Financial Education for Homeowners

|

|

|

- Alicia Heath

- 8 years ago

- Views:

Transcription

1 Financial Education for Homeowners

2 Tax Time Coalition of Central Ohio MISSION: To provide the central Ohio community with information about, and access to, free, high-quality tax assistance services and financial resources that enable low and moderate-income households achieve financial stability.

3

4 Tax Time Background Tax time is the most important financial moment of the year for low income households More than 55,000 of the lowest income working taxpayers in Franklin County pay to have their taxes prepared spending an average of $250 The average refund for a Tax Time client in 2013 was $1,018 In 2013, Tax Time helped 14,530 Franklin County families file their federal and state tax returns and receive $14.8 million in refunds

5 Financial Behavioral Change at Tax Time Tax Time is a great time to kick start savings habits Tax refund provides additional cash Clients are already thinking about finances Tax sites are already recruiting and training volunteers to work one on one with clients

6 Financial Resource Guide Education and Employment Financial Counseling & Credit Repair Additional Resources Additional Resources

7 Financial Coaching Connect taxpayers to financial opportunities at Tax Time free tax preparation sites Encourage taxpayers to develop a plan for their refund Achieve client-defined goals and support specific actions to meet these goals Address immediate financial issues and improve financial situations Facilitate decision-making and provide tools, resources, and referrals

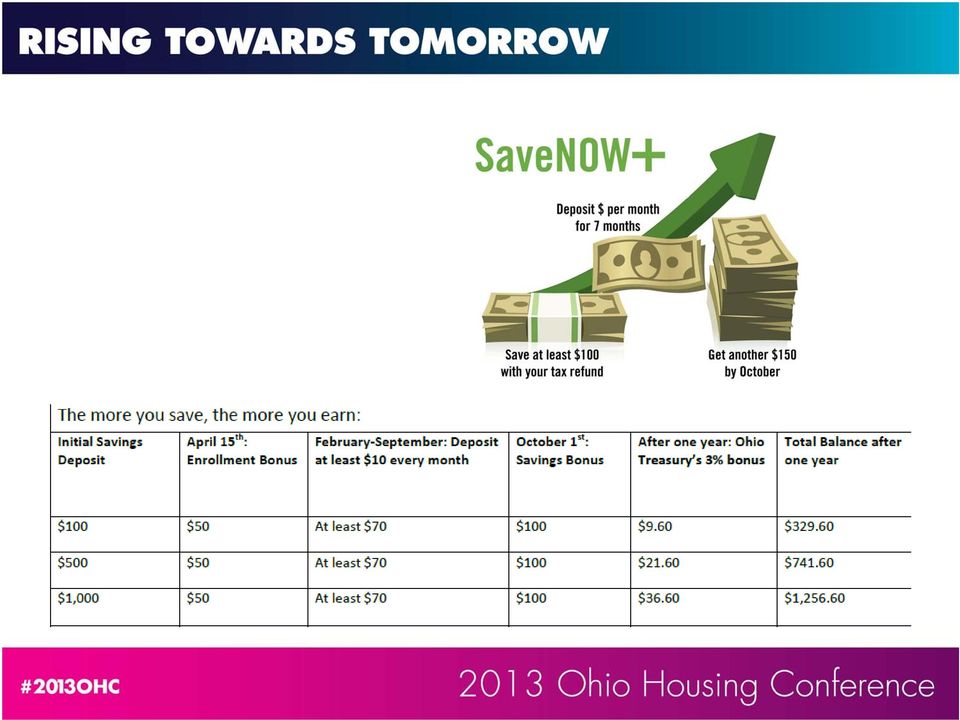

8 SaveNOW+ Unique, incentivized savings account designed to encourage development of regular savings habits Partnership between: - United Way of Central Ohio - The Ohio Treasurer of State s office, - The JP Morgan Chase Foundation - Nationwide Bank

9

10 Lessons Learned Tax sites are great locations to encourage financial behavioral change! Don t reinvent the wheel Recruit and train volunteers specifically for Financial Coaching Simplify the process Market the additional financial opportunities at tax time

11 Contact Information Sarah Harrigan Special Projects Manager, United Way of Central Ohio (614)

227-2733 Sarah.")

12 Using Behavioral Economics for Financial Empowerment: The NHSGC Model

13 What are assets? Income Savings Benefits Tax credits and deductions Education Housing/home equity Long-term savings/stocks/bonds Access to safe and sound financial services Assets move families beyond living paycheck to paycheck and give them tools to plan for the future. Getting by may require only a paycheck, but getting ahead requires a variety of assets, a financial safety net, education and health care.

14 Why do assets matter? Where does housing meet assets? Asset poverty rates and wealth gaps are worse than income poverty and distribution Assets help to increase: Household economic stability Educational attainment Economic mobility Community stability

15 Household Financial Security Framework LEARN Assets increase earning capacity Why Assets? Possession of knowledge and skills that enable navigation of and success in markets (labor, financial) have direct bearing on financial security: K-12 & Postsecondary Education: Basic literacy and math skills, plus commitment to lifelong learning are critical for employment and advancement Financial Education & Counseling: Timely, relevant, accurate information on basic budgeting, taxes, financial products and services, and use of credit Asset-specific Education: Preparation for homeownership, business ownership, postsecondary education, and financial investments EARN SAVE INVEST Wage Income + Business Income + Public &Employer Benefits + Tax Credits + Investment Income = INCOME Ability to Maximize Income Depends On: Access to reliable basic goods and services (housing, transportation, medical care, child care, food) Available quality job and business opportunities Access to public benefits and tax credits (e.g., EITC, Child Care) Asset ownership (higher education, home, business, financial investments) Knowledge and skills related to work, taxes and benefits INCOME - Current Consumption - Debt Payments = SAVINGS Ability to Save Depends On: Access to affordable basic goods and services (housing, transportation, medical care, child care, food) Convenient, low-cost financial products (transaction and savings vehicles, credit and insurance products) Convenient, affordable financial structures (e.g., direct deposit, automatic enrollment, online banking, bank location) Knowledge and skills related to money management, financial products,and credit building and repair. PROTECT SAVINGS + Borrowing + Public Incentives = ASSETS Ability to Build Assets Depends On: Price and appreciation of assets (higher education, home, business, financial investments) Affordable financing Access to public incentives (e.g., downpayment assistance, government loan guarantees, Pell Grants, IDA/CSA match) Knowledge and skills related to asset purchase and management Financial security gains must be protected against loss of income or assets, extraordinary costs, and harmful or predatory external forces. Insurance (public or private): Protects against loss of income or assets as well as against extraordinary costs (e.g. Unemployment, Disability, Life, Health/medical, Property) Consumer Protections: Protect Consumers from deceptive and/or predatory practices (e.g. predatory mortgage lending, payday lending, banking practices) Asset preservation: Depends on government policies (e.g. community investments, blight ordinances, foreclosure prevention) and market conditions

16 How are we bringing it into our model? Savings and assets provide a personal safety net during tough times and are essential to financial security and stability Two decades of product development and program delivery have demonstrated the right way for low- and moderate income people to build wealth: Structure and incentives to facilitate savings (behavioral economics) High quality and culturally relevant financial and asset-specific education Access to fair and reasonably priced credit Multiple approaches to poverty reduction and wealth creation Home ownership Business development and job creation Education and training

High quality and culturally relevant financial and asset-specific education Access to fair and reasonably priced credit Multiple")

17 Our programs on the continuum Homebuyer education (LEARN) Free tax preparation (EARN) Financial capabilities coaching (LEARN) Foreclosure prevention counseling (PROTECT) Cleveland Saves (SAVE) Down-Payment Assistance (INVEST) Reverse mortgage counseling (PROTECT) Consumer Law Center (PROTECT) Community LandTrust Program (INVEST)

Consumer Law Center (PROTECT) Community LandTrust Program")

18 What s next? IDAs (Combining housing and small home business) Child Savings Account assistance (Largest CSA creation in history) Alternatives to payday lending More affordable property units through LandTrust

Alternatives to payday lending")

19 DAVID ROTHSTEIN Director of Resource Development & Public Affairs NHS of Greater Cleveland x 340 DRothstein@nhscleveland.org Facebook LinkedIn Community Shares Twitter (@dbrothstein)

20 Comparisons

21 Why Coaching? Common Behavioral Biases Myopic Decision Frames Procrastination Difficulties with Self Regulation Inattention Coaching Components Set client-defined goals Develop action plan Identify resources, tools & services Monitor client progress Make referrals as needed

22 Field Experiment Ohio Housing Finance Agency s First Time Homebuyer Program June-December, 2011 MRB funded mortgages Online education and telephone counseling required MyMoneyPath Online financial assessment, redyellow-green cautions; then assigned randomly to treatment Online planning module Quarterly follow-up by letter, and phone (offer coaching)

23 Effects of Monitoring Mortgage Delinquency For the total sample, 12 percent of borrowers had experienced 60 day delinquency within the first 15 months after purchase. Slightly lower rates for treatment group: 11% compared with 13% Treatment effects concentrated among those with history of missed payments 12.9% delinquency, compared with 24.1% for control group Nearly cuts delinquency rate in half (46-48%) Mechanisms? Lower revolving debt (>$2,000 or more) Use of automatic payments Self-reported savings No evidence for budgeting behaviors

24 For Discussion How can we tailor financial education and counseling interventions to best meet the needs of low and moderate income homeowners in Ohio? At what point in the homeownership life cycle? What types of interventions? (education, counseling, coaching monitoring) What outcomes do we want to achieve?

25

26 Why Financial Education is Important Are You Ready to Own? Are you ready to own a home? Answer these questions to find out: Are you unhappy with renting? Do you have a steady income? Do you pay your rent and bills on time? Is your credit history in good shape? Do you have a Social Security Number or Individual Tax Identification Number (ITIN)? Do you plan to stay in the area for the next several years? Do you have some savings for a down payment and closing costs? Can you receive help from family, government programs or other agencies? Have you met with a counselor from a homeownership counseling agency? If you can answer yes to 6 or more of these questions, you are probably ready to become a homeowner.

27 Why Financial Education is Important Financial education is increasingly important for everyone. It is becoming essential for the average family trying to decide how to balance its budget, buy a home, fund the children s education and ensure an income when the parents retire. Of course people have always been responsible for managing their own finances on a day to day basis, determine what to spend on a holiday, how much to save for new furniture, savings or loans for a child s education are common concerns for most families. Recent developments have made financial education and awareness increasingly important for financial well-being. For one thing, the growing sophistication of financial markets means consumers are not just choosing between interest rates on two different bank loans or savings plans, but are rather being offered a variety of complex financial instruments for borrowing and saving, with a large range of options. At the same time, the responsibility and risk for financial decisions that will have a major impact on an individual s future life, notably pensions are being shifted increasingly to workers and away from government and employers. Many companies are eliminating pensions all together opting for such retirement options as 401K, 403b, IRAs, and a partridge in a pear tree.

28 Why Financial Education is Important Research in the United States shows that workers increase their participation in 401(k) retirement savings plans funded by employee and employer contributions when employers offer financial education programs, whether in the form of brochures or seminars. Mortgage counseling before people take on their loan has been found to be effective in reducing the risk of mortgage delinquency. Consumers who attend one-on-one counseling sessions on their personal finances have lower debt and fewer delinquencies. But while financial education is important, it is only one pillar of an adequate financial policy to improve financial literacy and access to financial services. Financial education can complement, but can never replace, other aspects of successful financial policy such as consumer protection and the regulation of financial institutions. Financial education should also go hand-in-hand with improving access to financial markets and services. Access to financial services is a significant issue in many emerging economies as well as for significant groups such as minorities or low income consumers who do not have bank accounts or are under-banked. But interesting consumers in financial education is no easy task. People taking part in a survey in Canada said they thought choosing the right investment for a retirement savings plan was more stressful than a visit to the dentist.

29 Why Financial Education is Important Financial education might also need to be complemented by other approaches to ensure an improvement in consumer financial well being. For example, some experts recommend that workers, when they become eligible, be automatically enrolled in defined contribution pension plans that include pre-determined contribution rates and investment allocations. Doesn t this sound like our old pension programs that are costly for employers to manage and fund? One key element for the future is persuading consumers that they need financial education and enabling them to access it. Also important is better financial education in schools. Today s high school graduates need to be a lot more financially literate than even their parents were if they are to manage their personal finances successfully through life. The role of financial institutions in providing financial education, not only to clients but also to their own staff, needs to be better defined and further promoted. More information is needed at both international and national levels on good programs and practices and on ways to promote access to financial services. Sharing information on successful experiences can be helpful to all.

30 Why Financial Education is Important What Is a Financially Educated Person? Personal financial education means different things to different people. For some it is broad, encompassing an understanding of economics and how household decisions are affected by economic conditions and circumstances. For others, it focuses on basic money management budgeting, saving, and investing. In reality, financial education probably can and does include all of these topics. Most financial literacy initiatives have very specific target audiences. But just as there are numerous initiatives, there are also numerous target audiences. Youth, military personnel, low-income families, first-time homebuyers, employees, church members, and women are all targets of one program or another. Since welfare reform, welfare-towork programs have also incorporated financial education. In essence, it would be difficult for a U.S. consumer not to be part of a target audience for at least one financial literacy initiative. However, there are a few target audiences that bear special mention. Because home ownership is both a major investment and a major asset for families, first time home buyers are a key audience for many financial literacy programs; these initiatives often target low- to moderate-income families. Some programs cover both pre-purchase and post-purchase topics, working with families over several years to clean up their credit records, find affordable housing, and prevent delinquency and default.

31 Why Financial Education is Important Financially educated implies that the outcome of financial education is what a financially educated person does includes behaviors such as paying bills on time, having manageable levels of credit, setting financial goals and having a way of achieving those goals through saving and investing, spending wisely, and so on. The behaviors may vary by income, family circumstance, and asset level, however. For example, we want all households to set financial goals; for some the goal may be having $200 in an emergency fund, while for others the goal may be having $20,000 for a down payment on a house. Less visible, but nonetheless important, are how these themes can be expanded to include community development. Having one s financial house in order can lead to stability of housing and family life, which can contribute to stable educational situations for children, and more involvement of families in their community, including participation in civic activities that range from a parent teacher organization to neighborhood planning board and beyond. A program housed within the Federal Deposit Insurance Corporation, Money Smart, seeks to help adults, young adults and small business enhance their money skills and create positive banking relationships. The goal of the program is to provide financial stability for individuals, families and small business owners as well as communities. While most literacy initiatives function in a preventive mode (i.e., trying to prevent people from getting into problems), some offer curative programs for consumers with credit problems. For many, this is a highly teachable moment in their financial lives. Recent bankruptcy reform legislation includes a provision for debtor education as part of Chapter 13 filings. Generally, these programs start off with a counseling format, customized to the consumers needs; but most organizations involved in credit counseling also offer basic financial education.

32 Why Financial Education is Important The Federal Reserve System is involved in financial education in several ways. The Board and the Reserve Banks are active in promoting awareness of the importance of financial education, increasing access to information about financial products and services, collaborating with educational and community organizations to provide financial education resources, and promoting research and identifying best practices for financial education. Robie K. Suggs PNC Bank 201 E 5 th Street Cincinnati, OH Robie.suggs@pnc.com

How To Get Financial Security

Assets & opportunity ProfILe: DALLAs ASSETS & OPPORTUNITY PROFILE Key highlights 39% of households in the City of Dallas live in asset poverty Cities have long been thought of as places of opportunity

Assets & opportunity ProfILe: DALLAs ASSETS & OPPORTUNITY PROFILE Key highlights 39% of households in the City of Dallas live in asset poverty Cities have long been thought of as places of opportunity

Virginia Individual Development Accounts Program. Program Design

Virginia Individual Development Accounts Program Program Design Revised January 2012 This program receives funding from the Virginia Department of Social Services, Virginia Housing Development Authority,

Virginia Individual Development Accounts Program Program Design Revised January 2012 This program receives funding from the Virginia Department of Social Services, Virginia Housing Development Authority,

Pre-Purchase Counseling Application

Pre-Purchase Counseling Application Guidance on purchasing a home and qualifying for downpayment assistance Pre-purchase counseling helps prepare the first-time homebuyer for the home purchase process

Pre-Purchase Counseling Application Guidance on purchasing a home and qualifying for downpayment assistance Pre-purchase counseling helps prepare the first-time homebuyer for the home purchase process

Affordable Housing Partnership Housing Counseling Program

Affordable Housing Partnership Housing Counseling Program ORGANIZATION AND STAFF INFORMATION Name of Organization: Affordable Housing Partnership of the Capital Region Inc. 255 Orange Street Albany, New

Affordable Housing Partnership Housing Counseling Program ORGANIZATION AND STAFF INFORMATION Name of Organization: Affordable Housing Partnership of the Capital Region Inc. 255 Orange Street Albany, New

TESTIMONY OF BARRY R. WIDES DEPUTY COMPTROLLER FOR COMMUNITY AFFAIRS OFFICE OF THE COMPTROLLER OF THE CURRENCY BEFORE THE

For Release Upon Delivery 10:00 a.m., April 15, 2008 TESTIMONY OF BARRY R. WIDES DEPUTY COMPTROLLER FOR COMMUNITY AFFAIRS OFFICE OF THE COMPTROLLER OF THE CURRENCY BEFORE THE COMMITTEE ON FINANCIAL SERVICES

For Release Upon Delivery 10:00 a.m., April 15, 2008 TESTIMONY OF BARRY R. WIDES DEPUTY COMPTROLLER FOR COMMUNITY AFFAIRS OFFICE OF THE COMPTROLLER OF THE CURRENCY BEFORE THE COMMITTEE ON FINANCIAL SERVICES

Resident & Community Services Programs

Resident & Community Services Programs 1 RCS Mission RCS programming is designed to improve the quality of life for residents of the Denver Housing Authority and neighboring communities by offering empowerment

Resident & Community Services Programs 1 RCS Mission RCS programming is designed to improve the quality of life for residents of the Denver Housing Authority and neighboring communities by offering empowerment

MSHDA s Homeownership Counseling Program. Sharon Evans Homeownership Division May 24, 2011

MSHDA s Homeownership Counseling Program Sharon Evans Homeownership Division May 24, 2011 The Homeownership Counseling Program supports the Michigan State Housing Development Authority s (MSHDA) mortgage

MSHDA s Homeownership Counseling Program Sharon Evans Homeownership Division May 24, 2011 The Homeownership Counseling Program supports the Michigan State Housing Development Authority s (MSHDA) mortgage

Foundation Communities Financial Coaching Guide for Homebuyers

Foundation Communities Financial Coaching Guide for Homebuyers Do you want to know if you are ready to buy a home? The following guide will help you determine whether homeownership is right around the

Foundation Communities Financial Coaching Guide for Homebuyers Do you want to know if you are ready to buy a home? The following guide will help you determine whether homeownership is right around the

DREAM HUGE BUILDING A FINANCIALLY EMPOWERED SAN FRANCISCO

DREAM HUGE BUILDING A FINANCIALLY EMPOWERED SAN FRANCISCO www.sfofe.org Dear Partners, Supporters, Colleagues and Friends, We launched our groundbreaking Kindergarten to College program with the campaign

DREAM HUGE BUILDING A FINANCIALLY EMPOWERED SAN FRANCISCO www.sfofe.org Dear Partners, Supporters, Colleagues and Friends, We launched our groundbreaking Kindergarten to College program with the campaign

2014 State of the Credit Counseling and Financial Education Sector. Delivered by Susan C. Keating. President and CEO

2014 State of the Credit Counseling and Financial Education Sector Delivered by Susan C. Keating President and CEO National Foundation for Credit Counseling 49 th Annual Leaders Conference Seattle, Washington

2014 State of the Credit Counseling and Financial Education Sector Delivered by Susan C. Keating President and CEO National Foundation for Credit Counseling 49 th Annual Leaders Conference Seattle, Washington

FINANCIAL EDUCATION AND CAPABILITY MEASUREMENT TOOLS - ADULT

FINANCIAL EDUCATION AND CAPABILITY MEASUREMENT TOOLS - ADULT The Success Measures Financial Education and Capability Tools document changes in consumers financial attitudes,behaviors, and resilience resulting

FINANCIAL EDUCATION AND CAPABILITY MEASUREMENT TOOLS - ADULT The Success Measures Financial Education and Capability Tools document changes in consumers financial attitudes,behaviors, and resilience resulting

Rethinking Home Ownership Policy for Low-Income Families

Rethinking Home Ownership Policy for Low-Income Families Informing Tenure Choices and Improving Financing Choices and Outcomes J. Michael Collins University of Wisconsin Madison A Home For Everyone 2013:

Rethinking Home Ownership Policy for Low-Income Families Informing Tenure Choices and Improving Financing Choices and Outcomes J. Michael Collins University of Wisconsin Madison A Home For Everyone 2013:

SMART-SAVINGS IDA PROGRAM PROGRAM HANDBOOK: POLICIES & PROCEDURES

SMART-SAVINGS IDA PROGRAM PROGRAM HANDBOOK: POLICIES & PROCEDURES BACKGROUND IDAs, or Individual Development Accounts, are special matched savings accounts designed to help families and individuals of

SMART-SAVINGS IDA PROGRAM PROGRAM HANDBOOK: POLICIES & PROCEDURES BACKGROUND IDAs, or Individual Development Accounts, are special matched savings accounts designed to help families and individuals of

FIELD EXPERIMENTS ON THE IMPACTS OF FINANCIAL PLANNING INTERVENTIONS

CFS Research Brief (FLRC 10-5) October 2011 FIELD EXPERIMENTS ON THE IMPACTS OF FINANCIAL PLANNING INTERVENTIONS FOR RECENT HOMEBUYERS By Stephanie Moulton, Cäzilia Loibl, J. Michael Collins, and Anya

CFS Research Brief (FLRC 10-5) October 2011 FIELD EXPERIMENTS ON THE IMPACTS OF FINANCIAL PLANNING INTERVENTIONS FOR RECENT HOMEBUYERS By Stephanie Moulton, Cäzilia Loibl, J. Michael Collins, and Anya

Strategies for success in financial education

Strategies for success in financial education by Robin G. Newberger, business economist, and Anna L. Paulson, vice president and senior financial economist, Financial Markets Group The Federal Reserve

Strategies for success in financial education by Robin G. Newberger, business economist, and Anna L. Paulson, vice president and senior financial economist, Financial Markets Group The Federal Reserve

You Can Buy a Home The keys to Homeownership

You Can Buy a Home The keys to Homeownership The keys to homeownership Buying a home is one of the most important purchases you ll ever make. Owning your own home helps you build wealth, save on taxes

You Can Buy a Home The keys to Homeownership The keys to homeownership Buying a home is one of the most important purchases you ll ever make. Owning your own home helps you build wealth, save on taxes

We are The Urban League of Philadelphia.

Program & service guide We are The Urban League of Philadelphia. We offer programs & services to empower the region s African American community. Since 1917, The Urban League of Philadelphia has been empowering

Program & service guide We are The Urban League of Philadelphia. We offer programs & services to empower the region s African American community. Since 1917, The Urban League of Philadelphia has been empowering

Latino Community Credit Union (LCCU , North Carolina

U.S. Department of the Treasury Office of Financial Education Community Financial Access Pilot: Elements of an Effective Banking the Unbanked Strategy Bank and credit union accounts serve three basic functions:

U.S. Department of the Treasury Office of Financial Education Community Financial Access Pilot: Elements of an Effective Banking the Unbanked Strategy Bank and credit union accounts serve three basic functions:

Homebuyer Program Orientation

Homebuyer Program Orientation 1405 E. McDowell Rd, Suite 100 Phoenix, Arizona 85006 Telephone: (602) 258-1659 1 Website: www.nhsphoenix.org History of NHS Phoenix NHS Phoenix was founded in 1975 and is

Homebuyer Program Orientation 1405 E. McDowell Rd, Suite 100 Phoenix, Arizona 85006 Telephone: (602) 258-1659 1 Website: www.nhsphoenix.org History of NHS Phoenix NHS Phoenix was founded in 1975 and is

Financial Wellness and Economic Inclusion

Financial Wellness and Economic Inclusion NPHS Financial Wellness and Economic Inclusion programs work together to assist underserved consumers to access, obtain and build assets that create pathways for

Financial Wellness and Economic Inclusion NPHS Financial Wellness and Economic Inclusion programs work together to assist underserved consumers to access, obtain and build assets that create pathways for

The majority of Canadians own their homes, and the number keeps growing. But some people believe they could never own a home.

Is home ownership right for you? The majority of Canadians own their homes, and the number keeps growing. But some people believe they could never own a home. Could this be you? Maybe you are not sure

Is home ownership right for you? The majority of Canadians own their homes, and the number keeps growing. But some people believe they could never own a home. Could this be you? Maybe you are not sure

Refund Anticipation Loans and Refund Anticipation Checks United Way of the Coastal Bend

S E X A T G N I FIL Income Tax Return Preparation Refund Anticipation Loans and Refund Anticipation Checks United Way of the Coastal Bend INTRODUCTION United Way of the Coastal Bend (UWCB) is a nonprofit

S E X A T G N I FIL Income Tax Return Preparation Refund Anticipation Loans and Refund Anticipation Checks United Way of the Coastal Bend INTRODUCTION United Way of the Coastal Bend (UWCB) is a nonprofit

H.E.L.P. COMMUNITY DEVELOPMENT CORP. Foreclosure Counseling Program DOCUMENT CHECKLIST

H.E.L.P. COMMUNITY DEVELOPMENT CORP. Foreclosure Counseling Program DOCUMENT CHECKLIST PLEASE COMPLETE ITEMS 1 AND 2 BELOW AND FAX OR MAIL BACK TO OUR OFFICE. Complete the INTAKE FORMS as thoroughly as

H.E.L.P. COMMUNITY DEVELOPMENT CORP. Foreclosure Counseling Program DOCUMENT CHECKLIST PLEASE COMPLETE ITEMS 1 AND 2 BELOW AND FAX OR MAIL BACK TO OUR OFFICE. Complete the INTAKE FORMS as thoroughly as

The Aspen Institute Initiative on Financial Security (Aspen IFS) proposes. incentives available to low- and middleincome

proposes. incentives available to low- and middleincome") BACK TO BASICS: A SAVINGS APPROACH TO HOMEOWNERSHIP Homeownership is a core American value. It epitomizes the American Dream and the be a springboard to the acquisition of other important assets like a

BACK TO BASICS: A SAVINGS APPROACH TO HOMEOWNERSHIP Homeownership is a core American value. It epitomizes the American Dream and the be a springboard to the acquisition of other important assets like a

Income Tax Return Preparation. Refund Anticipation Loans and Refund Anticipation Checks

S E X A T G N I FIL Income Tax Return Preparation Refund Anticipation Loans and Refund Anticipation Checks INTRODUCTION United Way for Greater Austin (UWATX) is an innovative, impact-driven organization

S E X A T G N I FIL Income Tax Return Preparation Refund Anticipation Loans and Refund Anticipation Checks INTRODUCTION United Way for Greater Austin (UWATX) is an innovative, impact-driven organization

Don t Become a Victim

Don t Become a Victim Life Smarts: 1. Determine the federal laws that assist consumers from becoming victims of predatory lending. What is predatory lending? Predatory lending is the unfair, deceptive,

Don t Become a Victim Life Smarts: 1. Determine the federal laws that assist consumers from becoming victims of predatory lending. What is predatory lending? Predatory lending is the unfair, deceptive,

Table of Contents. Money Smart for Adults Curriculum Page 2 of 21

Table of Contents Checking In... 3 Pre-Test... 4 What Is Credit?... 6 Collateral... 6 Types of Loans... 7 Activity 1: Which Loan Is Best?... 8 The Cost of Credit... 9 Activity 2: Borrowing Money Responsibly...

Table of Contents Checking In... 3 Pre-Test... 4 What Is Credit?... 6 Collateral... 6 Types of Loans... 7 Activity 1: Which Loan Is Best?... 8 The Cost of Credit... 9 Activity 2: Borrowing Money Responsibly...

Homeownership. Your First Steps toward. Getting Started. Know Your Finances. Which Mortgage Is Right for You?

Your First Steps toward Homeownership Identify the type of mortgage that meets your specific financial needs Getting Started Many people don t consider buying a home because they re afraid they can t afford

Your First Steps toward Homeownership Identify the type of mortgage that meets your specific financial needs Getting Started Many people don t consider buying a home because they re afraid they can t afford

Asset Poverty & New Orleans - A Profile

ASSETS & OPPORTUNITY PROFILE: NEW ORLEANS ASSETS & OPPORTUNITY PROFILE KEY HIGHLIGHTS of New Orleans working households don t have access to a vehicle Cities have long been thought of as places of opportunity

ASSETS & OPPORTUNITY PROFILE: NEW ORLEANS ASSETS & OPPORTUNITY PROFILE KEY HIGHLIGHTS of New Orleans working households don t have access to a vehicle Cities have long been thought of as places of opportunity

Neighborhood Housing Services of Greater Cleveland, Inc. Media Kit

Neighborhood Housing Services of Greater Cleveland, Inc. Media Kit Creating Homeownership - Building Communities. Neighborhood Housing Services of Greater Cleveland has been delivering exemplary programs

Neighborhood Housing Services of Greater Cleveland, Inc. Media Kit Creating Homeownership - Building Communities. Neighborhood Housing Services of Greater Cleveland has been delivering exemplary programs

COUNTERING CONSUMER DEBT IN BROOKLYN: Strengthening Communities by Raising Financial Literacy

COUNTERING CONSUMER DEBT IN BROOKLYN: Strengthening Communities by Raising Financial Literacy BROOKLYN BOROUGH PRESIDENT ERIC L. ADAMS Table of Contents Introduction.1 Causes of Brooklyn s Poor Credit...3

COUNTERING CONSUMER DEBT IN BROOKLYN: Strengthening Communities by Raising Financial Literacy BROOKLYN BOROUGH PRESIDENT ERIC L. ADAMS Table of Contents Introduction.1 Causes of Brooklyn s Poor Credit...3

Preparing for homeownership

Preparing for homeownership What we ll cover 1. Getting ready for homeownership 2. Mortgage basics 3. What you need to buy a home 4. Finding the right home 5. Resources 2 Getting ready for homeownership

Preparing for homeownership What we ll cover 1. Getting ready for homeownership 2. Mortgage basics 3. What you need to buy a home 4. Finding the right home 5. Resources 2 Getting ready for homeownership

CONTRACT FOR DEED. What Homebuyers and Sellers Need to Know to Achieve a Successful Outcome

CONTRACT FOR DEED What Homebuyers and Sellers Need to Know to Achieve a Successful Outcome Copyright 2012 CONTRACT FOR DEED Is it the right option for me? This publication is intended to provide advice

CONTRACT FOR DEED What Homebuyers and Sellers Need to Know to Achieve a Successful Outcome Copyright 2012 CONTRACT FOR DEED Is it the right option for me? This publication is intended to provide advice

58% 61% 17% 24% 12% 20% PROFILE. ASSetS & opportunity ProfILe: NewArk. key HIgHLIgHtS ABOUT THE PROFILE ASSETS & OPPORTUNITY

ASSetS & opportunity ProfILe: NewArk ASSETS & OPPORTUNITY PROFILE key HIgHLIgHtS 58% of Newark residents live in asset poverty Cities have long been thought of as places of opportunity for low-income workers

ASSetS & opportunity ProfILe: NewArk ASSETS & OPPORTUNITY PROFILE key HIgHLIgHtS 58% of Newark residents live in asset poverty Cities have long been thought of as places of opportunity for low-income workers

Remarks by. Thomas J. Curry Comptroller of the Currency. National Asian American Coalition. San Diego, California.

Remarks by Thomas J. Curry Comptroller of the Currency National Asian American Coalition San Diego, California October 18, 2013 Good evening. It s a pleasure to be here at the 10 th Anniversary Economic

Remarks by Thomas J. Curry Comptroller of the Currency National Asian American Coalition San Diego, California October 18, 2013 Good evening. It s a pleasure to be here at the 10 th Anniversary Economic

Keeping Your Home - Protect your investment

Keeping Your Home - Protect your investment People who plan, budget and save for successful homeownership have a much better chance of keeping a roof over their heads and building wealth as property values

Keeping Your Home - Protect your investment People who plan, budget and save for successful homeownership have a much better chance of keeping a roof over their heads and building wealth as property values

C E. Check Cashers. Direct Deposit. Identification to Open a Bank Account

M O R F H S CA S K C E CH Check Cashers Direct Deposit Identification to Open a Bank Account INTRODUCTION United Way for Greater Austin (UWATX) is a innovative, impact-driven organization that addresses

M O R F H S CA S K C E CH Check Cashers Direct Deposit Identification to Open a Bank Account INTRODUCTION United Way for Greater Austin (UWATX) is a innovative, impact-driven organization that addresses

City of Austin programs for. Healthy Homes and Financial Empowerment. We Can Help! Providing Opportunities, Changing Lives

City of Austin programs for Healthy Homes and Financial Empowerment We Can Help! Providing Opportunities, Changing Lives Neighborhood Housing and Community Development Office The City of Austin has several

City of Austin programs for Healthy Homes and Financial Empowerment We Can Help! Providing Opportunities, Changing Lives Neighborhood Housing and Community Development Office The City of Austin has several

Summary of the Housing and Economic Recovery Act of 2008

Summary of the Housing and Economic Recovery Act of 2008 On July 30, President Bush signed major housing legislation, HR 3221, the Housing and Economic Recovery Act of 2008. The bill restructures regulation

Summary of the Housing and Economic Recovery Act of 2008 On July 30, President Bush signed major housing legislation, HR 3221, the Housing and Economic Recovery Act of 2008. The bill restructures regulation

Credit Counseling. Credit Repair. Debt Management Plans. Debt Settlement and Negotiation. United Way of the Coastal Bend

K C A B G N I Y A P Credit Counseling Credit Repair Debt Management Plans Debt Settlement and Negotiation United Way of the Coastal Bend INTRODUCTION United Way of the Coastal Bend (UWCB) is a nonprofit

K C A B G N I Y A P Credit Counseling Credit Repair Debt Management Plans Debt Settlement and Negotiation United Way of the Coastal Bend INTRODUCTION United Way of the Coastal Bend (UWCB) is a nonprofit

2013 DENVER METRO MORTGAGE ASSISTANCE PLUS

2013 DENVER METRO MORTGAGE ASSISTANCE PLUS PROGRAM Down Payment Assistance of 4% (3% + 1% Origination) of the total mortgage amount - in exchange for a slightly higher mortgage interest rate! HISTORICALLY

2013 DENVER METRO MORTGAGE ASSISTANCE PLUS PROGRAM Down Payment Assistance of 4% (3% + 1% Origination) of the total mortgage amount - in exchange for a slightly higher mortgage interest rate! HISTORICALLY

Foreclosure Information & Assistance 2010 (updated 10/10)

") This information can also be found on the web at: http://humanservices.townofmanchester.org/elderly/documents/forclosureassistance2010.pdf Summary of P.A. 08-176 An Act Concerning Responsible Lending and

This information can also be found on the web at: http://humanservices.townofmanchester.org/elderly/documents/forclosureassistance2010.pdf Summary of P.A. 08-176 An Act Concerning Responsible Lending and

Survey of EITC Filers at Tax Preparation Sites

Survey of EITC Filers at Tax Preparation Sites February April 2007 Sandra Venner MASSCAP Asset Formation Initiative November 1, 2007 Consumer Use and Satisfaction Completed Surveys Completion rate BCAC

Survey of EITC Filers at Tax Preparation Sites February April 2007 Sandra Venner MASSCAP Asset Formation Initiative November 1, 2007 Consumer Use and Satisfaction Completed Surveys Completion rate BCAC

The Good Credit Game Alignment with Financial Education National Standards

The Good Credit Game Alignment with Financial Education National Standards There are a number of national standards for teaching personal finance and financial literacy. Many of the learning objectives

The Good Credit Game Alignment with Financial Education National Standards There are a number of national standards for teaching personal finance and financial literacy. Many of the learning objectives

9.1 PERSONAL FINANCIAL LITERACY

STRAND A: 9.1.4.A.1 9.1.4.A.2 9.1.4.A.3 9.1.8.A.1 9.1.8.A.2 9.1.8.A.3 9.1.8.A.4 9.1.8.A.5 9.1.8.A.6 9.1.8.A.7 9.1.12.A.1 9.1.12.A.2 9.1.12.A.3 9.1.12.A.4 9.1.12.A.5 9.1.12.A.6 9.1.12.A.7 9.1.12.A.8 9.1.12.A.9

STRAND A: 9.1.4.A.1 9.1.4.A.2 9.1.4.A.3 9.1.8.A.1 9.1.8.A.2 9.1.8.A.3 9.1.8.A.4 9.1.8.A.5 9.1.8.A.6 9.1.8.A.7 9.1.12.A.1 9.1.12.A.2 9.1.12.A.3 9.1.12.A.4 9.1.12.A.5 9.1.12.A.6 9.1.12.A.7 9.1.12.A.8 9.1.12.A.9

2012 HOUSEHOLD FINANCIAL PLANNING SURVEY

2012 HOUSEHOLD FINANCIAL PLANNING SURVEY A Summary of Key Findings July 23, 2012 Prepared for: Certified Financial Planner Board of Standards, Inc. and the Consumer Federation of America Prepared by: Princeton

2012 HOUSEHOLD FINANCIAL PLANNING SURVEY A Summary of Key Findings July 23, 2012 Prepared for: Certified Financial Planner Board of Standards, Inc. and the Consumer Federation of America Prepared by: Princeton

ASSET-DEVELOPMENT OPPORTUNITIES FOR DOMESTIC VIOLENCE AND SEXUAL ASSAULT SURVIVORS

ASSET-DEVELOPMENT OPPORTUNITIES FOR DOMESTIC VIOLENCE AND SEXUAL ASSAULT SURVIVORS KEY FACTS > More than one in three women have experienced domestic violence in their lifetime. 71 > Nearly one in five

ASSET-DEVELOPMENT OPPORTUNITIES FOR DOMESTIC VIOLENCE AND SEXUAL ASSAULT SURVIVORS KEY FACTS > More than one in three women have experienced domestic violence in their lifetime. 71 > Nearly one in five

34% 69% 12% 18% 23% 25% PROFILE. ASSeTS & opportunity ProfILe: SAN ANToNIo. KeY HIGHLIGHTS ABOUT THE PROFILE ASSETS & OPPORTUNITY

ASSeTS & opportunity ProfILe: SAN ANToNIo ASSETS & OPPORTUNITY PROFILE KeY HIGHLIGHTS 34% of San Antonio households live in asset poverty Cities have long been thought of as places of opportunity for low-income

ASSeTS & opportunity ProfILe: SAN ANToNIo ASSETS & OPPORTUNITY PROFILE KeY HIGHLIGHTS 34% of San Antonio households live in asset poverty Cities have long been thought of as places of opportunity for low-income

Financial Awareness Survey Report Massachusetts Office of Consumer Affairs and Business Regulation

Financial Awareness Survey Report Massachusetts Office of Consumer Affairs and Business Regulation Introduction Understanding and managing one s personal finances are important, particularly during a time

Financial Awareness Survey Report Massachusetts Office of Consumer Affairs and Business Regulation Introduction Understanding and managing one s personal finances are important, particularly during a time

STATEMENT OF ARTHUR J. MYERS ACTING DEPUTY UNDER SECRETARY OF DEFENSE (MILITARY COMMUNITY AND FAMILY POLICY) BEFORE THE

BEFORE THE") STATEMENT OF ARTHUR J. MYERS ACTING DEPUTY UNDER SECRETARY OF DEFENSE (MILITARY COMMUNITY AND FAMILY POLICY) BEFORE THE SUBCOMMITTEE ON OVERSIGHT OF GOVERNMENT MANAGEMENT, THE FEDERAL WORKFORCE, AND THE

STATEMENT OF ARTHUR J. MYERS ACTING DEPUTY UNDER SECRETARY OF DEFENSE (MILITARY COMMUNITY AND FAMILY POLICY) BEFORE THE SUBCOMMITTEE ON OVERSIGHT OF GOVERNMENT MANAGEMENT, THE FEDERAL WORKFORCE, AND THE

Policies and Procedures

Policies and Procedures Last revised March 2009 Table of Contents Mission & Vision... 2 Description of the Network... 3 Match Rate and Qualified Withdrawals... 3 Qualified asset purchase includes:... 4

Policies and Procedures Last revised March 2009 Table of Contents Mission & Vision... 2 Description of the Network... 3 Match Rate and Qualified Withdrawals... 3 Qualified asset purchase includes:... 4

Strategies to Support Work and Reduce Poverty Eileen Trzcinski

Strategies to Support Work and Reduce Poverty Eileen Trzcinski Overview of Low Income Working Families in Michigan 1998, the Michigan Budget and Tax Policy Project, an initiative of the Michigan League

Strategies to Support Work and Reduce Poverty Eileen Trzcinski Overview of Low Income Working Families in Michigan 1998, the Michigan Budget and Tax Policy Project, an initiative of the Michigan League

2015 State of the Financial Counseling and Education Sector. Susan C. Keating. President and CEO. National Foundation for Credit Counseling

2015 State of the Financial Counseling and Education Sector Susan C. Keating President and CEO National Foundation for Credit Counseling 50 th Annual Leaders Conference Indianapolis, Indiana September

2015 State of the Financial Counseling and Education Sector Susan C. Keating President and CEO National Foundation for Credit Counseling 50 th Annual Leaders Conference Indianapolis, Indiana September

City of Elyria, Ohio First-Time Homebuyer Assistance Program

Revised 10/07 City of Elyria, Ohio First-Time Homebuyer Assistance Program Location: City-wide (No Target Area for this program) Description/Purpose: This program is designed to provide assistance with

Revised 10/07 City of Elyria, Ohio First-Time Homebuyer Assistance Program Location: City-wide (No Target Area for this program) Description/Purpose: This program is designed to provide assistance with

CITY OF BAY VILLAGE DEPARTMENT OF COMMUNITY SERVICES DOWN PAYMENT ASSISTANCE PROGRAMS

CITY OF BAY VILLAGE DEPARTMENT OF COMMUNITY SERVICES DOWN PAYMENT ASSISTANCE PROGRAMS Cuyahoga County Loan and Grant Programs for Residents For application forms or more information on the programs below,

CITY OF BAY VILLAGE DEPARTMENT OF COMMUNITY SERVICES DOWN PAYMENT ASSISTANCE PROGRAMS Cuyahoga County Loan and Grant Programs for Residents For application forms or more information on the programs below,

HOME SAVINGS IDA PROGRAM

HOME SAVINGS IDA PROGRAM Program Overview The Home Savings Individual Development Account (IDA) Program is a special matched savings account program. The program is designed to assist incomeeligible, New

HOME SAVINGS IDA PROGRAM Program Overview The Home Savings Individual Development Account (IDA) Program is a special matched savings account program. The program is designed to assist incomeeligible, New

Tips for Homebuyers: Working with Agents & Lenders

Tips for Homebuyers: Working with Agents & Lenders by The Connecticut Department of Consumer Protection and The Connecticut Housing Finance Authority What to Know Before You Buy CONNECTICUT DEPARTMENT

Tips for Homebuyers: Working with Agents & Lenders by The Connecticut Department of Consumer Protection and The Connecticut Housing Finance Authority What to Know Before You Buy CONNECTICUT DEPARTMENT

Rapid Refund Costs Taxpayers Too Much $$$

the ALERT V. 2 6, N O. 1 A N E W S L E T T E R F O R S E N I O R S J A N / F E B / M A R C H / A P R I L 2 0 1 0 Rapid Refund Costs Taxpayers Too Much $$$ With more Seniors working to make ends meet, more

the ALERT V. 2 6, N O. 1 A N E W S L E T T E R F O R S E N I O R S J A N / F E B / M A R C H / A P R I L 2 0 1 0 Rapid Refund Costs Taxpayers Too Much $$$ With more Seniors working to make ends meet, more

It lets you pay for expenses you could not afford with cash, such as a college education, a new vehicle, furniture or a home.

USING CREDIT WISELY Credit Is An Important Financial Tool It lets you pay for expenses you could not afford with cash, such as a college education, a new vehicle, furniture or a home.

USING CREDIT WISELY Credit Is An Important Financial Tool It lets you pay for expenses you could not afford with cash, such as a college education, a new vehicle, furniture or a home.

United Way ALICE Report: Florida. Meet ALICE: seeing and serving families at the edge of poverty

United Way ALICE Report: Florida Meet ALICE: seeing and serving families at the edge of poverty Introduction and Overview Lars Gilberts Statewide ALICE Director United Way of Broward County Why do we need

United Way ALICE Report: Florida Meet ALICE: seeing and serving families at the edge of poverty Introduction and Overview Lars Gilberts Statewide ALICE Director United Way of Broward County Why do we need

Welcome! AFI Program Overview & Grant Application Process. AFI Resource Center 1-866-778-6037 info@idaresources.org

Welcome! AFI Program Overview & Grant Application Process AFI Resource Center 1-866-778-6037 info@idaresources.org Assets for Independence Special federally funded 5-year grants to organizations that enable

Welcome! AFI Program Overview & Grant Application Process AFI Resource Center 1-866-778-6037 info@idaresources.org Assets for Independence Special federally funded 5-year grants to organizations that enable

Section 8: Anti-Poverty Strategy

Section 8: Anti-Poverty Strategy Anti-Poverty Strategy City of Springfield Page 113 Goals, Programs, and Policies for Reducing Poverty Springfield is faced with an alarmingly high percentage of families

Section 8: Anti-Poverty Strategy Anti-Poverty Strategy City of Springfield Page 113 Goals, Programs, and Policies for Reducing Poverty Springfield is faced with an alarmingly high percentage of families

Trends in Homeownership and Mortgage Debt among Older Americans Office for Older Americans

June 24, 2015 Trends in Homeownership and Mortgage Debt among Older Americans Office for Older Americans Presentation for MHA Trusted Advisors Note: This document was used in support of a live discussion.

June 24, 2015 Trends in Homeownership and Mortgage Debt among Older Americans Office for Older Americans Presentation for MHA Trusted Advisors Note: This document was used in support of a live discussion.

Declaring Personal Bankruptcy

Declaring Personal Bankruptcy DECLARING PERSONAL BANKRUPTCY A declaration of personal bankruptcy doesn t carry the stigma it once did but it is, nonetheless, an admission that one is no longer able to

Declaring Personal Bankruptcy DECLARING PERSONAL BANKRUPTCY A declaration of personal bankruptcy doesn t carry the stigma it once did but it is, nonetheless, an admission that one is no longer able to

HOME BUYING MADE EASY. Live the dream of owning your own home.

HOME BUYING MADE EASY Live the dream of owning your own home. HOME buying Made Easy PNC, PNC AgentView and Home Insight are registered service marks of The PNC Financial Services Group, Inc. ( PNC ). PNC

HOME BUYING MADE EASY Live the dream of owning your own home. HOME buying Made Easy PNC, PNC AgentView and Home Insight are registered service marks of The PNC Financial Services Group, Inc. ( PNC ). PNC

GET CREDITWISE SM SM

GET CREDITWISE SM SM Table Of Contents October, 2006 Credit Matters 1 An introduction Establishing Credit 3 Begin building a solid financial base Using Credit Wisely 5 Narrowing your options Monitoring

GET CREDITWISE SM SM Table Of Contents October, 2006 Credit Matters 1 An introduction Establishing Credit 3 Begin building a solid financial base Using Credit Wisely 5 Narrowing your options Monitoring

HOME BUYING MADE EASY. Know what you need to get it right.

HOME BUYING MADE EASY Know what you need to get it right. HOME BUYING MADE EASY PNC, PNC AgentView and Home Insight are registered service marks of The PNC Financial Services Group, Inc. ( PNC ). PNC has

HOME BUYING MADE EASY Know what you need to get it right. HOME BUYING MADE EASY PNC, PNC AgentView and Home Insight are registered service marks of The PNC Financial Services Group, Inc. ( PNC ). PNC has

Wealth Inequity, Debt and Savings

Wealth Inequity, Debt and Savings Implications for Policy and Financial Services Sandra Venner FDIC Alliance for Economic Inclusion May 21, 2008 Today, government wealth building policy is primarily in

Wealth Inequity, Debt and Savings Implications for Policy and Financial Services Sandra Venner FDIC Alliance for Economic Inclusion May 21, 2008 Today, government wealth building policy is primarily in

FHLBanks: The Basics. For more information, visit www.fhlbanks.com.

FHLBanks: The Basics For more information, visit www.fhlbanks.com. The Federal Home Loan Banks (FHLBanks) are 11 private, wholesale banks regionally based throughout the U.S. They are cooperatively owned

FHLBanks: The Basics For more information, visit www.fhlbanks.com. The Federal Home Loan Banks (FHLBanks) are 11 private, wholesale banks regionally based throughout the U.S. They are cooperatively owned

Orlando Housing Authority

Orlando Housing Authority Orlando Housing Authority Primary Business Address Your Address Line 2 Your Address Line 3 Your Address Line 4 Phone: 555-555-5555 Fax: 555-555-5555 E-mail: someone@example.com

Orlando Housing Authority Orlando Housing Authority Primary Business Address Your Address Line 2 Your Address Line 3 Your Address Line 4 Phone: 555-555-5555 Fax: 555-555-5555 E-mail: someone@example.com

Home Buying Seminar. A presentation by The Summit Federal Credit Union

Summit Branches are located in Rochester (7), Seneca Falls (1), Buffalo (3), Syracuse (5) and Cortland (2) Home Buying Seminar A presentation by The Summit Federal Credit Union What We Will Cover Today

Summit Branches are located in Rochester (7), Seneca Falls (1), Buffalo (3), Syracuse (5) and Cortland (2) Home Buying Seminar A presentation by The Summit Federal Credit Union What We Will Cover Today

First-time Homebuyer Pathfinder Penny Bates

Penny Bates First-time homebuyers, and homebuyers in general, sometimes can be confused by the mortgage and home buying process. The recent mortgage crisis underlined the need for additional consumer financial

Penny Bates First-time homebuyers, and homebuyers in general, sometimes can be confused by the mortgage and home buying process. The recent mortgage crisis underlined the need for additional consumer financial

MEETING THE OREGON STATE STANDARDS FINANCIAL AVENUE CORE CONCEPT EARNING SPENDING SAVING BORROWING PROTECT

MEETING THE OREGON STATE STANDARDS Financial Avenue provides online courses to help students gain important knowledge about the basics of personal money management. The Financial Avenue online financial

MEETING THE OREGON STATE STANDARDS Financial Avenue provides online courses to help students gain important knowledge about the basics of personal money management. The Financial Avenue online financial

Revised September 2014

Revised September 2014 WELCOME TO HOMEOWNERSHIP Post Homeownership Guide A guide for the new home owner W A S H I N G T O N S T A T E H O U S I N G F I N A N C E C O M M I S S I O N S Home Advantage &

Revised September 2014 WELCOME TO HOMEOWNERSHIP Post Homeownership Guide A guide for the new home owner W A S H I N G T O N S T A T E H O U S I N G F I N A N C E C O M M I S S I O N S Home Advantage &

Roles of a Housing Counselor

Roles of a Counselor Homeowners! Get real help, free of charge from a HUD approved counseling agency. Denise Keiser, Executive Director Center for Financial Health Who is a housing counselor? Employed

Roles of a Counselor Homeowners! Get real help, free of charge from a HUD approved counseling agency. Denise Keiser, Executive Director Center for Financial Health Who is a housing counselor? Employed

VHDA. Homeownership Program Guidelines for Realtors & Lenders. Updated 04/04

VHDA Homeownership Program Guidelines for Realtors & Lenders Updated 04/04 2 Benefits of a VHDA Loan: Creative financing programs Reduced interest rates Lower monthly payments More house for less money

VHDA Homeownership Program Guidelines for Realtors & Lenders Updated 04/04 2 Benefits of a VHDA Loan: Creative financing programs Reduced interest rates Lower monthly payments More house for less money

United Way of the Bluegrass Back On Track

United Way of the Bluegrass Back On Track BACK ON TRACK CONTACT: United Way of the Bluegrass 2480 Fortune Drive, # 250 Lexington, KY 40509 backontrack@uwbg.org tel 859.233.4460 fax 859.259.3397 BACK ON

United Way of the Bluegrass Back On Track BACK ON TRACK CONTACT: United Way of the Bluegrass 2480 Fortune Drive, # 250 Lexington, KY 40509 backontrack@uwbg.org tel 859.233.4460 fax 859.259.3397 BACK ON

REALTORS CAN SELL HOUSES USING FHA

REALTORS CAN SELL HOUSES USING FHA WITHOUT SELLER-FUNDED DOWN PAYMENT ASSISTANCE Right now, the big buzz among REALTORS is the elimination of seller-funded down payment assistance with FHA products. If

REALTORS CAN SELL HOUSES USING FHA WITHOUT SELLER-FUNDED DOWN PAYMENT ASSISTANCE Right now, the big buzz among REALTORS is the elimination of seller-funded down payment assistance with FHA products. If

Student Debt Being Smart about Student Loans

Insight. Education. Analysis. S e p t e m b e r 2 0 1 4 Student Debt Being Smart about Student Loans By Kevin Chambers During the 2008 crisis, total American household debt fell. The amount of money borrowed

Insight. Education. Analysis. S e p t e m b e r 2 0 1 4 Student Debt Being Smart about Student Loans By Kevin Chambers During the 2008 crisis, total American household debt fell. The amount of money borrowed

Affordable Housing. A Foundation for Stable Communities

Affordable Housing A Foundation for Stable Communities AFFORDABLE HOUSING: A FOUNDATION FOR STABLE COMMUNITIES The importance of good-quality and equitable affordable housing plays a key role in the success

Affordable Housing A Foundation for Stable Communities AFFORDABLE HOUSING: A FOUNDATION FOR STABLE COMMUNITIES The importance of good-quality and equitable affordable housing plays a key role in the success

The New York Mortgage Coalition. Homebuyer Handbook. We d like to buy a home but we re on a limited budget...and we re not sure how to start.

The New York Mortgage Coalition Homebuyer Handbook We d like to buy a home but we re on a limited budget......and we re not sure how to start. let s check it out. nymc.org Fact 1: Two out of three people

The New York Mortgage Coalition Homebuyer Handbook We d like to buy a home but we re on a limited budget......and we re not sure how to start. let s check it out. nymc.org Fact 1: Two out of three people

Mary Dupont, Director of Financial Empowerment State of Delaware, DE Dept. of Health and Social Services mary.dupont@state.de.

Mary Dupont, Director of Financial Empowerment State of Delaware, DE Dept. of Health and Social Services mary.dupont@state.de.us 302-255-9245 http://www.youtube.com/watch?v=jrktcvurow8 www.standbymede.org

Mary Dupont, Director of Financial Empowerment State of Delaware, DE Dept. of Health and Social Services mary.dupont@state.de.us 302-255-9245 http://www.youtube.com/watch?v=jrktcvurow8 www.standbymede.org

Investments and Services. 2012 National Interagency Community Reinvestment t Conference

Community Development Investments and Services 2012 National Interagency Community Reinvestment t Conference Community Development Defined Affordable housing targeted to low- or moderate- income (LMI)

Community Development Investments and Services 2012 National Interagency Community Reinvestment t Conference Community Development Defined Affordable housing targeted to low- or moderate- income (LMI)

USDA Home Loans. USDA Income Limitations. What is a USDA Home Loan?

USDA Home Loans What is a USDA Home Loan? USDA Home Loans provide up to 100% financing for a home purchase or refinance. These loans are guaranteed by the USDA and are serviced by direct lenders that meet

USDA Home Loans What is a USDA Home Loan? USDA Home Loans provide up to 100% financing for a home purchase or refinance. These loans are guaranteed by the USDA and are serviced by direct lenders that meet

YOUR MONEY, YOUR GOALS. A financial empowerment toolkit for Social Services programs

YOUR MONEY, YOUR GOALS A financial empowerment toolkit for Social Services programs Consumer Financial Protection Bureau April 2015 Table of contents MODULE 1: Introduction to the toolkit...1 An introduction

YOUR MONEY, YOUR GOALS A financial empowerment toolkit for Social Services programs Consumer Financial Protection Bureau April 2015 Table of contents MODULE 1: Introduction to the toolkit...1 An introduction

Metro Interfaith Housing Counseling. Tell Us About Yourself. General Information Primary

Metro Interfaith Housing Counseling 21 New St, Binghamton, NY 13903 Phone: 607.723.0582 Fax: 607.722.8912 Tell Us About Yourself Print clearly. Use additional sheets if necessary. Information provided

Metro Interfaith Housing Counseling 21 New St, Binghamton, NY 13903 Phone: 607.723.0582 Fax: 607.722.8912 Tell Us About Yourself Print clearly. Use additional sheets if necessary. Information provided

Homebuyer Orientation

Homebuyer Orientation WHY PARTNER WITH A TRUSTED RESOURCE Buying your first home is usually the biggest financial investment in your life. The home buying process is complicated, and there are many important

Homebuyer Orientation WHY PARTNER WITH A TRUSTED RESOURCE Buying your first home is usually the biggest financial investment in your life. The home buying process is complicated, and there are many important

PROGRAM DESCRIPTION FY 2007 ANNUAL PROGRAM PERFORMANCE MEASURES. APPROPRIATION UNIT: Michigan State Housing Development Authority Date:02/12/08

PROGRAM DESCRIPTION FY 2007 ANNUAL PROGRAM PERFORMANCE MEASURES DEPARTMENT: Michigan Department of Labor & Economic Growth APPROPRIATION UNIT: Michigan State Housing Development Authority Date:02/12/08

PROGRAM DESCRIPTION FY 2007 ANNUAL PROGRAM PERFORMANCE MEASURES DEPARTMENT: Michigan Department of Labor & Economic Growth APPROPRIATION UNIT: Michigan State Housing Development Authority Date:02/12/08

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING From America Saves and Experian WHAT IS A CREDIT REPORT AND SCORE? A credit score is a three digit number that measures how likely you are to repay a

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING From America Saves and Experian WHAT IS A CREDIT REPORT AND SCORE? A credit score is a three digit number that measures how likely you are to repay a

www.fha.gov FHA s Role and Strategy to Help Vulnerable Homebuyers and Homeowners

FHA s Role and Strategy to Help Vulnerable Homebuyers and Homeowners FHA Helping Vulnerable Homeowners & Homebuyers Refinance Options for Non-FHA Foreclosure Prevention for FHA Support for Housing Counseling

FHA s Role and Strategy to Help Vulnerable Homebuyers and Homeowners FHA Helping Vulnerable Homeowners & Homebuyers Refinance Options for Non-FHA Foreclosure Prevention for FHA Support for Housing Counseling

Financial Education and Counseling Services

DEFINITION Financial Education and Counseling services provide educational services and programs to assist consumers with money management, budgeting, knowledge of resources needed to acquire housing,

DEFINITION Financial Education and Counseling services provide educational services and programs to assist consumers with money management, budgeting, knowledge of resources needed to acquire housing,

TEXAS STATE AFFORDABLE HOUSING CORPORATION 2014 ANNUAL ACTION PLAN

TEXAS STATE AFFORDABLE HOUSING CORPORATION 2014 ANNUAL ACTION PLAN TEXAS STATE AFFORDABLE HOUSING CORPORATION 2014 ANNUAL ACTION PLAN INTRODUCTION This plan is prepared in accordance with Texas Government

TEXAS STATE AFFORDABLE HOUSING CORPORATION 2014 ANNUAL ACTION PLAN TEXAS STATE AFFORDABLE HOUSING CORPORATION 2014 ANNUAL ACTION PLAN INTRODUCTION This plan is prepared in accordance with Texas Government

YOUR MONEY, YOUR GOALS. A financial empowerment toolkit for community volunteers

YOUR MONEY, YOUR GOALS A financial empowerment toolkit for community volunteers Consumer Financial Protection Bureau April 2015 Table of contents INTRODUCTION PART 1: Volunteers and financial empowerment...

YOUR MONEY, YOUR GOALS A financial empowerment toolkit for community volunteers Consumer Financial Protection Bureau April 2015 Table of contents INTRODUCTION PART 1: Volunteers and financial empowerment...

2010 NSP FIRST Mortgage Loan Program Summary Approved by THDA 05/07/2010

Description: Eligible Applicants: Maximum Household Interest Rate: Loan Term/ Type: Pre-Payment Penalty Subject to Recapture: Required Reserves: Down Payment Minimum Investment: Maximum Loan Amount: Homebuyer

Description: Eligible Applicants: Maximum Household Interest Rate: Loan Term/ Type: Pre-Payment Penalty Subject to Recapture: Required Reserves: Down Payment Minimum Investment: Maximum Loan Amount: Homebuyer

Homeowner s Equity Recovery Opportunity Loan Program (HERO) Expansion Program

Expansion Program") Homeowner s Equity Recovery Opportunity Loan Program (HERO) Expansion Program A mortgage loan program for purchasing and/or rehabilitating foreclosed, abandoned or bank-owned properties in Connecticut

Homeowner s Equity Recovery Opportunity Loan Program (HERO) Expansion Program A mortgage loan program for purchasing and/or rehabilitating foreclosed, abandoned or bank-owned properties in Connecticut

Affordable Homeownership

Housing and Human Services Division Affordable Homeownership Program Guidelines The City s Affordable Homeownership Program (also referred to as the Inclusionary Housing Program) provides homeownership

Housing and Human Services Division Affordable Homeownership Program Guidelines The City s Affordable Homeownership Program (also referred to as the Inclusionary Housing Program) provides homeownership

House Financial Services Committee. Subcommittee on Insurance, Housing and Community Opportunity. Hearing

House Financial Services Committee Subcommittee on Insurance, Housing and Community Opportunity Hearing HUD and NeighborWorks Housing Counseling Oversight The Honorable Debra Olson Board Member DuPage

House Financial Services Committee Subcommittee on Insurance, Housing and Community Opportunity Hearing HUD and NeighborWorks Housing Counseling Oversight The Honorable Debra Olson Board Member DuPage

HOME BUYING MADE EASY. Live the dream of owning your own home.

HOME BUYING MADE EASY Live the dream of owning your own home. sm Getting started For most of us, buying our first home is a dream come true. It s also a lengthy process where potential and sometimes very

HOME BUYING MADE EASY Live the dream of owning your own home. sm Getting started For most of us, buying our first home is a dream come true. It s also a lengthy process where potential and sometimes very

Home Buying Best Practices

LOAN AND HOME BUYING BEST PRACTICES About TSAHC The Texas State Affordable Housing Corporation (TSAHC) is a nonprofit housing corporation created at the direction of the Texas Legislature to facilitate

LOAN AND HOME BUYING BEST PRACTICES About TSAHC The Texas State Affordable Housing Corporation (TSAHC) is a nonprofit housing corporation created at the direction of the Texas Legislature to facilitate