The Solow Model. Zongye Huang 1. Dec, Capital University of Economics and Business

|

|

|

- Mildred Washington

- 7 years ago

- Views:

Transcription

1 The Solow Model Zongye Huang 1 1 International School of Economics and Management Capital University of Economics and Business Dec, 2016

2 Outline Solow Model with Social Planner The Social Planner Production and Technology Economic Equilibrium Decentralized Market Allocations The Economic Environment Solow Dynamics Discussions Consumption and Savings Human Capital

3 A General Equilibrium Model Most of the models in the growth literature share the same underlying structure. ˆ Demand side Preference ˆ Supply side Production technology ˆ Time dimension Dynamic nature We work with supply-side models ˆ Say's law fully applies. Supply creates its own demand. No idle resources. ˆ Population growth, creates its own demand, determining the level of employment. ˆ We can think of all these theories as theories for the evolution of potential output.

4 Outline Solow Model with Social Planner The Social Planner Production and Technology Economic Equilibrium Decentralized Market Allocations The Economic Environment Solow Dynamics Discussions Consumption and Savings Human Capital

5 The Social Planner's Problem I ˆ We start the analysis of the Solow model by pretending that there is a benevolent dictator, or a social planner, who governs all economic and social aairs. ˆ A decentralized competitive market environment coincide with the allocations dictated by the social planner. ˆ Time is discrete, t 0,1,2,... You can think of the period as a year, as a generation, or as any other arbitrary length of time. ˆ The economy is an isolated island with no international trade. There are no good market and production is centralized. ˆ Many households live in this island. Households are each endowed with one unit of labor, which they supply inelastically to the social planner.

6 The Social Planner's Problem II ˆ The social planner uses the entire labor force together with the accumulated aggregate capital stock to produce the one good of the economy. ˆ In each period, the social planner saves a constant fraction s (0, 1) of contemporaneous output. This is equivalent to assuming a constant marginal propensity to consume, or MPC. This is based on the stylized fact that the ratio of aggregate consumption to GDP is roughly constant over time. ˆ It is a closed economy. Saving is used for investment which will be added to the economy's capital stock, and distributes the remaining fraction uniformly across the households of the economy.

7 The Social Planner's Problem III ˆ We let ˆ L t : the number of households (and the size of the labor force) in period t, ˆ K t : the aggregate capital stock in the beginning of period t, ˆ Y t : the aggregate output in period t, ˆ C t : the aggregate consumption in period t, ˆ I t : the aggregate investment in period t.

8 Outline Solow Model with Social Planner The Social Planner Production and Technology Economic Equilibrium Decentralized Market Allocations The Economic Environment Solow Dynamics Discussions Consumption and Savings Human Capital

9 Production Technology The production technology is given by Y t = F (K t, A t L t ) (1) where F: R 2 + R + is a production function. We assume that F is continuous and (although not always necessary) twice dierentiable. A t is a labor-augmented productivity index, A t+1 = (1 + g)a t.

10 Neoclassical Production Function I We say that the technology is neoclassical if F satises the following properties: 1. Constant returns to scale (CRS), or linear homogeneity: F (µk,µa t L) = µf (K, A t L), µ > Positive and diminishing marginal products: F K (K, AL) > 0 F L (K, AL) > 0 F KK (K, AL) < 0 F LL (K, AL) < 0 where F x F x and F xz 2 F x z for x, z K,L.

11 Neoclassical Production Function II 3. Inada conditions: lim K K 0 = lim F L =, L 0 lim K K = lim F L = 0. L

12 Neoclassical Production Function

13 Intensive Form (Per Eective Labor) I Technology in intensive form: let y = Y AL, and k = K AL. Then, by CRS where By denition of f and F, y = f (k) f (k) = F (k,1). f (0) = 0, f (k) > 0 > f (k) lim (k) k 0 = lim (k) k = 0

14 Intensive Form (Per Eective Labor) II Also, F K (K, AL) = f (k) F L (K, AL) = f (k) f (k)k

15 Example: Cobb-Douglas Technology The Cobb-Douglas technology is given by F (K,AL) = K α (AL) 1 α. In this case, let k = K AL, f (k) = kα.

16 Outline Solow Model with Social Planner The Social Planner Production and Technology Economic Equilibrium Decentralized Market Allocations The Economic Environment Solow Dynamics Discussions Consumption and Savings Human Capital

17 Equilibrium Conditions I ˆ Remember that there is a single good, which can be either consumed or invested. Of course, the sum of aggregate consumption and aggregate investment can not exceed aggregate output. That is, the social planner faces the following resource constraint: C t + I t Y t. Equivalently, in ecient labor terms, c t = C t A t L t, i t = y t = Y t A t L t : c t + i t y t. I t A t L t,

18 Equilibrium Conditions II ˆ Suppose that population growth is n 0 per period. The size of the labor force then evolves over time as follow And we normalize L 0 = 1. L t = (1 + n)l t=1 = (1 + n) t L 0 ˆ Suppose that existing capital depreciates over time at a xed rate δ [0,1]. The capital stock in the beginning of next period is given by the non-depreciated part of current-period capital, plus contemporaneous investment. That is, the law of motion for capital is K t+1 = (1=δ)K t + I t. Equivalently, in ecient labor terms: (1 + g)(1 + n)k t+1 = (1=δ)k t + i t

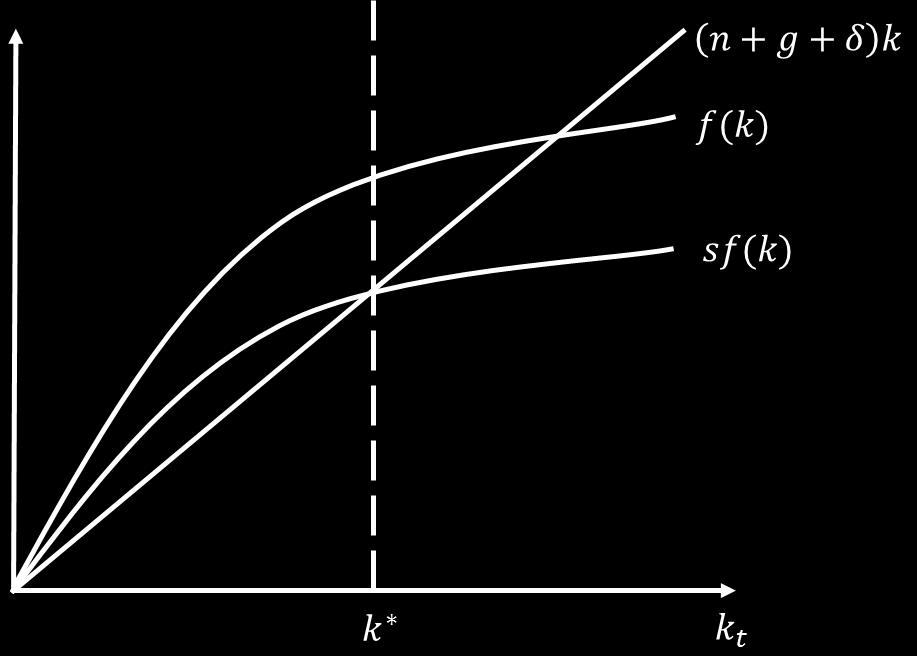

19 Equilibrium Conditions III ˆ If there is no population growth and technology improvement, the above equation is given by k t+1 = (1=δ)k t + i t The change in the capital stock is given by aggregate output, minus capital depreciation, minus aggregate consumption, k t+1 = y t + (1=δ)k t c t. ˆ Consumption is a portion of output, I t = sy t, and i t = s y t. Thus c t = (1 s)y t. We have k t+1 = sf (k t ) + (1=δ)k t (2) or ˆk k t k t = k t+1 k t = s f (k t) δ k t k t

20 Equilibrium Conditions IV There exist a k that makes ˆk = 0, which is a steady state. A steady state of the economy is dened as any level k such that, if the economy starts with k 0 = k, then k t = k for all t 1. That is, a steady state is any xed point k of equation (2), such that k = sf (k ) + (1 δ)k.

21 Transitional Dynamics I ˆ We are interested to know whether the economy will converge to the steady state if it starts away from it. Another way to ask the same question is whether the economy will eventually return to the steady state after an exogenous shock perturbs the economy and moves away from the steady state. ˆ For any k t < k, ˆk t > 0, k t+1 > k t, until it reaches k. On the other hand, for k t > k, ˆk t < 0, and k t+1 < k t. So, k is locally stable, meaning that the economy turn to go back to k with a small deviation from k.

22 Transitional Dynamics II ˆ In addition, we can let the φ(k t ) = f (k t) k t. The function φ gives the output-to-capital ratio in the economy. The properties of function f imply that φ is continuous (and twice dierentiable), decreasing, and satises the Inada conditions at k = 0 and k = : ˆ Recall φ (k t ) = f (k) k f (k) k 2 ˆk k t k t = F L k 2 < 0. = k t+1 k t = s f (k t) δ k t k t The rst component decreases monotonically. The system is also globally stable and transition is monotonic.

23 Transitional Dynamics III ˆ For any level of k below the steady-state level, the model dynamics move the economy toward the steady state (capital stock increases). ˆ For any initial level of k above the steady-state level, the dynamics move the economy toward the steady state (capital stock decreases). ˆ For any non-zero initial level of capital stock, this economy will move toward the steady state. Once it reaches the steady state, it will stay there.

24 Transitional Dynamics IV

25 Outline Solow Model with Social Planner The Social Planner Production and Technology Economic Equilibrium Decentralized Market Allocations The Economic Environment Solow Dynamics Discussions Consumption and Savings Human Capital

26 The Consumer's Problem I ˆ The consumer supplies labor L t to the market at market wage w t. The consumer owns all of the capital K t and rents this capital to the market at rental rate r t. The consumer owns the rm and receives its total prot π t. The consumer's income is then: Y t = r t K t + w t L t + π t ˆ Labor supply grows at an exogenous rate L n = t, L t which is equivalent to L t = e nt L 0.

27 The Consumer's Problem II ˆ Although there is only one consumer, since his/her labor supply is growing over time, you can think of this representing population growth. The consumer accumulates capital, which depreciates at the rate δ: K t = I t δk t where I t is gross investment. Notice that the price of capital is one. In one-good economy, we can always set the price to be one; this good is called the numerate good (in other words, all other prices are relative to this one). ˆ Similar with the case of social planer, the saving rate is exogenously given at s, therefore I t = sy t, K t = sy t δk t

28 The Firm's Problem ˆ The rm takes capital and labor and converts them into output (in the form of consumption and new capital), which is then sold back to the consumer. The rm's technology is described by the production function: Y t = F (K t,a t L t ) where A t is the level of technology at time t. It grows at an exogenous rate g: A t = g. A t ˆ Given factor prices, w t, r t, the rm is maximizing prots π t = F (K t, A t L t ) r t K t w t L t

29 Market Clearing All factors and goods are traded in competitive markets. And those market should clear: Y t = C t + I t L S t = L D t K S t = K D t

30 The Competitive Equilibrium I When we write down a macroeconomic model, we usually need to formally dene what an equilibrium in the market is. An equilibrium in this model is a sequence of factor prices {w t }, {r t } and allocations {K t,l t } such that 1. The capital stock K t, labor supply L t, and technology level A t are determined by above equations, with initial conditions K 0, L 0, and A 0, respectively. 2. Taking prices as given, the rm purchases capital K t and labor L t to maximize its prots. 3. Markets clear: the rm's demand for capital at price r t equals the supply, and the rm's labor demand at wage w t equals the supply of labor.

31 The Competitive Equilibrium II ˆ In general, an equilibrium has the same elements. The equilibrium itself is a vector or series of prices and allocations. ˆ We impose two types of conditions on them: ˆ The agents in the model choose allocations to maximize utility, taking prices as given. ˆ We impose the condition on prices that markets clear. ˆ Usually, in the applications we will see in this class, the market-clearing condition pins everything down.

32 Wages and Interest Rates Since factor markets are competitive, factors are rented by rms at their marginal products, and rm prots are zero. The wage, therefore, is: w t = F(K t,a t L t ) L t and the rental rate of capital is: r t = F(K t,a t L t ) K t Suppose that you invested in one unit of capital today. Tomorrow you would receive r t+1 in rents on that capital, and (1 δ) units of remaining capital. The net return on capital (i.e., the interest rate) is r t+1 δ.

33 Factor Shares and Output Elasticity I ˆ Suppose that we could estimate labor's share of output: α L = total wage paid GDP Generally, estimates of α L for the U.S. and similar economies are about Capital's share, α K, is therefore estimated to be about ˆ Gollin (2002) estimated labor shares for most countries in the range of We usually take α L = 2 3.

34 Factor Shares and Output Elasticity II ˆ The implied value of labor's share from the model: α L = w tl t Y t = Y t L t L t Y t Notice that this is the elasticity of output with respect to labor. Similarly, capital's share is the output elasticity of capital. ˆ In other words, Solow's model and the data together imply that a one percent increase in the labor force leads to a 0.64 percent increase in output, while a one percent increase in the capital stock increases output by 0.36 percent.

35 Outline Solow Model with Social Planner The Social Planner Production and Technology Economic Equilibrium Decentralized Market Allocations The Economic Environment Solow Dynamics Discussions Consumption and Savings Human Capital

36 Model Dynamics I Start by taking the derivative of k = K/AL with respect to time, using the chain rule (I've omitted time subscripts here): K k = AL K (AL) (A L + LA) 2 K = AL K L AL L K A AL A sy δk = kn kg AL = sy δk nk gk = sy (n + g + δ)k (3) where y = Y /(AL). Recall that Y = F (K,AL) and Y exhibits constant return to scale, so y = F (K/AL,1) = F (k,1) f (k).

37 Model Dynamics II Then (3) can be written as k = sf (k) (n + g + δ)k (4) This equation is called capital accumulation equation, or law of motion for capital. The rst term is gross investment (increases in capital per eective worker), while the second is decreases in capital per eective worker due to population growth, technological progress, and depreciation.

38 Model Dynamics III

39 Model Dynamics IV Taking natural logarithm on k, thus lnk t = lnk t lna t lnl t. Then, we take derivative on both sides, k t K = t g n k t K t = s Y t K t δ g n = s f (k t) k t (n + g + δ)

40 Balanced Growth Path I ˆ The balanced growth path is dened in the economy such that all variables (including aggregate variables, variables in per worker form and variables in per eective worker form) grow at constant rates. ˆ The growth rates could be zero, negative or positive. The growth rates of variables do not have to be the same. Recall the transformation, k t = K t A t L t, taking logarithm on both side, lnk t = lnk t lna t lnl t. And we take derivative on both sides, k t K = t A t L t. k t K t A t L t

41 Balanced Growth Path II By assumption, labor and knowledge are growing at rates n and g, respectively. k t = k on steady state, thus k t = 0. Thus, k t K = t n g. k t K t K t K t = n + g. For the growth rate of Y t, consider k k = s f (k) k (n + g + δ) = s y (n + g + δ) k

42 Balanced Growth Path III At the steady state, we have y = k n+g+δ s, Thus, k t = ẏt Y = t A t L t. k t y t Y t A t L t Y t Y t = n + g. Finally, capital per worker, K/L, and output per worker, Y /L, are growing at rate g. For example, if we dene K i = K t L t represents the capital stock per capita (per person), we have K it K it = g.

43 Balanced Growth Path IV ˆ Note that this growth rate is exogenousthere's nothing in the model that a country can change to increase its long-run growth rate. ˆ The growth rate of output per capita in the steady state does not depend on the savings rate, population growth rate, income level, or amount of capital. ˆ It depends ONLY on the rate of exogenous technological progress.

44 Outline Solow Model with Social Planner The Social Planner Production and Technology Economic Equilibrium Decentralized Market Allocations The Economic Environment Solow Dynamics Discussions Consumption and Savings Human Capital

45 Consumption and Savings I ˆ Since an exogenous fraction s of income is saved, we also know that the fraction (1 s) is consumed each period. In other words, C = (1 s)y, or in terms of eective units of labor, c = (1 s)y. ˆ In the steady state, consumption per worker grows at rate g. (Consumption per eective unit of labor, of course, is constant in the steady state.) ˆ Let's use discrete time here. Following the text, let c denote consumption per eective unit of labor on the balanced growth path (i.e., in the steady state). (Note! It is a steady state in terms of eective units of labor; it is a balanced growth path in per capita terms.) On the balanced growth path, sy = sf (k) = (n + g + δ)k, so c = f (k ) (n + g + δ)k

46 Consumption and Savings II ˆ Recall that k depends on n, g, δ, and s. We are interested in how a (permanent) change in the steady state aects the balanced growth path of consumption: c s = [f (k (s,n,g,δ)) (n + g + δ)] k (s,n,g,δ). (5) s ˆ At the steady state, we have sf (k ) = (n + g + δ)k. Take derivatives on both sides respect to s, we have f (k ) + f (k ) k s = (n + g + δ) k s.

47 Consumption and Savings III k s = = f (k ) (n + g + δ) sf (k ) = k f (k ) (n + g + δ)k sk f (k ) k f (k ) sf (k ) sk f (k ) > 0. Thus, k is positively related to s. Thus, the overall eect of saving rate on consumption depends on whether f (k ) is greater or less than (n + g + δ). In the steady state of this model, income goes only to (1) consumption, and (2) replacing lost capital per eective unit of labor (the fraction (n + g + δ) of k).

48 Consumption and Savings IV ˆ Recall also that we have diminishing returns to capital in this model. That means that f (k) is decreasing in the overall level of k. At low levels of k, then, f (k ) is generally greater than (n + g + δ), so that an increase in the savings rate increases steady-state consumption per ELU. At higher levels of k, though, f (k ) is less than (n + g + δ), so that the increase in savings causes a decrease in steady-state consumption per ELU. ˆ The golden rule level of savings, or the golden rule capital stock: the level of savings that maximizes steady-state consumption per eective labor. ˆ The rst-order conditions imply that consumption is maximized at the point where f (k) = (n + g + δ). This is the point at which the slopes of f (k) and (n + g + δ)k are equal.

49 Consumption and Savings V ˆ Note that this means that, although increasing the savings rate always increases the balanced growth path of income per worker, it does not always increase the balanced growth path of consumption.

50 Consumption and Savings VI

51 Solow Model with a Cobb-Douglass production function I ˆ Let's work through an example with a Cobb-Douglass production function Y t = K α t (A t L t ) 1 α. ˆ The other notation is standard. The intensive form of the production function is then y = F ( K AL,1) = ( K AL) α, so y = k α. We have sk α = (n + g + δ)k, and solve for the steady-state k : k s = ( n + g + δ )1/(1 α) (6)

52 Solow Model with a Cobb-Douglass production function II ˆ This is the steady-state level of capital per eective unit of labor (ELU). It is increasing in s, the savings rate, and decreasing in n (population growth), g (the rate of technological progress), and δ (depreciation). Also note that you could easily substitute this into the production function: y = k α. ˆ Recall the condition of golden rule level of consumption, = n + g + δ, thus we have αk α 1 t s Golden = α. ˆ Recall that s and n have no eect on the long-run growth rate of income per capita they only aect the steady-state level of income (per ELU).

53 Solow Model with a Cobb-Douglass production function III ˆ In the steady state, income per capita does grow, at g. Notice that a higher rate of technological growth (g) means two things: ˆ the economy grows faster in per capita terms in the steady state; ˆ the steady-state level of income (per ELU) is lower. The second is because with a higher g, more investment has to go to maintaining the existing level of capital per worker. ˆ It's more intuitive to think of this in terms of population growth, which is the same idea: the faster is population growth, the more investment needs to go to maintaining the current level per worker for the new workers.

54 Exercise Think about how each of the following developments aects the equilibrium diagram of the Solow model. Evaluate the eect on the steady state value of k: (a) The rate of depreciation falls; (b) the rate of technological progress rises; (c) population growth rate increases; (d) saving rate increases.

55 Outline Solow Model with Social Planner The Social Planner Production and Technology Economic Equilibrium Decentralized Market Allocations The Economic Environment Solow Dynamics Discussions Consumption and Savings Human Capital

56 Human Capital I In order to enrich our model, we want to include human capital. Human capital is a term we use to represent the stock of skills, education, competencies and other productivity-enhancing characteristics embedded in labor. Put dierently, human capital represents the eciency units of labor embedded in raw labor hours. Adding human capital to theory: the production function becomes: Y t = K α t H β t (A t L t ) 1 α β (7) H is the stock of human capital. We assume that it accumulates and depreciates exactly like physical capital; the savings rates for physical and human capital dier and are given by s k and s h respectively. Two rates of depreciation are, δ k and δ h, respectively.

57 H(t) A(t)L(t) Human Capital II Let h(t) =, the laws of motion of these two types of capital goods is given by k t = s k y t (n + g + δ k )k t ḣ t = s h y t (n + g + δ h )h t (8) where y t = k α t h β t. Assuming that α + β < 1, or that there are decreasing returns to all capital. At steady states, k = ḣ = 0. k t = s k kt α 1 h β t (n + g + δ k ) = 0 k t k t = s h kt α h β 1 t (n + g + δ h ) = 0 k t h t k t = s h s k n + g + δ k n + g + δ h

58 Human Capital III Thus, the steady states for the two capital stocks: k = [ ( s k n + g + δ k ) 1 β ( s h n + g + δ h ) β ] 1 1 α β h = [ ( s k n + g + δ k ) α ( s h n + g + δ h ) 1 α ] 1 1 α β If δ k = δ h = δ, we have s1 β k s β h k = ( ) 1/(1 α β) ; n + g + δ k h = ( sα k s1 α h n + g + δ h ) 1/(1 α β) (9)

Macroeconomics Lecture 1: The Solow Growth Model

Macroeconomics Lecture 1: The Solow Growth Model Richard G. Pierse 1 Introduction One of the most important long-run issues in macroeconomics is understanding growth. Why do economies grow and what determines

Macroeconomics Lecture 1: The Solow Growth Model Richard G. Pierse 1 Introduction One of the most important long-run issues in macroeconomics is understanding growth. Why do economies grow and what determines

CHAPTER 7 Economic Growth I

CHAPTER 7 Economic Growth I Questions for Review 1. In the Solow growth model, a high saving rate leads to a large steady-state capital stock and a high level of steady-state output. A low saving rate

CHAPTER 7 Economic Growth I Questions for Review 1. In the Solow growth model, a high saving rate leads to a large steady-state capital stock and a high level of steady-state output. A low saving rate

The Solow Model. Savings and Leakages from Per Capita Capital. (n+d)k. sk^alpha. k*: steady state 0 1 2.22 3 4. Per Capita Capital, k

k. sk^alpha. k*: steady state 0 1 2.22 3 4. Per Capita Capital, k") Savings and Leakages from Per Capita Capital 0.1.2.3.4.5 The Solow Model (n+d)k sk^alpha k*: steady state 0 1 2.22 3 4 Per Capita Capital, k Pop. growth and depreciation Savings In the diagram... sy =

Savings and Leakages from Per Capita Capital 0.1.2.3.4.5 The Solow Model (n+d)k sk^alpha k*: steady state 0 1 2.22 3 4 Per Capita Capital, k Pop. growth and depreciation Savings In the diagram... sy =

Universidad de Montevideo Macroeconomia II. The Ramsey-Cass-Koopmans Model

Universidad de Montevideo Macroeconomia II Danilo R. Trupkin Class Notes (very preliminar) The Ramsey-Cass-Koopmans Model 1 Introduction One shortcoming of the Solow model is that the saving rate is exogenous

Universidad de Montevideo Macroeconomia II Danilo R. Trupkin Class Notes (very preliminar) The Ramsey-Cass-Koopmans Model 1 Introduction One shortcoming of the Solow model is that the saving rate is exogenous

Chapters 7 and 8 Solow Growth Model Basics

Chapters 7 and 8 Solow Growth Model Basics The Solow growth model breaks the growth of economies down into basics. It starts with our production function Y = F (K, L) and puts in per-worker terms. Y L

Chapters 7 and 8 Solow Growth Model Basics The Solow growth model breaks the growth of economies down into basics. It starts with our production function Y = F (K, L) and puts in per-worker terms. Y L

University of Saskatchewan Department of Economics Economics 414.3 Homework #1

Homework #1 1. In 1900 GDP per capita in Japan (measured in 2000 dollars) was $1,433. In 2000 it was $26,375. (a) Calculate the growth rate of income per capita in Japan over this century. (b) Now suppose

Homework #1 1. In 1900 GDP per capita in Japan (measured in 2000 dollars) was $1,433. In 2000 it was $26,375. (a) Calculate the growth rate of income per capita in Japan over this century. (b) Now suppose

14.452 Economic Growth: Lectures 2 and 3: The Solow Growth Model

14.452 Economic Growth: Lectures 2 and 3: The Solow Growth Model Daron Acemoglu MIT November 1 and 3, 2011. Daron Acemoglu (MIT) Economic Growth Lectures 2 and 3 November 1 and 3, 2011. 1 / 96 Solow Growth

14.452 Economic Growth: Lectures 2 and 3: The Solow Growth Model Daron Acemoglu MIT November 1 and 3, 2011. Daron Acemoglu (MIT) Economic Growth Lectures 2 and 3 November 1 and 3, 2011. 1 / 96 Solow Growth

Economic Growth. (c) Copyright 1999 by Douglas H. Joines 1

Copyright 1999 by Douglas H. Joines 1") Economic Growth (c) Copyright 1999 by Douglas H. Joines 1 Module Objectives Know what determines the growth rates of aggregate and per capita GDP Distinguish factors that affect the economy s growth rate

Economic Growth (c) Copyright 1999 by Douglas H. Joines 1 Module Objectives Know what determines the growth rates of aggregate and per capita GDP Distinguish factors that affect the economy s growth rate

Lecture 3: Growth with Overlapping Generations (Acemoglu 2009, Chapter 9, adapted from Zilibotti)

") Lecture 3: Growth with Overlapping Generations (Acemoglu 2009, Chapter 9, adapted from Zilibotti) Kjetil Storesletten September 10, 2013 Kjetil Storesletten () Lecture 3 September 10, 2013 1 / 44 Growth

Lecture 3: Growth with Overlapping Generations (Acemoglu 2009, Chapter 9, adapted from Zilibotti) Kjetil Storesletten September 10, 2013 Kjetil Storesletten () Lecture 3 September 10, 2013 1 / 44 Growth

MASTER IN ENGINEERING AND TECHNOLOGY MANAGEMENT

MASTER IN ENGINEERING AND TECHNOLOGY MANAGEMENT ECONOMICS OF GROWTH AND INNOVATION Lecture 1, January 23, 2004 Theories of Economic Growth 1. Introduction 2. Exogenous Growth The Solow Model Mandatory

MASTER IN ENGINEERING AND TECHNOLOGY MANAGEMENT ECONOMICS OF GROWTH AND INNOVATION Lecture 1, January 23, 2004 Theories of Economic Growth 1. Introduction 2. Exogenous Growth The Solow Model Mandatory

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS Exam: ECON4310 Intertemporal macroeconomics Date of exam: Thursday, November 27, 2008 Grades are given: December 19, 2008 Time for exam: 09:00 a.m. 12:00 noon

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS Exam: ECON4310 Intertemporal macroeconomics Date of exam: Thursday, November 27, 2008 Grades are given: December 19, 2008 Time for exam: 09:00 a.m. 12:00 noon

Preparation course MSc Business&Econonomics: Economic Growth

Preparation course MSc Business&Econonomics: Economic Growth Tom-Reiel Heggedal Economics Department 2014 TRH (Institute) Solow model 2014 1 / 27 Theory and models Objective of this lecture: learn Solow

Preparation course MSc Business&Econonomics: Economic Growth Tom-Reiel Heggedal Economics Department 2014 TRH (Institute) Solow model 2014 1 / 27 Theory and models Objective of this lecture: learn Solow

Note on growth and growth accounting

CHAPTER 0 Note on growth and growth accounting 1. Growth and the growth rate In this section aspects of the mathematical concept of the rate of growth used in growth models and in the empirical analysis

CHAPTER 0 Note on growth and growth accounting 1. Growth and the growth rate In this section aspects of the mathematical concept of the rate of growth used in growth models and in the empirical analysis

The Real Business Cycle Model

The Real Business Cycle Model Ester Faia Goethe University Frankfurt Nov 2015 Ester Faia (Goethe University Frankfurt) RBC Nov 2015 1 / 27 Introduction The RBC model explains the co-movements in the uctuations

The Real Business Cycle Model Ester Faia Goethe University Frankfurt Nov 2015 Ester Faia (Goethe University Frankfurt) RBC Nov 2015 1 / 27 Introduction The RBC model explains the co-movements in the uctuations

Lecture 14 More on Real Business Cycles. Noah Williams

Lecture 14 More on Real Business Cycles Noah Williams University of Wisconsin - Madison Economics 312 Optimality Conditions Euler equation under uncertainty: u C (C t, 1 N t) = βe t [u C (C t+1, 1 N t+1)

Lecture 14 More on Real Business Cycles Noah Williams University of Wisconsin - Madison Economics 312 Optimality Conditions Euler equation under uncertainty: u C (C t, 1 N t) = βe t [u C (C t+1, 1 N t+1)

GDP: The market value of final goods and services, newly produced WITHIN a nation during a fixed period.

GDP: The market value of final goods and services, newly produced WITHIN a nation during a fixed period. Value added: Value of output (market value) purchased inputs (e.g. intermediate goods) GDP is a

GDP: The market value of final goods and services, newly produced WITHIN a nation during a fixed period. Value added: Value of output (market value) purchased inputs (e.g. intermediate goods) GDP is a

Long Run Growth Solow s Neoclassical Growth Model

Long Run Growth Solow s Neoclassical Growth Model 1 Simple Growth Facts Growth in real GDP per capita is non trivial, but only really since Industrial Revolution Dispersion in real GDP per capita across

Long Run Growth Solow s Neoclassical Growth Model 1 Simple Growth Facts Growth in real GDP per capita is non trivial, but only really since Industrial Revolution Dispersion in real GDP per capita across

ECON20310 LECTURE SYNOPSIS REAL BUSINESS CYCLE

ECON20310 LECTURE SYNOPSIS REAL BUSINESS CYCLE YUAN TIAN This synopsis is designed merely for keep a record of the materials covered in lectures. Please refer to your own lecture notes for all proofs.

ECON20310 LECTURE SYNOPSIS REAL BUSINESS CYCLE YUAN TIAN This synopsis is designed merely for keep a record of the materials covered in lectures. Please refer to your own lecture notes for all proofs.

Hello, my name is Olga Michasova and I present the work The generalized model of economic growth with human capital accumulation.

Hello, my name is Olga Michasova and I present the work The generalized model of economic growth with human capital accumulation. 1 Without any doubts human capital is a key factor of economic growth because

Hello, my name is Olga Michasova and I present the work The generalized model of economic growth with human capital accumulation. 1 Without any doubts human capital is a key factor of economic growth because

1 National Income and Product Accounts

Espen Henriksen econ249 UCSB 1 National Income and Product Accounts 11 Gross Domestic Product (GDP) Can be measured in three different but equivalent ways: 1 Production Approach 2 Expenditure Approach

Espen Henriksen econ249 UCSB 1 National Income and Product Accounts 11 Gross Domestic Product (GDP) Can be measured in three different but equivalent ways: 1 Production Approach 2 Expenditure Approach

Chapter 7: Economic Growth part 1

Chapter 7: Economic Growth part 1 Learn the closed economy Solow model See how a country s standard of living depends on its saving and population growth rates Learn how to use the Golden Rule to find

Chapter 7: Economic Growth part 1 Learn the closed economy Solow model See how a country s standard of living depends on its saving and population growth rates Learn how to use the Golden Rule to find

The previous chapter introduced a number of basic facts and posed the main questions

2 The Solow Growth Model The previous chapter introduced a number of basic facts and posed the main questions concerning the sources of economic growth over time and the causes of differences in economic

2 The Solow Growth Model The previous chapter introduced a number of basic facts and posed the main questions concerning the sources of economic growth over time and the causes of differences in economic

Economic Growth. Chapter 11

Chapter 11 Economic Growth This chapter examines the determinants of economic growth. A startling fact about economic growth is the large variation in the growth experience of different countries in recent

Chapter 11 Economic Growth This chapter examines the determinants of economic growth. A startling fact about economic growth is the large variation in the growth experience of different countries in recent

Finance 30220 Solutions to Problem Set #3. Year Real GDP Real Capital Employment

Finance 00 Solutions to Problem Set # ) Consider the following data from the US economy. Year Real GDP Real Capital Employment Stock 980 5,80 7,446 90,800 990 7,646 8,564 09,5 Assume that production can

Finance 00 Solutions to Problem Set # ) Consider the following data from the US economy. Year Real GDP Real Capital Employment Stock 980 5,80 7,446 90,800 990 7,646 8,564 09,5 Assume that production can

Towards a Structuralist Interpretation of Saving, Investment and Current Account in Turkey

Towards a Structuralist Interpretation of Saving, Investment and Current Account in Turkey MURAT ÜNGÖR Central Bank of the Republic of Turkey http://www.muratungor.com/ April 2012 We live in the age of

Towards a Structuralist Interpretation of Saving, Investment and Current Account in Turkey MURAT ÜNGÖR Central Bank of the Republic of Turkey http://www.muratungor.com/ April 2012 We live in the age of

14.452 Economic Growth: Lectures 6 and 7, Neoclassical Growth

14.452 Economic Growth: Lectures 6 and 7, Neoclassical Growth Daron Acemoglu MIT November 15 and 17, 211. Daron Acemoglu (MIT) Economic Growth Lectures 6 and 7 November 15 and 17, 211. 1 / 71 Introduction

14.452 Economic Growth: Lectures 6 and 7, Neoclassical Growth Daron Acemoglu MIT November 15 and 17, 211. Daron Acemoglu (MIT) Economic Growth Lectures 6 and 7 November 15 and 17, 211. 1 / 71 Introduction

I d ( r; MPK f, τ) Y < C d +I d +G

Y < C d +I d +G") 1. Use the IS-LM model to determine the effects of each of the following on the general equilibrium values of the real wage, employment, output, the real interest rate, consumption, investment, and the

1. Use the IS-LM model to determine the effects of each of the following on the general equilibrium values of the real wage, employment, output, the real interest rate, consumption, investment, and the

Name: Date: 3. Variables that a model tries to explain are called: A. endogenous. B. exogenous. C. market clearing. D. fixed.

Name: Date: 1 A measure of how fast prices are rising is called the: A growth rate of real GDP B inflation rate C unemployment rate D market-clearing rate 2 Compared with a recession, real GDP during a

Name: Date: 1 A measure of how fast prices are rising is called the: A growth rate of real GDP B inflation rate C unemployment rate D market-clearing rate 2 Compared with a recession, real GDP during a

This paper is not to be removed from the Examination Halls

This paper is not to be removed from the Examination Halls UNIVERSITY OF LONDON EC2065 ZA BSc degrees and Diplomas for Graduates in Economics, Management, Finance and the Social Sciences, the Diplomas

This paper is not to be removed from the Examination Halls UNIVERSITY OF LONDON EC2065 ZA BSc degrees and Diplomas for Graduates in Economics, Management, Finance and the Social Sciences, the Diplomas

2. With an MPS of.4, the MPC will be: A) 1.0 minus.4. B).4 minus 1.0. C) the reciprocal of the MPS. D).4. Answer: A

1.0 minus.4. B).4 minus 1.0. C) the reciprocal of the MPS. D).4. Answer: A") 1. If Carol's disposable income increases from $1,200 to $1,700 and her level of saving increases from minus $100 to a plus $100, her marginal propensity to: A) save is three-fifths. B) consume is one-half.

1. If Carol's disposable income increases from $1,200 to $1,700 and her level of saving increases from minus $100 to a plus $100, her marginal propensity to: A) save is three-fifths. B) consume is one-half.

VI. Real Business Cycles Models

VI. Real Business Cycles Models Introduction Business cycle research studies the causes and consequences of the recurrent expansions and contractions in aggregate economic activity that occur in most industrialized

VI. Real Business Cycles Models Introduction Business cycle research studies the causes and consequences of the recurrent expansions and contractions in aggregate economic activity that occur in most industrialized

19 : Theory of Production

19 : Theory of Production 1 Recap from last session Long Run Production Analysis Return to Scale Isoquants, Isocost Choice of input combination Expansion path Economic Region of Production Session Outline

19 : Theory of Production 1 Recap from last session Long Run Production Analysis Return to Scale Isoquants, Isocost Choice of input combination Expansion path Economic Region of Production Session Outline

Agenda. Productivity, Output, and Employment, Part 1. The Production Function. The Production Function. The Production Function. The Demand for Labor

Agenda Productivity, Output, and Employment, Part 1 3-1 3-2 A production function shows how businesses transform factors of production into output of goods and services through the applications of technology.

Agenda Productivity, Output, and Employment, Part 1 3-1 3-2 A production function shows how businesses transform factors of production into output of goods and services through the applications of technology.

Prot Maximization and Cost Minimization

Simon Fraser University Prof. Karaivanov Department of Economics Econ 0 COST MINIMIZATION Prot Maximization and Cost Minimization Remember that the rm's problem is maximizing prots by choosing the optimal

Simon Fraser University Prof. Karaivanov Department of Economics Econ 0 COST MINIMIZATION Prot Maximization and Cost Minimization Remember that the rm's problem is maximizing prots by choosing the optimal

INTRODUCTION TO ADVANCED MACROECONOMICS Preliminary Exam with answers September 2014

Duration: 120 min INTRODUCTION TO ADVANCED MACROECONOMICS Preliminary Exam with answers September 2014 Format of the mock examination Section A. Multiple Choice Questions (20 % of the total marks) Section

Duration: 120 min INTRODUCTION TO ADVANCED MACROECONOMICS Preliminary Exam with answers September 2014 Format of the mock examination Section A. Multiple Choice Questions (20 % of the total marks) Section

Sample Midterm Solutions

Sample Midterm Solutions Instructions: Please answer both questions. You should show your working and calculations for each applicable problem. Correct answers without working will get you relatively few

Sample Midterm Solutions Instructions: Please answer both questions. You should show your working and calculations for each applicable problem. Correct answers without working will get you relatively few

The RBC methodology also comes down to two principles:

Chapter 5 Real business cycles 5.1 Real business cycles The most well known paper in the Real Business Cycles (RBC) literature is Kydland and Prescott (1982). That paper introduces both a specific theory

Chapter 5 Real business cycles 5.1 Real business cycles The most well known paper in the Real Business Cycles (RBC) literature is Kydland and Prescott (1982). That paper introduces both a specific theory

Prep. Course Macroeconomics

Prep. Course Macroeconomics Intertemporal consumption and saving decision; Ramsey model Tom-Reiel Heggedal tom-reiel.heggedal@bi.no BI 2014 Heggedal (BI) Savings & Ramsey 2014 1 / 30 Overview this lecture

Prep. Course Macroeconomics Intertemporal consumption and saving decision; Ramsey model Tom-Reiel Heggedal tom-reiel.heggedal@bi.no BI 2014 Heggedal (BI) Savings & Ramsey 2014 1 / 30 Overview this lecture

CHAPTER 7: AGGREGATE DEMAND AND AGGREGATE SUPPLY

CHAPTER 7: AGGREGATE DEMAND AND AGGREGATE SUPPLY Learning goals of this chapter: What forces bring persistent and rapid expansion of real GDP? What causes inflation? Why do we have business cycles? How

CHAPTER 7: AGGREGATE DEMAND AND AGGREGATE SUPPLY Learning goals of this chapter: What forces bring persistent and rapid expansion of real GDP? What causes inflation? Why do we have business cycles? How

Econ 102 Aggregate Supply and Demand

Econ 102 ggregate Supply and Demand 1. s on previous homework assignments, turn in a news article together with your summary and explanation of why it is relevant to this week s topic, ggregate Supply

Econ 102 ggregate Supply and Demand 1. s on previous homework assignments, turn in a news article together with your summary and explanation of why it is relevant to this week s topic, ggregate Supply

CHAPTER 9 Building the Aggregate Expenditures Model

CHAPTER 9 Building the Aggregate Expenditures Model Topic Question numbers 1. Consumption function/apc/mpc 1-42 2. Saving function/aps/mps 43-56 3. Shifts in consumption and saving functions 57-72 4 Graphs/tables:

CHAPTER 9 Building the Aggregate Expenditures Model Topic Question numbers 1. Consumption function/apc/mpc 1-42 2. Saving function/aps/mps 43-56 3. Shifts in consumption and saving functions 57-72 4 Graphs/tables:

14.452 Economic Growth: Lecture 11, Technology Diffusion, Trade and World Growth

14.452 Economic Growth: Lecture 11, Technology Diffusion, Trade and World Growth Daron Acemoglu MIT December 2, 2014. Daron Acemoglu (MIT) Economic Growth Lecture 11 December 2, 2014. 1 / 43 Introduction

14.452 Economic Growth: Lecture 11, Technology Diffusion, Trade and World Growth Daron Acemoglu MIT December 2, 2014. Daron Acemoglu (MIT) Economic Growth Lecture 11 December 2, 2014. 1 / 43 Introduction

Intermediate Microeconomics (22014)

") Intermediate Microeconomics (22014) I. Consumer Instructor: Marc Teignier-Baqué First Semester, 2011 Outline Part I. Consumer 1. umer 1.1 Budget Constraints 1.2 Preferences 1.3 Utility Function 1.4 1.5

Intermediate Microeconomics (22014) I. Consumer Instructor: Marc Teignier-Baqué First Semester, 2011 Outline Part I. Consumer 1. umer 1.1 Budget Constraints 1.2 Preferences 1.3 Utility Function 1.4 1.5

Economic Growth: Theory and Empirics (2012) Problem set I

Problem set I") Economic Growth: Theory and Empirics (2012) Problem set I Due date: April 27, 2012 Problem 1 Consider a Solow model with given saving/investment rate s. Assume: Y t = K α t (A tl t ) 1 α 2) a constant

Economic Growth: Theory and Empirics (2012) Problem set I Due date: April 27, 2012 Problem 1 Consider a Solow model with given saving/investment rate s. Assume: Y t = K α t (A tl t ) 1 α 2) a constant

TRADE AND INVESTMENT IN THE NATIONAL ACCOUNTS This text accompanies the material covered in class.

TRADE AND INVESTMENT IN THE NATIONAL ACCOUNTS This text accompanies the material covered in class. 1 Definition of some core variables Imports (flow): Q t Exports (flow): X t Net exports (or Trade balance)

TRADE AND INVESTMENT IN THE NATIONAL ACCOUNTS This text accompanies the material covered in class. 1 Definition of some core variables Imports (flow): Q t Exports (flow): X t Net exports (or Trade balance)

Why Does Consumption Lead the Business Cycle?

Why Does Consumption Lead the Business Cycle? Yi Wen Department of Economics Cornell University, Ithaca, N.Y. yw57@cornell.edu Abstract Consumption in the US leads output at the business cycle frequency.

Why Does Consumption Lead the Business Cycle? Yi Wen Department of Economics Cornell University, Ithaca, N.Y. yw57@cornell.edu Abstract Consumption in the US leads output at the business cycle frequency.

Graduate Macro Theory II: Notes on Investment

Graduate Macro Theory II: Notes on Investment Eric Sims University of Notre Dame Spring 2011 1 Introduction These notes introduce and discuss modern theories of firm investment. While much of this is done

Graduate Macro Theory II: Notes on Investment Eric Sims University of Notre Dame Spring 2011 1 Introduction These notes introduce and discuss modern theories of firm investment. While much of this is done

2. Real Business Cycle Theory (June 25, 2013)

") Prof. Dr. Thomas Steger Advanced Macroeconomics II Lecture SS 13 2. Real Business Cycle Theory (June 25, 2013) Introduction Simplistic RBC Model Simple stochastic growth model Baseline RBC model Introduction

Prof. Dr. Thomas Steger Advanced Macroeconomics II Lecture SS 13 2. Real Business Cycle Theory (June 25, 2013) Introduction Simplistic RBC Model Simple stochastic growth model Baseline RBC model Introduction

Chapter 4 Consumption, Saving, and Investment

Chapter 4 Consumption, Saving, and Investment Multiple Choice Questions 1. Desired national saving equals (a) Y C d G. (b) C d + I d + G. (c) I d + G. (d) Y I d G. 2. With no inflation and a nominal interest

Chapter 4 Consumption, Saving, and Investment Multiple Choice Questions 1. Desired national saving equals (a) Y C d G. (b) C d + I d + G. (c) I d + G. (d) Y I d G. 2. With no inflation and a nominal interest

Introduction to the Economic Growth course

Economic Growth Lecture Note 1. 03.02.2011. Christian Groth Introduction to the Economic Growth course 1 Economic growth theory Economic growth theory is the study of what factors and mechanisms determine

Economic Growth Lecture Note 1. 03.02.2011. Christian Groth Introduction to the Economic Growth course 1 Economic growth theory Economic growth theory is the study of what factors and mechanisms determine

Exam 1 Review. 3. A severe recession is called a(n): A) depression. B) deflation. C) exogenous event. D) market-clearing assumption.

: A) depression. B) deflation. C) exogenous event. D) market-clearing assumption.") Exam 1 Review 1. Macroeconomics does not try to answer the question of: A) why do some countries experience rapid growth. B) what is the rate of return on education. C) why do some countries have high

Exam 1 Review 1. Macroeconomics does not try to answer the question of: A) why do some countries experience rapid growth. B) what is the rate of return on education. C) why do some countries have high

The Real Business Cycle model

The Real Business Cycle model Spring 2013 1 Historical introduction Modern business cycle theory really got started with Great Depression Keynes: The General Theory of Employment, Interest and Money Keynesian

The Real Business Cycle model Spring 2013 1 Historical introduction Modern business cycle theory really got started with Great Depression Keynes: The General Theory of Employment, Interest and Money Keynesian

Graduate Macro Theory II: The Real Business Cycle Model

Graduate Macro Theory II: The Real Business Cycle Model Eric Sims University of Notre Dame Spring 2011 1 Introduction This note describes the canonical real business cycle model. A couple of classic references

Graduate Macro Theory II: The Real Business Cycle Model Eric Sims University of Notre Dame Spring 2011 1 Introduction This note describes the canonical real business cycle model. A couple of classic references

Charles Jones: US Economic Growth in a World of Ideas and other Jones Papers. January 22, 2014

Charles Jones: US Economic Growth in a World of Ideas and other Jones Papers January 22, 2014 U.S. GDP per capita, log scale Old view: therefore the US is in some kind of Solow steady state (i.e. Balanced

Charles Jones: US Economic Growth in a World of Ideas and other Jones Papers January 22, 2014 U.S. GDP per capita, log scale Old view: therefore the US is in some kind of Solow steady state (i.e. Balanced

Study Questions for Chapter 9 (Answer Sheet)

") DEREE COLLEGE DEPARTMENT OF ECONOMICS EC 1101 PRINCIPLES OF ECONOMICS II FALL SEMESTER 2002 M-W-F 13:00-13:50 Dr. Andreas Kontoleon Office hours: Contact: a.kontoleon@ucl.ac.uk Wednesdays 15:00-17:00 Study

DEREE COLLEGE DEPARTMENT OF ECONOMICS EC 1101 PRINCIPLES OF ECONOMICS II FALL SEMESTER 2002 M-W-F 13:00-13:50 Dr. Andreas Kontoleon Office hours: Contact: a.kontoleon@ucl.ac.uk Wednesdays 15:00-17:00 Study

Revenue Structure, Objectives of a Firm and. Break-Even Analysis.

Revenue :The income receipt by way of sale proceeds is the revenue of the firm. As with costs, we need to study concepts of total, average and marginal revenues. Each unit of output sold in the market

Revenue :The income receipt by way of sale proceeds is the revenue of the firm. As with costs, we need to study concepts of total, average and marginal revenues. Each unit of output sold in the market

Charles I. Jones Maroeconomics Economic Crisis Update (2010 års upplaga) Kurs 407 Makroekonomi och ekonomisk- politisk analys

Kurs 407 Makroekonomi och ekonomisk- politisk analys") HHS Kurs 407 Makroekonomi och ekonomisk- politisk analys VT2011 Charles I. Jones Maroeconomics Economic Crisis Update Sebastian Krakowski Kurs 407 Makroekonomi och ekonomisk- politisk analys Contents Overview...

HHS Kurs 407 Makroekonomi och ekonomisk- politisk analys VT2011 Charles I. Jones Maroeconomics Economic Crisis Update Sebastian Krakowski Kurs 407 Makroekonomi och ekonomisk- politisk analys Contents Overview...

Preparation course MSc Business & Econonomics- Macroeconomics: Introduction & Concepts

Preparation course MSc Business & Econonomics- Macroeconomics: Introduction & Concepts Tom-Reiel Heggedal Economics Department 2014 TRH (Institute) Intro&Concepts 2014 1 / 20 General Information Me: Tom-Reiel

Preparation course MSc Business & Econonomics- Macroeconomics: Introduction & Concepts Tom-Reiel Heggedal Economics Department 2014 TRH (Institute) Intro&Concepts 2014 1 / 20 General Information Me: Tom-Reiel

Noah Williams Economics 312. University of Wisconsin Spring 2013. Midterm Examination Solutions

Noah Williams Economics 31 Department of Economics Macroeconomics University of Wisconsin Spring 013 Midterm Examination Solutions Instructions: This is a 75 minute examination worth 100 total points.

Noah Williams Economics 31 Department of Economics Macroeconomics University of Wisconsin Spring 013 Midterm Examination Solutions Instructions: This is a 75 minute examination worth 100 total points.

Technology and Economic Growth

Growth Accounting Formula Technology and Economic Growth A. %ΔY = %ΔA + (2/3) %ΔN + (1/3) %ΔK B. Ex. Suppose labor, capital, and technology each grow at 1% a year. %ΔY = 1 + (2/3) 1 + (1/3) 1 = 2 C. Growth

Growth Accounting Formula Technology and Economic Growth A. %ΔY = %ΔA + (2/3) %ΔN + (1/3) %ΔK B. Ex. Suppose labor, capital, and technology each grow at 1% a year. %ΔY = 1 + (2/3) 1 + (1/3) 1 = 2 C. Growth

ANSWERS TO END-OF-CHAPTER QUESTIONS

ANSWERS TO END-OF-CHAPTER QUESTIONS 9-1 Explain what relationships are shown by (a) the consumption schedule, (b) the saving schedule, (c) the investment-demand curve, and (d) the investment schedule.

ANSWERS TO END-OF-CHAPTER QUESTIONS 9-1 Explain what relationships are shown by (a) the consumption schedule, (b) the saving schedule, (c) the investment-demand curve, and (d) the investment schedule.

Real Business Cycle Models

Real Business Cycle Models Lecture 2 Nicola Viegi April 2015 Basic RBC Model Claim: Stochastic General Equlibrium Model Is Enough to Explain The Business cycle Behaviour of the Economy Money is of little

Real Business Cycle Models Lecture 2 Nicola Viegi April 2015 Basic RBC Model Claim: Stochastic General Equlibrium Model Is Enough to Explain The Business cycle Behaviour of the Economy Money is of little

Government Budget and Fiscal Policy CHAPTER

Government Budget and Fiscal Policy 11 CHAPTER The National Budget The national budget is the annual statement of the government s expenditures and tax revenues. Fiscal policy is the use of the federal

Government Budget and Fiscal Policy 11 CHAPTER The National Budget The national budget is the annual statement of the government s expenditures and tax revenues. Fiscal policy is the use of the federal

Calibration of Normalised CES Production Functions in Dynamic Models

Discussion Paper No. 06-078 Calibration of Normalised CES Production Functions in Dynamic Models Rainer Klump and Marianne Saam Discussion Paper No. 06-078 Calibration of Normalised CES Production Functions

Discussion Paper No. 06-078 Calibration of Normalised CES Production Functions in Dynamic Models Rainer Klump and Marianne Saam Discussion Paper No. 06-078 Calibration of Normalised CES Production Functions

Reference: Gregory Mankiw s Principles of Macroeconomics, 2 nd edition, Chapters 10 and 11. Gross Domestic Product

Macroeconomics Topic 1: Define and calculate GDP. Understand the difference between real and nominal variables (e.g., GDP, wages, interest rates) and know how to construct a price index. Reference: Gregory

Macroeconomics Topic 1: Define and calculate GDP. Understand the difference between real and nominal variables (e.g., GDP, wages, interest rates) and know how to construct a price index. Reference: Gregory

5. R&D based Economic Growth: Romer (1990)

") Prof. Dr. Thomas Steger Advanced Macroeconomics I Lecture SS 13 5. R&D based Economic Growth: Romer (1990) Introduction The challenge of modeling technological change The structure of the model The long

Prof. Dr. Thomas Steger Advanced Macroeconomics I Lecture SS 13 5. R&D based Economic Growth: Romer (1990) Introduction The challenge of modeling technological change The structure of the model The long

Chapter 13 Real Business Cycle Theory

Chapter 13 Real Business Cycle Theory Real Business Cycle (RBC) Theory is the other dominant strand of thought in modern macroeconomics. For the most part, RBC theory has held much less sway amongst policy-makers

Chapter 13 Real Business Cycle Theory Real Business Cycle (RBC) Theory is the other dominant strand of thought in modern macroeconomics. For the most part, RBC theory has held much less sway amongst policy-makers

In ation Tax and In ation Subsidies: Working Capital in a Cash-in-advance model

In ation Tax and In ation Subsidies: Working Capital in a Cash-in-advance model George T. McCandless March 3, 006 Abstract This paper studies the nature of monetary policy with nancial intermediaries that

In ation Tax and In ation Subsidies: Working Capital in a Cash-in-advance model George T. McCandless March 3, 006 Abstract This paper studies the nature of monetary policy with nancial intermediaries that

A Classical Monetary Model - Money in the Utility Function

A Classical Monetary Model - Money in the Utility Function Jarek Hurnik Department of Economics Lecture III Jarek Hurnik (Department of Economics) Monetary Economics 2012 1 / 24 Basic Facts So far, the

A Classical Monetary Model - Money in the Utility Function Jarek Hurnik Department of Economics Lecture III Jarek Hurnik (Department of Economics) Monetary Economics 2012 1 / 24 Basic Facts So far, the

7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Chapter. Key Concepts

Chapter 7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Key Concepts Aggregate Supply The aggregate production function shows that the quantity of real GDP (Y ) supplied depends on the quantity of labor (L ),

Chapter 7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Key Concepts Aggregate Supply The aggregate production function shows that the quantity of real GDP (Y ) supplied depends on the quantity of labor (L ),

NAME: INTERMEDIATE MICROECONOMIC THEORY SPRING 2008 ECONOMICS 300/010 & 011 Midterm II April 30, 2008

NAME: INTERMEDIATE MICROECONOMIC THEORY SPRING 2008 ECONOMICS 300/010 & 011 Section I: Multiple Choice (4 points each) Identify the choice that best completes the statement or answers the question. 1.

NAME: INTERMEDIATE MICROECONOMIC THEORY SPRING 2008 ECONOMICS 300/010 & 011 Section I: Multiple Choice (4 points each) Identify the choice that best completes the statement or answers the question. 1.

The Budget Deficit, Public Debt and Endogenous Growth

The Budget Deficit, Public Debt and Endogenous Growth Michael Bräuninger October 2002 Abstract This paper analyzes the effects of public debt on endogenous growth in an overlapping generations model. The

The Budget Deficit, Public Debt and Endogenous Growth Michael Bräuninger October 2002 Abstract This paper analyzes the effects of public debt on endogenous growth in an overlapping generations model. The

Unit 4: Measuring GDP and Prices

Unit 4: Measuring GDP and Prices ECO 120 Global Macroeconomics 1 1.1 Reading Reading Module 10 - pages 106-110 Module 11 1.2 Goals Goals Specific Goals: Understand how to measure a country s output. Learn

Unit 4: Measuring GDP and Prices ECO 120 Global Macroeconomics 1 1.1 Reading Reading Module 10 - pages 106-110 Module 11 1.2 Goals Goals Specific Goals: Understand how to measure a country s output. Learn

4. In the Solow model with technological progress, the steady state growth rate of total output is: A) 0. B) g. C) n. D) n + g.

0. B) g. C) n. D) n + g.") 1. The rate of labor augmenting technological progress (g) is the growth rate of: A) labor. B) the efficiency of labor. C) capital. D) output. 2. In the Solow growth model with population growth and technological

1. The rate of labor augmenting technological progress (g) is the growth rate of: A) labor. B) the efficiency of labor. C) capital. D) output. 2. In the Solow growth model with population growth and technological

Advanced Macroeconomics (ECON 402) Lecture 8 Real Business Cycle Theory

Lecture 8 Real Business Cycle Theory") Advanced Macroeconomics (ECON 402) Lecture 8 Real Business Cycle Theory Teng Wah Leo Some Stylized Facts Regarding Economic Fluctuations Having now understood various growth models, we will now delve into

Advanced Macroeconomics (ECON 402) Lecture 8 Real Business Cycle Theory Teng Wah Leo Some Stylized Facts Regarding Economic Fluctuations Having now understood various growth models, we will now delve into

The Cobb-Douglas Production Function

171 10 The Cobb-Douglas Production Function This chapter describes in detail the most famous of all production functions used to represent production processes both in and out of agriculture. First used

171 10 The Cobb-Douglas Production Function This chapter describes in detail the most famous of all production functions used to represent production processes both in and out of agriculture. First used

Microeconomics. Lecture Outline. Claudia Vogel. Winter Term 2009/2010. Part III Market Structure and Competitive Strategy

Microeconomics Claudia Vogel EUV Winter Term 2009/2010 Claudia Vogel (EUV) Microeconomics Winter Term 2009/2010 1 / 25 Lecture Outline Part III Market Structure and Competitive Strategy 12 Monopolistic

Microeconomics Claudia Vogel EUV Winter Term 2009/2010 Claudia Vogel (EUV) Microeconomics Winter Term 2009/2010 1 / 25 Lecture Outline Part III Market Structure and Competitive Strategy 12 Monopolistic

Problem 1. Steady state values for two countries with different savings rates and population growth rates.

Mankiw, Chapter 8. Economic Growth II: Technology, Empirics and Policy Problem 1. Steady state values for two countries with different savings rates and population growth rates. To make the problem more

Mankiw, Chapter 8. Economic Growth II: Technology, Empirics and Policy Problem 1. Steady state values for two countries with different savings rates and population growth rates. To make the problem more

E-322 Muhammad Rahman. Chapter 7: Part 2. Subbing (5) into (2): H b(1. capital is denoted as: 1

into (2): H b(1. capital is denoted as: 1") hapter 7: Part 2 5. Definition of ompetitive Equilibrium ompetitive equilibrium is very easy to derive because: a. There is only one market where the consumption goods are traded for efficiency units of

hapter 7: Part 2 5. Definition of ompetitive Equilibrium ompetitive equilibrium is very easy to derive because: a. There is only one market where the consumption goods are traded for efficiency units of

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Econ 111 Summer 2007 Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The classical dichotomy allows us to explore economic growth

Econ 111 Summer 2007 Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The classical dichotomy allows us to explore economic growth

SAMPLE PAPER II ECONOMICS Class - XII BLUE PRINT

SAMPLE PAPER II ECONOMICS Class - XII Maximum Marks 100 Time : 3 hrs. BLUE PRINT Sl. No. Form of Very Short Short Answer Long Answer Total Questions (1 Mark) (3, 4 Marks) (6 Marks) Content Unit 1 Unit

SAMPLE PAPER II ECONOMICS Class - XII Maximum Marks 100 Time : 3 hrs. BLUE PRINT Sl. No. Form of Very Short Short Answer Long Answer Total Questions (1 Mark) (3, 4 Marks) (6 Marks) Content Unit 1 Unit

Binary Adders: Half Adders and Full Adders

Binary Adders: Half Adders and Full Adders In this set of slides, we present the two basic types of adders: 1. Half adders, and 2. Full adders. Each type of adder functions to add two binary bits. In order

Binary Adders: Half Adders and Full Adders In this set of slides, we present the two basic types of adders: 1. Half adders, and 2. Full adders. Each type of adder functions to add two binary bits. In order

Lecture 2. Marginal Functions, Average Functions, Elasticity, the Marginal Principle, and Constrained Optimization

Lecture 2. Marginal Functions, Average Functions, Elasticity, the Marginal Principle, and Constrained Optimization 2.1. Introduction Suppose that an economic relationship can be described by a real-valued

Lecture 2. Marginal Functions, Average Functions, Elasticity, the Marginal Principle, and Constrained Optimization 2.1. Introduction Suppose that an economic relationship can be described by a real-valued

8. Average product reaches a maximum when labor equals A) 100 B) 200 C) 300 D) 400

100 B) 200 C) 300 D) 400") Ch. 6 1. The production function represents A) the quantity of inputs necessary to produce a given level of output. B) the various recipes for producing a given level of output. C) the minimum amounts

Ch. 6 1. The production function represents A) the quantity of inputs necessary to produce a given level of output. B) the various recipes for producing a given level of output. C) the minimum amounts

The economic determinants of technology shocks in a real business cycle model

Journal of Economic Dynamics & Control 27 (2002) 1 28 www.elsevier.com/locate/econbase The economic determinants of technology shocks in a real business cycle model Klaus Walde ;1 Department of Economics,

Journal of Economic Dynamics & Control 27 (2002) 1 28 www.elsevier.com/locate/econbase The economic determinants of technology shocks in a real business cycle model Klaus Walde ;1 Department of Economics,

Managerial Economics Prof. Trupti Mishra S.J.M. School of Management Indian Institute of Technology, Bombay. Lecture - 13 Consumer Behaviour (Contd )

") (Refer Slide Time: 00:28) Managerial Economics Prof. Trupti Mishra S.J.M. School of Management Indian Institute of Technology, Bombay Lecture - 13 Consumer Behaviour (Contd ) We will continue our discussion

(Refer Slide Time: 00:28) Managerial Economics Prof. Trupti Mishra S.J.M. School of Management Indian Institute of Technology, Bombay Lecture - 13 Consumer Behaviour (Contd ) We will continue our discussion

Common sense, and the model that we have used, suggest that an increase in p means a decrease in demand, but this is not the only possibility.

Lecture 6: Income and Substitution E ects c 2009 Je rey A. Miron Outline 1. Introduction 2. The Substitution E ect 3. The Income E ect 4. The Sign of the Substitution E ect 5. The Total Change in Demand

Lecture 6: Income and Substitution E ects c 2009 Je rey A. Miron Outline 1. Introduction 2. The Substitution E ect 3. The Income E ect 4. The Sign of the Substitution E ect 5. The Total Change in Demand

The Golden Rule. Where investment I is equal to the savings rate s times total production Y: So consumption per worker C/L is equal to:

The Golden Rule Choosing a National Savings Rate What can we say about economic policy and long-run growth? To keep matters simple, let us assume that the government can by proper fiscal and monetary policies

The Golden Rule Choosing a National Savings Rate What can we say about economic policy and long-run growth? To keep matters simple, let us assume that the government can by proper fiscal and monetary policies

1 Monopoly Why Monopolies Arise? Monopoly is a rm that is the sole seller of a product without close substitutes. The fundamental cause of monopoly is barriers to entry: A monopoly remains the only seller

1 Monopoly Why Monopolies Arise? Monopoly is a rm that is the sole seller of a product without close substitutes. The fundamental cause of monopoly is barriers to entry: A monopoly remains the only seller

Microeconomic Theory: Basic Math Concepts

Microeconomic Theory: Basic Math Concepts Matt Van Essen University of Alabama Van Essen (U of A) Basic Math Concepts 1 / 66 Basic Math Concepts In this lecture we will review some basic mathematical concepts

Microeconomic Theory: Basic Math Concepts Matt Van Essen University of Alabama Van Essen (U of A) Basic Math Concepts 1 / 66 Basic Math Concepts In this lecture we will review some basic mathematical concepts

The EU Enlargement, and Immigration from Eastern Europe

The EU Enlargement, and Immigration from Eastern Europe Olivier Blanchard October 2001 Let me start by sketching a toy model of immigration. Think of all the capital as being in the West (Western Europe).

The EU Enlargement, and Immigration from Eastern Europe Olivier Blanchard October 2001 Let me start by sketching a toy model of immigration. Think of all the capital as being in the West (Western Europe).

3 The Standard Real Business Cycle (RBC) Model. Optimal growth model + Labor decisions

Model. Optimal growth model + Labor decisions") Franck Portier TSE Macro II 29-21 Chapter 3 Real Business Cycles 36 3 The Standard Real Business Cycle (RBC) Model Perfectly competitive economy Optimal growth model + Labor decisions 2 types of agents

Franck Portier TSE Macro II 29-21 Chapter 3 Real Business Cycles 36 3 The Standard Real Business Cycle (RBC) Model Perfectly competitive economy Optimal growth model + Labor decisions 2 types of agents

Microeconomics Instructor Miller Practice Problems Labor Market

Microeconomics Instructor Miller Practice Problems Labor Market 1. What is a factor market? A) It is a market where financial instruments are traded. B) It is a market where stocks and bonds are traded.

Microeconomics Instructor Miller Practice Problems Labor Market 1. What is a factor market? A) It is a market where financial instruments are traded. B) It is a market where stocks and bonds are traded.

Profit Maximization. PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University

Profit Maximization PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 The Nature and Behavior of Firms A firm An association of individuals Firms Who have organized themselves

Profit Maximization PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 The Nature and Behavior of Firms A firm An association of individuals Firms Who have organized themselves

To give it a definition, an implicit function of x and y is simply any relationship that takes the form:

2 Implicit function theorems and applications 21 Implicit functions The implicit function theorem is one of the most useful single tools you ll meet this year After a while, it will be second nature to

2 Implicit function theorems and applications 21 Implicit functions The implicit function theorem is one of the most useful single tools you ll meet this year After a while, it will be second nature to

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 11 Perfect Competition - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Perfect competition is an industry with A) a

Chapter 11 Perfect Competition - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Perfect competition is an industry with A) a

Solution to Exercise 7 on Multisource Pollution

Peter J. Wilcoxen Economics 437 The Maxwell School Syracuse University Solution to Exercise 7 on Multisource Pollution 1 Finding the Efficient Amounts of Abatement There are two ways to find the efficient

Peter J. Wilcoxen Economics 437 The Maxwell School Syracuse University Solution to Exercise 7 on Multisource Pollution 1 Finding the Efficient Amounts of Abatement There are two ways to find the efficient

I. Introduction to Aggregate Demand/Aggregate Supply Model

University of California-Davis Economics 1B-Intro to Macro Handout 8 TA: Jason Lee Email: jawlee@ucdavis.edu I. Introduction to Aggregate Demand/Aggregate Supply Model In this chapter we develop a model

University of California-Davis Economics 1B-Intro to Macro Handout 8 TA: Jason Lee Email: jawlee@ucdavis.edu I. Introduction to Aggregate Demand/Aggregate Supply Model In this chapter we develop a model

Two-Period Consumer Model

Two-Period Consumer Model Of the expenditure components in the income-expenditure identity, the largest, by far, is consumption - spending by private households on final goods and services. For 2008, GDP

Two-Period Consumer Model Of the expenditure components in the income-expenditure identity, the largest, by far, is consumption - spending by private households on final goods and services. For 2008, GDP

= C + I + G + NX ECON 302. Lecture 4: Aggregate Expenditures/Keynesian Model: Equilibrium in the Goods Market/Loanable Funds Market

Intermediate Macroeconomics Lecture 4: Introduction to the Goods Market Review of the Aggregate Expenditures model and the Keynesian Cross ECON 302 Professor Yamin Ahmad Components of Aggregate Demand

Intermediate Macroeconomics Lecture 4: Introduction to the Goods Market Review of the Aggregate Expenditures model and the Keynesian Cross ECON 302 Professor Yamin Ahmad Components of Aggregate Demand