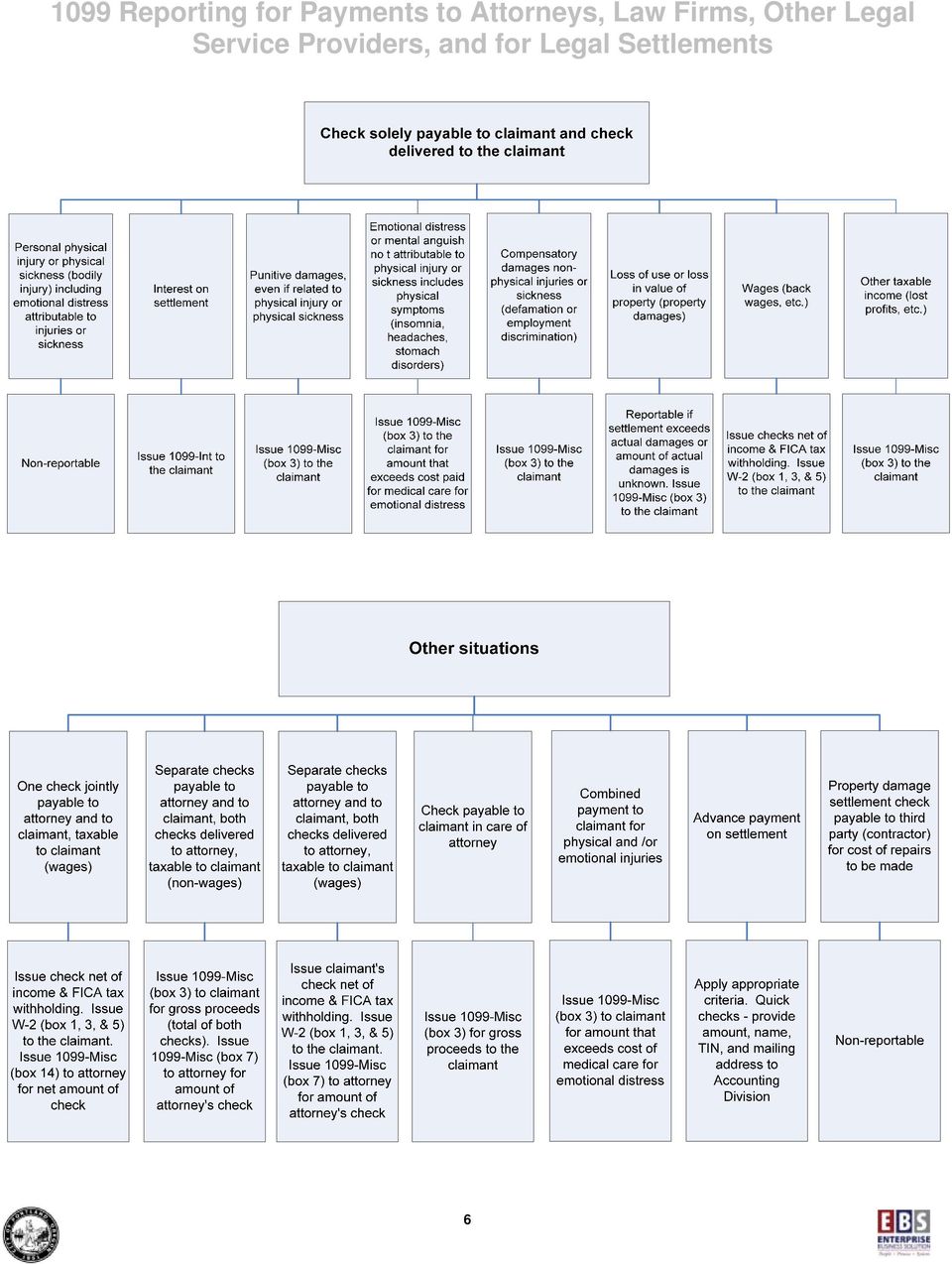

1099 Reporting for Payments to Attorneys, Law Firms, Other Legal Service Providers, and for Legal Settlements

|

|

|

- Elfrieda Hensley

- 8 years ago

- Views:

Transcription

1 1. How to report and record transactions for legal services provided by an attorney (non-employee of the City), law firm, or other provider of legal services including a corporation proving legal services per section 6045(f) 1

2 2. How to report and record transactions for gross proceeds of legal settlements if the check is payable to an attorney, law firm, or other provider of legal services including a corporation proving legal services per section 6045(f). (If the settlement is taxable (non-wage) income to the claimant, a second 1099-Misc (box 3) must be issued to the claimant.) Gross proceeds paid to an attorney, law firm or other provider of legal services including corporations providing legal services Reportable in Box 14 of the 1099-Misc (payments aggregating $600 or more during a calendar year) Prior to payment, obtain attorney's taxpayer identification number (TIN) & the name associated with it by the IRS IBIS name = Attorney's name associated with TIN by the IRS, Vendor name = Attorney & claimant's name IBIS = "MA" SAP = "FE 14" "FE" Misc & "14" - box 14 28% back up withholding required if no TIN or an incorrect TIN provided prior to payment SAP - Vendor name 1 = Attorney's name associated with TIN by the IRS The TIN provided needs to be for the attorney or firm named on the check. (If TIN for law firm is provided then law firm's name needs to be on the check) SAP - Vendor name 2 = Claimant's name and/or rest of a long attorney's name IBIS or SAP - Don't shorten names, no nicknames, allowable punctuation = a dash "-", a space " ", or an "&" 2

Prior to payment, obtain attorney's taxpayer identification number (TIN) & the name associated with it by the IRS IBIS - 1099 name = Attorney's name associated with TIN")

3 3. How to report and record transactions for gross proceeds of legal settlements if the check is payable to the claimant and the payment is for a taxable non-wage claim per section 6045(f) Settlement paid to claimant for taxable, nonwage claim (punitive damages, emotional distress, lost profits, defamation, & employment discrimination, etc.) Reportable in Box 3 of the 1099-Misc (Payments aggregating $600 or more during a calendar year) Prior to payment, obtain claimant's taxpayer identification number (TIN) & the name associated with it by the IRS IBIS - Vendor name and/or 1099 name = Name associated with TIN by the IRS IBIS = "M3" SAP = "FE 03" "FE" Misc & "03" - box 3 28% back up withholding required if no TIN or an incorrect TIN provided prior to payment SAP - Vendor name 1 = Name associated with TIN by the IRS SAP - For long vendor names you can also use Vendor name 2 IBIS or SAP - Don't shorten names, no nicknames, allowable punctuation = a dash "-", a space " ", or an "&" 3

4 4. How to report and record transactions so that a 1099-Misc will be issued to the claimant for gross proceeds of legal settlements when the check is payable to an attorney or a third party and the payment is for a taxable non-wage claim per section 6045(f) 4

5 5. For settlements, the type of information return (1099-Misc, 1099-Int, Form W-2, etc.) required depends on to whom the settlement check is payable, to whom the check is delivered, for what the settlement is for, and if it is taxable income to the claimant. 5

6 6

7 Discussion Issues: 1. In SAP, vendor name 1 (the first name printed on the check) has to be the name of the individual or firm that will receive the 1099-Misc, usually the attorney or law firm. The claimant s name can be on vendor name 2. This is necessary because there is no 1099 name field in SAP a. At this time, checks are typically paid as follows: Claimant name and his/her attorney, attorney name b. In SAP this needs to be reversed as follows: Attorney or law firm name and claimant, claimant name i. Does this affect the wording used in city ordinances or court judgments? ii. Does the Payments/Settlements/Recoveries/Judgments form need any revisions? iii. Are there other issues with making this change? 2. Currently, checks often name an individual attorney but the attorney is providing the TIN for his/her law firm. In IBIS, the 1099 name had to be changed to the firm s name. This is not necessarily in compliance with the reporting requirements (IRS section 6045(f)) a. According to the requirement, the TIN provided should be that of the attorney or law firm named on the check i. If the law firm s TIN is to be used, then vendor name 1 and the check should use the law firm s name instead of the attorney s name ii. If the attorney s name is to be used then the attorney needs to provide his/her TIN 1. If the attorney provides the law firm s TIN, this is an incorrect TIN and 28% withholding is required b. Is there any reason not to use the law firm s name? 3. Vendor names acceptable to and identifiable by the IRS for 1099s a. Typically, the vendor name can t use a nickname or abbreviation unless that is how it was registered with the IRS i. Robert Smith instead of Bob Smith ii. Northwest Legal Services instead of NW Legal Services b. The vendor name should not be an assumed business name (ABN). In SAP, an ABN can be entered in vendor name 2 i. Gatti & Gatti Law Firm PC instead of it s ABN, Gatti Gatti Maier Sayer Thayer & Associates c. The only punctuation allowed are dashes, -, spaces,, and the &. No commas, periods, etc. 4. Quick checks have been used for advances on settlement payments and possibly for settlement payments. These payments are not traceable, in IBIS, to the vendor (claimant or attorney). I don t know about SAP. To prepare 1099s, the Accounting Division will need a list of Quick Checks used for reportable payments including the check amount, name, TIN, mailing address, type of payment, etc. 7

4/4/2012. IRS 1099 Reporting of Settlements and Payments to Attorneys

4/4/2012 IRS 1099 Reporting of Settlements and Payments to Attorneys PROGRAM PRESENTED APRIL 10, 2012 1 1 Marianne Couch, JD Cokala Tax Information Reporting Solutions, LLC PO Box 2224 Ann Arbor, MI 48106

4/4/2012 IRS 1099 Reporting of Settlements and Payments to Attorneys PROGRAM PRESENTED APRIL 10, 2012 1 1 Marianne Couch, JD Cokala Tax Information Reporting Solutions, LLC PO Box 2224 Ann Arbor, MI 48106

Tax Reporting for Settlement Agreements. Training Session February 13, 2008

Tax Reporting for Settlement Agreements Training Session February 13, 2008 Presenters Bob Jaros Deputy State Controller 303-866-3765 Bob.Jaros@state.co.us 633 17 th Street, 15 th Floor Denver, CO 80202

Tax Reporting for Settlement Agreements Training Session February 13, 2008 Presenters Bob Jaros Deputy State Controller 303-866-3765 Bob.Jaros@state.co.us 633 17 th Street, 15 th Floor Denver, CO 80202

1099 PROCESSING TERMINOLOGY

1099 PROCESSING The Internal Revenue Service (IRS) requires that recipients of certain financial transactions pay taxes on those transactions. The providers of taxable benefits are required to notify the

1099 PROCESSING The Internal Revenue Service (IRS) requires that recipients of certain financial transactions pay taxes on those transactions. The providers of taxable benefits are required to notify the

Guide for End-of-Year AP Best Practices

HOW-TO Guide for End-of-Year AP Best Practices 2015-2016 Contents Year-End Checklist for Accounts Payable Sample Year-End Calendar Master Vendor File Clean-Up and Maintenance 1099 Misc. Reporting and Corrections

HOW-TO Guide for End-of-Year AP Best Practices 2015-2016 Contents Year-End Checklist for Accounts Payable Sample Year-End Calendar Master Vendor File Clean-Up and Maintenance 1099 Misc. Reporting and Corrections

FORM 1099 MISC REMINDERS FOR STATE AND LOCAL GOVERNMENTS

FORM 1099 MISC REMINDERS FOR STATE AND LOCAL GOVERNMENTS WHO MUST FILE Any entity conducting a trade or business is required to file Form 1099. Government Agencies and non-profit organizations are also

FORM 1099 MISC REMINDERS FOR STATE AND LOCAL GOVERNMENTS WHO MUST FILE Any entity conducting a trade or business is required to file Form 1099. Government Agencies and non-profit organizations are also

Taxation of Terminations, Settlements and Judges

2015 YLD Bridge the Gap Seminar Taxation of Terminations, Settlements and Judges 11:30 a.m.-12:00 p.m. Presented by: David Repp Dickinson Mackaman Tyler & Hagen PC 699 Walnut St. Suite 1600 Des Moines,

2015 YLD Bridge the Gap Seminar Taxation of Terminations, Settlements and Judges 11:30 a.m.-12:00 p.m. Presented by: David Repp Dickinson Mackaman Tyler & Hagen PC 699 Walnut St. Suite 1600 Des Moines,

Information Reporting Forms 1099. Sponsored by Office of Financial Management and Internal Revenue Service December 12, 2012

Information Reporting Forms 1099 Sponsored by Office of Financial Management and Internal Revenue Service December 12, 2012 Information Reporting Form Code Section 1098 6050H 1098-E 6050S 1098-T 6050S

Information Reporting Forms 1099 Sponsored by Office of Financial Management and Internal Revenue Service December 12, 2012 Information Reporting Form Code Section 1098 6050H 1098-E 6050S 1098-T 6050S

VISION Vendor Set up, W-9 Forms and Reportable Payment Processing FAQs

VISION Vendor Set up, W-9 Forms and Reportable Payment Processing FAQs 1. Question: I have had multiple requests from Finance to obtain a W-9 from new vendors that I requested to be set up in VISION or

VISION Vendor Set up, W-9 Forms and Reportable Payment Processing FAQs 1. Question: I have had multiple requests from Finance to obtain a W-9 from new vendors that I requested to be set up in VISION or

Employment Tax Considerations for Businesses When Addressing Litigation with Employees or Former Employees

Employment Tax Considerations for Businesses When Addressing Litigation with Employees or Former Employees William Hays Weissman Littler Mendelson, P.C. San Francisco, California It is a common fact of

Employment Tax Considerations for Businesses When Addressing Litigation with Employees or Former Employees William Hays Weissman Littler Mendelson, P.C. San Francisco, California It is a common fact of

GUIDE FOR TAX REPORTING AND WITHHOLDING OF SETTLEMENT AWARDS

GUIDE FOR TAX REPORTING AND WITHHOLDING OF SETTLEMENT AWARDS Office of the State Controller State of Colorado Revised January, 1997 I. Purpose The purpose of this guide is to provide information necessary

GUIDE FOR TAX REPORTING AND WITHHOLDING OF SETTLEMENT AWARDS Office of the State Controller State of Colorado Revised January, 1997 I. Purpose The purpose of this guide is to provide information necessary

REQUIREMENT TO FILE FORMS 1099

REQUIREMENT TO FILE FORMS 1099 The Internal Revenue Service ( IRS ) has begun focusing heavily on taxpayer compliance with information reporting laws. In just a few short years, Congress has sharply increased

REQUIREMENT TO FILE FORMS 1099 The Internal Revenue Service ( IRS ) has begun focusing heavily on taxpayer compliance with information reporting laws. In just a few short years, Congress has sharply increased

TAX IMPLICATIONS AND PRACTICAL IMPACTS OF DAMAGES IN EMPLOYMENT CASES

TAX IMPLICATIONS AND PRACTICAL IMPACTS OF DAMAGES IN EMPLOYMENT CASES Brian Jorgensen Jones Day 2727 N. Harwood Street Dallas, Texas 75201 (214) 969-3741 bmjorgensen@jonesday.com Stephen Harris Jones Day

TAX IMPLICATIONS AND PRACTICAL IMPACTS OF DAMAGES IN EMPLOYMENT CASES Brian Jorgensen Jones Day 2727 N. Harwood Street Dallas, Texas 75201 (214) 969-3741 bmjorgensen@jonesday.com Stephen Harris Jones Day

SETTLEMENTS AND JUDGMENTS YOU MEAN I HAVE TO PAY TAXES?

SETTLEMENTS AND JUDGMENTS YOU MEAN I HAVE TO PAY TAXES? By: Geoffrey N. Taylor, Esq. I. INCOME TO PLAINTIFF A. Distinction between settlements and judgments. B. Basic rule is the origin of claims test.

SETTLEMENTS AND JUDGMENTS YOU MEAN I HAVE TO PAY TAXES? By: Geoffrey N. Taylor, Esq. I. INCOME TO PLAINTIFF A. Distinction between settlements and judgments. B. Basic rule is the origin of claims test.

Payment Card and Third Party Network Transactions

Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable,

Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable,

Employers' Responsibilities When Making Settlements in Employment-Related Claims

Employers' Responsibilities When Making Settlements in Employment-Related Claims Contributed by: Elizabeth Erickson * & Ira B. Mirsky **, McDermott Will & Emery, LLP Employee litigation alleging discrimination

Employers' Responsibilities When Making Settlements in Employment-Related Claims Contributed by: Elizabeth Erickson * & Ira B. Mirsky **, McDermott Will & Emery, LLP Employee litigation alleging discrimination

The Tax Consequences of Settlement Agreements

COMPENSATION/Compliance The Tax Consequences of Settlement Agreements Compensation & Benefits Review 42(5) 426 431 2010 SAGE Publications Reprints and permission: http://www. sagepub.com/journalspermissions.nav

COMPENSATION/Compliance The Tax Consequences of Settlement Agreements Compensation & Benefits Review 42(5) 426 431 2010 SAGE Publications Reprints and permission: http://www. sagepub.com/journalspermissions.nav

TEN WAYS TAXES IMPACT LEGAL FEES

TEN WAYS TAXES IMPACT LEGAL FEES By Robert W. Wood 1 No one likes paying legal fees, but tax deductions make them less painful. For example, if your combined state and federal tax rate is 40%, $10,000

TEN WAYS TAXES IMPACT LEGAL FEES By Robert W. Wood 1 No one likes paying legal fees, but tax deductions make them less painful. For example, if your combined state and federal tax rate is 40%, $10,000

TAX TREATMENT OF RECOVERIES IN EMPLOYMENT DISPUTES

TAX TREATMENT OF RECOVERIES IN EMPLOYMENT DISPUTES Committee on Labor & Employment Law AUGUST 2009 THE ASSOCIATION OF THE BAR OF THE CITY OF NEW YORK 42 WEST 44 TH STREET, NEW YORK, NY 10036 TAX TREATMENT

TAX TREATMENT OF RECOVERIES IN EMPLOYMENT DISPUTES Committee on Labor & Employment Law AUGUST 2009 THE ASSOCIATION OF THE BAR OF THE CITY OF NEW YORK 42 WEST 44 TH STREET, NEW YORK, NY 10036 TAX TREATMENT

IRS GUIDELINES FOR FORM 1099 FOR STATE AND LOCAL GOVERNMENTS IRS Webinar: http://www.tax.gov/1099webinar/

1 IRS GUIDELINES FOR FORM 1099 FOR STATE AND LOCAL GOVERNMENTS IRS Webinar: http://www.tax.gov/1099webinar/ WHO MUST FILE Any entity conducting a trade or business is required to file Form 1099. Government

1 IRS GUIDELINES FOR FORM 1099 FOR STATE AND LOCAL GOVERNMENTS IRS Webinar: http://www.tax.gov/1099webinar/ WHO MUST FILE Any entity conducting a trade or business is required to file Form 1099. Government

Tax Information and Legal Matters

Tax Information and Legal Matters This section covers tax information and legal matters that affect your benefits. Income Tax Withholding Under federal and California law, CalSTRS will withhold income

Tax Information and Legal Matters This section covers tax information and legal matters that affect your benefits. Income Tax Withholding Under federal and California law, CalSTRS will withhold income

Structured Attorney s Fees

STRUCTURED SETTLEMENTS Structured Attorney s Fees Preparing for Your Financial Future 7/13 26169-13B Table of Contents Managing Your Retirement... 2 The Power of Tax Deferral... 3 Structured Attorney s

STRUCTURED SETTLEMENTS Structured Attorney s Fees Preparing for Your Financial Future 7/13 26169-13B Table of Contents Managing Your Retirement... 2 The Power of Tax Deferral... 3 Structured Attorney s

Elizabeth Erickson & Ira B. Mirsky, McDermott Will & Emery, LLP

Tax Consequences of Employment Cases Elizabeth Erickson & Ira B. Mirsky, McDermott Will & Emery, LLP Employment-related litigation is not only a major business concern it involves substantial tax ramifications

Tax Consequences of Employment Cases Elizabeth Erickson & Ira B. Mirsky, McDermott Will & Emery, LLP Employment-related litigation is not only a major business concern it involves substantial tax ramifications

enc3 Specifications for 1099 Reporting

Form enc3 1099 Format (11-2015) http://www.dornc.com/enc3/ North Carolina Department of Revenue P. O. Box 25000 Raleigh, NC 27640 (877) 252-3052 toll-free enc3 Specifications for 1099 Reporting Submit

Form enc3 1099 Format (11-2015) http://www.dornc.com/enc3/ North Carolina Department of Revenue P. O. Box 25000 Raleigh, NC 27640 (877) 252-3052 toll-free enc3 Specifications for 1099 Reporting Submit

SECTION FIVE FEDERAL AND STATE REQUIREMENTS TO BECOME A VENDOR FISCAL/EMPLOYER AGENT ISO

SECTION FIVE FEDERAL AND STATE REQUIREMENTS TO BECOME A VENDOR FISCAL/EMPLOYER AGENT ISO 5.1 Overview There are a number of federal and state requirements that an organization must fulfill in order to

SECTION FIVE FEDERAL AND STATE REQUIREMENTS TO BECOME A VENDOR FISCAL/EMPLOYER AGENT ISO 5.1 Overview There are a number of federal and state requirements that an organization must fulfill in order to

RECENT DEVELOPMENTS IN TAXATION OF COURT COSTS AND ATTORNEY FEES FOR INDIVIDUALS

NOTE: This article was referenced in the June 2005 In Brief in the article entitled, Taxes on Attorney Fees. It is a more detailed explanation of the issues discussed in that article. Our thanks to Philip

NOTE: This article was referenced in the June 2005 In Brief in the article entitled, Taxes on Attorney Fees. It is a more detailed explanation of the issues discussed in that article. Our thanks to Philip

JANUARY 2015 UPDATE ON PAYROLL, EMPLOYMENT TAXES AND INFORMATION RETURNS

JANUARY 2015 UPDATE ON PAYROLL, EMPLOYMENT TAXES AND INFORMATION RETURNS This letter sets forth employee payroll tax withholding rates, employer payroll tax rates in effect for 2015 and some pertinent

JANUARY 2015 UPDATE ON PAYROLL, EMPLOYMENT TAXES AND INFORMATION RETURNS This letter sets forth employee payroll tax withholding rates, employer payroll tax rates in effect for 2015 and some pertinent

RCUH Vendor File & IRS Form 1099 Reporting Requirements. October 2013

RCUH Vendor File & IRS Form 1099 Reporting Requirements October 2013 What s on the Agenda? The What and the Why Making improvements Vendor file & vendor records - What s in it Searching the file A new

RCUH Vendor File & IRS Form 1099 Reporting Requirements October 2013 What s on the Agenda? The What and the Why Making improvements Vendor file & vendor records - What s in it Searching the file A new

Employment Tax Issues

Employment Tax Issues Tip Reporting Guidance Rev. Rul. 2012-18, 2012-26 I.R.B. 1032 Issued July, 2013 Q&A 1 of Rev. Rul. 2012-18 reaffirms long time IRS position on tip wages vs. service charges (non-tip

Employment Tax Issues Tip Reporting Guidance Rev. Rul. 2012-18, 2012-26 I.R.B. 1032 Issued July, 2013 Q&A 1 of Rev. Rul. 2012-18 reaffirms long time IRS position on tip wages vs. service charges (non-tip

BULLETIN NUMBER: 259 March 2, 1998

STATE OF NEW YORK UNIFIED COURT SYSTEM OFFICE OF MANAGEMENT SUPPORT AGENCY BLDG. 4-19TH FLOOR 4 ESP, SUITE 2001 EMPIRE STATE PLAZA ALBANY, NEW YORK 12223-1450 (518) 474-4971 JONATHAN LIPPMAN Chief Administrative

STATE OF NEW YORK UNIFIED COURT SYSTEM OFFICE OF MANAGEMENT SUPPORT AGENCY BLDG. 4-19TH FLOOR 4 ESP, SUITE 2001 EMPIRE STATE PLAZA ALBANY, NEW YORK 12223-1450 (518) 474-4971 JONATHAN LIPPMAN Chief Administrative

tax information reporting

onesource tax information reporting IRC Section 6050W: FORM 1099-K TAX INFORMATION REPORTING FOR PAYMENTS IN SETTLEMENT OF TRANSACTIONS MADE THROUGH PAYMENT CARDS AND THIRD-PARTY NETWORKS With new Internal

onesource tax information reporting IRC Section 6050W: FORM 1099-K TAX INFORMATION REPORTING FOR PAYMENTS IN SETTLEMENT OF TRANSACTIONS MADE THROUGH PAYMENT CARDS AND THIRD-PARTY NETWORKS With new Internal

Internal Revenue Service Number: 200702006 Release Date: 1/12/2007 Index Number: 3406.00-00, 6041.03-00, 6041.05-00, 6045.00-00, 6049.

Internal Revenue Service Number: 200702006 Release Date: 1/12/2007 Index Number: 3406.00-00, 6041.03-00, 6041.05-00, 6045.00-00, 6049.01-00 -------------------------------- ------------------------------------

Internal Revenue Service Number: 200702006 Release Date: 1/12/2007 Index Number: 3406.00-00, 6041.03-00, 6041.05-00, 6045.00-00, 6049.01-00 -------------------------------- ------------------------------------

Notice 2014-21 SECTION 1. PURPOSE

1 Notice 2014-21 SECTION 1. PURPOSE This notice describes how existing general tax principles apply to transactions using virtual currency. The notice provides this guidance in the form of answers to frequently

1 Notice 2014-21 SECTION 1. PURPOSE This notice describes how existing general tax principles apply to transactions using virtual currency. The notice provides this guidance in the form of answers to frequently

DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE Washington, DC 20224. June 7, 2012

DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE Washington, DC 20224 Whistleblower Office June 7, 2012 Control Number: WO -25-0612-03 Expires Date: June 7, 2013 Impacted IRM: 25.2.2 MEMORANDUM FOR

DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE Washington, DC 20224 Whistleblower Office June 7, 2012 Control Number: WO -25-0612-03 Expires Date: June 7, 2013 Impacted IRM: 25.2.2 MEMORANDUM FOR

EnterpriseOne B73.3.1 IRS Form 1099 Processing (1998) PeopleBook

PeopleBook") EnterpriseOne B73.3.1 IRS Form 1099 Processing (1998) PeopleBook June 1999 J.D. Edwards World Source Company One Technology Way Denver, CO 80237 Portions of this document were reproduced from material

EnterpriseOne B73.3.1 IRS Form 1099 Processing (1998) PeopleBook June 1999 J.D. Edwards World Source Company One Technology Way Denver, CO 80237 Portions of this document were reproduced from material

QUALIFIED SETTLEMENT TRUSTS A Useful Tool in Multi-Party Litigation

2005, Davis, Malm & D Agostine, P.C. QUALIFIED SETTLEMENT TRUSTS A Useful Tool in Multi-Party Litigation Marjorie Suisman, Esq. Davis Malm & D Agostine P.C. I. Introduction. A Designated Settlement Fund

2005, Davis, Malm & D Agostine, P.C. QUALIFIED SETTLEMENT TRUSTS A Useful Tool in Multi-Party Litigation Marjorie Suisman, Esq. Davis Malm & D Agostine P.C. I. Introduction. A Designated Settlement Fund

Annual Payroll Tax Update

Annual Payroll Tax Update Krista Koster, CPA, MSA Tessa Keena, Senior Accountant Rates and Wage Bases Standard Mileage Rates Type 2015 2014 Business Miles * 56 cents Medical/moving * 23.5 cents Charitable

Annual Payroll Tax Update Krista Koster, CPA, MSA Tessa Keena, Senior Accountant Rates and Wage Bases Standard Mileage Rates Type 2015 2014 Business Miles * 56 cents Medical/moving * 23.5 cents Charitable

BEFORE THE TAX COMMISSION OF THE STATE OF IDAHO. On January 30, 2004, the Income Tax Audit Bureau (Bureau) of the Idaho State Tax

of the Idaho State Tax") BEFORE THE TAX COMMISSION OF THE STATE OF IDAHO In the Matter of the Protest of ) ) DOCKET NO. 17986 ) ) DECISION Petitioner. ) ) On January 30, 2004, the Income Tax Audit Bureau (Bureau) of the Idaho

BEFORE THE TAX COMMISSION OF THE STATE OF IDAHO In the Matter of the Protest of ) ) DOCKET NO. 17986 ) ) DECISION Petitioner. ) ) On January 30, 2004, the Income Tax Audit Bureau (Bureau) of the Idaho

ISSUES. (1) When are attorney s fees paid by an employer as part of a settlement agreement with a former employee subject to employment taxes?

When are attorney s fees paid by an employer as part of a settlement agreement with a former employee subject to employment taxes?") Office of Chief Counsel Internal Revenue Service Memorandum Release Number: 20133501F Release Date: 8/30/2013 CC:TEGE:FS:MABAL:MRLenius POSTF-129928-13 Release Number: Release Date: 8/30/2013 date: July

Office of Chief Counsel Internal Revenue Service Memorandum Release Number: 20133501F Release Date: 8/30/2013 CC:TEGE:FS:MABAL:MRLenius POSTF-129928-13 Release Number: Release Date: 8/30/2013 date: July

Volume No. 1 Policies & Procedures TOPIC NO. 20319 Cardinal Section No. 20300 Cash Disbursements Accounting

Table of Contents OVERVIEW... 3 Introduction to EFTPS...3 Tax Reporting Entity...3 Policy...3 To Enroll in EFTPS...3 Tax Payment Frequency...4 IRS Penalty...4 Additional Tax Types...4 PAYMENT PROCESSING

Table of Contents OVERVIEW... 3 Introduction to EFTPS...3 Tax Reporting Entity...3 Policy...3 To Enroll in EFTPS...3 Tax Payment Frequency...4 IRS Penalty...4 Additional Tax Types...4 PAYMENT PROCESSING

Section 7.13 INTERNAL REVENUE SERVICE REPORTING REQUIREMENTS

Section 7.13 INTERNAL REVENUE SERVICE REPORTING REQUIREMENTS Table of Contents PURPOSE...7-13-1 AUTHORITY...7-13-1 SCOPE...7-13-1 REFERENCES...7-13-1 TRAINING...7-13-1 FORMS...7-13-1 DEFINITIONS...7-13-2

Section 7.13 INTERNAL REVENUE SERVICE REPORTING REQUIREMENTS Table of Contents PURPOSE...7-13-1 AUTHORITY...7-13-1 SCOPE...7-13-1 REFERENCES...7-13-1 TRAINING...7-13-1 FORMS...7-13-1 DEFINITIONS...7-13-2

PROCESSING UTILITY PAYMENTS...

Function No. 20000 General TOPIC PROMPT PAYMENT Table of Contents OVERVIEW... 2 Introduction...2 POLICY... 2 Written Procedures...2 General Requirements...3 Payment Due Date...4 When Due Dates Don't Apply...4

Function No. 20000 General TOPIC PROMPT PAYMENT Table of Contents OVERVIEW... 2 Introduction...2 POLICY... 2 Written Procedures...2 General Requirements...3 Payment Due Date...4 When Due Dates Don't Apply...4

Tax Aspects of Settlements and Judgments

Tax Aspects of Settlements and Judgments Dominic L. Daher, MAcc, JD, LLM in Taxation Director of Internal Audit and Tax Compliance Adjunct Professor of Law University of San Francisco Dawn G. Mayer, JD,

Tax Aspects of Settlements and Judgments Dominic L. Daher, MAcc, JD, LLM in Taxation Director of Internal Audit and Tax Compliance Adjunct Professor of Law University of San Francisco Dawn G. Mayer, JD,

$ 2 Royalties. Form 1099-MISC 3 Other income. 4 Federal income tax withheld. 5 Fishing boat proceeds 6 Medical and health care payments

Attention: Do not download, print, and file Copy A with the IRS. Copy A appears in red, similar to the official IRS form, but is for informational purposes only. A penalty of 50 per information return

Attention: Do not download, print, and file Copy A with the IRS. Copy A appears in red, similar to the official IRS form, but is for informational purposes only. A penalty of 50 per information return

Attention: See IRS Publications 1141, 1167, 1179 and other IRS resources for information about printing these tax forms.

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

FEDERAL INCOME TAX AND PERSONAL INJURY JUDGMENTS AND SETTLEMENTS By Fred A. Simpson 1

FEDERAL INCOME TA AND PERSONAL INJURY JUDGMENTS AND SETTLEMENTS By Fred A. Simpson 1 For eighty years federal law did not impose income tax on damages or settlements on account of personal injuries. 2

FEDERAL INCOME TA AND PERSONAL INJURY JUDGMENTS AND SETTLEMENTS By Fred A. Simpson 1 For eighty years federal law did not impose income tax on damages or settlements on account of personal injuries. 2

1 Rents. 2 Royalties. $ 3 Other income. 5 Fishing boat proceeds. $ 7 Nonemployee compensation

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Form W-9. What happens if our church does not issue the required 1099s?

A 1099 is an IRS form your church will use to report to the IRS annual non-employee compensation totals of $600 or more paid to non-incorporated service and rental providers. Examples would be: - Guest

A 1099 is an IRS form your church will use to report to the IRS annual non-employee compensation totals of $600 or more paid to non-incorporated service and rental providers. Examples would be: - Guest

UNDERSTANDING YOUR FINANCIAL PACKAGE

UNDERSTANDING YOUR FINANCIAL PACKAGE UNDERSTANDING YOUR FINANCIAL AID Presenter: Lisa Wioskowski Financial Aid Coordinator, TGS Topics Cost of Attendance Federal Loans Fellowships Payments (Stipends) Non-compensatory

UNDERSTANDING YOUR FINANCIAL PACKAGE UNDERSTANDING YOUR FINANCIAL AID Presenter: Lisa Wioskowski Financial Aid Coordinator, TGS Topics Cost of Attendance Federal Loans Fellowships Payments (Stipends) Non-compensatory

UNDERSTANDING YOUR FORM W-2 AND 1042-S INFORMATION REGARDING YOUR FORM W-2 WAGE AND TAX STATEMENT

UNDERSTANDING YOUR FORM W-2 AND 1042-S INFORMATION REGARDING YOUR FORM W-2 WAGE AND TAX STATEMENT The Form W-2 is your wage and tax statement provided by your employer to provide information on your taxable

UNDERSTANDING YOUR FORM W-2 AND 1042-S INFORMATION REGARDING YOUR FORM W-2 WAGE AND TAX STATEMENT The Form W-2 is your wage and tax statement provided by your employer to provide information on your taxable

SETTLING CASES AND TAXES

SETTLING CASES AND TAXES WILLIAM A. ROBERTS The Roberts Law Firm (972) 661-1040 bill@therobertslawfirm.com State Bar of Texas 28 TH ANNUAL ADVANCED CIVIL TRIAL COURSE August 31 September 2, 2005 - Austin

SETTLING CASES AND TAXES WILLIAM A. ROBERTS The Roberts Law Firm (972) 661-1040 bill@therobertslawfirm.com State Bar of Texas 28 TH ANNUAL ADVANCED CIVIL TRIAL COURSE August 31 September 2, 2005 - Austin

How To Get A Structured Settlement Attorney S Fee Annuity

STRUCTURED SETTLEMENTS Structured Attorney s Fees Preparing for Your Financial Future 1/13 26169-13A Table of Contents Planning for the Future by Structuring the Attorney s Fee... 1 Managing Your Retirement...

STRUCTURED SETTLEMENTS Structured Attorney s Fees Preparing for Your Financial Future 1/13 26169-13A Table of Contents Planning for the Future by Structuring the Attorney s Fee... 1 Managing Your Retirement...

1 Rents. 2 Royalties. $ 3 Other income. 5 Fishing boat proceeds. $ 7 Nonemployee compensation

Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable,

Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable,

Notice of Proposed Rules Regarding Employment Taxation of Transfers Incident to Divorce

Part III - Administrative, Procedural, and Miscellaneous Notice of Proposed Rules Regarding Employment Taxation of Transfers Incident to Divorce Notice 2002-31 I. Overview and Purpose This notice sets

Part III - Administrative, Procedural, and Miscellaneous Notice of Proposed Rules Regarding Employment Taxation of Transfers Incident to Divorce Notice 2002-31 I. Overview and Purpose This notice sets

Vendor & Supplier Guide

Vendor & Supplier Guide IRS & FTB Withholding Guidelines for Foreign Payees California Institute of Technology Payment Services Department 1200 E. California Blvd., Suite 101, MC 103-6, Pasadena, CA 91125

Vendor & Supplier Guide IRS & FTB Withholding Guidelines for Foreign Payees California Institute of Technology Payment Services Department 1200 E. California Blvd., Suite 101, MC 103-6, Pasadena, CA 91125

Terms and Conditions for Tax Services

Terms and Conditions for Tax Services In the course of delivering services relating to tax return preparation, tax advisory, and assistance in tax controversy matters, Brady, Martz & Associates, P.C. (we

Terms and Conditions for Tax Services In the course of delivering services relating to tax return preparation, tax advisory, and assistance in tax controversy matters, Brady, Martz & Associates, P.C. (we

ADDITIONAL TOPICS. Glenn Gizzi. Fall/Winter 2013

ADDITIONAL TOPICS Glenn Gizzi Fall/Winter 2013 Registered Tax Return Preparer Program Jan. 18, 2013 U.S District Court enjoined the IRS from enforcing the regulatory requirements for registered tax return

ADDITIONAL TOPICS Glenn Gizzi Fall/Winter 2013 Registered Tax Return Preparer Program Jan. 18, 2013 U.S District Court enjoined the IRS from enforcing the regulatory requirements for registered tax return

Instructions to process IRS forms 1099 in PeopleSoft

Instructions to process IRS forms 1099 in PeopleSoft Step 1. Identify vendors designated as 1099 vendors for reporting purposes. From the Query Viewer menu, run the query LC_1099_VENDORS. Enter council

Instructions to process IRS forms 1099 in PeopleSoft Step 1. Identify vendors designated as 1099 vendors for reporting purposes. From the Query Viewer menu, run the query LC_1099_VENDORS. Enter council

New York Life Insurance Company

New York Life Insurance Company PO Box 30713 Tampa FL 33630-3713 Dear Beneficiary: Please accept our condolences on your recent loss. We understand this is a difficult time, and we hope that we can alleviate

New York Life Insurance Company PO Box 30713 Tampa FL 33630-3713 Dear Beneficiary: Please accept our condolences on your recent loss. We understand this is a difficult time, and we hope that we can alleviate

Lost Wages in Personal Injury Awards Are Not Taxable

letter to the editor Lost Wages in Personal Injury Awards Are Not Taxable by Francis J. Carney, Esq. TO THE EDITORS: Mike Deamer s piece in the last Utah Trial Journal on taxation of personal injury settlements

letter to the editor Lost Wages in Personal Injury Awards Are Not Taxable by Francis J. Carney, Esq. TO THE EDITORS: Mike Deamer s piece in the last Utah Trial Journal on taxation of personal injury settlements

Attachment S - Payroll End-to-End Processing Requirements

Instructions: Complete the spreadsheet by indicating how your proposed solution meets the requirements listed below by placing an "X" in the appropriate column. Include comments or alternatives that may

Instructions: Complete the spreadsheet by indicating how your proposed solution meets the requirements listed below by placing an "X" in the appropriate column. Include comments or alternatives that may

Office of Bar Counsel 525 West Jefferson P. O. Box 895 Boise, Idaho 83701 (208) 334-4500 Fax: (208) 334-2764 www.isb.idaho.gov

334-4500 Fax: (208) 334-2764 www.isb.idaho.gov") Office of Bar Counsel 525 West Jefferson P. O. Box 895 Boise, Idaho 83701 (208) 334-4500 Fax: (208) 334-2764 www.isb.idaho.gov CLIENT ASSISTANCE FUND CLAIM FORM GENERAL INFORMATION AND INSTRUCTIONS Under

Office of Bar Counsel 525 West Jefferson P. O. Box 895 Boise, Idaho 83701 (208) 334-4500 Fax: (208) 334-2764 www.isb.idaho.gov CLIENT ASSISTANCE FUND CLAIM FORM GENERAL INFORMATION AND INSTRUCTIONS Under

Structured Attorney s Fees

STRUCTURED SETTLEMENTS Structured Attorney s Fees Preparing for Your Financial Future 6/15 26169-15A Table of Contents Managing Your Retirement... 2 The Power of Tax Deferral... 3 Structured Attorney s

STRUCTURED SETTLEMENTS Structured Attorney s Fees Preparing for Your Financial Future 6/15 26169-15A Table of Contents Managing Your Retirement... 2 The Power of Tax Deferral... 3 Structured Attorney s

CLAIM FORM AND INSTRUCTIONS FOR THE ANTHEM SETTLEMENT FUND CLAIM FORM INSTRUCTIONS

CLAIM FORM AND INSTRUCTIONS FOR THE ANTHEM SETTLEMENT FUND CLAIM FORM INSTRUCTIONS IT IS VERY IMPORTANT THAT YOU READ THE ENCLOSED NOTICE OF PROPOSED SETTLEMENT IN ORDER TO FULLY UNDERSTAND YOUR RIGHTS

CLAIM FORM AND INSTRUCTIONS FOR THE ANTHEM SETTLEMENT FUND CLAIM FORM INSTRUCTIONS IT IS VERY IMPORTANT THAT YOU READ THE ENCLOSED NOTICE OF PROPOSED SETTLEMENT IN ORDER TO FULLY UNDERSTAND YOUR RIGHTS

Chapter 32a Medical Care Savings Account Act

Chapter 32a Medical Care Savings Account Act 31A-32a-101 Title and scope. (1) This chapter is known as the "Medical Care Savings Account Act." (a) This chapter applies only to a medical care savings account

Chapter 32a Medical Care Savings Account Act 31A-32a-101 Title and scope. (1) This chapter is known as the "Medical Care Savings Account Act." (a) This chapter applies only to a medical care savings account

AN ACT RELATING TO LABOR AND EMPLOYMENT; AMENDING THE MINIMUM WAGE ACT TO CREATE A PREFERENCE FOR CIVIL ACTIONS AND APPEALS

AN ACT RELATING TO LABOR AND EMPLOYMENT; AMENDING THE MINIMUM WAGE ACT TO CREATE A PREFERENCE FOR CIVIL ACTIONS AND APPEALS BROUGHT TO COLLECT UNPAID OR UNDERPAID WAGES TO BE HEARD BY THE COURT TO THE

AN ACT RELATING TO LABOR AND EMPLOYMENT; AMENDING THE MINIMUM WAGE ACT TO CREATE A PREFERENCE FOR CIVIL ACTIONS AND APPEALS BROUGHT TO COLLECT UNPAID OR UNDERPAID WAGES TO BE HEARD BY THE COURT TO THE

Death Benefit Distribution Claim Form Non-Spousal Beneficiary

Death Benefit Distribution Claim Form Non-Spousal Beneficiary READ THE ATTACHED IRS SPECIAL TAX NOTICE: IF THE PLAN ALLOWS FOR AN ANNUITY OPTION, READ THE WRITTEN EXPLANATION OF QUALIFIED JOINT AND 50%

Death Benefit Distribution Claim Form Non-Spousal Beneficiary READ THE ATTACHED IRS SPECIAL TAX NOTICE: IF THE PLAN ALLOWS FOR AN ANNUITY OPTION, READ THE WRITTEN EXPLANATION OF QUALIFIED JOINT AND 50%

Filing Your Tax Forms After an Exercise of Incentive Stock Options (ISOs)

") Filing Your Tax Forms After an Exercise of Incentive Stock Options (ISOs) As someone who has been granted Incentive Stock Options (ISOs), you should understand the tax consequences when you exercise the

Filing Your Tax Forms After an Exercise of Incentive Stock Options (ISOs) As someone who has been granted Incentive Stock Options (ISOs), you should understand the tax consequences when you exercise the

IMPORTANT CALENDAR YEAR 2015 TAX RETURN GUIDE

IMPORTANT CALENDAR YEAR 2015 TAX RETURN GUIDE MESABI TRUST Deutsche Bank Trust Company Americas, Corporate Trustee c/o DB Services America, Inc. Attn: Tax Operations 5022 Gate Parkway, Suite 200 Jacksonville,

IMPORTANT CALENDAR YEAR 2015 TAX RETURN GUIDE MESABI TRUST Deutsche Bank Trust Company Americas, Corporate Trustee c/o DB Services America, Inc. Attn: Tax Operations 5022 Gate Parkway, Suite 200 Jacksonville,

Tips on Completing Form 1099 Misc

Certified Public Accountants Medical Dental Practice Consultants Tips on Completing Form 1099 Misc Who Must File Form 1099 Misc Form 1099 is used to report made to certain vendors (see list below). When

Certified Public Accountants Medical Dental Practice Consultants Tips on Completing Form 1099 Misc Who Must File Form 1099 Misc Form 1099 is used to report made to certain vendors (see list below). When

Payer's RTN (optional) 1 Interest income. $ 2 Early withdrawal penalty. $ 3 Interest on U.S. Savings Bonds and Treas. obligations

1 Interest income. $ 2 Early withdrawal penalty. $ 3 Interest on U.S. Savings Bonds and Treas. obligations") Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

PROOF OF CLAIM AND RELEASE. Address: City:

Deadline For Submission: May 27, 2005 Toll Free: PROOF OF CLAIM AND RELEASE PPI *P-PPIF-APOC/1* STATEMENT OF CLAIM: Claim Number: Control Number: WRITE ANY NAME AND ADDRESS CORRECTIONS BELOW OR IF THERE

Deadline For Submission: May 27, 2005 Toll Free: PROOF OF CLAIM AND RELEASE PPI *P-PPIF-APOC/1* STATEMENT OF CLAIM: Claim Number: Control Number: WRITE ANY NAME AND ADDRESS CORRECTIONS BELOW OR IF THERE

Volume No. 1 Policies & Procedures TOPIC NO. 20319 Function No. 20000 General Accounting TOPIC ELECTRONIC FEDERAL TAX PAYMENTS PROCESSING

Table of Contents Overview... 3 Introduction to EFTPS... 3 Tax Reporting Entity... 3 Policy... 3 To Enroll in EFTPS... 3 Tax Payment Frequency... 4 IRS Penalty... 4 Payment Procedures--Form 941, Employer's

Table of Contents Overview... 3 Introduction to EFTPS... 3 Tax Reporting Entity... 3 Policy... 3 To Enroll in EFTPS... 3 Tax Payment Frequency... 4 IRS Penalty... 4 Payment Procedures--Form 941, Employer's

Instructions: Lines 1 through 21, on pages 1 and 2

Instructions: Lines 1 through 21, on pages 1 and 2 This form is to be used by individuals who receive income reported on Federal Forms W-2, W- 2G, Form 5754, 1099-MISC, and/or Federal Schedules C, E, F

Instructions: Lines 1 through 21, on pages 1 and 2 This form is to be used by individuals who receive income reported on Federal Forms W-2, W- 2G, Form 5754, 1099-MISC, and/or Federal Schedules C, E, F

STATE OF WYOMING WOLFS-109a Vendor Form

STATE OF WYOMING WOLFS-109a Vendor Form The State of Wyoming must have a properly completed form before payment will be made. PLEASE RETURN THIS FORM TO STATE AGENCY CONTACT VENDOR IS DOING BUSINESS WITH

STATE OF WYOMING WOLFS-109a Vendor Form The State of Wyoming must have a properly completed form before payment will be made. PLEASE RETURN THIS FORM TO STATE AGENCY CONTACT VENDOR IS DOING BUSINESS WITH

Computershare Investment Plan

Computershare Investment Plan A Direct Stock Purchase and Dividend Reinvestment Plan for Harley-Davidson, Inc. Common Stock For investors in This plan is sponsored and administered by Computershare Trust

Computershare Investment Plan A Direct Stock Purchase and Dividend Reinvestment Plan for Harley-Davidson, Inc. Common Stock For investors in This plan is sponsored and administered by Computershare Trust

BU Law Grammar Tool Kit

BU Law Grammar Tool Kit A note about this revision In order to align BU Law s communications with that of the overall style of Boston University, the School has made several changes to the accepted grammar,

BU Law Grammar Tool Kit A note about this revision In order to align BU Law s communications with that of the overall style of Boston University, the School has made several changes to the accepted grammar,

Freedman v. Weatherford International Ltd., et al. c/o GCG P.O. Box 10177 Dublin, OH 43017-3177 1-855-382-6459 PROOF OF CLAIM AND RELEASE

Must be Postmarked or Received No Later Than December 9, 2015 Freedman v Weatherford International Ltd, et al c/o GCG PO Box 10177 Dublin, OH 43017-3177 1-855-382-6459 WFR *P-WFR-POC/1* Claim Number: Control

Must be Postmarked or Received No Later Than December 9, 2015 Freedman v Weatherford International Ltd, et al c/o GCG PO Box 10177 Dublin, OH 43017-3177 1-855-382-6459 WFR *P-WFR-POC/1* Claim Number: Control

PROOF OF CLAIM AND RELEASE

DYP Securities Litigation 600 N. Jackson St., Ste. 3 Tel.: 866-274-4004 Fax: 610-565-7985 info@strategicclaims.net PROOF OF CLAIM AND RELEASE Deadline for Submission: October 9, 2013 IF YOU PURCHASED OR

DYP Securities Litigation 600 N. Jackson St., Ste. 3 Tel.: 866-274-4004 Fax: 610-565-7985 info@strategicclaims.net PROOF OF CLAIM AND RELEASE Deadline for Submission: October 9, 2013 IF YOU PURCHASED OR

Attention: See IRS Publications 1141, 1167, 1179 and other IRS resources for information about printing these tax forms.

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Wage Garnishments, Levies, And Child Support Withholding

Page 1 Wage Garnishments, Levies, And Child Support Withholding All Wage Garnishments, Levies, and Child Support Withholding Orders are processed by University Payroll Services. Do not accept any Withholding

Page 1 Wage Garnishments, Levies, And Child Support Withholding All Wage Garnishments, Levies, and Child Support Withholding Orders are processed by University Payroll Services. Do not accept any Withholding

FAQs on Cost-Basis Reporting for Brokers

FAQs on Cost-Basis Reporting for Brokers The IRS published a list of Frequently Asked Questions on the new expanded tax reporting requirement for brokers which include reporting their customer s tax basis

FAQs on Cost-Basis Reporting for Brokers The IRS published a list of Frequently Asked Questions on the new expanded tax reporting requirement for brokers which include reporting their customer s tax basis

I.R.C. 6501(c)(9) Exception to Statute of Limitations

(9) Exception to Statute of Limitations") Office of Chief Counsel Internal Revenue Service Memorandum Number: 20152201F Release Date: 5/29/2015 CC:SB:3:JAX:2:POSTF-106146-15 PTMcCary Via Electronic Mail Date: 03/13/2015 To: From: Miliene McCutcheon

Office of Chief Counsel Internal Revenue Service Memorandum Number: 20152201F Release Date: 5/29/2015 CC:SB:3:JAX:2:POSTF-106146-15 PTMcCary Via Electronic Mail Date: 03/13/2015 To: From: Miliene McCutcheon

Employer-Sponsored Coverage Reporting Requirements

Under ACA rules, all employers that offer self-insured health plans must report new, detailed information on every individual covered under their health plan. There are reporting requirements for self-insured

Under ACA rules, all employers that offer self-insured health plans must report new, detailed information on every individual covered under their health plan. There are reporting requirements for self-insured

Computershare Investment Plan

Computershare Investment Plan A Dividend Reinvestment Plan for Registered Shareholders of Abbott Laboratories Common Stock This plan is sponsored and administered by Computershare Trust Company, N.A. Not

Computershare Investment Plan A Dividend Reinvestment Plan for Registered Shareholders of Abbott Laboratories Common Stock This plan is sponsored and administered by Computershare Trust Company, N.A. Not

PART ONE PRACTICE AND PROCEDURE (60 minutes)

") PART ONE PRACTICE AND PROCEDURE (60 minutes) ANSWER THE QUESTIONS IN THIS PART OF THE EXAMINATION IN ANSWER BOOK/S SEPARATE FROM THE ANSWER BOOK/S CONTAINING ANSWERS TO OTHER PARTS OF THE EXAMINATION Question

PART ONE PRACTICE AND PROCEDURE (60 minutes) ANSWER THE QUESTIONS IN THIS PART OF THE EXAMINATION IN ANSWER BOOK/S SEPARATE FROM THE ANSWER BOOK/S CONTAINING ANSWERS TO OTHER PARTS OF THE EXAMINATION Question

Exempt Organizations Summary & Comments regarding the New Form 990

Exempt Organizations Summary & Comments regarding the New Form 990 The Internal Revenue Service has released a draft of the revised Form 990, annual tax return for non profit organizations. The purpose

Exempt Organizations Summary & Comments regarding the New Form 990 The Internal Revenue Service has released a draft of the revised Form 990, annual tax return for non profit organizations. The purpose

W-9/1099 Misc Instructions for QuickBooks

W-9/1099 Misc Instructions for QuickBooks I. 1099 Misc forms are given to individuals or companies that provide a service to you as a nonemployee or whom you pay rent to. Examples are accounting/bookkeeping,

W-9/1099 Misc Instructions for QuickBooks I. 1099 Misc forms are given to individuals or companies that provide a service to you as a nonemployee or whom you pay rent to. Examples are accounting/bookkeeping,

Computershare Investment Plan

Computershare Investment Plan A Direct Stock Purchase and Dividend Reinvestment Plan for Frontier Communications Corporation Common Stock For investors in This plan is sponsored and administered by Computershare

Computershare Investment Plan A Direct Stock Purchase and Dividend Reinvestment Plan for Frontier Communications Corporation Common Stock For investors in This plan is sponsored and administered by Computershare

1 of 5 11/21/2006 2:25 PM

1 of 5 11/21/2006 2:25 PM Internal Revenue Bulletin: 2006-40 October 2, 2006 Notice 2006-83 Individual Chapter 11 Debtors Table of Contents Section 1. PURPOSE Section 2. BACKGROUND AND GENERAL LEGAL PRINCIPLES

1 of 5 11/21/2006 2:25 PM Internal Revenue Bulletin: 2006-40 October 2, 2006 Notice 2006-83 Individual Chapter 11 Debtors Table of Contents Section 1. PURPOSE Section 2. BACKGROUND AND GENERAL LEGAL PRINCIPLES

CONTRACTOR APPLICATION HOUSING REHABILITATION PROGRAM

CITY OF GALVESTON GRANTS & HOUSING DEPARTMENT P.O. Box 779 Galveston, Texas 77553 Office (409) 797 3820 Fax (409) 797 3888 CONTRACTOR APPLICATION HOUSING REHABILITATION PROGRAM CONTRACTOR APPLICATION HOUSING

CITY OF GALVESTON GRANTS & HOUSING DEPARTMENT P.O. Box 779 Galveston, Texas 77553 Office (409) 797 3820 Fax (409) 797 3888 CONTRACTOR APPLICATION HOUSING REHABILITATION PROGRAM CONTRACTOR APPLICATION HOUSING

Goldstein & Guilliams PLC

Goldstein & Guilliams PLC Arts & Entertainment Law, Management, and Immigration www.ggartslaw.com Main: (646) 561-9886 Fax: (646) 561-9820 TAX WITHHOLDING REQUIREMENTS FOR FOREIGN GUEST ARTISTS As a general

Goldstein & Guilliams PLC Arts & Entertainment Law, Management, and Immigration www.ggartslaw.com Main: (646) 561-9886 Fax: (646) 561-9820 TAX WITHHOLDING REQUIREMENTS FOR FOREIGN GUEST ARTISTS As a general

PART 3 REPRESENTATION, PRACTICE, AND PROCEDURES. Taxpayer's ability to pay the tax (e.g., installment agreements, offer in compromise)

") PART 3 REPRESENTATION, PRACTICE, AND PROCEDURES Section 2: Representation before the IRS Part 3 Taxpayer s Financial Situation Taxpayer's ability to pay the tax (e.g., installment agreements, offer in

PART 3 REPRESENTATION, PRACTICE, AND PROCEDURES Section 2: Representation before the IRS Part 3 Taxpayer s Financial Situation Taxpayer's ability to pay the tax (e.g., installment agreements, offer in

NC CD-ROM Media Specifications for 1099 Reporting

Form DP-40 (Rev.12-2015) www.dornc.com North Carolina Department of Revenue P. O. Box 25000 Raleigh, NC 27640 (877) 252-3052 toll-free NC CD-ROM Media Specifications for 1099 Reporting Submit all information

Form DP-40 (Rev.12-2015) www.dornc.com North Carolina Department of Revenue P. O. Box 25000 Raleigh, NC 27640 (877) 252-3052 toll-free NC CD-ROM Media Specifications for 1099 Reporting Submit all information

Claims Submitted to the IRS Whistleblower Office under Section 7623. This Notice provides guidance to the public on how to file claims under Internal

Part III Administrative, Procedural, and Miscellaneous Claims Submitted to the IRS Whistleblower Office under Section 7623 Notice 2008-4 SECTION 1. PURPOSE This Notice provides guidance to the public on

Part III Administrative, Procedural, and Miscellaneous Claims Submitted to the IRS Whistleblower Office under Section 7623 Notice 2008-4 SECTION 1. PURPOSE This Notice provides guidance to the public on

Understanding Structured Settlements

ab Understanding Structured Settlements Table of Contents Financial Solutions for Unexpected Events...1 What Is a Structured Settlement? Flexible Payments...2 How Are Structured Settlements Funded?...3

ab Understanding Structured Settlements Table of Contents Financial Solutions for Unexpected Events...1 What Is a Structured Settlement? Flexible Payments...2 How Are Structured Settlements Funded?...3

Purchasing Cards and IRS Requirements. A Look at the Issues

Purchasing Cards and IRS Requirements A Look at the Issues Executive Summary Businesses that use purchasing cards must meet certain Internal Revenue Service (IRS) information reporting, withholding, and

Purchasing Cards and IRS Requirements A Look at the Issues Executive Summary Businesses that use purchasing cards must meet certain Internal Revenue Service (IRS) information reporting, withholding, and

NOTICE OF AMENDMENT TO THE DIRECT STOCK PURCHASE AND DIVIDEND REINVESTMENT PLAN SPONSORED BY COMPUTERSHARE TRUST COMPANY, N.A.

NOTICE OF AMENDMENT TO THE DIRECT STOCK PURCHASE AND DIVIDEND REINVESTMENT PLAN SPONSORED BY COMPUTERSHARE TRUST COMPANY, N.A. (the Plan ) Computershare Trust Company, N.A. is pleased to inform you that

NOTICE OF AMENDMENT TO THE DIRECT STOCK PURCHASE AND DIVIDEND REINVESTMENT PLAN SPONSORED BY COMPUTERSHARE TRUST COMPANY, N.A. (the Plan ) Computershare Trust Company, N.A. is pleased to inform you that

In connection with your investment at Lending Club, you may receive a Consolidated 1099 Package for 2015 containing certain tax forms.

Introduction In connection with your investment at Lending Club, you may receive a Consolidated 1099 Package for 2015 containing certain tax forms. This Tax Guide is designed to provide general information

Introduction In connection with your investment at Lending Club, you may receive a Consolidated 1099 Package for 2015 containing certain tax forms. This Tax Guide is designed to provide general information

Tax Information and Legal Matters

Tax Information and Legal Matters This section covers tax information and legal matters that affect your benefits. Income Tax Withholding Under federal and California law, CalSTRS will withhold income

Tax Information and Legal Matters This section covers tax information and legal matters that affect your benefits. Income Tax Withholding Under federal and California law, CalSTRS will withhold income