are expected to be completed prior to, or in, FY2014, and are not anticipated to recommence within the forecast period;

|

|

|

- Liliana Hodge

- 8 years ago

- Views:

Transcription

1 Rule 8(b): Forecast total annual Capital Expenditure specified for each FLSM Asset Class, expressed in nominal terms. (a) Telstra s annual inflation assumptions used in its forecasts of Operating Expenditure and Capital Expenditure [Explanatory statement request 9(a)] Details of Telstra s inflation assumptions are set out in section above. (b) The method used to determine the forecasts in Rule 8(b) [Explanatory statement request 9(b)] Introduction General approach Telstra adopted a "bottom up or project-level approach to prepare the forecasts in the response to the current BBM RKR request, mapping forecast estimates to the FLSM Asset Classes. In summary: (a) Telstra first identified the asset categories within its internal management accounts that correspond to a FLSM Asset Classes. Telstra then identified all IMC Codes (or projects) that involved expenditure on one or more of those asset categories. Projects that were excluded from the analysis were those that did not include expenditure on any of the FLSM Asset Classes or the underlying asset categories, as well as those projects that: (i) (ii) (iii) are expected to be completed prior to, or in, FY2014, and are not anticipated to recommence within the forecast period; were identified as involving only a trivial expenditure on the relevant FLSM Asset Classes (or a small and highly irregular expenditure over recent years); or were identified as being for NBN-related projects. (b) Once these projects were excluded, analysis was undertaken of the remaining set of relevant projects for the purposes of preparing the capital expenditure forecasts. Estimates of the forecast capital expenditure for these projects were determined by assessing (among other things): (i) (ii) (iii) (iv) recent historic trends in capital expenditure for that project; Telstra s broad capital planning and strategic direction including the resolution to maintain fixed line service standards during the transition to the NBN; trends in demand including significant increases in demand for fixed line broadband services and their likely impact on capital expenditure over the forecast period; and the impact of the NBN rollout (based on Telstra s understanding of the planned roll-out as at June 2013). Data sources used The ACCC developed a mapping of the asset categories used in Telstra s Asset Register to the FLSM Asset Classes. This mapping was used in preparing all of the financial data supplied under this BBM RKR response in accordance with the process set out below. PAGE 26/81

The method used to determine the forecasts in Rule 8(b) [Explanatory statement request 9(b)] Introduction General approach Telstra adopted a \"bottom up or project-level approach to prepare the")

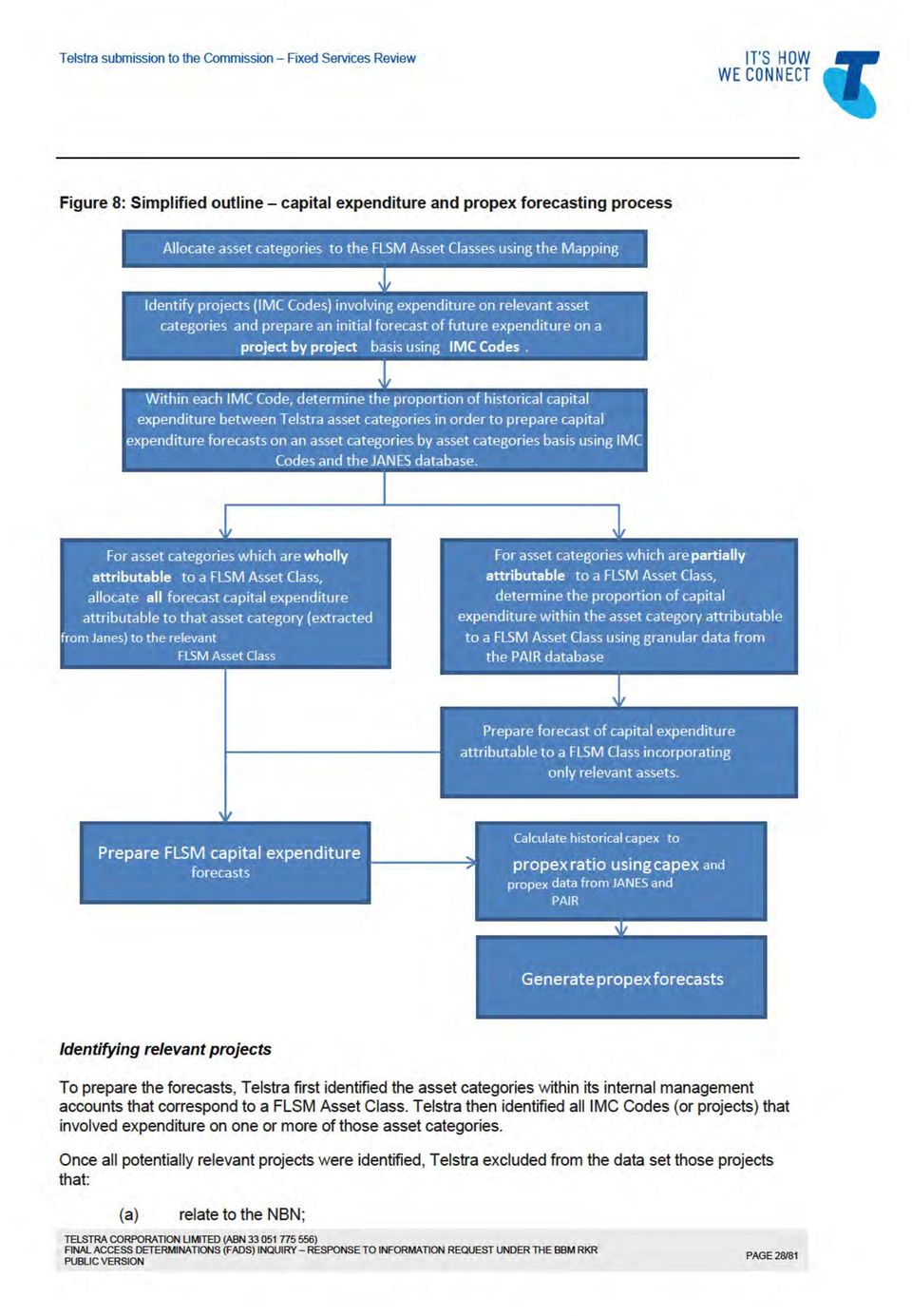

2 As set out above, Telstra plans its capital expenditure at the project level. Actual and forecast capital expenditure is recorded in Telstra s Investment Management Business Planning Database ( JANES ), grouping like projects into programs using program-specific codes ( IMC Codes ). Within each IMC Code, capital expenditure is further broken down into individual asset categories and codes. Telstra has grouped these asset categories and codes into the ACCC s FLSM Asset Classes using the mapping. In some instances it was also necessary for Telstra to analyse capital expenditure within a particular asset code at a more detailed, asset-by-asset level in order to ensure that the forecasts did not include any capital expenditure which was not properly attributable to a FLSM Asset Class. To do this, Telstra extracted more granular asset level data from its Project Assets and Investment Reporting ( PAIR ) database to determine actual historical expenditure. The PAIR database differs from the JANES in that it derives information from Systems, Applications and Products ( SAP ) data elements and so allows a more granular analysis of historical capital expenditure. This process is described in more detail below. The Investment Management group provided capital forecasts against the FLSM Asset Classes for each year of the forecast regulatory period in FY2014 dollars so each subsequent year was uplifted by the cumulative forecast inflation factor (see section above). Telstra s capital expenditure forecasts on Other Communications Plant and Equipment, Network Buildings/Support Assets and Indirect Capital Assets are not separately identified for the CAN and Core network by Telstra. For these FLSM Asset Classes, Telstra followed the methodology which was used by the ACCC for the previous regulatory period. The ACCC allocated the forecast capital expenditure for these asset classes to the corresponding CAN and Core asset classes in the FLSM based on the share of each asset s total depreciated value in the CAN and Core respectively (See Table 7 of the Comparison Statement for more detail). The capital expenditure forecasts were allocated between the CAN and Core using the same ratios. Overview of Telstra s capital expenditure and project-specific opex forecasting process A simplified diagram explaining the process used by Telstra to generate the FLSM capital expenditure and project-specific operating expenditure ( propex ) forecasts is set out in Figure 8 below: PAGE 27/81

3

4 (b) (c) (d) (e) are scheduled for completion in FY2014; do not involve material capital expenditure on an asset category falling within a FLSM Asset Class; involve significantly variable expenditure from year to year (such that future capital, and not material, expenditure cannot be accurately forecast); or will not have any significant impact on network build. As a result of this process, Telstra has excluded from its forecasts total capital expenditure of [C-I-C starts] [C-I-C ends] in FY2014 and [C-I-C starts] [C-I-C ends] in FY2015, including approximately [C-I-C starts] [C-I-C ends] in FY2014 of NBN-related capital expenditure (and [C-I-C starts] [C-I-C ends] in FY2015) from its forecasts. This comprises investments in Telstra s systems, processes and network infrastructure to support NBN-based retail and wholesale services (i.e. investments Telstra is making to facilitate its utilisation of the NBN as a service provider), as well as specific capital projects that Telstra is undertaking as a supplier of services and infrastructure to NBN Co. This is illustrated in Table 7 below. Table 7: Capital expenditure forecasts excluded projects ($m) [C-I-C starts] Reason for exclusion FY2014 ($m) FY2015 ($m) [C-I-C ends] Once the relevant projects were identified, Telstra then prepared an initial forecast of future capital expenditure for each of these IMC Codes on a project-by-project basis, using the following method: (a) (b) Telstra analysed its historical data over the past three years to identify capital expenditure trends on an IMC Code level (e.g. whether capital expenditure on particular projects was increasing, decreasing or remaining stable); and Telstra then prepared capital expenditure forecasts for each IMC Code having regard to these trends and the specific circumstances of each project. This process is illustrated in Figure 9 below. PAGE 29/81

![As a result of this process, Telstra has excluded from its forecasts total capital expenditure of [C-I-C starts] [C-I-C ends] in FY2014 and [C-I-C starts] [C-I-C ends] in FY2015, including](/docs-images/49/17054681/images/page_4.jpg "approximately [C-I-C starts] [C-I-C ends] in FY2014 of NBN-related capital expenditure (and [C-I-C starts] [C-I-C ends] in FY2015) from its forecasts.")

5 Figure 9: Identifying relevant IMC Codes Asset Summary Full Asset Category FLSM Mapping Raw Data IMC's of Interest Detailed IMC's of Interest Summary Derive list of IMC s that have had spend on Assets of Interest showing Asset Cats Derive list of IMC s that have had spend on Assets of Interest IMC's of Interst with Histoical Spend Download into Excel to forecast future spend Future Year Estimates Table Preparing capital expenditure forecasts at an asset class level As set out above, in order to prepare the FLSM forecasts requested by the ACCC, it was also necessary for Telstra to break down each of its project level capital expenditure forecasts into a series of more granular asset category level forecasts. To do this, Telstra calculated, for each IMC Code, the proportion of total capital expenditure attributable to each asset class over each of the previous three years as a percentage of total expenditure. These proportions were then forecast into future years having regard to the trends and the specific circumstances of each project. Telstra then applied these percentages to the capital expenditure PAGE 30/81

6 forecasts for each IMC Code to generate forecasts on an asset category by asset category basis. This process is illustrated in Figure 10 below: Figure 10: Calculating expenditure by Asset Class Raw Data Total by IMC Calculate (for each IMC) % of spend on Cost Accounts of total spend on each IMC. This is done for each financial year Asset Cat Percentage Furute Year Estimates Table2 Asset Cat Map FLSM Mappings IMC's of Interest Summary2 IMC Asset Yearly % Assets of Interest Forecast Calculate for each IMC(using IMC forecasts and % for Asset spend per IMC) the yearly forecast spend on Asset Cats Download into Excel to forecast future percentage Asset Cat % Forecast Allocating capital forecasts to the FLSM Asset Classes In the majority of cases, all assets within a particular asset category (e.g. CAN Copper Cables) are wholly attributable to the fixed line network and a single FLSM Asset Class. In these cases, Telstra allocated the asset category level forecasts directly to the relevant FLSM Asset Class ( Wholly- Allocated Asset Class Forecasts ). However, in some cases, Telstra s internal asset categories include assets which are both attributable to the FLSM Asset Classes and assets which do not fall within an FLSM Asset Class. Telstra has used the methodology set out below to account for these asset categories in its FLSM forecasts: Step 1 - Telstra analysed the granular historical capital expenditure data in its PAIR database on an asset-by-asset basis to identify those assets which should be assigned to an FLSM Asset Class and which should be excluded from the forecasts. Telstra used this data to calculate the proportion of historical capital expenditure within each asset category that was attributable to assets within an FLSM Asset Class. This is illustrated in Figure 11 below: PAGE 31/81

the yearly forecast spend on Asset Cats Download into Excel to forecast future percentage Asset Cat % Forecast Allocating capital")

7 Figure 11: Calculating historical expenditure on relevant assets Asset Hist Acct Inclusion Notes FLSM Mappings Asset Hist Acct Inclusions by Financial Year Inclusion Asset Cat Fin Year Total Inclusions % Step 2 - After calculating the proportion of capital expenditure within each asset category that should be allocated to a particular FLSM Asset Class, Telstra multiplied each asset categorylevel forecast by this percentage to generate a forecast of relevant capital expenditure within the asset category ( Pro-Rata Asset Class Forecasts ). This process is illustrated in Figure 12 below: PAGE 32/81

.")

8 Figure 12: Preparing Pro-Rata FLSM Asset Class Forecasts Inclusion Asset Cat Asset Hist Acct Total of Asset Cat Copy of Inclusions by Financial Year Identify Assets of Interest spend from 2009 onwards Copy of Q Inclusions % Calculate % of Asset Cat spend of Asset Cats of Interest. Download into Excel to forecast future percentage Inclusions % Forecast Step 3 - Telstra generated overall capital expenditure forecasts for each FLSM Asset Class by adding together the Wholly-Allocated FLSM Asset Class Forecasts and the Pro-Rata FLSM Asset Class Forecasts. (c) The assumptions used to determine the forecasts in Rule 8(b) [Explanatory statement request 9(c)] Details of the assumptions used to determine the forecasts in Rule 8(b) are set out below and in section 5.1.2(b) above. Capital expenditure which cannot be foreseen or quantified in advance From time to time, Telstra is required to undertake capital expenditure which either: (a) (b) cannot be foreseen or forecast; or can be predicted with a degree of certainty, but cannot accurately be quantified in advance. An example of the first category of capital expenditure is the South Brisbane Exchange Project, which involved unforeseen capital expenditure of approximately [C-I-C starts] [C-I-C ends] between FY2011 and FY2013 as a result of the construction of a Children's Hospital on a site occupied by the PAGE 33/81

9 former South Brisbane exchange. Telstra has not made any allowance or contingency in its capital expenditure forecasts for this category of expenditure. An example of the second category is disaster recovery expenditure (e.g. capital expenditure arising out of the Queensland floods or such as the Warrnambool exchange fire). Telstra has made an allowance in its forecasts of [C-I-C starts] [C-I-C ends] per annum for disaster rectification as it can predict with a reasonable degree of certainty that it will incur disaster recovery related capital expenditure over the forecast period. NBN rollout Telstra s capital expenditure forecasts are based on Telstra s view of the NBN rollout (and its consequent impact on fixed line network capital expenditure) as at June Telstra has prepared its capital expenditure forecasts based on currently approved projects. These projects have been, and continue to be funded by Telstra on the basis of the best information available in relation to the scope and timing of the NBN rollout as at June As described in more detail below, these investments are primarily intended to manage the migration from the legacy copper network to the NBN by maintaining existing service levels (in terms of network performance, reliability and fault levels) as far as practical while minimising investments in assets that will be stranded following the rollout of the NBN. Further, as noted in section 5.1.2(b) above, Telstra has excluded NBN-related capital expenditure from its forecasts. (d) The basis for the assumptions [Explanatory statement request 9(d)] See sections 5.1.2(b) and 5.1.2(c) above. (e) Any internal guidelines used by Telstra for either of the following purposes: (i) to assess the prudency of forecast Capital Expenditure [Explanatory statement request 9(e)] The response below sets out details of the capital expenditure planning processes that Telstra implements in relation to all proposed projects and services. These processes do not apply, and have not been implemented, exclusively for the purpose of preparing forecasts for the projects and asset types that are relevant to the FLSM. As set out above, Telstra has only deviated from these standard processes where necessary to meet the express requirements of the BBM RKR (for example, forecasts for periods beyond Telstra s standard 12 to 36 month business planning horizon). Overview of Telstra s capital expenditure planning framework and processes Telstra plans capital expenditure at a project level rather than at the FLSM Asset Class level used by the ACCC. As part of its planning process, each business unit prepares detailed capital expenditure forecasts three years in advance. Expenditure forecasts are revised each year taking into account actual expenditure in the previous year and anticipated expenditure trends. Each year, Telstra s board approves an overall capital expenditure envelope (currently approximately [C-I-C starts] [C-I-C ends] of sales). All capital expenditure (both on the fixed network and other networks and services) needs to be funded out of this envelope. Telstra has detailed capital management processes in place to allocate its capital expenditure budget between competing priorities. In particular, Telstra will generally only invest in a specific network, project, product or service if: PAGE 34/81

![Telstra has made an allowance in its forecasts of [C-I-C starts] [C-I-C ends] per annum for disaster rectification as it can predict with a reasonable degree of certainty that it will incur disaster](/docs-images/49/17054681/images/page_9.jpg "recovery related capital expenditure over the forecast period.")

10 (a) (b) (c) (d) the return on investment from the project is greater than that which would be available by investing in alternative projects; the investment is necessary for Telstra to meet customer service level expectations (e.g. investing in increased transmission capacity in response to increased data traffic); the investment is necessary to avoid service failures; or the investment is necessary to meet the Universal Service Obligation ( USO ) and other regulatory requirements. Compared to other regulated services providers (e.g. in the energy and gas sectors), Telstra s regulated services represent a relatively small proportion of its business (approximately [C-I-C starts] [C-I-C ends]) and all fixed line voice and fixed broadband revenue accounts for only approximately 25% of Telstra s total revenue. In addition, overall revenue from fixed services is declining, while revenue growth in other areas is increasing. In FY2013, revenue from fixed line services decreased by 2.7% while revenue from mobiles increased by 6%, NAS revenue increased by 17.7% and revenue from international businesses increased by 16.2%. Telstra also faces a significant risk that any new investments in the fixed network will be stranded once the NBN rollout is complete. In many cases therefore, returns from investments outside the fixed network are significantly more attractive than the returns available on investments in the fixed network. Telstra s fixed line investments are primarily intended to maintain existing services levels and to meet USO requirements while the NBN is rolled out. This internal competition for capital expenditure within Telstra, together with the factors set out above, ensure that Telstra s investment in fixed services is prudent. As outlined above, Telstra has prepared its capital expenditure forecasts using a bottom up or project level approach. This is a conservative approach which includes only projects that are currently underway and are expected to continue over the regulatory period. It does not account for unplanned or unforeseen capital expenditure. Matters to be taken into account in assessing the prudency of Telstra s capital expenditure forecasts The ACCC has stated (in clause 6.10 of the Fixed Principles Provisions (clause 6 of the Final Access Determination for the Declared Fixed Line Services)) that it will take the following matters into account in assessing the reasonableness of Telstra s capital expenditure forecasts: the access provider s level of capital expenditure in the previous regulatory period; reasons for proposed changes to capital expenditure from one regulatory period to the next regulatory period; whether the access provider s asset management and planning framework reflects best practice; any relevant regulatory obligations, or changes to such obligations, applicable to providing the relevant declared fixed line services; and any other matters relevant to whether forecast capital expenditures reflect prudent and efficient costs. These matters are addressed below. PAGE 35/81

11 Criteria 1 - Capital expenditure in the Previous Regulatory Period and Criteria 2 - Reasons for proposed changes to capital expenditure from one regulatory period to the next In order to comply with the requirements of the RKR, Telstra has developed a project level bottom up approach in preparing capital expenditure forecasts for the regulatory period the subject of the ACCC s BBM RKR request. The benefit of this approach is that it removes the need to allocate costs away from the FLSM for projects not within scope and for NBN specific projects. However, direct comparison to past period actuals is more complex. Telstra s forecasts do not simply adopt all capital expenditure at a project level that can be mapped to the relevant FLSM Asset Classes at the current point in time. Projects that are not within the scope of the FLSM or relevant to the RKR period have been excluded from the forecast. That is, projects that have already concluded by 30 June 2013 will not be included in the forecast. Projects specifically relating to the NBN are also excluded. As a result, comparing the forecast values to past period figures is difficult as the relevant capital expenditure to which these forecasts should be compared will not necessarily be drawn from the same set of projects included in the forecast estimates. These issues are set out in greater detail in the annexed Comparison Statement. Nevertheless, the following chart illustrates that based on those projects that have been included in the forecasts for the BBM RKR response, the actual value of capital expenditure within those same projects in the previous regulatory period was generally higher. Figure 13: Value of capital expenditure in projects included in forecast for BBM RKR response (Actual and Forecast) [C-I-C starts] [C-I-C ends] The above chart shows the forecast capital expenditure produced by the new method, and the capital expenditure for the preceding four years calculated using the same method. [C-I-C starts] [C-I-C ends]. However, this approach to comparing forecasts from the Previous Regulatory Period with forecasts using the new method only serves as a partial comparison, as it excludes projects (and associated capital expenditure) that would have occurred in prior regulatory periods but were excluded from the forecasts because, for example, they were unanticipated at the time that the forecasts were made (e.g. capital expenditure associated with the South Brisbane exchange and the Top Hat project). This is discussed in more detail in the Comparison Statement. PAGE 36/81

12

13 (d) (e) a capital management governance structure involving review and oversight of business cases by specialist committees; and processes for the ongoing review and monitoring of approved capital expenditure projects. Capital expenditure framework All capital expenditure by Telstra is required to be within the authorised capital expenditure envelope and in accordance with the relevant business unit s Strategic Investment Portfolio Roadmap ( Delivery Roadmap ). Delivery Roadmaps are approved by each business unit s Group Managing Director ( GMD ), the Portfolio Management Committee ( PMC ) and the Investment Management Committee ( IMBC ). Once approved, Delivery Roadmaps can only be varied with the approval of these decisionmaking bodies. All approved capital expenditure within a business unit s Delivery Roadmap must fall into one of the following five categories: (a) (b) (c) (d) (e) Strategic Initiatives; Tactical Discretionary (a prioritised list of relatively small investment projects managed at a local business unit level); Customer Demand Driven; Shared Infrastructure investment driven by customer demand; or Stay in Business. Allocation of the capital expenditure budget between business units Each year Telstra prepares a top down capital expenditure plan (allocating the overall capital expenditure envelope between competing business units) for the coming year, as part of its annual strategy discussions. Following this, each business unit prepares a bottom up estimate of capital expenditure broken down into the specific initiatives the business unit considers necessary to support that business unit s revenue targets. Once these initial estimates have been completed, each business unit ranks the individual initiatives it has identified in order of priority. The bottom up forecasts are then submitted to Telstra Corporate, where they are adjusted to fit within the plan, and funding is provisionally allocated to business units. Each business unit is then required to nominate: one additional project which it would undertake, if additional funding was available; and of the projects that have provisionally been allocated funding, the lowest priority project (i.e. the project which the business unit would abandon first if funding was decreased). The IMC reviews these projects and, where appropriate, adjusts the funding made available to business units by allocating funding previously allocated to low priority capital projects to capital projects within different business units which would otherwise be unfunded. PAGE 38/81

.")

14 Capital Management Governance Telstra has three tiers of capital management governance committees. With the exception of small expenditures of less than [C-I-C starts] [C-I-C ends], all new business cases must be approved by one or more of these committees before any expenditure can be incurred: (a) (b) (c) the IMC, which is the executive body responsible for providing strategic direction to the Capital Investment Programme and the review and approval of high impact project business cases. The IMC is chaired by Telstra s CEO. All capital expenditure projects with an expected expenditure exceeding [C-I-C starts] [C-I-C ends] require IMC approval; the PMC, which is responsible to the IMC for the management of the Capital Investment project portfolio. Its primary role is to ensure that projects are being executed at the right time and are delivering to agreed quality, time and cost expectations. Its focus is on strategic alignment, cross-functional alignment and achievability. The PMC has oversight over all portfolios progress and status. All capital expenditure projects with expected expenditure of between [C-I-C starts] [C-I-C ends] require PMC approval. Projects with capital expenditure exceeding [C-I-C starts] [C-I-C ends] must be reviewed and endorsed by the PMC before being submitted to the IMC; and the Portfolio Steering Committee ( PSC ) for each business unit, which is responsible for reviewing and approving all other business cases up to [C-I-C starts] [C-I-C ends]. Approval delegations These capital management governance arrangements are supported by the capital expenditure approval delegations described below: (a) Board approval All capital expenditure projects which exceed [C-I-C starts] [C- I-C ends] must be approved by the CEO, CFO and the board. IMC approval is required before a project can be submitted for CEO and CFO approval; and (b) GMD approval All capital expenditure projects with expected expenditure of between [C-I-C starts] [C-I-C ends] require GMD approval. Projects with capital expenditure exceeding [C-I-C starts] [C-I-C ends] must be reviewed and endorsed by the relevant GMD before being submitted to the CEO and CFO for approval. Business case requirements All discretionary investment decisions are required to be supported by a business case. Business cases must be: clearly linked to Telstra s physical, financial and performance targets; provide clear statements of accountability, deliverables, and measurements of benefit realisation; and demonstrate a clear linkage between the benefits from the investment and Telstra s overall profitability. In order to gain approval, proposals must also meet the following financial hurdles [C-I-C starts]: PAGE 39/81

15 [C-I-C ends] For demand driven and Asset Replacement & Operational Support ( AROS ) projects, the approval process differs slightly depending on whether the project is a new project or is stay in business expenditure on an existing project. All new demand-driven projects are required to be supported by a business case. For ongoing demand projects (e.g. projects that have already been approved by the IMC and have an approved business case in place), Telstra s processes do not require a further formal business case to be submitted for each release of additional funds. Rather, the business unit is required to submit a justification statement justifying the release of further funds by reference to forecast demand physicals, costs and revenues. Release and expenditure of funds All proposals are required to be funded out of the relevant business unit s budget before being submitted to a relevant committee for approval. Funds are released only after formal approval is obtained. Once funds have been released for a specific project, they are not transferable and cannot be applied against another project. In all cases, contracts cannot be entered into until a business case has been approved by the relevant committee. Funds can only be substituted to other projects by formal approval of the relevant committee under the governance framework. Review and monitoring Telstra has a variety of review mechanisms in place to monitor its capital spend. Project owners are responsible for ensuring that spend does not exceed funds released and for delivering the project on time, on scope and within budget. Business cases are required to be re-submitted to the relevant committee for approval if: it becomes clear that a project will vary from the original business case by [C-I-C starts] [C-I-C ends] or more; the scope of the approved business case is expected to change materially; or for multi-year projects, the cost or benefit varies adversely by more than [C-I-C starts] [C- I-C ends] within a budget year. As part of its standard approval process, the IMC may require a formal Post Implementation Review ( PIR ) to be scheduled as a condition of approving expenditure on a particular project. In addition to these formal project-specific reviews, Telstra conducts the following regular reviews of the capital expenditure program as a whole: the Executive Director of each business unit conducts a review of the business unit s capital expenditure each month; the PMC reviews company-wide capital expenditure on a monthly basis; and PAGE 40/81

, Telstra s processes do not require a further formal business case to be")

16 the IMC reviews company capital expenditure on a quarterly basis. Having regard to these matters, Telstra considers that its asset management and capital expenditure planning framework reflect best practice and ensure the reasonableness and prudency of any investment. Criteria 4 - Relevant regulatory obligations The key regulatory obligations that impact on the FLSM capital expenditure forecasts are: the USO, which obliges Telstra to provide new copper connections at greenfield and brownfield estates (regardless of whether or not those investments will be profitable); the Customer Service Guarantee framework, which obliges Telstra to meet performance standards and provide customers with financial compensation when these standards are not met; the National Reliability Framework requirements, which ensures faults are repaired within reasonable time frames; the Telecommunications Consumer Protections Code ( TCP ), which requires Telstra to implement better spend management tools including improvements in billing processes and credit management, and the introduction of unit pricing and notifications about data usage and expenditure thresholds; the legal interception rules (under the Telecommunications (Interception and Access) Act 1979) which require Telstra to cooperate with Australian law enforcement and security agencies to intercept communications, access stored communications and disclose telecommunications data in certain circumstances; the IT system changes associated with the Structural Separation Undertaking ( SSU ) which obliges Telstra to ensure staff within its retail business units do not have access to wholesale customer protected information; and privacy legislation which requires Telstra to protect its customers personal information from misuse, loss, unauthorised access, modification or disclosure. Telstra has considered each of these matters in preparing its capital expenditure forecasts. Criteria 5 - Other relevant matters For the reasons set out above, Telstra considers that: the nature and purpose of forecast capital expenditure on the fixed network (i.e. maintaining existing service levels during the migration to NBN); the need for capital expenditure projects on the fixed network to compete for funding with projects involving other services; and the approach which has been taken in preparing the forecasts, mean that the ACCC can have a high degree of confidence that the forecasts set out in this response are reasonable and reflect only prudent and efficient investment by Telstra in assets included in the FLSM Asset Classes over the regulatory period. PAGE 41/81

17

18

19

20 Table 8: Capital expenditure forecasts, by driver ($m) [C-I-C starts] Expenditure type FY2014 FY2015 FY2016 FY2017 FY2018 FY2019 Demand AROS Capitalised Interest Discretionary Total [C-I-C ends] A detailed description of the major investment drivers for each of these categories is set out below: Demand driven investments Fixed broadband data growth Telstra is currently experiencing very significant growth in fixed broadband data consumption, including on the ADSL network relevant to the FLSM. The significant growth in data consumption driven particularly by growth in ADSL network throughput - is shown in Figure 15 below: Figure 15: Fixed broadband data growth (Gbps) [C-I-C starts] [C-I-C ends] This growth is expected to continue over the forecast period. There are currently over 3m retail and wholesale ADSL SIO s nationally. As set out within the RKR, ADSL SIO volumes are forecast to decrease by June 2016 to approximately [C-I-C starts] [C-I-C ends] SIOs. However, at the same time demand at peak times on the ADSL network (peak usage) is expected to increase by over [C- PAGE 45/81

[C-I-C starts] [C-I-C")

21

22 This methodology has been in place since FY2009 and is supported by an auditable AROS database. Capitalised Interest Capitalised Interest that is related to borrowing costs directly attributable to the acquisition, construction or production of a qualifying asset are included in the cost of that asset. Such borrowing costs are capitalised as part of the cost of the asset when it is probable that they will result in future economic benefits to the entity and the costs can be measured reliably. Telstra s capitalised interest costs are driven directly by its costs of borrowing to fund the various projects included in the FLSM forecasts. In order to forecast future capitalised interest requirements, Telstra has averaged its capitalised interest over the past three years, and held this constant over the regulatory period. Discretionary expenditure Only a very small proportion [C-I-C starts] [C-I-C ends] of Telstra s forecast capital expenditure is discretionary expenditure. Telstra s discretionary capital expenditure is primarily driven by product development activities and activities directed towards generating productivity improvements. The small percentage of forecast capital expenditure falling under the discretionary expenditure category is consistent with Telstra s broader capital expenditure objectives with respect to the fixed line network over the forecast period namely, to maintain service levels (particularly in the presence of ongoing growth in broadband demand) and efficiently manage the transition from the PSTN and legacy fixed line services to the NBN. (g) A report comparing forecasts for the previous Regulatory Period with the actual Capital Expenditure for that period, and an explanation of any differences, trends and drivers; [Explanatory statement request 11(b)] Please refer to the Comparison Statement. (h) For discretionary projects, an explanation of any major differences in the types of investment undertaken compared to the forecasts; and [Explanatory statement request 11(c)] As the Previous Regulatory Forecasts were not prepared using a bottom up assessment of individual projects, it is not possible to provide a detailed explanation of any differences in actual project investment and forecast investment for particular discretionary projects. For further information in relation to the comparison of prior capital expenditure forecast to actual investment, please see the Comparison Statement. (i) Evidence that a review of Capital Expenditure projects was undertaken in accordance with any investment guidelines. [Explanatory statement request 11(d)] See above. PAGE 47/81

Fixed line services FAD inquiry: Disclosure of report provided by Telstra under the Building Block Model Record Keeping Rule. Consultation paper

Fixed line services FAD inquiry: Disclosure of report provided by Telstra under the Building Block Model Record Keeping Rule Consultation paper March 2014 Australian Competition and Consumer Commission

Fixed line services FAD inquiry: Disclosure of report provided by Telstra under the Building Block Model Record Keeping Rule Consultation paper March 2014 Australian Competition and Consumer Commission

COMPLIANCE REVIEW OF 2006/07 ASSET MANAGEMENT PLAN. Top Energy Limited

PB ASSOCIATES COMPLIANCE REVIEW OF 2006/07 ASSET MANAGEMENT PLAN Prepared for PB Associates Quality System: Document Identifier : 153162 Top Energy Final Report Revision : 2 Report Status : Final Date

PB ASSOCIATES COMPLIANCE REVIEW OF 2006/07 ASSET MANAGEMENT PLAN Prepared for PB Associates Quality System: Document Identifier : 153162 Top Energy Final Report Revision : 2 Report Status : Final Date

Project Evaluation Guidelines

Project Evaluation Guidelines Queensland Treasury February 1997 For further information, please contact: Budget Division Queensland Treasury Executive Building 100 George Street Brisbane Qld 4000 or telephone

Project Evaluation Guidelines Queensland Treasury February 1997 For further information, please contact: Budget Division Queensland Treasury Executive Building 100 George Street Brisbane Qld 4000 or telephone

OPERATIONAL EQUIVALENCE REPORT FOR THE JUNE QUARTER

OPERATIONAL EQUIVALENCE REPORT FOR THE JUNE QUARTER 31 August 2012 FINAL TELSTRA UNRESTRICTED OPERATIONAL EQUIVALENCE REPORT PAGE 1/18 Contents 1. Executive summary 3 2. Introduction 6 2.1. The interim

OPERATIONAL EQUIVALENCE REPORT FOR THE JUNE QUARTER 31 August 2012 FINAL TELSTRA UNRESTRICTED OPERATIONAL EQUIVALENCE REPORT PAGE 1/18 Contents 1. Executive summary 3 2. Introduction 6 2.1. The interim

Wandering Council Draft Plant Asset Management Plan

Wandering Council Draft Plant Asset Management Plan TABLE OF CONTENTS EXECUTIVE SUMMARY... 2 Context... 2 1 INTRODUCTION... 2 1.1 Background... 2 1.2 Goals and Objectives of Asset Management... 3 1.3 Pla

Wandering Council Draft Plant Asset Management Plan TABLE OF CONTENTS EXECUTIVE SUMMARY... 2 Context... 2 1 INTRODUCTION... 2 1.1 Background... 2 1.2 Goals and Objectives of Asset Management... 3 1.3 Pla

Frontier Networks Pty Ltd response to Superfast Broadband Access Service declaration draft decision

Frontier Networks Pty Ltd response to Superfast Broadband Access Service declaration draft decision PUBLIC VERSION 4 DECEMBER 2015 1 Frontier Networks Pty Ltd (Frontier) welcomes the opportunity to respond

Frontier Networks Pty Ltd response to Superfast Broadband Access Service declaration draft decision PUBLIC VERSION 4 DECEMBER 2015 1 Frontier Networks Pty Ltd (Frontier) welcomes the opportunity to respond

Contract and Vendor Management Guide

Contents 1. Guidelines for managing contracts and vendors... 2 1.1. Purpose and scope... 2 1.2. Introduction... 2 2. Contract and Vendor Management 2.1. Levels of management/segmentation... 3 2.2. Supplier

Contents 1. Guidelines for managing contracts and vendors... 2 1.1. Purpose and scope... 2 1.2. Introduction... 2 2. Contract and Vendor Management 2.1. Levels of management/segmentation... 3 2.2. Supplier

BUSINESS MANAGEMENT COMPLIANCE POLICY & MANUAL ADOPTED

F021 BUSINESS MANAGEMENT COMPLIANCE POLICY & MANUAL ADOPT... http://ln.burdekin.qld.gov.au/cis/policies.nsf/95f9bd5961a3b1aa4a2565a900141... Page 1 of 1 30/04/2013 Policy Register Category: Policy Number:

F021 BUSINESS MANAGEMENT COMPLIANCE POLICY & MANUAL ADOPT... http://ln.burdekin.qld.gov.au/cis/policies.nsf/95f9bd5961a3b1aa4a2565a900141... Page 1 of 1 30/04/2013 Policy Register Category: Policy Number:

STELLENBOSCH MUNICIPALITY

STELLENBOSCH MUNICIPALITY APPENDIX 9 BORROWING POLICY 203/204 TABLE OF CONTENTS. PURPOSE... 3 2. OBJECTIVES... 3 3. DEFINITIONS... 3 4. SCOPE OF THE POLICY... 4 5. LEGISLATIVE FRAMEWORK AND DELEGATION

STELLENBOSCH MUNICIPALITY APPENDIX 9 BORROWING POLICY 203/204 TABLE OF CONTENTS. PURPOSE... 3 2. OBJECTIVES... 3 3. DEFINITIONS... 3 4. SCOPE OF THE POLICY... 4 5. LEGISLATIVE FRAMEWORK AND DELEGATION

1. This Prudential Standard is made under paragraph 230A(1)(a) of the Life Insurance Act 1995 (the Act).

(a) of the Life Insurance Act 1995 (the Act).") Prudential Standard LPS 110 Capital Adequacy Objective and key requirements of this Prudential Standard This Prudential Standard requires a life company to maintain adequate capital against the risks associated

Prudential Standard LPS 110 Capital Adequacy Objective and key requirements of this Prudential Standard This Prudential Standard requires a life company to maintain adequate capital against the risks associated

Queensland Government Response to the Department of Broadband, Communications and the Digital Economy proposed consumer safeguard instruments on

Queensland Government Response to the Department of Broadband, Communications and the Digital Economy proposed consumer safeguard instruments on Universal Service Payphone Standards, Performance Benchmarks,

Queensland Government Response to the Department of Broadband, Communications and the Digital Economy proposed consumer safeguard instruments on Universal Service Payphone Standards, Performance Benchmarks,

2017 19 TasNetworks Regulatory Proposal Expenditure Forecasting Methodology

2017 19 TasNetworks Regulatory Proposal Expenditure Forecasting Methodology Version Number 1 26 June 2015 Tasmanian Networks Pty Ltd (ACN 167 357 299) Table of contents 1 Introduction... 1 2 Meeting our

2017 19 TasNetworks Regulatory Proposal Expenditure Forecasting Methodology Version Number 1 26 June 2015 Tasmanian Networks Pty Ltd (ACN 167 357 299) Table of contents 1 Introduction... 1 2 Meeting our

Procurement Policy. Finance Policy

1 Purpose Victoria University of Wellington (the University ) and its subsidiaries are large scale procurers of goods and services. To ensure continued accountability and robust governance, it is critical

1 Purpose Victoria University of Wellington (the University ) and its subsidiaries are large scale procurers of goods and services. To ensure continued accountability and robust governance, it is critical

FINANCIAL SERVICES TRAINING PACKAGE FNB99

FINANCIAL SERVICES TRAINING PACKAGE FNB99 This is Volume 12 of a 13-volume set. This volume should not be used in isolation but in the context of the complete set for the Financial Services Training Package.

FINANCIAL SERVICES TRAINING PACKAGE FNB99 This is Volume 12 of a 13-volume set. This volume should not be used in isolation but in the context of the complete set for the Financial Services Training Package.

TELSTRA CORPORATION LIMITED

TELSTRA CORPORATION LIMITED Fixed Services Review Response to other parties submissions to the Commission s Discussion paper on the Declaration Inquiry Response to the Commission s request for market information

TELSTRA CORPORATION LIMITED Fixed Services Review Response to other parties submissions to the Commission s Discussion paper on the Declaration Inquiry Response to the Commission s request for market information

Capital Adequacy: Advanced Measurement Approaches to Operational Risk

Prudential Standard APS 115 Capital Adequacy: Advanced Measurement Approaches to Operational Risk Objective and key requirements of this Prudential Standard This Prudential Standard sets out the requirements

Prudential Standard APS 115 Capital Adequacy: Advanced Measurement Approaches to Operational Risk Objective and key requirements of this Prudential Standard This Prudential Standard sets out the requirements

Changes in regulated electricity prices from 1 July 2012

Independent Pricing and Regulatory Tribunal FACT SHEET Changes in regulated electricity prices from 1 July 2012 Based on Draft Determination, 12 April 2012 The Independent Pricing and Regulatory Tribunal

Independent Pricing and Regulatory Tribunal FACT SHEET Changes in regulated electricity prices from 1 July 2012 Based on Draft Determination, 12 April 2012 The Independent Pricing and Regulatory Tribunal

GOVERNMENT RESPONSE TO ESCOSA S FINAL REPORT INQUIRY INTO 2008-09 METROPOLITAN AND REGIONAL WATER AND WASTEWATER PRICING PROCESS

TO ESCOSA S FINAL REPORT INQUIRY INTO 2008-09 METROPOLITAN AND REGIONAL WATER AND WASTEWATER PRICING PROCESS AREA OVERVIEW and ESCOSA identifies an alternative top-down approach to an input based, or bottom

TO ESCOSA S FINAL REPORT INQUIRY INTO 2008-09 METROPOLITAN AND REGIONAL WATER AND WASTEWATER PRICING PROCESS AREA OVERVIEW and ESCOSA identifies an alternative top-down approach to an input based, or bottom

Electricity network services. Long-term trends in prices and costs

Electricity network services Long-term trends in prices and costs Contents Executive summary 3 Background 4 Trends in network prices and service 6 Trends in underlying network costs 11 Executive summary

Electricity network services Long-term trends in prices and costs Contents Executive summary 3 Background 4 Trends in network prices and service 6 Trends in underlying network costs 11 Executive summary

Writing your charity s investment policy A guide

Writing your charity s investment policy A guide www.cfg.org.uk www.charityinvestorsgroup.org.uk Contents Introduction What is this guide for?... 1 Who is this guide for?... 1 Why have a written investment

Writing your charity s investment policy A guide www.cfg.org.uk www.charityinvestorsgroup.org.uk Contents Introduction What is this guide for?... 1 Who is this guide for?... 1 Why have a written investment

2014 Residential Electricity Price Trends

FINAL REPORT 2014 Residential Electricity Price Trends To COAG Energy Council 5 December 2014 Reference: EPR0040 2014 Residential Price Trends Inquiries Australian Energy Market Commission PO Box A2449

FINAL REPORT 2014 Residential Electricity Price Trends To COAG Energy Council 5 December 2014 Reference: EPR0040 2014 Residential Price Trends Inquiries Australian Energy Market Commission PO Box A2449

Electricity Settlements Company Ltd Framework Document

Electricity Settlements Company Ltd Framework Document This framework document has been drawn up by the Department of Energy and Climate Change in consultation with the Electricity Settlements Company.

Electricity Settlements Company Ltd Framework Document This framework document has been drawn up by the Department of Energy and Climate Change in consultation with the Electricity Settlements Company.

Attachment 20.27 SA Power Networks: Network Program Deliverability Strategy

Attachment 20.27 SA Power Networks: Network Program Deliverability Strategy Network Program Deliverability Strategy 2015-20 Regulatory Control Period SA Power Networks www.sapowernetworks.com.au Internal

Attachment 20.27 SA Power Networks: Network Program Deliverability Strategy Network Program Deliverability Strategy 2015-20 Regulatory Control Period SA Power Networks www.sapowernetworks.com.au Internal

Alternative infrastructure funding and financing

Alternative infrastructure funding and financing Research Paper (commissioned by the Queensland Government) 21 March 2016 Department Of Infrastructure, Local Government and Planning This page intentionally

Alternative infrastructure funding and financing Research Paper (commissioned by the Queensland Government) 21 March 2016 Department Of Infrastructure, Local Government and Planning This page intentionally

Changes in regulated electricity prices from 1 July 2012

Independent Pricing and Regulatory Tribunal FACT SHEET Changes in regulated electricity prices from 1 July 2012 Based on Final Determination, 13 June 2012 The Independent Pricing and Regulatory Tribunal

Independent Pricing and Regulatory Tribunal FACT SHEET Changes in regulated electricity prices from 1 July 2012 Based on Final Determination, 13 June 2012 The Independent Pricing and Regulatory Tribunal

SUBMISSION ON THE AER'S DRAFT DISTRIBUTION DETERMINATION 2011-2015, APPENDIX P: DEBT RAISING COSTS

SUBMISSION ON THE AER'S DRAFT DISTRIBUTION DETERMINATION 2011-2015, APPENDIX P: DEBT RAISING COSTS 19 August 2010 119476207 This submission sets out CitiPower Pty (CitiPower) and Powercor Australia Limited's

SUBMISSION ON THE AER'S DRAFT DISTRIBUTION DETERMINATION 2011-2015, APPENDIX P: DEBT RAISING COSTS 19 August 2010 119476207 This submission sets out CitiPower Pty (CitiPower) and Powercor Australia Limited's

PROJECT MANAGEMENT FRAMEWORK

PROJECT MANAGEMENT FRAMEWORK DOCUMENT INFORMATION DOCUMENT TYPE: DOCUMENT STATUS: POLICY OWNER POSITION: INTERNAL COMMITTEE ENDORSEMENT: APPROVED BY: Strategic document Approved Executive Assistant to

PROJECT MANAGEMENT FRAMEWORK DOCUMENT INFORMATION DOCUMENT TYPE: DOCUMENT STATUS: POLICY OWNER POSITION: INTERNAL COMMITTEE ENDORSEMENT: APPROVED BY: Strategic document Approved Executive Assistant to

Provisions, Contingent Liabilities and Contingent Assets

559 Accounting Standard (AS) 29 Provisions, Contingent Liabilities and Contingent Assets Contents OBJECTIVE SCOPE Paragraphs 1-9 DEFINITIONS 10-13 RECOGNITION 14-34 Provisions 14-25 Present Obligation

559 Accounting Standard (AS) 29 Provisions, Contingent Liabilities and Contingent Assets Contents OBJECTIVE SCOPE Paragraphs 1-9 DEFINITIONS 10-13 RECOGNITION 14-34 Provisions 14-25 Present Obligation

Gas transport tariffs calculation

Ad Hoc Expert Facility under the INOGATE project Support to Energy Market Integration and Sustainable Energy in the NIS (SEMISE) Gas transport tariffs calculation 1 TABLE OF CONTENTS 1. INTRODUCTION...

Ad Hoc Expert Facility under the INOGATE project Support to Energy Market Integration and Sustainable Energy in the NIS (SEMISE) Gas transport tariffs calculation 1 TABLE OF CONTENTS 1. INTRODUCTION...

International Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets

International Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets Objective The objective of this Standard is to ensure that appropriate recognition criteria and measurement

International Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets Objective The objective of this Standard is to ensure that appropriate recognition criteria and measurement

NORTH AYRSHIRE COUNCIL CORPORATE ASSET MANAGEMENT STRATEGY 2013-2023 JANUARY 2013

APPENDIX 1 NORTH AYRSHIRE COUNCIL CORPORATE ASSET MANAGEMENT STRATEGY 2013-2023 JANUARY 2013 Page 1 of 10 1. INTRODUCTION It is widely recognised that asset management is a core component of effective

APPENDIX 1 NORTH AYRSHIRE COUNCIL CORPORATE ASSET MANAGEMENT STRATEGY 2013-2023 JANUARY 2013 Page 1 of 10 1. INTRODUCTION It is widely recognised that asset management is a core component of effective

Review of PIRSA s Cost Recovery Policy and practices, including their application to the Fisheries and Aquaculture Industries Primary Industries and

Review of PIRSA s Cost Recovery Policy and practices, including their application to the Fisheries and Aquaculture Industries Primary Industries and Regions SA 29 July 2015 Contents Executive Summary...

Review of PIRSA s Cost Recovery Policy and practices, including their application to the Fisheries and Aquaculture Industries Primary Industries and Regions SA 29 July 2015 Contents Executive Summary...

Independent cost benefit analysis of broadband and review of regulation

Independent cost benefit analysis of broadband and review of regulation Volume II The costs and benefits of high speed broadband August 2014 1 of 196 The costs and benefits of high speed broadband This

Independent cost benefit analysis of broadband and review of regulation Volume II The costs and benefits of high speed broadband August 2014 1 of 196 The costs and benefits of high speed broadband This

Investa Funds Management Limited Funds Management Financial Risk Management. Policies and Procedures

Investa Funds Management Limited Funds Management Financial Risk Management Policies and Procedures August 2010 Investa Funds Management Limited Funds Management - - - Risk Management Policies and Procedures

Investa Funds Management Limited Funds Management Financial Risk Management Policies and Procedures August 2010 Investa Funds Management Limited Funds Management - - - Risk Management Policies and Procedures

Significant Forecasting Assumptions

Significant Forecasting Assumptions Budget and Forecasting Assumptions and Risk Assessment Schedule 10 of the Local Government Act 2002 requires that the Council identifies the significant forecasting

Significant Forecasting Assumptions Budget and Forecasting Assumptions and Risk Assessment Schedule 10 of the Local Government Act 2002 requires that the Council identifies the significant forecasting

Foreign Exchange Policy and Procedures

Foreign Exchange Policy and Procedures Commencement Date: 23 August, 2006 Category: Finance 1. PURPOSE The purpose of this policy is to regulate Foreign Currency transactions of Material amounts and to

Foreign Exchange Policy and Procedures Commencement Date: 23 August, 2006 Category: Finance 1. PURPOSE The purpose of this policy is to regulate Foreign Currency transactions of Material amounts and to

DEBT MANAGEMENT POLICY

DEBT MANAGEMENT POLICY This policy sets forth the principles that will govern the use of debt to finance University capital projects and assigns responsibilities for the management of University debt.

DEBT MANAGEMENT POLICY This policy sets forth the principles that will govern the use of debt to finance University capital projects and assigns responsibilities for the management of University debt.

INFORMATION TECHNOLOGY SECURITY STANDARDS

INFORMATION TECHNOLOGY SECURITY STANDARDS Version 2.0 December 2013 Table of Contents 1 OVERVIEW 3 2 SCOPE 4 3 STRUCTURE 5 4 ASSET MANAGEMENT 6 5 HUMAN RESOURCES SECURITY 7 6 PHYSICAL AND ENVIRONMENTAL

INFORMATION TECHNOLOGY SECURITY STANDARDS Version 2.0 December 2013 Table of Contents 1 OVERVIEW 3 2 SCOPE 4 3 STRUCTURE 5 4 ASSET MANAGEMENT 6 5 HUMAN RESOURCES SECURITY 7 6 PHYSICAL AND ENVIRONMENTAL

A Guide For Preparing The Financial Information Component Of An Asset Management Plan. Licensing, Monitoring and Customer Protection Division

A Guide For Preparing The Financial Information Component Of An Asset Management Plan Licensing, Monitoring and Customer Protection Division July 2006 Contents 1 Important Notice 2 2 Scope and purpose

A Guide For Preparing The Financial Information Component Of An Asset Management Plan Licensing, Monitoring and Customer Protection Division July 2006 Contents 1 Important Notice 2 2 Scope and purpose

LONG TERM FINANCIAL PLAN (INTERIM) 2012/13 to 2022/23

2012/13 to 2022/23") LONG TERM FINANCIAL PLAN (INTERIM) 2012/13 to 2022/23 INTRODUCTION Long term financial planning is a key element of the Integrated Planning and Reporting Framework. It is the mechanism that enables local

LONG TERM FINANCIAL PLAN (INTERIM) 2012/13 to 2022/23 INTRODUCTION Long term financial planning is a key element of the Integrated Planning and Reporting Framework. It is the mechanism that enables local

Financial Strategy 2016 2026

Financial Strategy 2016 2026 Table of Contents 1. Executive Summary and Overview... 4 1.1 Executive Summary... 4 1.1.1 The Financial Strategy and Long-Term Financial Forecast... 4 1.1.2 The Financial Strategy

Financial Strategy 2016 2026 Table of Contents 1. Executive Summary and Overview... 4 1.1 Executive Summary... 4 1.1.1 The Financial Strategy and Long-Term Financial Forecast... 4 1.1.2 The Financial Strategy

Polish Financial Supervision Authority. Guidelines

Polish Financial Supervision Authority Guidelines on the Management of Information Technology and ICT Environment Security for Insurance and Reinsurance Undertakings Warsaw, 16 December 2014 Table of Contents

Polish Financial Supervision Authority Guidelines on the Management of Information Technology and ICT Environment Security for Insurance and Reinsurance Undertakings Warsaw, 16 December 2014 Table of Contents

Report to Parliament No. 4 for 2011 Information systems governance and security. Financial and Assurance audit. Enhancing public sector accountability

Financial and Assurance audit Report to Parliament No. 4 for 2011 Information systems governance and security ISSN 1834-1128 Enhancing public sector accountability RTP No. 4 cover.indd 1 15/06/2011 3:19:31

Financial and Assurance audit Report to Parliament No. 4 for 2011 Information systems governance and security ISSN 1834-1128 Enhancing public sector accountability RTP No. 4 cover.indd 1 15/06/2011 3:19:31

Consultation paper: Broadband performance monitoring and reporting in the Australian Context

30 Mr Rod Sims Chairman Australian Competition and Consumer Commission Level 35, The Tower 360 Elizabeth Street Melbourne Central Melbourne Vic 3000 Dear Mr Sims Consultation paper: Broadband performance

30 Mr Rod Sims Chairman Australian Competition and Consumer Commission Level 35, The Tower 360 Elizabeth Street Melbourne Central Melbourne Vic 3000 Dear Mr Sims Consultation paper: Broadband performance

National Broadband Network Companies and Access Arrangements Bills

National Broadband Network Companies and Access Arrangements Bills Submission by the Australian Communications Consumer Action Network to the Department for Broadband, Communications and the Digital Economy

National Broadband Network Companies and Access Arrangements Bills Submission by the Australian Communications Consumer Action Network to the Department for Broadband, Communications and the Digital Economy

SCHEDULE 3 Generalist Claims 2015

SCHEDULE 3 Generalist Claims 2015 Nominal Insurer And Schedule 3 (Claims) Page: 1 of 23 Contents Overview... 3 1. Scope of Services... 4 1.1 Claims Services... 4 1.2 Claims Process... 5 1.3 Assessment

SCHEDULE 3 Generalist Claims 2015 Nominal Insurer And Schedule 3 (Claims) Page: 1 of 23 Contents Overview... 3 1. Scope of Services... 4 1.1 Claims Services... 4 1.2 Claims Process... 5 1.3 Assessment

ERGON ENERGY. Fleet. Capital Expenditure Forecast. Fleet Forecast Expenditure Summary 1

ERGON ENERGY Fleet Capital Expenditure O i Fleet Expenditure Summary 1 Contents Contents... 2 1. Introduction... 3 1.1 Purpose... 3 1.2 Summary of expenditure... 3 1.3 Customer outcomes... 4 2. Current

ERGON ENERGY Fleet Capital Expenditure O i Fleet Expenditure Summary 1 Contents Contents... 2 1. Introduction... 3 1.1 Purpose... 3 1.2 Summary of expenditure... 3 1.3 Customer outcomes... 4 2. Current

Provisions, Contingent Liabilities and Contingent Assets

HKAS 37 Issued November 2004 Revised March 2010 Effective for annual periods beginning on or after 1 January 2005 Hong Kong Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets

HKAS 37 Issued November 2004 Revised March 2010 Effective for annual periods beginning on or after 1 January 2005 Hong Kong Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets

COLOCATION SERVICE SCHEDULE

COLOCATION SERVICE SCHEDULE 1. DEFINITIONS AND INTERPRETATION 1.1 Definitions Capitalised terms in this Service Schedule not otherwise defined here have the meaning given in the Master Services Agreement:

COLOCATION SERVICE SCHEDULE 1. DEFINITIONS AND INTERPRETATION 1.1 Definitions Capitalised terms in this Service Schedule not otherwise defined here have the meaning given in the Master Services Agreement:

Classification and Impairment Provisions for Loans/Financing

Provisions for SECTION A... 1 1. Introduction... 1 2. Applicability... 1 3. Legal Provision... 2 4. Effective Date... 2 5. Documents Superseded... 2 SECTION B... 3 6. Compliance with the Malaysian Financial

Provisions for SECTION A... 1 1. Introduction... 1 2. Applicability... 1 3. Legal Provision... 2 4. Effective Date... 2 5. Documents Superseded... 2 SECTION B... 3 6. Compliance with the Malaysian Financial

PRICING AND FINANCIAL PROJECTIONS FOR PRIVATE HEALTH INSURERS

PRACTICE GUIDELINE 699.01 PRICING AND FINANCIAL PROJECTIONS FOR PRIVATE HEALTH INSURERS September 2012 INDEX 1. INTRODUCTION 3 1.1 Application 3 1.2 Classification 3 1.3 Background 3 1.4 Purpose 3 1.5

PRACTICE GUIDELINE 699.01 PRICING AND FINANCIAL PROJECTIONS FOR PRIVATE HEALTH INSURERS September 2012 INDEX 1. INTRODUCTION 3 1.1 Application 3 1.2 Classification 3 1.3 Background 3 1.4 Purpose 3 1.5

1.1 Approve the proposals for the roll-out of the new telephone system as set out in this report.

APPENDIX L Agenda Item No. 13 REPLACEMENT OF TELEPHONE SYSTEM Councillor Cartwright Leader of the Council 1.0 Purpose The purpose of this paper is to recommend the progressive roll-out of new telephone

APPENDIX L Agenda Item No. 13 REPLACEMENT OF TELEPHONE SYSTEM Councillor Cartwright Leader of the Council 1.0 Purpose The purpose of this paper is to recommend the progressive roll-out of new telephone

Contract Management Guideline

www.spb.sa.gov.au Contract Management Guideline Version 3.2 Date Issued January 2014 Review Date January 2014 Principal Contact State Procurement Board Telephone 8226 5001 Contents Overview... 3 Contract

www.spb.sa.gov.au Contract Management Guideline Version 3.2 Date Issued January 2014 Review Date January 2014 Principal Contact State Procurement Board Telephone 8226 5001 Contents Overview... 3 Contract

STANDARD FINANCIAL REPORTING P ROVISIONS, C ONTINGENT L IABILITIES AND C ONTINGENT A SSETS ACCOUNTING STANDARDS BOARD

ACCOUNTING STANDARDS BOARD SEPTEMBER 1998 FRS 12 12 P ROVISIONS, FINANCIAL REPORTING STANDARD C ONTINGENT L IABILITIES AND C ONTINGENT A SSETS ACCOUNTING STANDARDS BOARD Financial Reporting Standard 12

ACCOUNTING STANDARDS BOARD SEPTEMBER 1998 FRS 12 12 P ROVISIONS, FINANCIAL REPORTING STANDARD C ONTINGENT L IABILITIES AND C ONTINGENT A SSETS ACCOUNTING STANDARDS BOARD Financial Reporting Standard 12

GUIDELINES ON THE CLASSIFICATION AND IMPAIRMENT PROVISIONS FOR LOANS / FINANCING FOR LABUAN BANKS

GUIDELINES ON THE CLASSIFICATION AND IMPAIRMENT PROVISIONS FOR LOANS / FINANCING FOR LABUAN BANKS 1.0 Introduction 1.1 The Guidelines set out the minimum requirements on the classification of impaired

GUIDELINES ON THE CLASSIFICATION AND IMPAIRMENT PROVISIONS FOR LOANS / FINANCING FOR LABUAN BANKS 1.0 Introduction 1.1 The Guidelines set out the minimum requirements on the classification of impaired

DRAFT TEMPLATE FOR DISCUSSION CORPORATE GOVERNANCE COMPLIANCE STATEMENT

DRAFT TEMPLATE FOR DISCUSSION CORPORATE GOVERNANCE COMPLIANCE STATEMENT This template is designed for those companies wishing to report on their compliance with the Code of Corporate Governance of the

DRAFT TEMPLATE FOR DISCUSSION CORPORATE GOVERNANCE COMPLIANCE STATEMENT This template is designed for those companies wishing to report on their compliance with the Code of Corporate Governance of the

Capital Expenditure Guidelines

Division of Local Government Department of Premier and Cabinet Capital Expenditure Guidelines December 2010 These are Director General s Guidelines issued pursuant to section 23A of the Local Government

Division of Local Government Department of Premier and Cabinet Capital Expenditure Guidelines December 2010 These are Director General s Guidelines issued pursuant to section 23A of the Local Government

Good Practice Checklist

Investment Governance Good Practice Checklist Governance Structure 1. Existence of critical decision-making bodies e.g. Board of Directors, Investment Committee, In-House Investment Team, External Investment

Investment Governance Good Practice Checklist Governance Structure 1. Existence of critical decision-making bodies e.g. Board of Directors, Investment Committee, In-House Investment Team, External Investment

Resource Management. Determining and managing the people resources on projects can be complex as:

Baseline Resource Management RESOURCE MANAGEMENT Purpose To provide a procedure and associated guidelines to facilitate the management of project people resources. Overview This Phase is used to establish

Baseline Resource Management RESOURCE MANAGEMENT Purpose To provide a procedure and associated guidelines to facilitate the management of project people resources. Overview This Phase is used to establish

Implementation of the National Broadband Network Migration Assurance Policy Consultation Paper

Implementation of the National Broadband Network Migration Assurance Policy Consultation Paper iinet Feedback - Introduction iinet welcomes the opportunity to provide feedback on the Australian Government

Implementation of the National Broadband Network Migration Assurance Policy Consultation Paper iinet Feedback - Introduction iinet welcomes the opportunity to provide feedback on the Australian Government

Review of the Approach to Capital Investments

Review of the Approach to Capital Investments September 2011 This paper examines the RIC s current approach to assessing capital expenditure (Capex), reviews T&TEC s actual Capex and compares this with

Review of the Approach to Capital Investments September 2011 This paper examines the RIC s current approach to assessing capital expenditure (Capex), reviews T&TEC s actual Capex and compares this with

Business Council of Australia

Business Council of Australia Submission to the Department of Broadband, Communications and the Digital Economy on Regulatory Reform for 21st-Century Broadband June 2009 Table of Contents Key points...

Business Council of Australia Submission to the Department of Broadband, Communications and the Digital Economy on Regulatory Reform for 21st-Century Broadband June 2009 Table of Contents Key points...

Capital Works Management Framework

POLICY DOCUMENT Capital Works Management Framework Policy for managing risks in the planning and delivery of Queensland Government building projects Department of Public Works The concept of the asset

POLICY DOCUMENT Capital Works Management Framework Policy for managing risks in the planning and delivery of Queensland Government building projects Department of Public Works The concept of the asset

CODE FOR UNDERWRITING AGENTS: SYNDICATE EXPENSES. Explanatory Note. This code was issued in a regulatory bulletin 069/00 dated 12 September 2000

CODE FOR UNDERWRITING AGENTS: SYNDICATE EXPENSES This code was issued in a regulatory bulletin 069/00 dated 12 September 2000 Explanatory Note This code has been made under the Core Principles Byelaw in

CODE FOR UNDERWRITING AGENTS: SYNDICATE EXPENSES This code was issued in a regulatory bulletin 069/00 dated 12 September 2000 Explanatory Note This code has been made under the Core Principles Byelaw in

Agenda Item No: 2 Page Numbers: 1-6 EAST RIDING OF YORKSHIRE COUNCIL THE CABINET 1 FEBRUARY 2011

Report to: The Ca binet To appr ove as a correct record the Minutes of t he meeting of The Cabinet held on 1 Febr uary 2011 Contact Officer: 01 March 2011 Iain Edmiston Senior Committee Manager Telephone

Report to: The Ca binet To appr ove as a correct record the Minutes of t he meeting of The Cabinet held on 1 Febr uary 2011 Contact Officer: 01 March 2011 Iain Edmiston Senior Committee Manager Telephone

Considerations for firms thinking of using third-party technology (off-the-shelf) banking solutions

banking solutions") Financial Conduct Authority Considerations for firms thinking of using third-party technology (off-the-shelf) banking solutions Introduction 1. A firm has many choices when designing its operating model

Financial Conduct Authority Considerations for firms thinking of using third-party technology (off-the-shelf) banking solutions Introduction 1. A firm has many choices when designing its operating model

PASSENGER AND LIGHT COMMERCIAL VEHICLE

Governance Division Employment Policy Section ACTPS NON-EXECUTIVE PASSENGER AND LIGHT COMMERCIAL VEHICLE MANAGEMENT GUIDELINES May 2010 CONTENTS 1. DEFINITIONS 2. INTRODUCTION 3. FLEET MANAGEMENT AND REPORTING

Governance Division Employment Policy Section ACTPS NON-EXECUTIVE PASSENGER AND LIGHT COMMERCIAL VEHICLE MANAGEMENT GUIDELINES May 2010 CONTENTS 1. DEFINITIONS 2. INTRODUCTION 3. FLEET MANAGEMENT AND REPORTING

IP network. Collaboration of Governments and private sector, its impact on the success of Internet

IP network Day one Collaboration of Governments and private sector, its impact on the success of Internet IP applications services definitions Differences between IP networks and PSTN The European policies

IP network Day one Collaboration of Governments and private sector, its impact on the success of Internet IP applications services definitions Differences between IP networks and PSTN The European policies

SIP TRUNKS SERVICE SCHEDULE

SIP TRUNKS SERVICE SCHEDULE 1 SERVICE DESCRIPTION 1.1 This Service Schedule applies to SIP Trunks service (SIP Trunks Service). The SIP Trunks Service enables a switch to be connected to the PSTN via SIP/IP/RTP

SIP TRUNKS SERVICE SCHEDULE 1 SERVICE DESCRIPTION 1.1 This Service Schedule applies to SIP Trunks service (SIP Trunks Service). The SIP Trunks Service enables a switch to be connected to the PSTN via SIP/IP/RTP

APPLICATION OF THE KING III REPORT ON CORPORATE GOVERNANCE PRINCIPLES

APPLICATION OF THE KING III REPORT ON CORPORATE GOVERNANCE PRINCIPLES Ethical Leadership and Corporate Citizenship The board should provide effective leadership based on ethical foundation. that the company

APPLICATION OF THE KING III REPORT ON CORPORATE GOVERNANCE PRINCIPLES Ethical Leadership and Corporate Citizenship The board should provide effective leadership based on ethical foundation. that the company

EBA-GL-2015-02. 23 July 2015. Guidelines. on the minimum list of qualitative and quantitative recovery plan indicators

EBA-GL-2015-02 23 July 2015 Guidelines on the minimum list of qualitative and quantitative recovery plan indicators Contents EBA Guidelines on the minimum list of qualitative and quantitative recovery

EBA-GL-2015-02 23 July 2015 Guidelines on the minimum list of qualitative and quantitative recovery plan indicators Contents EBA Guidelines on the minimum list of qualitative and quantitative recovery

Objectives and key requirements of this Prudential Standard

Prudential Standard SPS 220 Risk Management Objectives and key requirements of this Prudential Standard This Prudential Standard establishes requirements for an RSE licensee to have systems for identifying,

Prudential Standard SPS 220 Risk Management Objectives and key requirements of this Prudential Standard This Prudential Standard establishes requirements for an RSE licensee to have systems for identifying,

Hutchison 3G Australia Public submission to the Commission regarding proposed changes to the RAF RKR's

Hutchison 3G Australia Public submission to the Commission regarding proposed changes to the RAF RKR's Table of Contents 1. Introduction 1 2. Executive Summary 1 3. Commercial-in-confidence 1 4. Timing

Hutchison 3G Australia Public submission to the Commission regarding proposed changes to the RAF RKR's Table of Contents 1. Introduction 1 2. Executive Summary 1 3. Commercial-in-confidence 1 4. Timing

Rule change request. 18 September 2013

Reform of the distribution network pricing arrangements under the National Electricity Rules to provide better guidance for setting, and consulting on, cost-reflective distribution network pricing structures

Reform of the distribution network pricing arrangements under the National Electricity Rules to provide better guidance for setting, and consulting on, cost-reflective distribution network pricing structures

Confident progress delivering transformation

Confident progress delivering transformation Q2 & half year results 2005/6 10th November 2005 BT Group plc Half year results 2005/6 Sir Christopher Bland -Chairman Forward-looking statements - caution

Confident progress delivering transformation Q2 & half year results 2005/6 10th November 2005 BT Group plc Half year results 2005/6 Sir Christopher Bland -Chairman Forward-looking statements - caution

Customer Responsiveness Strategy

Customer Responsiveness Strategy Dated 23 June 2006. Telstra Corporation Limited (ABN 33 051 775 556) ( Telstra ) Disclaimer This Customer Responsiveness Strategy is being published in furtherance of Telstra

Customer Responsiveness Strategy Dated 23 June 2006. Telstra Corporation Limited (ABN 33 051 775 556) ( Telstra ) Disclaimer This Customer Responsiveness Strategy is being published in furtherance of Telstra

Subject: Prudential Indicators 2016/17 to 2020/21

CLACKMANNANSHIRE COUNCIL THIS PAPER RELATES TO ITEM 04 ON THE AGENDA Report to: Special Council Date: 23 February 2016 Subject: Prudential Indicators 2016/17 to 2020/21 Report by: Depute Chief Executive

CLACKMANNANSHIRE COUNCIL THIS PAPER RELATES TO ITEM 04 ON THE AGENDA Report to: Special Council Date: 23 February 2016 Subject: Prudential Indicators 2016/17 to 2020/21 Report by: Depute Chief Executive

Reserve Bank of Fiji Insurance Supervision Policy Statement No. 8 MINIMUM REQUIREMENTS FOR RISK MANAGEMENT FRAMEWORKS OF LICENSED INSURERS IN FIJI

Reserve Bank of Fiji Insurance Supervision Policy Statement No. 8 NOTICE TO INSURANCE COMPANIES LICENSED UNDER THE INSURANCE ACT 1998 MINIMUM REQUIREMENTS FOR RISK MANAGEMENT FRAMEWORKS OF LICENSED INSURERS

Reserve Bank of Fiji Insurance Supervision Policy Statement No. 8 NOTICE TO INSURANCE COMPANIES LICENSED UNDER THE INSURANCE ACT 1998 MINIMUM REQUIREMENTS FOR RISK MANAGEMENT FRAMEWORKS OF LICENSED INSURERS

2 COMMENCEMENT DATE 5 3 DEFINITIONS 5 4 MATERIALITY 8. 5 DOCUMENTATION 9 5.1 Requirement for a Report 9 5.2 Content of a Report 9

PROFESSIONAL STANDARD 300 VALUATIONS OF GENERAL INSURANCE CLAIMS INDEX 1 INTRODUCTION 3 1.1 Application 3 1.2 Classification 3 1.3 Background 3 1.4 Purpose 4 1.5 Previous versions 4 1.6 Legislation and

PROFESSIONAL STANDARD 300 VALUATIONS OF GENERAL INSURANCE CLAIMS INDEX 1 INTRODUCTION 3 1.1 Application 3 1.2 Classification 3 1.3 Background 3 1.4 Purpose 4 1.5 Previous versions 4 1.6 Legislation and

APPLICATION OF KING III CORPORATE GOVERNANCE PRINCIPLES 2014

WOOLWORTHS HOLDINGS LIMITED CORPORATE GOVERNANCE PRINCIPLES 2014 CORPORATE GOVERNANCE PRINCIPLES 2014 CORPORATE GOVERNANCE PRINCIPLES 2014 This table is a useful reference to each of the King III principles

WOOLWORTHS HOLDINGS LIMITED CORPORATE GOVERNANCE PRINCIPLES 2014 CORPORATE GOVERNANCE PRINCIPLES 2014 CORPORATE GOVERNANCE PRINCIPLES 2014 This table is a useful reference to each of the King III principles

ACTUARIAL ADVICE TO A LIFE INSURANCE COMPANY OR FRIENDLY SOCIETY

PROFESSIONAL STANDARD 200 ACTUARIAL ADVICE TO A LIFE INSURANCE COMPANY OR FRIENDLY SOCIETY INDEX 1. INTRODUCTION 3 1.1 Application 3 1.2 About this standard 3 1.3 Other relevant documents 4 1.4 Background

PROFESSIONAL STANDARD 200 ACTUARIAL ADVICE TO A LIFE INSURANCE COMPANY OR FRIENDLY SOCIETY INDEX 1. INTRODUCTION 3 1.1 Application 3 1.2 About this standard 3 1.3 Other relevant documents 4 1.4 Background

Measuring performance Update to Insurance Key Performance Indicators

Measuring performance Update to Insurance Key Performance Indicators John Hele Member of Executive Board and CFO of ING Group Madrid 19 September 2008 www.ing.com Agenda Performance Indicators: Background

Measuring performance Update to Insurance Key Performance Indicators John Hele Member of Executive Board and CFO of ING Group Madrid 19 September 2008 www.ing.com Agenda Performance Indicators: Background

Maintained in accordance with Section 15.5 of the Undertakings given to the Competition Commission

Macquarie UK Broadcast Holdings Group Regulatory Accounting Principles and Methodologies Maintained in accordance with Section 15.5 of the Undertakings given to the Competition Commission Dated: 15 October

Macquarie UK Broadcast Holdings Group Regulatory Accounting Principles and Methodologies Maintained in accordance with Section 15.5 of the Undertakings given to the Competition Commission Dated: 15 October

REGULATORY ACCOUNTING GUIDELINES FOR TRINIDAD AND TOBAGO ELECTRICITY COMMISSION DRAFT FOR CONSULTATION

REGULATORY ACCOUNTING GUIDELINES FOR TRINIDAD AND TOBAGO ELECTRICITY COMMISSION DRAFT FOR CONSULTATION January 2008 C O N T E N T S Page No. 1. Overview 1 2. Introduction 3 3. RIC s Regulatory Framework

REGULATORY ACCOUNTING GUIDELINES FOR TRINIDAD AND TOBAGO ELECTRICITY COMMISSION DRAFT FOR CONSULTATION January 2008 C O N T E N T S Page No. 1. Overview 1 2. Introduction 3 3. RIC s Regulatory Framework

Engin response to ACCC discussion paper. Telstra s Undertakings for the PSTN Originating and Terminating and LCS Access Services

Engin response to ACCC discussion paper Telstra s Undertakings for the PSTN Originating and Terminating and LCS Access Services June 2006 Summary One of the main reasons engin entered the broadband telephony

Engin response to ACCC discussion paper Telstra s Undertakings for the PSTN Originating and Terminating and LCS Access Services June 2006 Summary One of the main reasons engin entered the broadband telephony

Financial Stability Standards for Securities Settlement Facilities

Attachment 4 Financial Stability Standards for Securities Settlement Facilities Introduction The Financial Stability Standards for Securities Settlement Facilities (SSF Standards) are determined under

Attachment 4 Financial Stability Standards for Securities Settlement Facilities Introduction The Financial Stability Standards for Securities Settlement Facilities (SSF Standards) are determined under

Telecom Half Year Result 6 months ended 31 December 2005

2 February 2006 MEDIA RELEASE Telecom Half Year Result 6 months ended 31 December 2005 Telecom today reported a net loss of NZ$466 million after tax for the half year to December 31, 2005, after a NZ$897

2 February 2006 MEDIA RELEASE Telecom Half Year Result 6 months ended 31 December 2005 Telecom today reported a net loss of NZ$466 million after tax for the half year to December 31, 2005, after a NZ$897

Executive Summary. Model Structure. General Economic Environment and Assumptions