INCOME TAX REFORM. What Does It Mean for Taxpayers?

|

|

|

- Georgina Kristina Roberts

- 8 years ago

- Views:

Transcription

1 BRIEFING PAPER INCOME TAX REFORM What Does It Mean for Taxpayers? Office of Legislative Research and General Counsel DECEMBER 2006 UTAH LEGISLATURE HIGHLIGHTS SB 4001, passed in the th Special Session, reduces taxes for nearly all residents who pay individual income tax. This tax reduction is the result of adjustments to the tax brackets and creation of a new flat tax option. Bracket adjustments provide a tax cut to nearly all resident filers. Single filers generally receive a benefit between $25 and $50. Married filers generally receive a benefit between $50 and $100. The flat tax option provides an additional tax cut, in varying amounts, to about 4% of resident taxpayers. Higher income returns generally receive a larger tax cut when measured by dollar amount. Lower income returns generally receive a larger tax cut when measured by percent reduction in tax liability and by reduction in the effective tax rate. SPECIAL SESSION INCOME TAX REFORM BILL In the September th Special Session, the Utah Legislature passed SB 4001, "Income Tax Amendments." This tax reform bill makes two main adjustments to the state's individual income tax system: bracket adjustments and a new flat tax computation. Bracket Adjustments. Beginning in tax year 2006, the new law expands the tax brackets applied to Utah taxable income under the traditional multiple rate computation and reduces the tax rate for the top bracket. Beginning in tax year 2009, the law also indexes tax brackets for inflation. Flat Tax Computation. Beginning in tax year 2007, the new law allows a taxpayer to utilize an alternative flat tax computation based on a flat rate of 5.35% of federal adjusted gross income (AGI), with certain additions to and subtractions from AGI. HOW ARE EFFECTS ESTIMATED? The Office of Legislative Research and General Counsel analyzed the new law's effects by applying SB 4001's 1 changes to tax year 2005 returns. Even though individual returns may vary from year to year, the trends from tax year 2005 should provide a general indication of SB 4001's impacts 2. WHAT ARE THE BRACKET ADJUSTMENTS? Beginning in tax year 2006, SB 4001 expands tax brackets and reduces the top bracket rate, as shown in Table 1 and Table 2 (page 2). In addition, the tax brackets are indexed for inflation, as measured by the Consumer Price Index, beginning in tax year The top bracket rate reduction from 7.00% to 6.98% provides an additional benefit to those with income taxed in the top bracket (about 80% of resident taxpayer returns). The Legislative Fiscal Analyst estimates that the new law will reduce individual income tax revenues by between $78 million and $85 million in FY 2008 and that a little more than half of this tax cut amount is attributable to the bracket adjustments. WHAT IS THE EFFECT OF BRACKET ADJUSTMENTS? This analysis utilizes three methods for assessing tax liability changes: (1) dollar reduction, (2) percent reduction in liability, and (3) effective rate reduction. Dollar reduction is the estimated amount of the tax cut. Percent reduction in liability is the dollar reduction as a percent of the tax liability prior to the bracket adjustments. Effective rate reduction is the dollar reduction as a percent of AGI. Each of these three measures examines the tax cut in a different way. Taken together, the three measures provide a good sense of the overall effect of the tax changes. For each method of analysis, we provide scatterplot charts in which each tax return is represented by a dot. 1

2 Table 1 Tax Brackets Applied to State Taxable Income Single and married filing separately Tax Year 2005 Tax Year 2006 Lower Upper Add Rate Lower Upper Add Rate $0 $863 $0 2.30% $0 $1,000 $0 2.30% $864 $1,726 $ % $1,001 $2,000 $ % $1,727 $2,588 $ % $2,001 $3,000 $ % $2,589 $3,450 $ % $3,001 $4,000 $ % $3,451 $4,313 $ % $4,001 $5,500 $ % $4,314 and up $ % $5,501 and up $ % Table 2 Tax Brackets Applied to State Taxable Income Married filing jointly and head of household Tax Year 2005 Tax Year 2006 Lower Upper Add Rate Lower Upper Add Rate $0 $1,726 $0 2.30% $0 $2,000 $0 2.30% $1,727 $3,450 $ % $2,001 $4,000 $ % $3,451 $5,176 $ % $4,001 $6,000 $ % $5,177 $6,900 $ % $6,001 $8,000 $ % $6,901 $8,626 $ % $8,001 $11,000 $ % $8,627 and up $ % $11,001 and up $ % The bracket adjustments provide a tax reduction to nearly all resident income tax payers (resident returns with positive tax liability). Higher income returns generally receive a larger tax cut when measured by dollar reduction, due primarily to the drop in the top bracket rate. Lower income returns generally receive a larger tax cut when measured by percentage reduction in tax liability or effective rate reduction, due mainly to the bracket expansion. Returns in lower brackets receive benefits that vary by bracket. A small number of taxpayers may not see a tax reduction because their taxable income falls in the lowest tax bracket or they have a tax liability that rounds to the same whole dollar amount as their previous liability. Dollar reduction. As shown in Chart 1 (page 4), most filers that are single or married filing separately receive a tax cut between $25 and $50, with the amount increasing as income rises. Most filers that are married filing jointly or head of household receive a tax cut between $50 and $100, with the amount increasing as income rises. Percent of liability reduction. As shown in Chart 2 (page 5), lower income returns generally receive a higher percentage tax cut from the bracket adjustments. Returns at or near the cutoff for the top bracket receive about a 9% reduction in their tax liability. This reduction percentage declines to a roughly 1% reduction in tax liability for returns with AGI greater than $100,000. Effective rate reduction. As shown in Chart 3 (page 5), lower income returns generally receive more of an effective rate reduction from the bracket adjustments. In other words, lower income returns generally receive a greater reduction as a percent of AGI. Filers at or near the cutoff for the top bracket receive about a 0.2% to 0.3% effective rate reduction. The effective rate reduction gradually declines to below 0.05% for most higher income returns. 2

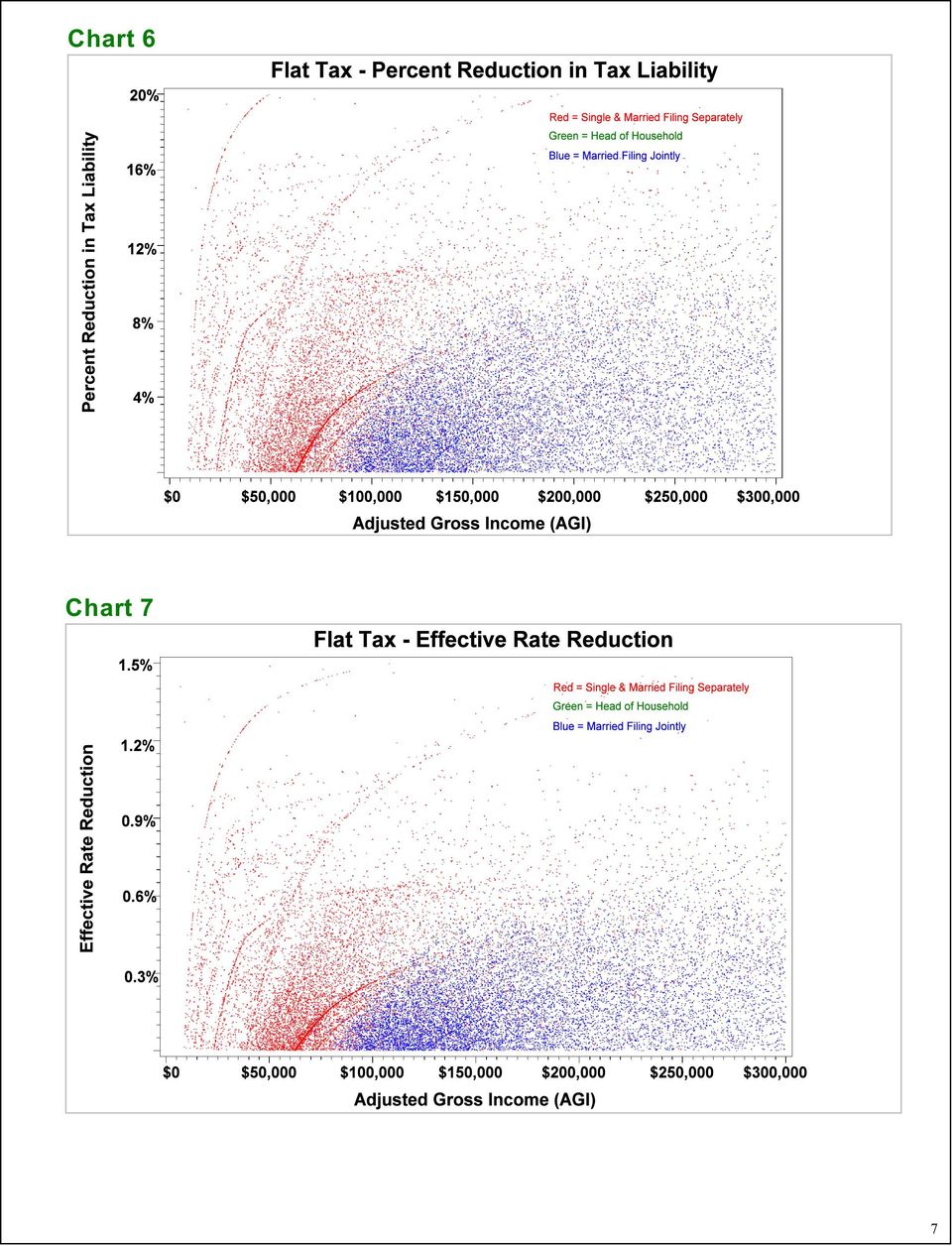

3 WHAT IS THE FLAT TAX COMPUTATION? Beginning in tax year 2007, SB 4001 allows a taxpayer to make a flat tax computation and pay the lesser of the multiple rate computation and the flat tax computation. Under the flat tax computation, a filer begins with AGI and makes certain additions to and subtractions from AGI (see Table 3). After making these adjustments to AGI, a taxpayer multiplies the resulting modified AGI amount by a flat tax rate of 5.35%. The taxpayer pays the lesser of the flat tax computation and the multiple rate computation. Under the flat tax computation, a taxpayer may not claim deductions from AGI for personal exemptions, the standard deduction, itemized deductions (such as mortgage interest, charitable contributions, and state and local taxes), the deduction for being age 65 or over, or the deduction for one half of the federal tax paid. Table 3 Flat Tax - Additions to and Subtractions from AGI Additions to AGI Subtractions from AGI Although in some individual cases the remaining flat tax additions to and subtractions from AGI may be significant, on a statewide basis, the flat tax computation tax base remains close to AGI. Because there are only a few relatively minor deductions allowed, the flat tax computation base is a broader tax base than the multiple rate computation tax base. The Legislative Fiscal Analyst estimates that slightly less than half of the tax cut enacted under SB 4001 is due to the flat tax computation. WHAT IS THE EFFECT OF THE FLAT TAX? Based on tax year 2005 data, about 30,000 returns initially benefit from the alternative flat tax calculation provided for in SB 4001 (about 4% of resident returns with a positive tax liability or about 3% of all resident returns). Although flat tax filers represent a fairly small percentage of resident taxpayer returns (4%), they represent a much larger share of AGI (22%) and tax liability (30%). Certain medical savings account withdrawals and penalties deducted on state individual income tax return Certain income tax amounts deducted from AGI by an estate or trust Certain lump sum distributions Child's income reported on a parent's return but not included in AGI Educational savings plan withdrawals that were deducted on a state individual income tax return but not used for qualified higher education purposes Other states' bond interest, under certain conditions Certain trust distributions received by a resident beneficiary Certain adoption expenses deducted on a state or federal individual income tax return Deductions required by federal law, treaty, or case law (US interest, certain American Indian income, railroad retirement income) Uintah-Ouray reservation income State tax refund included in AGI Through the flat tax computation, taxpayers give up about $2.1 billion in deductions (approximately 11% of total deductions claimed on resident taxpayer returns). However, this base expansion may be temporary, because it can vary by year as taxpayers annually select the tax computation providing the greatest benefit. As shown in Chart 4 (page 6), some higher income returns receive a larger tax cut when measured by dollar reduction, likely because these returns claim fewer deductions as a percentage of AGI. Other higher income returns receive tax cuts similar to lower income returns that use the flat tax. Chart 5 (page 6) also shows the distribution in the amount of tax cut. No obvious pattern emerges when measuring the tax cut by percent reduction in tax liability (Chart 6 on page 7) and effective rate reduction (Chart 7 on page 7). Using these two percentage measures, the benefits appear to be spread across income groups. Charts 8 through 13 (pages 8 to 10) show that those who benefit from the flat tax computation cross the spectrum of income, family size, and filing status type. 3

4 CONCLUSION SB 4001 of the 4th Special Session reduces taxes for nearly all residents who pay individual income tax, through changes to tax brackets and through a new flat tax option. Bracket adjustments provide a tax cut to nearly all resident filers. Single filers generally receive a benefit between $25 and $50. Married filers generally receive a benefit between $50 and $100. The flat tax option provides an additional tax cut, in varying amounts, to about 4% of resident taxpayers. Higher income returns generally receive a larger tax cut when measured by dollar amount, due primarily to the top bracket rate cut and the flat tax. Lower income returns generally receive a larger tax cut when measured by percent reduction in tax liability and by reduction in the effective tax rate, due primarily to the bracket expansion. NOTES 1. SB 3002 of the rd Special Session allows the Office of Legislative Research and General Counsel to obtain state tax return information, subject to stringent restrictions that protect taxpayers' privacy. Among these restrictions are: (1) the Tax Commission must remove personal identifying information prior to providing the return data; and (2) the Office may not present data in a way that would allow identification of a particular taxpayer. 2. No analysis of tax year 2005 returns can state precisely what will happen in the future when the enacted changes take place. Changes in income, deductions, credits, and tax for each individual return are likely, due to changes in personal circumstances and federal tax law. However, the general trends are likely to be similar between tax year 2005 and tax years 2006 and 2007 (when the enacted changes take place). It is also worth noting that an analysis using tax year 2004 returns produced substantially similar results. Chart 1 4

5 Chart 2 Chart 3 5

6 Chart 4 Chart 5 6

7 Chart 6 Chart 7 7

8 Flat Tax Filers by Income Range. Chart 8 and Chart 9 show the distribution of flat tax and multiple rate system filers by AGI range. The flat tax system has a greater proportion of higher income filers than the multiple rate system. Chart 8 Chart 9 8

9 Flat Tax Filers by Filing Status. Chart 10 and Chart 11 show the distribution of flat tax and multiple rate system filers by filing status. The flat tax system has a slightly greater proportion of filers who are single or married filing jointly. Chart 10 Chart 11 9

10 Flat Tax Filers by Family Size (# of Personal Exemptions). Chart 12 and Chart 13 show the distribution of flat tax and multiple rate system filers by the number of personal exemptions claimed, a general approximation for family size. The flat tax system has a somewhat higher proportion of returns with one or two exemptions. Chart 12 Chart 13 10

ATTENTION: NEW NC-4 WITHHOLDING FORMS ENCLOSED

North Carolina Department of Revenue ATTENTION: NEW NC-4 WITHHOLDING FORMS ENCLOSED IMMEDIATE ACTION REQUIRED North Carolina Department of Revenue TO: IMPORTANT NOTICE: NEW NC-4 REQUIRED FOR PAYMENTS BEGINNING

North Carolina Department of Revenue ATTENTION: NEW NC-4 WITHHOLDING FORMS ENCLOSED IMMEDIATE ACTION REQUIRED North Carolina Department of Revenue TO: IMPORTANT NOTICE: NEW NC-4 REQUIRED FOR PAYMENTS BEGINNING

Governor Walker's Tax Reform Initiative. Wisconsin Department of Revenue February 2013

Governor Walker's Tax Reform Initiative Wisconsin Department of Revenue February 2013 1 Tax Reform Goals Reduce Wisconsin's high tax burden Put more money in people's pockets Make Wisconsin more competitive

Governor Walker's Tax Reform Initiative Wisconsin Department of Revenue February 2013 1 Tax Reform Goals Reduce Wisconsin's high tax burden Put more money in people's pockets Make Wisconsin more competitive

NAR Frequently Asked Questions Health Insurance Reform

NEW MEDICARE TAX ON UNEARNED NET INVESTMENT INCOME Q-1: Who will be subject to the new taxes imposed in the health legislation? A: A new 3.8% tax will apply to the unearned income of High Income taxpayers.

NEW MEDICARE TAX ON UNEARNED NET INVESTMENT INCOME Q-1: Who will be subject to the new taxes imposed in the health legislation? A: A new 3.8% tax will apply to the unearned income of High Income taxpayers.

INSIGHT on the Issues

INSIGHT on the Issues The Saver s Credit: What Does It Do For Saving? AARP Public Policy Institute The saver s credit is one of very few tax incentives to promote savings that targets lowand middle-income

INSIGHT on the Issues The Saver s Credit: What Does It Do For Saving? AARP Public Policy Institute The saver s credit is one of very few tax incentives to promote savings that targets lowand middle-income

Higher Education Tax Benefits: Brief Overview and Budgetary Effects

Higher Education Tax Benefits: Brief Overview and Budgetary Effects Margot L. Crandall-Hollick Analyst in Public Finance Mark P. Keightley Analyst in Public Finance August 24, 2011 CRS Report for Congress

Higher Education Tax Benefits: Brief Overview and Budgetary Effects Margot L. Crandall-Hollick Analyst in Public Finance Mark P. Keightley Analyst in Public Finance August 24, 2011 CRS Report for Congress

Tax Relief in 2001 through 2011

in 2001 through 2011 Department of the Treasury May 2008 in 2001 through 2011 The tax relief enacted during the President s term in office, principally in the Economic Growth and Relief Reconciliation

in 2001 through 2011 Department of the Treasury May 2008 in 2001 through 2011 The tax relief enacted during the President s term in office, principally in the Economic Growth and Relief Reconciliation

THE GRADUATED PERSONAL INCOME TAX ASSESSMENT: FREQUENTLY ASKED QUESTIONS

LEGISLATIVE REVENUE OFFICE State Capitol Building 900 Court St. NE, Room H-197 Salem, Oregon 97301 Research Brief (503) 986-1266 FAX (503) 986-1770 http://www.leg.state.or.us/comm/lro/home.htm Number 3-03

LEGISLATIVE REVENUE OFFICE State Capitol Building 900 Court St. NE, Room H-197 Salem, Oregon 97301 Research Brief (503) 986-1266 FAX (503) 986-1770 http://www.leg.state.or.us/comm/lro/home.htm Number 3-03

SUBJECT: Distributional Information on Proposed Individual Income Tax Rate Reduction

Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 (608) 266-3847 Fax: (608) 267-6873 Email: fiscal.bureau@legis.wisconsin.gov Website: http://legis.wisconsin.gov/lfb February 25, 2013

Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 (608) 266-3847 Fax: (608) 267-6873 Email: fiscal.bureau@legis.wisconsin.gov Website: http://legis.wisconsin.gov/lfb February 25, 2013

Tax Subsidies for Health Insurance An Issue Brief

Tax Subsidies for Health Insurance An Issue Brief Prepared by the Kaiser Family Foundation July 2008 Tax Subsidies for Health Insurance Most workers pay both federal and state taxes for wages paid to them

Tax Subsidies for Health Insurance An Issue Brief Prepared by the Kaiser Family Foundation July 2008 Tax Subsidies for Health Insurance Most workers pay both federal and state taxes for wages paid to them

Highlights of the 2010 Tax Relief Act

On December 7, 200, President Barack Obama signed into law H.R. 4853, the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 200 (the 200 Tax Relief Act). This massive bill affects

On December 7, 200, President Barack Obama signed into law H.R. 4853, the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 200 (the 200 Tax Relief Act). This massive bill affects

Withholding Certificate for Pension or Annuity Payments

Web 12-14 NC-4P Withholding Certificate for Pension or Annuity Payments PURPOSE. Form NC-4P is for North Carolina residents who are recipients of income from pensions, annuities, and certain other deferred

Web 12-14 NC-4P Withholding Certificate for Pension or Annuity Payments PURPOSE. Form NC-4P is for North Carolina residents who are recipients of income from pensions, annuities, and certain other deferred

Federal Income Tax Information January 29, 2016 Page 2. 2016 Federal Income Tax Withholding Information - PERCENTAGE METHOD

Federal Income Tax Information January 29, 2016 Page 2 - PERCENTAGE METHOD ALLOWANCE TABLE Dollar Amount of Withholding Allowances Number of Biweekly Monthly Withholding Pay Period Pay Period Allowances

Federal Income Tax Information January 29, 2016 Page 2 - PERCENTAGE METHOD ALLOWANCE TABLE Dollar Amount of Withholding Allowances Number of Biweekly Monthly Withholding Pay Period Pay Period Allowances

Cut here and give this certificate to your employer. Keep the top portion for your records. North Carolina Department of Revenue

Web 2-15 NC-4 Employee s Withholding Allowance Certificate PURPOSE - Complete Form NC-4, Employee s Withholding Allowance Certificate, so that your employer can withhold the correct amount of State income

Web 2-15 NC-4 Employee s Withholding Allowance Certificate PURPOSE - Complete Form NC-4, Employee s Withholding Allowance Certificate, so that your employer can withhold the correct amount of State income

Tax Reform & Tax Relief Package

Tax Reform & Tax Relief Package The New Credit System Summary The new tax reform plan (LD 1495) uses new household credits in place of personal exemptions and standard and itemized deductions. These credits

Tax Reform & Tax Relief Package The New Credit System Summary The new tax reform plan (LD 1495) uses new household credits in place of personal exemptions and standard and itemized deductions. These credits

Who Must Make Estimated Tax Payments

2014 Form Estimated Income Tax for Estates and Trusts Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest information about developments related

2014 Form Estimated Income Tax for Estates and Trusts Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest information about developments related

United States General Accounting Office. Testimony Before the Committee on Finance, United States Senate

GAO United States General Accounting Office Testimony Before the Committee on Finance, United States Senate For Release on Delivery Expected at 10:00 a.m. EST on Thursday March 8, 2001 ALTERNATIVE MINIMUM

GAO United States General Accounting Office Testimony Before the Committee on Finance, United States Senate For Release on Delivery Expected at 10:00 a.m. EST on Thursday March 8, 2001 ALTERNATIVE MINIMUM

Withholding Certificate for Pension or Annuity Payments

NC-4P Web 11-13! Withholding Certificate for Pension or Annuity Payments North Carolina Department of Revenue Important: You must complete a new Form NC-4P for tax year 2014. As a result of recent law

NC-4P Web 11-13! Withholding Certificate for Pension or Annuity Payments North Carolina Department of Revenue Important: You must complete a new Form NC-4P for tax year 2014. As a result of recent law

NORTH CAROLINA GENERAL ASSEMBLY LEGISLATIVE FISCAL NOTE

NORTH CAROLINA GENERAL ASSEMBLY LEGISLATIVE FISCAL NOTE BILL NUMBER: SHORT TITLE: SPONSOR(S): House Bill 1429 (House Finance Committee Substitute, as amended) Financial Responsibility Act Representatives

NORTH CAROLINA GENERAL ASSEMBLY LEGISLATIVE FISCAL NOTE BILL NUMBER: SHORT TITLE: SPONSOR(S): House Bill 1429 (House Finance Committee Substitute, as amended) Financial Responsibility Act Representatives

INDIVIDUALS -- 2000 DEPARTMENT OF TAXATION -- STATE OF HAWAII

hawaii income patterns INDIVIDUALS -- 2000 DEPARTMENT OF TAXATION -- STATE OF HAWAII STATE OF HAWAII Benjamin J. Cayetano, Governor DEPARTMENT OF TAXATION Marie Y. Okamura, Director Grant B. Tanimoto,

hawaii income patterns INDIVIDUALS -- 2000 DEPARTMENT OF TAXATION -- STATE OF HAWAII STATE OF HAWAII Benjamin J. Cayetano, Governor DEPARTMENT OF TAXATION Marie Y. Okamura, Director Grant B. Tanimoto,

The Minnesota and Federal Dependent Care Tax Credits

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Nina Manzi, Legislative Analyst 651-296-5204 Updated: February 2014 The Minnesota and

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Nina Manzi, Legislative Analyst 651-296-5204 Updated: February 2014 The Minnesota and

PATRICK J. RUBEY & COMPANY, LTD. CERTIFIED PUBLIC ACCOUNTANTS

PATRICK J. RUBEY & COMPANY, LTD. CERTIFIED PUBLIC ACCOUNTANTS American Taxpayer Relief Act January 1, 2013 Here are the act s main tax features: Individual tax rates All the individual marginal tax rates

PATRICK J. RUBEY & COMPANY, LTD. CERTIFIED PUBLIC ACCOUNTANTS American Taxpayer Relief Act January 1, 2013 Here are the act s main tax features: Individual tax rates All the individual marginal tax rates

Current Individual Income Tax Rates 1. Federal Income Taxation Lecture 7 Slide 1

Current Individual Income Tax Rates 1 Federal Income Taxation Lecture 7 Slide 1 Current Individual Income Tax Rates 2 Federal Income Taxation Lecture 7 Slide 2 Income Tax Deductions and Credits A tax deduction

Current Individual Income Tax Rates 1 Federal Income Taxation Lecture 7 Slide 1 Current Individual Income Tax Rates 2 Federal Income Taxation Lecture 7 Slide 2 Income Tax Deductions and Credits A tax deduction

How do the 2016 Presidential Tax Plans Compare So Far?

How do the 2016 Presidential Tax Plans Compare So Far? 10-Year GDP Growth 10.0% 16.0% -1.0% 13.9% 15.0% -9.5% 11.5% 10-Year Capital Investment Growth 28.8% 46.6% -2.8% 43.9% 48.9% -18.6% 29% 10-Year Wage

How do the 2016 Presidential Tax Plans Compare So Far? 10-Year GDP Growth 10.0% 16.0% -1.0% 13.9% 15.0% -9.5% 11.5% 10-Year Capital Investment Growth 28.8% 46.6% -2.8% 43.9% 48.9% -18.6% 29% 10-Year Wage

Details and Analysis of Dr. Ben Carson s Tax Plan

FISCAL FACT Jan. 2016 No. 493 Details and Analysis of Dr. Ben Carson s Tax Plan By Kyle Pomerleau Director of Federal Projects Key Findings Dr. Ben Carson s tax plan would replace the federal income tax

FISCAL FACT Jan. 2016 No. 493 Details and Analysis of Dr. Ben Carson s Tax Plan By Kyle Pomerleau Director of Federal Projects Key Findings Dr. Ben Carson s tax plan would replace the federal income tax

Client Letter: Individual Tax Provisions of the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010

Source: Tax Legislation > 111th Congress (2009-2010) > Enacted > Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (P.L. 111-312) > Practice Tools > Client Letter: Individual

Source: Tax Legislation > 111th Congress (2009-2010) > Enacted > Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (P.L. 111-312) > Practice Tools > Client Letter: Individual

INTERACTION OF AUTOMATIC IRAS AND THE RETIREMENT SAVINGS CONTRIBUTIONS CREDIT (SAVER S CREDIT)

") INTERACTION OF AUTOMATIC IRAS AND THE RETIREMENT SAVINGS CONTRIBUTIONS CREDIT (SAVER S CREDIT) A Report Prepared for AARP By: Optimal Benefit Strategies, LLC Judy Xanthopoulos, PhD Mary M. Schmitt, Esq.

INTERACTION OF AUTOMATIC IRAS AND THE RETIREMENT SAVINGS CONTRIBUTIONS CREDIT (SAVER S CREDIT) A Report Prepared for AARP By: Optimal Benefit Strategies, LLC Judy Xanthopoulos, PhD Mary M. Schmitt, Esq.

Obama Administration Budget Proposals Would Expand Impact on Tax-Favored Retirement Benefits

February 9, 2015 If you have questions, please contact your regular Groom attorney or one of the attorneys listed below: David J. Ashner dashner@groom.com (202) 861-6330 Louis T. Mazawey lmazawey@groom.com

February 9, 2015 If you have questions, please contact your regular Groom attorney or one of the attorneys listed below: David J. Ashner dashner@groom.com (202) 861-6330 Louis T. Mazawey lmazawey@groom.com

MICHIGAN EARNED INCOME TAX CREDIT Tax Year 2013

MICHIGAN EARNED INCOME TAX CREDIT Office of Revenue and Tax Analysis Michigan Department of Treasury February 2015 MICHIGAN EARNED INCOME TAX CREDIT Office of Revenue and Tax Analysis Michigan Department

MICHIGAN EARNED INCOME TAX CREDIT Office of Revenue and Tax Analysis Michigan Department of Treasury February 2015 MICHIGAN EARNED INCOME TAX CREDIT Office of Revenue and Tax Analysis Michigan Department

TAX PROVISIONS IN THE AMERICAN TAXPAYER RELIEF ACT OF 2012 (ATRA) James Nunns and Jeffrey Rohaly Urban-Brookings Tax Policy Center January 9, 2013

James Nunns and Jeffrey Rohaly Urban-Brookings Tax Policy Center January 9, 2013") TAX PROVISIONS IN THE AMERICAN TAXPAYER RELIEF ACT OF 2012 (ATRA) James Nunns and Jeffrey Rohaly Urban-Brookings Tax Policy Center January 9, 2013 ABSTRACT The fiscal cliff debate culminated in the passage

TAX PROVISIONS IN THE AMERICAN TAXPAYER RELIEF ACT OF 2012 (ATRA) James Nunns and Jeffrey Rohaly Urban-Brookings Tax Policy Center January 9, 2013 ABSTRACT The fiscal cliff debate culminated in the passage

2014 Individual Income Tax Changes. Individual Income Tax Law changes effective for tax years beginning on or after January 1, 2014

2014 Individual Income Tax Changes Individual Income Tax Law changes effective for tax years beginning on or after January 1, 2014 Revised 10/15/2014 The NC Department of Revenue provides this information

2014 Individual Income Tax Changes Individual Income Tax Law changes effective for tax years beginning on or after January 1, 2014 Revised 10/15/2014 The NC Department of Revenue provides this information

Hawaii Individual Income Tax Statistics

Hawaii Individual Income Tax Statistics Tax Year 2012 Department of Taxation State of Hawaii Hawaii Individual Income Tax Statistics Tax Year 2012 Department of Taxation State of Hawaii November 2014 Prepared

Hawaii Individual Income Tax Statistics Tax Year 2012 Department of Taxation State of Hawaii Hawaii Individual Income Tax Statistics Tax Year 2012 Department of Taxation State of Hawaii November 2014 Prepared

The American Tax Relief Act of 2012 (HR 8, the Act )

") NATIONAL CAPITAL GIFT PLANNING COUNCIL The Fiscal Cliff, Taxes and Planned Giving: Where Are We Now? Robert E. Madden Susan Leahy BLANK ROME LLP JANUARY 9, 2013 The American Tax Relief Act of 2012 (HR

NATIONAL CAPITAL GIFT PLANNING COUNCIL The Fiscal Cliff, Taxes and Planned Giving: Where Are We Now? Robert E. Madden Susan Leahy BLANK ROME LLP JANUARY 9, 2013 The American Tax Relief Act of 2012 (HR

Client Letter: Individual Tax Provisions of the American Taxpayer Relief Act of 2012

Client Letter: Individual Tax Provisions of the American Taxpayer Relief Act of 2012 Dear Client, On January 2, 2013, President Obama signed the American Taxpayer Relief Act of 2012 (the Act) into law.

Client Letter: Individual Tax Provisions of the American Taxpayer Relief Act of 2012 Dear Client, On January 2, 2013, President Obama signed the American Taxpayer Relief Act of 2012 (the Act) into law.

Social Security and Taxes

Social Security and Taxes Social Security is a safety net for the middle class and a lifeline for millions more. For more than 60 percent of Americans age 65 and over, it provides over 50 percent of their

Social Security and Taxes Social Security is a safety net for the middle class and a lifeline for millions more. For more than 60 percent of Americans age 65 and over, it provides over 50 percent of their

Proposed Repeal of Income Tax Reciprocity Agreement with Wisconsin (January 2002)

") ISSUE BRIEF Proposed Repeal of Income Tax Reciprocity Agreement with Wisconsin (January 2002) The Governor s Supplemental Budget Recommendations for FY 2002-2003 propose to repeal the income tax reciprocity

ISSUE BRIEF Proposed Repeal of Income Tax Reciprocity Agreement with Wisconsin (January 2002) The Governor s Supplemental Budget Recommendations for FY 2002-2003 propose to repeal the income tax reciprocity

CALIFORNIA WITHHOLDING SCHEDULES FOR 2015

California provides two methods for determining the amount of wages and salaries to be withheld for state personal income tax: METHOD A - WAGE BRACKET TABLE METHOD (Limited to wages/salaries less than

California provides two methods for determining the amount of wages and salaries to be withheld for state personal income tax: METHOD A - WAGE BRACKET TABLE METHOD (Limited to wages/salaries less than

Crunch or Crucible? Upcoming Changes in the Federal Tax Law A Special Edition Tax Guide for Friends and Alumni of Pomona College

Upcoming Changes in the Federal Tax Law A Special Edition Tax Guide for Friends and Alumni of Pomona College Pomona College, Office of Trusts & Estates, 550 N. College Ave., Claremont, CA 91711 www.pomona.planyourlegacy.org

Upcoming Changes in the Federal Tax Law A Special Edition Tax Guide for Friends and Alumni of Pomona College Pomona College, Office of Trusts & Estates, 550 N. College Ave., Claremont, CA 91711 www.pomona.planyourlegacy.org

PROVISIONS ENACTED BY THE AMERICAN TAXPAYER RELIEF ACT OF 2012 THAT CREATE CONFORMITY ISSUES WITH A SIGNIFICANT IMPACT ON MAINE INCOME TAXES

PROVISIONS ENACTED BY THE AMERICAN TAXPAYER RELIEF ACT OF 2012 THAT CREATE CONFORMITY ISSUES WITH A SIGNIFICANT IMPACT ON MAINE INCOME TAXES INTRODUCTION Maine income and estate taxes are substantially

PROVISIONS ENACTED BY THE AMERICAN TAXPAYER RELIEF ACT OF 2012 THAT CREATE CONFORMITY ISSUES WITH A SIGNIFICANT IMPACT ON MAINE INCOME TAXES INTRODUCTION Maine income and estate taxes are substantially

Marginal and Average Income Tax Rates and Tax Support for Families with Children and Students as Family Income Increases 2015 Law

Marginal and Average Income Tax Rates and Tax Support for Families with Children and Students as Family Income Increases 2015 Law 2 The amount of income tax owed and tax benefits received at any level

Marginal and Average Income Tax Rates and Tax Support for Families with Children and Students as Family Income Increases 2015 Law 2 The amount of income tax owed and tax benefits received at any level

State Tax of Social Security Income. State Tax of Pension Income. State

State Taxation of Retirement Income The following chart shows generally which states tax retirement income, including and pension States shaded indicate they do not tax these forms of retirement State

State Taxation of Retirement Income The following chart shows generally which states tax retirement income, including and pension States shaded indicate they do not tax these forms of retirement State

Executive Summary. 204 N. First St., Suite C PO Box 7 Silverton, OR 97381 www.ocpp.org 503-873-1201 fax 503-873-1947

Executive Summary 204 N. First St., Suite C PO Box 7 Silverton, OR 97381 www.ocpp.org 503-873-1201 fax 503-873-1947 On Whose Backs? Tax Distribution, Income Inequality, and Plans for Raising Revenue By

Executive Summary 204 N. First St., Suite C PO Box 7 Silverton, OR 97381 www.ocpp.org 503-873-1201 fax 503-873-1947 On Whose Backs? Tax Distribution, Income Inequality, and Plans for Raising Revenue By

Unit 4: Taxes. Read this unit including websites. You may want to take your own notes.

Taxes Read Chapter 4 in the text. Read Chapter 7 of The Financial Checkup. Read this unit including websites. You may want to take your own notes. Are taxes your favorite topic? They are not the favorite

Taxes Read Chapter 4 in the text. Read Chapter 7 of The Financial Checkup. Read this unit including websites. You may want to take your own notes. Are taxes your favorite topic? They are not the favorite

OPTIONS TO REFORM THE DEDUCTION FOR HOME MORTGAGE INTEREST

OPTIONS TO REFORM THE DEDUCTION FOR HOME MORTGAGE INTEREST Chenxi Lu, Joseph Rosenberg, and Eric Toder December 8, 2015 ABSTRACT Taxpayers can currently deduct interest on up to $1 million in acquisition

OPTIONS TO REFORM THE DEDUCTION FOR HOME MORTGAGE INTEREST Chenxi Lu, Joseph Rosenberg, and Eric Toder December 8, 2015 ABSTRACT Taxpayers can currently deduct interest on up to $1 million in acquisition

PREVIEW. California Tax Facts. An Overview of the Golden State s Tax Structure

PREVIEW California Tax Facts An Overview of the Golden State s Tax Structure 1 PREVIEW California Tax Facts An Overview of the Golden State s Tax Structure 3 ABOUT THE CALIFORNIA TAX FOUNDATION The California

PREVIEW California Tax Facts An Overview of the Golden State s Tax Structure 1 PREVIEW California Tax Facts An Overview of the Golden State s Tax Structure 3 ABOUT THE CALIFORNIA TAX FOUNDATION The California

INDIVIDUAL TAX STRATEGIES

BY SCOTT HENSLEY SHENSLEY@STANCILCPA.COM DECEMBER 4, 2014 STANCIL & COMPANY CERTIFIED PUBLIC ACCOUNTANTS 4909 WINDY HILL DRIVE RALEIGH, NC 27609 919-872-1260 TOPICS TO BE COVERED TODAY WHAT IS TAX PLANNING

BY SCOTT HENSLEY SHENSLEY@STANCILCPA.COM DECEMBER 4, 2014 STANCIL & COMPANY CERTIFIED PUBLIC ACCOUNTANTS 4909 WINDY HILL DRIVE RALEIGH, NC 27609 919-872-1260 TOPICS TO BE COVERED TODAY WHAT IS TAX PLANNING

H.R. 1836 CONGRESSIONAL BUDGET OFFICE PAY-AS-YOU-GO ESTIMATE. Economic Growth and Tax Relief Reconciliation Act of 2001.

CONGRESSIONAL BUDGET OFFICE PAY-AS-YOU-GO ESTIMATE June 4, 2001 H.R. 1836 Economic Growth and Tax Relief Reconciliation Act of 2001 As cleared by the Congress on May 26, 2001 SUMMARY The Economic Growth

CONGRESSIONAL BUDGET OFFICE PAY-AS-YOU-GO ESTIMATE June 4, 2001 H.R. 1836 Economic Growth and Tax Relief Reconciliation Act of 2001 As cleared by the Congress on May 26, 2001 SUMMARY The Economic Growth

Why Some Tax Units Pay No Income Tax

Why Some Tax Units Pay No Income Tax Rachel Johnson, James Nunns, Jeffrey Rohaly, Eric Toder, Roberton Williams Urban-Brookings Tax Policy Center July 2011 ABSTRACT About 46 percent of American households

Why Some Tax Units Pay No Income Tax Rachel Johnson, James Nunns, Jeffrey Rohaly, Eric Toder, Roberton Williams Urban-Brookings Tax Policy Center July 2011 ABSTRACT About 46 percent of American households

Oregon Personal Income Tax Statistics

Oregon Personal Income Tax Statistics - 2014 Edition - Tax Year 2012 Oregon Personal Income Tax Statistics Characteristics of Filers 2014 Edition Tax Year 2012 150-101-406 (Rev. 3-14) To order additional

Oregon Personal Income Tax Statistics - 2014 Edition - Tax Year 2012 Oregon Personal Income Tax Statistics Characteristics of Filers 2014 Edition Tax Year 2012 150-101-406 (Rev. 3-14) To order additional

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences

We will continue to expand on the provisions of the taxpayer relief act as more information becomes available. If you have any questions please feel free to contact us. Congress passes 2012 Taxpayer Relief

We will continue to expand on the provisions of the taxpayer relief act as more information becomes available. If you have any questions please feel free to contact us. Congress passes 2012 Taxpayer Relief

Traditional IRA s Contribution rules-

A Traditional IRA is a retirement plan that allows you to save money for retirement. In the case of a traditional IRA, you may also be offered an immediate tax shelter for the contributions that you make

A Traditional IRA is a retirement plan that allows you to save money for retirement. In the case of a traditional IRA, you may also be offered an immediate tax shelter for the contributions that you make

LEGISLATIVE SERVICES AGENCY OFFICE OF FISCAL AND MANAGEMENT ANALYSIS 301 State House (317) 232-9855

232-9855") LEGISLATIVE SERVICES AGENCY OFFICE OF FISCAL AND MANAGEMENT ANALYSIS 301 State House (317) 232-9855 FISCAL IMPACT STATEMENT LS 7482 DATE PREPARED: Mar 30, 2001 BILL NUMBER: SB 199 BILL AMENDED: Mar 29,

LEGISLATIVE SERVICES AGENCY OFFICE OF FISCAL AND MANAGEMENT ANALYSIS 301 State House (317) 232-9855 FISCAL IMPACT STATEMENT LS 7482 DATE PREPARED: Mar 30, 2001 BILL NUMBER: SB 199 BILL AMENDED: Mar 29,

CAMP TAX REFORM DISCUSSION DRAFT PROVISIONS OF INTEREST TO COLLEGES AND UNIVERSITIES

Student & Family Education Tax Benefits American Opportunity Tax Credit (AOTC) Modifies and makes permanent the AOTC. Decreases current AOTC income phase out levels for eligibility to $43,000-$63,000 for

Student & Family Education Tax Benefits American Opportunity Tax Credit (AOTC) Modifies and makes permanent the AOTC. Decreases current AOTC income phase out levels for eligibility to $43,000-$63,000 for

The Impact of Proposed Federal Tax Reform on Farm Businesses

The Impact of Proposed Federal Tax Reform on Farm Businesses James M. Williamson and Ron Durst United States Department of Agriculture Economic Research Service Washington, DC Poster prepared for presentation

The Impact of Proposed Federal Tax Reform on Farm Businesses James M. Williamson and Ron Durst United States Department of Agriculture Economic Research Service Washington, DC Poster prepared for presentation

Roth 403(b): Is it right for you?

: Is it right for you?") Roth 403(b): Is it right for you? We recommend that you consult a tax or financial advisor about your individual situation. This material may be used in conjunction with the offering of shares of any Vanguard

Roth 403(b): Is it right for you? We recommend that you consult a tax or financial advisor about your individual situation. This material may be used in conjunction with the offering of shares of any Vanguard

2014 Tax Newsletter HIGHLIGHTS. Potential Tax Reform. 2014 Income Tax Rates. 2014 Tax Extenders. Repair Regulations. Affordable Care Act

5700 Crooks Rd., Ste. 201 Troy, MI 48098 Phone: 248.649.1600 2014 Tax Newsletter Dear Client: 1785 W. Stadium Blvd., Ste. 101 Ann Arbor, MI 48103 Phone: 734.665.6688 www.smcpafirm.com Although 2014 was

5700 Crooks Rd., Ste. 201 Troy, MI 48098 Phone: 248.649.1600 2014 Tax Newsletter Dear Client: 1785 W. Stadium Blvd., Ste. 101 Ann Arbor, MI 48103 Phone: 734.665.6688 www.smcpafirm.com Although 2014 was

Details and Analysis of Senator Bernie Sanders s Tax Plan

FISCAL FACT Jan. 2016 No. 498 Details and Analysis of Senator Bernie Sanders s Tax Plan By Alan Cole and Scott Greenberg Economist Analyst Key Findings: Senator Sanders (I-VT) would enact a number of policies

FISCAL FACT Jan. 2016 No. 498 Details and Analysis of Senator Bernie Sanders s Tax Plan By Alan Cole and Scott Greenberg Economist Analyst Key Findings: Senator Sanders (I-VT) would enact a number of policies

2011 Tax And Financial Planning Tables

2011 Tax and Financial PLanning Tables Investment Planning 2011 Tax And Financial Planning Tables Tax planning is an important component for your overall financial plan. 2011 Tax and Financial PLanning

2011 Tax and Financial PLanning Tables Investment Planning 2011 Tax And Financial Planning Tables Tax planning is an important component for your overall financial plan. 2011 Tax and Financial PLanning

Individual Retirement Arrangements (IRAs)

") Department of the Treasury Internal Revenue Service Publication 590 Cat. No. 15160x Individual Retirement Arrangements (IRAs) (Including Roth IRAs and Education IRAs) For use in preparing 1999 Returns

Department of the Treasury Internal Revenue Service Publication 590 Cat. No. 15160x Individual Retirement Arrangements (IRAs) (Including Roth IRAs and Education IRAs) For use in preparing 1999 Returns

LIFE INSURANCE DIVISION

TAX LAW SUMMARY American Taxpayer Relief Act MKTG-OC-1053A LIFE INSURANCE DIVISION TAX LAW SUMMARY American Taxpayer Relief Act INDIVIDUAL TAX PROVISIONS...3 Individual Tax Rates...3 Marriage Penalty Relief...4

TAX LAW SUMMARY American Taxpayer Relief Act MKTG-OC-1053A LIFE INSURANCE DIVISION TAX LAW SUMMARY American Taxpayer Relief Act INDIVIDUAL TAX PROVISIONS...3 Individual Tax Rates...3 Marriage Penalty Relief...4

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE CBO. The Distribution of Household Income and Federal Taxes, 2008 and 2009

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Percent 70 The Distribution of Household Income and Federal Taxes, 2008 and 2009 60 50 Before-Tax Income Federal Taxes Top 1 Percent 40 30 20 81st

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Percent 70 The Distribution of Household Income and Federal Taxes, 2008 and 2009 60 50 Before-Tax Income Federal Taxes Top 1 Percent 40 30 20 81st

The Child Tax Credit: Problems with the Refundable Portion

The Child Tax Credit: Problems with the Refundable Portion * Katherine D. Black and **Sheldon R. Smith Utah Valley State College This article discusses the current tax code with respect to the child tax

The Child Tax Credit: Problems with the Refundable Portion * Katherine D. Black and **Sheldon R. Smith Utah Valley State College This article discusses the current tax code with respect to the child tax

Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 (608) 266-3847 Fax: (608) 267-6873

266-3847 Fax: (608) 267-6873") Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 (608) 266-3847 Fax: (608) 267-6873 May 25, 2005 Joint Committee on Finance Paper #316 Increase Individual Income Tax Deduction for College

Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 (608) 266-3847 Fax: (608) 267-6873 May 25, 2005 Joint Committee on Finance Paper #316 Increase Individual Income Tax Deduction for College

2016 Individual Income Tax Rates, Standard Deductions, Personal Exemptions, and Filing Thresholds

15-Oct-15 2016 Individual Income Tax Rates, Standard Deductions, Personal Exemptions, and Filing Thresholds If your filing status is Single If your filing status is jointly $0 $9,275 10% $0 $18,550 10%

15-Oct-15 2016 Individual Income Tax Rates, Standard Deductions, Personal Exemptions, and Filing Thresholds If your filing status is Single If your filing status is jointly $0 $9,275 10% $0 $18,550 10%

The Minnesota Income Tax Marriage Credit

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Nina Manzi, Legislative Analyst, 651-296-5204 Joel Michael, Legislative Analyst, joel.michael@house.mn

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Nina Manzi, Legislative Analyst, 651-296-5204 Joel Michael, Legislative Analyst, joel.michael@house.mn

2015 YEAR-END INDIVIDUAL TAX PLANNING LETTER

2015 YEAR-END INDIVIDUAL TAX PLANNING LETTER Dear Reliance Accounting Clients, At this point in 2015, with the end of the year and the income tax filing deadline on the horizon, tax planning presents more

2015 YEAR-END INDIVIDUAL TAX PLANNING LETTER Dear Reliance Accounting Clients, At this point in 2015, with the end of the year and the income tax filing deadline on the horizon, tax planning presents more

Wealth Management Systems Inc. 2015 Tax Guide. What You Need to Know About the New Rules

Wealth Management Systems Inc. 2015 Tax Guide What You Need to Know About the New Rules Tax Guide 2015 This guide is not intended to be tax advice and should not be treated as such. Each individual s tax

Wealth Management Systems Inc. 2015 Tax Guide What You Need to Know About the New Rules Tax Guide 2015 This guide is not intended to be tax advice and should not be treated as such. Each individual s tax

SELECTED PROVISIONS OF MAJOR TAX LEGISLATION BY ACT 1981 to 2006 PROVISION ERTA 1981 TRA 1986 OBRA 1989 OBRA 1990 OBRA 1993 TRA 1997 EGTRRA 2001

SELECTED PROVISIONS OF MAJOR TAX LEGISLATION BY ACT 1981 to 2006 PROVISION ERTA 1981 TRA 1986 OBRA 1989 OBRA 1990 OBRA 1993 TRA 1997 EGTRRA 2001 Tax Rates Reduced marginal tax rates by 23% over 3 years,

SELECTED PROVISIONS OF MAJOR TAX LEGISLATION BY ACT 1981 to 2006 PROVISION ERTA 1981 TRA 1986 OBRA 1989 OBRA 1990 OBRA 1993 TRA 1997 EGTRRA 2001 Tax Rates Reduced marginal tax rates by 23% over 3 years,

Homestead Tax Credit

Homestead Tax Credit Prepared by Al Runde Wisconsin Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 Homestead Tax Credit Introduction The homestead tax credit program directs property

Homestead Tax Credit Prepared by Al Runde Wisconsin Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 Homestead Tax Credit Introduction The homestead tax credit program directs property

Appropriate Checklists for Year-End Tax Planning

LPL Financial Dennis R. Marvin, CFP Branch Manager 28025 Clemens Road Suite 2A Westlake, OH 44145 440-250-9990 Fax: 440-250-9986 dennis@marvinwealth.com www.marvinwealth.com Appropriate Checklists for

LPL Financial Dennis R. Marvin, CFP Branch Manager 28025 Clemens Road Suite 2A Westlake, OH 44145 440-250-9990 Fax: 440-250-9986 dennis@marvinwealth.com www.marvinwealth.com Appropriate Checklists for

NORTHEAST INVESTORS TRUST. 125 High Street Boston, MA 02110 Telephone: 800-225-6704

NORTHEAST INVESTORS TRUST traditional IRA INVESTOR S KIT 125 High Street Boston, MA 02110 Telephone: 800-225-6704 Table of Contents NORTHEAST INVESTORS TRUST TRADITIONAL IRA DISCLOSURE STATEMENT...1 INTRODUCTION...1

NORTHEAST INVESTORS TRUST traditional IRA INVESTOR S KIT 125 High Street Boston, MA 02110 Telephone: 800-225-6704 Table of Contents NORTHEAST INVESTORS TRUST TRADITIONAL IRA DISCLOSURE STATEMENT...1 INTRODUCTION...1

Roth IRAs The Roth IRA

Roth IRAs The Roth IRA 2010 and 2011 Questions & Answers What is a Roth Individual Retirement Account (Roth IRA)? A Roth IRA is a type of tax-preferred savings and investment account authorized by Internal

Roth IRAs The Roth IRA 2010 and 2011 Questions & Answers What is a Roth Individual Retirement Account (Roth IRA)? A Roth IRA is a type of tax-preferred savings and investment account authorized by Internal

Families. 2014 Tax Bill. Provision What Changed? Who Qualifies? What's the Benefit? Working Family Credit. Marriage Penalty Relief

Working Family 2014 Tax Bill Families Increased benefit for all who receive the credit. Simpler calculation that s easier to understand. 330,000 current and 13,000 new single or married taxpayers who meet

Working Family 2014 Tax Bill Families Increased benefit for all who receive the credit. Simpler calculation that s easier to understand. 330,000 current and 13,000 new single or married taxpayers who meet

The FY 2015 Budget Takes Steps toward Correcting DC s Unbalanced Tax System

DRAFTDRA An Affiliate of the Center on Budget and Policy Priorities 820 First Street NE, Suite 460 Washington, DC 20002 (202) 408-1080 Fax (202) 325-8839 www.dcfpi.org Testimony of Jenny Reed, Policy Director

DRAFTDRA An Affiliate of the Center on Budget and Policy Priorities 820 First Street NE, Suite 460 Washington, DC 20002 (202) 408-1080 Fax (202) 325-8839 www.dcfpi.org Testimony of Jenny Reed, Policy Director

Substitute W-4P Tax Withholding Certificate for Pension or Annuity Payments Wis. Stat. 40.08 (1)

") Substitute W-4P Tax Withholding Certificate for Pension or Annuity Payments Wis. Stat. 40.08 (1) Wisconsin Department of Employee Trust Funds 801 W Badger Road PO Box 7931 Madison WI 53707-7931 1-877-533-5020

Substitute W-4P Tax Withholding Certificate for Pension or Annuity Payments Wis. Stat. 40.08 (1) Wisconsin Department of Employee Trust Funds 801 W Badger Road PO Box 7931 Madison WI 53707-7931 1-877-533-5020

Slide 2. Income Taxes

Slide 1 Taxes Income taxes have been a part of American life since 1909 when the 16 th Amendment to the Constitution was ratified. You can t avoid taxes, so you might as well understand how taxes are structured

Slide 1 Taxes Income taxes have been a part of American life since 1909 when the 16 th Amendment to the Constitution was ratified. You can t avoid taxes, so you might as well understand how taxes are structured

Tax-Savvy Planning for College Expenses

3/31/14 Tax-Savvy Planning for College Expenses The American Opportunity Tax Credit Remains Available through 2017 If you are a parent with hopes of future college diplomas for your children, you are likely

3/31/14 Tax-Savvy Planning for College Expenses The American Opportunity Tax Credit Remains Available through 2017 If you are a parent with hopes of future college diplomas for your children, you are likely

An Overview of The Tax Relief Act on 2010

An Overview of The Tax Relief Act on 2010 On December 17, 2010, the President signed a multi-billion dollar tax cut package, the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act

An Overview of The Tax Relief Act on 2010 On December 17, 2010, the President signed a multi-billion dollar tax cut package, the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act

Income, Gift, and Estate Tax Update

Income, Gift, and Estate Tax Update Individual Income Tax Rates p. 1 Phil Harris Department of Agricultural and Applied Economics University of Wisconsin-Madison Marriage Penalty Relief p. 1 Capital Gains

Income, Gift, and Estate Tax Update Individual Income Tax Rates p. 1 Phil Harris Department of Agricultural and Applied Economics University of Wisconsin-Madison Marriage Penalty Relief p. 1 Capital Gains

*Brackets adjusted for inflation in future years. 2015 Long Term Capital Gains & Dividends Taxable income up to $413,200/$457,600 0% - 15%*

Income Tax Planning Overview The American Taxpayer Relief Act of 2012 extended prior law for certain income tax rates; however, it also increased income tax rates on upper income earners. Specifically,

Income Tax Planning Overview The American Taxpayer Relief Act of 2012 extended prior law for certain income tax rates; however, it also increased income tax rates on upper income earners. Specifically,

2015 -- S 0163 S T A T E O F R H O D E I S L A N D

======== LC000 ======== 01 -- S 01 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO TAXATION - PERSONAL INCOME TAX Introduced By: Senators Goldin,

======== LC000 ======== 01 -- S 01 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO TAXATION - PERSONAL INCOME TAX Introduced By: Senators Goldin,

National Small Business Network

National Small Business Network WRITTEN STATEMENT FOR THE RECORD US SENATE COMMITTEE ON FINANCE U.S. HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS JOINT HEARING ON TAX REFORM AND THE TAX TREATMENT

National Small Business Network WRITTEN STATEMENT FOR THE RECORD US SENATE COMMITTEE ON FINANCE U.S. HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS JOINT HEARING ON TAX REFORM AND THE TAX TREATMENT

Small Business Health Care Tax Credit: Frequently Asked Questions

Small Business Health Care Tax Credit: Frequently Asked Questions The new health reform law gives a tax credit to certain small employers that provide health care coverage to their employees, effective

Small Business Health Care Tax Credit: Frequently Asked Questions The new health reform law gives a tax credit to certain small employers that provide health care coverage to their employees, effective

How Can You Reduce Your Taxes?

RON GRAHAM AND ASSOCIATES LTD. 10585 111 Street NW, Edmonton, Alberta, T5M 0L7 Telephone (780) 429-6775 Facsimile (780) 424-0004 Email rgraham@rgafinancial.com How Can You Reduce Your Taxes? Tax Brackets.

RON GRAHAM AND ASSOCIATES LTD. 10585 111 Street NW, Edmonton, Alberta, T5M 0L7 Telephone (780) 429-6775 Facsimile (780) 424-0004 Email rgraham@rgafinancial.com How Can You Reduce Your Taxes? Tax Brackets.

Property Tax Relief: The $7 Billion Reality

August 2008 Property Tax Relief: The $7 Billion Reality In the spring of 2006, Texas lawmakers passed a massive package of school finance reforms. School tax rates for maintenance and operations were to

August 2008 Property Tax Relief: The $7 Billion Reality In the spring of 2006, Texas lawmakers passed a massive package of school finance reforms. School tax rates for maintenance and operations were to

American Taxpayer Relief Act of 2012- UPDATED

American Taxpayer Relief Act of 2012- UPDATED On January 2, 2013, the President signed the American Taxpayer Relief Act, thus ending the nation s brief stint over the fiscal cliff a confluence of expiring

American Taxpayer Relief Act of 2012- UPDATED On January 2, 2013, the President signed the American Taxpayer Relief Act, thus ending the nation s brief stint over the fiscal cliff a confluence of expiring

2010 Update for The Case Approach to Financial Planning: Writing a Financial Plan

2010 Update for The Case Approach to Financial Planning: Writing a Financial Plan The 2010 update includes a 2009 and 2010 version of the Financial Facilitator spreadsheet, a few errata, some 2009 and

2010 Update for The Case Approach to Financial Planning: Writing a Financial Plan The 2010 update includes a 2009 and 2010 version of the Financial Facilitator spreadsheet, a few errata, some 2009 and

Social Security Benefits and the 55.5% Tax Bracket. by Larry Layton CPA

Social Security Benefits and the 55.5% Tax Bracket by Larry Layton CPA Every year there is a lot of press regarding the need for Congress to step in and provide an income adjustment for the Alternative

Social Security Benefits and the 55.5% Tax Bracket by Larry Layton CPA Every year there is a lot of press regarding the need for Congress to step in and provide an income adjustment for the Alternative

THE IRA CHARITABLE ROLLOVER

THE IRA CHARITABLE ROLLOVER The IRA Charitable Rollover was first added to the Internal Revenue Code of 1986, as amended, under legislation enacted in 2006. It permitted individuals to roll over up to

THE IRA CHARITABLE ROLLOVER The IRA Charitable Rollover was first added to the Internal Revenue Code of 1986, as amended, under legislation enacted in 2006. It permitted individuals to roll over up to

BY REQUEST OF THE REVENUE AND TRANSPORTATION INTERIM COMMITTEE A BILL FOR AN ACT ENTITLED: "AN ACT REVISING CERTAIN PROVISIONS RELATED TO THE

SB00.0 SENATE BILL NO. INTRODUCED BY F. THOMAS BY REQUEST OF THE REVENUE AND TRANSPORTATION INTERIM COMMITTEE A BILL FOR AN ACT ENTITLED: "AN ACT REVISING CERTAIN PROVISIONS RELATED TO THE ADMINISTRATION

SB00.0 SENATE BILL NO. INTRODUCED BY F. THOMAS BY REQUEST OF THE REVENUE AND TRANSPORTATION INTERIM COMMITTEE A BILL FOR AN ACT ENTITLED: "AN ACT REVISING CERTAIN PROVISIONS RELATED TO THE ADMINISTRATION

Tax Subsidies for Private Health Insurance

Tax Subsidies for Private Health Insurance Matthew Rae, Gary Claxton, Nirmita Panchal, Larry Levitt The federal and state tax systems provide significant financial benefits for people with private health

Tax Subsidies for Private Health Insurance Matthew Rae, Gary Claxton, Nirmita Panchal, Larry Levitt The federal and state tax systems provide significant financial benefits for people with private health

CRS Report for Congress Received through the CRS Web

CRS Report for Congress Received through the CRS Web Order Code 96-20 EPW Updated January 10, 2001 Summary Individual Retirement Accounts (IRAs): Legislative Issues in the 106 th Congress James R. Storey

CRS Report for Congress Received through the CRS Web Order Code 96-20 EPW Updated January 10, 2001 Summary Individual Retirement Accounts (IRAs): Legislative Issues in the 106 th Congress James R. Storey

How To Get A Small Business Tax Credit

2010 FOCUS ON BUSINESS December 1, 2010 FEDERAL TAX UPDATE 2010 SMALL BUSINESS JOBS ACT & MISCELLANEOUS TAX PROVISIONS PRESENTED BY: DAVID P. VENISKEY, CPA TAX PARTNER EFP ROTENBERG, LLP TAX RATES Income

2010 FOCUS ON BUSINESS December 1, 2010 FEDERAL TAX UPDATE 2010 SMALL BUSINESS JOBS ACT & MISCELLANEOUS TAX PROVISIONS PRESENTED BY: DAVID P. VENISKEY, CPA TAX PARTNER EFP ROTENBERG, LLP TAX RATES Income

Department of Legislative Services

Department of Legislative Services Maryland General Assembly 2000 Session HB 12 House Bill 12 (Delegate Taylor, et al.) Ways and Means FISCAL NOTE Revised Income Tax Reduction This bill accelerates the

Department of Legislative Services Maryland General Assembly 2000 Session HB 12 House Bill 12 (Delegate Taylor, et al.) Ways and Means FISCAL NOTE Revised Income Tax Reduction This bill accelerates the

The Revenue and Taxpayer Impacts of the Income Tax Provisions of SB 407

The Revenue and Taxpayer Impacts of the Income Tax Provisions of SB 407 Tax Policy and Research Montana Department of Revenue December 2006 Executive Summary Senate Bill 407, enacted in the 2003 legislative

The Revenue and Taxpayer Impacts of the Income Tax Provisions of SB 407 Tax Policy and Research Montana Department of Revenue December 2006 Executive Summary Senate Bill 407, enacted in the 2003 legislative

Sidney Levine, David Graffagnino, Joseph DeRosa, & Jon Xynidis

December 2009 Dear Reader, The Senate passed a motion at the beginning of the Thanksgiving week to move forward on the Health Care Reform legislation removing a substantial roadblock for work on this bill.

December 2009 Dear Reader, The Senate passed a motion at the beginning of the Thanksgiving week to move forward on the Health Care Reform legislation removing a substantial roadblock for work on this bill.

Private Health Insurance: Changes Made by the Reconciliation Act of 2010 to Senate-Passed H.R. 3590

Private Health Insurance: Changes Made by the Reconciliation Act of 2010 to Senate-Passed H.R. 3590 Hinda Chaikind Specialist in Health Care Financing Bernadette Fernandez Analyst in Health Care Financing

Private Health Insurance: Changes Made by the Reconciliation Act of 2010 to Senate-Passed H.R. 3590 Hinda Chaikind Specialist in Health Care Financing Bernadette Fernandez Analyst in Health Care Financing

To Roth Or Not To Roth?

To Roth Or Not To Roth? 05.07.2015 FPA Rhode Island Michael E. Kitces MSFS, MTAX, CFP, CLU, ChFC, RHU, REBC, CASL Partner. Director of Research, Pinnacle Advisory Group Publisher. The Kitces Report, www.kitces.com

To Roth Or Not To Roth? 05.07.2015 FPA Rhode Island Michael E. Kitces MSFS, MTAX, CFP, CLU, ChFC, RHU, REBC, CASL Partner. Director of Research, Pinnacle Advisory Group Publisher. The Kitces Report, www.kitces.com

BUDGET PAPER C: PERSONAL INCOME TAXES

BUDGET PAPER C: PERSONAL INCOME TAXES This section presents detail on the changes to Provincial Personal Income Taxes which become effective during fiscal year 2000-01. I. PRINCE EDWARD ISLAND TAX REDUCTIONS

BUDGET PAPER C: PERSONAL INCOME TAXES This section presents detail on the changes to Provincial Personal Income Taxes which become effective during fiscal year 2000-01. I. PRINCE EDWARD ISLAND TAX REDUCTIONS

IRAs & Roth IRAs. IRA Opportunities. Contribution Limits For 2014 and 2015. Questions & Answers

IRAs & Roth IRAs IRA Opportunities Contribution Limits For 2014 and 2015 Questions & Answers What is the purpose of this brochure? It explains the basic tax rules for traditional IRAs and Roth IRAs. TRADITIONAL

IRAs & Roth IRAs IRA Opportunities Contribution Limits For 2014 and 2015 Questions & Answers What is the purpose of this brochure? It explains the basic tax rules for traditional IRAs and Roth IRAs. TRADITIONAL

Health-Care Reform. Begley Insurance Group, Inc. Mary Angelo 5225 Old Orchard Rd. Skokie, IL 60077 800-867-7074

Begley Insurance Group, Inc. Mary Angelo 5225 Old Orchard Rd. Skokie, IL 60077 800-867-7074 Health-Care Reform August 14, 2012 Page 1 of 8, see disclaimer on final page One primary goal of the Patient

Begley Insurance Group, Inc. Mary Angelo 5225 Old Orchard Rd. Skokie, IL 60077 800-867-7074 Health-Care Reform August 14, 2012 Page 1 of 8, see disclaimer on final page One primary goal of the Patient