Expert Meeting on CYBERLAWS AND REGULATIONS FOR ENHANCING E-COMMERCE: INCLUDING CASE STUDIES AND LESSONS LEARNED March 2015

|

|

|

- Derick Matthews

- 10 years ago

- Views:

Transcription

1 Expert Meeting on CYBERLAWS AND REGULATIONS FOR ENHANCING E-COMMERCE: INCLUDING CASE STUDIES AND LESSONS LEARNED March 2015 Cyberlaws and Regulations for Enhancing E-Commerce The Case for Payment Instruments and Systems By Maria Chiara Malaguti Senior Legal Expert Payments Systems Development Group World Bank The views reflected are those of the author and do not necessarily reflect the views of UNCTAD

2 CYBER LAWS AND REGULATIONS FOR ENHANCING E-COMMERCE THE CASE FOR PAYMENT INSTRUMENTS AND SYSTEMS MARIA CHIARA MALAGUTI Senior Legal Expert Payment Systems Development Group World Bank

3 INNOVATIVE RETAIL PAYMENT INSTRUMENTS

4 WB Global Financial Development Report 2014 Selected methods of payment 2011 mobiles electronically credit cards debit cards B:developing e. LB: developed e.

5 E-MONEY : STORED-VALUE PRODUCTS FOR UNBANKED POPULATION Pre-paid cards and mobiles Branchless-banking (international) remittances

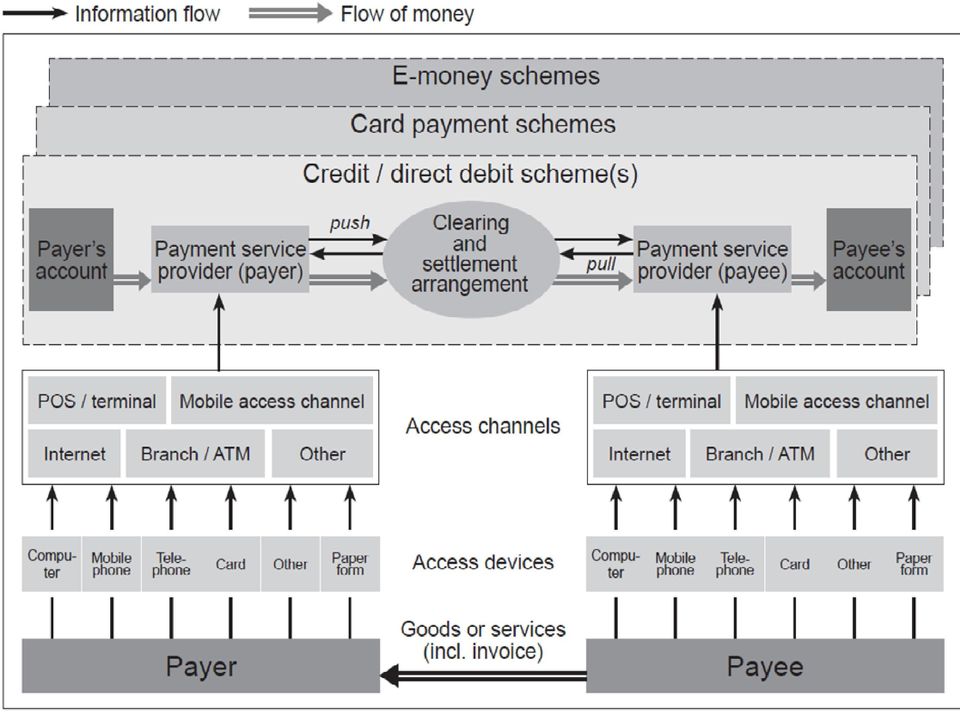

6 PAYMENT PROCESS Tables from CPSS, INNOVATIONS IN RETAIL PAYMENTS - May 2012 CPMI, NON-BANKS IN RETAIL PAYMENTS September 2014

7 CLEARING AND SETTLEMENT

8 Retail payments landscape stylized model

9 STAGE 1: PRE-TRANSACTION All activities involved in creating the initial infrastructure: payments customer acquisition provision of actual payment instrument (card issuance including personalization, delivery and activation, e-money wallet, cheque manufacturing) provision of related hardware, software and network infrastructure (ATM and POS terminals, cheque and card readers, application processing and web-hosting services, shopping cart software, cheque verification software, connection to payment gateway and related services) provision of security-related technology support (digital signature services, online transaction security systems) other value added services such as provision of data centre services, e-invoicing etc.

other value added services such as provision of data centre services, e-invoicing")

10 STAGE 2: AUTHORIZATION Processes and activities that enable a payment transaction to be authorized and approved before it can be completed: Provision of back-end services (connection between networks and payment instrument issuers, software and related services to issuers to enable pay-or-no-pay decision and fraud screening, checking funds availability and actual debit of payer s account etc) fraud and risk management services to customers and issuers of payment instruments (PIN verification and other identity authentication services, transaction monitoring, sending of alerts to customers) ex ante compliance services (database and application services for identifying and reporting of suspicious transactions).

ex ante compliance services (database and application services for identifying and reporting of")

11 STAGE 3: CLEARING Activities which enable the submission of claims by members in the payment system against each other and, calculation and dissemination of information relating to payment/receipt obligations of respective members: provision of services to merchants to sort their sales information and submit claims to respective networks calculation of net positions of members by networks ACH operators transmission of clearing orders distribution of advices, etc.

12 STAGE 4: SETTLEMENT Activities directly related to the posting of credits and debits in the account of the bank/financial institution with the settlement bank (central bank or any other bank) as well as in the accounts of the final payer (customer) and beneficiary (merchant or individual). It also includes activities related to (reversal) accounting for return of transactions/payments.

.")

13 STAGE 5: POST-TRANSACTION Processes and activities related to provision of various types of value added services for. statement generation (preparation, dispatch and notification of statements to consumers and merchants), reconciliation (matching invoices and payments), dispute resolution (chargeback and dispute processing services), reporting and data analysis, ex post compliance services (reporting to authorities for AML and terrorist financing, back-feeding to ex ante databases)

14 HOW DOES ALL OF THIS AFFECT REGULATION/LEGISLATION? HOW LEGAL BARRIERS AND REGULATORY ARBITRAGE AFFECT INNOVATION AND DEVELOPMENT?

15 MAJOR LEGAL ISSUES LINKED TO E-COMPONENT Legal recognition of electronic transfers and electronic archives [e-cheques] Data privacy and security Authentication/electronic signature Fraud and mistake [Irrevocability and finality of orders, enforceability of netting schemes, protection against insolvency]

16 MAJOR REGULATORY ISSUES LINKED TO E-COMPONENT Role of non-banks Risk governance Access to systems/competition (essential facilities? Silos models?) Interoperability Outsourcing and agency Stored-value instruments and protection of customers funds

Interoperability Outsourcing and agency Stored-value")

17 HIGH-LEVEL RECOMMENDATIONS FROM INTERNATIONAL BEST PRACTICES Eliminate legal barriers: you can use existing legal standards (UNCITRAL Model Law on Credit Transfers to be updated but still of good use) Innovation includes both: technology and business models. Consider them jointly Take a technology-neutral approach Proportionality as a value: not to under-regulate, not to over-regulate Adopt an holistic approach: innovation in payments has to be seen within the National Payments System

18 Settlemen t Processing Definitions Major issues Regulatory Objectives of the Central Bank -Finality -System -Clearing -Netting -Central Bank Accounts -Collateral -Central Securities Depositary (CSD) -Access to systems (Banks, MFI, Government, any PSP??) -Interoperability -Operational role of the CB/intraday credit -Oversight -Oversight -Designation vs. licensing of systems -Systemic risk (financial stability) -Systemic risk (financial stability) -Contestability of the market -Efficiency Legal issues -Finality -Netting -Insolvency -Protection of collateral Services to clients -Payment Service Provider (PSP) -Payment instrument -Who should be a PSP? (only banks, also MFI, any entity duly monitored, including money transfers and MNOs??) -Agents -Outsourcing -Oversight vs. supervision -License vs. approval vs. registration -Requirements to enter the market - E-money -On-going oversight -Contestability of the market -Efficiency -Consumer (users) protection -AML/KYC -Access to finance -Redress procedures -Electronic means of transfer (mistake, fraud, allocation of risks) --electronic records -Checks truncation

-Payment instrument -Who should be a PSP? (only banks, also MFI, any entity duly monitored, including money transfers and MNOs?")

19 NPSA Electronic Transactions Law Oversight regulation EFT regulation Guidelines Individual instruments Outsourcing/Agents

20 PPP Goals Thank you Payment Systems Development Group The World Bank 19

Expert Meeting on CYBERLAWS AND REGULATIONS FOR ENHANCING E-COMMERCE: INCLUDING CASE STUDIES AND LESSONS LEARNED. 25-27 March 2015

Expert Meeting on CYBERLAWS AND REGULATIONS FOR ENHANCING E-COMMERCE: INCLUDING CASE STUDIES AND LESSONS LEARNED 25-27 March 2015 Central Bank of Kenya Paper By Stephen Mwaura Nduati Head, National Payment

Expert Meeting on CYBERLAWS AND REGULATIONS FOR ENHANCING E-COMMERCE: INCLUDING CASE STUDIES AND LESSONS LEARNED 25-27 March 2015 Central Bank of Kenya Paper By Stephen Mwaura Nduati Head, National Payment

Selecting a Secure and Compliant Prepaid Reloadable Card Program

Selecting a Secure and Compliant Prepaid Reloadable Card Program Merchants and other distributors of prepaid general purpose reloadable (GPR) cards should review program compliance as an integral part

Selecting a Secure and Compliant Prepaid Reloadable Card Program Merchants and other distributors of prepaid general purpose reloadable (GPR) cards should review program compliance as an integral part

ACQUIRER OR ACQUIRING BANK A financial institution (often a bank) where a merchant has an account to process transactions and card payments

where a merchant has an account to process transactions and card payments") A TO Z JARGON BUSTER A ACQUIRER OR ACQUIRING BANK A financial institution (often a bank) where a merchant has an account to process transactions and card payments ATM Automated Teller Machine. Unattended,

A TO Z JARGON BUSTER A ACQUIRER OR ACQUIRING BANK A financial institution (often a bank) where a merchant has an account to process transactions and card payments ATM Automated Teller Machine. Unattended,

Code of Conduct for Mobile Money Providers

Code of Conduct for Mobile Money Providers SOUNDNESS OF SERVICES FAIR TREATMENT OF CUSTOMERS SECURITY OF THE MOBILE NETWORK AND CHANNEL VERSION 2 - OCTOBER 2015 Introduction This Code of Conduct identifies

Code of Conduct for Mobile Money Providers SOUNDNESS OF SERVICES FAIR TREATMENT OF CUSTOMERS SECURITY OF THE MOBILE NETWORK AND CHANNEL VERSION 2 - OCTOBER 2015 Introduction This Code of Conduct identifies

PAYMENT SYSTEMS IN GHANA

PAYMENT SYSTEMS IN GHANA OVERVIEW The payment system is the entire matrix of institutional infrastructure arrangements and processes in a country set up to enable economic agents (individuals, businesses,

PAYMENT SYSTEMS IN GHANA OVERVIEW The payment system is the entire matrix of institutional infrastructure arrangements and processes in a country set up to enable economic agents (individuals, businesses,

Payment Card Industry (PCI) Data Security Standard

Data Security Standard") Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Self-Assessment Questionnaire D Service Providers For use with PCI DSS Version 3.1 Revision 1.1 July 2015 Section 1: Assessment

Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Self-Assessment Questionnaire D Service Providers For use with PCI DSS Version 3.1 Revision 1.1 July 2015 Section 1: Assessment

Payment Card Industry (PCI) Data Security Standard

Data Security Standard") Payment Card Industry (PCI) Data Standard Attestation of Compliance for Self-Assessment Questionnaire D Service Providers Version 3.1 April 2015 Section 1: Assessment Information Instructions for Submission

Payment Card Industry (PCI) Data Standard Attestation of Compliance for Self-Assessment Questionnaire D Service Providers Version 3.1 April 2015 Section 1: Assessment Information Instructions for Submission

Actorcard Prepaid Visa Card Terms & Conditions

Actorcard Prepaid Visa Card Terms & Conditions These Terms & Conditions apply to your Actorcard prepaid Visa debit card. Please read them carefully. In these Terms & Conditions: "Account" means the prepaid

Actorcard Prepaid Visa Card Terms & Conditions These Terms & Conditions apply to your Actorcard prepaid Visa debit card. Please read them carefully. In these Terms & Conditions: "Account" means the prepaid

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Smart cards that have erasable memory and are modifiable are. 1) A) EPROM cards B) EEPROM

Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Smart cards that have erasable memory and are modifiable are. 1) A) EPROM cards B) EEPROM

Chapter 12. Electronic Payment Systems. 2008 Pearson Prentice Hall, Electronic Commerce 2008, Efraim Turban, et al.

Chapter 12 Electronic Payment Systems 2008 Pearson Prentice Hall, Electronic Commerce 2008, Efraim Turban, et al. Learning Objectives 1. Understand the shifts that are occurring with regard to noncash

Chapter 12 Electronic Payment Systems 2008 Pearson Prentice Hall, Electronic Commerce 2008, Efraim Turban, et al. Learning Objectives 1. Understand the shifts that are occurring with regard to noncash

Chapter 12. Learning Objectives. Learning Objectives. Electronic Payment Systems

Chapter 12 Electronic Payment Systems 2008 Pearson Prentice Hall, Electronic Commerce 2008, Efraim Turban, et al. Learning Objectives 1. Understand the shifts that are occurring with regard to noncash

Chapter 12 Electronic Payment Systems 2008 Pearson Prentice Hall, Electronic Commerce 2008, Efraim Turban, et al. Learning Objectives 1. Understand the shifts that are occurring with regard to noncash

Section 1: Assessment Information

Section 1: Assessment Information Instructions for Submission This document must be completed as a declaration of the results of the service provider s self-assessment with the Payment Card Industry Data

Section 1: Assessment Information Instructions for Submission This document must be completed as a declaration of the results of the service provider s self-assessment with the Payment Card Industry Data

General Guidelines for the Development of Government Payment Programs

General Guidelines for the Development of Government Payment Programs Social Safety Nets Course Washington D.C., 15 December 2014 Massimo Cirasino, Head, Payment Systems Development Group The World Bank

General Guidelines for the Development of Government Payment Programs Social Safety Nets Course Washington D.C., 15 December 2014 Massimo Cirasino, Head, Payment Systems Development Group The World Bank

Mobile Banking, Financial Inclusion and Policy Challenges

Mobile Banking, Financial Inclusion and Policy Challenges Presentation to the 10 th IADI Annual Conference 19-20 October 2011, Warsaw, Poland Pierre-Laurent Chatain Prudential Oversight and Systemic Stability

Mobile Banking, Financial Inclusion and Policy Challenges Presentation to the 10 th IADI Annual Conference 19-20 October 2011, Warsaw, Poland Pierre-Laurent Chatain Prudential Oversight and Systemic Stability

AYMENTS SYSTEM COUNCIL. The Role of Banks Relative to Non-Banks in Electronic Money Operations

AYMENTS SYSTEM COUNCIL The Role of Banks Relative to Non-Banks in Electronic Money Operations A Paper by a Sub-committee of The Payments System Council September 2011 I Introduction Several factors have

AYMENTS SYSTEM COUNCIL The Role of Banks Relative to Non-Banks in Electronic Money Operations A Paper by a Sub-committee of The Payments System Council September 2011 I Introduction Several factors have

Mobile Payment in India - Operative Guidelines for Banks

Mobile Payment in India - Operative Guidelines for Banks 1. Introduction 1.1 With the rapid growth in the number of mobile phone subscribers in India (about 261 million as at the end of March 2008 and

Mobile Payment in India - Operative Guidelines for Banks 1. Introduction 1.1 With the rapid growth in the number of mobile phone subscribers in India (about 261 million as at the end of March 2008 and

BANK OF UGANDA MOBILE MONEY GUIDELINES, 2013 ARRANGEMENT OF PARAGRAPHS

BANK OF UGANDA MOBILE MONEY GUIDELINES, 2013 ARRANGEMENT OF PARAGRAPHS PART I PRELIMINARY 1. Citation and Commencement... 2 2. Background... 2 3. Objectives... 3 4. Application... 3 5. Interpretation...

BANK OF UGANDA MOBILE MONEY GUIDELINES, 2013 ARRANGEMENT OF PARAGRAPHS PART I PRELIMINARY 1. Citation and Commencement... 2 2. Background... 2 3. Objectives... 3 4. Application... 3 5. Interpretation...

Merchant Account Basics. A compilation of Braintree blog posts

Merchant Account Basics A compilation of Braintree blog posts Table of Contents I. A Brief History of the Credit Card Processing Industry... 3 II. Industry Overview... 4 The necessity of merchant accounts...

Merchant Account Basics A compilation of Braintree blog posts Table of Contents I. A Brief History of the Credit Card Processing Industry... 3 II. Industry Overview... 4 The necessity of merchant accounts...

Merchant Account Glossary of Terms

Merchant Account Glossary of Terms From offshore merchant accounts to the truth behind free merchant accounts, get answers to some of the most common and frequently asked questions. If you cannot find

Merchant Account Glossary of Terms From offshore merchant accounts to the truth behind free merchant accounts, get answers to some of the most common and frequently asked questions. If you cannot find

Payment Card Industry (PCI) Data Security Standard

Data Security Standard") Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.1 April 2015 Section 1: Assessment Information Instructions for Submission

Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.1 April 2015 Section 1: Assessment Information Instructions for Submission

ASIAN LAW AND ECONOMICS ASSOCATION 3 RD ANNUAL CONFERENCE

LAW GOVERNING ELECTRONIC BANKING: FAVOURING ECONOMIC GROWTH- THE INDIAN SCENARIO Paper presented by: B. Gopalakrishnan Senior Vice President (Law), UTI Bank Limited INTRODUCTION The face of the banking

LAW GOVERNING ELECTRONIC BANKING: FAVOURING ECONOMIC GROWTH- THE INDIAN SCENARIO Paper presented by: B. Gopalakrishnan Senior Vice President (Law), UTI Bank Limited INTRODUCTION The face of the banking

Global Internet Payment Processing Solution....expand your processing

Global Internet Payment Processing Solution...expand your processing Global Internet Payment Processing Solution Fast Easy Secure Convenient ecomm from emerchantpay is an end to end software solution hosted

Global Internet Payment Processing Solution...expand your processing Global Internet Payment Processing Solution Fast Easy Secure Convenient ecomm from emerchantpay is an end to end software solution hosted

Innovations in retail payments

Innovations in retail payments CPMI-BCRP Seminar Lima, Peru, 26-27 May 2016 The views expressed here are those of the authors only. No responsibility of them should be attributed to the Bank of Canada

Innovations in retail payments CPMI-BCRP Seminar Lima, Peru, 26-27 May 2016 The views expressed here are those of the authors only. No responsibility of them should be attributed to the Bank of Canada

Federal Financial Institutions Examination Council FFIEC. Retail Payment Systems RPS. February 2010 IT EXAMINATION HANDBOOK

Federal Financial Institutions Examination Council FFIEC Retail Payment Systems February 2010 RPS IT EXAMINATION HANDBOOK RETAIL PAYMENT SYSTEMS RISK MANAGEMENT Action Summary Financial institutions engaged

Federal Financial Institutions Examination Council FFIEC Retail Payment Systems February 2010 RPS IT EXAMINATION HANDBOOK RETAIL PAYMENT SYSTEMS RISK MANAGEMENT Action Summary Financial institutions engaged

Payment Card Industry (PCI) Data Security Standard

Data Security Standard") Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.1 April 2015 Section 1: Assessment Information Instructions for Submission

Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.1 April 2015 Section 1: Assessment Information Instructions for Submission

U.S. Mobile Payments Landscape NCSL Legislative Summit 2013

U.S. Mobile Payments Landscape NCSL Legislative Summit 2013 Marianne Crowe Vice President, Payment Strategies Federal Reserve Bank of Boston August 13, 2013 2 Agenda Overview of Mobile Payments Landscape

U.S. Mobile Payments Landscape NCSL Legislative Summit 2013 Marianne Crowe Vice President, Payment Strategies Federal Reserve Bank of Boston August 13, 2013 2 Agenda Overview of Mobile Payments Landscape

Evolving Mobile Payments Industry Landscape

Evolving Mobile Payments Industry Landscape Mobile Banking: Can the Unbanked Bank on It? Sargent Shriver National Center on Poverty Law webinar August 16, 2012 Marianne Crowe Federal Reserve Bank of Boston

Evolving Mobile Payments Industry Landscape Mobile Banking: Can the Unbanked Bank on It? Sargent Shriver National Center on Poverty Law webinar August 16, 2012 Marianne Crowe Federal Reserve Bank of Boston

Understanding the Digital Financial Ecosystem: Examples from Asia and the Pacific

Understanding the Digital Financial Ecosystem: Examples from Asia and the Pacific TRPC Pte Ltd Yoonee Jeong ITU REGIONAL ECONOMIC AND FINANCIAL FORUM OF TELECOMMUNICATIONS/ICTS FOR ASIA AND PACIFIC DIGITAL

Understanding the Digital Financial Ecosystem: Examples from Asia and the Pacific TRPC Pte Ltd Yoonee Jeong ITU REGIONAL ECONOMIC AND FINANCIAL FORUM OF TELECOMMUNICATIONS/ICTS FOR ASIA AND PACIFIC DIGITAL

Payment Card Industry (PCI) Data Security Standard

Data Security Standard") Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.0 February 2014 Section 1: Assessment Information Instructions for Submission

Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.0 February 2014 Section 1: Assessment Information Instructions for Submission

Spotlight on Product & Service: Worldpay - End-to-End Payments Secure Platform at Most Cost-Effective Rates. Accept payments. Anywhere. Anytime.

Newsletter Vol. 87 - Introduction Softengine News is dedicated to keeping you up to date with the latest information regarding SAP Business One systems, Softengine solutions and Best Business Practices.

Newsletter Vol. 87 - Introduction Softengine News is dedicated to keeping you up to date with the latest information regarding SAP Business One systems, Softengine solutions and Best Business Practices.

RFP#15-20 EXHIBIT E MERCHANT SERVICES INFORMATION SHEET

RFP#15-20 EXHIBIT E MERCHANT SERVICES INFORMATION SHEET A. Merchant Credit Card Processing 1. Describe your company s authorization method; list and describe alternative authorization methods. 2. What

RFP#15-20 EXHIBIT E MERCHANT SERVICES INFORMATION SHEET A. Merchant Credit Card Processing 1. Describe your company s authorization method; list and describe alternative authorization methods. 2. What

Cross-Border Payment Systems and International Remittances

Cross-Border Payment Systems and International Remittances Seminar Improving Central Bank Reporting and Procedures on Remittances Mexico City, Mexico, July 11-14, 2006 José Antonio García The World Bank

Cross-Border Payment Systems and International Remittances Seminar Improving Central Bank Reporting and Procedures on Remittances Mexico City, Mexico, July 11-14, 2006 José Antonio García The World Bank

Ambit Card Management Card Management Solution Suite

Ambit Card Management Card Management Solution Suite Darrell Parker, 43 head of alternative channels Sandra De Souza, 26 banking customer Ahmed Hassan, 46 head of cards Contents 1 Business Overview 4 Ambit

Ambit Card Management Card Management Solution Suite Darrell Parker, 43 head of alternative channels Sandra De Souza, 26 banking customer Ahmed Hassan, 46 head of cards Contents 1 Business Overview 4 Ambit

Payment Card Industry (PCI) Data Security Standard

Data Security Standard") Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.0 February 2014 Section 1: Assessment Information Instructions for Submission

Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.0 February 2014 Section 1: Assessment Information Instructions for Submission

Asian Payment Card Forum Growing the Business: Launching Successful Consumer Payments Products

Asian Payment Card Forum Growing the Business: Launching Successful Consumer Payments Products Dusit Thani Hotel, Bangkok, Thailand September 201 Information Brochure Focus in 2014 Payment Card Technology

Asian Payment Card Forum Growing the Business: Launching Successful Consumer Payments Products Dusit Thani Hotel, Bangkok, Thailand September 201 Information Brochure Focus in 2014 Payment Card Technology

CREDIT CARD PROCESSING GLOSSARY OF TERMS

CREDIT CARD PROCESSING GLOSSARY OF TERMS 3DES A highly secure encryption system that encrypts data 3 times, using 3 64-bit keys, for an overall encryption key length of 192 bits. Also called triple DES.

CREDIT CARD PROCESSING GLOSSARY OF TERMS 3DES A highly secure encryption system that encrypts data 3 times, using 3 64-bit keys, for an overall encryption key length of 192 bits. Also called triple DES.

Retail Payment Systems in Turkey

Republic of Turkey Undersecretariat of Treasury Retail Payment Systems in Turkey M. Alper BATUR Head of Department 5 th MEETING OF THE COMCEC FINANCIAL COOPERATION WORKING GROUP October 15, 2015 Ankara

Republic of Turkey Undersecretariat of Treasury Retail Payment Systems in Turkey M. Alper BATUR Head of Department 5 th MEETING OF THE COMCEC FINANCIAL COOPERATION WORKING GROUP October 15, 2015 Ankara

Payments Industry Glossary

Payments Industry Glossary 2012 First Data Corporation. All trademarks, service marks and trade names referenced in this material are the property of their respective owners. A ACH: Automated Clearing

Payments Industry Glossary 2012 First Data Corporation. All trademarks, service marks and trade names referenced in this material are the property of their respective owners. A ACH: Automated Clearing

PayLeap Guide. One Stop

PayLeap Guide One Stop PayLeap does it all. Take payments in person? Check. Payments over the phone or by mail? Check. Payments from mobile devices? Of course. Online payments? No problem. In addition

PayLeap Guide One Stop PayLeap does it all. Take payments in person? Check. Payments over the phone or by mail? Check. Payments from mobile devices? Of course. Online payments? No problem. In addition

Bangladesh Payment And Settlement Systems Regulations 2014

Bangladesh Payment And Settlement Systems Regulations 2014 Payment Systems Department Bangladesh Bank Table of Contents Description Page # 1. Short Title and Commencement 1 2. The Objectives of the Regulations

Bangladesh Payment And Settlement Systems Regulations 2014 Payment Systems Department Bangladesh Bank Table of Contents Description Page # 1. Short Title and Commencement 1 2. The Objectives of the Regulations

Payment Card Industry (PCI) Data Security Standard

Data Security Standard") Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.0 February 2014 Section 1: Assessment Information Instructions for Submission

Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.0 February 2014 Section 1: Assessment Information Instructions for Submission

Working Paper An Inclusive Approach to Digital Payments Ecosystems:

BETTERTHANCASH A L L I A N C E Improving Lives Through Digital Payments Working Paper An Inclusive Approach to Digital Payments Ecosystems: Accelerating the Transition from Cash Requires an Ecosystem Approach

BETTERTHANCASH A L L I A N C E Improving Lives Through Digital Payments Working Paper An Inclusive Approach to Digital Payments Ecosystems: Accelerating the Transition from Cash Requires an Ecosystem Approach

bi on Solution white paper

bi on Solution white paper Billon Solution Overview Despite concerted efforts for years, cash has not yet been eliminated. Mostly because not everyone has a bank account and debit card - an estimated 2.5

bi on Solution white paper Billon Solution Overview Despite concerted efforts for years, cash has not yet been eliminated. Mostly because not everyone has a bank account and debit card - an estimated 2.5

Guideline on Debit or Credit Cards Usage

CMSGu2012-04 Mauritian Computer Emergency Response Team CERT-MU SECURITY GUIDELINE 2011-02 Enhancing Cyber Security in Mauritius Guideline on Debit or Credit Cards Usage National Computer Board Mauritius

CMSGu2012-04 Mauritian Computer Emergency Response Team CERT-MU SECURITY GUIDELINE 2011-02 Enhancing Cyber Security in Mauritius Guideline on Debit or Credit Cards Usage National Computer Board Mauritius

Payment Card Industry (PCI) Data Security Standard

Data Security Standard") Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.0 February 2014 Section 1: Assessment Information Instructions for Submission

Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.0 February 2014 Section 1: Assessment Information Instructions for Submission

First Data E-commerce Payments Gateway

First Data E-commerce Payments Gateway High performance payment processing solution designed specifically to meet the requirements of global Card-Not-Present PSP When you partner with First Data for your

First Data E-commerce Payments Gateway High performance payment processing solution designed specifically to meet the requirements of global Card-Not-Present PSP When you partner with First Data for your

Bangladesh Payment and Settlement Systems Regulations, 2009

Bangladesh Payment and Settlement Systems Regulations, 2009 Payment Systems Division Department of Currency Management and Payment Systems Bangladesh Bank Table of Contents 1. Short Title and Commencement...

Bangladesh Payment and Settlement Systems Regulations, 2009 Payment Systems Division Department of Currency Management and Payment Systems Bangladesh Bank Table of Contents 1. Short Title and Commencement...

Guidelines for Card Issuance and Usage in Nigeria

CENTRAL BANK OF NIGERIA Guidelines for Card Issuance and Usage in Nigeria Ver. 2 GUIDELINES FOR CARD ISSUANCE AND USAGE IN NIGERIA SECTIONS/TA BLE OF CONTENTS 1.0 Preambles 3 2.0 Minimum Standards 3 3.0

CENTRAL BANK OF NIGERIA Guidelines for Card Issuance and Usage in Nigeria Ver. 2 GUIDELINES FOR CARD ISSUANCE AND USAGE IN NIGERIA SECTIONS/TA BLE OF CONTENTS 1.0 Preambles 3 2.0 Minimum Standards 3 3.0

Prepaid Card Terms and Conditions

Prepaid Card Terms and Conditions These terms and conditions apply to your Prepaid Card. You must read them carefully. In these terms and conditions "you" means the named Prepaid Cardholder and the authorised

Prepaid Card Terms and Conditions These terms and conditions apply to your Prepaid Card. You must read them carefully. In these terms and conditions "you" means the named Prepaid Cardholder and the authorised

Egyptian Retail Payments Service Providers

Egyptian Retail Payments Service Providers Introduction The retail payments market in Egypt is in its early stages of development. A survey was conducted to review of the current providers of retail payment

Egyptian Retail Payments Service Providers Introduction The retail payments market in Egypt is in its early stages of development. A survey was conducted to review of the current providers of retail payment

UK Payments Infrastructure: Exploring Opportunities

UK Payments Infrastructure: Exploring Opportunities 31 August 2014 www.kpmg.co.uk Table of figures Figure 1: Current UK payments infrastructure overview.... 9 Figure 2: UK payment schemes, infrastructure

UK Payments Infrastructure: Exploring Opportunities 31 August 2014 www.kpmg.co.uk Table of figures Figure 1: Current UK payments infrastructure overview.... 9 Figure 2: UK payment schemes, infrastructure

1i. What other gaps or opportunities not mentioned in the paper could be addressed to make improvements to the U.S. payment system?

Name: LORENZO GASTON Organization: SMART PAYMENT ASSOCIATION (SPA) Industry Segment: Technology Solution Provider/Processor General 1. Are you in general agreement with the payment system gaps and opportunities

Name: LORENZO GASTON Organization: SMART PAYMENT ASSOCIATION (SPA) Industry Segment: Technology Solution Provider/Processor General 1. Are you in general agreement with the payment system gaps and opportunities

Guideline Note Mobile Financial Services: Basic Terminology

Mobile Financial Services Working Group (MFSWG) Guideline Note Mobile Financial Services: Basic Terminology About AFI Guideline Notes This guideline note on mobile financial services (MFS) terminology

Mobile Financial Services Working Group (MFSWG) Guideline Note Mobile Financial Services: Basic Terminology About AFI Guideline Notes This guideline note on mobile financial services (MFS) terminology

BANK OF JAMAICA 1 February 2013. Guidelines for Electronic Retail Payment Services

BANK OF JAMAICA Guidelines for Electronic Retail Payment Services Foreword The Draft Guidelines for Retail Payment Services was published by the Bank of Jamaica (Bank) on 3 August 2012, with an invitation

BANK OF JAMAICA Guidelines for Electronic Retail Payment Services Foreword The Draft Guidelines for Retail Payment Services was published by the Bank of Jamaica (Bank) on 3 August 2012, with an invitation

Policies and Procedures. Merchant Card Services Office of Treasury Operations

Policies and Procedures Merchant Card Services Office of Treasury Operations 1 Welcome! Table of Contents: Introduction Establishing Payment Card Services Payment Card Acceptance Procedures Payment Card

Policies and Procedures Merchant Card Services Office of Treasury Operations 1 Welcome! Table of Contents: Introduction Establishing Payment Card Services Payment Card Acceptance Procedures Payment Card

E-commerce refers to paperless exchange of business information using following ways.

E-Commerce E-Commerce or Electronics Commerce is a methodology of modern business which fulfills the need of business organizations, vendors and customers to reduce cost and improve the quality of goods

E-Commerce E-Commerce or Electronics Commerce is a methodology of modern business which fulfills the need of business organizations, vendors and customers to reduce cost and improve the quality of goods

PAYMENT SYSTEMS REVIEW (FISCAL YEAR 2014-15)

") PAYMENT SYSTEMS REVIEW (FISCAL YEAR 214-15) PAYMENT SYSTEMS DEPARTMENT STATE BANK OF PAKISTAN Payment Systems Review Fiscal Year 214-15 TABLE OF CONTENTS 1. OVERVIEW OF COUNTRY S PAYMENT SYSTEMS... 4 2.

PAYMENT SYSTEMS REVIEW (FISCAL YEAR 214-15) PAYMENT SYSTEMS DEPARTMENT STATE BANK OF PAKISTAN Payment Systems Review Fiscal Year 214-15 TABLE OF CONTENTS 1. OVERVIEW OF COUNTRY S PAYMENT SYSTEMS... 4 2.

Account Management System Guide

Account Management System Guide Version 2.2 March 2015 Table of Contents Introduction...5 What is the Account Management System?...5 Accessing the Account Management System...5 Forgotten Password...5 Account

Account Management System Guide Version 2.2 March 2015 Table of Contents Introduction...5 What is the Account Management System?...5 Accessing the Account Management System...5 Forgotten Password...5 Account

Card Acceptance Best Practices to Manage Rates and Minimize Risk

Card Acceptance Best Practices to Manage Rates and Minimize Risk Kim Jackson VP, Transfund Merchant Services April 23, 2014 BOK Financial is registered with the National Association of State Boards of

Card Acceptance Best Practices to Manage Rates and Minimize Risk Kim Jackson VP, Transfund Merchant Services April 23, 2014 BOK Financial is registered with the National Association of State Boards of

An introduction to CashFlows and the provision of on-line card acceptance services we provide to Young Enterprise companies

An introduction to CashFlows and the provision of on-line card acceptance services we provide to Young Enterprise companies Q. What is CashFlows? A. CashFlows is a Financial Services company that provides

An introduction to CashFlows and the provision of on-line card acceptance services we provide to Young Enterprise companies Q. What is CashFlows? A. CashFlows is a Financial Services company that provides

Mutual legal recognition of electronic communications and electronic signatures and paperless trade facilitation: challenges and opportunities

Mutual legal recognition of electronic communications and electronic signatures and paperless trade facilitation: challenges and opportunities Luca Castellani Secretary, Working Group IV (Electronic Commerce)

Mutual legal recognition of electronic communications and electronic signatures and paperless trade facilitation: challenges and opportunities Luca Castellani Secretary, Working Group IV (Electronic Commerce)

EMP's vision is to be the leading electronic payments processing company in the emerging markets of Africa and the Middle East.

EMP's vision is to be the leading electronic payments processing company in the emerging markets of Africa and the Middle East. EMP's mission is to be at the forefront of the region's electronic payments

EMP's vision is to be the leading electronic payments processing company in the emerging markets of Africa and the Middle East. EMP's mission is to be at the forefront of the region's electronic payments

Payment Card Industry (PCI) Data Security Standard

Data Security Standard") Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.0 February 2014 Section 1: Assessment Information Instructions for Submission

Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.0 February 2014 Section 1: Assessment Information Instructions for Submission

New Regime for the Regulation of Payment Services in Europe

Financial Institutions Advisory and Financial Regulatory Group September 24, 2009 New Regime for the Regulation of Payment Services in Europe The EU Payment Services Directive, which establishes a new

Financial Institutions Advisory and Financial Regulatory Group September 24, 2009 New Regime for the Regulation of Payment Services in Europe The EU Payment Services Directive, which establishes a new

Adjustment A debit or credit to a cardholder or merchant account to correct a transaction error

Glossary of Terms A ABA Routing Number This 9-digit number is assigned by the American Banker s Association and is used to identify individual banks. When performing an ACH transfer from one bank account

Glossary of Terms A ABA Routing Number This 9-digit number is assigned by the American Banker s Association and is used to identify individual banks. When performing an ACH transfer from one bank account

SESSION 2: POLICIES AND REGULATION FOR FINANCIAL INCLUSION

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT Expert Meeting on THE IMPACT OF ACCESS TO FINANCIAL SERVICES, INCLUDING BY HIGHLIGHTING THE IMPACT ON REMITTANCES ON DEVELOPMENT: ECONOMIC EMPOWERMENT

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT Expert Meeting on THE IMPACT OF ACCESS TO FINANCIAL SERVICES, INCLUDING BY HIGHLIGHTING THE IMPACT ON REMITTANCES ON DEVELOPMENT: ECONOMIC EMPOWERMENT

CONTENTS. Concerns & views from stakeholders in the payment banks ecosystem... 5

CONTENTS Executive Summary... 3 Global experiences and recommendations...4 Concerns & views from stakeholders in the payment banks ecosystem... 5 Financial Inclusion PMJDY and its possible impact on Payment

CONTENTS Executive Summary... 3 Global experiences and recommendations...4 Concerns & views from stakeholders in the payment banks ecosystem... 5 Financial Inclusion PMJDY and its possible impact on Payment

Payment Card Industry (PCI) Data Security Standard

Data Security Standard") Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.1 April 2015 Section 1: Assessment Information Instructions for Submission

Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.1 April 2015 Section 1: Assessment Information Instructions for Submission

GLOSSARY OF MOST COMMONLY USED TERMS IN THE MERCHANT SERVICES INDUSTRY

GLOSSARY OF MOST COMMONLY USED TERMS IN THE MERCHANT SERVICES INDUSTRY Acquiring Bank The bank or financial institution that accepts credit and/or debit card payments for products or services on behalf

GLOSSARY OF MOST COMMONLY USED TERMS IN THE MERCHANT SERVICES INDUSTRY Acquiring Bank The bank or financial institution that accepts credit and/or debit card payments for products or services on behalf

GUIDANCE ON PAYMENT PROCESSOR RELATIONSHIPS (Revised July 2014)

") Federal Deposit Insurance Corporation 550 17th Street NW, Washington, D.C. 20429-9990 Financial Institution Letter FIL-127-2008 November 7, 2008 GUIDANCE ON PAYMENT PROCESSOR RELATIONSHIPS (Revised July

Federal Deposit Insurance Corporation 550 17th Street NW, Washington, D.C. 20429-9990 Financial Institution Letter FIL-127-2008 November 7, 2008 GUIDANCE ON PAYMENT PROCESSOR RELATIONSHIPS (Revised July

Payment Card Industry (PCI) Data Security Standard

Data Security Standard") Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.0 February 2014 Section 1: Assessment Information Instructions for Submission

Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 3.0 February 2014 Section 1: Assessment Information Instructions for Submission

CRM4M Accounting Set Up and Miscellaneous Accounting Guide Rev. 10/17/2008 rb

CRM4M Accounting Set Up and Miscellaneous Accounting Guide Rev. 10/17/2008 rb Topic Page Chart of Accounts 3 Creating a Batch Manually 8 Closing a Batch Manually 11 Cancellation Fees 17 Check Refunds 19

CRM4M Accounting Set Up and Miscellaneous Accounting Guide Rev. 10/17/2008 rb Topic Page Chart of Accounts 3 Creating a Batch Manually 8 Closing a Batch Manually 11 Cancellation Fees 17 Check Refunds 19

EuroCommerce position paper Online e-payments

EuroCommerce position paper Online e-payments 16 September 2011 EuroCommerce welcomes the opportunity to comment on online payment issues. We carried out a brief members' survey and consulted within the

EuroCommerce position paper Online e-payments 16 September 2011 EuroCommerce welcomes the opportunity to comment on online payment issues. We carried out a brief members' survey and consulted within the

Position Paper. issuers. how to leverage EC s regulation proposal. on interchange fees for card-based payment transactions

Position Paper issuers how to leverage EC s regulation proposal on interchange fees for card-based payment transactions The issuing landscape has dramatically changed over the last few years increased

Position Paper issuers how to leverage EC s regulation proposal on interchange fees for card-based payment transactions The issuing landscape has dramatically changed over the last few years increased

EDUCATION - TERMS 101

EDUCATION - TERMS 101 ACH (Automated Clearing House): A processing organization networked with others to exchange (clear and settle) electronic debit/credit transactions (no physical checks). ABA Routing

EDUCATION - TERMS 101 ACH (Automated Clearing House): A processing organization networked with others to exchange (clear and settle) electronic debit/credit transactions (no physical checks). ABA Routing

BERMUDA MONETARY AUTHORITY

BERMUDA MONETARY AUTHORITY DISCUSSION PAPER MONEY SERVICE BUSINESS, PAYMENT SERVICES, and FOREIGN EXCHANGE SERVICES. April 2014 TABLE OF CONTENTS I. Introduction...3 II. Background...4 III. Money Service

BERMUDA MONETARY AUTHORITY DISCUSSION PAPER MONEY SERVICE BUSINESS, PAYMENT SERVICES, and FOREIGN EXCHANGE SERVICES. April 2014 TABLE OF CONTENTS I. Introduction...3 II. Background...4 III. Money Service

Payment Gateway Proposal

Making payment easier Payment Gateway Proposal Sep 2014 INFICARE Pvt. Ltd. +977-1-4672716/ 4279727 [email protected] Non-Disclosure Statement The information in this proposal shall not be disclosed outside

Making payment easier Payment Gateway Proposal Sep 2014 INFICARE Pvt. Ltd. +977-1-4672716/ 4279727 [email protected] Non-Disclosure Statement The information in this proposal shall not be disclosed outside

Agent Registration. Program Guidelines. (For use in Asia Pacific, Central Europe, Middle East and Africa)

") (For use in Asia Pacific, Central Europe, Middle East and Africa) January 2012 Contents 1 INTRODUCTION... 3 1.1 BACKGROUND... 3 1.2 PURPOSE OF DOCUMENT... 4 1.3 WHO NEEDS TO BE REGISTERED?... 5 1.4 WHY

(For use in Asia Pacific, Central Europe, Middle East and Africa) January 2012 Contents 1 INTRODUCTION... 3 1.1 BACKGROUND... 3 1.2 PURPOSE OF DOCUMENT... 4 1.3 WHO NEEDS TO BE REGISTERED?... 5 1.4 WHY

Payments Gateways Opportunities for Acquirers

Payments Gateways Opportunities for Acquirers Peter Jones November 2011 Europe s acquiring market place has never been more competitive. All players are chasing revenues and volumes with the expectation

Payments Gateways Opportunities for Acquirers Peter Jones November 2011 Europe s acquiring market place has never been more competitive. All players are chasing revenues and volumes with the expectation

E-Commerce, Merchant Processing, EMV and General Best Practices for Municipalities

E-Commerce, Merchant Processing, EMV and General Best Practices for Municipalities T.C. Kennedy. CTP Senior Vice President Treasury & Payment Solutions SunTrust Bank Electronic Commerce Defined Segment

E-Commerce, Merchant Processing, EMV and General Best Practices for Municipalities T.C. Kennedy. CTP Senior Vice President Treasury & Payment Solutions SunTrust Bank Electronic Commerce Defined Segment

SIA CARD PROCESSING. Advanced, secure and digital payment solutions

SIA CARD PROCESSING Advanced, secure and digital payment solutions The card processing offering Best in class solutions suitable for any type of client Advanced SIA delivers a complete range of Pan-European

SIA CARD PROCESSING Advanced, secure and digital payment solutions The card processing offering Best in class solutions suitable for any type of client Advanced SIA delivers a complete range of Pan-European

Third Party Agent (TPA) Registration Program - TPA Types and Functional Descriptions

Registration Program - TPA Types and Functional Descriptions") Third Party Agent (TPA) Registration Program - TPA Types and Functional Descriptions Independent Sales Organizations (ISO) ISO Merchant (ISO M) Conducts merchant account or transaction processing solicitation,

Third Party Agent (TPA) Registration Program - TPA Types and Functional Descriptions Independent Sales Organizations (ISO) ISO Merchant (ISO M) Conducts merchant account or transaction processing solicitation,

How To Connect Bitcoin To A Bank Account

Bridging Crypto Currencies to traditional payment systems Miles Paschini Dec 4 th, 2014 2 Wave Crest Licensed emoney issuer in Gibraltar Principal members of Visa and MasterCard Transaction processor Clearing

Bridging Crypto Currencies to traditional payment systems Miles Paschini Dec 4 th, 2014 2 Wave Crest Licensed emoney issuer in Gibraltar Principal members of Visa and MasterCard Transaction processor Clearing

Payment & Settlement Systems in Sri Lanka and the Future Expectations. Ranjani Weerasinghe Director Payments and Settlements

Payment & Settlement Systems in Sri Lanka and the Future Expectations Ranjani Weerasinghe Director Payments and Settlements Outline Payments and Settlement Systems in the country Recent Developments Future

Payment & Settlement Systems in Sri Lanka and the Future Expectations Ranjani Weerasinghe Director Payments and Settlements Outline Payments and Settlement Systems in the country Recent Developments Future

RESERVE BANK OF MALAWI GUIDELINES FOR MOBILE PAYMENT SYSTEMS

RESERVE BANK OF MALAWI GUIDELINES FOR MOBILE PAYMENT SYSTEMS March 2011 2 Table of Contents ACRONYMS... 4 DEFINITIONS... 5 1.0 Introduction... 6 2.0 Mandate... 6 3.0 Objective... 6 4.0 Scope... 6 5.0 Application

RESERVE BANK OF MALAWI GUIDELINES FOR MOBILE PAYMENT SYSTEMS March 2011 2 Table of Contents ACRONYMS... 4 DEFINITIONS... 5 1.0 Introduction... 6 2.0 Mandate... 6 3.0 Objective... 6 4.0 Scope... 6 5.0 Application

Caribbean Electronic Payments

Caribbean Electronic Payments Company Profile Caribbean Electronic Payments Ltd. 1-13 Contents Introduction... 3 Mission & Core Values... 5 CEPAYMENTS Mission... 5 Our Core Values... 5 Innovation... 5

Caribbean Electronic Payments Company Profile Caribbean Electronic Payments Ltd. 1-13 Contents Introduction... 3 Mission & Core Values... 5 CEPAYMENTS Mission... 5 Our Core Values... 5 Innovation... 5

Saint Louis University Merchant Card Processing Policy & Procedures

Saint Louis University Merchant Card Processing Policy & Procedures Overview: Policies and procedures for processing credit card transactions and properly storing credit card data physically and electronically.

Saint Louis University Merchant Card Processing Policy & Procedures Overview: Policies and procedures for processing credit card transactions and properly storing credit card data physically and electronically.

An access number, dialed by a modem, that lets a computer communicate with an Internet Service Provider (ISP) or some other service provider.

or some other service provider.") TERM DEFINITION Access Number Account Number Acquirer Acquiring Bank Acquiring Processor Address Verification Service (AVS) Association Authorization Authorization Center Authorization Fee Automated Clearing

TERM DEFINITION Access Number Account Number Acquirer Acquiring Bank Acquiring Processor Address Verification Service (AVS) Association Authorization Authorization Center Authorization Fee Automated Clearing

RETHINKING CARDS BUSINESS. Erick Ho, Head of Payment Services, SunGard 17 September 2015. Break through.

RETHINKING CARDS BUSINESS Erick Ho, Head of Payment Services, SunGard 17 September 2015 Break through. Agenda 01 02 03 04 05 Trends and Growth in cards and payment business Sharpening Business Focus The

RETHINKING CARDS BUSINESS Erick Ho, Head of Payment Services, SunGard 17 September 2015 Break through. Agenda 01 02 03 04 05 Trends and Growth in cards and payment business Sharpening Business Focus The

Verified by Visa. Acquirer and Merchant Implementation Guide. U.S. Region. May 2011

Verified by Visa Acquirer and Merchant Implementation Guide U.S. Region Verified by Visa Acquirer and Merchant Implementation Guide U.S. Region VISA PUBLIC DISCLAIMER: THE RECOMMENDATIONS CONTAINED HEREIN

Verified by Visa Acquirer and Merchant Implementation Guide U.S. Region Verified by Visa Acquirer and Merchant Implementation Guide U.S. Region VISA PUBLIC DISCLAIMER: THE RECOMMENDATIONS CONTAINED HEREIN

authengin: A New Generation Financial Payment System for 21 st Century e- Banking and e- Commerce

authengin: A New Generation Financial Payment System for 21 st Century e- Banking and e- Commerce Technology that provides an opportunity to grow through new markets, new products and services and new

authengin: A New Generation Financial Payment System for 21 st Century e- Banking and e- Commerce Technology that provides an opportunity to grow through new markets, new products and services and new

FREQUENTLY ASKED QUESTIONS - CHARGEBACKS

FREQUENTLY ASKED QUESTIONS - CHARGEBACKS # Questions Answer 1 What is a Chargeback? A Chargeback is the term used by Banks for debiting a merchant s bank account due to successful return of a transaction

FREQUENTLY ASKED QUESTIONS - CHARGEBACKS # Questions Answer 1 What is a Chargeback? A Chargeback is the term used by Banks for debiting a merchant s bank account due to successful return of a transaction

Merchant Application Form for Credit and Debit Card Payment Gateway

Merchant Application Form for Credit and Debit Card Payment Gateway MERCHANT PRE-QUAPPLICATION FORM Merchant application form With this intake form you can apply for our online payment solutions. The information

Merchant Application Form for Credit and Debit Card Payment Gateway MERCHANT PRE-QUAPPLICATION FORM Merchant application form With this intake form you can apply for our online payment solutions. The information

Credit card: permits consumers to purchase items while deferring payment

General Payment Systems Cash: portable, no authentication, instant purchasing power, allows for micropayments, no transaction fee for using it, anonymous But Easily stolen, no float time, can t easily

General Payment Systems Cash: portable, no authentication, instant purchasing power, allows for micropayments, no transaction fee for using it, anonymous But Easily stolen, no float time, can t easily

Attestation of Compliance for Onsite Assessments Service Providers

Attestation of Compliance Service Providers Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 2.0 October 2010 Instructions for

Attestation of Compliance Service Providers Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 2.0 October 2010 Instructions for