a. CME Has Conducted an Initial Review of Detailed Trading Records

|

|

|

- Shanon Harper

- 8 years ago

- Views:

Transcription

1 TESTIMONY OF TERRENCE A. DUFFY EXECUTIVE CHAIRMAN CME GROUP INC. BEFORE THE Subcommittee on Capital Markets, Insurance and Government Sponsored Enterprises of the HOUSE COMMITTEE ON FINANCIAL SERVICES May 11, 2010 I am Terrence A. Duffy, executive chairman of CME Group Inc. Thank you Chairman Kanjorski and Ranking Member Garrett for inviting us to testify today. You asked us to discuss issues surrounding the activity in the equity markets on Thursday, May 6, 2010, including our thoughts on market integrity and how our markets functioned on that date, the effectiveness of the existing market structure rules and the role of technology in our markets. CME Group is the world s largest and most diverse derivatives marketplace. We are the parent of four separate regulated exchanges, including Chicago Mercantile Exchange Inc. ( CME ), the Board of Trade of the City of Chicago, Inc. ( CBOT ), the New York Mercantile Exchange, Inc. ( NYMEX ) and the Commodity Exchange, Inc. ( COMEX ). The CME Group Exchanges offer the widest range of benchmark products available across all major asset classes, including futures and options on futures based on interest rates, equity indexes, foreign exchange, energy, metals, agricultural commodities, and alternative investment products. The CME Group Exchanges serve the hedging, risk management and trading needs of our global customer base by facilitating transactions through the CME Globex electronic trading platform, our open outcry trading facilities in New York and Chicago, as well as through privately negotiated CME ClearPort transactions. The equity index futures contracts traded on CME Group designated contract markets provide an essential risk management function, allowing investors to hedge their exposure against a portfolio of shares or equity options. The most significant equity index futures contract traded on the CME Group Exchanges is the E-mini S&P 500 futures contract. In 2009, average daily volume for the E- mini S&P 500 futures contract was 2,207,596 contracts. I. Introduction Over the past four days, CME Group has engaged in a detailed analysis regarding trading activity in its markets on Thursday, May 6, Our preliminary review indicates that our markets functioned properly. We have identified no trading activity that appeared to be erroneous or contributed to the break in the cash equity market during this period. Moreover, no market participant in our markets reported that trades were executed in error nor did the CME Exchanges cancel ( bust ) or re-price any transactions as a result of the activity on May 6th. 1

2 In the following sections, we discuss: (1) the functioning of our markets on May 6, 2010, (2) the market dynamics in the futures market vis a vis the equity market, and (3) the relevant applicable CME and NYSE circuit breaker rules and (4) CME electronic functionality, particularly CME stop price logic functionality and price banding, among others, which serve to protect our markets. Finally, we have also included preliminary recommendations as to changes that could avoid a recurrence of this type of event in the future. II. The CME Markets Functioned Properly on May 6, 2010 a. CME Has Conducted an Initial Review of Detailed Trading Records CME Group analyzed trading volume and activity throughout May 6 and focused particularly on the activity taking place during the period of 1pm to 2pm Central Time. Total volume in the June E-mini S&P futures on May 6 th was 5.7 million contracts, with approximately 1.6 million or 28% transacted during the period from 1pm to 2pm Central Time. During that hour, the market traded in a range of to 1056, or points - beginning the hour at approximately 1142 and ending the hour at approximately More than 250 firms and 9,000 User IDs were active in the market during this period of time. During most of that hour, the bid/ask spread was a tick wide (.25 points) and the market traded in a largely orderly manner despite the significant sell off and subsequent rally. At approximately 1:45:28, following a sharp point decline over a period of approximately 500 milliseconds on the sale of 1100 contracts by multiple market participants, the bid/ask spread momentarily widened to 6.5 points or 26 ticks. At that point, one of CME Globex s risk management functionalities, a CME Globex Stop Price Logic event, which is discussed in more detail below, was triggered. As a result, the market was automatically paused for five seconds to allow liquidity to come into the market. The market subsequently reopened and was bid, at offered, and thereafter rallied more than 40 points to 1097 in the following three minutes. The Market Regulation Department reviewed a significant amount of activity during this period, a period that included more than 3 million system messages, and, in particular, reviewed the activity of entities whose trading activity during the one-hour period was significant and thus warranted further review. Market Regulation staff ultimately concluded that there were no anomalies represented by the level of activity or the trading strategies employed by market participants. b. CME Markets Provided an Important Price Discovery and Risk Transfer Function on May 6 From a broader perspective, the cumulative record of May 6 trading activity underscores the fact that CME s futures markets, due to their high level of liquidity, provided an important price discovery and risk transfer mechanism for all market participants on that day. 2

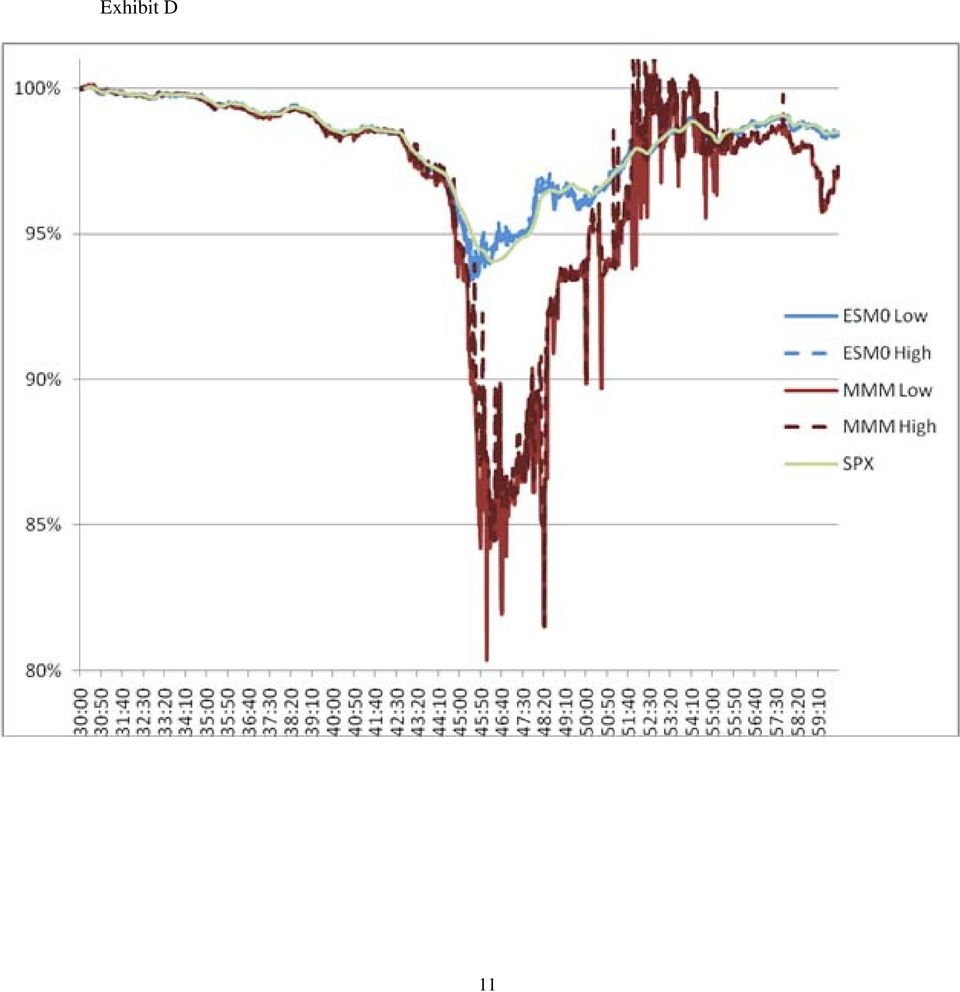

3 The second-by-second trading range, which is an indicator of the liquidity in the market, shows that futures had much tighter bid-ask spreads than the comparable Exchange Traded Fund or ETF. The ETF which is most comparable to the E-mini S&P 500 futures is the SPDR S&P 500 ETF Trust (SPY). This demonstrates that, while all the markets were less liquid than in normal times, the liquidity in the futures market degraded much less than in the ETF markets (which, in turn, degraded much less than the individual stocks, especially stocks that are thinly traded.) There is strong evidence that the futures market (E-mini S&P in particular) was much more liquid than the fragmented underlying stock market on May 6. During the period between 13:40 and 14:00, the volume of E-mini S&P (notionally adjusted) was 3 to 4 times greater than the SPY volume and, at the peak of the market s volatility, was to 8 to 10 times greater. The data does show that the E-mini S&P futures reached its low prior to the stock market reaching its lows. This is consistent with the role of the futures market in anticipating market movements. Futures contracts, by design, provide an indication of the market s view of the value of the underlying stock index. Casual observation may lead to the conclusion that the E- mini S&P futures prices appeared to lead the decline in the cash market. The chart, attached as Exhibit A, illustrates the comparative value of the E-mini, traded on the futures market, as compared to the equities markets. The chart demonstrates that while the E-mini S&P moved virtually in tandem with the comparable cash instrument until the moment when our Stop Price Logic was implemented which caused our matching engine to pause for 5 seconds. At the time the Stop Price Logic was implemented, the E-mini S&P ceased its drop, while the cash market continued its steep decline. The E-mini S&P then rallied significantly for the remainder of the trading session. We believe this recovery was positively influenced by our Stop Price Logic functionality which stabilized market activity. This functionality is not available in the securities market. Consequently, while the broad based index markets SPYs and CME E-mini S&P were substantially recovering, there were continued price declines in individual stocks which persisted for minutes (not seconds). If a seller made a decision to sell a large position, it was rational for that seller to turn to the most liquid market, notably the E-mini S&P futures contract, where there is significant market participant confidence. A review of the composition of the trading volume confirms that this was the case. Consequently, equity index futures perform an important price discovery function in the market. If the futures market had not been available as an alternative, the selling would have manifested itself somewhere else, potentially in a less liquid market, such as the underlying stock market or the OTC derivatives market. The relative tightness of the spread in the futures market underscores the fact that there were buyers in the market as well creating a concentration of liquidity that further supported the important price discovery and risk transfer role of the futures market. (Click to view additional data illustrating CME markets price discovery and risk transfer function, comparing Accenture, Procter & Gamble and 3M Company stock.) III. Circuit Breaker Rules One of the mechanisms that exchanges have implemented to curb market volatility are circuit breaker rules. Circuit breaker rules require an automatic halt in trading when pre-determined price levels are reached. CME Group Exchanges currently have circuit breaker rules in effect for 3

4 equity index products which are consistent with the circuit breaker rules in the underlying equity markets. The following is a brief history and summary of circuit breaker rules as developed by the equities markets and by CME. Circuit breaker rules were originally introduced following the September 1987 market crash. The circuit breakers were implemented uniformly across all equities and options exchanges and were set at a fixed price level tied to the DJIA. If the DJIA declined 250 points (approximately 12% of the Index) from the prior day s close, a trading halt was imposed; if the DJIA declined 400 points, a subsequent two-hour trading halt was triggered. This rule was embodied in NYSE Rule 80B. On October 27, 1997, the circuit breakers were triggered for the first time. A subsequent analysis of those events let to a modification of the circuit breaker rules to employ percentage declines of 10, 20 and 30% in the DJIA in lieu of the fixed point triggers previously used. That rule remains in effect. The CME also adopted price limit rules for its equity index contracts. These price limits were coordinated with the NYSE Rule 80B trading halts when the latter were adopted in The price limit structure and levels have changed several times as the Exchange has gained more experience and as the trading halts in the equity market have been modified. CMEs rules originally included several intermediate price limits -- called "speed bumps" triggered prior to a trading halt, which were in effect for ten-minute intervals. CME also imposed total daily limits on its domestic equity futures contracts, set at approximately a ten percent drop in the respective index. In 1998, when the circuit breaker rules at NYSE and the other equity exchanges were changed to the 10, 20 and 30% level, CME adopted a price limit system of 2.5, 5, 7.5 and 10% limits, with a total daily limit of 20%. Later in 1998, CME adopted a 15% speed bump which triggered a 10 minute reserve period in the market. In 2001, CME amended the price limits to eliminate the 2.5% limit on all domestic stock indexes. The limits were triggered at 5, 10, 15 and 20%. In January 2008, the decision was made to harmonize CMEs limits to be fully consistent with the NYSE Rule 80B (and also consistent with the methodology employed by the CBOT with respect to the DJIA futures). Consequently, the 5%, 7.5%, 10%, 15% and 20% limits were eliminated in favor of the 10%, 20% and 30% employed by the NYSE. CME did, however, retain the references to the specific stock index that is the subject of the futures contract rather than tying these limits to movements in the DJIA, meaning, for example, that the E-mini S&P 500 circuit breakers are tied to price movements in the related index. CME implements an unconditional futures trading halt in the equity index futures when the primary stock market is halted, regardless of whether a particular index product has hit a limit or not. CME also continued enforcement of 5% limit bid or offer policy during overnight electronic trading hours; if equity index futures are locked limited at 8:15 a.m. Central Time ( CT ) and remain so at 8:25 a.m. CT in the lead month futures contract, there will be a trading halt in effect until the commencement of regular trading hours (floor and electronic trading). During the trading halt, the Exchange will provide an Indicative Opening Price of the re-opening of trading on CME Globex, if applicable. If the lead month futures contract is no longer locked limit at 4

5 8:25 a.m. CT, trading will continue with the 5 percent limit in effect. At 8:30 a.m. CT, the 5 percent overnight electronic trading hours limit no longer will be applicable. On May 6 th, the declines in the DJIA were just short of 10% at a time of day when the 20% trigger was in effect. Consequently, the circuit breakers in the primary and the futures markets were not triggered. IV. CME Has Risk Management Controls to Mitigate the Potential for Disruption of its Markets In addition to the circuit breaker rules described above, CME has in place numerous risk management processes, procedures and systems to preserve the integrity of its market in light of the many risks associated with maintaining a primarily electronic market. For example, CME is the only exchange in the world that requires pre-execution credit controls. Appended to the testimony as Exhibit B is a detailed list and description of the multitude of controls that the CME employs on its CME Globex system, including credit controls, messaging volume controls and risk protection policies and procedures. There are certain risk protection tools employed by the CME which are important to note individually and which are relevant to today s discussion. One of these tools, CME Globex Stop Price Logic functionality, was employed on May 6 its operation and effect are also described below. a. Stop Price Logic Functionality The CME Globex system has a Stop Price Logic functionality which serves to mitigate artificial market spikes that can occur because of the continuous triggering, election and trading of stop orders due to insufficient liquidity. If elected stop orders would result in execution prices that exceed pre-defined thresholds, the market automatically enters a brief reserved state for a predetermined time period, generally ranging from 5 10 seconds. During this period, no orders are matched and new orders other than market orders may be entered and orders may be modified and cancelled. The momentary pause that occurs when stop price logic is triggered allows market participants the opportunity to provide liquidity and allows the market to regain equilibrium, thereby mitigating the potential for disruptive market moves. The stop spike price and time parameters in the E-mini S&P futures are 6 index points and 5 seconds, respectively. The Stop Price Logic was triggered on May 6 th in the E-mini S&P 500 equity index. At 1:45:27, one second prior to going into reserve state, the front month E-mini S&P 500 equity index futures contract was trading just under the level. Multiple parties entered the market selling and taking the market down to There was a stop order to sell 150 contracts at which moved the markets to This trade triggered another 150 lot stop at which sold the market down to At this time renewed buying from multiple firms absorbed the volume at which point, the market started to trade off of the lows. 5

6 The front month E-mini S&P 500 equity index futures market went into reserve state as a result of stop price logic functionality being triggered at 13:45:28. The market came out of this reserve state five seconds later. As a result of the stop, the decline in the E-minis halted and the market came out of the reserve state with an initial price of b. Price Banding Functionality To ensure fair, stable and orderly markets, CME Globex subjects all orders to price verification using a process called price banding. The platform utilizes separate mechanisms for futures price banding and options price banding. Price banding prevents the entry of erroneous orders such as a limit bid at a price well above the market or a limit offer at prices well below the market which could trigger a sequence of market-moving trades that require subsequent cancellations. c. Protection Points for Market and Stop orders This CME Globex functionality automatically assigns a limit price (Protection Point) to futures market orders and stop orders to preclude the execution of these types of orders at extreme prices in situations where there is insufficient liquidity to support the execution of the order within an exchange-specified parameter of the current market. The Protection Point values vary by product, and in the E-Mini S&P futures the Protection Point is established at 3 index points. The CME Globex system calculates the limit price for a Market Protected Order by applying the Protection Point value to the best bid or offer price (depending on the order s side of market) and by applying the Protection Point value to the trigger price for a Stop Protected Order. Any unmatched quantity remaining for a Market Protected or Stop Protected Order after it is executed to the Protection Point limit becomes a Limit Order at the limit price. d. Maximum Order Size Protection This CME Globex functionality prohibits entry of an order into the trading engine which exceeds a pre-determined quantity. For E-mini S&P 500 futures, the order size is 2,000 contracts. This functionality provides protection against the so-called fat finger trades. Additional credit controls serve as a check to ensure that a single market participant is not sending in continuous orders at the maximum order size if such trading cannot be supported. V. High Frequency Trading An important issue raised in this discussion is the contribution of high frequency traders ( HFTs ) to the current situation and their future role in the markets. As recently described in the SEC s Concept release on market structure, high frequency trading was identified as one of the most significant market structure developments in recent years. Although HFT is not clearly defined, it typically is used to refer to professional traders acting in a proprietary capacity that engage in strategies that generate a large number of trades on a daily basis. 6

7 CME believes that HFTs play an important role in the markets, particularly when such activities are engaged in with the types of risk management procedures detailed in the previous section. HFTs are an important part of daily trading activity in the marketplace and this has developed in response to technological and trading strategy advances. This represents the natural evolution of technological advancements and improvements in the marketplace and the percentage of trading volume attributable to HFTs will likely continue to increase in the future. There is evidence that HFTs increase liquidity and transparency in the marketplace and narrow spreads which allows investors to buy and sell securities at better prices and at lower costs. It is also important to note that not all HFTs are alike. A significant proportion of HFTs on the CME promote liquidity by providing continuous markets in our products. As illustrated by the events of May 6, in analyzing the role of one HFT, a majority of that entity s trading executed during the relevant one-hour period was related to that firm s market making activities. Thus, before considering restrictions on HFT activity, consideration should be given to the beneficial role played by HFTs in providing liquidity during normal market activity as well as during times of increased market turmoil. The use of high frequency trading by proprietary trading firms, investment banks, hedge funds and index traders, among others, has made the marketplace more efficient and competitive for all market participants. Any attempt to place significant restrictions or limitations on HFTs would be harmful to the marketplace and result in less efficient and less liquid markets. It is also important to note that automated trading or algorithmic trading has its origins in Europe. Accordingly, efforts to place limits or impose regulatory burdens on HFTs in the United States may encourage HFTs to shift the trading they currently conduct in the United States to Europe and other foreign jurisdictions that are already well-equipped to handle additional growth in both equities and futures. CME Globex employs many risk management policies and procedures which assist in the mitigation of risk associated with any type of electronic trading, including that of HFTs. In addition, the CME Group Exchanges are proactive in monitoring the trading activity of HFT entities. All Automated Trading Systems ( ATS ) using CME Globex are required to identify themselves as an ATS and register with the CME Group Exchanges. Subsequent to their registration, the CME Group Exchanges are able to monitor the trading activity of ATSs on both a real time and post-trade basis. CME has required ATS registration for its equity index products since This policy has now been expanded to ATS for all products and we currently have over 10,000 ATS registered. VI. Preliminary Recommendations As noted previously, CME has endeavored to extensively examine the activity in our markets on May 6, Based on our analysis to date, we would make the following preliminary recommendations regarding potential changes to improve the functioning of the markets during times of severe turmoil. Of course, as we continue to study the situation, we would be happy to contribute our further thoughts and recommendations. 7

8 Circuit breakers, including circuit breakers for individual stocks such as that implemented by the NYSE, must be harmonized across markets. The lack of consistency exacerbated the decline in certain individual stocks as the NYSE exercised its Liquidity Replenishment Rule to slow down its markets and orders were then directed to less liquid electronic trading venues. Stop price logic functionality should be adopted across markets, on a product by product basis, to prevent cascading downward market movements. The current circuit breaker levels of 10, 20 and 30 percent, the duration of the halt and the time of day at which such triggers are applicable, should be reevaluated in light of current market conditions to determine whether any changes are warranted. Any such changes must be implemented across all market venues. Exhibit A 8

9 Exhibit B 9

10 Exhibit C 10

11 Exhibit D 11

CME Group Exchanges and Their Functionality

TESTIMONY OF TERRENCE A. DUFFY EXECUTIVE CHAIRMAN CME GROUP INC. BEFORE THE Subcommittee on Capital Markets, Insurance and Government Sponsored Enterprises of the HOUSE COMMITTEE ON FINANCIAL SERVICES

TESTIMONY OF TERRENCE A. DUFFY EXECUTIVE CHAIRMAN CME GROUP INC. BEFORE THE Subcommittee on Capital Markets, Insurance and Government Sponsored Enterprises of the HOUSE COMMITTEE ON FINANCIAL SERVICES

STATEMENT OF GARY GENSLER CHAIRMAN, COMMODITY FUTURES TRADING COMMISSION BEFORE THE HOUSE OF REPRESENTATIVES COMMITTEE ON FINANCIAL SERVICES

STATEMENT OF GARY GENSLER CHAIRMAN, COMMODITY FUTURES TRADING COMMISSION BEFORE THE HOUSE OF REPRESENTATIVES COMMITTEE ON FINANCIAL SERVICES SUBCOMMITTEE ON CAPITAL MARKETS, INSURANCE, AND GOVERNMENT SPONSORED

STATEMENT OF GARY GENSLER CHAIRMAN, COMMODITY FUTURES TRADING COMMISSION BEFORE THE HOUSE OF REPRESENTATIVES COMMITTEE ON FINANCIAL SERVICES SUBCOMMITTEE ON CAPITAL MARKETS, INSURANCE, AND GOVERNMENT SPONSORED

STATEMENT OF GARY GENSLER CHAIRMAN, COMMODITY FUTURES TRADING COMMISSION BEFORE THE. May 20, 2010

STATEMENT OF GARY GENSLER CHAIRMAN, COMMODITY FUTURES TRADING COMMISSION BEFORE THE SENATE COMMITTEE ON BANKING, HOUSING, AND URBAN AFFAIRS SUBCOMMITTEE ON SECURITIES, INSURANCE, AND INVESTMENT May 20,

STATEMENT OF GARY GENSLER CHAIRMAN, COMMODITY FUTURES TRADING COMMISSION BEFORE THE SENATE COMMITTEE ON BANKING, HOUSING, AND URBAN AFFAIRS SUBCOMMITTEE ON SECURITIES, INSURANCE, AND INVESTMENT May 20,

Commodity Futures Trading Commission

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 (202) 418-5080 www.cftc.gov Testimony Testimony of Chairman Gary Gensler,

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 (202) 418-5080 www.cftc.gov Testimony Testimony of Chairman Gary Gensler,

Statement of Kevin Cronin Global Head of Equity Trading, Invesco Ltd. Joint CFTC-SEC Advisory Committee on Emerging Regulatory Issues August 11, 2010

Statement of Kevin Cronin Global Head of Equity Trading, Invesco Ltd. Joint CFTC-SEC Advisory Committee on Emerging Regulatory Issues August 11, 2010 Thank you, Chairman Schapiro, Chairman Gensler and

Statement of Kevin Cronin Global Head of Equity Trading, Invesco Ltd. Joint CFTC-SEC Advisory Committee on Emerging Regulatory Issues August 11, 2010 Thank you, Chairman Schapiro, Chairman Gensler and

Circuit Breakers: International Practices and Effectiveness

22 Articles and Speeches Circuit Breakers: International Practices and Effectiveness by Supervision of Markets Division of the Securities and Futures Commission Overview "Circuit breakers" and "price limits"

22 Articles and Speeches Circuit Breakers: International Practices and Effectiveness by Supervision of Markets Division of the Securities and Futures Commission Overview "Circuit breakers" and "price limits"

Flash Crash Retrospective: Limit Up-Limit Down is the Best Response

Flash Crash Retrospective: Limit Up-Limit Down is the Best Response Key Takeaways On May 6, 2010, while equities endured an historic crash, the CME s Stop Logic functionality curbed the downward movement

Flash Crash Retrospective: Limit Up-Limit Down is the Best Response Key Takeaways On May 6, 2010, while equities endured an historic crash, the CME s Stop Logic functionality curbed the downward movement

Financial Markets and Institutions Abridged 10 th Edition

Financial Markets and Institutions Abridged 10 th Edition by Jeff Madura 1 12 Market Microstructure and Strategies Chapter Objectives describe the common types of stock transactions explain how stock transactions

Financial Markets and Institutions Abridged 10 th Edition by Jeff Madura 1 12 Market Microstructure and Strategies Chapter Objectives describe the common types of stock transactions explain how stock transactions

Noble DraKoln. metals products Gold Futures vs. Gold ETFs: Understanding the Differences and Opportunities.

metals products Gold Futures vs. Gold ETFs: Understanding the Differences and Opportunities. Noble DraKoln Founder of Speculator Academy and author of Winning the Trading Game and Trade Like a Pro cmegroup.com/metals

metals products Gold Futures vs. Gold ETFs: Understanding the Differences and Opportunities. Noble DraKoln Founder of Speculator Academy and author of Winning the Trading Game and Trade Like a Pro cmegroup.com/metals

ELECTRONIC TRADING GLOSSARY

ELECTRONIC TRADING GLOSSARY Algorithms: A series of specific steps used to complete a task. Many firms use them to execute trades with computers. Algorithmic Trading: The practice of using computer software

ELECTRONIC TRADING GLOSSARY Algorithms: A series of specific steps used to complete a task. Many firms use them to execute trades with computers. Algorithmic Trading: The practice of using computer software

Managed Funds Association February 10, 2014

MFA Presentation before the CFTC Technology Advisory Committee Meeting On Risk Controls and System Safeguards for Automated Trading Environments Stuart J. Kaswell Executive Vice President and Managing

MFA Presentation before the CFTC Technology Advisory Committee Meeting On Risk Controls and System Safeguards for Automated Trading Environments Stuart J. Kaswell Executive Vice President and Managing

Note on New Products in F&O Segment. 2. Options Contracts with Longer Life/Tenure. 6. Exchange-traded Currency (Foreign Exchange) F&O Contracts

F&O Contracts") Note on New Products in F&O Segment Contents 1. Mini Contracts in Equity Indices 2. Options Contracts with Longer Life/Tenure 3. Volatility Index and F&O Contracts 4. Options on Futures 5. Bond Index and

Note on New Products in F&O Segment Contents 1. Mini Contracts in Equity Indices 2. Options Contracts with Longer Life/Tenure 3. Volatility Index and F&O Contracts 4. Options on Futures 5. Bond Index and

FIA PTG Whiteboard: Frequent Batch Auctions

FIA PTG Whiteboard: Frequent Batch Auctions The FIA Principal Traders Group (FIA PTG) Whiteboard is a space to consider complex questions facing our industry. As an advocate for data-driven decision-making,

FIA PTG Whiteboard: Frequent Batch Auctions The FIA Principal Traders Group (FIA PTG) Whiteboard is a space to consider complex questions facing our industry. As an advocate for data-driven decision-making,

RE: File No. S7-08-09; Proposed Amendments to Regulation SHO

Elizabeth M. Murphy, Secretary Securities and Exchange Commission 100 F Street NE Washington, DC 205491090 RE: File No. S7-08-09; Proposed Amendments to Regulation SHO Dear Ms. Murphy: Lime Brokerage LLC

Elizabeth M. Murphy, Secretary Securities and Exchange Commission 100 F Street NE Washington, DC 205491090 RE: File No. S7-08-09; Proposed Amendments to Regulation SHO Dear Ms. Murphy: Lime Brokerage LLC

From Traditional Floor Trading to Electronic High Frequency Trading (HFT) Market Implications and Regulatory Aspects Prof. Dr. Hans Peter Burghof

Market Implications and Regulatory Aspects Prof. Dr. Hans Peter Burghof") From Traditional Floor Trading to Electronic High Frequency Trading (HFT) Market Implications and Regulatory Aspects Prof. Dr. Hans Peter Burghof Universität Hohenheim Institut für Financial Management

From Traditional Floor Trading to Electronic High Frequency Trading (HFT) Market Implications and Regulatory Aspects Prof. Dr. Hans Peter Burghof Universität Hohenheim Institut für Financial Management

Trade, Hedge & be ahead of the Precious Metals Markets with Gold & Silver Futures. Why it makes sense?

GOLD & PRECIOUS METALS PRICE OUTLOOK SYMPOSIUM 2015 Trade, Hedge & be ahead of the Precious Metals Markets with Gold & Silver Futures. Why it makes sense? HARRIET HUNNABLE JUNE 2015 CME Group exchanges

GOLD & PRECIOUS METALS PRICE OUTLOOK SYMPOSIUM 2015 Trade, Hedge & be ahead of the Precious Metals Markets with Gold & Silver Futures. Why it makes sense? HARRIET HUNNABLE JUNE 2015 CME Group exchanges

Understanding the Flash Crash What Happened, Why ETFs Were Affected, and How to Reduce the Risk of Another

ViewPoint November 2010 Understanding the Flash Crash What Happened, Why ETFs Were Affected, and How to Reduce the Risk of Another Introduction There is a saying in the markets that liquidity is like oxygen:

ViewPoint November 2010 Understanding the Flash Crash What Happened, Why ETFs Were Affected, and How to Reduce the Risk of Another Introduction There is a saying in the markets that liquidity is like oxygen:

High Frequency Trading + Stochastic Latency and Regulation 2.0. Andrei Kirilenko MIT Sloan

High Frequency Trading + Stochastic Latency and Regulation 2.0 Andrei Kirilenko MIT Sloan High Frequency Trading: Good or Evil? Good Bryan Durkin, Chief Operating Officer, CME Group: "There is considerable

High Frequency Trading + Stochastic Latency and Regulation 2.0 Andrei Kirilenko MIT Sloan High Frequency Trading: Good or Evil? Good Bryan Durkin, Chief Operating Officer, CME Group: "There is considerable

CME Commodity Products. Trading Options on CME Random Length Lumber Futures

CME Commodity Products Trading Options on CME Random Length Lumber Futures Global Leadership in the Financial Marketplace CME is the largest and most diverse financial exchange in the world for trading

CME Commodity Products Trading Options on CME Random Length Lumber Futures Global Leadership in the Financial Marketplace CME is the largest and most diverse financial exchange in the world for trading

Energy Products. The energy Marketplace.

Energy Products The energy Marketplace. In a world of increasing volatility, customers around the globe rely on CME Group as their premier source for managing risk across all major asset classes offering

Energy Products The energy Marketplace. In a world of increasing volatility, customers around the globe rely on CME Group as their premier source for managing risk across all major asset classes offering

G100 VIEWS HIGH FREQUENCY TRADING. Group of 100

G100 VIEWS ON HIGH FREQUENCY TRADING DECEMBER 2012 -1- Over the last few years there has been a marked increase in media and regulatory scrutiny of high frequency trading ("HFT") in Australia. HFT, a subset

G100 VIEWS ON HIGH FREQUENCY TRADING DECEMBER 2012 -1- Over the last few years there has been a marked increase in media and regulatory scrutiny of high frequency trading ("HFT") in Australia. HFT, a subset

DEFINITIONS. ACT OR CEA The term "Act" or CEA shall mean the Commodity Exchange Act, as amended from time to time.

DEFINITIONS ACT OR CEA The term "Act" or CEA shall mean the Commodity Exchange Act, as amended from time to time. BLOCK TRADE A privately negotiated futures, option on futures or swaps transaction that

DEFINITIONS ACT OR CEA The term "Act" or CEA shall mean the Commodity Exchange Act, as amended from time to time. BLOCK TRADE A privately negotiated futures, option on futures or swaps transaction that

FINDINGS REGARDING THE MARKET EVENTS OF MAY 6, 2010

FINDINGS REGARDING THE MARKET EVENTS OF MAY 6, 21 REPORT OF THE STAFFS OF THE CFTC AND SEC TO THE JOINT ADVISORY COMMITTEE ON EMERGING REGULATORY ISSUES U.S. Commodity Futures Trading Commission Three

FINDINGS REGARDING THE MARKET EVENTS OF MAY 6, 21 REPORT OF THE STAFFS OF THE CFTC AND SEC TO THE JOINT ADVISORY COMMITTEE ON EMERGING REGULATORY ISSUES U.S. Commodity Futures Trading Commission Three

This paper sets out the challenges faced to maintain efficient markets, and the actions that the WFE and its member exchanges support.

Understanding High Frequency Trading (HFT) Executive Summary This paper is designed to cover the definitions of HFT set by regulators, the impact HFT has made on markets, the actions taken by exchange

Understanding High Frequency Trading (HFT) Executive Summary This paper is designed to cover the definitions of HFT set by regulators, the impact HFT has made on markets, the actions taken by exchange

CFTC Reauthorization

Order Code RS22028 Updated June 9, 2008 CFTC Reauthorization Mark Jickling Specialist in Financial Economics Government and Finance Division Summary Authorization for the Commodity Futures Trading Commission

Order Code RS22028 Updated June 9, 2008 CFTC Reauthorization Mark Jickling Specialist in Financial Economics Government and Finance Division Summary Authorization for the Commodity Futures Trading Commission

Guidance Respecting the Implementation of Single-Stock Circuit Breakers

Rules Notice Guidance Note UMIR Please distribute internally to: Institutional Legal and Compliance Retail Senior Management Trading Desk Contact: James E. Twiss Vice President, Market Regulation Policy

Rules Notice Guidance Note UMIR Please distribute internally to: Institutional Legal and Compliance Retail Senior Management Trading Desk Contact: James E. Twiss Vice President, Market Regulation Policy

Nine Questions Every ETF Investor Should Ask Before Investing

Nine Questions Every ETF Investor Should Ask Before Investing UnderstandETFs.org Copyright 2012 by the Investment Company Institute. All rights reserved. ICI permits use of this publication in any way,

Nine Questions Every ETF Investor Should Ask Before Investing UnderstandETFs.org Copyright 2012 by the Investment Company Institute. All rights reserved. ICI permits use of this publication in any way,

BEAR: A person who believes that the price of a particular security or the market as a whole will go lower.

Trading Terms ARBITRAGE: The simultaneous purchase and sale of identical or equivalent financial instruments in order to benefit from a discrepancy in their price relationship. More generally, it refers

Trading Terms ARBITRAGE: The simultaneous purchase and sale of identical or equivalent financial instruments in order to benefit from a discrepancy in their price relationship. More generally, it refers

9 Questions Every ETF Investor Should Ask Before Investing

9 Questions Every ETF Investor Should Ask Before Investing 1. What is an ETF? 2. What kinds of ETFs are available? 3. How do ETFs differ from other investment products like mutual funds, closed-end funds,

9 Questions Every ETF Investor Should Ask Before Investing 1. What is an ETF? 2. What kinds of ETFs are available? 3. How do ETFs differ from other investment products like mutual funds, closed-end funds,

Comparing E-minis and ETFs

STOCK INDEXES Comparing E-minis and ETFs SEPTEMBER 15, 2012 John W. Labuszewski Managing Director Research & Product Development 312-466-7469 jlab@cmegroup.com CME Group E-mini stock index futures and

STOCK INDEXES Comparing E-minis and ETFs SEPTEMBER 15, 2012 John W. Labuszewski Managing Director Research & Product Development 312-466-7469 jlab@cmegroup.com CME Group E-mini stock index futures and

General Risk Disclosure

General Risk Disclosure Colmex Pro Ltd (hereinafter called the Company ) is an Investment Firm regulated by the Cyprus Securities and Exchange Commission (license number 123/10). This notice is provided

General Risk Disclosure Colmex Pro Ltd (hereinafter called the Company ) is an Investment Firm regulated by the Cyprus Securities and Exchange Commission (license number 123/10). This notice is provided

CME Group 2012 Commodities Trading Challenge. Competition Rules and Procedures

Competition Rules and Procedures CME Group with assistance from CQG and the University of Houston, is sponsoring a commodities trading competition among colleges and universities. Students will compete

Competition Rules and Procedures CME Group with assistance from CQG and the University of Houston, is sponsoring a commodities trading competition among colleges and universities. Students will compete

FI report. Investigation into high frequency and algorithmic trading

FI report Investigation into high frequency and algorithmic trading FEBRUARY 2012 February 2012 Ref. 11-10857 Contents FI's conclusions from its investigation into high frequency trading in Sweden 3 Background

FI report Investigation into high frequency and algorithmic trading FEBRUARY 2012 February 2012 Ref. 11-10857 Contents FI's conclusions from its investigation into high frequency trading in Sweden 3 Background

White Paper Electronic Trading- Algorithmic & High Frequency Trading. PENINSULA STRATEGY, Namir Hamid

White Paper Electronic Trading- Algorithmic & High Frequency Trading PENINSULA STRATEGY, Namir Hamid AUG 2011 Table Of Contents EXECUTIVE SUMMARY...3 Overview... 3 Background... 3 HIGH FREQUENCY ALGORITHMIC

White Paper Electronic Trading- Algorithmic & High Frequency Trading PENINSULA STRATEGY, Namir Hamid AUG 2011 Table Of Contents EXECUTIVE SUMMARY...3 Overview... 3 Background... 3 HIGH FREQUENCY ALGORITHMIC

ForRelease: February i, 1988 (202) 254-8630

254-8630") , NEWS RELEASE Release: 2864-88 ForRelease: February i, 1988 Contact: Kate Hathaway (202) 254-8630 Washingtom--The Commodity Futures Trading Commission released today the final staff report on stock index

, NEWS RELEASE Release: 2864-88 ForRelease: February i, 1988 Contact: Kate Hathaway (202) 254-8630 Washingtom--The Commodity Futures Trading Commission released today the final staff report on stock index

Three Lafayette Centre 1155 21 st Street, NW Washington, DC 20581. 100 F Street, NE Washington, DC 20549. September 21, 2009

U.S. Commodity Futures Trading Commission The Honorable Gary Gensler Chairman Three Lafayette Centre 1155 21 st Street, NW Washington, DC 20581 U.S. Securities and Exchange Commission The Honorable Mary

U.S. Commodity Futures Trading Commission The Honorable Gary Gensler Chairman Three Lafayette Centre 1155 21 st Street, NW Washington, DC 20581 U.S. Securities and Exchange Commission The Honorable Mary

CHAPTER 8 CLEARING HOUSE AND PERFORMANCE BONDS GENERAL

800. CLEARING HOUSE 801. MANAGEMENT CHAPTER 8 CLEARING HOUSE AND PERFORMANCE BONDS GENERAL 802. PROTECTION OF CLEARING HOUSE 802.A. Default by Clearing Member or Other Participating Exchanges 802.B. Satisfaction

800. CLEARING HOUSE 801. MANAGEMENT CHAPTER 8 CLEARING HOUSE AND PERFORMANCE BONDS GENERAL 802. PROTECTION OF CLEARING HOUSE 802.A. Default by Clearing Member or Other Participating Exchanges 802.B. Satisfaction

Senate Economics Legislation Committee ANSWERS TO QUESTIONS ON NOTICE

Department/Agency: ASIC Question: BET 93-97 Topic: ASIC Complaints Reference: written - 03 June 2015 Senator: Lambie, Jacqui Question: 93. Given your extensive experience can you please detail what role

Department/Agency: ASIC Question: BET 93-97 Topic: ASIC Complaints Reference: written - 03 June 2015 Senator: Lambie, Jacqui Question: 93. Given your extensive experience can you please detail what role

High frequency trading

High frequency trading Bruno Biais (Toulouse School of Economics) Presentation prepared for the European Institute of Financial Regulation Paris, Sept 2011 Outline 1) Description 2) Motivation for HFT

High frequency trading Bruno Biais (Toulouse School of Economics) Presentation prepared for the European Institute of Financial Regulation Paris, Sept 2011 Outline 1) Description 2) Motivation for HFT

Carbon Market Development and Oversight. June 26, 2009 De Ana Dow, Managing Director, CME Group

Carbon Market Development and Oversight June 26, 2009 De Ana Dow, Managing Director, CME Group Contents I. CME Group and the Green Exchange Initiative II. Fundamentals of a Successful Carbon Market III.

Carbon Market Development and Oversight June 26, 2009 De Ana Dow, Managing Director, CME Group Contents I. CME Group and the Green Exchange Initiative II. Fundamentals of a Successful Carbon Market III.

9 Questions Every Australian Investor Should Ask Before Investing in an Exchange Traded Fund (ETF)

") SPDR ETFs 9 Questions Every Australian Investor Should Ask Before Investing in an Exchange Traded Fund (ETF) 1. What is an ETF? 2. What kinds of ETFs are available? 3. How do ETFs differ from other investment

SPDR ETFs 9 Questions Every Australian Investor Should Ask Before Investing in an Exchange Traded Fund (ETF) 1. What is an ETF? 2. What kinds of ETFs are available? 3. How do ETFs differ from other investment

COMEX ON CME GLOBEX GOLD SILVER COPPER ALUMINUM PLATINUM PALLADIUM ZINC

COMEX ON CME GLOBEX GOLD SILVER COPPER ALUMINUM PLATINUM PALLADIUM ZINC COMEX ON CME GLOBEX A major expansion of the precious and base metals futures markets on the New York Mercantile Exchange, Inc. makes

COMEX ON CME GLOBEX GOLD SILVER COPPER ALUMINUM PLATINUM PALLADIUM ZINC COMEX ON CME GLOBEX A major expansion of the precious and base metals futures markets on the New York Mercantile Exchange, Inc. makes

High Frequency Trading Volumes Continue to Increase Throughout the World

High Frequency Trading Volumes Continue to Increase Throughout the World High Frequency Trading (HFT) can be defined as any automated trading strategy where investment decisions are driven by quantitative

High Frequency Trading Volumes Continue to Increase Throughout the World High Frequency Trading (HFT) can be defined as any automated trading strategy where investment decisions are driven by quantitative

An Introduction to. CME Foreign Exchange Products

An Introduction to CME Foreign Exchange Products What Are Futures and Options? Futures contracts are standardized, legally binding agreements to buy or sell a specific product or financial instrument in

An Introduction to CME Foreign Exchange Products What Are Futures and Options? Futures contracts are standardized, legally binding agreements to buy or sell a specific product or financial instrument in

Using Currency Futures to Hedge Currency Risk

Using Currency Futures to Hedge Currency Risk By Sayee Srinivasan & Steven Youngren Product Research & Development Chicago Mercantile Exchange Inc. Introduction Investment professionals face a tough climate.

Using Currency Futures to Hedge Currency Risk By Sayee Srinivasan & Steven Youngren Product Research & Development Chicago Mercantile Exchange Inc. Introduction Investment professionals face a tough climate.

TRADING RULES ONLINE INDEX Asian Index (Non Gulir), CFD US Index (Non Gulir) Effective August 10, 2015

, CFD US Index (Non Gulir) Effective August 10, 2015") TRADING RULES ONLINE INDEX Asian Index (Non Gulir), CFD US Index (Non Gulir) Effective August 10, 2015 PRODUCTS Symbol Contract Size Asian Index Nikkei (NIK-Contract Month) USD 5.00 per index point Kontrak

TRADING RULES ONLINE INDEX Asian Index (Non Gulir), CFD US Index (Non Gulir) Effective August 10, 2015 PRODUCTS Symbol Contract Size Asian Index Nikkei (NIK-Contract Month) USD 5.00 per index point Kontrak

Comparing E-minis and ETFs

RESEARCH AND product DEVELOPMENT Comparing E-minis and ETFs John W. Labuszewski, Research and Product Development Brett Vietmeier, Equity Products April 2009 13,000 cmegroup.com 12,000 1 10,000 9,000 8,000

RESEARCH AND product DEVELOPMENT Comparing E-minis and ETFs John W. Labuszewski, Research and Product Development Brett Vietmeier, Equity Products April 2009 13,000 cmegroup.com 12,000 1 10,000 9,000 8,000

An objective look at high-frequency trading and dark pools May 6, 2015

www.pwc.com/us/investorresourceinstitute An objective look at high-frequency trading and dark pools May 6, 2015 An objective look at high-frequency trading and dark pools High-frequency trading has been

www.pwc.com/us/investorresourceinstitute An objective look at high-frequency trading and dark pools May 6, 2015 An objective look at high-frequency trading and dark pools High-frequency trading has been

ICE Futures uses the ICE trading platform which offers a variety of risk mitigation tools:

Profile of Exchange and FCM Risk Management Practices For Direct Access Customers As of December 3, 2007 Background The term direct market access is frequently used to describe a customer accessing a market

Profile of Exchange and FCM Risk Management Practices For Direct Access Customers As of December 3, 2007 Background The term direct market access is frequently used to describe a customer accessing a market

September 24, 2012. The Securities and Futures Commission 8/F Chater House 8 Connaught Road Central Hong Kong

The Securities and Futures Commission 8/F Chater House 8 Connaught Road Central Hong Kong Dear Sir or Madam: Re: Consultation Paper on the Regulation of Electronic Trading The Investment Company Institute

The Securities and Futures Commission 8/F Chater House 8 Connaught Road Central Hong Kong Dear Sir or Madam: Re: Consultation Paper on the Regulation of Electronic Trading The Investment Company Institute

FINANCIER. An apparent paradox may have emerged in market making: bid-ask spreads. Equity market microstructure and the challenges of regulating HFT

REPRINT FINANCIER WORLDWIDE JANUARY 2015 FINANCIER BANKING & FINANCE Equity market microstructure and the challenges of regulating HFT PAUL HINTON AND MICHAEL I. CRAGG THE BRATTLE GROUP An apparent paradox

REPRINT FINANCIER WORLDWIDE JANUARY 2015 FINANCIER BANKING & FINANCE Equity market microstructure and the challenges of regulating HFT PAUL HINTON AND MICHAEL I. CRAGG THE BRATTLE GROUP An apparent paradox

AUTOMATED TRADING RULES

AUTOMATED TRADING RULES FEBRUARY 2012 CONTENTS INTRODUCTION 3 ENTERING ORDERS 3 DIVISION OF MARKET 4 TRADING SESSIONS 4 1. TYPES OF TRANSACTIONS 5 1.1 Limit Orders 1.2 Market Orders 1.2.1 Touchline 1.2.2

AUTOMATED TRADING RULES FEBRUARY 2012 CONTENTS INTRODUCTION 3 ENTERING ORDERS 3 DIVISION OF MARKET 4 TRADING SESSIONS 4 1. TYPES OF TRANSACTIONS 5 1.1 Limit Orders 1.2 Market Orders 1.2.1 Touchline 1.2.2

FTS Real Time System Project: Stock Index Futures

FTS Real Time System Project: Stock Index Futures Question: How are stock index futures traded? In a recent Barron s article (September 20, 2010) titled Futures Are the New Options it was noted that there

FTS Real Time System Project: Stock Index Futures Question: How are stock index futures traded? In a recent Barron s article (September 20, 2010) titled Futures Are the New Options it was noted that there

How To Understand The Stock Market

We b E x t e n s i o n 1 C A Closer Look at the Stock Markets This Web Extension provides additional discussion of stock markets and trading, beginning with stock indexes. Stock Indexes Stock indexes try

We b E x t e n s i o n 1 C A Closer Look at the Stock Markets This Web Extension provides additional discussion of stock markets and trading, beginning with stock indexes. Stock Indexes Stock indexes try

Legislative Council Panel on Financial Affairs. Proposal of the Hong Kong Exchanges and Clearing Limited to introduce after-hours futures trading

Legislative Council Panel on Financial Affairs CB(1)2286/11-12(01) Proposal of the Hong Kong Exchanges and Clearing Limited to introduce after-hours futures trading Purpose This paper briefs Members on

Legislative Council Panel on Financial Affairs CB(1)2286/11-12(01) Proposal of the Hong Kong Exchanges and Clearing Limited to introduce after-hours futures trading Purpose This paper briefs Members on

The original purpose of futures contracts was to provide a facility for people to hedge their price risk.

Futures Bas sicss Propex Derivatives Pty Ltd 2012 The information in this document and related documents and communication is intended for educational purposes only and does not constitute advice. Redistribution

Futures Bas sicss Propex Derivatives Pty Ltd 2012 The information in this document and related documents and communication is intended for educational purposes only and does not constitute advice. Redistribution

Comments from NASDAQ OMX

October 2011 ESMA Consultation paper on Guidelines on systems and controls in a highly automated trading environment for trading platforms, investment firms and competent authorities Comments from NASDAQ

October 2011 ESMA Consultation paper on Guidelines on systems and controls in a highly automated trading environment for trading platforms, investment firms and competent authorities Comments from NASDAQ

SAXO BANK S BEST EXECUTION POLICY

SAXO BANK S BEST EXECUTION POLICY THE SPECIALIST IN TRADING AND INVESTMENT Page 1 of 8 Page 1 of 8 1 INTRODUCTION 1.1 This policy is issued pursuant to, and in compliance with, EU Directive 2004/39/EC

SAXO BANK S BEST EXECUTION POLICY THE SPECIALIST IN TRADING AND INVESTMENT Page 1 of 8 Page 1 of 8 1 INTRODUCTION 1.1 This policy is issued pursuant to, and in compliance with, EU Directive 2004/39/EC

Client Update CFTC Proposes Rules Regulating Automated Trading

1 Client Update CFTC Proposes Rules Regulating Automated Trading NEW YORK Byungkwon Lim blim@debevoise.com Aaron J. Levy ajlevy@debevoise.com On November 24, 2015, the Commodity Futures Trading Commission

1 Client Update CFTC Proposes Rules Regulating Automated Trading NEW YORK Byungkwon Lim blim@debevoise.com Aaron J. Levy ajlevy@debevoise.com On November 24, 2015, the Commodity Futures Trading Commission

1. Section 747 of the Dodd-Frank Wall Street Reform and Consumer Protection Act of

Case: 1:15-cv-09196 Document#: 1 Filed: 10/19/15 Page 1 of 36 PageiD #:1 UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF ILLINOIS, EASTERN DIVISION U.S. COMMODITY FUTURES TRADING COMMISSION,

Case: 1:15-cv-09196 Document#: 1 Filed: 10/19/15 Page 1 of 36 PageiD #:1 UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF ILLINOIS, EASTERN DIVISION U.S. COMMODITY FUTURES TRADING COMMISSION,

Risk Explanation for Exchange-Traded Derivatives

Risk Explanation for Exchange-Traded Derivatives The below risk explanation is provided pursuant to Hong Kong regulatory requirements relating to trading in exchange-traded derivatives by those of our

Risk Explanation for Exchange-Traded Derivatives The below risk explanation is provided pursuant to Hong Kong regulatory requirements relating to trading in exchange-traded derivatives by those of our

An Introduction to Nadex

An Introduction to Nadex AN INTODUCTION TO NADEX MULTIPLY YOUR TRADING OPPORTUNITIES, LIMIT YOUR RISK Discover a product set that: Allows you to trade in very small size (risking no more than a few dollars)

An Introduction to Nadex AN INTODUCTION TO NADEX MULTIPLY YOUR TRADING OPPORTUNITIES, LIMIT YOUR RISK Discover a product set that: Allows you to trade in very small size (risking no more than a few dollars)

Stock Trading Systems: A Comparison of US and China. April 30, 2016 Session 5 Joel Hasbrouck www.stern.nyu.edu/~jhasbrou

Stock Trading Systems: A Comparison of US and China April 30, 2016 Session 5 Joel Hasbrouck www.stern.nyu.edu/~jhasbrou 1 1. Regulatory priorities for capital formation and growth. 2 The information environment

Stock Trading Systems: A Comparison of US and China April 30, 2016 Session 5 Joel Hasbrouck www.stern.nyu.edu/~jhasbrou 1 1. Regulatory priorities for capital formation and growth. 2 The information environment

Options on. Dow Jones Industrial Average SM. the. DJX and DIA. Act on the Market You Know Best.

Options on the Dow Jones Industrial Average SM DJX and DIA Act on the Market You Know Best. A glossary of options definitions appears on page 21. The Chicago Board Options Exchange (CBOE) was founded in

Options on the Dow Jones Industrial Average SM DJX and DIA Act on the Market You Know Best. A glossary of options definitions appears on page 21. The Chicago Board Options Exchange (CBOE) was founded in

The Flash Crash: The Impact of High Frequency Trading on an Electronic Market

The Flash Crash: The Impact of High Frequency Trading on an Electronic Market Andrei Kirilenko MIT Sloan School of Management Albert S. Kyle University of Maryland Mehrdad Samadi University of North Carolina

The Flash Crash: The Impact of High Frequency Trading on an Electronic Market Andrei Kirilenko MIT Sloan School of Management Albert S. Kyle University of Maryland Mehrdad Samadi University of North Carolina

Exchange-Traded Funds

Exchange-Traded Funds Exchange Traded Funds (ETF s) are becoming popular investment vehicles for many investors. Most ETF s are cost effective, broad market funds. We have put together a layman s explanation

Exchange-Traded Funds Exchange Traded Funds (ETF s) are becoming popular investment vehicles for many investors. Most ETF s are cost effective, broad market funds. We have put together a layman s explanation

Stock Index Futures Spread Trading

S&P 500 vs. DJIA Stock Index Futures Spread Trading S&P MidCap 400 vs. S&P SmallCap 600 Second Quarter 2008 2 Contents Introduction S&P 500 vs. DJIA Introduction Index Methodology, Calculations and Weightings

S&P 500 vs. DJIA Stock Index Futures Spread Trading S&P MidCap 400 vs. S&P SmallCap 600 Second Quarter 2008 2 Contents Introduction S&P 500 vs. DJIA Introduction Index Methodology, Calculations and Weightings

CURRENCY FUTURES IN INDIA WITH SPECIAL REFERENCE TO CURRENCY FUTURES TRADED AT NSE

CURRENCY FUTURES IN INDIA WITH SPECIAL REFERENCE TO CURRENCY FUTURES TRADED AT NSE Vinayak R. Gramopadhye Assistant professor, ASM s Institute of International Business and Research, Pimpri, Pune-18 Abstract

CURRENCY FUTURES IN INDIA WITH SPECIAL REFERENCE TO CURRENCY FUTURES TRADED AT NSE Vinayak R. Gramopadhye Assistant professor, ASM s Institute of International Business and Research, Pimpri, Pune-18 Abstract

FINAL NOTICE. Michael Coscia. Date of Birth: 7 July 1962. Date: 3 July 2013 ACTION

FINAL NOTICE To: Michael Coscia Date of Birth: 7 July 1962 Date: 3 July 2013 ACTION 1. For the reasons given in this notice, the FCA hereby imposes on Michael Coscia a financial penalty of USD 903,176

FINAL NOTICE To: Michael Coscia Date of Birth: 7 July 1962 Date: 3 July 2013 ACTION 1. For the reasons given in this notice, the FCA hereby imposes on Michael Coscia a financial penalty of USD 903,176

Introduction to Metals Futures. Presented by Pete Mulmat and Dan Gramza September 25th, 2014

Introduction to Metals Futures Presented by Pete Mulmat and Dan Gramza September 25th, 2014 Disclaimer Futures trading is not suitable for all investors, and involves the risk of loss. Futures are a leveraged

Introduction to Metals Futures Presented by Pete Mulmat and Dan Gramza September 25th, 2014 Disclaimer Futures trading is not suitable for all investors, and involves the risk of loss. Futures are a leveraged

Do retail traders suffer from high frequency traders?

Do retail traders suffer from high frequency traders? Katya Malinova, Andreas Park, Ryan Riordan November 15, 2013 Millions in Milliseconds Monday, June 03, 2013: a minor clock synchronization issue causes

Do retail traders suffer from high frequency traders? Katya Malinova, Andreas Park, Ryan Riordan November 15, 2013 Millions in Milliseconds Monday, June 03, 2013: a minor clock synchronization issue causes

TRADING FUTURES ON THE SAXOTRADER PLATFORM

TRADING FUTURES ON THE SAXOTRADER PLATFORM Saxo Capital Markets Tel: +65 6303 7788 Web Site: www.saxomarkets.com.sg 1 TRADING FUTURES ON THE SAXOTRADER PLATFORM OPEN DEMO OPEN LIVE WORLDWIDE INVESTMENT

TRADING FUTURES ON THE SAXOTRADER PLATFORM Saxo Capital Markets Tel: +65 6303 7788 Web Site: www.saxomarkets.com.sg 1 TRADING FUTURES ON THE SAXOTRADER PLATFORM OPEN DEMO OPEN LIVE WORLDWIDE INVESTMENT

CONTRACTS FOR DIFFERENCE

CLIENT SERVICE AGREEMENT Halifax New Zealand Limited Client Service Agreement Product Disclosure Statement for CONTRACTS FOR DIFFERENCE Halifax New Zealand Limited Financial Services Provider No. 146605

CLIENT SERVICE AGREEMENT Halifax New Zealand Limited Client Service Agreement Product Disclosure Statement for CONTRACTS FOR DIFFERENCE Halifax New Zealand Limited Financial Services Provider No. 146605

Comparing E-minis and ETFs. John W. Labuszewski, Research and Product Development Brett Vietmeier, Equity Products April 2009

RESEARCH AND product DEVELOPMENT Comparing E-minis and ETFs John W. Labuszewski, Research and Product Development Brett Vietmeier, Equity Products April 2009 13,000 cmegroup.com 12,000 10,000 9,000 8,000

RESEARCH AND product DEVELOPMENT Comparing E-minis and ETFs John W. Labuszewski, Research and Product Development Brett Vietmeier, Equity Products April 2009 13,000 cmegroup.com 12,000 10,000 9,000 8,000

Chapter 8 Clearing House and Performance Bonds

800. CLEARING HOUSE Chapter 8 Clearing House and Performance Bonds The Exchange shall utilize the services of the CME Clearing House in order to protect market participants and to maintain the integrity

800. CLEARING HOUSE Chapter 8 Clearing House and Performance Bonds The Exchange shall utilize the services of the CME Clearing House in order to protect market participants and to maintain the integrity

CME Group/BM&FBOVESPA

Futures trading is not suitable for all investors, and involves the risk of loss. Futures are a leveraged investment, and because only a percentage of a contract s value is required to trade, it is possible

Futures trading is not suitable for all investors, and involves the risk of loss. Futures are a leveraged investment, and because only a percentage of a contract s value is required to trade, it is possible

Understanding Equity Markets An Overview. James R. Burns March 3, 2016

Understanding Equity Markets An Overview James R. Burns March 3, 2016 Agenda I. Trading Venues II. Regulatory Framework III. Recent Developments IV. Questions 2 Trading Venues 3 A Few Key Definitions Algorithmic

Understanding Equity Markets An Overview James R. Burns March 3, 2016 Agenda I. Trading Venues II. Regulatory Framework III. Recent Developments IV. Questions 2 Trading Venues 3 A Few Key Definitions Algorithmic

Request for Information on Evolving Treasury Market Structure (Docket No. TREAS-DO-2015-0013)

") , 2016 VIA ONLINE SUBMISSION (http://regulations.gov) David R. Pearl Office of the Executive Secretary U.S. Department of the Treasury 1500 Pennsylvania Avenue, NW Washington, DC 20220 Re: Request for

, 2016 VIA ONLINE SUBMISSION (http://regulations.gov) David R. Pearl Office of the Executive Secretary U.S. Department of the Treasury 1500 Pennsylvania Avenue, NW Washington, DC 20220 Re: Request for

BEST EXECUTION AND ORDER HANDLING POLICY

BEST EXECUTION AND ORDER HANDLING POLICY 1. INTRODUCTION 1.1 etoro (Europe) Ltd (the Company ) is an Investment Firm regulated by the Cyprus Securities and Exchange Commission ( CySEC ) with license number

BEST EXECUTION AND ORDER HANDLING POLICY 1. INTRODUCTION 1.1 etoro (Europe) Ltd (the Company ) is an Investment Firm regulated by the Cyprus Securities and Exchange Commission ( CySEC ) with license number

High-frequency trading: towards capital market efficiency, or a step too far?

Agenda Advancing economics in business High-frequency trading High-frequency trading: towards capital market efficiency, or a step too far? The growth in high-frequency trading has been a significant development

Agenda Advancing economics in business High-frequency trading High-frequency trading: towards capital market efficiency, or a step too far? The growth in high-frequency trading has been a significant development

RISK DISCLOSURE STATEMENT FOR SECURITY FUTURES CONTRACTS

RISK DISCLOSURE STATEMENT FOR SECURITY FUTURES CONTRACTS This disclosure statement discusses the characteristics and risks of standardized security futures contracts traded on regulated U.S. exchanges.

RISK DISCLOSURE STATEMENT FOR SECURITY FUTURES CONTRACTS This disclosure statement discusses the characteristics and risks of standardized security futures contracts traded on regulated U.S. exchanges.

CME Group Equity Quarterly Roll Analyzer

CME Group Equity Quarterly Roll Analyzer Guide to getting started How the world advances Each quarter during the roll period, CME Group s Equity Quarterly Roll Analyzer is populated with the current futures

CME Group Equity Quarterly Roll Analyzer Guide to getting started How the world advances Each quarter during the roll period, CME Group s Equity Quarterly Roll Analyzer is populated with the current futures

The Growth of High-Frequency Trading: Implications for Financial Stability

The Growth of High-Frequency Trading: Implications for Financial Stability William Barker and Anna Pomeranets Introduction High-frequency trading (HFT), which relies on computers to execute trades at high

The Growth of High-Frequency Trading: Implications for Financial Stability William Barker and Anna Pomeranets Introduction High-frequency trading (HFT), which relies on computers to execute trades at high

High Frequency Trading Background and Current Regulatory Discussion

2. DVFA Banken Forum Frankfurt 20. Juni 2012 High Frequency Trading Background and Current Regulatory Discussion Prof. Dr. Peter Gomber Chair of Business Administration, especially e-finance E-Finance

2. DVFA Banken Forum Frankfurt 20. Juni 2012 High Frequency Trading Background and Current Regulatory Discussion Prof. Dr. Peter Gomber Chair of Business Administration, especially e-finance E-Finance

CME Datamine TM EOD FAQ 8/26/2013

CME Datamine TM EOD FAQ 8/26/2013 Futures trading is not suitable for all investors, and involves the risk of loss. Futures are a leveraged investment, and because only a percentage of a contract s value

CME Datamine TM EOD FAQ 8/26/2013 Futures trading is not suitable for all investors, and involves the risk of loss. Futures are a leveraged investment, and because only a percentage of a contract s value

Research Paper No. 44: How short-selling activity affects liquidity of the Hong Kong stock market. 17 April 2009

Research Paper No. 44: How short-selling activity affects liquidity of the Hong Kong stock market 17 April 2009 Executive Summary 1. In October 2008, the SFC issued a research paper entitled Short Selling

Research Paper No. 44: How short-selling activity affects liquidity of the Hong Kong stock market 17 April 2009 Executive Summary 1. In October 2008, the SFC issued a research paper entitled Short Selling

Technology Advisory Committee

Technology Advisory Committee Subcommittee on Automated and High Frequency Trading Working Group 3 Oversight, Surveillance and Economic Analysis 6-20-2012 Working Group 3 Topics Tagging Attributes Assessment

Technology Advisory Committee Subcommittee on Automated and High Frequency Trading Working Group 3 Oversight, Surveillance and Economic Analysis 6-20-2012 Working Group 3 Topics Tagging Attributes Assessment

A More Informed Picture of Market Liquidity In the U.S. Corporate Bond Market

MARKETAXESS ON MARKETAXESS BID-ASK SPREAD INDEX (BASI) A More Informed Picture of Market Liquidity In the U.S. Corporate Bond Market MARKETAXESS ON MARKETAXESS ON is a forum for thought leadership and

MARKETAXESS ON MARKETAXESS BID-ASK SPREAD INDEX (BASI) A More Informed Picture of Market Liquidity In the U.S. Corporate Bond Market MARKETAXESS ON MARKETAXESS ON is a forum for thought leadership and

Special Executive Report

Special Executive Report S- 7258 December 11, 2014 Implementation of New NYMEX/COMEX Rule Regarding Special Price Fluctuation Limits for Certain NYMEX and COMEX Metals and Options Contracts Background

Special Executive Report S- 7258 December 11, 2014 Implementation of New NYMEX/COMEX Rule Regarding Special Price Fluctuation Limits for Certain NYMEX and COMEX Metals and Options Contracts Background

MARKET REGULATION ADVISORY NOTICE

MARKET REGULATION ADVISORY NOTICE Exchange Subject Rule References Rule 538 Advisory Date Advisory Number CME, CBOT, NYMEX & COMEX Exchange for Related Positions CME Group RA1311-5RR Revised Effective

MARKET REGULATION ADVISORY NOTICE Exchange Subject Rule References Rule 538 Advisory Date Advisory Number CME, CBOT, NYMEX & COMEX Exchange for Related Positions CME Group RA1311-5RR Revised Effective

Market Making and Liquidity Provision in Modern Markets

Canada STA 2015 Market Making and Liquidity Provision in Modern Markets Phil Mackintosh 2 What am I going to talk about? Why are Modern Markets Important? Trading is now physics at the speed of light Jan

Canada STA 2015 Market Making and Liquidity Provision in Modern Markets Phil Mackintosh 2 What am I going to talk about? Why are Modern Markets Important? Trading is now physics at the speed of light Jan

Guidance on Best Execution and Management of Orders

Rules Notice Guidance Note UMIR Please distribute internally to: Legal and Compliance Trading Desk Senior Management Institutional Contact: Kevin McCoy Senior Policy Analyst, Market Regulation Policy Telephone:

Rules Notice Guidance Note UMIR Please distribute internally to: Legal and Compliance Trading Desk Senior Management Institutional Contact: Kevin McCoy Senior Policy Analyst, Market Regulation Policy Telephone:

SAVI TRADING 2 KEY TERMS AND TYPES OF ORDERS. SaviTrading LLP 2013

SAVI TRADING 2 KEY TERMS AND TYPES OF ORDERS 1 SaviTrading LLP 2013 2.1.1 Key terms and definitions We will now explain and define the key terms that you are likely come across during your trading careerbefore

SAVI TRADING 2 KEY TERMS AND TYPES OF ORDERS 1 SaviTrading LLP 2013 2.1.1 Key terms and definitions We will now explain and define the key terms that you are likely come across during your trading careerbefore

Introduction to Weather Markets. Charles Piszczor

Introduction to Weather Markets Charles Piszczor March 22, 2012 Basic Overview Types of Weather Products Settlement Procedures Margining 2 CME Alternative Investments Weather Hurricane Rainfall, Snowfall

Introduction to Weather Markets Charles Piszczor March 22, 2012 Basic Overview Types of Weather Products Settlement Procedures Margining 2 CME Alternative Investments Weather Hurricane Rainfall, Snowfall

Algorithmic trading Equilibrium, efficiency & stability

Algorithmic trading Equilibrium, efficiency & stability Presentation prepared for the conference Market Microstructure: Confronting many viewpoints Institut Louis Bachelier Décembre 2010 Bruno Biais Toulouse

Algorithmic trading Equilibrium, efficiency & stability Presentation prepared for the conference Market Microstructure: Confronting many viewpoints Institut Louis Bachelier Décembre 2010 Bruno Biais Toulouse

RISK DISCLOSURE STATEMENT

RISK DISCLOSURE STATEMENT You should note that there are significant risks inherent in investing in certain financial instruments and in certain markets. Investment in derivatives, futures, options and

RISK DISCLOSURE STATEMENT You should note that there are significant risks inherent in investing in certain financial instruments and in certain markets. Investment in derivatives, futures, options and

Statement for the Record. On Behalf of the AMERICAN BANKERS ASSOCIATION. Before the

Statement for the Record On Behalf of the AMERICAN BANKERS ASSOCIATION Before the Subcommittee on Capital Markets, Insurance, and Government Sponsored Enterprises Committee on Financial Services United

Statement for the Record On Behalf of the AMERICAN BANKERS ASSOCIATION Before the Subcommittee on Capital Markets, Insurance, and Government Sponsored Enterprises Committee on Financial Services United

New ilink Architecture Phase 2 Pre-Launch Mock Trading Sessions

New ilink Architecture Phase 2 Pre-Launch Mock Trading Sessions Customer Test: January 30, 2016 February 20, 2016 March 5, 2016 1 Table of Contents Contents 1. Introduction & Overview... 3 2. Timeline...

New ilink Architecture Phase 2 Pre-Launch Mock Trading Sessions Customer Test: January 30, 2016 February 20, 2016 March 5, 2016 1 Table of Contents Contents 1. Introduction & Overview... 3 2. Timeline...

Message and Execution Throttles. Volatility Awareness Alert

Skadden Skadden, Arps, Slate, Meagher & Flom LLP & Affiliates If you have any questions regarding the matters discussed in this memorandum, please contact the following attorneys or call your regular Skadden

Skadden Skadden, Arps, Slate, Meagher & Flom LLP & Affiliates If you have any questions regarding the matters discussed in this memorandum, please contact the following attorneys or call your regular Skadden