Table of Contents How to Use the Closing Dis closure (CD) How to Compar e the Closing Dis closur e t o the L oan Estima

|

|

|

- Osborn Potter

- 8 years ago

- Views:

Transcription

1 1

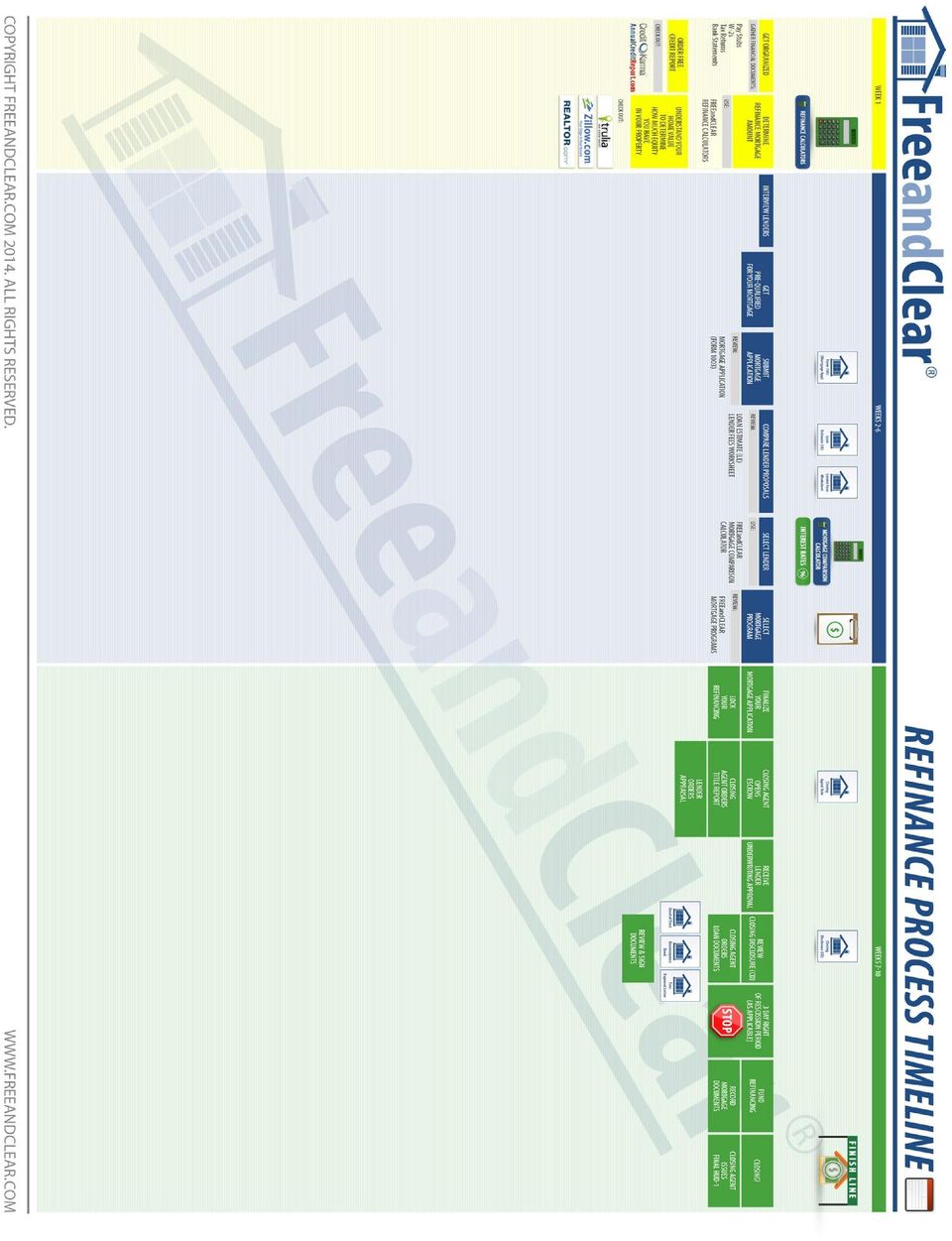

2 Table of Contents Refinance Process Checklist... Refinance Process Timeline... Refinance to Lower Your Interest Rate... Refinance to Reduce Your Mortgage Term... Refinance to Convert Your Adjustable Rate Mortgage (ARM) into a Fixed Rate Mortgage... Refinance to Consolidate High-Cost... Considering Total Interest Expense When Refinancing Your Mortgage to Consolidate High Cost Debt... Cash-Out Refinancing Overview... Comparing a Cash-Out Refinancing to a Separate Financing for a Major Purchase... Example: Comparing a Cash-Out Refinancing to a Separate Financing for a Major Purchase... Comparing Refinancing to a Home Equity Loan... Combining mortgage refinancing with the FREEandCLEAR Mortgage Acceleration Strategy... Refinance Lender Options... Mortgage Application (Form 1003) Overview... How to Use the Loan Estimate (LE) in a Refinance... How to Compare Refinancing Proposals and Pick the Right One for You... Get Pre-Approved for Your Refinancing... Understanding No Cost Refinancings... What mortgage program is right for me?... Mortgage Refinance Assistance Programs Summary... Should I Pay Discount Points to Lower My Interest Rate?... Should I Lock My Refinancing?... Settlement Agent Opens Escrow... Title Report and Title Insurance... Appraisal Report Overview

3 Table of Contents How to Use the Closing Disclosure (CD)... How to Compare the Closing Disclosure to the Loan Estimate... Review Mortgage Documents During the Right of Rescission Period... Record Documents and Fund Refinancing

4 Refinance Process Checklist You will likely have to provide extensive personal and financial documentation to refinance your mortgage This is so the lender can verify your income and assets and evaluate your creditworthiness The documents requested may vary somewhat by lender but will likely include the items listed on the right Having these documents available and organized at the beginning of the refinancing process will make things go much smoother Reviewing your personal finances in advance of the refinancing process will help you identify and resolve potential issues such as missing documents or errors you may find This will help you avoid potential delays and ensure that your refinancing is processed as quickly as possible The lender will also order your credit report as part of the refinancing application process You should review your credit score at the beginning of the refinancing process to make sure that there are no surprises when the lender does it 4

5 5

6 Refinance to Lower Your Interest Rate One of the most common reasons to refinance your mortgage is to lower your interest rate and monthly mortgage payment A frequent question that borrowers ask is how much lower than my current interest rate does the new interest rate have to be for it to make sense for me to refinance? A good rule of thumb to follow when refinancing is that the new interest rate should be a minimum of.75% lower than your existing interest rate So if your current interest rate is 5.0%, the new interest rate should be 4.25% or lower A reduction in interest rate of.75% or more allows you to reduce your monthly mortgage payment and typically recover your refinancing costs in 30 months or less The amount of time it takes you to recover your refinancing costs based on the amount of money you save on your new monthly mortgage payment is called the breakeven point When you refinance your mortgage you want the breakeven point to be 30 months or less The example below illustrates how refinancing your mortgage into a lower interest rate can save you money on your monthly mortgage payment For the example below we are holding the mortgage amount constant and assuming that the borrower pays closing costs but does not pay any discount points The example demonstrates that by refinancing the borrower is able to reduce his or her monthly mortgage payment by $170 and recover the cost of refinancing in twelve months You can also check out our FREEandCLEAR to learn whether it makes sense for you to refinance your mortgage 6

7 Refinance to Reduce Your Mortgage Term Another compelling reason to refinance is to reduce the term of your mortgage By reducing the term of your mortgage you can potentially save a significant amount of money over the life of your mortgage, even if the refinanced interest rate is not significantly lower than the original interest rate Although shorter term mortgages have lower interest rates than longer term mortgages reducing the term of your mortgage may not result in a significant reduction in your monthly mortgage payment because the mortgage balance is amortized over a shorter period of time By reducing the term of your mortgage, however, you can lower your interest rate and significantly reduce the number of monthly payments you make over the life of the mortgage, which will likely save you tens of thousands of dollars in interest expense If you can reduce your mortgage term and your interest rate by refinancing that is doubly good The example below illustrates the benefits of refinancing your mortgage to reduce the term of your mortgage. In this case, the mortgage term is reduced from 30 to 25 years We show a.50% reduction in interest rate, less than the.75% reduction in interest rate that typically justifies refinancing a mortgage We show the borrower refinancing the original mortgage after five years The refinanced mortgage has a lower mortgage amount than the original mortgage, reflecting the pay-down of principal in the first five years of the original mortgage In order to properly compare the original mortgage to the refinanced mortgage, we add the interest expense incurred during the first five years of the original mortgage to the interest expense incurred during the 25 year term of the refinanced mortgage. The combined total interest represents the true cost of borrowing the $380,000 mortgage amount We also assume that the borrower pays closing costs but does not pay any discount points The example demonstrates that by refinancing the borrower is able to save almost $30,000 in total interest expense over the life of the mortgage and reduce his or her monthly mortgage payment by almost $100 and recover the cost of refinancing in less than 20 months You can also check out our FREEandCLEAR to analyze how changing the term of your mortgage impacts your monthly mortgage payment and total interest expense over the life of a mortgage 7

8 Refinance to Convert Your Adjustable Rate Mortgage (ARM) into a Fixed Rate Mortgage One of the biggest risks of an adjustable rate mortgage (ARM) is that your monthly mortgage payment increases significantly if interest rates rise Refinancing an ARM into a fixed rate mortgage can protect a borrowers against potential future increases in his or her monthly mortgage payment and potentially save the borrower tens of thousands of dollars in interest expense over the life of the loan The example below demonstrates the benefits of converting an ARM mortgage into a fixed rate mortgage in an increasing interest rate environment In the example, the original mortgage is a 7/1 ARM that the borrower refinances at the end of year five The interest rate on the original mortgage is fixed for the first seven years and then is subject to adjust on an annual basis in years eight 8

9 Refinance to Convert Your Adjustable Rate Mortgage (ARM) into a Fixed Rate Mortgage (continued) For the purpose of this example, we show the fastest possible increase in the ARM s fully-indexed interest rate during the adjustable rate period until the interest rate reaches its life cap in year eight and remains at that level until the end of the mortgage At the end of year five, the borrower refinances the original 7/1 ARM into a 30 year fixed rate mortgage with an interest rate of 5.0% The principal amount of the mortgage does not change when the mortgage is refinanced We also assume that the borrower pays closing costs but does not pay any discount points The following chart compares monthly mortgage payment and total interest expense between the original 7/1 ARM and the refinanced 30 year fixed rate mortgage In years six and seven, the interest rate and monthly mortgage payment for the fixed rate mortgage are higher than the ARM s However, as interest rates increase when the ARM enters its adjustable rate period in year eight and beyond, the fixed rate mortgage offers the borrower lower monthly mortgage payments and lower total interest expense as compared to the ARM By refinancing into a fixed rate mortgage at the end of year five, the borrower gains certainty over his or her monthly mortgage payment, reduces his or her monthly mortgage payment by $425 per month in years 8 through 30 and saves a total of $76,224 in interest expense over the life of the mortgage While this example shows the worst case scenario for the 7/1 ARM, it also shows the significant benefits of refinancing an ARM into a fixed rate mortgage if you think interest rates are going to increase You can also check out our FREEandCLEAR to learn whether it makes sense for you to refinance your mortgage 9

10 Refinance to Convert Your Adjustable Rate Mortgage (ARM) into a Fixed Rate Mortgage (continued) The table below compares the original 7/1 ARM to a refinanced 30 year fixed rate mortgage put in place at the beginning of year six The table illustrates the savings in monthly mortgage payment beginning in year eight and total interest expense over the life of the mortgage realized by refinancing into a fixed rate mortgage 10

11 Refinance to Consolidate High-Cost If you have recurring debt with a high interest rate, such as credit card debt, it may make sense for you to refinance your mortgage and consolidate your high-cost debt into your mortgage By consolidating your high cost debt into your monthly mortgage payment, you may be able to lower your total monthly debt expense The example below demonstrates how refinancing enables you to use the equity in your house to eliminate expensive credit card debt and reduce your monthly debt expense In this example the borrower has a $380,000 fixed rate mortgage and $20,000 in credit card debt The mortgage has an interest rate of 5.0% and the credit card debt has an interest rate of 18% The borrower is five years into the mortgage and has a mortgage balance of approximately $348,950 The borrower refinances the mortgage at the original mortgage balance and uses the proceeds from the refinance of $31,050 (the difference between the amount of the refinanced mortgage and the current mortgage balance) to pay-off the high interest credit card debt and pay for the refinance costs. The borrower also keeps the $9,176 in proceeds leftover from the refinancing By refinancing the original mortgage and consolidating the high interest rate credit card debt, the borrower reduces his or her monthly debt expense by $322 You can also check out our FREEandCLEAR to determine whether it makes sense to do a debt consolidation refinancing 11

12 Considering Total Interest Expense When Refinancing Your Mortgage to Consolidate High Cost Debt It is important to consider total interest expense when you refinance your mortgage to consolidate high cost debt Unless you lower the interest rate of your mortgage when you refinance, you will pay more in total interest over the life of the refinanced mortgage, even if you lower your combined monthly mortgage and credit card payment by paying off your credit card debt By refinancing five years into the original mortgage, you are extending the mortgage term The original 30 year mortgage essentially becomes a 35 year mortgage when you refinance The longer the mortgage term, the greater the interest expense unless you are able to lower the interest rate In the example below we compare three cases: Not refinancing Refinancing at the same interest rate and paying off high-cost credit card debt Refinancing at a lower interest rate and paying off high-cost credit card debt For each case we examine the combined monthly mortgage and credit card payment and total interest expense over the life of the mortgage It is interesting to note that the refinance case where the interest rate is unchanged, the borrower reduces his or her combined monthly mortgage and credit card payment by $240 per month but pays $44,949 more in total interest over the life of the mortgage as compared to not refinancing even though the expensive credit card debt has been paid off by refinancing In the case where the borrower refinances at a lower interest rate, the borrower reduces his or her combined monthly mortgage and credit card payment by $465 per month and pays $36,051 less in total interest over the life of the mortgage as compared to not refinancing The borrower s primary goal may be to lower his or her total monthly debt expense, in which case both refinancing scenarios make sense If the borrower is focused on both total monthly debt expense and total interest expense over the life of the mortgage then he or she should only refinance if the interest rate can be lowered You can also check out our FREEandCLEAR to determine whether it makes sense to do a debt consolidation refinancing 12

13 Cash-Out Refinancing Overview Refinancing your mortgage may allow you to use the equity in your home to pay for a major expense such as college tuition In order to qualify for a cash-out refinancing you must have equity in your property, which means that the value of your property is greater than the amount of your current mortgage balance In a cash-out refinancing the amount of your refinanced mortgage is greater than the principal balance of your existing mortgage The borrower keeps the difference between the amount of the new mortgage and the principal balance of the existing mortgage and can use the money for a major expense In the example below we show a borrower that owns a property with a value of $400,000 who needs $50,000 to pay for college tuition The borrower originally took out a $300,000, 30 year fixed rate mortgage with a 5.0% interest rate to purchase the property The borrower is 10 years into the original mortgage and has a current mortgage balance of $244,000 The borrower has $156,000 in equity in the property $400,000 (property value ) - $244,000 (mortgage balance) = $156,000 in equity The borrower refinances the original mortgage with a 30 year fixed rate mortgage with an interest rate of 5.0%, so there is no change in interest rate The amount of the refinanced mortgage is $300,000, the same as the amount of the original mortgage By refinancing, the borrower is able to take out $56,000 in cash the difference between the amount of the new mortgage and the principal balance of the original mortgage to pay for college tuition and refinancing costs Because the interest rate and mortgage amount do not change, the borrower s monthly mortgage payment does not change Use the FREEandCLEAR to assess whether it makes sense to refinance your current mortgage to pay for a major purchase 13

14 Comparing a Cash-Out Refinancing to a Separate Financing for a Major Purchase In many situations it may not make sense to do a cash-out mortgage refinance to pay for a major purchase and instead it may make more sense to finance the purchase with a separate loan Depending on the interest rate and term that you are able to obtain for the separate financing, you may end up paying more in total interest when you do a cash-out refinancing This is because you are replacing short-term financing for the separate loan (for example, the length of a car loan is typically five-to-ten years) with long-term financing of a mortgage (the length of a mortgage is typically 15-to-30 years) The key factors that determine whether it makes sense to finance a major purchase separately or as part of a cash-out refinancing are the interest rates and terms of the mortgage and the separate financing plus the combined monthly payment of the financings Even in some cases where your mortgage interest rate is lower than the interest rate for the separate financing you may end up paying more in total interest expense over the life of the refinanced mortgage In evaluating whether it makes sense to do a cash-out refinancing to pay for a major purchase or to finance the purchase with a separate loan there may be a trade-off between having a lower monthly payment for a set number of years and paying more in total interest over the life of the mortgage In an ideal scenario a cash-out refinancing will allow you to reduce your mortgage interest rate or term, enabling you to lower your monthly mortgage payment, reduce your total interest expense over the life of the mortgage and take enough money out for a major purchase Otherwise, it may make more sense and save you money over the long term to keep your current mortgage in place and obtain separate financing for the major purchase 14

The key factors that determine whether it makes sense to finance a major purchase separately or as part of a")

15 Example: Comparing a Cash-Out Refinancing to a Separate Financing for a Major Purchase In many situations it may not make sense to do a cash-out mortgage refinance to pay for a major purchase such as college tuition or remodeling your home and instead it may make more sense to finance the purchase with a separate loan Depending on the interest rate and term that you are able to obtain for the separate financing, you may end up paying more in total interest when you do a cash-out refinancing This is because you are replacing short-term financing for the separate loan (for example, the length of a car loan is typically five-to-ten years) with long-term financing of a mortgage (the length of a mortgage is typically 15-to-30 years) In the first example, the borrower needs to decide if the lower monthly payment for the first ten years of the refinanced mortgage is more important than paying $117,600 more in total interest expense over the life of the mortgage as compared to not refinancing and obtaining a separate college tuition loan In the second example, it makes financial sense for the borrower to do a cash-out refinancing. Refinancing into a mortgage with a significantly lower interest rate enables the borrower to lower his or her monthly payment and reduce total interest expense over the life of the mortgage as compared to obtaining a separate college tuition loan You can also check out our FREEandCLEAR to assess whether it makes sense to refinance your current mortgage to pay for a major purchase 15

with long-term financing of a mortgage (the length of a mortgage is typically 15-to-30 years) In the first example, the borrower needs to decide")

16 Comparing Refinancing to a Home Equity Loan Borrowers looking to access the equity in their property to pay for a major typically decide between a cash-out refinancing or taking out a home equity loan or home equity line of credit The borrower may use the proceeds from a cash-out refinancing, home equity loan or home equity line of credit to pay for major expenses such as college tuition, home renovation, paying off credit card debt or buying a second home or investment property There are pros and cons to both financing options and the right answer depends on the borrower s financial situation and objectives Use our to determine whether it makes sense to refinance your current mortgage or obtain a home equity loan or line of credit to pay for a major purchase The interest rate and term for your existing mortgage and the length of time that you have been paying down your existing mortgage are all important factors in deciding what option is right for you The key factors that determine whether it makes sense to finance a major purchase with a cash-out refinancing or a home equity loan or line of credit are the length of time you have been paying down the existing mortgage as well as the interest rates and terms of the existing mortgage and home equity loan or line of credit In many situations it may not make sense to do a cash-out refinance to pay for a major purchase and instead it may make more sense to obtain a home equity loan or line of credit Unless you are able to reduce the interest rate and term of your existing mortgage it typically makes more sense financially for a borrower to select a home equity loan or line of credit than a cash-out refinancing This is because by refinancing your existing mortgage, unless you reduce the term of the new mortgage, you are basically starting over in paying back the original mortgage, which will cost you thousands of dollars more in interest expense For example, you are ten years into a $200, year mortgage and you refinance your mortgage with a new $200, year mortgage you have essentially converted your original 30 year mortgage into a 40 year mortgage, which means you pay thousands more in interest expense over the life of the loan The longer the mortgage the more interest expense you pay The example below demonstrates how a home equity loan can save you hundreds of thousands of dollars in total interest expense as compared to a cash-out refinancing In this example the borrower is ten years into the original $300,000 mortgage and wants $50,000 for a major purchase The two scenarios below compare obtaining a separate 15 year $50,000 home equity loan and not refinancing the original mortgage (Scenario 1) to a cash-out refinancing (Scenario 2) In this example, the borrower does not reduce his or her mortgage term or interest rate by refinancing and replaces the original 30 year $300,000 mortgage with a new 30 year $300,000 mortgage and takes $50,000 in cash out by refinancing As demonstrated by this example, because the borrower does not reduce his or her mortgage term or interest rate by refinancing, a cash-out refinancing costs the borrower thousands more in total interest expense over the terms of both the original and new mortgages When you add the interest expense from the first ten years of the original mortgage to the new refinanced mortgage, the borrower spends $111,250 more in total interest expense as compared to keeping the original mortgage and taking out a home equity loan This is because the borrower effectively extended the term of the original mortgage by 10 years (so the borrower makes 10 extra years of mortgage payments in Scenario 2) 16

17 Comparing Refinancing to a Home Equity Loan (continued) If you are also able to reduce both your interest rate and term when you refinance, a cash-out refinancing can save you money in total interest expense in the long run The second example below demonstrates how a cash-out refinancing can save you thousands of dollars in total interest expense as compared to keeping your original mortgage and obtaining a home equity loan if you are able to reduce your interest rate and term when you refinance In this example the borrower is ten years into the original $300,000 mortgage and wants $50,000 for a major purchase The two scenarios below compare obtaining a separate 15 year $50,000 home equity loan and not refinancing the original mortgage (Scenario 2) to a cash-out refinancing (Scenario 2) In this example, the borrower replaces the original 30 year $300,000 mortgage with a 5.00% interest rate with a new 20 year $300,000 mortgage with a 4.00% interest rate and takes $50,000 in cash out by refinancing As demonstrated by this example, because the borrower reduces his or her mortgage term and interest rate by refinancing, a cash-out refinancing saves the borrower thousands in total interest expense When you add the interest expense from the first ten years of the original mortgage to the new refinanced mortgage, the borrower saves $32,050 in total interest expense as compared to keeping the original mortgage and taking out a home equity loan Because the mortgage term was reduced from 30 years to 20 years, the borrower s monthly mortgage payment increases from $1,610 with the original mortgage to $1,818 with the new refinanced mortgage even though the mortgage amount stayed the same and the interest rate decreased The shorter the mortgage term, the higher the monthly mortgage payment but the lower the total interest expense over the life of the mortgage The new monthly mortgage payment of $1,818 is less than the $2,032 combined monthly payment of the original mortgage ($1,610) and the home equity loan ($422) 17

to a cash-out refinancing (Scenario")

18 Comparing Refinancing to a Home Equity Loan (continued) As these examples demonstrate, in comparing a refinancing to keeping your original mortgage and obtaining a home equity loan or line of credit there may be a trade-off between having a higher monthly payment for a set number of years (10 to 15 years for a home equity loan) and paying less in total interest over the life of the mortgage In an ideal scenario a refinancing will allow you to reduce your mortgage interest rate and term, enabling you to lower your monthly mortgage payment, reduce your total interest expense over the life of the mortgage and take out enough money for a major purchase Otherwise, if you can afford the higher monthly payment for a set number of years it typically makes more sense and saves you money in total interest expense over the long term to keep your current mortgage in place and obtain a home equity loan or line of credit Always remember to consider total interest expense when evaluating if you should refinance your existing mortgage or obtain a home equity loan or line of credit 18

19 Combining mortgage refinancing with the FREEandCLEAR Mortgage Acceleration Strategy If you are able to lower your interest rate and monthly mortgage payment by refinancing your mortgage you can apply the FREEandCLEAR mortgage acceleration strategy to save thousands of dollars in interest expense over the life of the mortgage The simplest way to apply the FREEandCLEAR Mortgage Acceleration Strategy in combination with a refinancing is to continue to make the same monthly mortgage payment that you were making prior to refinancing By paying more than the required monthly mortgage payment you accelerate the date when your mortgage is paid in full Accelerating your mortgage can reduce the term of your mortgage by a number of years and save you thousands of dollars in mortgage payments The example below compares the monthly mortgage payment, mortgage term and total interest expense between refinancing a mortgage and combining refinancing a mortgage with the FREEandCLEAR Mortgage Acceleration Strategy In the example, the borrower is five years into a $300,000, 30 year fixed rate mortgage with and interest rate of 5.0% and refinances into a new 30 year fixed rate mortgage with an interest rate of 4.0% In the refinance-only scenario, the borrower saves $178 on his or her monthly mortgage payment but pays $8,000 more in total interest expense over the term of the mortgage In the second scenario, the borrower combines the refinancing with the FREEandCLEAR Mortgage Acceleration Strategy and continues to make the same mortgage payment he or she made prior to refinancing as compared to the original mortgage The borrower s monthly mortgage payment does not change but paying more than the required monthly mortgage payment reduces the term of the mortgage by 69 months and saves the borrower $47,000 in interest expense over the life of the mortgage as compared to refinancing and not applying the FREEandCLEAR Mortgage Acceleration Strategy You can also check out our FREEandCLEAR and FREEandCLEAR to understand the benefits of refinancing as well as the FREEandCLEAR Mortgage Acceleration Strategy 19

20 Refinance Lender Options It is important to realize that even though you have an existing mortgage and lender you have options when refinance. You can use these options to create competition for your refinancing and make sure you are getting the best terms for your new mortgage There are several types of mortgage lenders including banks, mortgage brokers, mortgage bankers, credit unions and private investors and there are pros and cons to working with each type of lender. The table at the bottom of the page outlines your mortgage lender options and their positive and negatives Some mortgage lenders such as banks, mortgage bankers and credit unions are direct lender, which means they lend you money directly for your mortgage, potentially allowing them to offer you a lower interest rate Other lenders such as mortgage brokers do not fund mortgages directly but instead act as a personal mortgage shopper for borrowers and compare rates and fees from multiple funding lenders to find you the best terms for your mortgage, so you benefit from lender competition Private investors typically charge the highest interest rate and are used by borrowers who have poor credit or who are unable to qualify for a mortgage with other types of lenders Treat the refinancing process like you would any other major purchase, such as buying a car -- shop around, compare proposals from multiple lenders and negotiate the best terms for your refinancing In addition to speaking with your current lender, we highly recommend that you speak to several lenders when shopping for your refinancing including one lender from each category There is almost never any unique advantage to refinancing with your current lender select the lender that offers you the lowest interest rate with the lowest transaction costs Gathering and comparing mortgage proposals from several lenders will help ensure that you receive the best terms for your refinancing The table shows interest rates and fees for a selection of lenders in your area. You can also click to see a full list of lenders Use the to compare refinancing proposals and select the one that is right for you 20

21 Mortgage Application (Form 1003) Overview Just like when you obtain a mortgage to purchase a property, lenders require that borrowers submit a loan application when applying to refinance their mortgage Most lenders use a standard online or paper mortgage application but according to mortgage laws, if borrowers submit the following information they satisfy the legal definition of a mortgage application Name Income Social Security Number Property Address Estimated Property Value Estimated Mortgage Amount Be it for a mortgage to purchase a property or a refinancing almost all lenders use the same standard loan application form referred to as a Form 1003 We have provided an example loan application so you can understand the information required when you submit a loan application The loan application contains a lot of questions about a borrower s income, assets, debt and employment history Check out the FREEandCLEAR mortgage refinance checklist that lists the personal and financial documents you will likely have to provide to the lender when applying to refinance your mortgage. You will also use information from these documents to fill-out the loan application FREEandCLEAR recommends that you gather, organize and review these documents at the beginning of the refinance process The good news is that almost all lenders provide an online loan application which streamlines the process and allows you to submit the application from the comfort of your own home In most cases a loan application is required to receive refinancing proposals from lenders including the documents (Loan Estimate (LE) and Lender Fees Worksheet) that you can use to compare lenders and select your mortgage Lenders cannot charge borrowers a fee for submitting a mortgage application or for providing a Loan Estimate (LE). The lender must provide the borrower an LE that outlines a good faith estimate of key mortgage terms and costs within three business days of the borrower submitting a mortgage application. The only fee a lender can charge the borrower before providing the LE is a small credit report fee ($10 - $30) Lenders are not permitted to require the borrower to provide documents that verify the information on the borrower s mortgage application before proving the LE If a lender attempts to charge you to take a mortgage application or provide an LE, immediately stop working with that lender and report the lender to the Consumer Finance Protection Bureau (CFPB) You can and should submit mortgage applications to multiple lenders so that you can review and compare multiple refinancing proposals to find the mortgage that is right for you It is important to highlight that just because you submit a mortgage application to a lender and receive an LE does not obligate you to work with that lender on your refinancing Comparing mortgage proposals from multiple lenders is one of the best ways to ensure that you receive the best terms for your refinancing and FREEandCLEAR recommends this approach even it requires additional effort by the borrower Click to review interest rates for lenders in your area and contact them to apply for your refinancing 21

22 Mortgage Application (Form 1003) Overview (continued) Finalizing Your Mortgage Application After you finalize your lender selection you should move as quickly as possible to complete your refinancing At this point in the process, the lender that you have selected for your refinancing will likely ask you for numerous personal and financial documents to finalize your mortgage application In addition to requesting personal and financial documents, the lender will also order your credit report to include with your mortgage application FREEandCLEAR recommends that you review your credit score at the beginning of the refinance process to identify and address any potential issues before the lender reviews it The lender will add your financial documents and credit report to finalize your mortgage application 22

23 How to Use the Loan Estimate (LE) in a Refinance According to the TILA-RESPA Integrated Disclosure Rule (TRID), the lender must provide the borrower a Loan Estimate, also known as an LE, that outlines a good faith estimate of the key terms of the mortgage including interest rate, closing costs and mortgage features within three business days of the borrower submitting a loan application to the lender In a refinancing, the LE also indicates the cash-out the borrower receives or cash required from the borrower when the mortgage closes, including the pay-off of your existing mortgage or other debts How Borrowers Can Use the Loan Estimate The LE is a powerful tool that borrowers can use to review and compare refinance proposals from multiple lenders and decide if they want to move forward with the mortgage process The LE is a standard document that will be the same across all lenders. The figures may change as proposals vary across lenders, but the form itself will remain the same this allows you to more easily compare proposals from various lenders You can and should submit mortgage applications to multiple lenders so that you can review and compare multiple LEs to find the mortgage that is right for you Submitting a mortgage application and receiving an LE from a lender does not obligate you to work with that lender If a lender is unwilling to provide an LE this raises a significant red flag and you should consider working with other lenders When you compare LEs, you should focus on three key items that impact your up-front and long term mortgage costs: Interest Rate. This is the fee the lender charges you to borrow money until the loan is paid in full. The interest rate is on the top of page 1 of the LE. The lower the interest rate, the better. In some cases a lender will charge you a lower interest rate but higher closing costs so there may be a trade-off you have to consider. Additionally, different types of mortgages and mortgages with different lengths have different interest rates so make sure you are comparing mortgages with the same terms Closing Costs. Closing costs are the fees charged by the lender and numerous third parties to process and close your mortgage. The estimated closing costs figure is on the bottom of page 1 of the LE. In general, the lower the closing costs, the better but in some cases the lender may charge or the borrower may elect to pay higher closing costs to receive a lower interest rate Annual Percentage Rate (APR). In short, the APR represents what your interest rate would be if it included all up-front lender and closing costs so it is a way to use one figure to compare both the interest rate and closing costs for a mortgage. For example, if you have proposals from two lenders that are offering the same interest rate but one APR is higher than the other, then you know the lender with the higher APR is charging closing costs. The APR is on the top of page 3 of the LE You can use our to compare mortgage proposals from numerous lenders to find the mortgage with the lowest combination of interest rate and closing costs Although it is not required by law, you should also ask lenders for a Lender Fees Worksheet, which provides an additional breakdown of all the costs and expenses associated with a mortgage that you can use to compare lenders Select lenders from the table below or click to review lenders in your area and contact them about applying for your refinancing and receiving an LE. FREEandCLEAR recommends comparing LEs from three-to-four lenders to find the mortgage with the lowest rate and fees Prior to your mortgage closing, you can compare your LE with the Closing Disclosure (CD) document to ensure that your final, actual interest rate and closing costs did not increase significantly as compared to the initial estimate provided by the lender in the LE The CD is a document that the lender must provide to borrowers three days prior to the mortgage closing that details the final terms of your mortgage Significant differences between the LE and CD (e.g., an increase in interest rate or higher borrower costs), may be a sign that you are not getting the mortgage you thought you were. We go into this in more detail when we review the Closing Disclosure document 23

24 How to Use the Loan Estimate (LE) in a Refinance (continued) What Borrowers Should Know About the Loan Estimate The LE must be delivered by the lender to the borrower in-person or by or mail within three business days of the borrower submitting a mortgage application to the lender If the LE is provided by mail, it may take longer than three days for the borrower to actually receive it. For example, the lender may put the LE in the mail three days after the borrower submits a mortgage application and it may take an additional two-to-three days for the borrower to receive the document Lenders are not permitted to require the borrower to provide documents that verify the information on the borrower s mortgage application before proving the LE Lenders cannot charge borrowers a fee for submitting a mortgage application or for receiving an LE The only fee a lender can charge the borrower before providing the LE is a small credit report fee ($10 - $30) If a lender attempts to charge you to take a mortgage application or provide a LE, immediately stop working with that lender and report the lender to the Consumer Finance Protection Bureau (CFPB) The LE must be provided to the borrower in writing -- a verbal LE is not permitted If the lender provides the borrower a written estimate of the mortgage terms other than the LE, the estimate must include disclosure at the top of the estimate that indicates that the mortgage terms are subject to change If you are working with a mortgage broker either the mortgage broker or the funding lender may provide the LE but the funding lender is legally responsible for the LE document Lenders generally may not issue a revised LE because they made technical errors or underestimated fees. For example, if a lender makes a mistake on an LE, such as omitting a fee, the lender is responsible for the error and the borrower is not required to pay that fee Lenders can only issue a revised LE when they receive new or updated information about the borrower or mortgage that causes the interest rate or fees to increase Circumstances that may cause the terms of the mortgage to change include a revised credit report, receipt of the appraisal report, the borrower deciding to change the down payment or the borrower deciding to lock the interest rate during the course of the mortgage process A revised LE must be issued no later than three business days after the lender receives the updated information and no later than seven business days before the close of the mortgage FREEandCLEAR provides an example LE document as well as a detailed breakdown and explanation of the items on the LE 24

25 How to Compare Refinancing Proposals and Pick the Right One for You You should treat the refinancing process like you would any other major purchase, such as buying a car -- shop around, compare refinancing proposals from multiple lenders and select the best proposal. Follow the steps below to negotiate the best terms for your refinancing: Gather refinancing proposals from at least four lenders, including one mortgage broker There are different types of lenders such as banks, mortgage brokers, mortgage bankers and credit unions and they are ALL competing for your refinancing business Some mortgage lenders such as banks, mortgage bankers and credit unions are direct lenders, which means they lend you money directly for your mortgage, potentially allowing them to offer you a lower interest rate Other lenders such as mortgage brokers do not fund mortgages directly but instead act as a personal mortgage shopper for borrowers and compare rates and fees from multiple funding lenders to find you the best terms for your refinancing, so you benefit from lender competition Gathering proposals from at least four lenders will ensure that you have a range of options, which puts you in a stronger position when you negotiate your refinancing Request a Loan Estimate (LE) and Lender Fees Worksheet from the lenders you contact According to federal law, the lender must provide the borrower a Loan Estimate (LE), that outlines a good faith estimate of the key terms of the mortgage including interest rate, Annual Percentage Rate (APR), closing costs and mortgage features within three business days of the borrower submitting a loan application. If a lender refuses to provide an LE, this is a red flag and you should contact other lenders. The LE is a standard document that will be the same across all lenders this allows you to more easily compare refinance proposals from various lenders The Lender Fees Worksheet provides a detailed breakdown of all the costs and expenses associated with a mortgage refinancing including fees charged by lenders and other third parties. By law, the lender is not required to provide you with the worksheet, but will likely provide it to you if you ask Borrowers should use the information on interest rates and refinancing costs presented in these documents to compare refinancing proposals Please note that a lender cannot charge you to submit a mortgage application or to provide the LE and Lender Fees Worksheet Compare refinancing proposals When comparing mortgage proposals, we recommend that you focus on two key items that have the most impact on your up-front and long-term mortgage costs: 1) interest rate, and 2) closing costs. You can use the Loan Estimate (LE) and Lender Fees Worksheet to help with the comparison You can find the interest rate at the top of page one of the LE and the estimated closing costs at the bottom of page one. Page two of the LE provides a detailed, item-by-item breakdown of the all the mortgage closing cost items you are required to pay You should also use the Annual Percentage Rate (APR) on the top of page three of the LE to quickly compare and identify excessive closing costs. In short, the APR represents what your interest rate would be if it included all up-front lender and closing costs so it is a way to use one figure to compare both the interest rate and closing costs for a mortgage. If the APR is much higher than your interest rate then you know that the closing costs are relatively high and you may want to negotiate lower costs or change lenders. Additionally, if you have proposals from two lenders that are offering the same interest rate but one APR is higher than the other, then you know the lender with the higher APR is charging higher fees We outline these three items in the table below and tell you where to find them on the LE. Click on the LE rectangles under the cost items to see where each figure is located on the LE You can also use the Lender Fees Worksheet to perform a more detailed review of mortgage closing costs and negotiate specific cost items to reduce your overall mortgage costs When you compare refinancing proposals keep in mind that interest rates and closing costs vary by mortgage program. For example, a fixed rate mortgage typically has a higher interest rate than an adjustable rate mortgage. In some cases borrowers review different types and lengths of mortgages as part of their selection process so be sure you are comparing similar mortgage programs when selecting your lender 25

26 How to Compare Refinancing Proposals and Pick the Right One for You (continued) Negotiate the best terms Some lenders may offer a lower interest rate with higher fees while other lenders may offer a higher interest rate with lower fees Use this information to your advantage to negotiate the lowest interest rate and fees for your refinancing by seeing if a lender is willing to match the interest rate or fees offered by another lender Additionally, you can use the Lender Fees Worksheet to perform a more detailed review and comparison of refinancing closing costs. For example, one lender may charge an appraisal fee of $600 while another lender may only charge $500. Use information from the Lender Fees Worksheet to negotiate specific cost items and reduce your overall refinancing closing costs It takes extra time to compare and negotiate lender proposals but spending an extra hour or two can save you thousands of dollars over the life of your mortgage. For example, on a $300, year fixed rate mortgage, reducing your interest rate by just.125% will save you almost $8,000 in interest expense over the life of your mortgage Our enables you to take the information provided by lenders and input the interest rate and costs for multiple mortgages to compare them and select the refinancing that is right for you 26

27 Get Pre-Approved for Your Refinancing It is important to seek lender pre-approval at the beginning of the refinance process to ensure that you qualify for the refinancing Getting pre-approved can help you determine if refinanicng your existing mortgage is possible so that you can avoid wasting time and money on up-front transaction costs that may be non-refundable Understanding your lender options, asking the right questions and getting pre-approved for your refinancing at the beginning of the process will enable you to address potential issues up-front and eliminate unpleasant and expensive surprises The pre-approval process focuses the loan-to-value (LTV) ratio of the refinanced mortgage LTV represents the amount of your mortgage divided by the value of the property that you are refinancing For example, if you want to refinance a $400,000 mortgage on a property valued at $500,000, the loan-to-value ratio is 80% ($400,000 mortgage $500,000 property value =.80 = 80%) It is important to understand if the value of your property has changed since you obtained your existing mortgage as this will impact the LTV ratio and potentially your ability to qualify for the refinancing You can check out real estate web sites like Realtor, Trulia and Zillow to get an initial estimate of your poroperty s value Lenders may also have resources they can use to provide an initial estimate of the value of your property This will help determine if you have enough equity in your property to refinance your mortgage Lenders will typically offer their best interest rates on mortgages with an LTV of 80% or less If the value of your property has declined, your LTV ratio may go up (and potentially be greater than 80%) depending on the mortgage amount you are seeking The pre-approval process also focuses on borrower mortgage qualification, what size mortgage the borrower can afford and the borrower s ability to make the monthly mortgage payment and pay back the mortgage Getting pre-approved typically requires a borrower to provide certain personal and financial information to a lender Lenders typically require that borrowers submit pay stubs, bank statements and other personal financial documents to verify your income and assets The lender will also review your credit score Your personal employment or financial situation may have changed since you obtained your original mortgage which could impact your ability to refinance your loan Although somewhat unusual, some lenders may require that borrowers submit a full loan application to get pre-approved Mortgage pre-approval is typically subject to the borrower finalizing his or her mortgage application as well as lender review of the property appraisal, title report or abstract and other documentation required to close your mortgage Additionally, your mortgage pre-approval may also be based on a speciifc interest rate or mortgage program so if interest rates increase or you select a different mortgage program, it may affect your ability to receive final approval for the pre-approved mortgage amount It is important to highlight that getting pre-approved for your refinancing is different than getting pre-qualified Pre-qualification is a preliminary assessment of what size mortgage you qualify for and typically does not require borrowers to submit documents to verify their income and assets. Additionally, lenders typically do not pull your credit score to pre-qualify you Because the pre-approval process requires you to provide more information than getting pre-qualified, being pre-approved is much more valuable and beneficial to the borrower Finally, just because you are pre-qualified by a lender or submit a mortgage application to a lender does not obligate you to work with that lender to finalize your refinancing Even if you have been pre-qualified by a lender, FREEandCLEAR recommends that you compare refinancing proposals from multiple lenders to find the mortgage that is right for you Click to review lenders in your area and get pre-qualified 27

Table of Contents Reverse Mortgage O verview... Reverse Mortgage K ey Questions... 5 Reverse Mortgage Pros and Cons... 7 Reverse Mortgage Borr

1 Table of Contents Reverse Mortgage Overview... Reverse Mortgage Key Questions... Reverse Mortgage Pros and Cons... Reverse Mortgage Borrower Qualification... Reverse Mortgage Key Items... Reverse Mortgage

1 Table of Contents Reverse Mortgage Overview... Reverse Mortgage Key Questions... Reverse Mortgage Pros and Cons... Reverse Mortgage Borrower Qualification... Reverse Mortgage Key Items... Reverse Mortgage

HOME BUYING101. 701.255.0042 www.capcu.org i

HOME BUYING101 701.255.0042 www.capcu.org i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended,

HOME BUYING101 701.255.0042 www.capcu.org i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended,

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Guide to Purchasing a Home

Your journey to homeownership starts at your credit union. Purchasing your first home is a big decision, and it may even seem overwhelming. Rest assured Beacon Credit Union is here to assist you in understanding

Your journey to homeownership starts at your credit union. Purchasing your first home is a big decision, and it may even seem overwhelming. Rest assured Beacon Credit Union is here to assist you in understanding

A Consumer s Guide to Refinancing

A Consumer s Guide to Refinancing Have interest rates fallen? Or do you expect them to go up? Has your credit score improved enough so that you might be eligible for a lower-rate mortgage? Would you like

A Consumer s Guide to Refinancing Have interest rates fallen? Or do you expect them to go up? Has your credit score improved enough so that you might be eligible for a lower-rate mortgage? Would you like

How To Prequalify A Mortgage Loan

Automated Underwriting and Pre-Qualification Qualifying and Closing Borrowers Using a Functional Script Contents Introduction - Automated Underwriting and Pre-Qualification...2 Loan Officers Have Stopped

Automated Underwriting and Pre-Qualification Qualifying and Closing Borrowers Using a Functional Script Contents Introduction - Automated Underwriting and Pre-Qualification...2 Loan Officers Have Stopped

WELCOME COURSE OUTLINE

WELCOME COURSE OUTLINE Dear Home Buyer: Thank you for giving us the opportunity to help guide you through your home lending process. It is typically the largest financial transaction you will make and

WELCOME COURSE OUTLINE Dear Home Buyer: Thank you for giving us the opportunity to help guide you through your home lending process. It is typically the largest financial transaction you will make and

HOME FINANCING GUIDE

HOME FINANCING GUIDE SECTION 1: Mortgage Loans Available Fixed Rate Mortgages A fixed rate mortgage is a home loan with a rate that remains the same over the entire term of the loan, regardless of how

HOME FINANCING GUIDE SECTION 1: Mortgage Loans Available Fixed Rate Mortgages A fixed rate mortgage is a home loan with a rate that remains the same over the entire term of the loan, regardless of how

HOMEOWNERSHIP: Understanding What You Can Afford, Mortgages, and Closing Costs. Illinois Association of REALTORS. Springfield, IL 62701

Illinois Association of REALTORS 522 S. Fifth Street Springfield, IL 62701 www.illinoisrealtor.org www.yourillinoishome.com HOMEOWNERSHIP: Understanding What You Can Afford, Mortgages, and Closing Costs

Illinois Association of REALTORS 522 S. Fifth Street Springfield, IL 62701 www.illinoisrealtor.org www.yourillinoishome.com HOMEOWNERSHIP: Understanding What You Can Afford, Mortgages, and Closing Costs

The. Path. Refinancing. www.totalmortgage.com October. totalmortgage.com 877-868-2503

The Path Refinancing totalmortgage.com 877-868-2503 www.totalmortgage.com October 1 2012 The Path Refinancing Over time, many things change and need adjustment, and the reality is your home financing is

The Path Refinancing totalmortgage.com 877-868-2503 www.totalmortgage.com October 1 2012 The Path Refinancing Over time, many things change and need adjustment, and the reality is your home financing is

Is now a good time to refinance?

Is now a good time to refinance? Our Business Is The American Dream At Fannie Mae, we are in the American Dream business. Our Mission is to tear down barriers, lower costs, and increase the opportunities

Is now a good time to refinance? Our Business Is The American Dream At Fannie Mae, we are in the American Dream business. Our Mission is to tear down barriers, lower costs, and increase the opportunities

How To Get A Home Equity Line Of Credit

A GUIDE TO HOME EQUITY LINES OF CREDIT Call or visit one of our offices today to see what products in this guide we have to offer you! TABLE OF CONTENTS Introduction What is a home equity line of credit

A GUIDE TO HOME EQUITY LINES OF CREDIT Call or visit one of our offices today to see what products in this guide we have to offer you! TABLE OF CONTENTS Introduction What is a home equity line of credit

Borrow Wisely with these Keys: Local servicing Pre-approvals Competitive interest rates Personal service Tailored loan programs*

Your Home Financing Process Checklist As you prepare to purchase a home or refinance your loan, it s important to know what to expect along the way. Here, we ve outlined some of the general steps in the

Your Home Financing Process Checklist As you prepare to purchase a home or refinance your loan, it s important to know what to expect along the way. Here, we ve outlined some of the general steps in the

HOME BUYING101 TM %*'9 [[[ EPXEREJGY SVK i

HOME BUYING101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

HOME BUYING101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

HOMEBUYER S MORTGAGE GUIDE

WWW.WINTRUSTMORTGAGE.COM WINTRUST.COM/MYHOME HOMEBUYER S MORTGAGE GUIDE HELPFUL INFORMATION ABOUT THE MORTGAGE PROCESS TO GUIDE YOU AS YOU PURCHASE YOUR NEW HOME. www.wintrust.com/myhome WHY WINTRUST?

WWW.WINTRUSTMORTGAGE.COM WINTRUST.COM/MYHOME HOMEBUYER S MORTGAGE GUIDE HELPFUL INFORMATION ABOUT THE MORTGAGE PROCESS TO GUIDE YOU AS YOU PURCHASE YOUR NEW HOME. www.wintrust.com/myhome WHY WINTRUST?

FHA Home Loans 101 An Easy Reference Guide

FHA Home Loans 101 An Easy Reference Guide Updated for loans on or after January 26, 2015 Congratulations on Starting Your Journey to Home Ownership This guide offers a quick look at vital information

FHA Home Loans 101 An Easy Reference Guide Updated for loans on or after January 26, 2015 Congratulations on Starting Your Journey to Home Ownership This guide offers a quick look at vital information

THANK YOU FOR CHOOSING CAPITAL ONE BANK

KNOW ALL THE STEPS THANK YOU FOR CHOOSING CAPITAL ONE BANK WE RE HAPPY THAT YOU VE COME TO US FOR YOUR HOME LOAN NEEDS, AND WE LOOK FORWARD TO MAKING THE APPLICATION PROCESS AS CLEAR AS POSSIBLE. THIS

KNOW ALL THE STEPS THANK YOU FOR CHOOSING CAPITAL ONE BANK WE RE HAPPY THAT YOU VE COME TO US FOR YOUR HOME LOAN NEEDS, AND WE LOOK FORWARD TO MAKING THE APPLICATION PROCESS AS CLEAR AS POSSIBLE. THIS

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES This booklet was originally prepared by the Federal Reserve Board and the Office of Thrift Supervision in consultation with the following organizations: American

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES This booklet was originally prepared by the Federal Reserve Board and the Office of Thrift Supervision in consultation with the following organizations: American

TRID Survival Guide: Consumer Edition

TRID Survival Guide: Consumer Edition What you need to know about the TILA-RESPA Integrated Closing Disclosures. NFM Lending NMLS # 2893 Toll-Free: 1-888-233-0092 www.nfmlending.com Introduction NFM Lending

TRID Survival Guide: Consumer Edition What you need to know about the TILA-RESPA Integrated Closing Disclosures. NFM Lending NMLS # 2893 Toll-Free: 1-888-233-0092 www.nfmlending.com Introduction NFM Lending

Charting Your Course to Home Ownership

Charting Your Course to Home Ownership Twenty Questions to Ask Before Choosing a Mortgage To choose the best mortgage for yourself, you must know about the different types of mortgages. But, that s not

Charting Your Course to Home Ownership Twenty Questions to Ask Before Choosing a Mortgage To choose the best mortgage for yourself, you must know about the different types of mortgages. But, that s not

Adjustable Rate Mortgage (ARM) a mortgage with a variable interest rate, which adjusts monthly, biannually or annually.

a mortgage with a variable interest rate, which adjusts monthly, biannually or annually.") Glossary Adjustable Rate Mortgage (ARM) a mortgage with a variable interest rate, which adjusts monthly, biannually or annually. Amortization the way a loan is paid off over time in installments, detailing

Glossary Adjustable Rate Mortgage (ARM) a mortgage with a variable interest rate, which adjusts monthly, biannually or annually. Amortization the way a loan is paid off over time in installments, detailing

Obtain Information from Several Lenders

ESPAÑOL Shopping around for a home loan or mortgage will help you to get the best financing deal. A mortgage--whether it s a home purchase, a refinancing, or a home equity loan--is a product, just like

ESPAÑOL Shopping around for a home loan or mortgage will help you to get the best financing deal. A mortgage--whether it s a home purchase, a refinancing, or a home equity loan--is a product, just like

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES Federal Reserve Board Office of Thrift Supervision This booklet was originally prepared in consultation with the following organizations: American Bankers

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES Federal Reserve Board Office of Thrift Supervision This booklet was originally prepared in consultation with the following organizations: American Bankers

ORIGINAL 5/5 ADJUSTABLE RATE MORTGAGE LOAN 5/5 POWER PURCHASE MORTGAGE LOAN

5/5 ARM HOME LOAN RATES AND TERMS Effective October, 015 and subject to change. Get flexibility, stability and no closing costs 1 with SDCCU s 5/5 Adjustable Rate Mortgage Home Loan. Your rate can only

5/5 ARM HOME LOAN RATES AND TERMS Effective October, 015 and subject to change. Get flexibility, stability and no closing costs 1 with SDCCU s 5/5 Adjustable Rate Mortgage Home Loan. Your rate can only

Guide for Homebuyers

Guide for Homebuyers Tips for Getting a Safe Mortgage You Can Afford Q u i c k S u m m a ry Figure out what you can afford. Contact at least 3 different lenders or brokers. When you call, say: I m buying

Guide for Homebuyers Tips for Getting a Safe Mortgage You Can Afford Q u i c k S u m m a ry Figure out what you can afford. Contact at least 3 different lenders or brokers. When you call, say: I m buying

Consumer Handbook on Adjustable Rate Mortgages

Consumer Handbook on Adjustable Rate Mortgages Federal Reserve Board Office of Thrift supervision EQUAL HOUSING OPPORTUNITY This booklet was prepared in consultation with the following organizations: American

Consumer Handbook on Adjustable Rate Mortgages Federal Reserve Board Office of Thrift supervision EQUAL HOUSING OPPORTUNITY This booklet was prepared in consultation with the following organizations: American

Obtain Information from Several Lenders

Shopping around for a home loan or mortgage will help you to get the best financing deal. A mortgage--whether it s a home purchase, a refinancing, or a home equity loan--is a product, just like a car,

Shopping around for a home loan or mortgage will help you to get the best financing deal. A mortgage--whether it s a home purchase, a refinancing, or a home equity loan--is a product, just like a car,

Your Assets: Financing and Refinancing Properties

The Business Library Resource Report #35 Your Assets: Financing and Refinancing Properties Personal, Investment, and Business Properties! Basic Analysis of How and When! Fixed vs. Variable Interest Rate!

The Business Library Resource Report #35 Your Assets: Financing and Refinancing Properties Personal, Investment, and Business Properties! Basic Analysis of How and When! Fixed vs. Variable Interest Rate!

Outstanding mortgage balance

Using Home Equity There are numerous benefits to owning your own home. Not only does it provide a place to live, where you can decorate as you want, but it also provides a source of wealth. Over time,

Using Home Equity There are numerous benefits to owning your own home. Not only does it provide a place to live, where you can decorate as you want, but it also provides a source of wealth. Over time,

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES Federal Reserve Board Office of Thrift Supervision

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES Federal Reserve Board Office of Thrift Supervision This booklet was prepared in consultation with the following organizations: American Bankers Association

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES Federal Reserve Board Office of Thrift Supervision This booklet was prepared in consultation with the following organizations: American Bankers Association

MORTGAGE TERMS. Assignment of Mortgage A document used to transfer ownership of a mortgage from one party to another.

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

Consumer Handbook on Adjustable Rate Mortgages Published by: Federal Reserve Board Office of Thrift Supervision EQUAL HOUSING OPPORTUNITY This

Consumer Handbook on Adjustable Rate Mortgages Published by: Federal Reserve Board Office of Thrift Supervision EQUAL HOUSING OPPORTUNITY This booklet was prepared in consultation with the following organizations:

Consumer Handbook on Adjustable Rate Mortgages Published by: Federal Reserve Board Office of Thrift Supervision EQUAL HOUSING OPPORTUNITY This booklet was prepared in consultation with the following organizations:

HOMEBUYER S GUIDE. Know what it takes to buy your first home

HOMEBUYER S GUIDE Know what it takes to buy your first home homebuyer s guide If you re thinking about buying a home, we say congratulations. Most likely, it s the biggest purchase decision you ve made

HOMEBUYER S GUIDE Know what it takes to buy your first home homebuyer s guide If you re thinking about buying a home, we say congratulations. Most likely, it s the biggest purchase decision you ve made

Welcome. 1. Agenda. 2. Ground Rules. 3. Introductions. Your Own Home 2

Your Own Home Welcome 1. Agenda 2. Ground Rules 3. Introductions Your Own Home 2 Objectives If you are a pre-homebuyer: Explain the advantages and disadvantages of renting versus owning a home Identify

Your Own Home Welcome 1. Agenda 2. Ground Rules 3. Introductions Your Own Home 2 Objectives If you are a pre-homebuyer: Explain the advantages and disadvantages of renting versus owning a home Identify

Refinancing. Refinancing WISCONSIN HOMEOWNERSHIP PRESERVATION EDUCATION. Section Overview

People refinance their homes to take advantage of lower interest rates or to decrease their monthly payment. Sometimes it is done to create extra money for purchases (like a car) or for debt repayment.

People refinance their homes to take advantage of lower interest rates or to decrease their monthly payment. Sometimes it is done to create extra money for purchases (like a car) or for debt repayment.

Everything Guide to Mortgages Book: Find the Perfect Loan to Finance the Home of your Dreams (Everything (Business & Personal Finance))

)") Brochure More information from http://www.researchandmarkets.com/reports/2125178/ Everything Guide to Mortgages Book: Find the Perfect Loan to Finance the Home of your Dreams (Everything (Business & Personal

Brochure More information from http://www.researchandmarkets.com/reports/2125178/ Everything Guide to Mortgages Book: Find the Perfect Loan to Finance the Home of your Dreams (Everything (Business & Personal

Everything You Need to Know About Mortgage Refinancing

Everything You Need to Know About Mortgage Refinancing 1 Table of Contents Content Page Overview 3 Chapter 1: Types of Mortgages 4-8 Chapter 2: Types of Mortgage Interest 9-10 Chapter 3: Types of Lenders

Everything You Need to Know About Mortgage Refinancing 1 Table of Contents Content Page Overview 3 Chapter 1: Types of Mortgages 4-8 Chapter 2: Types of Mortgage Interest 9-10 Chapter 3: Types of Lenders

Section C. Maximum Mortgage Amounts on Streamline Refinances Overview

Section C. Maximum Mortgage Amounts on Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 General Information on 3-C-2 2 Without an Appraisal

Section C. Maximum Mortgage Amounts on Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 General Information on 3-C-2 2 Without an Appraisal

Refinancing Your Home Loan

Refinancing Your Home Loan Part 1: Should You Refinance? Reasons and Strategies Related Topics Part 2: Refinancing Costs Part 3: Reconveyance A Final Step When You Pay Off a Loan Quick summary: If you

Refinancing Your Home Loan Part 1: Should You Refinance? Reasons and Strategies Related Topics Part 2: Refinancing Costs Part 3: Reconveyance A Final Step When You Pay Off a Loan Quick summary: If you

Debt Management Options

Get and Stay on Track Debt Management Options Where should you start? The first step to determine which debt management tool is best for you is to review your financial situation and your financial goals.

Get and Stay on Track Debt Management Options Where should you start? The first step to determine which debt management tool is best for you is to review your financial situation and your financial goals.

Step-by-Step Home Mortgage Steps

1 Applicants with a good credit report will be in a stronger position to negotiate best rate and terms Your credit report is used by banks and other lending institutions to determine your creditworthiness.

1 Applicants with a good credit report will be in a stronger position to negotiate best rate and terms Your credit report is used by banks and other lending institutions to determine your creditworthiness.

RESIDENTIAL MORTGAGE PRODUCT INFORMATION DISCLOSURE

RESIDENTIAL MORTGAGE PRODUCT INFORMATION DISCLOSURE Whether you are buying a house or refinancing an existing mortgage, this information can help you decide what type of mortgage is right for you. You

RESIDENTIAL MORTGAGE PRODUCT INFORMATION DISCLOSURE Whether you are buying a house or refinancing an existing mortgage, this information can help you decide what type of mortgage is right for you. You

Mortgage Terms. Accrued interest Interest that is earned but not paid, adding to the amount owed.

Mortgage Terms Accrued interest Interest that is earned but not paid, adding to the amount owed. Negative amortization A rise in the loan balance when the mortgage payment is less than the interest due.

Mortgage Terms Accrued interest Interest that is earned but not paid, adding to the amount owed. Negative amortization A rise in the loan balance when the mortgage payment is less than the interest due.

JANUARY 2014. Shopping for a mortgage? What you can expect under federal rules

JANUARY 2014 Shopping for a mortgage? What you can expect under federal rules You ll be offered a mortgage that s set up to be affordable. When you apply for a mortgage, you may struggle to understand

JANUARY 2014 Shopping for a mortgage? What you can expect under federal rules You ll be offered a mortgage that s set up to be affordable. When you apply for a mortgage, you may struggle to understand

When calculating your monthly loan payments, the interest rate, and not the APR, is used.

FAQ on Mortgages RATE The posted interest rate is the actual rate used to calculate your monthly loan payment. The interest rate that you will be charged on your loan is set once you have completed our

FAQ on Mortgages RATE The posted interest rate is the actual rate used to calculate your monthly loan payment. The interest rate that you will be charged on your loan is set once you have completed our

BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING MORTGAGES

BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING MORTGAGES June 2015 Cat. No.: FC5-22/3-2015E-PDF ISBN: 978-0-660-02848-4 Her Majesty the Queen in Right of Canada (Financial Consumer

BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING MORTGAGES June 2015 Cat. No.: FC5-22/3-2015E-PDF ISBN: 978-0-660-02848-4 Her Majesty the Queen in Right of Canada (Financial Consumer

Instructor Guide Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum

Your Own Home Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Module Overview 1 Purpose 1 Objectives 1 Time 1 Materials and Equipment Needed to Present

Your Own Home Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Module Overview 1 Purpose 1 Objectives 1 Time 1 Materials and Equipment Needed to Present

First Timer s Guide PREParing First Time Homebuyers

First Timer s Guide PREParing First Time Homebuyers SO MANY QUESTIONS Maybe you live in the best apartment with a great landlord and don t want to change a thing. Or maybe you ve looked at the rent going

First Timer s Guide PREParing First Time Homebuyers SO MANY QUESTIONS Maybe you live in the best apartment with a great landlord and don t want to change a thing. Or maybe you ve looked at the rent going

Assumable mortgage: A mortgage that can be transferred from a seller to a buyer. The buyer then takes over payment of an existing loan.

MORTGAGE GLOSSARY Adjustable Rate Mortgage (ARM): A mortgage loan with payments usually lower than a fixed rate initially, but is subject to changes in interest rates. There are a variety of ARMs that

MORTGAGE GLOSSARY Adjustable Rate Mortgage (ARM): A mortgage loan with payments usually lower than a fixed rate initially, but is subject to changes in interest rates. There are a variety of ARMs that

Preparing for homeownership

Preparing for homeownership What we ll cover 1. Getting ready for homeownership 2. Mortgage basics 3. What you need to buy a home 4. Finding the right home 5. Resources 2 Getting ready for homeownership

Preparing for homeownership What we ll cover 1. Getting ready for homeownership 2. Mortgage basics 3. What you need to buy a home 4. Finding the right home 5. Resources 2 Getting ready for homeownership

How To Get A Home Equity Line Of Credit

WHAT YOU SHOULD KNOW ABOUT HOME EQUITY LINES OF CREDIT If you are in the market for credit, a home equity plan is one of several options that might be right for you. Before making a decision, however,

WHAT YOU SHOULD KNOW ABOUT HOME EQUITY LINES OF CREDIT If you are in the market for credit, a home equity plan is one of several options that might be right for you. Before making a decision, however,

Your home financing process checklist

Your home financing process checklist As you prepare to purchase a home or refinance your loan, it s important to know what to expect along the way. Here, we ve outlined some of the general steps in the

Your home financing process checklist As you prepare to purchase a home or refinance your loan, it s important to know what to expect along the way. Here, we ve outlined some of the general steps in the

Overview The Regulation The Loan Estimate (LE) The Closing Disclosure (CD) Loan Estimate (LE) Application Date LE Responsibility

The Closing Disclosure (CD) Loan Estimate (LE) Application Date LE Responsibility") To support your preparation efforts when implementing the TILA-RESPA Integrated Disclosure (TRID) rule effective for applications dated on or after October 3, 2015, we have created this Helpful Tips for

To support your preparation efforts when implementing the TILA-RESPA Integrated Disclosure (TRID) rule effective for applications dated on or after October 3, 2015, we have created this Helpful Tips for

The Federal Reserve Board. Consumer Handbook on Adjustable-Rate Mortgages

The Federal Reserve Board Consumer Handbook on Adjustable-Rate Mortgages Table of contents Consumer Handbook on Adjustable-Rate Mortgages i Mortgage shopping worksheet... 2 What is an ARM?... 4 How ARMs

The Federal Reserve Board Consumer Handbook on Adjustable-Rate Mortgages Table of contents Consumer Handbook on Adjustable-Rate Mortgages i Mortgage shopping worksheet... 2 What is an ARM?... 4 How ARMs

Fifth Third Home Buying Guide. A Guide to Residential Home Buying.

Fifth Third Home Buying Guide A Guide to Residential Home Buying. Important Contacts and Numbers. Use this page to record important information as you move through the homebuying process. Realtor/Builder

Fifth Third Home Buying Guide A Guide to Residential Home Buying. Important Contacts and Numbers. Use this page to record important information as you move through the homebuying process. Realtor/Builder

Quilty & Associates. May 8, 2013

Quilty & Associates May 8, 2013 Discussion Points Significance of HMDA On the Horizon Survival Tips Hot Spots Significance of HMDA HMDA Disclosure Requirements HMDA Poster must be displayed in the lobby

Quilty & Associates May 8, 2013 Discussion Points Significance of HMDA On the Horizon Survival Tips Hot Spots Significance of HMDA HMDA Disclosure Requirements HMDA Poster must be displayed in the lobby

Introduction. Instructor and student introductions. Module overview. Your Own Home

Introduction Instructor and student introductions. Module overview. 2 Student Introductions Your name. Your expectations, questions, and concerns about buying a home. 3 Purpose : Gives you information

Introduction Instructor and student introductions. Module overview. 2 Student Introductions Your name. Your expectations, questions, and concerns about buying a home. 3 Purpose : Gives you information

Buying your first home.

Financial Milestones: Buying your first home. What you should know to make the process easier and more rewarding. Everything you wanted to know about buying your first home Buying your first home can be

Financial Milestones: Buying your first home. What you should know to make the process easier and more rewarding. Everything you wanted to know about buying your first home Buying your first home can be

The Ultimate Mortgage Checklist

The Ultimate Mortgage Checklist The Rate 1. Is the rate you re quoting me the lowest I can possibly get, given my qualifications and mortgage preferences? 2. If I find a lower rate for a similar product

The Ultimate Mortgage Checklist The Rate 1. Is the rate you re quoting me the lowest I can possibly get, given my qualifications and mortgage preferences? 2. If I find a lower rate for a similar product

(FMS- Mortgage Package- 19 October 2011)