Do retail traders suffer from high frequency traders?

|

|

|

- Clara Weaver

- 10 years ago

- Views:

Transcription

1 Do retail traders suffer from high frequency traders? Katya Malinova, Andreas Park, Ryan Riordan November 15, 2013

2 Millions in Milliseconds Monday, June 03, 2013: a minor clock synchronization issue causes market-moving manufacturing data be released to select traders 15 milliseconds prior to the scheduled 10am release. Nanex (trading data analysis firm) estimates: $28 million worth of shares changed hands in 15 milliseconds 30,000 shares of SPY traded in 1 of these milliseconds (average SPY volume = 5.6 shares in a millisecond). 369 stocks were traded How many milliseconds does it take a human to blink?

.")

3 Millions in Milliseconds Monday, June 03, 2013: a minor clock synchronization issue causes market-moving manufacturing data be released to select traders 15 milliseconds prior to the scheduled 10am release. Nanex (trading data analysis firm) estimates: $28 million worth of shares changed hands in 15 milliseconds 30,000 shares of SPY traded in 1 of these milliseconds (average SPY volume = 5.6 shares in a millisecond). 369 stocks were traded How many milliseconds does it take a human to blink? milliseconds!

.")

4 The Rise of the Machines: Background How did the machines rise? What are the main concerns? What we do address?

5 Trading Under a Buttonwood Tree 1792 agreement created a club, later known as NYSE

6 A Trading Floor in the Early 20th Century

7 A Trading Floor in the 1980s and 1990s

8 A Trading Floor in the New Millennium

9 A Trading Floor in the New Millennium This is now the exchange!

10 A Trading Floor in the New Millennium These are the traders/the trader s gateways.

11 How did the machines rise? Technological advances Multiple electronic venues alongside traditional exchanges Trading venues compete for trading volume (and are for-profit!) need to offer attractive quotes encourage algorithmic trading Really, really fast trading & trading decisions at speeds way beyond human reaction time

need to offer attractive quotes encourage algorithmic trading Really, really")

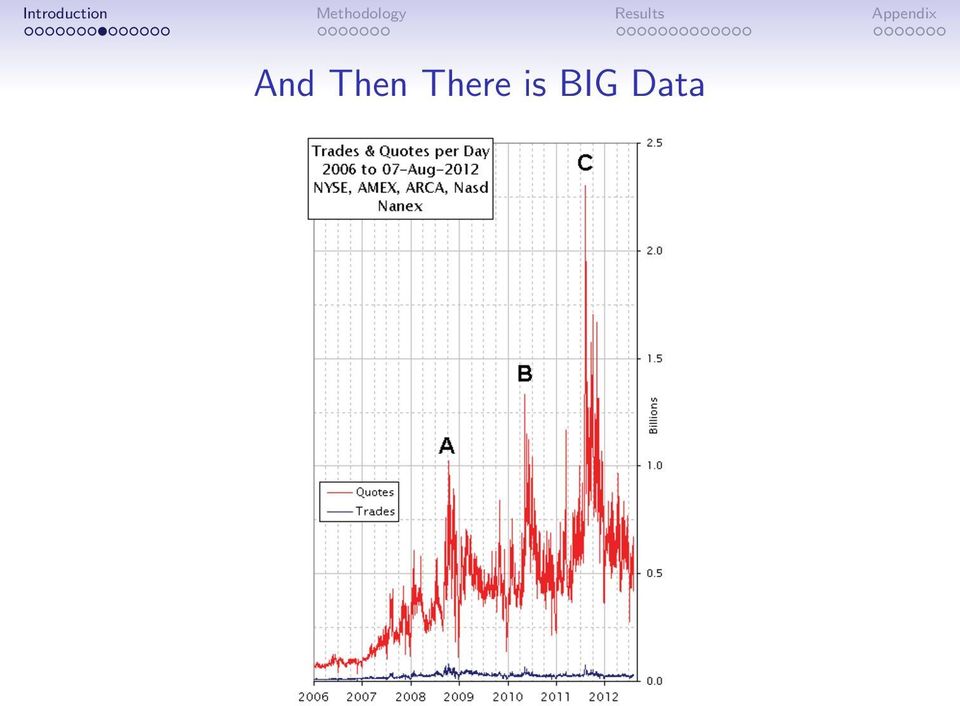

12 And Then There is BIG Data

13 HFT is contentious Uneven playing field? Systematic rent extraction? Incentives to collect/generate information? Price efficiency? Market stability?

14 What do we know about HFT/AT? 1. HFTs facilitate price efficiency Brogaard, Hendershott, and Riordan (2013) 2. HFTs make money Baron, Brogaard, Kirilenko (2012), Menkveld (2013) 3. Possible negative externalities Ye, Yao, Gai (2013); Egginton, Van Ness, and Van Ness (2013) 4. HFTs are a heterogenous group Hagströmer and Nordén (2013) 5. HFT/Quoting Activities/AT & liquidity (+) Hendershott, Jones, and Menkveld (2011) for AT; Hasbrouck and Saar (2013), Brogaard, Hagströmer, Nordén, and Riordan (2013) (-) Chakrabarty, Jain, Shkilko, Sokolov (2013) This paper: The impact of message-intensive AT on intraday costs & returns: market-wide vs. retail and institutional investors.

Hendershott, Jones, and Menkveld (2011) for AT; Hasbrouck and Saar (2013), Brogaard, Hagströmer, Nordén, and Riordan (2013) (-)")

15 A long run view Message = trade, order, cancellation, or modification HFT Messages and Bid Ask Spread log HFT messages basis points Log HFT Messages Bid Ask Spread

16 Research question: What is the impact of message-intensive trading? Message = trade, order, modification, or cancellation Casual observation: Suggests that as messaging activity (presumably by HFT) increases, market conditions improve. Problem 1: Causality? Do spreads go down because of HFT? Or vice versa? Difficult to disentangle technological progress, trading venue competition, new order types, lower trading costs. Problem 2: Who benefits and how? Can unsophisticated traders catch the low spread when quotes change at speeds beyond human reaction time? Is there a disadvantage to using limit orders? These now earn lower spreads and are more expensive to monitor.

17 The IIROC message fee Addressing problem 1: event causality The Investment Industry Regulatory Organization of Canada (IIROC) is a self-regulatory body for investment-dealers and trading activity in Canada. IIROC is funded by its members. IIROC charges dealers customers (some) April 01, 2012, IIROC switched their billing from volume-based to trade-based and message-based. Per message fee is relative to a trader s/dealer s share of messages across all marketplaces. fee is endogenous market participants did not know the amount ex-ante (ex-post message fee is $ ; typical HFT msg is for 100 shares). Per message fee is difficult to estimate (many marketplaces; so-called registered traders were exempt). Change scared those with high message traffic.

.")

18 Granular Data Addressing problem 2: Who benefits and how? Study traders with different levels of sophistication retail institutions Compute standard market quality measures; compare market-wide vs. per trader group. Study: costs and benefits to market vs. limit orders per group intraday returns to all the group s orders.

19 Data Very detailed data for the TSX for February to April 2012: all messages (orders, cancellations, trades, etc) trader-level unique identifiers for each order most detailed data available to exchanges and regulators. Focus on S&P/TSX Composite index constituents (our sample: 248 firms). Event study using March and April data. First: classify traders: message-intensive algo traders, retail, institutional.

20 Classification message-intensive algo traders: iat 1. For this classification: use 248 stocks plus 42 active ETFs 2. Compute the monthly (February 2012, pre-sample) sum of total messages (= trades, orders, cancellations, modifications, etc.) total trades 3. Compute the message-to-trade ratio. 4. Compute percentiles message-to-trade and total messages. 5. Classify as iat if 95th percentile message-to-trade and 95th percentile total number of messages

total trades 3. Compute the message-to-trade ratio. 4.")

21 Classification Retail Info from proprietary dataset that allows identification of a large number of retail traders. Specifically: traders that send market orders to Alpha IntraSpread. Important: Canada does not allow off-exchange internalization all retail orders hit public markets. Institutional Idea: find traders that build large positions. Compute the cumulative inventory per stock If abs value of the inventory ever exceeds $25 million and not iat or retail institutional

22 Summary Statistics Market iat Retail Instit s Units unique identifiers 3, share of $-volume % share of messages % msgs per minute per ID

23 Market Quality Measures TSX operates as a limit order book limit orders: set quotes, give others an option to trade market orders: trade against posted limit orders Bid-ask spread measures: 1. quoted spread: all posted/visible quotes 2. effective half-spread: uses prices that were actually paid 3. price impact: signed price movement after the trade (5 min). adverse selection costs for the limit order 4. realized half-spread effective half-spread minus price impact compensation for liquidity provision

24 Summary Statistics Market iat Retail Instit s Units % vol traded with LO % % limit order vol filled %

25 Summary Statistics Market iat Retail Instit s Units % vol traded with LO % % limit order vol filled % effective half-spread bps realized half-spread bps

26 1. Event study: Regression Methodology Two approaches dependent variable it = α 1 event t + α 2 VIX t + δ i + ǫ it 2. Instrumental Variable estimation: iat activity it = β 1 event t + β 2 VIX t + δ i + ǫ it dependent variable it = β 3iAT activityit + β 4 VIX t + δ i + ǫ it iat activity measured by %iat of all messages and ln(iat messages). For both cases: δ i are firm fixed effects and VIX t controls for market-wide fluctuations. Presentation: event study

27 Questions 1. What happens to iats and market quality after the fee is introduced? 2. How do the changes affect the trading costs for retail and institutional traders (vs. market average) and their order submission behaviour? 3. How did the change affect traders intraday returns?

28 Q.1: What happens to iat and market-wide measures? Assumption: message-intensive = market making. Baruch and Glosten (2013) support this theoretically. See also: Getco letter to IIROC. Need to frequently re-quote in response to new info. Predictions: 1. Market makers reduce (re-)quoting activities higher risk of being adversely selected require higher compensation (Copeland and Galai (1983), Foucault (1999)) 2. price impact of market orders ր and bid-ask spread ր (e.g., Bernales (2013) or Getco s comment to IIROC).

29 Q.1: The Impact of the Fee Change All measures are in basis points Time weighted quoted spread vs. %iat basis points percent pre sample iat classification period Mar 1 Apr 1 May 1 quoted spread, av. before/after quoted spread % iat messages, av before/after %iat messages

30 Q.1: Effect of iat on market quality time weighted quoted spread effective spread 5-minute price impact 5-minute realized spread event 0.49*** 0.35*** 0.82*** -0.44*** (0.14) (0.13) (0.19) (0.13) iat messages ց by 31%. Quoted, effective spreads, and price impact ր Realized spread (compensation for liquidity provision) ց.

31 Q.2: What happens to trading costs of retail and institutions? Market order trading costs: Prediction 1: higher market-wide spread higher per-group spread.

32 Q.2: What happens to trading costs of retail and institutions? Market order trading costs: Prediction 1: higher market-wide spread higher per-group spread. Adverse selection for limit orders: Based on Hoffman (2013) model of slow and fast traders. only fast traders are able to re-quote if new info arrives. slow traders are always adversely selected if new info arrives. Prediction 2: slow traders adverse selection costs not affected by changes in iat quoting.

33 Q.2: What happens to trading costs of retail and institutions? Market order trading costs: Prediction 1: higher market-wide spread higher per-group spread. Adverse selection for limit orders: Based on Hoffman (2013) model of slow and fast traders. only fast traders are able to re-quote if new info arrives. slow traders are always adversely selected if new info arrives. Prediction 2: slow traders adverse selection costs not affected by changes in iat quoting. Trading costs/returns for limit orders: No directional prediction. Idea: indifferent between a market and a limit order. relationship between profits to market orders, profits to limit orders, and the fill rate for limit orders.

34 Effective Spread Effective spreads paid for MO received on LO Retail (0.14) (0.15) Institutions 0.49*** 0.41*** (0.14) (0.14)

35 Adverse Selection: Price Impact Price Impact caused by MO suffered on LO Retail ** (0.24) (0.42) Institutions 0.99*** 1.14*** (0.24) (0.29)

36 Q2: Effect on retail and institutional traders behavior Changes in the usage of limit vs. market orders? % volume traded with LOs % volume submitted as LOs % orders submitted as LOs Retail event * (0.62) (0.54) (0.50) Institutional event -1.80** ** (0.71) (0.61) (0.63)

37 Q.2: What happens to trading costs of retail and institutions? Retail: no change in the spread paid for MO or the price impact of MO no change for MO face higher adverse selection on LO but no change in the spread received lose on LO. Institutions: higher price impact of MO after the change, yet underpay for this increase benefit on MO face higher adverse selection when using LO, yet undercompensated for it lose on LO

38 Realized Spread Realized spread paid for MO received on LO Retail * (0.25) (0.41) Institutions -0.48*** -0.71*** (0.18) (0.23)

39 Step 3: Effect of iat on intraday returns? Instead of a 5-minute benchmark, use the closing price Intraday return: profits from buying and selling. On day t, for each group, compute: profit t = sell $volume t buy $ volume t +(buy volume t sell volume t ) closing price t scale by: buy $ volume t +sell $ volume t gain/loss relative to the end-of-the-day price captures intraday price movements subsequent to trade Compute returns to: market orders limit orders all orders

40 Step 3: Effect of iat on trading costs & returns? Intraday Returns by Groups of Traders Intraday return mean (March) all market limit all market limit orders orders orders orders orders orders Retail traders -3.93** * (1.64) (1.49) (3.33) Institutional traders *** (1.11) (1.97) (1.79) Extensions

41 Summary IIROC fee change led to a significant reduction in message-intensive activities. Reduction caused an increase in market-wide bid-ask spread. Yet: retail traders costs for market orders are unaffected, but they lose more on limit orders. in our data, iat activities are beneficial for retail. Institutions pay larger spreads, but the increase is smaller than the increase in their price impact. institutions earn higher intraday returns on market orders. Easier to capitalize on information?

Do retail traders suffer from high frequency traders?

Do retail traders suffer from high frequency traders? Katya Malinova Andreas Park Ryan Riordan October 3, 2013 Abstract Using a change in regulatory fees in Canada in April 2012 that affected algorithmic

Do retail traders suffer from high frequency traders? Katya Malinova Andreas Park Ryan Riordan October 3, 2013 Abstract Using a change in regulatory fees in Canada in April 2012 that affected algorithmic

Shifting Sands: High Frequency, Retail, and Institutional Trading Profits over Time

Shifting Sands: High Frequency, Retail, and Institutional Trading Profits over Time Katya Malinova University of Toronto Andreas Park University of Toronto Ryan Riordan University of Ontario Institute

Shifting Sands: High Frequency, Retail, and Institutional Trading Profits over Time Katya Malinova University of Toronto Andreas Park University of Toronto Ryan Riordan University of Ontario Institute

High-frequency trading and execution costs

High-frequency trading and execution costs Amy Kwan Richard Philip* Current version: January 13 2015 Abstract We examine whether high-frequency traders (HFT) increase the transaction costs of slower institutional

High-frequency trading and execution costs Amy Kwan Richard Philip* Current version: January 13 2015 Abstract We examine whether high-frequency traders (HFT) increase the transaction costs of slower institutional

The Impact of the Dark Trading Rules

The Impact of the Dark Trading Rules Report prepared for the Investment Industry Regulatory Organization of Canada Carole Comerton-Forde, Katya Malinova, Andreas Park University of Melbourne University

The Impact of the Dark Trading Rules Report prepared for the Investment Industry Regulatory Organization of Canada Carole Comerton-Forde, Katya Malinova, Andreas Park University of Melbourne University

Regulating Dark Trading: Order Flow Segmentation and Market Quality

Regulating Dark Trading: Order Flow Segmentation and Market Quality Carole Comerton-Forde, Katya Malinova, Andreas Park IIROC and the Capital Markets Institute Forum on High Frequency Trading October 19,

Regulating Dark Trading: Order Flow Segmentation and Market Quality Carole Comerton-Forde, Katya Malinova, Andreas Park IIROC and the Capital Markets Institute Forum on High Frequency Trading October 19,

HFT and Market Quality

HFT and Market Quality BRUNO BIAIS Directeur de recherche Toulouse School of Economics (CRM/CNRS - Chaire FBF/ IDEI) THIERRY FOUCAULT* Professor of Finance HEC, Paris I. Introduction The rise of high-frequency

HFT and Market Quality BRUNO BIAIS Directeur de recherche Toulouse School of Economics (CRM/CNRS - Chaire FBF/ IDEI) THIERRY FOUCAULT* Professor of Finance HEC, Paris I. Introduction The rise of high-frequency

From Traditional Floor Trading to Electronic High Frequency Trading (HFT) Market Implications and Regulatory Aspects Prof. Dr. Hans Peter Burghof

Market Implications and Regulatory Aspects Prof. Dr. Hans Peter Burghof") From Traditional Floor Trading to Electronic High Frequency Trading (HFT) Market Implications and Regulatory Aspects Prof. Dr. Hans Peter Burghof Universität Hohenheim Institut für Financial Management

From Traditional Floor Trading to Electronic High Frequency Trading (HFT) Market Implications and Regulatory Aspects Prof. Dr. Hans Peter Burghof Universität Hohenheim Institut für Financial Management

(Risk and Return in High Frequency Trading)

") The Trading Profits of High Frequency Traders (Risk and Return in High Frequency Trading) Matthew Baron Princeton University Jonathan Brogaard University of Washington Andrei Kirilenko CFTC 8th Annual

The Trading Profits of High Frequency Traders (Risk and Return in High Frequency Trading) Matthew Baron Princeton University Jonathan Brogaard University of Washington Andrei Kirilenko CFTC 8th Annual

Fast Trading and Prop Trading

Fast Trading and Prop Trading B. Biais, F. Declerck, S. Moinas (Toulouse School of Economics) December 11, 2014 Market Microstructure Confronting many viewpoints #3 New market organization, new financial

Fast Trading and Prop Trading B. Biais, F. Declerck, S. Moinas (Toulouse School of Economics) December 11, 2014 Market Microstructure Confronting many viewpoints #3 New market organization, new financial

News Trading and Speed

News Trading and Speed Thierry Foucault, Johan Hombert, Ioanid Roşu (HEC Paris) 6th Financial Risks International Forum March 25-26, 2013, Paris Johan Hombert (HEC Paris) News Trading and Speed 6th Financial

News Trading and Speed Thierry Foucault, Johan Hombert, Ioanid Roşu (HEC Paris) 6th Financial Risks International Forum March 25-26, 2013, Paris Johan Hombert (HEC Paris) News Trading and Speed 6th Financial

High frequency trading

High frequency trading Bruno Biais (Toulouse School of Economics) Presentation prepared for the European Institute of Financial Regulation Paris, Sept 2011 Outline 1) Description 2) Motivation for HFT

High frequency trading Bruno Biais (Toulouse School of Economics) Presentation prepared for the European Institute of Financial Regulation Paris, Sept 2011 Outline 1) Description 2) Motivation for HFT

Should Exchanges impose Market Maker obligations? Amber Anand. Kumar Venkataraman. Abstract

Should Exchanges impose Market Maker obligations? Amber Anand Kumar Venkataraman Abstract We study the trades of two important classes of market makers, Designated Market Makers (DMMs) and Endogenous Liquidity

Should Exchanges impose Market Maker obligations? Amber Anand Kumar Venkataraman Abstract We study the trades of two important classes of market makers, Designated Market Makers (DMMs) and Endogenous Liquidity

High Frequency Quoting, Trading and the Efficiency of Prices. Jennifer Conrad, UNC Sunil Wahal, ASU Jin Xiang, Integrated Financial Engineering

High Frequency Quoting, Trading and the Efficiency of Prices Jennifer Conrad, UNC Sunil Wahal, ASU Jin Xiang, Integrated Financial Engineering 1 What is High Frequency Quoting/Trading? How fast is fast?

High Frequency Quoting, Trading and the Efficiency of Prices Jennifer Conrad, UNC Sunil Wahal, ASU Jin Xiang, Integrated Financial Engineering 1 What is High Frequency Quoting/Trading? How fast is fast?

Trading Fast and Slow: Colocation and Market Quality*

Trading Fast and Slow: Colocation and Market Quality* Jonathan Brogaard Björn Hagströmer Lars Nordén Ryan Riordan First Draft: August 2013 Current Draft: November 2013 Abstract: Using user-level data from

Trading Fast and Slow: Colocation and Market Quality* Jonathan Brogaard Björn Hagströmer Lars Nordén Ryan Riordan First Draft: August 2013 Current Draft: November 2013 Abstract: Using user-level data from

Dark trading and price discovery

Dark trading and price discovery Carole Comerton-Forde University of Melbourne and Tālis Putniņš University of Technology, Sydney Market Microstructure Confronting Many Viewpoints 11 December 2014 What

Dark trading and price discovery Carole Comerton-Forde University of Melbourne and Tālis Putniņš University of Technology, Sydney Market Microstructure Confronting Many Viewpoints 11 December 2014 What

News Trading and Speed

News Trading and Speed Thierry Foucault, Johan Hombert, and Ioanid Rosu (HEC) High Frequency Trading Conference Plan Plan 1. Introduction - Research questions 2. Model 3. Is news trading different? 4.

News Trading and Speed Thierry Foucault, Johan Hombert, and Ioanid Rosu (HEC) High Frequency Trading Conference Plan Plan 1. Introduction - Research questions 2. Model 3. Is news trading different? 4.

This paper sets out the challenges faced to maintain efficient markets, and the actions that the WFE and its member exchanges support.

Understanding High Frequency Trading (HFT) Executive Summary This paper is designed to cover the definitions of HFT set by regulators, the impact HFT has made on markets, the actions taken by exchange

Understanding High Frequency Trading (HFT) Executive Summary This paper is designed to cover the definitions of HFT set by regulators, the impact HFT has made on markets, the actions taken by exchange

- JPX Working Paper - Analysis of High-Frequency Trading at Tokyo Stock Exchange. March 2014, Go Hosaka, Tokyo Stock Exchange, Inc

- JPX Working Paper - Analysis of High-Frequency Trading at Tokyo Stock Exchange March 2014, Go Hosaka, Tokyo Stock Exchange, Inc 1. Background 2. Earlier Studies 3. Data Sources and Estimates 4. Empirical

- JPX Working Paper - Analysis of High-Frequency Trading at Tokyo Stock Exchange March 2014, Go Hosaka, Tokyo Stock Exchange, Inc 1. Background 2. Earlier Studies 3. Data Sources and Estimates 4. Empirical

ELECTRONIC TRADING GLOSSARY

ELECTRONIC TRADING GLOSSARY Algorithms: A series of specific steps used to complete a task. Many firms use them to execute trades with computers. Algorithmic Trading: The practice of using computer software

ELECTRONIC TRADING GLOSSARY Algorithms: A series of specific steps used to complete a task. Many firms use them to execute trades with computers. Algorithmic Trading: The practice of using computer software

How aggressive are high frequency traders?

How aggressive are high frequency traders? Björn Hagströmer, Lars Nordén and Dong Zhang Stockholm University School of Business, S 106 91 Stockholm July 30, 2013 Abstract We study order aggressiveness

How aggressive are high frequency traders? Björn Hagströmer, Lars Nordén and Dong Zhang Stockholm University School of Business, S 106 91 Stockholm July 30, 2013 Abstract We study order aggressiveness

The Impact of Co-Location of Securities Exchanges and Traders Computer Servers on Market Liquidity

The Impact of Co-Location of Securities Exchanges and Traders Computer Servers on Market Liquidity Alessandro Frino European Capital Markets CRC Vito Mollica Macquarie Graduate School of Management Robert

The Impact of Co-Location of Securities Exchanges and Traders Computer Servers on Market Liquidity Alessandro Frino European Capital Markets CRC Vito Mollica Macquarie Graduate School of Management Robert

Market Making and Liquidity Provision in Modern Markets

Canada STA 2015 Market Making and Liquidity Provision in Modern Markets Phil Mackintosh 2 What am I going to talk about? Why are Modern Markets Important? Trading is now physics at the speed of light Jan

Canada STA 2015 Market Making and Liquidity Provision in Modern Markets Phil Mackintosh 2 What am I going to talk about? Why are Modern Markets Important? Trading is now physics at the speed of light Jan

Toxic Arbitrage. Abstract

Toxic Arbitrage Thierry Foucault Roman Kozhan Wing Wah Tham Abstract Arbitrage opportunities arise when new information affects the price of one security because dealers in other related securities are

Toxic Arbitrage Thierry Foucault Roman Kozhan Wing Wah Tham Abstract Arbitrage opportunities arise when new information affects the price of one security because dealers in other related securities are

Trading Fast and Slow: Colocation and Market Quality*

Trading Fast and Slow: Colocation and Market Quality* Jonathan Brogaard Björn Hagströmer Lars Nordén Ryan Riordan First Draft: August 2013 Current Draft: December 2013 Abstract: Using user-level data from

Trading Fast and Slow: Colocation and Market Quality* Jonathan Brogaard Björn Hagströmer Lars Nordén Ryan Riordan First Draft: August 2013 Current Draft: December 2013 Abstract: Using user-level data from

Execution Costs of Exchange Traded Funds (ETFs)

") MARKET INSIGHTS Execution Costs of Exchange Traded Funds (ETFs) By Jagjeev Dosanjh, Daniel Joseph and Vito Mollica August 2012 Edition 37 in association with THE COMPANY ASX is a multi-asset class, vertically

MARKET INSIGHTS Execution Costs of Exchange Traded Funds (ETFs) By Jagjeev Dosanjh, Daniel Joseph and Vito Mollica August 2012 Edition 37 in association with THE COMPANY ASX is a multi-asset class, vertically

High Frequency Trading Background and Current Regulatory Discussion

2. DVFA Banken Forum Frankfurt 20. Juni 2012 High Frequency Trading Background and Current Regulatory Discussion Prof. Dr. Peter Gomber Chair of Business Administration, especially e-finance E-Finance

2. DVFA Banken Forum Frankfurt 20. Juni 2012 High Frequency Trading Background and Current Regulatory Discussion Prof. Dr. Peter Gomber Chair of Business Administration, especially e-finance E-Finance

Algorithmic trading Equilibrium, efficiency & stability

Algorithmic trading Equilibrium, efficiency & stability Presentation prepared for the conference Market Microstructure: Confronting many viewpoints Institut Louis Bachelier Décembre 2010 Bruno Biais Toulouse

Algorithmic trading Equilibrium, efficiency & stability Presentation prepared for the conference Market Microstructure: Confronting many viewpoints Institut Louis Bachelier Décembre 2010 Bruno Biais Toulouse

How Does Algorithmic Trading Improve Market. Quality?

How Does Algorithmic Trading Improve Market Quality? Matthew R. Lyle, James P. Naughton, Brian M. Weller Kellogg School of Management August 19, 2015 Abstract We use a comprehensive panel of NYSE limit

How Does Algorithmic Trading Improve Market Quality? Matthew R. Lyle, James P. Naughton, Brian M. Weller Kellogg School of Management August 19, 2015 Abstract We use a comprehensive panel of NYSE limit

Algorithmic Trading, High-Frequency Trading and Colocation: What does it mean to Emerging Market?

Algorithmic Trading, High-Frequency Trading and Colocation: What does it mean to Emerging Market? Ashok Jhunjhunwala, IIT Madras [email protected] HFTs are being pushed out of the more established markets,

Algorithmic Trading, High-Frequency Trading and Colocation: What does it mean to Emerging Market? Ashok Jhunjhunwala, IIT Madras [email protected] HFTs are being pushed out of the more established markets,

Toxic Equity Trading Order Flow on Wall Street

Toxic Equity Trading Order Flow on Wall Street INTRODUCTION The Real Force Behind the Explosion in Volume and Volatility By Sal L. Arnuk and Joseph Saluzzi A Themis Trading LLC White Paper Retail and institutional

Toxic Equity Trading Order Flow on Wall Street INTRODUCTION The Real Force Behind the Explosion in Volume and Volatility By Sal L. Arnuk and Joseph Saluzzi A Themis Trading LLC White Paper Retail and institutional

Intraday Patterns in High Frequency Trading: Evidence from the UK Equity Markets

Intraday Patterns in High Frequency Trading: Evidence from the UK Equity Markets Kiril Alampieski a and Andrew Lepone b 1 a Finance Discipline, Faculty of Economics and Business, University of Sydney,

Intraday Patterns in High Frequency Trading: Evidence from the UK Equity Markets Kiril Alampieski a and Andrew Lepone b 1 a Finance Discipline, Faculty of Economics and Business, University of Sydney,

Fast Aggressive Trading

Fast Aggressive Trading Richard Payne Professor of Finance Faculty of Finance, Cass Business School Global Association of Risk Professionals May 2015 The views expressed in the following material are the

Fast Aggressive Trading Richard Payne Professor of Finance Faculty of Finance, Cass Business School Global Association of Risk Professionals May 2015 The views expressed in the following material are the

Equilibrium High Frequency Trading

Equilibrium High Frequency Trading B. Biais, T. Foucault, S. Moinas Fifth Annual Conference of the Paul Woolley Centre for the Study of Capital Market Dysfunctionality London, June 2012 What s High Frequency

Equilibrium High Frequency Trading B. Biais, T. Foucault, S. Moinas Fifth Annual Conference of the Paul Woolley Centre for the Study of Capital Market Dysfunctionality London, June 2012 What s High Frequency

G100 VIEWS HIGH FREQUENCY TRADING. Group of 100

G100 VIEWS ON HIGH FREQUENCY TRADING DECEMBER 2012 -1- Over the last few years there has been a marked increase in media and regulatory scrutiny of high frequency trading ("HFT") in Australia. HFT, a subset

G100 VIEWS ON HIGH FREQUENCY TRADING DECEMBER 2012 -1- Over the last few years there has been a marked increase in media and regulatory scrutiny of high frequency trading ("HFT") in Australia. HFT, a subset

HIGH FREQUENCY TRADING AND ITS IMPACT ON MARKET QUALITY

HIGH FREQUENCY TRADING AND ITS IMPACT ON MARKET QUALITY Jonathan A. Brogaard Northwestern University Kellogg School of Management Northwestern University School of Law JD-PhD Candidate [email protected]

HIGH FREQUENCY TRADING AND ITS IMPACT ON MARKET QUALITY Jonathan A. Brogaard Northwestern University Kellogg School of Management Northwestern University School of Law JD-PhD Candidate [email protected]

a. CME Has Conducted an Initial Review of Detailed Trading Records

TESTIMONY OF TERRENCE A. DUFFY EXECUTIVE CHAIRMAN CME GROUP INC. BEFORE THE Subcommittee on Capital Markets, Insurance and Government Sponsored Enterprises of the HOUSE COMMITTEE ON FINANCIAL SERVICES

TESTIMONY OF TERRENCE A. DUFFY EXECUTIVE CHAIRMAN CME GROUP INC. BEFORE THE Subcommittee on Capital Markets, Insurance and Government Sponsored Enterprises of the HOUSE COMMITTEE ON FINANCIAL SERVICES

How To Understand The Role Of High Frequency Trading

High Frequency Trading and Price Discovery * by Terrence Hendershott (University of California at Berkeley) Ryan Riordan (Karlsruhe Institute of Technology) * We thank Frank Hatheway and Jeff Smith at

High Frequency Trading and Price Discovery * by Terrence Hendershott (University of California at Berkeley) Ryan Riordan (Karlsruhe Institute of Technology) * We thank Frank Hatheway and Jeff Smith at

What is High Frequency Trading?

What is High Frequency Trading? Released December 29, 2014 The impact of high frequency trading or HFT on U.S. equity markets has generated significant attention in recent years and increasingly in the

What is High Frequency Trading? Released December 29, 2014 The impact of high frequency trading or HFT on U.S. equity markets has generated significant attention in recent years and increasingly in the

CFDs and Liquidity Provision

2011 International Conference on Financial Management and Economics IPEDR vol.11 (2011) (2011) IACSIT Press, Singapore CFDs and Liquidity Provision Andrew Lepone and Jin Young Yang Discipline of Finance,

2011 International Conference on Financial Management and Economics IPEDR vol.11 (2011) (2011) IACSIT Press, Singapore CFDs and Liquidity Provision Andrew Lepone and Jin Young Yang Discipline of Finance,

THE IMPACT OF CO LOCATION OF SECURITIES EXCHANGES AND TRADERS COMPUTER SERVERS ON MARKET LIQUIDITY

THE IMPACT OF CO LOCATION OF SECURITIES EXCHANGES AND TRADERS COMPUTER SERVERS ON MARKET LIQUIDITY ALEX FRINO, VITO MOLLICA* and ROBERT I. WEBB This study examines the impact of allowing traders to co

THE IMPACT OF CO LOCATION OF SECURITIES EXCHANGES AND TRADERS COMPUTER SERVERS ON MARKET LIQUIDITY ALEX FRINO, VITO MOLLICA* and ROBERT I. WEBB This study examines the impact of allowing traders to co

Are Market Center Trading Cost Measures Reliable? *

JEL Classification: G19 Keywords: equities, trading costs, liquidity Are Market Center Trading Cost Measures Reliable? * Ryan GARVEY Duquesne University, Pittsburgh ([email protected]) Fei WU International

JEL Classification: G19 Keywords: equities, trading costs, liquidity Are Market Center Trading Cost Measures Reliable? * Ryan GARVEY Duquesne University, Pittsburgh ([email protected]) Fei WU International

FIA AND FIA EUROPE SPECIAL REPORT SERIES: ALGORITHMIC AND HIGH FREQUENCY TRADING

FIA AND FIA EUROPE SPECIAL REPORT SERIES: ALGORITHMIC AND HIGH FREQUENCY TRADING 18 February 2015 This Special Report is the fourth in the FIA and FIA Europe s series covering specific areas of the European

FIA AND FIA EUROPE SPECIAL REPORT SERIES: ALGORITHMIC AND HIGH FREQUENCY TRADING 18 February 2015 This Special Report is the fourth in the FIA and FIA Europe s series covering specific areas of the European

FAIR GAME OR FATALLY FLAWED?

ISN RESEARCH FAIR GAME OR FATALLY FLAWED? SOME COSTS OF HIGH FREQUENCY TRADING IN LOW LATENCY MARKETS June 2013 KEY POINTS The activity of High Frequency Traders (HF traders) in Australia s equity markets

ISN RESEARCH FAIR GAME OR FATALLY FLAWED? SOME COSTS OF HIGH FREQUENCY TRADING IN LOW LATENCY MARKETS June 2013 KEY POINTS The activity of High Frequency Traders (HF traders) in Australia s equity markets

High-Frequency Trading Competition

High-Frequency Trading Competition Jonathan Brogaard and Corey Garriott* May 2015 Abstract High-frequency trading (HFT) firms have been shown to influence market quality by exploiting a speed advantage.

High-Frequency Trading Competition Jonathan Brogaard and Corey Garriott* May 2015 Abstract High-frequency trading (HFT) firms have been shown to influence market quality by exploiting a speed advantage.

The Growth of High-Frequency Trading: Implications for Financial Stability

The Growth of High-Frequency Trading: Implications for Financial Stability William Barker and Anna Pomeranets Introduction High-frequency trading (HFT), which relies on computers to execute trades at high

The Growth of High-Frequency Trading: Implications for Financial Stability William Barker and Anna Pomeranets Introduction High-frequency trading (HFT), which relies on computers to execute trades at high

Analysis of High-frequency Trading at Tokyo Stock Exchange

This article was translated by the author and reprinted from the June 2014 issue of the Securities Analysts Journal with the permission of the Securities Analysts Association of Japan (SAAJ). Analysis

This article was translated by the author and reprinted from the June 2014 issue of the Securities Analysts Journal with the permission of the Securities Analysts Association of Japan (SAAJ). Analysis

Speed, Algorithmic Trading, and Market Quality around Macroeconomic News Announcements

TI 212-121/III Tinbergen Institute Discussion Paper Speed, Algorithmic Trading, and Market Quality around Macroeconomic News Announcements Martin L. Scholtus 1 Dick van Dijk 1 Bart Frijns 2 1 Econometric

TI 212-121/III Tinbergen Institute Discussion Paper Speed, Algorithmic Trading, and Market Quality around Macroeconomic News Announcements Martin L. Scholtus 1 Dick van Dijk 1 Bart Frijns 2 1 Econometric

Need For Speed? Low Latency Trading and Adverse Selection

Need For Speed? Low Latency Trading and Adverse Selection Albert J. Menkveld and Marius A. Zoican April 22, 2013 - very preliminary and incomplete. comments and suggestions are welcome - First version:

Need For Speed? Low Latency Trading and Adverse Selection Albert J. Menkveld and Marius A. Zoican April 22, 2013 - very preliminary and incomplete. comments and suggestions are welcome - First version:

High Frequency Trading Volumes Continue to Increase Throughout the World

High Frequency Trading Volumes Continue to Increase Throughout the World High Frequency Trading (HFT) can be defined as any automated trading strategy where investment decisions are driven by quantitative

High Frequency Trading Volumes Continue to Increase Throughout the World High Frequency Trading (HFT) can be defined as any automated trading strategy where investment decisions are driven by quantitative

Should Exchanges impose Market Maker obligations? Amber Anand Syracuse University. Kumar Venkataraman Southern Methodist University.

Should Exchanges impose Market Maker obligations? Amber Anand Syracuse University Kumar Venkataraman Southern Methodist University Abstract Using Toronto Stock Exchange data, we study the trades of Endogenous

Should Exchanges impose Market Maker obligations? Amber Anand Syracuse University Kumar Venkataraman Southern Methodist University Abstract Using Toronto Stock Exchange data, we study the trades of Endogenous

Stock Trading Systems: A Comparison of US and China. April 30, 2016 Session 5 Joel Hasbrouck www.stern.nyu.edu/~jhasbrou

Stock Trading Systems: A Comparison of US and China April 30, 2016 Session 5 Joel Hasbrouck www.stern.nyu.edu/~jhasbrou 1 1. Regulatory priorities for capital formation and growth. 2 The information environment

Stock Trading Systems: A Comparison of US and China April 30, 2016 Session 5 Joel Hasbrouck www.stern.nyu.edu/~jhasbrou 1 1. Regulatory priorities for capital formation and growth. 2 The information environment

Maker/taker pricing and high frequency trading

Maker/taker pricing and high frequency trading Economic Impact Assessment EIA12 Foresight, Government Office for Science Contents 1. Objective... 3 2. Background... 3 3. Existing make/take fee structure...

Maker/taker pricing and high frequency trading Economic Impact Assessment EIA12 Foresight, Government Office for Science Contents 1. Objective... 3 2. Background... 3 3. Existing make/take fee structure...

High-Frequency Trading and Price Discovery

High-Frequency Trading and Price Discovery Jonathan Brogaard University of Washington Terrence Hendershott University of California at Berkeley Ryan Riordan University of Ontario Institute of Technology

High-Frequency Trading and Price Discovery Jonathan Brogaard University of Washington Terrence Hendershott University of California at Berkeley Ryan Riordan University of Ontario Institute of Technology

High-frequency trading

Economics & politics Research Briefing February 7, 2011 High-frequency trading Better than its reputation? Over the past years, high-frequency trading has progressively gained a foothold in financial markets,

Economics & politics Research Briefing February 7, 2011 High-frequency trading Better than its reputation? Over the past years, high-frequency trading has progressively gained a foothold in financial markets,

High-frequency trading: towards capital market efficiency, or a step too far?

Agenda Advancing economics in business High-frequency trading High-frequency trading: towards capital market efficiency, or a step too far? The growth in high-frequency trading has been a significant development

Agenda Advancing economics in business High-frequency trading High-frequency trading: towards capital market efficiency, or a step too far? The growth in high-frequency trading has been a significant development

High Frequency Trading An Asset Manager s Perspective

NBIM Discussion NOTE #1-2013 High Frequency Trading An Asset Manager s Perspective In this note we review the rapidly expanding literature in the area of market microstructure, high frequency and computer-based

NBIM Discussion NOTE #1-2013 High Frequency Trading An Asset Manager s Perspective In this note we review the rapidly expanding literature in the area of market microstructure, high frequency and computer-based

Volatility Series Trading Halts

AUTHORS Ben Polidore Managing Director Head of ITG Algorithms [email protected] Philip Pearson, CFA Director ITG Algorithms [email protected] CONTACT Asia Pacific +852.2846.3500 Canada +1.416.874.0900

AUTHORS Ben Polidore Managing Director Head of ITG Algorithms [email protected] Philip Pearson, CFA Director ITG Algorithms [email protected] CONTACT Asia Pacific +852.2846.3500 Canada +1.416.874.0900

High Frequency Trading and the 2008 Shorting Ban

High Frequency Trading and the 2008 Shorting Ban Using the ban to estimate HFT s impact on markets challenge is it also impacted other short sellers Jonathan Brogaard Terrence Hendershott Ryan Riordan

High Frequency Trading and the 2008 Shorting Ban Using the ban to estimate HFT s impact on markets challenge is it also impacted other short sellers Jonathan Brogaard Terrence Hendershott Ryan Riordan

The Impacts of Automation and High Frequency Trading on Market Quality 1

The Impacts of Automation and High Frequency Trading on Market Quality 1 Robert Litzenberger 2, Jeff Castura and Richard Gorelick 3 In recent decades, U.S. equity markets have changed from predominantly

The Impacts of Automation and High Frequency Trading on Market Quality 1 Robert Litzenberger 2, Jeff Castura and Richard Gorelick 3 In recent decades, U.S. equity markets have changed from predominantly

High Frequency Trading around Macroeconomic News Announcements. Evidence from the US Treasury market. George J. Jiang Ingrid Lo Giorgio Valente 1

High Frequency Trading around Macroeconomic News Announcements Evidence from the US Treasury market George J. Jiang Ingrid Lo Giorgio Valente 1 This draft: November 2013 1 George J. Jiang is from the Department

High Frequency Trading around Macroeconomic News Announcements Evidence from the US Treasury market George J. Jiang Ingrid Lo Giorgio Valente 1 This draft: November 2013 1 George J. Jiang is from the Department

Nine Questions Every ETF Investor Should Ask Before Investing

Nine Questions Every ETF Investor Should Ask Before Investing UnderstandETFs.org Copyright 2012 by the Investment Company Institute. All rights reserved. ICI permits use of this publication in any way,

Nine Questions Every ETF Investor Should Ask Before Investing UnderstandETFs.org Copyright 2012 by the Investment Company Institute. All rights reserved. ICI permits use of this publication in any way,

What do we know about high-frequency trading? Charles M. Jones* Columbia Business School Version 3.4: March 20, 2013 ABSTRACT

What do we know about high-frequency trading? Charles M. Jones* Columbia Business School Version 3.4: March 20, 2013 ABSTRACT This paper reviews recent theoretical and empirical research on high-frequency

What do we know about high-frequency trading? Charles M. Jones* Columbia Business School Version 3.4: March 20, 2013 ABSTRACT This paper reviews recent theoretical and empirical research on high-frequency

Best Online Trading Platform Saudi Arabia

Best Online Trading Platform Saudi Arabia 2009 2009 A NEW CHAPTER BEGINS The kingdom of Saudi Arabia is about to witness a major development in the capital market with the launch of a new asset class (Exchange

Best Online Trading Platform Saudi Arabia 2009 2009 A NEW CHAPTER BEGINS The kingdom of Saudi Arabia is about to witness a major development in the capital market with the launch of a new asset class (Exchange

EVOLUTION OF CANADIAN EQUITY MARKETS

EVOLUTION OF CANADIAN EQUITY MARKETS This paper is the first in a series aimed at examining the long-term impact of changes in Canada s equity market structure. Our hope is that this series can help inform

EVOLUTION OF CANADIAN EQUITY MARKETS This paper is the first in a series aimed at examining the long-term impact of changes in Canada s equity market structure. Our hope is that this series can help inform

Non-Transparent Actively Managed ETFs A Revolution in the Making Exchange Traded Forum 2013 Toronto May 2, 2013

Non-Transparent Actively Managed ETFs A Revolution in the Making Exchange Traded Forum 2013 Toronto May 2, 2013 Jeffrey Shaul, CFA, FCSI, President and CEO The Coming Revolution in Actively Managed ETFs

Non-Transparent Actively Managed ETFs A Revolution in the Making Exchange Traded Forum 2013 Toronto May 2, 2013 Jeffrey Shaul, CFA, FCSI, President and CEO The Coming Revolution in Actively Managed ETFs

Delivering NIST Time to Financial Markets Via Common-View GPS Measurements

Delivering NIST Time to Financial Markets Via Common-View GPS Measurements Michael Lombardi NIST Time and Frequency Division [email protected] 55 th CGSIC Meeting Timing Subcommittee Tampa, Florida September

Delivering NIST Time to Financial Markets Via Common-View GPS Measurements Michael Lombardi NIST Time and Frequency Division [email protected] 55 th CGSIC Meeting Timing Subcommittee Tampa, Florida September

INTRODUCTION. This program should serve as just one element of your due diligence.

FOREX ONLINE LEARNING PROGRAM INTRODUCTION Welcome to our Forex Online Learning Program. We ve always believed that one of the best ways to protect investors is to provide them with the materials they

FOREX ONLINE LEARNING PROGRAM INTRODUCTION Welcome to our Forex Online Learning Program. We ve always believed that one of the best ways to protect investors is to provide them with the materials they

Working Paper SerieS. High Frequency Trading and Price Discovery. NO 1602 / november 2013. Jonathan Brogaard, Terrence Hendershott and Ryan Riordan

Working Paper SerieS NO 1602 / november 2013 High Frequency Trading and Price Discovery Jonathan Brogaard, Terrence Hendershott and Ryan Riordan ecb lamfalussy fellowship Programme In 2013 all ECB publications

Working Paper SerieS NO 1602 / november 2013 High Frequency Trading and Price Discovery Jonathan Brogaard, Terrence Hendershott and Ryan Riordan ecb lamfalussy fellowship Programme In 2013 all ECB publications

High Frequency Trading and Market Stability* Jonathan Brogaard. Thibaut Moyaert. Ryan Riordan. First Draft: October 2013. Current Draft May 2014

High Frequency Trading and Market Stability* Jonathan Brogaard Thibaut Moyaert Ryan Riordan First Draft: October 2013 Current Draft May 2014 This paper investigates the relationship between high frequency

High Frequency Trading and Market Stability* Jonathan Brogaard Thibaut Moyaert Ryan Riordan First Draft: October 2013 Current Draft May 2014 This paper investigates the relationship between high frequency

A Global Perspective on HFT and Market Making. Hans Pieterse March 2015, Sao Paulo

A Global Perspective on HFT and Market Making Hans Pieterse, Agenda Introduction Optiver Definition HFT Benefits HFT Role and benefits of a Market Maker Case Studies in Brazil: MM options and AMBEV Questions

A Global Perspective on HFT and Market Making Hans Pieterse, Agenda Introduction Optiver Definition HFT Benefits HFT Role and benefits of a Market Maker Case Studies in Brazil: MM options and AMBEV Questions

Towards an Automated Trading Ecosystem

Towards an Automated Trading Ecosystem Charles-Albert LEHALLE May 16, 2014 Outline 1 The need for Automated Trading Suppliers Users More technically... 2 Implied Changes New practices New (infrastructure)

Towards an Automated Trading Ecosystem Charles-Albert LEHALLE May 16, 2014 Outline 1 The need for Automated Trading Suppliers Users More technically... 2 Implied Changes New practices New (infrastructure)

Do High-Frequency Traders Anticipate Buying and Selling Pressure?

Do High-Frequency Traders Anticipate Buying and Selling Pressure? Nicholas H. Hirschey London Business School November 2013 Abstract High-frequency traders (HFTs) account for a substantial fraction of

Do High-Frequency Traders Anticipate Buying and Selling Pressure? Nicholas H. Hirschey London Business School November 2013 Abstract High-frequency traders (HFTs) account for a substantial fraction of

MiFID II Trading Venues And High Frequency Trading

MiFID II Trading Venues And High Frequency Trading MiFID II Trading Venues And High Frequency Trading This is the third part in a series of Legal Longs on the MiFID II Directive [2014/65/EU] and the Markets

MiFID II Trading Venues And High Frequency Trading MiFID II Trading Venues And High Frequency Trading This is the third part in a series of Legal Longs on the MiFID II Directive [2014/65/EU] and the Markets

WORKING WORKING PAPER PAPER

Japan Exchange Group, Inc. Visual Identity Design System Manual Japan Exchange Group, Inc. Japan Exchange Group, Inc. Visual Identity Design System Manual Visual Identity Design System Manual JPX JPX 17

Japan Exchange Group, Inc. Visual Identity Design System Manual Japan Exchange Group, Inc. Japan Exchange Group, Inc. Visual Identity Design System Manual Visual Identity Design System Manual JPX JPX 17

FI report. Investigation into high frequency and algorithmic trading

FI report Investigation into high frequency and algorithmic trading FEBRUARY 2012 February 2012 Ref. 11-10857 Contents FI's conclusions from its investigation into high frequency trading in Sweden 3 Background

FI report Investigation into high frequency and algorithmic trading FEBRUARY 2012 February 2012 Ref. 11-10857 Contents FI's conclusions from its investigation into high frequency trading in Sweden 3 Background

Empower Mobile Algorithmic Trading Services with Cloud Computing

Empower Mobile Algorithmic Trading Services with Cloud Computing Junwei Ma Southwestern University of Finance and Economics Abstract: Mobile devices can offer real time connection to stock exchange market

Empower Mobile Algorithmic Trading Services with Cloud Computing Junwei Ma Southwestern University of Finance and Economics Abstract: Mobile devices can offer real time connection to stock exchange market

Low-Latency Trading and Price Discovery without Trading: Evidence from the Tokyo Stock Exchange Pre-Opening Period

Low-Latency Trading and Price Discovery without Trading: Evidence from the Tokyo Stock Exchange Pre-Opening Period Preliminary and incomplete Mario Bellia, SAFE - Goethe University Loriana Pelizzon, Goethe

Low-Latency Trading and Price Discovery without Trading: Evidence from the Tokyo Stock Exchange Pre-Opening Period Preliminary and incomplete Mario Bellia, SAFE - Goethe University Loriana Pelizzon, Goethe

Corporate Bond Trading by Retail Investors in a Limit Order. Book Exchange

Corporate Bond Trading by Retail Investors in a Limit Order Book Exchange by Menachem (Meni) Abudy 1 and Avi Wohl 2 This version: May 2015 1 Graduate School of Business Administration, Bar-Ilan University,

Corporate Bond Trading by Retail Investors in a Limit Order Book Exchange by Menachem (Meni) Abudy 1 and Avi Wohl 2 This version: May 2015 1 Graduate School of Business Administration, Bar-Ilan University,

Algorithmic and advanced orders in SaxoTrader

Algorithmic and advanced orders in SaxoTrader Summary This document describes the algorithmic and advanced orders types functionality in the new Trade Ticket in SaxoTrader. This functionality allows the

Algorithmic and advanced orders in SaxoTrader Summary This document describes the algorithmic and advanced orders types functionality in the new Trade Ticket in SaxoTrader. This functionality allows the

The Effect of Short-selling Restrictions on Liquidity: Evidence from the London Stock Exchange

The Effect of Short-selling Restrictions on Liquidity: Evidence from the London Stock Exchange Matthew Clifton ab and Mark Snape ac a Capital Markets Cooperative Research Centre 1 b University of Technology,

The Effect of Short-selling Restrictions on Liquidity: Evidence from the London Stock Exchange Matthew Clifton ab and Mark Snape ac a Capital Markets Cooperative Research Centre 1 b University of Technology,

Statement of Kevin Cronin Global Head of Equity Trading, Invesco Ltd. Joint CFTC-SEC Advisory Committee on Emerging Regulatory Issues August 11, 2010

Statement of Kevin Cronin Global Head of Equity Trading, Invesco Ltd. Joint CFTC-SEC Advisory Committee on Emerging Regulatory Issues August 11, 2010 Thank you, Chairman Schapiro, Chairman Gensler and

Statement of Kevin Cronin Global Head of Equity Trading, Invesco Ltd. Joint CFTC-SEC Advisory Committee on Emerging Regulatory Issues August 11, 2010 Thank you, Chairman Schapiro, Chairman Gensler and

Market Microstructure & Trading Universidade Federal de Santa Catarina Syllabus. Email: [email protected], Web: www.sfu.ca/ rgencay

Market Microstructure & Trading Universidade Federal de Santa Catarina Syllabus Dr. Ramo Gençay, Objectives: Email: [email protected], Web: www.sfu.ca/ rgencay This is a course on financial instruments, financial

Market Microstructure & Trading Universidade Federal de Santa Catarina Syllabus Dr. Ramo Gençay, Objectives: Email: [email protected], Web: www.sfu.ca/ rgencay This is a course on financial instruments, financial