Statement of. Donald B. Marron 1 Director, Urban-Brookings Tax Policy Center Before the Senate Committee on Finance

|

|

|

- Cameron Miller

- 7 years ago

- Views:

Transcription

1 Statement of Donald B. Marron 1 Director, Urban-Brookings Tax Policy Center Before the Senate Committee on Finance The Future of Individual Tax Rates: Effects on Economic Growth and Distribution July 14, 2010 Chairman Baucus, Ranking Member Grassley, and Members of the Committee: Thank you for inviting me to appear today to discuss our individual income tax system. As this committee knows well, our nation faces difficult economic and fiscal challenges. In the aftermath of the worst financial crisis since the 1930s, almost 15 million workers are unemployed, about one-tenth of our work force. Almost 7 million of those workers have been unemployed for six months or longer. And millions more lack jobs but don t count in the statistics because they re too discouraged to look for work. Moderate economic growth is expected to lower those figures only gradually over the next few years. At the same time, budget deficits have rocketed to 60-year highs because of the financial crisis, the weak economy, and subsequent policy responses. As a result, the federal debt has grown from about 40 percent of gross domestic product (GDP) at the end of 2008 to about 60 percent of GDP today, the highest since just after World War II. Deficits should narrow in coming years as the economy recovers and as policy responses to the recession wind down. Our long-term fiscal outlook remains daunting, however, because of a fundamental imbalance between spending and revenues. Because of an aging population and rising health care costs, spending is expected to grow significantly faster than revenues over the next 25 years, pushing our nation deeper into debt. Today s discussion of the 2001 and 2003 tax cuts, which are scheduled to expire at the end of the year, thus comes at a challenging time when policymakers confront both nearterm economic weakness and long-term fiscal imbalances. Against that backdrop, my testimony makes six points: 1 My testimony draws heavily on the work of numerous Tax Policy Center colleagues. However, the views expressed are my own and should not be attributed to the Tax Policy Center, the Urban Institute, its board, or its funders. 1

2 1. Tax revenues are remarkably low today, relative to the size of the economy, but are scheduled to increase sharply in coming years. Under current law, revenues from the individual income tax will increase above record levels, relative to the economy, by 2020 and keep rising thereafter. That increase reflects a variety of factors, including the scheduled expiration of the 2001 and 2003 tax cuts, the expansion of the alternative minimum tax (AMT), real bracket creep, demographic changes, the recent health care legislation, and the expected economic rebound. 2. Full extension of the 2001 and 2003 tax cuts and indexation of the AMT would slow the growth of federal revenues substantially relative to the current law baseline. Individual income taxes would rise to a projected 9.2 percent of GDP in 2020, rather than 10.9 percent under current law. Over the 10-year budget window, that reduction would correspond to about $2.9 trillion in forgone revenue. 3. Full extension of the tax cuts and the AMT patch would provide larger tax reductions to higher-income taxpayers. Almost all taxpayers in the top half of the income distribution would receive a tax cut, compared with only a quarter of taxpayers in the bottom quintile. Taxpayers in the top quintile would see their effective tax rate decline by 3.1 percentage points on average; the average cut for the middle quintile would be 1.9 percentage points, and that for the bottom quintile would be 0.6 percentage points. 4. The middle-income tax cuts (rate reductions in the bottom four brackets, marriage penalty relief, and expanded credits) provide significant tax reductions not only to middle-income taxpayers, but also to most higher-income taxpayers. The upper-income tax cuts (rate reductions in the top two brackets and elimination of the phaseouts of personal exemptions and itemized deductions), in contrast, primarily benefit taxpayers in the top 1 percent of the income distribution. 5. The potential economic impact of extending some or all of the tax cuts involves four related issues: stimulus, long-term growth, economic efficiency, and fiscal impacts. Analysts disagree on the degree to which extending the tax cuts would provide stimulus, promote long-term growth, and improve efficiency. Most analysts believe, however, that the economic benefits of extending some or all of the tax cuts will be maximized if we offset the forgone revenue by reducing unproductive spending or raising offsetting revenues in a more efficient manner. 6. Regardless of what happens to the expiring tax cuts, policymakers should look for opportunities to pursue fundamental tax reforms that could simultaneously improve economic performance and, if necessary, raise more revenue. For any future level of government spending, income tax rates could be lower if policymakers take steps to broaden the tax base (by limiting special credits, deductions, and other tax expenditures), introduce a new broad-based consumption tax (e.g., a value-added tax), or rely more on environmental taxes (e.g., a carbon tax). 2

3 The Revenue Outlook It is well known that federal spending is projected to increase rapidly in coming years due to an aging population and rising health care costs. The Congressional Budget Office (CBO) projects, for example, that under current law spending would be 23.5 percent of GDP in 2020 and 27.6 percent of GDP in Federal spending averaged only 20.7 percent of GDP during the four decades from 1970 to Less well known is that federal revenues are also projected to increase rapidly. CBO estimates, for example, that revenues will rise to 20.7 percent of GDP in 2020 and 23.3 percent in 2035 if current law remains in place. To put those figures in context, note that federal revenues have averaged about 18.1 percent of GDP over the past 40 years. Because of the recession and stimulus measures, tax revenues today are remarkably low 14.9 percent of GDP in Indeed, they are the lowest they ve been since But that would quickly reverse under existing law. By 2020, revenues would near their all-time record (20.9 percent of GDP in 1944) and by 2035, revenues would be more than 25 percent higher than historical levels. Much of that increase would come from individual income taxes. CBO projects that under current law they will increase from 6.5 percent of GDP in 2010 to 10.9 percent in 2020 and 13.0 percent in 2035 (figure 1). That growth would take individual income taxes from their lowest level in 60 years, relative to the economy, to well above the record high of 10.2 percent in All figures in this section come from Congressional Budget Office, The Long-Term Budget Outlook, July

4 Revenues from individual income taxes would increase for six reasons. First, the economy will likely recover, lifting revenues from currently depressed levels. Second, both the 2001 and 2003 tax cuts 3 and the tax cuts enacted in the 2009 stimulus are scheduled to expire. Third, the alternative minimum tax, which is not indexed for inflation, will boost taxes for millions more taxpayers. Fourth, retiring baby boomers will make more taxable withdrawals from tax-deferred retirement accounts. Fifth, in a phenomenon known as real bracket creep, growing real (inflation-adjusted) incomes will push taxpayers into higher tax brackets and will reduce their eligibility for various credits, exemptions, and deductions. Finally, the excise tax on Cadillac health plans enacted in the recent health legislation and scheduled to take effect in 2018 will increase the portion of employee compensation that is taken in the form of taxable wages and salaries. Revenues would rise more gradually if Congress permanently extends some or all of the 2001 and 2003 tax cuts and the AMT patch. But individual income tax revenues would still increase faster than the economy because of the other factors. If the tax cuts alone were permanently extended, for example, revenues would rise to 10.0 percent of GDP in 2020 and 12.3 percent in If both the tax cuts and the AMT patch were extended permanently, revenue growth would be slower, with individual revenues rising to 9.2 percent of GDP in 2020 and 10.3 percent in CBO s projections indicate that permanent extension of the 2001 and 2003 individual income tax cuts alone would reduce revenues by about $1.7 trillion over the 10-year budget window ( ). Permanent extension with an AMT patch would reduce revenues by about $2.9 trillion. 4 As these figures demonstrate, there is an important interaction between the tax cuts and the AMT. The revenue cost of extending the tax cuts, by themselves, is moderated by the fact that an increasing number of taxpayers would be pushed onto the AMT. The revenue cost would be much larger if both the tax cuts and the AMT patch were permanently extended. The Tax Cuts The 2001 and 2003 tax laws made numerous changes to individual income taxes. 5 Expiring at the end of the year are those that 3 These two laws were the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) and the Jobs and Growth Tax Relief Reconciliation Act of 2003 (JGTRRA). 4 Throughout this testimony, I use current law as the baseline for measuring policy impacts. I thus treat as a tax cut any policies that extend some or all of the 2001 and 2003 tax provisions. Another approach would be to treat current policy the tax law that applies in 2010 as the baseline. Under that approach, allowing any of the 2001 and 2003 tax cuts to expire would amount to a tax increase. The figures in this testimony can be recast in those terms with an appropriate sign change. For example, if current policy is the baseline, then allowing all the tax cuts and the AMT patch to expire would amount to a $2.9 trillion tax increase over the budget window. 5 The 2001 law also reduced estate taxes expanding exemptions and lowering rates leading to full repeal (as of this writing) in Those changes are outside the scope of this testimony. 4

5 Lowered rates on ordinary income. The 28, 31, 36, and 39.6 percent tax rates were reduced to 25, 28, 33, and 35 percent, respectively. In addition, a new 10 percent tax bracket was carved out of the 15 percent bracket. Reduced the marriage penalty. The standard deduction and the width of the 15 percent tax bracket for married couples filing jointly were both increased to be twice those for single filers; they had previously been only 1.67 times as large. Reduced tax rates on capital gains and dividends. The tax rate on long-term capital gains was reduced from 10 to 0 percent for taxpayers in the 15 percent bracket and below and from 20 to 15 percent for filers in higher tax brackets. The tax rate on qualified dividends was lowered from ordinary tax rates to the lower long-term capital gains rates. Increased the child credit. The credit doubled from $500 to $1,000 per child and eligibility for refundable credits expanded. Increased other credits. The maximum child and dependent care credit increased, and the phaseout range for the earned income tax credit for married couples expanded, boosting the value of the credit for some families. Eliminated the phaseout of personal exemptions and limitation on itemized deductions that occur at high incomes. Those provisions are known as PEP and Pease (after the congressman who proposed the latter), respectively. Expanded tax incentives for education. The 2001 and 2003 laws also temporarily increased the exemption level for the AMT. A series of subsequent laws increased the exemption level through the end of The Distributional Effects of Extending the Individual Income Tax Cuts Individual income taxes are the single largest source of federal revenues. Other important sources include payroll taxes, corporate income taxes, and estate taxes. Under current law, the revenues from these federal taxes would average 23.5 percent of taxpayers cash income in 2012 (table 1). If the individual income tax cuts that originated in 2001 and 2003 were extended, along with the AMT patch, federal taxes would average 20.9 percent of cash income in Extending the individual income tax cuts would thus reduce the average tax rate by 2.6 percentage points or about 11 percent. 6 If all the 2001 and 2003 individual income tax cuts and the AMT patch were extended, nearly three-quarters of taxpayers would receive a tax cut compared with current law, but that likelihood varies with income. Only a quarter of taxpayers in the bottom quintile 6 As noted earlier, this analysis ignores any extension or reform of the estate tax. For purposes of calculating the figures in table 1, we have assumed that the estate tax remains at its 2009 level. 5

6 would receive a tax cut, while 99 percent of taxpayers in the top two quintiles would. 7 A key reason for this disparity is that many low-income taxpayers already have little or no income tax liability. 8 Some low-income taxpayers with no tax liability would nevertheless benefit from extending the increases in the refundable child credit and earned income credit that began with the 2001 law. The reductions in average tax rates show a similar pattern. The average tax rate would fall by 0.6 percentage points for taxpayers in the bottom quintile, but by 3.1 percentage points in the top quintile. That difference is primarily driven by the fact that so few taxpayers in the bottom quintile would receive a tax cut. Among those who would receive a tax cut, the differential still exists, but is smaller: an average tax cut of 2.3 percentage points for taxpayers in the bottom quintile who receive a tax cut versus 3.1 percentage points in the top. The size of the tax cut also varies significantly within the top quintile. 7 The appendix provides similar information by cash income level rather than income quintiles. 8 Roberton Williams, Why Nearly Half of Americans Pay No Federal Income Tax, Tax Notes, June 7, The share that pays no income tax will decline as the economy recovers and the temporary stimulus tax cuts, especially the Making Work Pay Credit, expire. 6

7 The average tax rate in the 80th to 95th income percentiles would fall by 2.8 percentage points, while the average tax rate in the top 1 percent would fall by 3.9 percentage points. In dollar terms, the largest tax reductions would go to taxpayers with the highest incomes and the highest tax burdens. Bottom-quintile taxpayers would receive an average cut of about $70 (a 0.6 percent increase in after-tax income), middle-quintile taxpayers about $970 (a 2.3 percent increase), and top-quintile taxpayers about $8,700 (a 4.3 percent increase). But, because current law tax rates increase with income, the tax cut as a share of taxes paid would be largest in the second quintile of the income distribution. As a result, those in the second quintile of taxpayers would pay a slightly smaller share of income taxes than they pay under current law, while the top three quintiles would pay a slightly larger share of federal taxes. Table 2 shows how the various provisions in the tax laws combine to reduce average effective tax rates. In interpreting these figures, keep in mind that the provisions interact with one another; as a result, the order in which the provisions are analyzed matters. In this case, the analysis proceeds from left to right. Starting with current law, the table first considers an AMT patch, 9 followed by the changes that benefit lower- and middleincome taxpayers as well as high-income ones (the 10 percent bracket and the 25 and 28 percent rates, marriage penalty relief, expansion of the child credit and credits for child 9 The most recent patch applied to The analysis assumes that Congress extends that patch with the exemption amount, rate bracket threshold, and exemption phaseout all indexed to inflation. 7

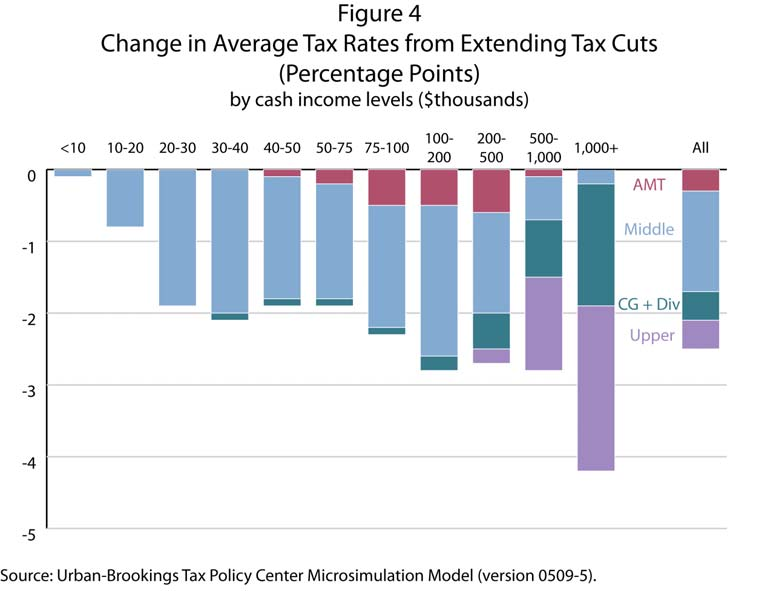

8 and dependent care and for education), and the changes that primarily benefit highincome taxpayers (lower rates on qualified dividends and long-term capital gains, eliminating PEP and Pease, and extending the top marginal rates of 33 and 35 percent). As one example of the potential interactions, the AMT patch would appear to have a larger effect if it came at the end of the stacking order rather than at the beginning, as in table 2. If the AMT patch came at the end, the reductions in the regular income tax would push more people onto the AMT. The effect of patching the AMT would then be larger, and the effect of the other tax cuts would be correspondingly smaller. The provision-by-provision changes cumulate to the total changes shown in table 1. For example, the 2.0 percentage point reduction in the average tax rate for the second quintile is explained by the reduction of tax rates in the lower brackets (0.9 percentage point), marriage penalty relief (0.2 percentage points), and the expansion of credits (0.9 percentage points). As the table demonstrates, several provisions often considered middle-income tax relief also provide benefits to taxpayers high in the income distribution. The rate reductions in the lower brackets, for example, reduce average tax rates by about a percentage point for taxpayers not only in the middle three quintiles of the income distribution, but in the top quintile. Marriage penalty relief similarly provides a sizable tax reduction in the top quintile. In contrast, the impacts of the provisions that are considered high-income tax relief are concentrated at high incomes. Eliminating PEP and Pease, for example, benefits taxpayers in the top 5 percent of the income distribution, while extending the two top marginal rate reductions primarily benefits the top 1 percent. To illustrate these differences, figures 2 and 3 condense the tax cuts into four groups: the AMT patch, the middle-income tax cuts (the lower brackets, marriage penalty relief, and expanded credits), the dividend and capital gains rate reductions, and the upperincome tax cuts (the two highest brackets and the elimination of PEP and Pease). Figure 2 shows the results by quintile, and figure 3 shows greater detail within the top quintile. 8

9 9

10 As these figures illustrate, the middle-income tax cuts (in blue) account for most of the tax reductions for taxpayers up to the 95th percentile of income and about half of the reductions in the 95th to 99th percentiles. The upper-income tax cuts (purple) and the rate reductions for capital gains and dividends (green) account for nearly all of the tax reductions for the top 1 percent of taxpayers. Economic Growth In considering the potential economic impacts of the tax cuts, policymakers should consider four related issues: whether extending them would provide helpful stimulus at a time of economic weakness; whether they would encourage long-run economic growth; whether they would reduce inefficiencies created by the tax system; and whether and how the resulting revenue reductions would be paid for. Stimulus. The U.S. economy clearly remains fragile. Although the overall economy has been growing for a year, the unemployment rate remains near 10 percent, and when one factors in the number of workers who are discouraged or cannot find full-time work, the underemployment rate is about 16 percent. History suggests that it takes a long time for economies to heal after financial crises, 10 and the recent crisis was particularly severe. As a result, most forecasters expect that it will take at least several years for the unemployment rate to decline to levels consistent with full employment. Given that outlook, it is reasonable to ask whether extending the tax cuts would provide near-term stimulus for the economy or, equivalently, would prevent any anti-stimulus that would occur from their expiration. The short answer to that question is clearly yes: extending the tax cuts would provide some demand-side stimulus to the economy. But that conclusion comes with several caveats. First, the amount of stimulus varies across the different tax provisions. All else equal, the cuts that go to middle- and lowincome taxpayers are likely to provide more demand-side stimulus in the near term, because they are less likely to be saved. Second, only some of the stimulus would show up in 2011, when it is presumably most beneficial. The remainder would show up in the first few months of 2012, when families file their tax returns and most receive tax refunds. When CBO examined this issue earlier in the year, it concluded that extending the tax cuts would provide some stimulus in 2011, but significantly less, on a bang-per-buck basis, than other options, such as extended unemployment benefits. 11 Third, the amount of stimulus would be greater if the tax cuts were extended on a permanent basis, rather than just for a year or two. Families would spend more of their 10 See, for example, Carmen M. Reinhart and Kenneth Rogoff, This Time Is Different: Eight Centuries of Financial Folly (Princeton University Press, 2009). 11 Congressional Budget Office, Policies for Increasing Economic Growth and Employment in 2010 and 2011, January

11 reduction if they believed it to be permanent. Moreover, permanent reductions in the tax rates on dividends and capital gains could lift the value of stocks and other assets, providing a wealth boost to consumer spending. Both of those effects would increase the demand-side stimulus from an extension. In addition, the potential supply-side responses would be enhanced if the tax cuts were perceived to be permanent. That additional stimulus would, of course, require a much larger reduction in future revenues (relative to the rising path implied by current law) than would a temporary reduction. Long-term growth. Over the long run, the key economic issue is whether extending the tax cuts would encourage work, saving, and investment and thereby boost economic growth. Such supply-side effects would primarily result from reductions in marginal tax rates on wages, salaries, investment income, and business income. Analysts disagree on the extent to which extending the tax cuts would have such beneficial effects on growth. On one hand, extending the tax cuts would indeed reduce marginal tax rates; those reductions would encourage work and investment. 12 On the other hand, many of the provisions do not reduce marginal tax rates (e.g., the increase in the child tax credit). All else equal, extending those provisions would tend to weaken supply-side incentives. The potential economic gains from extending the tax cuts would also be offset, at least in part, by the resulting increase in deficits and debt. Over time, deficits crowd out private-sector investment and thus reduce the productive capacity of the economy. For tax cuts to boost long-run growth, their positive supply-side effects would have to be large enough to overcome the drag from crowding out. Efficiency. A related issue is whether the tax cuts would improve economic efficiency. Our current tax system creates many undesirable distortions in economic activity. The deduction for mortgage interest, for example, encourages homeowners to take on larger mortgages. The exclusion for employer-provided health insurance encourages excessively broad insurance plans. The taxes on dividends and capital gains encourage businesses to finance themselves with debt rather than equity and to avoid corporate form, and the favorable treatment of capital gains relative to dividends encourages them to hoard cash rather than distribute it to shareholders. Higher marginal tax rates amplify all of these distortions. Fiscal impacts. Finally, there is the issue of whether and how any extension would be paid for. Given the revenue increases that will occur under existing law even if the tax cuts are extended (as noted in figure 1), some analysts argue that the tax cuts should be extended without offsets. Given the current imbalance in our budget, that is effectively arguing that unspecified future spending reductions or revenue increases would have to bridge the gap or that the United States should run up its debt even more quickly. But that latter course would eventually undermine private investment and weaken economic growth. For that reason, most analysts believe that the potential long-run economic 12 For one recent analysis, see Congressional Budget Office, An Analysis of the President s Budgetary Proposals for Fiscal Year 2011, March

12 benefits of a permanent extension would be maximized if policymakers offset the resulting deficit increases by spending reductions or less-distortionary tax increases. Some analysts have also argued that a temporary one- or two-year extension, without any offsets, would be appropriate to provide stimulus to our weak economy. Given extremely low borrowing rates (the 10-year Treasury rate is currently about 3 percent), the costs of financing the resulting increase in debt would likely not be a major immediate problem, but the additional borrowing would, of course, add to the debt burden in coming years. However, another strategy for near-term stimulus would be to pair a temporary extension of most or all of the tax cuts with offsetting spending reductions or revenue increases several years in the future. Most analysts believe that this approach would provide the greatest economic benefit, since it would combine short-term economic stimulus with a commitment to greater fiscal responsibility in the future. The Need for Fundamental Tax Reform As a closing note, I should emphasize that our current tax system is already highly inefficient and will not scale well if there are higher revenue demands in the future. Regardless of any near-term decisions they make about extending the tax cuts, policymakers should also begin to consider more fundamental reforms. In principle, there are substantial opportunities to reduce the economic burdens created by our tax system while raising the same or more revenue. One option would be to limit the numerous special credits, exclusions, and deductions that narrow our income tax base. Reducing such tax expenditures would allow for the economic benefits of lower rates and reduced distortions from the tax system. A second option would be to introduce a new, broad-based tax on consumption, such as a value-added tax, rather than to increase moredistortionary income taxes. Finally, the nation could raise additional revenue by taxing behaviors we want to discourage such as carbon emissions rather than behaviors that we would prefer to encourage such as working, saving, and investing For a longer discussion of the role of revenue options in addressing our fiscal challenges, see Donald B. Marron, America in the Red, National Affairs, March

13 Appendix: Distributional Analysis by Cash Income Level 13

14 14

Congressional Budget Office s Preliminary Analysis of President Obama s Fiscal Year 2012 Budget

Congressional Budget Office s Preliminary Analysis of President Obama s Fiscal Year 2012 Budget SUMMARY The Congressional Budget Office s (CBO) Preliminary Analysis of the President s FY 2012 Budget released

Congressional Budget Office s Preliminary Analysis of President Obama s Fiscal Year 2012 Budget SUMMARY The Congressional Budget Office s (CBO) Preliminary Analysis of the President s FY 2012 Budget released

United States General Accounting Office. Testimony Before the Committee on Finance, United States Senate

GAO United States General Accounting Office Testimony Before the Committee on Finance, United States Senate For Release on Delivery Expected at 10:00 a.m. EST on Thursday March 8, 2001 ALTERNATIVE MINIMUM

GAO United States General Accounting Office Testimony Before the Committee on Finance, United States Senate For Release on Delivery Expected at 10:00 a.m. EST on Thursday March 8, 2001 ALTERNATIVE MINIMUM

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE CBO. The Distribution of Household Income and Federal Taxes, 2008 and 2009

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Percent 70 The Distribution of Household Income and Federal Taxes, 2008 and 2009 60 50 Before-Tax Income Federal Taxes Top 1 Percent 40 30 20 81st

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Percent 70 The Distribution of Household Income and Federal Taxes, 2008 and 2009 60 50 Before-Tax Income Federal Taxes Top 1 Percent 40 30 20 81st

Reducing the Deficit by Increasing Individual Income Tax Rates

Reducing the Deficit by Increasing Individual Income Tax Rates Eric Toder, Jim Nunns, and Joseph Rosenberg March 2012 The authors are all affiliated with the Urban-Brookings Tax Policy Center. Toder is

Reducing the Deficit by Increasing Individual Income Tax Rates Eric Toder, Jim Nunns, and Joseph Rosenberg March 2012 The authors are all affiliated with the Urban-Brookings Tax Policy Center. Toder is

EXTENDING EXPIRING TAX CUTS AND AMT RELIEF WOULD COST $3.3 TRILLION THROUGH 2016 By Joel Friedman and Aviva Aron-Dine

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised March 15, 2006 EXTENDING EXPIRING TAX CUTS AND AMT RELIEF WOULD COST $3.3 TRILLION

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised March 15, 2006 EXTENDING EXPIRING TAX CUTS AND AMT RELIEF WOULD COST $3.3 TRILLION

EXTENDING THE PRESIDENT S TAX CUTS AND AMT RELIEF WOULD COST $4.4 TRILLION THROUGH 2018 By Aviva Aron-Dine

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised March 28, 2008 EXTENDING THE PRESIDENT S TAX CUTS AND AMT RELIEF WOULD COST

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised March 28, 2008 EXTENDING THE PRESIDENT S TAX CUTS AND AMT RELIEF WOULD COST

Note: This feature provides supplementary analysis for the material in Part 3 of Common Sense Economics.

1 Module C: Fiscal Policy and Budget Deficits Note: This feature provides supplementary analysis for the material in Part 3 of Common Sense Economics. Fiscal and monetary policies are the two major tools

1 Module C: Fiscal Policy and Budget Deficits Note: This feature provides supplementary analysis for the material in Part 3 of Common Sense Economics. Fiscal and monetary policies are the two major tools

The Bush Tax Cuts and the Economy

Thomas L. Hungerford Specialist in Public Finance September 3, 2010 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress 7-5700 www.crs.gov R41393 Summary

Thomas L. Hungerford Specialist in Public Finance September 3, 2010 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress 7-5700 www.crs.gov R41393 Summary

Q&A on tax relief for individuals & families

Q&A on tax relief for individuals & families A. Tax cuts individuals What are the new tax rates? The table below shows the new tax rates being rolled out from 1 October 2008, 1 April 2010 and 1 April 2011,

Q&A on tax relief for individuals & families A. Tax cuts individuals What are the new tax rates? The table below shows the new tax rates being rolled out from 1 October 2008, 1 April 2010 and 1 April 2011,

Highlights of the 2010 Tax Relief Act

On December 7, 200, President Barack Obama signed into law H.R. 4853, the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 200 (the 200 Tax Relief Act). This massive bill affects

On December 7, 200, President Barack Obama signed into law H.R. 4853, the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 200 (the 200 Tax Relief Act). This massive bill affects

TAX PROVISIONS IN THE AMERICAN TAXPAYER RELIEF ACT OF 2012 (ATRA) James Nunns and Jeffrey Rohaly Urban-Brookings Tax Policy Center January 9, 2013

James Nunns and Jeffrey Rohaly Urban-Brookings Tax Policy Center January 9, 2013") TAX PROVISIONS IN THE AMERICAN TAXPAYER RELIEF ACT OF 2012 (ATRA) James Nunns and Jeffrey Rohaly Urban-Brookings Tax Policy Center January 9, 2013 ABSTRACT The fiscal cliff debate culminated in the passage

TAX PROVISIONS IN THE AMERICAN TAXPAYER RELIEF ACT OF 2012 (ATRA) James Nunns and Jeffrey Rohaly Urban-Brookings Tax Policy Center January 9, 2013 ABSTRACT The fiscal cliff debate culminated in the passage

Client Letter: Individual Tax Provisions of the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010

Source: Tax Legislation > 111th Congress (2009-2010) > Enacted > Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (P.L. 111-312) > Practice Tools > Client Letter: Individual

Source: Tax Legislation > 111th Congress (2009-2010) > Enacted > Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (P.L. 111-312) > Practice Tools > Client Letter: Individual

Capital Gains Taxes: An Overview

Order Code 96-769 Updated January 24, 2007 Summary Capital Gains Taxes: An Overview Jane G. Gravelle Senior Specialist in Economic Policy Government and Finance Division Tax legislation in 1997 reduced

Order Code 96-769 Updated January 24, 2007 Summary Capital Gains Taxes: An Overview Jane G. Gravelle Senior Specialist in Economic Policy Government and Finance Division Tax legislation in 1997 reduced

Analysis of 2012 Federal Tax Reform, Part One: Proposed Federal Tax Plans Vary on Tax Equity

Analysis of 2012 Federal Tax Reform, Part One: Proposed Federal Tax Plans Vary on Tax Equity ISSUE BRIEF July 9, 2012 Ali Mickelson Tax Policy Analyst 789 Sherman St. Suite 300 Denver, CO 80203 www.cclponline.org

Analysis of 2012 Federal Tax Reform, Part One: Proposed Federal Tax Plans Vary on Tax Equity ISSUE BRIEF July 9, 2012 Ali Mickelson Tax Policy Analyst 789 Sherman St. Suite 300 Denver, CO 80203 www.cclponline.org

National Small Business Network

National Small Business Network WRITTEN STATEMENT FOR THE RECORD US SENATE COMMITTEE ON FINANCE U.S. HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS JOINT HEARING ON TAX REFORM AND THE TAX TREATMENT

National Small Business Network WRITTEN STATEMENT FOR THE RECORD US SENATE COMMITTEE ON FINANCE U.S. HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS JOINT HEARING ON TAX REFORM AND THE TAX TREATMENT

COST OF TAX CUT WOULD MORE THAN DOUBLE TO $5 TRILLION IN SECOND TEN YEARS. Tax Cut Would Worsen Deteriorating Long-Term Budget Forecast

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org http://www.cbpp.org Revised April 4, 2001 COST OF TAX CUT WOULD MORE THAN DOUBLE TO $5 TRILLION

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org http://www.cbpp.org Revised April 4, 2001 COST OF TAX CUT WOULD MORE THAN DOUBLE TO $5 TRILLION

CRS Report for Congress Received through the CRS Web

Order Code RS21992 Updated November 25, 2005 CRS Report for Congress Received through the CRS Web Extending the 2001, 2003, and 2004 Tax Cuts Summary Gregg Esenwein Specialist in Public Finance Government

Order Code RS21992 Updated November 25, 2005 CRS Report for Congress Received through the CRS Web Extending the 2001, 2003, and 2004 Tax Cuts Summary Gregg Esenwein Specialist in Public Finance Government

An Overview of The Tax Relief Act on 2010

An Overview of The Tax Relief Act on 2010 On December 17, 2010, the President signed a multi-billion dollar tax cut package, the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act

An Overview of The Tax Relief Act on 2010 On December 17, 2010, the President signed a multi-billion dollar tax cut package, the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act

Details and Analysis of Senator Bernie Sanders s Tax Plan

FISCAL FACT Jan. 2016 No. 498 Details and Analysis of Senator Bernie Sanders s Tax Plan By Alan Cole and Scott Greenberg Economist Analyst Key Findings: Senator Sanders (I-VT) would enact a number of policies

FISCAL FACT Jan. 2016 No. 498 Details and Analysis of Senator Bernie Sanders s Tax Plan By Alan Cole and Scott Greenberg Economist Analyst Key Findings: Senator Sanders (I-VT) would enact a number of policies

THE GRADUATED PERSONAL INCOME TAX ASSESSMENT: FREQUENTLY ASKED QUESTIONS

LEGISLATIVE REVENUE OFFICE State Capitol Building 900 Court St. NE, Room H-197 Salem, Oregon 97301 Research Brief (503) 986-1266 FAX (503) 986-1770 http://www.leg.state.or.us/comm/lro/home.htm Number 3-03

LEGISLATIVE REVENUE OFFICE State Capitol Building 900 Court St. NE, Room H-197 Salem, Oregon 97301 Research Brief (503) 986-1266 FAX (503) 986-1770 http://www.leg.state.or.us/comm/lro/home.htm Number 3-03

Tax Relief in 2001 through 2011

in 2001 through 2011 Department of the Treasury May 2008 in 2001 through 2011 The tax relief enacted during the President s term in office, principally in the Economic Growth and Relief Reconciliation

in 2001 through 2011 Department of the Treasury May 2008 in 2001 through 2011 The tax relief enacted during the President s term in office, principally in the Economic Growth and Relief Reconciliation

SELECTED PROVISIONS OF MAJOR TAX LEGISLATION BY ACT 1981 to 2006 PROVISION ERTA 1981 TRA 1986 OBRA 1989 OBRA 1990 OBRA 1993 TRA 1997 EGTRRA 2001

SELECTED PROVISIONS OF MAJOR TAX LEGISLATION BY ACT 1981 to 2006 PROVISION ERTA 1981 TRA 1986 OBRA 1989 OBRA 1990 OBRA 1993 TRA 1997 EGTRRA 2001 Tax Rates Reduced marginal tax rates by 23% over 3 years,

SELECTED PROVISIONS OF MAJOR TAX LEGISLATION BY ACT 1981 to 2006 PROVISION ERTA 1981 TRA 1986 OBRA 1989 OBRA 1990 OBRA 1993 TRA 1997 EGTRRA 2001 Tax Rates Reduced marginal tax rates by 23% over 3 years,

The 2001 and 2003 Tax Relief: The Benefit of Lower Tax Rates

FISCAL Au 2008 No. 141 FACT The 2001 and 2003 Tax Relief: The Benefit of Lower Tax Rates By Robert Carroll Summary Recent research on President Bush's tax relief in 2001 and 2003 has found that the lower

FISCAL Au 2008 No. 141 FACT The 2001 and 2003 Tax Relief: The Benefit of Lower Tax Rates By Robert Carroll Summary Recent research on President Bush's tax relief in 2001 and 2003 has found that the lower

Overview of the Federal Tax System

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 1-23-2014 Overview of the Federal Tax System Molly F. Sherlock Congressional Research Service Donald J. Marples

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 1-23-2014 Overview of the Federal Tax System Molly F. Sherlock Congressional Research Service Donald J. Marples

MACROECONOMIC ANALYSIS OF VARIOUS PROPOSALS TO PROVIDE $500 BILLION IN TAX RELIEF

MACROECONOMIC ANALYSIS OF VARIOUS PROPOSALS TO PROVIDE $500 BILLION IN TAX RELIEF Prepared by the Staff of the JOINT COMMITTEE ON TAXATION March 1, 2005 JCX-4-05 CONTENTS INTRODUCTION... 1 EXECUTIVE SUMMARY...

MACROECONOMIC ANALYSIS OF VARIOUS PROPOSALS TO PROVIDE $500 BILLION IN TAX RELIEF Prepared by the Staff of the JOINT COMMITTEE ON TAXATION March 1, 2005 JCX-4-05 CONTENTS INTRODUCTION... 1 EXECUTIVE SUMMARY...

Post Election Focus: Stars, Stripes & Taxes

Post Election Focus: Stars, Stripes & Taxes Presented By: Margo Cook, CPA December 6, 2012 Click HERE to listen to webinar. Post Election Focus: Stars, Stripes & Taxes Presented By: Margo Cook, CPA December

Post Election Focus: Stars, Stripes & Taxes Presented By: Margo Cook, CPA December 6, 2012 Click HERE to listen to webinar. Post Election Focus: Stars, Stripes & Taxes Presented By: Margo Cook, CPA December

Crunch or Crucible? Upcoming Changes in the Federal Tax Law A Special Edition Tax Guide for Friends and Alumni of Pomona College

Upcoming Changes in the Federal Tax Law A Special Edition Tax Guide for Friends and Alumni of Pomona College Pomona College, Office of Trusts & Estates, 550 N. College Ave., Claremont, CA 91711 www.pomona.planyourlegacy.org

Upcoming Changes in the Federal Tax Law A Special Edition Tax Guide for Friends and Alumni of Pomona College Pomona College, Office of Trusts & Estates, 550 N. College Ave., Claremont, CA 91711 www.pomona.planyourlegacy.org

AN ANALYSIS OF DONALD TRUMP S TAX PLAN

AN ANALYSIS OF DONALD TRUMP S TAX PLAN Jim Nunns, Len Burman, Jeff Rohaly, and Joe Rosenberg December 22, 2015 ABSTRACT This paper analyzes presidential candidate Donald Trump s tax proposal. His plan

AN ANALYSIS OF DONALD TRUMP S TAX PLAN Jim Nunns, Len Burman, Jeff Rohaly, and Joe Rosenberg December 22, 2015 ABSTRACT This paper analyzes presidential candidate Donald Trump s tax proposal. His plan

Client Letter: Individual Tax Provisions of the American Taxpayer Relief Act of 2012

Client Letter: Individual Tax Provisions of the American Taxpayer Relief Act of 2012 Dear Client, On January 2, 2013, President Obama signed the American Taxpayer Relief Act of 2012 (the Act) into law.

Client Letter: Individual Tax Provisions of the American Taxpayer Relief Act of 2012 Dear Client, On January 2, 2013, President Obama signed the American Taxpayer Relief Act of 2012 (the Act) into law.

Average Federal Income Tax Rates for Median-Income Four-Person Families

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org http://www.cbpp.org April 10, 2002 OVERALL FEDERAL TAX BURDEN ON MOST FAMILIES INCLUDING MIDDLE-

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org http://www.cbpp.org April 10, 2002 OVERALL FEDERAL TAX BURDEN ON MOST FAMILIES INCLUDING MIDDLE-

News Release Date: 1/8/13

News Release Date: 1/8/13 American Taxpayer Relief Act of 2012 Cross References H.R. 8, the American Taxpayer Relief Act of 2012 TheTaxBook, 2012 Tax Year, 1040 Edition/Deluxe Edition, pages 1-6 and 1-7.

News Release Date: 1/8/13 American Taxpayer Relief Act of 2012 Cross References H.R. 8, the American Taxpayer Relief Act of 2012 TheTaxBook, 2012 Tax Year, 1040 Edition/Deluxe Edition, pages 1-6 and 1-7.

Tax Reform: An Overview of Proposals in the 112 th Congress

Tax Reform: An Overview of Proposals in the 112 th Congress James M. Bickley Specialist in Public Finance January 14, 2011 Congressional Research Service CRS Report for Congress Prepared for Members and

Tax Reform: An Overview of Proposals in the 112 th Congress James M. Bickley Specialist in Public Finance January 14, 2011 Congressional Research Service CRS Report for Congress Prepared for Members and

tax planning strategies

tax planning strategies In addition to saving income taxes for the current and future years, effective tax planning can reduce eventual estate taxes, maximize the amount of funds you will have available

tax planning strategies In addition to saving income taxes for the current and future years, effective tax planning can reduce eventual estate taxes, maximize the amount of funds you will have available

Economic Effects of Reducing the Fiscal Restraint That Is Scheduled to Occur in 2013

MAY 2012 Economic Effects of Reducing the Fiscal Restraint That Is Scheduled to Occur in 2013 If the fiscal policies currently in place are continued in coming years, the revenues collected by the federal

MAY 2012 Economic Effects of Reducing the Fiscal Restraint That Is Scheduled to Occur in 2013 If the fiscal policies currently in place are continued in coming years, the revenues collected by the federal

GAO PATIENT PROTECTION AND AFFORDABLE CARE ACT. Effect on Long-Term Federal Budget Outlook Largely Depends on Whether Cost Containment Sustained

GAO United States Government Accountability Office Report to the Ranking Member, Committee on the Budget, U.S. Senate January 2013 PATIENT PROTECTION AND AFFORDABLE CARE ACT Effect on Long-Term Federal

GAO United States Government Accountability Office Report to the Ranking Member, Committee on the Budget, U.S. Senate January 2013 PATIENT PROTECTION AND AFFORDABLE CARE ACT Effect on Long-Term Federal

Higher Education Tax Benefits: Brief Overview and Budgetary Effects

Higher Education Tax Benefits: Brief Overview and Budgetary Effects Margot L. Crandall-Hollick Analyst in Public Finance Mark P. Keightley Analyst in Public Finance August 24, 2011 CRS Report for Congress

Higher Education Tax Benefits: Brief Overview and Budgetary Effects Margot L. Crandall-Hollick Analyst in Public Finance Mark P. Keightley Analyst in Public Finance August 24, 2011 CRS Report for Congress

Cutting Tax Preferences Is Key to Tax Reform and Deficit Reduction

Cutting Tax Preferences Is Key to Tax Reform and Deficit Reduction Donald B. Marron Director, Urban-Brookings Tax Policy Center www.taxpolicycenter.org Testimony before the Senate Committee on the Budget

Cutting Tax Preferences Is Key to Tax Reform and Deficit Reduction Donald B. Marron Director, Urban-Brookings Tax Policy Center www.taxpolicycenter.org Testimony before the Senate Committee on the Budget

INCOME TAX REFORM. What Does It Mean for Taxpayers?

BRIEFING PAPER INCOME TAX REFORM What Does It Mean for Taxpayers? Office of Legislative Research and General Counsel DECEMBER 2006 UTAH LEGISLATURE HIGHLIGHTS SB 4001, passed in the 2006 4th Special Session,

BRIEFING PAPER INCOME TAX REFORM What Does It Mean for Taxpayers? Office of Legislative Research and General Counsel DECEMBER 2006 UTAH LEGISLATURE HIGHLIGHTS SB 4001, passed in the 2006 4th Special Session,

A Dynamic Analysis of President Obama s Tax Initiatives

FISCAL FACT Mar. 2015 No. 455 A Dynamic Analysis of President Obama s Tax Initiatives By Stephen J. Entin Senior Fellow Executive Summary President Obama proposed a long list of changes to the tax system

FISCAL FACT Mar. 2015 No. 455 A Dynamic Analysis of President Obama s Tax Initiatives By Stephen J. Entin Senior Fellow Executive Summary President Obama proposed a long list of changes to the tax system

TAX RELIEF ACT UPDATED DECEMBER 29, 2010

2010 TAX RELIEF ACT UPDATED DECEMBER 29, 2010 TAX RELIEF, UNEMPLOYMENT INSURANCE RE-AUTHORIZATION, AND JOB CREATION ACT OF 2010 INTRODUCTION On December 17, 2010, President Obama signed the much-anticipated

2010 TAX RELIEF ACT UPDATED DECEMBER 29, 2010 TAX RELIEF, UNEMPLOYMENT INSURANCE RE-AUTHORIZATION, AND JOB CREATION ACT OF 2010 INTRODUCTION On December 17, 2010, President Obama signed the much-anticipated

Supplemental Unit 5: Fiscal Policy and Budget Deficits

1 Supplemental Unit 5: Fiscal Policy and Budget Deficits Fiscal and monetary policies are the two major tools available to policy makers to alter total demand, output, and employment. This feature will

1 Supplemental Unit 5: Fiscal Policy and Budget Deficits Fiscal and monetary policies are the two major tools available to policy makers to alter total demand, output, and employment. This feature will

TAX PRESIDENT-ELECT OBAMA S TAX PROPOSALS: A FORECAST

alert TAX NOVEMBER 2008 PUBLISHED BY THE EMERGING TAX ISSUES COMMITTEE CCH Tax Briefing: PRESIDENT-ELECT OBAMA S TAX PROPOSALS: A FORECAST President-Elect Brings Ambitious Tax Policy Agenda To Washington

alert TAX NOVEMBER 2008 PUBLISHED BY THE EMERGING TAX ISSUES COMMITTEE CCH Tax Briefing: PRESIDENT-ELECT OBAMA S TAX PROPOSALS: A FORECAST President-Elect Brings Ambitious Tax Policy Agenda To Washington

Obama Tax Compromise APPROVED by Congress

December 17, 2010 Obama Tax Compromise APPROVED by Congress on Thursday, December 16, 2010 The $858 billion tax deal negotiated by President Obama and Republican leadership was overwhelmingly approved

December 17, 2010 Obama Tax Compromise APPROVED by Congress on Thursday, December 16, 2010 The $858 billion tax deal negotiated by President Obama and Republican leadership was overwhelmingly approved

The Case for a Tax Cut

The Case for a Tax Cut Alan C. Stockman University of Rochester, and NBER Shadow Open Market Committee April 29-30, 2001 1. Tax Increases Have Created the Surplus Any discussion of tax policy should begin

The Case for a Tax Cut Alan C. Stockman University of Rochester, and NBER Shadow Open Market Committee April 29-30, 2001 1. Tax Increases Have Created the Surplus Any discussion of tax policy should begin

A HAND UP How State Earned Income Tax Credits Help Working Families Escape Poverty in 2004. Summary. By Joseph Llobrera and Bob Zahradnik

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org May 14, 2004 A HAND UP How State Earned Income Tax Credits Help Working Families Escape

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org May 14, 2004 A HAND UP How State Earned Income Tax Credits Help Working Families Escape

INTERACTION OF AUTOMATIC IRAS AND THE RETIREMENT SAVINGS CONTRIBUTIONS CREDIT (SAVER S CREDIT)

") INTERACTION OF AUTOMATIC IRAS AND THE RETIREMENT SAVINGS CONTRIBUTIONS CREDIT (SAVER S CREDIT) A Report Prepared for AARP By: Optimal Benefit Strategies, LLC Judy Xanthopoulos, PhD Mary M. Schmitt, Esq.

INTERACTION OF AUTOMATIC IRAS AND THE RETIREMENT SAVINGS CONTRIBUTIONS CREDIT (SAVER S CREDIT) A Report Prepared for AARP By: Optimal Benefit Strategies, LLC Judy Xanthopoulos, PhD Mary M. Schmitt, Esq.

ENTITY CHOICE AND EFFECTIVE TAX RATES

ENTITY CHOICE AND EFFECTIVE TAX RATES Prepared by Quantria Strategies, LLC for the National Federation of Independent Business and the S Corporation Association ENTITY CHOICE AND EFFECTIVE TAX RATES CONTENTS

ENTITY CHOICE AND EFFECTIVE TAX RATES Prepared by Quantria Strategies, LLC for the National Federation of Independent Business and the S Corporation Association ENTITY CHOICE AND EFFECTIVE TAX RATES CONTENTS

CHAPTER 1 Introduction to Taxation

CHAPTER 1 Introduction to Taxation CHAPTER HIGHLIGHTS A proper analysis of the United States tax system begins with an examination of the tax structure and types of taxes employed in the United States.

CHAPTER 1 Introduction to Taxation CHAPTER HIGHLIGHTS A proper analysis of the United States tax system begins with an examination of the tax structure and types of taxes employed in the United States.

The President s Agenda for Tax Relief

The President s Agenda for Tax Relief These are the basic ideas that guide my tax policy: lower income taxes for all, with the greatest help for those most in need. Everyone who pays income taxes benefits

The President s Agenda for Tax Relief These are the basic ideas that guide my tax policy: lower income taxes for all, with the greatest help for those most in need. Everyone who pays income taxes benefits

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences

We will continue to expand on the provisions of the taxpayer relief act as more information becomes available. If you have any questions please feel free to contact us. Congress passes 2012 Taxpayer Relief

We will continue to expand on the provisions of the taxpayer relief act as more information becomes available. If you have any questions please feel free to contact us. Congress passes 2012 Taxpayer Relief

In the Know December 30, 2010

In the Know December 30, 2010 On December 17, 2010, President Obama signed the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 aka the 2010 Tax Relief Act. Below we break

In the Know December 30, 2010 On December 17, 2010, President Obama signed the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 aka the 2010 Tax Relief Act. Below we break

Statement of. Eric J. Toder Institute Fellow, The Urban Institute and Urban-Brookings Tax Policy Center. Before the Senate Committee on Finance

Statement of Eric J. Toder Institute Fellow, The Urban Institute and Urban-Brookings Tax Policy Center Before the Senate Committee on Finance Tax Issues Related to Small Business Job Creation February

Statement of Eric J. Toder Institute Fellow, The Urban Institute and Urban-Brookings Tax Policy Center Before the Senate Committee on Finance Tax Issues Related to Small Business Job Creation February

ADMINISTRATION TAX-CUT RHETORIC AND SMALL BUSINESSES. By Joel Friedman

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org ADMINISTRATION TAX-CUT RHETORIC AND SMALL BUSINESSES By Joel Friedman September 28,

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org ADMINISTRATION TAX-CUT RHETORIC AND SMALL BUSINESSES By Joel Friedman September 28,

OPTIONS TO REFORM THE DEDUCTION FOR HOME MORTGAGE INTEREST

OPTIONS TO REFORM THE DEDUCTION FOR HOME MORTGAGE INTEREST Chenxi Lu, Joseph Rosenberg, and Eric Toder December 8, 2015 ABSTRACT Taxpayers can currently deduct interest on up to $1 million in acquisition

OPTIONS TO REFORM THE DEDUCTION FOR HOME MORTGAGE INTEREST Chenxi Lu, Joseph Rosenberg, and Eric Toder December 8, 2015 ABSTRACT Taxpayers can currently deduct interest on up to $1 million in acquisition

The Causes of the Shortfall: Declining Revenue

February 24, 2008 Moving From Surplus to Shortfall: The Critical State of Missouri s Revenue and Policy Options Tom Kruckemeyer, Chief Economist Amy Blouin, Executive Director With the 2008 Missouri Legislative

February 24, 2008 Moving From Surplus to Shortfall: The Critical State of Missouri s Revenue and Policy Options Tom Kruckemeyer, Chief Economist Amy Blouin, Executive Director With the 2008 Missouri Legislative

Create a Simple, Pro-Growth Tax System 5

Create a Simple, Pro-Growth Tax System 5 Introduction Reducing the federal debt to sustainable levels will require the tax system to raise more money as a share of the economy than it historically has

Create a Simple, Pro-Growth Tax System 5 Introduction Reducing the federal debt to sustainable levels will require the tax system to raise more money as a share of the economy than it historically has

Senate passes 2010 Tax Relief Act, featuring extension of Bush-era tax cuts & other tax breaks, plus stimulus measures

Senate passes 2010 Tax Relief Act, featuring extension of Bush-era tax cuts & other tax breaks, plus stimulus measures On December 15, the Senate passed, today by a vote of 81-19, the Tax Relief, Unemployment

Senate passes 2010 Tax Relief Act, featuring extension of Bush-era tax cuts & other tax breaks, plus stimulus measures On December 15, the Senate passed, today by a vote of 81-19, the Tax Relief, Unemployment

How do the 2016 Presidential Tax Plans Compare So Far?

How do the 2016 Presidential Tax Plans Compare So Far? 10-Year GDP Growth 10.0% 16.0% -1.0% 13.9% 15.0% -9.5% 11.5% 10-Year Capital Investment Growth 28.8% 46.6% -2.8% 43.9% 48.9% -18.6% 29% 10-Year Wage

How do the 2016 Presidential Tax Plans Compare So Far? 10-Year GDP Growth 10.0% 16.0% -1.0% 13.9% 15.0% -9.5% 11.5% 10-Year Capital Investment Growth 28.8% 46.6% -2.8% 43.9% 48.9% -18.6% 29% 10-Year Wage

Tax legislative outlook

Tax legislative outlook Fall 2010 and beyond Tax policy group November 2010 Agenda Election results Unfinished business Outlook for lame duck Challenges ahead Mid-term election results House 183 Democrats

Tax legislative outlook Fall 2010 and beyond Tax policy group November 2010 Agenda Election results Unfinished business Outlook for lame duck Challenges ahead Mid-term election results House 183 Democrats

2013 Year End Tax Planning Seminar

2013 Year End Tax Planning Seminar Walter H. Deyhle, CPA, CFP December 4, 2013 GRF s Tax Team 2 Disclosure This presentation and these materials are designed to provide accurate and authoritative information

2013 Year End Tax Planning Seminar Walter H. Deyhle, CPA, CFP December 4, 2013 GRF s Tax Team 2 Disclosure This presentation and these materials are designed to provide accurate and authoritative information

Five Flaws of the Current Pension System

The Administration s Savings Accounts Proposals: A Critique Peter Orszag and Gene Sperling November 13, 2003 Five Flaws of the Current Pension System 1. Few People Participate in the Current System Limited

The Administration s Savings Accounts Proposals: A Critique Peter Orszag and Gene Sperling November 13, 2003 Five Flaws of the Current Pension System 1. Few People Participate in the Current System Limited

Overview of the Philanthropic Impact of the American Taxpayer Relief Act of 2012

January 3, 2013 Overview of the Philanthropic Impact of the American Taxpayer Relief Act of 2012 A WHITE PAPER by Robert Sharpe Overview of the Philanthropic Impact of the American Taxpayer Relief Act

January 3, 2013 Overview of the Philanthropic Impact of the American Taxpayer Relief Act of 2012 A WHITE PAPER by Robert Sharpe Overview of the Philanthropic Impact of the American Taxpayer Relief Act

Tax Relief in the American Recovery and Reinvestment Act of 2009

Legislation and Policy Brief Volume 1 Issue 2 Spring 2009 - An Economy in Crisis: What Can Be Done? Article 2 9-24-2010 Tax Relief in the American Recovery and Reinvestment Act of 2009 Steven Gassert sg2702a@student.american.edu

Legislation and Policy Brief Volume 1 Issue 2 Spring 2009 - An Economy in Crisis: What Can Be Done? Article 2 9-24-2010 Tax Relief in the American Recovery and Reinvestment Act of 2009 Steven Gassert sg2702a@student.american.edu

Tax Reform & Tax Relief Package

Tax Reform & Tax Relief Package The New Credit System Summary The new tax reform plan (LD 1495) uses new household credits in place of personal exemptions and standard and itemized deductions. These credits

Tax Reform & Tax Relief Package The New Credit System Summary The new tax reform plan (LD 1495) uses new household credits in place of personal exemptions and standard and itemized deductions. These credits

Why a Credible Budget Strategy Will Reduce Unemployment and Increase Economic Growth. John B. Taylor *

Why a Credible Budget Strategy Will Reduce Unemployment and Increase Economic Growth John B. Taylor * Testimony Before the Joint Economic Committee of the Congress of the United States June 1, 011 Chairman

Why a Credible Budget Strategy Will Reduce Unemployment and Increase Economic Growth John B. Taylor * Testimony Before the Joint Economic Committee of the Congress of the United States June 1, 011 Chairman

The FY 2015 Budget Takes Steps toward Correcting DC s Unbalanced Tax System

DRAFTDRA An Affiliate of the Center on Budget and Policy Priorities 820 First Street NE, Suite 460 Washington, DC 20002 (202) 408-1080 Fax (202) 325-8839 www.dcfpi.org Testimony of Jenny Reed, Policy Director

DRAFTDRA An Affiliate of the Center on Budget and Policy Priorities 820 First Street NE, Suite 460 Washington, DC 20002 (202) 408-1080 Fax (202) 325-8839 www.dcfpi.org Testimony of Jenny Reed, Policy Director

United States Government Required Supplementary Information (Unaudited) For the Years Ended September 30, 2014, and 2013

For the Years Ended September 30, 2014, and 2013") REQUIRED SUPPLEMENTARY INFORMATION (UNAUDITED) 151 United States Government Required Supplementary Information (Unaudited) For the Years Ended September 30, 2014, and 2013 Fiscal Projections for the U.S.

REQUIRED SUPPLEMENTARY INFORMATION (UNAUDITED) 151 United States Government Required Supplementary Information (Unaudited) For the Years Ended September 30, 2014, and 2013 Fiscal Projections for the U.S.

How Much Do Americans Pay in Federal Taxes? April 15, 2014

How Much Do Americans Pay in Federal Taxes? April 15, 2014 One of the most hotly debated issues of our time is the fairness of our federal tax system. But too often, discussions are clouded and confused

How Much Do Americans Pay in Federal Taxes? April 15, 2014 One of the most hotly debated issues of our time is the fairness of our federal tax system. But too often, discussions are clouded and confused

Tax Issues Facing Small Business Donald B. Marron * Urban Institute & Urban-Brookings Tax Policy Center

Tax Issues Facing Small Business Donald B. Marron * Urban Institute & Urban-Brookings Tax Policy Center Testimony before the Small Business Committee, United States House of Representatives April 9, 2014

Tax Issues Facing Small Business Donald B. Marron * Urban Institute & Urban-Brookings Tax Policy Center Testimony before the Small Business Committee, United States House of Representatives April 9, 2014

Striking it Richer: The Evolution of Top Incomes in the United States (Update using 2006 preliminary estimates)

") Striking it Richer: The Evolution of Top Incomes in the United States (Update using 2006 preliminary estimates) Emmanuel Saez March 15, 2008 The recent dramatic rise in income inequality in the United

Striking it Richer: The Evolution of Top Incomes in the United States (Update using 2006 preliminary estimates) Emmanuel Saez March 15, 2008 The recent dramatic rise in income inequality in the United

Revenue-Raising Options to Help Close Minnesota s Budget Deficits in FY 2011-13

Revenue-Raising Options to Help Close Minnesota s Budget Deficits in FY 2011-13 Minnesota faces billion-dollar deficits in this biennium and the next Minnesota Needs a Balanced Approach to Solving Deficits

Revenue-Raising Options to Help Close Minnesota s Budget Deficits in FY 2011-13 Minnesota faces billion-dollar deficits in this biennium and the next Minnesota Needs a Balanced Approach to Solving Deficits

budget brief On Tuesday, August 3, legislative leaders proposed a new budget plan, including a tax swap that would increase some

UNDERSTANDING THE TAX SWAP budget brief AUGUST JUNE 2010 2005 On Tuesday, August 3, legislative leaders proposed a new budget plan, including a tax swap that would increase some of the state s personal

UNDERSTANDING THE TAX SWAP budget brief AUGUST JUNE 2010 2005 On Tuesday, August 3, legislative leaders proposed a new budget plan, including a tax swap that would increase some of the state s personal

Benjamin Franklin observed that nothing in life is certain except

Middle-Income Tax Rates: Trends and Prospects By Troy A. Davig and C. Alan Garner Benjamin Franklin observed that nothing in life is certain except death and taxes. But he was referring to the existence

Middle-Income Tax Rates: Trends and Prospects By Troy A. Davig and C. Alan Garner Benjamin Franklin observed that nothing in life is certain except death and taxes. But he was referring to the existence

How To Get A Lower Tax Bill

13 FINANCIAL PLANNING STRATEGIES FOR 2013 Timely, actionable ideas following the American Taxpayer Relief Act KEY TAKEAWAYS With the passing of the American Taxpayer Relief Act of 2012 in reaction to the

13 FINANCIAL PLANNING STRATEGIES FOR 2013 Timely, actionable ideas following the American Taxpayer Relief Act KEY TAKEAWAYS With the passing of the American Taxpayer Relief Act of 2012 in reaction to the

The primary purpose of a tax system is to support public goods and services. State and local taxes

Issue Brief UPDATED APRIL 2015 BY WILLIAM CHEN Who Pays Taxes in California? The primary purpose of a tax system is to support public goods and services. State and local taxes are the way that Californians

Issue Brief UPDATED APRIL 2015 BY WILLIAM CHEN Who Pays Taxes in California? The primary purpose of a tax system is to support public goods and services. State and local taxes are the way that Californians

January 27, 2010. Honorable Paul Ryan Ranking Member Committee on the Budget U.S. House of Representatives Washington, DC 20515.

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Douglas W. Elmendorf, Director January 27, 2010 Honorable Paul Ryan Ranking Member Committee on the Budget U.S. House of Representatives Washington,

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Douglas W. Elmendorf, Director January 27, 2010 Honorable Paul Ryan Ranking Member Committee on the Budget U.S. House of Representatives Washington,

Chapter 12: Gross Domestic Product and Growth Section 1

Chapter 12: Gross Domestic Product and Growth Section 1 Key Terms national income accounting: a system economists use to collect and organize macroeconomic statistics on production, income, investment,

Chapter 12: Gross Domestic Product and Growth Section 1 Key Terms national income accounting: a system economists use to collect and organize macroeconomic statistics on production, income, investment,

Life Insurance Companies and Products

Part B. Life Insurance Companies and Products The current Federal income tax treatment of life insurance companies and their products al.lows investors in such products to obtain a substantially higher

Part B. Life Insurance Companies and Products The current Federal income tax treatment of life insurance companies and their products al.lows investors in such products to obtain a substantially higher

Governor Walker's Tax Reform Initiative. Wisconsin Department of Revenue February 2013

Governor Walker's Tax Reform Initiative Wisconsin Department of Revenue February 2013 1 Tax Reform Goals Reduce Wisconsin's high tax burden Put more money in people's pockets Make Wisconsin more competitive

Governor Walker's Tax Reform Initiative Wisconsin Department of Revenue February 2013 1 Tax Reform Goals Reduce Wisconsin's high tax burden Put more money in people's pockets Make Wisconsin more competitive

How To Extend The Earned Income Tax Credit

Without Congressional Action, Improvements to Earned Income Tax Credit and Child Tax Credit Set to Expire in 2017 By Alex Meyer Earned Income Tax Credit (EITC) The Federal EITC was first enacted in 1975,

Without Congressional Action, Improvements to Earned Income Tax Credit and Child Tax Credit Set to Expire in 2017 By Alex Meyer Earned Income Tax Credit (EITC) The Federal EITC was first enacted in 1975,

June 2, 2003. Re: Jobs and Growth Tax Relief Reconciliation Act of 2003

June 2, 2003 Re: Jobs and Growth Tax Relief Reconciliation Act of 2003 On Wednesday, May 28, 2003, President Bush signed into law the third largest tax cut in U.S. history. The Jobs and Growth Tax Relief

June 2, 2003 Re: Jobs and Growth Tax Relief Reconciliation Act of 2003 On Wednesday, May 28, 2003, President Bush signed into law the third largest tax cut in U.S. history. The Jobs and Growth Tax Relief

tax planning strategies

tax planning strategies In addition to saving income taxes for the current and future years, tax planning can reduce eventual estate taxes, maximize the amount of funds you will have available for retirement,

tax planning strategies In addition to saving income taxes for the current and future years, tax planning can reduce eventual estate taxes, maximize the amount of funds you will have available for retirement,

LIFE INSURANCE DIVISION

TAX LAW SUMMARY American Taxpayer Relief Act MKTG-OC-1053A LIFE INSURANCE DIVISION TAX LAW SUMMARY American Taxpayer Relief Act INDIVIDUAL TAX PROVISIONS...3 Individual Tax Rates...3 Marriage Penalty Relief...4

TAX LAW SUMMARY American Taxpayer Relief Act MKTG-OC-1053A LIFE INSURANCE DIVISION TAX LAW SUMMARY American Taxpayer Relief Act INDIVIDUAL TAX PROVISIONS...3 Individual Tax Rates...3 Marriage Penalty Relief...4

PATRICK J. RUBEY & COMPANY, LTD. CERTIFIED PUBLIC ACCOUNTANTS

PATRICK J. RUBEY & COMPANY, LTD. CERTIFIED PUBLIC ACCOUNTANTS American Taxpayer Relief Act January 1, 2013 Here are the act s main tax features: Individual tax rates All the individual marginal tax rates

PATRICK J. RUBEY & COMPANY, LTD. CERTIFIED PUBLIC ACCOUNTANTS American Taxpayer Relief Act January 1, 2013 Here are the act s main tax features: Individual tax rates All the individual marginal tax rates

H.R. 1836 CONGRESSIONAL BUDGET OFFICE PAY-AS-YOU-GO ESTIMATE. Economic Growth and Tax Relief Reconciliation Act of 2001.

CONGRESSIONAL BUDGET OFFICE PAY-AS-YOU-GO ESTIMATE June 4, 2001 H.R. 1836 Economic Growth and Tax Relief Reconciliation Act of 2001 As cleared by the Congress on May 26, 2001 SUMMARY The Economic Growth

CONGRESSIONAL BUDGET OFFICE PAY-AS-YOU-GO ESTIMATE June 4, 2001 H.R. 1836 Economic Growth and Tax Relief Reconciliation Act of 2001 As cleared by the Congress on May 26, 2001 SUMMARY The Economic Growth

Executive Summary. 204 N. First St., Suite C PO Box 7 Silverton, OR 97381 www.ocpp.org 503-873-1201 fax 503-873-1947

Executive Summary 204 N. First St., Suite C PO Box 7 Silverton, OR 97381 www.ocpp.org 503-873-1201 fax 503-873-1947 On Whose Backs? Tax Distribution, Income Inequality, and Plans for Raising Revenue By

Executive Summary 204 N. First St., Suite C PO Box 7 Silverton, OR 97381 www.ocpp.org 503-873-1201 fax 503-873-1947 On Whose Backs? Tax Distribution, Income Inequality, and Plans for Raising Revenue By

Tax Expenditures and Social Policy: A Primer

Percent Tax Expenditures and Social Policy: A Primer Daniel Mandel What Are Tax Expenditures? Congress uses the tax code to promote a broad range of policy objectives. Rather than directly spend government

Percent Tax Expenditures and Social Policy: A Primer Daniel Mandel What Are Tax Expenditures? Congress uses the tax code to promote a broad range of policy objectives. Rather than directly spend government

Mutual Fund Tax Guide

2010 Mutual Fund Tax Guide TABLE OF CONTENTS Part 1 - Tax Items of Interest... 2-6 Part 2 - Tax Forms... 7-14 Form 1099-DIV...7 Form 1099-B...8 Form 1099-R...9 Form 1099-Q...10 Form 1099-INT...11 Form

2010 Mutual Fund Tax Guide TABLE OF CONTENTS Part 1 - Tax Items of Interest... 2-6 Part 2 - Tax Forms... 7-14 Form 1099-DIV...7 Form 1099-B...8 Form 1099-R...9 Form 1099-Q...10 Form 1099-INT...11 Form

ITEP. Tax Reform in Kentucky. Serious Problems, Stark Choices. Institute on Taxation and Economic Policy. Institute on Taxation and Economic Policy

Tax Reform in Kentucky Serious Problems, Stark Choices Institute on Taxation and Economic Policy June 2009 ITEP Institute on Taxation and Economic Policy 1616 P Street NW Washington, DC 20036 (202) 299-1066

Tax Reform in Kentucky Serious Problems, Stark Choices Institute on Taxation and Economic Policy June 2009 ITEP Institute on Taxation and Economic Policy 1616 P Street NW Washington, DC 20036 (202) 299-1066

The Minnesota and Federal Dependent Care Tax Credits

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Nina Manzi, Legislative Analyst 651-296-5204 Updated: February 2014 The Minnesota and

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Nina Manzi, Legislative Analyst 651-296-5204 Updated: February 2014 The Minnesota and

Federal Budget in Pictures CUT SPENDING // FIX THE DEBT // REDUCE THE TAX BURDEN$

2015 Federal Budget in Pictures CUT SPENDING // FIX THE DEBT // REDUCE THE TAX BURDEN$ 2015 Federal Budget in Pictures CUT SPENDING // FIX THE DEBT // REDUCE THE TAX BURDEN Thomas A. Roe Institute for

2015 Federal Budget in Pictures CUT SPENDING // FIX THE DEBT // REDUCE THE TAX BURDEN$ 2015 Federal Budget in Pictures CUT SPENDING // FIX THE DEBT // REDUCE THE TAX BURDEN Thomas A. Roe Institute for

cepr briefing paper Defaulting on The Social Security Trust Fund Bonds: Winner and Losers CENTER FOR ECONOMIC AND POLICY RESEARCH SUMMARY Dean Baker 1

cepr CENTER FOR ECONOMIC AND POLICY RESEARCH briefing paper Defaulting on The Social Security Trust Fund Bonds: Winner and Losers Dean Baker 1 July 23, 2001 SUMMARY The United States government has never

cepr CENTER FOR ECONOMIC AND POLICY RESEARCH briefing paper Defaulting on The Social Security Trust Fund Bonds: Winner and Losers Dean Baker 1 July 23, 2001 SUMMARY The United States government has never

Tax-Saving Opportunities for "Active" Business Owners

S CORPORATIONS Tax-Saving Opportunities for "Active" Business Owners S corporations now provide business owners with a unique opportunity to minimize earnings subject to both the recently imposed additional

S CORPORATIONS Tax-Saving Opportunities for "Active" Business Owners S corporations now provide business owners with a unique opportunity to minimize earnings subject to both the recently imposed additional

Bunting, Tripp IngleyLLP

Dear Clients and Friends, As the end of 2011 approaches, now is a good time to start year-end tax planning to minimize your individual and business tax burden. Generally, year-end tax planning involves

Dear Clients and Friends, As the end of 2011 approaches, now is a good time to start year-end tax planning to minimize your individual and business tax burden. Generally, year-end tax planning involves

Is there a revolution in American saving?

MPRA Munich Personal RePEc Archive Is there a revolution in American saving? John Tatom Networks Financial institute at Indiana State University May 2009 Online at http://mpra.ub.uni-muenchen.de/16139/

MPRA Munich Personal RePEc Archive Is there a revolution in American saving? John Tatom Networks Financial institute at Indiana State University May 2009 Online at http://mpra.ub.uni-muenchen.de/16139/

Revised May 20, 2010. Bill Would Provide Needed Economic Boost

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised May 20, 2010 BUDGETARY CONCERNS SHOULD NOT BE AN OBSTACLE TO PASSING THE NEW

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised May 20, 2010 BUDGETARY CONCERNS SHOULD NOT BE AN OBSTACLE TO PASSING THE NEW

The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education

POLICY BRIEF Visit us at: www.tiaa-crefinstitute.org. September 2004 The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education The 2004 Social

POLICY BRIEF Visit us at: www.tiaa-crefinstitute.org. September 2004 The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education The 2004 Social

The Tax Relief Program Worked: Make the Tax Cuts Permanent

The Tax Relief Program Worked: Make the Tax Cuts Permanent J. D. Foster, Ph.D. Tax relief worked. It put the federal tax burden on track toward its historic norm. Combined with an aggressive monetary policy,

The Tax Relief Program Worked: Make the Tax Cuts Permanent J. D. Foster, Ph.D. Tax relief worked. It put the federal tax burden on track toward its historic norm. Combined with an aggressive monetary policy,

The Minnesota Income Tax Marriage Credit

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Nina Manzi, Legislative Analyst, 651-296-5204 Joel Michael, Legislative Analyst, joel.michael@house.mn

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Nina Manzi, Legislative Analyst, 651-296-5204 Joel Michael, Legislative Analyst, joel.michael@house.mn

CTJ s Presidential Candidate Tax Policy Scorecard

CTJ s Presidential Candidate Tax Policy Scorecard In the past two decades, Congress has frequently discussed, and often enacted, substantial revisions to the federal tax code. During this period, members

CTJ s Presidential Candidate Tax Policy Scorecard In the past two decades, Congress has frequently discussed, and often enacted, substantial revisions to the federal tax code. During this period, members