The term structure of Russian interest rates

|

|

|

- Merryl Robbins

- 10 years ago

- Views:

Transcription

1 The term structure of Russian interest rates Stanislav Anatolyev New Economic School, Moscow Sergey Korepanov EvrazHolding, Moscow Corresponding author. Address: Stanislav Anatolyev, New Economic School, Nakhimovsky Pr., 47, Moscow, Russia. We would like to thank Dmitry Novikov for helpful discussions, and all members of the NES research project Dynamics and Predictability in Russian Financial Markets for useful comments and suggestions. 1

2 The term structure of Russian interest rates Abstract Using the series of Moscow Interbank Offer Rates, we estimate a flexible parametrization of the diffusion process following the approach of Aït-Sahalia (1996) of matching parametric and nonparametric estimates of the marginal density. On the basis of the estimated model we compute the implied term structure using simulations. Key words: Stochastic differential equation; Marginal density; Semi-parametric estimation; MIBOR; Term structure of interest rates. JEL classification numbers: G12, G15, C14, C15, C22 2

3 1 Introduction The term structure of interest rates is critical for pricing fixed-income securities. Termstructure modeling is one of the major success stories in the application of financial models to everyday business problems (Duffie, 2001, Chapter 7). A key element of a term structure is a model for the process followed by the instantaneous interest rate. There exist several ways to estimate a diffusion process each having its strengths and shortcomings. In earlier years researches attempted to parsimoniously specify the drift and diffusion functions so that the difference equation could be solved analytically (e.g., Cox, Ingersoll and Ross, 1985). Lately researchers have moved to estimating the functions nonparametrically, or specifying them in more flexible ways and utilizing computer-intensive methods. For example, Chan at al. (1992) run GMM on moment conditions that are approximately implied by popular parametrizations of the differential equation, while Stanton (1997) performs nonparametric estimation of first-order approximations to the drift and diffusion functions. Hansen and Scheinkman (1995) propose to run GMM on a set of moment conditions that are an exact implication of a flexibly parametrized differential equation; this approach, however, leads to unpleasant concerns about a choice of the so called test function (see Hansen et al., 1997). Another possibility to employ a flexible parametrization is the approach of Aït-Sahalia (1996) of constructing an estimator and specification test based on minimization of the distance between a non-parametric and implied parametric forms of a marginal density. Even though this approach suffers from information loss due to the use of a marginal density (Pritsker, 1997), the suggestion of Aït-Sahalia (1996) to base the specification test on a transitional density leads to considerable computational difficulties in implementing the test. In the present paper, using the series of Moscow Interbank Offer Rates (MIBOR), we explore some parametrizations of the differential equation and construct a reliable model for 3

4 the term structure that may be further used for many possible applications. The analysis of Russian interest rates from the position of continuous time modeling, to our knowledge, has been encountered only in Dvorkovitch et al. (2000) who modeled the demand for Russian Government securities from non-residents. The authors employed non-parametric estimation of the drift and diffusion using the Stanton (1997) methodology, without any further investigation of properties of the data-generating process. In contrast, we follow the approach of Aït-Sahalia (1996) to arrive at point parameter estimates and a specification test statistic; in order to obtain inferences on parameter values we use a simple bootstrap procedure. Finally, on the basis of the estimated semi-parametric model we compute the implied term structure of interest rates using simulations. The paper is organized as follows. In Section 2 we briefly describe the semi-parametric estimator and the specification test for correct parameterization of the model. In Section 3 we estimate a flexible specification for the drift and diffusion functions and test the model using the MIBOR series. In Section 4 we compute the term structure of interest rates. 2 Semi-parametric estimator and specification test To model the behavior of instantaneous interest rate, we use a diffusion process that admits the representation by the stationary stochastic differential equation dx t = µ(x t )dt + σ(x t )db t. It is known (e.g., Aït-Sahalia, 1996) that for a particular parameterization of the drift and diffusion functions µ(x, θ) and σ 2 (x, θ), the parametric form for the marginal density can be derived as π(x, θ) = ξ(θ) x σ 2 (x, θ) exp 2µ(s, θ) x 0 σ 2 (s, θ) ds, 4

methodology, without any further investigation of properties of the data-generating process.")

5 where ξ(θ) = ( + ( 1 x ) 1 σ 2 (x, θ) exp 2µ(s, θ) dx) x 0 σ 2 (s, θ) ds, where x 0 is arbitrary. Aït-Sahalia (1996) proposes the following estimator of θ based on the quadratic distance from the parametric marginal density and its non-parametric estimate: ˆθ = arg min q Θ + (π(x, q) ˆπ(x)) 2 π 0 (x)dx. (1) Here, π 0 (x) is the true marginal density, and ˆπ(x) is its non-parametric kernel estimator obtained from the sample {x i } n i=1 : ˆπ(x) = 1 nh n n ( ) x xi K, i=1 where K( ) is a kernel function and h n is a bandwidth parameter. By the analogy principle, we replace the integral in (1) by its sample analog 1 n h n n (π(x t, θ) ˆπ(x t )) 2. (2) t=1 Aït-Sahalia (1996) shows that this estimator is consistent and asymptotically normal: n(ˆθ θ0 ) d N(0, Ω M ), where Ω M is a complicated expression that depends on the kernel and the value of θ. The specification test is based on the idea that if the parameterization of the model is correct, the deviation of the parametric density from the non-parametric estimate should not be big. The test is based on the statistic ˆM = h n whose null asymptotic distribution is n (π(ˆθ, x i ) ˆπ(x i )) 2, i=1 h 1/2 n ( ˆM E M ) d N(0, V M ), where E M and V M may be estimated by ( + ) ( Ê M = K 2 1 (x)dx n ) n ˆπ(x i ) i=1 5

Here, π 0 (x) is the true marginal density, and ˆπ(x) is its non-parametric kernel estimator obtained from the sample {x i } n i=1 : ˆπ(x) = 1 nh n n ( ) x xi K, i=1 where K( ) is a kernel")

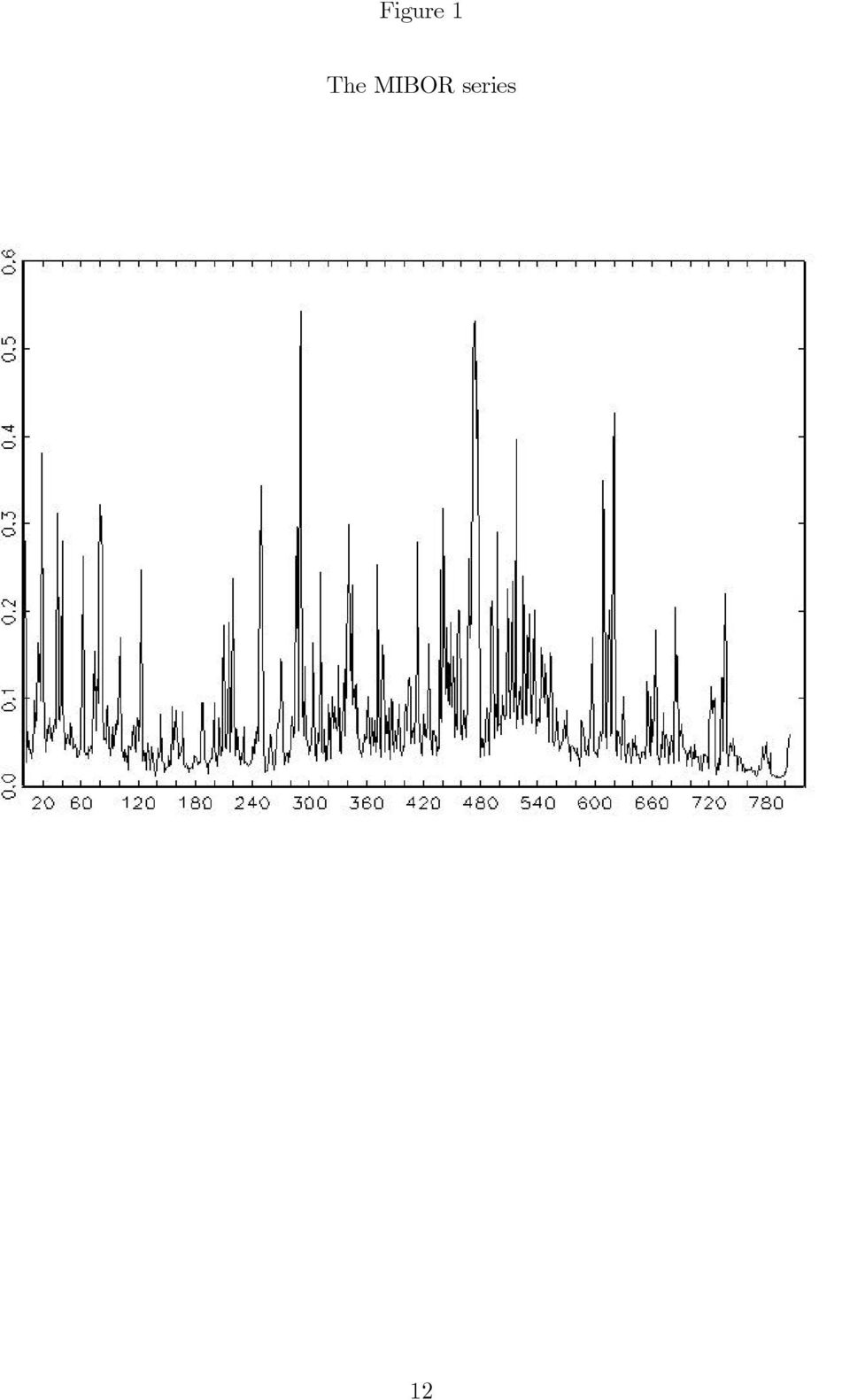

6 and ˆV M = ( + { + 2 ) ( 1 K(u)K(u + x)du} dx n For the Gaussian kernel which is used throughout, ) n ˆπ 3 (x i ). i=1 + K 2 (x)dx = 1 2 π, + { + } 2 K(u)K(u + x)du dx = 1 2 2π. To test the null hypothesis at the significance level α, the critical value is ĉ(α) = ÊM + z 1 α h n ˆVM, and the null hypothesis of correct specification is rejected if ˆM ĉ(α). 3 Empirical results The data is the series of daily observations of one-day MIBOR from January 1, 2000 to May 1, 2003, totaling to 805 observations. The data are obtained from the official Central Bank of Russia site. The rate is determined daily from interbank credit trades at the Moscow Interbank Currency Exchange. The instantaneous interest rate corresponding to the observed one was computed by r = 365 ln ) (1 + robs. 365 As can be seen from Figure 1, the MIBOR series looks much smoother than the Eurodollar rate (cf. Aït-Sahalia, 1996, Figure 2). The non-parametric estimator for the marginal density was computed 1 using the Gaussian kernel (other kernels produced very similar results), and shown in Figure 2. After some experimentation, h was set at To compute the critical value for the test statistic ˆM 1 All procedures were written in GAUSS. When numerical optimization was required, the optmum procedure was employed. 6

7 we employ the following characteristics of the data: 1 n n ˆπ(x i ) = 6.394, i=1 1 n n ˆπ 3 (x i ) = i=1 Then ÊM = 1.79, ˆV M = 74.6, and the 5% critical value is c 0.05 = First of all, fitting the popular Cox Ingersoll Ross (CIR), Vasicek (V) and Brennan Schwartz (BS) models CIR: µ(x, θ) = α 0 + α 1 x, σ(x, θ) = β 0 x, V: µ(x, θ) = α 0 + α 1 x, σ(x, θ) = β 0, BS: µ(x, θ) = α 0 + α 1 x, σ(x, θ) = β 0 x, has been completely unsuccessful: the test statistics are huge compared to the critical value (e.g., it equals ˆM = 72 for the CIR model). This demonstrates that these analytically attractive models are too simple (in particular, the linearity of the drift function) for the Russian interest rate data. In order to arrive at a flexible parametrization, we follow Stanton (1997) and estimate the first-order approximations to the drift and diffusion non-parametrically using the Nadaraya Watson estimator with the Gaussian kernel. As the forms of emerged curves are quite close to those in Aït-Sahalia (1996), we employ his parametrization µ(x, θ) = α 0 + α 1 x + α 2 x 2 + α 3 x, σ(x, θ) = β 0 + β 1 x + β 2 x β 3. Since computation of asymptotic standard errors is problematic because of a complicated form of the matrix Ω M, we employ a simple bootstrap procedure. As the proposed semiparametric estimator does not utilize information on transitional features of the data, there is no need to preserve the temporal structure of the series, hence we adopted the basic IID bootstrap resampling. The computational difficulties are present, however, because of the need to achieve convergence for each bootstrap sample. This precludes obtaining a large number of bootstrap estimates. In our procedure, the bootstrap sample contained 50 7

for the Russian interest rate data.")

8 estimates of the parameters vector. Standard errors were computed straightforwardly, taking into account that the bootstrap distribution is centered around estimated values rather than the true parameters. The estimation results are reported in Table 1 2, and the resulting marginal density is depicted on Figure 2. The value of the test statistics is ˆM = which is far smaller than the 5% critical value. Thus, the Aït-Sahalia (1996) flexible form fits the MIBOR data very well, and the estimated model has a strong mean reversion property. The MIBOR and Eurodollar deposit rates possess similar features, except that there is no evidence for several regimes in the MIBOR case. The two regimes for the Eurodollar are most probably due to a monetary policy shift in the beginning of 80 s, while there was no structural change in Russia during the period under consideration. Note also that the value of the test statistics is appreciably below the minimal one for the Eurodollar rate, which is a consequence of a greater smoothness of the MIBOR and the absence of regime switches. 4 The term structure One of most important applications of the diffusion model is derivation of the term structure of interest rates. If Λ t,s is a price at time t of a bond maturing time s, then it could be represented from the no-arbitrage principle as ( s )] Λ t,s = E t [exp r u du. t The term structure is usually represented as the yield curve y (τ) = ln(λ t,t+τ) τ 2 As a robustness check, we have also re-estimated the model after splitting the sample into two equal halves. All parameter estimates on the two subperiods (not shown) are quite close, and are withing two standard deviations from the estimates on Table 1. 8

flexible form fits the MIBOR data very well, and the estimated model has a strong mean reversion property.")

9 One way to compute the term structure is to explicitly solve the Feyman Kac differential equation. However, this option is unavailable for flexible parametrizations, hence we compute the term structure using simulations. The result is shown in Figure 3. The yield curve is monotonically increasing and slightly concave, without any humps. 5 Concluding remarks Using the spot MIBOR series, we have estimated a flexible parametrization of the diffusion process following the approach of Aït-Sahalia (1996). The Aït-Sahalia (1996) parametrization fitted the MIBOR series very well, with decisive acceptance of the model by the specification test. On the basis of the estimated model we have computed the implied term structure using simulations. The corresponding yield curve turns out to be increasing and slightly concave. References 1. Aït-Sahalia, Y., Testing continuous time models of the spot interest rate. Review of Financial Studies 9, Chan, K.C., Karolyi, G.A., Longstaff, F.A., Sanders A.B., An empirical comparison of alternative models of the short-term interest rate. Journal of Finance 47, Cox, J.C., Ingersoll, J.E. Jr., Ross, S.A., Theory of the term structure of interest rates. Econometrica 53, Dvorkovitch, A., Novikov, D., Urga, G., Risk factors influencing the demand for government securities by non-residents: The case of Russia before the August 1988 crisis. Working paper, IRMI, CUBS. 9

.")

10 5. Duffie, D., Dynamic asset pricing theory. Princeton University Press. 6. Hansen, L.P., Scheinkman, J.A., Back to the future: Generating moment implications for continuous time Markov processes. Econometrica 63, Hansen, L.P., Conley, T.G., Luttmer, E.G.J., Scheinkman, J.A., Short-term interest rates as subordinated diffusions. Review of Financial Studies 10, Pritsker, M., Nonparametric density estimation and tests of continuous time interest rate models. Review of Financial Studies 11, Stanton, R., A nonparametric model of term structure dynamics and the market price of interest rate risk. Journal of Finance 52,

11 Table 1 Estimates of parameters of the drift and diffusion functions Function µ(x, θ) σ(x, θ) Parameter α 0 α 1 α 2 α 3 β 0 β 1 β 2 β 3 Point estimate Standard error (0.55) (0.54) (0.36) (0.66) (0.01) (0.11) (0.24) (0.10) Notes: The estimates are obtained by minimizing (2), the sample distance between the parametric and non-parametric densities. The standard errors are obtained by bootstrap. For more details, see the text. 11

Notes: The estimates are obtained by minimizing (2), the sample distance between the parametric and")

12 Figure 1 The MIBOR series 12

13 Figure 2 Parametric andnon-parametric estimates ofthe marginal density 13

14 Figure 3 The term structure of interest rates 14

Bias in the Estimation of Mean Reversion in Continuous-Time Lévy Processes

Bias in the Estimation of Mean Reversion in Continuous-Time Lévy Processes Yong Bao a, Aman Ullah b, Yun Wang c, and Jun Yu d a Purdue University, IN, USA b University of California, Riverside, CA, USA

Bias in the Estimation of Mean Reversion in Continuous-Time Lévy Processes Yong Bao a, Aman Ullah b, Yun Wang c, and Jun Yu d a Purdue University, IN, USA b University of California, Riverside, CA, USA

INDIRECT INFERENCE (prepared for: The New Palgrave Dictionary of Economics, Second Edition)

") INDIRECT INFERENCE (prepared for: The New Palgrave Dictionary of Economics, Second Edition) Abstract Indirect inference is a simulation-based method for estimating the parameters of economic models. Its

INDIRECT INFERENCE (prepared for: The New Palgrave Dictionary of Economics, Second Edition) Abstract Indirect inference is a simulation-based method for estimating the parameters of economic models. Its

Pricing Interest-Rate- Derivative Securities

Pricing Interest-Rate- Derivative Securities John Hull Alan White University of Toronto This article shows that the one-state-variable interest-rate models of Vasicek (1977) and Cox, Ingersoll, and Ross

Pricing Interest-Rate- Derivative Securities John Hull Alan White University of Toronto This article shows that the one-state-variable interest-rate models of Vasicek (1977) and Cox, Ingersoll, and Ross

Do option prices support the subjective probabilities of takeover completion derived from spot prices? Sergey Gelman March 2005

Do option prices support the subjective probabilities of takeover completion derived from spot prices? Sergey Gelman March 2005 University of Muenster Wirtschaftswissenschaftliche Fakultaet Am Stadtgraben

Do option prices support the subjective probabilities of takeover completion derived from spot prices? Sergey Gelman March 2005 University of Muenster Wirtschaftswissenschaftliche Fakultaet Am Stadtgraben

ARBITRAGE-FREE OPTION PRICING MODELS. Denis Bell. University of North Florida

ARBITRAGE-FREE OPTION PRICING MODELS Denis Bell University of North Florida Modelling Stock Prices Example American Express In mathematical finance, it is customary to model a stock price by an (Ito) stochatic

ARBITRAGE-FREE OPTION PRICING MODELS Denis Bell University of North Florida Modelling Stock Prices Example American Express In mathematical finance, it is customary to model a stock price by an (Ito) stochatic

Local classification and local likelihoods

Local classification and local likelihoods November 18 k-nearest neighbors The idea of local regression can be extended to classification as well The simplest way of doing so is called nearest neighbor

Local classification and local likelihoods November 18 k-nearest neighbors The idea of local regression can be extended to classification as well The simplest way of doing so is called nearest neighbor

When to Refinance Mortgage Loans in a Stochastic Interest Rate Environment

When to Refinance Mortgage Loans in a Stochastic Interest Rate Environment Siwei Gan, Jin Zheng, Xiaoxia Feng, and Dejun Xie Abstract Refinancing refers to the replacement of an existing debt obligation

When to Refinance Mortgage Loans in a Stochastic Interest Rate Environment Siwei Gan, Jin Zheng, Xiaoxia Feng, and Dejun Xie Abstract Refinancing refers to the replacement of an existing debt obligation

Schonbucher Chapter 9: Firm Value and Share Priced-Based Models Updated 07-30-2007

Schonbucher Chapter 9: Firm alue and Share Priced-Based Models Updated 07-30-2007 (References sited are listed in the book s bibliography, except Miller 1988) For Intensity and spread-based models of default

Schonbucher Chapter 9: Firm alue and Share Priced-Based Models Updated 07-30-2007 (References sited are listed in the book s bibliography, except Miller 1988) For Intensity and spread-based models of default

Nonparametric adaptive age replacement with a one-cycle criterion

Nonparametric adaptive age replacement with a one-cycle criterion P. Coolen-Schrijner, F.P.A. Coolen Department of Mathematical Sciences University of Durham, Durham, DH1 3LE, UK e-mail: [email protected]

Nonparametric adaptive age replacement with a one-cycle criterion P. Coolen-Schrijner, F.P.A. Coolen Department of Mathematical Sciences University of Durham, Durham, DH1 3LE, UK e-mail: [email protected]

Affine-structure models and the pricing of energy commodity derivatives

Affine-structure models and the pricing of energy commodity derivatives Nikos K Nomikos [email protected] Cass Business School, City University London Joint work with: Ioannis Kyriakou, Panos Pouliasis

Affine-structure models and the pricing of energy commodity derivatives Nikos K Nomikos [email protected] Cass Business School, City University London Joint work with: Ioannis Kyriakou, Panos Pouliasis

The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series.

data, like asset returns or growth rates of macroeconomic time series.") Cointegration The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series. Economic theory, however, often implies equilibrium

Cointegration The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series. Economic theory, however, often implies equilibrium

The Fair Valuation of Life Insurance Participating Policies: The Mortality Risk Role

The Fair Valuation of Life Insurance Participating Policies: The Mortality Risk Role Massimiliano Politano Department of Mathematics and Statistics University of Naples Federico II Via Cinthia, Monte S.Angelo

The Fair Valuation of Life Insurance Participating Policies: The Mortality Risk Role Massimiliano Politano Department of Mathematics and Statistics University of Naples Federico II Via Cinthia, Monte S.Angelo

Maximum likelihood estimation of mean reverting processes

Maximum likelihood estimation of mean reverting processes José Carlos García Franco Onward, Inc. [email protected] Abstract Mean reverting processes are frequently used models in real options. For

Maximum likelihood estimation of mean reverting processes José Carlos García Franco Onward, Inc. [email protected] Abstract Mean reverting processes are frequently used models in real options. For

How To Model The Yield Curve

Modeling Bond Yields in Finance and Macroeconomics Francis X. Diebold, Monika Piazzesi, and Glenn D. Rudebusch* January 2005 Francis X. Diebold, Department of Economics, University of Pennsylvania, Philadelphia,

Modeling Bond Yields in Finance and Macroeconomics Francis X. Diebold, Monika Piazzesi, and Glenn D. Rudebusch* January 2005 Francis X. Diebold, Department of Economics, University of Pennsylvania, Philadelphia,

Short rate models: Pricing bonds in short rate models

IV. Shortratemodels:Pricingbondsinshortratemodels p.1/19 IV. Short rate models: Pricing bonds in short rate models Beáta Stehlíková Financial derivatives, winter term 2014/2015 Faculty of Mathematics,

IV. Shortratemodels:Pricingbondsinshortratemodels p.1/19 IV. Short rate models: Pricing bonds in short rate models Beáta Stehlíková Financial derivatives, winter term 2014/2015 Faculty of Mathematics,

Statistics in Retail Finance. Chapter 6: Behavioural models

Statistics in Retail Finance 1 Overview > So far we have focussed mainly on application scorecards. In this chapter we shall look at behavioural models. We shall cover the following topics:- Behavioural

Statistics in Retail Finance 1 Overview > So far we have focussed mainly on application scorecards. In this chapter we shall look at behavioural models. We shall cover the following topics:- Behavioural

No-arbitrage conditions for cash-settled swaptions

No-arbitrage conditions for cash-settled swaptions Fabio Mercurio Financial Engineering Banca IMI, Milan Abstract In this note, we derive no-arbitrage conditions that must be satisfied by the pricing function

No-arbitrage conditions for cash-settled swaptions Fabio Mercurio Financial Engineering Banca IMI, Milan Abstract In this note, we derive no-arbitrage conditions that must be satisfied by the pricing function

INTERNATIONAL COMPARISON OF INTEREST RATE GUARANTEES IN LIFE INSURANCE

INTERNATIONAL COMPARISON OF INTEREST RATE GUARANTEES IN LIFE INSURANCE J. DAVID CUMMINS, KRISTIAN R. MILTERSEN, AND SVEIN-ARNE PERSSON Abstract. Interest rate guarantees seem to be included in life insurance

INTERNATIONAL COMPARISON OF INTEREST RATE GUARANTEES IN LIFE INSURANCE J. DAVID CUMMINS, KRISTIAN R. MILTERSEN, AND SVEIN-ARNE PERSSON Abstract. Interest rate guarantees seem to be included in life insurance

Pricing European and American bond option under the Hull White extended Vasicek model

1 Academic Journal of Computational and Applied Mathematics /August 2013/ UISA Pricing European and American bond option under the Hull White extended Vasicek model Eva Maria Rapoo 1, Mukendi Mpanda 2

1 Academic Journal of Computational and Applied Mathematics /August 2013/ UISA Pricing European and American bond option under the Hull White extended Vasicek model Eva Maria Rapoo 1, Mukendi Mpanda 2

From the help desk: Bootstrapped standard errors

The Stata Journal (2003) 3, Number 1, pp. 71 80 From the help desk: Bootstrapped standard errors Weihua Guan Stata Corporation Abstract. Bootstrapping is a nonparametric approach for evaluating the distribution

The Stata Journal (2003) 3, Number 1, pp. 71 80 From the help desk: Bootstrapped standard errors Weihua Guan Stata Corporation Abstract. Bootstrapping is a nonparametric approach for evaluating the distribution

Pricing and calibration in local volatility models via fast quantization

Pricing and calibration in local volatility models via fast quantization Parma, 29 th January 2015. Joint work with Giorgia Callegaro and Martino Grasselli Quantization: a brief history Birth: back to

Pricing and calibration in local volatility models via fast quantization Parma, 29 th January 2015. Joint work with Giorgia Callegaro and Martino Grasselli Quantization: a brief history Birth: back to

PS 271B: Quantitative Methods II. Lecture Notes

PS 271B: Quantitative Methods II Lecture Notes Langche Zeng [email protected] The Empirical Research Process; Fundamental Methodological Issues 2 Theory; Data; Models/model selection; Estimation; Inference.

PS 271B: Quantitative Methods II Lecture Notes Langche Zeng [email protected] The Empirical Research Process; Fundamental Methodological Issues 2 Theory; Data; Models/model selection; Estimation; Inference.

On the long run relationship between gold and silver prices A note

Global Finance Journal 12 (2001) 299 303 On the long run relationship between gold and silver prices A note C. Ciner* Northeastern University College of Business Administration, Boston, MA 02115-5000,

Global Finance Journal 12 (2001) 299 303 On the long run relationship between gold and silver prices A note C. Ciner* Northeastern University College of Business Administration, Boston, MA 02115-5000,

The information content of lagged equity and bond yields

Economics Letters 68 (2000) 179 184 www.elsevier.com/ locate/ econbase The information content of lagged equity and bond yields Richard D.F. Harris *, Rene Sanchez-Valle School of Business and Economics,

Economics Letters 68 (2000) 179 184 www.elsevier.com/ locate/ econbase The information content of lagged equity and bond yields Richard D.F. Harris *, Rene Sanchez-Valle School of Business and Economics,

Black and Scholes - A Review of Option Pricing Model

CAPM Option Pricing Sven Husmann a, Neda Todorova b a Department of Business Administration, European University Viadrina, Große Scharrnstraße 59, D-15230 Frankfurt (Oder, Germany, Email: [email protected],

CAPM Option Pricing Sven Husmann a, Neda Todorova b a Department of Business Administration, European University Viadrina, Große Scharrnstraße 59, D-15230 Frankfurt (Oder, Germany, Email: [email protected],

The Best of Both Worlds:

The Best of Both Worlds: A Hybrid Approach to Calculating Value at Risk Jacob Boudoukh 1, Matthew Richardson and Robert F. Whitelaw Stern School of Business, NYU The hybrid approach combines the two most

The Best of Both Worlds: A Hybrid Approach to Calculating Value at Risk Jacob Boudoukh 1, Matthew Richardson and Robert F. Whitelaw Stern School of Business, NYU The hybrid approach combines the two most

Statistical Machine Learning

Statistical Machine Learning UoC Stats 37700, Winter quarter Lecture 4: classical linear and quadratic discriminants. 1 / 25 Linear separation For two classes in R d : simple idea: separate the classes

Statistical Machine Learning UoC Stats 37700, Winter quarter Lecture 4: classical linear and quadratic discriminants. 1 / 25 Linear separation For two classes in R d : simple idea: separate the classes

An Internal Model for Operational Risk Computation

An Internal Model for Operational Risk Computation Seminarios de Matemática Financiera Instituto MEFF-RiskLab, Madrid http://www.risklab-madrid.uam.es/ Nicolas Baud, Antoine Frachot & Thierry Roncalli

An Internal Model for Operational Risk Computation Seminarios de Matemática Financiera Instituto MEFF-RiskLab, Madrid http://www.risklab-madrid.uam.es/ Nicolas Baud, Antoine Frachot & Thierry Roncalli

Loan guarantee portfolios and joint loan guarantees with stochastic interest rates

The Quarterly Review of Economics and Finance 46 (2006) 16 35 Loan guarantee portfolios and joint loan guarantees with stochastic interest rates Chuang-Chang Chang a,, San-Lin Chung b, Min-Teh Yu c a Department

The Quarterly Review of Economics and Finance 46 (2006) 16 35 Loan guarantee portfolios and joint loan guarantees with stochastic interest rates Chuang-Chang Chang a,, San-Lin Chung b, Min-Teh Yu c a Department

How To Understand The Theory Of Probability

Graduate Programs in Statistics Course Titles STAT 100 CALCULUS AND MATR IX ALGEBRA FOR STATISTICS. Differential and integral calculus; infinite series; matrix algebra STAT 195 INTRODUCTION TO MATHEMATICAL

Graduate Programs in Statistics Course Titles STAT 100 CALCULUS AND MATR IX ALGEBRA FOR STATISTICS. Differential and integral calculus; infinite series; matrix algebra STAT 195 INTRODUCTION TO MATHEMATICAL

MEAN-REVERSION ACROSS MENA STOCK MARKETS: IMPLICATIONS FOR PORTFOLIO ALLOCATIONS

MEAN-REVERSION ACROSS MENA STOCK MARKETS: IMPLICATIONS FOR PORTFOLIO ALLOCATIONS Sam Hakim and Simon Neaime Energetix and American University of Beirut Working Paper 2026 Abstract Are stock market returns

MEAN-REVERSION ACROSS MENA STOCK MARKETS: IMPLICATIONS FOR PORTFOLIO ALLOCATIONS Sam Hakim and Simon Neaime Energetix and American University of Beirut Working Paper 2026 Abstract Are stock market returns

Parametric Curves. (Com S 477/577 Notes) Yan-Bin Jia. Oct 8, 2015

Yan-Bin Jia. Oct 8, 2015") Parametric Curves (Com S 477/577 Notes) Yan-Bin Jia Oct 8, 2015 1 Introduction A curve in R 2 (or R 3 ) is a differentiable function α : [a,b] R 2 (or R 3 ). The initial point is α[a] and the final point

Parametric Curves (Com S 477/577 Notes) Yan-Bin Jia Oct 8, 2015 1 Introduction A curve in R 2 (or R 3 ) is a differentiable function α : [a,b] R 2 (or R 3 ). The initial point is α[a] and the final point

Some Research Problems in Uncertainty Theory

Journal of Uncertain Systems Vol.3, No.1, pp.3-10, 2009 Online at: www.jus.org.uk Some Research Problems in Uncertainty Theory aoding Liu Uncertainty Theory Laboratory, Department of Mathematical Sciences

Journal of Uncertain Systems Vol.3, No.1, pp.3-10, 2009 Online at: www.jus.org.uk Some Research Problems in Uncertainty Theory aoding Liu Uncertainty Theory Laboratory, Department of Mathematical Sciences

Volatility Density Forecasting & Model Averaging Imperial College Business School, London

Imperial College Business School, London June 25, 2010 Introduction Contents Types of Volatility Predictive Density Risk Neutral Density Forecasting Empirical Volatility Density Forecasting Density model

Imperial College Business School, London June 25, 2010 Introduction Contents Types of Volatility Predictive Density Risk Neutral Density Forecasting Empirical Volatility Density Forecasting Density model

Stock Option Pricing Using Bayes Filters

Stock Option Pricing Using Bayes Filters Lin Liao [email protected] Abstract When using Black-Scholes formula to price options, the key is the estimation of the stochastic return variance. In this

Stock Option Pricing Using Bayes Filters Lin Liao [email protected] Abstract When using Black-Scholes formula to price options, the key is the estimation of the stochastic return variance. In this

Examples. David Ruppert. April 25, 2009. Cornell University. Statistics for Financial Engineering: Some R. Examples. David Ruppert.

Cornell University April 25, 2009 Outline 1 2 3 4 A little about myself BA and MA in mathematics PhD in statistics in 1977 taught in the statistics department at North Carolina for 10 years have been in

Cornell University April 25, 2009 Outline 1 2 3 4 A little about myself BA and MA in mathematics PhD in statistics in 1977 taught in the statistics department at North Carolina for 10 years have been in

MULTIPLE DEFAULTS AND MERTON'S MODEL L. CATHCART, L. EL-JAHEL

ISSN 1744-6783 MULTIPLE DEFAULTS AND MERTON'S MODEL L. CATHCART, L. EL-JAHEL Tanaka Business School Discussion Papers: TBS/DP04/12 London: Tanaka Business School, 2004 Multiple Defaults and Merton s Model

ISSN 1744-6783 MULTIPLE DEFAULTS AND MERTON'S MODEL L. CATHCART, L. EL-JAHEL Tanaka Business School Discussion Papers: TBS/DP04/12 London: Tanaka Business School, 2004 Multiple Defaults and Merton s Model

The Behavior of Bonds and Interest Rates. An Impossible Bond Pricing Model. 780 w Interest Rate Models

780 w Interest Rate Models The Behavior of Bonds and Interest Rates Before discussing how a bond market-maker would delta-hedge, we first need to specify how bonds behave. Suppose we try to model a zero-coupon

780 w Interest Rate Models The Behavior of Bonds and Interest Rates Before discussing how a bond market-maker would delta-hedge, we first need to specify how bonds behave. Suppose we try to model a zero-coupon

Markov modeling of Gas Futures

Markov modeling of Gas Futures p.1/31 Markov modeling of Gas Futures Leif Andersen Banc of America Securities February 2008 Agenda Markov modeling of Gas Futures p.2/31 This talk is based on a working

Markov modeling of Gas Futures p.1/31 Markov modeling of Gas Futures Leif Andersen Banc of America Securities February 2008 Agenda Markov modeling of Gas Futures p.2/31 This talk is based on a working

Notes on Black-Scholes Option Pricing Formula

. Notes on Black-Scholes Option Pricing Formula by De-Xing Guan March 2006 These notes are a brief introduction to the Black-Scholes formula, which prices the European call options. The essential reading

. Notes on Black-Scholes Option Pricing Formula by De-Xing Guan March 2006 These notes are a brief introduction to the Black-Scholes formula, which prices the European call options. The essential reading

On the mathematical theory of splitting and Russian roulette

On the mathematical theory of splitting and Russian roulette techniques St.Petersburg State University, Russia 1. Introduction Splitting is an universal and potentially very powerful technique for increasing

On the mathematical theory of splitting and Russian roulette techniques St.Petersburg State University, Russia 1. Introduction Splitting is an universal and potentially very powerful technique for increasing

Optimization of technical trading strategies and the profitability in security markets

Economics Letters 59 (1998) 249 254 Optimization of technical trading strategies and the profitability in security markets Ramazan Gençay 1, * University of Windsor, Department of Economics, 401 Sunset,

Economics Letters 59 (1998) 249 254 Optimization of technical trading strategies and the profitability in security markets Ramazan Gençay 1, * University of Windsor, Department of Economics, 401 Sunset,

Monte Carlo Methods in Finance

Author: Yiyang Yang Advisor: Pr. Xiaolin Li, Pr. Zari Rachev Department of Applied Mathematics and Statistics State University of New York at Stony Brook October 2, 2012 Outline Introduction 1 Introduction

Author: Yiyang Yang Advisor: Pr. Xiaolin Li, Pr. Zari Rachev Department of Applied Mathematics and Statistics State University of New York at Stony Brook October 2, 2012 Outline Introduction 1 Introduction

One-year reserve risk including a tail factor : closed formula and bootstrap approaches

One-year reserve risk including a tail factor : closed formula and bootstrap approaches Alexandre Boumezoued R&D Consultant Milliman Paris [email protected] Yoboua Angoua Non-Life Consultant

One-year reserve risk including a tail factor : closed formula and bootstrap approaches Alexandre Boumezoued R&D Consultant Milliman Paris [email protected] Yoboua Angoua Non-Life Consultant

Bootstrapping Big Data

Bootstrapping Big Data Ariel Kleiner Ameet Talwalkar Purnamrita Sarkar Michael I. Jordan Computer Science Division University of California, Berkeley {akleiner, ameet, psarkar, jordan}@eecs.berkeley.edu

Bootstrapping Big Data Ariel Kleiner Ameet Talwalkar Purnamrita Sarkar Michael I. Jordan Computer Science Division University of California, Berkeley {akleiner, ameet, psarkar, jordan}@eecs.berkeley.edu

Bandwidth Selection for Nonparametric Distribution Estimation

Bandwidth Selection for Nonparametric Distribution Estimation Bruce E. Hansen University of Wisconsin www.ssc.wisc.edu/~bhansen May 2004 Abstract The mean-square efficiency of cumulative distribution function

Bandwidth Selection for Nonparametric Distribution Estimation Bruce E. Hansen University of Wisconsin www.ssc.wisc.edu/~bhansen May 2004 Abstract The mean-square efficiency of cumulative distribution function

Marshall-Olkin distributions and portfolio credit risk

Marshall-Olkin distributions and portfolio credit risk Moderne Finanzmathematik und ihre Anwendungen für Banken und Versicherungen, Fraunhofer ITWM, Kaiserslautern, in Kooperation mit der TU München und

Marshall-Olkin distributions and portfolio credit risk Moderne Finanzmathematik und ihre Anwendungen für Banken und Versicherungen, Fraunhofer ITWM, Kaiserslautern, in Kooperation mit der TU München und

ANALYSIS OF EUROPEAN, AMERICAN AND JAPANESE GOVERNMENT BOND YIELDS

Applied Time Series Analysis ANALYSIS OF EUROPEAN, AMERICAN AND JAPANESE GOVERNMENT BOND YIELDS Stationarity, cointegration, Granger causality Aleksandra Falkowska and Piotr Lewicki TABLE OF CONTENTS 1.

Applied Time Series Analysis ANALYSIS OF EUROPEAN, AMERICAN AND JAPANESE GOVERNMENT BOND YIELDS Stationarity, cointegration, Granger causality Aleksandra Falkowska and Piotr Lewicki TABLE OF CONTENTS 1.

Consistent Pricing of FX Options

Consistent Pricing of FX Options Antonio Castagna Fabio Mercurio Banca IMI, Milan In the current markets, options with different strikes or maturities are usually priced with different implied volatilities.

Consistent Pricing of FX Options Antonio Castagna Fabio Mercurio Banca IMI, Milan In the current markets, options with different strikes or maturities are usually priced with different implied volatilities.

A Coefficient of Variation for Skewed and Heavy-Tailed Insurance Losses. Michael R. Powers[ 1 ] Temple University and Tsinghua University

![A Coefficient of Variation for Skewed and Heavy-Tailed Insurance Losses. Michael R. Powers[ 1 ] Temple University and Tsinghua University](/thumbs/35/17199255.jpg "A Coefficient of Variation for Skewed and Heavy-Tailed Insurance Losses. Michael R. Powers[ 1 ] Temple University and Tsinghua University") A Coefficient of Variation for Skewed and Heavy-Tailed Insurance Losses Michael R. Powers[ ] Temple University and Tsinghua University Thomas Y. Powers Yale University [June 2009] Abstract We propose a

A Coefficient of Variation for Skewed and Heavy-Tailed Insurance Losses Michael R. Powers[ ] Temple University and Tsinghua University Thomas Y. Powers Yale University [June 2009] Abstract We propose a

Dynamic Jump Intensities and Risk Premiums in Crude Oil Futures and Options Markets

Dynamic Jump Intensities and Risk Premiums in Crude Oil Futures and Options Markets Peter Christoffersen University of Toronto, CBS, and CREATES Kris Jacobs University of Houston and Tilburg University

Dynamic Jump Intensities and Risk Premiums in Crude Oil Futures and Options Markets Peter Christoffersen University of Toronto, CBS, and CREATES Kris Jacobs University of Houston and Tilburg University

Increasing for all. Convex for all. ( ) Increasing for all (remember that the log function is only defined for ). ( ) Concave for all.

Increasing for all (remember that the log function is only defined for ). ( ) Concave for all.") 1. Differentiation The first derivative of a function measures by how much changes in reaction to an infinitesimal shift in its argument. The largest the derivative (in absolute value), the faster is evolving.

1. Differentiation The first derivative of a function measures by how much changes in reaction to an infinitesimal shift in its argument. The largest the derivative (in absolute value), the faster is evolving.

Nonparametric Statistics

Nonparametric Statistics References Some good references for the topics in this course are 1. Higgins, James (2004), Introduction to Nonparametric Statistics 2. Hollander and Wolfe, (1999), Nonparametric

Nonparametric Statistics References Some good references for the topics in this course are 1. Higgins, James (2004), Introduction to Nonparametric Statistics 2. Hollander and Wolfe, (1999), Nonparametric

BayesX - Software for Bayesian Inference in Structured Additive Regression

BayesX - Software for Bayesian Inference in Structured Additive Regression Thomas Kneib Faculty of Mathematics and Economics, University of Ulm Department of Statistics, Ludwig-Maximilians-University Munich

BayesX - Software for Bayesian Inference in Structured Additive Regression Thomas Kneib Faculty of Mathematics and Economics, University of Ulm Department of Statistics, Ludwig-Maximilians-University Munich

Chapter 5: Bivariate Cointegration Analysis

Chapter 5: Bivariate Cointegration Analysis 1 Contents: Lehrstuhl für Department Empirische of Wirtschaftsforschung Empirical Research and und Econometrics Ökonometrie V. Bivariate Cointegration Analysis...

Chapter 5: Bivariate Cointegration Analysis 1 Contents: Lehrstuhl für Department Empirische of Wirtschaftsforschung Empirical Research and und Econometrics Ökonometrie V. Bivariate Cointegration Analysis...

Monte Carlo testing with Big Data

Monte Carlo testing with Big Data Patrick Rubin-Delanchy University of Bristol & Heilbronn Institute for Mathematical Research Joint work with: Axel Gandy (Imperial College London) with contributions from:

Monte Carlo testing with Big Data Patrick Rubin-Delanchy University of Bristol & Heilbronn Institute for Mathematical Research Joint work with: Axel Gandy (Imperial College London) with contributions from:

Master of Mathematical Finance: Course Descriptions

Master of Mathematical Finance: Course Descriptions CS 522 Data Mining Computer Science This course provides continued exploration of data mining algorithms. More sophisticated algorithms such as support

Master of Mathematical Finance: Course Descriptions CS 522 Data Mining Computer Science This course provides continued exploration of data mining algorithms. More sophisticated algorithms such as support

On Marginal Effects in Semiparametric Censored Regression Models

On Marginal Effects in Semiparametric Censored Regression Models Bo E. Honoré September 3, 2008 Introduction It is often argued that estimation of semiparametric censored regression models such as the

On Marginal Effects in Semiparametric Censored Regression Models Bo E. Honoré September 3, 2008 Introduction It is often argued that estimation of semiparametric censored regression models such as the

A non-gaussian Ornstein-Uhlenbeck process for electricity spot price modeling and derivatives pricing

A non-gaussian Ornstein-Uhlenbeck process for electricity spot price modeling and derivatives pricing Thilo Meyer-Brandis Center of Mathematics for Applications / University of Oslo Based on joint work

A non-gaussian Ornstein-Uhlenbeck process for electricity spot price modeling and derivatives pricing Thilo Meyer-Brandis Center of Mathematics for Applications / University of Oslo Based on joint work

Modelling Intraday Volatility in European Bond Market

Modelling Intraday Volatility in European Bond Market Hanyu Zhang ICMA Centre, Henley Business School Young Finance Scholars Conference 8th May,2014 Outline 1 Introduction and Literature Review 2 Data

Modelling Intraday Volatility in European Bond Market Hanyu Zhang ICMA Centre, Henley Business School Young Finance Scholars Conference 8th May,2014 Outline 1 Introduction and Literature Review 2 Data

Interpreting Kullback-Leibler Divergence with the Neyman-Pearson Lemma

Interpreting Kullback-Leibler Divergence with the Neyman-Pearson Lemma Shinto Eguchi a, and John Copas b a Institute of Statistical Mathematics and Graduate University of Advanced Studies, Minami-azabu

Interpreting Kullback-Leibler Divergence with the Neyman-Pearson Lemma Shinto Eguchi a, and John Copas b a Institute of Statistical Mathematics and Graduate University of Advanced Studies, Minami-azabu

Using kernel methods to visualise crime data

Submission for the 2013 IAOS Prize for Young Statisticians Using kernel methods to visualise crime data Dr. Kieran Martin and Dr. Martin Ralphs [email protected] [email protected] Office

Submission for the 2013 IAOS Prize for Young Statisticians Using kernel methods to visualise crime data Dr. Kieran Martin and Dr. Martin Ralphs [email protected] [email protected] Office

Exam P - Total 23/23 - 1 -

Exam P Learning Objectives Schools will meet 80% of the learning objectives on this examination if they can show they meet 18.4 of 23 learning objectives outlined in this table. Schools may NOT count a

Exam P Learning Objectives Schools will meet 80% of the learning objectives on this examination if they can show they meet 18.4 of 23 learning objectives outlined in this table. Schools may NOT count a

Non Parametric Inference

Maura Department of Economics and Finance Università Tor Vergata Outline 1 2 3 Inverse distribution function Theorem: Let U be a uniform random variable on (0, 1). Let X be a continuous random variable

Maura Department of Economics and Finance Università Tor Vergata Outline 1 2 3 Inverse distribution function Theorem: Let U be a uniform random variable on (0, 1). Let X be a continuous random variable

A Game Theoretical Framework for Adversarial Learning

A Game Theoretical Framework for Adversarial Learning Murat Kantarcioglu University of Texas at Dallas Richardson, TX 75083, USA muratk@utdallas Chris Clifton Purdue University West Lafayette, IN 47907,

A Game Theoretical Framework for Adversarial Learning Murat Kantarcioglu University of Texas at Dallas Richardson, TX 75083, USA muratk@utdallas Chris Clifton Purdue University West Lafayette, IN 47907,

CHINA S OFFICIAL RATES AND BOND YIELDS

CHINA S OFFICIAL RATES AND BOND YIELDS Longzhen Fan School of Management, Fudan University Anders C. Johansson Stockholm School of Economics Working Paper 3 March 2009 Postal address: P.O. Box 6501, S-113

CHINA S OFFICIAL RATES AND BOND YIELDS Longzhen Fan School of Management, Fudan University Anders C. Johansson Stockholm School of Economics Working Paper 3 March 2009 Postal address: P.O. Box 6501, S-113

The TED spread trade: illustration of the analytics using Bloomberg

The TED spread trade: illustration of the analytics using Bloomberg Aaron Nematnejad January 2003 1 The views, thoughts and opinions expressed in this article represent those of the author in his individual

The TED spread trade: illustration of the analytics using Bloomberg Aaron Nematnejad January 2003 1 The views, thoughts and opinions expressed in this article represent those of the author in his individual

**BEGINNING OF EXAMINATION** The annual number of claims for an insured has probability function: , 0 < q < 1.

**BEGINNING OF EXAMINATION** 1. You are given: (i) The annual number of claims for an insured has probability function: 3 p x q q x x ( ) = ( 1 ) 3 x, x = 0,1,, 3 (ii) The prior density is π ( q) = q,

**BEGINNING OF EXAMINATION** 1. You are given: (i) The annual number of claims for an insured has probability function: 3 p x q q x x ( ) = ( 1 ) 3 x, x = 0,1,, 3 (ii) The prior density is π ( q) = q,

Why Long Term Forward Interest Rates (Almost) Always Slope Downwards

Always Slope Downwards") Why Long Term Forward Interest Rates (Almost) Always Slope Downwards Roger H. Brown Warburg Dillon Read Stephen M. Schaefer London Business School, May 1, 2000 Corresponding author: Stephen M. Schaefer,

Why Long Term Forward Interest Rates (Almost) Always Slope Downwards Roger H. Brown Warburg Dillon Read Stephen M. Schaefer London Business School, May 1, 2000 Corresponding author: Stephen M. Schaefer,

Learning Curve Interest Rate Futures Contracts Moorad Choudhry

Learning Curve Interest Rate Futures Contracts Moorad Choudhry YieldCurve.com 2004 Page 1 The market in short-term interest rate derivatives is a large and liquid one, and the instruments involved are

Learning Curve Interest Rate Futures Contracts Moorad Choudhry YieldCurve.com 2004 Page 1 The market in short-term interest rate derivatives is a large and liquid one, and the instruments involved are

Does the Spot Curve Contain Information on Future Monetary Policy in Colombia? Por : Juan Manuel Julio Román. No. 463

Does the Spot Curve Contain Information on Future Monetary Policy in Colombia? Por : Juan Manuel Julio Román No. 463 2007 tá - Colombia - Bogotá - Colombia - Bogotá - Colombia - Bogotá - Colombia - Bogotá

Does the Spot Curve Contain Information on Future Monetary Policy in Colombia? Por : Juan Manuel Julio Román No. 463 2007 tá - Colombia - Bogotá - Colombia - Bogotá - Colombia - Bogotá - Colombia - Bogotá

Statistics Graduate Courses

Statistics Graduate Courses STAT 7002--Topics in Statistics-Biological/Physical/Mathematics (cr.arr.).organized study of selected topics. Subjects and earnable credit may vary from semester to semester.

Statistics Graduate Courses STAT 7002--Topics in Statistics-Biological/Physical/Mathematics (cr.arr.).organized study of selected topics. Subjects and earnable credit may vary from semester to semester.

Probability and Random Variables. Generation of random variables (r.v.)

") Probability and Random Variables Method for generating random variables with a specified probability distribution function. Gaussian And Markov Processes Characterization of Stationary Random Process Linearly

Probability and Random Variables Method for generating random variables with a specified probability distribution function. Gaussian And Markov Processes Characterization of Stationary Random Process Linearly

OPTIONS, FUTURES, & OTHER DERIVATI

Fifth Edition OPTIONS, FUTURES, & OTHER DERIVATI John C. Hull Maple Financial Group Professor of Derivatives and Risk Manage, Director, Bonham Center for Finance Joseph L. Rotinan School of Management

Fifth Edition OPTIONS, FUTURES, & OTHER DERIVATI John C. Hull Maple Financial Group Professor of Derivatives and Risk Manage, Director, Bonham Center for Finance Joseph L. Rotinan School of Management

RECOVERY RATES, DEFAULT PROBABILITIES AND THE CREDIT CYCLE

RECOVERY RATES, DEFAULT PROBABILITIES AND THE CREDIT CYCLE Max Bruche and Carlos González-Aguado CEMFI Working Paper No. 0612 September 2006 CEMFI Casado del Alisal 5; 28014 Madrid Tel. (34) 914 290 551.

RECOVERY RATES, DEFAULT PROBABILITIES AND THE CREDIT CYCLE Max Bruche and Carlos González-Aguado CEMFI Working Paper No. 0612 September 2006 CEMFI Casado del Alisal 5; 28014 Madrid Tel. (34) 914 290 551.

Import Prices and Inflation

Import Prices and Inflation James D. Hamilton Department of Economics, University of California, San Diego Understanding the consequences of international developments for domestic inflation is an extremely

Import Prices and Inflation James D. Hamilton Department of Economics, University of California, San Diego Understanding the consequences of international developments for domestic inflation is an extremely