Module 2: Job-order costing

|

|

|

- Ross Ward

- 9 years ago

- Views:

Transcription

1 Module 2: Job-order costing Required reading Overview Chapter 3, pages This module introduces the distinctions between two methods of determining unit costs of production joborder costing and process costing and presents an overview of the design and operation of a job-order costing system. (Module 3 focuses on process costing.) Particular attention is given to the procedures for assigning overhead costs to units of product. The module illustrates the flow of costs through the system for a typical manufacturing company, and addresses some of the problems of overhead application. In this module, you complete the design of a worksheet to calculate cost of goods manufactured and cost of goods sold using a spreadsheet program. Assignment reminder Assignment 1 (see Module 5) is due at the end of week 5 (see Course Schedule). It is a good idea to look at it now in order to familairize yourself with the requirements as you work through Modules 2-4. Topic outline and learning objectives 2.1 Job-order costing: Overview Compute predetermined overhead rates, and explain why estimated overhead costs (rather than actual overhead costs) are used in the costing process. (Level 1) 2.2 Job-order costing: Flow of costs Prepare journal entries to record the flow of direct materials cost, direct labour cost, and manufacturing overhead cost in a job-order costing system. (Level 1) 2.3 Using pretedermined overhead rates Apply overhead cost to Work in process by use of a predetermined overhead rate. (Level 1) 2.4 Complications of overhead application Compute any balance of under- or overapplied overhead cost for a period, and prepare the journal entry needed to close the balance into the appropriate accounts. (Level 1) 2.5 Job-order costing in service companies Explain the role of job-order costing in service companies. (Level 1) 2.6 Scrap and rework Prepare journal entries to deal with scrap and rework of unacceptable production. (Level 1) 2.7 Computer illustration 2.7-1: Cost schedules Construct worksheet templates to calculate schedules of cost of goods manufactured and cost of goods sold. (Level 1) Module summary Print this module

2 2.1 Job-order costing: Overview Learning objective LEVEL 1 Compute predetermined overhead rates, and explain why estimated overhead costs (rather than actual overhead costs) are used in the costing process. (Level 1) It is important that you understand the basic differences between the job-order and process costing systems and the types of companies that would use each method. Note the following two important items from the reading for this module: Discussion of the forms used Distinction between direct and indirect materials The job cost sheet (Exhibit 3-2) becomes the inventory subledger card for work in process. Labour costs may be recorded in many different formats. Study the document used for recording direct labour (Exhibit 3-3). Consider how this recording process might be made faster, or made more accurate, if the machines used in the different tasks were connected to a computer. Note: The explanation of overhead in the text is crucial to much of the rest of the course. You should clearly understand the need for, the approach to, and the effect of using predetermined overhead rates. To consider the question of why a predetermined overhead rate is needed, ask why smoothing is desirable even though a study of financial accounting might suggest otherwise. Within a fiscal year, production can and often does fluctuate. If production volume is unusually low for a given month, the unit cost of overhead assigned to inventory would tend to be very large because some overhead costs would not decrease in proportion to the decrease in production. Because assets are future benefits and because selling price, less costs to complete and sell (net realizable value), tends to reflect this, the future benefits can be used to justify normalized (smoothed) overhead. The greater unit cost resulting from the low production and the fixed overhead costs would likely mean that a write-down of the inventory to market value (net realizable value) would be required. Smoothing by the use of a normalized overhead would prevent such fluctuations in monthly inventory costs and incomes (due to the write-downs). Sufficient accuracy in estimating would be needed for costing and marketing. Note the following equations: Predetermined overhead rate Actual activity base = Overhead charged (or applied) to work in process. Manufacturing overhead is charged to Work in process at a predetermined rate for the reasons mentioned on page 78. While the example in the textbook uses direct labour-hours as the cost driver, other appropriate cost drivers can be used to apply manufacturing overhead, such as machine-hours, beds occupied, computer time, or flight-hours.

.")

3 2.2 Job-order costing: Flow of costs Learning objective LEVEL 1 Prepare journal entries to record the flow of direct materials cost, direct labour cost, and manufacturing overhead cost in a job-order costing system. (Level 1) The Work in process account is used to capture the costs of manufacturing the products, and includes the cost of direct materials, direct labour, and manufacturing overhead. For direct materials and direct labour, actual costs are charged to Work in process. As direct labour, direct materials, and manufacturing overhead are used, they are debited to Work in process. However, actual overhead costs must still be accounted for in some manner. That is where the Manufacturing overhead account comes into play. It is called a clearing account because it is cleared or emptied on a regular basis. The debit side of the Manufacturing overhead clearing account captures the actual cost of the various types of manufacturing overhead. These costs are, in turn, charged to specific jobs so the credit will clear the account, eventually bringing costs forward to Finished goods. Activity Job costing: The flow of costs This activity introduces you to the flow of costs in a manufacturing environment. Because it is important to work through from start to finish, allow minutes to complete the activity.

4 2.3 Using predetermined overhead rates Learning objective LEVEL 1 Apply overhead cost to Work in process by use of a predetermined overhead rate. (Level 1) The manufacturing overhead clearing account is cleared to Work in process and charged to specific jobs based on predetermined overhead rates. This system of charging overhead out at a predetermined overhead rate is called a "normal costing system." Ideally, the amount charged to specific jobs in this entry will equal the actual costs incurred. If so, the account will have a zero balance it will have been cleared. Topic 2.4 will describe how to clear any remaining balance if the amount charged to specific jobs in the above entry does not equal the actual costs incurred. Observe in Exhibit 3-11 how the Schedule of Cost of Goods Manufactured handles predetermined overhead. "Actual" overhead of $95,000 is charged by first "applying" $90,000 and then adjusting for "Underapplied overhead" of $5,000 (the difference between actual and applied overhead) to Cost of goods sold. If overhead had been overapplied, the difference would be subtracted from Cost of goods sold. Activity Overhead application and journal entries Work through this activity to reinforce your understanding of the cost flows for a manufacturing concern.

5 2.4 Complications of overhead application Learning objective LEVEL 1 Compute any balance of under- or overapplied overhead cost for a period, and prepare the journal entry needed to close the balance into the appropriate accounts. (Level 1) Determining whether a variance is underapplied or overapplied is the first difficulty in overhead application. To determine the answer, relate the actual overhead to the applied overhead. If actual overhead is greater than the applied, the variance is underapplied. Overapplied overhead is the reverse. Overapplied overhead occurs when the amount of overhead applied to jobs exceeds the actual costs. The closing, or disposition, of the overhead variance to Cost of goods sold is illustrated in entry (14) on page 92. This is the required treatment for underapplied overhead. The CICA Handbook Accounting recently issued section 3031, the Canadian equivalent to International Financial Reporting Standards IAS 2. Section 3031 states that for external reporting purposes, fixed overhead costs should be allocated based on normal capacity. Normal capacity is the production that is expected to be achieved on average over a number of periods or seasons under normal circumstances. This takes into account the time it takes to maintain equipment. This means that the denominator used to determine the overhead application rate will always be based on the normal capacity of the production facility. (Anticipated actual production should only be used if it "approximates" normal capacity.) Any production less than normal capacity may result in unallocated overhead at the end of the period. According to paragraph , for external reporting purposes this overhead is expensed to Cost of goods sold for the period. The same treatment applies to overapplied overhead. However, in periods of abnormally high production the overapplied overhead should be allocated to Work in process, Finished goods and Cost of goods sold so that inventories are not measured above cost. For interim reports, the variance may be deferred. What if the plant is a fruit processor operating for only six months of the year? Proration might be suggested except that, without inventories from production, there would be nothing to prorate to. If you prepared interim statements, would you want a large loss from the underapplied overhead or would you defer the overhead on the balance sheet as a deferred charge? While no definitive answer can be given, many managers prefer to defer the overhead variance. Method for proration In periods where production is greater than normal capacity, overhead may be overapplied. This will inflate inventory costs beyond the actual manufacturing overhead incurred. In this case, to reduce the balances in these accounts you can use current period production costs in Cost of goods sold, Work-in-process inventory, and Finished-goods inventory as the basis for prorating the overapplied overhead. If the accountant can determine the exact amount of "overhead applied" in each of the inventories and the Cost of goods sold, it is slightly more accurate to use these amounts (in the same way as shown for total costs) in order to allocate the overhead variance. Overhead and total costs may not be present in exactly the same proportions in inventories and in Cost of goods sold, resulting in the increase in accuracy. In practice, materiality considerations often lead to the more simplified approach shown in the textbook. When studying the example on pages in the textbook, note that the proration method of overhead will no longer be used for the handling of underapplied overhead, only for overapplied overhead in periods of abnormally high production. The equitable allocation of a single plant-wide overhead rate as compared to multiple overhead rates is an interesting point. The method of working with one is the same as working with many. Testing the effect on a variety of products would enable an accountant to determine if multiple rates are equitable.

6 2.5 Job-order costing in service companies Learning objective LEVEL 1 Explain the role of job-order costing in service companies. (Level 1) The principles of job-order costing apply equally in the service sector, where direct labour and overhead are typically the dominant costs. While the textbook does not devote a separate discussion to service companies, the review material at the end of the chapter includes problems that relate specifically to service companies. The principles of job-order costing are also applied on the international scene. However, the application of joborder costing varies from country to country depending on the needs of managers and the sophistication of the management process. (International job-order costing is non-examinable.) Chapter summary This topic marks the end of the textbook coverage of job-order costing. To ensure you understand this material and the corresponding terminology, read the summary on page 99 and work through the review problem.

7 2.6 Scrap and rework Learning objective LEVEL 1 Prepare journal entries to deal with scrap and rework of unacceptable production. (Level 1) A general problem in job costing is how to handle rejected units, rework labour, and scrap recovery. Note carefully the method shown in the following example. Example 2.6-1: Scrap and rework 1,000 units were started for Job good units were finished for Job 610. The total cost for Job 610 was $2,400. The total cost has already been recorded in Work in process. Situation A: Assuming no recovery on 60 bad units Alternative approaches: 1. Charge rejects to good units. Under this approach, Work in process for Job 610 will report the full cost of $2,400. Therefore, the actual cost of producing a good unit is $2.553, calculated as $2, or 2. Charge rejects to all jobs. Under this approach, the cost of the defective units will be charged to Manufacturing overhead and not to Job 610. The following entry will be made to remove the cost of the defective units from Work in process for Job 610: In the end, the cost of Job 610 will be reported at $2,256, that is, $2,400 $144. The unit cost for the 940 good units is $2.40. Technically, the second approach reallocates applied overhead back to actual overhead because the 60 units have an applied overhead component included in their cost. This could be avoided (if significant) by removing only the material and labour costs for the rejects and charging only these two elements in the preceding journal entry. Situation B: If scrap is recovered

8

9 2.7 Computer illustration 2.7-1: Cost schedules Learning objective LEVEL 1 Construct worksheet templates to calculate schedules of Cost of goods manufactured and Cost of goods sold. (Level 1) The following illustration uses a spreadsheet program to help us prepare these schedules. The spreadsheet demonstrates how to organize information related to Cost of goods manufactured and Cost of goods sold so that a change can be readily incorporated without redoing the actual schedules. Material provided Description A prebuilt worksheet M2P1, which you will complete. A completed solution worksheet M2P1S, to which you can compare your work. Chapter 3 (on pages 80-89) explains in detail the information required to prepare the schedules of Cost of goods manufactured and Cost of goods sold for the Rand Company. Required Complete the schedule of Cost of goods manufactured and Cost of goods sold using this procedure. Procedure: Cost schedules First familiarize yourself with the information in the textbook on Rand Company and how the various costs are calculated and recorded. Then perform the following steps: 1. Open the Excel file MA1M2P1.xls. (Before you begin working on the data files in this course, you must first download them and save them to your hard drive. Click the Data files link in the navigation pane, then follow the instructions for downloading and saving the files.) 2. Study the layout of the worksheet. Observe that cells A6 to D27 form the data table. Next examine the schedule of cost of goods manufactured, starting with row 28. Cells D51 to D55 are currently empty. 3. Study the formulas in the worksheet (for example, refer to the formula in cell C33). Pay particular attention to how the formulas in the schedule of Cost of goods manufactured reference the cells in the data table (for example, refer to the reference in cell C31). 4. Enter the missing formulas in cells D51 to D55. Do not enter numeric values in these cells. You must enter formulas that will result in the values shown in Exhibit 3-11 (page 89) of the text. 5. Enter formulas in cells D63 to D67 to complete the schedule of Cost of goods sold, which starts in row Save your completed worksheet. 7. Print a copy of your worksheet and compare it with the solution worksheet by clicking on the sheet tab M2P1S. If you do not obtain the same results, proceed to step 9; otherwise, go to step

10 Print a copy of the formulas and compare them with the formulas of the solution worksheet M2P1S. Correct any errors. 9. Assume management decided that two changes were necessary in the data table: Direct labour from $60,000 to $70,000 Depreciation from $18,000 to $15,000 Click the M2P1S sheet tab for the solution. Change the values in cells C15 and C22 to the new values. The Cost of goods manufactured (cell D55) should now show $168,000 instead of $158,000, and the adjusted Cost of goods sold (cell D67) should show $130,500 instead of $123,500. Note: According to IAS 16 paragraph 6, the systematic expensing of the original cost of physical assets over time is called depreciation.

should now show $168,000 instead of $158,000, and the adjusted Cost of goods sold (cell D67) should show $130,500 instead of")

11 Module 2 summary Job-order costing is used in organizations that offer a great variety of different products or services. One of the major issues is how to apply overhead to each order. Topic 2.1 addresses the issue by introducing the rationale of the predetermined overhead rate which is based on estimates. Topic 2.2 tracks the three basic cost components for each job. Topic 2.3 shows how to apply overhead cost to Work in process. Since the actual cost incurred during a period may differ from the overhead applied, a difference usually occurs. Topic 2.4 deals with the under or over application of overhead including how to dispose of these differences. The job-order costing method is versatile, and Topic 2.5 introduces its use in service companies. Topic 2.6 deals with how to handle flawed units in job-order systems. Topic 2.7 consists of a computer exercise that summarizes the flow of costs in a job-order system and prepares the schedules of Cost of goods manufactured and Cost of goods sold essential components of the income statement.

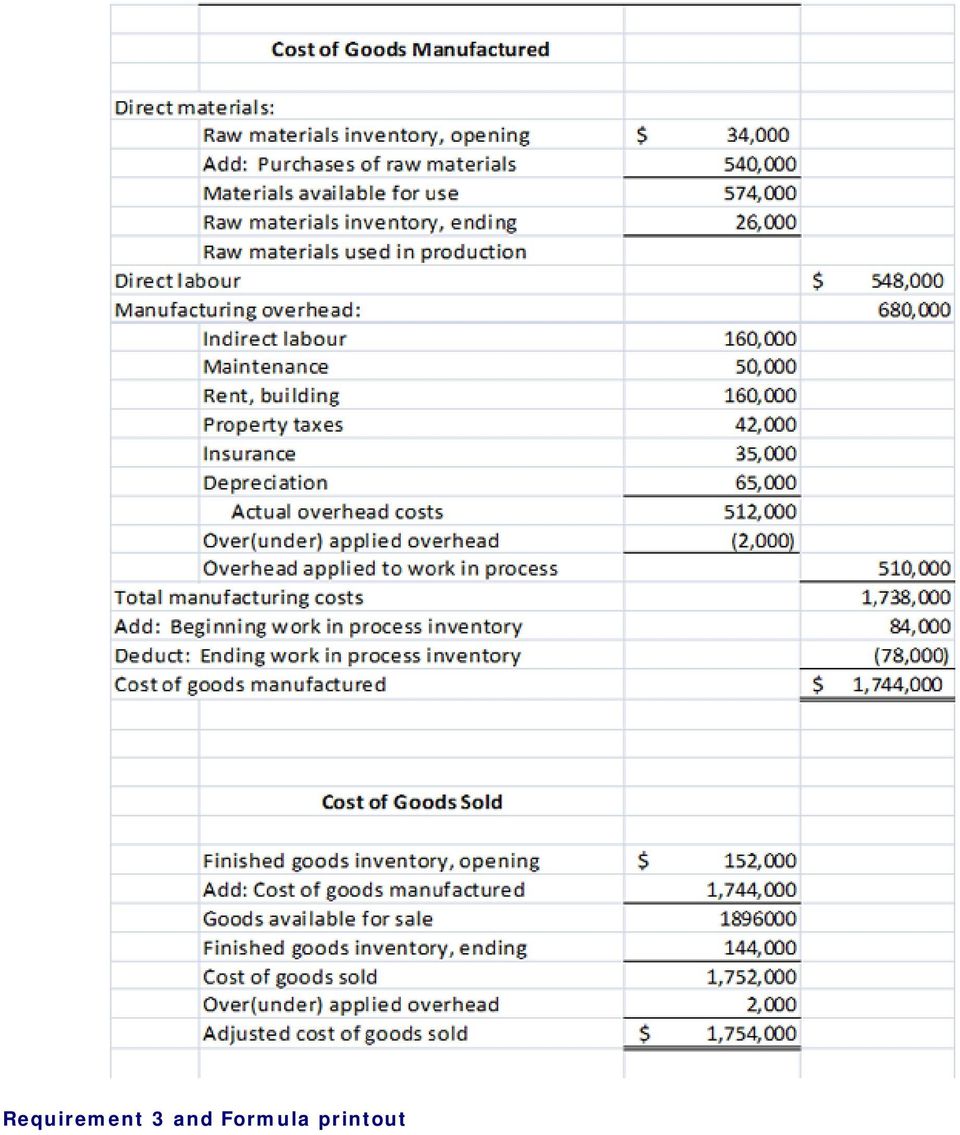

12 Module 2 self-test Question 1 Computer question Before you attempt this question, you should work through Computer illustration Description The Atlantic Manufacturing Company operates a job-order cost system and applies overhead cost to jobs on the basis of direct labour cost. In computing an overhead rate for the year, the company's estimates were: manufacturing overhead cost, $480,000; and direct labour cost, $640,000. The company's inventory accounts at the beginning and end of the year were as follows: January 1 December 31 (beginning of year) (end of year) Raw materials $34,000 $26,000 Work in process 84,000 78,000 Finished goods 152, ,000 The following actual costs were incurred during the year: Purchase of raw materials (all direct) $540,000 Direct labour cost 680,000 Manufacturing overhead costs: Insurance, factory 35,000 Depreciation of equipment 65,000 Indirect labour 160,000 Property taxes 42,000 Maintenance 50,000 Rent, building 160,000 Required Answer requirements 1, 4, and 5 manually. Use the following procedure to answer requirements 2 and a. Compute the predetermined overhead rate for the year. b. Compute the amount of under- or overapplied overhead for the year. 2. Prepare a schedule of cost of goods manufactured for the year. 3. Compute the cost of goods sold for the year. (Do not include any under- or overapplied overhead in your cost of goods sold figure.) What options are available for disposing of under- or overapplied overhead? If you choose to adjust Cost of goods sold, what would be your adjusted figure? 4. Job 189 was started and completed during the year. What price would have been charged to the customer if the job required $4,300 in materials and $6,600 in direct labour cost, and the company priced its jobs at 40% above cost to manufacture? 5. Direct labour made up $29,640 of the $78,000 ending Work in process inventory balance. Supply the information missing below: Direct materials $?

(end of year) Raw materials $34,000 $26,000 Work in process 84,000")

13 Procedure Direct labour 29,640 Manufacturing overhead? Work in process $ 78, Open the Excel file MA1M2Q1. 2. Examine the layout of the worksheet. Rows 6 to 24 form the data table and contain the data from the problem. Rows 26 to 48 contain a schedule of cost of goods manufactured and rows 52 to 60 contain a schedule of cost of goods sold. To complete requirement 2 3. Enter in cell C23 the overhead rate and in cell C24 the amount of overapplied or underapplied overhead for the year as calculated in requirement Enter in cells C29 to C32, D33, D34, C36 to C43, and D44 to D48 the appropriate formulas to complete the schedule of cost of goods manufactured. To complete requirement 3 5. Enter the formulas in column D of rows 54 to 60 to complete the schedule of cost of goods sold, and save your completed worksheet. 6. Answer the rest of requirement 3. Source: Ray H. Garrison, Eric W. Noreen, G.R. Chesley, and Raymond F. Carroll, Managerial Accounting, Sixth Canadian Edition, Problem 3-19, page 129. Copyright 2004, by McGraw-Hill Ryerson Limited. Adapted with permission. Solution Question 2 Multiple choice a. The predetermined overhead rate is $12.20 per direct-labor hour. Job 360 required 415 directlabour hours, of which 300 were incurred during October. How much overhead should be applied to Job 360 during October? 1. $1, $3, $4, $5,063 b. Production reports for the second quarter show the following data: Month Direct machine- hours Direct labour- hours Labour cost Materials cost January 18,000 24,000 $120,000 $64,000 February 24,000 20, ,000 57,000 March 20,000 18,000 88,000 90,000 Actual overhead for January, February, and March was $45,020, $60,000, and $50,100 respectively. Which variable above would be the most likely basis for allocating overhead? 1. Direct labour-hours 2. Labour cost 3. Direct machine-hours

14 4. Materials cost c. A job has been completed and has incurred $10,000 of direct material costs and $16,000 of direct labour. The customer wants to take delivery of the completed job but actual factory overhead costs will not be known until the end of the month. Which of the following should the company do? 1. Charge the customer $26,000 plus a mark-up on direct materials and direct labour. 2. Withhold the product until actual overhead costs are known. 3. Allocate overhead to job using a predetermined overhead rate. 4. Send an adjusted invoice to the customer when actual overhead costs are known. d. The following information is available for April: Job A Job B Job C Direct costs balance, April 1 $4,000 $6,400 April manufacturing costs 8,000 $3,600 Jobs A and B were finished and delivered to the clients. Job C was not completed at April 30. What was April's Cost of goods sold? 1. $3, $11, $14, $18,400 e. Job 621 is the only job remaining in Work in process at the end of June. The June 30 balance in Work in process is $24,000 of which $6,000 is direct material. Manufacturing overhead is allocated at the rate of $1.50 per $1.00 of direct labour. What is the amount of direct labour charged to Job 621? 1. $7, $10, $12, $18,000 f. When overhead is underapplied, the correct adjusting entry is which of the following? 1. Dr. Work in process and Cr. Cost of goods sold 2. Dr. Cost of goods sold and Cr. Manufacturing overhead 3. Dr. Manufacturing overhead and Cr. Cost of goods sold 4. Dr. Cost of goods sold and Cr. Work in process g. Direct labour was $90,000 and factory overhead applied on the basis of direct labour cost was $63,000. What was the predetermined overhead rate? 1. 30% 2. 43% 3. 70% % Use the following information to answer h) and i). The following is an excerpt from DellCo's accounting information system: Indirect factory materials $ 48,000 Direct manufacturing materials 114,000 Indirect office wages 14,000 Manufacturing overhead applied 182,000

15 Factory depreciation 86,000 Office depreciation 14,000 Direct office wages 32,000 Factory supervisors, salaries 36,000 Supplies, factory 7,000 h. Based on the information above, what value will be debited to the Manufacturing overhead account? 1. $177, $182, $191, $205,000 i. Based on the information above, what value will be debited to the Work in process account regarding manufacturing overhead? 1. $177, $182, $191, $205,000 j. The following data is available for the month of January: January Labour cost $232,500 Actual Manufacturing overhead $273,060 If Manufacturing overhead is applied at the rate of 120% of direct manufacturing labour costs, what would be the under- or overapplied overhead? 1. $5,940 overapplied 2. $40,560 overapplied 3. $54,612 underapplied 4. $95,172 overapplied k. The overapplied balance of manufacturing overhead is $720,000, a significant amount. The ending balances of wwork in process, Finished goods, and Cost of goods sold are $232,000, $162,400, and $185,600, respectively. Assuming that $720,000 is to be allocated to each of these accounts based on ending balances, which of the following is correct? 1. Work in process will be debited for $232, Finished goods will be credited for $201, Finished goods will be credited for $162, Cost of goods sold will be credited for $185,600. l. A $516,000 credit balance in Manufacturing overhead at the end of the period means which of the following? 1. Manufacturing overhead is $516,000 overapplied. 2. Manufacturing overhead applied is $516, Manufacturing overhead is $516,000 underapplied. 4. Actual overhead is $516,000. Solution Question 3

16 Textbook, Exercise 3-15, pages Solution Question 4 Textbook, Problem 3-30, pages Solution Question 5 Textbook, Problem 3-21, pages Solution Question 6 Textbook, Problem 3-25, pages Solution Question 7 Textbook, Question 3-2, page 104. Solution Question 8 Textbook, Question 3-18, page 105. Solution

17 Self-test 2 Solution 1 Computer solution Requirement 1 a. Estimated overhead cost Estimated direct labour cost = $480,000 $640,000 = 75% Actual manufacturing overhead costs: Indirect labour $160,000 Property taxes 42,000 Depreciation of equipment 65,000 Maintenance 50,000 Insurance 35,000 Rent, building 160,000 Total actual costs $512,000 Applied manufacturing overhead costs: $680,000 * 75% 510,000 Underapplied overhead (DR) ($2,000) Requirement 2 and Solution printout MA1: MODULE 2: QUESTION 1: requirements 2 and 3 CGA-CANADA

($2,000) Requirement 2")

18 Requirement 3 and Formula printout

19 The manufacturing overhead variance is closed to the Cost of goods sold account if the overhead is underapplied for the period. In periods of abnormally high production the overapplied overhead should be allocated to Work in process, Finished goods, and Cost of goods sold so that inventories are not measured above cost. Under- or overapplied overhead can be deferred to the Balance Sheet when interim financial statements are produced during the year or where large seasonal variations occur in output, but relatively

20 constant overhead costs exist and predetermined overhead amounts are used to smooth out fluctuations in overhead costs. Resulting significant debits or credits can be carried forward to year-end, and a final disposition of these amounts can be made using either of the other two methods discussed above. If the choice were made to adjust Cost of goods sold, the adjusted figure would be $1,754,000 Requirement 4 Direct materials $ 4,300 Direct labour 6,600 Overhead applied ($6,600 75%) 4,950 Cost to manufacture $ 15,850 $15, % = $22,190 price to the customer Requirement 5 The amount of overhead cost in ending Work in process would be: $29,640 direct labour cost 75% = $22,230 The amount of direct material cost in ending Work in process would be: Total ending Work in process $ 78,000 Deduct: Direct labour $(29,640) Manufacturing overhead 22,230 51,870 $ 26,130 The completed schedule of costs in ending Work in process would be: Direct materials $ 26,130 Direct labour 29,640 Manufacturing overhead 22,230 Total Work in process $ 78,000 Source: Ray H. Garrison, Eric W. Noreen, G.R. Chesley, and Raymond F. Carroll, Solutions Manual to accompany Managerial Accounting, Sixth Canadian Edition. Copyright 2004, by McGraw-Hill Ryerson Limited. Adapted with permission.

21 Self-test 2 Solution 2 Multiple choice a. 2) b. 3) c. 3) d. 4) e. 1) $ = $3,660 Calculating an overhead rate based on machine-hours is the most constant (about $2.50), which indicates a strong cause and effect relationship between the two costs. Using a predetermined overhead rate provides a mechanism for assigning overhead costs to jobs as they are completed. $4,000 + $6,400 + $8,000 = $18,400 cost of goods sold for April. $18,000 = 1.5x + x $18,000 = 2.5x x = $7,200 direct labour f. 2) g. 3) h. 1) When overhead is underapplied, actual overhead incurred is greater than what has been applied. Therefore, the underapplied amount, equal to the difference between actual and applied, is added or debited to Cost of goods sold and credited to the Manufacturing overhead account. $63,000 $90,000 =.70 or 70% predetermined overhead rate. The Manufacturing overhead account is debited for actual overhead costs, which include the following: Indirect factory materials $48,000 + Factory depreciation $86,000 + Factory supervisors' salaries $36,000 + Supplies, factory $7,000 = $177,000 debited to Manufacturing overhead. i. 2) j. 1) k. 2) The Work in process account is debited for applied overhead of $182,000. $232, = $279,000 applied; $279,000 $273,060 = $5,940 overapplied.

22 Work in process will be credited for a 40% share ($232,000 $580,000 = 40%) of the $720,000 = $288,000; Finished goods will be credited for a 28% share ($162,400 $580,000 = 28%) of the $720,000 = $201,600; and Cost of goods sold will be credited for a 32% share ($185,600 $580,000 = 32%) of the $720,000 = $230,400. l. 1) The balance in Manufacturing overhead at the end of the period reflects under- or overapplied overhead. A credit balance of $516,000 indicates that overhead applied was greater than actual manufacturing overhead by $516,000 (in other words, $516,000 overapplied).

23 Self-test 2 Solution 3 Exercise 3-15 Requirement 1 Milling Department: Assembly Department: Requirement 2 Overhead applied Milling Department: 90 MHs $8.50 per MH $765 Assembly Department: $ % 200 Total overhead cost applied $965 Requirement 3 Yes; if some jobs required a large amount of machine time and little labour cost, they would be charged substantially less overhead cost if a plantwide rate based on direct labour cost were being used. It appears, for example, that this would be true of job 407 which required considerable machine time to complete, but required only a small amount of labour cost. Source: Ray H. Garrison, G.R. Chesley, and Raymond F. Carroll, Solutions Manual to accompany Managerial Accounting, Eight Canadian Edition. Copyright 2010, by McGraw-Hill Ryerson Limited. Reproduced with permission.

24 Self-test 2 Solution 4 Problem 3-30 Requirement 1 1. $150,000 direct materials cost 160% = $240,000 applied.

25 2. 3. Southworth Company

26 Schedule of Cost of Goods Manufactured Direct materials: Raw materials inventory, beginning... $ 18,000 Purchases of raw materials ,000 Materials available for use ,000 Raw materials inventory, ending... 10,000 Materials used in production... $150,000 Direct labour ,000 Manufacturing overhead applied to work in process ,000 Total manufacturing cost ,000 Add: Work in process, beginning... 24, ,000 Deduct: Work in process, ending... 40,000 Cost of goods manufactured... $590, Cost of Goods Sold... 3,000 Manufacturing Overhead... 3,000 Schedule of cost of goods sold: Finished goods inventory, beginning... $ 35,000 Add: Cost of goods manufactured ,000 Goods available for sale ,000 Finished goods inventory, ending... 25,000 Unadjusted cost of goods sold ,000 Add underapplied overhead... 3,000 Adjusted cost of goods sold... $603, Southworth Company Income Statement Sales... $1,000,000 Cost of goods sold ,000 Gross margin ,000 Selling and administrative expenses: Salaries expense... $145,000 Advertising expense ,000 Depreciation expense... 5,000 Rent expense... 18,000 Miscellaneous expense... 17, ,000 Operating income... $ 82, Direct materials... $ 3,600 Direct labour (400 hours $11 per hour)... 4,400 Manufacturing overhead cost applied (160% $3,600)... 5,760 Total manufacturing cost... 13,760

27 Add markup (75% $13,760)... 10,320 Total billed price of Job $24,080 $24, units = $48.16 per unit. Source: Ray H. Garrison, G.R. Chesley, and Raymond F. Carroll, Solutions Manual to accompany Managerial Accounting, Eighth Canadian Edition. Copyright 2010, by McGraw-Hill Ryerson Limited. Reproduced with permission.

28 Self-test 2 Solution 5 Problem and Manufacturing overhead was overapplied by $3,000 for the year. This balance would be allocated

29 between Work in Process, Finished Goods, and Cost of Goods Sold in proportion to the current period costs in these accounts. The allocation would be: Work in process, 12/31... $ 21, % Finished goods, 12/ , Cost of goods sold, 12/ , $376, % Manufacturing overhead... 3,000 Work in process (5.6% $3,000)... $ 168 Finished goods (14.6% $3,000)... $ 438 Cost of goods sold (79.8% $3,000)... $2, Fantastic Props, Inc. Income Statement For the year ended December 31 Sales... $450,000 Cost of goods sold ($300,000 $2,394) ,606 Gross margin ,394 Selling and administrative expenses: Salaries expense... $75,000 Depreciation expense... 5,000 Insurance expense Shipping expense... 40, ,800 Operating income... $ 31,594 Source: Ray H. Garrison, G.R. Chesley, and Raymond F. Carroll, Solutions Manual to accompany Managerial Accounting, Eighth Canadian Edition. Copyright 2010, by McGraw-Hill Ryerson Limited. Reproduced with permission.

30 Self-test 2 Solution 6 1. Preparation Department predetermined overhead rate: 2. Fabrication Department predetermined overhead rate: 3. Preparation Department overhead applied: 350 machine-hours $5.20 per machine-hour... $1,820 Fabrication Department overhead applied: $1,200 direct materials cost 180%... 2,160 Total overhead cost... $3,980 Total cost of Job 127: Preparation Fabrication Total Direct materials... $ 940 $1,200 $2,140 Direct labour ,690 Manufacturing overhead... 1,820 2,160 3,980 Total cost... $3,470 $4,340 $7,810 Unit product cost for Job 127: 4. Preparation Fabrication Manufacturing overhead cost incurred... $390,000 $740,000 Manufacturing overhead cost applied: 73,000 machine-hours $5.20 per machine-hour ,600 $420,000 direct materials cost 180% ,000 Underapplied (or overapplied) overhead... $ 10,400 $(16,000) Source: Ray H. Garrison, G.R. Chesley, and Raymond F. Carroll, Solutions Manual to accompany Managerial Accounting, Eighth Canadian Edition. Copyright 2010, by McGraw-Hill Ryerson Limited. Reproduced with permission.

31 Self-test 2 Solution 7 Question 3-2 Job-order costing is used in situations where many different products or services that require separate costing are produced each period. Process costing is used in situations where a single, homogeneous product, such as cement, bricks, or gasoline, is produced for long periods. Source: Ray H. Garrison, G.R. Chesley, and Raymond F. Carroll, Solutions Manual to accompany Managerial Accounting, Eighth Canadian Edition. Copyright 2010, by McGraw-Hill Ryerson Limited. Reproduced with permission.

32 Self-test 2 Solution 8 Question 3-18 Yes, predetermined overhead rates in general smooth product costs when costs change during a year or where production volume varies. The predetermined overhead rate is computed by using the yearly estimated total overhead divided by the estimated base for the year. This rate is used to calculate the product cost for each period. The product cost becomes an average cost rather than an actual cost which would include the fluctuations. Source: Ray H. Garrison, G.R. Chesley, and Raymond F. Carroll, Solutions Manual to accompany Managerial Accounting, Eighth Canadian Edition. Copyright 2010, by McGraw-Hill Ryerson Limited. Reproduced with permission.

Module 3: Process costing

Module 3: Process costing Required reading Overview Chapter 4, pages 129-152 Reading 3-1: "Comparing the weighted-average and the FIFO methods of costing" Reading 3-2: "Spoilage" Module 3 helps you gain

Module 3: Process costing Required reading Overview Chapter 4, pages 129-152 Reading 3-1: "Comparing the weighted-average and the FIFO methods of costing" Reading 3-2: "Spoilage" Module 3 helps you gain

Module 4: Cost behaviour and cost-volume-profit analysis

Page 1 of 28 Module 4: Cost behaviour and cost-volume-profit analysis Required reading Chapter 5, pages 187-213 Chapter 6, pages 230-253 Appendix 6A, pages 256-258 Overview The way in which a cost responds

Page 1 of 28 Module 4: Cost behaviour and cost-volume-profit analysis Required reading Chapter 5, pages 187-213 Chapter 6, pages 230-253 Appendix 6A, pages 256-258 Overview The way in which a cost responds

n System Design Job Order Costing n What is Product Costing n Types of Product Costing n When and how to use Job-Order Costing McGraw-Hill /Irwin

2-1 Today s Lecture Management Accounting Lecture 7 (Chapter 2) Systems Design: n System Design Job Order Costing n What is Product Costing n Types of Product Costing n When and how to use n Journal entries

2-1 Today s Lecture Management Accounting Lecture 7 (Chapter 2) Systems Design: n System Design Job Order Costing n What is Product Costing n Types of Product Costing n When and how to use n Journal entries

AGENDA: JOB-ORDER COSTING

TM 3-1 AGENDA: JOB-ORDER COSTING A. The documents in a job-order costing system. 1. Materials requisition form. 2. Direct labor time ticket. 3. Job cost sheet. B. Applying overhead using a predetermined

TM 3-1 AGENDA: JOB-ORDER COSTING A. The documents in a job-order costing system. 1. Materials requisition form. 2. Direct labor time ticket. 3. Job cost sheet. B. Applying overhead using a predetermined

Quiz Chapter 3 - Solutions. 1. The manufacturing operation that would be most likely to use a job-order costing system is:

Quiz Chapter 3 - Solutions 1. The manufacturing operation that would be most likely to use a job-order costing system is: A) toy manufacturing. B) candy manufacturing. C) crude oil refining. D) shipbuilding.

Quiz Chapter 3 - Solutions 1. The manufacturing operation that would be most likely to use a job-order costing system is: A) toy manufacturing. B) candy manufacturing. C) crude oil refining. D) shipbuilding.

There are two basic types of cost accounting systems:

CHAPTER 2 JOB ORDER COSTING Managerial Accounting, Fourth Edition 2-1 Cost Accounting Systems There are two basic types of cost accounting systems: 2-2 LO 1: Explain the characteristics and purposes of

CHAPTER 2 JOB ORDER COSTING Managerial Accounting, Fourth Edition 2-1 Cost Accounting Systems There are two basic types of cost accounting systems: 2-2 LO 1: Explain the characteristics and purposes of

Module 1: Basic concepts of management accounting

Page 1 of 18 Module 1: Basic concepts of management accounting Required reading Chapter 1, pages 4-23 ERH, Section C3: "Code of ethical principles and rules of conduct" Reading 1-1: "Moral responsibility

Page 1 of 18 Module 1: Basic concepts of management accounting Required reading Chapter 1, pages 4-23 ERH, Section C3: "Code of ethical principles and rules of conduct" Reading 1-1: "Moral responsibility

CSUN GATEWAY. Managerial Accounting Study Guide

CSUN GATEWAY Managerial Accounting Study Guide Table of Contents 1. Introduction to Managerial Accounting 2. Introduction to Cost Terms and Cost Concepts 3. Allocation of Manufacturing Overhead Costs 4.

CSUN GATEWAY Managerial Accounting Study Guide Table of Contents 1. Introduction to Managerial Accounting 2. Introduction to Cost Terms and Cost Concepts 3. Allocation of Manufacturing Overhead Costs 4.

McGraw-Hill /Irwin 2-2 A company produces many units of a single product. One unit of product is indistinguishable from other units of product.

Chapter 2-1 Chapter 2 Systems Design: Job-Order Costing McGraw-Hill /Irwin The McGraw-Hill Companies, Inc., 2007 Learning Objective LO1 To distinguish between process costing and job-order costing and

Chapter 2-1 Chapter 2 Systems Design: Job-Order Costing McGraw-Hill /Irwin The McGraw-Hill Companies, Inc., 2007 Learning Objective LO1 To distinguish between process costing and job-order costing and

Exam 1 Chapters 1-3 Key

Exam 1 Chapters 1-3 Key 1. Which of the following should NOT be included as part of manufacturing overhead at a company that makes office furniture? A. Sheet steel in a file cabinet made by the company.

Exam 1 Chapters 1-3 Key 1. Which of the following should NOT be included as part of manufacturing overhead at a company that makes office furniture? A. Sheet steel in a file cabinet made by the company.

Exercise 17-1 (15 minutes)

") Exercise 17-1 (15 minutes) 1. 2002 2001 Sales... 100.0% 100.0 % Less cost of goods sold... 63.2 60.0 Gross margin... 36.8 40.0 Selling expenses... 18.0 17.5 Administrative expenses... 13.6 14.6 Total expenses...

Exercise 17-1 (15 minutes) 1. 2002 2001 Sales... 100.0% 100.0 % Less cost of goods sold... 63.2 60.0 Gross margin... 36.8 40.0 Selling expenses... 18.0 17.5 Administrative expenses... 13.6 14.6 Total expenses...

Chapter 3 Notes Page 1

Chapter 3 Notes Page 1 Job-Order System There are basically two approaches to assign manufacturing costs to products produced or services rendered: Job-Order Costing and Process Costing. The approach that

Chapter 3 Notes Page 1 Job-Order System There are basically two approaches to assign manufacturing costs to products produced or services rendered: Job-Order Costing and Process Costing. The approach that

Systems design: job-order costing

Chapter 3 Systems design: job-order costing Learning objectives LEARNING OBJECTIVE After studying Chapter 3, you should be able to: 1 Distinguish between process costing and job-order costing 2 Identify

Chapter 3 Systems design: job-order costing Learning objectives LEARNING OBJECTIVE After studying Chapter 3, you should be able to: 1 Distinguish between process costing and job-order costing 2 Identify

how to prepare a profit and loss (income) statement

statement") business builder 3 how to prepare a profit and loss (income) statement amegy bank business resource center how to prepare a profit and loss (income) statement 2 how to prepare a profit and loss (income)

business builder 3 how to prepare a profit and loss (income) statement amegy bank business resource center how to prepare a profit and loss (income) statement 2 how to prepare a profit and loss (income)

BUSINESS BUILDER 3 HOW TO PREPARE A PROFIT AND LOSS (INCOME) STATEMENT

STATEMENT") BUSINESS BUILDER 3 HOW TO PREPARE A PROFIT AND LOSS (INCOME) STATEMENT zions business resource center 2 how to prepare a profit and loss (income) statement A Profit and Loss (P&L) or income statement measures

BUSINESS BUILDER 3 HOW TO PREPARE A PROFIT AND LOSS (INCOME) STATEMENT zions business resource center 2 how to prepare a profit and loss (income) statement A Profit and Loss (P&L) or income statement measures

Lesson 5: Inventory. 5.1 Introduction. 5.2 Manufacturer or Retailer?

Lesson 5: Inventory 5.1 Introduction Whether it is a brick and mortar or digital store, for many businesses, inventory management is a key cog of their operations. Managing inventory is an important key

Lesson 5: Inventory 5.1 Introduction Whether it is a brick and mortar or digital store, for many businesses, inventory management is a key cog of their operations. Managing inventory is an important key

House Published on www.jps-dir.com

I. Cost - Volume - Profit (Break - Even) Analysis A. Definitions 1. Cost - Volume - Profit (CVP) Analysis: is a means of predicting the relationships among revenues, variable costs, and fixed costs at

I. Cost - Volume - Profit (Break - Even) Analysis A. Definitions 1. Cost - Volume - Profit (CVP) Analysis: is a means of predicting the relationships among revenues, variable costs, and fixed costs at

CHAPTER 9. Cost accounting systems CONTENTS

CHAPTER 9 Cost accounting systems CONTENTS 9.1 Job order costing and factory overhead 9.2 Job order costing 9.3 Process costing 9.4 Calculating unit costs with process costing 9.5 Cost of production reports

CHAPTER 9 Cost accounting systems CONTENTS 9.1 Job order costing and factory overhead 9.2 Job order costing 9.3 Process costing 9.4 Calculating unit costs with process costing 9.5 Cost of production reports

Gleim / Flesher CMA Review 15th Edition, 1st Printing Part 1 Updates

Page 1 of 8 Gleim / Flesher CMA Review 15th Edition, 1st Printing Part 1 Updates NOTE: Text that should be deleted from the outline is displayed as struck through with a red background. New text is shown

Page 1 of 8 Gleim / Flesher CMA Review 15th Edition, 1st Printing Part 1 Updates NOTE: Text that should be deleted from the outline is displayed as struck through with a red background. New text is shown

Principles of Cost Accounting, 16th Edition, Edward J. VanDerbeck, 2013 Cengage Learning. All Rights Reserved. May not be copied, scanned, or

Principles of Cost Accounting, 16th Edition, Edward J. VanDerbeck, 2013 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted

Principles of Cost Accounting, 16th Edition, Edward J. VanDerbeck, 2013 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted

International Accounting Standards

International Accounting Standards The Key Issues in IAS 2 and 11 Background In this second of my series on international accounting standards, I have chosen to look at the two standards covering the topic

International Accounting Standards The Key Issues in IAS 2 and 11 Background In this second of my series on international accounting standards, I have chosen to look at the two standards covering the topic

Pool Canvas. Question 1 Multiple Choice 0 points Modify Remove. Question 2 Multiple Choice 0 points Modify Remove

Page 1 of 21 TEST BANK > CONTROL PANEL > POOL MANAGER > POOL CANVAS Pool Canvas Add, modify, and remove questions. Select a question type from the Add Question drop-down list and click Go to add questions.

Page 1 of 21 TEST BANK > CONTROL PANEL > POOL MANAGER > POOL CANVAS Pool Canvas Add, modify, and remove questions. Select a question type from the Add Question drop-down list and click Go to add questions.

DRAFT. Accounting for a Merchandising Business. SECTION 10.1 REVIEW QUESTIONS (page 401) 1. 5. 6. 7. 8. 10. 11. 12. 13. 14. 15. 16. 17.

1. 5. 6. 7. 8. 10. 11. 12. 13. 14. 15. 16. 17.") CHAPTER 10 Accounting for a Merchandising Business SECTION 10.1 REVIEW QUESTIONS (page 401) 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 324 Accounting 1 Student Workbook Copyright 2013 Pearson

CHAPTER 10 Accounting for a Merchandising Business SECTION 10.1 REVIEW QUESTIONS (page 401) 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 324 Accounting 1 Student Workbook Copyright 2013 Pearson

Blended Value Business Plan Pro Forma Income Statement User Guide

Blended Value Business Plan Pro Forma Income Statement User Guide OVERVIEW A business plan goes beyond the forecasting of a Feasibility Study. It provides details on the multiple factors required to develop

Blended Value Business Plan Pro Forma Income Statement User Guide OVERVIEW A business plan goes beyond the forecasting of a Feasibility Study. It provides details on the multiple factors required to develop

International Accounting Standard 2 Inventories

International Accounting Standard 2 Inventories Objective 1 The objective of this Standard is to prescribe the accounting treatment for inventories. A primary issue in accounting for inventories is the

International Accounting Standard 2 Inventories Objective 1 The objective of this Standard is to prescribe the accounting treatment for inventories. A primary issue in accounting for inventories is the

VOLUME 4, CHAPTER 20: JOB ORDER COST ACCOUNTING SUMMARY OF MAJOR CHANGES. All changes are denoted by blue font.

VOLUME 4, CHAPTER 20: JOB ORDER COST ACCOUNTING SUMMARY OF MAJOR CHANGES All changes are denoted by blue font. Substantive revisions are denoted by a * preceding the section, paragraph, table, or figure

VOLUME 4, CHAPTER 20: JOB ORDER COST ACCOUNTING SUMMARY OF MAJOR CHANGES All changes are denoted by blue font. Substantive revisions are denoted by a * preceding the section, paragraph, table, or figure

NEPAL ACCOUNTING STANDARDS ON INVENTORIES CONTENTS Paragraphs

NAS 04 NEPAL ACCOUNTING STANDARDS ON INVENTORIES CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9-32 Cost of inventories 10-21 Costs of purchase 11 Costs of conversion

NAS 04 NEPAL ACCOUNTING STANDARDS ON INVENTORIES CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9-32 Cost of inventories 10-21 Costs of purchase 11 Costs of conversion

Job Costing. Product Costing Systems PART I INTRODUCTION TO COST MANAGEMENT. After studying this chapter, you should be able to...

Cost : A C H A P T E R F O U R PART I INTRODUCTION TO COST MANAGEMENT Job Costing After studying this chapter, you should be able to.... Explain the types of costing systems. Explain the strategic role

Cost : A C H A P T E R F O U R PART I INTRODUCTION TO COST MANAGEMENT Job Costing After studying this chapter, you should be able to.... Explain the types of costing systems. Explain the strategic role

Module 1: Basic concepts of management accounting

Module 1: Basic concepts of management accounting Required reading Chapter 1, pages 4-23 ERH, Section C3: "Code of ethical principles and rules of conduct" Reading 1-1: "Moral responsibility within the

Module 1: Basic concepts of management accounting Required reading Chapter 1, pages 4-23 ERH, Section C3: "Code of ethical principles and rules of conduct" Reading 1-1: "Moral responsibility within the

Job-order Costing; T-Accounts; Income Statement

JOB-ORDER COSTING 1 Job-order Costing; T-Accounts; Income Statement Gold Nest Company is a family-owned enterprise that makes birdcages in Chinatown. A popular pastime among older Chinese men is to take

JOB-ORDER COSTING 1 Job-order Costing; T-Accounts; Income Statement Gold Nest Company is a family-owned enterprise that makes birdcages in Chinatown. A popular pastime among older Chinese men is to take

This is How Are Operating Budgets Created?, chapter 9 from the book Accounting for Managers (index.html) (v. 1.0).

(v. 1.0).") This is How Are Operating Budgets Created?, chapter 9 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

This is How Are Operating Budgets Created?, chapter 9 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

Financial Statements for Manufacturing Businesses

Management Accounting 31 Financial Statements for Manufacturing Businesses Importance of Financial Statements Accounting plays a critical role in decision-making. Accounting provides the financial framework

Management Accounting 31 Financial Statements for Manufacturing Businesses Importance of Financial Statements Accounting plays a critical role in decision-making. Accounting provides the financial framework

Chapter 4. Systems Design: Process Costing. Types of Costing Systems Used to Determine Product Costs

4-1 Types of Systems Used to Determine Product Costs Chapter 4 Process Job-order Systems Design: Many units of a single, homogeneous product flow evenly through a continuous production process. One unit

4-1 Types of Systems Used to Determine Product Costs Chapter 4 Process Job-order Systems Design: Many units of a single, homogeneous product flow evenly through a continuous production process. One unit

Valuation of Inventories

8 Accounting Standard (AS) 2 Valuation of Inventories Contents OBJECTIVE SCOPE Paragraphs 1-2 DEFINITIONS 3-4 MEASUREMENT OF INVENTORIES 5-25 Cost of Inventories 6-13 Costs of Purchase 7 Costs of Conversion

8 Accounting Standard (AS) 2 Valuation of Inventories Contents OBJECTIVE SCOPE Paragraphs 1-2 DEFINITIONS 3-4 MEASUREMENT OF INVENTORIES 5-25 Cost of Inventories 6-13 Costs of Purchase 7 Costs of Conversion

Planning your cash flow

Planning your cash flow Business Coach series Preparing the cash flow forecast Keeping on track Business Coach series The cash flow process The situation Money goes out earlier and faster than it comes

Planning your cash flow Business Coach series Preparing the cash flow forecast Keeping on track Business Coach series The cash flow process The situation Money goes out earlier and faster than it comes

1. Managerial accounting: A. is governed by generally accepted accounting principles. B. places emphasis on special-purpose information.

1. Managerial accounting: A. is governed by generally accepted accounting principles. B. places emphasis on special-purpose information. C. pertains to the entity as a whole and is highly aggregated. D.

1. Managerial accounting: A. is governed by generally accepted accounting principles. B. places emphasis on special-purpose information. C. pertains to the entity as a whole and is highly aggregated. D.

Society of Certified Management Accountants of Sri Lanka

Copyright Reserved Serial No Technician Stage March 2009 Examination Examination Date : 28 th March 2009 Number of Pages : 06 Examination Time: 9.30a:m.- 12.30p:m. Number of Questions: 05 Instructions

Copyright Reserved Serial No Technician Stage March 2009 Examination Examination Date : 28 th March 2009 Number of Pages : 06 Examination Time: 9.30a:m.- 12.30p:m. Number of Questions: 05 Instructions

REVIEW FOR EXAM NO. 1, ACCT-2302 (SAC) (Chapters 16-18)

(Chapters 16-18)") A. Chapter 16 (Managerial Accounting). 1. Purposes and Principles. (Page 956) REVIEW FOR EXAM NO. 1, ACCT-2302 (SAC) (Chapters 16-18) a. Provides economic/financial information (both historical and estimated)

A. Chapter 16 (Managerial Accounting). 1. Purposes and Principles. (Page 956) REVIEW FOR EXAM NO. 1, ACCT-2302 (SAC) (Chapters 16-18) a. Provides economic/financial information (both historical and estimated)

(b) financial instruments (Ind AS 32, Financial Instruments: Presentation and Ind AS 109, Financial Instruments and ); and

financial instruments (Ind AS 32, Financial Instruments: Presentation and Ind AS 109, Financial Instruments and ); and") Indian Accounting Standard (Ind AS) 2 Inventories (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold italic type indicate

Indian Accounting Standard (Ind AS) 2 Inventories (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold italic type indicate

STUDENT NAME: STUDENT ID:

MIDTERM EXAM AFM 102: Introduction to Managerial Accounting Sections 001, 002, 003 and 004 February 29, 2008: 4:30 6:00 PM Instructors: Rob Ducharme; Thomas Vance STUDENT NAME: STUDENT ID: TUTORIAL: Room:

MIDTERM EXAM AFM 102: Introduction to Managerial Accounting Sections 001, 002, 003 and 004 February 29, 2008: 4:30 6:00 PM Instructors: Rob Ducharme; Thomas Vance STUDENT NAME: STUDENT ID: TUTORIAL: Room:

UG802: COST MEASUREMENT AND COST ANALYSIS

UG802: COST MEASUREMENT AND COST ANALYSIS April 6, 2014 Kanokporn Rienkhemaniyom, Ph.D. Managerial Accounting - Overview Definition: A profession that involves partnering in management decision making,

UG802: COST MEASUREMENT AND COST ANALYSIS April 6, 2014 Kanokporn Rienkhemaniyom, Ph.D. Managerial Accounting - Overview Definition: A profession that involves partnering in management decision making,

29.1 COST SHEET : MEANING AND ITS IMPORTANCE

29 COST SHEET You are running a factory which manufactures electronic toys. You incur expenses on raw material, labour and other expenses which can be directly attibuted to cost and which cannot be directly

29 COST SHEET You are running a factory which manufactures electronic toys. You incur expenses on raw material, labour and other expenses which can be directly attibuted to cost and which cannot be directly

Indian Accounting Standard (Ind AS) 2 Inventories. Cost of agricultural produce harvested from biological assets 20

2 Inventories. Cost of agricultural produce harvested from biological assets 20") Contents OBJECTIVE Indian Accounting Standard (Ind AS) 2 Inventories Paragraphs 1 SCOPE 2-5 DEFINITIONS 6-8 MEASUREMENT OF INVENTORIES Cost of inventories 10-22 Costs of purchase Costs of conversion Other

Contents OBJECTIVE Indian Accounting Standard (Ind AS) 2 Inventories Paragraphs 1 SCOPE 2-5 DEFINITIONS 6-8 MEASUREMENT OF INVENTORIES Cost of inventories 10-22 Costs of purchase Costs of conversion Other

COST CLASSIFICATION AND COST BEHAVIOR INTRODUCTION

COST CLASSIFICATION AND COST BEHAVIOR INTRODUCTION LESSON# 1 Cost Accounting Cost Accounting is an expanded phase of financial accounting which provides management promptly with the cost of producing and/or

COST CLASSIFICATION AND COST BEHAVIOR INTRODUCTION LESSON# 1 Cost Accounting Cost Accounting is an expanded phase of financial accounting which provides management promptly with the cost of producing and/or

CASH FLOW STATEMENT & BALANCE SHEET GUIDE

CASH FLOW STATEMENT & BALANCE SHEET GUIDE The Agriculture Development Council requires the submission of a cash flow statement and balance sheet that provide annual financial projections for the business

CASH FLOW STATEMENT & BALANCE SHEET GUIDE The Agriculture Development Council requires the submission of a cash flow statement and balance sheet that provide annual financial projections for the business

SHEET 1: CASH FLOW PROJECTED

Blended Value Business Plan Cash Flow Forecast User Guide OVERVIEW The Cash Flow Forecast is the listing of the sources and expenditures of cash plus the timing of when the cash is moving in and out of

Blended Value Business Plan Cash Flow Forecast User Guide OVERVIEW The Cash Flow Forecast is the listing of the sources and expenditures of cash plus the timing of when the cash is moving in and out of

MODULE 7: FINANCIAL REPORTING AND ANALYSIS

MODULE 7: FINANCIAL REPORTING AND ANALYSIS Module Overview Businesses running ERP systems capture lots of data through daily activity. This data, which reflects such things as the organization's sales

MODULE 7: FINANCIAL REPORTING AND ANALYSIS Module Overview Businesses running ERP systems capture lots of data through daily activity. This data, which reflects such things as the organization's sales

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY. True-False Statements

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 K 17. 4

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 K 17. 4

Module 6: Transfer pricing

Page 1 of 18 Module 6: Transfer pricing Overview Module 6 focuses on decentralization and the impact of transfer pricing on decision making and costs within organizations. The self-test for the module

Page 1 of 18 Module 6: Transfer pricing Overview Module 6 focuses on decentralization and the impact of transfer pricing on decision making and costs within organizations. The self-test for the module

Intermediate Accounting

Intermediate Accounting Thomas H. Beechy Schulich School of Business, York University Joan E. D. Conrod Faculty of Management, Dalhousie University PowerPoint slides by: Bruce W. MacLean, Faculty of Management,

Intermediate Accounting Thomas H. Beechy Schulich School of Business, York University Joan E. D. Conrod Faculty of Management, Dalhousie University PowerPoint slides by: Bruce W. MacLean, Faculty of Management,

Multiple Choice Questions (45%)

") Multiple Choice Questions (45%) Choose the Correct Answer 1. The following information was taken from XYZ Company s accounting records for the year ended December 31, 2014: Increase in raw materials inventory

Multiple Choice Questions (45%) Choose the Correct Answer 1. The following information was taken from XYZ Company s accounting records for the year ended December 31, 2014: Increase in raw materials inventory

$20,000 invoice price 1,500 sales tax 500 freight 200 set-up (contractor) $22,200 total cost

$22,200 total cost") Section 2 DEPRECIATION UNDER GAAP (FOR BOOK PURPOSES) Introduction Most plant and equipment assets wear out or become obsolete over the years. Similarly, although land is not depreciated (because it does

Section 2 DEPRECIATION UNDER GAAP (FOR BOOK PURPOSES) Introduction Most plant and equipment assets wear out or become obsolete over the years. Similarly, although land is not depreciated (because it does

University of Waterloo Final Examination

University of Waterloo Final Examination Term: Winter Year: 2006 Student Name UW Student ID Number Place an X by the section in which you are registered: 1 (MWF 8:30 am to 9:20 am) 2 (MWF 9:30 am to 10:20

University of Waterloo Final Examination Term: Winter Year: 2006 Student Name UW Student ID Number Place an X by the section in which you are registered: 1 (MWF 8:30 am to 9:20 am) 2 (MWF 9:30 am to 10:20

Spreadsheet User Guide. First-Year Course

Spreadsheet User Guide with Solutions First-Year Course For Use With Glencoe Accounting: Online Learning Center Bothell, WA Chicago, IL Columbus, OH New York, NY CONTENTS Section 1 Introduction 1 Section

Spreadsheet User Guide with Solutions First-Year Course For Use With Glencoe Accounting: Online Learning Center Bothell, WA Chicago, IL Columbus, OH New York, NY CONTENTS Section 1 Introduction 1 Section

Accounting for a Merchandising Business

CHAPTER 10 Accounting for a Merchandising Business SECTION 10.1 REVIEW QUESTIONS (page 401) 1. A service business sells a service to the general public but does not deal in merchandise. For example, a

CHAPTER 10 Accounting for a Merchandising Business SECTION 10.1 REVIEW QUESTIONS (page 401) 1. A service business sells a service to the general public but does not deal in merchandise. For example, a

Accounting Building Business Skills. Learning Objectives: Learning Objectives: Paul D. Kimmel. Chapter Thirteen: Cost Accounting Systems

Accounting Building Business Skills Paul D. Kimmel Chapter Thirteen: Cost Accounting Systems PowerPoint presentation by Kate Wynn-Williams University of Otago, Dunedin 2003 John Wiley & Sons Australia,

Accounting Building Business Skills Paul D. Kimmel Chapter Thirteen: Cost Accounting Systems PowerPoint presentation by Kate Wynn-Williams University of Otago, Dunedin 2003 John Wiley & Sons Australia,

JOB ORDER COST 10 SYSTEMS AND OVERHEAD ALLOCATIONS

10-1 10-2 Chapter JOB ORDER COST 10 SYSTEMS AND OVERHEAD ALLOCATIONS To explain the purposes of cost accounting systems. LO1 10-3 10-4 Cost Accounting Systems Cost Accounting Systems Determining unit manufacturing

10-1 10-2 Chapter JOB ORDER COST 10 SYSTEMS AND OVERHEAD ALLOCATIONS To explain the purposes of cost accounting systems. LO1 10-3 10-4 Cost Accounting Systems Cost Accounting Systems Determining unit manufacturing

Cost Concepts and Behavior

Chapter 2 Cost Concepts and Behavior McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives L.O. 1 Explain the basic concept of cost. L.O. 2 Explain

Chapter 2 Cost Concepts and Behavior McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives L.O. 1 Explain the basic concept of cost. L.O. 2 Explain

NON-INTEGRAL OR COST LEDGER ACCOUNTING SYSTEM

CHAPTER 7 NON-INTEGRAL OR COST LEDGER ACCOUNTING SYSTEM INTRODUCTION Just as financial accounting system is maintained with certain objectives in view, cost accounting system is often distinctively maintained

CHAPTER 7 NON-INTEGRAL OR COST LEDGER ACCOUNTING SYSTEM INTRODUCTION Just as financial accounting system is maintained with certain objectives in view, cost accounting system is often distinctively maintained

Teaching the Budgeting Process Using a Spreadsheet Template

Teaching the Budgeting Process Using a Spreadsheet Template Benoît N. Boyer, Professor of Accounting and Chair of the Accounting and Information Systems Department, Sacred Heart University, Fairfield,

Teaching the Budgeting Process Using a Spreadsheet Template Benoît N. Boyer, Professor of Accounting and Chair of the Accounting and Information Systems Department, Sacred Heart University, Fairfield,

Job Order Costing YOUR LEARNING OBJECTIVES CHAPTER

CHAPTER 2 Job Order Costing YOUR LEARNING OBJECTIVES LO 2-1 Describe the key differences between job order costing and process costing. LO 2-2 Describe the source documents used to track direct materials

CHAPTER 2 Job Order Costing YOUR LEARNING OBJECTIVES LO 2-1 Describe the key differences between job order costing and process costing. LO 2-2 Describe the source documents used to track direct materials

Breakeven Analysis. Breakeven for Services.

Dollars and Sense Introduction Your dream is to operate a profitable business and make a good living. Before you open, however, you want some indication that your business will be profitable, if not immediately

Dollars and Sense Introduction Your dream is to operate a profitable business and make a good living. Before you open, however, you want some indication that your business will be profitable, if not immediately

Introduction to Financial Accounting: Assets [FA2]

![Introduction to Financial Accounting: Assets [FA2]](/thumbs/27/11917426.jpg "Introduction to Financial Accounting: Assets [FA2]") Page 1 of 5 Introduction to Financial Accounting: Assets [FA2] Course purpose Financial Accounting: Assets [FA2] is the second of five courses on this subject in the CGA program of professional studies.

Page 1 of 5 Introduction to Financial Accounting: Assets [FA2] Course purpose Financial Accounting: Assets [FA2] is the second of five courses on this subject in the CGA program of professional studies.

Financial Accounting Fundamentals [FA1] The broad aims of the course are to provide you with a sound introduction to the

![Financial Accounting Fundamentals [FA1] The broad aims of the course are to provide you with a sound introduction to the](/thumbs/25/5605098.jpg "Financial Accounting Fundamentals [FA1] The broad aims of the course are to provide you with a sound introduction to the") Page 1 of 5 Introduction to FA1 Course description and purpose Financial Accounting Fundamentals [FA1] is the first in a sequence of five courses in financial accounting and accounting theory in the CGA

Page 1 of 5 Introduction to FA1 Course description and purpose Financial Accounting Fundamentals [FA1] is the first in a sequence of five courses in financial accounting and accounting theory in the CGA

Marginal and. this chapter covers...

7 Marginal and absorption costing this chapter covers... This chapter focuses on the costing methods of marginal and absorption costing and compares the profit made by a business under each method. The

7 Marginal and absorption costing this chapter covers... This chapter focuses on the costing methods of marginal and absorption costing and compares the profit made by a business under each method. The

Copyright 2015 Pearson Canada Inc. 1

1 Building Blocks of Managerial Accounting CHAPTER 2 2 Distinguish among service, merchandising, and manufacturing companies OBJECTIVE 1 3 Service Companies Provide an intangible service only Largest sector

1 Building Blocks of Managerial Accounting CHAPTER 2 2 Distinguish among service, merchandising, and manufacturing companies OBJECTIVE 1 3 Service Companies Provide an intangible service only Largest sector

Accounting for Manufacturing

Accounting for Manufacturing 1 Accounting for Manufacturing and Inventory Impairments TABLE OF CONTENTS Accounting for manufacturing 2 Production activities 2 Production cost flows 3 Accounting for production

Accounting for Manufacturing 1 Accounting for Manufacturing and Inventory Impairments TABLE OF CONTENTS Accounting for manufacturing 2 Production activities 2 Production cost flows 3 Accounting for production

CHAPTER 4: SET UP POSTING GROUPS

Chapter 4: Set Up Posting Groups CHAPTER 4: SET UP POSTING GROUPS Objectives Introduction The objectives are: Explain and set up specific posting groups Explain and set up general posting groups Create

Chapter 4: Set Up Posting Groups CHAPTER 4: SET UP POSTING GROUPS Objectives Introduction The objectives are: Explain and set up specific posting groups Explain and set up general posting groups Create

Instructions for E-PLAN Financial Planning Template

Instructions for E-PLAN Financial Planning Template The EPLAN template will assist you in preparing financial projections for your existing business. The template uses Microsoft Excel to prepare your projected

Instructions for E-PLAN Financial Planning Template The EPLAN template will assist you in preparing financial projections for your existing business. The template uses Microsoft Excel to prepare your projected

CHAPTER 10 In-Class QUIZ

CHAPTER 10 In-Class QUIZ 1. A mixed cost function has a constant component of $20,000. If the total cost is $60,000 and the independent variable has the value 200, what is the value of the slope coefficient?

CHAPTER 10 In-Class QUIZ 1. A mixed cost function has a constant component of $20,000. If the total cost is $60,000 and the independent variable has the value 200, what is the value of the slope coefficient?

How To Calculate A Trial Balance For A Company

THE BASIC MODEL The accounting information system is designed to collect and organize data into information that is useful for stakeholders. The Accounting Equation The basic accounting equation is what

THE BASIC MODEL The accounting information system is designed to collect and organize data into information that is useful for stakeholders. The Accounting Equation The basic accounting equation is what

Lesson FA-20-020-01a. Job Cost Accounting System Part 1a

Lesson FA-20-020-01a Job Cost Accounting System Part 1a This workbook contains notes and worksheets to accompany the corresponding video lesson available online at: Permission is granted for educators

Lesson FA-20-020-01a Job Cost Accounting System Part 1a This workbook contains notes and worksheets to accompany the corresponding video lesson available online at: Permission is granted for educators

Accounting for a Merchandising Business

Chapter 11 Accounting for a Merchandising Business ANSWERS TO SECTION 11.1 REVIEW QUESTIONS (text p. 428) The Merchandising Business 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 1. 2. 3. 4. 14. 15. Copyright

Chapter 11 Accounting for a Merchandising Business ANSWERS TO SECTION 11.1 REVIEW QUESTIONS (text p. 428) The Merchandising Business 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 1. 2. 3. 4. 14. 15. Copyright

This Chapter Addresses the Following Questions:

ch05.qxd 9/27/04 4:19 PM Page 174 CHAPTER Job Costing In Brief Custom products and services, which are produced singly or in small batches, need to be valued for financial statements, tax reporting, and

ch05.qxd 9/27/04 4:19 PM Page 174 CHAPTER Job Costing In Brief Custom products and services, which are produced singly or in small batches, need to be valued for financial statements, tax reporting, and

COST ACCOUNTING STANDARD ON OVERHEADS

COST ACCOUNTING STANDARD ON OVERHEADS The following is the text of the COST ACCOUNTING STANDARD 3 (CAS- 3) issued by the Council of the Institute of Cost and Works Accountants of India on Overheads. The

COST ACCOUNTING STANDARD ON OVERHEADS The following is the text of the COST ACCOUNTING STANDARD 3 (CAS- 3) issued by the Council of the Institute of Cost and Works Accountants of India on Overheads. The

Module 4: Accounting for merchandising activities

Course Schedule Course Modules Review and Practice Exam Preparation Resources Module 4: Accounting for merchandising activities Overview In the first three modules, you studied how to determine income

Course Schedule Course Modules Review and Practice Exam Preparation Resources Module 4: Accounting for merchandising activities Overview In the first three modules, you studied how to determine income

Concepts in Enterprise Resource Planning. Chapter 5 Accounting in ERP Systems

Concepts in Enterprise Resource Planning Chapter 5 Accounting in ERP Systems Chapter Objectives Describe the differences between financial and managerial accounting. Identify and describe problems associated

Concepts in Enterprise Resource Planning Chapter 5 Accounting in ERP Systems Chapter Objectives Describe the differences between financial and managerial accounting. Identify and describe problems associated

COST AND MANAGEMENT ACCOUNTING

EXECUTIVE PROGRAMME COST AND MANAGEMENT ACCOUNTING SAMPLE TEST PAPER (This test paper is for practice and self study only and not to be sent to the institute) Time allowed: 3 hours Maximum marks : 100

EXECUTIVE PROGRAMME COST AND MANAGEMENT ACCOUNTING SAMPLE TEST PAPER (This test paper is for practice and self study only and not to be sent to the institute) Time allowed: 3 hours Maximum marks : 100

Introduction to Financial Accounting: Assets [FA2]

![Introduction to Financial Accounting: Assets [FA2]](/thumbs/30/13982281.jpg "Introduction to Financial Accounting: Assets [FA2]") Page 1 of 6 Introduction to Financial Accounting: Assets [FA2] Course purpose Financial Accounting: Assets [FA2] is the second of five courses on this subject in the CGA program of professional studies.

Page 1 of 6 Introduction to Financial Accounting: Assets [FA2] Course purpose Financial Accounting: Assets [FA2] is the second of five courses on this subject in the CGA program of professional studies.

CONSOLIDATED STATEMENT OF INCOME

CONSOLIDATED STATEMENT OF INCOME Notes Sales 1) 5,429,574 5,169,545 Cost of Goods Sold 2) 3,041,622 2,824,771 Gross Profit 2,387,952 2,344,774 Selling Expenses 3) 1,437,010 1,381,132 General and Administrative

CONSOLIDATED STATEMENT OF INCOME Notes Sales 1) 5,429,574 5,169,545 Cost of Goods Sold 2) 3,041,622 2,824,771 Gross Profit 2,387,952 2,344,774 Selling Expenses 3) 1,437,010 1,381,132 General and Administrative

Comprehensive Business Budgeting

Management Accounting 137 Comprehensive Business Budgeting Goals and Objectives Profit planning, commonly called master budgeting or comprehensive business budgeting, is one of the more important techniques

Management Accounting 137 Comprehensive Business Budgeting Goals and Objectives Profit planning, commonly called master budgeting or comprehensive business budgeting, is one of the more important techniques

Compiled Accounting Standard AASB 102

Compiled Accounting Standard AASB 102 Inventories This compiled Standard applies to annual reporting periods beginning on or after 1 January 2009 that end on or after 30 June 2009. Early application is

Compiled Accounting Standard AASB 102 Inventories This compiled Standard applies to annual reporting periods beginning on or after 1 January 2009 that end on or after 30 June 2009. Early application is

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods TABLE OF CONTENTS

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Institute of Certified Management Accountants of Sri Lanka

Copyright Reserved Serial No Managerial Level Pilot Paper Instructions to Candidates 1. Time allowed is three (3) hours (with an additional reading time of 15 minutes). 2. Answer all questions in Part

Copyright Reserved Serial No Managerial Level Pilot Paper Instructions to Candidates 1. Time allowed is three (3) hours (with an additional reading time of 15 minutes). 2. Answer all questions in Part

PROJECTING YOUR CASH FLOW

THE BUSINESS ENTERPRISE CENTRE S GUIDE TO PROJECTING YOUR CASH FLOW The Business Enterprise Centre is a member of Last updated 16 Jan 2015 TD Page 1 of 26 Preface A cash flow statement reports the outflow

THE BUSINESS ENTERPRISE CENTRE S GUIDE TO PROJECTING YOUR CASH FLOW The Business Enterprise Centre is a member of Last updated 16 Jan 2015 TD Page 1 of 26 Preface A cash flow statement reports the outflow

C&I LOAN EVALUATION UNDERWRITING GUIDELINES. A Whitepaper

C&I LOAN EVALUATION & UNDERWRITING A Whitepaper C&I Lending Commercial and Industrial, or C&I Lending, has long been a cornerstone product for many successful banking institutions. Also known as working

C&I LOAN EVALUATION & UNDERWRITING A Whitepaper C&I Lending Commercial and Industrial, or C&I Lending, has long been a cornerstone product for many successful banking institutions. Also known as working

Absorption Costing - Overview

Absorption Costing - Overview 1. Overview of Absorption costing and Variable Costing 2. Review how costs for Manufacturing are transferred to the product 3. Job Order Vs. Process Costing 4. Overhead Application

Absorption Costing - Overview 1. Overview of Absorption costing and Variable Costing 2. Review how costs for Manufacturing are transferred to the product 3. Job Order Vs. Process Costing 4. Overhead Application

CHAPTER 12. Cost Sheet ( or) Statement of Cost ELEMENTS OF COST