualified borrowers

Why DU Refi Plus Fannie Mae DU Refi Plus Helping borrowers efficiently refinance Fannie Mae loans 2 Why DU Refi Plus Provides a competitively-priced, streamline refinance option to qualified borrowers

ELIGIBILITY MATRIX. Table of Contents. Standard Eligibility Requirements - Desktop Underwriter Page 2

ELIGIBILITY MATRIX The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio requirements for conventional first mortgages eligible for delivery to Fannie Mae. The Eligibility Matrix

ELIGIBILITY MATRIX The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio requirements for conventional first mortgages eligible for delivery to Fannie Mae. The Eligibility Matrix

CHAPTER 9 PRODUCT MATRIX

Contents CHAPTER 9 PRODUCT MATRIX Conventional Conforming Loans 2 Secondary Market Arms... 4 HARP (Fannie DU Refi Plus & Freddie Open Access)... 5 Rural Housing 5 VA Programs. 5 Jumbo Programs 5 My Community

Contents CHAPTER 9 PRODUCT MATRIX Conventional Conforming Loans 2 Secondary Market Arms... 4 HARP (Fannie DU Refi Plus & Freddie Open Access)... 5 Rural Housing 5 VA Programs. 5 Jumbo Programs 5 My Community

Section 2.08 - Jumbo Solution Second Mortgage

- In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 3 Loan Terms... 4 Assumptions... 4 Eligible First and Second Mortgage Products...

- In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 3 Loan Terms... 4 Assumptions... 4 Eligible First and Second Mortgage Products...

Lesson 13: Applying for a Mortgage Loan

1 Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 2 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit unions

1 Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 2 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit unions

Financing Residential Real Estate

Financing Residential Real Estate Chapter 1: Finance and Investment Borrowing Money to Buy a Home Investments and Returns Types of Investments Ownership Investments Debt Investments Securities Investment

Financing Residential Real Estate Chapter 1: Finance and Investment Borrowing Money to Buy a Home Investments and Returns Types of Investments Ownership Investments Debt Investments Securities Investment

DU REFI PLUS FIXED AND 5/1 LIBOR ARM - APP DATE ON OR AFTER 12-1-2011 REVISED 5/25/2012

DU REFI PLUS FIXED AND 5/1 LIBOR ARM - APP DATE ON OR AFTER 12-1-2011 REVISED 5/25/2012 DEFINITION OF DU REFI-PUS: Loan is serviced by an Outside Lender Existing Loan is owned by Fannie Mae All loans must

DU REFI PLUS FIXED AND 5/1 LIBOR ARM - APP DATE ON OR AFTER 12-1-2011 REVISED 5/25/2012 DEFINITION OF DU REFI-PUS: Loan is serviced by an Outside Lender Existing Loan is owned by Fannie Mae All loans must

Section 2.04 - DU Refi Plus Loan Program

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 5 Existing Mortgage Eligibility Requirements...

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 5 Existing Mortgage Eligibility Requirements...

MORTGAGE LOAN ORIGINATION SOLUTIONS

MORTGAGE SOLUTIONS Technology, workflow and business strategies to impact your bottom line RUN YOUR BUSINESS AT A LOWER COST Your LOS shouldn t just originate, process and fund loans. It should be treated

MORTGAGE SOLUTIONS Technology, workflow and business strategies to impact your bottom line RUN YOUR BUSINESS AT A LOWER COST Your LOS shouldn t just originate, process and fund loans. It should be treated

Standard Eligibility Matrix. DU Refi Plus Matrix. Refi Plus Matrix. Desktop Underwriter Version 9.3 (P. 2 3) (P. 4) (P.

(P. 4) (P.") PROGRAMS: Standard Eligibility Matrix Desktop Underwriter Version 9.3 (P. 2 3) DU Refi Plus Matrix (P. 4) Refi Plus Matrix (P. 5) COMMERCE HOME MORTGAGE WHOLESALE / 2030 MAIN STREET, SUITE 500 / IRVINE,

PROGRAMS: Standard Eligibility Matrix Desktop Underwriter Version 9.3 (P. 2 3) DU Refi Plus Matrix (P. 4) Refi Plus Matrix (P. 5) COMMERCE HOME MORTGAGE WHOLESALE / 2030 MAIN STREET, SUITE 500 / IRVINE,

19 FREQUENTLY ASKED QUESTIONS

19 FREQUENTLY ASKED QUESTIONS TERMS & CONDITIONS Q. What is the Total Debt To Income ratio allowed under the Program? A. The Total Debt To Income ratio cannot exceed 45.00%. There are no exceptions to

19 FREQUENTLY ASKED QUESTIONS TERMS & CONDITIONS Q. What is the Total Debt To Income ratio allowed under the Program? A. The Total Debt To Income ratio cannot exceed 45.00%. There are no exceptions to

Using the Broker s Credit Report for Underwriting Wholesale Version 12.23.2013

Using the Broker s Credit Report for Underwriting Wholesale Version 12.23.2013 Pacific Union Financial, LLC (PacUnion) will accept a Broker s credit report for underwriting purposes as long as the following

Using the Broker s Credit Report for Underwriting Wholesale Version 12.23.2013 Pacific Union Financial, LLC (PacUnion) will accept a Broker s credit report for underwriting purposes as long as the following

E MORTGAGE MANAGEMENT, LLC 703 VA HIGH BALANCE PRODUCT GUIDELINES

E MORTGAGE MANAGEMENT, LLC 703 VA HIGH BALANCE PRODUCT GUIDELINES 4/30/2014 Mortgage Eligibility Product Code Short Description Long Description Description VF30HB 30 YR VA HB VF30HB - 30 YR VA HIGH BALANCE

E MORTGAGE MANAGEMENT, LLC 703 VA HIGH BALANCE PRODUCT GUIDELINES 4/30/2014 Mortgage Eligibility Product Code Short Description Long Description Description VF30HB 30 YR VA HB VF30HB - 30 YR VA HIGH BALANCE

Submitting a loan to Freedom Mortgage through our Banking channel

Submitting a loan to Freedom Mortgage through our Banking channel Account Executive: Zaida Dykes at Freedom Mortgage (760) 500-9743 cell (866) 861-3500 office www.freedomwholesale.com FHA ID 7515901820

Submitting a loan to Freedom Mortgage through our Banking channel Account Executive: Zaida Dykes at Freedom Mortgage (760) 500-9743 cell (866) 861-3500 office www.freedomwholesale.com FHA ID 7515901820

ditech BUSINESS LENDING FREDDIE MAC ELIGIBLE FIXED RATE TEXAS HOME EQUITY PRODUCT

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage Servicing retained 10 to 30 years in 5 year increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans are permitted Qualified

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage Servicing retained 10 to 30 years in 5 year increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans are permitted Qualified

FMC Product and Credit Guidance for Wholesale Divisions

FMC Product and Credit Guidance for Divisions Ineligible Product Programs and Properties FMC does not accept Loan Prospector AUS for Conventional, FHA or VA loans The Negative Equity FHA (MHA) loan program

FMC Product and Credit Guidance for Divisions Ineligible Product Programs and Properties FMC does not accept Loan Prospector AUS for Conventional, FHA or VA loans The Negative Equity FHA (MHA) loan program

Announcement 08-34 December 16, 2008. Project Eligibility Review Service and Changes to Condominium and Cooperative Project Policies

Announcement 08-34 December 16, 2008 Amends these Guides: Selling Project Eligibility Review Service and Changes to Condominium and Cooperative Project Policies Introduction Announcement 07-18, Lender

Announcement 08-34 December 16, 2008 Amends these Guides: Selling Project Eligibility Review Service and Changes to Condominium and Cooperative Project Policies Introduction Announcement 07-18, Lender

FNMA 97% HFA Preferred

FNMA 97% HFA Preferred Underwriting, Processing & Loan Submission Overview Rev. 9.18.14 Welcome! This training presentation is specific to Conventional loans with LTVs from 95.01% to 97% only. For guidelines

FNMA 97% HFA Preferred Underwriting, Processing & Loan Submission Overview Rev. 9.18.14 Welcome! This training presentation is specific to Conventional loans with LTVs from 95.01% to 97% only. For guidelines

Conventional Loan Program Guide Fixed Rate, 5/1 ARM and 7/1 ARM

Fixed Rate, 5/1 ARM and 7/1 ARM Wholesale Lending December 14, 2015 Program Overview... 5 Credit Philosophy... 5 Ability to Repay and Qualified Mortgage... 5 Program Parameters... 6 Eligible Programs...

Fixed Rate, 5/1 ARM and 7/1 ARM Wholesale Lending December 14, 2015 Program Overview... 5 Credit Philosophy... 5 Ability to Repay and Qualified Mortgage... 5 Program Parameters... 6 Eligible Programs...

Page 1 of 9 Table of Contents

Page 1 of 9 Table of Contents LTV MATRIX... 2 PROGRAM SUMMARY... 3 LOAN AMOUNTS... 3 Conforming... 3 High Balance... 3 LOAN PROGRAM CODES... 3 LOAN TERMS... 3 ADJUSTMENT RATE DETAILS... 4 ELIGIBLE PROPERTY

Page 1 of 9 Table of Contents LTV MATRIX... 2 PROGRAM SUMMARY... 3 LOAN AMOUNTS... 3 Conforming... 3 High Balance... 3 LOAN PROGRAM CODES... 3 LOAN TERMS... 3 ADJUSTMENT RATE DETAILS... 4 ELIGIBLE PROPERTY

6/25/2013. Construction-To-Perm Lending Rules. Comparing Fannie to Freddie. Why? How It Works. MortgageCurrentcy.com. New Construction Niche

Construction-To-Perm Lending Rules Comparing Fannie to Freddie MortgageCurrentcy.com Why? New Construction Niche Do More Business with Builders Affiliation with Community Banks How It Works 6 Month Construction

Construction-To-Perm Lending Rules Comparing Fannie to Freddie MortgageCurrentcy.com Why? New Construction Niche Do More Business with Builders Affiliation with Community Banks How It Works 6 Month Construction

FHA Streamline (Full Credit and Non-Credit Qualifying)

") . This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

. This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

Announcement 09-19 June 08, 2009. Miscellaneous Underwriting, Eligibility, and Property-Related Updates

Announcement 09-19 June 08, 2009 Amends these Guides: Selling Miscellaneous Underwriting, Eligibility, and Property-Related Updates Introduction Fannie Mae conducted a comprehensive review of current underwriting

Announcement 09-19 June 08, 2009 Amends these Guides: Selling Miscellaneous Underwriting, Eligibility, and Property-Related Updates Introduction Fannie Mae conducted a comprehensive review of current underwriting

VHDA. Homeownership Program Guidelines for Realtors & Lenders. Updated 04/04

VHDA Homeownership Program Guidelines for Realtors & Lenders Updated 04/04 2 Benefits of a VHDA Loan: Creative financing programs Reduced interest rates Lower monthly payments More house for less money

VHDA Homeownership Program Guidelines for Realtors & Lenders Updated 04/04 2 Benefits of a VHDA Loan: Creative financing programs Reduced interest rates Lower monthly payments More house for less money

VA IRRRL GUIDELINES. Table of Contents

Page 1 of 8 Table of Contents LTV MATRIX... 3 PROGRAM SUMMARY... 3 LOAN AMOUNTS... 3 LOAN PROGRAM CODES... 3 LOAN TERMS... 3 ADJUSTMENT RATE DETAILS... 3 ELIGIBLE PROPERTY TYPES... 3 INELIGIBLE PROPERTY

Page 1 of 8 Table of Contents LTV MATRIX... 3 PROGRAM SUMMARY... 3 LOAN AMOUNTS... 3 LOAN PROGRAM CODES... 3 LOAN TERMS... 3 ADJUSTMENT RATE DETAILS... 3 ELIGIBLE PROPERTY TYPES... 3 INELIGIBLE PROPERTY

Announcement 08-16 June 25, 2008

Announcement 08-16 June 25, 2008 Amends these Guides: Selling Bankruptcy, Foreclosure, and Conversion of Principal Residence Policy Changes; and Revised Property Value Representation and Warranty Requirements

Announcement 08-16 June 25, 2008 Amends these Guides: Selling Bankruptcy, Foreclosure, and Conversion of Principal Residence Policy Changes; and Revised Property Value Representation and Warranty Requirements

HARP and Refi-to-Mod

Quick Start Guide HARP and Refi-to-Mod Supporting Fannie Mae s Home Affordable Refinance Programs, Freddie Mac s Relief Refi and Open Access Programs, and Non-GSE-Eligible Refi-to-Mod Table of Contents

Quick Start Guide HARP and Refi-to-Mod Supporting Fannie Mae s Home Affordable Refinance Programs, Freddie Mac s Relief Refi and Open Access Programs, and Non-GSE-Eligible Refi-to-Mod Table of Contents

Announcement 08-05 March 6, 2008. Temporary Increase to Our Conventional Loan Limits

Announcement 08-05 March 6, 2008 Amends these Guides: Selling Temporary Increase to Our Conventional Loan Limits Introduction The Economic Stimulus Act of 2008, signed into law on February 13, 2008, establishes

Announcement 08-05 March 6, 2008 Amends these Guides: Selling Temporary Increase to Our Conventional Loan Limits Introduction The Economic Stimulus Act of 2008, signed into law on February 13, 2008, establishes

V600 Introduction to Mortgage Lending. Robin J Wybenga, CFO, TBA Credit Union [email protected] 231.946.7090

V600 Introduction to Mortgage Lending Robin J Wybenga, CFO, TBA Credit Union [email protected] 231.946.7090 Introduction Objectives 1. Identify the key benefits your CU gains by offering real estate lending

V600 Introduction to Mortgage Lending Robin J Wybenga, CFO, TBA Credit Union [email protected] 231.946.7090 Introduction Objectives 1. Identify the key benefits your CU gains by offering real estate lending

- WHOLESALE - Summary of Procedures

- WHOLESALE - Summary of Procedures Welcome to Wintrust Mortgage Corporation s Wholesale Lending Program! We look forward to exceeding your expectations while serving your wholesale needs. To ensure you

- WHOLESALE - Summary of Procedures Welcome to Wintrust Mortgage Corporation s Wholesale Lending Program! We look forward to exceeding your expectations while serving your wholesale needs. To ensure you

Product Overview. Minimum Loan Amount $25,000. Maximum Loan Amount 1 Unit $417,000. Occupancy Owner occupied primary residence and second homes.

Product Overview The Federal Housing Finance Agency (FHFA) announced changes to the Home Affordable Refinance Program (HARP) in an effort to attract more eligible borrowers who can benefit from refinancing

Product Overview The Federal Housing Finance Agency (FHFA) announced changes to the Home Affordable Refinance Program (HARP) in an effort to attract more eligible borrowers who can benefit from refinancing

Updated: July 11, 2013

Common DU Errors Updated: July, 0 0 Rushmore Loan Management Services LLC. All rights reserved. Intended for use by Mortgage Professionals only. Additional criteria may apply. Common DU Errors Credit Provider

Common DU Errors Updated: July, 0 0 Rushmore Loan Management Services LLC. All rights reserved. Intended for use by Mortgage Professionals only. Additional criteria may apply. Common DU Errors Credit Provider

DU User s Guide for VA Loans

DU User s Guide for VA Loans 1999 2008 Fannie Mae. All rights reserved. Desktop Originator, DO, Desktop Underwriter, and DU, are registered trademarks of Fannie Mae. pmiaura is a service mark of PMI Mortgage

DU User s Guide for VA Loans 1999 2008 Fannie Mae. All rights reserved. Desktop Originator, DO, Desktop Underwriter, and DU, are registered trademarks of Fannie Mae. pmiaura is a service mark of PMI Mortgage

VA FIXED RATE PROGRAM HIGHLIGHTS

Program Summary Loan Term & Program Category Entitlement These guidelines represent underwriting requirements for VA fixed rate mortgages. Also review the VA Lender s Handbook for any guidelines not specifically

Program Summary Loan Term & Program Category Entitlement These guidelines represent underwriting requirements for VA fixed rate mortgages. Also review the VA Lender s Handbook for any guidelines not specifically

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Construction Conversion and Renovation Mortgages

Conversion and Renovation Mortgages Use this summary of requirements to help you process, underwrite and deliver Conversion and Renovation Mortgages. For complete information on Conversion and Renovation

Conversion and Renovation Mortgages Use this summary of requirements to help you process, underwrite and deliver Conversion and Renovation Mortgages. For complete information on Conversion and Renovation

FHA Home Loans 101 An Easy Reference Guide

FHA Home Loans 101 An Easy Reference Guide Updated for loans on or after June 3, 2013 Congratulations on Starting Your Journey to Home Ownership This guide offers a quick look at vital information you

FHA Home Loans 101 An Easy Reference Guide Updated for loans on or after June 3, 2013 Congratulations on Starting Your Journey to Home Ownership This guide offers a quick look at vital information you

Table of Contents How to Use the Closing Dis closure (CD)... 42 How to Compar e the Closing Dis closur e t o the L oan Estima

... 42 How to Compar e the Closing Dis closur e t o the L oan Estima") 1 Table of Contents Refinance Process Checklist... Refinance Process Timeline... Refinance to Lower Your Interest Rate... Refinance to Reduce Your Mortgage Term... Refinance to Convert Your Adjustable

1 Table of Contents Refinance Process Checklist... Refinance Process Timeline... Refinance to Lower Your Interest Rate... Refinance to Reduce Your Mortgage Term... Refinance to Convert Your Adjustable

Credit. 3.3-A General Requirements_. 3.3-B Credit Analysis. Section 3.3: Credit

Credit 3.3-A General Requirements_ Obtain at least one, preferably two or three, credit scores for each borrower; all available scores must be obtained. The scores must be obtained from all major repositories

Credit 3.3-A General Requirements_ Obtain at least one, preferably two or three, credit scores for each borrower; all available scores must be obtained. The scores must be obtained from all major repositories

VA Refinance Cash Out

VA Refinance Cash Out This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected

VA Refinance Cash Out This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected

ELIGIBILITY MATRIX. Table of Contents. Standard Eligibility Requirements - Desktop Underwriter Page 2

ELIGIBILITY MATRIX The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio requirements for conventional first mortgages eligible for delivery to Fannie Mae. The Eligibility Matrix

ELIGIBILITY MATRIX The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio requirements for conventional first mortgages eligible for delivery to Fannie Mae. The Eligibility Matrix

FHA Office of Single Family Housing. Training: Origination Through Post-Closing/ Endorsement

Training: Origination Through Post-Closing/ Endorsement 1 Module 8A Programs and Products: Refinance Single Family Housing Policy Handbook 4000.1 Title II Insured Housing Program Forward Mortgages Origination

Training: Origination Through Post-Closing/ Endorsement 1 Module 8A Programs and Products: Refinance Single Family Housing Policy Handbook 4000.1 Title II Insured Housing Program Forward Mortgages Origination

Freddie Mac Updates its Quality Control Requirements

Freddie Mac Updates its Quality Control Requirements by Anna DeSimone, President of Bankers Advisory, Inc.* Freddie Mac has updated Chapters 46 and 48 of the Seller/Servicer Guide regarding preand post-closing

Freddie Mac Updates its Quality Control Requirements by Anna DeSimone, President of Bankers Advisory, Inc.* Freddie Mac has updated Chapters 46 and 48 of the Seller/Servicer Guide regarding preand post-closing

The. Path. Refinancing. www.totalmortgage.com October. totalmortgage.com 877-868-2503

The Path Refinancing totalmortgage.com 877-868-2503 www.totalmortgage.com October 1 2012 The Path Refinancing Over time, many things change and need adjustment, and the reality is your home financing is

The Path Refinancing totalmortgage.com 877-868-2503 www.totalmortgage.com October 1 2012 The Path Refinancing Over time, many things change and need adjustment, and the reality is your home financing is

Max LTV/CLTV. Units. Max Debt Ratio Purchase or Refinance. 700 1 70% $1,500,000 40% Rate/Term Refinance Cash-Out N/A

Jumbo Series 3 Summary Product Types Minimum Loan Amount 5/1 and 7/1 ARMs $417,001 or Fannie/Freddie loan limits 5/1 ARM qualifies at the greater of the fully indexed rate or Note rate +2%. 7/1 ARM qualifies

Jumbo Series 3 Summary Product Types Minimum Loan Amount 5/1 and 7/1 ARMs $417,001 or Fannie/Freddie loan limits 5/1 ARM qualifies at the greater of the fully indexed rate or Note rate +2%. 7/1 ARM qualifies

FREDDIE MAC RELIEF REFI OPEN ACCESS INVESTOR 12, RETAIL ONLY

FREDDIE MAC RELIEF REFI OPEN ACCESS INVESTOR 12, RETAIL ONLY To determine if the mortgage is currently owned or securitized by Freddie Mac, the following website may be used: https://ww3.freddiemac.com/corporate/

FREDDIE MAC RELIEF REFI OPEN ACCESS INVESTOR 12, RETAIL ONLY To determine if the mortgage is currently owned or securitized by Freddie Mac, the following website may be used: https://ww3.freddiemac.com/corporate/

Information Access Training Support Crescent

Crescent Mortgage Company DU Refi Plus & LP Open Access Question and Answer Updated 4-16-2012 Fowler Williams, President Information Access Training Support Crescent I. Mortgage Insurance II. Appraisal

Crescent Mortgage Company DU Refi Plus & LP Open Access Question and Answer Updated 4-16-2012 Fowler Williams, President Information Access Training Support Crescent I. Mortgage Insurance II. Appraisal

Appraisal A written analysis prepared by a qualified appraiser and estimating the value of a property

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

Section C. Maximum Mortgage Amounts on Streamline Refinances Overview

Section C. Maximum Mortgage Amounts on Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 General Information on 3-C-2 2 Without an Appraisal

Section C. Maximum Mortgage Amounts on Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 General Information on 3-C-2 2 Without an Appraisal

HOMEBUYER S MORTGAGE GUIDE

WWW.WINTRUSTMORTGAGE.COM WINTRUST.COM/MYHOME HOMEBUYER S MORTGAGE GUIDE HELPFUL INFORMATION ABOUT THE MORTGAGE PROCESS TO GUIDE YOU AS YOU PURCHASE YOUR NEW HOME. www.wintrust.com/myhome WHY WINTRUST?

WWW.WINTRUSTMORTGAGE.COM WINTRUST.COM/MYHOME HOMEBUYER S MORTGAGE GUIDE HELPFUL INFORMATION ABOUT THE MORTGAGE PROCESS TO GUIDE YOU AS YOU PURCHASE YOUR NEW HOME. www.wintrust.com/myhome WHY WINTRUST?

Introduction to Renovation Lending. Presented by: Jane King Freedom Mortgage

Introduction to Renovation Lending Presented by: Jane King Freedom Mortgage Agenda Renovation Lending Overview of renovation products Identifying the right borrower Identifying the right property Evaluating

Introduction to Renovation Lending Presented by: Jane King Freedom Mortgage Agenda Renovation Lending Overview of renovation products Identifying the right borrower Identifying the right property Evaluating

Data Entry: You can create the 1003 loan application data in DO/DU in one of the following ways:

DO/DU Case #4: VA Mortgage Purpose: Get practice using Desktop Originator /Desktop Underwriter (DO /DU ) to evaluate a VA mortgage for borrowers purchasing a primary residence. By using the data provided

DO/DU Case #4: VA Mortgage Purpose: Get practice using Desktop Originator /Desktop Underwriter (DO /DU ) to evaluate a VA mortgage for borrowers purchasing a primary residence. By using the data provided

Announcement 09-29 September 22, 2009

Announcement 09-29 September 22, 2009 Amends these Guides: Selling Updates to Minimum Credit Scores, Mortgage Insurance, Pricing for Certain Desktop Underwriter Loans, Biweekly Loans, and Special Feature

Announcement 09-29 September 22, 2009 Amends these Guides: Selling Updates to Minimum Credit Scores, Mortgage Insurance, Pricing for Certain Desktop Underwriter Loans, Biweekly Loans, and Special Feature

`2 TERMS AND CONDITIONS

`2 TERMS AND CONDITIONS Each House Key Program Mortgage Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184, VA, USDA Rural Development, and Conventional

`2 TERMS AND CONDITIONS Each House Key Program Mortgage Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184, VA, USDA Rural Development, and Conventional

Variable Names & Descriptions

Variable Names & Descriptions Freddie Mac provides loan-level information at PC issuance and on a monthly basis for all newly issued fixed-rate and adjustable-rate mortgage (ARM) PC securities issued after

Variable Names & Descriptions Freddie Mac provides loan-level information at PC issuance and on a monthly basis for all newly issued fixed-rate and adjustable-rate mortgage (ARM) PC securities issued after

Announcement 08-11 May 16, 2008. Jumbo-Conforming Mortgage Loans Expanded Eligibility and Products

Announcement 08-11 May 16, 2008 Amends these Guides: Selling Jumbo-Conforming Mortgage Loans Expanded Eligibility and Products Introduction Announcement 08-05, Temporary Increase to Our Conventional Loan

Announcement 08-11 May 16, 2008 Amends these Guides: Selling Jumbo-Conforming Mortgage Loans Expanded Eligibility and Products Introduction Announcement 08-05, Temporary Increase to Our Conventional Loan